The U.S. government is making its most aggressive move yet to secure critical mineral supply chains—and small-cap mining stocks may be the biggest beneficiaries.

President Donald Trump is preparing to launch Project Vault, a first-of-its-kind $12 billion strategic stockpile of critical minerals designed to break America’s dependence on China. Modeled after the Strategic Petroleum Reserve, the initiative will target minerals essential to modern industry: rare earths, cobalt, gallium, nickel, and antimony—materials that power electric vehicles, semiconductors, defense systems, jet engines, and consumer electronics.

For investors focused on small-cap and emerging resource companies, this announcement represents more than a policy shift. It’s a potentially transformative multi-year demand catalyst.

Why Project Vault Changes the Game

Project Vault pools $10 billion in financing from the U.S. Export-Import Bank with $1.67 billion in private capital, creating a centralized procurement system that will buy and store minerals on behalf of major manufacturers including General Motors, Boeing, Stellantis, Google, and GE Vernova. Three global commodities trading firms—Hartree, Traxys, and Mercuria—will manage sourcing and logistics.

Unlike traditional defense-focused stockpiles, this program explicitly targets civilian supply chains. It offers participating manufacturers two critical advantages: price stability and guaranteed access during supply disruptions. Companies commit to purchasing materials at a predetermined price and can later buy them back at the same cost—a mechanism designed to eliminate volatility and enable long-term production planning.

The implications for upstream producers are significant. Government-backed demand provides the certainty mining companies need to justify capital investment, accelerate development timelines, and secure project financing.

The Small-Cap Advantage

Markets responded immediately. Shares of USA Rare Earth, Critical Metals Corp., United States Antimony, and NioCorp Developments all surged following the announcement, signaling investor recognition of a fundamental truth: supply security requires actual production, not just strategic intent.

This creates a disproportionate opportunity for small-cap miners.

Large diversified mining companies already generate stable cash flow from multiple commodities. Smaller miners, by contrast, often operate single-asset projects concentrated in exactly the minerals Project Vault prioritizes. For these companies, government-backed offtake agreements and improved access to financing could fundamentally alter project economics—transforming marginal assets into commercially viable operations.

Put simply: Project Vault de-risks production at the precise stage where small mining companies struggle most—the transition from exploration to commercial scale.

The timing reflects geopolitical reality. China’s export restrictions last year exposed the brittleness of Western supply chains, forcing some U.S. manufacturers to curtail production. Project Vault is Washington’s financial response—a clear signal that the federal government will actively intervene to reshape critical mineral markets.

The U.S. has also established cooperation agreements with key allies including Australia, Japan, and Malaysia, reinforcing a non-China supply network. This geopolitical alignment strengthens the long-term investment case for North American and allied-jurisdiction producers, who now benefit from both policy support and structural demand shifts.

Project Vault is more than a stockpile—it’s a demand guarantee underwritten by the U.S. government. For small-cap investors, this could mark the start of a sustained revaluation cycle for select critical mineral producers, particularly those nearing production or capable of supplying rare earths and strategic metals domestically.

The framework changes the risk-reward equation. Companies with credible projects in favorable jurisdictions now have a potential counterparty whose commitment extends beyond market cycles. That’s a fundamentally different investment environment than what existed even six months ago.

Bottom Line

Selectivity remains essential—not every critical mineral stock will benefit equally. But the broader narrative is unmistakable: critical minerals have moved from niche sector to national priority, and the market is already repricing accordingly.

For investors positioned in quality small-cap producers, Project Vault may prove to be the catalyst they’ve been waiting for.

Fourth quarter 2025 net income of $82.7 million and Adjusted EBITDA of $191.1 million, up 406.2% and 54.1%, respectively, year-over-year

Record full year and fourth quarter 2025 oil & gas royalty volumes, up 7.2% and 20.2%, respectively, year-over-year

Fourth quarter 2025 coal production volumes increased to 8.2 million tons produced, representing a year-over-year increase of 18.7%

Full year 2025 total revenue of $2.2 billion, net income of $311.2 million, and Adjusted EBITDA of $698.7 million

Total and net leverage ratios as of December 31, 2025, were 0.66 times and 0.56 times, respectively

On January 27, 2026, declared quarterly cash distribution of $0.60 per unit, or $2.40 per unit annualized

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported financial and operating results for the quarter and full year ended December 31, 2025 (the “2025 Quarter” and “2025 Full Year”, respectively). This release includes comparisons of results to the quarter and year ended December 31, 2024 (the “2024 Quarter” and “2024 Full Year”, respectively), as well as to the quarter ended September 30, 2025 (the “Sequential Quarter”). All references in the text of this release to “net income” refer to “net income attributable to ARLP.” For a definition of Adjusted EBITDA and Segment Adjusted EBITDA Expense and related reconciliations to comparable GAAP financial measures, please see the end of this release.

For the 2025 Quarter net income increased $66.3 million to $82.7 million, or $0.64 per basic and diluted limited partner unit, compared to $16.3 million, or $0.12 per basic and diluted limited partner unit for the 2024 Quarter as a result of reduced operating expenses, lower impairment charges and increased investment income, partially offset by lower revenues and a decrease in the fair value of our digital assets during the 2025 Quarter. Total revenues decreased 9.2% to $535.5 million in the 2025 Quarter compared to $590.1 million for the 2024 Quarter primarily due to lower coal sales and transportation revenues, partially offset by record oil & gas royalty volumes. Adjusted EBITDA increased 54.1% to $191.1 million in the 2025 Quarter compared to $124.0 million in the 2024 Quarter.

Compared to the Sequential Quarter, total revenues decreased by 6.3% due to lower coal sales volumes and prices, partially offset by higher other revenues. Net income decreased by 13.1% compared to the Sequential Quarter as a result of lower revenues and a decrease in the fair value of our digital assets, partially offset by reduced operating expenses and increased investment income. Adjusted EBITDA for the 2025 Quarter increased by 2.8% compared to the Sequential Quarter.

Total revenues decreased 10.4% to $2.19 billion for the 2025 Full Year compared to $2.45 billion for the 2024 Full Year primarily due to lower coal sales pricing and transportation revenues. Net income for the 2025 Full Year was $311.2 million, or $2.40 per basic and diluted limited partner unit, compared to $360.9 million, or $2.77 per basic and diluted limited partner unit, for the 2024 Full Year as a result of lower revenues and a decrease in the fair value of our digital assets in the 2025 Full Year, partially offset by reduced operating expenses and increased investment income. Adjusted EBITDA for the 2025 Full Year was $698.7 million compared to $714.2 million for the 2024 Full Year.

CEO Commentary

“Our team delivered solid performance to close out the fourth quarter and full year,” commented Joseph W. Craft III, Chairman, President and Chief Executive Officer. “We achieved record Oil & Gas royalty volumes, underscoring the quality of our minerals portfolio. In our coal operations, the Illinois Basin continued to perform well, highlighted by Hamilton’s record year for clean tons and yield. While Appalachia costs increased sequentially primarily due to an unplanned outage at a key customer’s plant that required production adjustments at Mettiki and lower recoveries at Tunnel Ridge, we expect Appalachia costs to improve in 2026 as mining progresses in the new district at Tunnel Ridge.”

Mr. Craft continued, “Industry fundamentals strengthened during the quarter. The December 2025 PJM capacity auction for 2027-2028 delivery years cleared at the FERC‑approved cap across the entire region, with every megawatt of coal capacity selected. At the same time, reserve margins fell below PJM targets, reinforcing the critical need to keep existing, reliable baseload resources online as data center and industrial load growth accelerates. The Trump administration this month reestablished the National Coal Council, citing coal’s critical importance to our country’s economic competitiveness and national security, warning that the United States cannot win the global AI race without coal.”

Mr. Craft concluded, “During the fourth quarter, we also recognized investment income of $17.5 million related to our share of the increase in the fair value of a coal-fired power plant indirectly owned and operated by an equity method investee. This investment aligns with our strategy to allocate a portion of excess cash flows into investments that we believe will generate attractive returns for our unitholders.”

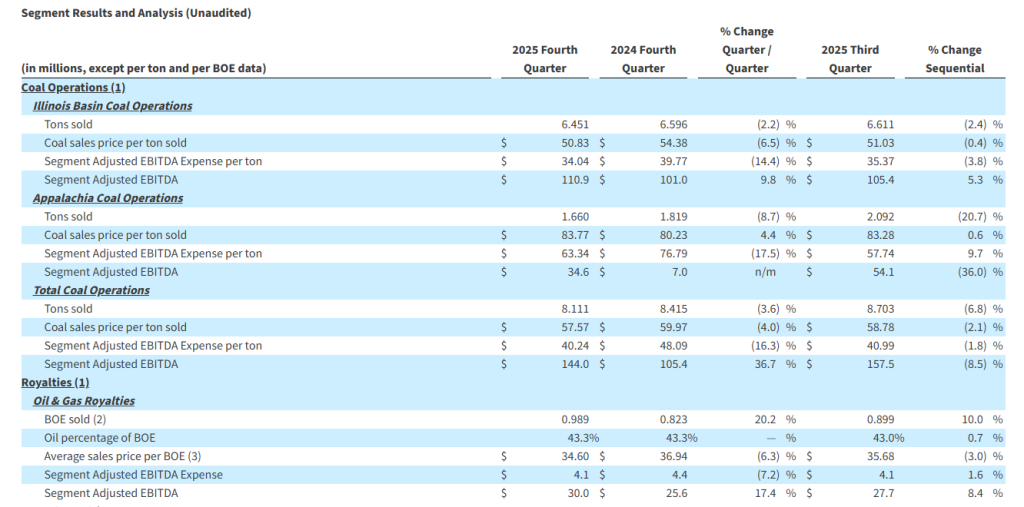

Coal Operations

Coal sales volumes decreased by 2.2% and 2.4% in the Illinois Basin compared to the 2024 Quarter and Sequential Quarter, respectively, due primarily to decreased tons sold from our River View mine as a result of transportation delays and the timing of committed sales. Reduced export sales volumes from Gibson South also contributed to the reduction in coal sales volumes in the Illinois Basin compared to the 2024 Quarter. In Appalachia, tons sold decreased by 8.7% and 20.7% compared to the 2024 Quarter and Sequential Quarter, respectively, due to reduced sales volumes across the region, primarily caused by timing of committed sales at our Mettiki mine, a longwall move at Tunnel Ridge and lower recoveries at Tunnel Ridge and Mettiki. Coal sales price per ton sold decreased by 6.5% in the Illinois Basin compared to the 2024 Quarter as a result of the expiration of higher priced legacy contracts. In Appalachia, coal sales price per ton sold increased by 4.4% compared to the 2024 Quarter primarily due to higher domestic and export pricing as well as an increased sales mix of higher priced MC Mining and Mettiki sales volumes in the 2025 Quarter. ARLP ended the 2025 Quarter with total coal inventory of 1.1 million tons, representing an increase of 0.4 million tons and 0.1 million tons compared to the end of the 2024 Quarter and Sequential Quarter, respectively.

Segment Adjusted EBITDA Expense per ton in the Illinois Basin decreased by 14.4% and 3.8% compared to the 2024 Quarter and Sequential Quarter, respectively, due primarily to increased production at our Hamilton mine resulting from fewer longwall move days and improved recoveries during the 2025 Quarter. In Appalachia, Segment Adjusted EBITDA Expense per ton for the 2025 Quarter decreased by 17.5% compared to the 2024 Quarter due to increased production at our Mettiki and MC Mining operations and higher recoveries at MC Mining and Tunnel Ridge. Compared to the Sequential Quarter, Segment Adjusted EBITDA Expense per ton increased by 9.7% in Appalachia primarily due to reduced recoveries across the region and lower production at our Mettiki and Tunnel Ridge operations.

Royalties

Segment Adjusted EBITDA for the Oil & Gas Royalties segment increased to $30.0 million in the 2025 Quarter compared to $25.6 million and $27.7 million in the 2024 Quarter and Sequential Quarter, respectively, due to record oil & gas royalty volumes, which increased 20.2% and 10.0%, respectively, partially offset by lower average sales price per BOE.

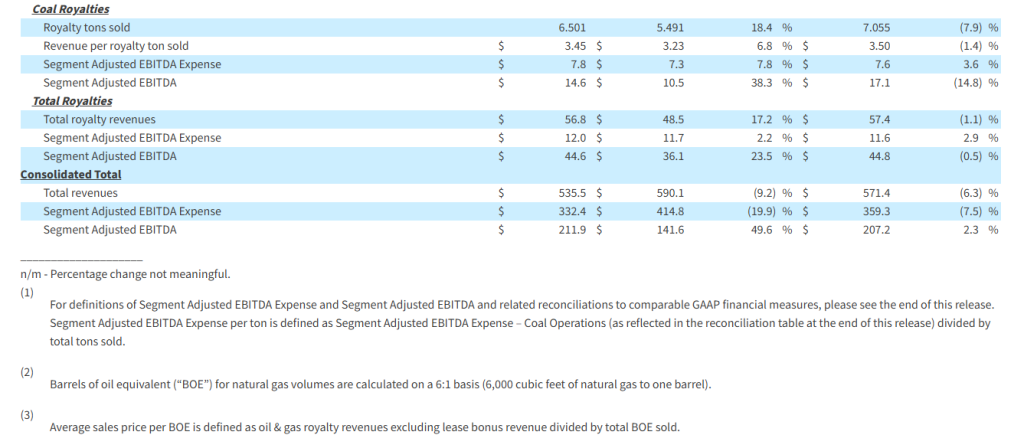

Segment Adjusted EBITDA for the Coal Royalties segment increased to $14.6 million in the 2025 Quarter compared to $10.5 million in the 2024 Quarter due to higher royalty tons sold, primarily from Tunnel Ridge, and higher average royalty rates per ton received from the Partnership’s mining subsidiaries. Compared to the Sequential Quarter, Segment Adjusted EBITDA for the Coal Royalties segment decreased 14.8% as a result of lower royalty tons sold and royalty rates per ton.

Growth Investments

During the 2025 Quarter, equity method investment income increased $22.0 million primarily driven by a higher increase in the value of our share of the net assets of the companies in which we hold interests. This included approximately $17.5 million related to our share of the increase in the fair value of a coal-fired power plant indirectly owned and operated by an equity method investee.

Balance Sheet and Liquidity

As of December 31, 2025, total debt and finance leases were outstanding in the amount of $463.7 million. The Partnership’s total and net leverage ratios were 0.66 times and 0.56 times debt to trailing twelve months Adjusted EBITDA, respectively, as of December 31, 2025. ARLP ended the 2025 Quarter with total liquidity of $518.5 million, which included $71.2 million of cash and cash equivalents and $447.3 million of borrowings available under its revolving credit and accounts receivable securitization facilities. ARLP also held 592 bitcoins valued at $51.8 million as of December 31, 2025.

Distributions

On January 27, 2026, the Board of Directors of ARLP’s general partner (the “Board”) approved a cash distribution to unitholders for the 2025 Quarter of $0.60 per unit (an annualized rate of $2.40 per unit), payable on February 13, 2026, to all unitholders of record as of the close of trading on February 6, 2026.

Outlook

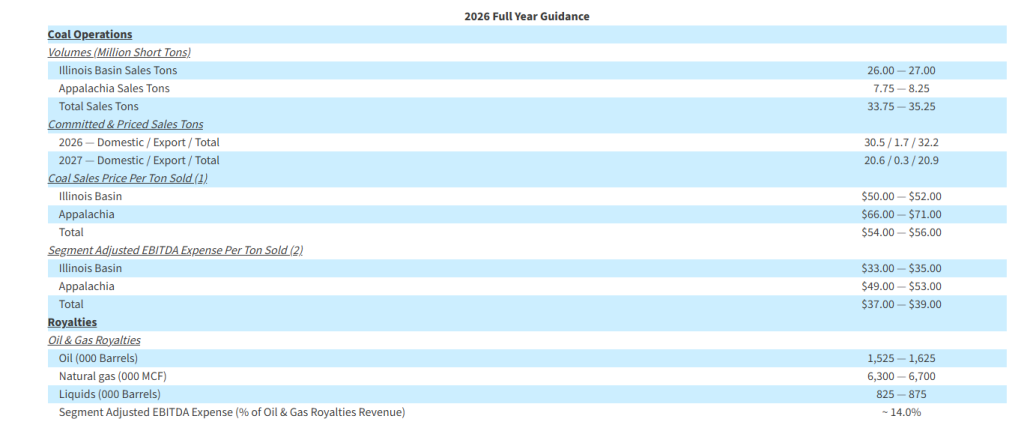

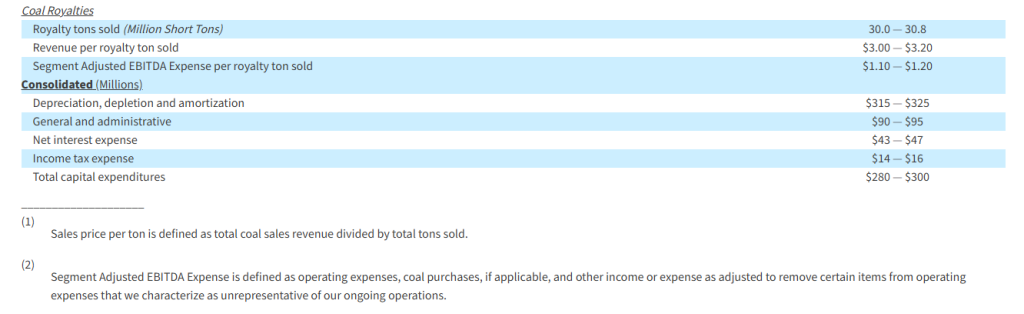

“Looking ahead to 2026, oil & gas royalty volumes are expected to be near 2025 Full Year record levels at the high end of our 2026 guidance,” commented Mr. Craft. “Over the past week, commodity benchmark pricing has been volatile, with 2026 oil futures down 3-8% and natural gas futures up 10-15% compared to 2025 averages. February Henry Hub futures climbed to $7.46 per MMBtu on its final trading day compared to $3.68 per MMBtu at the beginning of this year. Lower crude oil prices have created a softer backdrop for acquisition activity. However, we were successful in completing $14.4 million in oil & gas mineral acquisitions during the 2025 Quarter and we remain committed to growing our minerals portfolio moving forward. At the midpoint of our 2026 guidance, coal royalty tons sold are expected to be six million tons, or 25% above 2025, reflecting higher volumes at our Hamilton and Tunnel Ridge mines.”

“Turning to our coal operations, we expect another year of strong operational and financial performance as we build on the progress achieved in 2025,” continued Mr. Craft. “Our 2026 guidance reflects the anticipated impact of reduced coal sales volumes at our Mettiki mine as disclosed in last week’s WARN Act notices. Notwithstanding these reductions, our guidance reflects higher planned coal sales tons in 2026, where previous capital investments in equipment and mine development are driving meaningful productivity gains with total sales tons expected to exceed 2025 levels by 0.8 million to 2.3 million tons, primarily across the Illinois Basin and at Tunnel Ridge. Customer demand across our core markets remains strong, and we have already committed and priced more than 93% of our 2026 sales tons guidance range at the midpoint.”

Mr. Craft added, “We expect improved operating expenses per ton sold in the Illinois Basin and at Tunnel Ridge to help offset lower coal sales prices per ton sold year-over-year, supporting our efforts to preserve margins while maintaining our focus on cost discipline and execution.”

Mr. Craft concluded, “With tightening domestic coal supply, robust contracting activity, and growing electricity demand, our longer-term outlook continues to be promising. Supported by our logistical advantages, cost structure, and strong balance sheet, we believe Alliance will continue to demonstrate its ability to serve as a reliable supply partner and is preparing to meet increased customer demand.”

ARLP is providing the following guidance for the full year ending December 31, 2026:

Conference Call

A conference call regarding ARLP’s 2025 Quarter and Full Year financial results and 2026 guidance is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13757920.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the second largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is positioning itself as a reliable energy partner for the future by pursuing opportunities that support the growth and development of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial and operational performance, coal and oil & gas consumption and expected future prices, our ability to increase or maintain unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, infrastructure projects at our existing properties, growth in domestic electricity demand, preserving liquidity and maintaining financial flexibility, our future repurchases of units, and the impact of recently announced tax legislation. These risks to our ability to achieve these outcomes include, but are not limited to, the following: decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion, the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels and the planned retirement of coal-fired power plants in the U.S.; our ability to provide fuel for growth in domestic energy demand, should it materialize; changes in macroeconomic and market conditions and market volatility, and the impact of such changes and volatility on our financial position; changes in global economic and geo-political conditions or changes in industries in which our customers operate; changes in commodity prices, demand and availability which could affect our operating results and cash flows; the effects of a prolonged government shutdown; impacts of geopolitical events, including the conflicts in Ukraine and in the Middle East and the potential for conflict in Venezuela; the severity, magnitude and duration of any future pandemics and impacts of such pandemics and of businesses’ and governments’ responses to such pandemics on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers and operators, available liquidity and capital sources and broader economic disruptions; actions of the major oil-producing countries with respect to oil production volumes and prices and the direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by the operators of the properties in which we hold oil & gas mineral interests due to low commodity prices or the lack of downstream demand or storage capacity; risks associated with the expansion of and investments into the infrastructure of our operations and properties, including the timing of such investments coming online; our ability to identify and complete acquisitions and to successfully integrate such acquisitions into our business and achieve the anticipated benefits therefrom; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, Matrix Design Group, LLC, and our investments in emerging and other infrastructure and technology companies; dependence on significant customer contracts, and failure of customers to renew existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws, and the results of central bank policy actions including interest rates, bank failures, and associated liquidity risks; the effects of and changes in taxes or tariffs and other trade measures adopted or threatened by the United States and foreign governments, including the imposition of or increase in tariffs on steel and/or other raw materials; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, such as the Environmental Protection Agency’s emissions regulations for coal-fired power plants, and state legislation seeking to impose liability on a wide range of energy companies under greenhouse gas “superfund” laws, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ attention to environmental, social, and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor; our ability to maintain satisfactory relations with our employees; increases in labor costs, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortage of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these, and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2024, filed on February 27, 2025, and ARLP’s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2025, June 30, 2025 and September 30, 2025, filed on May 9, 2025, August 7, 2025 and November 7, 2025, respectively. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Phase 1b Data For Second Year After Transplantation Presented. Eledon presented data from its Phase 1b trial at the American Society of Transplant Surgeons (ASTS) meeting in January 2026. The presentation included data from 8 patients that had reached 24 months after transplantation, compared with 12 patients evaluated 12 months after transplantation presented in August 2025. These new data show a continued improvement in kidney function during the second year.

New Data Show Durability With Improvements. The 24-month data shows eGFR in tegoprubart patients continued to improve during months 12 to 24 after transplantation. The eGFR levels were restored to normal levels within 1 month after transplantation and were maintained for up to 2 years. Although this is a small number of patients, we see the result as consistent with prior data and our expectations for organ survival.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Resources Connection, Inc. provides agile consulting services in North America, Europe, and the Asia Pacific. The company offers finance and accounting services, including process transformation and optimization, financial reporting and analysis, technical and operational accounting, merger and acquisition due diligence and integration, audit readiness, preparation and response, implementation of new accounting standards, and remediation support. It also provides information management services, such as program and project management, business and technology integration, data strategy, and business performance management. In addition, the company offers corporate advisory, strategic communications, and restructuring services; and corporate governance, risk, and compliance management services, such as contract and regulatory compliance, enterprise risk management, internal controls management, and operation and information technology (IT) audits. Further, it provides supply chain management services comprising strategy development, procurement and supplier management, logistics and materials management, supply chain planning and forecasting, and unique device identification compliance; and human capital services, including change management, organization development and effectiveness, compensation and incentive plan strategies, and optimization of human resources technology and operations. Additionally, the company offers legal and regulatory supporting services for commercial transactions, global compliance initiatives, law department operations, and law department business strategies and analytics. It also provides policyIQ, a proprietary cloud-based governance, risk, and compliance software application. The company was formerly known as RC Transaction Corp. and changed its name to Resources Connection, Inc. in August 2000. Resources Connection, Inc. was founded in 1996 and is headquartered in Irvine, California.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Cost Out. Last week, RGPauthorized a reduction of its global management and administrative workforce intended to reduce cost structure through enhanced efficiencies and streamlined operations. The Company expects the reduction in force to result in annual cost savings of $6-$8 million. Restructuring charges of approximately $3 million are expected to be recognized in the third and fourth quarters of fiscal 2026. The workforce reduction should be substantially completed by the end of fiscal 2026.

Additive. Last week’s announcement is on top of the October RIF, which also is expected to yield annual savings of $6 million to $8 million. Combined, the two actions could reduce expenses in the $12-$16 million range. These efforts are part of an even deeper assessment across the entire organization to streamline organizational structure, simplify processes, and adopt automation and AI to ensure RGP’s cost structure is adequately sized to the current revenue levels.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kelly (Nasdaq: KELYA, KELYB) connects talented people to companies in need of their skills in areas including Science, Engineering, Education, Office, Contact Center, Light Industrial, and more. We’re always thinking about what’s next in the evolving world of work, and we help people ditch the script on old ways of thinking and embrace the value of all workstyles in the workplace. We directly employ nearly 350,000 people around the world and connect thousands more with work through our global network of talent suppliers and partners in our outsourcing and consulting practice. Revenue in 2021 was $4.9 billion. Visit kellyservices.com and let us help with what’s next for you.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Sale Completed. On Friday, Hunt Equity Opportunities, a subsidiary of Hunt Companies, acquired the 3,039,240 Class B shares previously held by the Terence E. Adderley Revocable Trust K. Hunt now has effective control of Kelly, as owner of 92.2% of the voting Class B shares. According to James Christopher Hunt, CEO of Hunt, “Hunt is very excited about the value creation opportunities ahead for Kelly. We look forward to supporting Chris Layden, CEO of Kelly, and the rest of the Company’s management team as they focus on accelerating growth and realizing Kelly’s full potential.”

Board Changes. As part of the transition, four Hunt designees have been named to Kelly’s Board, with five former Kelly directors leaving the Board, which will now consist of 8 members. Mr. Hunt has been named Chairman of the Board.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Gold and silver prices suffered a brutal reversal on Friday, marking one of the sharpest pullbacks in modern precious metals trading as a crowded bullish trade rapidly unwound. Gold futures plunged as much as 11%, briefly falling below $4,800 per ounce before stabilizing near $4,900, while silver collapsed more than 25% in its steepest one-day decline on record. The violent sell-off followed months of near-parabolic gains that had pushed both metals to historic highs and attracted increasingly speculative positioning.

The sudden reversal unfolded amid a broader risk-off move across global markets. Equities sold off sharply after President Trump nominated former Federal Reserve governor Kevin Warsh to succeed Jerome Powell as Fed chair, a decision markets interpreted as potentially restoring a more hawkish tilt to monetary policy. The US dollar strengthened in response, with the dollar index rising nearly 1%, adding pressure to metals that had benefited heavily from dollar weakness earlier this year.

Strategists largely agreed that the sell-off, while extreme, was not entirely unexpected. “The higher metals rise, the more likely 2026 will mark enduring price peaks — notably for silver — if history is a guide,” Bloomberg Intelligence senior commodity strategist Mike McGlone wrote, pointing to the speed and magnitude of the rally as warning signs. Gold and silver had become emblematic of the so-called “debasement trade,” fueled by expectations of aggressive rate cuts, fiscal expansion, and declining confidence in fiat currencies.

Ole Hansen, head of commodity strategy at Saxo Bank, warned earlier this week that the metals rally was entering a “dangerous phase.” According to Hansen, volatility itself became the catalyst for collapse. As price swings intensified, liquidity thinned, making the market vulnerable to forced selling. Once prices began to fall, leveraged positions were quickly unwound, accelerating losses and overwhelming buyers.

Gold’s rally had been particularly striking. Just days earlier, prices surged past $5,500 per ounce after the Federal Reserve held rates steady and Chair Jerome Powell offered limited resistance to a weakening dollar. Goldman Sachs had recently reiterated a bullish year-end target of $5,400, citing increased participation from private-sector investors and sustained demand for inflation hedges. That optimism evaporated quickly as sentiment flipped from fear of missing out to fear of being last out.

Silver’s decline was even more dramatic. After topping $120 per ounce earlier this week, the metal fell to around $87, still up roughly 28% year to date but far removed from its peak. Silver’s dual role as both a monetary and industrial metal tends to amplify volatility, and its explosive rise in 2025 left prices especially vulnerable to sharp corrections. JPMorgan analysts had cautioned earlier this month that silver had “significantly overshot” forecasted averages, even as they acknowledged the difficulty of calling a top in a momentum-driven market.

Despite the scale of the drop, some analysts argue the long-term bull case for precious metals may not be fully broken. Persistent fiscal deficits, geopolitical uncertainty, and structural shifts in global reserves could continue to support gold over time. Still, Friday’s crash served as a stark reminder that even the most compelling macro narratives can unravel quickly when trades become crowded — and that volatility cuts both ways.