Global equity funds experienced a sharp rise in inflows during the week ending November 5, signaling a renewed appetite for risk assets even as markets undergo a modest correction. According to LSEG Lipper data, investors poured $22.37 billion into global equity funds—the largest weekly allocation since early October—suggesting confidence in longer-term fundamentals despite short-term volatility.

The surge in investor enthusiasm comes as global markets digest a 1.6% decline in the MSCI World Index following last week’s record highs. Rather than retreating, many investors appear to view the dip as an opportunity to increase exposure to equities, particularly in transformative areas such as artificial intelligence. Optimism around accelerating AI-linked mergers, acquisitions, and corporate spending has continued to provide a tailwind for tech and growth-oriented sectors.

U.S. equity funds led the inflow spike, attracting $12.6 billion, also marking their strongest week since October 1. Meanwhile, investors allocated $5.95 billion to Asian equity funds and $2.41 billion to European funds, demonstrating broad global participation in the recent buying momentum.

The technology sector remained at the center of this trend, posting $4.29 billion in inflows—the largest weekly gain since at least 2022. As companies increasingly adopt AI tools, automation systems, and advanced cloud infrastructure, investors continue to position themselves ahead of long-term earnings growth tied to innovation.

Outside of equities, flows into fixed-income assets also maintained strength. Bond funds saw their 29th consecutive week of inflows, totaling $10.37 billion. Corporate bond funds drew $3.48 billion, while short-term bond funds added $2.36 billion, reflecting sustained demand for income-generating assets amid shifting rate expectations.

Money market funds saw a dramatic resurgence in popularity as well, gathering $146.95 billion, the highest level of inflows in ten months. These vehicles remain attractive for investors seeking liquidity and stability as central banks near the end of their global tightening cycles.

Meanwhile, gold and precious metals funds saw continued weakness, with withdrawals totaling $554 million for a second straight week. As risk appetite increases and real yields remain firm, interest in defensive commodities has waned, redirecting capital back into equities and fixed income.

Emerging markets also participated in the positive momentum. Emerging market equity funds recorded their second consecutive weekly inflow of $1.61 billion, though emerging market bond funds saw an outflow of $1.73 billion. This suggests a cautious but growing willingness to take equity exposure in developing regions while avoiding currency and rate-sensitive debt markets.

Taken together, the data reflects a market environment where investors are increasingly willing to deploy capital into areas tied to innovation, earnings growth, and global expansion—even as geopolitical uncertainty and short-term corrections continue. With AI driving renewed confidence and central banks shifting toward a more neutral stance, many investors appear to be positioning themselves for the next leg of the equity market cycle.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Advancing parallel projects. In addition to its exploration project in Ecuador, the company is advancing two projects in France, a gold exploration project in Brittany, and a nickel recovery project in Corsica. In October, Aurania announced a third project near Turin, Italy, where it is evaluating the recovery of nickel and cobalt from the waste tailings of the former Balangero asbestos mine. The projects in Corsica and Italy offer significant environmental benefits for the nearby communities, along with the economic benefit of recovering valuable critical metals.

Private placement financing. On November 20, Aurania announced a non-brokered private placement financing of up to 12,500,000 units at a price of C$0.12 per unit to raise gross proceeds of up to C$1,500,000. Each unit will consist of one common share and one common share purchase warrant. A warrant will entitle the holder to purchase one common share at an exercise price of C$0.25 per warrant for a period of 24 months following the closing of the offering.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Bridging the Compensation, Culture, and Compliance Gaps for Value Realization in 2025

The Healthcare and Life Sciences (HCLS) sector continues to be a powerhouse for global Mergers & Acquisitions (M&A) activity, driven by digitalization, specialized therapeutics, and the imperative for integrated care models. When European entities acquire US counterparts, the primary risk to deal value shifts from financial modeling to human capital integration. In 2025, transatlantic HCLS deals face an unprecedented trifecta of challenges: navigating the US’s competitive, burnout-driven talent market; identifying and realizing true operational synergies; and bridging the fundamental divide between US and EU compensation and benefits philosophies. Successfully integrating talent across these vastly different labor ecosystems is now the defining feature of deal success.

The Fierce Pursuit of Specialized US HCLS Talent

The US HCLS talent market in 2025 is defined by scarcity, rising costs, and high turnover – especially for highly specialized roles in advanced therapeutics, bioinformatics, and AI-driven diagnostics. Would-be European acquirers of US HCLS companies must move beyond reactive hiring to adopt future-ready strategies:

Skills-First & AI Operationalization: The industry is moving toward skills-based hiring, particularly for critical roles that drive transformation and innovation (e.g., Gene Editing, GenAI). While AI is being widely operationalized to streamline administrative burdens (scheduling, screening, drafting job descriptions), it has yet to be proven as a strategic tool for high-level talent strategy or predicting cultural fit. Smart integration plans, therefore, should prioritize leveraging AI to accelerate efficiency while reserving human expertise for assessment and strategic sourcing.

EVP and Retention over Recruitment: High turnover, burnout, and the rise of non-traditional healthcare employers (tech, consulting) have made retention the top priority. The Employer Value Proposition (EVP) must be hyper-personalized and focused on fostering Equity, Inclusion, and Belonging (EIB), shifting the focus from simply who is hired to who stays, grows, and thrives. Post-merger, US employees often prioritize clear career pathways, flexibility, and supportive management when choosing to remain with the combined entity.

Proactive Pipelining: Due to the shrinking talent pool, organizations might rely heavily on talent pipelining and targeted outbound campaigns, establishing relationships with specialized talent before roles are officially posted. Integration teams could leverage the European target’s existing academic partnerships or regional centers of excellence to feed into the US-side pipeline for highly technical roles.

Operational Synergies: A Shift to Scope and Capability

Transatlantic HCLS M&A is increasingly dominated by scope deals—acquisitions focused on new technology, market access, or specific clinical capabilities, rather than simple scale. Synergy capture in these deals is more complex and requires aggressive planning that goes beyond traditional cost-cutting:

Revenue Synergies in R&D and Market Access: The most significant value tends to be found in revenue synergies, such as combining the European acquirer’s innovative R&D capabilities and global footprint with the US target’s vast commercialization strength and specialized talent access. Due diligence must build complex synergy models to validate these revenue forecasts, which are inherently more difficult to predict than cost savings.

Consolidating Back-Office Functions: Classic operational synergies still apply, particularly in consolidating redundant non-patient-facing functions. Examples include streamlining financial administration, IT infrastructure, and back-office services like Revenue Cycle Management (RCM) or billing. This consolidation can lead to immediate cost savings and process standardization but must be executed early in the integration lifecycle to realize value.

Cultural Alignment as a Synergist: Synergy capture is often derailed by poor cultural alignment. Integration planning should prioritize blending cultural elements early on. For a European company acquiring a US firm, navigating different approaches to hierarchy, risk tolerance, and work-life balance will be crucial to retaining the very R&D or specialized operational talent the deal was meant to secure.

Navigating the Transatlantic Compensation & Benefits Chasm

The starkest challenge in harmonizing US and EU operations lies in aligning compensation, benefits, and labor practices, which reflect fundamentally different societal models:

The Salary and Contribution Divide: US salaries are generally higher, often dramatically so for specialized roles (e.g., mid-level tech salaries can show a 30–50% gap). However, the underlying employer cost structure differs significantly. US employers bear steep costs for private, market-driven healthcare ($8,000 to $16,000+ per employee annually), while EU employers bear heavy social charges and payroll contributions that fund state-backed universal healthcare and pensions. Integration teams should employ dual benchmarks, modeling both equal salaries (for equity assessment) and market-specific total compensation (for budget control).

Mandated Benefits and Labor Law: Europe offers generous, often legally mandated benefits, including a minimum of 20+ paid vacation days, comprehensive parental leave, and stricter labor protections regarding notice periods and dismissal costs. In contrast, US benefits are a competitive tool, varying widely by state and company size. Attempting to impose a US-centric “low vacation, high private insurance” model on EU operations could result in catastrophic talent loss and non-compliance with local labor law.

Compliance Complexity: The US operates under a fragmented legal structure of both federal (e.g., ACA and COBRA and state-specific laws (sick leave, minimum wage, worker classification), whereas the EU operates under centralized directives, but implementation varies across 27 Member States (e.g., Spain and Portugal requiring 14-month salaries). HR teams must deploy local expertise to avoid compliance pitfalls, particularly around worker classification and termination processes.

In conclusion, successful transatlantic HCLS M&A requires HR integration teams to treat human capital as a strategic asset, not just a line item. Value is realized when the best of both labor ecosystems is preserved, harmonizing compensation and benefits while leveraging the combined entity’s specialized talent pools through proactive, skills-focused strategies.

In the next installment of our Europe-US Cross-Border HCLS M&A series, we move from people to data, tackling the ultimate transatlantic compliance hurdle: the clash between GDPR and HIPAA. Learn how European acquirers can avoid major fines and deal breaks by meticulously auditing and integrating data governance across two radically different legal frameworks.

About the Authors:

Nathan Caliis a Managing Partner atNoble Capital Marketswith more than 18 years of Capital Markets experience. He has been a lead Managing Director/Head of the Healthcare and Life Sciences Investment Banking and Advisory franchise at NOBLE since 2017 and was previously a sell-side equity analyst for 9 years. Nathan is a Board Member of Precise Bio, a tissue engineering, biomaterials, and cell technologies company, including cardiology, orthopedics, and dermatology. He was previously a board observer of Eledon Pharmaceuticals (ELDN:NASDAQ, f.k.n.a. Anelixis Therapeutics, Inc.), a phase II biotechnology company. Prior to joining NOBLE, Nathan gained investment experience as a portfolio account analyst/manager at Franklin Templeton Investments. Nathan also currently holds series 7, 79, 86, and 87 FINRA designations.

Hinesh Patel, MCMI ChMCis a Partner in CNM LLP’sLos Angeles Office with over 20 years of experience in accounting. He leads and oversees the firm’s Accounting and Transaction Advisory practice. He brings a vast knowledge of US GAAP, technical accounting, and International Financial Reporting Standards (IFRS) reporting requirements to his role at CNM. Hinesh primarily focuses on technical accounting, IPO readiness, SEC reporting, and mergers and acquisitions. Prior to joining CNM, Hinesh worked as a Senior Manager at Deloitte with a primary focus in the technology, manufacturing, consumer business and entertainment industries for both public and private companies. He has assisted various companies through the IPO process and advised on a range of accounting services including technical accounting, financial reporting, and new business processes requirements.

Matthew (Matt) Podowitzis the founder and Principal Consultant ofPathfinder Advisors LLC, bringing experience on 400+ global M&A engagements to his clients. He specializes in the critical operational and technology aspects of M&A transactions, providing due diligence, carve-out, integration, and value creation services. Known for practical, actionable advice derived from extensive hands-on experience with healthcare and life sciences transactions, Matt helps companies, investment banks, and private equity firms navigate complex cross-border HCLS M&A through every step of the transaction lifecycle. Leveraging his perspective as a dual US/EU citizen, he provides seamless support for transactions in both markets. His background includes leadership roles at firms like Ernst & Young, Grant Thornton, and CFGI.

Chris Raphaelyis the Co-Chair ofCozen O’Connor’sHealth Care & Life Sciences Practice where he provides sophisticated transactional and regulatory counsel to an array of health care providers and investors in the health care industry. His practice focuses on mergers, acquisitions, and divestiture transactions for health care clients and the comprehensive regulatory schemes requisite to doing business in the health care space. Chris routinely handles matters involving payer negotiations, payment disputes and contract enforcement, accountable care organizations, management services organization, clinically integrated networks, value based payment arrangements, pharmacy benefit management and third party administrator contracts for self-insured employers, digital health, organizational and governance structures, HIPAA, information privacy and security, tax exemption, Stark Law, fraud and abuse matters, clinical integration, medical staff relations, facility and professional licensing, Pennsylvania’s Medical Marijuana Act, and general compliance. Prior to joining the firm, Chris served as the deputy general counsel to Jefferson Health System and general counsel to the system’s accountable care organization and captive professional liability insurance companies.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

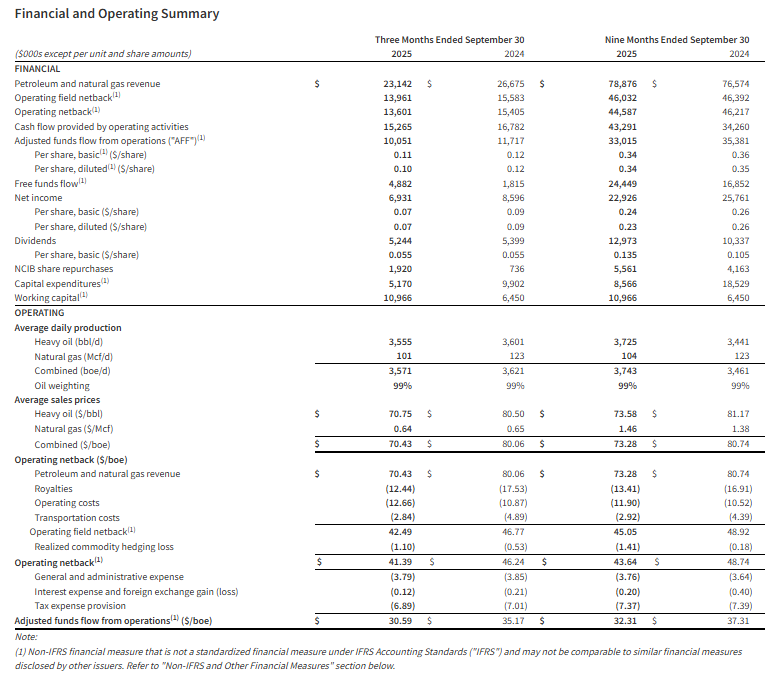

Third quarter financial results. Hemisphere reported revenue of C$23.1 million in Q3, down from C$26.7 million in the prior-year period, but slightly above our estimate of C$21.6 million, due to better-than-expected pricing. Net income totaled C$6.9 million, or C$0.07 per share, compared to C$8.6 million, or C$0.09 per share, last year, and in line with our forecast of C$6.9 million, or C$0.07 per share. Average daily production of 3,571 boe/d (99% heavy oil) declined 1% year-over-year due to summer workover downtime, but wasn’t far off from our estimate of 3,606 boe/d. Adjusted funds flow (AFF) from operations was C$10.1 million, or C$0.10 per share, roughly in line with our estimate of C$10.0 million, or C$0.10 per share.

Updating estimates. Reflecting slightly better than expected Q3 results but modestly lower 2025 production guidance of 3,600–3,700 boe/d, we are adjusting our full-year forecasts. We now expect 2025 revenue of C$92.7 million, compared to our prior estimate of C$93.7 million. Our operating cost assumption increased modestly to C$38.1 million from C$37.9 million. We now project 2025 net income of C$26.5 million, or C$0.27 per share, versus our previous forecast of C$27.4 million, or C$0.27 per share. AFF is projected at C$40.0 million, up from our earlier estimate of C$41.0 million. For 2026, we are holding our forecast steady with revenue of C$93.7 million, net income of C$27.7 million, or C$0.29 per share, and AFF of C$39.7 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong Q3 results. The company reported Q3 revenue of $97.6 million and adj. EBITDA of $26.7 million. While revenue was slightly below our estimate of $100.0 million, adj. EBITDA strongly outperformed our estimate of $7.2 million. Notably, the strong adj. EBITDA figure was largely driven by more efficient use of marketing spend, which decreased by 43% from the year earlier comparable period.

Key operating metrics. Bookings and monthly paying users (MPU) decreased by 4% and 16%, respectively, compared with the prior year period, but the decrease was expected as the company is focused on the quality of gameplay and retaining high-quality users. Furthermore, the company’s strategy is showing early signs of success, as average bookings per paying user (ABPPU) increased from $92 in Q3’24 to $107 in Q3’25.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The Federal Reserve’s latest Beige Book, released Wednesday, paints a picture of an economy losing momentum as 2025 draws to a close. With consumer spending weakening, hiring slowing, and businesses facing persistent cost pressures, the report arrives at a critical moment: just two weeks before the Fed’s next interest rate decision — and during a time when official data remains delayed due to a record-long government shutdown.

The Beige Book, which compiles anecdotal insights from businesses across all 12 Federal Reserve districts, showed that consumer spending declined further during the first half of November. Retailers reported softer foot traffic and more price-sensitive consumers, a sign that household budgets may be tightening again after a relatively steady summer.

At the same time, the US labor market — which has remained resilient for years — is now showing clearer signs of softening. According to the report, employers are scaling back hiring, implementing freezes, and trimming hours. Some firms indicated they were only replacing departing employees rather than adding new roles, while others attributed reduced hiring needs to efficiency gains from artificial intelligence, which is increasingly being used to automate entry-level or repetitive tasks.

Rising health insurance premiums are adding to the strain, increasing labor costs even as companies attempt to limit headcount.

Tariffs and Costs Keep Inflation Sticky, Even as Demand Softens

On the inflation front, the Beige Book noted that tariffs have pushed input costs higher for manufacturers and retailers, though companies vary in how much they pass along to consumers. Some are raising prices selectively based on customer sensitivity, while others feel strong competitive pressure to absorb the costs — squeezing profit margins.

However, the report also showed that prices for some materials have declined due to sluggish demand, delayed tariff implementation, or reduced tariff rates. This mixed environment reflects the broader disinflation trend the Fed has been monitoring closely.

Still, most businesses expect cost pressures to continue, even if they are hesitant to raise prices significantly in the near term.

Why the Beige Book Matters: Rising Odds of a December Rate Cut

With many government economic indicators delayed, the Beige Book is now one of the few timely sources of insight available to the Fed ahead of its December 10 policy meeting. And based on the slowdown in both spending and hiring, investors are increasingly convinced that the central bank will act.

Market expectations for a December rate cut climbed above 85%, rising sharply this week following comments from multiple Fed officials. New York Fed President John Williams said there is “room” for a near-term cut, while San Francisco Fed President Mary Daly and Fed Governor Chris Waller both signaled concern about the softening labor market.

However, not all policymakers agree. Boston Fed President Susan Collins and Kansas City Fed President Jeff Schmid have urged caution, pointing to mixed inflation signals and warning against moving too quickly.

With consumer spending cooling, hiring softening, and inflation pressures lingering, the Fed’s Beige Book suggests an economy that is decelerating — but not collapsing. Whether that slowdown is enough to justify a December rate cut will be decided in less than two weeks, making this one of the most pivotal policy moments of the year.

Vancouver, British Columbia–(Newsfile Corp. – November 25, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) provides its financial and operating results for the three and nine months ended September 30, 2025, declares a quarterly dividend payment to shareholders, and provides an operations update.

Q3 2025 Highlights

Attained quarterly production of 3,571 boe/d (99% heavy oil).

Generated quarterly revenue of $23.1 million.

Achieved total operating and transportation costs of $15.50/boe.

Delivered operating netback1 of $13.6 million or $41.39/boe for the quarter.

Realized quarterly adjusted funds flow from operations (“AFF”)1 of $10.1 million or $30.59/boe.

Initiated a 2025 fall drilling program with $5.2 million in capital expenditures1.

Generated quarterly free funds flow1 of $4.9 million.

Exited the third quarter with a positive working capital1 position of $11.0 million.

Paid a special dividend of $2.9 million ($0.03/share) to shareholders on August 15, 2025.

Paid a quarterly base dividend of $2.4 million ($0.025/share) to shareholders on September 12, 2025.

Purchased and cancelled 1.0 million shares for $1.9 million under the Company’s Normal Course Issuer Bid (“NCIB”).

Renewed the Company’s NCIB.

(1) Operating netback, adjusted funds flow from operations (AFF), free funds flow, capital expenditures, and working capital are non-IFRS measures, or when expressed on a per share or boe basis, non-IFRS ratio, that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Non-IFRS financial measures and ratios are not standardized financial measures under IFRS and may not be comparable to similar financial measures disclosed by other issuers. Refer to the section “Non-IFRS and Other Specified Financial Measures”.

Selected financial and operational highlights should be read in conjunction with Hemisphere’s unaudited condensed interim consolidated financial statements and related notes, and the Management’s Discussion and Analysis for the three and nine months ended September 30, 2025 which are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Quarterly Dividend

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on December 30, 2025 to shareholders of record as of the close of business on December 9, 2025. The dividend is designated as an eligible dividend for income tax purposes.

With the payment of the fourth quarter dividend, Hemisphere anticipates returning a minimum of $21.6 million to shareholders in 2025, including $9.6 million in quarterly base dividends, $5.8 million in two special dividends, and $6.2 million through NCIB share repurchases and cancellations. Based on the Company’s current market capitalization of $205 million (94.6 million shares issued and outstanding at a market close price of $2.17 per share on November 24, 2025), this represents an annualized yield of 10.5% to Hemisphere’s shareholders.

Operations Update

During the third quarter of 2025, Hemisphere’s production averaged 3,571 boe/d (99% heavy oil), representing a slight decrease of approximately 1% from the same period in 2024. The Company completed a number of workovers during the summer months, which contributed to production downtime during the quarter. However, September production of approximately 3,800 boe/d (99% heavy oil) was back in line with average levels of 3,830 boe/d (99% heavy oil) during the first six months of the year. This performance highlights the stability and low-decline characteristics of Hemisphere’s polymer flood assets in Atlee Buffalo, particularly given that no new wells had been placed on production since the Company’s third-quarter drilling program in 2024.

Throughout 2025, Hemisphere has taken a cautious approach to capital spending amid volatility in the global economy and oil markets, which resulted in delaying its drilling program until later in the year. In September the Company commenced a fall drilling program, which finished in early November. The new wells have just recently been put on production and will continue to be optimized over the coming months.

In October, Hemisphere successfully completed a scheduled facility turnaround and resolved unexpected issues with its power generation and injection systems. Although this short-term disruption will affect overall fourth-quarter production, all systems are now fully operational. November production has averaged approximately 3,800 boe/d (99% heavy oil, field estimate from November 1-22, 2025). Management anticipates fourth-quarter production will range between 3,400 – 3,500 boe/d (99% heavy oil) following this outage.

At the Company’s Marsden, Saskatchewan property, Hemisphere is continuing to evaluate its polymer pilot project. It has been approximately one year since injection commenced, and while an oil production response has not yet been noted, the data being collected is providing insights into reservoir performance. The Hemisphere team plans to advance its pilot project by evaluating the potential effects of producer/injector well spacing, polymer type and injection water, as well as reservoir heterogeneity and composition.

During its fall drilling program, Hemisphere attempted to test a second oil-bearing zone within its Marsden landbase. Unfortunately, drilling challenges prevented Hemisphere from being able to access the reservoir, and the Company is reviewing alternatives for future evaluation of the prospect.

Management anticipates WTI oil prices will average close to US$65 per barrel in 2025 and expects to exceed Hemisphere’s adjusted funds flow guidance estimate of $40 million for this price scenario, while projecting total capital expenditures to be on budget. This outlook holds despite the Company deferring its drilling program until late in the third quarter and experiencing unscheduled production downtime in the second half of the year. As a result, Hemisphere now estimates average annual 2025 production will be approximately 3,600 – 3,700 boe/d (99% heavy oil), compared to its original guidance of 3,900 boe/d (99% heavy oil).

The Company expects to release details on its 2026 guidance in January as part of its forward development planning. Supported by approximately $11 million in working capital, an undrawn credit facility, and strong cash flow from its low-decline production base, Hemisphere is well positioned with a robust balance sheet to pursue potential acquisition opportunities while continuing to deliver shareholder returns.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood enhanced oil recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Americans hitting the road for Thanksgiving are getting an unexpected gift this year: significantly cheaper gas. For the first time in several years, more than half of U.S. states now report average gasoline prices below $3 per gallon — a welcome relief as millions prepare for the busiest travel week of the holiday season.

According to AAA, the national average sits at $3.05 per gallon, almost identical to this time last year. But the national figure doesn’t tell the full story. Twenty-eight states — especially across the Midwest, Great Plains, and Gulf Coast — have already fallen below $3. Some stations in Oklahoma have even posted $1.99 per gallon, marking the first sustained return of sub-$2 fuel since 2021.

Why Prices Are Falling — and Why Investors Care

Although seasonal patterns always help bring prices down in late fall, this year’s decline is being driven more directly by market forces that investors are watching closely. As colder weather approaches, drivers naturally consume less fuel, and refineries switch to winter blends that cost less to produce. These shifts usually bring moderate price relief.

But this time, the move is more significant because crude oil prices have been trending sharply downward. Both Brent and West Texas Intermediate — the world’s key oil benchmarks — have dropped more than 17% since January. Negotiations surrounding a potential peace plan between Ukraine and Russia have reduced geopolitical pressure on oil supply, causing traders to unwind long positions and reassess risk premiums.

For the energy sector, these developments have created a very different landscape than earlier in the year. Falling crude prices generally translate into softer revenue outlooks for oil producers, refiners, and integrated energy companies. As a result, energy stocks — which were among the strongest performers in previous cycles — have been trading with heightened volatility. Investors watching tickers like XOM, CVX, MPC, VLO, and major ETF benchmarks such as XLE are seeing direct impacts from this price retreat.

Market Opportunities and Risks

Lower gas prices often boost consumer spending in other categories, potentially supporting retail, travel, and hospitality stocks. But the inverse is true for segments tied to crude oil production. Drillers, exploration companies, and refiners tend to experience narrowing margins when crude prices decline.

However, for long-term investors, falling prices can also create strategic entry points into quality energy names. Historically, the energy sector has been one of the most cyclical in the market, and downturns have often preceded periods of renewed growth — especially when global demand rebounds or supply conditions tighten.

The Broader Economic Picture

California and Washington remain outliers with prices above $4 per gallon, but across most of the U.S., the current price movements are easing pressure on households that have been battling inflation on multiple fronts. With oil markets stable and demand softening as winter approaches, analysts expect gas prices to trend even lower heading into Christmas.

For consumers, it means more affordable travel. For markets, it signals shifting momentum in the energy sector. And for investors, it highlights a key moment to assess where the next opportunity might emerge — whether in undervalued energy stocks, travel-sector plays that benefit from lower fuel costs, or diversified holdings that capture both trends.

As the holiday season begins, falling gas prices are offering immediate relief on the road and setting the stage for important shifts in the energy and stock markets.

Codere Online refers, collectively, to Codere Online Luxembourg, S.A. and its subsidiaries. Codere Online launched in 2014 as part of the renowned casino operator Codere Group. Codere Online offers online sports betting and online casino through its state-of-the art website and mobile application. Codere currently operates in its core markets of Spain, Italy, Mexico, Colombia, Panama and the City of Buenos Aires (Argentina). Codere Online’s online business is complemented by Codere Group’s physical presence throughout Latin America, forming the foundation of the leading omnichannel gaming and casino presence in the region.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 Results. The company reported Q3 revenue of €51.6 million, essentially flat with the prior year period and below our estimate of €56.0 million. Adj. EBITDA of €2.9 million was modestly better than our estimate of €2.6 million. Notably, when excluding the impact of the Mexican Peso devaluation in Q3, revenue was up roughly 3% over the prior year period.

Solid fundamentals. Notably, while the company benefited from an 11% increase in monthly active customers, it was largely offset by a 10% decrease in monthly average spend, primarily attributed to the Mexican Peso devaluation. Moreover, the company recorded 85,000 first-time deposit customers in Q3, a 26% y-o-y. Importantly, the company’s cost per acquisition was €167, which is its lowest since Q1 2023.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Progress on multiple fronts. Century Lithium’s 100%-owned Angel Island Lithium Project hosts one of the largest known sediment-hosted lithium resources in the United States. Century is advancing an integrated end-to-end solution to convert lithium-bearing claystone into battery-grade lithium carbonate. Century has completed and submitted all baseline and environmental studies to the U.S. Bureau of Land Management (BLM) in advance of Angel Island’s Plan of Operations and is working on an update to the 2024 Feasibility Study. Submission of the Plan of Operations will begin the federal permitting process under the National Environmental Policy Act.

Demonstration plant. The company has relocated its Demonstration Plant from Amargosa Valley, Nevada, to its 20-acre facility at the Tonopah Airport, where it will continue research, development, and material handling. The relocation is intended to consolidate operations, improve logistical efficiency, and lower costs.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Awards. With the Federal government once again open, contract awards are once again being announced by the Department of War. VVX’s award momentum continues, providing the Company with a solid base of business going into 2026, in our view.

Iraq F-16. On November 20th, subsidiary Vectrus Systems LLC. was awarded a $252.1 million cost-plus fixed-fee indefinite contract action for base support services in support of the Iraq F-16 program. Recall, this is one of the major $1 billion-plus contracts V2X has recently won. This contract provides for base operating support, base life support, and security services at the Martyr BG Ali Flaih Air Base in Iraq, and is expected to be complete by September 24, 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Modest Q3 results. SEGG’s reported modest revenues and an operating loss for its Q3. The financial performance underscores the early-stage nature of the business and reflects the limited current monetization across its portfolio. We did not anticipate that the Q3 financial results were going to be meaningful. More importantly, are the steps that the company is taking to make acquisitions and build its businesses.

All-Sports facility pushed out. The company’s venture to launch its All-Sports Arena in Boca Raton appears to be stalled as it negotiates a broader lease arrangement with the landlord, seeking as much as 140,000 square feet instead of the original 100,000 square feet. This broader arrangement should allow a better customer experience, given the ability to add more experiential components, such as Formula I simulators.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Final Permitting Pathway for Industrial-Scale Facility. Comstock Metals received eligibility for its Air Quality Permit from the Nevada Division of Environmental Protection (NDEP), completing the major regulatory requirements needed to commission its 100,000-ton-per-year solar panel recycling facility in Silver Springs, Nevada. The approval keeps commissioning on track for the first quarter of 2026, with equipment deliveries expected before year-end. The facility is designed to process more than three million end-of-life panels annually using Comstock’s certified zero-landfill system that recovers aluminum, glass, silver, and other metals. We expect the facility to begin ramping up operations during the second quarter of 2026.

A Leading U.S. Solar Recycling Platform. This marks the first industrial solar recycling air permit issued in Nevada and reinforces Comstock’s leading position to accommodate a growing national waste stream. With most legacy U.S. solar panels deployed across Nevada, California, and Arizona, the Silver Springs, Nevada hub positions Comstock to serve more than half of the domestic decommissioning market. The Comstock Metals team is evaluating additional processing and storage locations to support broader expansion as panel retirements accelerate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.