Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Transformation Plan on Track. The enterprise transformation is now roughly 70% complete. Notably, the diversification is away from the automotive industry. Of the $160 million (peak value) of new wins over the past seven quarters, one-quarter are non-auto, and about half of the pipeline is now in non-auto verticals.

New Business. NN shifted the business development focus to closing and winning immediate ramp up sales, given the softness in certain end markets. The Company now has 120 programs that are ramping up this year worth $55 million in annualized sales, an increase over the 50 programs reported at the end of 4Q24.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – US and China agreed to a 90-day truce slashing tariffs, sparking a major market rally. – Retailers and energy stocks surged as sectors hit hardest by tariffs saw renewed investor interest. – Investors should remain cautious, as the deal is temporary and economic data will shape the next move.

Markets exploded higher Monday as Wall Street celebrated a surprise truce between the United States and China, easing months of investor anxiety over escalating tariffs. The temporary agreement—which reduces reciprocal tariffs and establishes a 90-day negotiation window—was met with enthusiasm from institutional and retail investors alike. But while the relief rally was immediate and broad-based, the question remains: is this just a short-term bounce, or the start of a more durable rebound?

Under the new deal, the U.S. will slash tariffs on Chinese imports from 145% to 30%, while China will reduce its levies on American goods from 125% to 10%. That’s a dramatic step down in trade barriers, at least temporarily, and it caught markets off guard. The Dow Jones surged over 1,000 points, the S&P 500 gained 2.9%, and the tech-heavy Nasdaq led the charge with a nearly 4% jump.

Big Tech names that had been under pressure from trade war concerns—like Nvidia, Apple, and Amazon—posted strong gains. However, it wasn’t just megacaps moving higher. The broad nature of the rally suggests optimism is spilling over into sectors that were directly affected by tariffs, including retail, manufacturing, and commodity-linked industries.

Retailers in particular could be big winners. Analysts at CFRA and Telsey Advisory Group noted that the tariff pause may have “saved the holiday season,” allowing companies to import critical inventory at lower costs just in time for the back-to-school and Christmas shopping periods. Companies such as Five Below, Yeti, and Boot Barn all saw noticeable gains on the news.

Oil prices also responded positively, with West Texas Intermediate crude climbing over 2% as traders embraced a “risk-on” environment. This could bode well for small energy producers and service firms that had been squeezed by demand worries tied to trade tensions.

Still, not everyone is celebrating unconditionally. Federal Reserve Governor Adriana Kugler warned that tariffs, even at reduced levels, still act as a “negative supply shock” that may push prices higher and slow economic activity. With inflation data, retail sales, and producer prices all set to drop later this week, investors will soon get a better sense of the underlying economic landscape.

For investors, this is a critical moment to reassess market exposure. While the 90-day truce is a positive step, it’s a temporary one. Volatility could return quickly if trade talks stall or inflation surprises to the upside. Still, the sharp market reaction highlights that sentiment had grown too pessimistic—and that even incremental progress can unlock upside.

If the rally holds, it could mark a broader shift in market tone heading into summer. For now, the rebound has begun. Whether it continues depends on what comes next from Washington and Beijing.

Key Points: – April’s CPI showed the slowest annual increase since February 2021, offering some relief from persistent inflation pressures. – Core categories like shelter, medical care, and some food items continue to climb, keeping financial strain high for many consumers. – The full effect of President Trump’s new tariffs hasn’t materialized in CPI data yet—future inflation may hinge on trade policy outcomes.

Inflation in the United States slowed in April to its lowest annual rate in over four years, offering a tentative sign of relief for policymakers and consumers alike. But under the surface, essential costs—like food, shelter, and medical care—continued to pressure household budgets, highlighting the uneven nature of disinflation in the current economic environment.

According to data released Tuesday by the Bureau of Labor Statistics, the Consumer Price Index (CPI) rose 2.3% over the previous year, down slightly from March’s 2.4%. This marks the smallest annual increase since February 2021. On a monthly basis, prices ticked up 0.2%, lower than economists’ expectations and a deceleration from previous months.

The slowdown comes amid heightened attention to President Donald Trump’s recent tariffs, which began to take effect in April. So far, their full impact has not shown up in inflation data, but analysts warn the effects may be delayed. “There isn’t a lot of evidence of tariffs boosting the CPI in April, but this shouldn’t be surprising—it takes time,” noted Oxford Economics’ Ryan Sweet.

Despite the broad deceleration in inflation, many everyday necessities remain stubbornly expensive. Shelter costs, which make up about a third of the CPI basket, rose 0.3% month-over-month and 4% from the previous year—still the largest contributor to overall inflation.

Medical care was another driver, rising 0.5% in April and 3.1% annually. Hospital services and nursing home care climbed even more sharply, up 3.6% and 4.6%, respectively. Prescription drug prices were also up, increasing 0.4% month-over-month.

Food prices presented a mixed picture. Grocery costs declined 0.4% from March, led by significant drops in prices for eggs, cereal, and hot dogs. Yet key categories such as meat and dairy remain well above year-ago levels. Ground beef prices, for instance, are 10% higher than this time last year, and steaks are up 7%.

Eating out also continues to climb in cost, with restaurant prices rising 0.4% in April and nearly 4% over the past year.

Consumer goods categories like furniture, bedding, appliances, and toys—some of which are most directly impacted by tariffs—showed modest increases in April. Furniture and bedding prices rose 1.5%, while appliances were up 0.8%.

Although tariffs were initially expected to drive prices higher more broadly, the effect may be blunted or deferred due to a 90-day pause recently announced by the White House, applying to most countries except China. A baseline 10% duty remains in place globally, leaving future pricing trends dependent on trade policy developments.

While the latest inflation report offers encouraging signs that price pressures are easing, the Federal Reserve is unlikely to pivot its interest rate policy soon. Inflation remains above the Fed’s 2% target, and “core” inflation—excluding food and energy—remained flat at 2.8% year-over-year.

For American households, modest relief at the gas pump or in the grocery aisle may be welcome, but rising healthcare and housing costs continue to erode real income gains. The road to price stability is still uncertain—and the next few months will be critical in determining whether inflation has truly turned a corner or is merely catching its breath.

FDA PDUFA goal date of August 15, 2025, for TNX-102 SL for the management of fibromyalgia; if approved, TNX-102 SL would become the first new drug for treating fibromyalgia in more than 15 years

Announced positive topline results from Phase 1 study of TNX-1500, a next generation anti-CD40L mAb candidate in development for prevention of kidney transplant rejection and treatment of autoimmune disorders

Cash and cash equivalents of $131.7 million reported as of March 31, 2025; Current cash sufficient to fund operations into the second quarter of 2026

CHATHAM, N.J., May 12, 2025 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a fully-integrated biopharmaceutical company with marketed products and a pipeline of development candidates, today announced financial results for the first quarter ended March 31, 2025, and provided an overview of recent operational highlights.

“We believe TNX-102 SL (cyclobenzaprine HCl sublingual tablets)* is on track to become a new therapeutic option for patients suffering with fibromyalgia,” said Seth Lederman, M.D., Chief Executive Officer of Tonix. “TNX-102 SL would be the first member of a new class of FDA approved drugs for fibromyalgia. TNX-102 SL is a non-opioid analgesic that targets fibromyalgia’s characteristic disturbed sleep to improve the widespread pain of fibromyalgia, while also being well tolerated. Our focus continues to be on the upcoming U.S. Food and Drug Administration (FDA) Prescription Drug User Fee Act (PDUFA) goal date of August 15, 2025, for a decision on the market authorization on TNX-102 SL for the management of fibromyalgia. We are building out our commercial team for the anticipated product launch in the fourth quarter of this year. Tonix believes it has sufficient cash to fund operations beyond these key milestones.”

Dr. Lederman continued, “Beyond TNX-102 SL for fibromyalgia, we are encouraged by the continued achievements in our pipeline, including positive Phase 1 results for TNX-1500, a next generation anti-CD40L Fc-modified humanized monoclonal antibody (mAb) in development for prevention of kidney transplant rejection and pre-clinical results for TNX-801, a live-virus vaccine in development for preventing mpox and smallpox. We look forward to providing additional updates to each of these promising programs in 2025.”

TNX-102 SL (cyclobenzaprine HCl sublingual tablets): 5.6 mg, once-daily at bedtime small molecule for the management of fibromyalgia (FM) – a centrally-acting, non-opioid analgesic.

In March 2025, Tonix announced that FDA will not require an Advisory Committee meeting to discuss the Company’s New Drug Application (NDA) for TNX-102 SL for the management of fibromyalgia. The FDA previously granted Fast Track designation to TNX-102 SL for the management of fibromyalgia in 2024, a designation intended to expedite FDA review of important new drugs to treat serious conditions and fill an unmet medical need.

In December 2024, the NDA for TNX-102 SL for fibromyalgia was accepted by FDA with a PDUFA goal date of August 15, 2025. The NDA was based upon two Phase 3 studies of TNX-102 SL in fibromyalgia that showed statically significant reduction in the chronic, widespread pain associated with fibromyalgia. TNX-102 SL was generally well tolerated and has no known addictive properties. If approved by the FDA, TNX-102 SL would be the first member of a new class of tertiary amine tricyclic (TAT) non-opioid analgesic drugs for fibromyalgia and the first new drug available for treating fibromyalgia in more than 15 years. Fibromyalgia affects more than 10 million adults in the U.S., most of whom are women.

In April 2025, Tonix presented data and analyses of TNX-102 SL treatment and effects on fibromyalgia at the American Academy of Pain Medicine (AAPM) 2025 Annual Meeting, held in Austin, Texas, in a poster presentation titled, “Sublingual Cyclobenzaprine (TNX-102 SL) for Fibromyalgia: Efficacy and Safety in Two Randomized, Placebo-Controlled Trials.”

In March 2025, the Company presented data and analyses of TNX-102 SL treatment and effects on fibromyalgia at the 7th International Congress on Controversies in Fibromyalgia, held in Vienna, Austria, in an oral presentation titled, “Transmucosal Sublingual Cyclobenzaprine (TNX-102 SL) Treatment of Fibromyalgia at Bedtime to Target Non-Restorative Sleep Showed Durable Pain Reduction in Two Double-Blind Randomized Phase 3 Studies.”

TNX-102 SL in development for the treatment of acute stress reaction (ASR) and acute stress disorder (ASD), and prophylaxis against development of posttraumatic stress disorder (PTSD)

The U.S. Department of Defense-funded Optimizing Acute Stress Reaction Interventions (OASIS) trial will be conducted by the University of North Carolina under an investigator-initiated investigational new drug (IND) application. The OASIS trial will examine the safety and efficacy of TNX-102 SL to reduce adverse posttraumatic neuropsychiatric sequelae among patients in the emergency department (ED) after a motor vehicle collision. Fourteen days of bedtime TNX-102 SL will be dosed and tested in the immediate aftermath of motor vehicle collision. The study will test the potential for TNX-102 SL to target trauma-related sleep disturbance and its ability to facilitate recovery from ASR and to prevent PTSD. The program has the potential to provide military personnel with a new treatment option that improves warfighter performance and resilience when administered in the early aftermath of traumatic events in the war theater. The study is expected to be initiated in the second quarter of 2025.

TNX-1300 (recombinant double mutant cocaine esterase): under investigation for biologic for cocaine intoxication

The National Institutes of Health (NIH)’s National Institute of Drug Abuse (NIDA) previously awarded Tonix a Cooperative Agreement grant for approximately $5 million to support development of TNX-1300.

TNX-1300 has been granted Breakthrough Therapy designation by the FDA.

The Company discontinued enrollment and terminated the Phase 2 CATALYST study of its TNX-1300 double-mutant cocaine esterase 200 mg, i.v. solution product candidate for the treatment of cocaine intoxication because enrollment in this emergency department-based study was slower than projected. The Company is evaluating new study designs and new endpoints for further development of TNX-1300. The CATALYST study was not discontinued for safety or efficacy reasons.

Immunology Pipeline

TNX-1500 (anti-CD40L Fc-modified humanized monoclonal antibody): third generation anti-CD40L monoclonal antibody under investigation for prophylaxis for organ transplant rejection and treatment of autoimmune disorders.

In February 2025, Tonix announced positive topline results from its Phase 1, single ascending dose (SAD) first-in-human trial of TNX-1500 in healthy participants. The objectives of the Phase 1 trial were to assess the safety, tolerability, pharmacokinetics, and pharmacodynamics of intravenous TNX-1500, as well as to support dosing in a planned Phase 2 trial in kidney transplant recipients, pending alignment with the FDA. All objectives were met and support proceeding to a Phase 2 trial. TNX-1500 blocked the primary and secondary antibody responses to a test antigen at the 10 mg/kg and 30 mg/kg i.v. doses, showed mean half-life of 34-38 days for the 10 mg/kg and 30 mg/kg doses (supporting monthly dosing for future efficacy trials) and was generally well-tolerated with a favorable safety profile.

The first proposed indication for TNX-1500 is prophylaxis of organ rejection in adult patients receiving a kidney transplant; but multiple additional indications are possible, including the treatment of autoimmune diseases. Preclinical studies have shown that TNX-1500 maintains the activity of first-generation monoclonal antibodies (mAbs), yet with reduced risk of thrombotic complications. Pharmacokinetic data support a monthly i.v. dosing regimen. This analysis together with TNX-1500’s activity and tolerability in animal models, suggests that the protein engineering of TNX-1500’s Fc region has achieved its design goals.

Infectious Disease Pipeline

TNX-801 (recombinant horsepox virus, minimally replicative live vaccine): potential vaccine to protect against mpox and smallpox.

In April 2025, the company presented data on TNX-801 in an oral presentation at the World Vaccine Congress Washington 2025, held in Washington, D.C. The presentation titled “A Novel Single-Dose, Attenuated Live, Minimally Replicative Mpox Vaccine” highlighted positive preclinical efficacy data, demonstrating that TNX-801 protected animals from mpox and rabbitpox and was well tolerated, even in immunocompromised animals. Durable protection of rabbits from lethal rabbitpox infection was present six months after vaccination. In September 2024, Tonix announced that the WHO’s preferred target product profile (TPP), released at the WHO sponsored Mpox Research and Innovation Scientific Conference, aligns with the characteristics of TNX-801.

In March 2025, Tonix announced it was awarded a grant from the Medical CBRN Defense Consortium (MCDC) to support the development of TNX-801. The grant will allow Tonix to develop a commercialization plan for TNX-801.

Corporate and Partnerships – Recent Highlights*

In April 2025, the Company announced it has entered into a collaborative research agreement with Makana Therapeutics, a global leader in the field of xenotransplantation, to study Tonix’s anti-CD40L (CD40 ligand, also called CD154) monoclonal antibody candidate, TNX-1500, in combination with Makana’s human-compatible pig organs and cells for the treatment of organ failure. TNX-1500 is an investigational, humanized Fc-modified IgG4 anti-CD40L antibody with high affinity for CD40L. The preclinical research and development collaboration has the potential to span multiple Makana programs including kidney, heart and islet cell xenotransplant.

In April 2025, Tonix announced the launch of TONIX ONE™, a fully-integrated digital platform designed to provide resources to help patients better understand and manage their migraine condition. TONIX ONE provides an intuitive, comprehensive journey for patients by offering educational resources about migraine and the limitations of oral medications which can sometimes lead to delayed or ineffective symptom relief. The platform also connects patients directly to independent migraine specialists via telehealth services and e-prescription requests, simplifying and accelerating access to treatment.

During the first quarter of 2025, the Company announced the promotion of Siobhan Fogarty to Chief Technical Officer and the appointment of Gary Ainsworth as its new Vice President, Market Access.

Financial – Recent Highlight

As of March 31, 2025, Tonix had $131.7 million of cash and cash equivalents, compared to $98.8 million as of December 31, 2024. Net cash used in operations was approximately $16.6 million for first quarter 2025, compared to net cash used in operations of $17.6 for the same period in 2024.

On July 30, 2024, the Company entered into a Sales Agreement with AGP pursuant to which the Company may issue and sell, from time to time, shares of the Company’s common stock having an aggregate offering price of up to $250.0 million in at-the-market sales. During the three months ended March 31, 2025, the Company sold approximately 2.7 million shares of common stock for net proceeds of approximately $59.8 million. Subsequent to March 31, 2025, the Company sold 0.6 million shares of common stock under the Sales Agreement, for net proceeds of approximately $9.9 million.

The Company believes that its cash resources at March 31, 2025, along with the net proceeds of $9.9 million raised from equity offerings in the second quarter of 2025, will meet its planned operating and capital expenditure requirements into the second quarter of 2026.

Subsequent to March 31, 2025, the Company repurchased 150,000 of its shares of common stock outstanding under a share repurchase program, for a gross aggregate cost of approximately $2.9 million.

First Quarter 2025 Financial Results

Net product revenue for the first quarter 2025 was approximately $2.4 million compared to $2.5 million for the same period in 2024. Net product revenue consisted of combined net sales of Zembrace® SymTouch® and Tosymra®. Cost of Sales for the first quarter 2025 was approximately $0.9 million compared to $1.7 million for the same period in 2024.

Research and development expenses for the first quarter 2025 were $7.4 million, compared to $12.9 million for the same period in 2024. This decrease is predominantly due to decreased clinical, non-clinical, manufacturing and employee-related expenses.

Selling, general and administrative expenses for the first quarter 2025 were $10.1 million, compared to $9.3 for the same period in 2024. The increase was primarily due to an increase in sales and marketing expenses offset by a decrease in employee-related expenses resulting from a reduction in workforce in earlier 2024.

Net loss available to common stockholders was $16.8 million, or $2.84 per share, basic and diluted, for the first quarter 2025, compared to net loss of $14.9 million, or $535.72 per share, basic and diluted, for the same period in 2024. The basic and diluted weighted average common shares outstanding for the first quarter 2025 was 5,927,231 compared to 27,886 shares for the same period in 2024.

About Tonix Pharmaceuticals Holding Corp.*

Tonix is a fully integrated biopharmaceutical company focused on transforming therapies for pain management and vaccines for public health challenges. Tonix’s development portfolio is focused on central nervous system (CNS) disorders. Tonix’s priority is to advance TNX-102 SL, a product candidate for the management of fibromyalgia, for which an NDA was submitted based on two statistically significant Phase 3 studies for the management of fibromyalgia and for which a PDUFA (Prescription Drug User Fee act) goal date of August 15, 2025 has been assigned for a decision on marketing authorization. In March 2025 the FDA guided that no Advisory Committee Meeting will be required for this NDA. The FDA has also granted Fast Track designation to TNX-102 SL for the management of fibromyalgia. TNX-102 SL is also being developed to treat acute stress reaction and acute stress disorder under a Physician-Initiated IND at the University of North Carolina in the OASIS study funded by the U.S. Department of Defense (DoD). Tonix’s immunology development portfolio consists of biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is an Fc-modified humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft rejection and for the treatment of autoimmune diseases. Tonix’s infectious disease portfolio includes TNX-801, a vaccine in development for mpox and smallpox, as well as TNX-4200 for which Tonix has a contract with the U.S. Department of Defense’s (DoD’s) Defense Threat Reduction Agency (DTRA) for up to $34 million over five years. TNX-4200 is a small molecule broad-spectrum antiviral agent targeting CD45 for the prevention or treatment of infections to improve the medical readiness of military personnel in biological threat environments. Tonix owns and operates a state-of-the art infectious disease research facility in Frederick, Md. Tonix Medicines, our commercial subsidiary, markets Zembrace® SymTouch® (sumatriptan injection) 3 mg and Tosymra® (sumatriptan nasal spray) 10 mg for the treatment of acute migraine with or without aura in adults.

* Tonix’s product development candidates are investigational new drugs or biologics. Their efficacy and safety have not been established and have not been approved for any indication.

Zembrace SymTouch, Tosymra and TONIX ONE are trademarks of Tonix Medicines. All other marks are property of their respective owners.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the failure to successfully market any of our products; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2024, as filed with the Securities and Exchange Commission (the “SEC”) on March 18, 2025, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Company to Provide Corporate Updates Including New Developments, First Quarter 2025 Overview and Financial Results; Conference Call to be Held Wednesday, May 14, 2025, at 4:30 P.M. Eastern Time

May 12, 2025 16:05 ET

MIAMI, May 12, 2025 (GLOBE NEWSWIRE) — SKYX (NASDAQ: SKYX) (d/b/a “SKYX Technologies”), a highly disruptive advanced and smart home platform technology company for homes and buildings, with more than 97 issued and pending patents globally and a portfolio of over 60 lighting and home décor websites, announces today that it will host a Corporate Update call and present its first quarter 2025 overview and financial results. The conference call will be held on Wednesday, May 14, 2025, at 4:30 p.m. Eastern Time.

SKYX Participating Members will Include:

Rani Kohen, Founder and Executive Chairman

Steve Schmidt, SKYX President, (Former CEO of Nielsen Data Corporation and former President of Office Depot International)

Lenny Sokolow, Co-CEO

Marc Boisseau, CFO

SKYX Platforms – Q1 2025

Date: Wednesday, May 14, 2025 Time: 4:30 p.m. Eastern Time U.S./Canada Dial-in: 1-412-317-5180 International Dial-in: 1-844-825-9789

Please dial in at least 10 minutes before the start of the call to ensure timely participation.

A playback of the call will be available until June 14, 2025. To listen, call within the United States and Canada or when calling internationally. Please use the replay pin number 10199972. A webcast is also available at the following link: https://viavid.webcasts.com/starthere.jsp?ei=1720256&tp_key=6be89e23ca

About SKYX Platforms Corp. As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 97 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Third Quarter of Fiscal Year 2025 – Consolidated Earnings Highlights

Revenue of $408.2 million

Net income of $26.0 million

Adjusted EBITDA* of $37.7 million

Fiscal Year 2025 Guidance Ranges:

Revenue expected in a range of $1.500 billion to $1.575 billion

Net income (loss) expected in a range of $(1) million to $28 million

Adjusted EBITDA* expected in a range of $115 million to $140 million

Third Quarter Fiscal Year 2025 – Segment Highlights

Senior

Revenue of $169.4 million

Adjusted EBITDA* of $45.7 million

Approved Medicare Advantage policies of 168,001

Healthcare Services

Revenue of $189.6 million

Adjusted EBITDA* of $6.4 million

105,523 SelectRx members

Life

Revenue of $45.8 million

Adjusted EBITDA* of $6.4 million

OVERLAND PARK, Kan.–(BUSINESS WIRE)– SelectQuote, Inc. (NYSE: SLQT) reported consolidated revenue for the third quarter of fiscal year 2025 of $408.2 million compared to consolidated revenue for the third quarter of fiscal year 2024 of $376.4 million. Consolidated net income for the third quarter of fiscal year 2025 was $26.0 million compared to consolidated net income for the third quarter of fiscal year 2024 of $8.6 million. Finally, consolidated Adjusted EBITDA* for the third quarter of fiscal year 2025 was $37.7 million compared to consolidated Adjusted EBITDA* for the third quarter of fiscal year 2024 of $46.6 million.

SelectQuote Chief Executive Officer, Tim Danker, remarked, “We are very proud of the service and value we delivered to America’s seniors over this past year’s highly unique Medicare Advantage season. SelectQuote’s agent-led model paired with our technology-enabled information advantage made our platform more valuable than ever to participants in the healthcare ecosystem. Policy features changed materially and plan termination activity from carriers was significantly higher than historical averages. Through that volatility and confusion, SelectQuote’s agents again delivered remarkable and efficient service, highlighted by a 15% increase in year-over-year policy close rates. SelectQuote is organized to help each and every customer as an individual and despite significant change, our agents were able to help a higher percentage of them this year than last. Strong execution in our Senior business paired with continued performance in Healthcare Services and our Life division all contributed to successful consolidated results for our fiscal 3rd quarter.”

* See “Non-GAAP Financial Measures” below.

Segment Results

We currently have three reportable segments: 1) Senior, 2) Healthcare Services and 3) Life. The performance measures of the segments include total revenue and Adjusted EBITDA.* Costs of commissions and other services revenue, cost of goods sold-pharmacy revenue, marketing and advertising, selling, general, and administrative, and technical development operating expenses that are directly attributable to a segment are reported within the applicable segment. Indirect costs of revenue, marketing and advertising, selling, general, and administrative, and technical development operating expenses are allocated to each segment based on varying metrics such as headcount. Adjusted EBITDA is our segment profit measure to evaluate the operating performance of our business. We define Adjusted EBITDA as income (loss) before income tax expense (benefit) plus: (i) interest expense, net; (ii) depreciation and amortization; (iii) share-based compensation; (iv) goodwill, long-lived asset, and intangible assets impairments; (v) transaction costs; (vi) loss on disposal of property, equipment and software, net; (vii) other non-recurring expenses and income; (viii) changes in fair value of warrant liabilities. Adjusted EBITDA Margin is calculated as Adjusted EBITDA divided by revenue.

Senior

Financial Results

The following table provides the financial results for the Senior segment for the periods presented:

Operating Metrics

Submitted Policies

Submitted policies are counted when an individual completes an application with our licensed agent and provides authorization to the agent to submit the application to the insurance carrier partner. The applicant may have additional actions to take before the application will be reviewed by the insurance carrier.

The following table shows the number of submitted policies for the periods presented:

Approved Policies

Approved policies represents the number of submitted policies that were approved by our insurance carrier partners for the identified product during the indicated period. Not all approved policies will go in force.

* See “Non-GAAP Financial Measures” below.

The following table shows the number of approved policies for the periods presented:

Lifetime Value of Commissions per Approved Policy

Lifetime value of commissions per approved policy represents commissions estimated to be collected over the estimated life of an approved policy based on multiple factors, including but not limited to, contracted commission rates, carrier mix and expected policy persistency with applied constraints. The lifetime value of commissions per approved policy is equal to the sum of the commission revenue due upon the initial sale of a policy, and when applicable, an estimate of future renewal commissions.

The following table shows the lifetime value of commissions per approved policy for the periods presented:

Healthcare Services

Financial Results

The following table provides the financial results for the Healthcare Services segment for the periods presented:

Operating Metrics

Members

The total number of SelectRx members represents the amount of active customers to which an order has been shipped and the prescriptions per day represents the total average prescriptions shipped per business day. These two metrics are the primary drivers of revenue for Healthcare Services.

* See “Non-GAAP Financial Measures” below.

The following table shows the total number of SelectRx members as of the periods presented:

The total number of SelectRx members increased by 41% as of March 31, 2025, compared to March 31, 2024, due to our strategy to grow SelectRx membership.

The following table shows the average prescriptions shipped per day for the periods presented:

Combined Senior and Healthcare Services – Consumer Per Unit Economics

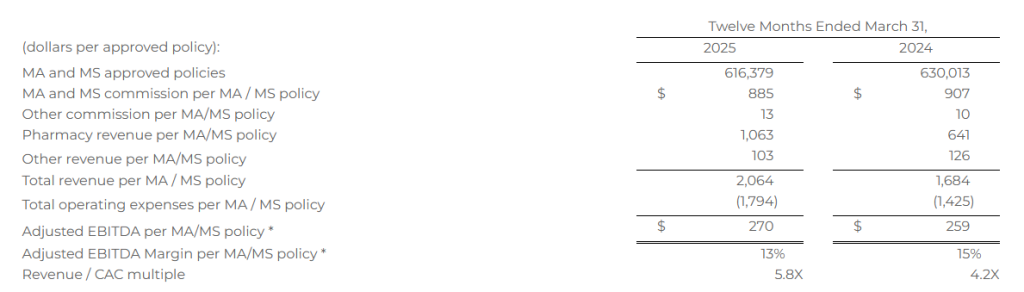

The opportunity to leverage our existing database and distribution model to improve access to healthcare services for our consumers has created a need for us to review our key metrics related to our per unit economics. As we think about the revenue and expenses for Healthcare Services, we note that they are primarily driven by the marketing acquisition costs associated with the sale of an MA or MS policy, some of which costs are allocated directly to Healthcare Services, and therefore determined that our per unit economics measure should include components from both Senior and Healthcare Services. See details of revenue and expense items included in the calculation below.

Combined Senior and Healthcare Services consumer per unit economics represents total MA and MS commissions; other product commissions; other revenues, including revenues from Healthcare Services; and operating expenses associated with Senior and Healthcare Services, each shown per number of approved MA and MS policies over a given time period. Management assesses the business on a per-unit basis to help ensure that the revenue opportunity associated with a successful policy sale is attractive relative to the marketing acquisition cost. Because not all acquired leads result in a successful policy sale, all per-policy metrics are based on approved policies, which is the measure that triggers revenue recognition.

The MA and MS commission per MA/MS policy represents the LTV for policies sold in the period. Other commission per MA/MS policy represents the LTV for other products sold in the period, including DVH prescription drug plan, and other products, which management views as additional commission revenue on our agents’ core function of MA/MS policy sales. Pharmacy revenue per MA/MS policy represents revenue from SelectRx, and other revenue per MA/MS policy represents revenue from Population Health, production bonuses, marketing development funds, lead generation revenue, and adjustments from the Company’s reassessment of its cohorts’ transaction prices. Total operating expenses per MA/MS policy represents all of the operating expenses within Senior and Healthcare Services. The revenue to customer acquisition cost (“CAC”) multiple represents total revenue as a multiple of total marketing acquisition cost, which represents the direct costs of acquiring leads. These costs are included in marketing and advertising expense within the total operating expenses per MA/MS policy.

The following table shows combined Senior and Healthcare Services consumer per unit economics for the periods presented. Based on the seasonality of Senior and the fluctuations between quarters, we believe that the most relevant view of per unit economics is on a rolling 12-month basis. All per MA/MS policy metrics below are based on the sum of approved MA/MS policies, as both products have similar commission profiles.

Total revenue per MA/MS policy increased 23% for the twelve months ended March 31, 2025, compared to the twelve months ended March 31, 2024, primarily due to the increase in pharmacy revenue. Total operating expenses per MA/MS policy increased 26% for the twelve months ended March 31, 2025, compared to the twelve months ended March 31, 2024, driven by an increase in cost of goods sold-pharmacy revenue for Healthcare Services due to the growth of the business.

Life

Financial Results

The following table provides the financial results for the Life segment for the periods presented:

Operating Metrics

Life premium represents the total premium value for all policies that were approved by the relevant insurance carrier partner and for which the policy document was sent to the policyholder and payment information was received by the relevant insurance carrier partner during the indicated period. Because our commissions are earned based on a percentage of total premium, total premium volume for a given period is the key driver of revenue for our Life segment.

The following table shows term and final expense premiums for the periods presented:

* See “Non-GAAP Financial Measures” below.

Earnings Conference Call

SelectQuote, Inc. will host a conference call with the investment community on May 12, 2025, beginning at 8:30 a.m. ET. To register for this conference call, please use this link: https://registrations.events/direct/Q4I54780976. After registering, a confirmation will be sent via email, including dial-in details and unique conference call codes for entry. Registration is open through the live call, but to ensure you are connected for the full call we suggest registering at least 10 minutes before the start of the call. The event will also be webcasted live via our investor relations website https://ir.selectquote.com/investor-home/default.aspx.

Non-GAAP Financial Measures

This release includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures. To supplement our financial statements presented in accordance with GAAP and to provide investors with additional information regarding our GAAP financial results, we have presented in this release Adjusted EBITDA and Adjusted EBITDA Margin, which are non-GAAP financial measures. These non-GAAP financial measures are not based on any standardized methodology prescribed by GAAP and are not necessarily comparable to similarly titled measures presented by other companies. We define Adjusted EBITDA as net income (loss) before income tax expense (benefit), plus interest expense, depreciation and amortization, changes in fair value of warrant liabilities, and certain add-backs for non-cash or non-recurring expenses, including restructuring and share-based compensation expenses. The most directly comparable GAAP measure is income (loss) before tax expense (benefit). We define Adjusted EBITDA Margin as Adjusted EBITDA divided by revenue. The most directly comparable GAAP measure is net income margin. We monitor and have presented in this release Adjusted EBITDA and Adjusted EBITDA Margin because they are key measures used by our management and Board of Directors to understand and evaluate our operating performance, to establish budgets, and to develop operational goals for managing our business. In particular, we believe that excluding the impact of these expenses in calculating Adjusted EBITDA can provide a useful measure for period-to-period comparisons of our core operating performance. We believe that these non-GAAP financial measures help identify underlying trends in our business that could otherwise be masked by the effect of the expenses that we exclude in the calculations of these non-GAAP financial measures. Accordingly, we believe that these financial measures provide useful information to investors and others in understanding and evaluating our operating results, enhancing the overall understanding of our past performance and future prospects. Reconciliations of net income (loss) before income tax expense (benefit) to Adjusted EBITDA are presented below beginning on page 12.

Forward Looking Statements

This release contains forward-looking statements. These forward-looking statements reflect our current views with respect to, among other things, future events and our financial performance. These statements are often, but not always, made through the use of words or phrases such as “may,” “should,” “could,” “predict,” “potential,” “believe,” “will likely result,” “expect,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “projection,” “would” and “outlook,” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature. These forward-looking statements are not historical facts, and are based on current expectations, estimates and projections about our industry, management’s beliefs and certain assumptions made by management, many of which, by their nature, are inherently uncertain and beyond our control. Accordingly, we caution you that any such forward-looking statements are not guarantees of future performance and are subject to risks, assumptions and uncertainties that are difficult to predict. Although we believe that the expectations reflected in these forward-looking statements are reasonable as of the date made, actual results may prove to be materially different from the results expressed or implied by the forward-looking statements.

There are or will be important factors that could cause our actual results to differ materially from those indicated in these forward-looking statements, including, but not limited to, the following: our reliance on a limited number of insurance carrier partners and any potential termination of those relationships or failure to develop new relationships; existing and future laws and regulations affecting the health insurance market; changes in health insurance products offered by our insurance carrier partners and the health insurance market generally; insurance carriers offering products and services directly to consumers; changes to commissions paid by insurance carriers and underwriting practices; competition with brokers, exclusively online brokers and carriers who opt to sell policies directly to consumers; competition from government-run health insurance exchanges; developments in the U.S. health insurance system; our dependence on revenue from carriers in our senior segment and downturns in the senior health as well as life, automotive and home insurance industries; our ability to develop new offerings and penetrate new vertical markets; risks from third-party products; failure to enroll individuals during the Medicare annual enrollment period; our ability to attract, integrate and retain qualified personnel; our dependence on lead providers and ability to compete for leads; failure to obtain and/or convert sales leads to actual sales of insurance policies; access to data from consumers and insurance carriers; accuracy of information provided from and to consumers during the insurance shopping process; cost-effective advertisement through internet search engines; ability to contact consumers and market products by telephone; global economic conditions, including inflation; disruption to operations as a result of future acquisitions; significant estimates and assumptions in the preparation of our financial statements; impairment of goodwill; potential litigation and other legal proceedings or inquiries; our existing and future indebtedness; our ability to maintain compliance with our debt covenants; access to additional capital; failure to protect our intellectual property and our brand; fluctuations in our financial results caused by seasonality; accuracy and timeliness of commissions reports from insurance carriers; timing of insurance carriers’ approval and payment practices; factors that impact our estimate of the constrained lifetime value of commissions per policyholder; changes in accounting rules, tax legislation and other legislation; disruptions or failures of our technological infrastructure and platform; failure to maintain relationships with third-party service providers; cybersecurity breaches or other attacks involving our systems or those of our insurance carrier partners or third-party service providers; our ability to protect consumer information and other data; failure to market and sell Medicare plans effectively or in compliance with laws; and and other factors related to our pharmacy business, including manufacturing or supply chain disruptions, access to and demand for prescription drugs, and regulatory changes or other industry developments that may affect our pharmacy operations. For a further discussion of these and other risk factors that could impact our future results and performance, see the section entitled “Risk Factors” in the most recent Annual Report on Form 10-K (the “Annual Report”) and subsequent periodic reports filed by us with the Securities and Exchange Commission. Accordingly, you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and, except as otherwise required by law, we do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise.

About SelectQuote:

Founded in 1985, SelectQuote (NYSE: SLQT) pioneered the model of providing unbiased comparisons from multiple, highly-rated insurance companies, allowing consumers to choose the policy and terms that best meet their unique needs. Two foundational pillars underpin SelectQuote’s success: a strong force of highly-trained and skilled agents who provide a consultative needs analysis for every consumer, and proprietary technology that sources and routes high-quality leads. Today, the Company operates an ecosystem offering high touchpoints for consumers across insurance, pharmacy, and virtual care.

With an ecosystem offering engagement points for consumers across insurance, Medicare, pharmacy, and value-based care, the company now has three core business lines: SelectQuote Senior, SelectQuote Healthcare Services, and SelectQuote Life. SelectQuote Senior serves the needs of a demographic that sees around 10,000 people turn 65 each day with a range of Medicare Advantage and Medicare Supplement plans. SelectQuote Healthcare Services is comprised of the SelectRx Pharmacy, a Patient-Centered Pharmacy Home™ (PCPH) accredited pharmacy, SelectPatient Management, a provider of chronic care management services, and Healthcare Select which proactively connects consumers with a wide breadth of healthcare services supporting their needs.

RESTON, Va., May 12, 2025 /PRNewswire/ — V2X, Inc. (NYSE:VVX) today announced that its Board of Directors has approved a share repurchase program under which the Company may purchase, from time to time, up to $100 million of the Company’s common stock for a three-year term ending on May 12, 2028.

Jeremy C. Wensinger, President and Chief Executive Officer of V2X stated, “We are excited to announce a $100 million share repurchase program, which reflects the strength in our business and our commitment to enhancing shareholder returns through a disciplined capital allocation strategy. We are focused on maximizing shareholder returns while investing for growth, which is supported by our strong end markets, revenue visibility, backlog, balance sheet, and high free cash flow.”

The purchases under the share repurchase program may be made from time to time (i) through open market purchases, block trades, privately negotiated transactions, one or more trading plans adopted in accordance with Rule 10b5-1 of the Securities Exchange Act of 1934, as amended, or any combination of the foregoing, in each case in accordance with applicable laws, rules and regulations or (ii) in such other manner as will comply with the provisions of the Securities Exchange Act of 1934, as amended. The timing, manner, price and amount of any share repurchases will be determined by V2X in its discretion and will be subject to market and economic conditions, prevailing share prices, loan covenants, applicable legal and regulatory requirements, alternative investment opportunities, and other factors. The share repurchase program does not require V2X to repurchase shares of its common stock and it may be amended, suspended or discontinued at any time.

About V2X V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Safe Harbor Statement Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 (the “Act”): Certain material presented herein includes forward-looking statements intended to qualify for the safe harbor from liability established by the Act. These forward-looking statements include, but are not limited to, the strength of our business, our commitment to enhancing shareholder returns, capital allocation strategy and investing for growth.

Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “could,” “potential,” “continue” or similar terminology. These statements are based on the beliefs and assumptions of the management of the Company based on information currently available to management.

These forward-looking statements are not guarantees of future performance, conditions, or results, and involve a number of known and unknown risks, uncertainties, assumptions, and other important factors, many of which are outside our management’s control, which could cause actual results to differ materially from the results discussed in the forward-looking statements. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from the Company’s historical experience and our present expectations or projections. For a discussion of some of the risks and uncertainties that could cause actual results to differ from such forward-looking statements, see the risks and other factors detailed from time to time in our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and other filings with the SEC.

We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Key Points: – Pan American buys MAG Silver in a $2.1B deal, adding a major stake in the Juanicipio mine. – Boosts silver exposure and solidifies Pan American as a leading producer in the Americas. – Positive signal for small caps as sector consolidation could drive M&A interest in junior miners.

Pan American Silver Corp. (NYSE: PAAS) has announced a definitive agreement to acquire all outstanding shares of MAG Silver Corp. (NYSEAM: MAG) in a deal valued at approximately $2.1 billion. This acquisition will grant Pan American a 44% stake in the Juanicipio mine in Mexico, a high-grade, low-cost silver operation managed by Fresnillo plc. The transaction includes $500 million in cash and 0.755 Pan American shares per MAG share, subject to proration.

For MAG shareholders, the deal offers an immediate premium of about 21% over the closing price and 27% over the 20-day volume-weighted average price as of May 9, 2025. Post-acquisition, MAG shareholders will own approximately 14% of Pan American, providing exposure to a diversified portfolio of ten silver and gold mines across seven countries.

Pan American’s acquisition of MAG Silver enhances its position as a leading silver producer. Juanicipio is expected to produce between 14.7 million and 16.7 million ounces of silver in 2025, with Pan American’s share being 6.5 to 7.3 million ounces. The mine’s cash costs and all-in sustaining costs are forecasted to range between ($1.00) to $1.00 and $6.00 to $8.00 per silver ounce sold, respectively, for 2025. Additionally, the acquisition adds 58 million ounces of silver to Pan American’s proven and probable mineral reserves, 19 million ounces to measured and indicated resources, and 35 million ounces to inferred resources.

The deal also includes MAG’s exploration projects, Deer Trail in Utah and Larder in Ontario, offering further growth opportunities. Pan American plans to leverage its experience operating in the Americas for over 30 years to integrate these assets effectively.

For junior miners and small-cap investors, this acquisition underscores the trend of consolidation in the mining industry. As larger companies seek to acquire high-quality assets, junior miners with promising projects may become attractive targets. This dynamic can lead to increased valuations for small-cap mining stocks, offering potential opportunities for investors.

However, consolidation can also lead to reduced competition and fewer standalone investment options in the junior mining space. Investors should carefully assess the implications of such deals on their portfolios, considering both the potential for gains through acquisitions and the changing landscape of available investment opportunities.

The transaction is expected to close in the second half of 2025, pending customary closing conditions, including regulatory approvals. All directors and executive officers of MAG have agreed to vote in favor of the transaction.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Initiating coverage with an Outperform rating and $23 price target. Sky Harbour Group (NYSE: SKYH) is a specialized aviation infrastructure developer focused on private and business aviation hangar facilities. It develops premium-grade hangar campuses under long-term ground lease agreements. With low land costs, tax-exempt financing, and strong tenant demand, we believe SKYH is positioned to deliver robust rental revenue growth and long-term free cash flow generation.

High-margin leasing model. Sky Harbour leases airport land at favorable long-term rates that are often under $1 per square foot annually. While only a fraction (1/4-1/3) of the land footprint is usable as rentable hangar space, this space can command upwards of $40 per square foot in rent. This creates a significant spread for SKYH. Furthermore, the company owns a prefabricated steel manufacturer, allowing for cost controls and delivery reliability.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Ocugen, Inc. is a biotechnology company focused on developing and commercializing novel gene therapies, biologicals, and vaccines. The lead product in its gene therapy program, OCU400, is in Phase 1/2 clinical trials for retinitis pigmentosa.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Clinical Programs Meet Or Beat Expected Timeframes. Ocugen reported a 1Q25 loss of $15.4 million or $(0.05) per share, consistent with our estimates. The company’s three clinical trial continue to progress on schedule, with the first BLA application expected in mid-2026. Its fourth product, OCU200, initiated Phase 1 patient treatment during the quarter. Cash balance on March 31 was $38.1 million, projected to fund operations through early FY2026.

OCU400 Trial Continues To Lead The Way. The OCU400 liMeliGhT (pronounced “Limelight”) Phase 3 trial in RP continues to enroll patients, with completion expected around YE2025. The study enrolls patients over 5 years of age with any combination of over 100 mutations that cause RP. These patients are at stages ranging from early to advanced RP.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Moving Forward. MariMed brands continue to capture more share across the markets served. The Company expanded into 70 new storefronts in the quarter. Although MariMed’s brands are already top sellers in their markets, we believe there is a significant opportunity to seize additional market share.

1Q25. Revenue in the first quarter of 2025 of $38 million was virtually unchanged from the first quarter of 2024. We had projected $38.8 million. Adjusted EBITDA was $2.56 million, down from $4.66 million last year. Reported net loss was $5.4 million, or $0.01/sh, compared to a net loss of $1.3 million, or breakeven, last year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

1Q25. In the first quarter of 2025, revenue increased $25.4 million to $302.6 million from $277.2 million in 1Q24. We had forecast revenue of $290 million. Kratos reported adjusted EBITDA of $26.7 million, compared to $26 million in 1Q24 and our $22.5 million estimate. Diluted GAAP EPS was $0.03 versus breakeven last year. Adjusted EPS was $0.12 up from $0.11 last year.

Positioning. With expectations the Defense budget will soon exceed $1 trillion and a major emphasis from the government on increasing innovation, reducing cost, increasing efficiencies, receiving more for less, and rapidly fielding relevant hardware and systems now, we believe Kratos is extremely well positioned.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kelly (Nasdaq: KELYA, KELYB) connects talented people to companies in need of their skills in areas including Science, Engineering, Education, Office, Contact Center, Light Industrial, and more. We’re always thinking about what’s next in the evolving world of work, and we help people ditch the script on old ways of thinking and embrace the value of all workstyles in the workplace. We directly employ nearly 350,000 people around the world and connect thousands more with work through our global network of talent suppliers and partners in our outsourcing and consulting practice. Revenue in 2021 was $4.9 billion. Visit kellyservices.com and let us help with what’s next for you.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 Results. The Company recorded revenue of $1.16 billion, up 11.5% year-over-year, in line with our estimate of $1.16 billion. Adj. EBITDA came in at $34.9 million, up 4.8% over the prior year period and modestly lower than our estimate of $36.5 million. Adj. EBITDA margin decreased 20 basis points to 3.0%. Furthermore, Kelly reported net income of $0.16/sh. On an adjusted basis, EPS was $0.39/sh compared to $0.56/sh last year and our estimate of $0.60/sh.

MRP Integration. The majority of MRP operations were absorbed into the SET segment. However, MRP’s Sevenstep business, along with the OCG and P&I segments, have been combined into Enterprise Talent Management (ETM). In connection with the integration and realignment, Kelly took a $10.7 million charge in the quarter.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.