Kelly (Nasdaq: KELYA, KELYB) connects talented people to companies in need of their skills in areas including Science, Engineering, Education, Office, Contact Center, Light Industrial, and more. We’re always thinking about what’s next in the evolving world of work, and we help people ditch the script on old ways of thinking and embrace the value of all workstyles in the workplace. We directly employ nearly 350,000 people around the world and connect thousands more with work through our global network of talent suppliers and partners in our outsourcing and consulting practice. Revenue in 2021 was $4.9 billion. Visit kellyservices.com and let us help with what’s next for you.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 Results. The Company recorded revenue of $1.16 billion, up 11.5% year over year, in line with our estimate of $1.16 billion. Adj. EBITDA came in at $34.9 million, up 4.8% over the prior year period and modestly lower than our estimate of $36.5 million. Adj. EBITDA margin decreased 20 basis points to 3.0%. Furthermore, Kelly reported net income of $0.16/sh. On an adjusted basis, EPS was $0.39/sh compared to $0.56/sh last year and our estimate of $0.60/sh.

Solid Results. The y-o-y revenue growth of 11.5% was largely driven by the Company’s May 2024 acquisition of Motion Recruitment Partners (MRP). On an organic basis, total revenue was only up 0.2%, which includes a 0.8% decrease in revenue from U.S. federal contractors and a 6.3% increase in Education segment revenue.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

For more than 45 years, 1-800-Flowers.com has offered truly original floral arrangements, plants and unique gifts to celebrate birthdays, anniversaries, everyday occasions, and seasonal holidays, and to deliver comfort during times of grief. Backed by a caring team obsessed with service, 1-800-Flowers.com provides customers thoughtful ways to express themselves and connect with the most important people in their lives. 1-800-Flowers.com is part of the 1-800-FLOWERS.COM, Inc. family of brands. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fiscal Q3 disappoints. Fiscal Q3 revenues of $311.5 million was well below our $367.8 million estimate. Adj. EBITDA loss of $38.6 million was below our seasonal loss estimate of $12.4 million. In spite of a good Valentine’s Day, fiscal third quarter results were adversely affected by weakened consumer confidence and macro economic forces.

Pulls guidance. In lieu of recent trade policies and a weakened consumer, management pulled fiscal full year 2025 guidance. We estimate that fiscal Q4 revenues will decline roughly 6.3% (including the benefit of Easter) and that the company will report an adj. EBITDA loss of $20.5 million. Fiscal full year 2025 revenue and adj. EBIDA are revised to $1.687 billion and $29.2 million, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

DLH delivers improved health and readiness solutions for federal programs through research, development, and innovative care processes. The Company’s experts in public health, performance evaluation, and health operations solve the complex problems faced by civilian and military customers alike, leveraging digital transformation, artificial intelligence, advanced analytics, cloud-based applications, telehealth systems, and more. With over 2,300 employees dedicated to the idea that “Your Mission is Our Passion,” DLH brings a unique combination of government sector experience, proven methodology, and unwavering commitment to public health to improve the lives of millions. For more information, visit www.DLHcorp.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Moving Forward. While the path forward has been more challenging than we had anticipated, we believe DLH remains on the right path to strong operating results. We believe the Company’s core competencies are well aligned with the Federal government’s goals.

New Business. Management expects some $1 billion of business to be awarded by the end of the fiscal year, providing a substantial opportunity for DLH to win its fair share and drive organic growth in 2026. Yesterday, the Company announced it had been awarded a five year task order valued at up to $37.7 million to continue delivering scientific research and development, modeling & simulation, artificial intelligence, machine learning, robotic process automation, biomedical engineering, and cloud-enabled big data analytic solutions for the Telemedicine and Advanced Technology Research Center.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

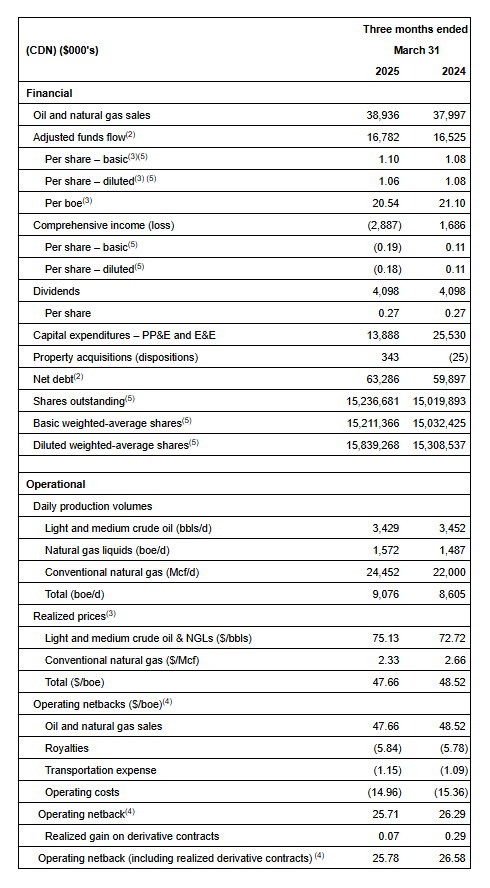

First quarter financial results. InPlay Oil reported a first quarter net loss of C$2.9 million or C$0.18 per share compared to net income of C$1.7 million or C$0.02 per share during the prior year period. This was below our net income estimate of C$4.2 million or C$0.15 per share, primarily due to an unrealized loss on derivative contracts of C$4.6 million and higher-than-expected expenses. Moreover, commodity prices declined slightly during the first quarter, leading to lower revenues of C$38.4 million compared to our estimate of C$40.4 million.

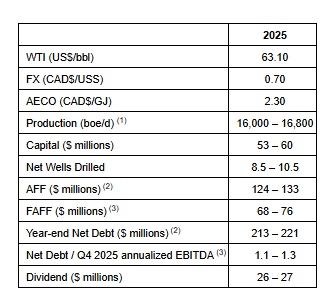

Corporate 2025 guidance. The company generated quarterly production of 9,076 barrels of oil equivalent per day (boe/d), a 5% increase year-over-year and above our expectations of 8,800 boe/d. The company is raising its estimated field production expectations to 21,500 boe/d, a marked increase from 18,750 boe/d, and expects 2025 full year production to be in the range of 16,000 to 16,800 boe/d. Revenue guidance has been adjusted downward to C$46.75 to C$51.75 boe/d from C$56.50 to C$61.50 boe/d. Adjusted funds flow is expected to be between C$124 million and C$133 million, down from $204 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Townsquare is a community-focused digital media and digital marketing solutions company with market leading local radio stations, principally focused outside the top 50 markets in the U.S. Our assets include a subscription digital marketing services business, Townsquare Interactive, providing website design, creation and hosting, search engine optimization, social media and online reputation management as well as other digital monthly services for approximately 26,800 SMBs; a robust digital advertising division, Townsquare IGNITE, a powerful combination of a) an owned and operated portfolio of more than 330 local news and entertainment websites and mobile apps along with a network of leading national music and entertainment brands, collecting valuable first party data, and b) a proprietary digital programmatic advertising technology stack with an in-house demand and data management platform; and a portfolio of 321 local terrestrial radio stations in 67 U.S. markets strategically situated outside the Top 50 markets in the United States. Our portfolio includes local media brands such as WYRK.com, WJON.com, and NJ101.5.com and premier national music brands such as XXLmag.com, TasteofCountry.com, UltimateClassicRock.com and Loudwire.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid first quarter results. Total company revenues were down a modest 1% to $98.7 million, in line with our $98.5 million estimate. Digital revenues increased 6.4%, nearly completely offsetting the weakness in legacy broadcast. Notably, Digital revenue in the quarter represented 57% of total revenue, but, more importantly, 62% of total company adj. EBITDA. Q1 adj. EBITDA of $18.1 million was better than our $17.0 million estimate.

Ignite continues to be on fire. Ignite, the company’s programmatic/advertising solutions business, increased revenues an attractive 7.6% in the quarter. Management indicated that the growth of Ignite will be enhanced by its white label initiative, which is expected to account for $10 million in revenue in 2025 and is expected to grow to $50 million in the next 3 to 5 years and with a 20% operating margin.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Saga Communications, Inc. is a broadcast company whose business is primarily devoted to acquiring, developing and operating radio stations. Saga currently owns or operates broadcast properties in 27 markets, including 79 FM and 33 AM radio stations. Saga’s strategy is to operate top billing radio stations in mid sized markets, defined as markets ranked (by market revenues) from 20 to 200. Saga’s radio stations employ a myriad of programming formats, including Active Rock, Adult Album Alternative, Adult Contemporary, Country, Classic Country, Classic Hits, Classic Rock, Contemporary Hits Radio, News/Talk, Oldies and Urban Contemporary. In operating its stations, Saga concentrates on the development of strong decentralized local management, which is responsible for the day-to-day operations of the stations in their market area and is compensated based on their financial performance as well as other performance factors that are deemed to effect the long-term ability of the stations to achieve financial objectives. Saga began operations in 1986 and became a publicly traded company in December 1992. The stock trades on NASDAQ under the ticker symbol “SGA”.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 Results. The company reported Q1 revenue of $24.2 million and an adj. EBITDA loss of $0.5 million, both of which declined over the prior year period, but were modestly better than our estimates of $23.0 million and a loss of $1.1 million, respectively, as illustrated in Figure #1 Q1 Results. Notably, the company is focused on its blended digital growth strategy and improving profitability. We believe the company’s strategic actions are a step in the right direction for returning toward revenue and adj. EBITDA growth.

Digital growth strategy. The company’s blended growth strategy combines radio and digital advertising to provide a consistent message to customers on both mediums and to drive radio listeners to digital platforms. Notably, year to date, the company has generated digital revenue of $5.3 million, surpassing the company’s $5.0 million generated for full year 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A Solid Start. ONE Group reported results modestly above our expectations for 1Q25. The accomplishments were driven by another quarter of sequential improvement in comparable sales trends, positive comparable sales at the Benihana restaurants, and strong positive transaction growth of 4.1% at the flagship STK brand.

1Q25 Results. ONE Group reported revenue of $211.1 million, up nearly 150% y-o-y, driven by the May 2024 Benihana acquisition. Same Store Sales declined 3.2%, compared to guidance of a negative 3-4%. Adjusted EBITDA was $25.2 million, up from $7.6 million. Adjusted EPS came in at $0.14, compared to an adjusted loss of $0.02/sh last year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

Lucky Strike Entertainment is one of the world’s premier location-based entertainment platforms. With over 360 locations across North America, Lucky Strike Entertainment provides experiential offerings in bowling, amusements, water parks, and family entertainment centers. The company also owns the Professional Bowlers Association, the major league of bowling and a growing media property that boasts millions of fans around the globe. For more information on Lucky Strike Entertainment, please visit ir.luckystrikeent.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Lackluster Q3 Results. The company reported Q3 revenue of $339.9 million and adj. EBITDA of $117.3 million, both of which were lower than our estimates of $360.0 million and $130 million, respectively, as illustrated in Figure #1 Q3 Results. Notably, the soft results were largely driven by a decrease in corporate events in California and Seattle, and partially offset by high single digit increase in food sales and stable retail and league business. While Q3 results were lackluster, we believe the company will gain momentum heading into the summer.

Favorable developments. The company’s Summer Season Pass program, aimed at driving retail traffic, increased sales by more than 200% compared with this time last year. Additionally, the company is heading into summer with three water parks and seven family entertainment centers that were acquired this year. We believe the company is well positioned to benefit from its enhanced scale, in spite of the economic uncertainty.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

Key Points: – IonQ has agreed to acquire Capella Space to accelerate its development of a global quantum key distribution (QKD) network. – Capella’s radar imaging satellites will help enable space-based secure communication for defense and commercial sectors. – The acquisition follows IonQ’s broader strategy to dominate quantum networking through vertical integration and space-based infrastructure

Quantum computing firm IonQ is doubling down on its ambitions in secure communication. On Wednesday, the Maryland-based company announced a deal to acquire Capella Space, a satellite imaging firm known for its synthetic aperture radar (SAR) technology, in a move designed to supercharge its push into quantum networking.

The acquisition marks a pivotal moment for IonQ, as it shifts from primarily offering quantum computing solutions to developing a space-based quantum key distribution (QKD) network. QKD is seen as essential for enabling unhackable communication channels in a future where classical encryption could be rendered obsolete by quantum computers.

Capella, based in San Francisco, operates four commercial satellites that collect high-resolution X-band SAR imagery, useful for intelligence, disaster response, and maritime surveillance. The company has additional satellite launches planned for this year, which will expand its imaging capabilities and support IonQ’s space-to-space and space-to-ground QKD efforts.

According to IonQ CEO Niccolo de Masi, the acquisition will “deepen and accelerate IonQ’s quantum networking leadership” by combining Capella’s satellite infrastructure with IonQ’s quantum technologies. “We have an exceptional opportunity to accelerate our vision for the quantum internet,” he said.

In addition to providing satellite assets, Capella also brings a valuable facility security clearance, enabling closer collaboration with U.S. defense and intelligence agencies—key customers for quantum-secure communications.

The Capella deal is the latest in a string of strategic moves by IonQ. Earlier this year, it acquired Qubitekk, a specialist in quantum networking, and Lightsynq Technologies, a startup founded by former Harvard researchers focused on quantum memory. IonQ has also signed a memorandum of understanding with Intellian Technologies, a satellite hardware manufacturer, to explore integrating quantum networking into future satellite ground systems.

Capella CEO Frank Backes echoed the enthusiasm, saying the integration of Capella’s radar imaging with IonQ’s quantum computing would enhance global defense and commercial missions through “ultra-secure environments.”

The transaction, expected to close in the second half of 2025 pending regulatory approval, continues a trend of quantum-tech consolidation as players position themselves to meet anticipated demand for secure communications in both government and private sectors. As cyber threats grow and classical encryption ages, the ability to offer end-to-end quantum-secure channels—especially via space infrastructure—may become a competitive necessity.

IonQ’s aggressive strategy has drawn investor interest, with its stock gaining momentum in recent weeks. As the quantum industry matures, vertical integration—spanning hardware, software, and infrastructure—is becoming increasingly critical.

If successful, IonQ’s vision for a global quantum-secure network could reshape how sensitive data is protected and transmitted across borders, laying the groundwork for a new era of secure, quantum-powered communication.

Key Points: – Tripledot Studios acquires AppLovin’s mobile gaming division for $800 million, expanding its global footprint. – The deal includes 10 studios and popular titles, boosting Tripledot’s daily active users to over 25 million. – AppLovin receives a 20% equity stake in Tripledot, signaling a strategic shift towards its core adtech business

In a significant move within the mobile gaming industry, London-based Tripledot Studios has announced the acquisition of AppLovin’s mobile gaming division for approximately $800 million. The transaction, structured as a combination of cash and equity, will see AppLovin become a minority shareholder in Tripledot, holding a 20% stake.

This acquisition encompasses 10 studios and a suite of popular titles, including “Wordscapes,” “Project Makeover,” and “Game of War.” With this expansion, Tripledot’s operational scale will increase to 12 studios across 23 cities, serving over 25 million daily active users and generating nearly $2 billion in annual gross revenue.

Founded in 2017, Tripledot Studios has rapidly ascended in the mobile gaming sector, known for hits like “Woodoku” and “Solitaire.com.” The company’s co-founder and CEO, Lior Shiff, emphasized the strategic importance of this deal, stating, “Acquiring AppLovin’s games portfolio is a big step towards achieving our goal of becoming the world’s most successful mobile game studio.”

For AppLovin, this divestiture marks a strategic pivot towards its core competency in advertising technology. The company, which provides software for app monetization and marketing, reported strong first-quarter earnings, with a 40% year-over-year increase in revenue to $1.48 billion. AppLovin’s CEO, Adam Foroughi, acknowledged the company’s shift, noting, “We’ve never been a game developer at heart,” and expressed confidence in Tripledot’s ability to nurture the acquired studios.

The mobile gaming industry has experienced a slowdown following a pandemic-induced surge, with a 6% decline in downloads last year due to market saturation. Despite these challenges, Tripledot has maintained profitability since its second year of operation, leveraging a diversified portfolio and advertising-driven revenue models.

Analysts view this acquisition as a consolidation move that positions Tripledot among the top-tier independent mobile game companies globally. The deal is expected to close by early summer 2025, pending regulatory approvals. Tripledot plans to invest further in artificial intelligence to enhance game development efficiency and user experience.

Key Points: – The U.S. will reduce tariffs on UK steel and aluminum to 0%, and lower car import duties to 10% for up to 100,000 vehicles annually. – The UK will eliminate tariffs on U.S. ethanol and expand access for American agricultural products, while maintaining strict food safety standards. – Both nations will initiate negotiations on a technology partnership focusing on AI, bioengineering, and quantum computing

In a significant development, President Donald Trump announced a new trade agreement with the United Kingdom on May 8, 2025. This marks the first major bilateral pact since the U.S. imposed sweeping tariffs earlier this year, signaling a potential shift in the ongoing global trade tensions.

Key Highlights of the Deal:

Tariff Reductions: The agreement includes a reduction of U.S. tariffs on U.K.-made steel from 25% to 0% and on car exports from 27.5% to 10%.

Agricultural Access: The U.K. will remove tariffs on U.S. ethanol and provide increased market access for American beef, machinery, and agricultural products.

Digital Services: Concessions were made regarding digital service taxes that impact U.S. tech companies, aiming to ease tensions in the technology sector.

Market Reactions:

The announcement had immediate effects on the markets. U.S. stocks experienced an uptick, with the Dow Jones Industrial Average and S&P 500 both rising by over 1%. Investors viewed the deal as a positive step towards stabilizing trade relations and reducing economic uncertainty.

Unresolved Issues:

Despite the progress, several aspects remain under negotiation. Notably, the U.K. has maintained its food and animal welfare standards, meaning U.S. beef exports will still face regulatory hurdles. Additionally, the reduction in car tariffs applies only to the first 100,000 vehicles imported annually, aligning with current export levels.

Broader Implications:

This deal comes amid a backdrop of global trade tensions, with the U.S. having imposed a 10% baseline tariff on imports from nearly every country, along with higher tariffs on specific sectors like steel, aluminum, and automobiles. The agreement with the U.K. could serve as a template for future negotiations with other trade partners, potentially easing some of the strain caused by recent protectionist measures.

Conclusion:

The U.S.-U.K. trade agreement represents a noteworthy development in international trade relations. While it addresses key sectors and provides a framework for cooperation, the deal’s limited scope and the persistence of certain tariffs indicate that significant challenges remain. As negotiations continue, stakeholders will be closely monitoring how this agreement influences broader trade dynamics and economic policies.

TROY, Mich., May 08, 2025 (GLOBE NEWSWIRE) — Kelly (Nasdaq: KELYA, KELYB), a leading specialty talent solutions provider, today announced results for the first quarter of 2025.

Q1 revenue of $1.16 billion, up 11.5% year-over-year reflecting previously disclosed acquisitions, and up 0.2% on an organic basis

Q1 operating earnings of $10.8 million; $22.1 million on an adjusted basis, down 4.3% versus the prior year period

Q1 adjusted EBITDA of $34.9 million, up 4.8% versus the prior year; adjusted EBITDA margin decreased 20 basis points (bps) to 3.0%

Company expects year-over-year revenue growth of 6.0% to 7.0% in Q2. Also expects Q2 year-over-year adjusted EBITDA margin decline of 20 to 30 bps, with anticipated margin expansion in Q3 and Q4, and for the full year.

“In the first quarter, Kelly delivered organic revenue growth that was in-line with our expectations, and once again outperformed the market. Our performance was driven primarily by continued strength in Education, as well as growing demand for our higher-margin outcome-based solutions within the semiconductor and renewables sectors,” said Peter Quigley, president and chief executive officer. “Through our ongoing focus on efficiency and effectiveness, we are well prepared to navigate this rapidly evolving macroeconomic environment while driving further progress on our specialty growth journey. By staying close with our customers and executing our strategic priorities, Kelly will be well positioned to capitalize when demand rebounds.”

Financial Results for the thirteen-week period ended March 30, 2025:

Revenue of $1.16 billion, an 11.5% increase compared to the corresponding quarter of 2024 resulting primarily from the May 2024 acquisition of Motion Recruitment Partners, LLC (“MRP”). Excluding the impact of the MRP acquisition, revenue was up 0.2% on an organic basis, includes approximately 0.8% of revenue decline due to reduced demand for U.S. federal government contractors and growth of 6.3% in the Education segment.

Operating earnings of $10.8 million, compared to earnings of $26.8 million reported in the first quarter of 2024. Adjusted earnings1 were $22.1 million in the first quarter of 2025 and $23.1 million in the first quarter of 2024. Adjusted EBITDA1 of $34.9 million, an increase of 4.9% versus the prior year period. Adjusted EBITDA margin of 3.0%, a decrease of 20 basis points driven primarily by near-term margin pressure in SET reflecting timing of revenue trends and related expense actions.

Earnings per share was $0.16 compared to earnings per share of $0.70 in the first quarter of 2024. On an adjusted basis1, earnings per share were $0.39 in the first quarter of 2025 compared to $0.56 per share in the corresponding quarter of 2024. The year-over-year decline includes $0.15 of increased net interest expense due to an elevated cash balance in the prior year quarter and debt incurred in Q2 2024 in conjunction with the MRP acquisition.

1 Adjusted measures represent non-GAAP financial measures. Refer to our reconciliation of non-GAAP financial measures to the most closely related GAAP measure included in this document.

Quarterly Cash Dividend:

Kelly also reported that on May 6, its board of directors declared a dividend of $0.075 per share. The dividend is payable on June 3, 2025 to stockholders of record as of the close of business on May 19, 2025.

In conjunction with its earnings release, Kelly has published a financial presentation and will host a live webcast of a conference call with financial analysts at 9 a.m. ET on May 8 to review the results from the quarter and answer questions. The presentation and a link to the live webcast will be accessible through the Company’s public website on the Investor Relations page under Events & Presentations. The webcast will be recorded, and a replay will be available within one hour of completion of the event through the same link as the live webcast.

Forward-Looking Statements:

This release contains statements that are forward looking in nature and, accordingly, are subject to risks and uncertainties. These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. Statements that are not historical facts, including statements about Kelly’s financial expectations, are forward-looking statements. Factors that could cause actual results to differ materially from those contained in this release include, but are not limited to, (i) changing market and economic conditions, (ii) disruption in the labor market and weakened demand for human capital resulting from technological advances, loss of large corporate customers and government contractor requirements, (iii) the impact of laws and regulations (including federal, state and international tax laws), (iv) unexpected changes in claim trends on workers’ compensation, unemployment, disability and medical benefit plans, (v) litigation and other legal liabilities (including tax liabilities) in excess of our estimates, (vi) our ability to achieve our business’s anticipated growth strategies, (vii) our future business development, results of operations and financial condition, (viii) damage to our brands, (ix) dependency on first parties for the execution of critical functions, (x) conducting business in foreign countries, including foreign currency fluctuations, (xi) availability of temporary workers with appropriate skills required by customers, (xii) cyberattacks or other breaches of network or information technology security, and (xiii) other risks, uncertainties and factors discussed in this release and in the Company’s filings with the Securities and Exchange Commission. In some cases, forward-looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “target,” “aim,” “estimate,” “intend,” “plan,” “believe,” “potential,” “continue,” “is/are likely to” or other similar expressions. All information provided in this press release is as of the date of this press release and we undertake no duty to update any forward-looking statement to conform the statement to actual results or changes in the Company’s expectations.

About Kelly®

Kelly Services, Inc. (Nasdaq: KELYA, KELYB) helps companies recruit and manage skilled workers and helps job seekers find great work. Since inventing the staffing industry in 1946, we have become experts in the many industries and local and global markets we serve. With a network of suppliers and partners around the world, we connect more than 400,000 people with work every year. Our suite of outsourcing and consulting services ensures companies have the people they need, when and where they are needed most. Headquartered in Troy, Michigan, we empower businesses and individuals to access limitless opportunities in industries such as science, engineering, technology, education, manufacturing, retail, finance, and energy. Revenue in 2024 was $4.3 billion. Learn more at kellyservices.com.

CALGARY, AB, May 8, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) announces its financial and operating results for the three months ended March 31, 2025 and an updated 2025 capital budget following the successful completion of the strategic acquisition of Cardium light oil focused assets (the “Acquired Assets“) in the Pembina area of Alberta (the “Acquisition“) from Obsidian Energy Ltd. And certain of its affiliates (collectively “Obsidian“). InPlay’s condensed unaudited interim financial statements and notes, as well as Management’s Discussion and Analysis (“MD&A”) for the three months ended March 31, 2025 will be available at “www.sedarplus.ca” and on our website at “www.inplayoil.com“. All figures presented herein reflect the Company’s six (6) to one (1) share consolidation, which was effective April 14, 2025. An updated corporate presentation will be available on our website shortly.

First Quarter 2025 Highlights

Achieved average quarterly production of 9,076 boe/d(1) (55% light crude oil and NGLs), a 5% increase over Q1 2024 and ahead of internal forecasts.

Generated strong quarterly Adjusted Funds Flow (“AFF”)(2) of $16.8 million ($1.10 per basic share(3)).

Returned $4.1 million to shareholders by way of monthly dividends, equating to a 16% yield relative to the current share price. Since November 2022 InPlay has distributed $44 million in dividends including dividends declared to date.

Maintained a strong operating income profit margin(3) of 54%.

Improved field operating netbacks(3) to $25.71/boe, an increase of 3% compared to Q4 2024.

First quarter results exceeded expectations, driven in part by the outperformance of newly drilled wells at Pembina Cardium Unit #7 (PCU#7). A two well pad delivered average initial production (“IP”) rates of 677 boe/d (75% light oil and NGLs) over the first 30 days and 492 boe/d (66% light oil and NGLs) over the first 60 days, both significantly above expectations. Over the initial two-month period, production from these wells was more than 100% above our type curve. These wells ranked in the top-ten for production rates for all Cardium wells in the basin for the month of March.

Complementing InPlay’s strong operational momentum, Obsidian drilled four (4.0 net) wells on the Acquired Assets in the first quarter. The first two (2.0 net) wells, which started production mid quarter, are outperforming our internal type curve by approximately 50% with average IP rates of 304 boe/d (91% light oil and NGLs) over the first 30 days and 295 boe/d (85% light oil and NGLs) over the first 60 days. The remaining two wells, brought online in the final days of the first quarter, are performing more than 350% above our internal type curve, with average IP rates per well of 887 boe/d (88% light oil and NGLs) over their initial 30 day period.

The Company is very excited about the highly accretive Pembina Acquisition announced February 19, 2025 and had anticipated strong results from the combined assets. The exceptional results from the first quarter drilling program, combined with the outperformance of base production, have driven current field estimated production to approximately 21,500 boe/d (64% light oil and NGLs) significantly exceeding what we had initially forecasted at the announcement of the Acquisition. Given the current volatility in commodity prices, this material outperformance provides the Company with significant flexibility to scale back our capital program, providing “more for less” while maintaining our production forecasts, allowing for more aggressive debt repayment even in a lower pricing environment.

2025 Capital Budget and Associated Guidance

Following the closing of the highly accretive Acquisition on April 7, 2025, InPlay is pleased to provide initial pro forma guidance inclusive of the Acquired Assets. This guidance reflects the exceptional operational performance across the Company’s expanded asset base, while taking into account the current volatile commodity price environment. It also underscores InPlay’s continued commitment to maximizing free cash flow to support ongoing debt reduction, while positioning the Company to support its return to shareholder strategy.

InPlay’s Board has approved an updated capital program of $53 – $60 million for 2025. InPlay plans to drill approximately 5.5 – 7.5 net Extended Reach Horizontal (“ERH”) Cardium wells over the remainder of the year. A significant portion of the remaining 2025 capital budget is expected to be directed toward the Acquired Assets, which (as outlined above) continue to materially outperform internally modelled type curves. Cost efficiencies realized through InPlay’s recent drilling program, combined with the application of InPlay’s drilling and completion techniques to the Acquired Assets, are expected to further enhance well economics. Capital will also be spent tying in certain InPlay assets into the newly acquired facilities, eliminating significant trucking costs, and marks the first step in our synergy cost savings strategy. Due to the outperformance of production across our asset base, InPlay has reduced total capital spending for the remainder of 2025 by approximately 30% (relative to initial expectations) without reducing production estimates.

Key highlights of the updated 2025 capital program include:

Production per Share Growth:

Forecasted average annual production of 16,000 – 16,800 boe/d(1) (60% – 62% light oil and NGLs), a 15% increase (based on mid-point) in production per weighted average share compared to 2024 despite 30% less capital spending than initially expected, driven by:

Lower corporate base decline rate of 24% due to the favorable decline profile of the Acquired Assets;

Improved corporate netbacks driven by the higher oil and liquids weighting of the Acquired Assets; and

Enhanced capital efficiencies from high graded drilling inventory of the pro forma assets.

FAFF Generation and Dividend Sustainability:

AFF(2) per weighted average share(4) of $5.00 – $5.35, a 13% increase (based on mid-point) compared to 2024.

Free adjusted funds flow (“FAFF”)(3) of $68 – $76 million equating to a 35% – 40% FAFF Yield(3), a 10x increase (based on mid-point) in FAFF per share compared to 2024 despite a 17% year over year reduction in forecasted WTI price.

Top Tier Returns:

Total return of 50% – 55% after combining FAFF Yield and production per share growth(4), which is expected to be at the high end of our peer group.

Debt Reduction:

Excess FAFF(3) is planned to be used to reduce debt.

Projected year-end Net Debt(2) of $213 – $221 million equating to a $31 – $39 million reduction from closing of the Acquisition.

Year-end Net Debt to Q4 2025 annualized EBITDA(3) ratio of 1.1x – 1.3x.

InPlay continues to monitor global trade and commodity dynamics, including United States tariffs on Canada. Capital spending will be weighted towards the back end of the year with drilling expected to resume again in August, providing ample time to finalize capital spending allocation depending on commodity pricing and continued asset performance. As a result of minimal capital spending in the second quarter, InPlay anticipates generating significant FAFF which will be directed to reducing debt. InPlay will remain flexible and will make decisions based on our core strategy of disciplined capital allocation, maintaining financial strength to ensure the long term sustainability of our strategy and return to shareholder program.

Updated 2025 Guidance Summary:

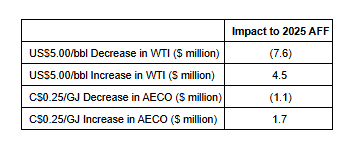

Following closing of the Acquisition, a significant hedging program was undertaken to help provide downside commodity price protection. As further detailed in the hedging summary section in this press release, InPlay has hedged approximately 75% of its net after royalty oil production and 67% of its net after royalty production on a BOE basis for the remainder of 2025. InPlay’s strong hedge book provides insulation to the current commodity price volatility which is highlighted in the sensitivity table below.

With low decline high netback assets, a flexible budget, a resilient balance sheet, and becoming a larger company, InPlay remains well positioned to sustainably navigate future commodity price cycles. Adhering to this disciplined strategy has allowed the Company to navigate previous commodity price cycles including the COVID-19 pandemic price environment.

Financial and Operating Results:

First Quarter 2025 Financial & Operations Overview:

The year has begun with strong momentum as production for the quarter exceeded internal forecasts, largely due to the outperformance of new ERH wells in PCU#7. Three (3.0 net) ERH wells were brought online at the end of February as part of a $13.9 million capital program, inclusive of $1.4 million invested in well optimization initiatives which continues to lower corporate declines. Production averaged 9,076 boe/d(1) (55% light crude oil and NGLs) in the quarter, a 5% increase from 8,605 boe/d(1) in the first quarter of 2024.

Notably, a two well pad drilled in PCU#7 exceeded expectations, delivering average IP rates of 677 boe/d (75% light oil and NGLs) and 492 boe/d (66% light oil and NGLs) per well over their first 30 and 60 days, respectively, which is over 100% above our internally modeled type curve for these wells.

Obsidian drilled four (4.0 net) wells on the Acquired Assets in the first quarter. The first two (2.0 net) wells, which came on production mid quarter, are outperforming the internal type curve with IP rates averaging 304 boe/d (91% light oil and NGLs) and 295 boe/d (85% light oil and NGLs) over the first 30 and 60 days, respectively (approximately 50% above our internally modelled type curve). The last two wells were brought online in the final days of the quarter and are performing significantly above internal forecasts with IP rates averaging 887 boe/d (88% light oil and NGLs) per well over their first 30 days (more than 350% above our type curve).

AFF for the quarter was $16.8 million. In addition, the Company returned $4.1 million ($0.09 per share) in base dividends to shareholders which equates to a yield of 16% based on the current share price. Net debt at quarter-end totaled $63 million, with a net debt to EBITDA ratio(3) of 0.8x, reflecting a healthy financial position.

On behalf of the entire InPlay team and the Board of Directors, we thank our shareholders for their continued support as we advance our strategy of disciplined growth, returns, and long-term value creation. We are excited to report our progress with respect to the strategic Acquisition.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

")