Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q4 results. The company reported sequential revenue growth in Q4 with revenue of $136.8 million (up from $135.3 million in Q3), better than our estimate of $125.1 million. Adj. EBITDA was $12.0 million, better than our estimate of $6.4 million.

Margin improvement. The strong adj. EBITDA margins of 8.8% in Q4 were the highest of any quarter in 2024. The impressive margins were driven by better transaction spreads at the company’s kiosks, armored transport cost reductions, and lower rents in some kiosk locations. Moreover, the company benefitted from a falloff of initial public company costs (in comparison to the prior year period).

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q4 pre-release. On Monday, SKYX pre-released its Q4 revenue results, reporting revenue of $23.7 million (largely aligning with our estimate of $24.0 million). Notably, the company’s revenue grew throughout 2024, from $19.0 million in Q1 to $21.4 million, $22.2 million, and $23.7 million, in the subsequent quarters.

Key leadership additions. The company recently announced the additions of Huey Long as Head of E-commerce and Greg St. John as President of Lighting, Fans and Smart Home Products. Mr. Long previously served as director of e-commerce for Amazon and as an executive at both Ashley Furniture and Walmart. Mr. St. John previously served as head of lighting at Home Depot as well as CEO of EGLO.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Business Wins. Kratos has been awarded a number of new and additions to existing contracts in March. We view these developments positively, although we remain watchful as to the impact of the ongoing continuing resolution for the Federal budget and its implications on new awards in 2025.

BQM-177A Awards. Kratos was awarded $3.4 million from the U.S. Navy for the base year of its next Contractor Logistics Support and Engineering Services contract, supporting BQM-177A aerial target system operations. If all four option years awarded under this contract are exercised, this contract has a potential value of $19.1 million. The Company also received $59.3 million for an additional 70 BQM-177A Subsonic Aerial Target aircraft through the exercise of the contract option for Full Rate Production (FRP) Lot 6.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Net Income Was Within Expectations. Gyre Therapeutics reported 4Q24 Net Income Attributable to Common Shareholders of $(0.1) million or $(0.00) per share and FY2024 Net Income of $12.1 million, or $0.14 per basic share and $0.05 per fully diluted share. Revenues were $105.8 million in FY2024 with gross margins of 96.3%, consistent with our revenue estimates of $101.4 million and 96.2% gross margins. As of December 31, 2024, cash on hand was $51.2 million. Separately, results of the Phase 3 clinical trial for Hydronidone will be announced in 2Q25.

Hydronidone Data Announcement Pushed To 2Q25. In its quarterly press release, the company stated that data from the Phase 3 clinical trial for Hydronidone will be announced in 2Q25, although we had expected the data in 1Q25. We do not see this as a significant delay, as it extends the timeframe by 2 to 14 weeks. We believe this can still allow for regulatory filing in China during FY2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2025 preview. We anticipate that the company’s revenue momentum will build throughout the year as new business signings take effect. Moreover, with the prospect of additional efficiencies from initiatives such as corporate-level cost reductions, and a reduction in real estate footprint, we expect adj. EBITDA margins to expand as the year progresses.

Quarterly outlook. In Q1, we expect $767 million in revenue and $14 million in adj. EBITDA, a modest 1.8% margin. However, based on growing revenue and increasing efficiency, we expect adj. EBITDA margins to improve in each subsequent quarter, culminating in margins of nearly 8% in Q4. Given our Q4 revenue estimate of $830 million, we believe the company will exit 2025 with revenue and adj. EBITDA run rates in line with its stated target ($3.2B-$3.3B in annual revenue and 8% adj. EBITDA margins).

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

– GM and Nvidia are partnering to integrate AI-powered solutions into vehicle design, advanced driver-assistance systems (ADAS), and factory automation. – GM will leverage Nvidia’s Omniverse platform for digital factory planning, optimizing manufacturing processes, and improving robotics. – Nvidia continues its push into the automotive industry, competing with rivals in AI-driven vehicle technology.

General Motors and Nvidia have announced a major collaboration aimed at revolutionizing the automotive industry with AI-driven technology. This strategic partnership will see GM leveraging Nvidia’s advanced artificial intelligence solutions across multiple facets of its business, from vehicle development to factory optimization.

“The era of physical AI is here, and together with GM, we’re transforming transportation, from vehicles to the factories where they’re made,” said Jensen Huang, Nvidia founder and CEO. “We are thrilled to partner with GM to build AI systems tailored to their vision, craft, and know-how.”

A central component of this partnership is GM’s adoption of Nvidia’s Omniverse platform, which enables the creation of “digital twins”—virtual replicas of real-world environments. GM has already been experimenting with Omniverse since 2022 to digitally simulate its design centers and optimize vehicle development. This new collaboration extends those efforts, incorporating Nvidia’s AI-powered solutions into GM’s assembly plants and production facilities.

Beyond manufacturing, GM will integrate Nvidia’s Drive AGX platform into its next-generation vehicles. This hardware will support future advanced driver-assistance systems (ADAS) and enhance in-cabin safety features. The partnership positions GM to further compete in the race toward fully autonomous and AI-enhanced vehicles, an area where competitors like Tesla and Mercedes-Benz have been making significant strides.

While GM has relied on Nvidia’s graphics processing units (GPUs) for AI model training, this expanded agreement takes their collaboration to a new level. The financial terms of the deal were not disclosed, but Nvidia has been known to license Omniverse for $4,500 per GPU, per year. Given the scale of GM’s operations, the automaker is expected to require a substantial number of GPUs to power its AI-driven initiatives.

The announcement coincides with Nvidia’s GTC AI conference, where the company has been showcasing its advancements in AI and simulation technology. The move comes as both Nvidia and GM navigate competitive and regulatory challenges, including increased competition from China and evolving U.S. trade policies. GM’s stock has dropped roughly 8% in 2025, while Nvidia has seen a 12% decline, underscoring the pressure both companies face to innovate and expand their market presence.

GM CEO Mary Barra highlighted the broader implications of the partnership, stating, “AI not only optimizes manufacturing processes and accelerates virtual testing but also helps us build smarter vehicles while empowering our workforce to focus on craftsmanship. By merging technology with human ingenuity, we unlock new levels of innovation in vehicle manufacturing and beyond.”

With over 20 other automakers—including Mercedes-Benz, Volvo, and Volkswagen—already using Nvidia’s automotive AI solutions, this partnership further cements Nvidia’s role in the future of intelligent vehicles. As demand for AI-powered automotive solutions continues to grow, this collaboration between GM and Nvidia represents a significant step forward in reshaping how vehicles are designed, built, and driven.

OCU200 has a very favorable safety and tolerability profile

No serious adverse events related to the study drug have been reported

Dosing of the second cohort has been approved

MALVERN, Pa., March 18, 2025 (GLOBE NEWSWIRE) — Ocugen, Inc. (“Ocugen” or the “Company”) (NASDAQ: OCGN), a pioneering biotechnology leader in gene therapies for blindness diseases, today announced that the Data and Safety Monitoring Board (DSMB) for the OCU200 clinical trial recently convened and reviewed safety data following dosing of the first cohort in the dose-escalation portion of the Phase 1 study and approved continuation of dosing in the second cohort. OCU200 is a novel fusion protein consisting of two human proteins, tumstatin and transferrin, with the potential to treat diabetic macular edema (DME).

“OCU200 is given intravitreally,” said Peter Chang, MD, FACS, Co-President and Partner of the Massachusetts Eye Research and Surgery Institution (MERSI). “No serious adverse events related to OCU200 have been reported to date.”

The OCU200 Phase 1 clinical trial is a multicenter, open-label, dose-escalation study to assess drug safety via intravitreal injection in three cohorts: low dose (0.025 mg), medium dose (0.05 mg), and high dose (0.1 mg). All subjects will receive two doses six weeks apart, and patients will be followed for up to 6 months.

“It is encouraging that we have successfully completed dosing in the low dose cohort for OCU200, a novel biologic that has a very favorable safety and tolerability profile,” said Dr. Huma Qamar, Chief Medical Officer at Ocugen. “There remains a considerable unmet medical need for the 30% to 40% of DME patients who do not respond to current anti-VEGF therapies. OCU200 holds the promise of potentially benefiting all DME, diabetic retinopathy (DR), and wet age-related macular degeneration (wet AMD) patients.”

Approximately 12 million people in the United States and 130 million people worldwide are affected by DME, DR, or wet AMD. Patients affected by them share common symptoms, such as blurriness in vision and progressive vision loss, as the diseases progress. The formation of fragile and leaky new blood vessels leads to fluid accumulation in and around the retina, causing damage to vision.

OCU200 has the potential to change the treatment landscape for DME, DR, and wet AMD with its unique mechanism of action, binding the active component—tumstatin—to integrin receptors on active endothelial cells that play a crucial role in disease pathogenesis.

OCU200 brings an innovative biologic candidate to Ocugen’s ophthalmology portfolio targeting blindness diseases. The Company intends to complete the Phase 1 OCU200 clinical trial in the second half of 2025 and to provide preliminary safety and efficacy updates throughout the year.

About OCU200

OCU200 is a recombinant fusion protein that consists of two parts connected by a linker: tumstatin, the active component, acts as an anti-inflammatory, anti-VEGF agent by binding to integrin receptors; and transferrin, which targets the drug to the choroid and retina by binding transferrin receptors on endothelial cells. These features will potentially enable OCU200 to reduce the vascular permeability, inflammation, and neovascularization that drive the pathophysiology of DME, DR, and wet AMD at a significantly lower dose compared to currently approved therapies.

About Ocugen, Inc.

Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patients’ lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on X and LinkedIn.

Cautionary Note on Forward-Looking Statements Thispressreleasecontainsforward-lookingstatementswithinthemeaningofThePrivateSecuritiesLitigationReformActof1995,including,butnot limited to, statements regarding qualitative assessments of available data, potential benefits, expectations for ongoing clinical trials, anticipated regulatory filings and anticipated development timelines,whicharesubjecttorisksanduncertainties.Wemay,insomecases,usetermssuchas “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations, including,butnotlimitedto,therisksthatpreliminary,interimandtop-lineclinicaltrialresultsmaynotbeindicativeof,andmaydifferfrom,finalclinical data;the ability of OCU200 to perform in humans in a manner consistent with nonclinical or preclinical study data;thatunfavorablenewclinicaltrialdatamayemergeinongoingclinicaltrialsorthroughfurtheranalysesofexistingclinicaltrialdata;thatearlier non-clinicalandclinicaldataandtestingofmaynotbepredictiveoftheresultsorsuccessoflaterclinicaltrials;andthatthatclinicaltrialdataare subject to differing interpretations and assessments, including by regulatory authorities.Theseandotherrisksanduncertaintiesaremorefully describedinourperiodicfilingswiththeSecuritiesandExchangeCommission(SEC),includingtheriskfactorsdescribedinthesectionentitled“Risk Factors”inthequarterlyandannualreportsthatwefilewiththeSEC.Anyforward-lookingstatementsthatwemakeinthispressreleasespeakonlyas ofthedateofthispressrelease.Exceptasrequiredbylaw,weassumenoobligationtoupdateforward-lookingstatementscontainedinthispress release whether as a result of new information, future events, or otherwise, after the date of this press release.

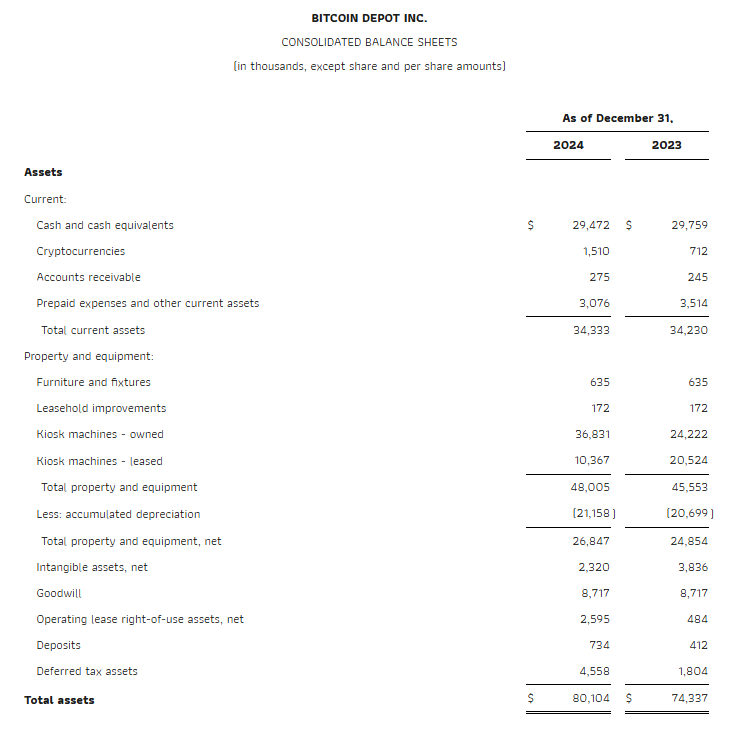

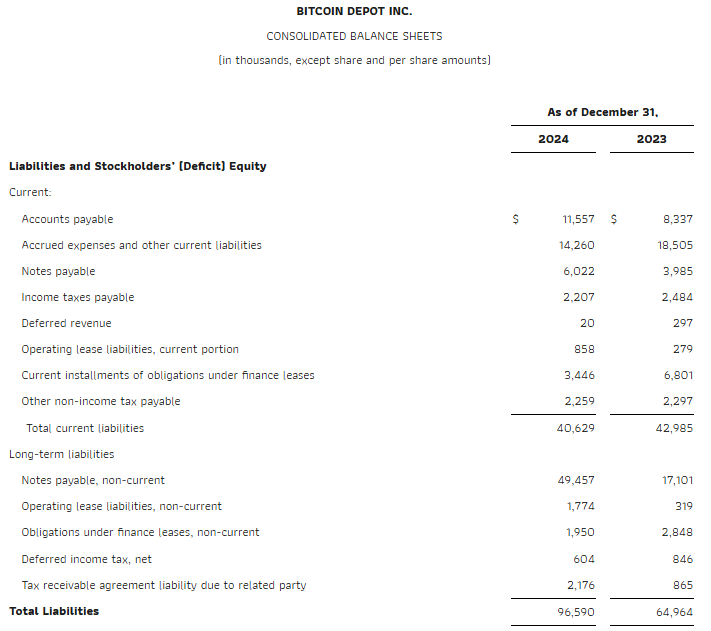

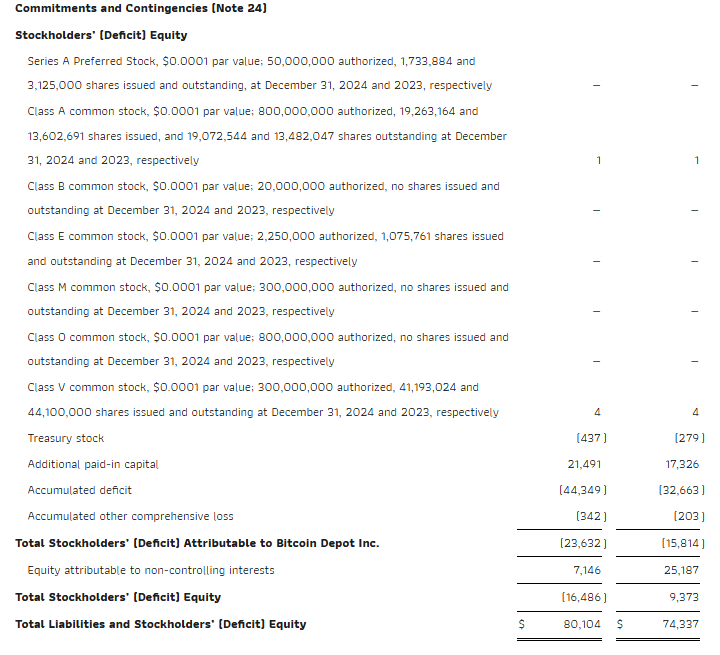

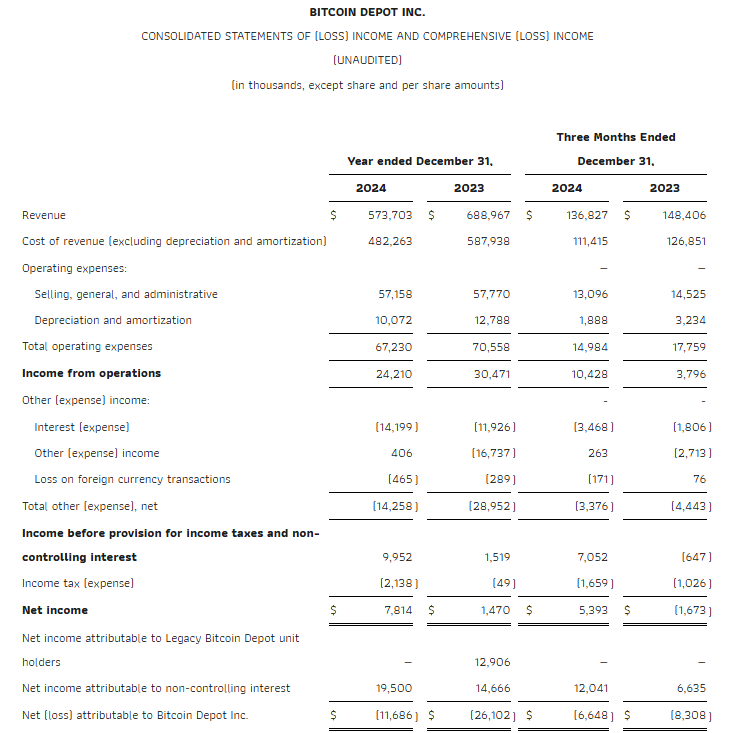

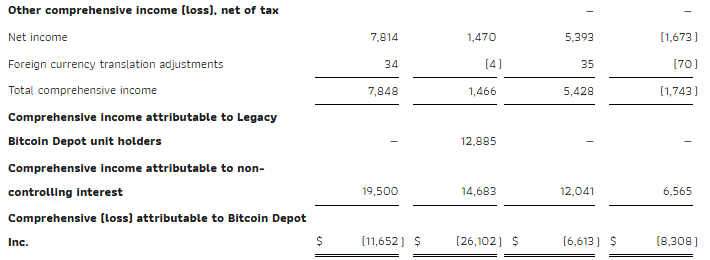

Q4 Revenue of $136.8 Million Compared to $148.4 Million in the Prior Year Quarter

Q4 Operating Expenses Down 16% Year-Over-Year to $15.0 Million

Q4 Net Income up Significantly to $5.4 Million Compared to a Net Loss of $1.7 Million in the Prior Year Quarter

Q4 Adjusted Gross Profit up 18% Year-Over-Year to $25.4 Million

Q4 Adjusted EBITDA up 34% Year-Over-Year to $12.0 Million

ATLANTA, March 18, 2025 (GLOBE NEWSWIRE) — Bitcoin Depot Inc. (“Bitcoin Depot” or the “Company”), a U.S.-based Bitcoin ATM operator and leading fintech company, today reported financial results for the fourth quarter and full year ended December 31, 2024. Bitcoin Depot will host a conference call and webcast at 10:00 a.m. ET today. An earnings presentation and link to the webcast will be made available at ir.bitcoindepot.com.

“As we highlighted in our fourth-quarter pre-announcement, 2024 ended on a strong note, driven by sequential revenue growth and substantial improvements in adjusted EBITDA, both sequentially and year-over-year,” said Brandon Mintz, CEO and Founder of Bitcoin Depot. “In the fourth quarter, we made significant progress in expanding our Bitcoin ATM network and optimizing existing machines to enhance profitability — and the results speak for themselves.

“Looking ahead, we are confident that the optimization efforts we implemented throughout 2024 will begin to positively impact our financial performance as we move through 2025. With our aggressive international and domestic kiosk expansion strategy, we anticipate that 2025 will mark a strong return to growth for the business. As part of this, we are reintroducing financial guidance, projecting robust growth in the first quarter. Additionally, we remain committed to leveraging our strong cash flow to drive shareholder value initiatives, including the potential for a cash dividend. We have also continued to strengthen our Bitcoin treasury holdings, recently increasing our total to 94 BTC, reflecting our confidence in Bitcoin as a valuable financial asset and an integral part of our business model.”

Fourth Quarter 2024 Financial Results

Revenue in the fourth quarter of 2024 was $136.8 million compared to $148.4 million in the fourth quarter of 2023. This decline was driven by the impact of unfavorable legislation that was passed in California that went into effect in January 2024, along with the Company’s continued process of relocating underperforming kiosks to optimize fleet profitability.

Total operating expenses declined 16% to $15.0 million for the fourth quarter of 2024 compared to $17.8 million for the fourth quarter of 2023 due to the costs of going public in 2023 that did not recur in 2024.

Net income for the fourth quarter of 2024 increased significantly to $5.4 million compared to a net loss of $1.7 million for the fourth quarter of 2023. The increase was due to lower depreciation and amortization and lower operating expenses in 2024.

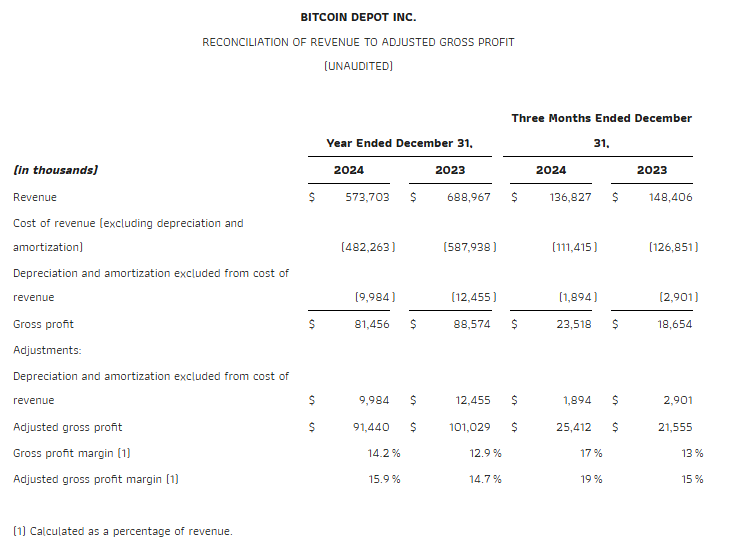

Adjusted gross profit, a non-GAAP measure, in the third quarter of 2024 increased 18% to $25.4 million from $21.6 million for the fourth quarter of 2023. Adjusted gross profit margin, a non-GAAP measure, in the fourth quarter of 2024 increased approximately 400 basis points to 18.6% compared to 14.5% in the fourth quarter of 2023. Please see “Explanation and Reconciliation of Non-GAAP Financial Measures” below.

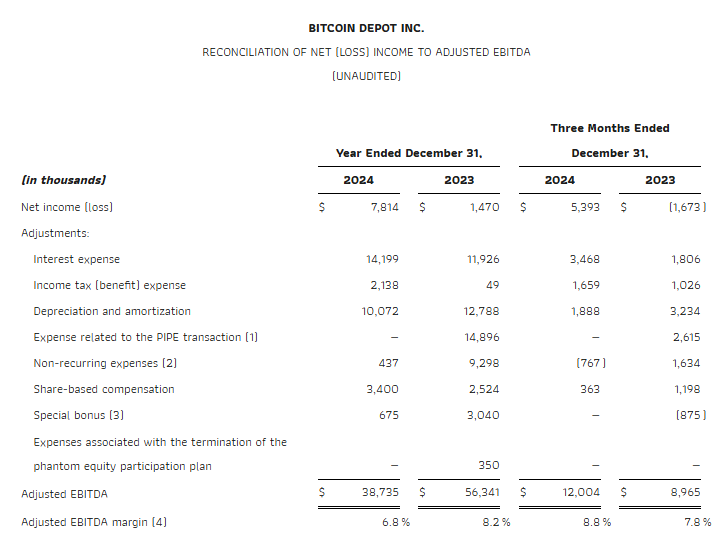

Adjusted EBITDA, a non-GAAP measure, in the fourth quarter of 2024 increased 34% to $12.0 million compared to $9.0 million for the fourth quarter of 2023. The increase was primarily due to the higher net income. Please see “Explanation and Reconciliation of Non-GAAP Financial Measures” below.

Full Year 2024 Financial Results

Revenue in 2024 was $573.7 million from $689.0 million in 2023. This decline was largely driven by the impact of unfavorable legislation that was passed in California that went into effect in January 2024, along with the Company’s continued process of relocating underperforming kiosks in order to optimize fleet profitability.

Total operating expenses declined 5% to $67.2 million compared to $70.6 million in 2023 due to the costs of going public in 2023 that did not recur in 2024 as well as other cost saving measures.

Net income in 2024 increased by 432% to $7.8 million compared to $1.5 million in 2023. The increase was primarily due to expenses with going public in 2023 that did not recur in 2024 along with other expense reductions.

Adjusted gross profit, a non-GAAP measure, in 2024 was $91.4 million compared to $101.0 million in 2023. The adjusted gross profit margin, a non-GAAP measure, in 2024 increased 120 basis points to 15.9% compared to 14.7% in 2023. Please see “Explanation and Reconciliation of Non-GAAP Financial Measures” below.

Adjusted EBITDA, a non-GAAP measure, in 2024 was $38.7 million compared to $56.3 million in 2023. The decline was due to the lower revenue. Please see “Explanation and Reconciliation of Non-GAAP Financial Measures” below.

Cash, cash equivalents, and cryptocurrencies were $31.0 million as of the end of 2024 compared to $30.5 million at the end of 2023.

Q1 2025 Outlook

Q1 2025 is off to a very strong start as we continue to see growth from our relocation strategy. We anticipate Q1 revenues to be between $151 million and $154 million which would represent growth of between 9% and 11% compared to Q1 2024.

We are projecting adjusted EBITDA for Q1 2025 to be between $12 million and $14 million which would represent growth of over 200% compared to Q1 of 2024.

Conference Call

Bitcoin Depot will hold a conference call at 10:00 a.m. Eastern time (7:00 a.m. Pacific time) today to discuss its financial results for the fourth quarter and full year ended December 31, 2024.

Call Date: Tuesday, March 18, 2025 Time: 10:00 a.m. Eastern time (7:00 a.m. Pacific time)

Phone Instructions U.S. dial-in: 646-968-2525 International dial-in: 888-596-4144 Conference ID: 8224936

A replay of the call will be available beginning after 2:00 p.m. Eastern time through March 25, 2025.

U.S. & Canada replay number: 800-770-2030 U.S. toll number: 609-800-9909 Conference ID: 8224936

If you have any difficulty connecting with the conference call, please contact Bitcoin Depot’s investor relations team at 1-949-574-3860.

About Bitcoin Depot

Bitcoin Depot Inc. (Nasdaq: BTM) was founded in 2016 with the mission to connect those who prefer to use cash to the broader, digital financial system. Bitcoin Depot provides its users with simple, efficient and intuitive means of converting cash into Bitcoin, which users can deploy in the payments, spending and investing space. Users can convert cash to bitcoin at Bitcoin Depot kiosks in 48 states and at thousands of name-brand retail locations in 29 states through its BDCheckout product. The Company has the largest market share in North America with over 8,400 kiosk locations as of February 25, 2025. Learn more at www.bitcoindepot.com.

This press release and any oral statements made in connection herewith include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Exchange Act of 1934, as amended. Forward-looking statements are any statements other than statements of historical fact, and include, but are not limited to, statements regarding the expectations of plans, business strategies, objectives and growth and anticipated financial and operational performance, including our growth strategy and ability to increase deployment of our products and services, our ability to strengthen our financial profile, and worldwide growth in the adoption and use of cryptocurrencies. These forward-looking statements are based on management’s current beliefs, based on currently available information, as to the outcome and timing of future events. Forward-looking statements are often identified by words such as “anticipate,” “appears,” “approximately,” “believe,” “continue,” “could,” “designed,” “effect,” “estimate,” “evaluate,” “expect,” “forecast,” “goal,” “initiative,” “intend,” “may,” “objective,” “outlook,“ ”plan,“ ”potential,“ ”priorities,“ ”project,“ ”pursue,“ ”seek,“ ”should,“ ”target,“ ”when,“ ”will,“ ”would,” or the negative of any of those words or similar expressions that predict or indicate future events or trends or that are not statements of historical matters, although not all forward-looking statements contain such identifying words. In making these statements, we rely upon assumptions and analysis based on our experience and perception of historical trends, current conditions, and expected future developments, as well as other factors we consider appropriate under the circumstances. We believe these judgments are reasonable, but these statements are not guarantees of any future events or financial results. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by any investor as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond our control.

These forward-looking statements are subject to a number of risks and uncertainties, including changes in domestic and foreign business, market, financial, political and legal conditions; failure to realize the anticipated benefits of the business combination; risks relating to the uncertainty of our projected financial information; future global, regional or local economic and market conditions; the development, effects and enforcement of laws and regulations; our ability to manage future growth; our ability to develop new products and services, bring them to market in a timely manner and make enhancements to our platform; the effects of competition on our future business; our ability to issue equity or equity-linked securities; the outcome of any potential litigation, government and regulatory proceedings, investigations and inquiries; and those factors described or referenced in filings with the Securities and Exchange Commission. If any of these risks materialize or our assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that we do not presently know or that we currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In addition, forward-looking statements reflect our expectations, plans or forecasts of future events and views as of the date of this press release. We anticipate that subsequent events and developments will cause our assessments to change.

We caution readers not to place undue reliance on forward-looking statements. Forward-looking statements speak only as of the date they are made, and we undertake no obligation to update publicly or otherwise revise any forward-looking statements, whether as a result of new information, future events, or other factors that affect the subject of these statements, except where we are expressly required to do so by law. All written and oral forward-looking statements attributable to us are expressly qualified in their entirety by this cautionary statement.

Explanation and Reconciliation of Non-GAAP Financial Measures

Bitcoin Depot reports its financial results in accordance with accounting principles generally accepted in the United States of America (“GAAP”). This press release includes both historical and projected Adjusted EBITDA, Adjusted Gross Profit, and certain ratios and other metrics derived therefrom such as Adjusted EBITDA margin and Adjusted Gross Profit margin, which are not prepared in accordance with GAAP.

Bitcoin Depot defines Adjusted EBITDA as net income before interest expense, income tax expense, depreciation and amortization, non-recurring expenses, share-based compensation, expenses related to the PIPE financing and miscellaneous cost adjustments. Such items are excluded from Adjusted EBITDA because these items are non-cash in nature, or because the amount and timing of these items is unpredictable, not driven by core results of operations and renders comparisons with prior periods and competitors less meaningful. In addition, Bitcoin Depot defines Adjusted Gross Profit (a non-GAAP financial measure) as revenue less cost of revenue (excluding depreciation and amortization) and depreciation and amortization adjusted to add back depreciation and amortization. Bitcoin Depot believes Adjusted EBITDA and Adjusted Gross Profit each provide useful information to investors and others in understanding and evaluating Bitcoin Depot’s results of operations, as well as provide a useful measure for period-to-period comparisons of Bitcoin Depot’s business performance. Adjusted EBITDA and Adjusted Gross Profit are each key measurements used internally by management to make operating decisions, including those related to operating expenses, evaluate performance and perform strategic and financial planning. However, you should be aware that Adjusted EBITDA and Adjusted Gross Profit are not measures of financial performance calculated in accordance with GAAP and may exclude items that are significant in understanding and assessing Bitcoin Depot’s financial results, and further, that Bitcoin Depot may incur future expenses similar to those excluded when calculating these measures. Bitcoin Depot primarily relies on GAAP results and uses both Adjusted EBITDA and Adjusted Gross Profit on a supplemental basis. Neither Adjusted EBITDA or Adjusted Gross Profit should be considered in isolation from, or as an alternative to, net income, cash flows from operations or other measures of profitability, liquidity or performance under GAAP and may not be indicative of Bitcoin Depot’s historical or future operating results. Bitcoin Depot’s computation of both Adjusted EBITDA and Adjusted Gross Profit may not be comparable to other similarly titled measures computed by other companies because not all companies calculate such measures in the same fashion. As such, undue reliance should not be placed on such measures.

Due to the high variability and difficulty in making accurate forecasts and projections of some of the information excluded from the projections of Adjusted EBITDA, together with some of the excluded information not being ascertainable or accessible, Bitcoin Depot is unable to quantify certain amounts that would be required to be included in the most directly comparable GAAP financial measures without unreasonable effort. Consequently, no disclosure of estimated comparable GAAP measures is included and no reconciliation of the forward-looking non-GAAP financial measures is included.

The following table presents a reconciliation of Net (loss) income to Adjusted EBITDA for the periods indicated:

The following table presents a reconciliation of revenue to Adjusted Gross Profit for the periods indicated:

Data from pivotal Phase 3 trial in CHB-associated liver fibrosis expected in Q2 2025

Commercial launch in the PRC of generic nintedanib for the treatment of IPF and avatrombopag maleate tablets for the treatment of CLD-associated thrombocytopenia expected in 2025

Initiation of U.S. Phase 2 trial of F351 in MASH-associated liver fibrosis expected in 2025

Full year 2025 total revenue guidance of $118 to $128 million

SAN DIEGO, March 17, 2025 (GLOBE NEWSWIRE) — Gyre Therapeutics (“Gyre”) (Nasdaq: GYRE), a self-sustainable, commercial-stage biotechnology company with clinical development programs focusing on organ fibrosis, today announced financial results for the fourth quarter and full year ended December 31, 2024 and provided a business update.

“2025 is shaping up to be a pivotal year for Gyre across both our commercial-stage and clinical-stage portfolios. We plan to expand and enhance our commercial product offerings through the additions of nintedanib for IPF, SSc-ILD and PF-ILD, as well as avatrombopag for CLD-associated thrombocytopenia and chronic idiopathic thrombocytopenia (“ITP”). Given our proven track record and extensive sales and marketing platform, we are confident in our ability to successfully launch and expand these two products in the PRC,” said Han Ying, Ph.D., Chief Executive Officer of Gyre Therapeutics. “In parallel, we expect to share topline data from our pivotal Phase 3 trial in CHB-associated liver fibrosis in the second quarter of 2025, which will help inform our U.S. Phase 2 proof-of-concept trial of F351 in MASH-associated liver fibrosis.”

Full Year 2024 Business Highlights and Upcoming Milestones

Commercial-Stage Updates

ETUARY (Pirfenidone) sales update: For the year ended December 31, 2024, Gyre Pharmaceuticals generated $105.0 million primarily in sales of ETUARY.

Nintedanib: In May 2024, Gyre Pharmaceuticals executed a comprehensive agreement with Jiangsu Wangao Pharmaceuticals Co., Ltd. to obtain the drug registration certificate for and became the marketing authorization holder of nintedanib, the other product approved for the treatment of treatment of idiopathic pulmonary fibrosis (“IPF”). In addition, it has also been approved for the treatment of SSc-ILD and PF-ILD. Gyre Pharmaceuticals plans to initiate commercialization of the nintedanib product in the PRC in 2025.

Avatrombopag: In June 2024, Gyre Pharmaceuticals received approval from China’s National Medical Products Administration (“NMPA”) for avatrombopag maleate tablets for the treatment of thrombocytopenia associated with chronic liver disease (“CLD”) and chronic idiopathic thrombocytopenia (“ITP”) in adult patients undergoing elective diagnostics procedures or therapy. Gyre Pharmaceuticals plans to begin commercialization of avatrombopag in 2025.

Pipeline Development Updates

F351 (Hydronidone):

All patients completed 52-week pivotal Phase 3 trial in chronic hepatitis B (“CHB”)-associated liver fibrosis in the PRC. In October 2024, Gyre Pharmaceuticals announced the last patient completed the 52-week pivotal Phase 3 trial. The trial is evaluating 248 patients with CHB-associated liver fibrosis in the PRC with a primary endpoint of the reduction of the liver fibrosis score (Ishak Scoring System) by at least one stage after taking F351 in combination with entecavir. Gyre expects to report topline data in the second quarter of 2025.

Plans to initiate a Phase 2 clinical trial in metabolic dysfunction-associated steatohepatitis (“MASH”)-associated liver fibrosis in 2025. Pending the results from the pivotal Phase 3 trial in CHB-associated liver fibrosis, Gyre intends to initiate a Phase 2 proof-of-concept trial in the U.S. to evaluate F351 for the treatment of MASH-associated liver fibrosis in 2025.

F573:

F573 is a caspase inhibitor and a potential Category 1 new drug for the treatment of acute/acute on-chronic liver failure (“ALF/ACLF”). Completion of the Phase 2 clinical trial of F573 as a treatment for ALF/ACLF is expected by the end of 2026.

F230:

F230, a selective endothelin receptor agonist for the treatment of pulmonary arterial hypertension (“PAH”), is expected to begin a Phase 1 trial in 2025.

F528:

F528, a novel anti-inflammation agent with the potential to modify the progression of chronic obstructive pulmonary disease (“COPD”), is undergoing preclinical studies as a potential first-line therapy for the treatment of COPD. Gyre plans to submit an IND application in 2026.

Corporate Updates

In January 2025, appointed Ping Zhang to the Company’s Board of Directors as the lead independent director and member of the Nominating Committee. In addition, Ying Luo, Ph.D., resigned as Chairman and member of the Board of Directors of Gyre and Gyre Pharmaceuticals, Gyre’s majority indirectly owned subsidiary in the People’s Republic of China (“PRC”), to focus on other responsibilities at GNI Group Ltd. Songjiang Ma has been appointed Chairman of the Board of Directors of Gyre Pharmaceuticals.

Financial Results

Cash Position

As of December 31, 2024, Gyre had cash, cash equivalents, short-term and long-term bank deposits of $51.2 million.

Financial Results for the Three Months Ended December 31, 2024

Revenues: Revenues for the three months ended December 31, 2024 were $27.9 million, compared to $27.1 million for the same period in 2023. The $0.8 million increase was primarily driven by a $1.0 million increase in ETUARY’s revenue and a $0.2 million decrease in generic drug revenue. The growth in ETUARY sales was attributed to the active expansion of the IPF treatment market, increased market penetration, and a stronger focus on ETUARY sales. To support future revenue growth, Gyre Pharmaceuticals plans to commercially launch two new products, nintedanib and avatrombopag, in 2025, which will be supported by its extensive sales and marketing platform in the PRC.

Cost of Revenues: For the three months ended December 31, 2024, cost of revenues was $1.2 million, compared to $1.3 million for the same period in 2023. The $0.1 million decrease was primarily driven by a $0.2 million decrease in generic drug cost due to the decrease in sales and a $0.1 million decrease in factory stoppage loss due to factory renovation in 2023, offset by a $0.2 million increase due to the increase of ETUARY’s cost due to the increase in sales.

Selling and Marketing Expense: For the three months ended December 31, 2024, selling and marketing expense was $16.9 million, compared to $16.5 million for the same period in 2023. The increase was primarily driven by a $2.1 million increase in promotion expense and conference expenses, offset by a $1.1 million decrease in selling and marketing payroll costs, a $0.3 million decrease in stock-based compensation expense and a $0.3 million decrease in travel and miscellaneous expenses.

Research and Development Expense: For the three months ended December 31, 2024, research and development expense was $3.7 million, compared to $4.6 million for the same period in 2023. The decrease was primarily driven by a $0.5 million decrease in pre-clinical and clinical research expenses and a $0.5 million decrease in stock-based compensation expense, offset by a $0.1 million increase in miscellaneous expense.

General and Administrative Expense: For the three months ended December 31, 2024, general and administrative expense was $5.5 million, compared to $10.1 million for the same period in 2023. The decrease was primarily driven by a $5.8 million decrease in stock-based compensation cost, offset by a $0.8 million increase in the functional and administrative department’s personnel cost and a $0.4 million increase in professional expense, including legal and consulting fees.

Income (Loss) from Operations: For the three months ended December 31, 2024, income from operations was $0.7 million, compared to $91.1 million loss from operation for the same period in 2023. The increase in income from operations was driven primarily by acquired in-process research and development expense recognized in the fourth quarter of 2023 and there was no such expense in the same period in 2024.

Net Income (Loss): For the three months ended December 31, 2024, net income was $0.6 million, compared to $101.0 million net loss for the same period in 2023.

Non-GAAP Adjusted Net Income: For the three months ended December 31, 2024, non-GAAP adjusted net income was $1.1 million, compared to $2.1 million for the same period in 2023. The decrease was primarily driven by the costs of being a public company for three months in 2024, as compared to two months in 2023.

Financial Results for the Full Year Ended December 31, 2024

Revenues: Revenues for the full year ended December 31, 2024 were $ 105.8 million, compared to $113.5 million for the same period in 2023. The $7.7 million decrease was primarily driven by a $7.1 million decrease in ETUARY’s revenue and a $0.6 million decrease in generic drug revenue as a result of decreased sales volumes. The decrease in ETUARY and generic drug sales volumes was due to fluctuations in the Chinese economy that significantly affected demand for anti-fibrosis drugs and decreasing healthcare spending generally. To support future revenue growth, Gyre plans to commercially launch two new products, nintedanib and avatrombopag, in 2025, which will be supported by Gyre Pharmaceuticals’ extensive sales and marketing platform across the PRC.

Cost of Revenues: For the full year ended December 31, 2024, cost of revenues was $3.9 million, compared to $4.6 million for the same period in 2023. The $0.7 million decrease was primarily driven by a $0.5 million factory stoppage loss due to factory renovation in 2023, which did not occur in 2024, and a $0.2 million decrease due to decreased sales volumes.

Selling and Marketing Expense: For the full year ended December 31, 2024, selling and marketing expense was $57.5 million, compared to $61.2 million for the same period in 2023. The decrease was primarily driven by a $2.4 million decrease in conference costs and promotion expense due to decreased sales activities, a $0.9 million decrease in selling and marketing payroll costs due to the decrease of sales of ETUARY in 2024, a $0.3 million decrease in share base compensation expense, and a $0.1 million decrease in miscellaneous expenses.

Research and Development Expense: For the full year ended December 31, 2024, research and development expense was $12.0 million, compared to $13.8 million for the same period in 2023. The decrease was primarily from Gyre Pharmaceuticals, and was driven by a $0.3 million decrease in materials and utilities, a $1.3 million decrease in pre-clinical research expense due to several research and development projects advancing to the clinical trials stage or reaching the application phase in 2024, and a $0.4 million decrease in staff cost due to reduced headcount, and a $0.5 million decrease in stock-based compensation, related to options being fully vested in 2023, which did not occur in 2024, This overall decrease was partially offset by a 0.7 million increase in general research and development expense from Gyre Therapeutics due to increased consulting fees.

General and Administrative Expense: For the full year ended December 31, 2024, general and administrative expense was $16.1 million, compared to $14.7 million for the same period in 2023. The increase was primarily driven by costs associated with being a public company, including a $1.9 million increase in professional expense, a $2.1 million increase in miscellaneous expenses and a $3.0 million increase in the functional and administrative department’s personnel cost, offset by a $5.6 million decrease in stock-based compensation cost.

Income (loss) from Operations: For the full year ended December 31, 2024, income from operations was $16.2 million, compared to $67.2 million loss for the same period in 2023. The increase in income from operations was driven primarily by acquired in-process research and development expense recognized in 2023 and there was no such expense in the same period in 2024.

Net Income (loss): For the full year ended December 31, 2024, net income was $17.9 million, compared to $85.5 million net loss for the same period in 2023.

Non-GAAP Adjusted Net Income: For the full year ended December 31, 2024, non-GAAP adjusted net income was $16.9 million, compared to $25.4 million for the same period in 2023. The decrease was primarily driven by a $7.7 million decline in revenue and a $1.1 million increase in operating expenses. Despite these changes, the gross profit margin remained consistent.

Full Year 2025 Financial Guidance

For the full year 2025, the Company expects to generate revenues of $118 to $128 million, representing growth of 11.3% to 20.8% over 2024 revenue, primarily driven by the anticipated commercial launches of nintedanib and avatrombopag and sales of ETUARY.

Guidance Range

Total Revenue

$118 to $128 million

Please note the following regarding the total revenue guidance:

Guidance assumes a constant foreign currency exchange rate.

Guidance assumes no significant economic disruption or downturn.

Use of Non-GAAP Financial Measures by Gyre Therapeutics, Inc.

Gyre reports financial results in accordance with accounting principles generally accepted in the United States (“GAAP”). This release presents the financial measure “adjusted net income,” which is not calculated in accordance with GAAP. The most directly comparable GAAP measure for this non-GAAP financial measure is “net income.” Adjusted net income presents Gyre’s results of operations after excluding gain from change in fair value of warrants, stock-based compensation, and provision for income taxes. This is meant to supplement, and not substitute, Gyre’s financial information presented in accordance with GAAP. Adjusted net income as defined by Gyre may not be comparable to similar non-GAAP measures presented by other companies. Management believes that presenting adjusted net income provides investors with additional useful information in evaluating the Gyre’s performance and valuation. See the reconciliation of adjusted net income to net income in the section titled “Reconciliation of GAAP to Non-GAAP Financial Measures” below.

About Hydronidone (F351)

F351 is a structural analogue of the approved anti-fibrotic (IPF) drug Pirfenidone and has been shown to inhibit in vitro both p38γ kinase activity and TGF-β1-induced excessive collagen synthesis in hepatic stellate cells (“HSCs”), which are recognized as critical event in the development and progression of fibrosis in the liver. This is further supported by its anti-proliferative effects on the HSCs in the liver. In vitro anti-fibrotic effects of F351 were also confirmed in several established in vivo models of liver fibrosis such as CCI4-induced liver fibrosis mouse model, DMN-induced liver fibrosis rat model, and HSA-induced liver rat model, as well as mouse model of MASH fibrosis (CCI4+Western High Fat Diet).

About Gyre Pharmaceuticals

Gyre Pharmaceuticals is a commercial-stage biopharmaceutical company committed to the research, development, manufacturing and commercialization of innovative drugs for organ fibrosis. Its flagship product, ETUARY® (Pirfenidone capsule), was the first approved treatment for IPF in the PRC in 2011 and has maintained a prominent market share (2024 net sales of $105.0 million). In addition, Gyre Pharmaceuticals is evaluating F351 in a Phase 3 clinical trial in CHB-associated liver fibrosis in the PRC, which is expected to readout topline data by Q2 2025. F351 received Breakthrough Therapy designation by the NMPA Center for Drug Evaluation in March 2021. Gyre Pharmaceuticals is also developing treatments for PD, DKD, COPD, PAH and ALF/ACLF. In October 2023, Gyre Therapeutics acquired an indirect majority interest in Gyre Pharmaceuticals (also known as Beijing Continent Pharmaceuticals Co., Ltd.).

About Gyre Therapeutics

Gyre Therapeutics is a biopharmaceutical company headquartered in San Diego, CA, with a primary focus on the development and commercialization of F351 (Hydronidone) for the treatment of MASH-associated fibrosis in the U.S. Gyre’s development strategy for F351 in MASH is based on the company’s experience in MASH rodent model mechanistic studies and CHB-induced liver fibrosis clinical studies. Gyre is also advancing a diverse pipeline in the PRC through its indirect controlling interest in Gyre Pharmaceuticals, including ETUARY therapeutic expansions, F573, F528, and F230.

Forward-Looking Statements

This press release contains “forward-looking statements” within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, which statements are subject to substantial risks and uncertainties and are based on estimates and assumptions. All statements, other than statements of historical facts included in this press release, are forward-looking statements, including statements concerning: the expectations regarding Gyre’s research and development efforts, timing of expected clinical readouts, including timing of topline data from Gyre Pharmaceuticals’ Phase 3 clinical trial evaluating F351 for the treatment of CHB-associated liver fibrosis in the PRC, initiation of Gyre’s Phase 2 trial in the U.S. for F351 for the treatment of MASH-associated liver fibrosis, timing of completion of Gyre’s Phase 2 clinical trial in the PRC of F573 for ALF/ACLF, initiation of Phase 1 trial of F230 for the treatment of PAH and IND submission of F528 in COPD, the expectations regarding commercial launch of nintedanib and avatrombopag maleate tablets, interactions with regulators, expectations regarding future product sales, and Gyre’s financial position and cash resources. In some cases, you can identify forward-looking statements by terms such as “may,” “might,” “will,” “objective,” “intend,” “should,” “could,” “can,” “would,” “expect,” “believe,” “design,” “estimate,” “predict,” “potential,” “plan” or the negative of these terms, and similar expressions intended to identify forward-looking statements. These statements reflect our plans, estimates, and expectations, as of the date of this press release. These statements involve known and unknown risks, uncertainties and other factors that could cause our actual results to differ materially from the forward-looking statements expressed or implied in this press release. Actual results and the timing of events could differ materially from those anticipated in such forward-looking statements as a result of these risks and uncertainties, which include, without limitation: Gyre’s ability to execute on its clinical development strategies; positive results from a clinical trial may not necessarily be predictive of the results of future or ongoing clinical trials; the timing or likelihood of regulatory filings and approvals; competition from competing products; the impact of general economic, health, industrial or political conditions in the United States or internationally; the sufficiency of Gyre’s capital resources and its ability to raise additional capital. Additional risks and factors are identified under “Risk Factors” in Gyre’s Annual Report on Form 10-K for the year ended December 31, 2023 filed on March 27, 2024 and in other filings with the Securities and Exchange Commission.

Gyre expressly disclaims any obligation to update any forward-looking statements whether as a result of new information, future events or otherwise, except as required by law.

Townsquare is a community-focused digital media and digital marketing solutions company with market leading local radio stations, principally focused outside the top 50 markets in the U.S. Our assets include a subscription digital marketing services business, Townsquare Interactive, providing website design, creation and hosting, search engine optimization, social media and online reputation management as well as other digital monthly services for approximately 26,800 SMBs; a robust digital advertising division, Townsquare IGNITE, a powerful combination of a) an owned and operated portfolio of more than 330 local news and entertainment websites and mobile apps along with a network of leading national music and entertainment brands, collecting valuable first party data, and b) a proprietary digital programmatic advertising technology stack with an in-house demand and data management platform; and a portfolio of 321 local terrestrial radio stations in 67 U.S. markets strategically situated outside the Top 50 markets in the United States. Our portfolio includes local media brands such as WYRK.com, WJON.com, and NJ101.5.com and premier national music brands such as XXLmag.com, TasteofCountry.com, UltimateClassicRock.com and Loudwire.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q4 results. The company reported Q4 revenue of $117.8 million, up 2.6% year over year, and adj. EBITDA of $31.2 million, up 25.8%, both of which were modestly better than our estimates of $115.0 million and $30.4 million, respectively. Notably, the company’s digital businesses were a key revenue growth driver, up a strong 11%. Digital revenue comprised 52% of total company revenue. Notably, revenue momentum appears favorable into the second quarter.

Digital leads the way. Total digital revenue growth of 11% was comprised of digital advertising growth of 15% and a swing toward revenue growth in its subscription digital marketing solutions (DMS) of 1.9%. DMS returned to revenue growth for the first time since Q4 of 2022. Second quarter digital revenue continues to be strong, expected to increase a solid 7.3% in Q2.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Full-year 2024 financial results. InPlay Oil reported full-year net income and earnings per share of C$9.5 million and C$0.10, respectively, below our estimates of approximately C$11.4 million and C$0.12. The variance was primarily due to lower-than-expected natural gas revenue driven by weaker AECO pricing. Production for the year averaged 8,712 barrels of oil equivalent per day (boe/d) compared to 9,025 boe/d in 2023. Consequently, revenue decreased to C$153.7 million compared to C$179.4 million in 2023. Adjusted funds flow in 2024 was C$68.5 million, down from C$91.8 million in 2023.

Updated 2025 estimates. Please note that our revised estimates assume the closing of the pending Pembina acquisition on April 15th, 2025. For 2025, our oil and gas revenue estimate is C$333.5 million compared to our prior estimate of C$159.4 million. We have raised our 2025 AFF and EPS estimates to C$161.6 million and C$0.27, respectively, from C$71.7 million and C$0.14. We forecast net income of C$40.9 million, up from our previous estimate of C$13.2 million. Our 2025 estimates are based on an average annual production of 15,879 boe/d compared to our prior forecast of 8,901 boe/d.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q Results. Total revenue for the quarter was $26.1 million, as the HPC business added $14.4 million from last year. We estimated revenue of $29.6 million. Higher G&A and D&A costs partially offset a $43.4 million digital asset gain, resulting in an operating income of $28.8 million. Net income was $29.0 million from $17,700 a year ago. Adjusted EBITDA was $40.1 million from $14.0 million last year.

Pipeline Building Up. Management noted that demand has surged for the B200 GPUs, and with the introduction of DeepSeek, customers are also in demand of the H100 and H200 GPUs. Furthermore, the Company’s data center pipeline has expanded to 510MW from 288MW last quarter. With the increase in demand and management in active discussions with potential customers, we expect more agreements to be announced sooner rather than later.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).Bit Digital (BTBT) – Building on its Pipeline

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Google’s $32 billion acquisition of Wiz marks its largest purchase ever, highlighting its commitment to cloud security – Founded in 2020, Wiz achieved $100 million in annual recurring revenue in just 18 months before accepting Google’s offer – Despite initial resistance to acquisition, Wiz will maintain multi-cloud functionality across AWS, Azure, and Oracle Cloud

Google has announced a definitive agreement to acquire Wiz, a fast-growing cloud security startup, for $32 billion in an all-cash deal. The acquisition, set to close in 2026, marks Google’s most significant purchase ever, surpassing its $12.5 billion Motorola deal in 2012. Wiz will become part of Google Cloud, strengthening the tech giant’s security capabilities amid rising cybersecurity threats and AI-driven advancements.

According to Google, the integration will leverage their cloud infrastructure leadership and AI expertise to enhance and scale Wiz’s solutions across major cloud platforms. This strategic combination aims to benefit customers and partners throughout the cloud ecosystem.

Founded in 2020, Wiz has grown rapidly under the leadership of co-founder Assaf Rappaport. The company reached $100 million in annual recurring revenue within just 18 months and has since positioned itself as a major player in cloud security. Wiz’s product portfolio includes prevention, detection, and response solutions that appeal to enterprises seeking robust cybersecurity defenses in increasingly complex environments.

Initially, Wiz had resisted acquisition offers. In July 2024, CNBC reported that Wiz walked away from a $23 billion acquisition offer from Google, choosing instead to pursue an initial public offering (IPO). Rappaport cited concerns over antitrust scrutiny and investor sentiment as factors in the decision. However, the latest agreement indicates a shift in strategy, with Wiz seeing Google’s backing as an opportunity to accelerate innovation rather than going public.

Rappaport has expressed that joining Google Cloud will dramatically accelerate their innovation capabilities beyond what would be possible as an independent company. This represents a significant change in perspective from their earlier position.

Google’s move to acquire Wiz is part of its broader effort to bolster its cybersecurity offerings. In 2022, the company acquired cybersecurity firm Mandiant for $5.4 billion, enhancing its threat detection and incident response capabilities. With Wiz’s cloud security expertise now joining the fold, Google positions itself to compete more effectively with industry rivals like Microsoft, which has also invested heavily in security software as cloud adoption continues to accelerate.

Despite the acquisition, Wiz’s products will continue to operate across competing platforms, including Amazon Web Services, Microsoft Azure, and Oracle Cloud. This cross-platform approach ensures that existing customers can maintain their security infrastructure without disruption, a critical factor for enterprises with multi-cloud strategies.

The deal is expected to face regulatory scrutiny, particularly as Alphabet, Google’s parent company, is already battling an antitrust lawsuit over its dominance in online search. However, Wall Street analysts believe that President Donald Trump’s administration may take a more favorable stance on tech industry mergers, potentially easing regulatory hurdles for this landmark acquisition.

With cybersecurity threats becoming more sophisticated and cloud adoption continuing to grow, Google’s acquisition of Wiz signals a strategic move to fortify its security offerings and drive long-term growth in the cloud computing space, where security has become a decisive factor for enterprise customers choosing between cloud providers.