Toronto, Ontario–(Newsfile Corp. – February 25, 2025) – Aurania Resources Ltd. (TSXV: ARU) (OTCQB: AUIAF) (FSE: 20Q) (“Aurania” or the “Company”) is pleased to announce the appointment of Ms. Carolina Lasso as Vice President, Corporate Social Responsibility.

Carolina Lasso has 20 years of experience in corporate social responsibility, public policy, and strategic communications. She has led sustainable development initiatives for rural and vulnerable communities, strengthening public-private partnerships and international cooperation. In her role as Head of Corporate Social Responsibility and Government Relations at Aurania’s subsidiary company, Ecuasolidus, she has driven high impact CSR strategies, securing the social license to operate and fostering strong community and stakeholder engagement. She also served as Executive Director of the Step Forward Foundation since 2019, overseeing ninety-two development projects in education, health, water, and economic growth. Previously, she worked at the Ministry of Foreign Affairs of Colombia (2010-2017) where she managed border development programs across Colombia’s borders and oversaw the Amazon region, working with Indigenous communities, FARC reintegration efforts, and conflict-affected populations. Ms. Lasso developed post-conflict reintegration models and led initiatives benefiting seventy-seven municipalities. She is fluent in Spanish and English, with intermediate proficiency in French. Ms. Lasso holds a Bachelor’s Degree in International Relations, a Postgraduate Diploma in Peacebuilding and Armed Conflict Resolution, and a Master’s Degree in Political Science. This appointment is subject to approval by the TSX Venture Exchange.

“Carolina tackles tasks and challenges with creativity and determination, thinking outside of the box whilst building strong relationships along the way. She has been a driving force behind Aurania’s CSR efforts, always leading with purpose, determination, and vision,” stated Dr. Keith Barron, Chairman and CEO. “In her expanded role, Carolina will oversee and guide all of our CSR initiatives, ensuring that Aurania’s commitment to sustainability and community engagement continues to grow across all our operations.”

Pursuant to the Company’s Stock Option Plan, the Board of Directors has granted Ms. Lasso 20,000 Stock Options in the Company at an exercise price of C$0.37 each. The Options have a 5-year expiry term and shall vest as to one-third immediately, with an additional one-third vesting one year from their date of grant, and the final one-third vesting two years after their date of grant.

About Aurania

Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and copper in South America. Its flagship asset, The Lost Cities – Cutucu Project, is located in the Jurassic Metallogenic Belt in the eastern foothills of the Andes mountain range of southeastern Ecuador.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Noble Capital Markets’ Emerging Growth Virtual Equity Conference – June 3-4, 2026

Set to be an immersive experience, bringing together investors, industry leaders, and experts from middle market public companies across all sectors. Featuring:

Corporate presentations with Fireside-style Q&A session proctored by Noble’s analysts and bankers

Scheduled 1×1 meetings with qualified investors

Up to 50 presenting companies, representing a wide array of sectors.

Noble’s investor base extends beyond traditional institutions to include family offices, money managers, and high-net-worth individuals who actively engage in smaller cap, open market transactions.

Noble’s investors crave the undervalued investment idea.

And not just investors that attend the live event. Channelchek will host replays of the corporate presentations and Q&A sessions right here, for all investors to view, free of charge, for the rest of the year.

Participation in conferences, both in-person and virtually, has proven to help in boosting awareness and liquidity. And Noble’s service offerings extend well beyond the conference circuit; our events are an extension of the year-round investor access we provide.

Ready to Register to Present? Click the link below:

Townsquare is a community-focused digital media and digital marketing solutions company with market leading local radio stations, principally focused outside the top 50 markets in the U.S. Our assets include a subscription digital marketing services business, Townsquare Interactive, providing website design, creation and hosting, search engine optimization, social media and online reputation management as well as other digital monthly services for approximately 26,800 SMBs; a robust digital advertising division, Townsquare IGNITE, a powerful combination of a) an owned and operated portfolio of more than 330 local news and entertainment websites and mobile apps along with a network of leading national music and entertainment brands, collecting valuable first party data, and b) a proprietary digital programmatic advertising technology stack with an in-house demand and data management platform; and a portfolio of 321 local terrestrial radio stations in 67 U.S. markets strategically situated outside the Top 50 markets in the United States. Our portfolio includes local media brands such as WYRK.com, WJON.com, and NJ101.5.com and premier national music brands such as XXLmag.com, TasteofCountry.com, UltimateClassicRock.com and Loudwire.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New credit agreement. On February 19, 2025, the company entered into a five year $490 million credit agreement with Bank of America. The agreement is comprised of a $470 million term loan and a $20 million revolving credit facility, both of which mature on February 19, 2030. Notably, we believe the favorable agreement provides the company with a long runway and should assuage investor debt refinancing concerns.

Termination of old agreement. The company utilized net proceeds from the new credit agreement and its cash position to immediately retire its prior credit agreement. As such, $453 million from the term loan and roughly $10 million from the revolving credit facility were used to retire the outstanding $467.4 million 6.875% senior secured notes that were due in 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

For more than 70 years, Vectrus has provided critical mission support for our customers’ toughest operational challenges. As a high-performing organization with exceptional talent, deep domain knowledge, a history of long-term customer relationships, and groundbreaking technical expertise, we deliver innovative, mission-matched solutions for our military and government customers worldwide. Whether it’s base operations support, supply chain and logistics, IT mission support, engineering and digital integration, security, or maintenance, repair and overhaul, our customers count on us for on-target solutions that increase efficiency, reduce costs, improve readiness, and strengthen national security. Vectrus is headquartered in Colorado Springs, Colo., and includes about 8,100 employees spanning 205 locations in 28 countries. In 2021, Vectrus generated sales of $1.8 billion. For more information, visit the company’s website at www.vectrus.com or connect with Vectrus on Facebook, Twitter, and LinkedIn.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Records. Driven by on-contract growth and new awards, V2X posted record quarterly revenue, adjusted EBITDA, and cash flow. Full year contract wins of $5.5 billion were another record. With capabilities aligned with the Trump Administration’s goals and a large addressable market, we believe V2X is well positioned to capture additional growth going forward.

4Q Results. Revenue grew 11.4% to $1.158 billion from $1.04 billion in 4Q23. Adjusted EBITDA came in at $86.2 million, up from $82 million last year. V2X reported adjusted EPS of $1.33 in 4Q24, up from $1.22 a year ago. Adjusted OCF hit $168 million compared to $76 million in the year ago period.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

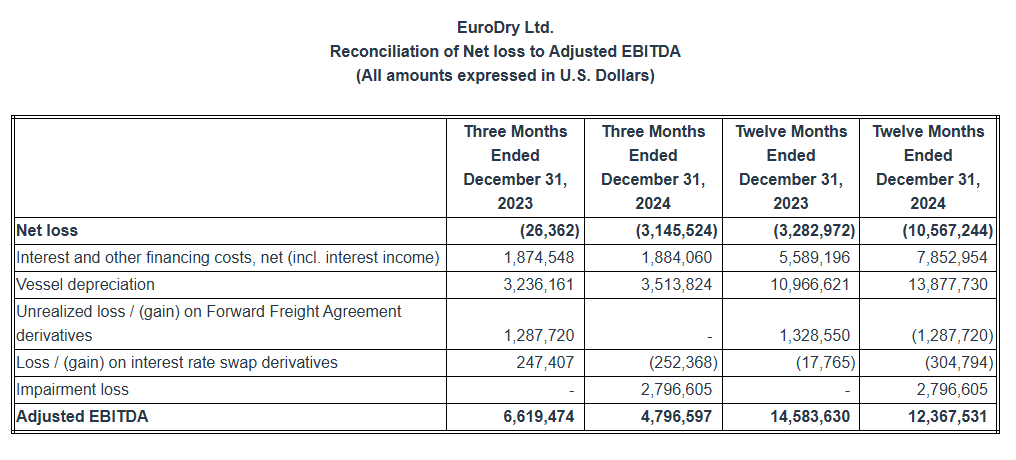

Fourth quarter financial results. EuroDry Ltd. reported an adjusted fourth-quarter net loss to controlling shareholders of $0.7 million, or ($0.25) per share, compared to adjusted net income of $1.9 million, or $0.70 per share, during the prior year period. Adjusted EBITDA declined to $4.8 million compared to $6.6 million during the prior year period. The year-over-year decline is due to low market rates as trade volume has fallen amid a slowdown in the Chinese economy.

Full year 2024 earnings and updated 2025 estimates. For the full year 2024, adjusted EBITDA and earnings per share declined to $12.4 million and ($3.02), respectively, from $14.6 million and $0.12 in 2023. We have lowered our 2025 adjusted EBITDA and EPS estimates to $19.6 million and ($0.43), respectively, from $22.0 million and ($0.34). While we expect spot and one-year time charter equivalent rates to improve throughout the year, our estimates have been lowered compared to our previous expectations due to weak market conditions.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Optimization study identifies sources of lower cost.Century Lithium recently completed an initial internal optimization study of its Angel Island Lithium project. The review identified cost reductions of up to 25%, or $395.2 million, associated with the project’s Phase I capital expenditures totaling $1,580.7 billion. Recall the most recent feasibility study dated April 29, 2024, contemplates three phases of production with the capital costs associated with the second and third phases amounting to $657.0 million and $1,338.5 billion, respectively.

Key areas of focus.Among other potential cost savings, the study identified opportunities to reduce capital costs through changes in the flow sheet, equipment selection, and updated vendor quotes in the processing areas of filtration, direct lithium extraction, and the chlor-alkali plant. The study also identified potential areas where modification of site facilities and the elimination of inefficiencies could streamline the process from mining to the production of battery-grade lithium. We expect that some of these efficiencies may extend to Phases II and III thus offering the potential for additional savings.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CHICAGO–(BUSINESS WIRE)– MAIA Biotechnology, Inc., (NYSE American: MAIA) (“MAIA”, the “Company”), a clinical-stage biopharmaceutical company developing targeted immunotherapies for cancer, today announced that it has entered into definitive agreements for the purchase and sale of an aggregate of 952,300 shares of common stock at a purchase price of $1.50 per share, in a non-brokered private placement to accredited investors and certain Company directors. Each share of common stock is being offered together with a warrant to purchase one share of common stock at an exercise price of $1.85 per share, which price represents the greater of the book or market value of the stock on the date the definitive agreements were executed (subject to customary adjustments as set forth in the warrants). The warrants are exercisable commencing one year following issuance and have a term of six years from the initial issuance date. The securities being sold to Company directors participating in the offering are being issued pursuant to the Company’s 2021 Equity Incentive Plan. The private placement is expected to close on or about February 26, 2025, subject to the satisfaction of customary closing conditions.

The gross proceeds from the offering are expected to be approximately $1.43 million, prior to offering expenses payable by the Company. The Company closed a private placement of approximately $2.7 million on February 24, 2025 and the aggregate gross proceeds from both private placements are expected to be $4.1 million, prior to deducting offering expenses payable by the Company. The Company intends to use the combined net proceeds received from the two private placements to fund the starting cost for Part C of the Phase 2 THIO -101 clinical trial and for working capital.

The securities described above are being offered in a private placement under Section 4(a)(2) of the Securities Act of 1933, as amended (the “Securities Act”), and/or Regulation D promulgated thereunder and, along with the shares of common stock underlying the warrants, have not been registered under the Securities Act or applicable state securities laws and do not have registration rights. Accordingly, the warrants and underlying shares of common stock may not be offered or sold in the United States except pursuant to an effective registration statement or an applicable exemption from the registration requirements of the Securities Act and such applicable state securities laws. The securities issued in the Private Placement will be “restricted securities” under the U.S. Securities Act.

This press release shall not constitute an offer to sell or a solicitation of an offer to buy these securities, nor shall there be any sale of these securities in any state or other jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such state or other jurisdiction.

About MAIA Biotechnology, Inc.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Forward-Looking Statements

MAIA cautions that all statements, other than statements of historical facts contained in this press release, are forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels or activity, performance or achievements to be materially different from those anticipated by such statements. The use of words such as “may,” “might,” “will,” “should,” “could,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “project,” “intend,” “future,” “potential,” or “continue,” and other similar expressions are intended to identify forward-looking statements. However, the absence of these words does not mean that statements are not forward-looking. For example, all statements we make regarding (i) the initiation, timing, cost, progress and results of our preclinical and clinical studies and our research and development programs, (ii) our ability to advance product candidates into, and successfully complete, clinical studies, (iii) the timing or likelihood of regulatory filings and approvals, (iv) our ability to develop, manufacture and commercialize our product candidates and to improve the manufacturing process, (v) the rate and degree of market acceptance of our product candidates, (vi) the size and growth potential of the markets for our product candidates and our ability to serve those markets, (vii) our expectations regarding our ability to obtain and maintain intellectual property protection for our product candidates; (viii) the completion of the offering and (ix) the satisfaction of customary closing conditions related to the offering, are forward looking. All forward-looking statements are based on current estimates, assumptions and expectations by our management that, although we believe to be reasonable, are inherently uncertain. Any forward-looking statement expressing an expectation or belief as to future events is expressed in good faith and believed to be reasonable at the time such forward-looking statement is made. However, these statements are not guarantees of future events and are subject to risks and uncertainties and other factors beyond our control that may cause actual results to differ materially from those expressed in any forward-looking statement. Any forward-looking statement speaks only as of the date on which it was made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. In this release, unless the context requires otherwise, “MAIA,” “Company,” “we,” “our,” and “us” refers to MAIA Biotechnology, Inc. and its subsidiaries.

Indo-Pacific revenue growth of 27% y/y driven by increased demand

Book-to-bill of 1.2x in the quarter and total backlog of $12.5 billion as of December 31, 2024

Record net income of $25.0 million; Adjusted net income1 of $42.7 million, up 10% y/y

Grew adjusted EBITDA1 $4.1 million y/y to $86.2 million, with a margin of 7.4%

Diluted EPS of $0.78; Adjusted diluted EPS1 of $1.33, up 9% y/y

Strong year-to-date cash flow from operations of $254 million

Achieved net debt reduction of $210 million and 2.6x net leverage ratio1

RESTON, Va., Feb. 24, 2025 /PRNewswire/ — V2X, Inc. (NYSE: VVX) announced fourth quarter and full-year 2024 financial results.

“Our growth momentum continued into the fourth quarter with revenue increasing 11% year-over-year, driven by solid growth in all geographies and underscored by 27% growth in the Indo-Pacific region, as the DoD continues to focus on enhancing readiness and deterrence,” said Jeremy Wensinger, President and Chief Executive Officer. “The combination of our unique mission insight, comprehensive full lifecycle capabilities, and 80-year reputation as a trusted partner is yielding results through expansion in key theaters, exceptional financial performance, and recent awards, which achieved a book-to-bill of 1.2x. The leading indicators in our business remain strong with a $12.5 billion backlog, limited recompetes, and a robust pipeline of new opportunities.”

Mr. Wensinger continued, “Looking ahead, we are excited about the future. We believe our track record of enhancing outcomes and increasing value for customers through innovation, modernization, and improved operational performance can enable the DoD to solve its very real challenge of having to be prepared for today while planning for the threats of tomorrow.”

Mr. Wensinger concluded, “I’d like to recognize the 16,000 plus V2X employees for all their contributions and performance throughout the year and in particular during the fourth quarter. We thank you for all you have done and continue to do for our nation and our company.”

Fourth Quarter 2024 Results

“V2X reported record revenue of $1.16 billion in the quarter, which represents 11% year-over-year growth,” said Shawn Mural, Senior Vice President and Chief Financial Officer. “We closed the year with strong performance across all financial metrics, driven by double digit topline growth and excellent cash generation.”

“For the quarter, the Company reported operating income of $51.6 million and adjusted operating income1 of $80.6 million. V2X delivered record adjusted EBITDA1 of $86.2 million, with a margin of 7.4%. Fourth quarter GAAP diluted EPS was $0.78. Adjusted diluted EPS1 for the quarter increased 9% year-over-year to $1.33.”

“Fourth quarter net cash provided by operating activities was $223.1 million. Adjusted net cash provided by operating activities1 increased 122% year-over-year to $168.2 million.”

“Our continued focus on cash generation and debt reduction yielded notable results with net debt improving $210 million dollars year-over-year. At the end of the fourth quarter, net debt for V2X was $874 million. Our commitment to achieve a net leverage ratio at or below 3.0x was a company-wide priority. I’m pleased to report that we demonstrated excellent performance on this front, delivering a net leverage ratio1 of 2.6x at the end of the fourth quarter, which represents a 0.7x improvement year-over-year.”

“Total backlog as of December 31, 2024, was $12.5 billion. Funded backlog was $2.3 billion. Book-to-bill in the quarter was approximately 1.2x.”

Full-Year 2024 Results

“Full-year revenue was $4.32 billion, up 9% year-over-year. The Company reported full-year operating income of $159.2 million and adjusted operating income1 of $286.2 million. Full-year adjusted EBITDA1 was $310.2 million with a margin of 7.2%. Full-year GAAP diluted EPS was $1.08. Adjusted diluted EPS1 for 2024 was $4.34, increasing 16% year-over-year. On a year-to-date basis, net cash provided by operating activities was $254.2 million. Adjusted net cash provided by operating activities1 was $161.0 million.”

2025 Guidance

Mr. Mural concluded, “The trends in our business remain positive and we believe our strategy to deliver full lifecycle solutions that increase efficiency, reduce costs, modernize capabilities, improve readiness, and strengthen national security provides substantial opportunities for future growth and value creation. For 2025 we are setting the mid-point of our guidance for revenue and Adjusted EBITDA1 at $4.44 billion and $313 million, respectively. This assumes revenue and adjusted EBITDA to be weighted more heavily in the second half of the year. Revenue guidance at the mid-point assumes approximately 4% contribution from recompetes.”

Guidance for 2025 is as follows:

$ millions, except for per share amounts

2025 Guidance

2025 Mid-Point

Revenue

$4,375

$4,500

$4,438

Adjusted EBITDA1

$305

$320

$313

Adjusted Diluted Earnings Per Share1

$4.45

$4.85

$4.65

Adjusted Net Cash Provided by Operating Activities1

$150

$170

$160

The Company is not providing a quantitative reconciliation with respect to the foregoing forward-looking non-GAAP measures in reliance on the “unreasonable efforts” exception set forth in SEC rules because certain financial information, the probable significance of which cannot be determined, is not available and cannot be reasonably estimated. For example, unusual, one-time, non-ordinary, or non-recurring costs, which relate to M&A, integration and related activities cannot be reasonably estimated. Forward-looking statements are based upon current expectations and are subject to factors that could cause actual results to differ materially from those suggested here, including those factors set forth in the Safe Harbor Statement below.

Fourth Quarter Conference Call

Management will conduct a conference call with analysts and investors at 4:30 p.m. ET on Monday, February 24, 2025. U.S.-based participants may dial in to the conference call at 877-300-8521, while international participants may dial 412-317-6026. A live webcast of the conference call as well as an accompanying slide presentation will be available here: https://app.webinar.net/W6kmnm4z8V9

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through March 10, 2025, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 10195666.

Presentation slides that will be used in conjunction with the conference call will also be made available online in advance on the “investors” section of the company’s website at https://gov2x.com. V2X recognizes its website as a key channel of distribution to reach public investors and as a means of disclosing material non-public information to comply with its obligations under the U.S. Securities and Exchange Commission (“SEC”) Regulation FD.

1

See “Key Performance Indicators and Non-GAAP Financial Measures” for descriptions and reconciliations.

About V2X V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Safe Harbor Statement Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 (the “Act”): Certain material presented herein includes forward-looking statements intended to qualify for the safe harbor from liability established by the Act. These forward-looking statements include, but are not limited to, all the statements and items listed under “2025 Guidance” above and other assumptions contained therein for purposes of such guidance, other statements about our 2025 performance outlook, revenue, contract opportunities, and any discussion of future operating or financial performance.

Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “could,” “potential,” “continue” or similar terminology. These statements are based on the beliefs and assumptions of the management of the Company based on information currently available to management. Forward-looking statements in this press release, include, but are not limited to our future performance and capabilities; our expectations regarding the pipeline of new opportunities; our belief in our ability to achieve budget efficiencies; future net leverage ratio; and our belief in our ability to achieve our total year guidance.

These forward-looking statements are not guarantees of future performance, conditions, or results, and involve a number of known and unknown risks, uncertainties, assumptions, and other important factors, many of which are outside our management’s control, which could cause actual results to differ materially from the results discussed in the forward-looking statements. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from the Company’s historical experience and our present expectations or projections. For a discussion of some of the risks and uncertainties that could cause actual results to differ from such forward-looking statements, see the risks and other factors detailed from time to time in our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and other filings with the SEC.

We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Key Points: – Eli Lilly (LLY) is acquiring Organovo’s (ONVO) FXR program, including lead drug candidate FXR314, for further development. – Organovo will receive an upfront payment along with milestone-based regulatory and commercial payouts. – ONVO stock surged over 200% following the announcement.

In a significant move for the biotechnology sector, Organovo Holdings, Inc. (Nasdaq: ONVO) announced the sale of its FXR program, including its lead candidate FXR314, to pharmaceutical giant Eli Lilly and Company (NYSE: LLY). The acquisition, disclosed on Tuesday, marks a pivotal moment for Organovo as it aligns its proprietary 3D human tissue technology with a global leader in drug development.

The FXR program, focused on inflammatory bowel disease (IBD), is a major step toward advancing novel treatment approaches. Organovo’s Executive Chairman, Keith Murphy, expressed confidence in Lilly’s ability to further develop FXR314, highlighting the company’s world-class expertise and commitment to patient care.

Under the agreement, Organovo will receive an upfront cash payment, with additional milestone payments contingent on regulatory approvals and commercial success. While the specific financial terms remain undisclosed, the market’s response has been overwhelmingly positive.

Following the announcement, ONVO shares skyrocketed by over 200%, reflecting investor optimism about the deal’s potential impact. Lilly’s stock also saw a modest gain of 2.32% as the acquisition strengthens its pipeline in the IBD treatment space.

For Organovo, this transaction reinforces its ability to leverage its cutting-edge 3D tissue technology for drug development partnerships. The company, known for pioneering bioprinting innovations, has been positioning itself as a key player in personalized medicine and regenerative therapies.

For Eli Lilly, the acquisition aligns with its broader strategy of expanding its immunology portfolio. FXR314’s development complements Lilly’s existing research efforts in inflammatory diseases, further cementing its position as a leader in next-generation therapeutics.

With FXR314 now under Lilly’s stewardship, the biotech industry will closely monitor its progression into Phase 2 trials. If successful, the drug could represent a breakthrough in IBD treatment, addressing a significant unmet medical need.

As Organovo pivots towards future innovation, and Lilly integrates this promising asset into its pipeline, investors and analysts alike will be watching closely to gauge the long-term benefits of this high-profile acquisition.

SKYX Advanced and Smart Plug & Play Technologies to be utilized in Cavco’s High-End Premium Manufactured Homes at the World Largest Builders’ Show IBS

Since its Inception Cavco Homes is Estimated to Have Sold Nearly 1 Million Homes and Close to 20,000 Homes Annually During the Past Years

As SKYX Continues to Increase its U.S. and Canada Market Penetration, its Technologies will be Used in Cavco’s High-End Homes including the New Leading Premium Homes Skye View and Bungalow Models, in Show Village during the International Builders’ Show in Las Vegas February 25-27, 2025

MIAMI, Feb. 24, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive advanced and smart home platform technology company for homes and buildings, with more than 97 issued and pending patents globally and over 60 lighting and home décor websites, announces it will collaborate with Cavco Industries, Inc., a U.S. leading prefabricated home manufacturer to utilize SKYX’s advanced and smart plug & play technologies in Cavco’s premium prefabricated homes during the International Builders’ Show (IBS). SKYX’s technologies will be used in Cavco’s high-end homes, including their new leading premium homes Skye View and Bungalow models, in Show Village during the International Builders’ Show place in Las Vegas from February 25-27, 2025.

SKYX’s advance and smart plug & play platform technologies makes homes and buildings become advanced, safe, and smart instantly while significantly saving time and cost as well as adding substantial value to developers and homeowners.

Cavco is a leading U.S. manufacturer of prefabricated homes. As a publicly traded company, it ranks among the largest producers of manufactured and modular homes in the nation, renowned for its high-quality, premium designs. Cavco specializes in designing and producing factory-built housing products, which are distributed through an extensive network of independent and company-owned retailers. Since its inception, it is estimated that Cavco has sold nearly one million homes, with recent annual sales approaching 20,000 units.

Tim Gage, National Vice President of Cavco’s Park Models, and Specialty Homes said, “We are excited to utilize SKYX’s game-changing safe plug and play technology in our Cavco Park Model prefabricated homes at the IBS Pro Builder Show Village. We welcome people to visit our premium homes including our Skye View and Bungalow models to see how we utilize SKYX’s technologies. I strongly believe that the SKYX technology can become the standard for new construction, as it provides, safety, time saving, and smart capabilities, while advancing and adding significant value to our homes.”

Rani Kohen, Founder/Inventor and Executive Chairman, of SKYX Platforms, said, “We are truly excited to collaborate with a U.S. leading premium prefabricated home manufacturer such as Cavco during the world’s largest building show, IBS. This is another step toward our goal of making homes and buildings become advanced, safe, and smart as the new standard. We look forward to continuing to demonstrate our advanced smart platform technology’s ability to make homes and buildings become smarter and safer instantly, while significantly advancing buildings and saving time and costs for developers.”

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 97 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Recent Studies Support Diversified Vaccine Strategies, Aligning with GeoVax’s MVA-Based GEO-CM04S1 for Enhanced Protection, Particularly for Immunocompromised Populations

ATLANTA, GA, February 24, 2025 – GeoVax Labs, Inc. (Nasdaq: GOVX), a clinical-stage biotechnology company specializing in immunotherapies and vaccines, today reaffirms the critical role that mRNA vaccines have played in combating the COVID-19 pandemic and highlights the growing recognition of the need for complementary vaccine platforms, particularly for immunocompromised patients and those requiring broader, more durable immunity.

The rapid development and deployment of mRNA vaccines were pivotal in mitigating the initial impact of the pandemic, offering a timely and effective response. However, the scientific literature continues to underscore the importance of a diversified vaccine strategy directed towards enhanced durability and expanded protection against variants for populations that may not mount a sufficiently strong immune response to a single vaccine platform. GeoVax’s Modified Vaccinia Ankara (MVA)-based vaccine candidates, such as GEO-CM04S1 (COVID-19), may complement other existing vaccine platforms by addressing specific challenges.

Building a More Resilient Vaccine Landscape

Recent scholarly analyses, including research from leading experts(1) and a strategic review by the Biomedical Advanced Research and Development Authority (BARDA)(2), stress the importance of broadening vaccine portfolios beyond mRNA. These publications highlight areas where alternative vaccine platforms, such as viral-vector and live-attenuated vaccines, may provide advantages in durability, cellular immunity, and accessibility.

GeoVax’s MVA-based vaccines may offer an alternative approach, by utilizing a well-established vaccine vector, particularly in high-risk populations. Unlike current mRNA COVID-19 vaccines, GEO-CM04S1 expresses both the Spike (S) and Nucleocapsid (N) antigens, to elicit a broader immune response. This enhanced immunogenicity may be especially valuable for immunocompromised individuals, including transplant recipients and cancer patients, who often exhibit suboptimal responses to mRNA vaccines.

GeoVax’s MVA-based COVID-19 vaccine can serve as an important addition to the global immunization strategy by offering:

Enhanced Immune Response: The inclusion of both Spike and Nucleocapsid antigens in GEO-CM04S1 is intended to elicit a more comprehensive immune response, potentially reducing the need for frequent boosters.

Durability and Broader Variant Protection: Studies suggest measures of T-cell responses induced by GEO-CM04S1 elicit protection against emerging variants, minimizing the need for frequent reformulation.

Better Suitability for Immunocompromised Populations: Clinical trials demonstrate that GEO-CM04S1 elicits robust T-cell responses in patients unable to generate adequate antibody responses to conventional (spike-only) COVID-19 vaccines. This is critical for individuals with immune systems compromised by disease (eg cancers, genetic defects) or immunosuppressive therapies.

Scalability and Global Accessibility: GeoVax is further addressing vaccine availability with plans to transition manufacturing to a Next-Generation MVA manufacturing platform, with the potential for improved production efficiency and reduced costs, facilitating global distribution.

A Proven Technology with a Strong Safety Record

MVA was originally developed as a safer smallpox vaccine. MVA-based vaccines have been safely administered for decades. MVA’s extensive track record aligns with the U.S. Department of Health and Human Services’ (HHS) emphasis on vaccine safety, durability, and transparency. The well-documented safety and efficacy of MVA-based vaccines positions them as an important complement to existing mRNA-based approaches.

Government and Industry Support for Diversified Vaccine Strategies

Under BARDA’s $5 billion Project NextGen initiative, GeoVax was awarded a contract to conduct a 10,000-participant Phase 2b clinical trial evaluating an Omicron-updated version of GEO-CM04S1 in a comparison format against an approved mRNA COVID-19 vaccine. This study aims to validate the value of multi-antigen MVA-based COVID-19 vaccines in long-term pandemic preparedness and protection against future health threats.

Positioning for the Future of Vaccine Innovation

“The success of mRNA vaccines in responding to COVID-19 has been remarkable, but the evolving nature of infectious diseases calls for a diversified, complementary approach to immunization,” said David Dodd, Chairman & CEO of GeoVax. “Our MVA-based vaccines offer enhanced protection for those who need it most, including immunocompromised patients and populations requiring longer-lasting immunity. We are committed to advancing vaccine innovation in collaboration with public and private stakeholders.”

As the industry moves towards a more integrated and diversified vaccine ecosystem, GeoVax’s MVA-based vaccines should provide a scalable, durable, and globally accessible solution that enhances the existing landscape, ensuring broader protection for all populations.

References:

Plotkin, S. A., Robinson, J. M., Fitchett, J. R. A., & Gershburg, E. (2024). Vaccine development should be polytheistic, not monotheistic. Clinical Infectious Diseases, 79(6), 1518–1520. https://doi.org/10.1093/cid/ciae460

Parish, L. A., Rele, S., Hofmeyer, K. A., Luck, B. B., & Wolfe, D. N. (2025). Strategic and technical considerations in manufacturing viral vector vaccines for the Biomedical Advanced Research and Development Authority threats. Vaccines, 13(73). https://doi.org/10.3390/vaccines13010073

About GeoVax

GeoVax Labs, Inc. is a clinical-stage biotechnology company developing novel vaccines for many of the world’s most threatening infectious diseases and therapies for solid tumor cancers. The company’s lead clinical program is GEO-CM04S1, a next-generation COVID-19 vaccine for which GeoVax was recently awarded a BARDA-funded contract to sponsor a 10,000-participant Phase 2b clinical trial to evaluate the efficacy of GEO-CM04S1 versus an approved COVID-19 vaccine. In addition, GEO-CM04S1 is currently in three Phase 2 clinical trials, being evaluated as (1) a primary vaccine for immunocompromised patients such as those suffering from hematologic cancers and other patient populations for whom the current authorized COVID-19 vaccines are insufficient, (2) a booster vaccine in patients with chronic lymphocytic leukemia (CLL) and (3) a more robust, durable COVID-19 booster among healthy patients who previously received the mRNA vaccines. In oncology the lead clinical program is evaluating a novel oncolytic solid tumor gene-directed therapy, Gedeptin®, having recently completed a multicenter Phase 1/2 clinical trial for advanced head and neck cancers. A Phase 2 clinical trial in first recurrent head and neck cancer, evaluating Gedeptin® combined with an immune checkpoint inhibitor is planned. GeoVax has a strong IP portfolio in support of its technologies and product candidates, holding worldwide rights for its technologies and products. The Company has a leadership team who have driven significant value creation across multiple life science companies over the past several decades. For more information about the current status of our clinical trials and other updates, visit our website: www.geovax.com.

Forward-Looking Statements

This release contains forward-looking statements regarding GeoVax’s business plans. The words “believe,” “look forward to,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Actual results may differ materially from those included in these statements due to a variety of factors, including whether: GeoVax is able to obtain acceptable results from ongoing or future clinical trials of its investigational products, GeoVax’s immuno-oncology products and preventative vaccines can provoke the desired responses, and those products or vaccines can be used effectively, GeoVax’s viral vector technology adequately amplifies immune responses to cancer antigens, GeoVax can develop and manufacture its immuno-oncology products and preventative vaccines with the desired characteristics in a timely manner, GeoVax’s immuno-oncology products and preventative vaccines will be safe for human use, GeoVax’s vaccines will effectively prevent targeted infections in humans, GeoVax’s immuno-oncology products and preventative vaccines will receive regulatory approvals necessary to be licensed and marketed, GeoVax raises required capital to complete development, there is development of competitive products that may be more effective or easier to use than GeoVax’s products, GeoVax will be able to enter into favorable manufacturing and distribution agreements, and other factors, over which GeoVax has no control.

Further information on our risk factors is contained in our periodic reports on Form 10-Q and Form 10-K that we have filed and will file with the SEC. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

ATHENS, Greece, Feb. 24, 2025 (GLOBE NEWSWIRE) — EuroDry Ltd. (NASDAQ: EDRY, the “Company” or “EuroDry”), an owner and operator of drybulk vessels and provider of seaborne transportation for drybulk cargoes, announced today its results for the three and twelve-month periods ended December 31, 2024.

Fourth Quarter 2024 Highlights:

Total net revenues of $14.5 million.

Net loss attributable to controlling shareholders, of $3.3 million or $1.20 loss per share basic and diluted.

Adjusted net loss1 attributable to controlling shareholders, for the quarter of $0.7 million, or, $0.25 per share basic and diluted which excludes among other items an impairment charge of $2.8 million on one of our vessels.

Adjusted EBITDA1 was $4.8 million.

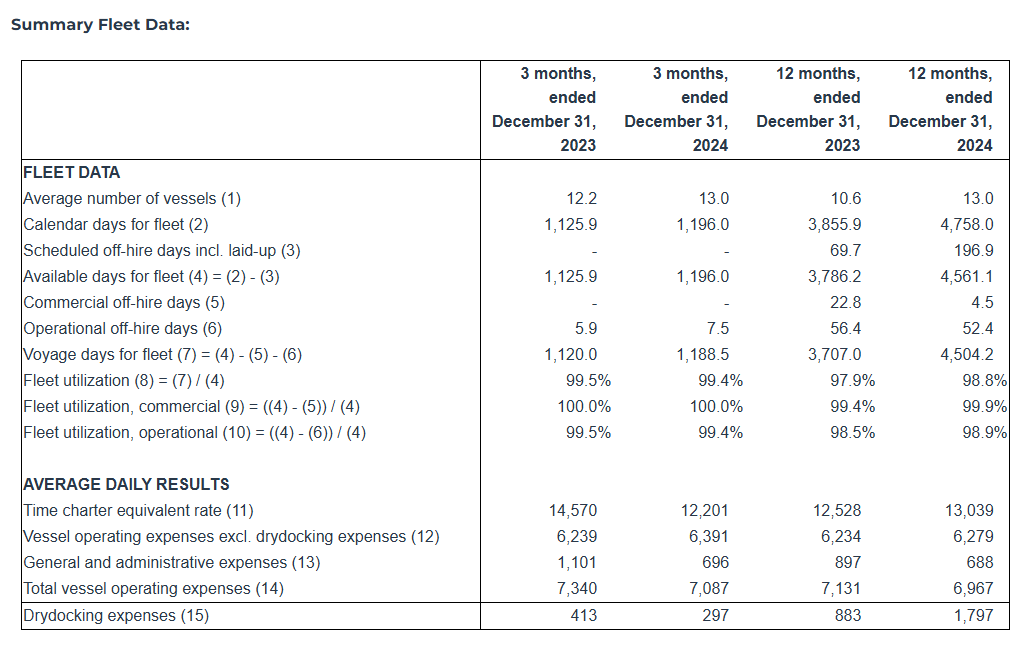

An average of 13.0 vessels were owned and operated during the fourth quarter of 2024 earning an average time charter equivalent rate of $12,201 per day.

To date, about $5.3 million has been used to repurchase 334,674 shares of the Company, under our share repurchase plan of up to $10 million, announced in August 2022.

Recent developments:

In November 2024, the Company signed two contracts with Nantong Xiangyu Shipbuilding for the construction of two 63,500 DWT ultramax bulk carriers. Both vessels are geared, eco, and are built to EEDI phase 3 design standard. The two newbuildings are scheduled to be delivered during the second and third quarters of 2027. The total consideration for the two newbuilding contracts is approximately $71.8 million and will be financed with a combination of debt and equity.

The Company on January 29, 2025, signed an agreement to sell M/V Tasos, a 75,100 dwt drybulk vessel, built in 2000, for demolition, for approximately $5 million. The vessel is expected to be delivered to its buyers, an unaffiliated third party, until early-March 2025, upon completion of her present charter. As a result of the vessel sale, we expect to record a gain of approximately $2.1million.

Full Year 2024 Highlights:

Total net revenues of $61.1 million.

Net loss attributable to controlling shareholders, of $9.7 million, or $3.54 loss per share basic and diluted.

Adjusted net loss1 attributable to controlling shareholders, for the period was $8.2 million or $3.02 adjusted loss per share basic and diluted.

Adjusted EBITDA1 was $12.4 million.

An average of 13.0 vessels were owned and operated during the twelve months of 2024 earning an average time charter equivalent rate of $13,039 per day.

Aristides Pittas, Chairman and CEO of EuroDry commented: “During the last couple of months of 2024 and during January and February of 2025, the drybulk market dropped to rates not seen since the early days of the COVID pandemic and touched decade-long lows last seen in 2016. It appears that a combination of low trade volumes due to low demand from China combined with a record low percentage of the fleet tied up in ports more than counterbalanced the low fleet growth during the period. There is some expectation, though, that the various stimuli packages released by the Chinese government during the fourth quarter of 2024 would start showing results in the near future; such stimuli combined with the typical seasonal recovery of the drybulk markets during the second quarter could lead to a noticeable recovery of the charter rates as already indicated by the forward (“FFA”) market.

“The low market of the fourth quarter was reflected in our results for the period although our vessels achieved better charters than market averages indicate. And while the low market of January and February 2025 will affect our first quarter results, we expect a recovery of the market in March and during the second quarter of 2025 to return us to profitability as our fleet is positioned to take full advantage of it having passed most drydockings in 2024. At the same time, as prices for vessels have also weakened, we are diligent in searching for potential investment opportunities; and to help finance such opportunities should they arise, we have committed to sell our eldest vessel M/V Tasos, as we recently announced.”

Tasos Aslidis, Chief Financial Officer of EuroDry commented: “In the fourth quarter of 2024 the Company operated an average of 13.0 vessels, versus 12.2 vessels during the same period last year. Our net revenues decreased to $14.5 million in the fourth quarter of 2024 compared to $15.9 million during the same period of last year. Our vessels earned in the fourth quarter of 2024 approximately 16.3% lower time charter equivalent rates compared to the corresponding period of 2023. At the same time, total daily vessel operating expenses, including management fees, general and administrative expenses but excluding drydocking costs, during the fourth quarter of 2024, averaged $7,087 per vessel per day, as compared to $7,340 for the same period of last year and $6,967 per vessel per day for the year 2024 as compared to $7,131 per vessel per day for the same period of 2023. The decreased total vessel operating expenses in the recent periods are attributable to the significantly lower daily general and administrative expenses. General and administrative expenses for the same period of 2023 included additional costs incurred in relation to the formation of a partnership with a number of investors represented by NRP Project Finance AS (“NRP Investors”) regarding the ownership of the entities owning M/V Christos K and M/V Maria (the “Partnership”).

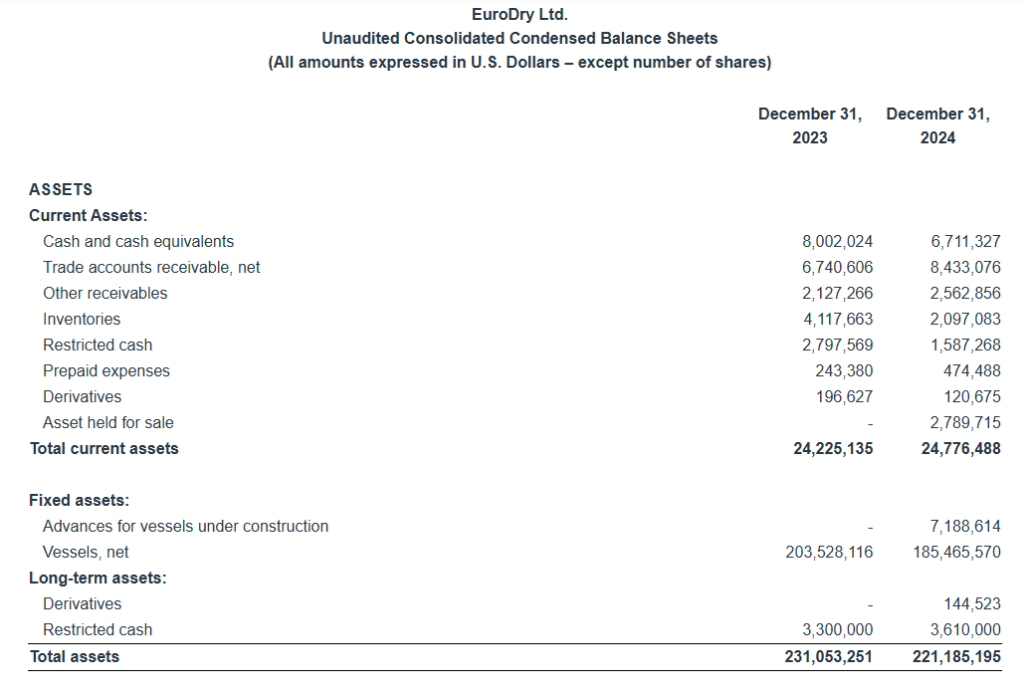

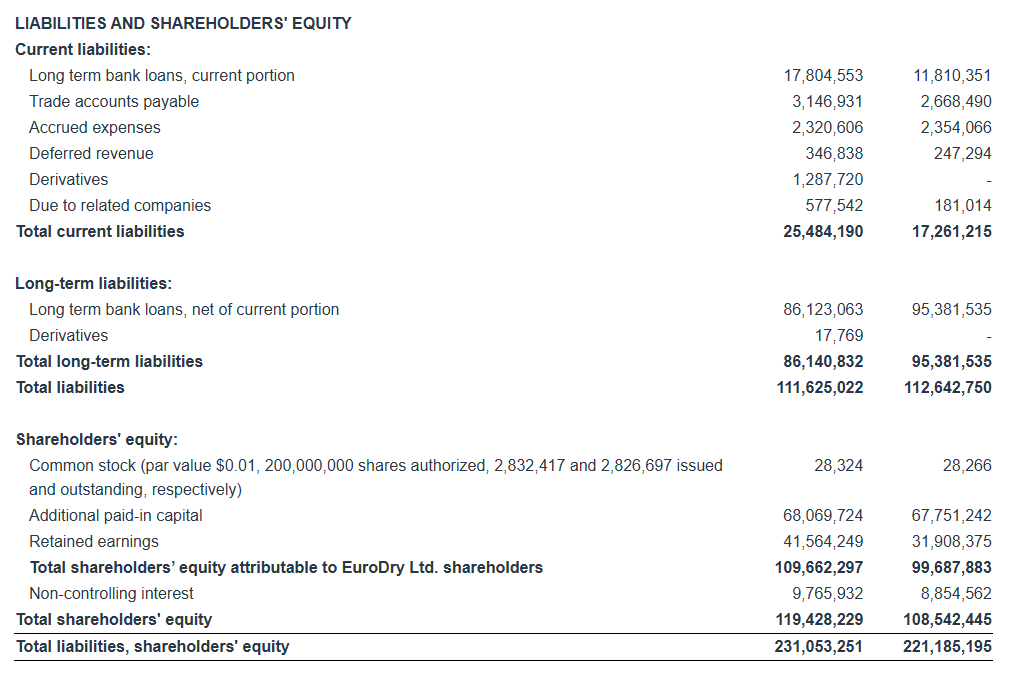

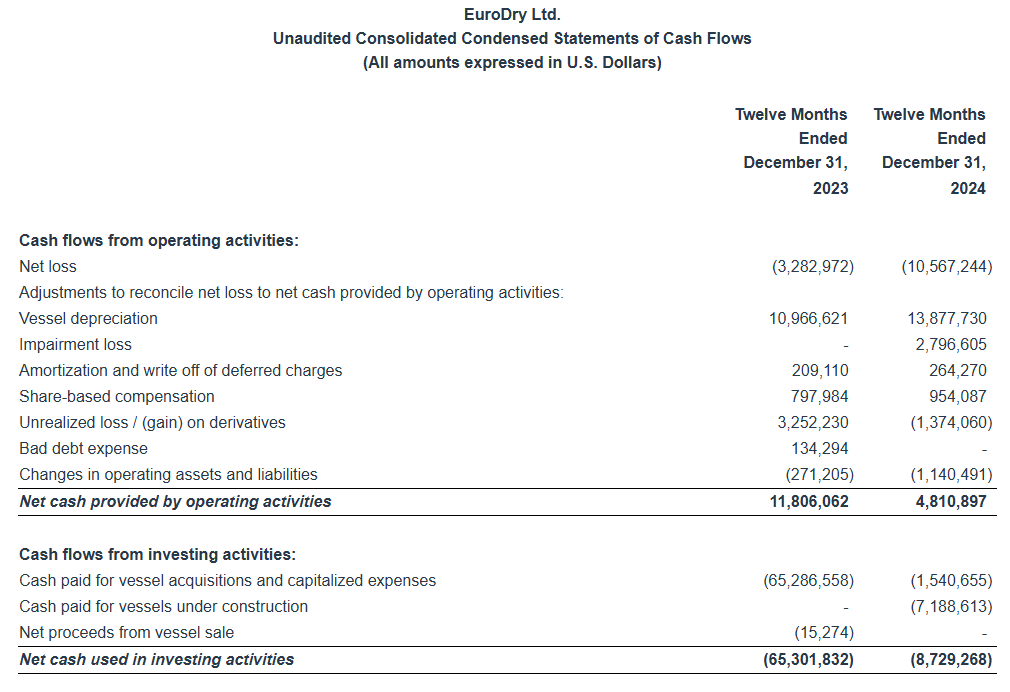

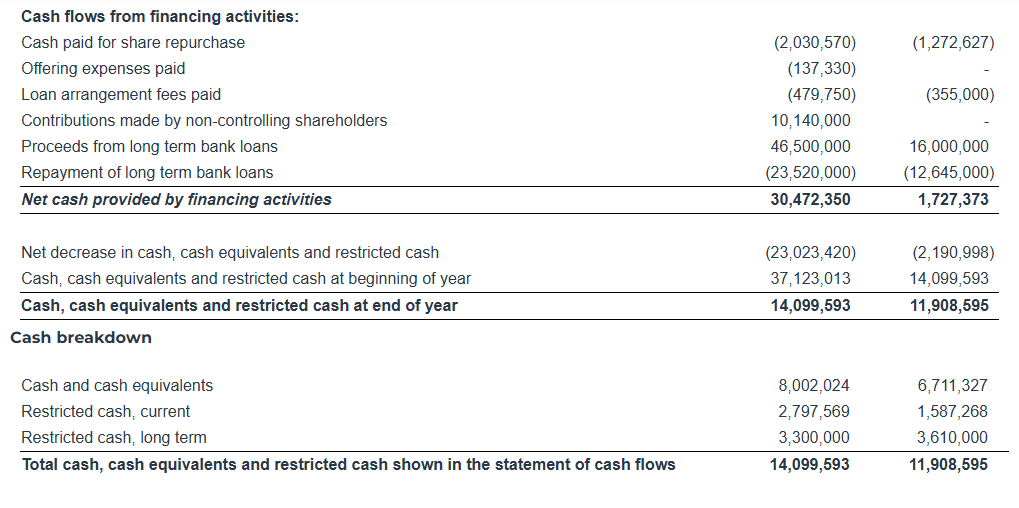

“Adjusted EBITDA during the fourth quarter of 2024 was $4.8 million versus $6.6 million in the fourth quarter of last year, and $12.4 million versus $14.6 million for the respective twelve-month periods of 2024 and 2023, respectively. As of December 31, 2024, our outstanding debt (excluding the unamortized loan fees) was $108.2 million versus unrestricted and restricted cash of $11.9 million. As of the same date, our scheduled debt repayments over the next 12 months amounted to about $12.1 million (excluding the unamortized loan fees).”

Fourth Quarter 2024 Results: For the fourth quarter of 2024, the Company reported total net revenues of $14.5 million representing a 8.8% decrease over total net revenues of $15.9 million during the fourth quarter of 2023. This was the result of the lower time charter rates our vessels earned in the fourth quarter of 2024, partly offset by the higher average number of vessels operated compared to the same period of 2023. On average, 13.0 vessels were owned and operated during the fourth quarter of 2024 earning an average time charter equivalent rate of $12,201 per day compared to 12.2 vessels in the same period of 2023 earning on average $14,570 per day.

For the fourth quarter of 2024, voyage expenses, net amounted to $0.9 million and mainly relate to vessels repositioning between charters and expenses during operational off-hire time. For the same period of 2023 voyage expenses net amounted to $0.6 million.

Vessel operating expenses were $6.6 million for the fourth quarter of 2024 as compared to $6.1 million for the same period of 2023. The increase is mainly attributable to the increased number of vessels operating in the fourth quarter of 2024 compared to the corresponding period in 2023.

Depreciation expense for the fourth quarter of 2024 amounted to $3.5 million, as compared to $3.2 million for the same period of 2023. This increase is again due to the higher number of vessels operating in the fourth quarter of 2024 as compared to the same period of 2023.

General and administrative expenses for the fourth quarter of 2024 were $0.8 million compared to $1.2 million of the fourth quarter of 2023. The decrease is mainly attributable to an additional cost of $0.44 million that was incurred during the last quarter of 2023 in relation to the formation of the Partnership.

Related party management fees for the fourth quarter of 2024 increased to $1.1 million from $1.0 million for the same period of 2023 as a result of an adjustment for inflation in the daily vessel management fee, effective from January 1, 2024, increasing the daily vessel management fee from 775 Euros to 810 Euros, as well as the increased number of vessels operating in the fourth quarter of 2024 compared to the corresponding period in 2023, partly offset by the favorable movement of the euro/dollar exchange rate.

During the fourth quarter of 2024 and 2023, none of our vessels underwent drydocking. The total cost for the fourth quarter of 2024 and 2023 of $0.4 million and $0.5 million, respectively, relates to drydocking expenses incurred in relation to upcoming drydockings.

In the fourth quarter of 2024 the Company recorded an impairment charge of $2.8 million. The impairment was booked to reduce the carrying amount of a drybulk vessel (M/V “Santa Cruz”) to its estimated market value, since based on the Company’s impairment test results it was determined that its carrying amount was not recoverable. No such cost existed in the fourth quarter of 2023.

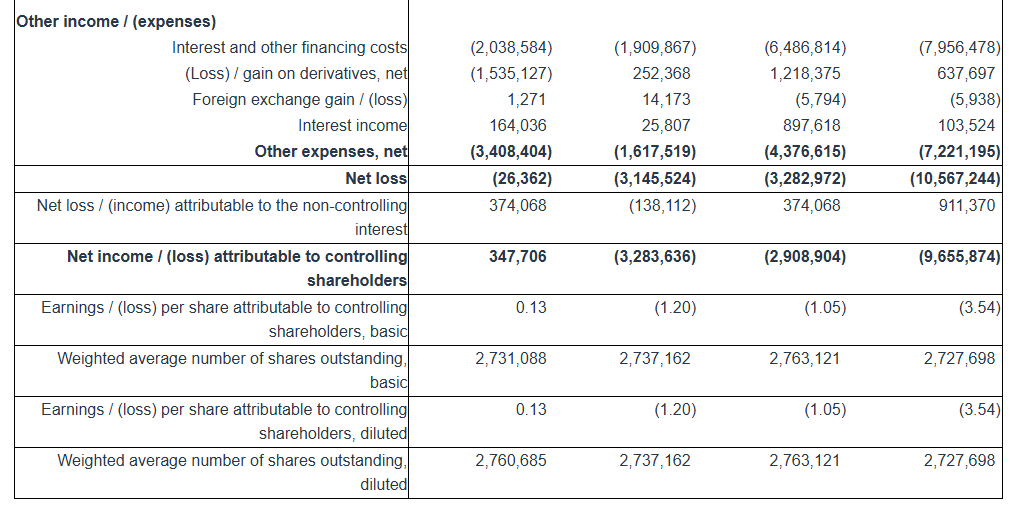

Interest and other financing costs for the fourth quarter of 2024 decreased to $1.9 million as compared to $2.0 million for the same period of 2023. Interest expense during the fourth quarter of 2024 was slightly lower mainly due to the slightly decreased benchmark rates of our loans, partly offset by the increased average debt during the period as compared to the same period of last year.

For the three months ended December 31, 2024, the Company recognized a gain on an interest rate swap of $0.25 million, as compared to a loss on an interest rate swap of $0.25 million and a loss on forward freight agreement (“FFA”) contracts of $1.3 million for the same period of 2023.

Interest income for the fourth quarter of 2024 amounted to $0.03 million compared to $0.16 million for the same period of 2023. The decrease in interest income is attributable to lower cash balances maintained during the fourth quarter of 2024 compared to the corresponding period in 2023.

The Company reported a net loss for the period of $3.1 million and a net loss attributable to controlling shareholders for the period of $3.3 million, as compared to a net loss of $0.03 million and a net income attributable to controlling shareholders of $0.3 million for the same period of 2023. The net income attributable to the non-controlling interest of $0.1 million in the fourth quarter of 2024 represents the income attributable to the 39% ownership of the Partnership.

Adjusted EBITDA for the fourth quarter of 2024 was $4.8 million compared to $6.6 million achieved during the fourth quarter of 2023.

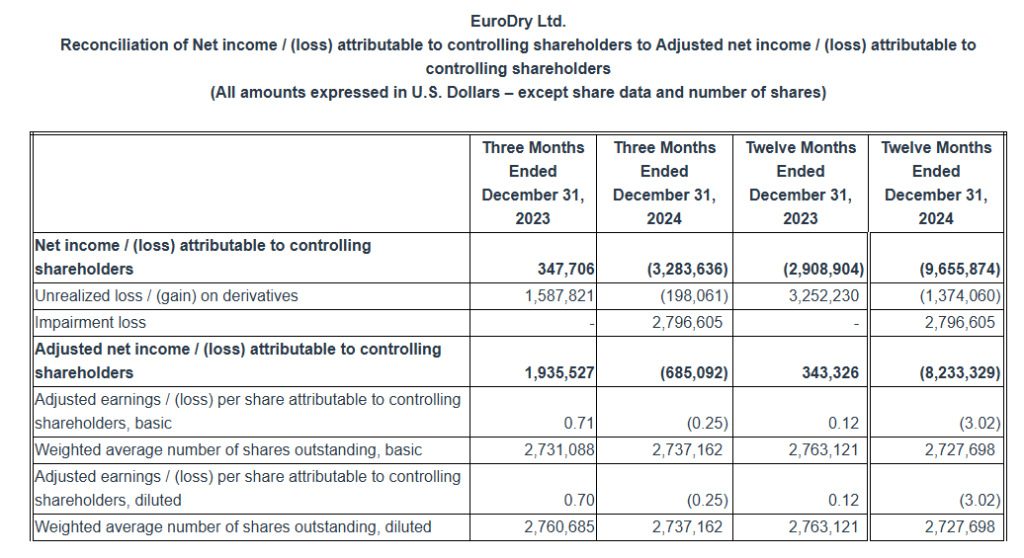

Basic and diluted loss per share attributable to controlling shareholders for the fourth quarter of 2024 was $1.20 calculated on 2,737,162 basic and diluted weighted average number of shares outstanding, compared to earnings per share of $0.13, calculated on 2,731,088 basic and 2,760,685 diluted weighted average number of shares outstanding for the fourth quarter of 2023.

Excluding the effect on the net loss attributable to controlling shareholders for the quarter of the unrealized loss / (gain) on derivatives and the impairment loss on a vessel, the adjusted loss per share attributable to controlling shareholders for the quarter ended December 31, 2024 would have been $0.25 basic and diluted, compared to adjusted earnings of $0.71 and $0.70 per share basic and diluted, respectively, for the quarter ended December 31, 2023. Usually, security analysts do not include the above items in their published estimates of earnings per share.

Full Year 2024 Results: For the full year of 2024, the Company reported total net revenues of $61.1 million representing a 28.3% increase over total net revenues of $47.6 million during the twelve months of 2023, as a result of the increased number of vessels operated during the year and the slightly higher time charter equivalent rates earned by our vessels in the twelve months of 2024 compared to the same period of 2023. On average, 13.0 vessels were owned and operated during the twelve months of 2024 earning an average time charter equivalent rate of $13,039 per day compared to 10.6 vessels in the same period of 2023 earning on average $12,528 per day.

For the twelve months of 2024, voyage expenses, net, were $6.1 million and mainly relate to vessels repositioning between charters and expenses during operational off-hire time. For the same period of 2023, voyage expenses, net, were $4.0 million and mainly relate to expenses incurred by one of our vessels while employed under a voyage charter, vessels repositioning between charters and expenses during the detention of one of our vessels in Corpus Christi.

Vessel operating expenses were $25.7 million for the twelve months of 2024 as compared to $20.8 million for the same period of 2023. The increase is mainly attributable to the increased number of vessels operating in 2024 compared to the corresponding period in 2023.

Depreciation expense for the year 2024 was $13.9 million compared to $11.0 million during the same period of 2023, again, mainly due to the higher number of vessels operating in the same period.

Related party management fees for the year of 2024 were increased to $4.2 million from $3.3 million for the same period of 2023 as a result of an adjustment for inflation in the daily vessel management fee, effective from January 1, 2024, increasing the daily vessel management fee from 775 Euros to 810 Euros and the increased number of vessels operated.

General and administrative expenses during the twelve months of 2024 were $3.3 million compared to $3.5 million during the same period in 2023. The decrease is attributable to an additional cost of $0.44 million that was incurred during the last quarter of 2023 in relation to the formation of the Partnership, partly offset by the increased cost of our stock incentive plan in 2024.

During the twelve months of 2023, we recorded a provision of $0.5 million for anticipated costs related to the detention of one of our vessels in Corpus Christi presented as other operating loss.

In 2023, we wrote-off certain trade receivables by recording a bad debt expense of $0.1 million. In 2024, we had no bad debt expense.

In the twelve months of 2024, seven of our vessels completed their special survey with drydocking for a total cost of $8.5 million. In the twelve months of 2023, three of our vessels completed their special or intermediate survey with drydocking and one vessel passed her intermediate survey in water (in lieu of drydock), for a total cost of $3.4 million.

Interest and other financing costs for the twelve months of 2024 amounted to $8.0 million compared to $6.5 million for the same period of 2023. Interest expense for the twelve months of 2024 was higher due to the increased average debt as compared to the same period of last year.

For the twelve months ended December 31, 2024, the Company recognized a $0.1 million unrealized gain and a $0.2 million realized gain on one interest rate swap, as well as a 1.3 million unrealized gain and a $1.0 million realized loss on FFA contracts as compared to a $1.9 million unrealized loss and a $1.9 million realized gain on interest rate swaps, as well as a 1.3 million unrealized loss and a $2.5 million realized gain on FFA contracts for the same period of 2023.

Interest income for 2024 amounted to $0.1 million compared to $0.9 million interest income for the same period of 2023. The decrease of interest income is attributable to lower cash balances maintained during the twelve months of 2024 compared to the corresponding period in 2023.

The Company reported a net loss for the period of $10.6 million and a net loss attributable to controlling shareholders of $9.7 million, as compared to a net loss of $3.3 million and a net loss attributable to controlling shareholders of $2.9 million, for the same period of 2023. The net loss attributable to the non-controlling interest of $0.9 million in 2024 represents the loss attributable to the 39% ownership of the Partnership.

Adjusted EBITDA for the twelve months of 2024 was $12.4 million compared to $14.6 million achieved during the twelve months of 2023.

Basic and diluted loss per share attributable to controlling shareholders for the twelve months of 2024 was $3.54, calculated on 2,727,698 basic and diluted weighted average number of shares outstanding, compared to basic and diluted loss per share attributable to controlling shareholders for the twelve months of 2023 of $1.05, calculated on 2,763,121 basic and diluted weighted average number of shares outstanding.

Excluding the effect on the net loss attributable to controlling shareholders for the year of the unrealized loss / (gain) on derivatives and the impairment loss on a vessel, the adjusted loss per share attributable to controlling shareholders for the year ended December 31, 2024 would have been $3.02 basic and diluted, compared to adjusted earnings per share of $0.12 basic and diluted for the same period of 2023. As previously mentioned, usually, security analysts do not include the above items in their published estimates of earnings per share.

(1) Average number of vessels is the number of vessels that constituted the Company’s fleet for the relevant period, as measured by the sum of the number of calendar days each vessel was a part of the Company’s fleet during the period divided by the number of calendar days in that period.

(2) Calendar days. We define calendar days as the total number of days in a period during which each vessel in our fleet was owned by us including off-hire days associated with major repairs, drydockings or special or intermediate surveys or days of vessels in lay-up. Calendar days are an indicator of the size of our fleet over a period and affect both the amount of revenues and the amount of expenses that we record during that period.

(3) The scheduled off-hire days including vessels laid-up are days associated with scheduled repairs, drydockings or special or intermediate surveys or days of vessels in lay-up.

(4) Available days. We define available days as the total number of Calendar days in a period net of scheduled off-hire days incl. laid up. We use available days to measure the number of days in a period during which vessels were available to generate revenues.

(5) Commercial off-hire days. We define commercial off-hire days as days a vessel is idle without employment.

(6) Operational off-hire days. We define operational off-hire days as days associated with unscheduled repairs or other off-hire time related to the operation of the vessels.

(7) Voyage days. We define voyage days as the total number of days in a period during which each vessel in our fleet was in our possession net of commercial and operational off-hire days. We use voyage days to measure the number of days in a period during which vessels actually generate revenues or are sailing for repositioning purposes.

(8) Fleet utilization. We calculate fleet utilization by dividing the number of our voyage days during a period by the number of our available days during that period. We use fleet utilization to measure a company’s efficiency in finding suitable employment for its vessels and minimizing the amount of days that its vessels are off-hire for reasons such as unscheduled repairs or days waiting to find employment.

(9) Fleet utilization, commercial. We calculate commercial fleet utilization by dividing our available days net of commercial off-hire days during a period by our available days during that period.

(10) Fleet utilization, operational. We calculate operational fleet utilization by dividing our available days net of operational off-hire days during a period by our available days during that period.

(11) Time charter equivalent rate, or TCE, is a measure of the average daily net revenue performance of our vessels. Our method of calculating TCE is determined by dividing time charter revenue and voyage charter revenue net of voyage expenses by voyage days for the relevant time period. Voyage expenses primarily consist of port, canal and fuel costs that are unique to a particular voyage, which would otherwise be paid by the charterer under a time charter contract, or are related to repositioning the vessel for the next charter. TCE provides additional meaningful information in conjunction with time charter revenue and voyage charter revenue, the most directly comparable GAAP measure, because it assists our management in making decisions regarding the deployment and use of our vessels and because we believe that it provides useful information to investors regarding our financial performance. TCE is a standard shipping industry performance measure used primarily to compare period-to-period changes in a shipping company’s performance despite changes in the mix of charter types (i.e., spot voyage charters, time charters, pool agreements and bareboat charters) under which the vessels may be employed between the periods. Our definition of TCE may not be comparable to that used by other companies in the shipping industry.

(12) We calculate daily vessel operating expenses, which include crew costs, provisions, deck and engine stores, lubricating oil, insurance, maintenance and repairs and related party management fees by dividing vessel operating expenses and related party management fees by fleet calendar days for the relevant time period. Drydocking expenses are reported separately.

(13) Daily general and administrative expenses are calculated by us by dividing general and administrative expenses by fleet calendar days for the relevant time period.

(14) Total vessel operating expenses, or TVOE, is a measure of our total expenses associated with operating our vessels. We compute TVOE as the sum of vessel operating expenses, related party management fees and general and administrative expenses; drydocking expenses are not included. Daily TVOE is calculated by dividing TVOE by fleet calendar days for the relevant time period.

(15) Daily drydocking expenses are calculated by us by dividing drydocking expenses by the fleet calendar days for the relevant period. Drydocking expenses include expenses during drydockings that would have been capitalized and amortized under the deferral method. Drydocking expenses could vary substantially from period to period depending on how many vessels underwent drydocking during the period. The Company expenses drydocking expenses as incurred.

Conference Call and Webcast: Today, February 24, 2025 at 9:00 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

Conference Call details: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “EuroDry” to the operator and/or conference ID 13751962. Click here for additional participant International Toll -Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

Audio webcast – Slides Presentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.eurodry.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the fourth quarter ended December 31, 2024, will also be available in PDF format 10 minutes prior to the conference call and webcast, accessible on the company’s website (www.eurodry.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

Adjusted EBITDA Reconciliation: EuroDry Ltd. considers Adjusted EBITDA to represent net loss before interest and other financing costs, income taxes, depreciation, unrealized loss / (gain) on Forward Freight Agreement derivatives (“FFAs”), loss / (gain) on interest rate swap derivatives and impairment loss. Adjusted EBITDA does not represent and should not be considered as an alternative to net loss, as determined by United States generally accepted accounting principles, or GAAP. Adjusted EBITDA is included herein because it is a basis upon which the Company assesses its financial performance because the Company believes that this non-GAAP financial measure assists our management and investors by increasing the comparability of our performance from period to period by excluding the potentially disparate effects between periods of, financial costs, unrealized loss / (gain) on FFAs, loss / (gain) on interest rate swap derivatives, depreciation and impairment loss. The Company’s definition of Adjusted EBITDA may not be the same as that used by other companies in the shipping or other industries.

Adjusted net income / (loss) attributable to controlling shareholders and Adjusted earnings / (loss) per share attributable to controlling shareholders Reconciliation:

EuroDry Ltd. considers Adjusted net income / (loss) attributable to controlling shareholders, to represent net income / (loss) before unrealized loss / (gain) on derivatives, which includes FFAs and interest rate swaps, and impairment loss. Adjusted net income / (loss) attributable to controlling shareholders and Adjusted earnings / (loss) per share attributable to common shareholders are included herein because we believe they assist our management and investors by increasing the comparability of the Company’s fundamental performance from period to period by excluding the potentially disparate effects between periods of the aforementioned items , which may significantly affect results of operations between periods. Adjusted net income / (loss) attributable to controlling shareholders and Adjusted earnings / (loss) per share attributable to common shareholders do not represent and should not be considered as an alternative to net income / (loss) attributable to controlling shareholders or earnings / (loss) per share attributable to common shareholders, as determined by GAAP. The Company’s definition of Adjusted net income / (loss) attributable to controlling shareholders and Adjusted earnings / (loss) per share attributable to common shareholders may not be the same as that used by other companies in the shipping or other industries. Adjusted net income / (loss) attributable to controlling shareholders and Adjusted earnings / (loss) per share attributable to common shareholders are not adjusted for all non-cash income and expense items that are reflected in our statement of cash flows.

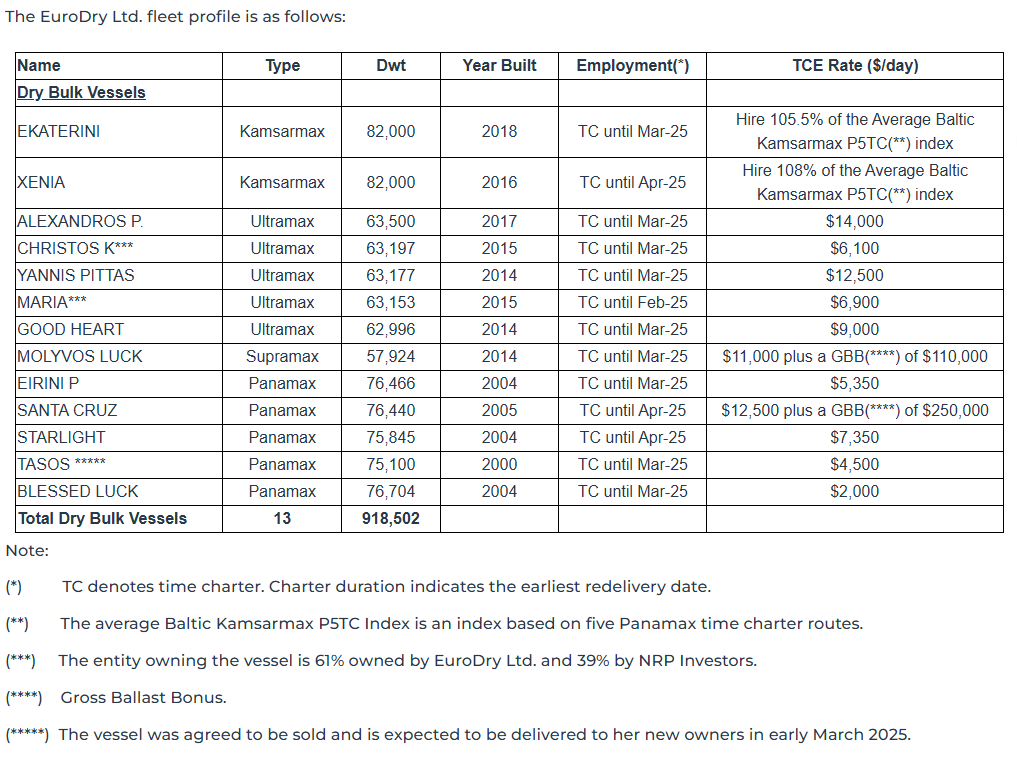

About EuroDry Ltd. EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd into a separate listed public company. EuroDry was spun-off from Euroseas Ltd on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY.

EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day-to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

The Company has a fleet of 13 vessels, including 5 Panamax drybulk carriers, 5 Ultramax drybulk carriers, 2 Kamsarmax drybulk carriers and 1 Supramax drybulk carrier. EuroDry’s 13 drybulk carriers have a total cargo capacity of 918,502 dwt. After the delivery of two Ultramax vessels in 2027 and the completion of the sale of one Panamax vessel, the Company’s fleet will consist of 14 vessels with a total carrying capacity of 970,402 dwt.