DLH delivers improved health and readiness solutions for federal programs through research, development, and innovative care processes. The Company’s experts in public health, performance evaluation, and health operations solve the complex problems faced by civilian and military customers alike, leveraging digital transformation, artificial intelligence, advanced analytics, cloud-based applications, telehealth systems, and more. With over 2,300 employees dedicated to the idea that “Your Mission is Our Passion,” DLH brings a unique combination of government sector experience, proven methodology, and unwavering commitment to public health to improve the lives of millions. For more information, visit www.DLHcorp.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

1Q Results. Revenue for the quarter was $90.8 million, below our estimate of $97 million and last year’s revenue of $97.9 million. Net income totaled $1.1 million, or diluted EPS of $0.08, compared to $2.2 million or $0.15 in the prior year. EBITDA was $9.9 million compared to $11.1 million last year and is in line with our estimate of $10 million.

Year-Over-Year Impact. Management indicated several factors impacted the year-over-year comparison of its TPS platform. For example, during the first quarter, one of the Company’s recompetes was awarded to a small business. This resulted from the prior administration’s Executive Order to unbundle contracts during the recompete cycle and reserve portions for small businesses. Additionally, acquired contracts that were won as a small business transitioned in the latter quarters of 2024, and other small, non-strategic projects were winding down or fully completed.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updated 2024 guidance. Inplay Oil modestly lowered its 2024 production guidance to 8,700 to 8,750 boe/d from 8,700 to 9,000. Additionally, the company lowered its expectations for crude oil prices and slightly raised expense guidance. Due to these changes, the adjusted funds flow (AFF) is expected to range from C$68 million to C$70 million compared to prior guidance of C$70 million to C$73 million. Capital expenditures for 2024 are expected to come in at around C$63 million compared to original expectations of C$64-67 million. The savings are mainly due to cost efficiencies from the Pembina Cardium Unit #7 (PCU7) drilling program.

Outlook for 2025. Management has planned a capital-efficient program in 2025. The company expects to increase production by 2%, in the range of 8,650 to 9,150 boe/d, compared to 2024, while spending around C$20 million less. The total capital budget for 2025 is C$41 million to C$44 million and will primarily be directed toward the Pembina Cardium Unit #7 property. Management expects adjusted funds flow (AFF) to benefit from lower capital expenditures and anticipates 2025 AFF to be between C$69 million and C$75 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A market leader with a strong growth profile. AZZ is the leading independent provider of hot dip galvanizing and coil coating solutions to a broad range of end markets. We expect AZZ Precoat Metals’ new manufacturing facility in Washington, Missouri to contribute to top-line growth in fiscal year 2026 while capital expenditures decline. Approximately 75% of the facility’s production is already committed and could generate roughly $50 million to $60 million in revenue on an annualized basis once production is fully ramped.

Fiscal 2026 corporate guidance. AZZ Inc. released financial guidance for fiscal year 2026 and expects sales in the range of $1.625 billion to $1.725 billion, adjusted EBITDA in the range of $360 million to $400 million, and adjusted diluted EPS of $5.50 to $6.10. Fiscal year 2026 guidance includes an increase in the Metal Coatings EBITDA margin expectations to a range of 27% to 32% from 25% to 30%, while Precoat Metals EBITDA margin expectations are unchanged at 17% to 22%.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – TPG Rise Climate will acquire Altus Power for $5.00 per share in a $2.2 billion deal, taking the company private to accelerate clean energy expansion. – Altus Power’s Board of Directors unanimously approved the transaction, which represents a 66% premium to its October 2024 stock price and is expected to close in Q2 2025. – This acquisition aligns with TPG Rise Climate’s strategy to scale climate solutions, leveraging its expertise in clean energy infrastructure to support Altus Power’s growth.

Altus Power, the largest owner of commercial-scale solar in the U.S., has announced that it has entered into a definitive agreement to be acquired by TPG through its TPG Rise Climate Transition Infrastructure strategy. Under the terms of the agreement, TPG will acquire Altus at $5.00 per share, valuing the company at approximately $2.2 billion, including outstanding debt. Upon completion of the transaction, Altus Power will become a privately held company.

Strategic Rationale and Market Impact

On October 15, 2024, Altus Power initiated a formal review of strategic alternatives. Today’s purchase price represents a 66% premium to Altus’ closing price on that date. The company expects this acquisition to bolster its ability to provide greater value to both commercial and Community Solar customers while expanding access to clean electric power.

“This transaction represents a pivotal moment for Altus Power,” said Gregg Felton, CEO of Altus Power. “We are incredibly excited to partner with TPG Rise Climate to continue to build our position as the leading commercial-scale provider of clean electric power to businesses and households from coast to coast. TPG Rise Climate’s deep expertise in the clean energy sector, investment-oriented mindset, and value-driven approach to infrastructure development align perfectly with our vision. This partnership strengthens our ability to serve both our Community Solar and commercial clients with clean electric power at a time when demand for power is expected to grow substantially. As a private company, Altus Power will be better positioned for continued long-term growth, which we believe will allow us to scale our operations, drive innovation, and enhance the value we deliver to our customers. Together with TPG Rise Climate, we believe we are poised to accelerate clean energy adoption and ensure more businesses and communities have access to the power they need for a sustainable future.”

Transaction Details

The Board of Directors of Altus has unanimously approved the transaction and recommends that Altus stockholders vote to adopt the merger agreement.

The deal is contingent upon majority approval by Class A stockholders.

The transaction is expected to close in Q2 2025.

About TPG Rise Climate

TPG Rise Climate is the dedicated climate investing platform of TPG, a leading global alternative asset management firm. With dedicated pools of capital across private equity, transition infrastructure, and the Global South, TPG Rise Climate focuses on climate-related investments that benefit from the expertise of TPG’s investment professionals and its global network of executives, advisors, and corporate partners. As part of TPG’s $25 billion global impact investing platform, TPG Rise Climate invests broadly in the climate sector, emphasizing clean electrons, clean molecules and materials, and negative emissions.

About Altus Power

Altus Power is a leader in commercial-scale solar energy, providing clean, renewable energy solutions for businesses and communities across the U.S. The company is currently traded on the New York Stock Exchange under the ticker symbol AMPS.

Key Points: – Above Food Ingredients Inc. (NASDAQ: ABVE) has signed a Letter of Intent to acquire Palm Global Technologies Ltd. in a $180 million share exchange, expanding into Agri-Tech, FinTech, and carbon credit securitization. – Palm Global’s proprietary AI, blockchain, and decentralized finance technologies will enhance Above Food’s vertically integrated food systems, supporting sustainable agriculture and economic empowerment for millions of farmers. – Following the acquisition, Palm Global’s Peter Knez will become Chairman and CEO of the combined companies, with definitive agreements expected to be finalized and closed in the near term.

Above Food Ingredients Inc. (NASDAQ: ABVE), a leader in sustainable, vertically integrated food systems, has signed a Letter of Intent (LOI) to acquire Palm Global Technologies Ltd., a next-generation innovator in technology, sustainability, and global food markets. The acquisition is expected to strengthen Above Food’s position in Agri-Tech, FinTech, and carbon credit securitization, further advancing its commitment to sustainable food production and innovation.

Strategic Rationale and Industry Impact

The transaction will integrate Above Food’s vertically integrated food systems with Palm Global’s groundbreaking technologies, alliances, and global reach. Palm Global’s proprietary AI, blockchain, and decentralized finance technologies are designed to drive economic empowerment, education, and sustainable growth, particularly in underserved markets, benefiting tens of millions of farmers worldwide.

“This transformative acquisition positions Above Food to redefine global agriculture and sustainability while unlocking a number of significant opportunities in high-growth markets,” said Lionel Kambeitz, Founder and CEO of Above Food. “Palm Global’s innovative technologies, combined with its mission to drive economic empowerment, align perfectly with our vision for sustainable food solutions worldwide.”

Palm Global’s Technological and Strategic Contributions

AI, Blockchain, and DeFi Technologies – Palm Global’s solutions enhance efficiency, security, and accessibility in the global food supply chain.

Partnerships with Governments and Institutions – Palm Global collaborates with entities like the Peace for Life Foundation, IIMSAM, and global institutions to accelerate technology adoption among farmers.

Strategic Global Alliances – The acquisition allows Above Food to leverage Palm Global’s extensive partnerships to develop, utilize, and maximize R&D capabilities in agronomy and genomics.

The newly combined entity will enable innovative initiatives such as regenerative agriculture and grow-to-order food solutions, creating customized approaches to meet evolving consumer and agricultural needs.

Transaction Details and Leadership Transition

The LOI outlines a share exchange valuing Palm Global at approximately $180 million.

Definitive agreements are expected this month, with approvals and closing anticipated soon after.

Peter Knez, currently on Palm Global’s Board of Directors, will assume the role of Chairman and CEO of the combined companies.

Future Outlook

This merger is set to enhance global food security, promote sustainable agriculture, and create economic opportunities in underserved markets through technological innovation and strategic partnerships. By combining resources, Above Food and Palm Global aim to drive the next wave of transformation in sustainable food production and agricultural technology.

Strategic Progress Across COVID-19, Mpox, Oncology Therapies and AI Integration Positions GeoVax for Strong Momentum

Atlanta, GA – February 5, 2025 – GeoVax Labs, Inc. (Nasdaq: GOVX), a clinical-stage biotechnology company developing immunotherapies and vaccines against cancers and infectious diseases, today outlined its 2025 strategic milestones and business outlook. Building on a history of delivering on key commitments, GeoVax enters 2025 with a robust pipeline, a catalyst-rich milestone schedule, and an unwavering commitment to addressing unmet medical needs on a global scale.

An Important Year Ahead for GEO-CM04S1, a Next-Generation COVID-19 Vaccine

GEO-CM04S1 continues to demonstrate potential for both immunocompromised patients and as a booster vaccine for those previously inoculated with mRNA vaccines. In 2025, the Company anticipates completion of the evaluation trial among Chronic Lymphocytic Leukemia (CLL) patients, a patient population recognized to currently have minimal COVID-19 vaccine options. Interim data reported in Q4 2024 suggest GEO-CM04S1 may offer superior immune responses to CLL patients compared to an mRNA vaccine.

GeoVax also expects to report final results from its healthy adults booster trial, offering valuable data on the vaccine’s safety and immunogenicity profile. Another pivotal milestone for GEO-CM04S1 in 2025 is the anticipated initiation of patient enrollment in the BARDA-funded Project NextGen Phase 2b trial, which will evaluate GEO-CM04S1 compared to an authorized mRNA vaccine within a 10,000-patient study. As both a booster and a primary vaccine for immune-compromised patient populations, GEO-CM04S1 remains central to GeoVax’s mission to address the ongoing and evolving challenges of COVID-19.

As part of its strategy, GeoVax will continue to explore and establish strategic partnerships and collaborations to accelerate the development, commercialization, and global accessibility of GEO-CM04S1.

GEO-MVA: Addressing Biosecurity and Global Health Gaps

GEO-MVA, a vaccine designed to combat Mpox and Smallpox, has emerged as a critical solution amid rising global biosecurity concerns. In 2025, the Company plans to initiate clinical evaluations for GEO-MVA while continuing discussions with various stakeholders regarding the opportunity to utilize GEO-MVA among underserved populations in regions including Africa. With ongoing geopolitical and logistical challenges limiting vaccine availability, GEO-MVA’s ability to offer multi-disease protection, minimal refrigeration needs, and scalability through implementation of an advanced MVA manufacturing process, GEO-MVA represents a potential transformative resource for both national biosecurity strategies and global health initiatives.

GeoVax recognizes that addressing these critical global challenges requires collaborative efforts. In 2025, the Company will actively pursue strategic partnerships with governments, NGOs, and private-sector stakeholders to maximize the impact and reach of its GEO-MVA platform.

Gedeptin: Unlocking Potential in Solid Tumor Cancer Therapy

GeoVax’s oncology program, centered around Gedeptin®, continues to progress in addressing unmet medical needs in solid tumor therapies. Following encouraging results from Phase 1 and Phase 1/2 trials, Gedeptin is advancing into a Phase 2 clinical trial in 2025, where it will be evaluated in combination with an immune checkpoint inhibitor, targeting first recurrent head and neck cancer. This trial aims to validate the potential synergy between Gedeptin’s targeted gene-directed enzyme prodrug therapy and the powerful immune responses activated by checkpoint inhibitors.

As an FDA-designated Orphan Drug for anatomically accessible oral and pharyngeal cancers, Gedeptin is strategically positioned to address not only head and neck cancers but also other solid tumor indications, such as triple-negative breast cancer, soft tissue sarcoma and melanoma. GeoVax’s clinical roadmap for Gedeptin represents a significant market opportunity, with the potential to reshape how these cancers are treated worldwide.

GeoVax remains open to collaborations with oncology leaders, academic research institutions, and industry partners to further enhance the clinical impact and commercial success of Gedeptin.

Next-Generation Manufacturing: Pioneering Scalable Vaccine Production

To amplify the value of its clinical programs, GeoVax is also focused on advancing MVA vaccine manufacturing through validation of continuous cell line manufacturing processes, ensuring consistent, high-quality vaccine production capabilities. These advancements address long-standing challenges in vaccine scalability and cost-effectiveness, positioning GeoVax as a leader in MVA-based vaccine manufacturing solutions, potentially implementing a proprietary MVA manufacturing process supporting more flexible, localized MVA manufacturing at lower production cost, specifically enabling vaccine self-sufficiency manufacturing in low-middle income regions such as Africa.

GeoVax recognizes that strong manufacturing partnerships are vital to bringing these innovations to market efficiently and cost-effectively. The Company plans to collaborate with manufacturing partners worldwide to scale up production capabilities and meet the growing global demand for MVA-based vaccines.

AI Integration: Optimizing Processes and Driving Innovation

In alignment with its 2025 objectives, GeoVax has expanded the integration of Artificial Intelligence (AI) across its vaccine development and cancer immunotherapy activities. Leveraging AI is anticipated to accelerate vaccine development, optimize cancer therapies, streamline clinical trials, and enhance manufacturing processes, potentially in the following manners:

Vaccine and Therapy Innovation: Predicting pathogen mutations and optimizing GEO-CM04S1 and Gedeptin® design, ensuring effectiveness in variant-proof vaccines and cancer therapies.

Clinical Trial Optimization: Refining patient selection, accelerating recruitment, and enhancing diversity for trials targeting high-risk and underserved populations.

Streamlined Manufacturing: Enhancing scalability and logistics, enabling efficient production and distribution, particularly in underserved regions.

Addressing a $55+ Billion Pipeline Market Opportunity

GeoVax’s pipeline addresses significant unmet and underserved medical needs worldwide in both infectious disease vaccines and oncology, representing a collective potential global market opportunity in excess of $55 billion. Each program—GEO-CM04S1, GEO-MVA, and Gedeptin—addresses significant gaps in existing treatment and prevention strategies, backed by emerging clinical data and a focus towards achieving the necessary regulatory milestones in support of product registration.

David Dodd, Chairman & CEO of GeoVax, commented: “2024 was a transformative year for GeoVax, and our focus and commitment in 2025 is unwavering, focused on critically needed unmet medical needs. Our pipeline, enriched with value-driven milestones, positions us well for successful growth and development. Collaborations and partnerships remain core to our strategy, ensuring our innovations reach those who need them most. With GEO-CM04S1, GEO-MVA, Gedeptin, our MVA manufacturing advancements, and leveraging AI to optimize our processes and drive innovation, we are prepared to make meaningful contributions to global health, delivering value to our fellow shareholders, various stakeholders and, providing compelling career development opportunities to our staff colleagues.”

For further details on GeoVax’s pipeline and strategic initiatives, please visit www.geovax.com.

About GeoVax

GeoVax Labs, Inc. is a clinical-stage biotechnology company developing novel vaccines for many of the world’s most threatening infectious diseases and therapies for solid tumor cancers. The company’s lead clinical program is GEO-CM04S1, a next-generation COVID-19 vaccine for which GeoVax was recently awarded a BARDA-funded contract to sponsor a 10,000-participant Phase 2b clinical trial to evaluate the efficacy of GEO-CM04S1 versus an approved COVID-19 vaccine. In addition, GEO-CM04S1 is currently in three Phase 2 clinical trials, being evaluated as (1) a primary vaccine for immunocompromised patients such as those suffering from hematologic cancers and other patient populations for whom the current authorized COVID-19 vaccines are insufficient, (2) a booster vaccine in patients with chronic lymphocytic leukemia (CLL) and (3) a more robust, durable COVID-19 booster among healthy patients who previously received the mRNA vaccines. In oncology the lead clinical program is evaluating a novel oncolytic solid tumor gene-directed therapy, Gedeptin®, having recently completed a multicenter Phase 1/2 clinical trial for advanced head and neck cancers. A Phase 2 clinical trial in first recurrent head and neck cancer, evaluating Gedeptin® combined with an immune checkpoint inhibitor is planned to initiate during the first half of 2025. GeoVax has a strong IP portfolio in support of its technologies and product candidates, holding worldwide rights for its technologies and products. The Company has a leadership team who have driven significant value creation across multiple life science companies over the past several decades. For more information about the current status of our clinical trials and other updates, visit our website: www.geovax.com.

Forward-Looking Statements

This release contains forward-looking statements regarding GeoVax’s business plans. The words “believe,” “look forward to,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Actual results may differ materially from those included in these statements due to a variety of factors, including whether: GeoVax is able to obtain acceptable results from ongoing or future clinical trials of its investigational products, GeoVax’s immuno-oncology products and preventative vaccines can provoke the desired responses, and those products or vaccines can be used effectively, GeoVax’s viral vector technology adequately amplifies immune responses to cancer antigens, GeoVax can develop and manufacture its immuno-oncology products and preventative vaccines with the desired characteristics in a timely manner, GeoVax’s immuno-oncology products and preventative vaccines will be safe for human use, GeoVax’s vaccines will effectively prevent targeted infections in humans, GeoVax’s immuno-oncology products and preventative vaccines will receive regulatory approvals necessary to be licensed and marketed, GeoVax raises required capital to complete development, there is development of competitive products that may be more effective or easier to use than GeoVax’s products, GeoVax will be able to enter into favorable manufacturing and distribution agreements, and other factors, over which GeoVax has no control.

Further information on our risk factors is contained in our periodic reports on Form 10-Q and Form 10-K that we have filed and will file with the SEC. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

FDA-cleared amended trial design; First site initiation expected Q1 2025

PRINCETON, N.J., Feb. 05, 2025 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB) (“PDS Biotech” or the “Company”), a late-stage immunotherapy company focused on transforming how the immune system targets and kills cancers, today reaffirmed the Company’s guidance of initiating its VERSATILE-003 Phase 3 clinical trial of Versamune® HPV plus pembrolizumab for first-line treatment of recurrent and/or metastatic (R/M) HPV16-positive head and neck squamous cell cancer (HNSCC) in the first quarter of this year.

PDS Biotech submitted its updated clinical protocol on November 15, 2024, amending the Investigational New Drug (IND) application. The window for comments from the U.S. Food and Drug Administration (FDA) has passed, and the Company is on track to initiate site activation in the first quarter of 2025. The Company has received Fast Track designation from the FDA for the combination of Versamune® HPV and pembrolizumab in R/M HNSCC. (See VERSATILE-002 Phase 2 clinical results here.)

“The integral elements for trial initiation are ready, including alignment with the FDA,” said Frank Bedu-Addo, PhD, President and Chief Executive Officer of PDS Biotech. “We look forward to initiating VERSATILE-003 this quarter and advancing the combination of Versamune® HPV plus pembrolizumab to potentially provide improved outcomes for patients with HPV16-positive R/M HNSCC.”

HPV16-positive patients represent a large, fast-growing subgroup in need of targeted therapies to treat the underlying cause of the cancer. A recently validated companion diagnostic to confirm HPV16-positive HNSCC will be utilized during the patient screening process of the VERSATILE-003 trial.

“HPV16-positive HNSCC is poised to become the dominant type of HNSCC in the US and EU,” said Kirk Shepard, M.D., PDS Biotech’s Chief Medical Officer. “Confirming HPV16 status with a potentially commercializable test is essential to effectively identifying the patients suitable to receive Versamune HPV. This will be the first investigational use of this type of companion diagnostic in a Phase 3 clinical trial in HNSCC.”

For more information on VERSATILE-003, visit ClinicalTrials.gov (Identifier: NCT06790966).

About PDS Biotechnology PDS Biotechnology is a late-stage immunotherapy company focused on transforming how the immune system targets and kills cancers. The Company plans to initiate a pivotal clinical trial to advance its lead program in advanced HPV16-positive head and neck squamous cell cancers. PDS Biotech’s lead investigational T-cell stimulating immunotherapy Versamune® HPV is being developed in combination with a standard-of-care immune checkpoint inhibitor, and also in a triple combination including PDS01ADC, an IL-12 fused antibody drug conjugate (ADC), and a standard-of-care immune checkpoint inhibitor.

Forward Looking Statements This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for Versamune® HPV, PDS01ADC and other Versamune® based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning Versamune® HPV, PDS01ADC and other Versamune® based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to the Company’s currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; the Company’s ability to continue as a going concern; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the other risks, uncertainties, and other factors described under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in the documents we file with the U.S. Securities and Exchange Commission. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

Versamune® is a registered trademark of PDS Biotechnology Corporation.

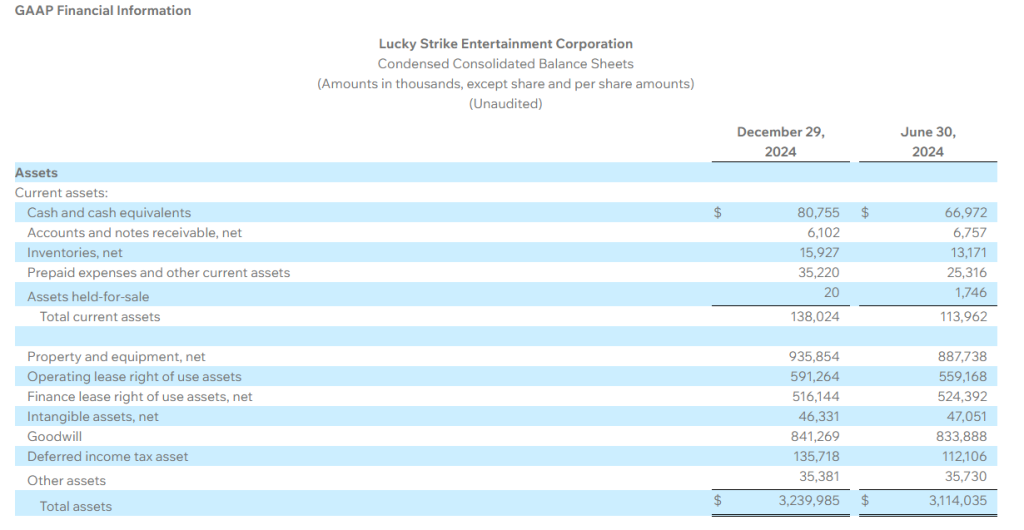

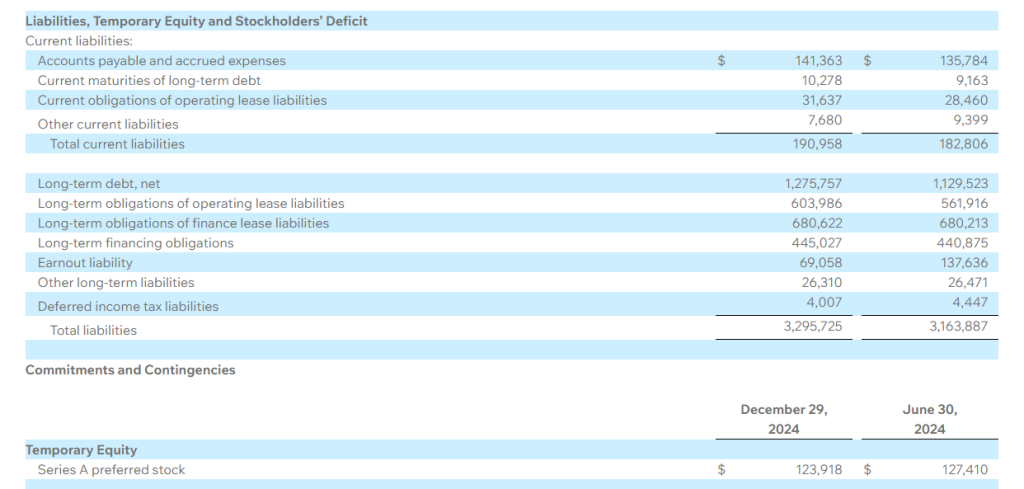

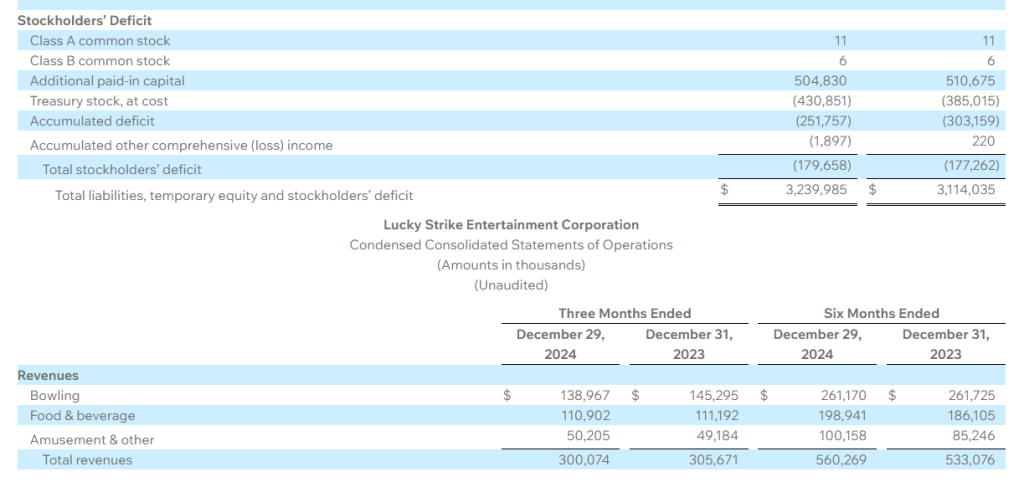

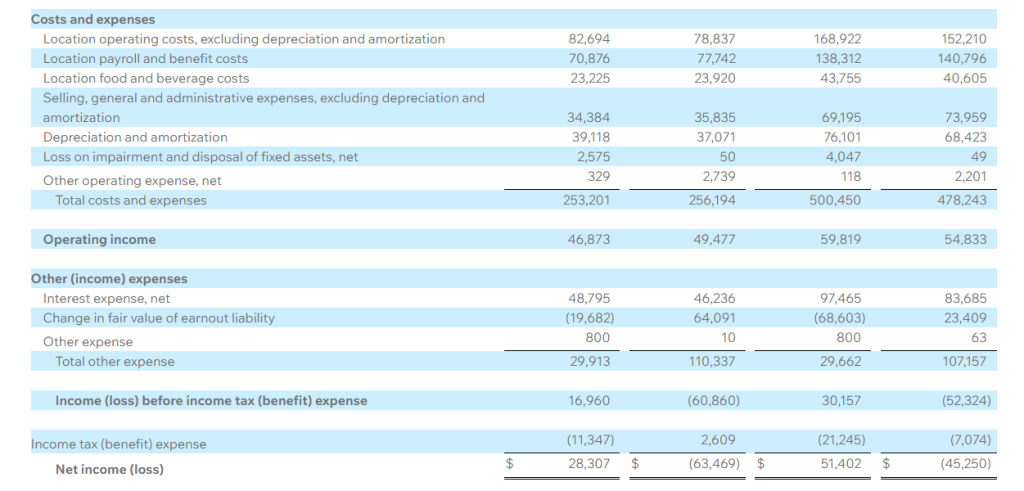

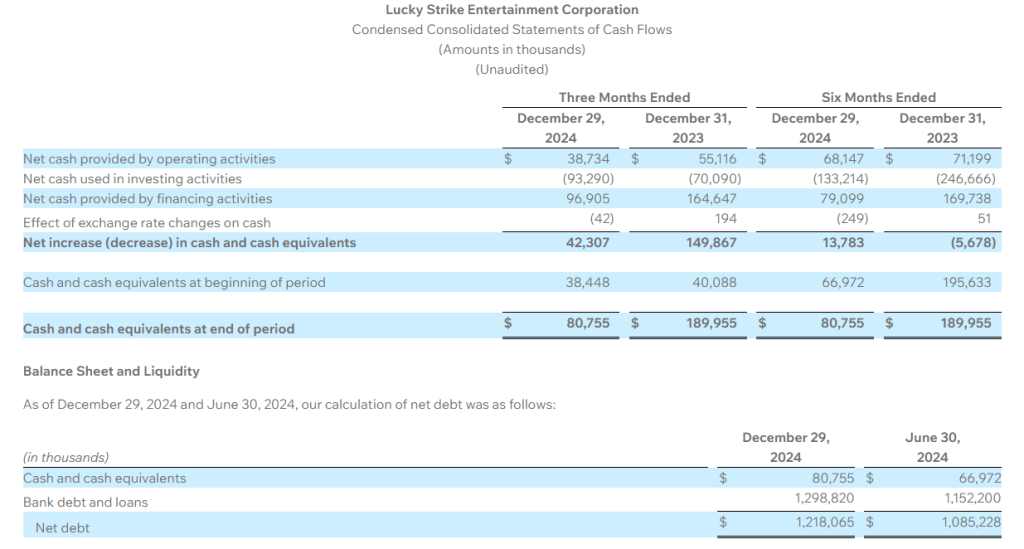

RICHMOND, Va.–(BUSINESS WIRE)– Lucky Strike Entertainment (NYSE: LUCK), one of the world’s premier operators of location-based entertainment, today provided financial results for the second quarter of the 2025 Fiscal Year, which ended on December 29, 2024.

Quarter Highlights:

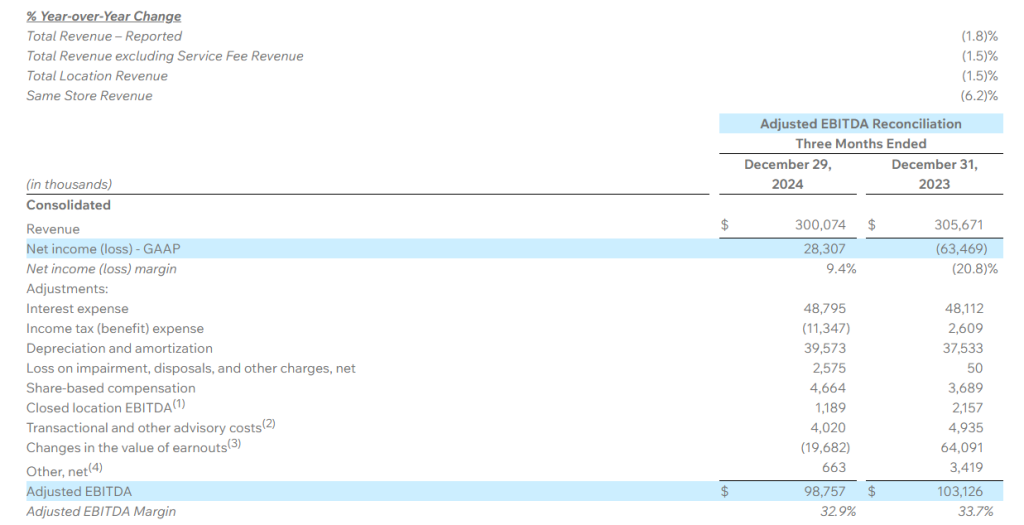

Revenue decreased 1.8% to $300.1 million from $305.7 million in the previous year

Same Store Revenue decreased 6.2% versus the prior year

Net income of $28.3 million versus prior year loss of $63.5 million

Adjusted EBITDA of $98.8 million versus $103.1 million in the prior year

From September 30, 2024 through February 5, 2025, opened four new builds and acquired one bowling location, six family entertainment centers and one water park. Total locations in operation as of February 5, 2025 is 364

“This most recent quarter came with heightened macroeconomic uncertainty. We began the quarter with the corporate events business on hold due to concerns over the election outcome. Compounding this was Thanksgiving falling later in the year, shortening the corporate holiday events window by about a third. And finally, New Year’s Eve fell into our next quarter vs being in the second quarter last year. Our sticky leagues business continued to grow, and retail walk-in customer traffic has been steady despite headlines of the weak consumer,” said Founder, Chairman, and CEO Thomas Shannon. “During this quarter, we opened four new Lucky Strike centers—two in Denver, one in the heart of Beverly Hills, and one in Ladera Ranch, California. Lucky Strike Beverly Hills and Lucky Strike Ladera Ranch each generated over $1 million in revenue within their first 30 days of operation. They represent an evolution of our best-in-class product that underscores our position as leaders in consumer entertainment. We also began the rebranding of centers to Lucky Strike, with four centers converted to date and the rollout ramping up.”

“In the quarter, we acquired Boomer’s which added six family entertainment centers and one stunning water park to our portfolio. Those assets operate at losses during the winter periods and generate significant cash flow during the summer months. We look forward to incremental earnings during our seasonally slow Fourth and First quarters,” said Bobby Lavan, Chief Financial Officer.

Share Repurchase and Capital Return Program Update

From September 30, 2024 through January 31, 2025, the Company repurchased 5.1 million shares of Class A common stock for approximately $56 million. The company has $101 million currently remaining under the share repurchase program.

The Board of Directors declared a quarterly cash dividend of $0.055 per share of common stock for the second quarter of fiscal year 2025. The dividend will be payable on March 7, 2025, to stockholders of record on February 21, 2025.

Fiscal Year 2025 Guidance

The Company reiterated financial guidance for fiscal year 2025. We expect total Revenue to be up mid-single digits to 10%+ year-over-year, which equates to $1.23 billion to $1.28 billion of total Revenue. Adjusted EBITDA margin is expected to be 32% to 34%, which equates to Adjusted EBITDA of $390 million to $430 million.

Investor Webcast Information

Listeners may access an investor webcast hosted by Lucky Strike Entertainment. The webcast and results presentation will be accessible at 10:00 AM ET on February 5, 2025 in the Events & Presentations section of the Lucky Strike Entertainment Investor Relations website at https://ir.luckystrikeent.com/overview/default.aspx.

About Lucky Strike Entertainment

Lucky Strike Entertainment is one of the world’s premier location-based entertainment platforms. With over 360 locations across North America, Lucky Strike Entertainment provides experiential offerings in bowling, amusements, water parks, and family entertainment centers. The company also owns the Professional Bowlers Association, the major league of bowling and a growing media property that boasts millions of fans around the globe. For more information on Lucky Strike Entertainment, please visit IR.LuckyStrikeEnt.com.

Forward Looking Statements

Some of the statements contained in this press release are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that involve risk, assumptions and uncertainties, such as statements of our plans, objectives, expectations, intentions and forecasts. These forward-looking statements are generally identified by the use of forward-looking terminology, including the terms “anticipate,” “believe,” “confident,” “continue,” “could,” “estimate,” “expect,” “intend,” “likely,” “may,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “target,” “will,” “would” and, in each case, their negative or other various or comparable terminology. These forward-looking statements reflect our views with respect to future events as of the date of this release and are based on our management’s current expectations, estimates, forecasts, projections, assumptions, beliefs and information. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to have been correct. All such forward-looking statements are subject to risks and uncertainties, many of which are outside of our control, and could cause future events or results to be materially different from those stated or implied in this document. It is not possible to predict or identify all such risks. These risks include, but are not limited to: our ability to design and execute our business strategy; changes in consumer preferences and buying patterns; our ability to compete in our markets; the occurrence of unfavorable publicity; risks associated with long-term non-cancellable leases for our locations; our ability to retain key managers; risks associated with our substantial indebtedness and limitations on future sources of liquidity; our ability to carry out our expansion plans; our ability to successfully defend litigation brought against us; our ability to adequately obtain, maintain, protect and enforce our intellectual property and proprietary rights and claims of intellectual property and proprietary right infringement, misappropriation or other violation by competitors and third parties; failure to hire and retain qualified employees and personnel; the cost and availability of commodities and other products we need to operate our business; cybersecurity breaches, cyber-attacks and other interruptions to our and our third-party service providers’ technological and physical infrastructures; catastrophic events, including war, terrorism and other conflicts; public health emergencies and pandemics, such as the COVID-19 pandemic, or natural catastrophes and accidents; changes in the regulatory atmosphere and related private sector initiatives; fluctuations in our operating results; economic conditions, including the impact of increasing interest rates, inflation and recession; and other factors described under the section titled “Risk Factors” in the Company’s Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission (the “SEC”) by the Company on September 5, 2024, as well as other filings that the Company will make, or has made, with the SEC, such as Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this press release and in other filings. We expressly disclaim any obligation to publicly update or review any forward-looking statements, whether as a result of new information, future developments or otherwise, except as required by applicable law.

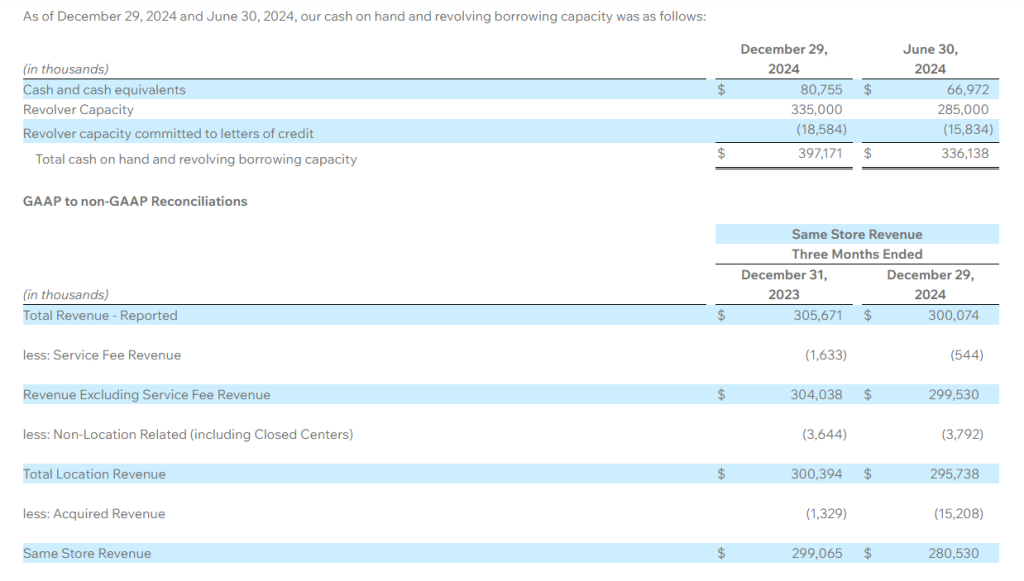

Non-GAAP Financial Measures

To provide investors with information in addition to our results as determined under Generally Accepted Accounting Principles (“GAAP”), we disclose Revenue Excluding Service Fee Revenue, Total Location Revenue, Same Store Revenue and Adjusted EBITDA as “non-GAAP measures”, which management believes provide useful information to investors because each measure assists both investors and management in analyzing and benchmarking the performance and value of our business. Accordingly, management believes that these measurements are useful for comparing general operating performance from period to period, and management relies on these measures for planning and forecasting of future periods. Additionally, these measures allow management to compare our results with those of other companies that have different financing and capital structures. These measures are not financial measures calculated in accordance with GAAP and should not be considered as a substitute for revenue, net income, or any other operating performance or liquidity measure calculated in accordance with GAAP, and may not be comparable to a similarly titled measure reported by other companies. Our fiscal year 2025 guidance measures (other than revenue) are provided on a non-GAAP basis without a reconciliation to the most directly comparable GAAP measure because the Company is unable to predict with a reasonable degree of certainty certain items contained in the GAAP measures without unreasonable efforts. For the same reasons, the Company is unable to address the probable significance of the unavailable information. Such items include, but are not limited to, acquisition related expenses, share-based compensation and other items not reflective of the company’s ongoing operations.

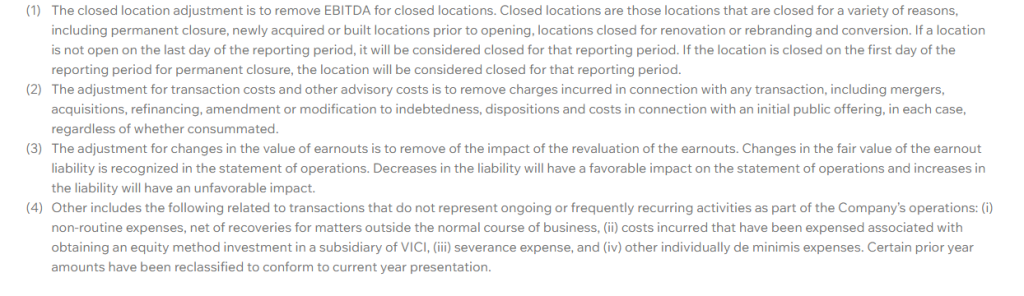

Revenue Excluding Service Fee Revenue represents total Revenue less Service Fee Revenue. Total Location Revenue represents total Revenue less Non-Location Related Revenue, Revenue from Closed Locations, and Service Fee Revenue, if applicable. Same Store Revenue represents total Revenue less Non-Location Related Revenue, Revenue from Closed Locations, Service Fee Revenue, if applicable, and Acquired Revenue. Adjusted EBITDA represents Net Income (Loss) before Interest Expense, Income Taxes, Depreciation and Amortization, Impairment and Other Charges, Share-based Compensation, EBITDA from Closed Locations, Foreign Currency Exchange Loss (Gain), Asset Disposition Loss (Gain), Transactional and other advisory costs, changes in the value of earnouts, and other.

The Company considers Revenue Excluding Service Fee Revenue as an important financial measure because it provides a financial measure of revenue directly associated with consumer discretionary spending and Total Location Revenue as an important financial measure because it provides a financial measure of revenue directly associated with location operations. The Company also considers Same Store Revenue as an important financial measure because it provides comparable revenue for locations open for the entire duration of both the current and comparable measurement periods.

The Company considers Adjusted EBITDA as an important financial measure because it provides a financial measure of the quality of the Company’s earnings. Other companies may calculate Adjusted EBITDA differently than we do, which might limit its usefulness as a comparative measure. Adjusted EBITDA is used by management in addition to and in conjunction with the results presented in accordance with GAAP. We have presented Adjusted EBITDA solely as a supplemental disclosure because we believe it allows for a more complete analysis of results of operations and assists investors and analysts in comparing our operating performance across reporting periods on a consistent basis by excluding items that we do not believe are indicative of our core operating performance. Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are that Adjusted EBITDA:

do not reflect every expenditure, future requirements for capital expenditures or contractual commitments;

do not reflect changes in our working capital needs;

do not reflect the interest expense, or the amounts necessary to service interest or principal payments, on our outstanding debt;

do not reflect income tax (benefit) expense, and because the payment of taxes is part of our operations, tax expense is a necessary element of our costs and ability to operate;

do not reflect non-cash equity compensation, which will remain a key element of our overall equity based compensation package; and

do not reflect the impact of earnings or charges resulting from matters we consider not to be indicative of our ongoing operations.

Lucky Strike Entertainment Corporation Investor Relations IR@LSEnt.com

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

MAIA Provides Phase 2 Interim Data Update In NSCLC. The Phase 2 THIO-101 trial is testing the combination of THIO with cemiplimab (Libtayo), a PD-1 checkpoint inhibitor from Regeneron, in patients with advanced non-small lung cancer (NSCLC). Median overall survival was 16.9 months, compared with expected survival of 5.8 months. Importantly, the lower limit of the statistical confidence intervals for the trial shows a 99% chance of surviving 10.8 months, a statistically significant result.

Combination Uses Two Mechanisms Of Action. The THIO-101 trial combines the killing effects from THIO with the PD-1 inhibition from cemiplimab. THIO uses its telomere targeting to damage cancer cell DNA, causing cell death. This also stimulates an immune response in the tumor through the cGAS/STING pathway and T-cell responses. Cemiplimab provides a second mechanism, allowing the immune cells to recognize and kill the cancer cells.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Office Depot, Inc., together with its subsidiaries, supplies a range of office products and services. It offers merchandise, such as general office supplies, computer supplies, business machines and related supplies, and office furniture through its chain of office supply stores under the Office Depot, Foray, Ativa, Break Escapes, Worklife, and Christopher Lowell brand names. The company also provides graphic design, printing, reproduction, mailing, shipping, and other services through design, print, and ship centers. It has operations throughout North America, Europe, Asia, and Central America. The company also sells its products and services through direct mail catalogs, contract sales force, Internet sites, and retail stores, through a mix of company-owned operations, joint ventures, licensing and franchise agreements, alliances, and other arrangements. As of December 31, 2008, Office Depot operated 1,267 North American retail division office supply stores and 162 international division retail stores, as well as participated under licensing and merchandise arrangements in 98 stores. The company was founded in 1986 and is based in Boca Raton, Florida.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Award. Another in a string of new business, ODP Corporation announced its Business Solutions segment is participating in a new award for a multi-year furniture contract with Region 4 Education Service Center (ESC) that brings the potential of up to $500 million in total annual revenue. After a challenging 2024 for Business Solutions, the new year has started positively with the recent contract awards that have the potential to drive top line growth for the segment.

Details. The new contract enables the ODP Business Solutions Workspace Interiors team to offer compliant cooperative purchasing solutions through OMNIA Partners, providing furniture, installation, and related services to K-12 schools, higher education institutions, and cities and counties across the U.S. The new contract grants OMNIA Partners members access to a comprehensive range of products.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Full year and fourth quarter 2024 financial results. On a full year basis, Alliance generated 2024 adjusted EBITDA of $714.2 million and earnings per unit (EPU) of $2.77, respectively, compared to $933.1 million and $4.81 in 2023. Fourth quarter adjusted EBITDA was $124.0 million, and EPU amounted to $0.12, respectively, compared to $185.4 million and $0.88 during the prior year period. Fourth quarter and full year results were impacted by lower coal volumes, operational challenges within ARLP’s coal operations in Appalachia, and a $30.1 million non-cash asset impairment charge which had a negative impact of ~$0.24 per unit.

Management guidance for 2025. Coal sales are expected to be in the range of 32.25 million to 34.25 million tons, while the sales price of coal per ton is expected to be in the range of $57.00 to $61.00. Segmented adjusted EBITDA expense per ton sold is expected to be $40.00 to $44.00. The company has committed and priced 26.0 million tons of its 2025 sales volume, including 23.5 million for the domestic market and 2.5 million tons for the export market.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Teladoc Health is acquiring Catapult Health for $65 million to enhance its preventive care and at-home diagnostic testing capabilities, further strengthening its integrated healthcare solutions. – Catapult Health’s VirtualCheckup program will enable Teladoc to expand its chronic condition management services and seamlessly connect high-risk patients to virtual care programs. – This acquisition comes as Teladoc seeks to regain momentum following its 2020 Livongo acquisition, which initially valued the combined company at $37 billion but has since declined to a market cap under $2 billion.

Teladoc Health has announced a definitive agreement to acquire Catapult Health, a move aimed at strengthening its preventive care and chronic condition management capabilities while expanding its at-home diagnostic testing offerings. This acquisition aligns with Teladoc’s strategy to enhance virtual care accessibility and effectiveness for its over 93 million members.

Catapult Health is recognized for its innovative approach to at-home wellness and diagnostic testing, which integrates virtual clinical support and high-touch patient engagement. Teladoc plans to leverage these capabilities to further enrich its industry-leading suite of integrated healthcare solutions.

“This acquisition will help advance our strategy in meaningful ways — from giving more members access to convenient and impactful wellness and preventive care, to unlocking greater value for our customers,” said Chuck Divita, Chief Executive Officer of Teladoc Health. “Catapult Health brings an experienced team and a strong culture of innovation, and we are thrilled to welcome them to Teladoc Health.”

Strategic Objectives and Synergies

Teladoc Health’s integrated care strategy is built on four key pillars:

Expanding Membership and Service Utilization – Enhancing the accessibility and engagement of healthcare services for existing and new members.

Leveraging Clinical Expertise and Product Breadth – Strengthening healthcare outcomes by integrating a broader range of clinical solutions.

Growing International Presence – Extending Teladoc’s reach beyond domestic markets to serve a global population.

Advancing Mental Health Solutions – Building upon its existing leadership in virtual mental health services.

Catapult Health’s flagship VirtualCheckup program exemplifies its innovation in preventive care. The at-home wellness exam provides members with a simple diagnostic kit, allowing them to collect blood samples, measure blood pressure, and submit other key health data. Following this, a virtual consultation with a licensed healthcare professional ensures timely assessment and guidance.

For members identified with high-risk factors or chronic conditions, Catapult’s clinicians can seamlessly enroll them into Teladoc’s condition management programs, including diabetes, hypertension, pre-diabetes, and weight management. Additionally, members can be referred to Teladoc’s virtual mental health specialists and primary care providers for continued support.

Transaction Details

The acquisition is structured as an all-cash transaction valued at $65 million, with up to $5 million in contingent earnout consideration. Catapult Health reported $30 million in trailing 12-month revenue as of Q3 2024. Upon closing, Catapult will be integrated into Teladoc’s Integrated Care segment. The deal is expected to close in Q1 2025.

Impact and Market Expansion

Catapult Health currently serves over 3 million people through its partnerships with hundreds of employer clients. The company is recognized for its strong customer satisfaction, clinical outcomes, and cost-saving benefits, including an estimated $1,400 average savings per participant over a three-year period due to early disease detection and health risk identification.

Teladoc’s Market Challenges and Context

This acquisition comes after a tumultuous period for Teladoc. Following its acquisition of Livongo in 2020, the combined companies had an enterprise value of $37 billion. However, Teladoc’s stock has struggled since then, with a current market capitalization just under $2 billion. The acquisition of Catapult Health represents a strategic effort to regain momentum and strengthen its position in the evolving telehealth market.

Key Points: – The U.S. trade deficit reached $918.4 billion in 2024, marking the second-largest annual total, while December’s deficit set a record at $98.4 billion. – Strong consumer demand, a robust U.S. dollar, and rising imports—particularly in industrial supplies and consumer goods—outpaced export growth, widening the trade gap. – Escalating trade tensions, including newly imposed and proposed tariffs on Mexico, Canada, and China, could further disrupt trade flows and market stability in 2025.

The U.S. trade deficit surged to $918.4 billion in 2024, marking the second-highest annual total in history. This 17% increase from 2023 was driven primarily by a sharp rise in imports, which climbed 6.6% to $4.11 trillion, outpacing export growth of 3.9% to $3.19 trillion.

According to the U.S. Census Bureau and the Bureau of Economic Analysis, December’s trade deficit reached a record-high $98.4 billion, up $19.5 billion from November. Monthly exports dropped to $266.5 billion, while imports surged to $364.9 billion.

Key Trends in 2024 Trade Data

Record Merchandise Trade: The U.S. set all-time highs for total merchandise trade, imports, and the December monthly trade deficit.

Regional Trade Concentration: Nearly 41% of total U.S. trade involved Mexico, Canada, and China.

Strong Consumer Demand: Americans continued spending on imported goods such as weight-loss drugs, auto parts, computers, and food, supported by a strong U.S. dollar that made foreign products more affordable.

Declining Vehicle Exports: U.S. auto-related exports fell by $10.8 billion, largely due to intensified competition from China’s expanding auto industry.

Growth in Services Sector: Foreign spending on U.S. travel, business, and financial services helped boost service sector exports, which reached $1.107 trillion, up $81.2 billion from 2023.

Policy and Market Impact

Trade flows could face further disruption in 2025 as President Trump escalates trade tensions. This week, the administration imposed—then temporarily paused—25% tariffs on imports from Mexico and Canada. Trump has also proposed an additional 10% tariff on all Chinese imports, building on existing 25% duties from his first term. In response, China announced $20 billion in retaliatory tariffs and new export restrictions on critical minerals.

The U.S. posted its largest bilateral trade deficit with China at $295.4 billion, while also running record deficits with Mexico, Vietnam, India, Taiwan, South Korea, and the European Union. Meanwhile, Trump has made reducing the trade deficit “to zero” a primary policy objective and is considering imposing tariffs on the EU and UK.

Economic Context

A strong U.S. economy and a robust dollar fueled demand for imports, even as American exports faced headwinds in global markets. The U.S. trade deficit as a share of GDP rose to 3.1% in 2024, up from 2.8% in 2023. Many essential goods, such as consumer products and apparel, are no longer produced domestically, further reinforcing America’s reliance on imports.

As businesses rushed to import goods ahead of potential tariff hikes, the trade deficit soared in December, setting a record for the highest monthly deficit and contributing to the second-largest annual trade gap in U.S. history. With ongoing trade disputes and policy shifts, global trade flows could remain volatile in the months ahead.