BY THE COMTECH EDITORIAL TEAM – FEB 5, 2024 | 3 MIN READ

MELVILLE, N.Y. – February 5, 2024– Comtech (NASDAQ: CMTL) announced today that Washington State recently awarded the company a $48 million contract extension to continue providing Next Generation 911 (NG911) services over the next five years, with the option to extend through 2034.

Washington State initially contracted Comtech to design, deploy and operate next generation public safety technologies and secure and reliable communications capabilities in 2016, making Washington a national leader in the application of NG911 services.

“We value our continued partnership with Washington State and have worked collaboratively over the past eight years to deploy one of the most robust and advanced NG911 systems in the United States,” said Ken Peterman, President and CEO, Comtech. “This contract extension award further demonstrates the state of Washington’s trust of our NG911 capabilities to support the state’s public safety mission. As we continue to support the state of Washington, we look forward to exploring emerging capabilities like artificial intelligence to equip first responders with life-saving insights at the speed of relevance.”

“The Washington State NG911 enterprise system provides people in crisis with a more effective 911 service and has saved countless lives in the eight years since we initially partnered with Comtech,” said Adam Wasserman, Assistant Director for Emergency Communications, Washington State Emergency Management Division. “Our NG911 system keeps pace with the ever-evolving communications technologies used by the citizens in our state. In addition, due to the increased reliability, resilience and security, as well as the designed interoperability with other 911 centers – intrastate, interstate, and international (Canada) – the Washington State NG911 enterprise system is more effective at collecting and disseminating initial situational awareness during major emergencies and disasters.”

As one of the most trusted providers of public safety technologies, Comtech is continuing to expand its NG911 offerings for governments and emergency response providers around the world. The company’s NG911 systems are designed to adapt and continuously evolve over time to meet the needs of emerging use cases as well as future applications.

About the State of Washington 911 Coordination Office

The 911 Unit of the Emergency Management Division works to ensure the seamless operation of the statewide 911 communications system, ensuring uniform, prompt, and efficient access to public safety services for the citizens and visitors to the state of Washington.

Washington has 86 Public Safety Answering Points (911 centers) that cover all 39 counties within the state. The PSAPs are connected to the statewide Emergency Services IP Network (ESInet), which delivers location information of the 911 caller as well as other data needed.

In addition to contracting for the statewide 911 network, the 911 Unit provides fiscal and technical assistance to counties and PSAPs to support 911 operations. The 911 Unit continues to drive the evolution of the 911 network to accommodate the advances in communication technologies such as wireless, VoIP-based communications and the myriad of upcoming non-traditional technologies.

About Comtech

Comtech Telecommunications Corp. is a leading global technology company providing terrestrial and wireless network solutions, next-generation 911 emergency services, satellite and space communications technologies, and cloud native capabilities to commercial and government customers around the world. Our unique culture of innovation and employee empowerment unleashes a relentless passion for customer success. With multiple facilities located in technology corridors throughout the United States and around the world, Comtech leverages our global presence, technology leadership, and decades of experience to create the world’s most innovative communications solutions.For more information, please visit www.comtech.com.

Forward-Looking Statements

Certain information in this press release contains statements that are forward-looking in nature and involve certain significant risks and uncertainties. Actual results and performance could differ materially from such forward-looking information. The Company’s Securities and Exchange Commission filings identify many such risks and uncertainties. Any forward-looking information in this press release is qualified in its entirety by the risks and uncertainties described in such Securities and Exchange Commission filings.

CHELMSFORD, MA / ACCESSWIRE / February 5, 2024 / Harte Hanks, Inc. (NASDAQ:HHS), a leading global customer experience company focused on bringing companies closer to customers for 100 years, today announced the appointment of two senior executives to newly-created roles reporting to Kelly Waller, Senior Vice President of Sales and Marketing.

Varsha Tomar was named Vice President, Partnerships, and will oversee the identification, cultivation, and management of strategic B2B sales partnerships that will enable Harte Hanks to drive incremental revenue. She will oversee joint alliances, resellers/white labelers of Harte Hanks services and manage a team of Inside Partner Account Managers. Ms. Tomar joins Harte Hanks from HealthEquity, where she was Director of Business Operations after previously serving as Global Head of Go-To-Market Strategy for Finastra.

Luke Kenny was named Sr. Director of International Sales and Client Expansion. Based in Portugal, Mr. Kenny has nearly two decades of experience as a sales director and demand generation expert across EMEA and APAC for B2B organizations, including Finastra and FIS. At Harte Hanks, he will focus on sales as well as supporting and growing business from existing European clients. He is also tasked with overseeing the growth of the sales teams throughout the region. Harte Hanks has offices in the UK, Romania and Belgium.

“As we continue to implement our transformation growth plan, these two strategic hires will help us meet our goals of expanding our sales and marketing organization routes to market and expanding our global footprint,” commented Ms. Waller.

About Harte Hanks:

Harte Hanks (NASDAQ:HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract and engage their customers.

Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands, including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony and IBM among others. Headquartered in Chelmsford, Massachusetts, Harte Hanks has over 2,500 employees in offices across the Americas, Europe, and Asia Pacific.

As used herein, “Harte Hanks” or “the Company” refers to Harte Hanks, Inc. and/or its applicable operating subsidiaries, as the context may require. Harte Hanks’ logo and name are trademarks of Harte Hanks.

Certain statements discussed in this release as well as in other reports, materials and oral statements that the Company releases from time to time to the public may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Generally, words such as “anticipate,” “estimate,” “expect,” “project,” “intend,” “believe,” “plan,” “target,” “forecast” and similar expressions are intended to identify forward- looking statements. Such forward-looking statements concern management’s expectations, strategic objectives, business prospects, anticipated economic performance and financial condition and other similar matters. Forward-looking statements are inherently uncertain and subject to a variety of assumptions, risks and uncertainties that could cause actual results to differ materially from those anticipated or expected by the management of the Company. These statements are not guarantees of future performance and actual events or results may differ significantly from these statements. Given these risk factors, investors and analysts should not place undue reliance on forward-looking statements. Forward-looking statements speak only as of the date of the document in which they are made. The Company disclaims any obligation or undertaking to provide any updates or revisions to any forward-looking statement to reflect any change in the Company’s expectations or any change in events, conditions or circumstances on which the forward-looking statement is based, except as required by law. It is advisable, however, to consult any further disclosures the Company makes in its filings with the Securities and Exchange Commission, including Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K (if any). These statements constitute the Company’s cautionary statements under the Private Securities Litigation Reform Act of 1995.

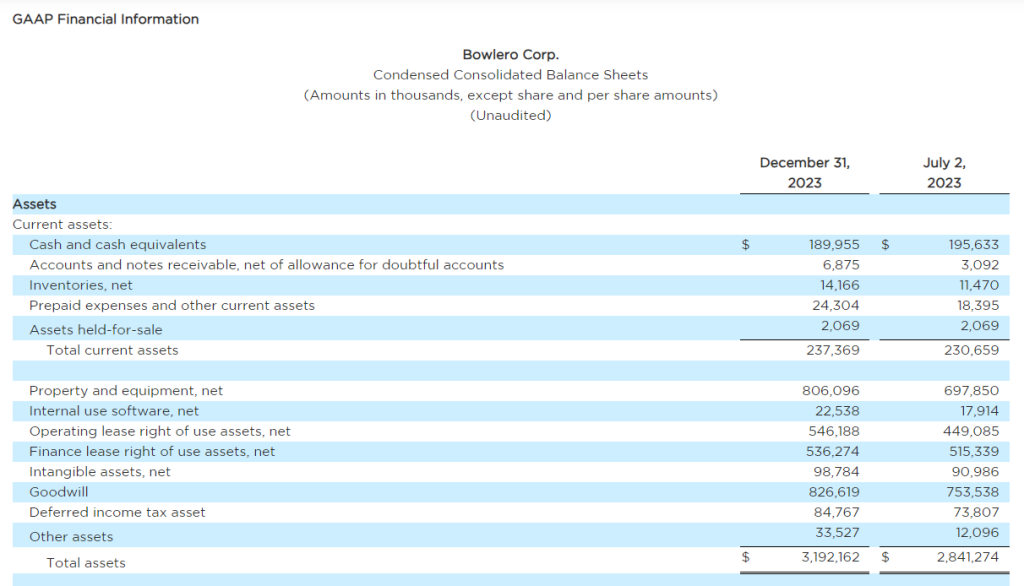

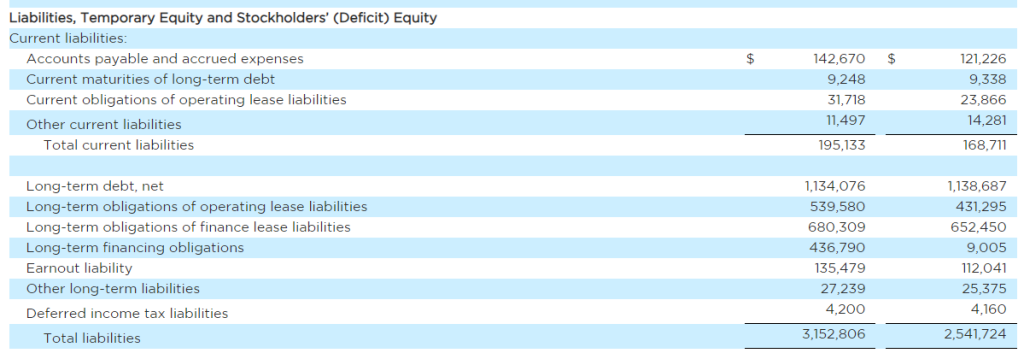

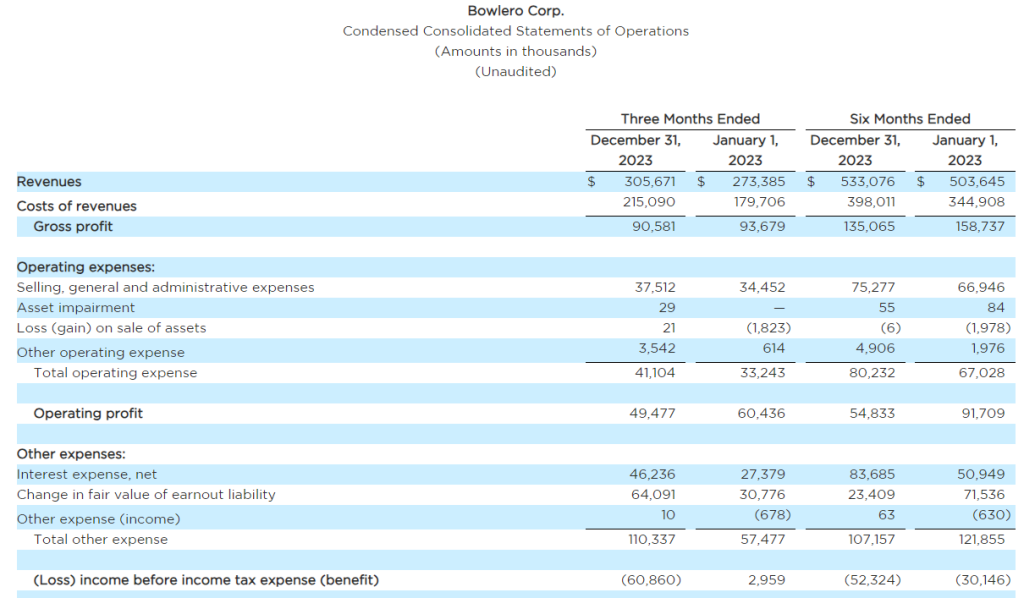

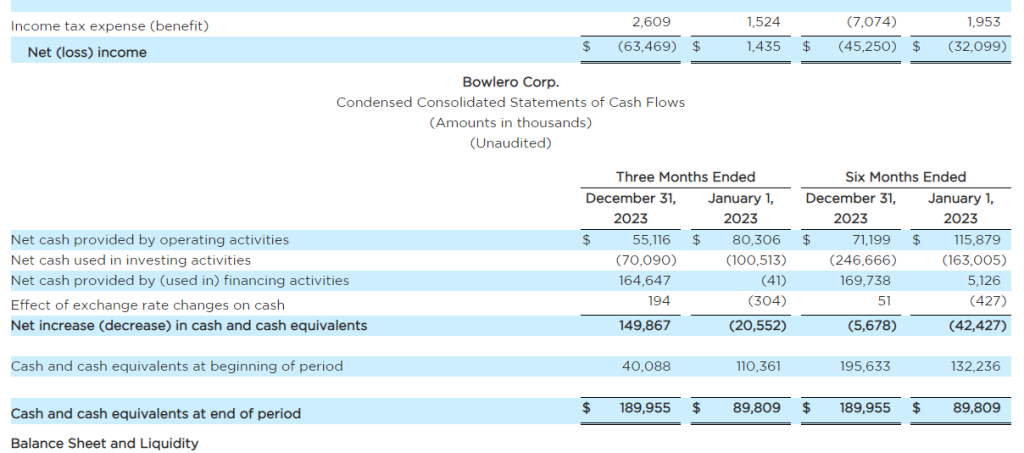

RICHMOND, Va.–(BUSINESS WIRE)– Bowlero Corp. (NYSE: BOWL) (“Bowlero” or the “Company”), one of the world’s premier operators of location-based entertainment, today provided financial results for the second quarter of the 2024 Fiscal Year, which ended on December 31, 2023.

Quarter Highlights:

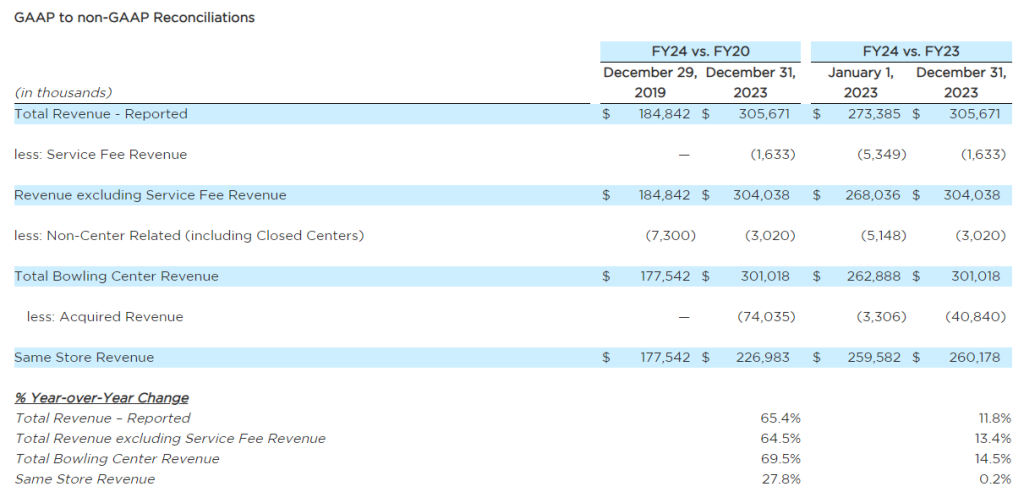

Revenue increased 11.8% to $305.7 million versus the prior year and increased 65.4% versus 2QFY20 (quarter ended December 29, 2019)

Revenue excluding Service Fee Revenue increased 13.4% to $304.0 million versus the prior year and was up 64.5% versus 2QFY20

Total Bowling Center Revenue increased 14.5% versus the prior year and was up 69.5% versus 2QFY20

Same Store Revenue increased 0.2% versus the prior year and grew 27.8% versus 2QFY20

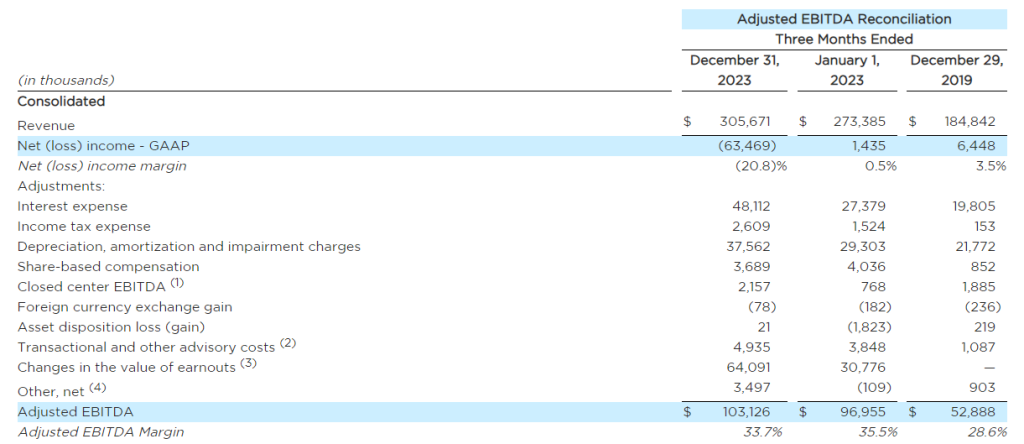

Net loss of $63.5 million versus prior year income of $1.4 million and income of $6.4 million in 2QFY20, which includes $64.1 million of expense from the non-cash impact of the earnouts for the current period

Adjusted EBITDA of $103.1 million versus prior year of $97.0 million and $52.9 million in 2QFY20

Added 3 locations during the quarter, 2 from acquisitions and 1 new build-out, bringing year-to-date new centers to 21

Total locations in operation as of February 5, 2024 is 350

“Second quarter fiscal year 2024 saw double-digit total growth, amplifying our ability to grow the business despite difficult comparatives as we come out of the record-breaking COVID rebound. Our acquisition of Lucky Strike represents a major milestone for the Company as we focus on higher revenue properties and continue to grow our location count. That deal brought together flagship properties with our best-in-class operators and event sales platform, driving results higher than expectations. We are expanding the well-known Lucky Strike brand by opening our first Lucky Strike new build in Moorpark, California, and the new Lucky Strike Miami will soon follow.,” said Thomas Shannon, Founder and Chief Executive Officer of Bowlero.

Mr. Shannon continued, “In the quarter, our event business was up over thirty percent and continues to drive the strength of our overall business. Same-store revenue was positive in the quarter, driven by the reset of mid-week promotions, improved pricing dynamics on the weekend, and strong execution from our events team. Acquisitions and new builds contributed $41 million of revenue in the quarter and the Lucky Strike acquisition is ahead of our profitability targets. We are taking a cautious approach to the third quarter due to meaningful weather headwinds in the first three weeks of January but expect to make up that softness in the rest of the third quarter and fourth quarter and continue to expect double-digit revenue growth in fiscal year 2024.”

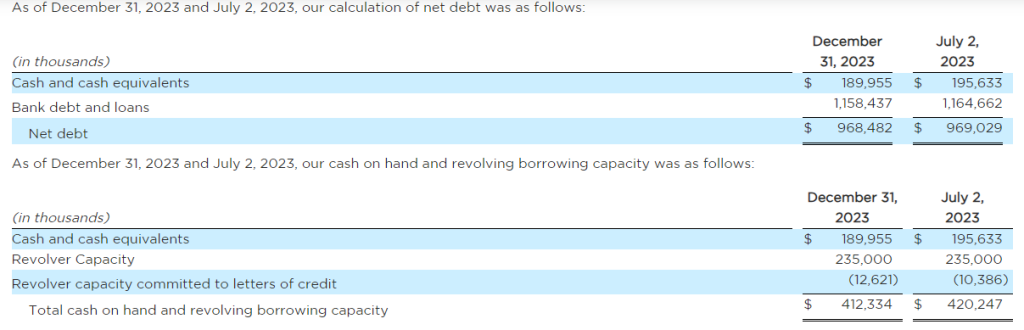

Bobby Lavan, Chief Financial Officer, added, “In the quarter, we received $409 million net proceeds from our sale-leaseback transaction with Vici. We used proceeds to pay down our revolver balance in full, fund acquisitions including Lucky Strike, and accelerate our capital investment plan. We ended the quarter with $190 million of cash and $412 million of total liquidity.”

Share Repurchases

During the quarter, the Company repurchased approximately 7.5 million shares of Class A common stock for approximately $80 million. In the first quarter of fiscal year 2024, the company repurchased approximately 12.1 million shares for approximately $131 million, bringing total repurchases in the first half of fiscal year 2024 to approximately 19.6 million. Since 2021, the Company has spent approximately $432 million retiring all SPAC-related warrants, repurchasing 31.0 million shares of common stock, and 4.9 million as-converted preferred shares, reducing common stock outstanding by about 20%.

On February 2, 2024, the Board of Directors authorized a time extension and an increase to the share repurchase program, replenishing the authorized repurchase amount to $200 million and removing the program expiration date. The timing of the repurchases and the actual amount repurchased will depend on a variety of factors, including the market price of the Company’s shares, general market and economic conditions, and other factors.

Dividend

The Board of Directors of the Company has approved the initiation of a quarterly dividend program. The Board of Directors declared an initial quarterly cash dividend of $0.055 per share of common stock for the third quarter of fiscal 2024. The dividend will be payable on March 8, 2024, to stockholders of record on February 23, 2024. The Company intends to pay a cash dividend on a quarterly basis going forward, subject to market conditions and approval by the Company’s Board of Directors.

Fiscal Year 2024 and Third Quarter 2024 Guidance

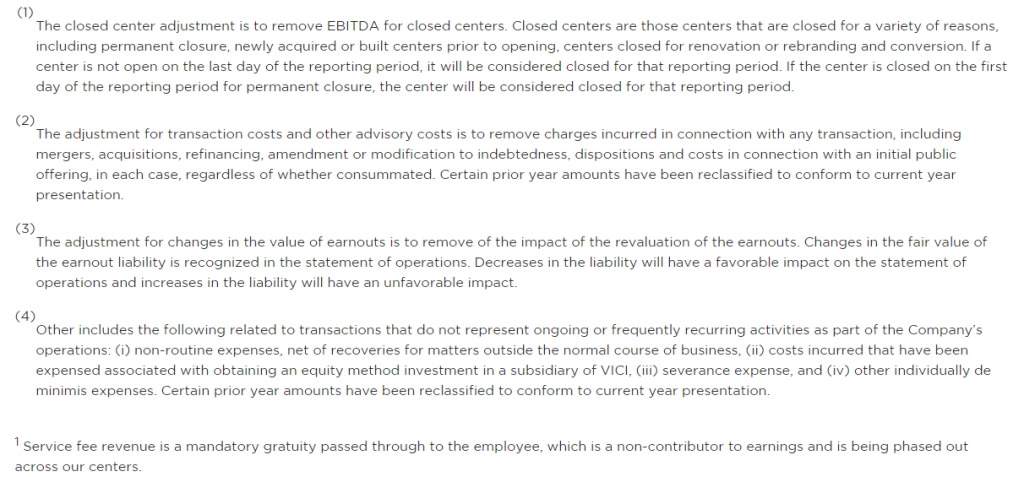

The Company reiterated financial guidance for fiscal year 2024. The Company expects Revenue to be up 10% to 15% in fiscal year 2024, excluding the $21 million of Service Fee Revenue1 from prior year revenue, equating to $1.14 billion to $1.19 billion. Adjusted EBITDA margin is expected to be 32% to 34%, which equates to Adjusted EBITDA of $365 million to $405 million. The Company expects the third quarter of fiscal year 2024 to have Revenue Excluding Service Fee Revenue of $335 million to $350 million and Adjusted EBITDA of $128 million to $143 million.

The Company is updating its investment guidance based on expanding growth opportunities in fiscal year 2025. The Company expects to reinvest heavily in the business in fiscal year 2024, with more than $190 million allocated to acquisitions (up from $160 million), $40 million to new builds, and $80 million to conversions and growth (up from $75 million). Maintenance capital expenditures are expected to be $45 million.

Investor Webcast Information

Listeners may access an investor webcast hosted by Bowlero. The webcast and results presentation will be accessible at 10:00 AM ET on February 5, 2024, in the Events & Presentations section of the Bowlero Investor Relations website at https://ir.bowlerocorp.com/overview/default.aspx.

About Bowlero Corp.

Bowlero Corporation is one of the world’s premier operators of location-based entertainment. With approximately 350 locations across North America, the Company serves more than 40 million guest visits annually through a family of brands that include Lucky Strike, Bowlero and AMF. In 2019, Bowlero acquired the Professional Bowlers Association, the major league of bowling and a growing media property that boasts millions of fans around the globe. For more information on Bowlero, please visit BowleroCorp.com.

Forward Looking Statements

Some of the statements contained in this press release are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that involve risk, assumptions and uncertainties, such as statements of our plans, objectives, expectations, intentions and forecasts. These forward-looking statements are generally identified by the use of forward-looking terminology, including the terms “anticipate,” “believe,” “confident,” “continue,” “could,” “estimate,” “expect,” “intend,” “likely,” “may,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “target,” “will,” “would” and, in each case, their negative or other various or comparable terminology. These forward-looking statements reflect our views with respect to future events as of the date of this release and are based on our management’s current expectations, estimates, forecasts, projections, assumptions, beliefs and information. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to have been correct. All such forward-looking statements are subject to risks and uncertainties, many of which are outside of our control, and could cause future events or results to be materially different from those stated or implied in this document. It is not possible to predict or identify all such risks. These risks include, but are not limited to: our ability to design and execute our business strategy; changes in consumer preferences and buying patterns; our ability to compete in our markets; the occurrence of unfavorable publicity; risks associated with long-term non-cancellable leases for our centers; our ability to retain key managers; risks associated with our substantial indebtedness and limitations on future sources of liquidity; our ability to carry out our expansion plans; our ability to successfully defend litigation brought against us; our ability to adequately obtain, maintain, protect and enforce our intellectual property and proprietary rights and claims of intellectual property and proprietary right infringement, misappropriation or other violation by competitors and third parties; failure to hire and retain qualified employees and personnel; the cost and availability of commodities and other products we need to operate our business; cybersecurity breaches, cyber-attacks and other interruptions to our and our third-party service providers’ technological and physical infrastructures; catastrophic events, including war, terrorism and other conflicts; public health emergencies and pandemics, such as the COVID-19 pandemic, or natural catastrophes and accidents; changes in the regulatory atmosphere and related private sector initiatives; fluctuations in our operating results; economic conditions, including the impact of increasing interest rates, inflation and recession; and other factors described under the section titled “Risk Factors” in the Company’s Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission (the “SEC”) by the Company on September 11, 2023, as well as other filings that the Company will make, or has made, with the SEC, such as Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this press release and in other filings. We expressly disclaim any obligation to publicly update or review any forward-looking statements, whether as a result of new information, future developments or otherwise, except as required by applicable law.

Non-GAAP Financial Measures

To provide investors with information in addition to our results as determined under Generally Accepted Accounting Principles (“GAAP”), we disclose Revenue Excluding Service Fee Revenue, Total Bowling Center Revenue, Same Store Revenue and Adjusted EBITDA as “non-GAAP measures”, which management believes provide useful information to investors because each measure assists both investors and management in analyzing and benchmarking the performance and value of our business. Accordingly, management believes that these measurements are useful for comparing general operating performance from period to period, and management relies on these measures for planning and forecasting of future periods. Additionally, these measures allow management to compare our results with those of other companies that have different financing and capital structures. These measures are not financial measures calculated in accordance with GAAP and should not be considered as a substitute for revenue, net income, or any other operating performance or liquidity measure calculated in accordance with GAAP, and may not be comparable to a similarly titled measure reported by other companies. Our third quarter and fiscal year 2024 guidance measures (other than revenue) are provided on a non-GAAP basis without a reconciliation to the most directly comparable GAAP measure because the Company is unable to predict with a reasonable degree of certainty certain items contained in the GAAP measures without unreasonable efforts. For the same reasons, the Company is unable to address the probable significance of the unavailable information. Such items include, but are not limited to, acquisition related expenses, stock-based compensation and other items not reflective of the company’s ongoing operations.

Revenue Excluding Service Fee Revenue represents Total Revenue less Service Fee Revenue. Total Bowling Center Revenue represents Total Revenue less Non-Center Related Revenue, Revenue from Closed Centers (as defined below), and Service Fee Revenue, if applicable. Same Store Revenue represents Total Revenue less Non-Center Related Revenue, Revenue from Closed Centers, Service Fee Revenue, if applicable, and Acquired Revenue. Adjusted EBITDA represents Net Income (Loss) before Interest Expense, Income Taxes, Depreciation and Amortization, Share-based Compensation, EBITDA from Closed Centers, Foreign Currency Exchange Loss (Gain), Asset Disposition Loss (Gain), Transactional and other advisory costs, changes in the value of earnouts, and other.

The Company considers Revenue Excluding Service Fee Revenue as an important financial measure because provides a financial measure of revenue directly associated with consumer discretionary spending and Total Bowling Center Revenue as an important financial measure because it provides a financial measure of revenue directly associated with bowling center operations. The Company also considers Same Store Revenue as an important financial measure because it provides comparable revenue for centers open for the entire duration of both the current and comparable measurement periods.

The Company considers Adjusted EBITDA as an important financial measure because it provides a financial measure of the quality of the Company’s earnings. Other companies may calculate Adjusted EBITDA differently than we do, which might limit its usefulness as a comparative measure. Adjusted EBITDA is used by management in addition to and in conjunction with the results presented in accordance with GAAP. We have presented Adjusted EBITDA solely as a supplemental disclosure because we believe it allows for a more complete analysis of results of operations and assists investors and analysts in comparing our operating performance across reporting periods on a consistent basis by excluding items that we do not believe are indicative of our core operating performance. Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are that Adjusted EBITDA:

do not reflect every expenditure, future requirements for capital expenditures or contractual commitments;

do not reflect changes in our working capital needs;

do not reflect the interest expense, or the amounts necessary to service interest or principal payments, on our outstanding debt;

do not reflect income tax (benefit) expense, and because the payment of taxes is part of our operations, tax expense is a necessary element of our costs and ability to operate;

do not reflect non-cash equity compensation, which will remain a key element of our overall equity based compensation package; and

do not reflect the impact of earnings or charges resulting from matters we consider not to be indicative of our ongoing operations.

Comtech Telecommunications Corp. engages in the design, development, production, and marketing of products, systems, and services for advanced communications solutions in the United States and internationally. It operates in three segments: Telecommunications Transmission, Mobile Data Communications, and RF Microwave Amplifiers. The Telecommunications Transmission segment provides satellite earth station equipment and systems, over-the-horizon microwave systems, and forward error correction technology, which are used in various commercial and government applications, including backhaul of wireless and cellular traffic, broadcasting (including HDTV), IP-based communications traffic, long distance telephony, and secure defense applications. The Mobile Data Communications segment provides mobile satellite transceivers, and computers and satellite earth station network gateways and associated installation, training, and maintenance services; supplies and operates satellite packet data networks, including arranging and providing satellite capacity; and offers microsatellites and related components. The RF Microwave Amplifiers segment designs, develops, manufactures, and markets satellite earth station traveling wave tube amplifiers (TWTA) and broadband amplifiers. Its amplifiers are used in broadcast and broadband satellite communication; defense applications, such as telecommunications systems and electronic warfare systems; and commercial applications comprising oncology treatment systems, as well as to amplify signals carrying voice, video, or data for air-to-satellite-to-ground communications. The company serves satellite systems integrators, wireless and other communication service providers, broadcasters, defense contractors, military, governments, and oil companies. Comtech markets its products through independent representatives and value-added resellers. The company was founded in 1967 and is headquartered in Melville, New York.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

GFSR. Late last week, Comtech received notice from the U.S. Army Contracting Command to move forward on the Company’s previously announced $544 million Global Field Service Representative (GFSR) contract. Recall, this award had been under protest. With the notice, Comtech can now begin to fulfill the contract. Comtech was originally awarded the $544 million contract in October 2023.

Contract Details. The GFSR program provides ongoing communications and IT infrastructure support for the Army, Air Force, Navy, Marine Corps, and NATO-enabling U.S. and coalition forces to maintain robust, resilient, and secure connectivity for global all-domain operations in all environments. Under this contract, Comtech will provide onsite professional engineering services, as well as supply and support the Company’s market leading satellite and terrestrial networking communications technologies for the Project Manager Tactical Network (PM TN) in the GFSR support program.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Management releases initial fiscal 2025 guidance. Management projects sales of $1.5-$1.6 billion (Noble est. $1.57b), adjusted ebitda of $300-$350 million ($345m), and adjusted diluted EPS of $4.25-$4.75 ($4.50). Guidance assumes $10-$12m of income from its unconsolidated subsidiary ($9.3m), capital expenditures of $100-$120m ($90m), and $60-$100m of debt deleverage ($40m). Management assumes working capital improvements which we have not assumed in our models. Management also reconfirmed fiscal 2024 guidance.

We are not changing our estimates, but will monitor the areas in which we differ with guidance. Our model projects estimates that at the high end of the range for sales and adjusted ebitda but below unconsolidated sub earnings, capital expenditures, and debt reduction. Given that our estimates are generally in line with guidance, we are not making changes at this time. Instead, we will monitor the discrepancies quarterly and make adjustments as needed.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

In a strategic move aimed at addressing the soaring demand for its revolutionary weight-loss drug, Wegovy, Novo Holdings, the parent company of Novo Nordisk, has disclosed plans to acquire contract drug maker Catalent for $11.5 billion in cash. This acquisition is poised to fortify Novo Nordisk’s production capabilities in response to the extraordinary demand for innovative weight loss and diabetes medications.

Novo Holdings will acquire Catalent for $11.5 billion in cash. As part of the deal, Novo Nordisk will purchase three Catalent fill-finish sites, bolstering the production of Wegovy and other crucial medications. The acquisition is strategically driven by the exceptional demand for Wegovy and Ozempic over the past year.

Novo anticipates that the deal will have a low single-digit percentage negative impact on operating profit growth in 2024 and 2025. The terms include the acquisition of all outstanding shares of Catalent for $63.50 per share in cash, representing a premium of 16.5% to the company’s last trading price. Novo will also assume Catalent’s debt, bringing the total enterprise value of the deal to $16.5 billion.

The acquisition is expected to gradually increase Novo’s filling capacity, with notable effects expected from 2026 onwards. The three fill-finish sites, located in Italy, Belgium, and Bloomington, Indiana, will play a crucial role in supporting Novo Nordisk’s expanding drug portfolio.

In the growing obesity drug market, Novo Nordisk faces competition from Eli Lilly’s Zepbound. Analysts estimate that the obesity drug market could reach $100 billion by the end of the decade, highlighting the immense potential for companies in this sector.

The acquisition aligns seamlessly with Novo Holdings’ strategy of investing in established life science companies with significant long-term potential. Catalent’s expertise in enabling pharmaceutical, biotech, and consumer health partners is in harmony with Novo Holdings’ commitment to improving health and sustainability.

The merger is anticipated to close by the end of calendar year 2024, subject to customary closing conditions, Catalent stockholder approval, and regulatory approvals. Catalent’s Board unanimously recommends that stockholders vote in favor of the merger, following an evaluation of value-maximizing alternatives.

Kasim Kutay, CEO of Novo Holdings, expressed excitement about the partnership with Catalent and emphasized their commitment to supporting Catalent’s growth and mission to develop products that enhance lives.

Novo Holdings’ acquisition of Catalent represents a strategic move to strengthen production capabilities and meet the escalating demand for transformative medications like Wegovy. As the merger progresses, it not only positions Novo Nordisk for continued success in the competitive pharmaceutical landscape but also aligns with Novo Holdings’ broader mission of investing in high-quality life sciences companies for the betterment of society and the planet. The industry will be closely watching the outcome of this significant acquisition, anticipating positive impacts on Novo Nordisk’s product development and market position.

Mark your calendars! Don’t miss Noble Capital Markets’ Emerging Growth Virtual Healthcare Equity Conference on April 17-18. This exclusive virtual event connects investors with 50 leading public biotech, healthcare services, and medical device companies. Presenting company slots are available…Read More

In a significant development within the metallurgical industry, Acerinox’s wholly owned U.S. subsidiary, North American Stainless, is set to acquire Haynes International (HAYN), a leading developer, manufacturer, and marketer of technologically advanced high-performance alloys. The all-cash transaction, valued at $798 million, positions Acerinox to fortify its global leadership in the high-performance alloy segment.

Under the definitive agreement, Acerinox will acquire all outstanding shares of Haynes for $61.00 per share in cash, reflecting a premium of approximately 22% to Haynes’s six-month volume-weighted average share price ending February 2, 2024. The enterprise value of the deal stands at approximately $970 million. The transaction has received unanimous approval from the Boards of Directors of both Haynes and Acerinox.

Strategic Benefits for Acerinox:

Global Leadership: Strengthens Acerinox’s global leadership in the high-performance alloy segment.

U.S. Market Expansion: Expands Acerinox’s presence in the U.S. market, creating new opportunities in the aerospace sector.

Strategic Investment: Haynes to reinvest around $200 million over the next four years, particularly in Haynes’s Kokomo operations, to establish an integrated HPA and stainless steel platform.

Synergies and Growth: Anticipates annual synergies of $71 million, primarily unlocked through the $200 million investment, fostering growth and margin enhancements.

Complementary Businesses: Creates additional value through the combination of complementary businesses, expanding U.S. operating capabilities and establishing a worldwide sales and distribution network.

Accelerated Growth: Provides a strong platform to accelerate growth in high-performance alloys and specialty stainless in North America.

R&D Capabilities: Adds extensive R&D capabilities and a significant patent portfolio, reinforcing Acerinox’s innovation potential.

Haynes’s Perspective:

Significant Premium: Delivers substantial value to Haynes stockholders, offering a premium of approximately 22% to the six-month volume-weighted average share price.

Long-Term Success: Ensures the long-term success of Haynes by validating the strength of the business and providing access to Acerinox’s financial strength and expertise.

Strategic Investment: The $170 million investment in Haynes’ operations supports continued growth in both flat and round products for the global market.

Enhanced Capacity: Positions Haynes to meet dynamic customer demands by increasing manufacturing capacity and offering more differentiated products, applications, and services with faster lead times.

Rich Heritage: Merges Haynes’ 112-year-strong foundation and leadership in high-performance alloys with the largest fully integrated stainless-steel company in the U.S.

Regarding the transaction, Noble Capital Markets Senior Research Analyst Mark Reichman stated, “In our opinion, the transaction provides a fair return for Haynes’ shareholders. Additionally, Acerinox has committed to investing $170 million into Haynes’ operations which will support the modernization and growth of the company’s global business in both flat and round products.” Mark initiated research coverage on Haynes International on February 16, 2023.

The information contained in this article, other than Mark’s quote, was derived from the individual press releases issued by the companies involved in this transaction. This press releases can be found here:

Haynes International (HAYN) is currently covered by Noble Capital Markets Senior Analyst Mark Reichman. Noble Capital Markets, Inc. is a subsidiary of Noble Financial Group, Inc., the parent company of Channelchek. All equity research on Channelchek is provided by Noble Capital Markets. No part of this article was prepared by Noble’s analysts. Please view Mark’s most recent research report on Haynes International for any applicable disclosures.

In a recent interview on “60 Minutes,” Federal Reserve Chair Jerome Powell underscored the central bank’s commitment to a cautious approach regarding interest rate cuts in the upcoming year. Powell emphasized that any rate adjustments would likely unfold at a slower pace than market expectations, signaling a deliberate strategy in response to prevailing economic conditions.

Powell expressed confidence in the current state of the economy, highlighting the need for substantial evidence of sustained inflation movement toward the 2% target before considering rate cuts. He also assured the general public that the upcoming presidential election would not influence the Federal Reserve’s decision-making process.

Powell indicated that the Federal Open Market Committee (FOMC) is unlikely to make its first move, in the form of a rate cut, in March. This statement contrasted with market expectations, which have been making aggressive bets on multiple rate cuts throughout the year.

While market pricing suggests the possibility of five quarter-percentage points reductions, Powell aligned with the FOMC’s December “dot plot,” which indicated three potential moves. This clarification sought to manage expectations and temper speculation surrounding the timing and extent of rate adjustments.

Powell acknowledged that inflation remains above the Fed’s target but has stabilized. The robust job market, with 353,000 non-farm jobs added in January, adds to the Federal Reserve’s positive outlook. Powell identified geopolitical events as the primary risk to the economy.

Following the interview, U.S. stocks experienced a decline, reacting to Powell’s cautious stance on rate cuts. The market had previously seen a week of volatility, concluding with weekly gains driven by a strong January jobs report and positive corporate earnings updates.

Powell addressed public perception of inflation, noting that while the official data may show stability, people are experiencing higher prices for basic necessities. He highlighted the dissatisfaction among the public with the current economic situation despite its overall strength. Powell clarified the distinction between inflation and the absolute price level of goods and services. He explained that people’s dissatisfaction often stems from the rising prices of essential items like bread, milk, eggs, and meats, even though the overall economy is performing well.

Powell acknowledged the challenge in communicating economic concepts to the public, noting the discrepancy between public sentiment and economic indicators. He addressed the professional investing public’s understanding of the rate of change in inflation compared to the general public’s focus on the absolute price level.

Powell’s reaffirmation of a cautious approach to rate cuts serves as a crucial communication strategy to manage market expectations and maintain confidence in the economic outlook. The interview highlighted the Federal Reserve’s commitment to data-driven decisions and its consideration of various economic factors in determining the timing and extent of any potential rate adjustments.

CALGARY, AB, Feb. 1, 2024 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.015 per common share payable on February 29, 2024, to shareholders of record at the close of business on February 15, 2024. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

SOURCE InPlay Oil Corp.

For further information: please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632, www.inplayoil.com; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

Saga Communications, Inc. is a broadcast company whose business is primarily devoted to acquiring, developing and operating radio stations. Saga currently owns or operates broadcast properties in 27 markets, including 79 FM and 33 AM radio stations. Saga’s strategy is to operate top billing radio stations in mid sized markets, defined as markets ranked (by market revenues) from 20 to 200. Saga’s radio stations employ a myriad of programming formats, including Active Rock, Adult Album Alternative, Adult Contemporary, Country, Classic Country, Classic Hits, Classic Rock, Contemporary Hits Radio, News/Talk, Oldies and Urban Contemporary. In operating its stations, Saga concentrates on the development of strong decentralized local management, which is responsible for the day-to-day operations of the stations in their market area and is compensated based on their financial performance as well as other performance factors that are deemed to effect the long-term ability of the stations to achieve financial objectives. Saga began operations in 1986 and became a publicly traded company in December 1992. The stock trades on NASDAQ under the ticker symbol “SGA”.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Highlights from recent NDR. This report provides highlights of a recent Non Deal Road Show to investors in South Florida on January 30th and 31st. Chris Forgy, CEO, and Sam Bush, CFO, reinforced our favorable investment premise for the company.

A lot of headroom for growth. Management appeared sanguine about its revenue growth opportunities given its developing Digital businesses and focus on National, Non Traditional Revenue (Events), and e-commerce revenues. Digital revenue accounts for only 11% of its total revenue giving it a lot of headroom for growth, with some peers as much as 50% of revenue.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

DLH delivers improved health and readiness solutions for federal programs through research, development, and innovative care processes. The Company’s experts in public health, performance evaluation, and health operations solve the complex problems faced by civilian and military customers alike, leveraging digital transformation, artificial intelligence, advanced analytics, cloud-based applications, telehealth systems, and more. With over 2,300 employees dedicated to the idea that “Your Mission is Our Passion,” DLH brings a unique combination of government sector experience, proven methodology, and unwavering commitment to public health to improve the lives of millions. For more information, visit www.DLHcorp.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Waiting on a Budget. The Continuing Resolution continues to hamper DLH’s growth efforts. The Company has plenty of opportunity and stands ready to capitalize on new RFPs. We believe once a budget is passed, there should be a strong flow of new business opportunity for DLH, which will drive organic growth.

1Q24 Bottom Line. The first quarter bottom line was positively impacted by two items. First, due to the CR and bidding opportunities, G&A costs fell to $7.7 million from $10.2 million in 4Q23. G&A costs are likely to remain somewhat muted until a more normal bidding environment emerges. The second was an abnormally low tax rate, 0.5% versus a more typical 25%, due to some discrete items.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Feasibility study expected in the first quarter of 2024. Century’sClayton Valley lithium project is among the most advanced pre-permitted lithium projects in North America with the third largest deposit in the United States. In2023, the company focused on pilot plant operations with the project feasibility study (FS) expected to be complete in the first quarter of 2024. Production will be consistent with the earlier preliminary feasibility study (PFS) although the company is examining the benefits of a phased approach to full scale production.

Feasibility study expectations. While weexpect the feasibility study to reflect higher capital and operating costs, the economics may improve relative to the PFS due to several factors. These include: 1) a higher base case pricing assumption for lithium carbonate equivalent that could be in the range of US$22,000 to US$25,000 per tonne compared to US$9,500 per tonne used in the PFS, 2) a potential economic benefit from the by-product sales of sodium hydroxide, 3) the leaching process will be based on using hydrochloric acid instead of sulfuric acid, and 4) the project will likely incorporate lower cost renewable solar or geothermal power. Based on improvements to the process flowsheet since the publication of the PFS, we expect a compelling feasibility study.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Agreement. On Wednesday, Bit Digital finalized an agreement with Coinmint for 6 megawatts (MW) of incremental hosting capacity to power its miners, with the facility located in Massena, New York. The agreements brings the Company’s total contracted hosting capacity with Coinmint to approximately 46 MW, and has an initial one-year term with automatic three-month renewals.

New Machines. To fill the new capacity, Bit Digital purchased 2,340 S19k Pro mining units for $3.4 million, or approximately $13/TH. These mining units represent approximately 260PH/s with an average efficiency of 23 J/TH. The Company expects the miners to be delivered to the facility and hashing by the end of February 2024. We believe that more hosting agreements and purchases are to follow, given the Company’s goal of doubling its active mining fleet to approximately 6.0EH/s during 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.