FORT WAYNE, Ind., Feb. 08, 2024 (GLOBE NEWSWIRE) — Vera Bradley, Inc. (Nasdaq: VRA) (the “Company”) today announced that it plans to report results for the fourth quarter and fiscal year ended February 3, 2024 at 8:00 a.m. Eastern Time on Wednesday, March 13, 2024.

The Company will host a conference call to discuss its financial results at 9:30 a.m. Eastern Time that same day. A live webcast of the conference call will be available on the Investor Relations section of the Company’s website, www.verabradley.com. Alternatively, interested parties may dial into the call at (877) 407-0779, and enter the access code 13742953. A replay will be available shortly after the conclusion of the call and remain available through March 27, 2024. To access the recording, listeners should dial (844) 512-2921, and enter the access code 13742953.

ABOUT VERA BRADLEY, INC.

Vera Bradley, Inc. operates two unique lifestyle brands – Vera Bradley and Pura Vida. Vera Bradley and Pura Vida are complementary businesses, both with devoted, emotionally connected, and multi-generational female customer bases; alignment as causal, comfortable, affordable, and fun brands; positioning as “gifting” and socially-connected brands; strong, entrepreneurial cultures; a keen focus on community, charity, and social consciousness; multi-channel distribution strategies; and talented leadership teams aligned and committed to the long-term success of their brands.

Vera Bradley, based in Fort Wayne, Indiana, is a leading designer of women’s handbags, luggage and other travel items, fashion and home accessories, and unique gifts. Founded in 1982 by friends Barbara Bradley Baekgaard and Patricia R. Miller, the brand is known for its innovative designs, iconic patterns, and brilliant colors that inspire and connect women unlike any other brand in the global marketplace.

In July 2019, Vera Bradley, Inc. acquired a 75% interest in Creative Genius, Inc., which also operates under the name Pura Vida Bracelets (“Pura Vida”). Pura Vida, based in La Jolla, California, is a digitally native, highly engaging lifestyle brand founded in 2010 by friends Paul Goodman and Griffin Thall. Pura Vida has a differentiated and expanding offering of bracelets, jewelry, and other lifestyle accessories. The Company acquired the remaining 25% of Pura Vida in January 2023.

PONTE VEDRA, Fla., Feb. 8, 2024 — Cadrenal Therapeutics, Inc. (Nasdaq: CVKD), a biopharmaceutical company developing tecarfarin, a novel Vitamin K Antagonist (VKA) for unmet needs in anticoagulation (blood thinning) therapy, today announced the appointment of Jeff Cole to the newly created position of Chief Operating Officer. In this role, Mr. Cole will be responsible for the Company’s manufacturing and supply chain operations, intellectual property, commercialization strategies, and supporting partnering activities for tecarfarin.

Mr. Cole brings over 25 years of experience in global pharmaceutical manufacturing and commercial operations, finance, and corporate development to the Company. This includes senior executive roles at both private and publicly-traded companies such as Espero BioPharma, Valeant Pharmaceuticals International (now Bausch Health Companies), and Legacy Pharmaceuticals. Mr. Cole co-founded Espero, a biopharmaceutical company focusing on the late-stage development and commercialization of medicines to treat cardiovascular diseases, and served as Board Director, President, and Chief Financial Officer where he was responsible for the company’s supply chain, commercialization, and multiple licensing and M&A transactions.

“Jeff is an extremely accomplished pharmaceutical operations executive with a deep understanding of product development, manufacturing, and commercialization. His experience will serve Cadrenal well as we advance our tecarfarin clinical program and evaluate partnering opportunities,” commented Quang Pham, Founder, Chairman and Chief Executive Officer of Cadrenal Therapeutics.

While at Valeant, Mr. Cole held roles of increasing responsibility, including as General Manager, Vice President of Corporate Development, and Chief Financial Officer of North America, where revenue more than tripled during his tenure. As General Manager at Valeant, Mr. Cole managed a division of U.S. prescription and OTC products across multiple therapeutic areas with responsibility for product development, supply, and commercial operations. Prior to the pharmaceutical industry, Mr. Cole served as Principal in the Financial Management Consulting practice at PricewaterhouseCoopers.

“I am excited to be joining the team at Cadrenal at a pivotal time when demand is increasing for a new anticoagulation therapy to address the unmet needs for patients with left ventricular assist devices (LVADs), antiphospholipid syndrome (APS), and those with end-stage kidney disease (ESKD) and atrial fibrillation (AFib),” added Jeff Cole. “I look forward to leveraging my experience to advance tecarfarin to the market and help those underserved patient groups.”

Mr. Cole holds an MBA with honors from the University of Michigan and a BS in accounting from the University of Southern California.

ABOUT CADRENAL THERAPEUTICS, INC.

Cadrenal Therapeutics is developing tecarfarin for unmet needs in anticoagulation therapy. Tecarfarin is a late-stage novel oral and reversible anticoagulant (blood thinner) to prevent heart attacks, strokes, and deaths due to blood clots in patients with certain medical conditions. Tecarfarin has orphan drug and fast track designations from the FDA for the prevention of systemic thromboembolism (blood clots) of cardiac origin in patients with end-stage kidney disease (ESKD) and atrial fibrillation (AFib). Cadrenal is also pursuing additional regulatory strategies for unmet needs in anticoagulation therapy for patients with left ventricular assist devices (LVADs) and those with thrombotic antiphospholipid syndrome (APS). Tecarfarin is specifically designed to leverage a different metabolism pathway than the oldest and most commonly prescribed Vitamin K Antagonist (warfarin). Tecarfarin has been evaluated in eleven (11) human clinical trials and more than 1,000 individuals. In Phase 1, Phase 2, and Phase 2/3 clinical trials, tecarfarin has generally been well-tolerated in both healthy adult subjects and patients with chronic kidney disease. For more information, please visit: www.cadrenal.com.

Safe Harbor Statement

Any statements contained in this press release about future expectations, plans, and prospects, as well as any other statements regarding matters that are not historical facts, may constitute “forward-looking statements.” These statements include statements regarding the Mr. Cole’s experience serving the Company well as it advances its tecarfarin clinical program and evaluates partnering opportunities and leveraging Mr. Cole’s experience to advance tecarfarin to the market and help underserved patient groups. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “target,” “will,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. Actual results may differ materially from those indicated by such forward-looking statements as a result of various important factors, including the expected contribution from Mr. Cole and the ability to advance tecarfarin with patients with left ventricular assist devices (LVADs), thrombotic APS, and those with AFib and ESKD and the other risk factors described in the Company’s Annual Report on Form 10-K for the year ended December 31, 2022, and the Company’s subsequent filings with the SEC, including subsequent periodic reports on Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Any forward-looking statements contained in this press release speak only as of the date hereof and, except as required by federal securities laws, the Company specifically disclaims any obligation to update any forward-looking statement, whether as a result of new information, future events, or otherwise.

For more information, please contact:

Cadrenal Therapeutics: Matthew Szot, CFO 858-337-0766 press@cadrenal.com

Investors: Lytham Partners, LLC Robert Blum, Managing Partner 602-889-9700 CVKD@lythampartners.com

CULVER CITY, Calif., Feb. 08, 2024 (GLOBE NEWSWIRE) — Snail, Inc. (Nasdaq: SNAL) (“Snail” or “the Company”), a leading, global independent developer and publisher of interactive digital entertainment today announced the introduction of game-changing updates to ARK: Survival Ascended’s dev kit, setting the stage for an influx of creativity and customization within the ARK universe.

ARK Survival Ascended’s “Custom Cosmetic” system is a feature that takes player expression to new levels. This innovative update empowers players to apply user-generated costumes to characters and dinosaurs, while also enabling the creation of skins for armor, weapons and all the game’s structures. Beyond the aesthetic appeal, this system introduces new functionalities, including network messaging and limited persistent replicated data storage. The introduction of this system allows for visual variety and functional enhancement through player-created cosmetics, all achieved seamlessly without the need for server updates or loading onto a server. In early February 2024, phase 1 of the system will be activated, allowing players to manually install Custom Cosmetic Mods, unlocking a realm of creative expression on Official Servers. Ultimately, Custom Cosmetic Mods will be automatically downloaded in the background when encountered during gameplay; this automatic download feature is set to go live Q2 2024.

As a glimpse into the creative potential of the dev kit update, Snail Games, Studio Wild Card, and OverWolf offered a sneak peek into “Super ARK Bros,” a two-player side-scroller example mod set to be released early February. This work-in-progress showcases a simple game framework, independent of ARK: Survival Ascended’s gameplay code. This serves as an example of how creators will be able to utilize Unreal Engine 5 to craft their own unique games, with the freedom to make as many or as few changes as they desire, all of which can be released on ARK Survival Ascended.

But that’s not all. In celebration of love, Snail Games is delighted to announce that this year’s “Love Evolved” Valentine’s Day event, will become a permanent fixture as a mod within ARK: Survival Ascended. Survivors can feel the love in the air whenever they desire!

“These updates mark a pivotal moment in the evolution of ARK: Survival Ascended,” says Jim Tsai, Chief Executive Officer of Snail, Inc. “The introduction of the Custom Cosmetic system and the simple game framework on the ARK SDK represent our unwavering commitment to providing continuous support to our modding community. We can’t wait to witness the incredible creations our community will bring to life.”

Snail Games invites players to embrace these transformative changes and anticipates a dynamic and vibrant future for user generated content in ARK: Survival Ascended.

About Snail, Inc.

Snail is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs and mobile devices.

Forward-Looking Statements

This press release contains statements that constitute forward-looking statements. Many of the forward-looking statements contained in this press release can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “may,” “predict,” “continue,” “estimate” and “potential,” or the negative of these terms or other similar expressions. Forward-looking statements appear in a number of places in this press release and include, but are not limited to, statements regarding Snail’s intent, belief or current expectations. These forward-looking statements include information about possible or assumed future results of Snail’s business, financial condition, results of operations, liquidity, plans and objectives. The statements Snail makes regarding the following matters are forward-looking by their nature: growth prospects and strategies; launching new games and additional functionality to games that are commercially successful, including the launch of ARK: Survival Ascended, ARK: The Animated Series and ARK 2; expectations regarding significant drivers of future growth; its ability to retain and increase its player base and develop new video games and enhance existing games; competition from companies in a number of industries, including other game developers and publishers and both large and small, public and private Internet companies; its relationships with third-party platforms such as Xbox Live and Game Pass, PlayStation Network, Steam, Epic Games Store, the Apple App Store, the Google Play Store, My Nintendo Store and the Amazon Appstore; expectations for future growth and performance; and assumptions underlying any of the foregoing.

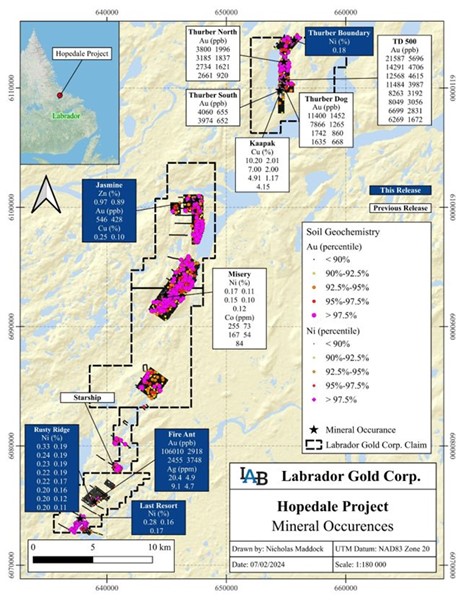

TORONTO, Feb. 08, 2024 (GLOBE NEWSWIRE) — Labrador Gold Corp. (TSX.V:LAB | OTCQX:NKOSF | FNR: 2N6) (“LabGold” or the “Company”) is pleased to announce the results of the 2023 exploration program at its 100% owned Hopedale Project in Labrador. The district scale Hopedale property covers a 43km strike length of the Florence Lake greenstone belt which has characteristics typical of greenstone belts around the world but has been underexplored by comparison.

Highlights

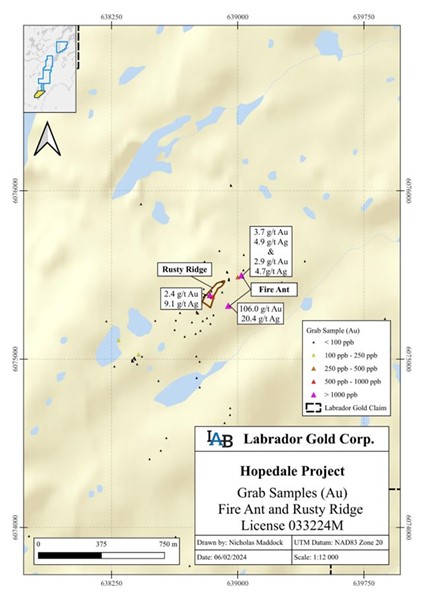

Fire Ant gold occurrence

high-grade gold up to 106g/t with 20.4g/t Ag in rock grab samples

mineralization traced over approximately 200 metres strike length

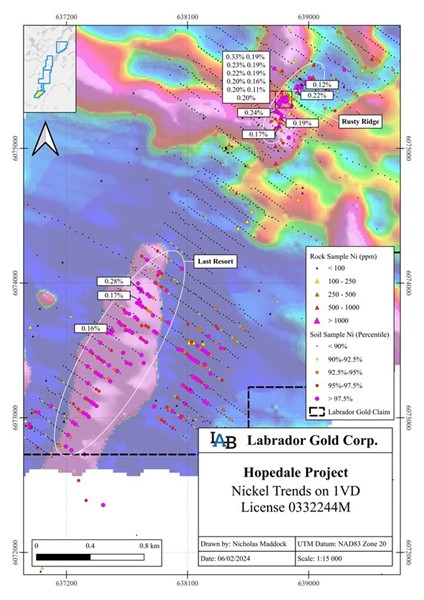

Rusty Ridge and Last Resort nickel occurrences

anomalous Ni area at Rusty Ridge extended to 550m

rock samples up to 0.28% Ni and soil samples up to 0.23% Ni

Identified a new anomalous nickel area (Last Resort) over a strike length of 1.6km coincident with a significant magnetic high

Jasmine zinc occurrence

anomalous zinc zone identified over 400m at Jasmine with values up to 0.97% Zn in rock and 0.22% in soil

Jasmine also shows high copper and gold values indicating potential for volcanogenic style mineralization

Thurber Boundary copper occurrence

highest copper in soil value (3,493 ppm) found on the property to date identified in a 400m anomalous trend

Eight occurrences identified on the Hopedale project to date reflecting multiple mineralization styles including orogenic gold, magmatic Ni sulphide, copper-silver vein and Zn-rich volcanogenic massive sulphide

Significant gold and silver in rock grab samples was found in the Rusty Ridge area with a high of 106g/t Au and 20.4 g/t Ag, 3.7g/t Au and 4.9g/t Ag and 2.9g/t Au and 4.7g/t Ag. This newly discovered mineralization named the Fire Ant occurrence, is hosted in gossanous felsic volcanic rocks close to the contact with ultramafic volcanic rocks and has been traced over a strike length of approximately 200 metres.

Work during 2022 found significant nickel anomalies in soil and rock at an area named Rusty Ridge. The anomalies occur in ultramafic rocks indicating potential for magmatic nickel style mineralization. One of the goals of the 2023 exploration program was to follow up and extend these anomalies. A total of 14 grab samples of rock assayed over 0.1% Ni and included values up to 0.28% Ni while nickel values in soil up to 2,271ppm (0.23%) show a significant northeast-southwest trend extending the anomalous area over 550m. Approximately 1.2km south of Rusty Ridge, anomalous nickel in soil samples was outlined over a 1.6km strike length and is coincident with a significant magnetic high. Six of the samples assayed over 1,000ppm (0.1%) Ni with a high of 2,271ppm (0.23%) Ni. Limited rock sampling showed assays of 0.28%, 0.17% and 0.16% Ni in grab samples in this area named Last Resort.

The highest copper value in soil (3,493ppm) on the property to date was recorded at Thurber Boundary, where it forms a northeast-southwest trend over approximately 500 metres. The location of the soil anomaly is in a similar stratigraphic location, close to the contact of mafic and ultramafic volcanic rocks, as the high grade (3.31% Cu over 0.76m and 1.55% Cu over 1m in channel samples) Kaapak copper occurrence approximately 3 kilometres to the south.

In addition to the copper, nickel and gold found during the exploration program, anomalous zinc was found in soil samples (up to 0.22%) and rock (up to 0.97%) in the Jasmine area. The anomalous zone extends over approximately 400 metres and is coincident with a contact highlighted by a change from magnetic high to magnetic low. The Jasmine area is also known to have high copper and gold values indicating potential for volcanogenic massive sulphide deposits.

“Our 2023 exploration program over the district scale Hopedale property confirmed the significant prospectivity of the Rusty Ridge area for nickel associated with ultramafic rocks and identified a new area, Last Resort, with similar potential for magmatic sulphide type mineralization,” said Roger Moss, President and CEO of Labrador Gold. “The highest grade gold found on the property to date, 106g/t Au and 20.4g/t Ag, was sampled at a new occurrence, Fire Ant, in the Rusty Ridge area and brings the number of significant gold occurrences on the property to five. Potential for zinc-rich volcanogenic massive sulphide was identified at Jasmine as well as a significant copper in soil anomaly at Thurber Boundary. Work conducted by LabGold at Hopedale demonstrates that the Florence Lake greenstone belt contains many of the same mineralization styles seen in some of the most productive greenstone belts elsewhere in the world.”

Figure 1. Location of the nickel, copper, gold and zinc occurrences on the Hopedale Property.

Figure 2. Highlights of nickel in soil and rock samples over Rusty Ridge and Last Resort Occurrences.

Figure 3. Location of high-grade gold mineralization at Fire Ant occurrence.

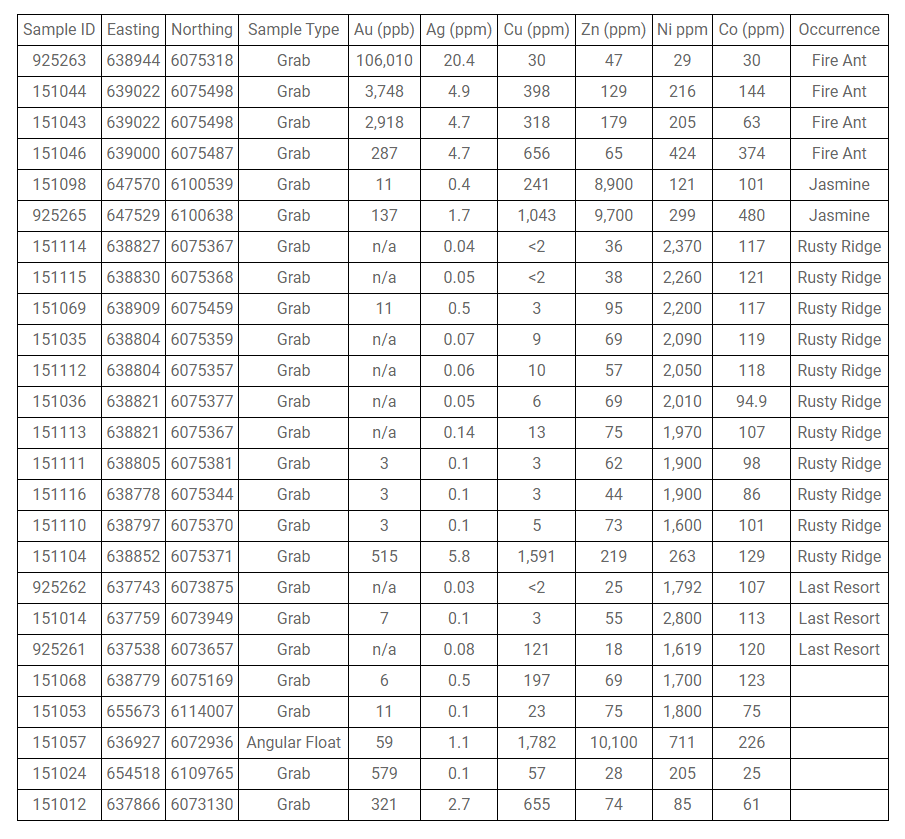

Table 1. Highlights of rock samples assays from 2023 exploration program. Note that grab samples are selective samples and may not be representative of the mineralization found on the property. n/a = not assayed.

QA/QC

Rock samples comprise grab samples, which are selective samples and not necessarily representative of mineralization found on the property. Samples were securely stored prior to shipping to analytical labs for assay. Rock samples were assayed at Eastern Analytical Laboratory in Springdale, an ISO/IEC17025 accredited laboratory for gold by standard 30g fire assay with atomic absorption finish as well as by ICP-OES for an additional 34 elements. Additional samples were sent to SGS Canada for whole rock assays by borate fusion XRF and ICP-MS/AES. Soil samples were submitted to SGS for gold by standard 30g fire assay with atomic absorption finish as well as ICP-MS for an additional 48 elements. The company submits blanks and certified reference standards amounting to 5% of each sample batch.

Qualified Person

Roger Moss, PhD., P.Geo., President and CEO of LabGold, a Qualified Person in accordance with Canadian regulatory requirements as set out in NI 43-101, has read and approved the scientific and technical information that forms the basis for the disclosure contained in this release.

The Company gratefully acknowledges the Newfoundland and Labrador Ministry of Natural Resources’ 2023 Junior Exploration Assistance (JEA) Program and the Atlantic Canada Opportunities Agency’s Critical Minerals Assistance for its financial support for exploration of the Hopedale property.

About Labrador Gold Labrador Gold is a Canadian based mineral exploration company focused on the acquisition and exploration of prospective gold projects in Eastern Canada.

Labrador Gold’s flagship property is the 100% owned Kingsway project in the Gander area of Newfoundland. The four licenses comprising the Kingsway project cover approximately 12km of the Appleton Fault Zone which is associated with numerous gold occurrences in the region. Infrastructure in the area is excellent located just 18km from the town of Gander with road access to the project, nearby electricity and abundant local water. LabGold is drilling a projected 100,000 metres targeting high-grade epizonal gold mineralization along the Appleton Fault Zone with encouraging results.

The Hopedale property covers much of the Florence Lake greenstone belt that stretches over 60 km. The belt is typical of greenstone belts around the world but has been underexplored by comparison. Work to date by Labrador Gold show gold anomalies in rocks, soils and lake sediments over a 3 kilometre section of the northern portion of the Florence Lake greenstone belt. Four gold occurrences lie along this trend, three of which Thurber North, TD500 and Thurber South were discovered by LabGold. Anomalous gold in soil and lake sediment samples also occur over approximately 40 km along the southern section of the greenstone belt. LabGold’s recent exploration has also demonstrated the potential for the critical metals copper, nickel and cobalt in the belt.

The Company has 170,009,979 common shares issued and outstanding and trades on the TSX Venture Exchange under the symbol LAB.

For more information please contact: Roger Moss, President and CEO Tel: 416-704-8291

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release .

Forward-Looking Statements: This news release contains forward-looking statements that involve risks and uncertainties, which may cause actual results to differ materially from the statements made. When used in this document, the words “may”, “would”, “could”, “will”, “intend”, “plan”, “anticipate”, “believe”, “estimate”, “expect” and similar expressions are intended to identify forward-looking statements. Such statements reflect our current views with respect to future events and are subject to risks and uncertainties. Many factors could cause our actual results to differ materially from the statements made, including those factors discussed in filings made by us with the Canadian securities regulatory authorities. Should one or more of these risks and uncertainties, such as actual results of current exploration programs, the general risks associated with the mining industry, the price of gold and other metals, currency and interest rate fluctuations, increased competition and general economic and market factors, occur or should assumptions underlying the forward looking statements prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, or expected. We do not intend and do not assume any obligation to update these forward-looking statements, except as required by law. Shareholders are cautioned not to put undue reliance on such forward-looking statements .

Conference Call to be held Thursday, February 29 at 8:00 a.m. Central Time

HOUSTON, Feb. 08, 2024 (GLOBE NEWSWIRE) — Orion Group Holdings, Inc. (NYSE: ORN) (the “Company”), a leading specialty construction company, today announced that it will issue its financial results for the fourth quarter and full year ended December 31, 2023, on Wednesday, February 28, 2024, after the close of the stock market.

A conference call and audio webcast with analysts and investors will be held the next day, February 29, at 8:00 a.m. Central Time/9:00 a.m Eastern Time to discuss the results and answer questions.

Orion Group Holdings, Inc., a leading specialty construction company serving the infrastructure, industrial and building sectors, provides services both on and off the water in the continental United States, Alaska, Hawaii, Canada and the Caribbean Basin through its marine segment and its concrete segment. The Company’s marine segment provides construction and dredging services relating to marine transportation facility construction, marine pipeline construction, marine environmental structures, dredging of waterways, channels and ports, environmental dredging, design, and specialty services. Its concrete segment provides turnkey concrete construction services including place and finish, site prep, layout, forming, and rebar placement for large commercial, structural and other associated business areas. The Company is headquartered in Houston, Texas with regional offices strategically located across its operating areas. (oriongroupholdingsinc.com)

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

A proposed new sports streaming service. The Walt Disney Company, Fox Corporation, and Warner Bros. Discovery announced that it plans to launch a new live sports streaming service in the fall 2024. The new service is expected to be offered directly to consumers through an app on a subscription basis.

A lot to work out. There are a number of variables that need to be worked out, including the pricing of the new services. Recent media reports have the streaming service priced at a hefty $40 per month. The app will not include all sports programming and is expected to target sports fans that do not subscribe to a pay-TV package. As such, there will be a limited audience and could even help to expand the reach of local TV stations.

An over-reaction? Television stocks, including our current covered companies, E.W. Scripps (SSP) and Gray Television (GTN) dropped 24% and 15%, respectively. Investors seem to expect that the new service will be a threat to the companies’ retransmission revenue. And, in the case of Scripps, investors may believe that the new potential service will be in competition of Scripps’ Sports strategy.

Impact on Retrans revenue? The service could accelerate cable subscriber declines, but cord cutters likely will subscribe to a virtual service or connected TV for local channels. Such a move would be neutral to TV broadcasters given that broadcasters are paid Retrans on these platforms as well. In terms of Scripps Sports, we believe that it likely will not affect its local sports strategy and that it could offer opportunities for partnerships on it national sports strategy.

Compelling opportunity. We believe that the sell-off in TV stocks is over done. There appears to be a favorable risk/reward relationship for an industry cycling into an improving fundamental story in 2024, with the influx of high margin Political advertising, a swing toward favorable Retrans revenue growth, lowered debt leverage, and compelling stock valuations. Our favorites are E.W. Scripps and Gray Television. Please see our recent reports on SSP and GTN for stock valuations, ratings, price targets and important disclosure information.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Publication Shows Multiple Activities of THIO In SCLC. MAIA announced the publication of an article in the peer-reviewed journal Nature Communications that discusses the dual mechanism of action and effects of THIO in small cell lung cancer (SCLC). This is another tumor type in which THIO has been shown to have direct killing effects on cancer cells and activation the cGAS-STING signaling pathway that leads to an immune response. We see this as consistent with previous data confirming THIO benefits.

MAIA Is Developing THIO For Both Major Lung Cancers. Out of all lung cancer cases, non-small cell lung cancer (NSCLC) comprises about 87% while small cell (SCLC) comprises about 13%. Although less common than NSCLC, SCLC is highly aggressive and highly metastatic. SCLC cells have high telomerase activity that enables their high proliferation rate and immortality. MAIA has received Orphan drug designation from the FDA for SCLC, while the Phase 2 THIO-101 trial is testing THIO in NSCLC.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Results. Fourth quarter revenue totaled $491.2 million, up from $471.4 million last year and in-line with our $495 million projection. Adjusted EBITDA for the quarter was $90 million, compared to $87.7 million last year and our $82 million estimate. CXW reported adjusted net income of $26.4 million and adjusted EPS of $0.23, beating our estimates of $17.5 million and $0.18, respectively, and improving from $25 million and $0.22 last year.

Strong Business Momentum. The better than expected results were driven by ongoing population and resulting occupancy increases. CoreCivic ended the year at 74% occupancy, the highest quarterly level since 2Q20. Labor availability and wage inflation are normalizing, resulting in improving margins. We expect these trends to continue in 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The biggest publicly traded oil companies in the West had a clear message for investors this earnings season: We’re going to keep paying you billions in dividends and stock buybacks, no matter how much our profits fluctuate.

BP, Chevron, ExxonMobil, Shell and TotalEnergies doled out over $111 billion to shareholders in 2023, an all-time record for the group, according to a Reuters analysis. This lavish payout comes even as the companies’ combined net profits sank 37% from 2022’s windfall heights of $196 billion.

It’s a calculated move to reassure investors, particularly major institutional shareholders like pension funds, that the oil supermajors still deserve a place in their portfolios despite LAST year’s stark reminder of the sector’s persistent volatility.

For over a decade, Big Oil has seen its status as a stalwart, dividend-paying pillar of investors’ portfolios slowly erode. The energy sector’s weighting in the S&P 500 index sat at just 4.4% in January, down dramatically from 14% in 2012.

Several factors catalyzed this decline: poor capital discipline leading to wasted spending and subsequent dividend cuts, huge swings in oil and gas prices, the rise of the tech sector, and growing concerns about oil’s role in climate change.

But Russia’s invasion of Ukraine in 2023 sparked an unexpected fossil fuel rally, with Brent crude prices averaging over $100 per barrel and natural gas prices skyrocketing. The oil giants cashed in with their highest profits ever, starkly highlighting the sector’s persistent upside potential.

Now with economic headwinds buffeting energy markets, their mammoth payouts to shareholders seek to underscore oil’s reliability versus more speculative investments. “During a time of geopolitical turmoil and economic uncertainty, our objective remained unchanged: safely deliver higher returns and lower carbon,” said Chevron CEO Mike Wirth after announcing a 6% dividend increase.

Besides dividends, oil majors are channeling these record buybacks to shareholders. Exxon Mobil alone spent $35 billion last year snapping up its own shares, while Shell has vowed “complete predictability” around shareholder returns.

This focus on payouts over production indicates Big Oil has absorbed the lessons of overspending on large-scale projects with uncertain demand outlooks. After former CEO John Browne spearheaded a failed push for aggressive growth at BP, lease write-downs of $60 billion soon followed.

Now with the transition to cleaner energy casting further uncertainty over long-term oil demand, companies are tightly rationing investment. Bernstein analyst Oswald Clint said investors “absolutely remember the sins of the past investment cycles and are pretty determined not to repeat those.”

While Exxon and Chevron are still expanding oil output, others like BP and Shell plan to cut production over this decade as part of their climate strategies. But all are aligning around far greater capital discipline and what they call “high-grading” their portfolios.

Rather than chasing growth, new projects must meet stricter hurdles for returns, emissions, and regulations. Tobias Wagner of Moody’s Investors Service expects only minimal investment increases industry-wide in 2024 given the cautious outlook.

So even as society decarbonizes, the oil supermajors are making a case that their stocks can still reward shareholders through the transition. Yet it remains to be seen whether investors who have fled the sector for greener pastures like clean energy and tech will find these guarantees compelling enough to return.

General Motors (GM) announced Wednesday its largest investment yet to lock up critical raw materials needed for its ambitious electric vehicle (EV) production plans. The Detroit automaker said it will spend $19 billion over the next decade to source cathode materials from South Korean supplier LG Chem.

The materials—including nickel, cobalt, manganese and aluminum—are key ingredients for the lithium-ion batteries that power EVs. Under the agreement spanning 2026-2035, LG Chem will ship over 500,000 tons of cathode materials to GM’s joint battery cell plants with LG spinoff Ultium Cells in the United States.

GM stated this is enough supply for approximately 5 million EVs with an estimated range of over 300 miles per charge. The materials will come from an LG Chem plant currently under construction in Tennessee.

For GM, signing a long-term purchase agreement helps mitigate risks around securing sufficient future EV battery supplies amid intensifying competition. As automakers collectively invest billions to shift their lineups to mostly EVs by 2030, critical mineral shortages could constrain production plans.

“This contract builds on GM’s commitment to create a strong, sustainable battery EV supply chain to support our fast-growing EV production needs,” said Jeff Morrison, GM vice president of global purchasing and supply chain.

The LG Chem deal ranks among the largest—if not the largest—EV supply contract inked by GM to date. It highlights an urgency by the company to lock up raw materials as the global auto industry accelerates its electric shift. GM aspires to exclusively sell EVs by 2035.

However, the 14-year LG Chem agreement also implies GM may be adapting its EV strategy to account for adoption happening slower than anticipated. The original pact was scheduled to expire in 2030, but GM extended it another five years.

After initially forecasting aggressive EV sales growth, GM has pulled back on targets amid steeping battery costs and strained consumer budgets. “We’re also being a little bit prudent about the pace at which the transition occurs,” said CEO Mary Barra.

Nonetheless, GM remains laser-focused on its EV future. It recently announced a $650 million investment to expand production of its profitable full-size SUVs—but as electric versions only by 2024. “We have the manufacturing flexibility to build EVs at scale,” said Barra.

For investors, GM’s major bet on EVs represents an opportunity to capitalize on the immense growth projected in the electric vehicle market over the next decade. Research firm IDTechEx forecasts the EV market will balloon from $287 billion in 2021 to over $1.3 trillion by 2031 as adoption accelerates globally. GM’s plan to phase out gas-powered cars and transition to an all-electric lineup positions it as a leading EV player in this booming new automotive era.

Meanwhile, LG Chem said it aims to “bolster cooperation with GM in the North American market” through the expanded cathode materials agreement. The supplier has jockeyed with China’s CATL for the title of world’s top EV battery maker.

For both LG and GM, ensuring cathode supply security with a US-based plant mitigates geopolitical risks. President Biden’s Inflation Reduction Act requires automakers to source critical minerals domestically or from allies to qualify for EV tax credits.

While the road to an all-electric future remains bumpy, GM’s huge bet on sourcing vital battery ingredients shows its commitment to phasing out the internal combustion engine. As Barra stated, “We’re on our way to an all-electric portfolio.”

Bitcoin Depot Plans to Install Bitcoin ATMs in Locations Across the US South

ATLANTA, Feb. 07, 2024 (GLOBE NEWSWIRE) — Bitcoin Depot Inc. (“Bitcoin Depot” or the “Company”) (NASDAQ: BTM), a U.S.-based Bitcoin ATM operator and leading fintech company, today announced a retail partnership with a leading operator of convenience stores in the U.S.

Bitcoin Depot plans to install its BTMs in an additional 63 stores across multiple metropolitan areas, strengthening Bitcoin Depot’s retail footprint. This partnership augments Bitcoin Depot’s comprehensive growth plan, which focuses on increasing its BTM network and continuing to build a robust pipeline of major regional and national retail partners. Last month, the Company announced an additional partnership that includes a deployment of nearly 1,000 BTMs nationally.

“This expansion aligns with our commitment to bringing Bitcoin to the masses,” said Bitcoin Depot CEO Brandon Mintz. “Our goal is to bring easy and convenient crypto access to a plethora of communities while creating unmatched value for our retail partners and welcoming new customers.”

This expansion allows Bitcoin Depot customers to purchase Bitcoin in easy and accessible c-store locations across the South where a variety of additional amenities are available. As part of the partnership, additional Bitcoin Depot’s kiosks will now be available in the following states including Alabama, Arkansas, Arizona, Florida, Georgia, Illinois, Kansas, Kentucky, Louisiana, Maine, Michigan, North Carolina, Mississippi, Ohio, Pennsylvania, South Carolina, Tennessee, Texas, Virginia, and West Virginia.

Bitcoin Depot’s products and services provide an intuitive, quick, and convenient process for converting cash into Bitcoin, giving users the ability to access the broader digital financial system by conveniently purchasing Bitcoin at Bitcoin ATMs in 48 states. In addition to Bitcoin ATMs, Bitcoin Depot also has BDCheckout enabled for customers to fund their wallets with cash at participating retail locations in 28 states nationwide.

About Bitcoin Depot Bitcoin Depot Inc. (Nasdaq: BTM) was founded in 2016 with the mission to connect those who prefer to use cash to the broader, digital financial system. Bitcoin Depot provides its users with simple, efficient and intuitive means of converting cash into Bitcoin, which users can deploy in the payments, spending and investing space. Users can convert cash to bitcoin at Bitcoin Depot kiosks in 48 states and at thousands of name-brand retail locations in 29 states through its BDCheckout product. The Company has the largest market share in North America with approximately 6,400 kiosk locations as of September 30, 2023. Learn more at www.bitcoindepot.com

Contacts:

Investors Cody Slach, Alex Kovtun Gateway Group 949-574-3860 btm@gateway-grp.com

Media Christina Lockwood, Brenlyn Motlagh, Ryan Deloney Gateway Group 949-574-3860 btm@gateway-grp.com

THIO treatment leads to profound activation of innate and adaptive anti-tumor responses

THIO depletes cancer initiating cells (CICs) and thus diminishes tumor initiation and metastasis-forming potential in various in vivo models

THIO previously awarded orphan drug designation (ODD) by FDA for small cell lung cancer (SCLC) treatment

CHICAGO–(BUSINESS WIRE)– MAIA Biotechnology, Inc., (NYSE American: MAIA) (“MAIA”, the “Company”), a clinical-stage biopharmaceutical company developing targeted immunotherapies for cancer, today announced the publication of extensive work describing preclinical studies for lead candidate THIO in small cell lung cancer (SCLC) in the peer-reviewed scientific journal Nature Communications. The reported findings from the research, conducted in collaboration with the University of Texas Southwestern (UTSW) scientists, led by corresponding author Dr. Esra Akbay, demonstrate the immune-enhancing, metastasis-reducing effects of MAIA’s telomere-targeting agent THIO (6TdG) in several well-characterized in vitro and in vivo models of SCLC.

“This publication highlights a rather unique dual mechanism of action for THIO as a first-in-clinic telomere-targeted anticancer agent for potential treatment of SCLC,” said Sergei M. Gryaznov, PhD., MAIA’s Chief Scientific Officer. “In addition to the direct and potent cancer cell depletion activity, the observed specific interferons stimulation, immune responses-enhancement, and metastasis-reducing effects of THIO provide solid scientific foundation for further advancement of this compound in clinical development.”

A prominent characteristic of lung cancer small cells is their reliance on telomerase activity, a key enzyme essential for the continuous proliferation of SCLC. While 85-90% of all human cancers are telomerase positive, SCLCs are nearly all telomerase positive1, suggesting that telomerase targeting may be an effective strategy in the treatment of SCLC.

Key findings in the published paper include:

Human and mouse SCLC lines are sensitive to THIO (6TdG) treatment in vitro and in vivo

THIO decreases cancer initiating cells and diminishes tumor initiation potential in vitro and in vivo

Low doses of THIO are effective in treating metastatic mouse SCLC tumors

THIO activates type-I interferon pathway through cGAS-STING signaling

THIO is highly effective in combination with ionizing radiation treatment regiments

“With few, if any, effective treatments for small cell lung cancer, there is a widespread need for innovative therapeutic strategies. The positive outcomes reported in our publication show THIO’s potential as a new therapeutic approach,” said Vlad Vitoc, M.D., MAIA’s Chairman and Chief Executive Officer. “THIO already holds Orphan Drug Designation for SCLC, underscoring the FDA’s recognition of THIO’s potential to improve outcomes for this highly lethal disease. With the positive preclinical and clinical data we have obtained to date for THIO, we have entered the Phase 2 planning stage for a clinical trial of THIO in SCLC along with two other cancers.”

Orphan Products Development grants orphan designation status to drugs and biologics that are intended for the treatment, diagnosis or prevention of rare diseases, or conditions that affect fewer than 200,000 people in the U.S. Orphan Drug Designation provides certain benefits, including financial incentives, to support clinical development and the potential for up to seven years of market exclusivity for the drug for the designated orphan indication in the U.S. if the drug is ultimately approved for its designated indication.

About the Publication

Nature Communications, volume 15, article number: 672 (2024), “A telomere-targeting drug depletes cancer initiating cells and promotes anti-tumor immunity in small cell lung cancer,” published 22 January 2024. Co-author disclosures included in manuscript.

About Small Cell Lung Cancer

Small cell lung cancer (SCLC) accounts for 13% of lung cancers. As the deadliest of all lung cancers, SCLC is one of the leading causes of cancer-related mortality in United States with 30,000 deaths annually. It is less common than non-small cell lung cancer (NSCLC), but is more aggressive and rapidly spreads (metastasizes) throughout the body.

About THIO

THIO (6-thio-dG or 6-thio-2’-deoxyguanosine) is a first-in-class investigational telomere-targeting agent currently in clinical development to evaluate its activity in Non-Small Cell Lung Cancer (NSCLC). Telomeres, along with the enzyme telomerase, play a fundamental role in the survival of cancer cells and their resistance to current therapies. The modified nucleoside 6-thio-2’-deoxyguanosine (THIO) induces telomerase-dependent telomeric DNA modification, DNA damage responses, and selective cancer cell death. THIO-damaged telomeric fragments accumulate in cytosolic micronuclei activating both innate (cGAS/STING) and adaptive (T-cell) immune responses. The sequential treatment with THIO followed by PD-(L)1 inhibitors resulted in profound and persistent tumor regression in advanced, in vivo cancer models by induction of cancer type–specific immune memory. THIO is presently developed as a second or later line of treatment for NSCLC for patients that have progressed beyond the standard-of-care regimen of existing checkpoint inhibitors.

About MAIA Biotechnology, Inc.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Forward Looking Statements

MAIA cautions that all statements, other than statements of historical facts contained in this press release, are forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels or activity, performance or achievements to be materially different from those anticipated by such statements. The use of words such as “may,” “might,” “will,” “should,” “could,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “project,” “intend,” “future,” “potential,” or “continue,” and other similar expressions are intended to identify forward looking statements. However, the absence of these words does not mean that statements are not forward-looking. For example, all statements we make regarding (i) the initiation, timing, cost, progress and results of our preclinical and clinical studies and our research and development programs, (ii) our ability to advance product candidates into, and successfully complete, clinical studies, (iii) the timing or likelihood of regulatory filings and approvals, (iv) our ability to develop, manufacture and commercialize our product candidates and to improve the manufacturing process, (v) the rate and degree of market acceptance of our product candidates, (vi) the size and growth potential of the markets for our product candidates and our ability to serve those markets, and (vii) our expectations regarding our ability to obtain and maintain intellectual property protection for our product candidates, are forward looking. All forward-looking statements are based on current estimates, assumptions and expectations by our management that, although we believe to be reasonable, are inherently uncertain. Any forward-looking statement expressing an expectation or belief as to future events is expressed in good faith and believed to be reasonable at the time such forward-looking statement is made. However, these statements are not guarantees of future events and are subject to risks and uncertainties and other factors beyond our control that may cause actual results to differ materially from those expressed in any forward-looking statement. Any forward-looking statement speaks only as of the date on which it was made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. In this release, unless the context requires otherwise, “MAIA,” “Company,” “we,” “our,” and “us” refers to MAIA Biotechnology, Inc. and its subsidiaries.

_________________________________ 1 Hiyama, K. et al. Telomerase activity in small-cell and non-small-cell lung cancers. J Natl Cancer Inst 87, 895-902, doi:10.1093/jnci/87.12.895 (1995).

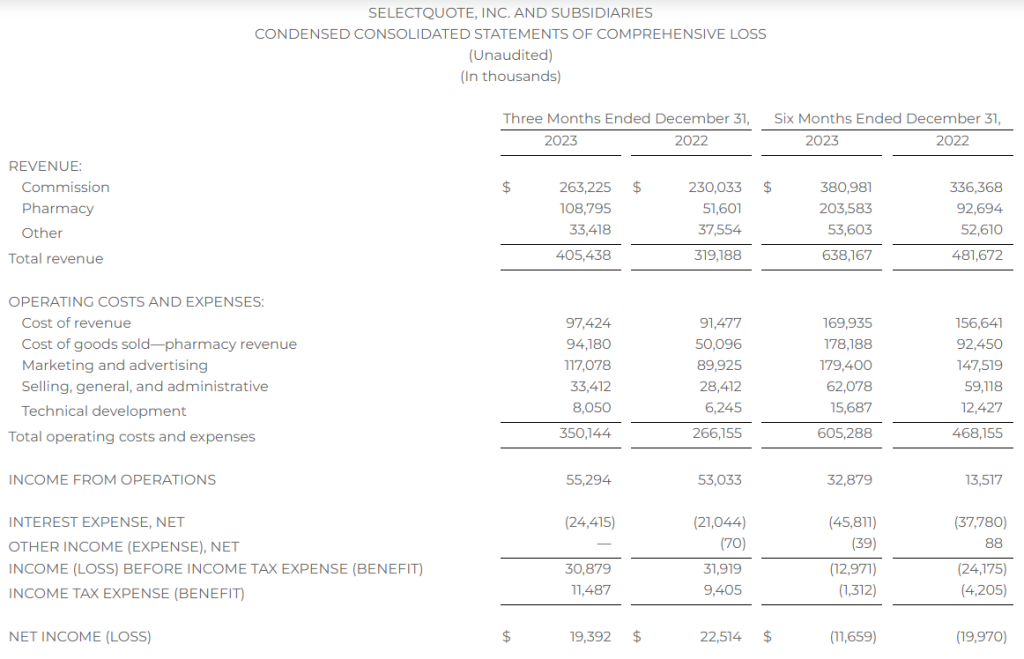

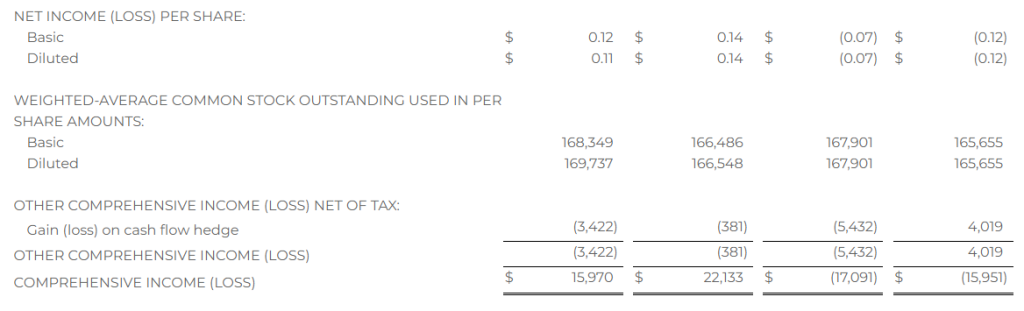

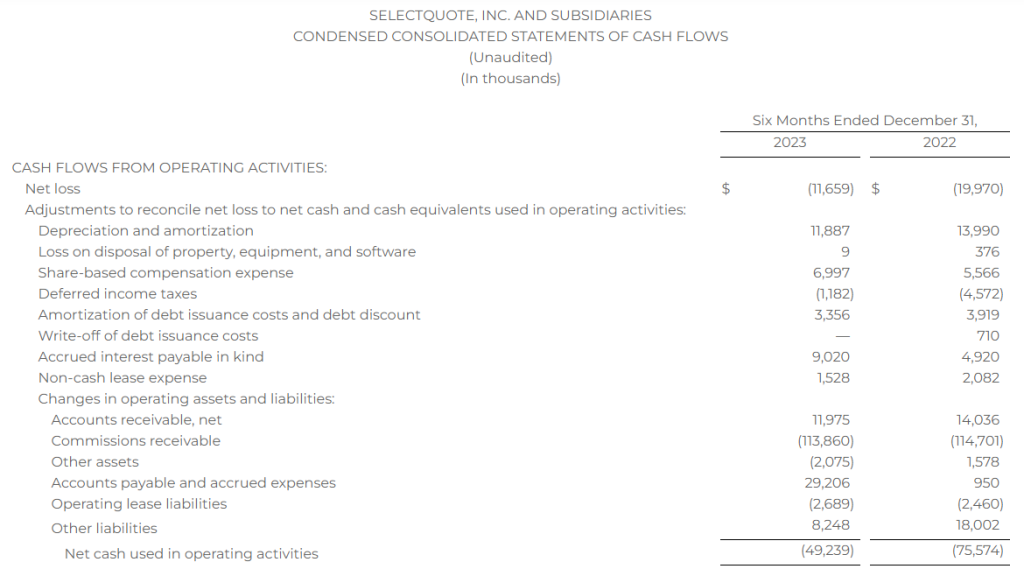

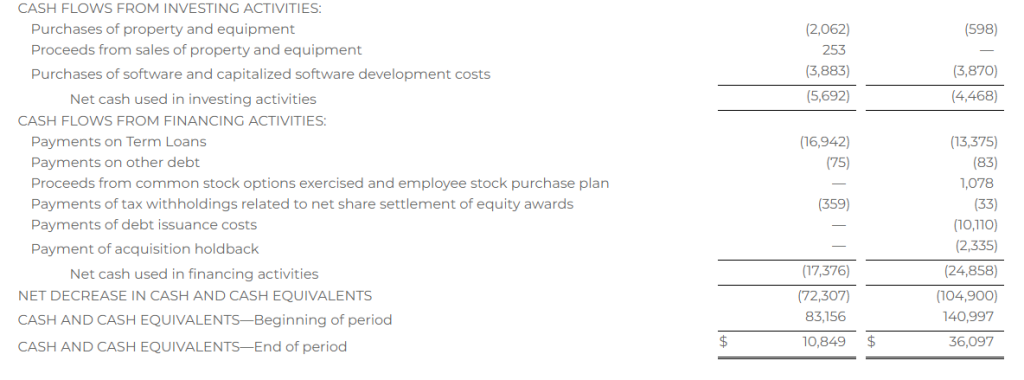

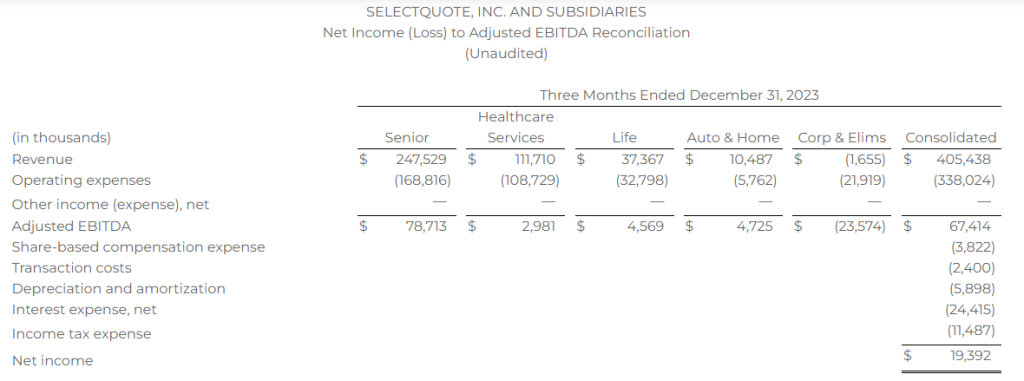

Second Quarter of Fiscal Year 2024 – Consolidated Earnings Highlights

Revenue of $405.4 million

Net income of $19.4 million

Adjusted EBITDA* of $67.4 million

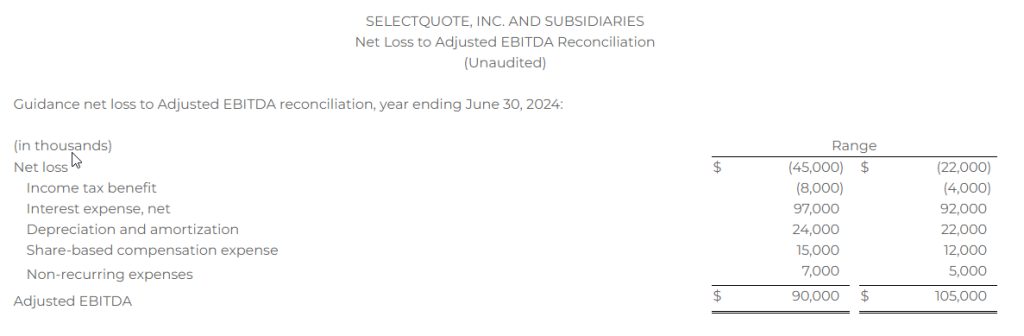

Raising Fiscal Year 2024 Guidance Ranges:

Revenue expected in a range of $1.23 billion to $1.3 billion vs prior range of $1.05 billion to $1.2 billion

Net loss expected in a range of $45 million to $22 million vs prior range of $50 million to $22 million

Adjusted EBITDA* expected in a range of $90 million to $105 million vs prior range of $80 million to $105 million

Second Quarter of Fiscal Year 2024 – Segment Highlights

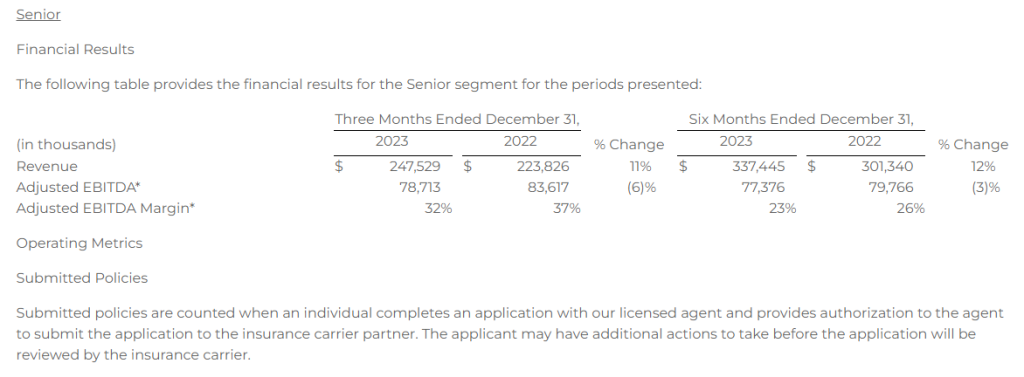

Senior

Revenue of $247.5 million

Adjusted EBITDA* of $78.7 million

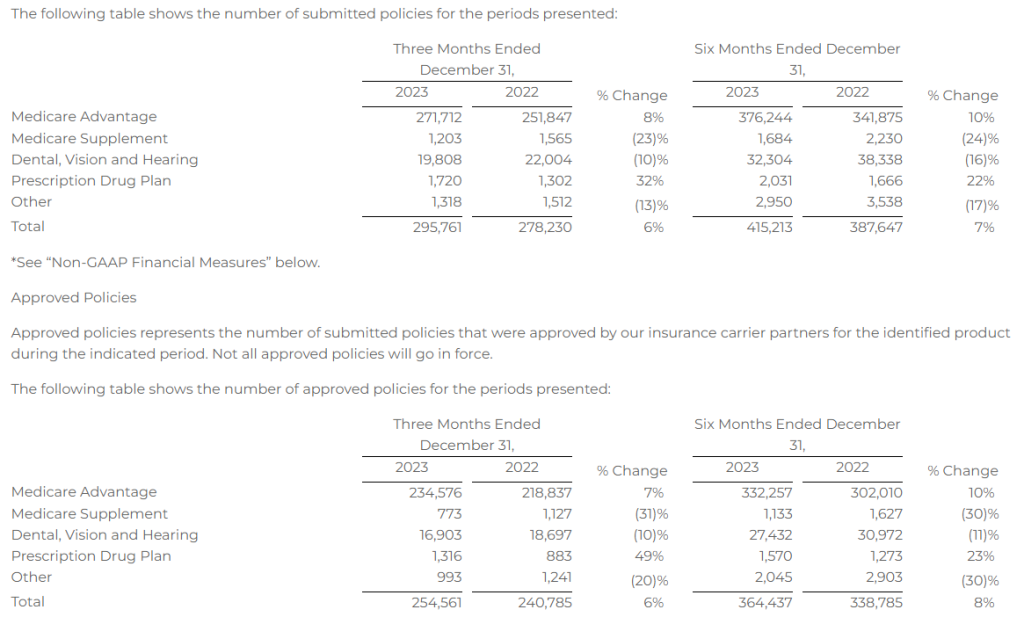

Approved Medicare Advantage policies of 234,576

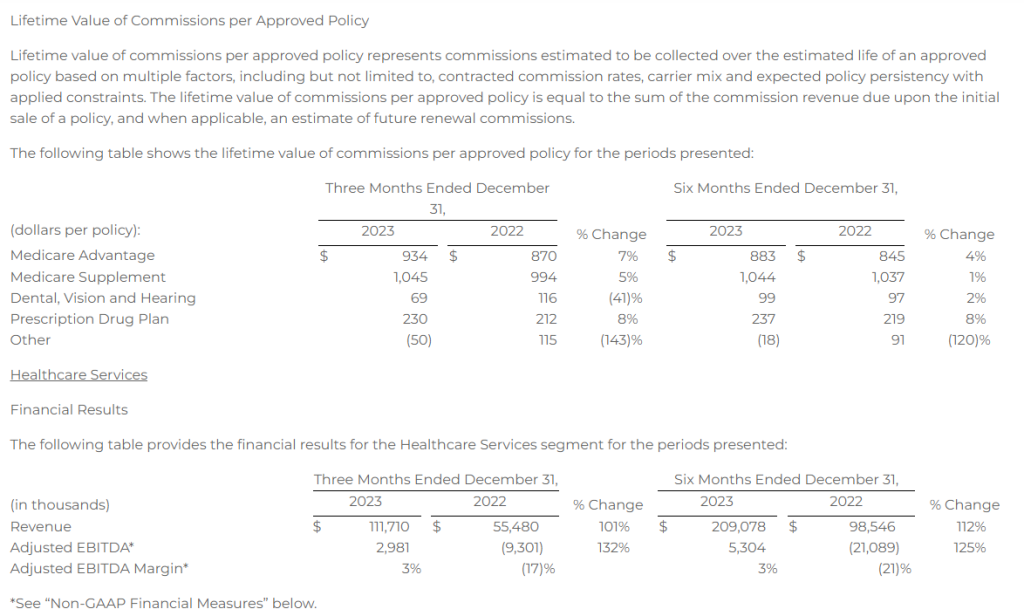

Healthcare Services

Revenue of $111.7 million

Adjusted EBITDA* of $3.0 million

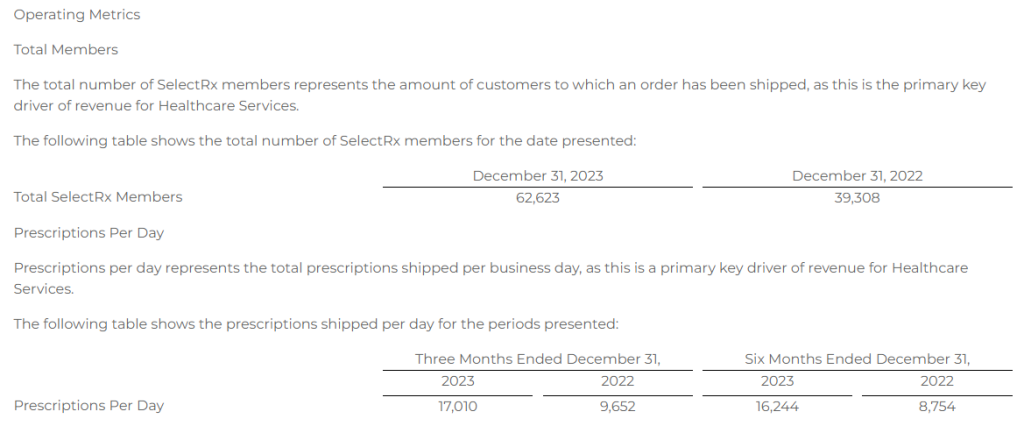

Over 62,000 SelectRx members

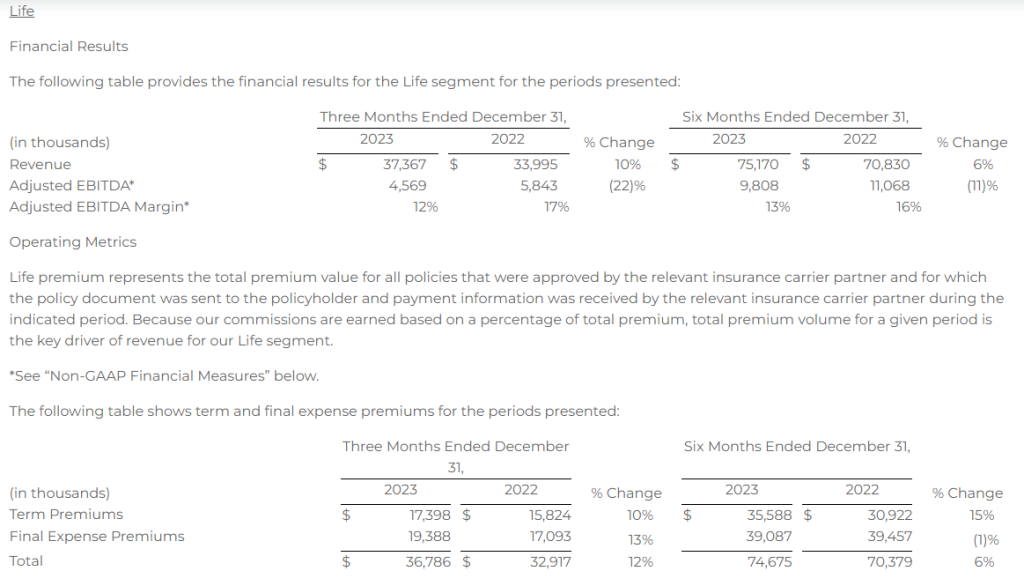

Life

Revenue of $37.4 million

Adjusted EBITDA* of $4.6 million

Auto & Home

Revenue of $10.5 million

Adjusted EBITDA* of $4.7 million

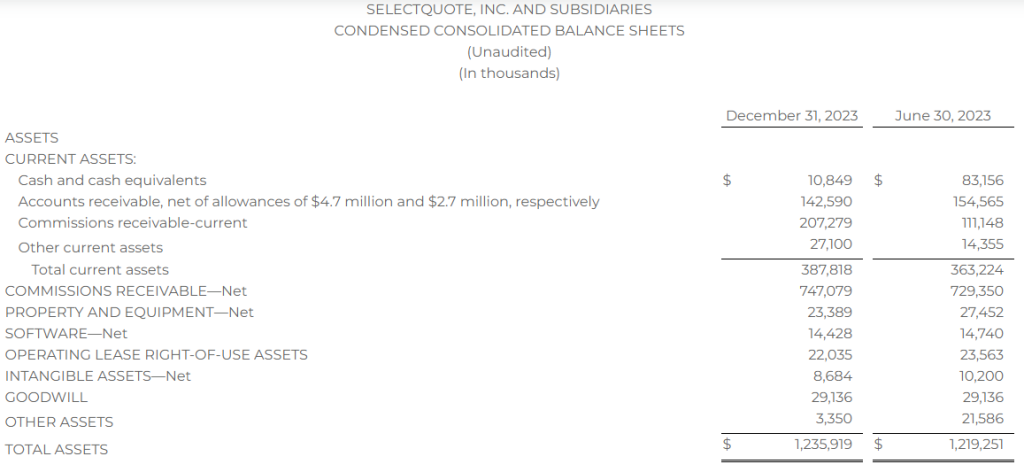

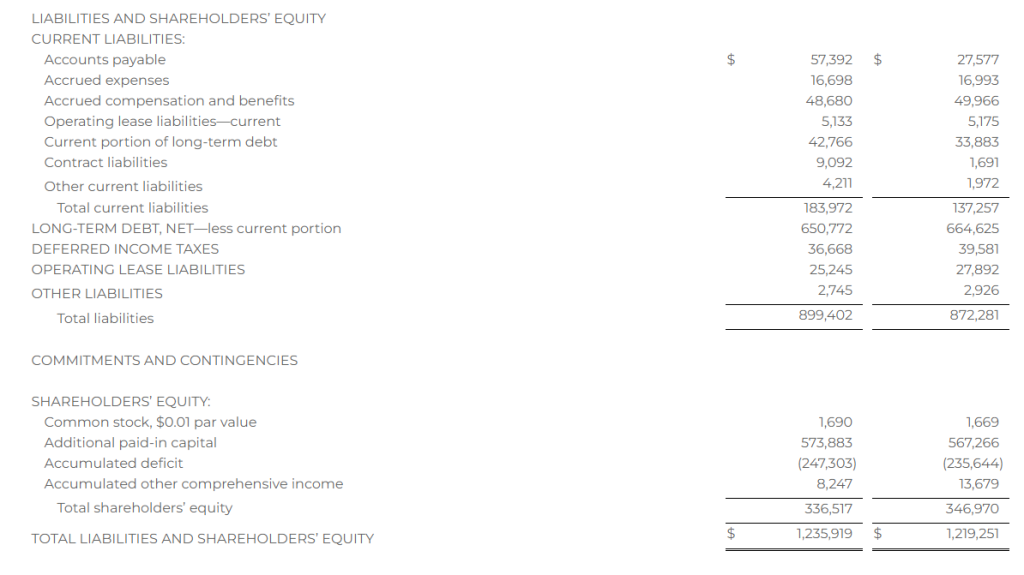

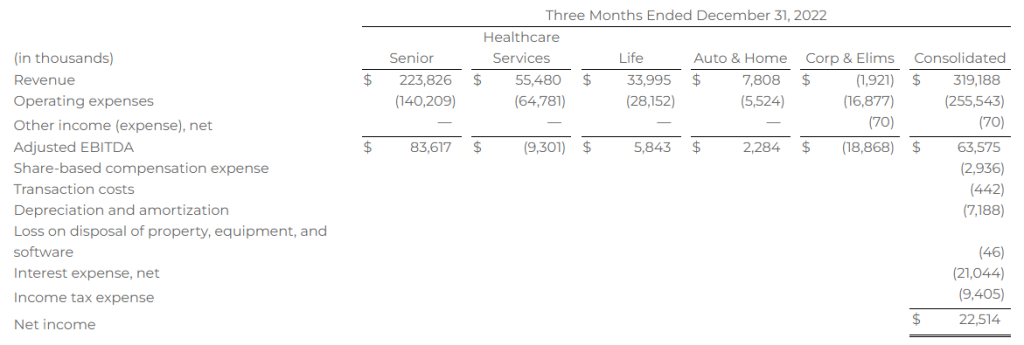

OVERLAND PARK, Kan.–(BUSINESS WIRE)– SelectQuote, Inc. (NYSE: SLQT) reported consolidated revenue for the second quarter of fiscal year 2024 of $405.4 million, compared to consolidated revenue for the second quarter of fiscal year 2023 of $319.2 million. Consolidated net income for the second quarter of fiscal year 2024 was $19.4 million, compared to consolidated net income for the second quarter of fiscal year 2023 of $22.5 million. Finally, consolidated Adjusted EBITDA* for the second quarter of fiscal year 2024 was $67.4 million, compared to consolidated Adjusted EBITDA* for the second quarter of fiscal year 2023 of $63.6 million.

Chief Executive Officer Tim Danker stated, “The second quarter marked SelectQuote’s eighth consecutive quarter of performance ahead of expectations, and we remain confident that our strategy to prioritize predictable and cash efficient growth will continue to generate value for both our customers and shareholders. We are also pleased with our progress on operating cash flow and now anticipate that SelectQuote will approach positive free cash flow in fiscal 2024.”

“SelectQuote drove strong results throughout the annual enrollment period for Medicare Advantage where our Senior business grew revenues by double digits, and our second quarter Adjusted EBITDA margin of 32% remains attractive. These strong Senior operating results were a function of higher tenured agent productivity and solid policyholder persistency, which we expect to benefit SelectQuote in the open enrollment period as well.”

“Additionally, Healthcare Services, and our SelectRx business specifically, drove substantial growth in excess of our original forecast. As of the end of the second quarter, SelectRx members have surpassed 62,000, which is in excess of our original expectation for the full year. More importantly, the business was again Adjusted EBITDA profitable.”

Mr. Danker continued, “We are pleased to increase our fiscal year 2024 outlook based on the strength of both businesses year-to-date.”

Segment Results

We currently report on four segments: 1) Senior, 2) Healthcare Services, 3) Life, and 4) Auto & Home. The performance measures of the segments include total revenue, Adjusted EBITDA,* and Adjusted EBITDA Margin.* Costs of revenue, cost of goods sold-pharmacy revenue, marketing and advertising, selling, general, and administrative, and technical development operating expenses that are directly attributable to a segment are reported within the applicable segment. Indirect costs of revenue, marketing and advertising, selling, general, and administrative, and technical development operating expenses are allocated to each segment based on varying metrics such as headcount. Adjusted EBITDA is calculated as total revenue for the applicable segment less direct and allocated costs of revenue, cost of goods sold, marketing and advertising, technical development, and selling, general, and administrative operating costs and expenses, excluding depreciation and amortization expense; gain or loss on disposal of property, equipment, and software; share-based compensation expense; and non-recurring expenses such as severance payments and transaction costs.

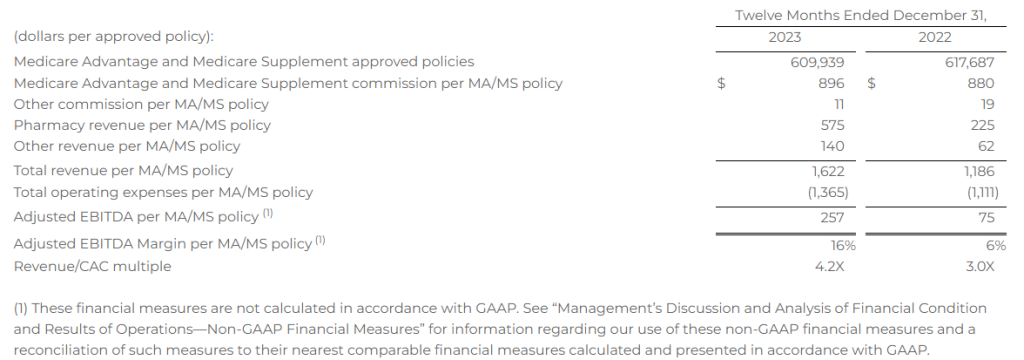

Combined Senior and Healthcare Services – Consumer Per Unit Economics

The opportunity to leverage our existing database and distribution model to improve access to healthcare services for our consumers has created a need for us to review our key metrics related to our per unit economics. As we think about the revenue and expenses for Healthcare Services, we note that they are derived from the marketing acquisition costs associated with the sale of an MA or MS policy, some of which costs are allocated directly to Healthcare Services, and therefore determined that our per unit economics measure should include components from both Senior and Healthcare Services. See details of revenue and expense items included in the calculation below.

Combined Senior and Healthcare Services consumer per unit economics represents total MA and MS commissions; other product commissions; other revenues, including revenues from Healthcare Services; and operating expenses associated with Senior and Healthcare Services, each shown per number of approved MA and MS policies over a given time period. Management assesses the business on a per-unit basis to help ensure that the revenue opportunity associated with a successful policy sale is attractive relative to the marketing acquisition cost. Because not all acquired leads result in a successful policy sale, all per-policy metrics are based on approved policies, which is the measure that triggers revenue recognition.

The MA and MS commission per MA/MS policy represents the LTV for policies sold in the period. Other commission per MA/MS policy represents the LTV for other products sold in the period, including DVH prescription drug plan, and other products, which management views as additional commission revenue on our agents’ core function of MA/MS policy sales. Pharmacy revenue per MA/MS policy represents revenue from SelectRx, and other revenue per MA/MS policy represents revenue from Population Health, production bonuses, marketing development funds, lead generation revenue, and adjustments from the Company’s reassessment of its cohorts’ transaction prices. Total operating expenses per MA/MS policy represents all of the operating expenses within Senior and Healthcare Services. The revenue to customer acquisition cost (“CAC”) multiple represents total revenue as a multiple of total marketing acquisition costs, which represents the direct costs of acquiring leads. These costs are included in marketing and advertising expense within the total operating expenses per MA/MS policy.

The following table shows combined Senior and Healthcare Services consumer per unit economics for the periods presented. Based on the seasonality of Senior and the fluctuations between quarters, we believe that the most relevant view of per unit economics is on a rolling 12-month basis. All per MA/MS policy metrics below are based on the sum of approved MA/MS policies, as both products have similar commission profiles.

Total revenue per MA/MS policy increased 37% for the twelve months ended December 31, 2023, compared to the twelve months ended December 31, 2022, primarily due to the increase in pharmacy revenue. Total operating expenses per MA/MS policy increased 23% for the twelve months ended December 31, 2023, compared to the twelve months ended December 31, 2022, driven by a 100% increase in operating expenses related to SelectRx due to the growth of the business, offset by a 3% decrease in other operating expenses driven by a decrease in marketing and advertising costs for the second half of fiscal year 2023 compared to the second half of fiscal year 2022.

*See “Non-GAAP Financial Measures” below.

Earnings Conference Call

SelectQuote, Inc. will host a conference call with the investment community today, Wednesday, February 7, 2024, beginning at 8:30 a.m. ET. To register for this conference call, please use this link: https://www.netroadshow.com/events/login?show=3bad4d79&confId=59966. After registering, a confirmation will be sent via email, including dial-in details and unique conference call codes for entry. Registration is open through the live call, but to ensure you are connected for the full call we suggest registering at least 10 minutes before the start of the call. The event will also be webcasted live via our investor relations website https://ir.selectquote.com/investor-home/default.aspx.

Non-GAAP Financial Measures

This release includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures. To supplement our financial statements presented in accordance with GAAP and to provide investors with additional information regarding our GAAP financial results, we have presented in this release Adjusted EBITDA and Adjusted EBITDA Margin, which are non-GAAP financial measures. These non-GAAP financial measures are not based on any standardized methodology prescribed by GAAP and are not necessarily comparable to similarly titled measures presented by other companies. We define Adjusted EBITDA as income (loss) before interest expense, income tax expense (benefit), depreciation and amortization, and certain add-backs for non-cash or non-recurring expenses, including restructuring and share-based compensation expenses. The most directly comparable GAAP measure is net income (loss). We define Adjusted EBITDA Margin as Adjusted EBITDA divided by revenue. The most directly comparable GAAP measure is net income margin. We monitor and have presented in this release Adjusted EBITDA and Adjusted EBITDA Margin because they are key measures used by our management and Board of Directors to understand and evaluate our operating performance, to establish budgets and to develop operational goals for managing our business. In particular, we believe that excluding the impact of these expenses in calculating Adjusted EBITDA can provide a useful measure for period-to-period comparisons of our core operating performance.

We believe that these non-GAAP financial measures help identify underlying trends in our business that could otherwise be masked by the effect of the expenses that we exclude in the calculations of these non-GAAP financial measures. Accordingly, we believe these financial measures provide useful information to investors and others in understanding and evaluating our operating results, enhancing the overall understanding of our past performance and future prospects. Reconciliations of the differences between the non-GAAP financial measures included herein and their most directly comparable GAAP financial measures are set forth below beginning on page 12.

Forward Looking Statements

This release contains forward-looking statements. These forward-looking statements reflect our current views with respect to, among other things, future events and our financial performance. These statements are often, but not always, made through the use of words or phrases such as “may,” “should,” “could,” “predict,” “potential,” “believe,” “will likely result,” “expect,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “projection,” “would” and “outlook,” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature. These forward-looking statements are not historical facts, and are based on current expectations, estimates and projections about our industry, management’s beliefs and certain assumptions made by management, many of which, by their nature, are inherently uncertain and beyond our control. Accordingly, we caution you that any such forward-looking statements are not guarantees of future performance and are subject to risks, assumptions and uncertainties that are difficult to predict. Although we believe that the expectations reflected in these forward-looking statements are reasonable as of the date made, actual results may prove to be materially different from the results expressed or implied by the forward-looking statements.

There are or will be important factors that could cause our actual results to differ materially from those indicated in these forward-looking statements, including, but not limited to, the following: the impacts of the COVID-19 pandemic and any other public health events, our reliance on a limited number of insurance carrier partners and any potential termination of those relationships or failure to develop new relationships; existing and future laws and regulations affecting the health insurance market; changes in health insurance products offered by our insurance carrier partners and the health insurance market generally; insurance carriers offering products and services directly to consumers; changes to commissions paid by insurance carriers and underwriting practices; competition with brokers, including exclusively online brokers and carriers who opt to sell policies directly to consumers; competition from government-run health insurance exchanges; developments in the U.S. health insurance system; our dependence on revenue from carriers in our senior segment and downturns in the senior health as well as life, automotive and home insurance industries; our ability to develop new offerings and penetrate new vertical markets; risks from third-party products; failure to enroll individuals during the Medicare annual enrollment period; our ability to attract, integrate and retain qualified personnel; our dependence on lead providers and ability to compete for leads; failure to obtain and/or convert sales leads to actual sales of insurance policies; access to data from consumers and insurance carriers; accuracy of information provided from and to consumers during the insurance shopping process; cost-effective advertisement through internet search engines; ability to contact consumers and market products by telephone; global economic conditions, including inflation; disruption to operations as a result of future acquisitions; significant estimates and assumptions in the preparation of our financial statements; impairment of goodwill; potential litigation and other legal proceedings or inquiries; our existing and future indebtedness; our ability to maintain compliance with our debt covenants and meet our scheduled repayment obligations under out debt arrangement; our ability to access to additional capital on acceptable terms; failure to protect our intellectual property and our brand; fluctuations in our financial results caused by seasonality; accuracy and timeliness of commissions reports from insurance carriers; timing of insurance carriers’ approval and payment practices; factors that impact our estimate of the constrained lifetime value of commissions per policyholder; changes in accounting rules, tax legislation and other legislation; disruptions or failures of our technological infrastructure and platform; failure to maintain relationships with third-party service providers; cybersecurity breaches or other attacks involving our systems or those of our insurance carrier partners or third-party service providers; our ability to protect consumer information and other data; failure to market and sell Medicare plans effectively or in compliance with laws; and other factors related to our pharmacy business, including manufacturing or supply chain disruptions, access to and demand for prescription drugs, and regulatory changes or other industry developments that may affect our pharmacy operations. For a further discussion of these and other risk factors that could impact our future results and performance, see the section entitled “Risk Factors” in the most recent Annual Report on Form 10-K and subsequent periodic reports filed by us with the Securities and Exchange Commission. Accordingly, you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and, except as otherwise required by law, we do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise.

About SelectQuote:

Founded in 1985, SelectQuote (NYSE: SLQT) provides solutions that help consumers protect their most valuable assets: their families, health, and property. The company pioneered the model of providing unbiased comparisons from multiple, highly-rated insurance companies allowing consumers to choose the policy and terms that best meet their unique needs. Two foundational pillars underpin SelectQuote’s success: a strong force of highly-trained and skilled agents who provide a consultative needs analysis for every consumer, and proprietary technology that sources and routes high-quality leads.

With an ecosystem offering high touchpoints for consumers across insurance, medicare, pharmacy, and value-based care, the company now has four core business lines: SelectQuote Senior, SelectQuote Healthcare Services, SelectQuote Life, and SelectQuote Auto and Home. SelectQuote Senior serves the needs of a demographic that sees around 10,000 people turn 65 each day with a range of Medicare Advantage and Medicare Supplement plans. SelectQuote Healthcare Services is comprised of the SelectRx Pharmacy, a Patient-Centered Pharmacy Home™ (PCPH) accredited pharmacy, and Population Health which proactively connects consumers with a wide breadth of healthcare services supporting their needs.