FORT WAYNE, Ind., Jan. 16, 2024 (GLOBE NEWSWIRE) — Vera Bradley, Inc. (NASDAQ: VRA) (the “Company”) today announced that Bradley (“Brad”) Weston, seasoned retail executive and former Chief Executive Officer of Party City Holdings, Inc., has been nominated to join its Board of Directors.

“We are so pleased to welcome Brad Weston as the newest member of the Vera Bradley, Inc. Board of Directors,” commented Jackie Ardrey, Chief Executive Officer of the Company. “As we continue to make progress on Project Restoration, our strategic plan to drive long-term profitable growth and deliver value to our shareholders, Brad’s wealth of omnichannel retail experience, strong merchandising background, and visionary leadership will be invaluable assets.”

Weston is a battle-tested executive with a diverse background, having successfully operated in mature, start-up, turnaround/transformation, and high-growth situations over his 35-year retail career. Most recently, Weston served as the Chief Executive Officer of Party City Holdings, Inc., a role he assumed at the start of the COVID-19 pandemic following a short period leading the company’s retail division. Previously, he spent seven years with Petco Animal Supplies, Inc. in roles of increasing responsibility from Chief Merchandising Officer to President and Chief Executive Officer. He also led the merchant organization at Dick’s Sporting Goods from 2008 to 2011 as Chief Merchandising Officer.

Weston’s merchandising expertise is grounded in the fundamentals he learned early in his career. Over 18 years, he successfully rose through the ranks at May Department Stores from Executive Trainee to Senior Vice President, General Merchandising Manager, Ready-to-Wear. He holds a bachelor’s degree in business administration with a finance and marketing emphasis from the University of California, Berkeley.

In addition to his appointment to the Vera Bradley, Inc. Board of Directors, Weston is currently a member of the Board of Directors for Boot Barn, Inc. He has previously served in Director roles for Party City Holdings, Inc.; Petco; the National Retail Federation; and The Sports Authority.

Weston will join Vera Bradley Inc.’s seven other board members: Jackie Ardrey, CEO; Barbara Bradley Baekgaard, Co-Founder of Vera Bradley; Kristina Cashman, former Chief Financial Officer of restaurant group PF Chang’s; Robert J. Hall, Chairman of the Vera Bradley Board of Directors and President of Green Gables Partners; Mary Lou Kelley, former President, E-Commerce for Best Buy; Frances P. Philip, Lead Independent Director of the Vera Bradley Board of Directors and former Chief Merchandising Officer of L.L. Bean, Inc.; and Carrie Tharp, Vice President of Strategic Industries for Google Cloud.

About Vera Bradley, Inc. Vera Bradley, Inc. operates two unique lifestyle brands – Vera Bradley and Pura Vida. Vera Bradley and Pura Vida are complementary businesses, both with devoted, emotionally-connected, and multi-generational female customer bases; alignment as casual, comfortable, affordable, and fun brands; positioning as “gifting” and socially-connected brands; strong, entrepreneurial cultures; a keen focus on community, charity, and social consciousness; multi-channel distribution strategies; and talented leadership teams aligned and committed to the long-term success of their brands.

Vera Bradley, based in Fort Wayne, Indiana, is a leading designer of women’s handbags, luggage and other travel items, fashion and home accessories, and unique gifts. Founded in 1982 by friends Barbara Bradley Baekgaard and Patricia R. Miller, the brand is known for its innovative designs, iconic patterns, and brilliant colors that inspire and connect women unlike any other brand in the global marketplace.

In July 2019, Vera Bradley, Inc. acquired a 75% interest in Creative Genius, Inc., which also operates under the name Pura Vida Bracelets (“Pura Vida”). Pura Vida, based in La Jolla, California, is a digitally native, highly-engaging lifestyle brand founded in 2010 by friends Paul Goodman and Griffin Thall. Pura Vida has a differentiated and expanding offering of bracelets, jewelry, and other lifestyle accessories. The Company acquired the remaining 25% of Pura Vida in January 2023.

The Company has three reportable segments: Vera Bradley Direct (“VB Direct”), Vera Bradley Indirect (“VB Indirect”), and Pura Vida. The VB Direct business consists of sales of Vera Bradley products through Vera Bradley Full-Line and Factory Outlet stores in the United States, www.verabradley.com, Vera Bradley’s online outlet site, and the Vera Bradley annual outlet sale in Fort Wayne, Indiana. The VB Indirect business consists of sales of Vera Bradley products to approximately 1,600 specialty retail locations throughout the United States, as well as select department stores, national accounts, third party e-commerce sites, and third-party inventory liquidators, and royalties recognized through licensing agreements related to the Vera Bradley brand. The Pura Vida segment consists of sales of Pura Vida products through the Pura Vida websites, www.puravidabracelets.com, www.puravidabracelets.ca, and www.puravidabracelets.eu; through the distribution of its products to wholesale retailers and department stores; and through its Pura Vida retail stores.

Vera Bradley Safe Harbor Statement Certain statements in this release are “forward-looking statements” made pursuant to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements reflect the Company’s current expectations or beliefs concerning future events and are subject to various risks and uncertainties that may cause actual results to differ materially from those that we expected, including: possible adverse changes in general economic conditions and their impact on consumer confidence and spending; possible inability to predict and respond in a timely manner to changes in consumer demand; possible loss of key management or design associates or inability to attract and retain the talent required for our business; possible inability to maintain and enhance our brands; possible inability to successfully implement the Company’s long-term strategic plans; possible inability to successfully open new stores, close targeted stores, and/or operate current stores as planned; incremental tariffs or adverse changes in the cost of raw materials and labor used to manufacture our products; possible adverse effects resulting from a significant disruption in our distribution facilities; or business disruption caused by pandemics. More information on potential factors that could affect the Company’s financial results is included from time to time in the “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of the Company’s public reports filed with the SEC, including the Company’s Form 10-K for the fiscal year ended January 28, 2023. We undertake no obligation to publicly update or revise any forward-looking statement.

Added In-flight metrics will further enhance campaign performance

NEW YORK, Jan. 16, 2024 /PRNewswire/ — AdTheorent Holding Company, Inc. (Nasdaq: ADTH), a machine-learning pioneer and industry leader using privacy-forward solutions to deliver measurable value for programmatic advertisers, and Adelaide, the leader in attention-based media quality measurement, today announced a partnership enabling AdTheorent to utilize Adelaide’s attention-based metrics for campaign optimization and to quantify digital advertising campaign impact.

Adelaide’s omnichannel AU metric is used for attention-based quality measurement across digital advertising campaigns. The AU score goes beyond viewability, using modeling to evaluate various qualifiers, including ad placement context, position, duration, business outcomes, and eye tracking. With access to Adelaide data, AdTheorent can use top attention-driving tactics to drive campaign performance across multiple formats and channels including display, online video, and connected television (CTV). In addition to AU scores, AdTheorent advertisers can gain insight into metrics such as Cost Per AU and Performance by Feature (i.e., creative, device, etc.). Additionally, AdTheorent can utilize Adelaide measurement in conjunction with other studies, such as sales lift, brand awareness, and visitation, to determine the impact of attention-based metrics on business outcomes.

“AdTheorent’s ML-powered DSP puts advertisers first by executing highly successful campaigns that are free from waste and inefficiency, and by driving tangible business outcomes across a variety of advertiser-specified KPIs,” said Jim Lawson, CEO, AdTheorent. “We are excited about our partnership with Adelaide which allows us to optimize and measure campaigns utilizing insightful attention-based metrics.”

“AU offers predictive insights into campaign performance with unmatched precision. Its integration into AdTheorent’s DSP means advertisers can easily secure higher-quality media and drive better outcomes at scale,” said Marc Guldimann, CEO & Co-founder, Adelaide. “We’re excited to collaborate with AdTheorent to make attention data actionable, steering advertisers towards smarter investment decisions and an understanding of true media quality.”

About AdTheorent AdTheorent (Nasdaq: ADTH) uses advanced machine learning technology and privacy-forward solutions to deliver impactful advertising campaigns for marketers. AdTheorent’s machine learning-powered media buying platform powers its predictive targeting, predictive audiences, geo-intelligence, audience extension solutions and in-house creative capability, Studio A\T. Leveraging only non-sensitive data and focused on the predictive value of machine learning models, AdTheorent’s product suite and flexible transaction models allow advertisers to identify the most qualified potential consumers coupled with the optimal creative experience to deliver superior results, measured by each advertiser’s real-world business goals.

AdTheorent is consistently recognized with numerous technology, product, growth and workplace awards. AdTheorent was named “Best Buy-Side Programmatic Platform” in the 2023 Digiday Technology Awards and was honored with an AI Breakthrough Award and “Most Innovative Product” (B.I.G. Innovation Awards) for five consecutive years. Additionally, AdTheorent is the only seven-time recipient of Frost & Sullivan’s “Digital Advertising Leadership Award.” AdTheorent is headquartered in New York, with fourteen offices across the United States and Canada. For more information, visit adtheorent.com.

About Adelaide Adelaide is the leader in attention-based media quality measurement. Our mission is to bring increased transparency and fairness to advertising by supplying the market with a precise, omnichannel media quality metric connected to business outcomes. Adweek has called Adelaide’s AU “the attention economy’s most widely recognized metric.” Proven to predict full-funnel outcomes more accurately than any existing metric, AU helps the world’s largest brands make smarter investment decisions, activate attention data programmatically, and drive better performance. Adelaide is named after the global epicenter of evidence-based marketing in southern Australia and headquartered in New York City. For more information, visit adelaidemetrics.com.

This new innovative motor system will create lighter-weight, high performance mining equipment and help electrify heavy industry.

TULSA, Okla.–(BUSINESS WIRE)– Infinitum, creator of the sustainable air-core motor, and Matrix Design Group, LLC (“Matrix”), a wholly owned subsidiary of Alliance Resource Partners, L.P. (“ARLP”) and leading safety and productivity technology provider for mining and industrial applications, today announced an agreement to jointly develop and distribute high-efficiency, reliable motors and advanced motor controllers designed specifically for the mining industry.

Under the agreement, Matrix will integrate Infinitum’s smaller, lighter motor technology into mining equipment of ARLP’s operating subsidiaries to provide performance validation in production environments for the jointly developed products. In addition to supporting installations at ARLP operations, Matrix plans to offer the products to third-party mining customers around the globe.

Infinitum’s patented motor technology will replace traditional, heavy iron-core motors with a motor system that is 50% smaller and lighter, uses 66% less copper, and consumes 10% less energy, and is expected to offer mining companies and equipment manufacturers a more efficient, reliable alternative.

“Working with ARLP and Matrix expands Infinitum’s ability to sustainably power heavy machinery with our lightweight, power-dense motors that use less energy, material and waste,” said Ben Schuler, founder and Chief Executive Officer, Infinitum. “We’re excited to join forces with a mining leader like ARLP to make a greater impact towards electrifying and decarbonizing heavy industry.”

Over the past 15 years, Matrix has become a leader in collision avoidance and proximity detection technologies, providing safety and productivity solutions for ARLP and many other mining companies, while extending its reach beyond the U.S. and to other industrial applications. This agreement builds upon that success and enables the development of proven products that provide technological advancements in support of rapidly expanding customer needs.

Joseph W. Craft III, ARLP Chairman, President and Chief Executive Officer commented, “This collaboration with Infinitum represents a natural progression and extension of our strategic investment in the company. We believe their groundbreaking motor technology will bring much needed innovation to the mining industry by delivering more efficient and higher performing production equipment, which will enable companies such as ours to improve mining processes, reduce operating costs, and boost productivity.”

Infinitum, ARLP, and Matrix have collaborated since 2022, when ARLP made an initial investment in Infinitum as part of the company’s Series D funding.

About Infinitum

Infinitum has raised the bar for a new generation of motors that is better for the planet and people. The company’s patented air core motors offer superior performance in half the weight and size, at a fraction of the carbon footprint of traditional motors, making them pound for pound the most efficient in the world. Infinitum’s electric motors open up sustainable design possibilities for the machines we rely on to be smaller, lighter and quieter, improving our quality of life while also saving energy and reducing waste. Based in Austin, Texas, Infinitum is led by a team of industry experts and pioneers. To learn more, visit goinfinitum.com.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure. News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

About Matrix Design Group, LLC

A leading technology provider in the mining and industrial sectors, Matrix is a wholly owned subsidiary of Alliance Resource Partners, L.P. Since 2006, its core business has been mining safety and providing operations-friendly applications that meet evolving industry regulations. Today, it is developing customer-driven suites of innovative, leading-edge products that balance product advancement in its existing markets with expansion into new, sustainable growth markets.

Headquartered in Newburgh, Indiana, the Matrix Team embraces the concept of hard work, working smart, and collaborating on product development with its customers and strategic partners. As technology evolves, Matrix incorporates the latest innovations, such as artificial intelligence, cloud management, and real-world analytics into its next-generation products. The Matrix Quality Management System (QMS) is certified as being in conformity with ISO 9001:2015 by Intertek. For more information, please visit MatrixTeam.com.

Infinitum Media Contact: Erin Gilmore Activate PR on behalf of Infinitum egilmore@activateprmktg.com 512-466-4559

ARLP Investor Relations Contact: Cary P. Marshall Senior Vice President and Chief Financial Officer 918-295-7673 investorrelations@arlp.com

SAN DIEGO, Jan. 16, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a Technology Company in Defense, National Security and Global Markets, announced today that it has recently received approximately $50 million in awards for Products and Hardware, including for and in support of Counter Unmanned Aerial System (CUAS), Air Defense and Radar Systems. The $50 million total includes contracts and programs that were awarded to Kratos on a single award or sole source basis. Kratos is an industry leader in systems, hardware and microwave electronics, including for and in support of CUAS, unmanned aerial drone, missile, radar and air defense related systems. At Kratos, affordability is a technology, with Kratos offerings envisioned and designed up front, for rapid, low-cost manufacturing and production, at scale and in large quantities. Work under these recently received awards will be performed at secure Kratos manufacturing facilities and customer locations. Due to security related, competitive and other considerations, no additional information will be provided.

Eric DeMarco, President and CEO of Kratos, said, “Kratos’ technology, products, software and systems are supporting the U.S. warfighter and our allies defense and security related needs and requirements, including in current contested and high intensity conflict areas globally. Kratos’ ability to rapidly develop, produce and provide relevant, affordable solutions at scale and in quantity, we believe, is a competitive differentiator for our Company, customers, teammates and partners, and an important element of today’s global security and defense environment.”

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly design, develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we utilize proven, leading-edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach reducing cost, schedule and risk, and enabling us to be first to market with cost effective solutions. Kratos is known as the innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front, for successful rapid, large quantity, low-cost future manufacturing and as a competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos’ primary business areas include, virtualized ground systems for satellites and space vehicles, including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 25, 2022, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

Kratos Press Contact: Yolanda White 858-812-7302 Direct

MALVERN, Pa., Jan. 16, 2024 (GLOBE NEWSWIRE) — Ocugen, Inc. (Ocugen or the Company) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines, today announced that Bob Smith, former Senior Vice President, Global Gene Therapy Business at Pfizer, has joined the Company’s Business Advisory Board (BAB). The BAB was established in June 2023 to assist in driving public/private partnerships with governments around the world; pursuing business collaborations, partnerships, and licensing opportunities; creating awareness of the Company’s differentiated capabilities; and promoting access to the Company’s therapies around the world.

“Bob has the experience Ocugen needs to pursue business development activities with companies that have the size and scale to bring our gene therapies through to commercialization,” said Dr. Shankar Musunuri, Chairman, CEO and Co-founder of Ocugen. “He is a consummate healthcare professional who truly understands the need to drive the pipeline so that we can ultimately get our first-in-class gene therapies to patients with blindness diseases.”

For nearly eight years, Mr. Smith led Pfizer’s global gene therapy business, including the strategic and operational development and implementation of Pfizer’s end-to-end, enterprise-wide efforts to be an industry leader in gene therapy. He is an accomplished biopharmaceutical executive with over thirty-five years’ experience in a variety of alliance management, business development, commercial, corporate strategy, mergers and acquisitions, and research and development executive leadership roles.

“I am impressed with the science behind Ocugen’s modifier gene therapy programs and look forward to introducing this novel approach to potential business partners,” said Mr. Smith. “Having previously worked with members of the Ocugen leadership team at Wyeth and Pfizer, I welcome the opportunity to join the BAB and support their short- and long-term goals for the company.”

Mr. Smith joins Connie Collingsworth, Senator Pat Toomey, Ambassador Joseph W. Westphal, Ph.D., and Dennis Carey, Ph.D. on the BAB. These advisors will work alongside the Executive Leadership Team to strengthen Ocugen’s network across a variety of stakeholders.

About Ocugen, Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patient’s lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on X and LinkedIn.

Cautionary Note on Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, which are subject to risks and uncertainties. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations. These and other risks and uncertainties are more fully described in our periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.

RICHMOND, Va.–(BUSINESS WIRE)– Bowlero Corporation (NYSE: BOWL), the global leader in bowling entertainment, announced today the signing of Ten Pin in Hilliard, Ohio, the company’s 20th center acquisition in fiscal 2024. During the second quarter of fiscal 2024, Bowlero Corp. completed the acquisitions of Niles Bowling center in Niles, IL and BAM! Entertainment Center in Holland, MI. The total FY 2024 investment in acquisitions thus far, including the 14 Lucky Strike centers is $145.9 million.

Bowlero Corp. opened Lucky Strike Moorpark in Moorpark, CA, northwest of Los Angeles, in December. This is Bowlero’s first new build using the Lucky Strike brand since it was acquired in September. Lucky Strike Moorpark, a 43,000 sq. ft. entertainment center in Ventura County, features 40 bowling lanes, an arcade with over 80 games, and a spectacular sports bar. This is Bowlero Corp.’s 52nd center in California and the fifth Lucky Strike branded center in the state.

“These strategic acquisitions and the opening of Lucky Strike in Moorpark underscore our commitment to expanding our presence and enhancing the bowling entertainment experience across prime markets,” stated Thomas Shannon, Founder, Chairman and CEO of Bowlero Corp. “We look forward to continuing the expansion of the iconic Lucky Strike brand, leveraging its established brand equity, and delivering premium experiences to a broad audience.”

The company provided an update on its ongoing share repurchase program. Bowlero repurchased approximately 7.5 million shares of its common stock in the second quarter of fiscal 2024, totaling an aggregate purchase price of approximately $80 million. In the first quarter of FY 2024, the company repurchased approximately 12.1 million shares for approximately $131 million, bringing total share repurchases in the first half of fiscal 2024 to approximately 19.6 million. Since Bowlero’s IPO, the company has spent approximately $432 million retiring all SPAC-related warrants, 31.0 million shares of common stock and 4.9 million as-converted preferred shares, reducing common stock outstanding by approximately 20%. Bowlero Corp. anticipates continuing its share repurchase program through the balance of fiscal 2024 and beyond, subject to market and other conditions.

Bowlero Corp. is positioned for continued growth, with a focus on strategic acquisitions, innovative developments, and shareholder value creation. The company anticipates further growth and expansion in the coming year.

About Bowlero Corp

Bowlero is the global leader in bowling entertainment. With approximately 350 bowling centers across North America, Bowlero serves more than 40 million guest visits annually through a family of brands that include Bowlero, Lucky Strike and AMF. In 2019, Bowlero acquired the Professional Bowlers Association, the major league of bowling, which boasts thousands of members and millions of fans across the globe. For more information on Bowlero, please visit BowleroCorp.com.

Forward Looking Statements

Some of the statements contained in this press release are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that involve risk, assumptions and uncertainties, such as statements of our plans, objectives, expectations, intentions and forecasts. These forward-looking statements are generally identified by the use of forward-looking terminology, including the terms “anticipate,” “believe,” “confident,” “continue,” “could,” “estimate,” “expect,” “intend,” “likely,” “may,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “target,” “will,” “would” and, in each case, their negative or other various or comparable terminology. These forward-looking statements reflect our views with respect to future events as of the date of this release and are based on our management’s current expectations, estimates, forecasts, projections, assumptions, beliefs and information. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to have been correct. All such forward-looking statements are subject to risks and uncertainties, many of which are outside of our control, and could cause future events or results to be materially different from those stated or implied in this document. It is not possible to predict or identify all such risks. These risks include, but are not limited to: our ability to design and execute our business strategy; changes in consumer preferences and buying patterns; our ability to compete in our markets; the occurrence of unfavorable publicity; risks associated with long-term non-cancellable leases for our centers; our ability to retain key managers; risks associated with our substantial indebtedness and limitations on future sources of liquidity; our ability to carry out our expansion plans; our ability to successfully defend litigation brought against us; our ability to adequately obtain, maintain, protect and enforce our intellectual property and proprietary rights and claims of intellectual property and proprietary right infringement, misappropriation or other violation by competitors and third parties; failure to hire and retain qualified employees and personnel; the cost and availability of commodities and other products we need to operate our business; cybersecurity breaches, cyber-attacks and other interruptions to our and our third-party service providers’ technological and physical infrastructures; catastrophic events, including war, terrorism and other conflicts; public health emergencies and pandemics, such as the COVID-19 pandemic, or natural catastrophes and accidents; changes in the regulatory atmosphere and related private sector initiatives; fluctuations in our operating results; economic conditions, including the impact of increasing interest rates, inflation and recession; and other factors described under the section titled “Risk Factors” in the Company’s Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission (the “SEC”) by the Company on September 11, 2023, as well as other filings that the Company will make, or has made, with the SEC, such as Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this press release and in other filings. We expressly disclaim any obligation to publicly update or review any forward-looking statements, whether as a result of new information, future developments or otherwise, except as required by applicable law.

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) will report its fourth quarter 2023 financial results before the market opens on Monday, January 29, 2024. Alliance management will discuss these results during a conference call beginning at 10:00 a.m. Eastern that same day.

To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13743714.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

Investor Relations Contact Cary P. Marshall Senior Vice President and Chief Financial Officer (918) 295-7673 investorrelations@arlp.com

British telecommunications giant Vodafone has announced a 10-year, $1.5 billion strategic partnership with Microsoft to bring next-generation artificial intelligence (AI), cloud, and Internet of Things (IoT) capabilities to Vodafone’s markets across Europe and Africa.

The deal reflects both companies’ ambitions to be at the forefront of AI and digital transformation. By combining forces, they aim to enhance Vodafone’s customer experience, network operations, and business offerings for the 300 million consumer and enterprise customers it serves.

Transforming Customer Service with AI

A major focus of the partnership will be transforming Vodafone’s customer service using AI and natural language processing. Microsoft will provide access to its Azure OpenAI platform, including technologies like GPT-3.5 for generating conversational text.

Vodafone plans to invest heavily in building customized AI models using Microsoft’s tools. This includes enhancing TOBi, Vodafone’s digital assistant chatbot, to deliver more personalized and intelligent customer interactions across text, voice, and video channels.

More consistent and contextualized responses from TOBi could improve customer satisfaction and loyalty while reducing operational costs for Vodafone. The two companies will also collaborate on conversational AI and digital twin capabilities to optimize Vodafone’s network operations.

Transitioning to the Cloud

Another key element of the deal is transitioning Vodafone away from reliance on its own data centers. It will adopt Microsoft Azure as its preferred cloud platform, migrating workloads and infrastructure to Azure’s global footprint.

This should provide Vodafone with more flexibility, scalability, and cost efficiency. Azure’s extensive compliance and security controls will also help Vodafone meet strict regulatory requirements for its markets.

Vodafone plans to train and certify hundreds of employees as Azure experts to enable the shift. The cloud transition can allow Vodafone to retire legacy systems, consolidate data platforms, and leverage new technologies like AI more quickly.

Microsoft’s Equity Investment in Vodafone’s IoT Business

To deepen integration between the two companies, Microsoft will also become an equity investor in Vodafone’s IoT division when it spins out as a separate business in 2024.

Vodafone’s IoT platform connects over 120 million devices globally across areas like asset tracking, smart metering, and automotive. Microsoft’s investment reflects the strategic value it sees in Vodafone’s IoT leadership.

Together, they aim to scale Vodafone’s IoT solutions on Azure’s global infrastructure and combine them with Microsoft’s own IoT cloud services. This can drive faster time-to-market for new solutions. Microsoft also wants to leverage Vodafone’s IoT data and networks in sustainability and digital twin projects across multiple industries.

Empowering Mobile Finance in Africa

In Africa, the partnership has a strong focus on expanding access to mobile financial services. Vodafone operates the popular M-Pesa platform which pioneered mobile money across Eastern Africa.

Microsoft will provide AI capabilities to enhance functions like credit assessment for M-Pesa users. The goal is to drive financial inclusion and provide intelligent financial tools to the unbanked population in Vodafone’s African footprint.

Microsoft and Vodafone will also cooperate to improve digital skills and literacy for small businesses by providing bundled connectivity, devices, and software through the new partnership. This aligns with both companies’ commitments to empower digital transformation and economic opportunity in the region.

An Ambitious Partnership for the AI and Cloud Era

The scale of the newly announced partnership reflects Vodafone and Microsoft’s shared ambition to shape the future of technology and connectivity. By combining Vodafone’s reach across emerging markets with Microsoft’s leading cloud and AI enterprise offerings, they want to enable inclusive digital experiences for consumers and businesses worldwide.

The deal demonstrates the transformational power of AI and cloud to reinvent customer service, improve operational efficiency, and develop innovative business models. As 5G networks expand globally over the next decade, the partnership lays the groundwork for Vodafone to transition itself into a future-ready technology leader.

Gregory Aurand, Senior Vice President, Equity Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Large Growing Complex Medicare Market. About 66.4 million Americans were covered by Medicare in calendar 2022 and the Medicare 65 and older population is expected to reach more than 93 million people by 2060. GoHealth has already helped 10 million Americans and seeks to be the consumer Medicare health plan destination in this growing market. As the market grows more complex with a greater number of plan offerings, GoHealth’s platform simplifies the annual Medicare private plan shopping process.

Proprietary Offering Platform. GoHealth is driving growth in the Medicare Advantage and Medicare Supplemental markets through its pressure-free unbiased consumer-centric Encompass Solution platform that utilizes its proprietary data machine-learning PlanFit Checkup technology.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Optimism For A Good 2024. In this report, we provide our advertising outlook for 2024 and provide our best picks to play the expected advertising rebound. Our take on the year is based on an improving economic outlook, particularly in the second half of the year, and heavy influx of Political advertising. Our favorable advertising outlook is based on a resilient labor market and lower interest rates to avoid a recession in 2024.

Have we seen thetrough for this cycle? With our economic scenario in mind, we anticipate an improving economic environment in the second half of 2024. Notably, we believe that advertising trends are improving into the first quarter 2024, with the rate of decline moderating for both Radio and Television.

National advertising expected to strengthen. The weakness in National was the biggest issue for broadcasters in 2023. We believe that National advertising trends should improve in 2024 both from the perspective of a sluggish consumer in the first half and from an improving economic outlook in the second half.

How big will Political be?We anticipate a strong political advertising environment in 2024, an increase of 13% to roughly $10 billion from 2020 levels. Importantly, about half of the high margin political advertising dollars are expected to be spent with television broadcasters.

Highlights of favorite picks for 2024. Media stocks are typically early cycle stocks, which tend to outperform in the midst of the economic downturn or trough as investors begin to anticipate economic improvement. We believe media stocks are timely and offer a compelling return potential given depressed valuations. In addition, some companies pay a dividend, offering attractive total return potential.

Investment Appraisal

Optimism For A Good 2024

The fortunes of advertising based companies are driven by the economy and the health of the consumer. As such, we start this report with our take on the economy in 2024. On December 4th, at Florida Atlantic University (FAU) in Boca Raton, Florida, Noblecon19 hosted an economic panel to discuss the business environment outlook for 2024. The economic panel consisted of a diverse group of industry professionals with a wide range of expertise and experience. In our economic outlook for 2024, we take into consideration the perspective of Jose Torres, Senior Economist at Interactive Brokers.

Mr. Torres highlighted 2023 as a resilient year for consumer spending, which was driven by excess pandemic savings accumulated in 2020 and 2021. Mr. Torres anticipates a slowdown in consumer spending and a strong labor market in 2024. Notably, he believes a resilient labor market will keep consumers spending and will keep the country from falling into a recession. Additionally, Mr. Torres highlighted that Personal Consumption Expenditures (PCE) annualized inflation over the last six months is running near 2.5%, which is very close to the FED’s goal of 2.0%. With moderating inflation pressures, Mr. Torres highlighted that the FED is likely to cut rates in March of 2024, which would be beneficial for small and mid-cap companies. While Mr. Torres largely has a positive outlook for 2024 and beyond, a point of concern was the federal government’s growing interest expense on debt, he noted that the government will eventually have to reduce spending or accept 3% – 3.5% inflation over the long-term.

The general U.S. economy is expected to soften in 2024, particularly in the first half, with a prospect that the economy could slip into recession. Our economic scenario for 2024 anticipates the economy will soften in the first half of the year and rebound in the second half of the year due to the prospect of a lower interest rate environment and resilient labor market.

The video of the Economic Perspectives panel may be viewed here.

Small Cap Cycle?

Small cap investors have gone through a rough period. For the past several years, investors have anticipated an economic downturn. With these concerns, investors turned toward “safe haven” large cap stocks, which by and large can weather economic downturns and have significant trading volume should investors need to sell their positions. Notably, there is a sizable valuation disparity between the two classes, large cap and small cap, one of the largest since 1999. Some of the small cap stocks we follow trade at a modest 2.5 times Enterprise Value to EBITDA, compared with large cap valuations as high as 15 times. We believe the disparity is due to higher risk in the small cap stocks, given that some companies may not be cash flow positive, have capital needs, or have limited share float. However, investors seem to have overlooked small cap stocks with favorable fundamentals. While small cap stocks are more speculative than large caps, many are growing revenues and cash flow, have capable balance sheets, and/or are cash flow positive. In our view, the valuation gap should resolve itself over time for attractive emerging growth stocks. Some market strategists suggest that small cap stocks trade at the most undervalued in the market.

Dan Thelen, Managing Director of small cap equity at Ancora Advisors, highlighted the valuation gap between small cap and large cap stocks during the economic panel at Noblecon19 on December 5, 2023. Mr. Thelen noted that investors are not recognizing the risk mitigation efforts small cap companies have undertaken in the high interest rate environment. He believes that changes small cap companies have implemented are not reflected in stock prices and should be a tailwind moving forward. Again, his comments can be viewed on the video of the Economic Perspectives panel here.

2024 Advertising Outlook

In our advertising outlook for 2024, we take into consideration the perspective of Lisa Knutson, Chief Operating Officer (COO) of E.W Scripps. Ms. Knutson is on the frontline of the economy as one of the largest TV broadcasters in the country. As a speaker on the Noblecon19 economic panel, she depicted the local and national advertising markets as a tale of two cities. Notably, Ms. Knutson highlighted resilience in local advertising and sequential improvement over the past few quarters in the auto advertising category. Additionally, she highlighted green shoots in local advertising, particularly in the services, home improvement and retail advertising categories. Importantly, political ad spend for the 2024 election cycle is expected to be approximately $10 billion, which is roughly a 13% increase from 2020, as illustrated in Figure #1 Political Ad Spend. About half of the high margin political advertising dollars are expected to be spent with television broadcasters. Our advertising forecast for television, radio and digital are highlighted later in this report.

Figure #1 Political Ad spend

Source: Statista

Stock Recommendations

With our economic scenario in mind, we have identified certain media stocks that should perform well and/or lead the industry as economic prospects improve. Media stocks are typically early cycle stocks. This means that the stocks tend to outperform in the midst of the economic downturn or trough as investors begin to anticipate economic improvement. In addition, small cap stocks in general have been out of favor, with many stocks trading at historic low stock valuations (over the past several economic cycles) and also relative to the valuations of leadership stocks, such as the Magnificent 7 (Apple, Microsoft, Alphabet (Google), Netflix, Amazon, Nvidia and Tesla). This report highlights some of our favorite picks for 2024. Our favorites include companies that are leveraged to benefit from the influx of Political advertising and improving economy, generate positive free cash flow, and have capable balance sheets to invest it growth initiatives. Finally, we recommend stocks that have compelling valuations and/or pay a dividend to provide an attractive total return investment opportunity.

Digital Media & Technology

Decelerating Revenue Growth, But Faster Than Other Advertising Categories

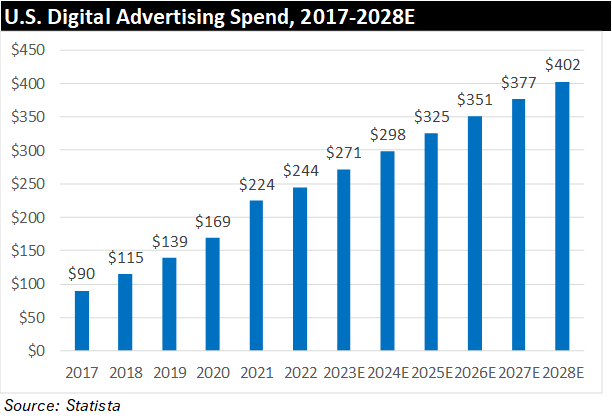

Digital Advertising has been growing rapidly over the past several years, bolstered by cord-cutting trends and generally, by an increasingly digital world. Digital Advertising includes various categories of advertising, such as audio, video, influencer, search, banner, and others. According to Statista, U.S. Digital Advertising spending is expected to grow at 15% Compound Annual Growth Rate (CAGR), from 2017-2028, from $90.1 billion to $402.1 billion. Figure #2 U.S. Digital Advertising Spend illustrates the 2017-2028 forecast, which is inclusive of the various different sub-categories of Digital Advertising.

Figure #2 U.S. Digital Advertising Spend

Source: Statista

Specifically in 2024, U.S. Digital Advertising is expected to grow a healthy 10% above 2023 levels, according to Statista. There are some categories of Digital Advertising, however, that are expected to grow especially fast in 2024, such as Connected TV (CTV) advertising, programmatic advertising, and influencer advertising. All three categorizations of Digital advertising are estimated to have above-average growth in 2024. According to Statista, influencer advertising in the U.S. will grow at 14% in 2024, while, according to eMarketer, U.S. programmatic and CTV advertising will grow at 13% and 17%, respectively.

In our view, there are several key factors strengthening these verticals. For example, influencer advertising allows brands to reach younger demographics through personalities those audiences trust. Moreover, during a time when there is uncertainty around the future of cookies and other forms of User IDs for targeted advertising, influencer advertising offers an alternative vehicle for audience targeting. Google has indicated plans to no longer use 3rd party cookies to deliver advertising in 2024, although the implementation of this plan has been delayed multiple times before. Additionally, we believe cord cutting is a major factor in the growth of connected TV, likely to be a strong growth vertical for programmatic digital advertising.

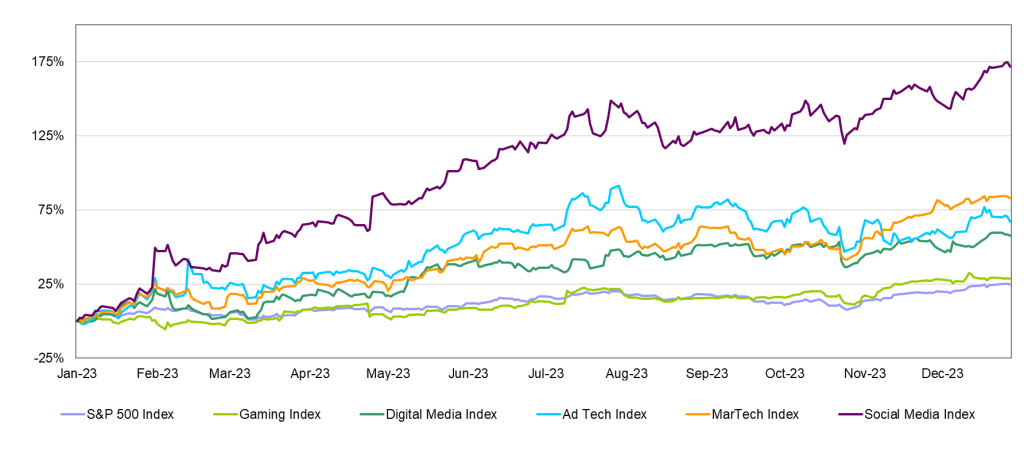

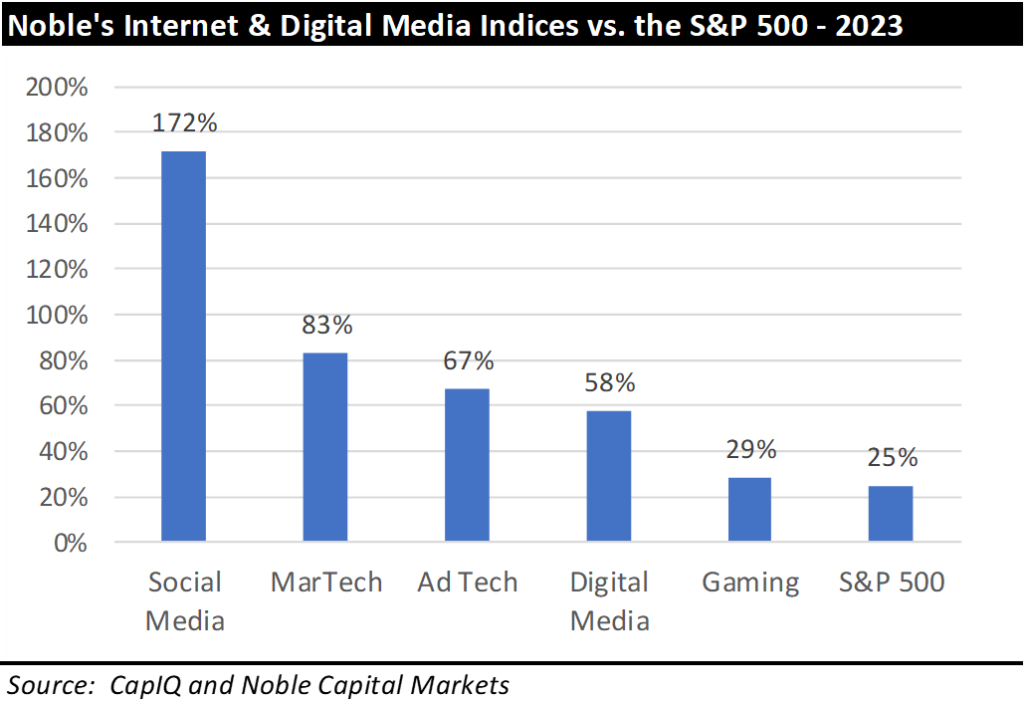

Noble’s Digital Media indices fared well over the past year with most outperforming the S&P 500 over that span, as illustrated in Figure #4 Digital Media LTM Performance. Most recently, the Social Media and Marketing Tech indices have performed strongest, up 18.9% and 24.2%, respectively, over the last 3-months. Figure #3 Digital Media 3-month Performance illustrates the last quarter’s performance by Noble’s Digital Media indices. However, many of the indices were skewed positively by the strong stock performance of the larger cap constituents. For example, META was up 194% over the trailing 12 months, while Adobe (ADBE) and Salesforce (CRM) also performed well, up 77% and 98%, over the same timeframe, respectively. Yet, in Q4 the performance disparity began to abate with the smaller cap constituents of Noble’s Digital indices contributing more to the positive returns, for the most part. We believe this could signal the beginning of shift towards the smaller cap stocks that had depressed valuations in 2023 relative to their large cap counterparts.

Despite the large cap versus small cap valuation disparity in 2023, there are several small cap stocks that performed well over the past 12 months, outshining respective indices. Notably, Direct Digital Holdings (DRCT) was up roughly 500% over the past year. Most of the runup of DRCT occurred late in Q4, after the company reported results far exceeding Street estimates. In our view, DRCT was substantially undervalued and is beginning to be discovered by more investors. Importantly, the increased trading activity has put the stock on investing screens for institutional, small cap investors. Another notable small cap performance was Townsquare Media (TSQ), which has a large Digital Advertising component to its business. TSQ was up 45% in the past year.

Below, we outlined some of the investment highlights for our closely followed Digital Media companies. In addition, Figure #5 Ad Tech Industry Comparables highlights the stock valuations of the sector. As the chart depicts, our favorite stocks current trade well below the averages for the industry and some of the larger cap names. One of our closely followed companies, AdTheorent, is a stand out. Near current levels, the ADTH shares trade at a modest 2.5 times Enterprise Value to our 2024 Adj. EBITDA estimate, well below the 15.1 times average for the sector. Given the compelling stock valuation, we highlight this company as our current favorite in the industry. In addition, the Direct Digital shares trade at 10 times Enterprise Value to our 2024 Adj. EBITDA estimate, well below the 15.1 times industry average. As such, we view the DRCT shares as compelling.

Figure #3 Digital Media 3-month Performance

Source: Capital IQ

Figure #4 Digital Media LTM Performance

Source: Capital IQ

Direct Digital Holdings (DRCT) – Programmatic Advertising. We view DRCT as a compelling play on the Programmatic Advertising market. The company operates a sell-side platform (SSP), in addition to servicing buy-side advertising clients through managing their digital advertising strategies. Importantly, the company’s niche comes from its deep relationships with multi-cultural publishers, a key competitive advantage in our view. In 2024, we estimate the company’s revenue will grow 30% above our 2023 forecast with adj. EBITDA growth of 33%. For research reports and important disclosures, please click here.

AdTheorent (ADTH) – Programmatic Advertising. ADTH is a unique play on programmatic advertising with cutting-edge audience targeting capabilities, powered by its machine learning (ML) platform. Due to its ML platform, the company does not need to use third-party cookies and other forms of user IDs to target audiences. Not only does this position the company well for Google’s phasing our of third-party cookies, but it also allows the company to offer clients a privacy-forward method of audience targeting. Some key verticals for the company include the healthcare industry as well as connected TV. For research reports and important disclosures, please click here.

Townsquare Media (TSQ) – Programmatic & SMB Digital Advertising. TSQ is a media company that has transformed from primarily a radio station operator to a Digital Advertising business, boasting multiple digital verticals. We believe it is a compelling play on the digital transition occurring in small business across the country. The company provides comprehensive digital marketing services to small and medium-sized businesses in its radio markets, leveraging its deep local relationships. Additionally, the company operates a programmatic advertising business, which is benefiting from the growth of CTV. For research reports and important disclosures, please click here.

Entravision Communications (EVC) – Programmatic & Social Media Advertising. EVC is one of our favorite social media advertising plays. The company serves as Meta’s exclusive ad agency in several emerging markets, such as, certain regions of Latin America. It also represents TikTok in parts of Asia. In addition, the company owns a programmatic agency, known as Smadex. For research reports and important disclosures, please click here.

Figure #5 Ad Tech Industry Comparables

Source: Noble estimates & Company filings

Traditional Media

The Largest Caps Performed The Best

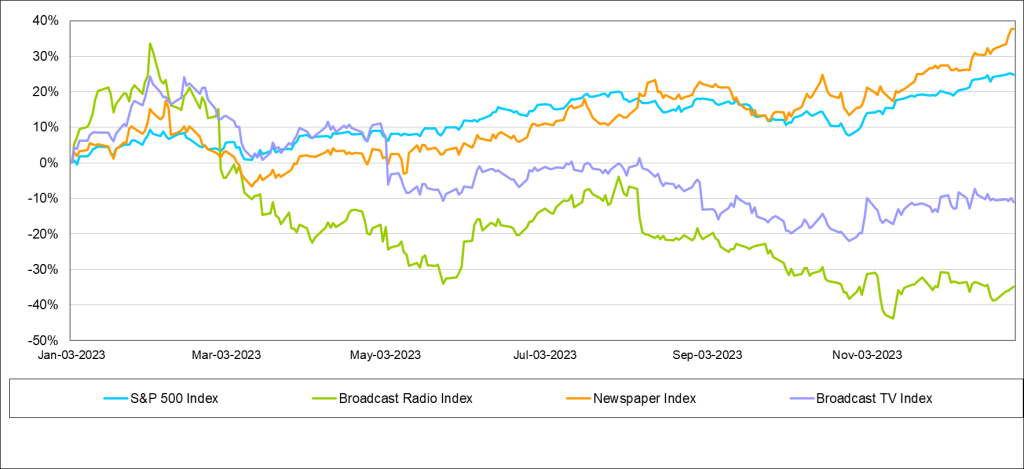

The Newspaper Index was the only traditional media sector that outperformed the general market in the past quarter and trailing 12 months, as illustrated in Figure #7 Traditional Media LTM Performance. In the latest quarter, Newspaper stocks outperformed the general market, up 20.4% versus down 11.2% for the general market as measured by the S&P 500 Index. Notably, our index performances are market cap weighted, meaning larger cap stocks have a greater impact on index return than small cap stocks. In Q4, only two stocks in the Newspaper index, NYT and NWSA, posted positive returns. These were the largest cap stocks in the index. In Q4, NWSA and NYT were up 22.4% and 18.9%, respectively. For full year 2023, four out of the five companies in the Newspaper index posted positive returns, the strongest performers were NYT and NWSA, up 50.9% and 34.9%, respectively. The Broadcast TV Index was up a modest 5.2% for the quarter and down 11% over the past year. The worst performing index over the last quarter was the Radio Broadcast index, down on 10.9%, as Illustrated in Figure #6 Traditional Media 3-Month Performance. Additionally, the Radio stocks were the worst performing group over the last year as well, down 34.9%. While the Radio Broadcast Index and Broadcast TV Index had a tough year in 2023, we believe both indices should improve in 2024. We highlight some of our favorites in the sector commentary below.

Figure #6 Traditional Media 3-month Performance

Source: Capital IQ

Figure #7 Traditional Media LTM Performance

Source: Capital IQ

Television Broadcast

Looking For A Better 2024

The Television industry had a tough year with soft core advertising and the absence of the year earlier Political advertising. Television revenues are estimated to have declined as much as 20% in 2023 inclusive of the absence of year earlier Political advertising. Total core television advertising is expected to have decline 3% in 2023, which excludes Political advertising, reflecting disproportionately weak National advertising and resilient Local advertising. Importantly, Television advertising accounts for less than 50% of total television revenue, with Retransmission revenue largely accounting for the balance. With growth in Retransmission revenue, we estimate that total Television revenue declined roughly 10% in 2023.

We believe that revenue trends will improve in 2024 for the TV industry, supported by an influx of Political advertising and moderating trends in core National advertising. Nonetheless, given the exceptional Political advertising year that is expected, core advertising is expected to decline in 2024, with some advertising being displaced by the large volume of Political. We anticipate that Core advertising will decline roughly 2.3% in 2024, with total TV advertising up nearly 30% (reflective of the influx of Political). Total Television revenue, which includes Retransmission revenues, are expected to increase roughly 20%.

We believe that the TV industry has some long term fundamental headwinds, which include continued weak audience trends, cord cutting (which adversely affects Retransmission revenue growth opportunities), and shifts in National advertising toward Digital and Influence Marketing. Offsetting these trends are Connected TV and prospects for new revenue opportunities offered by the new broadcast standard, ATSC 3.0. Importantly, the very high margin Political advertising every even year allows the industry to reduce debt and/or return capital to shareholders.

Our closely followed Television companies, E.W. Scripps and Gray TV, are among the two companies best positioned to benefit for the influx of Political advertising. Both are in swing markets that should disproportionately benefit from Political. In the case of E.W. Scripps, the company has a developed business model that benefits from cord cutting as consumers switch toward Connected TV and Over The Air Networks. Furthermore, in 2024, E.W. Scripps will benefit from double digit growth in Retransmission revenue as 75% of its subscribers have been renegotiated at significantly higher rates. Both companies, E.W. Scripps and Gray, are highly debt levered. As such, we believe that paring down debt should improve the equity value of the shares in 2024. In addition, we believe that both companies have compelling stock valuations. While the SSP and the GTN shares trade near the industry averages, the industry averages are well below past cycles. We would look for multiple expansion as economic prospects improve. At the same time, as free cash flow improves from high margin Political advertising, debt reduction should allow for a swing toward improved equity values. As such, the shares of SSP and GTN represent a compelling way to play both an improved economic outlook towards the second half of 2024 and influx of high margin Political advertising. Again, SSP has the benefit of strong growth of Retransmission revenue, as well.

E.W. Scripps (SSP): One of the nation’s largest TV station broadcasters and unique play on the trend toward cable cord cutting. Scripps has nationwide over the air networks that can be viewed with a digital antennae that do not require a cable or satellite service. Given its orientation toward national networks, the company is expected to disproportionately benefit from the influx of national advertising. In addition, the company’s TV stations are located in swing States and in hotly contested markets that should benefit from the influx of Political advertising in 2024. We believe the level of Political will be closely watched by investors as the high margin Political advertising will allow the company to aggressive pare down debt, assuaging investor concerns over its current leverage. For research reports and important disclosures, please click here.

Gray Television (GTN): One of the nation’s largest television broadcasters, the company has historically led the industry in terms of revenue and disproportionately benefits from the influx of Political advertising. In addition, the company is expected to benefit in 2024 from its investment in the development of its studios in the Atlanta area called Assembly Atlanta. The company has yet to disclose the full benefit of the current lease arrangement. We believe that the value of the development and the stream of lease payments are not fully reflected in the current stock valuation. Furthermore, the company is expected to aggressively pare down debt through the influx of high margin Political advertising and the lease payments. In our view, the shares should react well to debt reduction. For research reports and important disclosures, please click here.

Figure #8 TV Industry Comparables

Source: Noble estimates & Company filings

Radio Broadcast

Debt Struggles

Based on our estimates and our closely followed companies, Radio advertising is expected to have decreased 5.5% for the full year 2023. Illustrated in Figure #9 Radio Advertising Revenue. This decline reflected the adverse impact of rising interest rates and significant inflation, which hurt many consumer oriented advertising categories, as well as financials. In addition, we believe that Radio struggled with some headwinds from declines in listenership, as many consumers continue to work remotely post Covid pandemic. Local advertising was more resilient than National, which tends to be more economically sensitive. We estimate that Local advertising was down 6%, while National was down 19%. The results are expected to reflect the absence of Political advertising from the year earlier biennial elections. Digital advertising was a bright spot, increasing 6%, largely offsetting the decline in National revenue.

Figure #9 Radio Advertising Revenue

Source: Statista

Looking forward toward 2024, we expect Radio advertising trends to improve throughout the year, with the expectation that December 2023 may have been the trough for this economic cycle. Both Local and National advertisers should begin to anticipate improved economic conditions with the expectation that the Fed will lower interest rates late in the first quarter. Even though the economy is anticipated to continue to weaken in the first half 2024, advertisers may advertise to drive customer traffic and in anticipation of improved economic conditions. We anticipate that the year will start off weak, with the first quarter 2024 revenue expected to be down, but a more moderate decrease between 3% to 4%. Notably, the industry does not receive a significant amount of Political advertising in the first quarter.

In 2024, we expect consumer spending to soften, which will have an adverse affect on consumer oriented advertising, particularly Retail. Auto advertising is expected to buck that trend. In our view, auto manufacturers and dealers will likely step up advertising and promotions to lure consumers. Assuming lowered interest rates, we expect that Financial advertising should improve in the second half of the year, as well. Revenues are expected to be second half weighted, with improving core advertising trends and the benefit of the influx of Political advertising. Radio does not typically receive a significant amount of Political advertising, but it accounts for a meaningful 3% of total core advertising for the year. Political advertising largely falls in the third and fourth quarter. In addition, National advertising trends should improve in the second half as economic prospects improve. Digital advertising is expected to grow but more moderately than 2023, which is expected to be up 6%. We believe that Digital will increase near 5%, but some companies that have less developed Digital businesses, should report faster growth.

In total, based on our closely followed companies, we anticipate Radio revenue growth of 5.6% in 2024. Our estimate is inclusive of our Political advertising outlook.

We encourage investors to take a basket approach to investing in the industry, as most companies should benefit from the improving fundamentals in 2024. Below we have outlined some of the investment highlights for our closely followed Radio companies. In addition, Figure #10 Radio Industry Comparables highlight the stock valuations of the sector, which are currently trading at recession type valuations levels.

Beasley Broadcast (BBGI): We believe that the company will reflect above average revenue and cash flow growth in 2024 due to the prospect of fast growth of its developing Digital businesses. Digital accounted for roughly 20% of the company’s total revenues in 2023 and are expected to be a key revenue driver in 2024. In addition, the company’s stations are located in large, swing State markets and should benefit from the influx of Political advertising. The company does carry above average debt loads, but we expect that the company will pare down debt by roughly $20 million from current levels. The company’s target debt levels are $250 million by year end. For a Beasley Broadcast report and important disclosures, please click here.

Cumulus Media (CMLS): The company is viewed as a leveraged play on a recovery in National advertising. Given the company’s Network business, which is virtually all National advertising, roughly 50% of total company revenues are derived from National advertising. This is significantly higher than the industry average, which is roughly 12%. National advertising is expected to rebound as economic prospects improve in 2024. In addition, the company should disproportionately benefit from the influx of Political advertising. We estimate $23.5 million in high margin Political advertising, a 20% increase from the last Presidential election cycle, expected to total roughly 3.7% of 2024 advertising revenues. For research reports and important disclosures, please click here.

Entravision (EVC): Radio represents a small portion of total company revenues as the company has transitioned toward a Digital agency business model. Over 80% of total company revenues comes from its Digital businesses. As such, Entravision should grow faster than Radio industry averages as its Digital business is expected to grow. Furthermore, Entravision has one of the best balance sheets in the industry, expected to have virtually no net debt by year end. Finally, the EVC shares are among the cheapest in the industry, as highlighted in Figure # Radio Industry Comparables. For research reports and important disclosures, please click here.

Saga Communications (SGA): Historically, the company has led the industry in terms of revenue and cash flow growth. Over the past few years, it lost that honor as the industry moved to expand its fast growing digital operations. Most recently, Saga has regained its top spot as it has developed its Digital operations and non traditional radio revenue. While the industry has moved Digital to account for as much as 50% of total company revenues, Saga currently is at a more modest %. Nonetheless, its nascent Digital operations are growing at a rapid rate, allowing total company revenues to exceed industry averages. Saga has one of the best balance sheets in the industry, with a large cash position and virtually no debt. Furthermore, the company pays an attractive dividend, and, as such, represents an attractive total return potential. The SGA shares are largely undiscovered, trading at one of the cheapest stock valuation in the radio sector. For research reports and important disclosures, please click here.

Salem Media Group (SALM): Salem has a relatively stable Radio advertising business given its orientation toward the sale of long and short form block programming. Recently, the company tripped a debt covenant which created investor anxiety over its high debt leverage. The company recently announced that it plans to sell its Salem Church Products division for $30 million, it refinanced its revolver, and announced the sale of its money losing book publishing company, Regnery. In addition to these measures, the company has streamlined its management team and lowered costs. Recently, the company decided to delist, rather than seek alternatives to remain on its current exchange. In addition, the company has not closed on its planned sale of its Church Products division. As such, we believe that the company has significant hurdles to put itself on a path toward free cash flow generation and debt reduction. For research reports and important disclosures, please click here.

Townsquare Media (TSQ): Townsquare has led the charge toward a Digital transformation, with over 50% of its revenues from its Digital businesses. Importantly, its Digital businesses have margins are in line or better than its traditional Broadcast business. While a segment of its Digital business declined in 2023, we expect that it will regain its revenue momentum in 2024, particularly in the second half. At that time, the company is expected to benefit from an influx of high margin Political advertising, as well. We believe that the company has one of the best Digital strategies in the industry and is widely viewed as the model for other aspiring Digital divisions at other Radio companies. The shares trade below that of its industry peers, in spite of its above average revenue and cash flow growth. For research reports and important disclosures, please click here.

Figure #10 Radio Industry Comparables

Source: Noble estimates & Company filings

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

Internet & Digital Media Stocks – Investors Rewarded with Exceptional Returns in 2023