DENVER, Aug. 8, 2023 /CNW/ – Schwazze, (OTCQX: SHWZ) (NEO: SHWZ) (“Schwazze” or the “Company”), a multi-state operating cannabis company with assets in Colorado and New Mexico, announces the grand opening of its medical and recreational dispensary, R.Greenleaf Hobbs, which opened on Saturday, August 5, 2023. The new store is located at 1901 Joe Harvey Blvd #130 in Hobbs, NM 88240. Store operating hours are 8a to 11p Monday through Saturday; 8a to 8p on Sunday.

The R.Greenleaf Hobbs store opening continues the Company’s expansion throughout New Mexico and comes on the heels of eight additional R.Greenleaf store openings since Schwazze’s acquisition of the retail banner in February 2022. This opening along with the recent acquisition of Everest brings Schwazze’s total number of New Mexico retail dispensaries to 33. All locations serve the needs of medical patients as well as recreational adult-use consumers.

“We are excited to be a part of the growing cannabis community in New Mexico and to open an additional R.Greenleaf dispensary in the state. The team has been hard at work preparing to serve our customers in and around the city of Hobbs offering a wide variety of quality products serviced by dedicated, knowledgeable staff,” said Ken Bair, Senior Vice President of New Mexico Retail.

Since April 2020, Schwazze has acquired, opened, or announced the planned acquisition of 62 cannabis retail dispensaries (bannered as Star Buds, Emerald Fields, R. Greenleaf, Standing Akimbo, and Everest) as well as eight cultivation facilities and three manufacturing plants across Colorado and New Mexico. In May 2021, Schwazze launched its Biosciences division, and in August 2021 it commenced home delivery services in Colorado.

About Schwazze

Schwazze (OTCQX: SHWZ NEO: SHWZ) is building a premier vertically integrated regional cannabis company with assets in Colorado and New Mexico and will continue to take its operating system to other states where it can develop a differentiated regional leadership position. Schwazze is the parent company of a portfolio of leading cannabis businesses and brands spanning seed to sale. The Company is committed to unlocking the full potential of the cannabis plant to improve the human condition. Schwazze is anchored by a high-performance culture that combines customer-centric thinking and data science to test, measure, and drive decisions and outcomes. The Company’s leadership team has deep expertise in retailing, wholesaling, and building consumer brands at Fortune 500 companies as well as in the cannabis sector. Schwazze is passionate about making a difference in our communities, promoting diversity and inclusion, and doing our part to incorporate climate-conscious best practices.

Medicine Man Technologies, Inc. was Schwazze’s former operating trade name. The corporate entity continues to be named Medicine Man Technologies, Inc. Schwazze derives its name from the pruning technique of a cannabis plant to enhance plant structure and promote healthy growth.

Forward-Looking Statements

This press release contains “forward-looking statements.” Such statements may be preceded by the words “plan,” “will,” “may,” “continue,” “predicts,” or similar words. Forward-looking statements are not guarantees of future events or performance, are based on certain assumptions, and are subject to various known and unknown risks and uncertainties, many of which are beyond the Company’s control and cannot be predicted or quantified. Consequently, actual events and results may differ materially from those expressed or implied by such forward-looking statements. Such risks and uncertainties include, without limitation, risks and uncertainties associated with (i) our inability to manufacture our products and product candidates on a commercial scale on our own or in collaboration with third parties; (ii) difficulties in obtaining financing on commercially reasonable terms; (iii) changes in the size and nature of our competition; (iv) loss of one or more key executives or scientists; (v) difficulties in securing regulatory approval to market our products and product candidates; (vi) our ability to successfully execute our growth strategy in Colorado and outside the state, (vii) our ability to consummate the acquisition described in this press release or to identify and consummate future acquisitions that meet our criteria, (viii) our ability to successfully integrate acquired businesses, including the acquisition described in this press release, and realize synergies therefrom, (ix) the ongoing COVID-19 pandemic, * the timing and extent of governmental stimulus programs, and (xi) the uncertainty in the application of federal, state and local laws to our business, and any changes in such laws. More detailed information about the Company and the risk factors that may affect the realization of forward-looking statements is set forth in the Company’s filings with the Securities and Exchange Commission (SEC), including the Company’s Annual Report on Form 10-K and its Quarterly Reports on Form 10-Q. Investors and security holders are urged to read these documents free of charge on the SEC’s website at http://www.sec.gov. The Company assumes no obligation to publicly update or revise its forward-looking statements as a result of new information, future events or otherwise except as required by law.

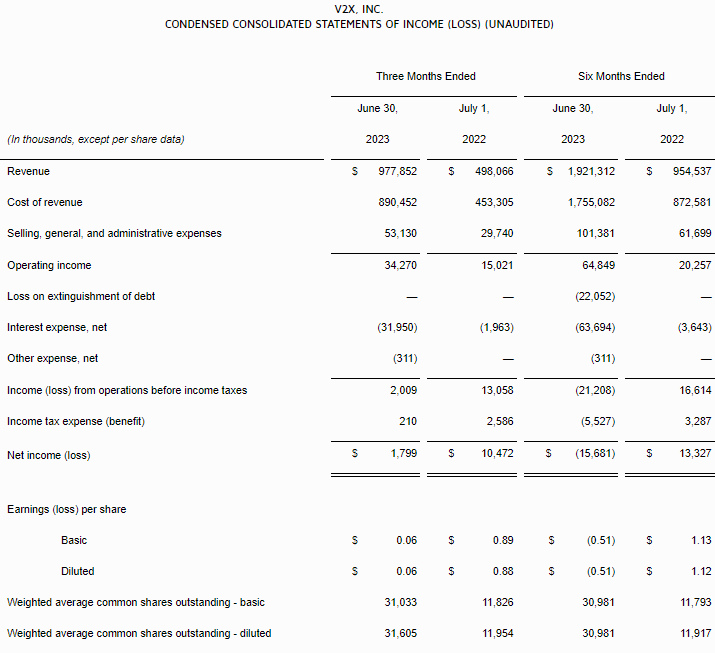

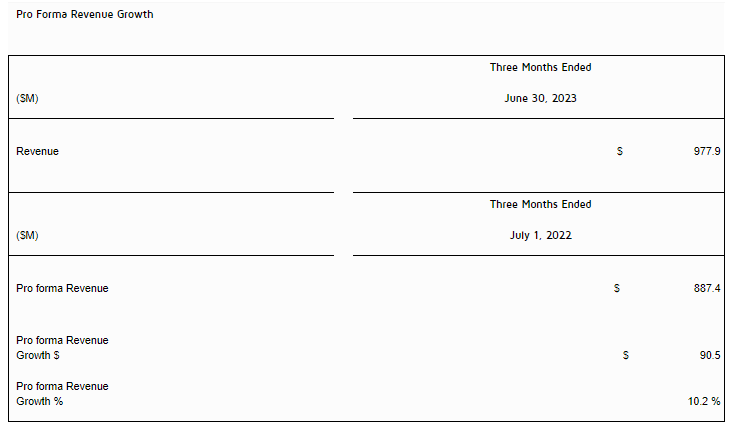

Revenue of $977.9 million, up 10.2% y/y on a pro forma basis

Awarded significant bookings of $2.1 billion, driving backlog +10% sequentially to $13.0 billion

Reported operating income of $34.3 million; adjusted operating income1 of $70.5 million

Adjusted EBITDA1 of $76.4 million with a margin1 of 7.8%

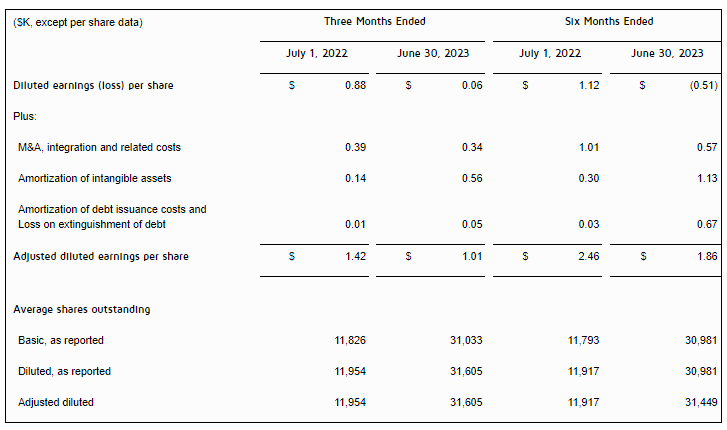

Diluted EPS of $0.06; adjusted diluted EPS1 of $1.01

Improved net debt to EBITDA1 leverage ratio ~0.4x to 3.48x

2023 Guidance:

Increasing mid-point of 2023 revenue, adjusted EBITDA1, and adjusted diluted EPS1 guidance

MCLEAN, Va., Aug. 8, 2023 /PRNewswire/ — V2X, Inc. (NYSE:VVX) announced second quarter 2023 financial results.

“V2X reported strong results in the second quarter with revenue increasing 10.2% year-over-year, on a pro forma basis,” said Chuck Prow, President and Chief Executive Officer of V2X. “Adjusted EBITDA1 for the quarter was $76.4 million and 7.8% margin resulting from solid revenue volume and benefits from program performance. Bookings activity in the quarter was strong at $2.1 billion in awards to V2X. This yielded total backlog of $13.0 billion, representing 10% growth sequentially. Our new business and recompete wins in addition to scope expansion on existing programs bolster our backlog position and set us up for positive momentum leading into 2024. Furthermore, with over $5 billion in bids under evaluation and a 12-month pipeline of ~$19 billion, the outlook for V2X remains robust.”

“Revenue growth in the quarter was generated by continued expansion on existing programs, contribution from new awards, as well as success in securing recompete wins late last year and in early 2023,” said Mr. Prow. “Our teams continued to further drive momentum by successfully expanding work scope on our core programs. Several notable wins late last year and in the first half of 2023 have also helped to push revenue growth. We continue to experience growth in the Pacific or INDOPACOM, and see significant long-term opportunity to further support increasing mission requirements in the region.”

Mr. Prow continued, “We were successful in capturing several key new business pursuits during the quarter. First, we were awarded a $100 million five-year task order with the Department of State to provide logistics support internationally. This represents our most substantive and strategic win with the Department of State and is the culmination of a multi-year client engagement and targeted growth campaign. Our agility and high level of readiness to support mission requirements was a key strategic differentiator for V2X in this award. Looking ahead, we see significant opportunity to leverage our comprehensive capabilities and footprint to further support the global missions of this important client. I am also pleased to announce that we are seeing results executing our sell through business model, which is leveraging our highly technical, development, integration, production, and modernization capabilities. During the quarter, V2X finalized three separate efforts with new clients that utilize our engineering, integration and manufacturing capabilities. We were also awarded an engineering development and prototyping effort with a new client that we believe will lead to new proprietary products with enduring follow-on business.”

“In addition to new awards, during the second quarter, we were awarded over $520 million in recompetes,” said Mr. Prow. “This includes an eight-year, $328 million contract with Naval Facilities Systems Command (NAVFAC) Southeast in support of the Naval Station at Guantanamo Bay. This contract includes all aspects of infrastructure sustainment, including the application of our unique converged solutions. We also secured a five-year recompete contract valued at over $122 million with NAVAIR Fleet Readiness Center Southwest for depot level maintenance support services. Transition to the new contract started in early July. These two recompete wins, along with our first quarter win of Naval Test Wing Pacific reflect the realization of our deliberate growth-oriented client campaign. These efforts are yielding growth, which further diversify our client portfolio. We are thrilled to have been selected for these important programs and remain focused on helping the Navy succeed with the missions that they serve.”

Mr. Prow concluded, “We are harnessing the combined solutions of V2X and are seeing momentum that we believe will drive growth and create value. For example, V2X’s robust modernization and sustainment capabilities are a significant differentiator and we are making excellent progress leveraging our engineering and manufacturing center of excellence. This includes opportunities such as modernizing and improving the effectiveness of the F-16 Fighting Falcon and further expanding our proprietary Gateway Mission Router 1000 across various platforms to provide cutting edge situational awareness in support of the DoD’s Joint All Domain Command and Control (JADC2) effort.”

Second Quarter 2023 Results

On July 5, 2022 (“Closing Date”), Vectrus, Inc. (“Vectrus”) completed its merger (the “Merger”) with Vertex Aerospace Services Holding Corp. (“Vertex”), thereby forming V2X, Inc. Second quarter 2022 “reported results” reflect the contributions of Vectrus from April 1, 2022, through June 30, 2022, unless otherwise noted. Comparisons to historical periods are relative to legacy Vectrus results, unless otherwise noted.

Revenue of $977.9 million, up 10.2% y/y on a pro forma basis

Operating income of $34.3 million, including merger and integration related costs of $13.6 million, and amortization of acquired intangible assets of $22.6 million

Adjusted operating income1 of $70.5 million

Adjusted EBITDA1 of $76.4 million with a 7.8% adjusted EBITDA margin1

Diluted EPS of $0.06

Adjusted diluted EPS1 of $1.01

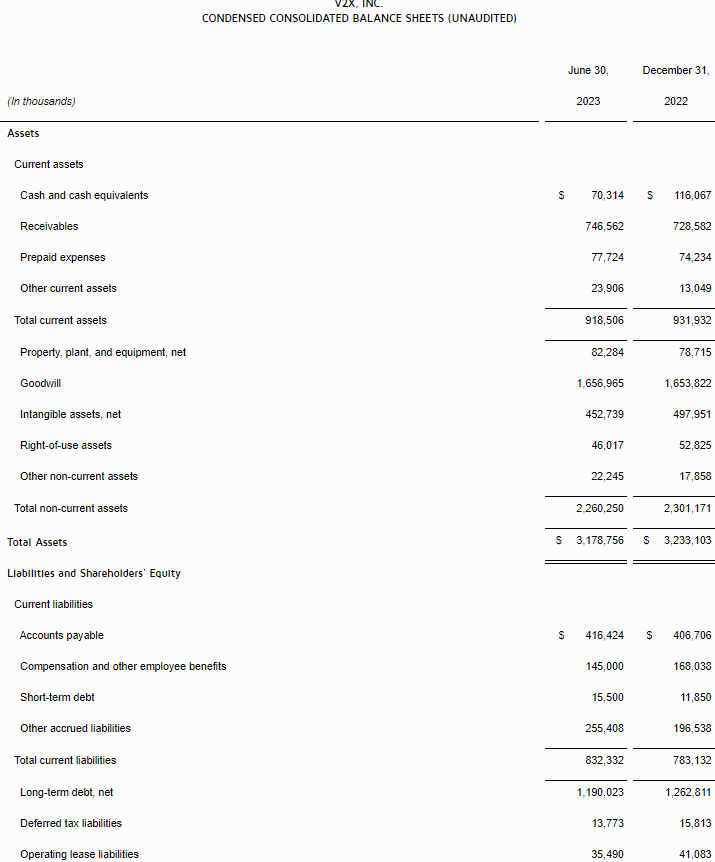

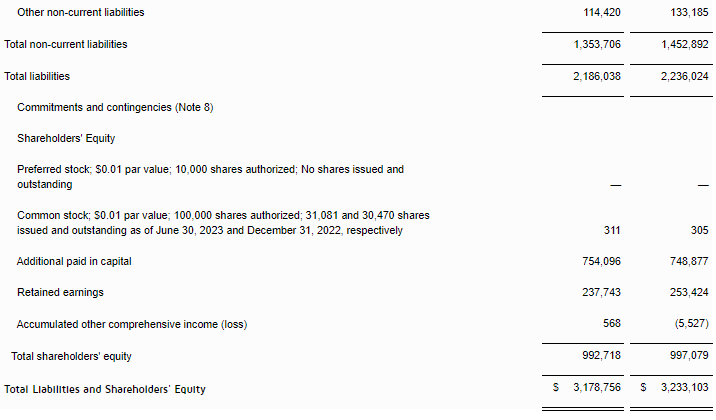

Net debt as of June 30, 2023 of $1,176.6 million

Total backlog as of June 30, 2023 of $13.0 billion

“Our financial results for the second quarter were impressive across the board,” said Susan Lynch, Senior Vice President and Chief Financial Officer. “Pro forma revenue increased 10.2% year-over-year to $977.9 million. Revenue growth was achieved via expansion on existing programs, the contribution from new business wins awarded in late 2022 and securing key recompete programs in the first half of 2023. Advancing and protecting our core in addition to growth through new pursuit wins is fundamental to V2X delivering on its commitments. To date in 2023, we have witnessed an acceleration of deliverables that were originally contemplated to be recognized in the second half of the year. The results this quarter represent achievement of expanding in our core markets and capturing new business with approximately $900 million in new contract awards in the first half of 2023.”

For the quarter, the Company reported operating income of $34.3 million and adjusted operating income1 of $70.5 million. Adjusted EBITDA1 was $76.4 million with a margin of 7.8%. First quarter diluted EPS was $0.06, due primarily to merger and integration related costs, amortization of acquired intangible assets, and interest expense. Adjusted diluted EPS1 for the quarter was $1.01.

Ms. Lynch continued, “At the end of the quarter, net debt for V2X was $1,176.6 million, a $112 million reduction from the prior quarter. Net consolidated indebtedness to EBITDA1 (net leverage ratio) was 3.48x, representing a ~0.4x improvement over the prior quarter. We remain focused on reducing debt and expect that our leverage ratio will continue to improve in the second half of 2023.”

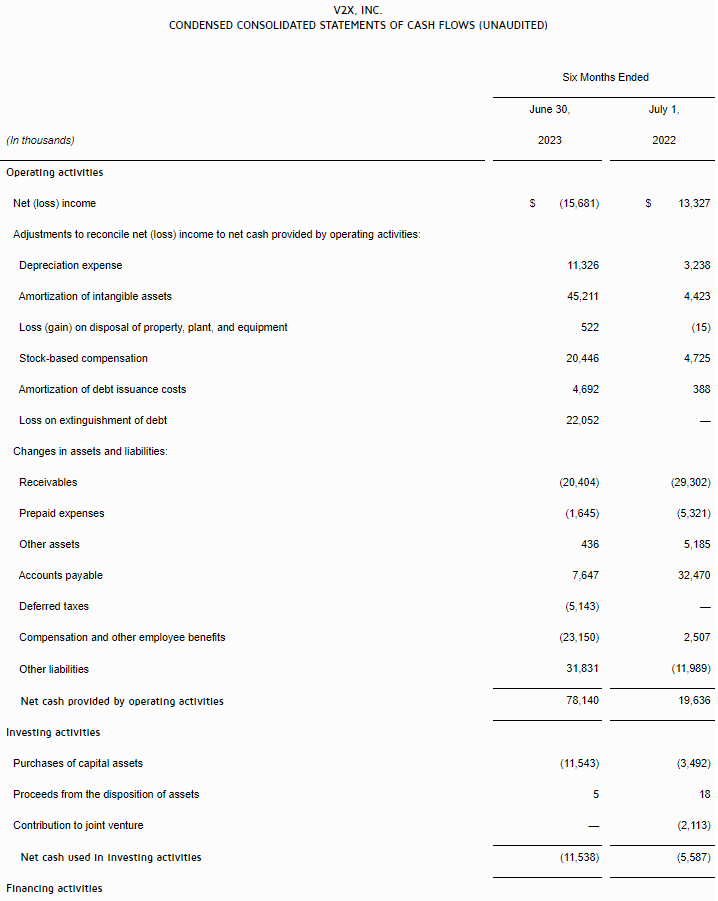

“Net cash provided by operating activities for the quarter was $116.6 million. Adjusted net cash provided by operating activities1 was $10.9 million, adding back $7.3 million of M&A and integration costs, and removing the contribution of the master accounts receivable purchase or “MARPA” facility of $113 million,” said Ms. Lynch.

Total backlog as of June 30, 2023, was $13.0 billion, increasing approximately $1.2 billion over last quarter reflecting successful expansion on existing programs along with significant new contract and recompete awards. Funded backlog was $3.1 billion. The trailing twelve-month book-to-bill was 1.3x.

2023 Guidance

Ms. Lynch concluded, “I am pleased with our results this quarter and for the first half of the year. Our teams continue to work together seamlessly, making notable progress on integration milestones while driving results across the board. As such, the Company is raising the mid-point of its 2023 revenue, adjusted EBITDA1, and adjusted diluted EPS1 guidance.” Guidance for 2023 is as follows:

$ millions, except for per share amounts

2023 Guidance (Updated)

2023 Mid-Point (Updated)

Revenue

$3,850

$3,950

$3,900

Adjusted EBITDA1

$295

$310

$303

Adjusted Diluted Earnings Per Share1

$3.85

$4.30

$4.08

Adjusted Net Cash Provided by Operating Activities 1

$115

$135

$125

Forward-looking statements are based upon current expectations and are subject to factors that could cause actual results to differ materially from those suggested here, including those factors set forth in the Safe Harbor Statement below.

Second Quarter 2023 Conference Call

Management will conduct a conference call with analysts and investors at 4:30 p.m. ET on Tuesday, August 8, 2023. U.S.-based participants may dial in to the conference call at 877-506-6380, while international participants may dial 412-542-4198. A live webcast of the conference call as well as an accompanying slide presentation will be available here: https://app.webinar.net/lZEXpEOLx9J

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through August 22, 2023, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 10179631.

Presentation slides that will be used in conjunction with the conference call will also be made available online in advance on the “investors” section of the company’s website at https://gov2x.com. V2X recognizes its website as a key channel of distribution to reach public investors and as a means of disclosing material non-public information to comply with its obligations under the U.S. Securities and Exchange Commission (“SEC”) Regulation FD.

Footnotes: 1 See “Key Performance Indicators and Non-GAAP Financial Measures” for descriptions and reconciliations.

About V2X

V2X builds smart solutions designed to integrate physical and digital infrastructure – from base to battlefield – by aligning people, actions, and outputs. Formed by the merger of Vectrus and Vertex, we bring a combined 120 years of successful mission support. Our lifecycle solutions improve security, streamline logistics, and enhance readiness.

The Company delivers a comprehensive suite of integrated solutions across the operations and logistics, aerospace, training, and technology markets to national security, defense, civilian and international clients. Our global team of approximately 15,000 employees brings innovation to every point in the mission lifecycle, from preparation to operations, to sustainment, as it tackles the most complex challenges with agility, grit, and dedication.

Safe Harbor Statement

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 (the “Act”): Certain material presented herein includes forward-looking statements intended to qualify for the safe harbor from liability established by the Act. These forward-looking statements include, but are not limited to, all the statements and items listed under “2023 Guidance” above and other assumptions contained therein for purposes of such guidance, other statements about our 2023 performance outlook, revenue, contract opportunities, and any discussion of future operating or financial performance.

Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “could,” “potential,” “continue” or similar terminology. These statements are based on the beliefs and assumptions of the management of the Company based on information currently available to management.

These forward-looking statements are not guarantees of future performance, conditions, or results, and involve a number of known and unknown risks, uncertainties, assumptions, and other important factors, many of which are outside our management’s control, that could cause actual results to differ materially from the results discussed in the forward-looking statements. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from the Company’s historical experience and our present expectations or projections. For a discussion of some of the risks and uncertainties that could cause actual results to differ from such forward-looking statements, see the risks and other factors detailed from time to time our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and other filings with the SEC.

We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Key Performance Indicators and Non-GAAP Measures

The primary financial performance measures we use to manage our business and monitor results of operations are revenue trends and operating income trends. Management believes that these financial performance measures are the primary drivers for our earnings and net cash from operating activities. Management evaluates its contracts and business performance by focusing on revenue, operating income, and operating margin. Operating income represents revenue less both cost of revenue and selling, general and administrative (SG&A) expenses. Cost of revenue consists of labor, subcontracting costs, materials, and an allocation of indirect costs, which includes service center transaction costs. SG&A expenses consist of indirect labor costs (including wages and salaries for executives and administrative personnel), bid and proposal expenses and other general and administrative expenses not allocated to cost of revenue. We define operating margin as operating income divided by revenue.

We manage the nature and amount of costs at the program level, which forms the basis for estimating our total costs and profitability. This is consistent with our approach for managing our business, which begins with management’s assessing the bidding opportunity for each contract and then managing contract profitability throughout the performance period.

In addition to the key performance measures discussed above, we consider adjusted net income, adjusted diluted earnings per share, adjusted operating income, adjusted EBITDA, adjusted EBITDA margin, adjusted operating cash flow, and pro forma revenue to be useful to management and investors in evaluating our operating performance, and to provide a tool for evaluating our ongoing operations. This information can assist investors in assessing our financial performance and measures our ability to generate capital for deployment among competing strategic alternatives and initiatives. We provide this information to our investors in our earnings releases, presentations, and other disclosures.

Adjusted net income, adjusted diluted earnings per share, adjusted operating income, adjusted EBITDA, adjusted EBITDA margin, adjusted operating cash flow, and pro forma revenue, however, are not measures of financial performance under GAAP and should not be considered a substitute for financial measures determined in accordance with GAAP. Definitions and reconciliations of these items are provided below.

Pro forma revenue is defined as the combined results of our operations for the three months ended June 30, 2023 and July 1, 2022 as if the Merger had occurred on January 1, 2021.

Adjusted operating income is defined as operating income, adjusted to exclude items that may include, but are not limited to, significant charges or credits, and unusual and infrequent non-operating items that impact current results but are not related to our ongoing operations, such as M&A, integration, and related costs.

Adjusted EBITDA is defined as operating income, adjusted to exclude depreciation and amortization of intangible assets, and items that may include, but are not limited to, significant charges or credits, and unusual and infrequent non-operating items that impact current results but are not related to our ongoing operations, such as M&A, integration, and related costs.

Adjusted EBITDA margin is defined as adjusted EBITDA divided by revenue.

Adjusted net income is defined as net income, adjusted to exclude items that may include, but are not limited to, significant charges or credits, and unusual and infrequent non-operating items that impact current results but are not related to our ongoing operations, such as M&A, integration and related costs, amortization of acquired intangible assets, amortization of debt issuance costs, and loss on extinguishment of debt.

Adjusted diluted earnings per share is defined as adjusted net income divided by the weighted average diluted common shares outstanding.

Cash interest, net is defined as interest expense, net adjusted to exclude amortization of debt issuance costs.

Adjusted operating cash flow is defined as net cash provided by (or used in) operating activities adjusted to exclude infrequent non-operating items, such as M&A payments and related costs.

In this document, the Company presents certain forward-looking non-GAAP metrics. The Company does not provide outlook on a GAAP basis because the items that the Company excludes from GAAP to calculate the comparable non-GAAP measure can be dependent on future events that are less capable of being controlled or reliably predicted by management and are not part of the Company’s routine operating activities. Additionally, management does not forecast many of the excluded items for internal use and therefore cannot create or rely on outlook done on a GAAP basis. The occurrence, timing, and amount of any of the items excluded from GAAP to calculate non-GAAP measures could significantly impact the Company’s fiscal 2023 GAAP results.

CONTACT:

V2X, Inc. Mike Smith, CFA 719-637-5773 ir@gov2x.com

President and Chief Operating Officer Thomas Tedford Appointed Chief Executive Officer Effective October 1, 2023; Boris Elisman to Continue as Executive Chairman Before Retiring in the first half of 2024

LAKE ZURICH, Ill,–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) (the “Company” or “ACCO Brands”), one of the world’s largest suppliers of select categories of branded academic, consumer and business products, today announced its Board of Directors has appointed the Company’s President and Chief Operating Officer, Thomas Tedford, as CEO effective October 1, 2023. Mr. Tedford has also been elected a member of the board effective that date. Mr. Tedford will succeed ACCO Brands current CEO, Boris Elisman, who will continue as Executive Chairman until his retirement in the first half of 2024. He has notified the Board that he will not stand for reelection at the 2024 stockholders’ meeting.

“The appointment of Tom as ACCO Brands next CEO is part of a succession plan that Boris and the Board have been preparing over the past few years,” stated Lead Independent Director, Thomas Kroeger. “We have worked closely with Tom and have full confidence in his commitment to creating value for our shareholders. He brings deep knowledge of our industry, our customers, the overall Company, and its operating segments to his new role. Tom has worked closely with Boris and the Board in developing and executing on the Company’s strategic transformation and will continue to do so, assuring a smooth and seamless transition of leadership and positioning us for profitable growth.”

“On behalf of everyone at ACCO Brands, we would like to thank Boris for his exemplary leadership and dedicated service as CEO. Boris’s innumerable contributions during his 18-year tenure, the last 10 leading the Company as CEO, have successfully expanded the growth opportunities for the Company,” Mr. Kroger concluded.

Mr. Elisman said, “During my tenure at ACCO Brands, the Company and the industry have undergone significant changes and I am proud of our teams’ accomplishments during this period. Having worked closely with Tom for many years, I know the company is in great hands to continue to progress and accelerate profitable growth. It has been my privilege to lead this great company, and I look forward to continuing to serve as Executive Chairman to ensure a smooth transition.”

Mr. Tedford commented, “It is an honor to have the opportunity to lead ACCO Brands and our talented team of dedicated employees as we build upon the current momentum in our business. Boris has been a great mentor and a tremendous leader. I have worked with him for more than a decade and appreciate his leadership and bold actions to transform ACCO Brands. I look forward to continuing to work closely with Boris to complete this leadership transition.”

“I am grateful for the support of our Board of Directors and am excited to work with them and our executive leadership team. I believe there are immense opportunities to enhance our leadership position in key categories, grow through share gains and new innovative product solutions, optimize our supply chain, and improve our margin profile as we remain focused on delivering shareholder value and customer satisfaction. Near-term we are committed to prioritizing our free cash flow towards supporting our dividend and debt reduction,” added Mr. Tedford.

Thomas Tedford Bio

Mr. Tedford joined ACCO Brands in 2010 and was named President and Chief Operating Officer in 2021. From 2011 to 2021, Mr. Tedford served first as Executive Vice President and President of ACCO Brands Americas ultimately becoming Executive Vice President and President, ACCO Brands, North America. During his tenure, he successfully led the operational, cultural and leadership integrations of key strategic acquisitions, the introduction of new products and the development of new markets. Prior to joining ACCO Brands, Mr. Tedford had 15 years of progressive sales, sales leadership, marketing, operational and executive management experience, operating in highly competitive and demanding industries. Mr. Tedford has expertise addressing complex challenges, optimizing performance, developing growth strategies, innovating product solutions, and building high-performing teams.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn, play, and thrive. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

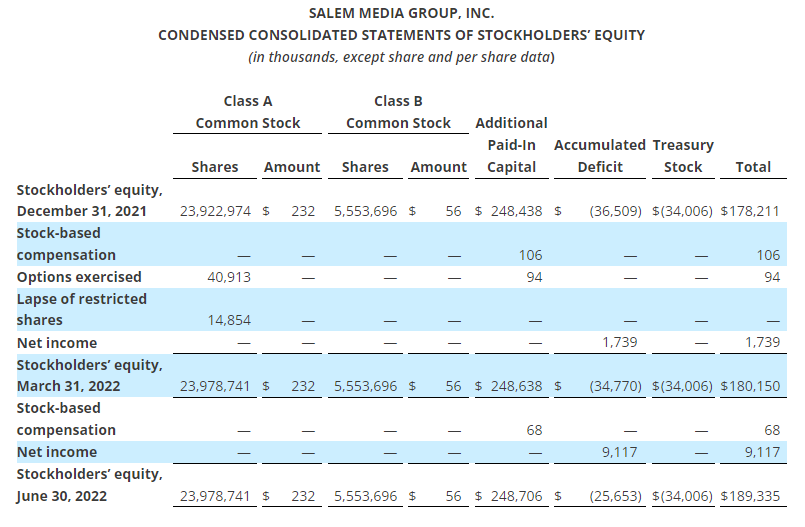

IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (the “company”) (Nasdaq: SALM) released its results for the three and six months ended June 30, 2023.

Second Quarter 2023 Results

For the three months ended June 30, 2023 compared to the three months ended June 30, 2022:

Consolidated

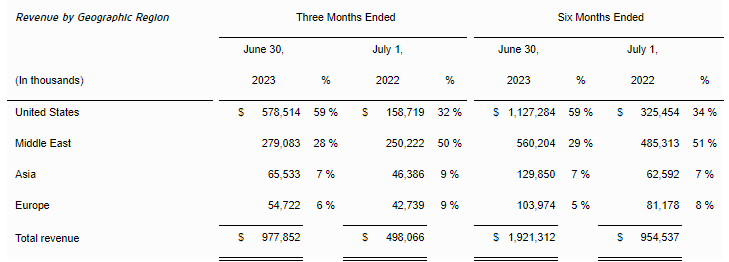

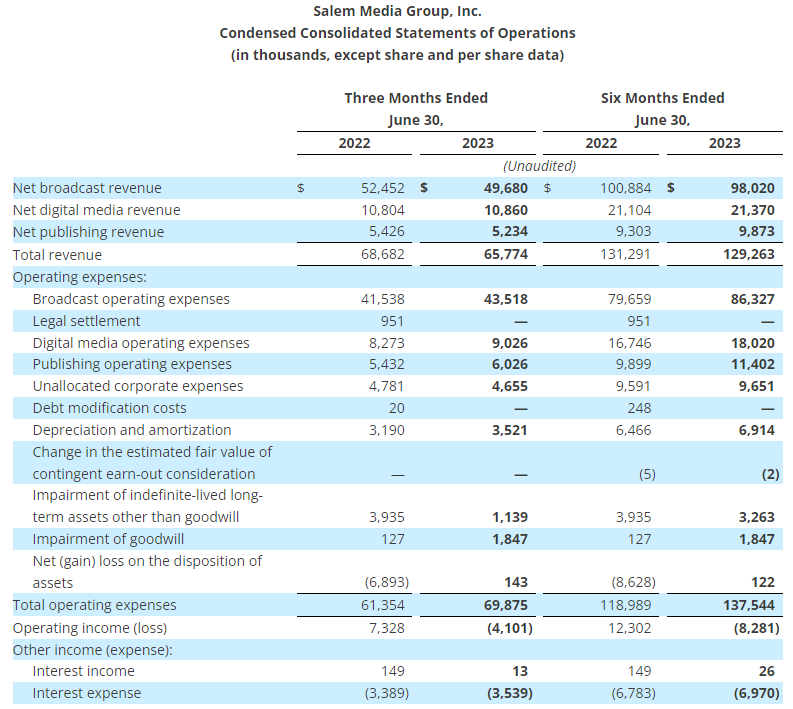

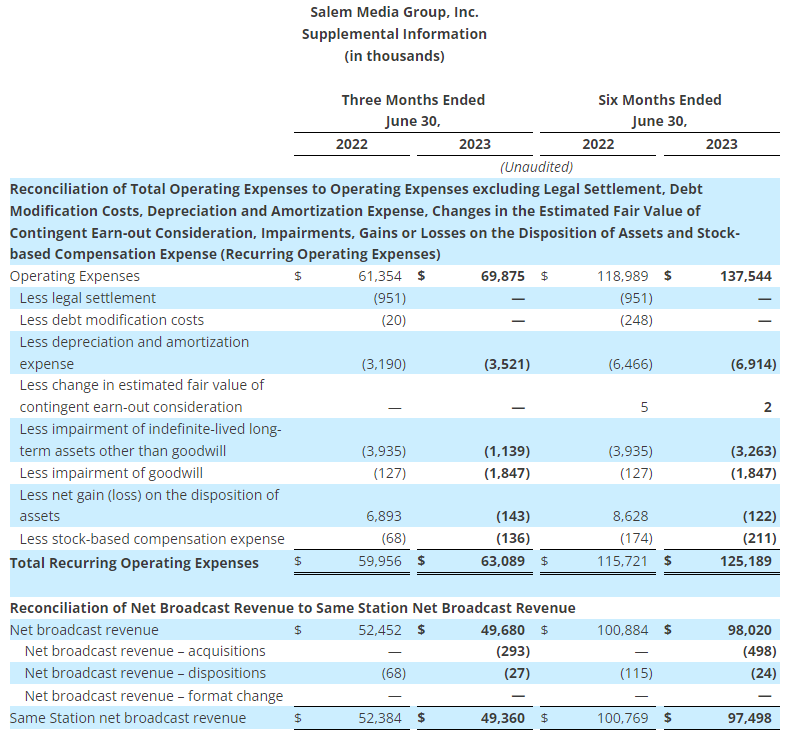

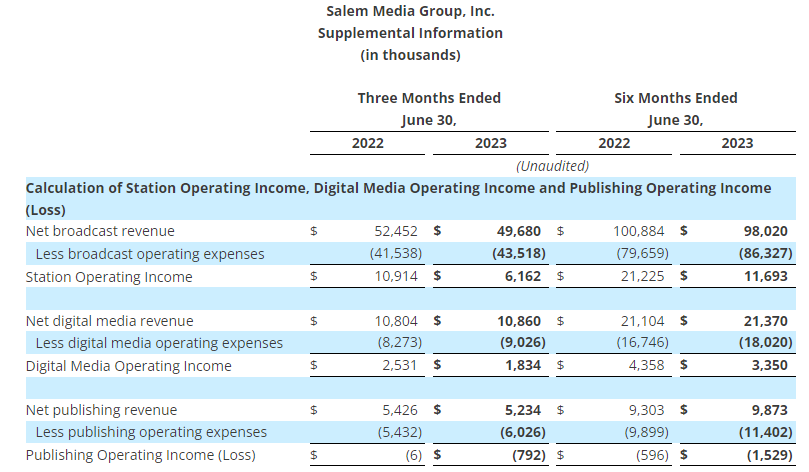

Total revenue decreased 4.2% to $65.8 million from $68.7 million;

Total operating expenses increased 13.9% to $69.9 million from $61.4 million;

Operating expenses, excluding stock-based compensation expense, debt modification costs, gains and losses on the sale or disposition of assets, impairments, depreciation expense and amortization expense (1) increased 5.2% to $63.1 million from $60.0 million;

The company had an operating loss of $4.1 million as compared to operating income of $7.3 million;

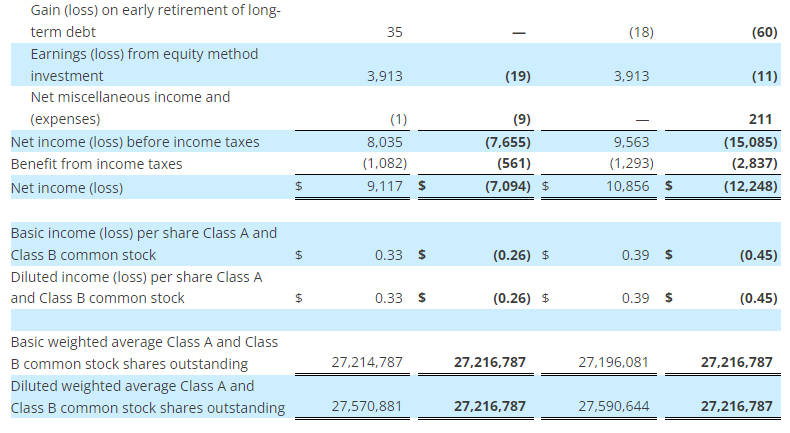

The company had a net loss of $7.1 million, or $0.26 net loss per share, compared to net income of $9.1 million, or $0.33 net income per diluted share;

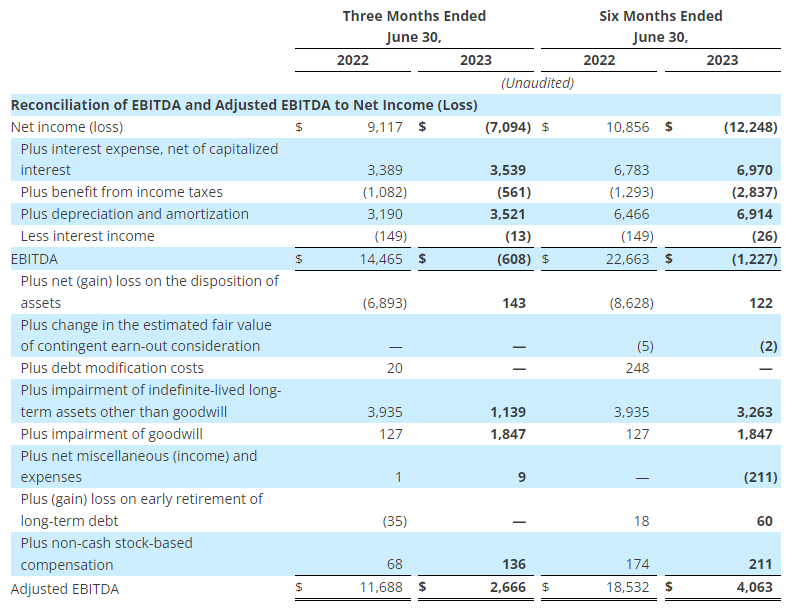

EBITDA (1) decreased to $(0.6) million from $14.5 million; and

Adjusted EBITDA (1) decreased 77.2% to $2.7 million from $11.7 million.

Broadcast

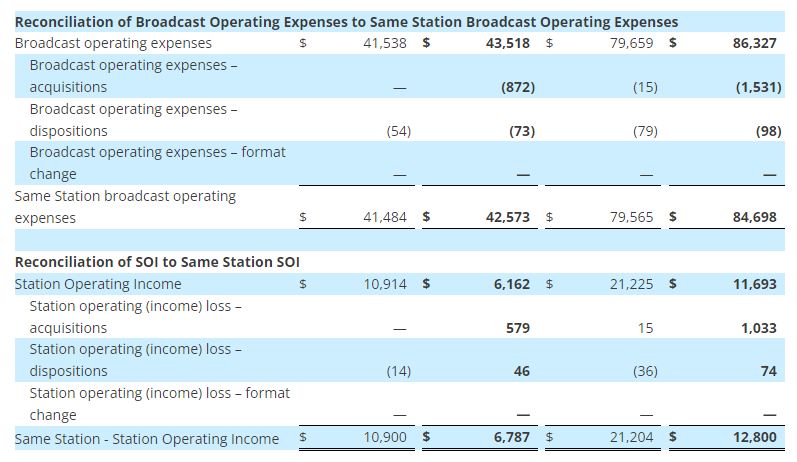

Net broadcast revenue decreased 5.3% to $49.7 million from $52.5 million;

Station Operating Income (“SOI”) (1) decreased 43.5% to $6.2 million from $10.9 million;

Same Station (1) net broadcast revenue decreased 5.8% to $49.4 million from $52.4 million; and

Same Station SOI (1) decreased 37.7% to $6.8 million from $10.9 million.

Digital Media

Digital media revenue increased 0.5% to $10.9 million from $10.8 million; and

Digital Media Operating Income (1) decreased 27.5% to $1.8 million from $2.5 million.

Publishing

Publishing revenue decreased 3.5% to $5.2 million from $5.4 million; and

Publishing Operating Loss (1) increased to $0.8 million from $6,000.

Included in the results for the three months ended June 30, 2023 are:

A $1.8 million ($1.4 million, net of tax, or $0.05 per share) impairment charge to the value of goodwill in Townhall;

A $1.1 million ($0.8 million, net of tax, or $0.03 per share) impairment charge to the value of broadcast licenses in Portland and San Francisco;

A $0.1 million ($0.1 million, net of tax) net loss on the disposition of assets; and

A $0.1 million non-cash compensation charge ($0.1 million, net of tax) related to the expense of stock options.

Included in the results for the three months ended June 30, 2022 are:

A $6.9 million ($5.1 million, net of tax, or $0.19 per diluted share) net gain on the disposition of assets reflects a $6.5 million pre-tax gain on the sale of land used in the company’s Denver, Colorado broadcast operations and a $0.5 million pre-tax gain on the sale of the company’s radio stations in Louisville, Kentucky that was offset by losses from various fixed asset disposals;

A $3.9 million ($2.9 million, net of tax, or $0.11 per share) impairment charge to the value of broadcast licenses in Columbus, Dallas, Greenville, Honolulu, Orlando, Portland, and Sacramento;

A $0.1 million ($0.1 million, net of tax) goodwill impairment charge; and

A $0.1 million ($0.1 million, net of tax) non-cash compensation charge related to the expense of stock options.

Per share numbers are calculated based on 27,216,787 diluted weighted average shares for the three months ended June 30, 2023, and 27,570,881 diluted weighted average shares for the three months ended June 30, 2022.

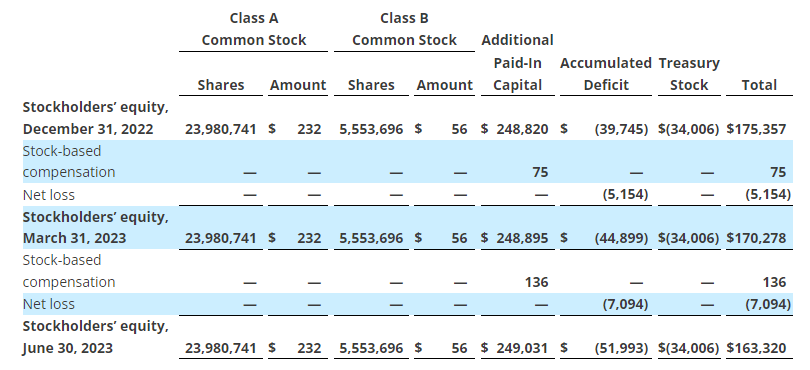

Year to Date 2023 Results

For the six months ended June 30, 2023 compared to the six months ended June 30, 2022:

Consolidated

Total revenue decreased 1.5% to $129.3 million from $131.3 million;

Total operating expenses increased 15.6% to $137.5 million from $119.0 million;

Operating expenses, excluding gains or losses on the disposition of assets, stock-based compensation expense, debt modification costs, changes in the estimated fair value of contingent earn-out consideration, impairments, depreciation expense and amortization expense (1) increased 8.2% to $125.2 million from $115.7 million;

The company had an operating loss of $8.3 million as compared to operating income of $12.3 million;

The company recognized $3.9 million in film distribution income from an unconsolidated equity investment in the six months ended June 30, 2022;

The company had a net loss of $12.2 million, or $0.45 net loss per share, compared to net income of $10.9 million, or $0.39 net income per diluted share;

EBITDA (1) decreased to $(1.2) million from $22.7 million; and

Adjusted EBITDA (1) decreased 78.1% to $4.1 million from $18.5 million.

Broadcast

Net broadcast revenue decreased 2.8% to $98.0 million from $100.9 million;

SOI (1) decreased 44.9% to $11.7 million from $21.2 million;

Same station (1) net broadcast revenue decreased 3.2% to $97.5 million from $100.8 million; and

Same station SOI (1) decreased 39.6% to $12.8 million from $21.2 million.

Digital media

Digital media revenue increased 1.3% to $21.4 million from $21.1 million; and

Digital media operating income (1) decreased 23.1% to $3.4 million from $4.4 million.

Publishing

Publishing revenue increased 6.1% to $9.9 million from $9.3 million; and

Publishing Operating Loss (1) increased 156.5% to $1.5 million from $0.6 million.

Included in the results for the six months ended June 30, 2023 are:

A $3.2 million ($2.4 million, net of tax, or $0.09 per share) impairment charge to the value of broadcast licenses in Miami, Portland and San Francisco;

A $1.8 million ($1.4 million, net of tax, or $0.05 per share) impairment charge to the value of goodwill in Townhall;

A $0.1 million loss on the early retirement of long-term debt associated with the 2024 Notes; and

A $0.2 million ($0.1 million, net of tax, or $0.01 per share) non-cash compensation charge related to the expense of stock options.

Included in the results for the six months ended June 30, 2022 are:

A $8.6 million ($6.4 million, net of tax, or $0.23 per diluted share) net gain on the disposition of assets relates primarily to the $6.5 million pre-tax gain on the sale of land used in the company’s Denver, Colorado broadcast operations, the $1.8 million pre-tax gain on sale of land used in the company’s Phoenix, Arizona broadcast operations, and $0.5 million pre-tax gain on the sale of the company’s radio stations in Louisville, Kentucky offset by various fixed asset disposals;

A $3.9 million ($2.9 million, net of tax, or $0.11 per share) impairment charge to the value of broadcast licenses in Columbus, Dallas, Greenville, Honolulu, Orlando, Portland, and Sacramento;

A $0.1 million ($0.1 million, net of tax) goodwill impairment charge;

A $0.2 million ($0.2 million, net of tax, or $0.01 per share) charge for debt modification costs; and

A $0.2 million ($0.1 million, net of tax) non-cash compensation charge related to the expense of stock options.

Per share numbers are calculated based on 27,216,787 diluted weighted average shares for the six months ended June 30, 2023, and 27,590,644 diluted weighted average shares for the six months ended June 30, 2022.

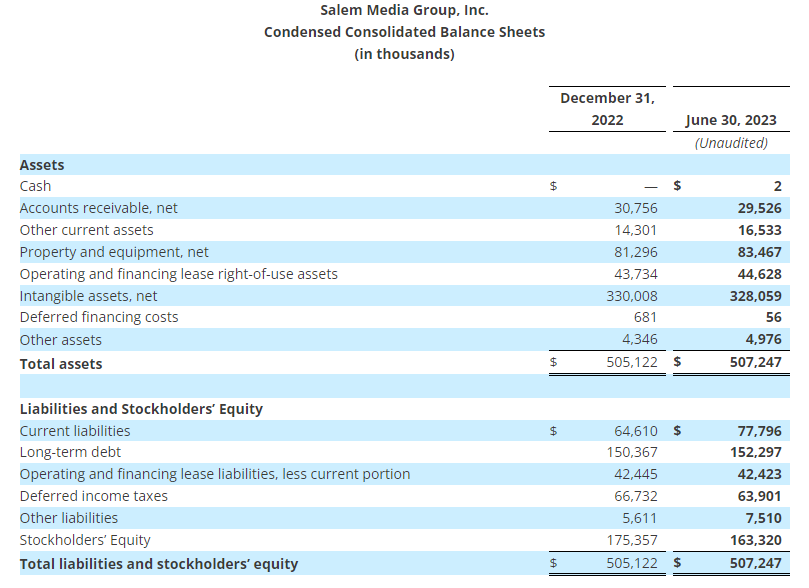

Balance Sheet

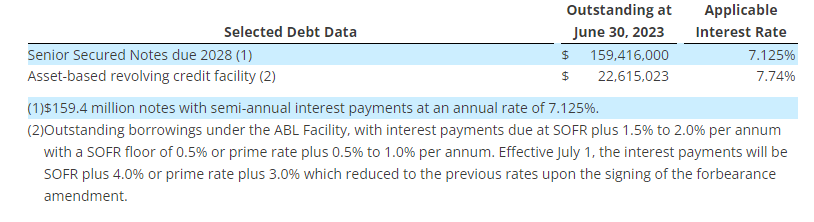

As of June 30, 2023, the company had $159.4 million outstanding on the 7.125% senior secured notes due 2028 (“2028 Notes”) and $22.6 million outstanding on the ABL facility.

Effective June 30, 2023, the company was not in compliance with its fixed charge coverage ratio. On August 7, 2023 the company signed a forbearance whereby the bank agreed not to exercise remedies on the default during the month of August. Additionally, the notional amount of the revolver was reduced from $30.0 million to $25.0 million with a minimum availability of $1.0 million. Finally, the interest rate associated with the revolver increased by two percentage points effective July 1, 2023 through the date of the forbearance amendment.

Acquisitions and Divestitures

The following transactions were completed since April 1, 2023:

On July 21, 2023 the company closed the sale of radio station KNTS-AM in Seattle, Washington for $0.2 million.

On July 13, 2023 the company closed the sale of radio station KLFE-AM in Seattle, Washington for $0.5 million. Radio station KLFE-AM was being programmed under a Time Brokerage Agreement (“TBA”) as of August 1, 2022.

On May 25, 2023, the company entered into a rental income purchase agreement with a related party to sell the assignment of the rents from its Greenville, South Carolina radio transmitter site for $3.5 million commencing on June 1, 2023 resulting in a pre-tax gain of $3.3 million.

Pending transactions:

On June 29, 2023 the company entered into an agreement to sell radio station KSAC-FM in Sacramento, California for $1.0 million subject to approval of the Federal Communications Commission (“FCC”). Radio station KSAC-FM will begin being programmed under a TBA on August 1, 2023. Based on its plan to sell the station, the company recorded an estimated pre-tax loss on the sale of assets of $3.3 million at June 30, 2023, reflecting the sales price as compared to the carrying value of the assets and the estimated cost to sell. The company expects to close the sale in the fourth quarter of this year.

Conference Call Information

The company will host a teleconference to discuss its results on August 8, 2023 at 4:00 p.m. Central Time. To access the teleconference, please dial (888) 770-7291, and then ask to be joined into the Salem Media Group Second Quarter 2023 call or listen via the investor relations portion of the company’s website, located at investor.salemmedia.com. A replay of the teleconference will be available through August 22, 2023 and can be heard by dialing (800) 770-2030, passcode 2413416 or on the investor relations portion of the company’s website, located at investor.salemmedia.com.

Follow us on Twitter @SalemMediaGrp.

Third Quarter 2023 Outlook

For the third quarter of 2023, the company is projecting total revenue to decline between 3% and 5% from the third quarter 2022 total revenue of $66.9 million. Excluding the impact of the 2022 political revenue, the company would project total revenue to decline between 1% and 3%. The company is also projecting operating expenses before gains or losses on the sale or disposal of assets, stock-based compensation expense, legal settlement, changes in the estimated fair value of contingent earn-out consideration, impairments, depreciation expense and amortization expense (“Recurring Operating Expenses”) to be between a decrease of 1% and increase of 2% compared to the third quarter of 2022 Recurring Operating Expenses of $60.8 million.

A reconciliation of Recurring Operating Expenses (a non-GAAP measure) to the most directly comparable GAAP measure is not available without unreasonable efforts on a forward-looking basis due to the potential high variability, complexity and low visibility with respect to the charges excluded from this non-GAAP financial measure, in particular, the change in the estimated fair value of earn-out consideration, impairments and gains or losses from the disposition of fixed assets. The company expects the variability of the above charges may have a significant, and potentially unpredictable, impact on its future GAAP financial results.

About Salem Media Group, Inc.

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape. Learn more about Salem Media Group, Inc. at www.salemmedia.com, Facebook and Twitter.

Forward-Looking Statements

Statements used in this press release that relate to future plans, events, financial results, prospects or performance are forward-looking statements as defined under the Private Securities Litigation Reform Act of 1995. Actual results may differ materially from those anticipated as a result of certain risks and uncertainties, including but not limited to the ability of the company to close and integrate announced transactions, market acceptance of the company’s radio station formats, competition from new technologies, inflation and other adverse economic conditions, and other risks and uncertainties detailed from time to time in the company’s reports on Forms 10-K, 10-Q, 8-K and other filings filed with or furnished to the Securities and Exchange Commission. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The company undertakes no obligation to update or revise any forward-looking statements to reflect new information, changed circumstances or unanticipated events.

(1)

Regulation G

Management uses certain non-GAAP financial measures defined below in communications with investors, analysts, rating agencies, banks and others to assist such parties in understanding the impact of various items on its financial statements. The company uses these non-GAAP financial measures to evaluate financial results, develop budgets, manage expenditures and as a measure of performance under compensation programs.

The company’s presentation of these non-GAAP financial measures should not be considered as a substitute for or superior to the most directly comparable financial measures as reported in accordance with GAAP.

Regulation G defines and prescribes the conditions under which certain non-GAAP financial information may be presented in this earnings release. The company closely monitors EBITDA, Adjusted EBITDA, Station Operating Income (“SOI”), Same Station net broadcast revenue, Same Station broadcast operating expenses, Same Station Operating Income, Digital Media Operating Income, Publishing Operating Loss, and operating expenses excluding gains or losses on the disposition of assets, stock-based compensation, changes in the estimated fair value of contingent earn-out consideration, impairments, depreciation and amortization, all of which are non-GAAP financial measures. The company believes that these non-GAAP financial measures provide useful information about its core operating results, and thus, are appropriate to enhance the overall understanding of its financial performance. These non-GAAP financial measures are intended to provide management and investors a more complete understanding of its underlying operational results, trends and performance.

The company defines Station Operating Income (“SOI”) as net broadcast revenue minus broadcast operating expenses. The company defines Digital Media Operating Income as net Digital Media Revenue minus Digital Media Operating Expenses. The company defines Publishing Operating Loss as net Publishing Revenue minus Publishing Operating Expenses. The company defines EBITDA as net income before interest, taxes, depreciation, and amortization. The company defines Adjusted EBITDA as EBITDA before gains or losses on the disposition of assets, before debt modification costs, before changes in the estimated fair value of contingent earn-out consideration, before impairments, before net miscellaneous income and expenses, before (gain) loss on early retirement of long-term debt and before non-cash compensation expense. SOI, Digital Media Operating Income, Publishing Operating Loss, EBITDA and Adjusted EBITDA are commonly used by the broadcast and media industry as important measures of performance and are used by investors and analysts who report on the industry to provide meaningful comparisons between broadcasters. SOI, Digital Media Operating Income, Publishing Operating Loss, EBITDA and Adjusted EBITDA are not measures of liquidity or of performance in accordance with GAAP and should be viewed as a supplement to and not a substitute for or superior to its results of operations and financial condition presented in accordance with GAAP. The company’s definitions of SOI, Digital Media Operating Income, Publishing Operating Loss, EBITDA and Adjusted EBITDA are not necessarily comparable to similarly titled measures reported by other companies.

The company defines Same Station net broadcast revenue as broadcast revenue from its radio stations and networks that the company owns or operates in the same format on the first and last day of each quarter, as well as the corresponding quarter of the prior year. The company defines Same Station broadcast operating expenses as broadcast operating expenses from its radio stations and networks that the company owns or operates in the same format on the first and last day of each quarter, as well as the corresponding quarter of the prior year. The company defines Same Station SOI as Same Station net broadcast revenue less Same Station broadcast operating expenses. Same Station operating results include those stations that the company owns or operates in the same format on the first and last day of each quarter, as well as the corresponding quarter of the prior year. Same Station operating results for a full calendar year are calculated as the sum of the Same Station operating results for each of the four quarters of that year. The company uses Same Station operating results, a non-GAAP financial measure, both in presenting its results to stockholders and the investment community, and in its internal evaluations and management of the business. The company believes that Same Station operating results provide a meaningful comparison of period over period performance of its core broadcast operations as this measure excludes the impact of new stations, the impact of stations the company no longer owns or operates, and the impact of stations operating under a new programming format. The company’s presentation of Same Station operating results is not intended to be considered in isolation or as a substitute for the financial information prepared and presented in accordance with GAAP. The company’s definition of Same Station operating results is not necessarily comparable to similarly titled measures reported by other companies.

For all non-GAAP financial measures, investors should consider the limitations associated with these metrics, including the potential lack of comparability of these measures from one company to another.

The Supplemental Information tables that follow the condensed consolidated financial statements provide reconciliations of the non-GAAP financial measures that the company uses in this earnings release to the most directly comparable measures calculated in accordance with GAAP. The company uses non-GAAP financial measures to evaluate financial performance, develop budgets, manage expenditures, and determine employee compensation. The company’s presentation of this additional information is not to be considered as a substitute for or superior to the directly comparable measures as reported in accordance with GAAP.

The company defines EBITDA (1) as net income before interest, taxes, depreciation, and amortization. The table below presents a reconciliation of EBITDA (1) to Net Income (Loss), the most directly comparable GAAP measure. EBITDA (1) is a non-GAAP financial performance measure that is not to be considered a substitute for or superior to the directly comparable measures reported in accordance with GAAP. The company defines Adjusted EBITDA (1) as EBITDA (1) before gains or losses on the disposition of assets,before debt modification costs, before changes in the estimated fair value of contingent earn-out consideration, before impairments, before net miscellaneous income and expenses, before (gain) loss on early retirement of long-term debt, and before non-cash compensation expense. The table below presents a reconciliation of Adjusted EBITDA (1) to Net Income (Loss), the most directly comparable GAAP measure. Adjusted EBITDA (1) is a non-GAAP financial performance measure that is not to be considered a substitute for or superior to the directly comparable measures reported in accordance with GAAP.

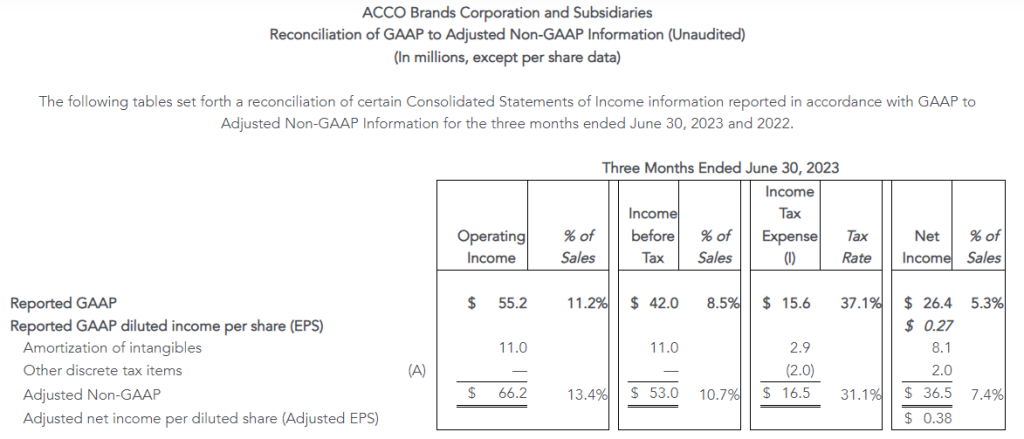

Reported net sales of $494 million, with gross margin expanding 450 basis points

Operating income of $55 million, flat to prior year; adjusted operating income of $66 million grew 14% year over year

EPS of $0.27; adjusted EPS of $0.38, above Company’s outlook

Net operating cash outflow improved $59 million year to date driven by improved working capital management

Maintains full year 2023 adjusted EPS outlook of $1.08 to $1.12

Raises full year 2023 free cash flow outlook to at least $110 million

Lowered end of year consolidated leverage ratio outlook

August 08, 2023 04:00 PM Eastern Daylight Time

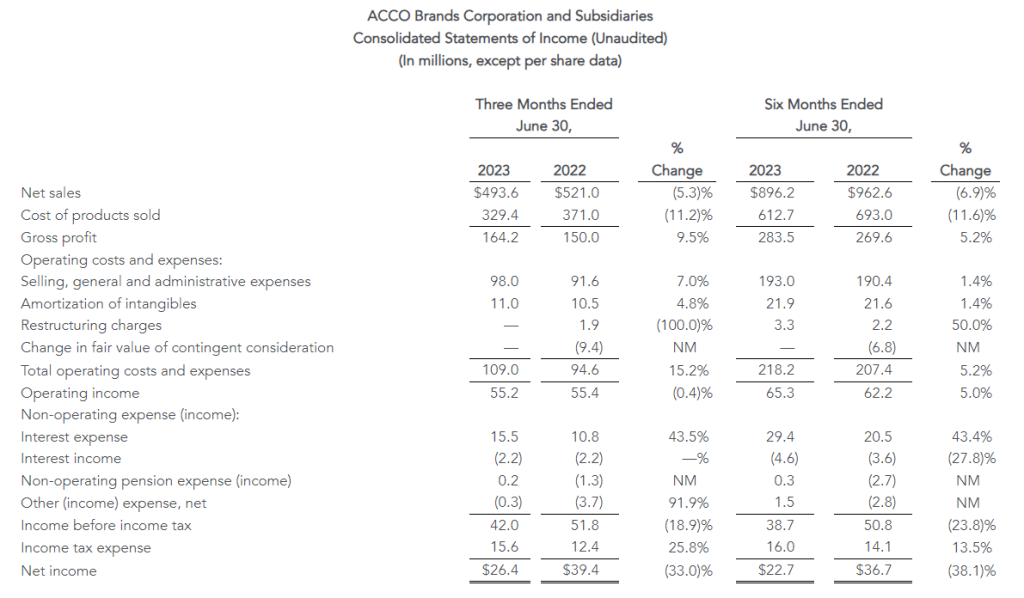

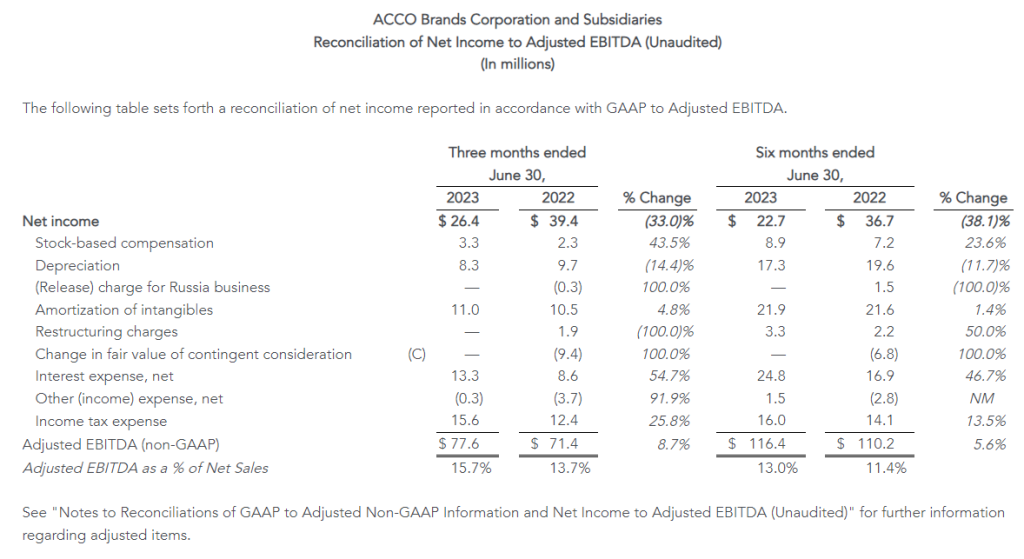

LAKE ZURICH, Ill.–(BUSINESS WIRE)–ACCO Brands Corporation (NYSE: ACCO) today announced its second quarter and first six-month results for the period ended June 30, 2023.

“Our top priority entering 2023 was to restore our margin profile, and I’m pleased to report that we have made great progress on that front in the first half. Second quarter and year-to-date gross margin expanded 450 and 360 basis points, respectively, due to greater traction from our pricing, productivity and restructuring initiatives. This has yielded much better than expected adjusted EPS. The higher operating profits experienced through the first six months give us confidence in our full year 2023 outlook for adjusted EPS and free cash flow. While we are pleased with the strong start of the year, we are more cautious on the second half demand environment. With improved working capital management, we are well positioned to end the year with a lower leverage ratio than previously expected. We remain committed to supporting our quarterly dividend and reducing debt with our strong cash flow” said Boris Elisman, Chairman and Chief Executive Officer of ACCO Brands.

“Our results reflect the resilience of our brands and the transformative actions undertaken to expand our product categories, broaden our geographic reach, bring innovative new consumer-centric products to market and streamline our cost structure. We remain confident that our strategy has us positioned to deliver sustainable organic growth as global economies improve,” concluded Mr. Elisman.

Second Quarter Results

Net sales declined 5.3 percent to $493.6 million from $521.0 million in 2022. Adverse foreign exchange reduced sales by $0.8 million, or 0.2 percent. Comparable sales fell 5.1 percent. Both reported and comparable sales declines were due to reduced volume, reflecting a more challenging macroeconomic environment, especially in our EMEA segment, and weaker global sales of computer accessories.

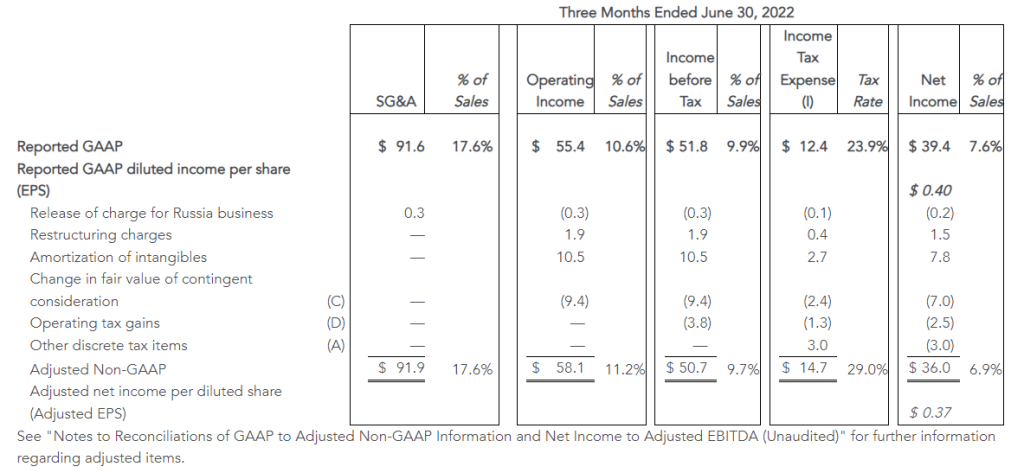

Operating income was $55.2 million versus $55.4 million in 2022. In 2022, operating income benefitted from income related to a change in the value of the PowerA contingent earnout of $9.4 million, partially offset by $1.9 million in restructuring charges. Adjusted operating income increased 14 percent to $66.2 million from $58.1 million in the prior year. This increase reflects improved gross margin from the effect of cumulative global pricing and cost reduction actions, partially offset by negative fixed cost leverage and higher SG&A expense primarily due to an increase in incentive compensation.

The Company reported net income of $26.4 million, or $0.27 per share, compared with prior year net income of $39.4 million, or $0.40 per share. Reported net income in 2023 reflects higher interest, tax and non-operating pension expenses. Reported net income in 2022 benefited from the items noted above in operating income. Adjusted net income was $36.5 million, or $0.38 per share, compared with $36.0 million, or $0.37 per share in 2022. Adjusted net income reflects the increase in adjusted operating income, partially offset by higher interest and non-operating pension expenses.

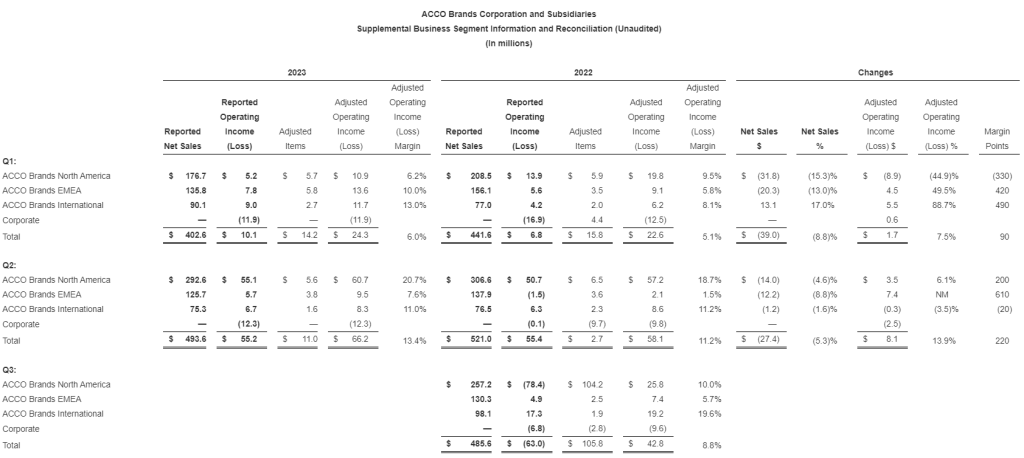

Business Segment Results

ACCO Brands North America – Secondquarter segment net sales of $292.6 million decreased 4.6 percent versus the prior year. Adverse foreign exchange reduced sales by 0.5 percent. Comparable sales of $294.2 million were down 4.1 percent. Both decreases reflect softer demand from business and retail customers due to a weaker macroeconomic environment and lower volumes for computer accessories. These factors more than offset stronger pricing, and volume growth in gaming accessories. Timing for some back-to-school sales was earlier than anticipated.

Second quarter operating income in North America was $55.1 million versus $50.7 million a year earlier, and adjusted operating income was $60.7 million compared to $57.2 million a year ago. Both increases reflect the benefit of pricing and cost actions and favorable mix, which more than offset the impact of lower sales and negative fixed cost leverage.

ACCO Brands EMEA – Secondquarter segment net sales of $125.7 million decreased 8.8 percent versus the prior year. Favorable foreign exchange increased sales by 0.3 percent. Comparable sales of $125.3 million decreased 9.1 percent versus the prior-year period. Both reported and comparable sales declines reflect reduced demand due to a weaker environment in the region and lower volumes for technology accessories. This more than offset the effect of cumulative pricing actions.

Second quarter operating income in EMEA was $5.7 million versus a loss of $1.5 million a year earlier, and adjusted operating income was $9.5 million compared to $2.1 million a year ago. The increases in both reported operating income and adjusted operating income reflect improved gross margins from the cumulative effect of price increases and cost savings actions more than offsetting negative fixed cost leverage.

ACCO Brands International – Secondquarter segment sales of $75.3 million decreased 1.6 percent versus the prior year. Favorable foreign exchange increased sales by 0.7 percent. Comparable sales of $74.8 million decreased 2.3 percent versus the year-ago period. Both sales decreases reflect lower volumes due to weaker economies in Asia and Australia, mostly offset by growth in Latin America.

Second quarter operating income in the International segment was $6.7 million versus $6.3 million a year earlier, with the increase due to lower restructuring expense. Adjusted operating income was $8.3 million compared to $8.6 million a year ago.

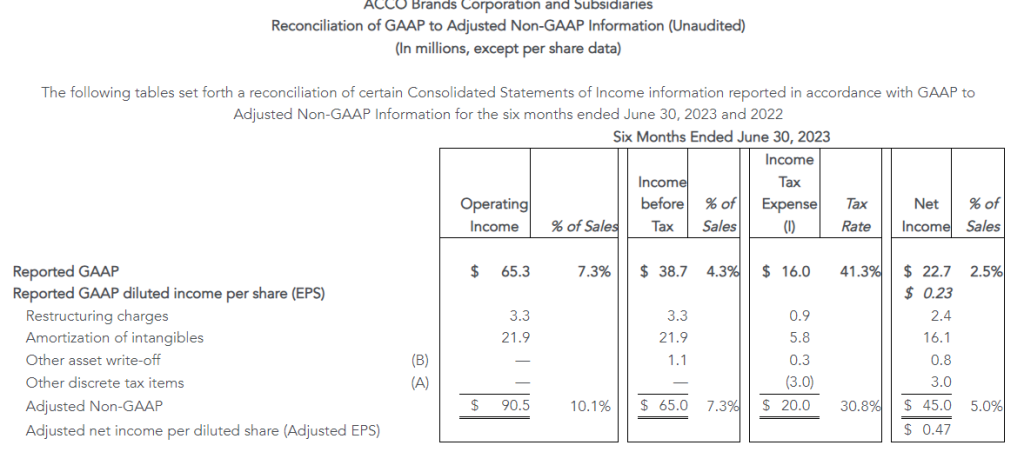

Six Month Results

Net sales decreased 6.9 percent to $896.2 million from $962.6 million in 2022. Adverse foreign exchange reduced sales by $11.4 million, or 1.2 percent. Comparable sales decreased 5.7 percent. Both reported and comparable sales declines reflect lower volume, especially in EMEA and North America due to the challenging macroeconomic environment, lower sales of technology accessories, and the timing of back-to-school shipments and lower channel inventory compared to a year ago. These more than offset the benefit of price increases across all segments, and volume growth in Latin America.

Operating income of $65.3 million compares to operating income of $62.2 million in 2022, which included a benefit of $6.8 million related to a change in the value of the PowerA contingent earnout. Adjusted operating income of $90.5 million increased from $80.7 million last year. Both reported and adjusted operating income increases reflect the benefit of global price increases and cost reduction initiatives, partially offset by higher SG&A expense primarily due to increased incentive compensation.

Net income was $22.7 million, or $0.23 per share, compared with net income of $36.7 million, or $0.37 per share, in 2022. Reported net income in 2023 reflects higher interest, tax and non-operating pension expenses. Reported net income in 2022 benefitted from the items noted above in operating income. Adjusted net income was $45.0 million, compared with $46.4 million in 2022, and adjusted earnings per share were $0.47 for both year periods. Adjusted net income reflects the increase in adjusted operating income offset by higher interest and non-operating pension expenses.

Capital Allocation and Dividend

Year to date, the Company improved its operating cash outflow by $58.6 million to $39.3 million versus $97.9 million in the prior year, driven primarily by improved working capital management. Adjusted free cash flow improved by $50.1 million and was an outflow of $45.4 million versus an outflow of $95.5 million a year earlier. Adjusted free cash flow in 2022 excludes the contingent earnout payment.

On August 1, 2023, ACCO Brands announced that its board of directors declared a regular quarterly cash dividend of $0.075 per share. The dividend will be paid on September 12, 2023, to stockholders of record at the close of business on August 22, 2023.

Full Year 2023 and Third Quarter Outlook

The Company is updating its full year 2023 outlook and providing a 3Q outlook. For the full year, reported sales are expected to be down 1 percent to 3 percent, including a 1.5 percent positive impact from foreign exchange. The Company is also maintaining its full year adjusted EPS outlook to be in the range of $1.08 to $1.12. Mid-teen growth in adjusted operating income is expected to be partially offset by higher interest and non-cash non-operating pension expenses. The Company is raising its 2023 free cash flow outlook to at least $110 million and expects to end the year with a consolidated leverage ratio of 3.3x to 3.5x, lower than previously expected.

In the third quarter, reported sales are expected to be flat to down 3 percent, which includes approximately a 4 percent positive impact from foreign exchange. Adjusted EPS is expected to be in the range of $0.21 to $0.24, which compares to $0.25 of adjusted EPS in the prior-year third quarter.

Webcast

At 8:30 a.m. ET on August 9, 2023, ACCO Brands Corporation will host a conference call to discuss the Company’s second quarter 2023 results. The call will be broadcast live via webcast. The webcast can be accessed through the Investor Relations section of www.accobrands.com. The webcast will be in listen-only mode and will be available for replay following the event.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn, play and thrive. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

Non-GAAP Financial Measures

In addition to financial results reported in accordance with generally accepted accounting principles (GAAP), we have provided certain non-GAAP financial information in this earnings release to aid investors in understanding the Company’s performance. Each non-GAAP financial measure is defined and reconciled to its most directly comparable GAAP financial measure in the “About Non-GAAP Financial Measures” section of this earnings release.

Forward-Looking Statements

Statements contained herein, other than statements of historical fact, particularly those anticipating future financial performance, business prospects, growth, strategies, business operations and similar matters, results of operations, liquidity and financial condition, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on the beliefs and assumptions of management based on information available to us at the time such statements are made. These statements, which are generally identifiable by the use of the words “will,” “believe,” “expect,” “intend,” “anticipate,” “estimate,” “forecast,” “project,” “plan,” and similar expressions, are subject to certain risks and uncertainties, are made as of the date hereof, and we undertake no duty or obligation to update them. Because actual results may differ materially from those suggested or implied by such forward-looking statements, you should not place undue reliance on them when deciding whether to buy, sell or hold the Company’s securities.

Our outlook is based on certain assumptions, which we believe to be reasonable under the circumstances. These include, without limitation, assumptions regarding the impact of the war in Ukraine; the impact of inflation and global economic uncertainties, fluctuations in foreign currency exchange rates and acquisitions; and the other factors described below.

Among the factors that could cause our actual results to differ materially from our forward-looking statements are: our ability to successfully execute our restructuring plans and realize the benefits of our productivity initiatives; our ability to obtain additional price increases and realize longer-term cost reductions; the ongoing impact of the COVID-19 pandemic; a relatively limited number of large customers account for a significant percentage of our sales; issues that influence customer and consumer discretionary spending during periods of economic uncertainty or weakness; risks associated with foreign currency exchange rate fluctuations; challenges related to the highly competitive business environment in which we operate; our ability to develop and market innovative products that meet consumer demands and to expand into new and adjacent product categories that are experiencing higher growth rates; our ability to successfully expand our business in emerging markets and the exposure to greater financial, operational, regulatory, compliance and other risks in such markets; the continued decline in the use of certain of our products; risks associated with seasonality; the sufficiency of investment returns on pension assets, risks related to actuarial assumptions, changes in government regulations and changes in the unfunded liabilities of a multi-employer pension plan; any impairment of our intangible assets; our ability to secure, protect and maintain our intellectual property rights, and our ability to license rights from major gaming console makers and video game publishers to support our gaming accessories business; continued disruptions in the global supply chain; risks associated with inflation and other changes in the cost or availability of raw materials, transportation, labor, and other necessary supplies and services and the cost of finished goods; risks associated with outsourcing production of certain of our products, information technology systems and other administrative functions; the failure, inadequacy or interruption of our information technology systems or its supporting infrastructure; risks associated with a cybersecurity incident or information security breach, including that related to a disclosure of personally identifiable information; our ability to grow profitably through acquisitions; our ability to successfully integrate acquisitions and achieve the financial and other results anticipated at the time of acquisition, including planned synergies; risks associated with our indebtedness, including limitations imposed by restrictive covenants, our debt service obligations, and our ability to comply with financial ratios and tests; a change in or discontinuance of our stock repurchase program or the payment of dividends; product liability claims, recalls or regulatory actions; the impact of litigation or other legal proceedings; our failure to comply with applicable laws, rules and regulations and self-regulatory requirements, the costs of compliance and the impact of changes in such laws; our ability to attract and retain qualified personnel; the volatility of our stock price; risks associated with circumstances outside our control, including those caused by public health crises, such as the occurrence of contagious diseases, severe weather events, war, terrorism and other geopolitical incidents; and other risks and uncertainties described in “Part I, Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2022, and in other reports we file with the Securities and Exchange Commission.

About Non-GAAP Financial Measures

We explain below how we calculate each of our non-GAAP financial measures and a reconciliation of our current period and historical non-GAAP financial measures to the most directly comparable GAAP financial measures follows.

We use our non-GAAP financial measures both to explain our results to stockholders and the investment community and in the internal evaluation and management of our business. We believe our non-GAAP financial measures provide management and investors with a more complete understanding of our underlying operational results and trends, facilitate meaningful period-to-period comparisons and enhance an overall understanding of our past and future financial performance.

Our non-GAAP financial measures exclude certain items that may have a material impact upon our reported financial results such as restructuring charges, transaction and integration expenses associated with material acquisitions, the impact of foreign currency exchange rate fluctuations and acquisitions, unusual tax items, goodwill impairment charges, and other non-recurring items that we consider to be outside of our core operations. These measures should not be considered in isolation or as a substitute for, or superior to, the directly comparable GAAP financial measures and should be read in connection with the Company’s financial statements presented in accordance with GAAP.

Our non-GAAP financial measures include the following:

Comparable Sales : Represents net sales excluding the impact of material acquisitions, if any, with current-period foreign operation sales translated at prior-year currency rates. We believe comparable sales are useful to investors and management because they reflect underlying sales and sales trends without the effect of material acquisitions and fluctuations in foreign exchange rates and facilitate meaningful period-to-period comparisons. We sometimes refer to comparable sales as comparable net sales.

Adjusted Selling, General and Administrative (SG&A) Expenses : Represents selling, general and administrative expenses excluding transaction and integration expenses related to material acquisitions. We believe adjusted SG&A expenses are useful to investors and management because they reflect underlying SG&A expenses without the effect of expenses related to acquiring and integrating acquisitions that we consider to be outside our core operations and facilitate meaningful period-to-period comparisons.

Adjusted Operating Income/Adjusted Income Before Taxes/Adjusted Net Income/Adjusted Net Income Per Diluted Share:Represents operating income, income before taxes, net income, and net income per diluted share excluding restructuring and goodwill impairment charges, the amortization of intangibles, the amortization of the step-up in value of inventory, the change in fair value of contingent consideration, transaction and integration expenses associated with material acquisitions, non-recurring items in interest expense or other income/expense such as expenses associated with debt refinancing, a bond redemption, or a pension curtailment, and other non-recurring items as well as all unusual and discrete income tax adjustments, including income tax related to the foregoing. We believe these adjusted non-GAAP financial measures are useful to investors and management because they reflect our underlying operating performance before items that we consider to be outside our core operations and facilitate meaningful period-to-period comparisons. Senior management’s incentive compensation is derived, in part, using adjusted operating income and adjusted net income per diluted share, which is derived from adjusted net income. We sometimes refer to adjusted net income per diluted share as adjusted earnings per share or adjusted EPS.

Adjusted Income Tax Expense/Rate:Represents income tax expense/rate excluding the tax effect of the items that have been excluded from adjusted income before taxes, unusual income tax items such as the impact of tax audits and changes in laws, significant reserves for cash repatriation, excess tax benefits/losses, and other discrete tax items. We believe our adjusted income tax expense/rate is useful to investors because it reflects our baseline income tax expense/rate before benefits/losses and other discrete items that we consider to be outside our core operations and facilitates meaningful period-to-period comparisons.

Adjusted EBITDA: Represents net income excluding the effects of depreciation, stock-based compensation expense, amortization of intangibles, the change in fair value of contingent consideration, interest expense, net, other (income) expense, net, and income tax expense, the amortization of the step-up in value of inventory, transaction and integration expenses associated with material acquisitions, restructuring and goodwill impairment charges, non-recurring items in interest expense or other income/expense such as expenses associated with debt refinancing, a bond redemption, or a pension curtailment and other non-recurring items. We believe adjusted EBITDA is useful to investors because it reflects our underlying cash profitability and adjusts for certain non-cash charges, and items that we consider to be outside our core operations and facilitates meaningful period-to-period comparisons.

Free Cash Flow/Adjusted Free Cash Flow: Free cash flow represents cash flow from operating activities less cash used for additions to property, plant and equipment. Adjusted free cash flow represents free cash flow, less cash payments made for contingent earnouts, plus cash proceeds from the disposition of assets. We believe free cash flow and adjusted free cash flow are useful to investors because they measure our available cash flow for paying dividends, funding strategic material acquisitions, reducing debt, and repurchasing shares.

Consolidated Leverage Ratio: Represents balance sheet debt, plus debt origination costs and less any cash and cash equivalents divided by adjusted EBITDA. We believe that consolidated leverage ratio is useful to investors since the company has the ability to, and may decide to use, a portion of its cash and cash equivalents to retire debt.

We also provide forward-looking non-GAAP comparable sales, adjusted earnings per share, free cash flow, adjusted free cash flow, adjusted EBITDA, and adjusted tax rate, and historical and forward-looking consolidated leverage ratio. We do not provide a reconciliation of these forward-looking and historical non-GAAP measures to GAAP because the GAAP financial measure is not currently available and management cannot reliably predict all the necessary components of such non-GAAP measures without unreasonable effort or expense due to the inherent difficulty of forecasting and quantifying certain amounts that are necessary for such a reconciliation, including adjustments that could be made for restructuring, integration and acquisition-related expenses, the variability of our tax rate and the impact of foreign currency fluctuation and material acquisitions, and other charges reflected in our historical results. The probable significance of each of these items is high and, based on historical experience, could be material.

Christopher McGinnis Investor Relations (847) 796-4320

For more than 70 years, Vectrus has provided critical mission support for our customers’ toughest operational challenges. As a high-performing organization with exceptional talent, deep domain knowledge, a history of long-term customer relationships, and groundbreaking technical expertise, we deliver innovative, mission-matched solutions for our military and government customers worldwide. Whether it’s base operations support, supply chain and logistics, IT mission support, engineering and digital integration, security, or maintenance, repair and overhaul, our customers count on us for on-target solutions that increase efficiency, reduce costs, improve readiness, and strengthen national security. Vectrus is headquartered in Colorado Springs, Colo., and includes about 8,100 employees spanning 205 locations in 28 countries. In 2021, Vectrus generated sales of $1.8 billion. For more information, visit the company’s website at www.vectrus.com or connect with Vectrus on Facebook, Twitter, and LinkedIn.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Another Excellent Quarter. Driven by expansion of existing programs, new awards, and recompete wins, V2X reported excellent results for 2Q23. Revenue of $977.9 million was up 10.2% on a pro forma basis, and well above our $905 million forecast. Adjusted EBITDA came in at $76.4 million, versus our $64.5 million estimate. Adjusted diluted EPS was $1.01 compared to our $0.74 estimate.

Opportunity Remains Robust. V2X was awarded approximately $2.1 billion of awards in the quarter, with a book-to-bill of 2.2x. Backlog grew 10% to $13 billion. The Company has $5 billion of bids awaiting award and we believe V2X is well positioned to win its fair share. The overall market opportunity exceeds $160 billion.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Soft Q2 results. Revenues of $65.8 million were better than our $64.2 million estimate, driven by improved Digital Media and Publishing revenue. Adj. EBITDA of $2.7 million was below our $3.8 million estimate, reflecting higher than expected expenses as the company continues heightened investments to ramp its digital businesses.

Lowering full year 2023 adj. EBITDA estimate. Flowing through the Q2 results and our Q3 and Q4 revisions, we are largely maintaining our full year 2023 revenue estimate at $261.6 million and lowering our full year 2023 adj. EBITDA estimate from $18.5 million to $16.1 million. We are maintaining our full year 2024 adj. EBITDA estimate of $26.9 million at this time, which conservatively anticipates an influx of roughly $6.8 million in high margin Political advertising.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Saga Communications, Inc. is a broadcast company whose business is primarily devoted to acquiring, developing and operating radio stations, television stations and state radio networks. Saga currently owns or operates broadcast properties in 26 markets, including 61 FM and 30 AM radio stations, 3 state radio networks, 2 farm radio networks, 5 television stations and 4 low power television stations. Saga’s strategy is to operate top billing radio and television stations in mid sized markets, defined as markets ranked (by market revenues) from 20 to 200. Saga’s radio stations employ a myriad of programming formats, including Classic Hits, Adult Contemporary, Active Rock, Oldies, News/Talk, Country and Classical. Saga’s television stations are affiliated with CBS and Fox in Joplin, MO; CBS in Greenville, MS; ABC, Fox, NBC, Telemundo and Univision in Victoria, TX. In operating its stations, Saga concentrates on the development of strong decentralized local management, which is responsible for the day-to-day operations of the stations in their market area and is compensated based on their financial performance as well as other performance factors that are deemed to effect the long-term ability of the stations to achieve financial objectives. Saga began operations in 1986 and became a publicly traded company in December 1992. The stock trades on the NYSE Amex under the ticker symbol “SGA”.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.