Humans are 8% Virus – How the Ancient Viral DNA in Your Genome Plays a Role in Human Disease and Development

HERVs, or human endogenous retroviruses, make up around 8% of the human genome, left behind as a result of infections that humanity’s primate ancestors suffered millions of years ago. They became part of the human genome due to how they replicate.

Like modern HIV, these ancient retroviruses had to insert their genetic material into their host’s genome to replicate. Usually this kind of viral genetic material isn’t passed down from generation to generation. But some ancient retroviruses gained the ability to infect germ cells, such as egg or sperm, that do pass their DNA down to future generations. By targeting germ cells, these retroviruses became incorporated into human ancestral genomes over the course of millions of years and may have implications for how researchers screen and test for diseases today.

Active Viral Genes in the Human Genome

Viruses insert their genomes into their hosts in the form of a provirus. There are around 30 different kinds of human endogenous retroviruses in people today, amounting to over 60,000 proviruses in the human genome. They demonstrate the long history of the many pandemics humanity has been subjected to over the course of evolution. Scientists think these viruses once widely infected the population, since they have become fixed in not only the human genome but also in chimpanzee, gorilla and other primate genomes.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Seth Blumsack, Professor of Energy and Environmental Economics and International Affairs, Penn State and Aidan Burn, PhD Candidate in Genetics, Tufts University.

Research from our lab and others has demonstrated that HERV genes are active in diseased tissue, such as tumors, as well as during human embryonic development. But how active HERV genes are in healthy tissue was still largely unknown.

To answer this question, our lab decided to focus on one group of HERVs known as HML-2. This group is the most recently active of the HERVs, having gone extinct less than 5 million years ago. Even now, some of its proviruses within the human genome still retain the ability to make viral proteins.

We examined the genetic material in a database containing over 14,000 donated tissue samples from all across the body. We looked for sequences that matched each HML-2 provirus in the genome and found 37 different HML-2 proviruses that were still active. All 54 tissue samples we analyzed had some evidence of activity of one or more of these proviruses. Furthermore, each tissue sample also contained genetic material from at least one provirus that could still produce viral proteins.

The Role of HERVs in Human Health and Disease

The fact that thousands of pieces of ancient viruses still exist in the human genome and can even create protein has drawn a considerable amount of attention from researchers, particularly since related viruses still active today can cause breast cancer and AIDS-like disease in animals.

Whether the genetic remnants of human endogenous retroviruses can cause disease in people is still under study. Researchers have spotted virus-like particles from HML-2 in cancer cells, and the presence of HERV genetic material in diseased tissue has been associated with conditions such as Lou Gehrig’s disease, or amyotrophic lateral sclerosis, as well as multiple sclerosis and even schizophrenia.

Our study adds a new angle to this data by showing that HERV genes are present even in healthy tissue. This means that the presence of HERV RNA may not be enough to connect the virus to a disease.

Importantly, it also means that HERV genes or proteins may no longer be good targets for drugs. HERVs have been explored as a target for a number of potential drugs, including antiretroviral medication, antibodies for breast cancer and T-cell therapies for melanoma. Treatments using HERV genes as a cancer biomarker will also need to take into account their activity in healthy tissue.

On the other hand, our research also suggests that HERVs could even be beneficial to people. The most famous HERV embedded in human and animal genomes, syncytin, is a gene derived from an ancient retrovirus that plays an important role in the formation of the placenta. Pregnancy in all mammals is dependent on the virus-derived protein coded in this gene.

Similarly, mice, cats and sheep also found a way to use endogenous retroviruses to protect themselves against the original ancient virus that created them. While these embedded viral genes are unable to use their host’s machinery to create a full virus, enough of their damaged pieces circulate in the body to interfere with the replication cycle of their ancestral virus if the host encounters it. Scientists theorize that one HERV may have played this protective role in people millions of years ago. Our study highlights a few more HERVs that could have been claimed or co-opted by the human body much more recently for this same purpose.

Unknowns Remain

Our research reveals a level of HERV activity in the human body that was previously unknown, raising as many questions as it answered.

There is still much to learn about the ancient viruses that linger in the human genome, including whether their presence is beneficial and what mechanism drives their activity. Seeing if any of these genes are actually made into proteins will also be important.

Answering these questions could reveal previously unknown functions for these ancient viral genes and better help researchers understand how the human body reacts to evolution alongside these vestiges of ancient pandemics.

Planning for a Changing Market Environment is Not Without Risks

There are two upcoming events, one scheduled and one not. They each have the potential and perhaps are even likely, to jolt or shift financial markets for a period longer than the ordinary disruptions traders and investors experience over the course of any month. These two items are the U.S. elections, which are approaching quickly, and a resolution of the Russia and Ukraine war.

Mid-Terms

On the U.S. side of the Atlantic, the mid-term election is thought of as a referendum on the person in the Oval Office and their party. The democrats who are in power in both legislative branches and also hold the executive branch are likely to lose the House and perhaps the Senate. The gridlock that would unfold if this occurs would include many government spending plans that have helped drive some investment sectors since January 2021. However, the party currently controlling both are viewed by many market participants as not “Wall Street-friendly,” so this could also weigh into market direction. And just as critical for investors, it would have the ability to shift which sectors are winners and which investments one may wish to lighten up in.

European War

In Europe, the war means a lot of things to those that live there. Focusing only from a global investor standpoint, one’s mind first turns to the energy sector. If the outcome is one where Russia largely has its way and annexes a large portion of Ukraine, how long would it take for normalcy to resume? And what would that look like? If, instead, Putin, who is leading the charge, loses power or his resolve, what would this mean for stocks, commodity prices, and overall investor mood? Should investors pre-think all scenarios and have a plan for each?

What Investment Experts Say

Channelchek spoke to a couple of highly respected, highly credentialed money managers and investment experts and asked about pre-planning.

Eric Lutton, CFA is Chief Investment Officer, at Sound Income Strategies. Eric doesn’t expect Putin to be removed, but cautions that if he is, depending on what follows, it may not automatically be good for markets. He said, “If Putin was “pushed” out of power, a highly unlikely scenario, but if it were to happen, it would mean more unknowns for the market, which would probably be taken as another negative.” Lutton, who has spent a great deal of time in Russia and Northern Europe, explains, “A vacuum of power in Russia would not be a good thing and could escalate the current situation.” Eric believes if a leader chosen by the West was installed, “inflation would fall, and the Fed could ease up on the rate increases.” Lutton does not think that is a scenario we will see any time soon.

The Sound Income Strategies CIO thinks the media overplays any real risk of Putin dropping a nuclear device so close to Russia on land it seeks to annex. But he did entertain the thought, as I pressured him for hypothetical scenario analysis and investment planning thoughts. “As for investors, if a bomb falls, either Putin or a false flag operation, you’d want to be in 100% cash! No place would be safe other than perhaps a handful of industrial defense or war contractors,” Said Eric Lutton.

As it relates to the November 8th mid-term elections, Eric Lutton isn’t expecting a huge “red wave” win. He points to the notion that there are people that would avoid voting red even if it was clear that the policies would better serve the populace. Eric does, however expect Republicans to gain a majority in the House and Senate. Even if they only gain a majority in one branch, Lutton says, “I do think there will be a slight pop in the market, but short-lived as the main factors will be the Fed, inflation, supply chain and ongoing conflict in Ukraine.”

Robert Johnson, PhD, CFA, CAIA, is the CEO and Chair at Economic Index Associates. He apologetically offered conventional wisdom, suggesting that it could be a mistake for investors to, “…concern themselves with broad market moves or the crisis du jour.” Johnson, instead, recommends more tried and true portfolio implementation. This includes suggesting the creation of an Investment Policy Statement (IPS). Dr. Johnson explains that clearly defining, in advance, and in accordance with one’s time horizon and other specifics, such as liquidity needs and tax situation, will define the ground rules necessary during temporary hiccups in the market.

As it relates to a personal investment policy statement, the Chair of Economic Index Associates says it is best to develop a policy statement in calm, less volatile markets. He says’ “The whole point of an IPS is to guide you through changing market conditions. It should not be changed as a result of market fluctuations.” He did allow for individual changes in circumstances,” It only needs to be revised when your individual circumstances change — perhaps a divorce or other unanticipated life change.”

As added testimony to what Dr. Johnson knew was less than groundbreaking thoughts on the subject of the two future events and what to do in each, he offered, “ I had a former co-worker who, in the run-up to the 2016 election, was convinced that Hillary Clinton was going to win and the stock market was going to crash. So, immediately prior to the election, he sold out of stocks and went to cash. Stocks surged the day following Trump’s victory, and my co-worker bought back into the market — at a higher price.”

Take-Away

Market hiccups are often short-lived.

While it is prudent to keep your eyes open and know what risks and potential rewards may be, it may also be smart to keep investing within specific boundaries. Those boundaries are best defined when volatility and predictability are average. Within the boundaries, there can be room to lighten up or overweight, but not in ways that pull the investor substantially out of line with their original goal while using the predefined arsenal of stocks, bonds, or other financial products.

If the U.S. Was in a Recession, This Week’s Numbers May Show It Has grown Out of It

A big focus of traders this week will be positioning for the FOMC meeting next week and its announcement on Wednesday, November 2nd. Members of the committee that have commented in recent weeks have left little doubt that the Federal Reserve’s fight against inflation is continuing, and a 75 bp hike can be expected. Additional comments on monetary policy from Fed governors aren’t expected this week as there is a communications blackout period in effect (midnight Saturday, October 22nd through midnight Thursday, October 27th).

There will be global interest rate commotion as more rate hikes outside the U.S. are likely. The first is on Wednesday by the Bank of Canada, followed on Thursday by the European Central Bank. The forecast consensus for each is 75bp upward.

The conversation on Thursday may move from “is the U.S. going into a recession to, has the U.S. just come out of a recession?” While the first two-quarters of receding growth have never officially been declared a recession, the first look at GDP for the third quarter is out on Thursday, and it is expected to show growth during the quarter. If this occurs markets, the stock market could trade, either way, a sigh of relief that the economy is growing or fear that the Fed now has the room it needs to keep applying the interest rate brakes.

What’s on Tap for investors:

Monday 10/24

• At 9:45 AM Purchasing Managers Index (PMI) flash report will be released. Expectations are for the number to come in around 51.2. This leading indicator of economic activity is an early estimate of private sector output. It contains information from surveys of around 1,000 manufacturing and service sector companies. The flash data are released ten days ahead of the final report and are based on 85 percent of the full survey.

Tuesday 10/25

• At 10:00 AM, the Consumer Confidence survey will be released. Expectations are for a decline of 2.0 points to 106.0 in October, this would be after it exceeded expectations in September and August.

• At 10 AM, the Richmond Fed Manufacturing Index will be reported. The consensus is -3. Last month the report came in at 0.0, which was above the consensus estimates. The headline index number is a composite of the new orders, shipments, and employment indexes in the Richmond Fed’s manufacturing sector. It provides insight into the state of the manufacturing sector.

• At 1 PM, U.S. Money Supply is released for September. During August M2 rose by $1.8 billion.

• Noble Capital Markets will host a roadshow in St. Louis with Harte Hanks (HHS). Qualified Investors of all levels, including registered representatives, are welcome to attend at no cost, and with no obligation to invest. More information here.

Wednesday 10/26

• At 8:30 AM, International Trade in Goods (advance) will be reported. The consensus is for a U.S. trade deficit of 87.8 billion. This would represent a widening of more dollars spent purchasing goods from abroad than goods purchased from the U.S. The numbers may offer insight into the impact that the strong dollar has had on reducing demand for U.S.-made products.

• At 8:30 AM, Wholesale Inventories (Advance) for September are expected to have shown an increase of 1.1%. If inventories are growing fast relative to GDP, then both production and employment may have to slow down the road. And if inventories are lagging behind growth, there may be an undersupply to be made up for later.

• At 10:00 PM, New Home Sales are expected to show a rate of 585 thousand during September. This number surprised to the upside the previous period. The report is important to those trading securities as it indicates economic momentum, future demand for goods, and confidence in the ability to afford a big expense. New home sales multiply through other areas of the economy as new homeowners set their homes with furniture, appliances, and services.

Thursday 10/27

• At 8:30 AM, investors will get their first look at GDP for the third quarter. The number is supposed to show the first sign of growth in 2022. Consensus expectations are for growth of 2.3% during the third quarter. Stock market investors may wrestle with whether the good news is bad news or bad news is good news as the market finds a direction after this report and ahead of a rate decision the following week.

• At 8:30 AM, Durable Goods Orders are released. The consensus is for a .6% increase in the headline number and .2% ex-transportation. Durable goods are new orders placed with U.S. manufacturers for factory hard goods. The report also contains information on shipments, unfilled orders, and inventories. Investors get insight into how busy factories will be in the coming months. This is a leading indicator with direct implications for economic growth

• At 8:30 AM Jobless Claims are reported for the week ending 10/22/22. The expectations are for there to be 223,000 new claims. Surprises on one side or the other are important as healthy employment is one the Federal Reserve mandates.

• At 10:30 AM, The U.S. Energy Information Administration (EIA) releases its weekly report on natural gas. Energy supply and demand balance impact prices of fuel that can ripple through the entire economy.

Friday 10/28

• At 8:30 AM, Personal Income and Outlays are reported. This report includes the PCE Price index that is considered to be the Feds preferred inflation indicator. The consensus for Personal Income is +.3%. The consensus for the PCE gauge is +.3% which would equate to a year-over-year inflation rate of +6.3%.

• At 10:00 AM, Consumer Sentiment is expected to come in at 59.7; the previous month the number reported was 59.8. Consumer spending accounts for 66% of the economy. Consumer appetite is a big influencer on investments. For stocks, strong economic growth translates to healthy corporate profits and higher stock prices. For bonds, the focus is whether economic growth goes overboard and leads to inflation.

What Else

It’s earnings season, and big market moves can occur should closely watch names miss their expected earnings numbers. On Tuesday this could include GE, Microsoft, and GM. Wednesday Ford reports, Thursday MacDonalds, Merck, Mastercard, and U.S. Steel. On Friday Exxon and Alliance Bernstein will make public their third quarter earnings.

Housing Is Getting Less Affordable. Governments Are Making It Worse

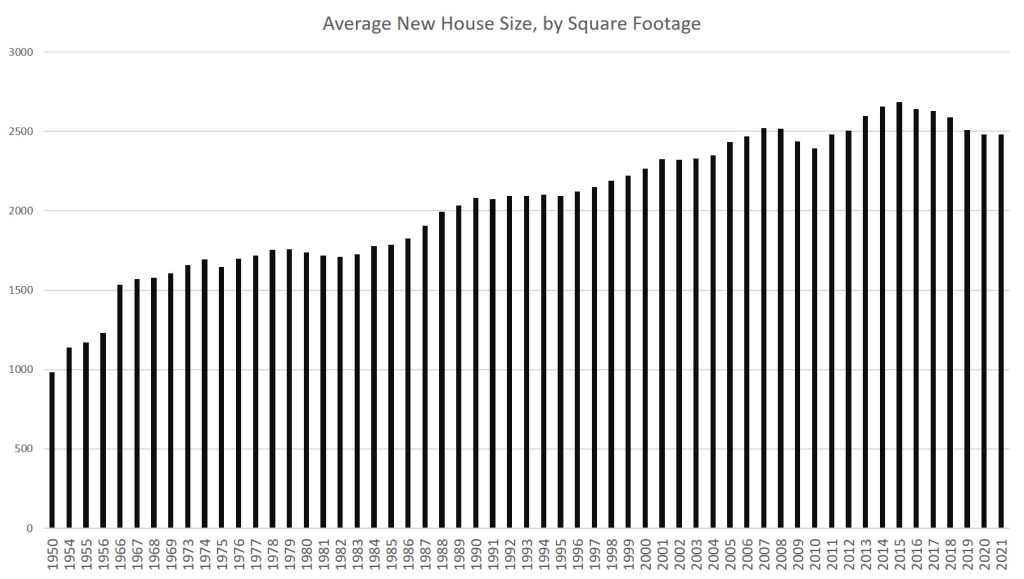

The average square footage in new single-family houses has been declining since 2015. House sizes tend to fall just during recessionary periods. It happened from 2008 to 2009, from 2001 to 2002, and from 1990 to 1991.

But even with strong economic-growth numbers well into 2019, it looks like demand for houses of historically large size may have finally peaked even before the 2020 recession and our current economic malaise. (Square footage in new multifamily construction has also increased.)

According to Census Bureau data, the average size of new houses in 2021 was 2,480 square feet. That’s down 7 percent from the 2015 peak of 2,687.

2015’s average, by the way, was an all-time high and represented decades of near-relentless growth in house sizes in the United States since the Second World War. Indeed, in the 48 years from 1973 to 2015, the average size of new houses increased by 62 percent from 1,660 to 2,687 square feet. At the same time, the quality of housing also increased substantially in everything from insulation, to roofing materials, to windows, and to the size and availability of garages.

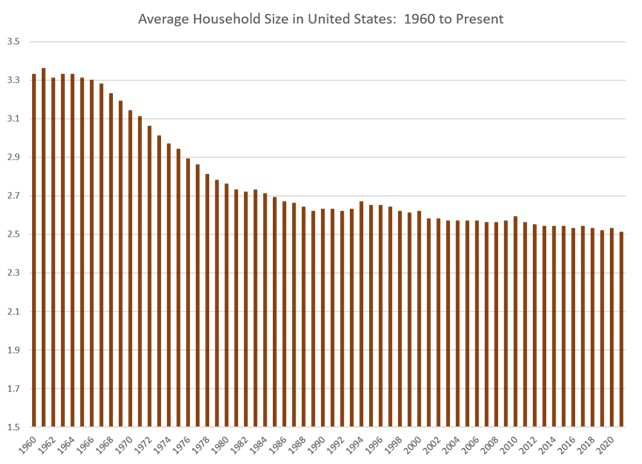

Meanwhile, the size of American households during this period decreased 16 percent from 3.01 to 2.51 people.

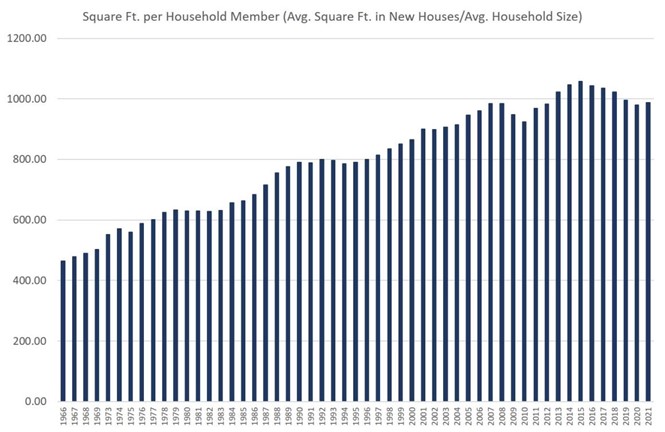

Yet, even with that 7 percent decline in house size since 2015, the average new home in America as of 2021 was still well over 50 percent larger than they were in the 1960s. Home size isn’t exactly falling off a cliff. US homes, on a square-foot-per-person basis, remain quite large by historical standards. Since 1973, square footage per person in new houses has nearly doubled, rising from 503 square feet per person in 1973 to 988 square feet person in 2021. By this measure, new house size actually increased from 2020 to 2021.

This continued drive upward in new home size can be attributed in part to the persistence of easy money over the past decade. Even as homes continued to stay big—and thus stay comparatively expensive—it was not difficult to find buyers for them. Continually falling mortgage rates to historical lows below even 3 percent in many cases meant buyers could simply borrow more money to buy big houses.

But we may have finally hit the wall on home size. In recent months we’re finally starting to see evidence of falling home sales and falling home prices. It’s only now, with mortgage rates surging, inflation soaring, and real wages falling—and thus home price affordability falling—that there are now good reasons for builders to think “wow, maybe we need to build some smaller, less costly homes.” There are many reasons to think that they won’t, and that for-purchase homes will simply become less affordable. But it’s not the fault of the builders.

This wouldn’t be a problem in a mostly-free market in which builders could easily adjust their products to meet the market where it’s at. In a flexible and generally free market, builders would flock to build homes at a price level at which a large segment of the population could afford to buy those houses. But that’s not the sort of economy we live in. Rather, real estate and housing development are highly regulated industries at both the federal level and at the local level. Thanks to this, it is becoming more and more difficult for builders to build smaller houses at a time when millions of potential first-time home buyers would gladly snatch them up.

How Government Policy Led to a Codification of Larger, More Expensive Houses

In recent decades, local governments have continued to ratchet up mandates as to how many units can be built per acre, and what size those new houses can be. As The Washington Post reported in 2019, various government regulations and fees, such as “impact fees,” which are the same regardless of the size of the unit, “incentivize developers to build big.” The Post continues, “if zoning allows no more than two units per acre, the incentive will be to build the biggest, most expensive units possible.”

Moreover, community groups opposed to anything that sounds like “density” or “upzoning” will use the power of local governments to crush developer attempts to build more affordable housing. However, as The Post notes, at least one developer has found “where his firm has been able to encourage cities to allow smaller buildings the demand has been strong. For those building small, demand doesn’t seem to be an issue.”

Similarly, in an article last month at The New York Times, Emily Badger notes the central role of government regulations in keeping houses big and ultimately increasingly unaffordable. She writes how in recent decades,

“Land grew more expensive. But communities didn’t respond by allowing housing on smaller pieces of it. They broadly did the opposite, ratcheting up rules that ensured builders couldn’t construct smaller, more affordable homes. They required pricier materials and minimum home sizes. They wanted architectural flourishes, not flat facades. …”

It is true that in many places empty land has increased in price, but in areas where the regulatory burden is relatively low—such as Houston—builders have nonetheless responded with more building of housing such as townhouses.

In many places, however, regulations continue to push up the prices of homes.

Badger notes that in Portland, Oregon, for example, “Permits add $40,000-$50,000. Removing a fir tree 36 inches in diameter costs another $16,000 in fees.” A lack of small “starter homes” is not due to an unwillingness on the part of builders. Governments have simply made smaller home unprofitable.

“You’ve basically regulated me out of anything remotely on the affordable side,” said Justin Wood, the owner of Fish Construction NW.

In Savannah, Ga., Jerry Konter began building three-bed, two-bath, 1,350-square-foot homes in 1977 for $36,500. But he moved upmarket as costs and design mandates pushed him there.

“It’s not that I don’t want to build entry-level homes,” said Mr. Konter, the chairman of the National Association of Home Builders. “It’s that I can’t produce one that I can make a profit on and sell to that potential purchaser.”

Those familiar with how local governments zone land and set building standards will not be surprised by this. Local governments, pressured by local homeowners, will intervene to keep lot sizes large, and to pass ordinances that keep out housing that might be seen by voters as “too dense” or “too cheap-looking.”

Yet, as much as existing homeowners and city planners would love to see nothing but upper middle-class housing with three-car garages along every street, the fact is that not everyone can afford this sort of housing. But that doesn’t mean people in the middle can only afford a shack in a shanty town either — so long as governments will allow more basic housing to be built.

But there are few signs of many local governments relenting on their exclusionary housing policies, and the result has been an ossified housing policy designed to reinforce existing housing, while denying new types of housing that is perhaps more suitable to smaller households and a more stagnant economic environment.

Eventually, though, something has to give. Either governments persist indefinitely with restrictions on “undesirable” housing — which means housing costs skyrocket — or local governments finally start to allow builders to build housing more appropriate to the needs of the middle class.

If current trends continue, we may finally see real pressure to get local governments to allow more building of more affordable single-family homes, or duplexes, or townhouses. If interest rates continue to march upward, this need will become only more urgent. Moreover, as homebuilding materials continue to become more expensive thanks to 40-year highs in inflation—thanks to the Federal Reserve—there will be even more need to find ways to cut regulatory costs in other areas.

For now, the results have been spotty. But where developers are allowed to actually build for a middle-class clientele, it looks like there’s plenty of demand.

About the Author

Ryan McMaken (@ryanmcmaken) is a senior editor at the Mises Institute. Ryan has a bachelor’s degree in economics and a master’s degree in public policy and international relations from the University of Colorado. He is the author of Breaking Away: The Case for Secession, Radical Decentralization, and Smaller Polities (forthcoming) and Commie Cowboys: The Bourgeoisie and the Nation-State in the Western Genre. He was a housing economist for the State of Colorado.

Fat brands inc. Reports third quarter 2022 financial results

OCTOBER 20, 2022

Conference call and webcast today at 5:00 p.m. ET

LOS ANGELES, Oct. 20, 2022 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT) (“FAT Brands” or the “Company”) today reported fiscal third quarter 2022 financial results for the 13-week period ending September 25, 2022.

Andy Wiederhorn, President and CEO of FAT Brands, commented, “We are impressed with the strong performance FAT Brands experienced in the third quarter as evidenced by our robust unit development and profitable revenue growth. Our sales resilience is a testament to our diverse portfolio of brands with average checks ranging from approximately $8 to $37.”

“Our organic growth strategy remains strong with 38 store openings in the third quarter. This week, we are set to surpass 100 openings for the year and remain on track to open 125 new restaurants in 2022, a new milestone for FAT Brands. Looking ahead to 2023, we plan to continue this robust unit growth with over 130 units slated to open. Additionally, during the third quarter, we signed 180 new franchise agreements bringing our total pipeline to over 1,000 new locations which is expected to represent a 60% increase in EBITDA over the next several years.”

“We are also extremely impressed with how our 2021 acquisitions have seamlessly fit into our portfolio and the demand we are experiencing for them from our franchisee base. We will continue to evaluate strategic acquisitions, particularly, brands that fit within our current operations that have a proven track record of long-term, sustainable and profitable operating performance or that provide us with the opportunity to expand our factory business.”

“We also continue to work on reducing our cost of capital. To that end, we expect to redeem shares of our Series B Cumulative Preferred Stock in the coming weeks. This will yield significant cash flow savings as our securitization facility, which will fund the transaction, has a lower cost of capital than the preferred share dividend rate.”

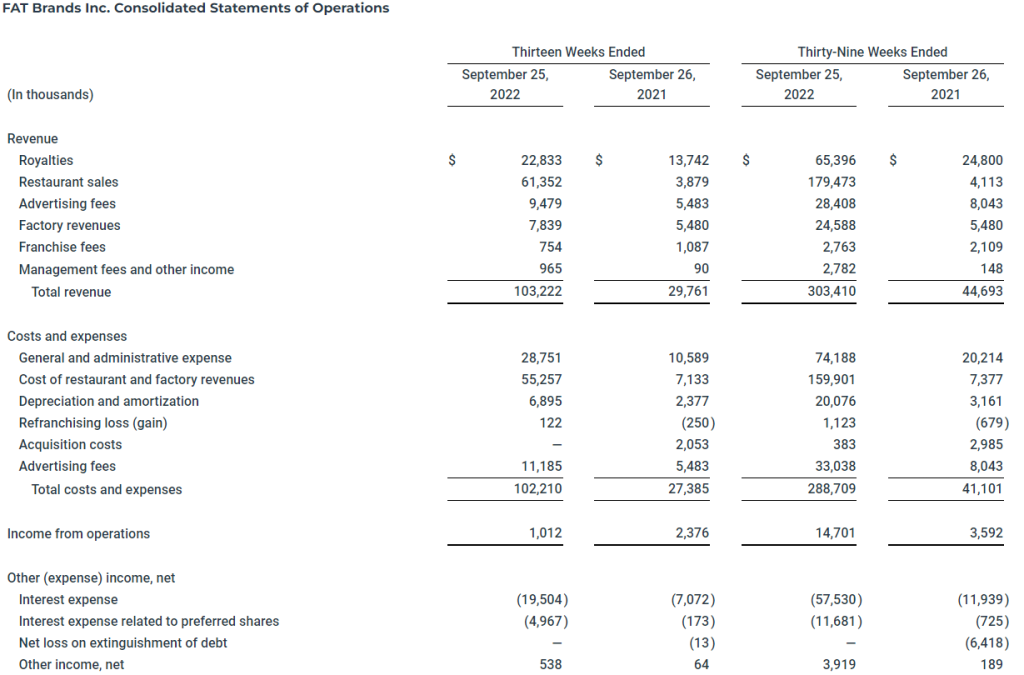

Fiscal Third Quarter 2022 Highlights

Total revenue improved 247% to $103.2 million compared to $29.8 million in the third quarter of 2021

System-wide sales growth of 57% in the third quarter of 2022 compared to the prior year quarter

Year-to-date system-wide same-store sales growth of 7.0% in the third quarter of 2022 compared to the prior year

38 new store openings during the third quarter of 2022

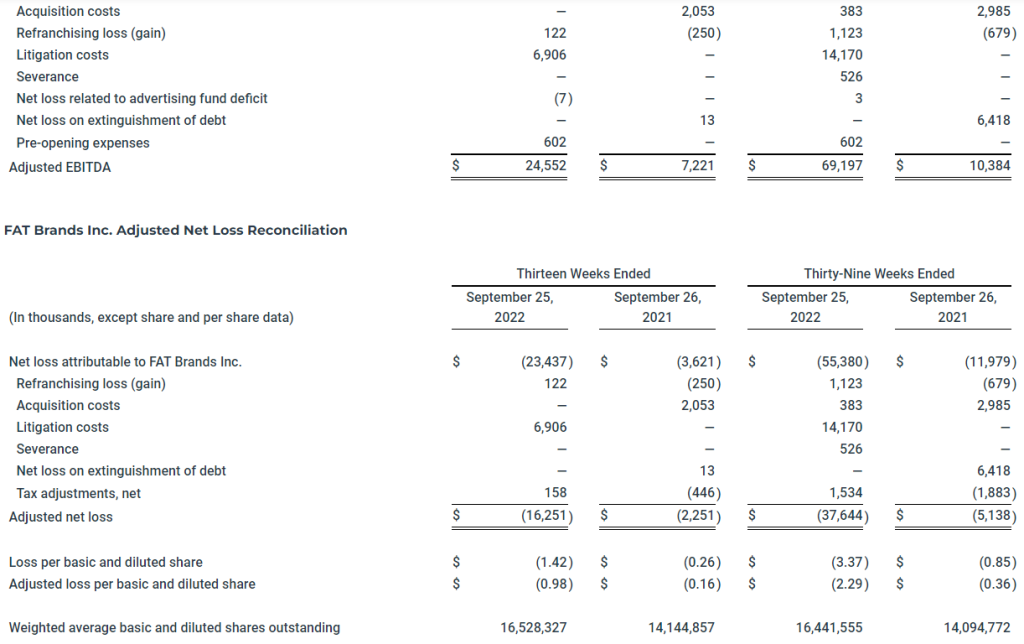

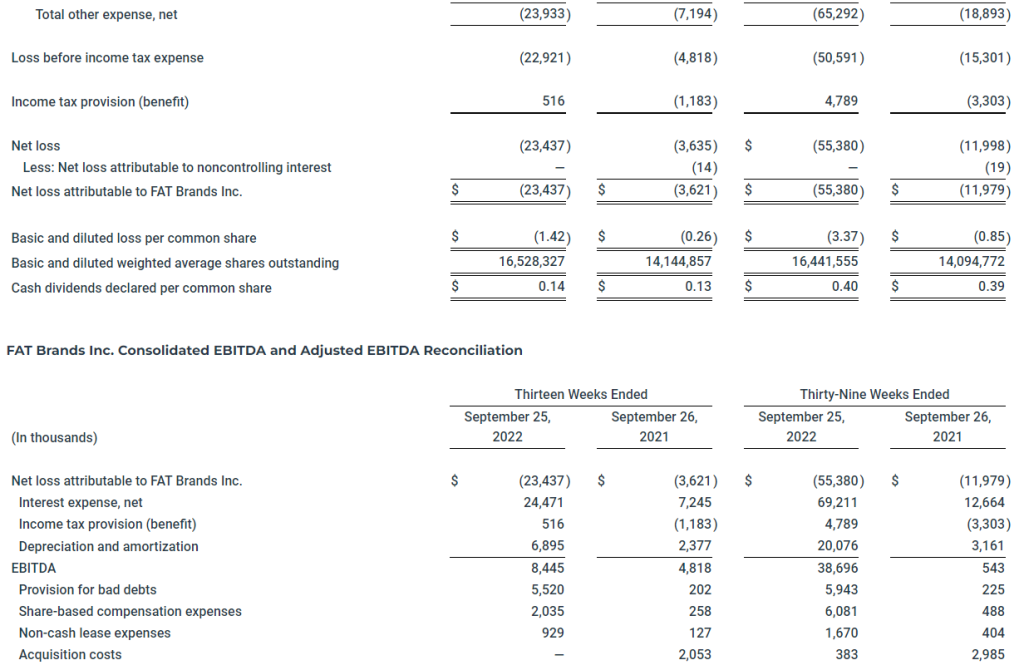

Net loss of $23.4 million, or $1.42 per diluted share, compared to $3.6 million, or $0.26 per diluted share, in the third quarter of 2021

Adjusted EBITDA(1) of $24.6 million compared to $7.2 million in the third quarter of 2021

Adjusted net loss(1) of $16.3 million, or $0.98 per diluted share, compared to $2.3 million, or $0.16 per diluted share, in the third quarter of 2021

(1) EBITDA, Adjusted EBITDA and adjusted net loss are non-GAAP measures defined below, under “Non-GAAP Measures”. Reconciliation of GAAP net loss to EBITDA, adjusted EBITDA and adjusted net loss are included in the accompanying financial tables.

Summary of Third Quarter 2022 Financial Results

Total revenue increased $73.5 million, or 247%, in the third quarter of 2022, to $103.2 million compared to $29.8 million in the same period of 2021. The increase reflects revenue from the acquisition of Global Franchise Group in July 2021, the acquisition of Twin Peaks in October 2021, the acquisitions of Fazoli’s and Native Grill & Wings in December 2021 (collectively, the “2021 Acquisitions”) and the continuing recovery from the negative effects of the COVID-19 pandemic on royalties from restaurant sales.

Costs and expenses increased $74.8 million, or 273%, in the third quarter of 2022 to $102.2 million compared to the same period in the prior year, primarily due to the 2021 Acquisitions.

General and administrative expense increased $18.2 million, or 172%, in the third quarter of 2022 compared to the same period in the prior year, primarily due to the 2021 Acquisitions, increased compensation costs, professional fees related to pending litigation and government investigations, and travel, reflecting the significant expansion of the organization.

Cost of restaurant and factory revenues totaled $55.3 million in the third quarter of 2022 and was related to the operations of the company-owned restaurant locations and the dough factory operated by Global Franchise Group associated with the 2021 Acquisitions.

Depreciation and amortization increased $4.5 million, or 190% in the third quarter of 2022 compared to the same period in the prior year, primarily due to depreciation of company-owned restaurant property and equipment and amortizing intangible assets related to the 2021 Acquisitions.

Refranchising losses in the third quarter of 2022 were $0.1 million and were comprised of restaurant costs and expenses, net of food sales. Refranchising gains in the third quarter of 2021 were $0.3 million and were comprised of $0.5 million in net gains related to refranchised restaurants, partially offset by $0.2 million in restaurant operating costs, net of food sales.

Advertising expenses increased $5.7 million in the third quarter of 2022 compared to the prior year period. These expenses vary in relation to advertising revenues and reflect advertising expenses related to the 2021 Acquisitions and the increase in customer activity as the recovery from COVID continues.

Total other expense, net for the third quarters of 2022 and 2021 was $23.9 million and $7.2 million, respectively, primarily comprised of net interest expense of $24.5 million and $7.2 million, respectively.

Adjusted net loss was $16.3 million, or $0.98 per diluted share, in the third quarter of 2022 compared to $2.3 million, or $0.16 per diluted share, in the third quarter of 2021.

Key Financial Definitions

New store openings – The number of new store openings reflects the number of stores opened during a particular reporting period. The total number of new stores per reporting period and the timing of stores openings has, and will continue to have, an impact on our results.

Same-store sales growth – Same-store sales growth reflects the change in year-over-year sales for the comparable store base, which we define as the number of stores open and in the FAT Brands system for at least one full fiscal year. For stores that were temporarily closed, sales in the current and prior period are adjusted accordingly. Given our focused marketing efforts and public excitement surrounding each opening, new stores often experience an initial start-up period with considerably higher than average sales volumes, which subsequently decrease to stabilized levels after three to six months. Additionally, when we acquire a brand, it may take several months to integrate fully each location of said brand into the FAT Brands platform. Thus, we do not include stores in the comparable base until they have been open and in the FAT Brands system for at least one full fiscal year. For 2022, the comparable store base does not include concepts acquired during fiscal 2021.

System-wide sales growth – System wide sales growth reflects the percentage change in sales in any given fiscal period compared to the prior fiscal period for all stores in that brand only when the brand is owned by FAT Brands. Because of acquisitions, new store openings and store closures, the stores open throughout both fiscal periods being compared may be different from period to period.

Conference Call and Webcast

FAT Brands will host a conference call and webcast to discuss its fiscal third quarter 2022 financial results today at 5:00 PM ET. Hosting the conference call and webcast will be Andy Wiederhorn, President and Chief Executive Officer, and Ken Kuick, Chief Financial Officer.

The conference call can be accessed live over the phone by dialing 1-877-704-4453 from the U.S. or 1-201-389-0920 internationally. A replay will be available after the call until Thursday, October 27, 2022, and can be accessed by dialing 1-844-512-2921 from the U.S. or 1-412-317-6671 internationally. The passcode is 13733381. The webcast will be available at www.fatbrands.com under the “Investors” section and will be archived on the site shortly after the call has concluded.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses and franchises and owns over 2,300 units worldwide. For more information, please visit www.fatbrands.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements relating to the future financial and operating results of the Company, estimates of future EBITDA, the timing and performance of new store openings, our expected redemption of Series B Cumulative Preferred Stock, our ability to conduct future accretive acquisitions, our pipeline of new store locations, and the recovery of our business from the COVID-19 pandemic. Forward-looking statements generally use words such as “expect,” “foresee,” “anticipate,” “believe,” “project,” “should,” “estimate,” “will,” “plans,” “forecast,” and similar expressions, and reflect our expectations concerning the future. Forward-looking statements are subject to significant business, economic and competitive risks, uncertainties and contingencies, many of which are difficult to predict and beyond our control, which could cause our actual results to differ materially from the results expressed or implied in such forward-looking statements. We refer you to the documents that we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other risks and uncertainties that could cause our actual results to differ materially from our current expectations and from the forward-looking statements contained in this press release. We undertake no obligation to update any forward-looking statements to reflect events or circumstances occurring after the date of this press release.

Non-GAAP Measures (Unaudited)

This press release includes the non-GAAP financial measures of EBITDA, adjusted EBITDA and adjusted net loss.

EBITDA is defined as earnings before interest, taxes, and depreciation and amortization. We use the term EBITDA, as opposed to income from operations, as it is widely used by analysts, investors, and other interested parties to evaluate companies in our industry. We believe that EBITDA is an appropriate measure of operating performance because it eliminates the impact of expenses that do not relate to business performance. EBITDA is not a measure of our financial performance or liquidity that is determined in accordance with generally accepted accounting principles (“GAAP”), and should not be considered as an alternative to net income (loss) as a measure of financial performance or cash flows from operations as measures of liquidity, or any other performance measure derived in accordance with GAAP.

Adjusted EBITDA is defined as EBITDA (as defined above), excluding expenses related to acquisitions, refranchising gain or losses, impairment charges, and certain non-recurring or non-cash items that the Company does not believe directly reflect its core operations and may not be indicative of the Company’s recurring business operations.

Adjusted net loss is a supplemental measure of financial performance that is not required by or presented in accordance with GAAP. Adjusted net loss is defined as net loss plus the impact of adjustments and the tax effects of such adjustments. Adjusted net loss is presented because we believe it helps convey supplemental information to investors regarding our performance, excluding the impact of special items that affect the comparability of results in past quarters to expected results in future quarters. Adjusted net loss as presented may not be comparable to other similarly titled measures of other companies, and our presentation of adjusted net loss should not be construed as an inference that our future results will be unaffected by excluded or unusual items. Our management uses this non-GAAP financial measure to analyze changes in our underlying business from quarter to quarter based on comparable financial results.

Reconciliations of net loss attributable to FAT Brands Inc. presented in accordance with GAAP to EBITDA, adjusted EBITDA, and adjusted net loss are set forth in the tables below.

Seanergy Maritime Holdings Corp. is the only pure-play Capesize ship-owner publicly listed in the US. Seanergy provides marine dry bulk transportation services through a modern fleet of Capesize vessels. The Company’s operating fleet consists of 17 Capesize vessels with an average age of approximately 12 years and aggregate cargo carrying capacity of approximately 3,011,083 dwt. The Company is incorporated in the Marshall Islands and has executive offices in Glyfada, Greece. The Company’s common shares trade on the Nasdaq Capital Market under the symbol “SHIP” and its Class B warrants under “SHIPZ”.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

We are making adjustments to our models to reflect lower shipping rates. Dry bulk shipping rates have been weak in the third quarter. As a result, we are lowering the assumed rate for uncommitted ships to $19,500/day from $23,650/day. Management guided analysts to a $23,650/day number when reporting second quarter results but now believes the rate will be below $20,000/day. Every $1,000 reduction in uncommitted daily TCE rates reduces net income by $1.1 million or $0.01 per share.

We are also raising our interest expense estimate to reflect higher interest rates. We are raising our third quarter interest expense estimate to $5.0 million from $3.5 million to reflect higher LIBOR rates. LIBOR rates have increased from 0.1% to more than 4.0% in the last twelve months. We are also formally incorporating the $28 million term loan that was announced last week into our models.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Pangaea Logistics Solutions Ltd. (NASDAQ: PANL) provides logistics services to a broad base of industrial customers who require the transportation of a wide variety of dry bulk cargoes, including grains, pig iron, hot briquetted iron, bauxite, alumina, cement clinker, dolomite, and limestone. The Company addresses the transportation needs of its customers with a comprehensive set of services and activities, including cargo loading, cargo discharge, vessel chartering, and voyage planning. Learn more at www.pangaeals.com.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

We are adjusting our models to reflect lower shipping rates in the third quarter. Although shipping rates remains high relative to historical levels, they have decreased relative to peak levels reached this spring.

We are lowering our revenue, cashflow and earnings estimates in response. We now project third-quarter and 2022 revenues of $158.6 million an $714.1 million, respectively, down from our previous estimates of $182.3 million and $752.2 million. Our new EBITDA estimates are $9.6 million and $112.2 million, down from $33.31 million and $142.4 million. We now estimate earnings per share of $(0.08) and $1.27 as compared to $0.45 and $1.93.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Drilling continues at the Big Vein target. Labrador Gold released results from recent drilling associated with its 100,000-meter drill program at its 100%-owned Kingsway gold project targeting the Appleton Fault Zone over a 12-kilometer strike length. A total of 58,265 meters have been drilled to date with assays pending for samples from approximately 3,100 meters of core. Currently, one rig is drilling at the Golden Glove target while two rigs are drilling at Big Vein to test for extensions of mineralization in both directions. With drilling at the CSAMT target completed, a third rig is being deployed at Big Vein.

High grade assay results. Hole K-22-190 from the north end of Big Vein returned an intersection of 30.67 grams of gold per tonne over 1.1 meters from 208.85 meters depth that included 99.31 grams of gold over 0.3 meters. At Big Vein Southwest, Hole K-22-184 intersected 4.67 grams of gold per tonne over 1.64 meters from 336.25 meters depth that included 8.97 grams of gold per tonne over 0.75 meters. Drilling has returned several significant intercepts at the north end of Big Vein, including 6.07 grams of gold per tonne over 19 meters in Hole K-21-111. Results from Hole K-22-190 underscore the high-grade prospectivity of the area.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Kruh Well 28 finds oil formation in addition to previously announced gas reservoir. Indo reported reaching final depth in its fourth well in the Kruh field. As has been the case with the other three wells, oil has been discovered, this time with a wider oil band that had been expected. The company previously reported discovering natural gas at shallower levels as had been the case in Kruh Well 27. We view drilling in the Kruh Field as largely developmental so the successful discovery of hydrocarbons was not a surprise. It will take at least a month to complete the well before we can learn flow rate information, but management maintains that the wells have a twelve-month payback at current oil prices.

Well success prompts further seismic studies. Indo is planning to conduct new seismic operations across the entire Kruh Block to optimize drilling locations. The company still plans on drilling 18 wells in the block (four have been completed). Seismic studies will push back the drilling program twelve months into the 2024-25 time frame and will not begin until Kruh 27 and 28 have been brought on line. We had modeled six wells in 2023 and eight in 2024 and are pushing all drilling back a year. Indonesia Energy has faced a series of delays in its drilling program due to COVID, weather, and other factors.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Genco Shipping & Trading Limited, incorporated on September 27, 2004, transports iron ore, coal, grain, steel products and other drybulk cargoes along shipping routes through the ownership and operation of drybulk carrier vessels. The Company is engaged in the ocean transportation of drybulk cargoes around the world through the ownership and operation of drybulk carrier vessels. As of December 31, 2016, its fleet consisted of 61 drybulk carriers, including 13 Capesize, six Panamax, four Ultramax, 21 Supramax, two Handymax and 15 Handysize drybulk carriers, with an aggregate carrying capacity of approximately 4,735,000 deadweight tons (dwt). Of the vessels in its fleet, 15 are on spot market-related time charters, and 27 are on fixed-rate time charter contracts. As of December 31, 2016, additionally, 19 of the vessels in its fleet were operating in vessel pools.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

We are adjusting in response to lower third-quarter shipping rates. Our third-quarter and 2022 revenues estimates for Genco have been modestly reduced to $130.6 million and $535.2 million. Our third-quarter and 2022 EBITDA estimates are now $68.7 million and $258.0 million, down from $70.8 million and $264.3 million. Our third-quarter and 2022 EPS estimates are now $1.21 and $4.52, down from $1.25 and $4.66.

Our rating on the shares of Genco remains Outperform with a $28 price target. Lower shipping rates will adversely affect near-term results but does not change our long-term positive view of the shipping industry and Genco, in specific.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

We are lowering our assumed TCE shipping rate for non-fixed vessels. We are lowering third-quarter TCE rates to $20,000/day from $23,000/day to reflect weaker shipping rates in the quarter. The impact on EuroDry cash flow and earnings is somewhat muted relative to other shipping companies given fixed rates for the bulk of its fleet. Nevertheless, we are adjusting downward our estimates to reflect the impact on ships tied to market prices.

Revenues, EBITDA and EPS estimate all come down slightly. Our new third quarter and 2022 revenues estimates are $25.4 million and $96.3 million, down from $26.1 million and $98.4 million. Our new third quarter and 2022 EBITDA estimates are $13.1 million and $55.5 million, down from $13.7 million and $57.1 million. Our new third quarter and 2022 EPS estimates are $3.27 and $14.88, down from $3.48 and $15.44.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Eagle Bulk Shipping Inc. (“Eagle”) is a US-based drybulk owner-operator focused on the Supramax/Ultramax mid-size asset class, which ranges from 50,000 and 65,000 deadweight tons in size; these vessels are equipped with onboard cranes allowing for the self-loading and unloading of cargoes, a feature which distinguishes them from the larger classes of drybulk vessels and provides for greatly enhanced flexibility and versatility- both with respect to cargo diversity and port accessibility. The Company transports a broad range of major and minor bulk cargoes around the world, including coal, grain, ore, pet coke, cement, and fertilizer. Eagle operates out of three offices, Stamford (headquarters), Singapore, and Hamburg, and performs all aspects of vessel management in-house including: commercial, operational, technical, and strategic.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

We are lowering our estimates for Eagle Bulk Shipping to reflect lower shipping rates. We have lowered our assumed TCE shipping rates to reflect recent pricing. In response, we are lowering our third quarter and 2022 revenue estimates to $168.9 million and $710.9 million respectively, down from $193.2 million and $760.0 million.

Lower revenues means lower EBITDA and EPS estimates. Adjusting our models for lower pricing and revenues results in a decline in third quarter and 2022 EBITDA to $93.2 million and $362.7 million, down from $117.6 million and $411.8 million. EPS for the quarter and year are reduced to $4.24 and $15.55, down from $5.49 and $18.07.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating estimates. Coal prices continued to exhibit strength during the third quarter and we believe the outlook for oil and gas prices remains favorable. We have increased our 2022 adjusted EBITDA and adjusted EPU estimates to $951.9 million and $4.90 from $945.3 and $4.85, respectively. Our 2023 estimates remain unchanged. We have assumed the partnership declares third and fourth quarter per unit cash distributions of $0.45 and $0.50, respectively.

New Ventures team. Alliance recently announced the formation of a New Ventures team, led by Andrew Woodward and Matthew Lewis, to make strategic investments in energy and infrastructure that promote decarbonization. The team will identify, develop, and execute commercial opportunities outside of the company’s existing businesses to enhance growth and the company’s ability to serve the evolving energy needs of the market.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.