ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 700 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For additional information, visit www.ISG-One.com

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

1Q23 Results. All-time record revenue of $78.5 million, up 8.2% y-o-y. Currency translation negatively impacted reported revenue by $2.1 million. By geography, Americas revenue rose 17% to $48.4 million, Europe was down 2% on a reported basis and up 5% on a constant currency basis to $23.1 million, and Asia-Pacific revenue of $7 million was down 8% on a reported basis and down 3% on a constant currency basis. We were at $74 million.

Results Continued. But higher direct costs and expenses for advisors negatively impacted operating income. Direct costs were up 11.9% to 62.7% of revenue compared to 60.6% in 1Q22. Operating income was down 9% to $7.1 million from $7.7 million. Net income was down 29% to $3.5 million, or $0.07/sh. Adjusted EPS was $0.12/sh. We had projected EPS of $0.08 and adjusted EPS of $0.12.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Blackboxstocks, Inc. is a financial technology and social media hybrid platform offering real-time proprietary analytics and news for stock and options traders of all levels. Our web-based software employs “predictive technology” enhanced by artificial intelligence to find volatility and unusual market activity that may result in the rapid change in the price of a stock or option. Blackbox continuously scans the NASDAQ, New York Stock Exchange, CBOE, and all other options markets, analyzing over 10,000 stocks and up to 1,500,000 options contracts multiple times per second. We provide our users with a fully interactive social media platform that is integrated into our dashboard, enabling our users to exchange information and ideas quickly and efficiently through a common network. We recently introduced a live audio/video feature that allows our members to broadcast on their own channels to share trade strategies and market insight within the Blackbox community. Blackbox is a SaaS company with a growing base of users that spans 42 countries; current subscription fees are $99.97 per month or $959.00 annually. For more information, go to: www.blackboxstocks.com .

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Merger. Blackboxstocks announced its intent to merger with Evtec Group. BLBX shareholders are expected to retain 8.34% of the combined company’s common stock post-merger. While details of the transaction are limited, management believes the transaction will provide significant and long-term value for BLBX shareholders. Blackboxstocks will operate as a subsidiary of Evtec. In its just filed 10-K for 2022, the Company noted it was exploring strategic alternatives.

Who Is Evtec Group? A private U.K.-based company, Evtec Group is a leading parts supplier for luxury brands in the EV and performance automotive market. The acquisition of Blackboxstocks provides Evtec with a pathway to become publicly traded in the U.S., while enabling Blackboxstocks access to capital needed to take the next step forward in its business, in our view.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Blackboxstocks, Inc. is a financial technology and social media hybrid platform offering real-time proprietary analytics and news for stock and options traders of all levels. Our web-based software employs “predictive technology” enhanced by artificial intelligence to find volatility and unusual market activity that may result in the rapid change in the price of a stock or option. Blackbox continuously scans the NASDAQ, New York Stock Exchange, CBOE, and all other options markets, analyzing over 10,000 stocks and up to 1,500,000 options contracts multiple times per second. We provide our users with a fully interactive social media platform that is integrated into our dashboard, enabling our users to exchange information and ideas quickly and efficiently through a common network. We recently introduced a live audio/video feature that allows our members to broadcast on their own channels to share trade strategies and market insight within the Blackbox community. Blackbox is a SaaS company with a growing base of users that spans 42 countries; current subscription fees are $99.97 per month or $959.00 annually. For more information, go to: www.blackboxstocks.com .

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A Ratio Set. Yesterday, Blackboxstocks announced that the Company has filed an amendment to the Company’s articles of incorporation with the Nevada Secretary of State to set a Reverse Stock Split ratio of one-for-four. The amendment took effect on April 10, 2023 at 4:01 p.m. Eastern Daylight Time, and split-adjusted basis trading begins on April 11, 2023. The exchange agent for the split will be Securities Transfer Corporation.

The Process. The amendment process to the articles was started last month when the Board of Directors of the Company adopted resolutions advising and recommending to stockholders to approve a reverse stock split of one-for-seven. The stockholders voted to approve the split and amendment in the same month. The Board later approved the split ratio to be at one-to-four on April 7, 2023.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

One Stop Systems, Inc. (OSS) designs and manufactures innovative AI Transportable edge computing modules and systems, including ruggedized servers, compute accelerators, expansion systems, flash storage arrays, and Ion Accelerator™ SAN, NAS, and data recording software for AI workflows. These products are used for AI data set capture, training, and large-scale inference in the defense, oil and gas, mining, autonomous vehicles, and rugged entertainment applications. OSS utilizes the power of PCI Express, the latest GPU accelerators and NVMe storage to build award-winning systems, including many industry firsts, for industrial OEMs and government customers. The company enables AI on the Fly® by bringing AI datacenter performance to ‘the edge,’ especially on mobile platforms, and by addressing the entire AI workflow, from high-speed data acquisition to deep learning, training, and inference. OSS products are available directly or through global distributors. For more information, go to www.onestopsystems.com.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q22 Results. Revenue of $18.2 million, up 2.7% y-o-y, but about $1 million below expectations as the Disguise business was weaker than expected. We had forecast $19 million. Driven by one-time items, OSS reported a GAAP net loss of $3.3 million, or a loss of $0.16/sh in the quarter, compared to a loss of $386,243, or a loss of $0.02/sh per share last year. We had forecast net income of $0.4 million, or $0.02 per share.

Military Opportunities Expanding. OSS is now engaged with eight of the top 10 largest military prime contractors in the U.S., with multiple prime contractor bids to the DOD using OSS products. OSS has won two new military programs already in 2023, with eight more in the pipeline.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comtech Telecommunications Corp. engages in the design, development, production, and marketing of products, systems, and services for advanced communications solutions in the United States and internationally. It operates in three segments: Telecommunications Transmission, Mobile Data Communications, and RF Microwave Amplifiers. The Telecommunications Transmission segment provides satellite earth station equipment and systems, over-the-horizon microwave systems, and forward error correction technology, which are used in various commercial and government applications, including backhaul of wireless and cellular traffic, broadcasting (including HDTV), IP-based communications traffic, long distance telephony, and secure defense applications. The Mobile Data Communications segment provides mobile satellite transceivers, and computers and satellite earth station network gateways and associated installation, training, and maintenance services; supplies and operates satellite packet data networks, including arranging and providing satellite capacity; and offers microsatellites and related components. The RF Microwave Amplifiers segment designs, develops, manufactures, and markets satellite earth station traveling wave tube amplifiers (TWTA) and broadband amplifiers. Its amplifiers are used in broadcast and broadband satellite communication; defense applications, such as telecommunications systems and electronic warfare systems; and commercial applications comprising oncology treatment systems, as well as to amplify signals carrying voice, video, or data for air-to-satellite-to-ground communications. The company serves satellite systems integrators, wireless and other communication service providers, broadcasters, defense contractors, military, governments, and oil companies. Comtech markets its products through independent representatives and value-added resellers. The company was founded in 1967 and is headquartered in Melville, New York.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Convergence. Yesterday, Comtech announced Al Yah Satellite Communications Company PJSC (Yahsat), the United Arab Emirates’ flagship satellite solutions provider, awarded the Company $29 million to deliver communications technologies and location services that will operate on Yahsat’s Thuraya 4-NGS satellite constellation.

Details. Comtech will design, develop, install, integrate, and test communications and location-based technologies for Yahsat’s Location Tracking Services Platform and User Terminals. Comtech’s offerings will help enable blended satellite and terrestrial technologies communications and enhanced location-based services for end users of Yahsat’s network.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 700 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For additional information, visit www.ISG-One.com

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Continuing the Trend. Like the previous quarter, the momentum for ISG has been positive in terms of demand for the Company’s digital services along with cost optimization services as companies are continuing to navigate a volatile economic environment. In addition, the Company had $108 million in recurring revenue for the year, exceeding the Company’s goal of $100 million, which brings along higher margins.

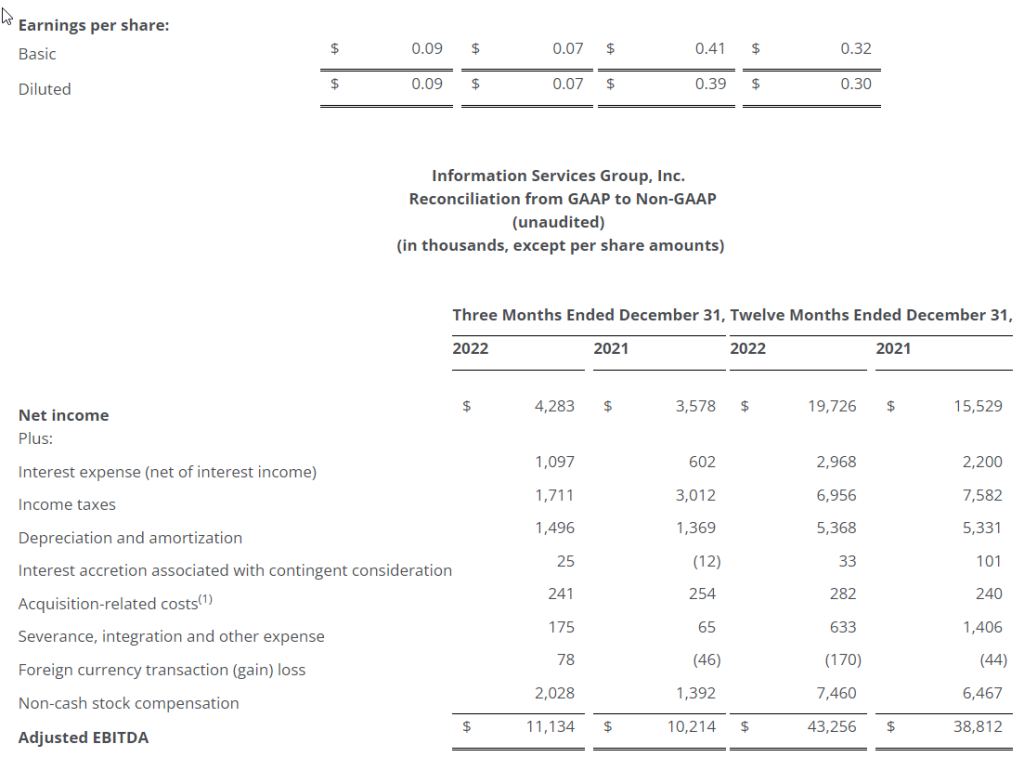

4Q Results. ISG reported revenues for the fourth quarter were a record $74.2 million, up 7% from $69.6 million in the prior year, and up 11% in constant currency. We estimated revenue at $71.0 million. Net income was a record $4.3 million, or diluted EPS of $0.09, compared to $3.6 million, or $0.07 per fully diluted share, in the prior year. Adjusted EBITDA was at a record $11.1 million, up 9% from the prior-year fourth quarter.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comtech Telecommunications Corp. engages in the design, development, production, and marketing of products, systems, and services for advanced communications solutions in the United States and internationally. It operates in three segments: Telecommunications Transmission, Mobile Data Communications, and RF Microwave Amplifiers. The Telecommunications Transmission segment provides satellite earth station equipment and systems, over-the-horizon microwave systems, and forward error correction technology, which are used in various commercial and government applications, including backhaul of wireless and cellular traffic, broadcasting (including HDTV), IP-based communications traffic, long distance telephony, and secure defense applications. The Mobile Data Communications segment provides mobile satellite transceivers, and computers and satellite earth station network gateways and associated installation, training, and maintenance services; supplies and operates satellite packet data networks, including arranging and providing satellite capacity; and offers microsatellites and related components. The RF Microwave Amplifiers segment designs, develops, manufactures, and markets satellite earth station traveling wave tube amplifiers (TWTA) and broadband amplifiers. Its amplifiers are used in broadcast and broadband satellite communication; defense applications, such as telecommunications systems and electronic warfare systems; and commercial applications comprising oncology treatment systems, as well as to amplify signals carrying voice, video, or data for air-to-satellite-to-ground communications. The company serves satellite systems integrators, wireless and other communication service providers, broadcasters, defense contractors, military, governments, and oil companies. Comtech markets its products through independent representatives and value-added resellers. The company was founded in 1967 and is headquartered in Melville, New York.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q23 Results. Revenue of $133.7 million was up 2.0% sequentially, within guidance, and is the fifth consecutive quarter of growth. Y-o-Y revenue was up 11.1%. We were at $133.5 million. Adjusted EBITDA totaled $11.3 million, versus $9.8 million in 2Q22. We were at $11 million. Comtech reported a net loss of $6.5 million, or a loss of $0.23 per share, compared to a net loss of $23.5 million, or $0.89 per share last year. Adjusted EPS was $0.09 versus $0.18. We had forecast a net loss of $3.2 million, or a loss of $0.12 per share and adjusted EPS of $0.15.

Strong Bookings. Bookings remained strong in the fiscal second quarter at $167.5 million, up from $102.9 million in the year ago period. Quarter-end backlog was $702 million, up from $668.2 million at the end of the first quarter, and a level last seen in July 2019.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

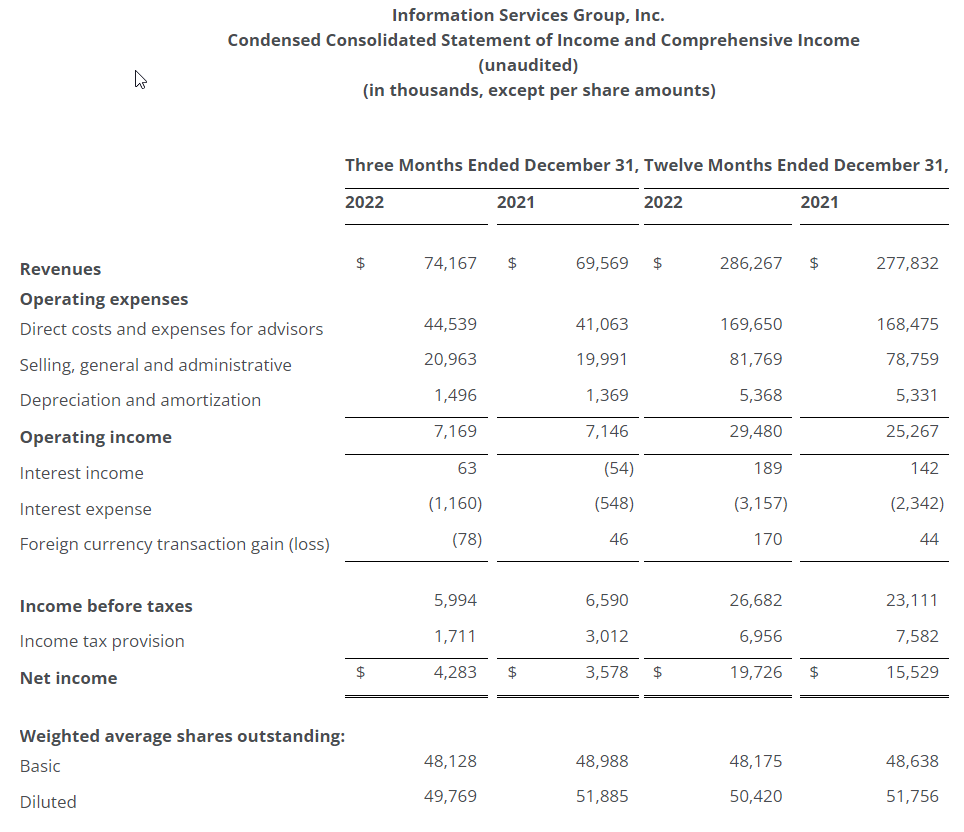

Reports fourth-quarter GAAP revenues of $74 million,an all-time quarterly high, exceeding guidance and including a negative FX impact of $3.2 million

Reports fourth-quarter net income of $4 million, GAAP EPS of $0.09 and adjusted EPS of $0.13, all fourth-quarter records

Reports record fourth-quarter adjusted EBITDA of $11 million, exceeding guidance

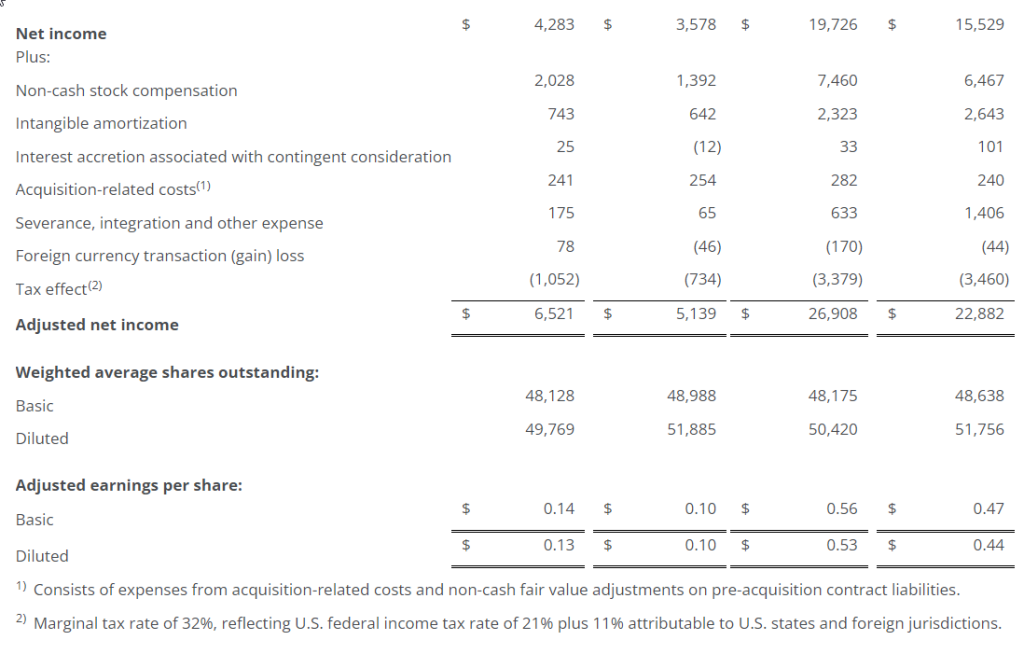

Achieves record full-year results: GAAP revenues of $286 million, up 8% in constant currency; operating income of $29 million, up 17%; net income of $20 million, up 27%; adjusted net income of $27 million, up 18%, GAAP EPS of $0.39, up 30%; adjusted EPS of $0.53, up 20%; adjusted EBITDA of $43 million, up 11%

Declares first-quarter dividend of $0.04 per share, payable March 31, 2023, to shareholders of record as of March 20, 2023

As previously announced, amends credit agreement to include more favorable terms, an extended maturity date, elimination of $4.3 million of mandatory annual principal payments, and conversion to an all-revolving credit facility with $140 million of borrowing capacity

Sets first-quarter guidance: revenues between $73 million and $75 million and adjusted EBITDA between $10 million and $11 million

STAMFORD, Conn.–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III), a leading global technology research and advisory firm, today announced record financial results for the fourth quarter and full year ended December 31, 2022.

“ISG delivered our best quarterly and full-year performance in our 17-year history—on every key financial metric,” said Michael P. Connors, chairman and CEO. “Fourth-quarter revenue and profitability reached record highs, led by double-digit operating growth in the Americas and Europe as client demand for efficiency and optimization escalates. Our suite of client solutions in digital transformation, cost optimization, research, workplace and governance services, supported by our successful ISG NEXT operating model, is a winning combination.”

Some clients, especially those in industries and geographies facing the toughest market conditions, are turning to ISG to help them optimize their IT and operating environments, Connors said. “Clients trust ISG for our unmatched combination of data, insights, expertise, tools and solutions to help streamline their technology and operating environments, reinvest in continuous transformation and get the most out of the collaboration between people and technology,” he said.

Fourth-Quarter 2022 Results

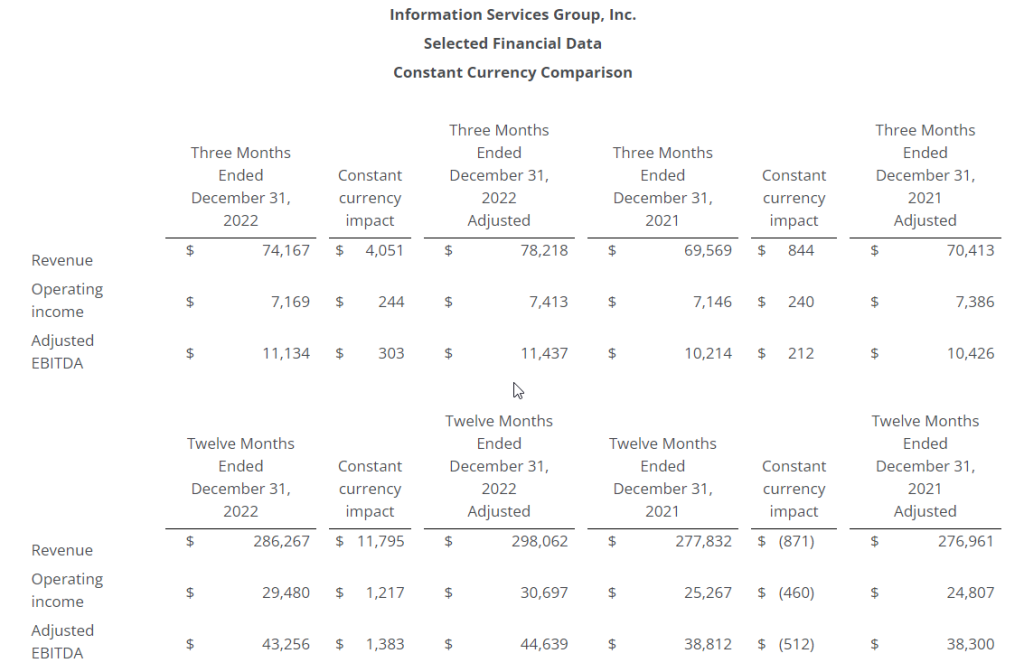

Reported revenues for the fourth quarter were a record $74.2 million, up 7 percent from $69.6 million in the prior year, and up 11 percent in constant currency. Currency translation negatively impacted reported revenues by $3.2 million versus the prior year. Reported revenues were $43.6 million in the Americas, up 12 percent; $23.9 million in Europe, up 1 percent on a reported basis and up 12 percent in constant currency; and $6.7 million in Asia Pacific, down 4 percent on a reported basis and up 5 percent in constant currency, all versus the prior year.

ISG reported fourth-quarter operating income of $7.2 million, flat versus the prior year. Reported fourth-quarter net income was a record $4.3 million, up 20 percent, compared with net income of $3.6 million in the prior year. Fully diluted earnings per share was a record $0.09, compared with $0.07 per fully diluted share in the prior year. Net income margin (calculated by dividing net income by reported revenues) increased to 5.8 percent, from 5.1 percent in the fourth quarter of 2021.

Adjusted net income (a non-GAAP measure defined below under “Non-GAAP Financial Measures”) for the fourth quarter was $6.5 million, or a record $0.13 per share on a fully diluted basis, compared with adjusted net income of $5.1 million, or $0.10 per share on a fully diluted basis, in the prior year’s fourth quarter.

Fourth-quarter adjusted EBITDA (a non-GAAP measure defined below under “Non-GAAP Financial Measures”) was a record $11.1 million, up 9 percent from the prior-year fourth quarter. Adjusted EBITDA margin (a non-GAAP measure calculated by dividing adjusted EBITDA by reported revenues) was 15 percent, up 33 basis points from the prior year.

Full-Year 2022 Results

Reported revenues for the full-year were a record $286.3 million, up 3 percent versus the prior-year, and up 8 percent in constant currency. Currency translation negatively impacted reported revenues by $12.7 million versus 2021. Reported revenues were $166.7 million in the Americas, up 4 percent; $89.9 million in Europe, flat on a reported basis and up 12 percent in constant currency; and $29.7 million in Asia Pacific, up 8 percent on a reported basis and up 16 percent in constant currency, all versus the prior year.

ISG reported record full-year operating income of $29.5 million, up 17 percent from $25.3 million in the prior year. The firm also reported record net income and fully diluted earnings per share of $19.7 million and $0.39, respectively, versus net income of $15.5 million and earnings per share of $0.30 in the prior year. Net income margin (calculated by dividing net income by reported revenues) increased to 6.9 percent, from 5.6 percent in the same period last year.

Adjusted net income (a non-GAAP measure defined below under “Non-GAAP Financial Measures”) for the full year was a record $26.9 million, or $0.53 per share on a fully diluted basis, compared with adjusted net income of $22.9 million, or $0.44 per share on a fully diluted basis, in the prior year.

Full-year adjusted EBITDA (a non-GAAP measure defined below under “Non-GAAP Financial Measures”) reached a record $43.3 million, up 11 percent from the prior year. Adjusted EBITDA margin (a non-GAAP measure calculated by dividing adjusted EBITDA by reported revenues) was a record 15 percent, up more than 110 basis points from the prior year.

Other Financial and Operating Highlights

ISG generated $6.6 million of cash from operations in the fourth quarter, compared with $2.5 million in the prior year, and $11.1 million for the full year. The firm’s cash balance totaled $30.6 million at December 31, 2022, up from $19.7 million at September 30, 2022.

During the fourth quarter, ISG paid dividends of $2.0 million, paid down $1.1 million of debt and drew down $9.0 million on its revolving credit agreement with the funds used for the acquisition of Change 4 Growth and for general operating purposes. As of December 31, 2022, ISG had $79.2 million in debt outstanding, compared with $74.5 million at the end of the fourth quarter last year. The firm’s gross-debt-to-adjusted-EBITDA ratio (a non-GAAP measure calculated by dividing outstanding debt by adjusted EBITDA) was 1.8 times, a record low for year end.

“Our strong operating results allowed us to return $23.6 million of capital to our shareholders in the form of dividends and share repurchases in 2022,” Connors said. “It also allowed us to amend our existing credit agreement, converting it to an all-revolver facility, with more favorable terms and an extended maturity date.”

Amended Credit Agreement

As previously announced, on February 22, 2023, ISG successfully amended the credit agreement that the firm originally entered into on March 10, 2020. The amended agreement provides $140 million of borrowing capacity at more favorable terms, converts the previous term and revolving loan into an all-revolving credit facility, eliminates $4.3 million of mandatory annual principal payments under the previous agreement, and extends the maturity date of the previous agreement by three years, to February 2028.

2023 First-Quarter Revenue and Adjusted EBITDA Guidance

“For the first quarter, ISG is targeting revenues of between $73 million and $75 million – including 200 basis points of FX headwinds – and adjusted EBITDA of between $10 million and $11 million. We will continue to monitor the macroeconomic environment, including the impact of FX, inflation and other factors, and adjust our business plans accordingly.”

Quarterly Dividend

The ISG Board of Directors declared a first-quarter dividend of $0.04 per share, payable on March 31, 2023, to shareholders of record as of March 20, 2023.

Conference Call

ISG has scheduled a call for 9 a.m., U.S. Eastern Time, Friday, March 10, 2023, to discuss the company’s fourth-quarter results. The call can be accessed by dialing +1 833-470-1428; or, for international callers, by dialing +1 929-526-1599. The access code is 356636. A recording of the conference call will be accessible on ISG’s website (www.isg-one.com) for approximately four weeks following the call.

Forward-Looking Statements

This communication contains “forward-looking statements” which represent the current expectations and beliefs of management of ISG concerning future events and their potential effects. Statements contained herein including words such as “anticipate,” “believe,” “contemplate,” “plan,” “estimate,” “target,” “expect,” “intend,” “will,” “continue,” “should,” “may,” and other similar expressions, are “forward-looking statements” under the Private Securities Litigation Reform Act of 1995. These forward-looking statements are not guarantees of future results and are subject to certain risks and uncertainties that could cause actual results to differ materially from those anticipated. Those risks relate to inherent business, economic and competitive uncertainties and contingencies relating to the businesses of ISG and its subsidiaries including without limitation: (1) failure to secure new engagements or loss of important clients; (2) ability to hire and retain enough qualified employees to support operations; (3) ability to maintain or increase billing and utilization rates; (4) management of growth; (5) success of expansion internationally; (6) competition; (7) ability to move the product mix into higher margin businesses; (8) general political and social conditions such as war, political unrest and terrorism; (9) healthcare and benefit cost management; (10) ability to protect ISG and its subsidiaries’ intellectual property or data and the intellectual property or data of others; (11) currency fluctuations and exchange rate adjustments; (12) ability to successfully consummate or integrate strategic acquisitions; (13) outbreaks of diseases, including coronavirus, or similar public health threats or fear of such an event; and (14) engagements may be terminated, delayed or reduced in scope by clients. Certain of these and other applicable risks, cautionary statements and factors that could cause actual results to differ from ISG’s forward-looking statements are included in ISG’s filings with the U.S. Securities and Exchange Commission. ISG undertakes no obligation to update or revise any forward-looking statements to reflect subsequent events or circumstances.

Non-GAAP Financial Measures

ISG reports all financial information required in accordance with U.S. generally accepted accounting principles (GAAP). In this release, ISG has presented both GAAP financial results as well as non-GAAP information for the three and twelve months ended December 31, 2022, and December 31, 2021. ISG believes that evaluating its ongoing operating results will be enhanced if it discloses certain non-GAAP information. These non-GAAP financial measures exclude non-cash and certain other special charges that many investors believe may obscure the user’s overall understanding of ISG’s current financial performance and the Company’s prospects for the future. ISG believes that these non-GAAP measures provide useful information to investors because they improve the comparability of the financial results between periods and provide for greater transparency of key measures used to evaluate the Company’s performance.

ISG provides adjusted EBITDA (defined as net income plus interest, taxes, depreciation and amortization, foreign currency transaction gains/losses, non-cash stock compensation, interest accretion associated with contingent consideration, acquisition-related costs, and severance, integration and other expense), adjusted net income (defined as net income plus amortization of intangible assets, non-cash stock compensation, foreign currency transaction gains/losses, interest accretion associated with contingent consideration, acquisition-related costs, and severance, integration and other expense, on a tax-adjusted basis), adjusted net income per diluted share, adjusted EBITDA margin, gross-debt-to-adjusted-EBITDA ratio and selected financial data on a constant currency basis which are non-GAAP measures that the Company believes provide useful information to both management and investors by excluding certain expenses and financial implications of foreign currency translations, which management believes are not indicative of ISG’s core operations. These non-GAAP measures are used by ISG to evaluate the Company’s business strategies and management’s performance.

We evaluate our results of operations on both an as reported and a constant currency basis. The constant currency presentation, which is a non-GAAP financial measure, excludes the impact of year-over-year fluctuations in foreign currency exchange rates. We believe providing constant currency information provides valuable supplemental information regarding our results of operations, thereby facilitating period-to-period comparisons of our business performance and is consistent with how management evaluates the Company’s performance. We calculate constant currency percentages by converting our current and prior-periods local currency financial results using the same point in time exchange rates and then compare the adjusted current and prior period results. This calculation may differ from similarly titled measures used by others and, accordingly, the constant currency presentation is not meant to be a substitution for recorded amounts presented in conformity with GAAP, nor should such amounts be considered in isolation.

Management believes this information facilitates comparison of underlying results over time. Non-GAAP financial measures, when presented, are reconciled to the most closely applicable GAAP measure. Non-GAAP measures are provided as additional information and should not be considered in isolation or as a substitute for results prepared in accordance with GAAP. A reconciliation of the forward-looking non-GAAP estimates contained herein to the corresponding GAAP measures is not being provided, due to the unreasonable efforts required to prepare it.

About ISG

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 900 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs 1,600 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For more information, visit www.isg-one.com.

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 700 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For additional information, visit www.ISG-One.com

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q22 Results. ISG reported record fourth quarter revenue of $74.2 million, up from $69.6 million in the year ago period. FX negatively impacted revenue by $3.2 million. We had estimated $71 million. Fourth quarter net income was $4.3 million, GAAP EPS was $0.09, and adjusted EPS was $0.13. Adjusted EBITDA was $11.1 million, a 9% increase year-over-year. We forecasted net income of $4.45 million, EPS of $0.09, adjusted EPS of $0.13, and adjusted EBITDA of $10.6 million.

Segment Results. Reported revenues were $43.6 million in the Americas, up 12%; $23.9 million in Europe, up 1% on a reported basis and up 12% in constant currency; and $6.7 million in Asia Pacific, down 4% on a reported basis and up 5% in constant currency, all versus the prior year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Blackboxstocks, Inc. is a financial technology and social media hybrid platform offering real-time proprietary analytics and news for stock and options traders of all levels. Our web-based software employs “predictive technology” enhanced by artificial intelligence to find volatility and unusual market activity that may result in the rapid change in the price of a stock or option. Blackbox continuously scans the NASDAQ, New York Stock Exchange, CBOE, and all other options markets, analyzing over 10,000 stocks and up to 1,500,000 options contracts multiple times per second. We provide our users with a fully interactive social media platform that is integrated into our dashboard, enabling our users to exchange information and ideas quickly and efficiently through a common network. We recently introduced a live audio/video feature that allows our members to broadcast on their own channels to share trade strategies and market insight within the Blackbox community. Blackbox is a SaaS company with a growing base of users that spans 42 countries; current subscription fees are $99.97 per month or $959.00 annually. For more information, go to: www.blackboxstocks.com .

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Partnership. On Friday, Blackboxstocks announced a partnership with Boosted.ai to enhance artificial intelligence within the Blackbox platform. The platform will be leveraging the partnership to provide actionable alerts for both day trading and long term investment strategies. The partnership will provide Blackboxstocks’ retail investors with sophisticated investment tools and strategies that were previously only available to institutional investors. We view the partnership as beneficial to the Blackbox platform for both new and existing users, along with being an additive to potential marketing to garner new users.

Who Is Boosted.ai? Boosted.ai helps institutional investors energize their equity portfolios with artificial intelligence. Through its point-and-click AI software – Boosted Insights – Boosted.ai assists asset managers in finding opportunities for their funds. Boosted Insights uses machine learning to empower fund managers to augment their investment process to source new ideas, manage risk, and create alpha.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Blackboxstocks, Inc. is a financial technology and social media hybrid platform offering real-time proprietary analytics and news for stock and options traders of all levels. Our web-based software employs “predictive technology” enhanced by artificial intelligence to find volatility and unusual market activity that may result in the rapid change in the price of a stock or option. Blackbox continuously scans the NASDAQ, New York Stock Exchange, CBOE, and all other options markets, analyzing over 10,000 stocks and up to 1,500,000 options contracts multiple times per second. We provide our users with a fully interactive social media platform that is integrated into our dashboard, enabling our users to exchange information and ideas quickly and efficiently through a common network. We recently introduced a live audio/video feature that allows our members to broadcast on their own channels to share trade strategies and market insight within the Blackbox community. Blackbox is a SaaS company with a growing base of users that spans 42 countries; current subscription fees are $99.97 per month or $959.00 annually. For more information, go to: www.blackboxstocks.com .

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

CEO Form 4. On February 27th, the SEC released a Form 4 filing by CEO Gust Kepler that reported Mr. Kepler’s purchase of 1,130,002 BLBX shares on February 23rd at a price of $3 per share. The purchased increased Mr. Kepler’s direct common stock holding to 3,462,070 shares. According to the Company, this was a private transaction not conducted on an exchange. Mr. Kepler also owned 3,269,998 Series A Preferred shares as of December 27, 2022 that can be converted into common shares.

Investor Reaction. On Monday, BLBX shares rose 47% to close at $0.81 on 16.8 million shares traded. Normal average daily volume is 554,000 shares and the last time BLBX shares traded consistently in the $3 level was back in 2021, excluding a one-time spike in the share price in April 2022.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Firm improves financial flexibility, eliminates mandatory annual principal payments under new all-revolver facility with more favorable terms, extended maturity date

STAMFORD, Conn.–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III), a leading global technology research and advisory firm, today announced it has successfully amended its $140 million credit facility at more favorable terms, to improve the firm’s financial flexibility.

The new credit agreement amends the previous agreement entered into on March 10, 2020. Key updates include:

Converting the previous term and revolving loan into an all-revolving credit facility

Eliminating $4.3 million of mandatory annual principal payments due in 2023 and 2024

Extending the maturity date of the previous agreement by three years, to February 2028

“Our amended credit facility greatly enhances our financial flexibility and offers further validation of our robust business performance that enabled these enhancements,” said Michael P. Connors, chairman and CEO of ISG. “We thank our lenders for their partnership and confidence in our ability to deliver long-term sustainable growth and value for our shareholders.”

BofA Securities Inc. was the Sole Lead Arranger and Sole Bookrunner on the transaction.

Additional details about the amended credit agreement can be found in the Form 8-K ISG filed today with the U.S. Securities and Exchange Commission, a link to which can be found on ISG’s website.

Forward-Looking Statements

This communication contains “forward-looking statements” which represent the current expectations and beliefs of management of ISG concerning future events and their potential effects. Statements contained herein including words such as “anticipate,” “believe,” “contemplate,” “plan,” “estimate,” “target,” “expect,” “intend,” “will,” “continue,” “should,” “may,” and other similar expressions, are “forward-looking statements” under the Private Securities Litigation Reform Act of 1995. These forward-looking statements are not guarantees of future results and are subject to certain risks and uncertainties that could cause actual results to differ materially from those anticipated. Those risks relate to inherent business, economic and competitive uncertainties and contingencies relating to the businesses of ISG and its subsidiaries including without limitation: (1) failure to secure new engagements or loss of important clients; (2) ability to hire and retain enough qualified employees to support operations; (3) ability to maintain or increase billing and utilization rates; (4) management of growth; (5) success of expansion internationally; (6) competition; (7) ability to move the product mix into higher margin businesses; (8) general political and social conditions such as war, political unrest and terrorism; (9) healthcare and benefit cost management; (10) ability to protect ISG and its subsidiaries’ intellectual property or data and the intellectual property or data of others; (11) currency fluctuations and exchange rate adjustments; (12) ability to successfully consummate or integrate strategic acquisitions; (13) outbreaks of diseases, including coronavirus, or similar public health threats or fear of such an event; and (14) engagements may be terminated, delayed or reduced in scope by clients. Certain of these and other applicable risks, cautionary statements and factors that could cause actual results to differ from ISG’s forward-looking statements are included in ISG’s filings with the U.S. Securities and Exchange Commission. ISG undertakes no obligation to update or revise any forward-looking statements to reflect subsequent events or circumstances.

About ISG

ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 800 clients, including 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For more information, visit www.isg-one.com.

Comtech Telecommunications Corp. engages in the design, development, production, and marketing of products, systems, and services for advanced communications solutions in the United States and internationally. It operates in three segments: Telecommunications Transmission, Mobile Data Communications, and RF Microwave Amplifiers. The Telecommunications Transmission segment provides satellite earth station equipment and systems, over-the-horizon microwave systems, and forward error correction technology, which are used in various commercial and government applications, including backhaul of wireless and cellular traffic, broadcasting (including HDTV), IP-based communications traffic, long distance telephony, and secure defense applications. The Mobile Data Communications segment provides mobile satellite transceivers, and computers and satellite earth station network gateways and associated installation, training, and maintenance services; supplies and operates satellite packet data networks, including arranging and providing satellite capacity; and offers microsatellites and related components. The RF Microwave Amplifiers segment designs, develops, manufactures, and markets satellite earth station traveling wave tube amplifiers (TWTA) and broadband amplifiers. Its amplifiers are used in broadcast and broadband satellite communication; defense applications, such as telecommunications systems and electronic warfare systems; and commercial applications comprising oncology treatment systems, as well as to amplify signals carrying voice, video, or data for air-to-satellite-to-ground communications. The company serves satellite systems integrators, wireless and other communication service providers, broadcasters, defense contractors, military, governments, and oil companies. Comtech markets its products through independent representatives and value-added resellers. The company was founded in 1967 and is headquartered in Melville, New York.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Investor Meetings. We hosted Comtech CEO Ken Peterman and CFO Michael Bondi for a series of investor meetings in South Florida last week. In the meetings, CEO Peterman outlined the current progress made and future opportunities under his strategy to right the ship and grow from there.

The Present. Management spent time reviewing the actions already taken in regard to implementing the ONE Comtech vision. We expect the initial benefits of bringing the Company under one roof, including cost savings, more efficient use of capital, and the capture of additional business, will begin to flow into operating results in a noticeable way during the second half of fiscal 2023.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.