New home sales rang in 2026 with a troubling signal. January sales of newly built homes collapsed 17.6% month over month to a seasonally adjusted annualized rate of 587,000 units — the slowest pace since 2022 — according to data released Thursday by the U.S. Census Bureau. The drop was far steeper than analysts had projected, and it arrived against a backdrop that was supposed to be improving.

Year over year, sales were down 11.3%, with December’s already-soft numbers revised even lower. For homebuilders — many of them small and mid-cap companies already managing tight margins and bloated inventory — the report adds urgency to a housing sector that has yet to find solid footing.

The January data reflects signed contracts from a period when the average 30-year fixed mortgage rate was hovering between 6% and 6.2%, according to Mortgage News Daily. Rates have since climbed to 6.36%, meaning conditions in the months ahead are unlikely to produce a meaningful rebound without a catalyst. The Federal Reserve’s decision Wednesday to hold rates steady at 3.5%–3.75% — with the dot plot pointing to just one cut in 2026 — offers little relief for rate-sensitive buyers sitting on the sidelines.

To move inventory, builders have been reaching deeper into their toolkits. The median price of a new home sold in January fell to $400,500, a decline of 6.8% year over year. Yet the discounts aren’t clearing the market fast enough. Inventory climbed to a 9.7-month supply, up from eight months in December and 7.8% higher than a year ago. Completed homes sitting unsold are now near levels not seen since 2009.

The pain is spreading into March. An estimated 37% of builders cut prices in March, up from 36% in February, according to the National Association of Home Builders. Nearly two-thirds of builders are deploying additional incentives including mortgage rate buydowns to pull buyers across the finish line — a strategy that protects top-line revenue while quietly compressing margins.

Sales declined across every region, but the drops were not equal. The Northeast and Midwest could partially blame harsh winter weather. The West has no such excuse — sales there fell nearly 22% from December, suggesting demand destruction that runs deeper than seasonal disruption. Sun Belt markets, after years of speculative overbuilding, continue to be among the hardest hit.

For investors tracking small and mid-cap homebuilders, the January report is a reminder that volume recovery and margin recovery are not the same story. Companies relying heavily on incentive-driven sales risk deteriorating earnings quality even as unit counts look stable. With the Fed on hold, mortgage rates sticky above 6%, and consumer confidence still fragile, the setup for the spring selling season — typically the industry’s most critical window — looks challenged at best.

The pent-up demand is real. The question is whether affordability conditions improve fast enough to release it before builder balance sheets feel the weight.

The U.S. housing market showed renewed signs of life in November as pending home sales posted their strongest monthly increase in nearly two years. New data from the National Association of Realtors reveals that contract signings rose 3.3% compared with October, far exceeding expectations and signaling that buyer activity may be stabilizing after a prolonged slowdown.

Pending home sales are considered a leading indicator for the housing market because homes typically go under contract one to two months before a sale is finalized. The November increase pushed the Pending Home Sales Index up to 79.2, a notable improvement even though the reading remains below the long-term benchmark of 100, which reflects average activity levels in 2001. Compared with November of last year, pending sales increased 2.6%, suggesting demand is gradually recovering.

One of the most important drivers behind the uptick in housing activity has been improving affordability. Mortgage rates have eased from their recent highs, providing relief to buyers who had been priced out of the market. The average rate on a 30-year fixed mortgage has hovered near 6.2% in recent months, down from approximately 7% earlier in 2025 and well below levels seen during the summer. Even modest declines in interest rates can significantly reduce monthly mortgage payments, encouraging more buyers to re-enter the market.

Slower home price growth has also contributed to rising buyer confidence. After years of rapid appreciation, price gains have moderated across much of the country, helping incomes catch up with housing costs. At the same time, wage growth has remained relatively strong, further supporting affordability and boosting purchasing power.

Regionally, pending home sales rose across all parts of the United States in November. The West recorded the largest month-over-month increase at 9.2%, reflecting strong pent-up demand in markets that were previously among the most constrained by affordability challenges. Gains in the Midwest, South, and Northeast suggest the recovery is becoming more evenly distributed rather than concentrated in isolated markets.

Inventory levels, while still tight by historical standards, have improved compared with last year. More homes available for sale have given buyers greater flexibility and reduced competitive pressures that previously discouraged many from making offers. This gradual improvement in supply has helped support the rise in contract activity without reigniting runaway price growth.

Despite the positive momentum, the housing market remains in a fragile recovery phase. Overall home sales in 2025 are still expected to rank near three-decade lows, underscoring how deeply elevated interest rates disrupted activity over the past several years. Many homeowners remain reluctant to sell because doing so would mean giving up ultra-low mortgage rates secured before 2022.

Looking ahead, housing market forecasts suggest a slow and uneven normalization rather than a sharp rebound. Continued declines in mortgage rates, steady wage growth, and incremental improvements in inventory will be critical to sustaining buyer demand. November’s surge in pending home sales does not mark a full recovery, but it does indicate that homebuyer momentum is building and that the long housing slowdown may be starting to ease.

This combination of improving affordability, stabilizing prices, and renewed buyer interest positions the housing market for a potentially stronger 2026 if current trends continue.

WEST HARRISON, N.Y.–(BUSINESS WIRE)–Sky Harbour Group Corporation (NYSE: SKYH, SKYH WS) (“SHG” or the “Company”), an aviation infrastructure company building the first nationwide network of Home Base Operator (HBO) campuses for business aircraft, announced the closing of a $200 million tax-exempt warehouse drawdown committed bank facility. The initial borrower is Sky Harbour Capital II, LLC (“SKYH Capital II”), a wholly owned subsidiary of SHG. The lender and administrative agent is JPMorgan Chase Bank (“J.P. Morgan”). The initial tax-exempt note underlying the committed facility (the “JPM Facility”) was issued through the Public Finance Authority (Wisconsin) (“PFA”).

The JPM Facility’s principal terms include: drawdowns for eligible new hangar projects, 65% leverage, a 5-year bullet maturity, 80% of (SOFR+0.10%) plus a 200bps applicable margin as the tax-exempt annual interest rate, capitalized monthly interest during the first three years, and no prepayment penalty at the time of refinancing. At present, the applicable floating interest rate is approximately 5.60%. Subject to credit approval, the JPM Facility may be expanded to $300 million. Additional information may be found in our related filing under Form 8-K with the SEC.

Tal Keinan, Sky Harbour’s CEO, commented: “We thank our new lending partners at J.P. Morgan for their trust and their creativity in designing a facility that elegantly meets Sky Harbour’s specific needs.”

Francisco Gonzalez, Sky Harbour’s CFO, commented further: “After a highly competitive process that included numerous banks and products, we determined that the tax-exempt warehouse drawdown committed bank facility that closed yesterday is the most favorable and cost-efficient borrowing mechanism for the funding of our next set of projects. The JPM Facility provides us with flexibility to draw when we need to and refinance into long term bonds at the optimal time.”

McGuireWoods LLP acted as administrative agent and lender’s counsel to J.P. Morgan. Attolles Law, S.C. acted as issuer counsel to PFA. Greenberg Traurig, LLP acted as tax and bond counsel and Morrison & Foerster LLP acted as corporate counsel to the initial borrower, SKYH Capital II. Lexton Infrastructure Solutions LLC acted as financial advisor to the Company.

About Sky Harbour

Sky Harbour Group Corporation is an aviation infrastructure company developing the first nationwide network of Home-Basing campuses for business aircraft. The company develops, leases, and manages general aviation hangar campuses across the United States. Sky Harbour’s Home-Basing offering aims to provide private and corporate residents with the best physical infrastructure in business aviation, coupled with dedicated service, tailored specifically to based aircraft, offering the shortest time to wheels-up in business aviation. To learn more, visit www.skyharbour.group.

Forward Looking Statements

Certain statements made in this release are “forward looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995, including statements about the financial condition, results of operations, earnings outlook and prospects of SHG, including statements regarding our expectations for future results, our expectations for future ground leases, our expectations on future construction and development activities and lease renewals, and our plans for future financings. When used in this press release, the words “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions (or the negative versions of such words or expressions) are intended to identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. The forward-looking statements are based on the current expectations of the management of Sky Harbour Group Corporation (the “Company”) as applicable and are inherently subject to uncertainties and changes in circumstances. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. For more information about risks facing the Company, see the Company’s annual report on Form 10-K for the year ended December 31, 2024 and other filings the Company makes with the SEC from time to time. The Company’s statements herein speak only as of the date hereof, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Contacts

Sky Harbour Investor Relations: [email protected] Attn: Francisco X. Gonzalez

U.S. home sales showed signs of renewed momentum in July, offering a glimmer of relief for buyers and sellers navigating one of the tightest housing markets in years. According to data from the National Association of Realtors, sales of previously owned homes increased 2% from June to a seasonally adjusted annual rate of 4.01 million units. That figure also marked a 0.8% gain compared with July 2024, defying expectations of a modest decline.

The pickup in activity reflects contracts that were signed earlier in the summer, when mortgage rates began to edge down from their spring highs. The average 30-year fixed mortgage briefly exceeded 7% in May but had retreated to around 6.67% by the end of June. That shift helped unlock demand from buyers who had been sidelined by affordability challenges.

At the same time, supply conditions continued to improve. The number of homes available for sale at the end of July climbed to 1.55 million, up nearly 16% from a year ago. That level represents a 4.6-month supply at the current sales pace, the highest since May 2020 but still short of the six-month threshold considered a balanced market. For prospective buyers, the increase in inventory has translated into more choice and slightly less upward pressure on prices.

Even so, home values remain stubbornly high. The median price of an existing home sold in July reached $422,400, a record for the month and 0.2% higher than a year earlier. That marked the 25th consecutive month of annual price gains, underscoring how persistent demand and limited long-term supply continue to shape the market. Still, with wage growth now outpacing home price appreciation in some regions, economists suggest the market could be approaching an inflection point where affordability begins to improve.

Regional and price-segment dynamics reveal additional shifts. Sales activity has been strongest at the higher end of the market, with transactions on homes priced above $1 million jumping more than 7% from a year ago. In contrast, sales of properties priced below $250,000 remained flat or declined, squeezed by limited availability and still-elevated borrowing costs. In the South, where condominium prices have fallen over the past year, demand for that segment showed particular resilience.

Market behavior also reflects growing participation from investors and cash buyers. Investors accounted for 20% of transactions in July, up sharply from 13% a year earlier, likely taking advantage of the increased supply. Meanwhile, 31% of sales were completed with all cash, compared with 27% last July. That unusually high share suggests that wealth from equities and housing gains is playing a greater role in the market.

Homes are also taking longer to sell. The typical property stayed on the market for 28 days in July, compared with 24 days a year ago. First-time buyers accounted for just 28% of sales, slipping from both June and the same month last year, reflecting the ongoing affordability strain at the entry level of the market.

Overall, July’s data points to a housing sector that is slowly recalibrating. Rising inventory and moderating mortgage rates are offering incremental relief, yet prices remain elevated, and demand is concentrated in higher price tiers. Whether the market has reached a true turning point may depend on the Federal Reserve’s next moves on interest rates and how quickly supply can return to more balanced levels.

WEST HARRISON, N.Y.–(BUSINESS WIRE)– Sky Harbour Group Corporation (NYSE: SKYH, SKYH WS) (“SHG” or the “Company”), an aviation infrastructure company building the first nationwide Home Base Operator (HBO) network of campuses for business aircraft, announced the release of its unaudited financial results for the three months ended June 30, 2025 on Form 10-Q. The Company also announced the filing of its unaudited financial results for the three months ended June 30, 2025 for Sky Harbour Capital (Obligated Group) with MSRB/EMMA. Please see the following links to access the filings:

Financial Highlights on a Consolidated Basis include:

Constructed assets and construction in progress reached over $295 million at quarter end, an increase of $125 million year-over-year and $18 million as compared to the prior quarter.

Q2 2025 consolidated revenues increased 82% as compared to Q2 2024 and 18% as compared to the prior quarter.

Net cash used in operating activities was approximately $0.9 million for the quarter, a significant improvement from the $5 million used in prior quarter.

Strong liquidity and capital resources as of June 30th, 2025, with consolidated cash and US Treasuries totaling nearly $75 million.

Reiterating our guidance of reaching operating cash-flow breakeven on a consolidated run-rate basis by year-end 2025, supported by the commencement of revenues from campuses in Phoenix, Denver, Dallas and Seattle.

Financial Highlights at Sky Harbour Capital (Obligated Group) include:

Q2 2025 Obligated Group Revenues increased approximately 20% as compared to the prior quarter.

Net cash from operating activities (positive) reached approximately $2.2 million in Q2 2025, a 117% increase from the prior quarter.

Cash and US Treasuries at the Obligated Group totaled $37 million as of June 30th, 2025.

Update on Site Acquisition

Sky Harbour currently has campuses operating at Houston’s Sugar Land Regional Airport (SGR), Nashville International Airport (BNA), Miami Opa-Locka Executive Airport (OPF), San Jose Mineta International Airport (SJC), Camarillo Airport (CMA), Phoenix Deer Valley Airport (DVT), Dallas’s Addison Airport (ADS), Seattle’s King County International Airport – Boeing Field (BFI); one campus nearing construction completion at Denver’s Centennial Airport (APA); campuses in pre-development at Chicago Executive Airport (PWK), Sky Harbour’s first four New-York-metro area airports – Bradley International Airport (BDL), Hudson Valley Regional Airport (POU), Trenton-Mercer Airport (TTN), and Stewart International Airport (SWF); Orlando Executive Airport (ORL), Dulles International Airport (IAD), Salt Lake City International Airport (SLC), and Portland-Hillsboro Airport (HIO).

We reiterate our prior guidance of five additional airport ground leases to be announced by the end of 2025, for a total portfolio of 23 airports by year end.

Update on Construction and Development Activities, Change in Development Leadership

As reported on our monthly activity reports filed with MSRB/EMMA, and available on our website, Dallas Addison (ADS) achieved its first Certificates of Occupancy in Q2 and has commenced resident flight operations. Denver Centennial (APA) achieved its first Certificates of Occupancy last month and will commence resident flight operations in the coming weeks. Please see the following link for the last monthly construction report:

Miami Opa Locka (OPF) Phase 2 commenced construction in Q2 and is expected to be completed by Q2 2026.

Outgoing COO, Will Whitesell, who led the Company’s construction division, has entered an amicable separation agreement with the Company and has assisted in an orderly transfer of his responsibilities. The Company is grateful for Will’s commitment and his contributions and wishes him much success in his future endeavors.

Phil Amos, a 40-year veteran of the Pre-Engineered Metal Building (PEMB) industry, and co-founder of A&F Contractors, has joined Sky Harbour as Head of Construction and President of Sky Harbour’s newly-formed, wholly-owned development subsidiary, Ascend Aviation Services (“Ascend”). Ascend brings specialized airport construction-management and in-house General Contracting capabilities to Sky Harbour. Ascend is headquartered in Houston, TX, and staffed by veterans of the airport construction industry around the United States, including legacy members of the Sky Harbour development team. In addition to its construction management and general contracting functions, Ascend oversees the operations of Stratus Building Systems, Sky Harbour’s wholly-owned PEMB manufacturing subsidiary. Ascend and Stratus together constitute a vertically-integrated, specialized airport infrastructure developer. Mr. Amos, while at A&F, served as the general contractor for Sky Harbour’s first hangar campus at Sugar Land Regional Airport, which was delivered on time and under budget.

Update on Leasing Activities

Stabilized campuses: The Company continues to enjoy higher-than-forecast revenue per square foot at its stabilized campuses. Revenue per square foot continues to grow as legacy hangar leases turn or are renewed.

New campuses: The Company has executed the first six hangar leases at its new Denver, Dallas and Phoenix campuses, and is under LOI for additional leases. The Company expects to meet its revenue run-rate targets at the new campuses within six months.

Pre-leasing: The Company has initiated a pilot project at two airports – Bradley International Airport (BDL) and Dulles International Airport (IAD) to pre-lease hangar space prior to construction commencement. The objective is to take advantage of growing awareness of the Sky Harbour HBO value proposition within the US Business Aviation industry to a) reduce lease-up times, b) better curate resident communities, and c) integrate customized resident improvements during construction (as opposed to retrofitting). Hangar leases have been executed at both airports at revenue rates that present an introductory pricing advantage to pre-lease residents while still delivering above-target per-square-foot revenue to the Company. Additional pre-leases are under LOI.

Update on Airport Operations

As of Q3, the Company is conducting flight operations at nine airports.

Under the leadership of Marty Kretchman, Senior Vice President of Airports, the company has transitioned to a centralized operating model, featuring National Directors of Line Training; Facilities; and Ground Support Equipment (GSE).

Surveys of current residents indicate that Sky Harbour’s HBO service offering has become a key differentiating component of the Sky Harbour value proposition. The Company plans to continue to invest in constant improvement in airfield operations, through selective recruiting, rigorous training, detailed and thoughtful operating procedures, and constant innovation in collaboration with Sky Harbour residents.

Update on Capital Formation

After several quarters of “dual tracking” the review of various debt funding alternatives and proposals, the Company has decided to pursue a tax-exempt bank debt facility in lieu of a bond issue.

We are currently in advanced discussions with a major US financial institution for an expected five (5) year drawdown construction facility of $200 million, with an expected indicative interest rate of 80% of 3-month SOFR plus 200 basis points (~5.47% in the current market).

Our debt financing plan is to fund the next 5-6 airport projects using this facility and internal equity. The Company expects to replace this facility with permanent tax-exempt bonds in the next 3-4 years. We expect to close the facility on or about August 28th. However, we can provide no assurance on exact terms or the timing of this facility.

Tal Keinan commented: “As Sky Harbour navigates the transition from a tactical team, emphasizing agility, innovation and flexibility, to a high-growth organization, increasingly embracing process, discipline and specialization, five constants will continue to guide our leadership: 1) Obsessive focus on the Resident, 2) Commitment to building long-term shareholder value, 3) Uncompromising pursuit of professional excellence, 4) Cost-efficiency, and 5) Individual ownership of results. We value the reputation we are building in business aviation and intend to continue building it for years to come.”

About Sky Harbour

Sky Harbour Group Corporation is an aviation infrastructure company developing the first nationwide network of Home-Basing campuses for business aircraft. The company develops, leases, and manages general aviation hangar campuses across the United States. Sky Harbour’s Home-Basing offering aims to provide private and corporate residents with the best physical infrastructure in business aviation, coupled with dedicated service, tailored specifically to based aircraft, offering the shortest time to wheels-up in business aviation. To learn more, visit www.skyharbour.group.

Forward Looking Statements

Certain statements made in this release are “forward looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995, including statements about the financial condition, results of operations, earnings outlook and prospects of SHG, including statements regarding our expectations for future results, our expectations for future ground leases, our expectations on future construction and development activities and lease renewals, and our plans for future financings. When used in this press release, the words “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions (or the negative versions of such words or expressions) are intended to identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. The forward-looking statements are based on the current expectations of the management of Sky Harbour Group Corporation (the “Company”) as applicable and are inherently subject to uncertainties and changes in circumstances. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. For more information about risks facing the Company, see the Company’s annual report on Form 10-K for the year ended December 31, 2024 and other filings the Company makes with the SEC from time to time. The Company’s statements herein speak only as of the date hereof, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Key Performance Indicators

We use a number of metrics, including annualized revenue run rate per leased rentable square foot, to help us evaluate our business, measure our performance, identify trends affecting our business, formulate business plans, and make strategic decisions. Our key performance indicators may be calculated in a manner different than similar key performance indicators used by other issuers. These metrics are estimated operating metrics and not projections, nor actual financial results, and are not indicative of current or future performance.

Key Points: – Trump says his administration is exploring the removal of capital gains taxes on home sales. – The move could unlock capital, boost housing turnover, and benefit housing-related sectors. – Middle-market and small-cap real estate and home improvement firms could see upside from rising transaction activity.

In a surprising policy hint that could reshape the U.S. housing market, President Donald Trump said Tuesday his administration is “thinking about no tax on capital gains on houses.” The statement, delivered from the Oval Office, comes as part of a broader economic playbook aimed at fueling consumer momentum ahead of the 2026 election cycle.

Currently, profits from home sales are subject to capital gains taxes, though homeowners selling their primary residences can deduct up to $250,000 (single) or $500,000 (married) under existing law. Trump’s proposal — which aligns with a new bill introduced by Rep. Marjorie Taylor Greene — would eliminate capital gains tax altogether on home sales, potentially removing one of the biggest friction points in residential real estate.

For investors — particularly in the middle market and small-cap sectors — the implications could be significant.

Removing capital gains tax on homes could encourage long-time homeowners to sell, freeing up inventory in tight markets and fueling demand for adjacent sectors: real estate brokerages, mortgage services, homebuilders, renovation companies, and material suppliers. Small-cap firms in these industries, which have lagged amid high interest rates and a sluggish housing turnover rate, may find themselves back in favor.

The policy could also revive investor sentiment in the residential property space. With more liquidity available and tax incentives restored, buyers may re-enter the market more aggressively, especially if paired with a future Fed rate cut — something Trump alluded to when he said, “If the Fed would lower the rates, we wouldn’t even have to do that.”

From a strategic standpoint, eliminating taxes on home sales would shift housing from being just a lifestyle decision to a more liquid investment vehicle — benefiting not only homeowners but potentially boosting real estate stocks, REITs, and companies supporting the housing ecosystem.

Critics argue such a move could overheat the housing market or primarily benefit wealthier Americans. However, for investors with an eye on undervalued small-cap plays, this policy could be the catalyst that reopens stalled growth pipelines in sectors tied to home transactions — particularly construction, hardware, lending tech, and residential services.

It also ties into a broader trend: a return to asset-based investing over speculative tech — with hard assets like homes, precious metals, and infrastructure increasingly seen as reliable anchors during fiscal uncertainty.

While the proposal is far from finalized, the conversation alone signals that real estate is back on the national economic agenda — and may offer renewed upside for investors willing to look beyond the large caps.

Key Points: – Mortgage rates edge up — 30-year fixed rates rose to 6.89%, tracking higher Treasury yields. – Buyer affordability hit — High rates continue to suppress home sales and affordability. – Applications mixed — Purchase applications rose 3%, while refinance demand fell 7%.

Mortgage rates rose modestly this week, with the average 30-year fixed loan hitting 6.89%, up slightly from 6.86% the week before. The 15-year average also inched higher to 6.03%, reflecting the continued influence of Treasury yields, which have been volatile amid shifting economic signals.

The movement in mortgage rates follows recent fluctuations in the 10-year Treasury yield, a key benchmark for borrowing costs. Investors have been digesting a complex mix of developments, including the U.S. credit rating downgrade, the fiscal implications of proposed tax reforms, and evolving trade policy. While yields dipped slightly in recent days, overall borrowing costs remain elevated.

High mortgage rates continue to act as a headwind for the housing sector. According to newly released data, pending home sales dropped sharply in April, underscoring how rate-sensitive the market remains. Despite a modest weekly increase in home purchase applications, affordability challenges persist, particularly for first-time buyers and middle-income households.

This constrained environment has implications beyond real estate. A sluggish housing market can ripple through related industries—from homebuilding and furniture to construction materials and local services—potentially influencing performance in sectors that rely on consumer confidence and discretionary spending.

Although refinancing activity dropped by 7%, the slight increase in purchase applications signals that some buyers are still moving forward, especially those less sensitive to rate fluctuations or motivated by limited inventory. Nonetheless, sustained high rates may continue to delay broader recovery in housing-related demand.

In this climate, market participants are keeping a close eye on interest rate trends and consumer sentiment data, both of which remain central to shaping the economic outlook. As borrowing costs remain elevated, the pressure on housing and adjacent industries may persist—adding another layer of complexity to growth expectations in the months ahead.

Key Points: – Rocket Companies has announced a $1.75 billion all-stock acquisition of real estate brokerage Redfin. – Redfin’s stock surged over 76%, while Rocket’s shares dropped by 10% following the announcement. – The merger aims to streamline the home-buying process by integrating mortgage lending, brokerage, and real estate listings into one ecosystem.

Rocket Companies, a leading mortgage lender, has announced plans to acquire digital real estate brokerage Redfin in an all-stock transaction valued at $1.75 billion. The move seeks to integrate home search, brokerage services, mortgage lending, and title services under one platform, creating a more seamless and cost-efficient home-buying experience for consumers.

The acquisition is positioned as a strategic effort to modernize and consolidate the fragmented home-buying process. Rocket CEO Varun Krishna emphasized the inefficiencies in the current system, where home search, brokerage, mortgage, and title services exist in separate ecosystems. By combining Rocket’s mortgage and financing capabilities with Redfin’s online brokerage and home search platform, the companies aim to streamline the process and reduce transaction costs, which currently total around 10% of a home’s price.

Redfin, founded in 2004, operates a technology-driven real estate platform with over one million for-sale and rental listings and employs more than 2,200 agents. Rocket Companies, best known for its Rocket Mortgage brand, sees the acquisition as a natural fit to leverage artificial intelligence and automation to accelerate the homebuying process.

Following the announcement, Redfin shares skyrocketed by over 76%, reflecting investor enthusiasm for the deal’s potential to reshape the real estate industry. Meanwhile, Rocket’s stock fell by 10%, as investors weighed the financial implications of the transaction. The deal values Redfin at $12.50 per share, a 115% premium over its last closing price before the announcement.

Under the terms of the agreement, Redfin shareholders will receive approximately 0.8 shares of Rocket stock for each share of Redfin they own. Once the deal is finalized, current Rocket shareholders will own about 95% of the combined company, with Redfin shareholders controlling the remaining 5%. Rocket shareholders will also receive a special dividend of $0.80 per share.

The companies project that the merger will generate $200 million in cost synergies by 2027, including $140 million in operational efficiencies and an additional $60 million from enhanced collaboration between Redfin’s agents and Rocket’s financing platform. By aligning these services, the combined company aims to close home transactions faster and provide a more seamless customer experience.

Redfin CEO Glenn Kelman will continue to lead the business post-merger and will report directly to Rocket CEO Varun Krishna. The deal has been approved by both companies’ boards and is expected to close in the second or third quarter of 2025, pending regulatory approval and customary closing conditions.

This acquisition comes at a time of volatility in the housing market, with high mortgage rates and tight housing supply impacting affordability. Redfin’s stock, once trading near $96 per share at its pandemic peak in 2021, has struggled in the higher-rate environment. Rocket Companies, which went public in 2020, has similarly faced headwinds as mortgage demand has declined.

By integrating home search and mortgage lending, Rocket and Redfin could provide consumers with a more efficient home-buying experience. However, questions remain about execution risks and how regulators will view the increased consolidation of real estate services.

Key Points: – Existing home sales dropped 5.4% in June, indicating a market slowdown – Housing inventory increased by 23.4% year-over-year, yet prices continue to rise – Market shows signs of transitioning from a seller’s to a buyer’s market

The U.S. housing market is showing signs of a significant shift, as June’s home sales data points to a cooling market and a potential transition favoring buyers. According to the latest report from the National Association of Realtors (NAR), sales of previously owned homes declined by 5.4% in June compared to May, reaching an annualized rate of 3.89 million units. This marks the slowest sales pace since December and represents a 5.4% decrease from June of the previous year.

The slowdown in sales can be largely attributed to the spike in mortgage rates, which surpassed 7% in April and May. Although rates have slightly retreated to the high 6% range, the impact on buyer behavior is evident. Lawrence Yun, chief economist for the NAR, noted, “We’re seeing a slow shift from a seller’s market to a buyer’s market.”

One of the most significant changes in the market is the substantial increase in housing inventory. The number of available homes jumped 23.4% year-over-year to 1.32 million units at the end of June. While this represents a considerable improvement from the record lows seen recently, it still only amounts to a 4.1-month supply, falling short of the six-month supply typically considered balanced between buyers and sellers.

The surge in inventory is partly due to homes remaining on the market for longer periods. The average time a home spent on the market increased to 22 days, up from 18 days a year ago. This extended selling time, coupled with buyers’ increasing insistence on home inspections and appraisals, further indicates a shift in market dynamics.

Interestingly, despite the increased supply and slower sales, home prices continue to climb. The median price of an existing home sold in June reached $426,900, marking a 4.1% increase year-over-year and setting an all-time high for the second consecutive month. However, this price growth is not uniform across all segments of the market.

The higher end of the market, particularly homes priced over $1 million, was the only category experiencing sales gains compared to the previous year. In contrast, the most significant drop in sales occurred in the $250,000 and lower range. This disparity highlights the ongoing affordability challenges in the housing market, especially for first-time buyers and those seeking lower-priced homes.

The changing market conditions are also influencing buyer behavior. Cash purchases increased to 28% of sales, up from 26% a year ago, while investor activity slightly decreased to 16% of sales from 18% the previous year. These trends suggest that well-funded buyers are still active in the market, potentially taking advantage of the increased inventory and longer selling times.

Looking ahead, the market’s trajectory remains uncertain. Yun suggests that if inventory continues to increase, one of two scenarios could unfold: either home sales will rise, or prices may start to decrease if demand doesn’t keep pace with supply. The influx of smaller and lower-priced listings, as noted by Danielle Hale, chief economist for Realtor.com, could help moderate overall price growth and potentially improve affordability for some buyers.

As the housing market navigates this transition, both buyers and sellers will need to adjust their strategies. Buyers may find more options and negotiating power, while sellers may need to be more flexible on pricing and terms. The coming months will be crucial in determining whether this shift towards a buyer’s market solidifies or if other factors, such as potential changes in mortgage rates or economic conditions, alter the market’s trajectory once again.

Mortgage rates fell to their lowest level in seven months this past week, providing a glimmer of hope for homebuyers who have been sidelined by high borrowing costs.

The average rate on a 30-year fixed mortgage dropped to 6.60% according to Freddie Mac, down from a recent peak of nearly 8% in October 2023. While still high historically, the retreat back below 7% could draw more prospective homebuyers back into the market.

The dip in rates comes as the housing market is showing early signs of a potential turnaround after a dismal 2023. Home sales plunged nearly 18% last year as surging mortgage rates and stubbornly high prices made purchases unaffordable for many.

But January has seen some positive signals emerge. More homes are coming up for sale as sellers who waited out 2023 finally list their properties. Real estate brokerage Redfin reported a 9% annual increase in inventory in January, the first year-over-year gain since 2019.

At the same time, buyer demand is also perking back up with the improvement in affordability. Mortgage applications jumped 10% last week compared to the prior week according to the Mortgage Bankers Association. While purchase apps remain below year-ago levels, the turnaround suggests buyers are returning.

“If rates continue to ease, MBA is cautiously optimistic that home purchases will pick up in the coming months,” said Joel Kan, MBA’s Vice President of economic and industry forecasting.

The increase in supply and demand has some experts predicting the market may be primed for a rebound in the spring home shopping season. But whether the inventory can satisfy purchaser interest remains uncertain.

“As purchase demand continues to thaw, it will put more pressure on already depleted inventory for sale,” noted Freddie Mac Chief Economist Sam Khater.

Homebuilders have pulled back sharply on new construction as sales slowed over the past year. And many current owners are still hesitant to sell with mortgage rates on their existing homes likely much lower than what they could get today. That leaves the total number of homes available for sale still historically lean.

Nonetheless, agents are reporting more bidding wars again for the limited inventory available in some markets. While not at the frenzied pace of 2022, competition for the right homes is heating up. Experts say interested buyers may want to start making offers now before the selection gets picked over.

“I’m advising house hunters to start making offers now because the market feels pretty balanced,” said Heather Mahmood-Corley, a Redfin agent. “With activity picking up, I think prices will rise and bidding wars will become more common.”

The driver of the downturn in rates since late last year has been an overall cooling of inflation pressures. The Federal Reserve pushed the 30-year fixed mortgage above 7% for the first time in over 20 years with its aggressive interest rate hikes aimed at taming inflation.

But evidence is mounting that the Fed’s policy actions are having the desired effect. Consumer price increases have steadily moderated from 40-year highs last summer. The slower inflation has allowed the central bank to reduce the size of its rate hikes.

Markets now expect the Fed to lift its benchmark rate 0.25 percentage points at its next meeting, a smaller move compared to the 0.50 and 0.75 point hikes seen last year. The slower pace of increases has taken pressure off mortgage rates.

However, the Fed reiterated it plans to keep rates elevated for some time to ensure inflation continues easing. Most experts do not foresee the central bank cutting interest rates until 2024 at the earliest. That means mortgage rates likely won’t fall back to the ultra-low levels seen during the pandemic for years.

But for homebuyers who can manage the higher rates, the recent pullback provides some savings on monthly payments. On a $300,000 loan, the current average 30-year rate would mean about $140 less in the monthly mortgage bill versus the fall peak above 8%.

While housing affordability remains strained by historical standards, some buyers are jumping in now before rates potentially move higher again. People relocating or needing more space are finding ways to cope with the increased costs.

With some forecasts calling for home prices to edge lower in 2024, this year could provide an opportunity for buyers to get in after sitting out 2023’s rate surge. It may be a narrow window however. If demand accelerates faster than supply, the competition and price gains could return quickly.

Pending home sales in the U.S. unexpectedly plunged in October to their lowest levels since record-keeping began over two decades ago, even below readings seen during the housing crisis in 2008.

The National Association of Realtors (NAR) reported Thursday that its index of pending sales contracts signed on existing homes retreated 1.5% from September. On an annual basis, signings were a staggering 8.5% lower than the same month last year.

October’s reading marks a continuation of the housing market’s steep slide over the past year from blistering pandemic-era sales levels as mortgage rates rocket higher in the most dramatic housing finance shake-up in decades.

“Recent weeks’ successive declines in mortgage rates will help qualify more home buyers, but limited housing inventory is significantly preventing housing demand from fully being satisfied,” said NAR Chief Economist Lawrence Yun.

Spike in Mortgage Rates Strangles Demand

The October pending home sales data reflects buyer activity when popular 30-year fixed mortgage rates shot up above 8% in mid-October before settling back around 7% in more recent weeks.

Skyrocketing borrowing costs over the past year have rapidly depleted home shoppers’ budgets and purchasing power, squeezing huge numbers of Americans out of the market entirely and forcing others to downgrade to lower price points.

With the average rate on a 30-year fixed loan more than double year-ago levels despite the recent retreat, still-high financing costs in tandem with stubbornly elevated home prices continue dampening affordability and sales.

All U.S. regions saw contract signings decline on a monthly basis in October except the Northeast. The Western market, where homes are typically the nation’s most expensive, recorded the largest monthly drop.

Pending transactions fell across all price tiers below $500,000 while rising for homes above that threshold. The shift partly reflects moderately improving supply conditions on the high end, even as demand rapidly recedes at lower price points.

Home Prices Still Climbing for Now

Even against shrinking demand, exceedingly tight inventories of homes listed for sale have so far prevented any meaningful cooling in the torrid home price appreciation that’s stretched affordability near the breaking point for many buyers.

The median existing home sales price rose 6.6% on the year in October to $379,100. While marking a slowdown from mid-2021, when prices were soaring 20% annually, it still represents an acceleration over the 5.7% rate seen last October.

With few homes hitting the market, bidding wars continue breaking out for even modest starter homes in many areas. In such seller-favorable conditions, a plunge in overall sales does little to crimp further rapid home value growth.

Leading indicators suggest home prices likely still have further to climb before lackluster sales and eroding affordability force more substantive cooling. But shifts in home values and sales usually lag moves in rates and mortgage activity by several months.

“The significant decline in pending sales suggests…further weakness in closed existing home sales in upcoming months,” said Swiss bank UBS economist Jonathan Woloshin.

With mortgage activity plunging to a quarter-century low, actual completed sales are widely expected to continue deteriorating into early next year or beyond as the pipe of signed deals still working through the market keeps drying up.

Path Ahead for Housing Market

Most economists expect home sales will likely continue slumping over the next six months or so until lower financing costs combined with a slow improving inventory offer some stability.

“We think housing activity has little prospect of bottoming out until spring 2024, at the earliest,” said Nancy Vanden Houten of Oxford Economics. She projects existing home sales will fall nearly 25% in 2024 from current-year levels.

Other analysts say still-strong demographics and a solid job market should prevent an all-out housing collapse, but that robust spring and summer recovery rallies like those seen earlier this century are unlikely in coming years.

Instead, as mortgage rates settle somewhere above 6% and homes trickle back on the market, sales activity should slowly stabilize around 10-15% below 2018-2019 levels through 2024 and beyond – marking a ‘new normal’ after ultra-hot pandemic conditions.

“I expect mortgage rates to moderate…helping home sales firm up a bit, but still remain below pre-pandemic activity,” said Yun. With fresh records signaling just how devastating this year’s rate spike proved for buyers, Yun expects the spring thaw in housing demand could come slower next year than markets anticipate.

Without the Fed’s easy money, demand for housing would collapse, according to Ryan McMaken. McMaken, who authored the below article, is a former housing economist for the State of Colorado. He believes once the Fed pivots back to forcing down interest rates and again buying mortgage-backed securities (MBS), housing prices that have recently dipped, will again continue their march upward. He makes the case here that the housing market, without Fed support, faces difficult headwinds. – Paul Hoffman, Managing Editor, Channelchek

Last Friday, residential real estate brokerage firm Redfin released new data on home prices, showing that prices fell 0.6 percent in February, year over year. According to Redfin’s numbers, this was the first time that home prices actually fell since 2012. The year-over-year drop was pulled down by especially large declines in five markets: Austin (-11%), San Jose, California (-10.9%), Oakland (-10.4%), Sacramento (-7.7%), and Phoenix (-7.3%). According to Redfin, the typical monthly mortgage payment is now at a record high of $2,520.

The Redfin numbers come a few days before new numbers from the Case-Shiller home price index showing further slowing in home prices growth since late last year. The market’s expectation for December’s 20-city index had been -0.5 percent, month over month, and 5.8 percent, year over year. But the numbers came in worse (from the seller’s perspective) than was hoped. For December—the most recent monthly data available—the index ended up showing a month-over-month drop of -1.5 percent (seasonally adjusted), and a year-over-year gain of 4.6 percent (not seasonally adjusted).

By most accounts, the rapidly-slowing market faces headwinds thanks to rising interest rates, including the standard 30-year fixed mortgage, which is now back up over 6 percent. This puts homeownership out of reach for many first-time buyers and is also a big disincentive for current owners to “move-up” into higher-priced houses since any new home would come with a much higher mortgage rate than was available a year ago.

Not surprisingly, demand for new mortgages has plummeted. CNBC reported last week:

“Mortgage applications to purchase a home dropped 6% last week compared with the previous week, according to the Mortgage Bankers Association’s seasonally adjusted index. Volume was 44% lower than the same week one year ago and is now sitting at a 28-year low.”

So, sales have fallen and, at least according to Redfin, prices are falling too. This is what we should expect to see in any environment where the real estate market is not being incessantly fueled by easy money from the central bank. After all, easy money for real estate markets had been the main story since 2009. In recent months, however, the Fed has allowed interest rates to rise while pausing efforts to add more mortgage-backed securities (MBS) to the Fed’s portfolio. Without those key supports from policymakers, the real estate market simply lacks the market demand that is necessary to sustain rapid growth. Contrary to what countless mortgage brokers and real estate agents tell themselves and each other, there is precious little capitalism in real estate markets. It is a market that is thoroughly addicted to, and dependent on, continued stimulus and subsidization from the central bank.

Without the central bank propping up MBS demand in the secondary market, primary-market mortgage lenders have fewer dollars to throw around. That means higher interest rates and fewer eligible buyers. Similarly, by setting a higher target rate for the federal funds rate that banks must pay to manage liquidity, markets face less monetary growth in general. That comes with a lessening overall demand that—in the short term, at least—drives up incomes for both current and potential homebuyers.

Even worse, continued nominal income growth that does exist is not keeping up with price inflation. The result has been 22 months in a row of negative real wage growth, and that will translate to falling demand.

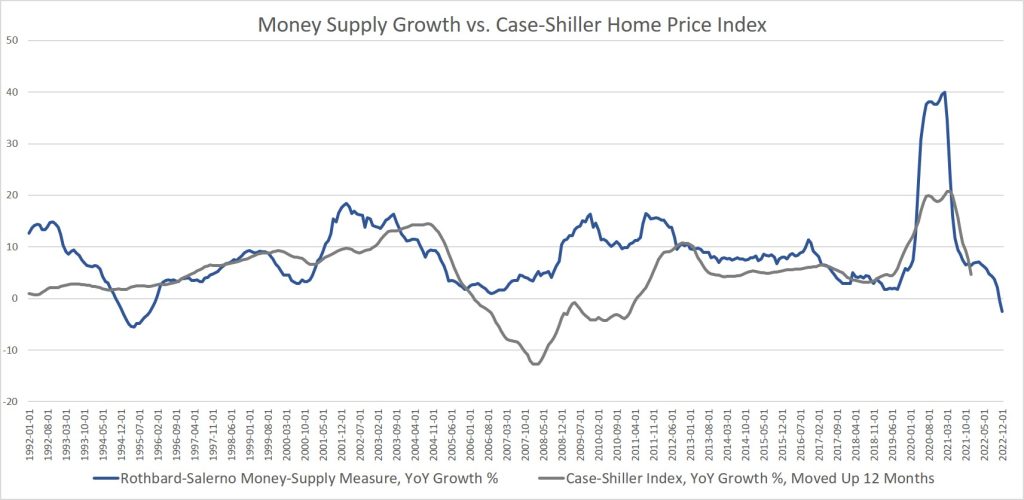

This close connection between easy money and demand for homes can be seen when we compare growth in the Case-Shiller index to growth in the money supply. This has been especially the case since 2009. As the graph shows, once money-supply growth begins to slow, a similar change occurs in home prices one year later.

As money-supply growth rapidly slowed after January 2021, we then saw a similar trend in home prices 12 months later, with a rapid deceleration in the Case-Shiller index. Remarkably, in November of last year, money-supply growth turned negative for the first time since 1994. That points toward continued drops in home prices throughout this year. If Redfin’s February numbers are any indicator, we should expect price growth to turn negative in the Case-Shiller numbers this spring.

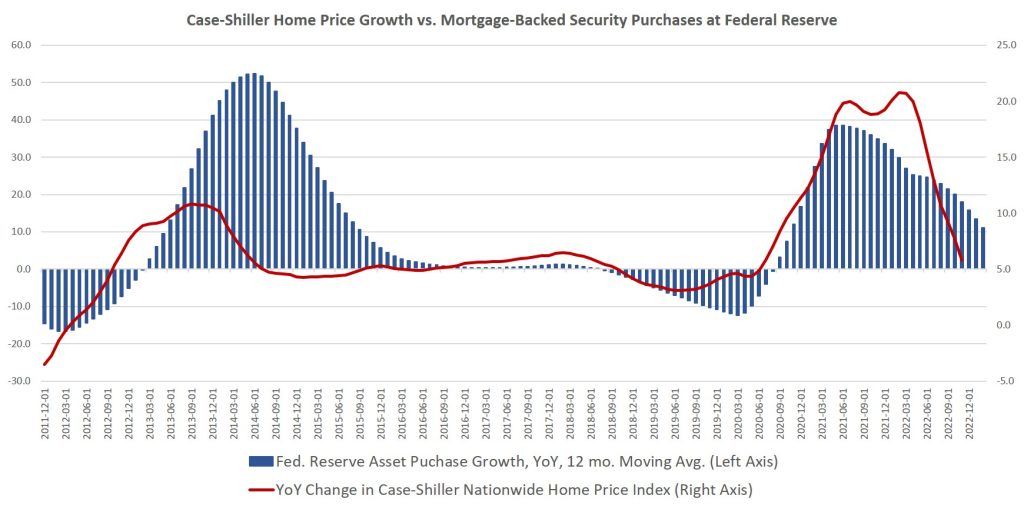

Now just imagine how much more lackluster real estate markets would be without the Fed buying up all those trillions in MBS over the past decade. It’s now been more than a decade since we had any idea what real estate prices actually would be without enormous amounts of stimulus from the Fed. The money-printing-for-mortgages scheme entered its first phase throughout 2009 and 2010, and then was almost non-stop from 2013 to 2022, topping out around $1.7 trillion in 2018. The Fed had begun to pull back on its MBS assets in 2018 and 2019, but of course reversed course in 2020 and engaged in a frenzy of new MBS buying. In that period the Fed purchased an additional $1.4 trillion in MBS. That finally ended (for now) in the fall of 2022. The Fed still holds over $2.6 trillion in MBS assets.

If we look at year-over-year changes in these MBS purchases along side Case-Shiller home prices, we again see a clear correlation:

It’s clear that once markets think the Fed may again increase its MBS purchases, home prices again surge. This close relationship should not surprise us since the volume of MBS purchases is a sizable portion of the overall market. Since 2020, the Fed’s MBS stockpile has equaled at least 20 percent of all the household mortgage debt in the United States. In early 2022, Fed-held MBS assets peaked at 24 percent of all US mortgage debt, but they still made up over 20 percent of the market as of late 2022.

Lest we think that real estate markets seem to be weathering the storm fairly well, let’s keep in mind this is all happening during a period when the unemployment rate is very low. Yes, the federal government has greatly exaggerated the amount of job growth that has occurred in the economy over the past 18 months. However, it’s also fairly clear that real estate markets are not yet seeing large numbers of unemployed workers who can’t pay their mortgages. When that does occur, we can expect an acceleration in falling home prices. For now, most mortgages are being paid, and even as real wages fall, most homeowners are cutting in places other than their mortgage payments. Once job losses do set in, all bets are off, and a wave of foreclosures will be likely. Many jobless workers won’t be able to sell quickly to avoid foreclosure either. With so few borrowers who can afford rising mortgage rates, there will be relatively few buyers. That’s when prices will really start to come down—when there is a mixture of motivated sellers and rising interest rates.

For now, though, the investor class remains relatively optimistic. Marcus Millichap CEO Hessam Nadji was on Fox Business last week flogging the now well-worn narrative that we should expect a “small recession,” but Nadji did not even entertain the idea that there might be sizable layoffs. Instead, he suggested that there is now a mere temporary softening of demand, and that will reverse itself once the Fed reverses course and embraces easy money again. In other words, the Fed will time everything perfectly, and it will be a “soft landing.”

This well captures the attitude of the “capitalists” heading the real estate industry right now. It’s all about the Fed. Without the Fed’s easy money, demand is down. Once the Fed pivots back to forcing down interest rates and buying up more MBS, well then happy times are here again. Gone is any discussion of worker productivity, savings, or other fundamentals that would drive demand in a areal capitalist market. All that matters now is a return to easy money. The real estate industry will get increasingly desperate for it. In 2023, it’s become the very foundation of their “market.”

About the Author

Ryan McMaken has a bachelors degree in economics and a master’s degree in public policy and international relations from the University of Colorado. He is the author of Breaking Away: The Case of Secession, Radical Decentralization, and Smaller Polities and Commie Cowboys: The Bourgeoisie and the Nation-State in the Western Genre. He was a housing economist for the State of Colorado. Ryan is a cohost of the Radio Rothbard podcast, has appeared on Fox News and Fox Business, and has been featured in a number of national print publications including Politico, The Hill, Bloomberg, and The Washington Post.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q22 Operating Results. CoreCivic reported revenue of $464.2 million, compared to $471.2 million in the year ago period and our estimate of $456 million. Higher expenses, related to labor costs, including hiring additional staff ahead of expected population increases, caused net income to be below our forecast. Driven by the gain on the McRae sale, reported net income was $68.3 million, or $0.58 per diluted share, versus our estimate of $72.5 million, or $0.61 per share.

La Palma Update. Ongoing expenses with the La Palma transition impacted 3Q22 but the good news is the transition should now be complete by yearend as opposed to 1Q23. With the ICE contract at La Palma expired, management believes the Company is well positioned to add additional ICE populations at its other Arizona facilities. Overall, CoreCivic is well positioned to accept additional populations, from the Federal government or state governments.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.