InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

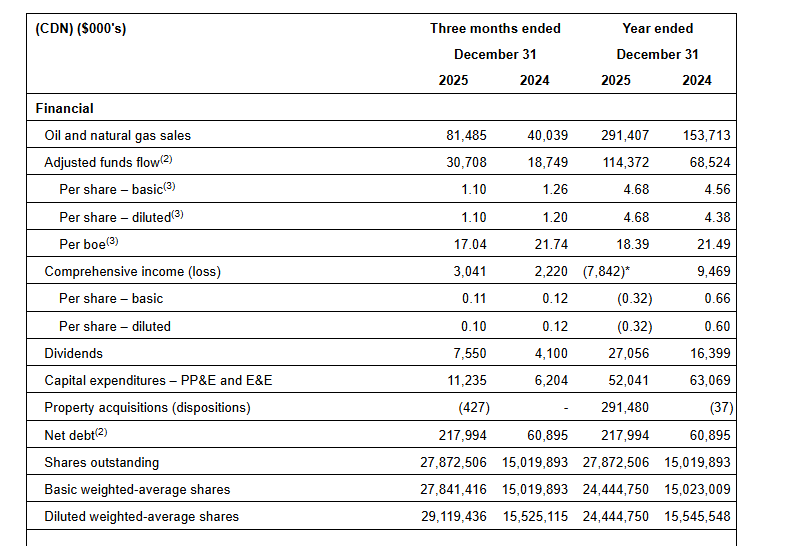

2025 financial results. InPlay Oil reported full-year 2025 adjusted funds flow (AFF) of C$114.4 million, or C$4.68 per share, above our estimate of C$112.9 million, or C$4.58 per share. Revenue for the year totaled C$291.4 million, ahead of our C$290.6 million forecast, as stronger Q4 production of 19,589 boe/d exceeded our estimate of 19,419 boe/d, in addition to stronger than expected AECO pricing. Full-year production averaged 17,043 boe/d, slightly above our 17,000 boe/d estimate.

Updated 2026 estimates. In the first quarter of 2026, we expect now revenues of C$79.9 million, AFF of C$27.4 million, and AFF per share of C$0.98, compared to prior estimates of C$79.0 million, C$26.6 million, and C$0.95, respectively. For the full-year 2026, we now estimate revenues of C$340.1 million, AFF of C$126.7 million, and AFF per share of C$4.53, up from C$340.1 million, C$125.2 million, and C$4.45. We are maintaining our production estimate of 18,605 boe/d in the first quarter and 18,900 boe/d for the year. These estimates are reflective of slightly higher commodity pricing.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, March 5, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to announce its financial and operating results for the three and twelve months ended December 31, 2025, along with the results of its independent oil and gas reserves evaluation effective December 31, 2025 (the “Reserve Report”) prepared by GLJ Ltd. (“GLJ”). InPlay’s audited annual financial statements and notes, and Management’s Discussion and Analysis (“MD&A”) for the year ended December 31, 2025 will be available at “www.sedarplus.ca” and the Company’s website at “www.inplayoil.com“. An updated corporate presentation will be available on our website in due course.

Message to Shareholders:

InPlay’s 2025 fiscal year marked a truly transformational chapter in the Company’s history, highlighted by the successful completion of the highly accretive April 2025 acquisition of Pembina assets in our core focus area. This strategic transaction significantly strengthened our already robust drilling inventory, expanded our operational scale, increased our ability to generate meaningful free adjusted funds flow (“FAFF”)(4) and enhanced the long-term sustainability and depth of our asset base.

InPlay’s long-term strategy is anchored in disciplined capital allocation, driving sustainable organic growth while pursuing strategic, accretive acquisitions; an approach supported by the Company’s proven track record of execution. InPlay has never been better positioned to advance this two-pronged growth strategy. The Company’s foundation was further strengthened in 2025 with the addition of Delek Group Ltd. (“Delek”) as a strategically aligned 32.7% shareholder. Delek has a strong history of value creation in the international energy markets with significant investments in the North Sea (Ithaca Energy plc) and the Mediterranean (NewMed Energy). Delek identified Canada as a stable and attractive jurisdiction with compelling return potential, positioning InPlay as a natural extension of its global energy investment strategy. Delek’s investment enhances InPlay’s financial strength and strategic flexibility, providing access to additional capital and alternative funding sources to support the Company’s growth strategy. Delek played a pivotal role in introducing InPlay to the Israeli capital markets and supporting the successful completion of the Company’s oversubscribed senior unsecured bond offering in February 2026. The offering was completed at an attractive cost of capital of 6.23%, further strengthening InPlay’s balance sheet and liquidity profile. InPlay looks forward to working closely with Delek to execute its long-term strategy of building a sustainable, growth-oriented Canadian oil and gas company focused on delivering top tier returns to shareholders.

During 2025, InPlay remained focused on operational execution, disciplined capital allocation and prioritizing FAFF while continuing to return capital to shareholders and pay down debt. Adjusted Funds Flow(2) (“AFF”) increased by 67% in 2025, delivering FAFF of $62 million. These results were achieved despite a 14% decline in WTI pricing, demonstrating the resilience and capital efficient nature of our light oil asset base. FAFF yield at year end was 18% (one of the highest in our peer group), dividends paid to shareholders were $27.1 million and debt repayment of $36 million post-acquisition close on April 7, 2025. The Company capitalized on its operational excellence to generate strong capital efficiencies during our 2025 capital program. Our team delivered some of the strongest-performing Cardium wells in 2025 with payouts averaging approximately seven months, underscoring the quality of our inventory and technical execution capabilities. This strong operational performance enabled us to increase production guidance over the course of the year while simultaneously reducing capital expenditures.

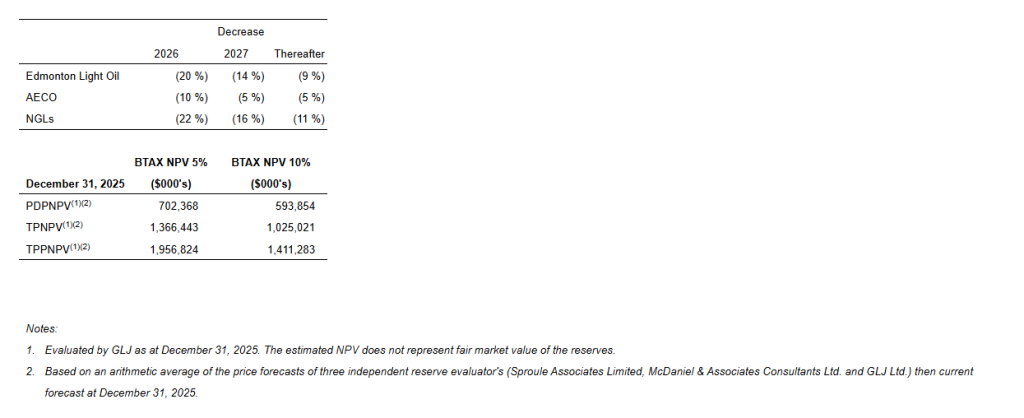

The Company’s exceptional 2025 reserve results reflect both the impact of the acquisition and strong operating results achieved during the year. Proved Developed Producing (“PDP”) reserves increased 179%, while a long reserve life index continues to underpin a low decline, high FAFF generating asset base. Despite a material year-over-year decrease in the benchmark Edmonton light oil price used in the Reserve Report (20% in 2026, 14% in 2027, 9% thereafter), the Company increased its Total Proved (“TP”) and Total Proved plus Probable (“TPP”) net asset value to $30.16/share and $44.02/share respectively, underscoring the significant intrinsic value embedded in our assets relative to current market levels.

Looking forward, InPlay is exceptionally well positioned to continue to execute key operational priorities, disciplined capital allocation and maximizing FAFF while continuing to return capital to shareholders. As announced on February 24, 2026, InPlay’s Board of Directors approved a 2026 capital budget of $66 – $74 million to drill 12 – 14 net horizontal Cardium wells. This program is forecast to result in annual average production of 18,600 – 19,200 boe/d(1) (60% – 62% light crude oil and NGLs), an 11% increase over 2025, resulting in a FAFF yield(4) of 11% – 15% (expected to be top tier amongst peers). The capital program is designed to be flexible and responsibly manage the pace of development, maintain operational and financial strength while remaining focused on delivering return of capital to shareholders.

2025 Financial and Operating Highlights:

Closed a transformational acquisition of Cardium-focused light oil assets in Pembina at highly accretive acquisition metrics (+45% AFF/share(3), +65% FAFF/share(3)), improving the Company’s sustainability through a lower decline rate, strong reserve life index and increased tier one drilling locations.

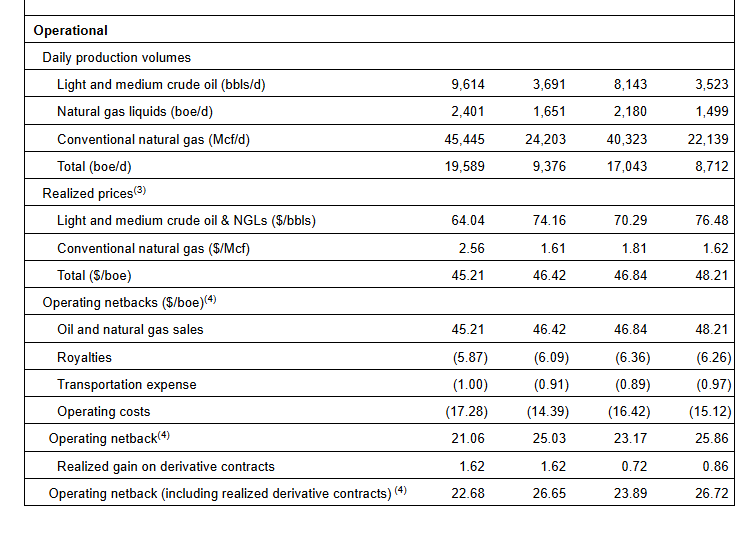

Achieved average annual production of 17,043 boe/d(1) (61% light crude oil and NGLs), a 96% increase from 2024.

Improved light oil production to 8,143 bbl/d, a 131% increase from 2024 and a 160% increase Q4 2025 over Q4 2024. Light crude oil weighting improved 20% from 2024.

Realized strong operating income of $144.1 million, a 75% increase from 2024, which resulted in an operating income profit margin(4) of 49%.

Generated AFF(2) of $114.4 million ($4.68 per weighted average basic share(3)), a 67% increase from 2024 despite a 14% decrease in WTI prices. Fourth quarter AFF totaled $30.7 million ($1.10 per weighted average basic share(3)), a 64% increase from 2024 even as WTI prices declined 16%. Fourth quarter AFF also increased 15% over Q3 2025.

Delivered FAFF of $62 million and distributed $27.1 million in dividends, equating to a 18% FAFF yield(4) and 8.7% dividend yield relative to year-end market capitalization. Since November 2022, total dividends distributed amounted to $69.7 million ($3.69 per share, including dividends declared to date in 2026).

Invested $52 million in development capital which was $1 million below the lower end of our May post-acquisition 2025 capital budget of $53 – $60 million and 17% less than 2024. Due to capital efficiencies, disciplined spending, and well outperformance, capital was 35% lower than our original capital forecast of $80 million on announcement on February 2025 to achieve production guidance.

Repaid $35 million of net debt from closing of the Pembina acquisition on April 7, 2025.

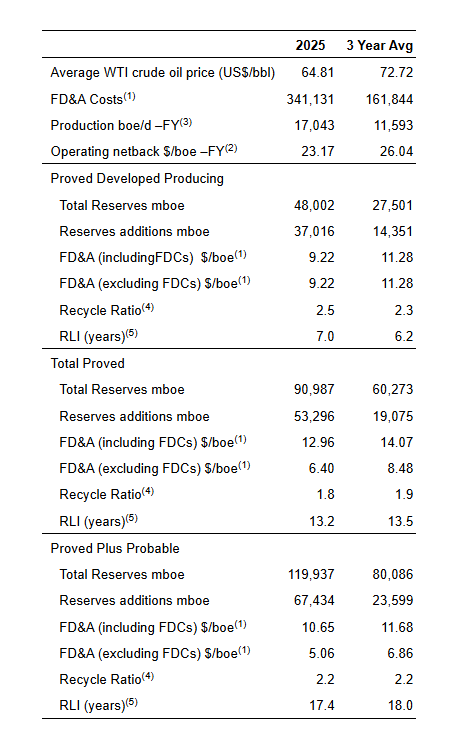

2025 Reserves Highlights(1):

InPlay’s capital efficient 2025 drilling program and accretive Pembina asset acquisition resulted in strong reserve results for 2025:

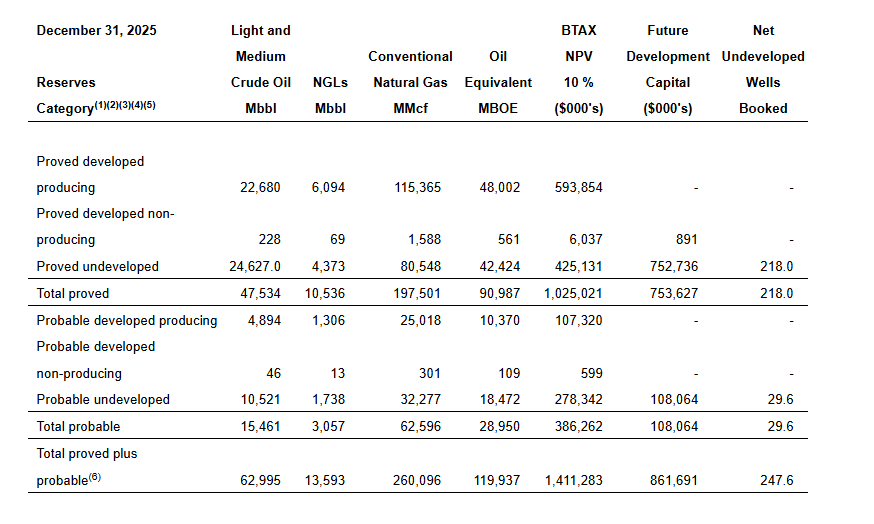

PDP reserves of 48,002 mboe (60% light and medium crude oil & NGLs), 179% increase from 2024.

TP reserves of 90,987 mboe (64% light and medium crude oil & NGLs), 107% increase from 2024.

TPP reserves of 119,937 mboe (64% light and medium crude oil & NGLs), 104% increase from 2024.

Achieved NPV BT10 reserve values(1) and Net Asset Value (“NAV”) per share of:

PDP: $594 million; $14.69/share

TP: $1,025 million; $30.16/share

TPP: $1,411 million; $44.02/share

Reserves life index (“RLI”)(2) of:

PDP: 7.0 years

TP: 13.2 years

TPP: 17.4 years

Delivered Finding, Development and Acquisition (“FD&A”) costs (including changes in future development costs) and recycle ratios(3) of:

PDP: $9.22/boe; 2.5x

TP: $12.96/boe; 1.8x

TPP: $10.65/boe; 2.2x

Replaced reserves(4) by:

PDP: 595%

TP: 857%

TPP: 1,084%

2025 development capital program (excluding acquisitions) added new light oil weighted production at a capital efficiency of $21,333 per boe/d

2026 Subsequent Event:

In February, InPlay closed an oversubscribed offering of senior unsecured bonds for total gross proceeds of C$242 million maturing on December 15, 2030 at an attractive interest rate of 6.23%. This bond is expected to reduce our cost of capital while diversifying the Company’s financing sources. Following the bond issuance, InPlay repaid and retired its term loan. The Company is now positioned with $190 million of available capacity on its fully undrawn revolving credit facility. Additionally, InPlay successfully mitigated exposure to fluctuations in the CAD/NIS exchange rate associated with the NIS-denominated senior unsecured bonds through the execution of foreign exchange hedging arrangements that fully cover all projected cash outflows, including principal repayments, over the next four years.

Financial and Operating Results:

2025 Financial & Operations Overview:

Our 2025 results are highlighted by our accretive acquisition of Pembina assets in April 2025, disciplined capital allocation and delivery of strong returns to shareholders. The acquisition was financed with an increase to our credit facilities, issuance of common shares and an oversubscribed $33.8 million bought deal equity financing.

We executed our capital program under budget, generated meaningful adjusted funds flow, returned $27.1 million to shareholders and paid down $35 million of net debt from closing of the Pembina acquisition on April 7, 2025. Production averaged 17,043 boe/d(1) (61% light crude oil & NGLs) in 2025 and 19,589 boe/d (61% light crude oil & NGLs) in the fourth quarter of 2025.

InPlay’s capital program for 2025 consisted of $52 million of exploration and development capital. Efficient operational execution in 2025 led to capital expenditures coming in $1 million below the low end of our May post-acquisition budget of $53 – $60 million and approximately 17% less than 2024 when production averaged 8,712 boe/d. The Company drilled, completed and brought on production ten (8.2 net) extended reach horizontal (“ERH”) Cardium wells during the year and completed a significant operated gas plant expansion and other facility projects. InPlay also spent $4.2 million on the successful abandonment of 31 wellbores, 90 pipelines and the reclamation of 32 well sites.

InPlay generated AFF of $114.4 million ($4.68 per basic share) during 2025 a 67% increase from 2024. These results were achieved despite a 14% decline in WTI pricing and lower than forecasted natural gas prices. Approximately $62 million in FAFF was generated resulting in a FAFF yield of 18%, evidencing our strong ability to generate meaningful FAFF.

Low crude oil prices during the year impacted the Company’s financial results with WTI decreasing 14% compared to 2024. This resulted in a 16% decrease from 2024 to our realized oil sales price, which was partially offset by realized hedging gains in the later part of the year. Significantly lower natural gas prices also impacted financial results offset with meaningful hedging gains realized throughout the year.

Operations Update:

In 2025, InPlay had one of our strongest drilling campaigns in the Company’s history. In the fourth quarter of 2025, InPlay continued its operational momentum by bringing on production five (5.0 net) operated wells. On average, the five wells delivered initial production (“IP”) rates of 429 boe/d (72% light crude oil and NGLs) per well over their first 90 days of production, approximately 66% above internal forecasts. The Company’s 2025 drilling program for the second half of 2025 continues to generate substantial returns for the Company through strong IP rates.

InPlay’s capital program for 2026 is underway with two (2.0 net) ERH wells being drilled to date which have recently come on production and are in the early cleanup stage. InPlay has also started drilling operations on a three (3.0 net) ERH well-pad which is expected to come on-line at the end of March. Approximately 7 – 9 net horizontal wells are planned for the remainder of the year, with most of the capital spend and production coming on-line from these wells in the second half of 2026.

Corporate Reserves Information:

The following summarizes certain information contained in the Reserve Report. The Reserve Report was prepared in accordance with the definitions, standards and procedures contained in the COGE Handbook and National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities (“NI 51-101”). Additional reserve information as required under NI 51-101 will be included in the Company’s Annual Information Form (“AIF”) which will be filed on SEDAR+ by the end of March 2026.

Net Present Values of Reserves:

InPlay achieved strong before tax estimated net present values (“NPV”) of future net revenues associated with our 2025 year-end reserves discounted at 10% (“NPV BT10”), although impacted by weaker future commodity prices in comparison to December 31, 2024 (refer to table below). The Company achieved NPV BT10 reserve values of $594 million (PDP), $1,025 million (TP) and $1,411 million (TPP) based on the three independent reserve evaluator average pricing, cost forecast and foreign exchange rates as at December 31, 2025 used in the Reserve Report. Commodity price decreases in the 2025 year-end reserve report compared to 2024 were as follows:

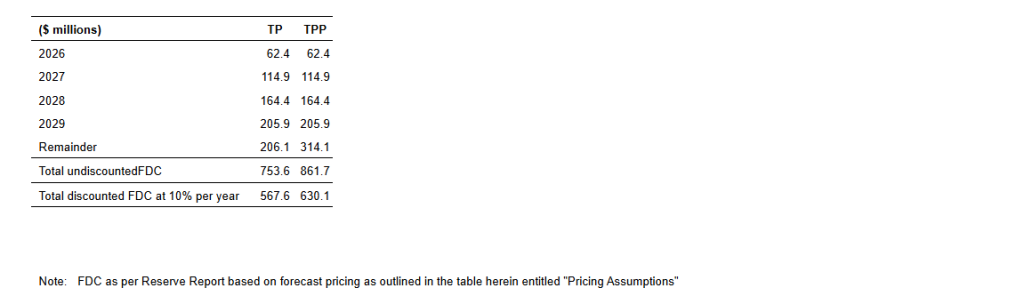

Future Development Costs (“FDCs”):

The following FDCs are included in the 2025 Reserve Report:

The $862 million of total FDC in the Total Proved and Probable Reserve Report generates approximately $710 million in future net present value discounted at 10%.

Performance Measures:

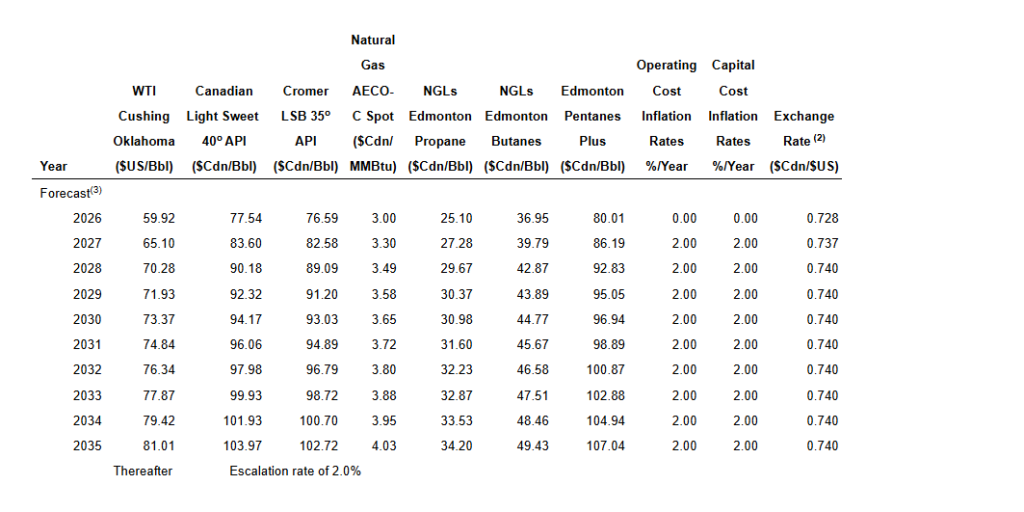

Pricing Assumptions:

The following tables set forth the benchmark reference prices, as at December 31, 2025, reflected in the Reserve Report. These price and cost assumptions were an arithmetic average of the price forecasts of three independent reserve evaluator’s (Sproule, McDaniel & Associates Consultants Ltd. and GLJ Ltd.) then current forecast and GLJ’s foreign exchange rate forecast at the effective date of the Reserve Report.

SUMMARY OF PRICING AND INFLATION RATE ASSUMPTIONS (1) as of December 31, 2025 FORECAST PRICES AND COSTS

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

Kevin Leonard Vice President Corporate & Business Development InPlay Oil Corp. Telephone: (587) 955-0635

CALGARY, AB, Feb. 26, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.09 per common share payable on March 31, 2026, to shareholders of record at the close of business on March 16, 2026. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp. InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

SOURCE InPlay Oil Corp.

For further information please contact:

Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

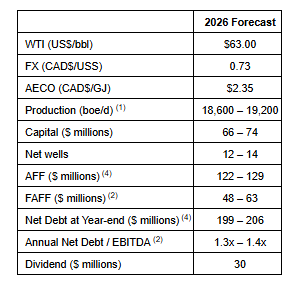

2026 guidance. InPlay approved a C$66 to C$74 million capital program targeting average production of 18,600 to 19,200 boe/d (~61% light oil and NGLs), representing approximately 11% growth over the estimated 2025 production of ~17,000 boe/d. Management forecasts adjusted funds flow (AFF) of C$122 to C$129 million and free adjusted funds flow (FAFF) of C$48 to C$63 million, implying an 11% to 15% FAFF yield. Year-end net debt is guided to C$199 to C$206 million, reflecting continued deleveraging.

Estimate revisions. We have adjusted our 2026 estimates to average production of 18,900 boe/d, revenue of C$338.3 million, and AFF of C$125.2 million, or C$4.45 per share. For Q1 2026, we have assumed production of 18,605 boe/d, revenue of C$79.0 million, and AFF of C$26.6 million, or C$0.95 per share. The first quarter carries heavier drilling activity, with five wells drilled and completed, most coming onstream late in the period, marking Q1 as the lightest production quarter of the year. We forecast 2026 capital expenditures of C$70 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY AB, Feb. 24, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) announces that its Board of Directors have approved a capital program of $66 – $74 million for 2026.

InPlay had a stellar 2025 with an accretive and transformational acquisition in our core area and a very successful drilling program. Throughout 2025, InPlay delivered improved capital efficiencies through the successful application of enhanced drilling and completion techniques, driving production results that exceeded internally modelled type curves while achieving well costs below budget. InPlay’s improved capital efficiencies allowed the Company to increase its production guidance three times during 2025 with reduced capital spending.

InPlay’s 2026 capital budget reflects a disciplined and capital efficient program focused on strong production growth, maximizing Free Adjusted Funds Flow (“FAFF”)(2) and debt reduction. The Company plans to drill 12 – 14 net horizontal Cardium wells during 2026, with the majority of capital directed toward its Cardium-focused light oil assets in Pembina. InPlay’s 2026 capital budget reflects the improved capital efficiencies realized in 2025.

Key highlights of the 2026 capital program include:

Production Growth:

Forecasted average annual production of 18,600 – 19,200 boe/d(1) (60% – 62% light oil and NGLs), an 11% increase (based on mid-point) compared to estimated 2025, driven by:

Low corporate base decline rate of 22% due to the favorable decline profile;

Strong corporate netbacks driven by high oil and liquids weighting; and

Enhanced capital efficiencies from high graded drilling inventory.

FAFF Generation and Dividend Sustainability:

AFF(2) of $122 – $129 million;

FAFF of $48 – $63 million equating to a 11% – 15% FAFF Yield(3). FAFF exceeds the base annual dividend of $30 million (based on the current monthly dividend rate of $0.09/share or $1.08/share annualized) insulating the Company in the event of commodity price fluctuations.

InPlay’s dividend represents a dividend yield of approximately 7.0% at the current share price.

Debt Reduction:

Excess FAFF(3) is planned to be used to reduce debt;

Year-end Net Debt(2) of $199 – $206 million.

InPlay currently has forecasted commodity pricing similar to peers who have previously released 2026 guidance. To mitigate downside risk, InPlay has implemented a comprehensive hedging program providing protection against current market volatility. Details of the Company’s current hedges are provided in the “Hedging Summary” section of the Reader Advisories.

The table below outlines InPlay’s 2026 guidance:

In the first quarter of 2026, the Company plans to have its most active capital spend quarter of the year with five (5.0 net) horizontal wells being drilled. To date, InPlay has drilled and recently completed a two (2.0 net) ERH well-pad which have recently come on production. InPlay has also started drilling operations on a three (3.0 net) ERH well-pad which is expected to come on-line at the end of March. The majority of the capital spend on the remaining 7 – 9 net horizontal wells planned for the year is expected to occur in the second half of 2026.

InPlay continues to closely monitor global trade, geopolitical and commodity dynamics, proactively evaluating capital plans in response to pricing volatility, inflationary cost pressures, and other factors affecting the business. The Company will remain flexible and make decisions based on our core strategy of disciplined capital allocation, maintaining financial strength to ensure the long term sustainability of our strategy and return to shareholder program. Should commodity prices improve and stabilize, the Company will remain disciplined and flexible, with the ability to swiftly adjust its capital activity to align with evolving market conditions.

2025 Update

The Company is finalizing its results for 2025 and expects to achieve production of approximately 17,000 boe/d(1) (61% light crude oil and liquids) in line with the mid-point of our last forecast of 16,900 – 17,100 boe/d and 600 boe/d ahead of the mid-point of our original post acquisition forecast of 16,000 – 16,800 boe/d. In comparison to average production of 8,712 boe/d in 2024, production increased by approximately 95% in 2025.

Looking ahead after a transformation year with efficient capital spending, we remain focused on continued profitable development of our high-return asset base and are committed to delivering strong returns to shareholders through 2026 and beyond. On behalf of the management team and Board of Directors, we extend our gratitude to our employees, shareholders and bondholders for their support of the Company and the Canadian oil and gas industry.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q4 2025 Estimate Revisions. We are adjusting Q4 estimates to reflect softer commodity pricing, with WTI averaging $59.10 per barrel versus our prior $60.00 estimate and wider differentials reducing realized Canadian pricing. We are lowering our revenue, adjusted funds flow (AFF), and AFF per share estimates to C$80.7 million, C$29.1 million, and C$1.04, respectively, from C$88.8 million, C$35.8 million, and C$1.28. Our production estimate remains unchanged at 19,419 boe/d.

FY 2025 Estimate Revisions. We are modestly lowering our full-year revenue, AFF, and AFF per share estimates to reflect lower fourth-quarter estimates. We now forecast revenue of C$290.6 million, AFF of C$112.9 million, and AFF per share of C$4.58, down from C$298.7 million, C$119.5 million, and C$4.85, respectively. Our outlook continues to assume average 2025 production of approximately 17,000 boe/d. We will update our 2026 estimates following the release of InPlay’s 2026 guidance.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, Feb. 11, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) is pleased to announce that it has completed its previously announced offering of 550 million New Israeli Shekels (“NIS“) (CAD$242 million) principal amount of senior unsecured bonds (the “Bonds“) in Israel (the “Offering“). The Bonds bear interest at a rate of 6.23% per annum and are due December 15, 2030.

InPlay is also pleased to announce that it has completed the listing of its common shares (“Common Shares“) and the Bonds on the Tel Aviv Stock Exchange (“TASE“). The Common Shares and the Bonds are expected to commence trading on the TASE on February 11, 2026 under the symbols IPO and IPO.B1, respectively.

InPlay intends to use the net proceeds from the Offering to repay the amount owing under the Company’s $110 million two-year amortizing term loan (CAD$93.0 million as at December 31, 2025), temporarily reduce, on a non permanent basis, amounts drawn under the Company’s approximately $190 million revolving credit facility (CAD$129.1 million as at December 31, 2025), to pay transaction expenses and/or for general corporate purposes.

The Bonds are denominated in NIS and interest will be payable semi-annually. In addition, three amortization payments of 6% of the principal amount of the Bonds will be due on December 15th of 2027, 2028 and 2029. Payment of principal and interest will not be linked to CAD. InPlay may, subject to certain conditions, at any time no earlier than sixty (60) days after the Bonds are listed on the TASE and at its sole discretion, redeem the Bonds in a full or partial early redemption. InPlay intends to be proactive in hedging its exposure to fluctuations in the CAD to NIS exchange rate.

This press release does not constitute an offer to sell, or a solicitation of an offer to buy, any security and shall not constitute an offer, solicitation or sale in any jurisdiction in which such an offer, solicitation, or sale would be unlawful.

This press release is not an offer of securities of the Company for sale in the United States or Canada. The Bonds have not and will not be registered under the U.S. Securities Act of 1933, as amended, nor qualified for distribution in Canada. The Bonds may not be offered or sold to a resident of Canada or for the benefit of a resident of Canada nor may they be sold in the United States except as pursuant to an applicable exemption from its registration requirements. No public offering of securities is being made in the United States or Canada.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands. The Common Shares trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

Kevin Leonard Vice President Corporate & Business Development InPlay Oil Corp. Telephone: (587) 955-0634

CURRENCY

NIS refers to New Israeli Shekels and CAD refers to Canadian Dollars. In this press release, unless otherwise explicitly written, the conversion of NIS to CAD is based on the base rate of NIS 2.27 for CAD$1.00.

FORWARD LOOKING STATEMENTS

This document contains certain forward–looking information and statements within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”, “may”, “will”, “project”, “should”, “believe”, “plans”, “intends”, “forecast” and similar expressions are intended to identify forward-looking information or statements. In particular, but without limiting the foregoing, this document contains forward-looking information and statements pertaining to the following: the Company’s business strategy, milestones and objectives; the intended use of proceeds of the Offering; the impact of the Offering on the Company; and InPlay’s expectations regarding managing its currency exposure.

Forward-looking statements or information are based on a number of material factors, expectations or assumptions of InPlay which have been used to develop such statements and information, but which may prove to be incorrect. Although InPlay believes that the expectations reflected in such forward-looking statements or information are reasonable, undue reliance should not be placed on forward-looking statements because InPlay can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: InPlay’s ability to manage currency exposure; the current U.S. economic, regulatory and/or trade policies; the impact of increasing competition; the general stability of the economic and political environment in which InPlay operates; the timely receipt of any required regulatory approvals; the ability of InPlay to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which InPlay has an interest in to operate the field in a safe, efficient and effective manner; the ongoing impact of the Russia/Ukraine conflict and war in the Middle East; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which InPlay operates; and the ability of InPlay to successfully market its oil and natural gas products. The forward-looking information and statements included herein are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward-looking information or statements including, without limitation: changes in industry regulations and legislation (including, but not limited to, tax laws, royalties, and environmental regulations); changes in industry regulations and legislation (including, but not limited to, tax laws, royalties, and environmental regulations); that (i) the tariffs that are currently in effect on goods exported from or imported into Canada continue in effect for an extended period of time, the tariffs that have been threatened are implemented, that tariffs that are currently suspended are reactivated, the rate or scope of tariffs are increased, or new tariffs are imposed, including on oil and natural gas, (ii) the U.S. and/or Canada imposes any other form of tax, restriction or prohibition on the import or export of products from one country to the other, including on oil and natural gas, and (iii) the tariffs imposed or threatened to be imposed by the U.S. on other countries and retaliatory tariffs imposed or threatened to be imposed by other countries on the U.S., will trigger a broader global trade war which could have a material adverse effect on the Canadian, U.S. and global economies, and by extension the Canadian oil and natural gas industry and the Company, including by decreasing demand for (and the price of) oil and natural gas, disrupting supply chains, increasing costs, causing volatility in global financial markets, and limiting access to financing; the continuing impact of the Russia/Ukraine conflict and war in the Middle East; potential changes to U.S. economic, regulatory and/or trade policies as a result of a change in government; inflation and the risk of a global recession; changes in our planned capital program; changes in our approach to shareholder returns; changes in commodity prices and other assumptions outlined herein; the potential for variation in the quality of the reservoirs in which InPlay operates; changes in the demand for or supply of InPlay’s products; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans or strategies of InPlay or by third party operators of InPlay’s properties; changes in InPlay’s credit structure, increased debt levels or debt service requirements; inaccurate estimation of InPlay’s light crude oil and natural gas reserve and resource volumes; limited, unfavorable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time-to-time in InPlay’s continuous disclosure documents filed on SEDAR+ including InPlay’s Annual Information Form dated March 31, 2025 and the annual management’s discussion & analysis for the year ended December 31, 2024.

The forward-looking statements contained in this document speak only as of the date hereof and InPlay does not assume any obligation to publicly update or revise any of the included forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

READER ADVISORY

NO SECURITIES REGULATORY AUTHORITY HAS EXPRESSED AN OPINION ABOUT THE BONDS AND IT IS AN OFFENCE TO CLAIM OTHERWISE. THE OFFERING CONSTITUTES A PUBLIC OFFERING FOR INVESTORS OF THE BONDS ONLY IN THOSE JURISDICTIONS WHERE THEY MAY LAWFULLY BE OFFERED FOR SALE AND THEREIN ONLY BY PERSONS PERMITTED TO SELL SUCH BONDS. THE BONDS HAVE NOT BEEN, AND WILL NOT BE, QUALIFIED FOR DISTRIBUTION IN ANY JURISDICTION OF CANADA AND MAY NOT BE OFFERED, SOLD, OR DELIVERED DIRECTLY OR INDIRECTLY IN ANY JURISDICTION OF CANADA OR TO RESIDENTS OF CANADA.

NO ADVERTISEMENT, SOLICITATION OR NEGOTIATION DIRECTLY OR INDIRECTLY IN FURTHERANCE OF ANY SALES OF THE BONDS DESCRIBED IN THIS PRESS RELEASE HAS OCCURRED OR WILL OCCUR IN CANADA. BY PURCHASING THE BONDS, EACH PURCHASER REPRESENTS AND WARRANTS TO THE COMPANY THAT SUCH PURCHASER IS NOT A RESIDENT OF CANADA AND THAT SUCH PURCHASER DOES NOT HAVE ANY INTENTION TO DISTRIBUTE SUCH BONDS IN CANADA OR HOLD SUCH BONDS FOR THE BENEFIT OF RESIDENTS OF CANADA.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Bond offering details. InPlay announced a senior unsecured bond issuance in Israel for up to 550 million New Israeli Shekels (NIS), or approximately C$241 million. Three amortization payments of 6% of the principal amount of the bonds will be due on December 15 of 2027, 2028, and 2029, and the fourth and last amortization payment of the remaining 82% will be due on December 15, 2030. The offering is expected to close on or around February 12, 2026, subject to certain conditions.

Expanding capital market access. Beyond the financing itself, we view the transaction as a strategic expansion of InPlay’s funding base outside of Canada. InPlay received interest from over 40 institutional investors in the oversubscribed offering and, to date, has accepted tenders for NIS 550 million of the bonds. The transaction further strengthens InPlay’s diversified financing sources while reducing its overall cost of capital.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, Feb. 2, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.09 per common share payable on February 27, 2026, to shareholders of record at the close of business on February 13, 2026. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

CALGARY AB, Jan. 2, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.09 per common share payable on January 30, 2026, to shareholders of record at the close of business on January 15, 2026. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

CALGARY, AB, Dec. 1, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.09 per common share payable on December 31, 2025, to shareholders of record at the close of business on December 15, 2025. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

CALGARY, AB, Nov. 3, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.09 per common share payable on November 28, 2025, to shareholders of record at the close of business on November 14, 2025. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

SOURCE InPlay Oil Corp.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632, www.inplayoil.com; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating third quarter 2025 estimates. While we are maintaining our third-quarter production forecast of 18,695 barrels of oil equivalent per day (boe/d), we lowered our third-quarter 2025 revenue, adjusted funds flow (AFF), and AFF per share estimates to C$86.8 million, C$28.0 million, and C$1.00, respectively, from C$89.3 million, C$38.9 million, and C$1.39. These changes reflect modestly lower commodity pricing, along with higher royalty costs and operating expenses. We expect third-quarter operating expenses to be elevated due to turnaround activity and downtime associated with the recently completed gas plant expansion.

Revising full-year 2025 estimates. For the full year 2025, we forecast revenue of C$301.9 million, AFF of C$116.3 million, and AFF per share of C$4.71, compared to prior estimates of C$306.7 million, C$131.8 million, and C$5.34. These reductions primarily reflect a weaker pricing environment, partially offset by a modest increase in our full-year production forecast to 16,851 boe/d from 16,800, driven by higher fourth quarter production expectations.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

")

")

")

")

")