")

Research News and Market Data on IPOOF

Mar 05, 2026, 07:30 ET

CALGARY, AB, March 5, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to announce its financial and operating results for the three and twelve months ended December 31, 2025, along with the results of its independent oil and gas reserves evaluation effective December 31, 2025 (the “Reserve Report”) prepared by GLJ Ltd. (“GLJ”). InPlay’s audited annual financial statements and notes, and Management’s Discussion and Analysis (“MD&A”) for the year ended December 31, 2025 will be available at “www.sedarplus.ca” and the Company’s website at “www.inplayoil.com“. An updated corporate presentation will be available on our website in due course.

Message to Shareholders:

InPlay’s 2025 fiscal year marked a truly transformational chapter in the Company’s history, highlighted by the successful completion of the highly accretive April 2025 acquisition of Pembina assets in our core focus area. This strategic transaction significantly strengthened our already robust drilling inventory, expanded our operational scale, increased our ability to generate meaningful free adjusted funds flow (“FAFF”)(4) and enhanced the long-term sustainability and depth of our asset base.

InPlay’s long-term strategy is anchored in disciplined capital allocation, driving sustainable organic growth while pursuing strategic, accretive acquisitions; an approach supported by the Company’s proven track record of execution. InPlay has never been better positioned to advance this two-pronged growth strategy. The Company’s foundation was further strengthened in 2025 with the addition of Delek Group Ltd. (“Delek”) as a strategically aligned 32.7% shareholder. Delek has a strong history of value creation in the international energy markets with significant investments in the North Sea (Ithaca Energy plc) and the Mediterranean (NewMed Energy). Delek identified Canada as a stable and attractive jurisdiction with compelling return potential, positioning InPlay as a natural extension of its global energy investment strategy. Delek’s investment enhances InPlay’s financial strength and strategic flexibility, providing access to additional capital and alternative funding sources to support the Company’s growth strategy. Delek played a pivotal role in introducing InPlay to the Israeli capital markets and supporting the successful completion of the Company’s oversubscribed senior unsecured bond offering in February 2026. The offering was completed at an attractive cost of capital of 6.23%, further strengthening InPlay’s balance sheet and liquidity profile. InPlay looks forward to working closely with Delek to execute its long-term strategy of building a sustainable, growth-oriented Canadian oil and gas company focused on delivering top tier returns to shareholders.

During 2025, InPlay remained focused on operational execution, disciplined capital allocation and prioritizing FAFF while continuing to return capital to shareholders and pay down debt. Adjusted Funds Flow(2) (“AFF”) increased by 67% in 2025, delivering FAFF of $62 million. These results were achieved despite a 14% decline in WTI pricing, demonstrating the resilience and capital efficient nature of our light oil asset base. FAFF yield at year end was 18% (one of the highest in our peer group), dividends paid to shareholders were $27.1 million and debt repayment of $36 million post-acquisition close on April 7, 2025. The Company capitalized on its operational excellence to generate strong capital efficiencies during our 2025 capital program. Our team delivered some of the strongest-performing Cardium wells in 2025 with payouts averaging approximately seven months, underscoring the quality of our inventory and technical execution capabilities. This strong operational performance enabled us to increase production guidance over the course of the year while simultaneously reducing capital expenditures.

The Company’s exceptional 2025 reserve results reflect both the impact of the acquisition and strong operating results achieved during the year. Proved Developed Producing (“PDP”) reserves increased 179%, while a long reserve life index continues to underpin a low decline, high FAFF generating asset base. Despite a material year-over-year decrease in the benchmark Edmonton light oil price used in the Reserve Report (20% in 2026, 14% in 2027, 9% thereafter), the Company increased its Total Proved (“TP”) and Total Proved plus Probable (“TPP”) net asset value to $30.16/share and $44.02/share respectively, underscoring the significant intrinsic value embedded in our assets relative to current market levels.

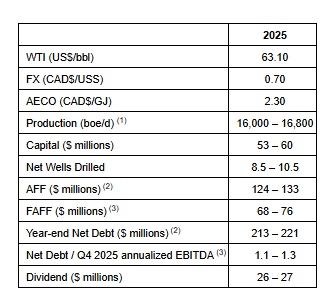

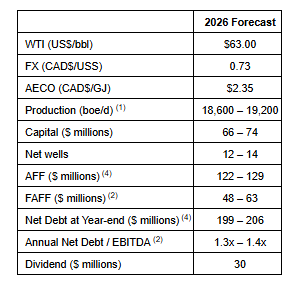

Looking forward, InPlay is exceptionally well positioned to continue to execute key operational priorities, disciplined capital allocation and maximizing FAFF while continuing to return capital to shareholders. As announced on February 24, 2026, InPlay’s Board of Directors approved a 2026 capital budget of $66 – $74 million to drill 12 – 14 net horizontal Cardium wells. This program is forecast to result in annual average production of 18,600 – 19,200 boe/d(1) (60% – 62% light crude oil and NGLs), an 11% increase over 2025, resulting in a FAFF yield(4) of 11% – 15% (expected to be top tier amongst peers). The capital program is designed to be flexible and responsibly manage the pace of development, maintain operational and financial strength while remaining focused on delivering return of capital to shareholders.

2025 Financial and Operating Highlights:

- Closed a transformational acquisition of Cardium-focused light oil assets in Pembina at highly accretive acquisition metrics (+45% AFF/share(3), +65% FAFF/share(3)), improving the Company’s sustainability through a lower decline rate, strong reserve life index and increased tier one drilling locations.

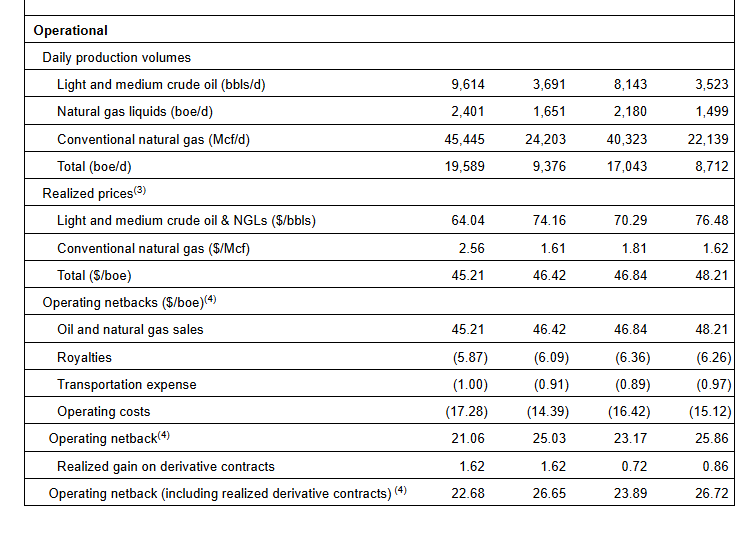

- Achieved average annual production of 17,043 boe/d(1) (61% light crude oil and NGLs), a 96% increase from 2024.

- Improved light oil production to 8,143 bbl/d, a 131% increase from 2024 and a 160% increase Q4 2025 over Q4 2024. Light crude oil weighting improved 20% from 2024.

- Realized strong operating income of $144.1 million, a 75% increase from 2024, which resulted in an operating income profit margin(4) of 49%.

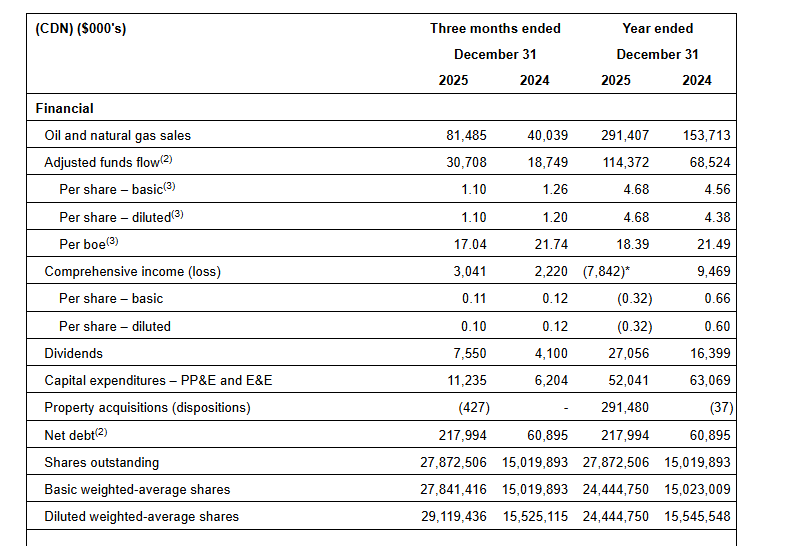

- Generated AFF(2) of $114.4 million ($4.68 per weighted average basic share(3)), a 67% increase from 2024 despite a 14% decrease in WTI prices. Fourth quarter AFF totaled $30.7 million ($1.10 per weighted average basic share(3)), a 64% increase from 2024 even as WTI prices declined 16%. Fourth quarter AFF also increased 15% over Q3 2025.

- Delivered FAFF of $62 million and distributed $27.1 million in dividends, equating to a 18% FAFF yield(4) and 8.7% dividend yield relative to year-end market capitalization. Since November 2022, total dividends distributed amounted to $69.7 million ($3.69 per share, including dividends declared to date in 2026).

- Invested $52 million in development capital which was $1 million below the lower end of our May post-acquisition 2025 capital budget of $53 – $60 million and 17% less than 2024. Due to capital efficiencies, disciplined spending, and well outperformance, capital was 35% lower than our original capital forecast of $80 million on announcement on February 2025 to achieve production guidance.

- Repaid $35 million of net debt from closing of the Pembina acquisition on April 7, 2025.

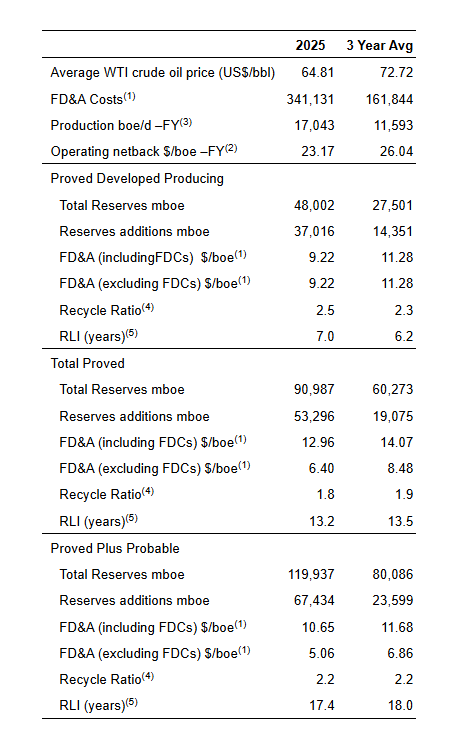

2025 Reserves Highlights(1):

- InPlay’s capital efficient 2025 drilling program and accretive Pembina asset acquisition resulted in strong reserve results for 2025:

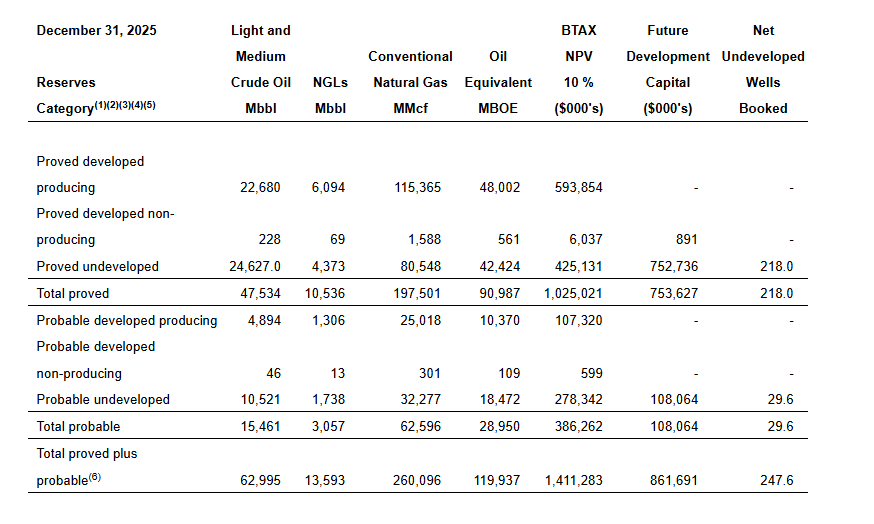

- PDP reserves of 48,002 mboe (60% light and medium crude oil & NGLs), 179% increase from 2024.

- TP reserves of 90,987 mboe (64% light and medium crude oil & NGLs), 107% increase from 2024.

- TPP reserves of 119,937 mboe (64% light and medium crude oil & NGLs), 104% increase from 2024.

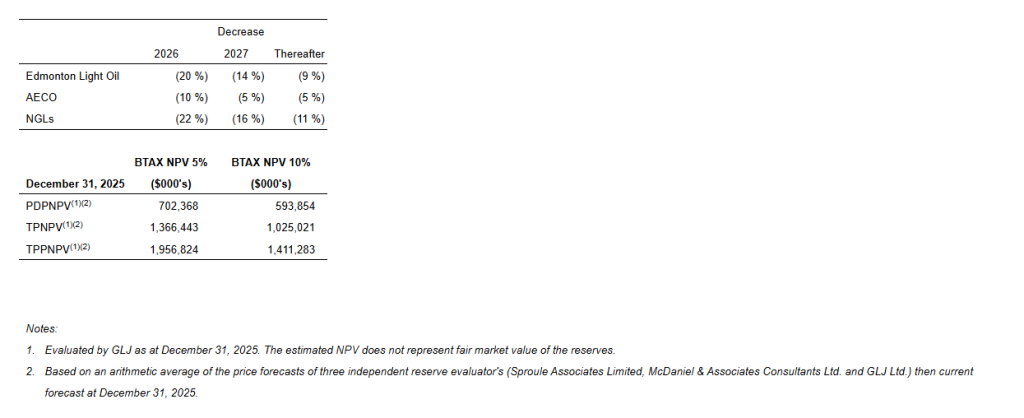

- Achieved NPV BT10 reserve values(1) and Net Asset Value (“NAV”) per share of:

- PDP: $594 million; $14.69/share

- TP: $1,025 million; $30.16/share

- TPP: $1,411 million; $44.02/share

- Reserves life index (“RLI”)(2) of:

- PDP: 7.0 years

- TP: 13.2 years

- TPP: 17.4 years

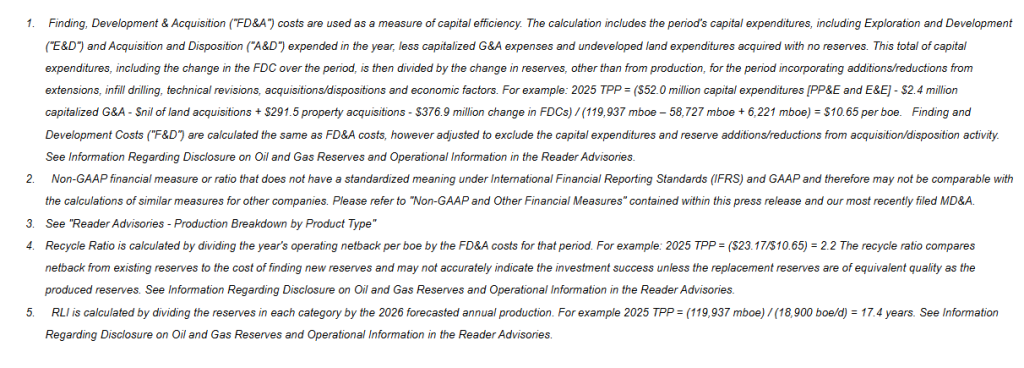

- Delivered Finding, Development and Acquisition (“FD&A”) costs (including changes in future development costs) and recycle ratios(3) of:

- PDP: $9.22/boe; 2.5x

- TP: $12.96/boe; 1.8x

- TPP: $10.65/boe; 2.2x

- Replaced reserves(4) by:

- PDP: 595%

- TP: 857%

- TPP: 1,084%

- 2025 development capital program (excluding acquisitions) added new light oil weighted production at a capital efficiency of $21,333 per boe/d

2026 Subsequent Event:

In February, InPlay closed an oversubscribed offering of senior unsecured bonds for total gross proceeds of C$242 million maturing on December 15, 2030 at an attractive interest rate of 6.23%. This bond is expected to reduce our cost of capital while diversifying the Company’s financing sources. Following the bond issuance, InPlay repaid and retired its term loan. The Company is now positioned with $190 million of available capacity on its fully undrawn revolving credit facility. Additionally, InPlay successfully mitigated exposure to fluctuations in the CAD/NIS exchange rate associated with the NIS-denominated senior unsecured bonds through the execution of foreign exchange hedging arrangements that fully cover all projected cash outflows, including principal repayments, over the next four years.

Financial and Operating Results:

2025 Financial & Operations Overview:

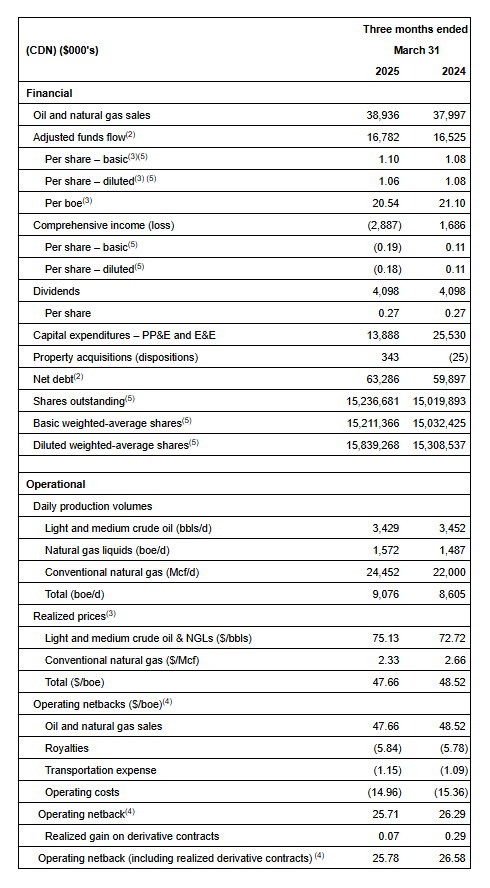

Our 2025 results are highlighted by our accretive acquisition of Pembina assets in April 2025, disciplined capital allocation and delivery of strong returns to shareholders. The acquisition was financed with an increase to our credit facilities, issuance of common shares and an oversubscribed $33.8 million bought deal equity financing.

We executed our capital program under budget, generated meaningful adjusted funds flow, returned $27.1 million to shareholders and paid down $35 million of net debt from closing of the Pembina acquisition on April 7, 2025. Production averaged 17,043 boe/d(1) (61% light crude oil & NGLs) in 2025 and 19,589 boe/d (61% light crude oil & NGLs) in the fourth quarter of 2025.

InPlay’s capital program for 2025 consisted of $52 million of exploration and development capital. Efficient operational execution in 2025 led to capital expenditures coming in $1 million below the low end of our May post-acquisition budget of $53 – $60 million and approximately 17% less than 2024 when production averaged 8,712 boe/d. The Company drilled, completed and brought on production ten (8.2 net) extended reach horizontal (“ERH”) Cardium wells during the year and completed a significant operated gas plant expansion and other facility projects. InPlay also spent $4.2 million on the successful abandonment of 31 wellbores, 90 pipelines and the reclamation of 32 well sites.

InPlay generated AFF of $114.4 million ($4.68 per basic share) during 2025 a 67% increase from 2024. These results were achieved despite a 14% decline in WTI pricing and lower than forecasted natural gas prices. Approximately $62 million in FAFF was generated resulting in a FAFF yield of 18%, evidencing our strong ability to generate meaningful FAFF.

Low crude oil prices during the year impacted the Company’s financial results with WTI decreasing 14% compared to 2024. This resulted in a 16% decrease from 2024 to our realized oil sales price, which was partially offset by realized hedging gains in the later part of the year. Significantly lower natural gas prices also impacted financial results offset with meaningful hedging gains realized throughout the year.

Operations Update:

In 2025, InPlay had one of our strongest drilling campaigns in the Company’s history. In the fourth quarter of 2025, InPlay continued its operational momentum by bringing on production five (5.0 net) operated wells. On average, the five wells delivered initial production (“IP”) rates of 429 boe/d (72% light crude oil and NGLs) per well over their first 90 days of production, approximately 66% above internal forecasts. The Company’s 2025 drilling program for the second half of 2025 continues to generate substantial returns for the Company through strong IP rates.

InPlay’s capital program for 2026 is underway with two (2.0 net) ERH wells being drilled to date which have recently come on production and are in the early cleanup stage. InPlay has also started drilling operations on a three (3.0 net) ERH well-pad which is expected to come on-line at the end of March. Approximately 7 – 9 net horizontal wells are planned for the remainder of the year, with most of the capital spend and production coming on-line from these wells in the second half of 2026.

Corporate Reserves Information:

The following summarizes certain information contained in the Reserve Report. The Reserve Report was prepared in accordance with the definitions, standards and procedures contained in the COGE Handbook and National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities (“NI 51-101”). Additional reserve information as required under NI 51-101 will be included in the Company’s Annual Information Form (“AIF”) which will be filed on SEDAR+ by the end of March 2026.

Net Present Values of Reserves:

InPlay achieved strong before tax estimated net present values (“NPV”) of future net revenues associated with our 2025 year-end reserves discounted at 10% (“NPV BT10”), although impacted by weaker future commodity prices in comparison to December 31, 2024 (refer to table below). The Company achieved NPV BT10 reserve values of $594 million (PDP), $1,025 million (TP) and $1,411 million (TPP) based on the three independent reserve evaluator average pricing, cost forecast and foreign exchange rates as at December 31, 2025 used in the Reserve Report. Commodity price decreases in the 2025 year-end reserve report compared to 2024 were as follows:

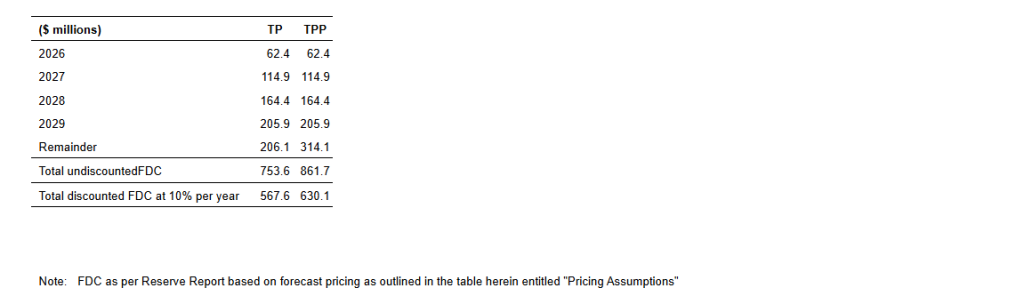

Future Development Costs (“FDCs”):

The following FDCs are included in the 2025 Reserve Report:

The $862 million of total FDC in the Total Proved and Probable Reserve Report generates approximately $710 million in future net present value discounted at 10%.

Performance Measures:

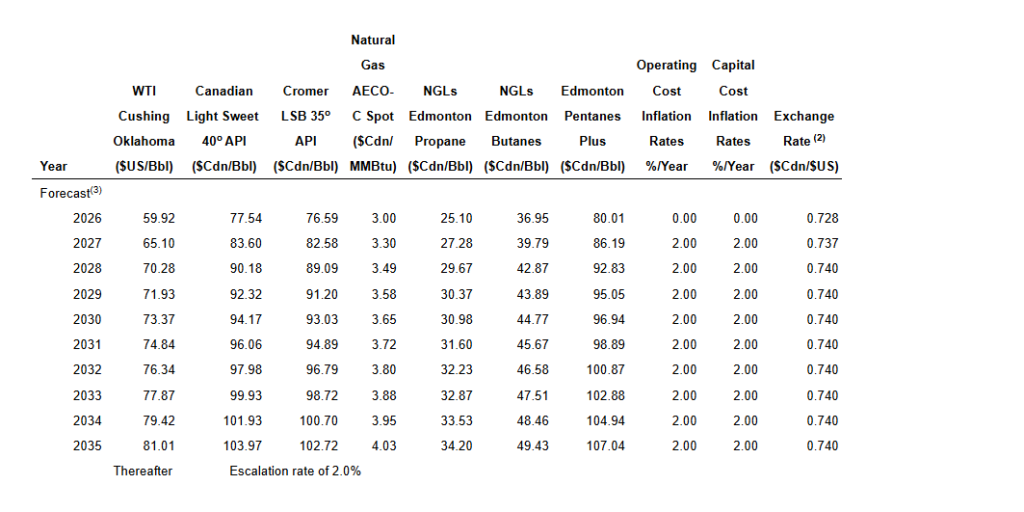

Pricing Assumptions:

The following tables set forth the benchmark reference prices, as at December 31, 2025, reflected in the Reserve Report. These price and cost assumptions were an arithmetic average of the price forecasts of three independent reserve evaluator’s (Sproule, McDaniel & Associates Consultants Ltd. and GLJ Ltd.) then current forecast and GLJ’s foreign exchange rate forecast at the effective date of the Reserve Report.

SUMMARY OF PRICING AND INFLATION RATE ASSUMPTIONS (1)

as of December 31, 2025

FORECAST PRICES AND COSTS

For further information please contact:

| Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632 | Kevin Leonard Vice President Corporate & Business Development InPlay Oil Corp. Telephone: (587) 955-0635 |

")

")

")

")

")

")

")

")

")