HOUSTON, Nov. 26, 2024 (GLOBE NEWSWIRE) — Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) (NASDAQ: GLDD), the largest provider of dredging services in the United States, announced today that its President and Chief Executive Officer, Lasse Petterson, and Senior Vice President and Chief Financial Officer, Scott Kornblau, will present at NobleCon20 – Noble Capital Markets’ Twentieth Annual Emerging Growth Equity Conference at Florida Atlantic University, Executive Education Complex, in Boca Raton, Florida on Tuesday, December 3, 2024, at 10:30 AM Eastern Standard Time.

A high-definition video webcast of the presentation will be available the following day on the Company’s website https://investor.gldd.com/investor-relations and as part of a complete catalog of presentations available at Noble Capital Markets’ Conference website: www.nobleconference.com and on Channelchek www.channelchek.com the investor portal created by Noble. The webcast will be archived on the company’s website, the NobleCon website, and on Channelchek.com for 90 days following the event.

The Company Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 134-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

About Noble Capital Markets, Inc. Established in 1984, Noble Capital Markets is an SEC / FINRA registered full-service investment bank and advisory firm with an award-winning research team and proprietary investor distribution platform. We deliver middle market expertise to entrepreneurs, corporations, financial sponsors, and investors. Over the past 40 years, Noble has raised billions of dollars for companies and published more than 45,000 equity research reports. Noble launched www.channelchek.com in 2018 – an investor community dedicated exclusively to public emerging growth and their industries. Channelchek is the first service to offer institutional-quality research to the public, for FREE at every level without a subscription. More than 7,000 public emerging growth companies are listed on the site, and content including equity research, webcasts, and industry articles.

Cautionary Note Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking” statements as defined in Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), the Private Securities Litigation Reform Act of 1995 (the “PSLRA”) or in releases made by the Securities and Exchange Commission (the “SEC”), all as may be amended from time to time. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of Great Lakes and its subsidiaries, or industry results, to differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements. Statements that are not historical fact are forward-looking statements. These cautionary statements are being made pursuant to the Exchange Act and the PSLRA with the intention of obtaining the benefits of the “safe harbor” provisions of such laws. Great Lakes cautions investors that any forward-looking statements made by Great Lakes are not guarantees or indicative of future events.

Although Great Lakes believes that its plans, intentions and expectations reflected in this press release are reasonable, actual events could differ materially. The forward-looking statements contained in this press release are made only as of the date hereof and Great Lakes does not have or undertake any obligation to update or revise any forward-looking statements whether as a result of new information, subsequent events or otherwise, unless otherwise required by law.

For further information contact: Tina Baginskis Director, Investor Relations 630-574-3024

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or “the Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy and process industries, today announced that Christopher J. Thome, Vice President – Finance and Chief Financial Officer, and Matt Malone, Vice President of Graham Corporation and General Manager of Barber-Nichols, will present and host investor meetings at the Noble Capital Markets Emerging Growth Equity Conference at the Florida Atlantic University in Boca Raton on Wednesday, December 4, 2024.

The Company presentation is scheduled to begin at 10:30 a.m. Eastern Time. A high-definition video webcast of the presentation will be available the following day at GHM Investor Relations, and as part of a complete catalog of presentations available at Noble Capital Markets’ Conference website and on Channelchek the investor portal created by Noble. The webcast will be archived on the company’s website, the NobleCon website, and on Channelchek.com for 90 days following the event.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy, and process industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Kelly’s acquisition of Children’s Therapy Center (CTC) further expands growth opportunities in the high-margin, high-demand therapeutic services segment.

The integration of CTC into Kelly Education’s Pediatric Therapy Services will bolster service delivery, offering Minnesota school districts access to comprehensive therapy solutions to address the increasing demand arising from student special education needs.

The addition of CTC brings increased scale to the current network of licensed therapists, enabling flexible practice in clinics or schools.

TROY, Mich., Nov. 19, 2024 (GLOBE NEWSWIRE) — Today, Kelly (Nasdaq: KELYA, KELYB) announced that it has acquired Children’s Therapy Center (CTC). Specializing in occupational, physical, and speech therapy for children from birth to eighteen, CTC operates from its headquarters in Eagan, MN, with an additional office in Apple Valley, MN. This acquisition will integrate CTC into Kelly Education’s Pediatric Therapy Services (PTS) portfolio. This provides opportunities for Minnesota school districts, including those who currently partner with Teachers On Call (TOC), a Kelly Education Company, to integrate PTS’s related therapy services to meet the growing demand of student special education needs. The terms of the acquisition were not disclosed.

“Children’s Therapy Center’s people-focused culture aligns well with Kelly’s values,” said Nicola Soares, president of Kelly Education. “CTC’s therapist-focused model emphasizes provider-child relationships and is dedicated to achieving positive outcomes for children. This expansion also enables us to bring value to the Center’s strong therapist retention practices by offering flexibility to practice in either school or clinical settings, underscoring our commitment to growth and comprehensive service delivery.”

CTC offers diverse interventions supported by continuous professional development for its therapists. Focused on delivering best-in-class service and ensuring the highest standards of care, CTC is committed to strong compliance, implementing robust processes to ensure adherence to federal, state, and local regulations.

“I am excited about the direction of this innovative adoption by Kelly Education’s PTS specialty brand, bringing together our unique strengths to advance holistic care for children,” said Sue Fuller, founder of Children’s Therapy Center. “This collaboration represents a unified vision and offers a remarkable opportunity to transform how we deliver services, ensuring that every child receives the support necessary for their growth and well-being.”

About Kelly

Kelly (Nasdaq: KELYA, KELYB) helps companies recruit and manage skilled workers and helps job seekers find great work. Since inventing the staffing industry in 1946, we have become experts in the many industries and local and global markets we serve. With a network of suppliers and partners, we connect job seekers around the world with meaningful work. Our suite of outsourcing and consulting services ensures companies have the people they need, when and where they are needed most. Headquartered in Troy, Michigan, we empower businesses and individuals to access limitless opportunities in industries such as science, engineering, technology, education, manufacturing, retail, finance, and energy. Visit kellyservices.com.

About Kelly Education

Kelly Education powers the future of learning through customized workforce solutions, including hiring and recruiting, business management, professional development, academic and social-emotional support across the full continuum of education––from PreK-12, special education, and therapeutic services to executive search and beyond. Kelly Education is a business of Kelly (Nasdaq: KELYA, KELYB), a global workforce solutions provider that connects businesses and individuals with limitless opportunities through meaningful work. Learn more at kellyeducation.com or connect with us on LinkedIn, Facebook, and X.

Forward-Looking Statements

This release contains statements that are forward looking in nature and, accordingly, are subject to risks and uncertainties. These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. Statements that are not historical facts, including statements about Kelly’s financial expectations, are forward-looking statements. Factors that could cause actual results to differ materially from those contained in this release include, but are not limited to, (i) changing market and economic conditions, (ii) disruption in the labor market and weakened demand for human capital resulting from technological advances, loss of large corporate customers and government contractor requirements, (iii) the impact of laws and regulations (including federal, state and international tax laws), (iv) unexpected changes in claim trends on workers’ compensation, unemployment, disability and medical benefit plans, (v) litigation and other legal liabilities (including tax liabilities) in excess of our estimates, (vi) our ability to achieve our business’s anticipated growth strategies, (vi) our future business development, results of operations and financial condition, (vii) damage to our brands, (viii) dependency on third parties for the execution of critical functions, (ix) conducting business in foreign countries, including foreign currency fluctuations, (x) availability of temporary workers with appropriate skills required by customers, (xi) cyberattacks or other breaches of network or information technology security, and (xii) other risks, uncertainties and factors discussed in this release and in the Company’s filings with the Securities and Exchange Commission. In some cases, forward-looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “target,” “aim,” “estimate,” “intend,” “plan,” “believe,” “potential,” “continue,” “is/are likely to” or other similar expressions. All information provided in this press release is as of the date of this press release and we undertake no duty to update any forward-looking statement to conform the statement to actual results or changes in the Company’s expectations.

HOUSTON, Nov. 18, 2024 (GLOBE NEWSWIRE) — Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) (NASDAQ: GLDD), the largest provider of dredging services in the United States, announced that its newly launched Multi Cat dredge support vessels, Cape Hatteras and Cape Canaveral, have been awarded the prestigious 2024 Significant Boat of the Year title at the International WorkBoat Show. This award underscores the Company’s commitment to safety, innovation, and operational excellence in the dredging and maritime sectors.

The Cape Hatteras and Cape Canaveral, built by Conrad Shipyard in Morgan City, Louisiana, are 99-foot Damen 3013 Multi Cat vessels equipped with cutting-edge technology and features that elevate both safety and efficiency in dredging operations.

Chris Gunsten, Senior Vice President of Project Services and Fleet Engineering at Great Lakes commented, “These vessels represent a milestone for our Company and the dredging industry. The Multi Cat design introduces critical safety enhancements by enabling pipe handling and connection work to take place securely on deck, significantly reducing the risk of man overboard incidents. The vessels are a perfect fit with our Company’s strong safety culture and already have shown their ability to improve our dredging efficiency while supporting vital shoreline protection and waterway maintenance.”

The Cape Hatteras and Cape Canaveral vessels are not only the first Damen Multi Cats built in the U.S., but also represent a major step forward in supporting dredging operations with enhanced safety, reduced manual labor, and greater operational flexibility. Their design eliminates the need for additional floating support vessels, contributing to improved operational efficiency and reduced environmental impact. The vessels’ cutting-edge equipment ensures safe and effective navigation and communication on complex dredging projects.

Lasse Petterson, Great Lakes’ President and Chief Executive Officer commented, “Great Lakes is committed to leveraging advanced technologies to maintain and improve U.S. shorelines and waterways. These Multi Cat vessels are integral to the Company’s mission to lead the dredging industry with innovative, safe, and efficient solutions.”

The Company

Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 134-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Cautionary Note Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking” statements as defined in Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), the Private Securities Litigation Reform Act of 1995 (the “PSLRA”) or in releases made by the Securities and Exchange Commission (the “SEC”), all as may be amended from time to time. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of Great Lakes and its subsidiaries, or industry results, to differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements. Statements that are not historical fact are forward-looking statements. These cautionary statements are being made pursuant to the Exchange Act and the PSLRA with the intention of obtaining the benefits of the “safe harbor” provisions of such laws. Great Lakes cautions investors that any forward-looking statements made by Great Lakes are not guarantees or indicative of future events.

Although Great Lakes believes that its plans, intentions and expectations reflected in this press release are reasonable, actual events could differ materially. The forward-looking statements contained in this press release are made only as of the date hereof and Great Lakes does not have or undertake any obligation to update or revise any forward-looking statements whether as a result of new information, subsequent events or otherwise, unless otherwise required by law.

For further information contact: Tina Baginskis Director, Investor Relations 630-574-3024

Kratos Led Team Will Design, Implement and Operate Ground Infrastructure Supporting Interoperability Across Multi-Vendor LEO Constellations Using its Kratos OpenSpace® Platform

SAN DIEGO, Nov. 13, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in the defense, national security and global markets, announced today that it has been awarded a contract valued at a maximum of $116.7 million over five years to create and operate an Advanced Fire Control Ground Infrastructure (AFCGI) for the U.S. Space Development Agency’s (SDA) Advanced Fire Control (AFC) program. The AFC will deliver integrated space and ground elements to demonstrate advanced fire control missions for missile defense.

Advanced fire control brings highly sophisticated systems for space-based sensing. These systems enable precise, real-time coordination for tracking operations in space for effective responses to threats. Among its applications, the AFCGI will support SDA’s Fire-control On Orbit-support-to-the-war Fighter program, also known as FOO Fighter or F2, which is tasked with detecting and tracking advanced missile threats, including hypersonic missiles.

As the AFCGI prime contractor, Kratos will lead a team of partner companies to:

Deliver and manage ground segment resources, including ground entry points and terrestrial network connections;

Fit-out and manage a government-owned, contractor-operated (GOCO) facility called the Demonstration Operations Center;

Manage a government-procured, contractor-operated cloud environment to provide cloud services, including hosting space vehicle mission operations center software and interfacing with mission partner systems; and,

Provide program management, systems engineering, integration, verification, and operations and maintenance of the AFC ground infrastructure.

Members of the Kratos-led team include ASRC Federal Systems Solutions, LLC, Peraton, Inc., Sphinx Defense, Inc. and Stellar Solutions, Inc.

Core to the AFCGI, Kratos will provide a Ground Resource Manager (GRM) which will be built for the FOO Fighter program and designed to support any future fire control demonstrations. Built upon Kratos’s OpenSpace Ground Platform, the GRM will ensure interoperability to support new space vehicles built by multiple manufacturers from multiple AFC constellations. OpenSpace is an orchestrated, software-defined and cloud-native platform based on accepted industry standards. With it, these satellite manufacturers will be able to synchronize their Command and Control (C2) missions into the AFCGI infrastructure, and new network elements and software applications will integrate seamlessly into the AFCGI. The GRM will act as the hub for the AFC constellations, serving to demonstrate modern capabilities as they evolve to support increasingly sophisticated operational programs.

Phil Carrai, President of Kratos’ Space Division stated, “Advancements in missile technology and hypersonics that can travel at more than 3000 mph present new adversarial threats and will require new defensive capabilities to identify, track and respond to them rapidly. The AFCGI will serve as a standing sandbox for exploring and validating new technologies, solutions and techniques to address these threats with commensurate speed and agility. The GRM will enable the Space Force to capitalize on best of breed technologies from across the most advanced developers, and seamlessly integrate and orchestrate their operations.”

About Kratos OpenSpace Kratos’ OpenSpace family of solutions enables the digital transformation of satellite ground systems to become a more dynamic and powerful part of the space network. The family consists of three product lines: OpenSpace SpectralNet for converting satellite RF signals to be used in digital environments; OpenSpace quantum products, which are virtual versions of traditional hardware components; and the OpenSpace Platform, the first commercially available, fully orchestrated, software-defined ground system. These three OpenSpace lines enable government agencies, commercial satellite operators and other service providers to implement digital operations at their own pace and in ways that meet their unique mission goals and business models. For more information about the OpenSpace family visit www.KratosDefense.com/OpenSpace.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements

Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 31, 2023, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

Company delivers 83% year-over-year revenue growth with strong gross margin

Raises mid-point of full year Adjusted EBITDA guidance

CHICAGO, Nov. 12, 2024 (GLOBE NEWSWIRE) — FreightCar America, Inc. (NASDAQ: RAIL) (“FreightCar America” or the “Company”), a diversified manufacturer and supplier of railroad freight cars, railcar parts and components, today reported results for the third quarter ended September 30, 2024.

Third Quarter 2024 Highlights

Revenues of $113.3 million on 961 railcar deliveries, compared to revenues of $61.9 million on 503 railcar deliveries in the third quarter of 2023, up 83% and 91% respectively

Gross margin of 14.3% with gross profit of $16.2 million, compared to gross margin of 14.9% with gross profit of $9.2 million in the third quarter of 2023

Net loss of ($107.0) million, or ($3.57) per share and Adjusted net income of $7.3 million, or $0.08 per share, driven by a ($110.0) million non-cash loss on warrant liability due to a significant appreciation in share price

Adjusted EBITDA of $10.9 million, compared to Adjusted EBITDA of $3.5 million in the third quarter of 2023, up 211%

Ended the quarter with a backlog of 3,611 units valued at $372 million

“We again demonstrate the power of our disciplined approach to growth and operational excellence. Delivering another solid quarter, that continues the momentum for a record-setting year out of our operating facility. Our team has consistently followed through on our commitments, with robust product shipments and adaptable operating capabilities. This reinforces our ability to meet our customers’ needs while improving our gross margins, and further demonstrates the power of our value proposition. We continue to showcase our ability to secure business through innovative solutions, and our ease of doing business which has led to a consistent higher quality of earnings,” commented Nick Randall, President and Chief Executive Officer of FreightCar America.

Randall continued, “Our pipeline is invigorated, with consistent demand across a broad range of railcar types. As we head into the fourth quarter, we are well positioned to sustain this momentum through our differentiated offerings and unique market approach. Our commitment to innovation and operational flexibility sets us apart in the industry, ensuring that we deliver long-term value for our customers and shareholders.”

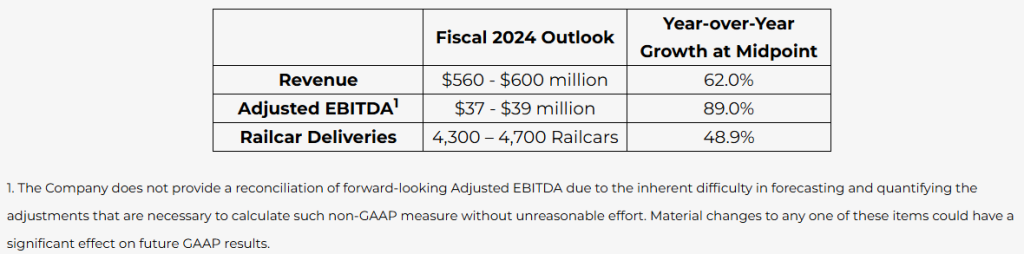

Fiscal Year 2024 Outlook

The Company has updated its outlook for fiscal year 2024 as follows:

Mike Riordan, Chief Financial Officer of FreightCar America, commented, “Given our strong order activity and delivery performance year to date, we are narrowing and raising the mid-point of our previously issued full-year EBITDA guidance to between $37 million and $39 million while reaffirming our previously stated revenue and delivery guidance. As we move forward, I am confident in our ability to achieve profitable growth and cash generation across the enterprise with an even stronger financial profile.”

Third Quarter 2024 Conference Call & Webcast Information

The Company will host a conference call and live webcast on Tuesday, November 12 at 11:00 a.m. (Eastern Time) to discuss its third quarter 2024 financial results. FreightCar America invites shareholders and other interested parties to listen to its financial results conference call via the following live and recorded methods:

Teleconference: Dial-in numbers for the live Conference Call are (877) 407-0789 or (201) 689-8562. Please call in at least 10 minutes prior to the start time of the call. An audio replay may be accessed at (844) 512-2921 or (412) 317-6671; Passcode: 13749627.

About FreightCar America

FreightCar America, headquartered in Chicago, Illinois, is a leading designer, producer and supplier of railroad freight cars, railcar parts and components. We also specialize in railcar repairs, complete railcar rebody services and railcar conversions that repurpose idled rail assets back into revenue service. Since 1901, our customers have trusted us to build quality railcars that are critical to economic growth and instrumental to the North American supply chain. To learn more about FreightCar America, visit www.freightcaramerica.com.

Forward-Looking Statements

This press release contains statements relating to our expected financial performance, financial condition, and/or future business prospects, events and/or plans that are “forward-looking statements” as defined under the Private Securities Litigation Reform Act of 1995. Forward-looking statements represent our estimates and assumptions only as of the date of this press release. Our actual results may differ materially from the results described in or anticipated by our forward-looking statements due to certain risks and uncertainties. These risks and uncertainties relate to, among other things, the cyclical nature of our business; adverse geopolitical, economic and market conditions, including inflation; material disruption in the movement of rail traffic for deliveries; fluctuating costs of raw materials including steel and aluminum; future changes in U.S. tax laws and regulations or interpretations thereof; delays in the delivery of raw materials; our ability to maintain relationships with our suppliers of railcar components; our reliance upon a small number of customers that represent a large percentage of our sales; the variable purchase patterns of our customers and the timing of completion, delivery and customer acceptance of orders; the highly competitive nature of our industry; the risk of lack of acceptance of our new railcar offerings, and other competitive factors. The factors listed above are not exhaustive. New factors emerge from time to time that may cause our business not to develop as we expect, and it is not possible for us to predict all of them. We expressly disclaim any duty to provide updates to any forward-looking statements made in this press release, whether as a result of new information, future events or otherwise.

Non-GAAP Financial Measures

This press release includes measures not derived in accordance with generally accepted accounting principles (“GAAP”), such as EBITDA, Adjusted EBITDA, Adjusted net income (loss) and Adjusted EPS. These non-GAAP measures should not be considered in isolation or as a substitute for any measure derived in accordance with GAAP and may also be inconsistent with similar measures presented by other companies. Reconciliations of these measures to the applicable most closely comparable GAAP measures, and reasons for the Company’s use of these measures, are presented in the attached pages.

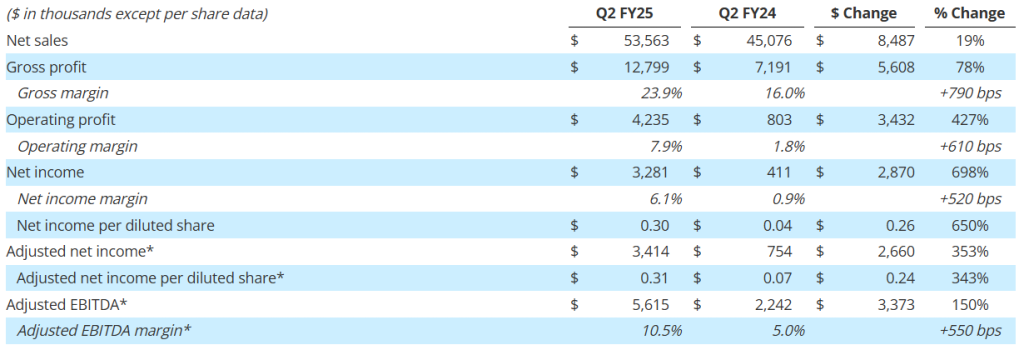

Revenue increased 19% to $53.6 million, driven by strength across its markets

Margin expansion fueled by sales growth and execution: Gross margin improved 790 basis points to 23.9% of sales, net margin increased 520 basis points to 6.1% of sales, and adjusted EBITDA1 margin expanded 550 basis points to 10.5% of sales

Net income per diluted share was $0.30 in the second quarter; adjusted net income per diluted share¹ was $0.31

Strong orders of $63.7 million, driven by demand from defense, space, and refining, resulted in a book-to-bill ratio of 1.2x and a record backlog of $407 million1

Strong balance sheet with no debt, $32.3 million in cash, and access to $43 million under its revolving credit facility at quarter end to support growth initiatives

Raised full year guidance for gross margin and adjusted EBITDA¹ to reflect improved profitability

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy, and process industries, today reported financial results for its second quarter for the fiscal year ending March 31, 2025 (“fiscal 2025”). Results for the quarter include the P3 Technologies, LLC (“P3”) acquisition, which closed on November 9, 2023.

“Our team’s efforts to diversify and strengthen the business over the past few years are clearly yielding results, as shown by our record second-quarter performance,” commented Daniel J. Thoren, President and Chief Executive Officer. “Strong sales growth in our markets, along with exceptional execution throughout the business, have driven meaningful margin expansion. Our strategic emphasis on higher-margin opportunities and operational efficiencies has been a key driver of this success.”

Mr. Thoren added, “We are also focused on recruiting and retaining top talent, and have initiatives to enhance our supply chain, which helps us to improve performance and manage our risk. These initiatives, along with our strengthened balance sheet, robust orders2, and growing backlog2, we believe positions us well to sustain growth and profitability for the next several years. Importantly, we have raised our full-year adjusted EBITDA guidance, keeping us firmly on track to achieve our FY2027 target of low to mid-teen adjusted EBITDA margins.”

Second Quarter Fiscal 2025 Performance Review

(All comparisons are with the same prior-year period unless noted otherwise.)

*Graham believes that, when used in conjunction with measures prepared in accordance with U.S. generally accepted accounting principles, adjusted net income, adjusted net income per diluted share, adjusted EBITDA and adjusted EBITDA margin, which are non-GAAP measures, help in the understanding of its operating performance. See attached tables and other information on pages 10 and 11 for important disclosures regarding Graham’s use of these non-GAAP measures.

Record quarterly net sales of $53.6 million increased 19%, or $8.5 million, and included $0.9 million of incremental sales from P3. Sales to the defense market grew by $5.8 million, or 23%, driven by the expansion of new defense programs, the ramp-up of existing programs, and the timing of key project milestones. Additionally, higher refining and chemical/petrochemical sales contributed $2.2 million to the growth, largely reflecting the timing of capital improvement projects. Aftermarket sales to the refining, chemical/petrochemical, and defense markets of $9.8 million remained strong but were $1.5 million lower than the prior year record levels. See supplemental data for a further breakdown of sales by market and region.

Gross margin expanded 790 basis points to 23.9%, driven by the leverage on higher volume, a favorable mix toward higher margin projects, improved pricing, and better execution. Additionally, gross profit for the quarter benefited $0.4 million, or approximately 80 basis points, due to the $2.1 million grant from the BlueForge Alliance. This grant is reimbursing the Company for the cost of its defense welder training programs in Batavia and related equipment. Graham expects to realize similar gross profit benefits from the grant over the next two quarters, or for the remainder of fiscal 2025.

Selling, general and administrative expense (“SG&A”), including amortization, totaled $9.2 million, or 17.1% of sales, up $2.8 million compared with the prior year. This increase reflects the Company’s continued investments in its operations, employees, and technology. Notable contributors to the increase included $0.4 million of incremental costs related to P3, $0.3 million increase in the supplemental performance bonus for Barber-Nichols employees2, $0.2 million for enterprise resource planning (“ERP”) conversion costs at the Batavia facility, and $0.2 million of incremental research and development expenses. The remainder of the increase in SG&A was primarily related to increased costs associated with the Company’s growth and various other initiatives.

Included in other operating income for the second quarter of fiscal 2025 was a $0.6 million reversal of a previously accrued contingent earnout liability for P3. The reversal was not due to any lost orders, but rather a delayed project that extended beyond the earnout period.

Cash Management and Balance Sheet

Cash provided by operating activities totaled $22.6 million for the six month period ending September 30, 2024, nearly double the amount from the comparable period in fiscal 2024. As of September 30, 2024, cash and cash equivalents were $32.3 million, up from $16.9 million at the end of fiscal 2024.

Capital expenditures of $6.5 million for the first six months of fiscal 2025 were focused on capacity expansion and productivity improvements. The Company increased its expected fiscal 2025 capital expenditures to be in the range of $13.0 million to $18.0 million from its previous expectations of $10.0 million to $15.0 million due to a land purchase in Arvada, CO, and plans to build a liquid hydrogen and oxygen testing facility to support future growth and customer needs.

The Company had no debt outstanding at September 30, 2024 with $43 million available on its senior secured revolving credit facility after taking into account outstanding letters of credit.

Orders for the three-month period ended September 30, 2024, were $63.7 million, resulting in a book-to-bill ratio of 1.2x. Defense orders represented 48% of total orders and included a contract to supply the MK19 air turbine pump for the torpedo ejection system on the Columbia-class submarine. Space orders, which can fluctuate due to the timing of projects, saw a meaningful increase to $13.5 million, which included a contract for the cryogenic recirculation pump that provides thermal conditioning for upper stage engines on launch vehicles in space. Refining orders totaled $10.6 million and were driven by continued strength in aftermarket demand and the timing of new capital projects.

Backlog at quarter end reached a record $407.0 million, up 30% over the prior-year period and up 3% sequentially. Approximately 35% to 45% of orders currently in backlog are expected to be converted to sales in the next twelve months and another 30% to 40% is expected to convert to sales over the following year. The majority of orders expected to convert beyond twelve months are for the defense industry, specifically the U.S. Navy.

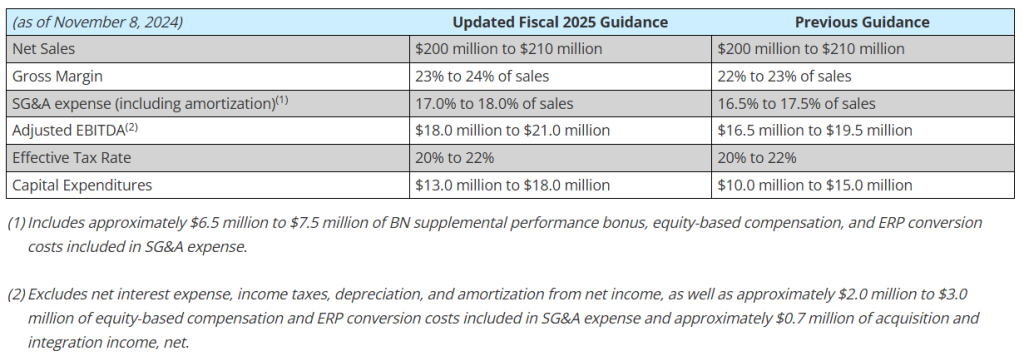

Fiscal 2025 Outlook

The Company’s outlook for 2025 was updated as follows:

Webcast and Conference Call

GHM’s management will host a conference call and live webcast on November 8, 2024 at 11:00 a.m. Eastern Time (“ET”) to review its financial results as well as its strategy and outlook. The review will be accompanied by a slide presentation, which will be made available immediately prior to the conference call on GHM’s investor relations website.

A question-and-answer session will follow the formal presentation. GHM’s conference call can be accessed by calling (201) 689-8560. Alternatively, the webcast can be monitored from the events section of GHM’s investor relations website.

A telephonic replay will be available from 3:00 p.m. ET today through Friday, November 15, 2024. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13749103 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy, and process industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “expects,” “future,” “outlook,” “anticipates,” “believes,” “could,” “guidance,” ”may”, “will,” “plan” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, profitability of future projects and the business, its ability to deliver to plan, its ability to continue to strengthen relationships with customers in the defense industry, its ability to secure future projects and applications, expected expansion and growth opportunities, anticipated sales, revenues, adjusted EBITDA, adjusted EBITDA margins, capital expenditures and SG&A expenses, the timing of conversion of backlog to sales, orders, market presence, profit margins, tax rates, foreign sales operations, customer preferences, changes in market conditions in the industries in which it operates, changes in general economic conditions and customer behavior, forecasts regarding the timing and scope of the economic recovery in its markets, and its acquisition and growth strategy, are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

Non-GAAP Financial Measures

Adjusted EBITDA is defined as consolidated net income (loss) before net interest expense, income taxes, depreciation, amortization, other acquisition related expenses, and other unusual/nonrecurring expenses. Adjusted EBITDA margin is defined as Adjusted EBITDA as a percentage of sales. Adjusted EBITDA and Adjusted EBITDA margin are not measures determined in accordance with generally accepted accounting principles in the United States, commonly known as GAAP. Nevertheless, Graham believes that providing non-GAAP information, such as Adjusted EBITDA and Adjusted EBITDA margin, is important for investors and other readers of Graham’s financial statements, as it is used as an analytical indicator by Graham’s management to better understand operating performance. Moreover, Graham’s credit facility also contains ratios based on Adjusted EBITDA. Because Adjusted EBITDA and Adjusted EBITDA margin are non-GAAP measures and are thus susceptible to varying calculations, Adjusted EBITDA, and Adjusted EBITDA margin, as presented, may not be directly comparable to other similarly titled measures used by other companies.

Adjusted net income and adjusted net income per diluted share are defined as net income and net income per diluted share as reported, adjusted for certain items and at a normalized tax rate. Adjusted net income and adjusted net income per diluted share are not measures determined in accordance with GAAP, and may not be comparable to the measures as used by other companies. Nevertheless, Graham believes that providing non-GAAP information, such as adjusted net income and adjusted net income per diluted share, is important for investors and other readers of the Company’s financial statements and assists in understanding the comparison of the current quarter’s and current fiscal year’s net income and net income per diluted share to the historical periods’ net income and net income per diluted share. Graham also believes that adjusted net income per share, which adds back intangible amortization expense related to acquisitions, provides a better representation of the cash earnings of the Company.

Forward-Looking Non-GAAP Measures

Forward-looking adjusted EBITDA and adjusted EBITDA margin are non-GAAP measures. The Company is unable to present a quantitative reconciliation of these forward-looking non-GAAP financial measures to their most directly comparable forward-looking GAAP financial measures because such information is not available, and management cannot reliably predict the necessary components of such GAAP measures without unreasonable effort largely because forecasting or predicting our future operating results is subject to many factors out of our control or not readily predictable. In addition, the Company believes that such reconciliations would imply a degree of precision that would be confusing or misleading to investors. The unavailable information could have a significant impact on the Company’s fiscal 2025 financial results. These non-GAAP financial measures are preliminary estimates and are subject to risks and uncertainties, including, among others, changes in connection with purchase accounting, quarter-end, and year-end adjustments. Any variation between the Company’s actual results and preliminary financial estimates set forth above may be material.

Key Performance Indicators

In addition to the foregoing non-GAAP measures, management uses the following key performance metrics to analyze and measure the Company’s financial performance and results of operations: orders, backlog, and book-to-bill ratio. Management uses orders and backlog as measures of current and future business and financial performance, and these may not be comparable with measures provided by other companies. Orders represent written communications received from customers requesting the Company to provide products and/or services. Backlog is defined as the total dollar value of net orders received for which revenue has not yet been recognized. Management believes tracking orders and backlog are useful as they often times are leading indicators of future performance. In accordance with industry practice, contracts may include provisions for cancellation, termination, or suspension at the discretion of the customer.

The book-to-bill ratio is an operational measure that management uses to track the growth prospects of the Company. The Company calculates the book-to-bill ratio for a given period as net orders divided by net sales.

Given that each of orders, backlog, and book-to-bill ratio are operational measures and that the Company’s methodology for calculating orders, backlog and book-to-bill ratio does not meet the definition of a non-GAAP measure, as that term is defined by the U.S. Securities and Exchange Commission, a quantitative reconciliation for each is not required or provided.

New facility will enable testing of liquid hydrogen (LH2), liquid oxygen (LOX) and liquid methane (LCH4)

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“Graham” or “the Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy and process industries, announced today its plans to construct a state-of-the-art cryogenic propellant testing facility in Florida, near its P3 Technologies, LLC subsidiary. Leveraging Graham’s longstanding expertise in the cryogenic and space launch industries, this new facility will help to meet increasing demand for efficient, scalable testing solutions in key markets, including Space, Defense, New Energy, and potential applications in the medical field.

The facility will offer a cost-effective, timely alternative to existing testing centers, which often prioritize flagship programs and leave other critical programs with limited options. This new facility will enable liquid hydrogen (LH2), liquid oxygen (LOX), and liquid methane (LCH4) testing at pressurized, sub-cooled, or saturated conditions, and is ideally suited for testing pumps, components, fluid management systems, and combustion devices. By expanding Graham’s capabilities in cryogenic propellant testing, the Company aims to better support both current and future customer programs, adding agility and depth to its testing services in response to diverse and evolving program requirements.

“We believe this new testing facility will strengthen our position as a trusted partner by directly addressing customer needs for timely and cost-effective cryogenic propellant testing, complementing our existing capabilities and advancing the support we can offer current programs,” said Dan Thoren, Graham Corporation President and Chief Executive Officer. “This investment underscores our commitment to supporting both current and future customer programs through innovative and accessible testing solutions, while enhancing Graham’s role across the Space, Defense, and New Energy sectors.”

The project will be executed over the next year, with initial tests anticipated to begin by mid-2025. The facility is projected to achieve a cash payback period of approximately two to three years and deliver an internal rate of return exceeding 20%, representing a strategic investment in Graham’s future.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy, and process industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “can,” “expects,” “potential,” “will,” “plans,” “aims,” “believe,” “projected,” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, the completion of the testing facility within the projected timeline, the Company’s ability to capitalize on the potential benefits of the new facility and timing to realize expected returns on investment, the estimated total market opportunity and the Company’s ability to capitalize on such market opportunity. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission, including under the heading entitled “Risk Factors,” its quarterly reports on Form 10-Q, and other filings it makes with the Securities and Exchange Commission. Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

New Zeus Motors are in Production and Ready for Use

SAN DIEGO, Nov. 07, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in Defense, National Security and Global Markets, today announced that its Zeus 1 and Zeus 2 Solid Rocket Motors (SRMs) completed their first successful flight on October 24, 2024, from the NASA Wallops Flight Facility in Virginia. This milestone launch provides the qualifications necessary to transition the Zeus SRMs to test programs supporting the U.S. Department of Defense, Foreign Allies, NASA, and commercial launch sponsors.

Kratos Zeus Solid Rocket Motors Complete Successful First Flight at Wallops

The flight test featured a Kratos two-stage Zeus 1 – Zeus 2 suborbital launch vehicle and provided substantial data to support rocket motor evaluation for use by future customers and sponsors who have baselined the Zeus rocket motors as part of their future test plans. Kratos expects to have production motors ready in the first quarter of 2025.

Kratos developed the Zeus family of SRMs in direct response to the need for affordable commercial launch vehicle stages for hypersonic test, ballistic missile targets, scientific research, sounding rocket and special customer missions. Kratos applied its significant rocket launch experience to establish the Zeus 1 and Zeus 2 motor specifications in close coordination with respective customer and user communities. Kratos internally funded development of the Zeus SRMs which are designed and manufactured to Kratos’ specifications by key merchant supplier and partner, L3Harris Technologies. L3Harris is on contract to begin delivering production motors to Kratos in the first quarter of 2025.

George Rumford, Director of the Department of Defense Test Resource Management Center, said, “Advancements in solid rocket motor development are critical to achieving rapid, affordable hypersonic testing.”

Dave Carter, President of Kratos’ Defense & Rocket Support Services Division, said, “I couldn’t be prouder of our whole team. They met the challenge to deliver these robust motors to market as fast as possible and meet the growing demand for rapid, reliable testing. The motors performed exceptionally well against predictions and are ready for immediate use by the broader test and research community.”

The Zeus 1 and Zeus 2 are high-performance, 32.5-inch diameter SRMs providing substantial performance improvements over similar legacy rockets. They are purposely designed to be fully compatible with existing payloads and launch infrastructure to enable rapid integration of new technologies and advanced payloads, including those currently under development by Kratos. These and other key attributes will provide Kratos and our customers with opportunities to fly more often, faster and farther, using fewer stages, and at a substantially reduced cost.

The Zeus SRM family is designed with versatility and affordability in mind as a complement to Kratos’ other internally funded investments such as the Erinyes hypersonic test “flyer” that debuted in June of this year. Kratos’ investments in the hypersonic and other relevant areas create a versatile family of test and evaluation products that offer complete systems. With the Zeus SRMs, the Erinyes, and other Kratos front end systems, Kratos is one of the only companies boasting both launcher and flyer systems within one organization, providing unmatched innovation, disruptive capabilities, mission responsiveness and affordability to the customer.

Eric DeMarco, President & CEO of Kratos Defense & Security Solutions, Inc., said, “Kratos is laser focused on supporting the Department of Defense, U.S. National Security requirements and working with our government partners to reinvigorate our country’s defense industrial base. Zeus’ successful mission is representative of the value Kratos’ strategy delivers to our stakeholders, with Kratos’ internally funded investments allowing us to rapidly develop and be first to market with affordable relevant systems for our partners and customers.”

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading-edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value-add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 31, 2023, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

Third Quarter 2024 Revenues of $275.9 Million Compared with Third Quarter 2023 Revenues of $274.6 Million

Third Quarter 2024 Unmanned Systems Revenues of $64.2 Million Compared with Third Quarter 2023 Revenues of $56.7 Million

Third Quarter 2024 Consolidated Book to Bill Ratio of 1.0 to 1 and Last Twelve Months Ended September 29, 2024 Consolidated Book to Bill Ratio of 1.1 to 1

Third Quarter 2024 Consolidated Bookings of $267.2 Million and Last Twelve Months Ended September 29, 2024 Consolidated Bookings of $1.240 Billion

Affirms Full Year 2024 Financial Forecast

SAN DIEGO, Nov. 07, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq:KTOS), a Technology Company in the Defense, National Security and Global Markets, today reported its third quarter 2024 financial results, including Revenues of $275.9 million, Operating Income of $6.5 million, Net Income of $3.2 million, Adjusted EBITDA of $24.6 million and a consolidated book to bill ratio of 1.0 to 1.0.

Included in third quarter 2024 Net Income and Operating Income is non-cash stock compensation expense of $7.2 million and Company-funded Research and Development (R&D) expense of $9.9 million.

Kratos reported third quarter 2024 GAAP Net Income attributable to Kratos of $3.2 million and Earnings Per Share of $0.02 compared to a GAAP Net Loss attributable to Kratos of $1.6 million and a GAAP Net Loss per share of $0.01 for the third quarter of 2023. Adjusted EPS was $0.11 for the third quarter of 2024 compared to $0.12 for the third quarter of 2023.

Third quarter 2024 Revenues of $275.9 million increased $1.3 million, or 0.5 percent, from third quarter 2023 Revenues of $274.6 million. Including the impact of the Sierra Technical Services, Inc. (STS) acquisition on a pro forma basis as if acquired at the beginning of 2023, Unmanned Systems reported 8.7 percent organic revenue growth. Kratos Turbine Technologies, Microwave Products, C5ISR, Defense Rocket Support and Training Solutions businesses in KGS also all reported organic revenue growth, offset by the previously reported and expected decline of approximately $24.2 million in the Space and Satellite business, primarily resulting from the industry related impact from OEM delays in the manufacture and delivery of software defined satellites.

Third quarter 2024 Cash Flow Generated from Operations was $6.1 million, which includes working capital requirements for increases in prepaid assets, inventory balances, vendor required deposits and reduction in deferred revenue or customer prepayment balances. Free Cash Flow Used in Operations was $9.2 million after funding of $15.3 million of capital expenditures, including the continued manufacture of two production lots of Kratos Valkyrie unmanned tactical jet drone aircraft prior to contract award.

For the third quarter of 2024, Kratos’ Unmanned Systems Segment (KUS) generated Revenues of $64.2 million, compared to $56.7 million in the third quarter of 2023, with organic revenue growth of 8.7 percent, driven primarily by increased target drone production, and reflects the pro forma impact of the STS acquisition as if acquired at the beginning of 2023. KUS’s Operating Income was $0.4 million in the third quarter of 2024 compared to Operating Income of $2.6 million in the third quarter of 2023, primarily reflecting the mix of revenues and resources.

KUS’s Adjusted EBITDA for the third quarter of 2024 was $3.6 million, compared to third quarter 2023 KUS Adjusted EBITDA of $5.4 million, reflecting the mix of revenues and resources.

KUS’s book-to-bill ratio for the third quarter of 2024 was 0.5 to 1.0 and 1.1 to 1.0 for the last twelve months ended September 29, 2024, with bookings of $32.6 million for the three months ended September 29, 2024, and bookings of $295.1 million for the last twelve months ended September 29, 2024. Total backlog for KUS at the end of the third quarter of 2024 was $273.9 million compared to $305.5 million at the end of the second quarter of 2024.

For the third quarter of 2024, Kratos’ Government Solutions Segment (KGS) generated Revenues of $211.7 million compared to $217.9 million in the third quarter of 2023, reflecting aggregate organic revenue increases of $18.0 million generated by the Kratos’ Turbine Technologies, Microwave Products, C5ISR, Defense Rocket Support and Training Solutions businesses in KGS, offset by the previously reported and expected decline of $24.2 million in the Space and Satellite business, as noted above.

KGS reported operating income of $13.5 million in the third quarter of 2024 compared to $15.9 million in the third quarter of 2023, primarily reflecting the revenue volume and mix of revenues and resources. Third quarter 2024 KGS Adjusted EBITDA was $21.0 million, compared to third quarter 2023 KGS Adjusted EBITDA of $22.3 million, reflecting the mix in revenues, revenue volume and resources.

For the third quarter of 2024 and the last twelve months ended September 29, 2024, KGS reported a book-to-bill ratio of 1.1 to 1.0, and bookings of $234.6 million and $945.0 million for the three and last twelve months ended September 29, 2024, respectively. KGS’s total backlog at the end of the third quarter of 2024 was $1.02 billion, as compared to $997.2 million at the end of the second quarter of 2024.

For the third quarter of 2024, Kratos reported consolidated bookings of $267.2 million and a book-to-bill ratio of 1.0 to 1.0, with consolidated bookings of $1.24 billion and a book-to-bill ratio of 1.1 to 1.0 for the last twelve months ended September 29, 2024. Consolidated backlog was $1.294 billion on September 29, 2024 and $1.303 billion on June 30, 2024. Kratos’ bid and proposal pipeline was $12.0 billion at September 29 and June 30, 2024. Backlog at September 29, 2024 was comprised of funded backlog of $1.098 billion and unfunded backlog of $195.4 million.

Eric DeMarco, Kratos’ President and CEO, said, “Kratos’ strategy of making internally funded investments, to be first to market with relevant hardware, software and systems, in coordination with our partners and customers is working, as reflected in our financial results and our $12 billion opportunity pipeline. A recent representative example of this success is the successful flight of Kratos’ Zeus 1 and Zeus 2 system solid rocket motor stack with our customer’s payload, positioning Kratos for potential growth above our current future revenue year over year 10% target beginning in 2026.”

Mr. DeMarco went on, “Consistent with the success of and opportunities from Kratos’ strategy, earlier this year we completed an equity raise to position the Company to ensure successful execution on programs we have received and expect to receive. As an update to the related investments we are making: Kratos is currently manufacturing ~ 165 jet drones a year and we are now positioned to increase to ~400 a year including Valkyrie. Kratos can now produce ~10,000 small jet engines annually for drones and missiles, Kratos Microwave Electronics’ expansion in Israel is on track for a Q2 2025 completion, including an additional new manufacturing facility, an expanded existing manufacturing facility and a space & satellite qualified capability; we have identified the site for our new rocket system production and integration facility including for Zeus, Oriole and Erinyes and plan to break ground by the end of this year; and we have now identified the site for our new turbofan engine facility. Importantly, each of these expansion initiatives have existing programs, customer funded backlog or opportunities, or are in conjunction with a partner.”

Mr. DeMarco continued, “We continue to make progress in Kratos’ tactical drone business, with Kratos’ Apollo drone program now in contract documentation and Kratos’ Athena drone program under contract. Additionally, we have had recent successful Valkyrie flights with the U.S. Marines, Navy and Office of the Secretary of Defense, and Kratos recently has been selected on a new tactical drone opportunity. Importantly, our Ghost Works is on track to fly both a Kratos tactical drone and Kratos target drone in 2025 with Kratos internally funded, developed and manufactured jet engines, which will provide increased performance and electrical power, at reduced cost. Kratos Ghost Works is also expecting to fly the newest version of Kratos Valkyrie in 2025, as we make internally funded investments and continue to expand the Valkyrie families’ capability set and further drive down its operating and overall cost, and our newest 5th Generation drone is also scheduled for first flight in 2025 in conjunction with our customer.”

Mr. DeMarco concluded, “We are in a generational recapitalization of strategic weapon systems, with Kratos being an industry leader in hardware, software and systems for mission critical National Security and Defense applications. Expected growth drivers for Kratos in 2025 include; Kratos Erinyes, Zeus, Dark Fury, Oriole and other relevant rocket systems; Kratos jet engine and propulsion systems for missiles, drones, supersonic and space systems; microwave electronics and C5ISR products for air defense, CUAS, missile and radar systems and jet target drone systems.”

Financial Guidance

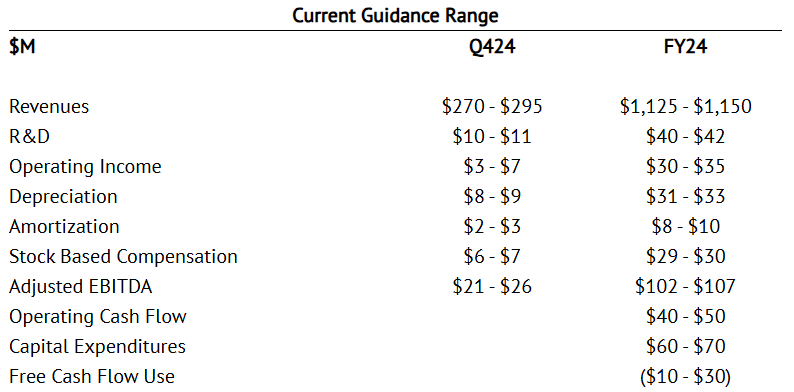

We are providing our initial 2024 fourth quarter financial guidance and affirming our full year 2024 guidance today, which ranges include our current forecasted business mix assumptions and expected contract execution and delivery schedules. Our financial guidance also includes our expectations and assumptions for our supply chain’s execution, and for employee sourcing, hiring, retention and related costs. We have also taken into consideration in our affirmed fiscal 2024 guidance the Federal Fiscal Year 2025 Continuing Resolution Authorization (CRA) which began on October 1, 2024, and under such expected CRA, no new program or contract awards, no increases in existing production contract funding, and no transition from program development to production are expected.

Our fourth quarter and full year 2024 guidance ranges are as follows:

For Kratos’ Fiscal year 2025, we are currently forecasting base case Revenue growth of approximately 10%, and Adjusted EBITDA growth. Our industry is currently operating under a Federal Fiscal Year 2025 CRA, which began October 1, 2024 and which is currently expected to continue into Kratos’ Fiscal 2025. There was also an approximate 6-month Federal Fiscal 2024 CRA, which was previously resolved in March 2024, Kratos’ current 2024 fiscal year. Additionally, the recent election will impact the Administration, House and Senate. Accordingly, we will be providing our detailed 2025 Revenue, Adjusted EBITDA, Cash Flow and other financial forecast information and guidance when we report our Fiscal 2024 results, currently expected to be in late February 2025. This will provide Kratos additional time to assess the impacts of these ongoing and recent events, if any, on National Security priorities, our 2025 business mix, contractual and program funding and timing assumptions and potential fiscal year 2025 fiscal quarter to quarter impacts. Kratos’ base case financial forecast does not assume or include any potential tactical drone program production.

Management will discuss the Company’s financial results, on a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern) today. The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions

Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com