Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New time charter contract. Euroseas executed a new time charter contract for the M/V Rena P, a 4,250 twenty-foot equivalent unit (TEU) intermediate containership. The charter contract is at a gross daily rate of $35,500 for a minimum period of 35 months and a maximum period of 37 months at the charterer’s option. The contract is expected to take effect on August 21, 2025, in continuation of its present charter. The contract is anticipated to contribute roughly $29.0 million in EBITDA during the minimum contract period. The new contract strengthens the company’s charter coverage to 88% in 2025 and 54% in 2026.

Updating estimates. The new charter contract for $35,500 represents a significant improvement compared to the previous rate of $21,000. Consequently, we have increased our 2025 adjusted EBITDA and EPS estimates to $145.1 million and $14.20, respectively, from $139.1 million and $13.35. In addition to the M/V Rena P, our estimates reflect updated time charter contract information for the M/V Marcos, M/V Synergy Antwerp, M/V Synergy Keelung, and M/V EM Hydra.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q4 pre-release. On Monday, SKYX pre-released its Q4 revenue results, reporting revenue of $23.7 million (largely aligning with our estimate of $24.0 million). Notably, the company’s revenue grew throughout 2024, from $19.0 million in Q1 to $21.4 million, $22.2 million, and $23.7 million, in the subsequent quarters.

Key leadership additions. The company recently announced the additions of Huey Long as Head of E-commerce and Greg St. John as President of Lighting, Fans and Smart Home Products. Mr. Long previously served as director of e-commerce for Amazon and as an executive at both Ashley Furniture and Walmart. Mr. St. John previously served as head of lighting at Home Depot as well as CEO of EGLO.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Business Wins. Kratos has been awarded a number of new and additions to existing contracts in March. We view these developments positively, although we remain watchful as to the impact of the ongoing continuing resolution for the Federal budget and its implications on new awards in 2025.

BQM-177A Awards. Kratos was awarded $3.4 million from the U.S. Navy for the base year of its next Contractor Logistics Support and Engineering Services contract, supporting BQM-177A aerial target system operations. If all four option years awarded under this contract are exercised, this contract has a potential value of $19.1 million. The Company also received $59.3 million for an additional 70 BQM-177A Subsonic Aerial Target aircraft through the exercise of the contract option for Full Rate Production (FRP) Lot 6.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 131-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Buyback Program. On Friday, Great Lakes Dredge & Dock Corporation announced that its Board of Directors has authorized a share repurchase program pursuant to which the Company may repurchase up to $50 million of its common stock. At the current price, the $50 million equates to 5.78 million GLDD shares or approximately 8.6% of the outstanding common. The share repurchase program expires on March 14, 2026.

Rationale. According to management, “Our business is strong, as we delivered in 2024 the second best results in our Company’s history. The outlook for 2025 and 2026 is also strong, with $1.2 billion in backlog as of December 31, 2024. Our new build program is also expected to be substantially completed in 2025. We believe the Company’s current share price does not reflect the strength of our business and that a share repurchase program will be accretive to our shareholders.”

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Shelf registration. FreightCar recently filed a universal shelf registration statement pertaining to the offer and sale from time to time of up to $200 million in aggregate of the company’s common stock, preferred stock, debt securities, new warrants, rights or units, and the resale by a selling stockholder, affiliates of PIMCO, of up to 17,038,583 shares of common stock. PIMCO has now registered the shares associated with its warrants which enables them to sell shares over time following the exercise of the warrants. The warrants are already reflected in RAIL’s fully diluted share count and in our financial model.

Cleaner financial reporting. The change in the fair market value of the warrant liability fluctuates each quarter in line with the change in RAIL’s stock price during the period. The valuation adjustment reflects accounting for the warrant holder’s investment. For the full year 2024, the company recognized a $99.5 million non-cash adjustment due to the change in the fair market value of the warrant liability. All shares underlying the warrants have been reflected as part of the weighted shares outstanding since their issuance in prior years. Eliminating the warrant liability and need to report on the change in its fair market value could narrow the difference between GAAP and adjusted earnings.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

HOUSTON, March 14, 2025 (GLOBE NEWSWIRE) — Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) (Nasdaq: GLDD), the largest provider of dredging services in the United States, today announced that its Board of Directors has authorized a share repurchase program pursuant to which the Company may repurchase up to $50 million of its common stock.

“Our business is strong, as we delivered in 2024 the second best results in our Company’s history,” said Lasse Petterson, President and Chief Executive Officer. “The outlook for 2025 and 2026 is also strong with $1.2 billion in backlog as of December 31, 2024. Our new build program is also expected to be substantially completed in 2025. We believe the Company’s current share price does not reflect the strength of our business and that a share repurchase program will be accretive to our shareholders.”

The Company may repurchase shares of common stock from time to time through open market purchases, in privately negotiated transactions, or by other means, including through the use of trading plans intended to qualify under Rule 10b5-1 under the Securities Exchange Act of 1934, as amended, in accordance with applicable securities laws and other restrictions. The timing and total amount of stock repurchases will depend upon business, economic and market conditions, corporate and regulatory requirements, prevailing stock prices, and other considerations. The share repurchase program expires on March 14, 2026, may be modified, suspended, or discontinued at any time at the Company’s discretion, and does not obligate the Company to acquire any amount of common stock.

The Company

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States, which is complemented with a long history of performing significant international projects. In addition, Great Lakes is fully engaged in expanding its core business into the offshore energy industry. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 135-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Certain statements in this press release may constitute “forward-looking” statements, as defined in Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), the Private Securities Litigation Reform Act of 1995 (the “PSLRA”) or in releases made by the Securities and Exchange Commission (the “SEC”), all as may be amended from time to time. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of Great Lakes and its subsidiaries, or industry results, to differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements. Statements that are not historical fact are forward-looking statements. Forward-looking statements can be identified by, among other things, the use of forward-looking language, such as the words “plan,” “believe,” “expect,” “anticipate,” “intend,” “estimate,” “project,” “may,” “would,” “could,” “should,” “seeks,” “are optimistic,” “commitment to” or “scheduled to,” or other similar words, or the negative of these terms or other variations are being made pursuant to the Exchange Act and the PSLRA with the intention of obtaining of these terms or comparable language, or by discussion of strategy or intentions. These cautionary statements have the benefit of the “safe harbor” provisions of such laws. Great Lakes cautions investors that any forward-looking statements made by Great Lakes are not guarantees or indicative of future performance. Important assumptions and other important factors that could cause actual results to differ materially from those forward-looking statements with respect to Great Lakes include, but are not limited to: a reduction in government funding for dredging and other contracts, or government cancellation of such contracts, or the inability of the Corps to let bids to market; our ability to qualify as an eligible bidder under government contract criteria and to compete successfully against other qualified bidders in order to obtain government dredging and other contracts; the political environment and governmental fiscal and monetary policies; cost over-runs, operating cost inflation and potential claims for liquidated damages, particularly with respect to our fixed-price contracts; the timing of our performance on contracts and new contracts being awarded to us; significant liabilities that could be imposed were we to fail to comply with government contracting regulations; project delays related to the increasingly negative impacts of climate change or other unusual, non-historical weather patterns; costs necessary to operate and maintain our existing vessels and the construction of new vessels, including with respect to changes in applicable regulations or standards; equipment or mechanical failures; pandemic, epidemic or outbreak of an infectious disease; disruptions to our supply chain for procurement of new vessel build materials or maintenance on our existing vessels; capital and operational costs due to environmental regulations; market and regulatory responses to climate change, including proposed regulations concerning emissions reporting and future emissions reduction goals; contract penalties for any projects that are completed late; force majeure events, including natural disasters, war and terrorists’ actions; changes in the amount of our estimated backlog; significant negative changes attributable to large, single customer contracts; our ability to obtain financing for the construction of new vessels, including our new offshore energy vessel; our ability to secure contracts to utilize our new offshore energy vessel; unforeseen delays and cost overruns related to the construction of our new vessels; any failure to comply with the Jones Act provisions on coastwise trade, or if those provisions were modified, repealed or interpreted differently; our ability to comply with anti-discrimination laws, including those pertaining to diversity, equity and inclusion programs; fluctuations in fuel prices, particularly given our dependence on petroleum-based products; impacts of nationwide inflation on procurement of new build and vessel maintenance materials; our ability to obtain bonding or letters of credit and risks associated with draws by the surety on outstanding bonds or calls by the beneficiary on outstanding letters of credit; acquisition integration and consolidation, including transaction expenses, unexpected liabilities and operational challenges and risks; divestitures and discontinued operations, including retained liabilities from businesses that we sell or discontinue; potential penalties and reputational damage as a result of legal and regulatory proceedings; any liabilities imposed on us for the obligations of joint ventures and similar arrangements and subcontractors; increased costs of certain material used in our operations due to newly imposed tariffs; unionized labor force work stoppages; any liabilities for job-related claims under federal law, which does not provide for the liability limitations typically present under state law; operational hazards, including any liabilities or losses relating to personal or property damage resulting from our operations; our substantial amount of indebtedness, which makes us more vulnerable to adverse economic and competitive conditions; restrictions on the operation of our business imposed by financing terms and covenants; impacts of adverse capital and credit market conditions on our ability to meet liquidity needs and access capital; limitations on our hedging strategy imposed by statutory and regulatory requirements for derivative transactions; foreign exchange risks, in particular, related to the new offshore energy vessel build; losses attributable to our investments in privately financed projects; restrictions on foreign ownership of our common stock; restrictions imposed by Delaware law and our charter on takeover transactions that stockholders may consider to be favorable; restrictions on our ability to declare dividends imposed by our financing agreements or Delaware law; significant fluctuations in the market price of our common stock, which may make it difficult for holders to resell our common stock when they want or at prices that they find attractive; changes in previously recorded net revenue and profit as a result of the significant estimates made in connection with our methods of accounting for recognized revenue; maintaining an adequate level of insurance coverage; our ability to find, attract and retain key personnel and skilled labor; disruptions, failures, data corruptions, cyber-based attacks or security breaches of the information technology systems on which we rely to conduct our business; and impairments of our goodwill or other intangible assets. For additional information on these and other risks and uncertainties, please see Item 1A. “Risk Factors” of Great Lakes’ Annual Report on our most recent Form 10-K and in other securities filings by Great Lakes with the SEC.

Although Great Lakes believes that its plans, intentions and expectations reflected in or suggested by such forward looking statements are reasonable, actual results could differ materially from a projection or assumption in any forward-looking statements. Great Lakes’ future financial condition and results of operations, as well as any forward-looking statements, are subject to change and inherent risks and uncertainties. The forward-looking statements contained in this press release are made only as of the date hereof and Great Lakes does not have or undertake any obligation to update or revise any forward-looking statements whether as a result of new information, subsequent events or otherwise, unless otherwise required by law.

For further information contact: Eric M. Birge Vice President of Investor Relations EMBirge@gldd.com 313-220-3053

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Full year 2024 financial results. FreightCar America generated 2024 adjusted net income to common stockholders of $4.4 million or $0.15 per share compared to a loss of $11.0 million or $(0.39) per share in 2023 and our estimate of $5.5 million or $0.17 per share. Gross margin as a percentage of revenue increased to 12.0% compared to 11.7% in FY 2023. Revenue and rail car deliveries increased to $559.4 million and 4,362 compared to $358.1 million and 3,022 in 2023. We had forecast revenue of $577.4 million and deliveries of 4,550. Adjusted EBITDA increased to $43.0 million compared to $20.1 million in 2023 and our estimate of $38.3 million. Full year adjusted free cash flow amounted to $21.7 million versus $(17.6) million in 2023.

Full Year 2025 corporate guidance. Management issued full year 2025 guidance. Railcar deliveries are expected to be in the range of 4,500 to 4,900, revenue is expected to be in the range of $530 million to $595 million, and adjusted EBITDA is expected to be in the range of $43 to $49 million. Compared to 2024, railcar deliveries, revenue, and adjusted EBITDA are expected to increase 7.7%, 0.6%, and 7.0%, respectively, at the midpoints of guidance.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

RESTON, Va., March 11, 2025 /PRNewswire/ — V2X, Inc. (NYSE: VVX) was awarded a new $100 million contract to support the U.S. Navy’s Aegis Ashore facilities in Poland. These facilities are a crucial component of NATO’s missile defense system, designed to detect, track, and intercept ballistic missiles in flight. As a key element in transatlantic security, this site strengthens NATO’s defense against the increasing threat of ballistic missiles.

“This contract underscores our commitment to high-consequence missions,” said Jeremy C. Wensinger, President and Chief Executive Officer of V2X. For the past four years, V2X has provided support services at the U.S. Navy’s Aegis Ashore sister site in Romania. “This award marks a significant step in strengthening NATO’s defense and protecting European populations against global threats,” Wensinger added.

The contract is firm-fixed-price with a one-year base period, seven one-year options, and an additional six-month extension.

About V2X

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Media Contact Angelica Spanos Deoudes Senior Director, Marketing and Communications Angelica.Deoudes@goV2X.com 571-338-5195

Investor Contact Mike Smith, CFA Vice President, Treasury, Corporate Development and Investor Relations IR@goV2X.com

Accelerating operational momentum through strategic portfolio actions

Provides outlook and guidance for full year 2025

NEW ALBANY, Ohio, March 10, 2025 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI), a diversified industrial products and services company, today announced financial results for its fourth quarter and full year ended December 31, 2024.

As a result of completing our strategic portfolio actions, the following are reported as discontinued operations: (1) the Industrial Automation segment, and (2) the financial information from the Cab Structures facility that was previously reported in Vehicle Solutions and Aftermarket and Accessories. CVG has three reportable segments for 2024: Vehicle Solutions, Electrical Systems and Aftermarket & Accessories. The results and comparisons presented below reflect continuing operations unless otherwise noted.

Fourth Quarter 2024 Highlights(Compared with prior-year period, where comparisons are noted)

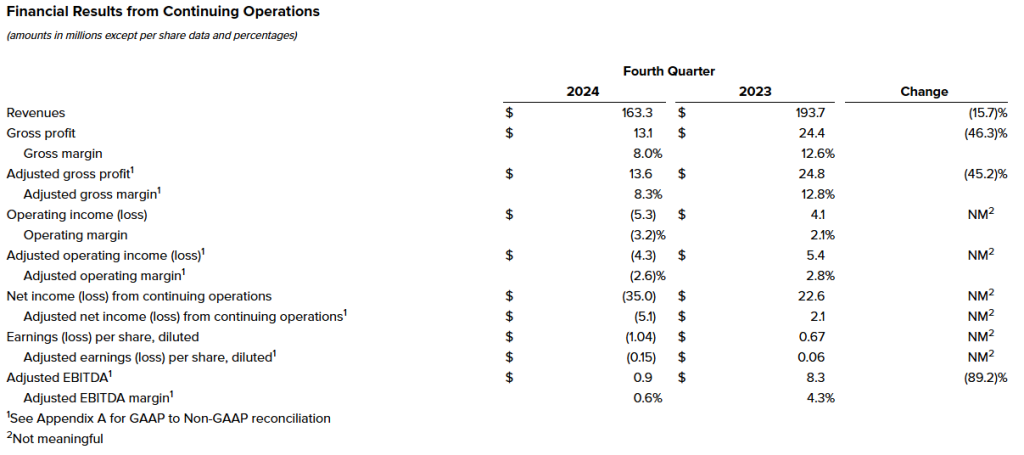

Revenue of $163.3 million, down 15.7% due primarily to a global softening in Construction and Agriculture customer demand and drop-in Class 8 Heavy Truck builds.

Operating loss of $5.3 million, and adjusted operating loss of $4.3 million, down compared to operating income of $4.1 million and adjusted operating income of $5.4 million. The decrease in operating income was driven primarily by lower sales volumes and operational inefficiencies.

Net loss from continuing operations of $35.0 million, or $(1.04) per diluted share, compared to net income of $22.6 million, or $0.67 per diluted share. Net loss included a non-cash tax valuation allowance of $28.8 million. Adjusted net loss from continuing operations of $5.1 million, or $(0.15) per diluted share, compared to adjusted net income of $2.1 million, or $0.06 per diluted share.

Adjusted EBITDA of $0.9 million, down 89.2%, with an adjusted EBITDA margin of 0.6%, down from 4.3%.

The sale of CVG’s Industrial Automation business closed on October 30, 2024, allowing CVG to focus on its core segments.

Full Year 2024 Highlights(Compared with prior-year period, where comparisons are noted)

Revenue of $723.4 million, down 13.4%, driven by a global softening in customer demand and the wind-down of certain programs in our Vehicle Solutions segment.

New business wins in excess of $97 million when fully ramped; these wins were concentrated in our Electrical Systems segment, predominantly outside of Construction and Agriculture end markets.

Operating loss of $0.8 million, down $40.6 million, and adjusted operating income of $6.5 million, down $35.2 million. The decrease in operating income was due to lower sales volumes and operational inefficiencies.

Continued shifting production capacity to new, lower-cost facilities in Morocco and Mexico, in an effort to improve operating leverage.

James Ray, President and Chief Executive Officer, said, “2024 was a year of meaningful change for CVG. Over the course of the year, we undertook immediate and decisive actions, including the divestitures of non-strategic assets and businesses, and improvement initiatives that we believe position us for future accretive growth. Even in the face of continued external market headwinds, we believe the improvement initiatives executed in 2024 will unlock significant operational efficiencies that we have already started to benefit from in 2025. Additionally, we were pleased to open our new Morocco facility and we continue to ramp up our facility in Aldama, Mexico.”

Mr. Ray continued, “Moving forward, our team is focused on accelerating the operational momentum we’ve built, driving margin accretive growth through a product-focused, operationally efficient enterprise strategy. With a stronger foundation, and as our key end markets stabilize, we expect that we will continue to strengthen the company’s position in the market and deliver value for our stakeholders.”

Andy Cheung, Chief Financial Officer, added, “CVG delivered results consistent with our adjusted full-year guidance ranges, which reflect the Company’s past portfolio and restructuring actions. We anticipate that the benefits from these strategic efforts will become more apparent in 2025 despite notable end market softening and the slower than expected ramp of new business wins. We believe that these organizational improvements, combined with working capital and inventory reductions driving increased cash generation this year, will greatly improve our ability to continue paying down debt. We have implemented a more focused business strategy and continue to streamline our enterprise cost structure. We expect to see EBITDA growth and margin expansion in 2025 which are reflected in our full year 2025 guidance ranges.”

Consolidated Results from Continuing Operations

Fourth Quarter 2024 Results

Fourth quarter 2024 revenues were $163.3 million compared to $193.7 million in the prior year period, a decline of 15.7%. The decrease in revenues is due primarily to lower sales as a result of a softening in customer demand in our Vehicle Solutions and Electrical Systems segments.

Operating loss for the fourth quarter 2024 was $5.3 million compared to operating income of $4.1 million in the prior year period. Excluding special costs, the fourth quarter of 2024 adjusted operating loss was $4.3 million, down from adjusted operating income of $5.4 million in 2023. The decline in adjusted operating income was driven primarily by the impact of lower sales volumes, unfavorable mix, and operational inefficiencies.

Interest expense was $2.2 million and $2.3 million for the fourth quarter ended December 31, 2024 and 2023, respectively.

Net loss from continuing operations was $35.0 million, or $(1.04) per diluted share, for the fourth quarter 2024 compared to net income of $22.6 million, or $0.67 per diluted share, in the prior year period.

At December 31, 2024, the Company had $50.5 million outstanding borrowings on its revolving credit facility, $26.6 million of cash and $84.4 million availability from revolving credit facilities, resulting in total liquidity of $111.0 million.

Fourth Quarter 2024 Segment Results (Compared with prior-year period, where comparisons are noted)

Vehicle Solutions Segment

Revenues were $91.4 million compared to $107.1 million for the prior year period, a decrease of 14.7% primarily due to lower sales volume as a result of decreased customer demand and the wind-down of certain programs.

Operating income for the fourth quarter 2024 was $1.7 million compared to $3.6 million in the prior year period, a decrease of 52.5%, primarily due to lower customer demand, operational remediation investments, and increased freight costs. The fourth quarter of 2024 adjusted operating income was $2.8 million compared to $4.0 million in the prior year period, a decrease of 30.5%.

Electrical Systems Segment

Revenues were $40.3 million compared to $56.2 million in the prior year period, a decrease of 28.3%, primarily resulting from a global softening in the Construction & Agriculture end-markets.

Operating loss was $1.7 million compared to operating income of $6.7 million, a decrease of 125.2% primarily attributable to lower sales volumes and unfavorable foreign exchange.

Aftermarket and Accessories Segment

Revenues were $31.6 million compared to $30.4 million in the prior year period, an increase of 4.0%, primarily resulting from slightly higher customer demand driving increased volumes.

Operating income was $3.2 million compared to $3.3 million in the prior year period, a decrease of 4.6%. The decrease in operating income was increased manufacturing costs. The fourth quarter of 2024 adjusted operating income was $3.1 million compared to $3.3 million in the prior year period.

Outlook

CVG is providing the following outlook for the full year 2025:

Metric

2025 Outlook ($ millions)

Net Sales

$670 – $710

Adjusted EBITDA

$25 – $30

This outlook reflects, among others, current industry forecasts for North American Class 8 truck builds. According to ACT Research, 2025 North American Class 8 truck production levels are expected to be at 316,000 units. The 2024 actual Class 8 truck builds according to the ACT Research was 332,382 units.

Construction and Agriculture end markets are projected to decline approximately 5-10% in 2025. However, we expect contribution from new business wins outside of Construction and Agriculture end markets in Electrical Systems to soften this decline.

Effective January 1, 2025, the Company announced a new organizational structure designed to enhance alignment with its customers and end markets. Under this new structure, CVG will reorganize its vertical business units into the following three operating divisions and reporting segments: Global Electrical Systems, Global Seating, Trim Systems and Components. As part of this realignment, the Company’s Aftermarket & Accessories business unit will be absorbed in these three segments. Its seating and electrical portfolio will transition to Global Seating and Global Electrical Systems, respectively. Its wiper systems will become part of the newly formed Trim Systems and Components business unit in addition to the trim and components businesses from the prior Vehicle Solutions segment. CVG expects this structure to enhance clarity and focus, with each business unit positioned to deliver on its specific strategic and operational objectives.

GAAP to Non-GAAP Reconciliation

A reconciliation of GAAP to non-GAAP financial measures referenced in this release is included as Appendix A to this release.

Conference Call

A conference call to discuss this press release is scheduled for Tuesday, March 11, 2025, at 8:30 a.m. ET. Management intends to reference the Q4 2024 Earnings Call Presentation posted on our website during the conference call. To participate, dial (800) 549-8228 using conference code 45919. International participants dial (289) 819-1520 using conference code 45919.

This call is being webcast and can be accessed through the “Investors” section of CVG’s website at www.cvgrp.com, where it will be archived for one year.

A telephonic replay of the conference call will be available for a period of two weeks following the call. To access the replay, dial (888) 660-6264 using access code 45919 and international callers can dial (289) 819-1325 using access code 45919.

Company Contact

Andy Cheung Chief Financial Officer CVG IR@cvgrp.com

Commercial Vehicle Group, Inc. and its subsidiaries, is a global provider of systems, assemblies and components to the global commercial vehicle market and the electric vehicle markets. We deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries, and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A of the Securities Act of 1933, as amended. For this purpose, any statements contained herein that are not statements of historical fact, including without limitation, certain statements herein regarding industry outlook, the Company’s expectations for future periods with respect to its plans to improve financial results, the future of the Company’s end markets changes in the Class 8 and Class 5-7 North America truck build rates, performance of the global construction and agricultural equipment business, the Company’s prospects in the wire harness and electric vehicle markets, the Company’s initiatives to address customer needs, organic growth, the Company’s strategic plans and plans to focus on certain segments, competition faced by the Company, volatility in and disruption to the global economic environment, including global supply chain constraints, inflation and labor shortages, tariffs and counter-measures, financial covenant compliance, anticipated effects of acquisitions or divestitures, production of new products, plans for capital expenditures and our results of operations or financial position and liquidity, may be deemed to be forward-looking statements. Without limiting the foregoing, the words “believe”, “anticipate”, “plan”, “expect”, “intend”, “will”, “should”, “could”, “would”, “project”, “continue”, “likely”, and similar expressions, as they relate to us, are intended to identify forward-looking statements. The important factors discussed in “Item 1A – Risk Factors” in the Company’s Annual Report on Form 10-K, among others, could cause actual results to differ materially from those indicated by forward-looking statements made herein and presented elsewhere by management from time to time. Such forward-looking statements represent management’s current expectations and are inherently uncertain. Investors are warned that actual results may differ from management’s expectations. Additionally, various economic and competitive factors could cause actual results to differ materially from those discussed in such forward-looking statements, including, but not limited to, factors which are outside our control.

Any forward-looking statement that we make in this press release speaks only as of the date of such statement, and we undertake no obligation to update any forward-looking statement or to publicly announce the results of any revision to any of those statements to reflect future events or developments. Comparisons of results for current and any prior periods are not intended to express any future trends or indications of future performance, unless specifically expressed as such, and should only be viewed as historical data.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

AVAIL joint venture. Through a joint venture, AZZ owns a non-controlling 40% interest in Avail Infrastructure Solutions with the remaining 60% owned by the Fernweh Group LLC. Avail recently executed a definitive agreement to sell its Electrical Products Group to nVent Electric plc (NYSE: NVT) for $975 million, subject to adjustments. The transaction is expected to close during the first half of the 2025 calendar year. AZZ will continue to own a 40% interest in Avail which will consist of its Industrial Lighting and Welding Solutions businesses.

Use of proceeds. AZZ will use its share of the transaction proceeds to further reduce debt or fund potential M&A activity. The gain on the transaction will be treated as a one-time adjustment to net income and EPS. A reduction in the $16 million to $18 million of joint venture equity income included in AZZ’s fiscal year 2026 guidance is expected to be offset by interest savings. While AZZ is not adjusting its fiscal year 2026 earnings guidance, debt reduction will be higher than the range of $140 million to $160 million provided in their guidance.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Remain on Track. The first full year of NN’s transformation produced significant results, although the improvements were somewhat obscured in the GAAP reported results. With the successful change in the business trajectory, NN remains on track to achieve its 2028 financial goals of $650 million of net sales, with an adjusted EBITDA margin in the 12-13% range.

More Transformation in 2025. Management is not resting on its laurels. 2025 will continue the transformation plan with specific emphasis on improving or eliminating underperforming business, additional costs out, new business wins, and balance sheet improvement through a debt refinance.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Seanergy Maritime Holdings Corp. is a prominent pure-play Capesize shipping company listed in the U.S. capital markets. Seanergy provides marine dry bulk transportation services through a modern fleet of Capesize vessels. The Company’s operating fleet consists of 18 vessels (1 Newcastlemax and 17 Capesize) with an average age of approximately 13.4 years and an aggregate cargo carrying capacity of approximately 3,236,212 dwt. Upon completion of the delivery of the previously announced Capesize vessel acquisition, the Company’s operating fleet will consist of 19 vessels (1 Newcastlemax and 18 Capesize) with an aggregate cargo carrying capacity of approximately 3,417,608 dwt. The Company is incorporated in the Marshall Islands and has executive offices in Glyfada, Greece. The Company’s common shares trade on the Nasdaq Capital Market under the symbol “SHIP”.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fourth quarter financial results. Seanergy Maritime reported fourth quarter adjusted EBITDA and earnings per share (EPS) of $20.4 million and $0.34, respectively, exceeding our estimates of $19.3 million and $0.27. Revenue was modestly above our estimate due to better-than-expected available operating days, while expenses were marginally lower-than-expected, driven by operational efficiencies for voyage and vessel expenses. Operating income was $10.7 million compared to our estimate of $10.1 million.

2025 market outlook. Capesize rates fell in early 2025 due to an increase in the effective supply of vessels caused by low congestion in ports and smaller vessels taking on cargo typically reserved for the Capesize fleet. However, Capesize market rates have since rebounded and are expected to stay relatively steady throughout 2025. Limited new vessel orders and deliveries, increasing environmental regulations, and rising iron ore and bauxite exports are supporting Cape vessel rates amid a broader downturn in the dry-bulk market.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Year of Transformation. Management highlighted its first full year of transformation, as the Company upgraded leadership positions and added to its Stamped Products, Electrical, and Medical teams. They also secured new business to offset rationalized business and create a path to y-o-y growth, increased gross margins, and decreased leverage to name a few actions. Lastly, the underperforming plants are expected to generate positive EBITDA in the new year compared to a negative $11.5 million last year.

New Business Wins. The Company had $73 million of new business wins for the fiscal year, surpassing the previous year of $63 million. As for 2025, the Company has $13 million in new wins year-to-date and remains on pace towards its guidance of $60-$70 million in new wins for the year. These wins are expected to soon ramp into Company sales as well, with roughly $21 million of new business expected to launch in Q1 2025 across multiple plants and countries.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.