Delivered GrossMargin of 15%, Expansion of 250Basis Points OperatingCashFlowof$8.5 Million andAdjustedFreeCashFlowof$7.9Million Strong Order Intake Driven by Operational Flexibility, Reaffirmed Full Year Guidance

CHICAGO, Aug. 04, 2025 (GLOBE NEWSWIRE) — FreightCar America, Inc. (NASDAQ: RAIL) (“FreightCar America” or the “Company”), a diversified manufacturer and supplier of railroad freight cars, railcar parts and components, today reported results for the second quarter ended June 30, 2025.

SecondQuarter 2025Highlights

Revenues of $118.6 million, compared to $147.4 million in the second quarter of 2024, with railcar deliveries of 939 units compared to 1,159 units in the prior year period

Gross margin of 15.0% with gross profit of $17.8 million, compared to gross margin of 12.5% with gross profit of $18.4 million in the second quarter of 2024

Net income of $11.7 million, or $0.34 per share, and Adjusted net income of $3.8 million, or $0.11 per share, reflecting a $51.9 million benefit from a valuation allowance release, partially offset by a $47.6 million non-cash adjustment from the change in warrant liability due to share price appreciation

Adjusted EBITDA was $10.0 million, representing a margin of 8.4%, compared to $12.1 million and a margin of 8.2% in the second quarter of 2024

Received new orders for 1,226 railcars within the quarter valued at $106.9 million

Ended the quarter with a backlog of 3,624 units valued at $316.9 million, up approximately 300 units from prior quarter, reflecting strong order activity and healthy demand

“In the second fiscal quarter, we delivered on our commercial excellence initiatives across the business, supported by strong order intake and healthy customer demand,” said Nick Randall, President and Chief Executive Officer of FreightCar America. “We increased utilization across our four production lines, delivered improved productivity, and benefited from a richer product mix from disciplined pricing. Our ability to remain agile and responsive to customer needs continues to be a key differentiator, particularly in rebuilds and conversions, enabling us to capture meaningful opportunities in a dynamic market.”

Randall continued, “While broader market uncertainty earlier in the year delayed some order activity, we believe the underlying fundamentals point to a meaningful replacement cycle ahead. As that takes shape, our agile manufacturing presence positions us well to capture incremental demand and grow our share. At the same time, we continue to advance our growth strategy by investing in our tank car capabilities, which we expect will strengthen our cost position and support long-term value creation.”

FiscalYear2025 Outlook

The Company has reaffirmed outlook for fiscal year 2025 as follows:

Fiscal2025 Outlook

Year-over-Year GrowthatMidpoint

Railcar Deliveries

4,500 – 4,900 Railcars

7.7%

Revenue

$530 – $595 million

0.6%

AdjustedEBITDA1

$43 – $49 million

7.0%

1. The Company does not provide a reconciliation of forward-looking Adjusted EBITDA guidance due to the inherent difficulty in forecasting and quantifying adjustments necessary to calculate such non-GAAP measure without unreasonable effort. Material changes to such adjustments, including warrant liability and non-core operating items, could affect future GAAP results.

Mike Riordan, Chief Financial Officer of FreightCar America, added, “We’re pleased to reaffirm our full-year guidance, supported by strong margin performance and continued commercial execution across the business, with order activity supporting our healthy backlog. In addition, this quarter marked our fifth consecutive quarter of positive operating cash flow, reflecting the consistency and sustainability of our cash generation engine. Our focus on working capital discipline and operational efficiency has positioned us well to maintain momentum and invest in growth opportunities as we deliver strong performance in the second half of the year.”

SecondQuarter 2025 ConferenceCall&Webcast Information

The Company will host a conference call and live webcast on Tuesday, August 5, at 11:00 a.m. (Eastern Time) to discuss its second quarter 2025 financial results. FreightCar America invites shareholders and other interested parties to listen to its financial results conference call. Teleconference details are as follows:

An audio replay of the conference call will be available beginning at 3:00 p.m. (Eastern Time) on Tuesday, August 5, 2025, until 11:59 p.m. (Eastern Time) on Tuesday, August 19, 2025. To access the replay, please dial (844) 512-2921 or (412) 317-6671. The replay passcode is 13754875. An archived version of the webcast will also be available on the FreightCar America Investor Relations website.

AboutFreightCarAmerica

FreightCar America, headquartered in Chicago, Illinois, is a leading designer, producer and supplier of railroad freight cars, railcar parts and components. We also specialize in railcar repairs, complete railcar rebody services and railcar conversions that repurpose idled rail assets back into revenue service. Since 1901, our customers have trusted us to build quality railcars that are critical to economic growth and instrumental to the North American supply chain. To learn more about FreightCar America, visit www.freightcaramerica.com.

Forward-LookingStatements

This press release contains statements relating to our expected financial performance, financial condition, and/or future business prospects, events and/or plans that are “forward-looking statements” as defined under the Private Securities Litigation Reform Act of 1995. Forward-looking statements represent our estimates and assumptions only as of the date of this press release. Our actual results may differ materially from the results described in or anticipated by our forward-looking statements due to certain risks and uncertainties. These risks and uncertainties relate to, among other things, the cyclical nature of our business; adverse geopolitical, economic and market conditions, including inflation; material disruption in the movement of rail traffic for deliveries; fluctuating costs of raw materials, including steel and aluminum; delays in the delivery of raw materials; our ability to maintain relationships with our suppliers of railcar components; our reliance upon a small number of customers that represent a large percentage of our sales; the variable purchase patterns of our customers and the timing of completion; delivery and customer acceptance of orders; the highly competitive nature of our industry; the risk of lack of acceptance of our new railcar offerings; potential unexpected changes in laws, rules, and regulatory requirements, including tariffs and trade barriers (including recent United States tariffs imposed or threatened to be imposed on China, Canada, Mexico and other countries and any retaliatory actions taken by such countries); and other competitive factors. The factors listed above are not exhaustive. New factors emerge from time to time that may cause our business not to develop as we expect, and it is not possible for us to predict all of them. We expressly disclaim any duty to provide updates to any forward-looking statements made in this press release, whether as a result of new information, future events or otherwise.

Non-GAAPFinancialMeasures

This press release includes measures not derived in accordance with generally accepted accounting principles (“GAAP”), such as EBITDA, Adjusted EBITDA, Adjusted net income (loss), Adjusted EPS, Free cash flow and Adjusted free cash flow. These non-GAAP measures should not be considered in isolation or as a substitute for any measure derived in accordance with GAAP and may also be inconsistent with similar measures presented by other companies. Reconciliations of these measures to the applicable most closely comparable GAAP measures, and reasons for the Company’s use of these measures, are presented in the attached pages.

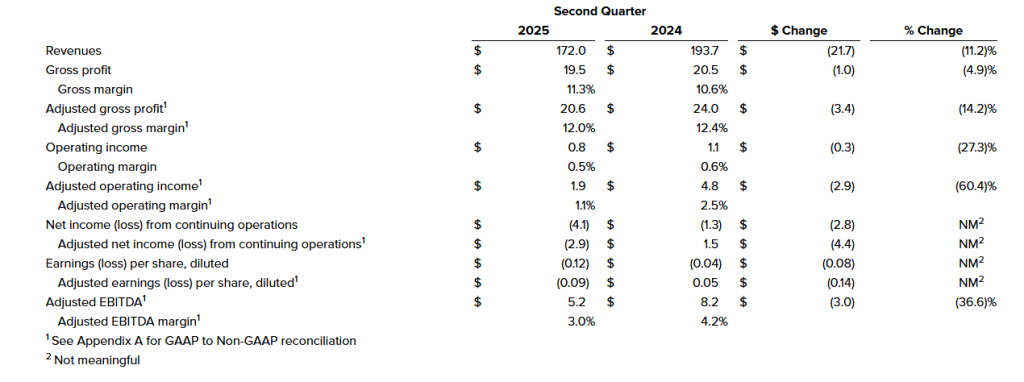

Second quarter sales of $172 million, EPS of $(0.12), Adjusted EBITDA of $5.2 million Continued strong free cash flow generation Updates full year 2025 guidance

NEW ALBANY, Ohio, Aug. 04, 2025 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI), a diversified industrial products and services company, today announced financial results for its second quarter ended June 30, 2025.

Second Quarter 2025 Highlights(Results from Continuing Operations; compared with prior year, where comparisons are noted)

Revenues of $172.0 million, down 11.2%, primarily due to softening in global demand.

Operating income of $0.8 million, adjusted operating income of $1.9 million, down compared to operating income of $1.1 million and adjusted operating income of $4.8 million. The decrease in operating income was driven primarily by lower sales volumes.

Net loss from continuing operations of $4.1 million, or $(0.12) per diluted share and adjusted net loss of $2.9 million, or $(0.09) per diluted share, compared to net loss from continuing operations of $1.3 million, or $(0.04) per diluted share and adjusted net income of $1.5 million, or $0.05 per diluted share.

Adjusted EBITDA of $5.2 million, down 36.6%, with an adjusted EBITDA margin of 3.0%, down from 4.2%.

Free cash flow of $17.3 million, up $16.5 million, due to better working capital management. Net debt decreased $31.8 million compared to the year end 2024 level.

Gross margin expansion of 80 basis points versus Q1 2025 due to operational efficiency improvements.

James Ray, President and Chief Executive Officer, said, “Despite continued macroeconomic volatility, particularly a softening in Construction and Agriculture and Class 8 end markets and ongoing concerns around tariff impacts, we were pleased with continued momentum in our second quarter results, which were highlighted by strong free cash generation. During the quarter, we made progress in implementing operational improvements and right sizing our manufacturing footprint, which drove sequential gross margin improvement for the second consecutive quarter. Additionally, as part of our efforts to preserve margin performance, we are continuing our efforts to further reduce our targeted SG&A levels, and we are having constructive negotiations with customers as it relates to mitigating tariff impacts.”

Mr. Ray continued, “We are encouraged by the improved performance in our Global Electrical Systems segment, driven by new business wins outside of the Construction and Agriculture end markets, which continue to see lower demand. The Global Electrical Systems segment also saw margin expansion despite revenues being flat year-over-year. Across our enterprise, we remain focused on execution, delivery, and driving operational efficiency, while managing the potential impact of trade policy.”

Andy Cheung, Chief Financial Officer, added, “We were pleased to see continued strong free cash generation in the quarter, as well as continued improvement in gross margin, as the benefits of our strategic initiatives take hold. Given our successful working capital initiatives, we are raising our free cash outlook to at least $30 million for the full fiscal year. Continued free cash generation and debt paydown remain key focus areas moving forward. During the quarter, we completed the refinancing of our credit facilities, which will further benefit our strategic initiatives and provide increased financial flexibility as we look to drive further cost reductions, margin improvement, and overall operational efficiency.”

Second Quarter Financial Results from Continuing Operations (amounts in millions except per share data and percentages)

Consolidated Results from Continuing Operations

Second Quarter 2025 Results

Second quarter 2025 revenues were $172.0 million, compared to $193.7 million in the prior year period, a decrease of 11.2%. The overall decrease in revenues was due to lower sales as a result of a softening in customer demand across all segments.

Operating income in the second quarter 2025 was $0.8 million compared to $1.1 million in the prior year period. The decrease in operating income was attributable to the impact of lower sales volumes. Second quarter 2025 adjusted operating income was $1.9 million, compared to $4.8 million in the prior year period.

Interest associated with debt and other expenses was $2.3 million and $2.4 million for the second quarter 2025 and 2024, respectively.

Net loss from continuing operations was $4.1 million, or $(0.12) per diluted share, for the second quarter 2025 compared to net loss of $1.3 million, or $(0.04) per diluted share, in the prior year period. Second quarter 2025 adjusted net loss from continuing operations was $2.9 million, or $(0.09) per diluted share, compared to adjusted net income of $1.5 million, or $0.05 per diluted share.

On June 30, 2025, the Company had $30.3 million of outstanding borrowings on its U.S. revolving credit facility and $4.2 million outstanding borrowings on its China credit facility, $45.3 million of cash and $90.6 million of availability from the credit facilities (subject to customary borrowing base and other conditions), resulting in total liquidity of $135.9 million.

Second Quarter 2025 Segment Results

Global Seating Segment

Revenues were $74.5 million compared to $82.4 million for the prior year period, a decrease of 9.6%, due to lower sales volume as a result of decreased customer demand.

Operating income was $2.7 million, compared to $2.1 million in the prior year period, an increase of 29.1%, primarily attributable to lower SG&A expenses. Second quarter 2025 adjusted operating income was $3.1 million compared to $2.9 million in the prior year period.

Global Electrical Systems Segment

Revenues were $53.6 million compared to $53.6 million in the prior year period, essentially flat.

Operating income was $0.7 million compared to an operating loss of $0.5 million in the prior year period. The increase in operating income was primarily attributable to lower salary expense and lower restructuring costs in the current period compared to the prior period. Second quarter 2025 adjusted operating income was $1.2 million compared to $0.8 million in the prior year period.

Trim Systems and Components Segment

Revenues were $43.9 million compared to $57.6 million in the prior year period, a decrease of 23.8%, primarily as a result of decreased customer demand.

Operating income was $0.1 million compared to $2.3 million in the prior year period, a decrease of $2.2 million. The decrease in operating income was primarily attributable to lower sales volumes. Second quarter 2025 adjusted operating income was $0.3 million compared to $4.0 million in the prior year period.

Outlook

CVG updated the Company’s outlook for the full year 2025, based on current market conditions:

Metric

Prior 2025 Outlook ($ millions)

2025 Outlook ($ millions)

Net Sales

$660- $690

$650- $670

Adjusted EBITDA

$22 – $27

$21 – $25

Free Cash Flow

> $20

> $30

This outlook reflects, among others, current industry forecasts for North America Class 8 truck builds. According to ACT Research, 2025 North American Class 8 truck production levels are expected to be at 252,000 units. The 2024 actual Class 8 truck builds according to the ACT Research was 332,372 units.

Construction and Agriculture end markets are projected to decline approximately 5-15% in 2025. However, we expect the contribution from new business wins outside of Construction and Agriculture end markets in Electrical Systems to soften this decline.

GAAP to Non-GAAP Reconciliation

A reconciliation of GAAP to non-GAAP financial measures referenced in this release is included as Appendix A to this release.

Conference Call

A conference call to discuss this press release is scheduled for Tuesday, August 5, 2025, at 8:30 a.m. ET. Management intends to reference the Q2 2025 Earnings Call Presentation during the conference call. To participate, dial (800) 549-8228 using conference code 72110. International participants dial (289) 819-1520 using conference code 72110.

This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com, where it will be archived for one year.

A telephonic replay of the conference call will be available for a period of two weeks following the call. To access the replay, dial (888) 660-6264 using access code 72110#.

Company Contact Andy Cheung Chief Financial Officer CVG IR@cvgrp.com

Investor Relations Contact Ross Collins or Stephen Poe Alpha IR Group CVGI@alpha-ir.com

About CVG

CVG is a global provider of systems, assemblies and components to the global commercial vehicle market and the electric vehicle market. We deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Forward-Looking Statements

This press release contains forward-looking statements that are subject to risks and uncertainties. These statements often include words such as “believe”, “anticipate”, “plan”, “expect”, “intend”, “will”, “should”, “could”, “would”, “project”, “continue”, “likely”, and similar expressions. In particular, this press release may contain forward-looking statements about the Company’s expectations for future periods with respect to its plans to improve financial results, the future of the Company’s end markets, changes in the Class 8 and Class 5-7 North America truck build rates, performance of the global construction and agricultural equipment business, the Company’s prospects in the wire harness and electric vehicle markets, the Company’s initiatives to address customer needs, organic growth, the Company’s strategic plans and plans to focus on certain segments, competition faced by the Company, volatility in and disruption to the global economic environment including global supply chain constraints, inflation and labor shortages, tariffs and counter-measures, financial covenant compliance, anticipated effects of acquisitions, production of new products, plans for capital expenditures, and the Company’s financial position or other financial information. These statements are based on certain assumptions that the Company has made in light of its experience as well as its perspective on historical trends, current conditions, expected future developments and other factors it believes are appropriate under the circumstances. Actual results may differ materially from the anticipated results because of certain risks and uncertainties, including those included in the Company’s filings with the SEC. There can be no assurance that statements made in this press release relating to future events will be achieved. The Company undertakes no obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time. All subsequent written and oral forward-looking statements attributable to the Company or persons acting on behalf of the Company are expressly qualified in their entirety by such cautionary statements.

Other Information

Throughout this document, certain numbers in the tables or elsewhere may not sum due to rounding. Rounding may have also impacted the presentation of certain year-on-year percentage changes.

WEST CHICAGO, Ill., July 31, 2025 /PRNewswire/ — Titan International, Inc. (NYSE: TWI) (“Titan” or the “Company”), a leading global manufacturer of off-highway wheels, tires, assemblies, and undercarriage products, today reported financial results for the second quarter ended June 30, 2025. The full earnings release including a reconciliation of GAAP to Non-GAAP figures can be found in the investor relations section of the Company’s website at https://ir.titan-intl.com/news-and-events/news-releases/default.aspx.

Q2 2025 Key Figures

Revenues of $461 million

Gross margin of 15%

Adjusted EBITDA of $30 million

Free Cash Flow of $4 million

Paul Reitz, President and Chief Executive Officer, commented, “Our One Titan team continued to execute, enabling the Company to report revenues and Adjusted EBITDA within our guidance range, as well as positive free cash flow for the quarter. Overall conditions in our end markets are currently defined primarily by the impact of higher interest rates and tariff uncertainty. On a longer-term basis, we are encouraged by the broad support the recently-passed legislation included for farmers.”

Mr. Reitz continued, “Among the highlights from our second quarter, we were able to maintain gross and EBITDA margins which continued to be meaningfully above where they were during the last cyclical trough. We also continued to focus on expanding our reach via our one-stop-shop strategy and our focus on innovation, and we expect those efforts to help drive growth when broad-based industry demand resumes. In the near term, we remain confident that wheel and tire inventories throughout the chain are reaching levels where the only path forward is up. We are well-positioned as a leader in our industry and fully expect to see improving financial results as macro tailwinds begin to emerge.”

Company Outlook

David Martin, Chief Financial Officer, added, “We expect third quarter sales to be between $450 million and $475 million with Adjusted EBITDA between $25 million and $30 million, which are both improvements compared to the third quarter of 2024.”

About Titan

Titan International, Inc. (NYSE: TWI) is a leading global manufacturer of off-highway wheels, tires, assemblies, and undercarriage products. Headquartered in West Chicago, Illinois, the Company globally produces a broad range of products to meet the specifications of original equipment manufacturers (OEMs) and aftermarket customers in the agricultural, earthmoving/construction, and consumer markets. For more information, visit www.titan-intl.com.

Safe Harbor Statement

This press release contains forward-looking statements. These forward-looking statements are covered by the safe harbor for “forward-looking statements” provided by the Private Securities Litigation Reform Act of 1995. The words “believe,” “expect,” “anticipate,” “plan,” “would,” “could,” “potential,” “may,” “will,” and other similar expressions are intended to identify forward-looking statements, which are generally not historical in nature. These forward-looking statements are based on our current expectations and beliefs concerning future developments and their potential effect on us. Although we believe the assumptions upon which these forward-looking statements are based are reasonable, these assumptions are subject to significant risks and uncertainties, and are subject to change based on various factors, some of which are beyond Titan International, Inc.’s control. As a result, any of these assumptions could prove to be inaccurate and the forward-looking statements based on these assumptions could be incorrect. The matters discussed in these forward-looking statements are subject to risks, uncertainties, and other factors that could cause actual results and trends to differ materially from those made, projected, or implied in or by the forward-looking statements depending on a variety of uncertainties or other factors including, but not limited to, the effect of a recession on the Company and its customers and suppliers; changes in the Company’s end-user markets into which the Company sells its products as a result of domestic and world economic or regulatory influences or otherwise; changes in the marketplace, including new products and pricing changes by the Company’s competitors; the Company’s ability to maintain satisfactory labor relations; unfavorable outcomes of legal proceedings; the Company’s ability to comply with current or future regulations applicable to the Company’s business and the industry in which it competes or any actions taken or orders issued by regulatory authorities; availability and price of raw materials; levels of operating efficiencies; the effects of the Company’s indebtedness and its compliance with the terms thereof; changes in the interest rate environment and their effects on the Company’s outstanding indebtedness; unfavorable product liability and warranty claims; actions of domestic and foreign governments, including the imposition of additional tariffs; geopolitical and economic uncertainties relating to the countries in which the Company operates or does business; risks associated with acquisitions, including difficulty in integrating operations and personnel, disruption of ongoing business, and increased expenses; results of investments; the effects of potential processes to explore various strategic transactions, including potential dispositions; fluctuations in currency translations; risks associated with environmental laws and regulations; risks relating to our manufacturing facilities, including that any of our material facilities may become inoperable; risks relating to financial reporting, internal controls, tax accounting, and information systems; and the other risks and factors detailed in the Company’s periodic reports filed with the Securities and Exchange Commission, including the disclosures under “Risk Factors” in those reports. These forward-looking statements are made only as of the date hereof. The Company cautions that any forward-looking statements included in this press release are subject to a number of risks and uncertainties, and the Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, changed circumstances or future events, or for any other reason, except as required by law.

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or “the Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries, today announced that it has been awarded a follow-on order to produce mission-critical hardware for the MK48 Mod 7 Heavyweight Torpedo program valued at approximately $25.5 million.

Matthew J. Malone, President and CEO, commented, “This follow-on award underscores our competitive position as a trusted supplier of mission-critical components to the U.S. Navy and allied defense programs. It reflects the strength of our engineering capabilities, highly skilled and engaged workforce, and precision manufacturing expertise. We’ve made targeted investments to improve operational efficiency to fulfill current and future demand, positioning us to drive recurring revenue, expand margins, and deliver long-term value to shareholders.”

Graham manufactures and tests the alternators and regulators for the MK48 Mod 7 Heavyweight Torpedo through its Barber-Nichols subsidiary in Arvada, CO.

About Graham Corporation Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy, & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “expects,” “future,” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, profitability of future projects and the business, its ability to deliver to plan, its ability to secure future projects and applications, are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

CHARLOTTE, N.C., July 24, 2025 (GLOBE NEWSWIRE) — NN, Inc. (NASDAQ: NNBR), a global diversified industrial company that engineers and manufactures high-precision components and assemblies, announced today that it will release its second quarter 2025 financial results for the period ended June 30th, 2025, after the close of the market on Wednesday, August 6th, 2025. The Company will hold a related conference call on Thursday, August 7th, 2025, at 9:00 a.m. E.T. Participants on the call are asked to register five to ten minutes prior to the scheduled start time by dialing 1-888-999-3182 and from outside the U.S. at 1-848-280-6330.

The conference call will be webcast simultaneously and in its entirety through the NN, Inc. Investor Relations website. Shareholders, media representatives and others may participate in the webcast by registering through the Investor Relations section on the company’s website at https://investors.nninc.com/.

For those who are unavailable to listen to the live call, a replay will be available shortly after the call on NN’s website through August 8th, 2026.

About NN, Inc. NN, Inc., a global diversified industrial company, combines advanced engineering and production capabilities with in-depth materials science expertise to design and manufacture high-precision components and assemblies for a variety of markets on a global basis. Headquartered in Charlotte, North Carolina, NN has facilities in North America, Europe, South America, and Asia. For more information about the company and its products, please visit www.nninc.com.

Investor Relations: Joe Caminiti or Stephen Poe NNBR@alpha-ir.com 312-445-2870

CHARLOTTE, N.C., July 22, 2025 (GLOBE NEWSWIRE) — NN, Inc. (NASDAQ: NNBR), a global diversified industrial company that engineers and manufactures high-precision components and assemblies, today announced Timothy Erro has joined as its new Vice President and Chief Commercial Officer. In this position, Mr. Erro will lead NN’s global commercial team and report directly to Harold Bevis, President and CEO.

NN has a successful new business program and as a function of this early success, the Company is announcing a commitment to expand this program with this announced leadership change. NN has shown strong initial results in the last two years.

Approximately $160 million of new business wins since launching the initiative in 2023, with success primarily in the Company’s traditional markets and emerging success in electrical and medical end markets.

NN’s new business pipeline remains robust at more than $700 million across all products and targeted growth areas.

NN is revising and increasing its overall new business objectives:

Increasing its targets and the pace for achieving new wins, specifically in electrical and medical markets;

Setting higher annual award goals; and

Strategically expanding product offerings and solutions.

Tim Erro has led a highly successful global team and program, and has overseen a significant amount of business growth and new wins, including:

Leading a global team effort that has averaged more than $50 million per year in new business wins of electrical products, more than three times the historical annual new business wins generated by NN’s Power Solutions division; and

Entering eight new markets, through which his teams have added many new customers in pursuit of electrical products and systems that fit his prior company’s operating assets and know-how.

Harold Bevis, President and Chief Executive Officer of NN commented, “Tim brings an outstanding track record with him and is currently leading one of the most successful new wins programs in the electrical industry globally. He is an expert at entering new markets and expanding market share in existing markets. He has a great blend of technical and commercial expertise, operations know-how, and executive leadership experience, all of which align with our commercial strategy and will help take NN’s growth program to the next level. He and I have worked together in the past, where he led a tremendously successful global program focused on electrical and electronic products at a much larger scale than our current program. His track record of developing and leading high-performing sales organizations will help us achieve our goals faster.”

Erro has more than 30 years of experience with electrical and electronic products across a wide variety of end markets and global geographies, including:

Mr. Bevis concluded, “From our past experience together, I can attest that Tim will increase our focus, pace, hit rates, and the accountability of our global commercial team along our chosen paths. He will strengthen our team and immediately bring in new talent. As part of our enhanced commercial efforts, we especially want to grow at a more accelerated pace in electrical products and medical products.”

Tim Erro commented, “I am excited to join NN’s leadership team and am eager to put my background and industry experience to work in strengthening NN’s commercial results and our global team. Our engineering and production capabilities are unique and highly valued in the market, and I look forward to working with the talented team at NN to set even higher goals and achieve them with consistency. This is going to be an exciting next phase for NN, and I plan to bring in additional experienced veterans to lead the way with our customers.”

Mr. Erro brings an extensive commercial and operations background with him. Prior to joining NN, he served as VP of Global Sales and New Business Development for Commercial Vehicle Group, Inc., and has had a focused set of sales and operations roles at Aptiv (formerly Delphi Automotive), Leoni Wiring Systems, General Motors, and United Technologies Automotive. A highlight of his engineering tenure includes leading the design and execution of fully functional concept vehicles for major global auto shows, showcasing advanced technology trends and innovations. Mr. Erro also proudly served 12 years in the US Navy reserves. He holds a Bachelor of Science in Mechanical Engineering from Youngstown State University.

About NN, Inc.

NN, Inc., a global diversified industrial company, combines advanced engineering and production capabilities with in-depth materials science expertise to design and manufacture high-precision components and assemblies for a variety of markets on a global basis. Headquartered in Charlotte, North Carolina, NN has facilities in North America, Europe, South America, and Asia. For more information about the company and its products, please visit www.nninc.com.

Investor Relations: Joe Caminiti or Stephen Poe, Investors NNBR@alpha-ir.com 312-445-2870

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries, announced that it will release its first quarter fiscal year 2026 financial results before financial markets open on Tuesday, August 5, 2025.

The Company will host a conference call and webcast to review its financial and operating results, strategy, and outlook. A question-and-answer session will follow.

First Quarter Fiscal Year 2026 Financial Results Conference Call

Tuesday, August 5, 2025 11:00 a.m. Eastern Time Phone: (412) 317-5195 Internet webcast link and accompanying slide presentation: ir.grahamcorp.com

A telephonic replay will be available from 3:00 p.m. ET on the day of the teleconference through Tuesday, August 12, 2025. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 10201479 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

ABOUT GRAHAM CORPORATION

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space, industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Refinancing extends maturity to 2030 and increases flexibility

NEW ALBANY, OHIO, June 30, 2025 (GLOBE NEWSWIRE) — Commercial Vehicle Group (together with its subsidiaries, the “Company” or “CVG”) (NASDAQ: CVGI), a diversified industrial products and services company, today announced that on June 27, 2025 it had closed on $210 million in senior secured credit facilities, consisting of (i) a $95 million senior secured term loan facility (the “Term Loan”) with TCW Asset Management Company LLC (together with certain of its affiliates, the “TCW Group”), as agent, and (ii) a $115 million senior secured asset-based revolving credit facility (the “ABL Facility” and together with the Term Loan, the “Senior Secured Credit Facilities”) with Bank of America, N.A., as agent. The ABL Facility amended and restated the Company’s existing senior secured revolving credit facility with Bank of America, N.A., as agent (the “Existing Facility”), and a portion of the proceeds of the Senior Secured Credit Facilities was used to refinance outstanding obligations under the Existing Facility in an aggregate principal amount of $120,100,000.

Andy Cheung, Chief Financial Officer, said, “We are pleased to announce the successful refinancing of our debt facilities maturing in 2027, which marks an important milestone as we continue to advance our strategic operational initiatives. The new facilities provide a long runway of funding certainty and increased financial flexibility as we look to drive further cost reductions, margin improvement, and overall operational efficiency. Moving forward, we remain committed to deleveraging the balance sheet through free cash generation and disciplined debt paydown.”

Term Loan of $95 million

Obligations under the Term Loan will mature on June 27, 2030.

The Term Loan will have tiered interest costs based on the consolidated total leverage ratio ranging from SOFR plus 8.75% with a leverage ratio < 3.50x to SOFR plus 10.75% with a leverage ratio > 6.25x. The SOFR floor is 2.00%. The initial interest rate payable under the Term Loan is SOFR plus 9.75%.

Until June 28, 2028, voluntary prepayments of the Term Loan are subject to a premium, calculated as a percentage of the obligations so prepaid under the Term Loan, equal to (x) from June 27, 2025 until June 27, 2027, 4.00%, (y) from June 28, 2026 until June 27, 2028, 2.00% and (z) thereafter, none. The Term Loan is also subject to an excess cash flow sweep and certain other customary mandatory prepayment requirements.

The Term Loan will be subject to certain financial covenants:

a consolidated total leverage ratio covenant, tested quarterly, which will be initially set at 7.25x, with step-downs to 6.50x at December 31, 2025, 6.00x at March 31, 2026, 5.25x at June 30, 2026, and additional quarterly 0.25x step-downs until a ratio of 4.00x applicable from and after September 30, 2027.

a maximum consolidated capital expenditure covenant, capped at $20 million in any fiscal year, and a sublimit of $10 million for foreign capital expenditures.

a 30-day rolling minimum average liquidity requirement of $15 million.

ABL Facility of $115 million

Obligations under the ABL Facility will mature on June 27, 2030, springing to the date that is 91 days prior to the maturity of the Term Loan.

The initial principal amount of the ABL Facility is $115 million, subject to availability under a borrowing base based on the Company’s US and UK inventory and receivables. The ABL Facility comprises of a US subfacility in an initial principal amount of $100 million (the “US Subfacility”) and a UK subfacility in an initial principal amount of $15 million (the “UK Subfacility”), in each case subject to availability under their respective borrowing bases. The US Subfacility further has a FILO tranche in a principal amount of $12.5 million, subject to availability under its borrowing base.

The ABL Facility will be available in US Dollars, Pounds Sterling and Euros, and borrowings will accrue interest at SOFR, SONIA or EURIBOR, with margins based on average daily availability ranging from 1.50% if average daily availability > $50 million to 2.00% if average daily availability < $30 million. The FILO tranche will accrue interest at a 1% higher rate. The Company is also required to pay an unused line fee of 0.25% on any unutilized commitments under the ABL Facility.

The Company will be required to comply with a maximum fixed charge coverage ratio of 1.00x, tested quarterly, during any trigger period. Such period shall be triggered upon availability dropping below the greater of 10% of the line cap and $10 million, and such period shall end upon availability exceeding this threshold for 30 consecutive days.

Warrants

In connection with the financing, TCW Group affiliates received five-year warrants for the purchase of up to 3,934,776 shares of the company’s common stock, issued in two equal tranches. The tranches have an exercise price of $1.58 and $2.07, respectively. Until the fourth anniversary after issuance, the Company has the right to repurchase up to 50% of each tranche of warrants at a price equal to $1.40 or $1.00, respectively, above the applicable exercise price. Upon a refinancing of the new credit agreement, the holders can require the Company to repurchase up to 50% of each tranche at a price equal to the stock price of the common stock at the time of repurchase less the exercise price. The warrants contain customary anti-dilution adjustments. The Company has provided the holders with certain information and registration rights, including agreeing to file a registration statement within 45 days to register the resale of the shares underlying the warrants.

The Company will file a Current Report on Form 8-K with the United States Securities Exchange Commission that will contain further details regarding the terms of the of the transactions.

Company Contact Andy Cheung Chief Financial Officer CVG IR@cvgrp.com

Investor Relations Contact Ross Collins or Stephen Poe Alpha IR Group CVGI@alpha-ir.com

About CVG

CVG is a global provider of systems, assemblies and components to the global commercial vehicle market and the electric vehicle market. We deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Forward-Looking Statements

This press release contains forward-looking statements that are subject to risks and uncertainties. These statements often include words such as “believe”, “anticipate”, “plan”, “expect”, “intend”, “will”, “should”, “could”, “would”, “project”, “continue”, “likely”, and similar expressions. In particular, this press release may contain forward-looking statements about the Company’s expectations for future periods with respect to its plans to improve financial results, the future of the Company’s end markets, changes in the Class 8 and Class 5-7 North America truck build rates, performance of the global construction and agricultural equipment business, the Company’s prospects in the wire harness, and electric vehicle markets, the Company’s initiatives to address customer needs, organic growth, the Company’s strategic plans and plans to focus on certain segments, competition faced by the Company, volatility in and disruption to the global economic environment and the Company’s financial position or other financial information. These statements are based on certain assumptions that the Company has made in light of its experience as well as its perspective on historical trends, current conditions, expected future developments and other factors it believes are appropriate under the circumstances. Actual results may differ materially from the anticipated results because of certain risks and uncertainties, including those included in the Company’s filings with the SEC. There can be no assurance that statements made in this press release relating to future events will be achieved. The Company undertakes no obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time. All subsequent written and oral forward-looking statements attributable to the Company or persons acting on behalf of the Company are expressly qualified in their entirety by such cautionary statements.

FORT WORTH, Texas, June 25, 2025 /PRNewswire/ — AZZ Inc. (NYSE: AZZ), the leading independent provider of hot-dip galvanizing and coil coating solutions, today announced it will conduct a conference call to review the financial results for the first quarter fiscal year 2026 at 11:00 a.m. ET on Thursday, July 10, 2025. The Company will issue a press release reporting first quarter financial results after the market closes on July 9, 2025.

Conference Call Details Interested parties can access the conference call by dialing (844) 855-9499 or (412) 317-5497 (international). A webcast of the call will be available on the Company’s Investor Relations page at http://www.azz.com/investor-relations.

A replay of the call will be available at (877) 344-7529 or (412) 317-0088 (international), replay access code: 2234808, through July 17, 2025, or by visiting http://www.azz.com/investor-relations for the next 12 months.

About AZZ Inc. AZZ Inc. is the leading independent provider of hot-dip galvanizing and coil coating solutions to a broad range of end-markets. Collectively, our business segments provide sustainable, unmatched metal coating solutions that enhance the longevity and appearance of buildings, products and infrastructure that are essential to everyday life. For more information, please refer to www.azz.com.

Safe Harbor Statement Certain statements herein about our expectations of future events or results constitute forward-looking statements for purposes of the safe harbor provisions of The Private Securities Litigation Reform Act of 1995. You can identify forward-looking statements by terminology such as “may,” “could,” “should,” “expects,” “plans,” “will,” “might,” “would,” “projects,” “currently,” “intends,” “outlook,” “forecasts,” “targets,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue,” or the negative of these terms or other comparable terminology. Such forward-looking statements are based on currently available competitive, financial, and economic data and management’s views and assumptions regarding future events. Such forward-looking statements are inherently uncertain, and investors must recognize that actual results may differ from those expressed or implied in the forward-looking statements. Forward-looking statements speak only as of the date they are made and are subject to risks that could cause them to differ materially from actual results. Certain factors could affect the outcome of the matters described herein. This press release may contain forward-looking statements that involve risks and uncertainties including, but not limited to, changes in customer demand for our manufactured solutions, including demand by the construction markets, the industrial markets, and the metal coatings markets. We could also experience additional increases in labor costs, components and raw materials including zinc and natural gas, which are used in our hot-dip galvanizing process, paint used in our coil coating process; supply-chain vendor delays; customer requested delays of our manufactured solutions; delays in additional acquisition opportunities; an increase in our debt leverage and/or interest rates on our debt, of which a significant portion is tied to variable interest rates; availability of experienced management and employees to implement AZZ’s growth strategy; a downturn in market conditions in any industry relating to the manufactured solutions that we provide; economic volatility, including a prolonged economic downturn or macroeconomic conditions such as inflation or changes in the political stability in the United States and other foreign markets in which we operate; tariffs; acts of war or terrorism inside the United States or abroad; and other changes in economic and financial conditions. AZZ has provided additional information regarding risks associated with the business, including in Part I, Item 1A. Risk Factors, in AZZ’s Annual Report on Form 10-K for the fiscal year ended February 28, 2025, and other filings with the SEC, available for viewing on AZZ’s website at www.azz.com and on the SEC’s website at www.sec.gov.

You are urged to consider these factors carefully when evaluating the forward-looking statements herein and are cautioned not to place undue reliance on such forward-looking statements, which are qualified in their entirety by this cautionary statement. These statements are based on information as of the date hereof and AZZ assumes no obligation to update any forward-looking statements, whether as a result of new information, future events, or otherwise.

Company Contact: David Nark, Senior Vice President of Marketing, Communications, and Investor Relations AZZ Inc. (817) 810-0095 www.azz.com

Investor Contact: Sandy Martin or Phillip Kupper Three Part Advisors (214) 616-2207 or (817) 368-2556 www.threepa.com

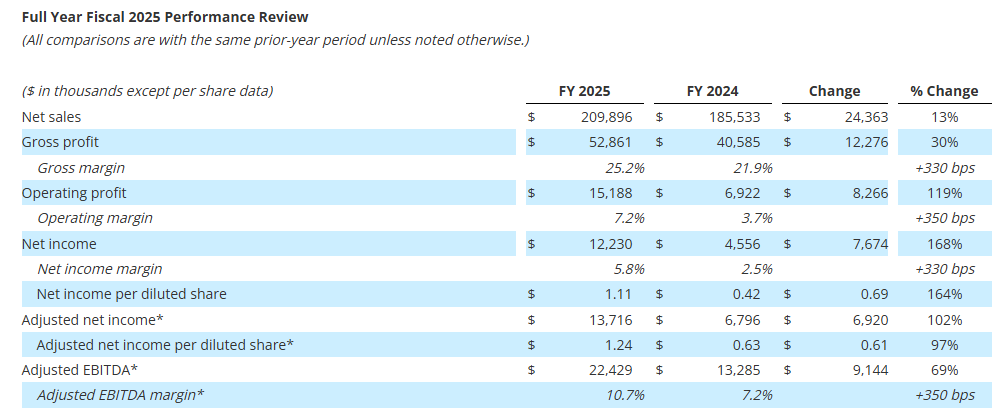

Fourth quarter 2025 results reflect continued strength in the business

Revenue grew 21% to $59.3 million driven by strength across all markets

Gross margin expanded 110 basis points to 27.0% and achieved operating margin of 9.3% compared to 3.1% in the prior-year period

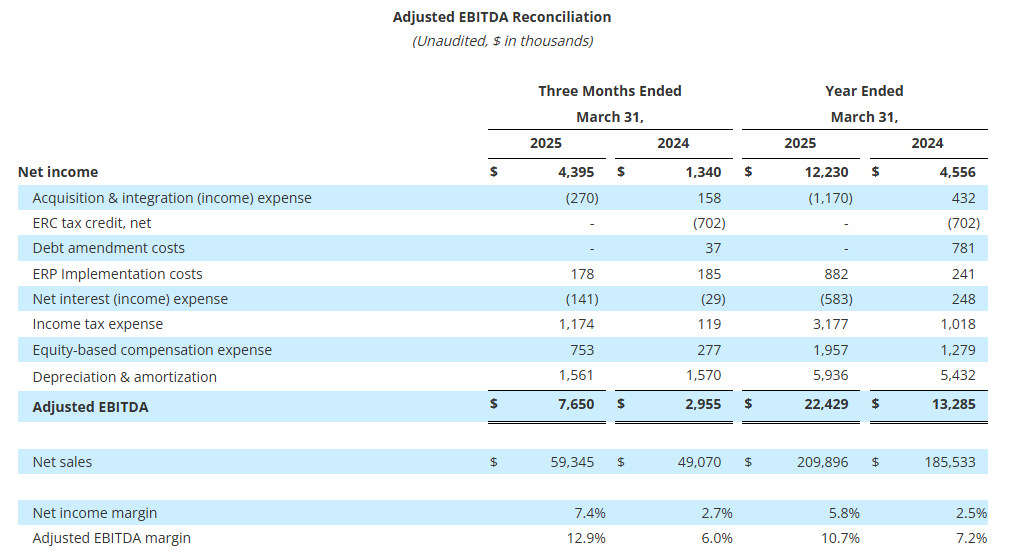

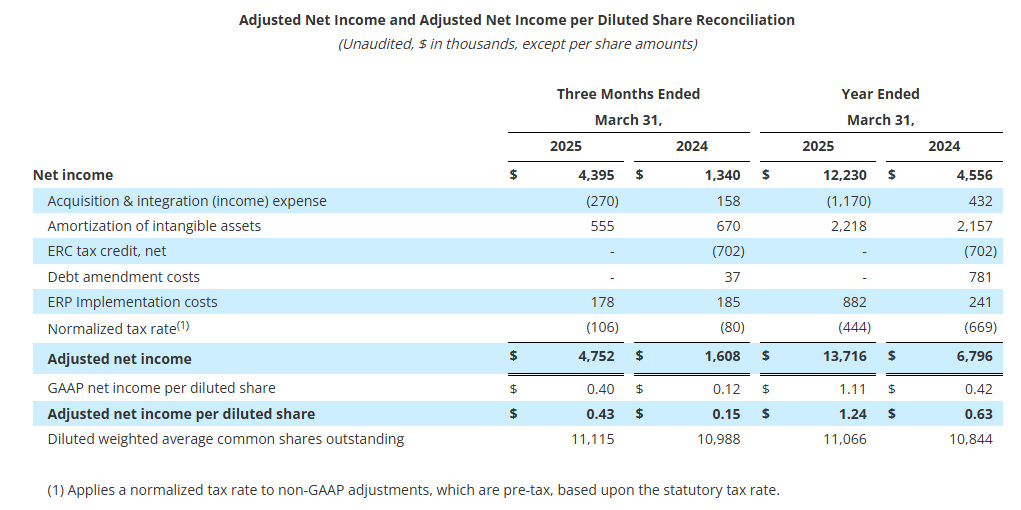

Net Income was $4.4 million; Adjusted net income1 was $4.8 million and Adjusted EBITDA1 was $7.7 million or 12.9% of sales

Fiscal 2025 results demonstrate strong execution on Graham’s long-term strategic plan

Sales growth of 13% driven by Defense projects and Space demand

Gross Margin Expanded 330 Basis Points to 25.2%

Net Income was $12.2 million compared with $4.6 million in prior fiscal year; achieved Adjusted EBITDA1 of $22.4 million or 10.7% of sales

Received full year orders2 of $231.1 million, which represented a Book-to-Bill ratio2 of 1.1x

Record Backlog of $412.3 million

Initiated fiscal 2026 guidance with revenue of $225 million to $235 million, up 10% at Mid-Point over fiscal 2025 with Adjusted EBITDA1 in the range of $22 million to $28 million, up 12% at the mid-point over fiscal 2025

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries, today reported financial results for the fourth quarter and fiscal year 2025 ending March 31, 2025 (“fiscal 2025”).

“We closed fiscal 2025 with strong momentum, as our fourth quarter results reflected solid execution and sustained demand across our diversified product portfolio,” said Daniel J. Thoren, Chief Executive Officer. “We continue to advance projects with an expected 20%+ ROIC1, including automated welding, the expansion of our Batavia, NY facility, and a new cryogenic testing facility in Florida, which will drive enhanced margins and create additional revenue opportunities.”

Mr. Thoren continued, “Looking ahead to fiscal 2026, we are well-positioned to achieve our long-term growth and profitability targets and are strategically looking to invest in key organic and inorganic growth opportunities.”

Management Transition

As previously announced on February 6, 2025, Graham began a planned management transition aligned with its succession strategy. Effective June 10, 2025, Chief Executive Officer Daniel J. Thoren will transition to Executive Chairman and Strategic Advisor. Matt Malone, currently President and Chief Operating Officer, will succeed him as CEO.

Jonathan W. Painter, Chairman of the Board, will transition to Lead Independent Director. Additionally, Michael E. Dixon, promoted to General Manager of Barber-Nichols in February 2025, will assume the role of Vice President of Graham Corporation and General Manager of Barber-Nichols.

“It has been a career highlight and honor to lead Graham Corporation over the last four years and I want to thank our Board and each one of our employees for their commitment and belief in our mission to build better companies, supply mission critical equipment to our customers, and deliver superior performance to our investors,” said Mr. Thoren. “The company is well positioned to achieve its 2027 goals we set in 2022, and I have every confidence in Matt to lead the company to even greater achievements beyond that.”

1Adjusted net income, Adjusted EBITDA and ROIC are non-GAAP measures. See attached tables and other information for important disclosures regarding Graham’s use of these non-GAAP measures.

2Orders, backlog and book-to-bill ratio are key performance metrics. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics.

*Graham believes that, when used in conjunction with measures prepared in accordance with U.S. generally accepted accounting principles, adjusted net income, adjusted net income per diluted share, adjusted EBITDA and adjusted EBITDA margin, which are non-GAAP measures, help in the understanding of its operating performance. See attached tables and other information provided at the end of this press release for important disclosures regarding Graham’s use of these non-GAAP measures.

We have updated our end market disclosures to better align with how management evaluates the business and product portfolio. As part of this change, revenue previously classified as Refining, Chemical/Petrochemical, and Other, which included New Energy product sales, will now be consolidated into one market, which has been renamed “Energy & Process.” The Defense and Space end market classifications remain unchanged. Prior period amounts have been updated to reflect this change.

Quarterly net sales of $59.3 million increased 21%, or $10.3 million. Sales to the Defense market grew by $7.7 million, or 28% from the prior year period, driven by growth in existing programs, better execution, improved pricing, and the timing of key project milestones. Energy & Process sales contributed $1.8 million to growth driven by increased sales of capital equipment to foreign markets and higher aftermarket sales. Aftermarket sales to the Energy & Process and Defense markets of $12.1 million remained strong and were 3.3% higher than the prior year. See supplemental data for a further breakdown of sales by market and region.

Gross profit for the quarter increased $3.3 million to $16.0 million compared to the prior-year period of $12.7 million. As a percentage of sales, gross profit margin increased 110 basis points to 27.0%, compared to the fiscal fourth quarter of 2024. This increase was driven by leverage on higher volume, better execution, and improved pricing, partially offset by higher incentive compensation compared to the prior year period.

Selling, general and administrative expense (“SG&A”), including amortization, totaled $10.8 million, or 18.1% of sales, down $0.3 million compared with the prior year. This decrease reflects the timing of various project expenses partially offset by higher salaries and performance-based compensation as we continue to invest in our people, our processes and our technology to drive long-term sustainable growth.

*Graham believes that, when used in conjunction with measures prepared in accordance with U.S. generally accepted accounting principles, adjusted net income, adjusted net income per diluted share, adjusted EBITDA and adjusted EBITDA margin, which are non-GAAP measures, help in the understanding of its operating performance. See attached tables and other information provided at the end of this press release for important disclosures regarding Graham’s use of these non-GAAP measures.

Net sales of $209.9 million increased 13%, or $24.4 million. Incremental revenue from the acquisition of P3 Technologies (“P3”) in November 2023 accounted for $2.8 million of this increase. Sales to the Defense market grew by $22.4 million, or 23% from the prior year, driven by the addition of new Defense programs, the growth of existing programs, better execution, improved pricing and the timing of key project milestones. Additionally, net sales to the Space industry for fiscal 2025 increased 11% over the prior year primarily due to the addition of P3. Finally, net sales to the Energy & Process industry for fiscal 2025 was consistent with the prior year as increased sales to Asia and the Middle-East were offset by a $2.7 million decline in aftermarket sales from the record levels of fiscal 2024, but which remain strong. See supplemental data for a further breakdown of sales by market and region.

Gross profit for the year increased $12.3 million to $52.9 million compared to the prior-year period of $40.6 million. As a percentage of sales, gross profit margin increased 330 basis points to 25.2%, compared to fiscal 2024. This increase was driven by leverage on higher volume, better execution, and improved pricing. Additionally, fiscal 2025 gross profit benefited $1.3 million from a grant received from the BlueForge Alliance earlier this fiscal year to reimburse Graham for the cost of the Company’s Defense welder training programs in Batavia and related equipment. The Company currently does not expect to receive any additional welder training grants in fiscal 2026.

SG&A, including amortization, totaled $38.9 million, or 18.5% of sales, up $5.3 million compared with the prior year. This increase reflects the Company’s continued investments in its people, processes, and technology to drive long-term sustainable growth including costs related to the implementation of a new enterprise resource planning (“ERP”) system at our Batavia facility, incremental costs related to P3, and increased research and development investment, among others.

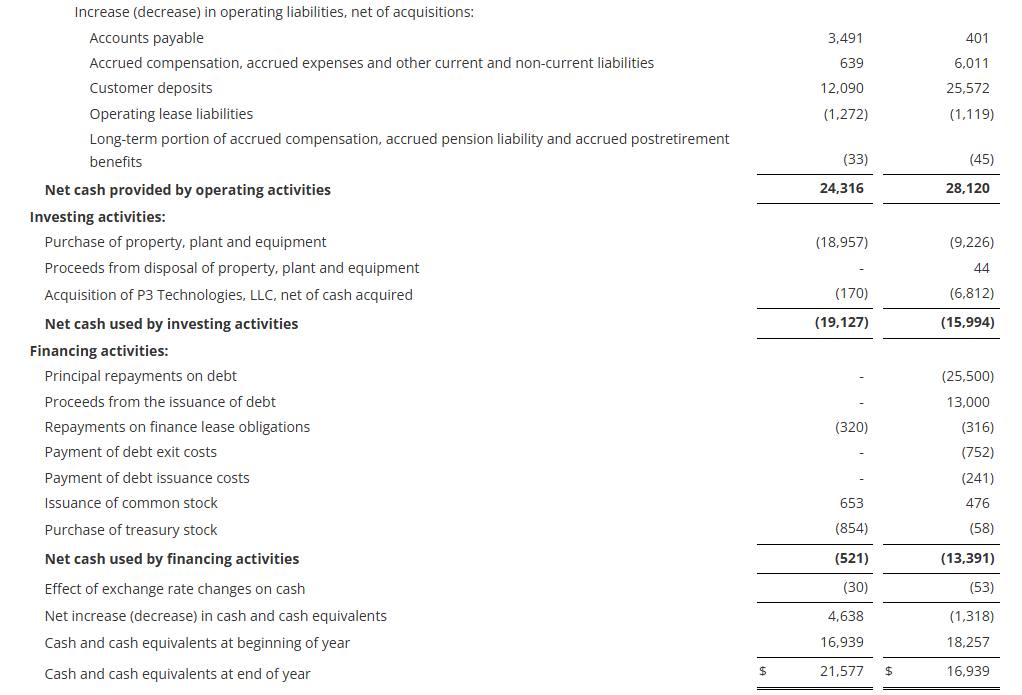

Cash Management and Balance Sheet

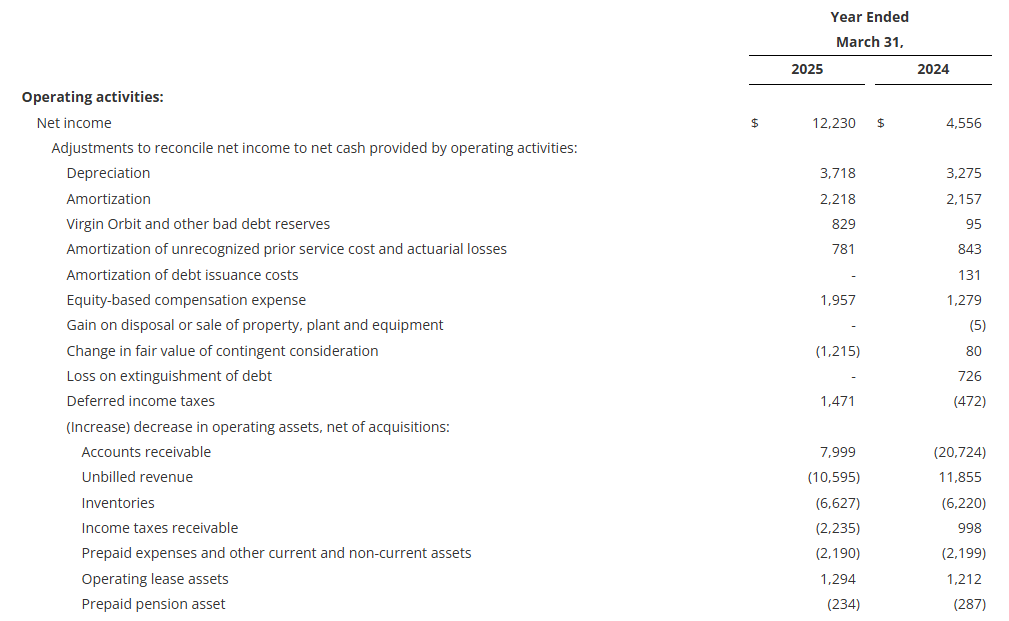

Cash provided by operating activities totaled $24.3 million for the year-ending March 31, 2025, a decrease of $3.8 million from the comparable period in fiscal 2024. As of March 31, 2025, cash and cash equivalents were $21.6 million, up from $16.9 million at the end of fiscal 2024.

Capital expenditures for fiscal 2025 were $19.0 million, focused on capacity expansion, increasing capabilities, and productivity improvements. All major capital projects are on time and on budget.

The Company had no debt outstanding March 31, 2025 with $44.7 million available on its revolving credit facility after taking into account outstanding letters of credit.

Orders, Backlog, and Book-to-Bill Ratio

See supplemental data filed with the Securities and Exchange Commission on Form 8-K and provided on the Company’s website for a further breakdown of orders and backlog by market. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics ($ in millions).

Orders for the fourth quarter of fiscal 2025 increased to $86.9 million, including $50.0 million, of a $136.5 million total contract value, to procure long-lead time materials for follow-on contracts to support the U.S. Navy’s Virginia Class Submarine program. Aftermarket orders for the Energy & Process and Defense markets remained strong and totaled $11.8 million for the fourth quarter of fiscal 2025, an increase of 50% over the prior year.

For fiscal 2025, orders decreased to $231.1 million, primarily due to a record level of orders in fiscal 2024 as a result of follow-on orders for critical U.S. Navy programs related to the Columbia Class submarine and Ford Class carrier programs. Aftermarket orders in fiscal 2025 for the Energy & Process, and Defense markets increased 8% to $46.6 million, compared with fiscal 2024.

Orders tend to be lumpy given the nature of our business (i.e. large capital projects) and in particular, orders to the Defense industry, which span multiple years and can be significantly larger in size. Book-to-bill for fiscal 2025 was 1.1x.

Backlog as of March 31, 2025, was $412.3 million, a 5% increase over the prior-year period. Approximately 45% of orders currently in backlog are expected to be converted to sales in the next twelve months and another 25% to 30% are expected to convert to sales within one to two years. Approximately 83% of our backlog at March 31, 2025 was to the Defense industry, which we believe provides stability and visibility to our business.

Fiscal 2026 Outlook

“I am pleased to announce our fiscal 2026 outlook, which reflects the continued momentum in our business and the initial impacts of the strategic investments we have made. The Company is deploying capital to support our organic and inorganic growth initiatives, while making strategic improvements to enhance our operations and drive margin expansion, which is being enabled by our strong balance sheet. The outlook we are providing reflects the expected impact of tariffs on our fiscal 2026 results, which we estimate to be approximately $2.0 million to $5.0 million. This is subject to change based on the fluidity of global trade policy,” said Christopher Thome, Chief Financial Officer.

(as of June 9, 2025)

Fiscal 2026 Guidance

Net Sales

$225 million to $235 million

Gross Margin(1)

24.5% to 25.5% of sales

SG&A expense (including amortization)(2)

17.5% to 18.5% of sales

Adjusted EBITDA(1)(3)

$22 million to $28 million

Effective Tax Rate

20% to 22%

Capital Expenditures

$15.0 million to $18.0 million

(1)

Includes the estimated impact of increased tariffs over the prior year of approximately $2.0 million to $5.0 million.

(2)

Includes approximately $6.0 million to $7.0 million of Barber-Nichols supplemental performance bonus, equity-based compensation, and enterprise resource planning (“ERP”) conversion costs included in SG&A expense.

(3)

Excludes net interest expense (income), income taxes, depreciation, and amortization from net income, as well as approximately $2.0 million to $3.0 million of equity-based compensation and ERP conversion costs included in SG&A expense, net.

Our expectations for sales and profitability assumes that we will be able to operate our production facilities at planned capacity, have access to our global supply chain including our subcontractors, do not experience any global disruptions, and experience no impact from any other unforeseen events.

Webcast and Conference Call

GHM’s management will host a conference call and live webcast on June 9, 2025 at 11:00 a.m. Eastern Time (“ET”) to review its financial results as well as its strategy and outlook. The review will be accompanied by a slide presentation, which will be made available immediately prior to the conference call on GHM’s investor relations website.

A question-and-answer session will follow the formal presentation. GHM’s conference call can be accessed by calling (201) 689-8560. Alternatively, the webcast can be monitored from the events section of GHM’s investor relations website.

A telephonic replay will be available from 3:00 p.m. ET today through Monday, June 16, 2025. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13753289 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “continue,” “expects,” “future,” “goal,” “outlook,” “anticipates,” “believes,” “could,” “guidance,” ”may”, “will,” “plan” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, profitability of future projects and the business, its ability to deliver to plan, its ability to continue to strengthen relationships with customers in the Defense industry, its ability to secure future projects and applications, expected expansion and growth opportunities, anticipated sales, revenues, adjusted EBITDA, adjusted EBITDA margins, capital expenditures and SG&A expenses, the timing of conversion of backlog to sales, orders, market presence, profit margins, tax rates, foreign sales operations, customer preferences, changes in market conditions in the industries in which it operates, changes in general economic conditions and customer behavior, forecasts regarding the timing and scope of the economic recovery in its markets, and its acquisition and growth strategy, are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

Non-GAAP Financial Measures

Adjusted EBITDA is defined as consolidated net income (loss) before net interest expense, income taxes, depreciation, amortization, other acquisition related expenses, and other unusual/nonrecurring expenses. Adjusted EBITDA margin is defined as Adjusted EBITDA as a percentage of sales. Adjusted EBITDA and Adjusted EBITDA margin are not measures determined in accordance with generally accepted accounting principles in the United States, commonly known as GAAP. Nevertheless, Graham believes that providing non-GAAP information, such as Adjusted EBITDA and Adjusted EBITDA margin, is important for investors and other readers of Graham’s financial statements, as it is used as an analytical indicator by Graham’s management to better understand operating performance. Moreover, Graham’s credit facility also contains ratios based on Adjusted EBITDA. Because Adjusted EBITDA and Adjusted EBITDA margin are non-GAAP measures and are thus susceptible to varying calculations, Adjusted EBITDA, and Adjusted EBITDA margin, as presented, may not be directly comparable to other similarly titled measures used by other companies.

Adjusted net income and adjusted net income per diluted share are defined as net income and net income per diluted share as reported, adjusted for certain items and at a normalized tax rate. Adjusted net income and adjusted net income per diluted share are not measures determined in accordance with GAAP, and may not be comparable to the measures as used by other companies. Nevertheless, Graham believes that providing non-GAAP information, such as adjusted net income and adjusted net income per diluted share, is important for investors and other readers of the Company’s financial statements and assists in understanding the comparison of the current quarter’s and current fiscal year’s net income and net income per diluted share to the historical periods’ net income and net income per diluted share. Graham also believes that adjusted net income per share, which adds back intangible amortization expense related to acquisitions, provides a better representation of the cash earnings of the Company.

ROIC is defined as a return on invested capital and is calculated by dividing net operating profit after taxes by the total invested capital. ROIC is not a measure determined in accordance with GAAP. Nevertheless, Graham believes that providing ROIC is important for investors and other readers of Graham’s financial statements, as it is used as an analytical indicator by Graham’s management to better understand profitability and efficiency of use of capital for certain projects. Because ROIC is a non-GAAP measure and is thus susceptible to varying calculations, ROIC, as presented, may not be directly comparable to other similarly titled measures used by other companies.

Forward-Looking Non-GAAP Measures

Forward-looking ROIC, adjusted EBITDA and adjusted EBITDA margin are non-GAAP measures. The Company is unable to present a quantitative reconciliation of these forward-looking non-GAAP financial measures to their most directly comparable forward-looking GAAP financial measures because such information is not available, and management cannot reliably predict the necessary components of such GAAP measures without unreasonable effort largely because forecasting or predicting our future operating results is subject to many factors out of our control or not readily predictable. In addition, the Company believes that such reconciliations would imply a degree of precision that would be confusing or misleading to investors. The unavailable information could have a significant impact on the Company’s fiscal 2025 financial results. These non-GAAP financial measures are preliminary estimates and are subject to risks and uncertainties, including, among others, changes in connection with purchase accounting, quarter-end, and year-end adjustments. Any variation between the Company’s actual results and preliminary financial estimates set forth above may be material.

Key Performance Indicators

In addition to the foregoing non-GAAP measures, management uses the following key performance metrics to analyze and measure the Company’s financial performance and results of operations: orders, backlog, and book-to-bill ratio. Management uses orders and backlog as measures of current and future business and financial performance, and these may not be comparable with measures provided by other companies. Orders represent written communications received from customers requesting the Company to provide products and/or services. Backlog is defined as the total dollar value of net orders received for which revenue has not yet been recognized. Management believes tracking orders and backlog are useful as they often times are leading indicators of future performance. In accordance with industry practice, contracts may include provisions for cancellation, termination, or suspension at the discretion of the customer.

The book-to-bill ratio is an operational measure that management uses to track the growth prospects of the Company. The Company calculates the book-to-bill ratio for a given period as net orders divided by net sales.

Given that each of orders, backlog, and book-to-bill ratio are operational measures and that the Company’s methodology for calculating orders, backlog and book-to-bill ratio does not meet the definition of a non-GAAP measure, as that term is defined by the U.S. Securities and Exchange Commission, a quantitative reconciliation for each is not required or provided.

Acquisition and integration (income) expense are incremental costs that are directly related to and as a result of the P3 acquisition or the subsequent accounting for the contingent earn-out liability. These costs (income) may include, among other things, professional, consulting and other fees, system integration costs, and contingent consideration fair value adjustments. ERP implementation costs primarily relate to consulting costs (training, data conversion, and project management) incurred in connection with the ERP system being implemented throughout our Batavia, New York facility in order to enhance efficiency and productivity and are not expected to recur once the project is completed. Debt amendment costs consist of accelerated write-offs of unamortized deferred debt issuance costs and discounts, prepayment penalties and attorney fees in connection with the amendment of our credit facility in October 2023.

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy, and process industries, announced that it will release its fourth quarter and fiscal year 2025 financial results before financial markets open on Monday, June 9, 2025.

The Company will host a conference call and webcast to review its financial and operating results, strategy, and outlook. A question-and-answer session will follow.

Fourth Quarter Fiscal Year 2025 Financial Results Conference Call

Monday, June 9, 2025 11:00 a.m. Eastern Time Phone: (201) 689-8560 Internet webcast link and accompanying slide presentation: ir.grahamcorp.com

A telephonic replay will be available from 3:00 p.m. ET on the day of the teleconference through Monday, June 16, 2025. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13753289 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

ABOUT GRAHAM CORPORATION Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy and process industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems.

Graham routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Secures $136.5 million contract to support the Virginia class submarine program

Strengthens Graham’s position as a critical supplier to U.S. Navy’s submarine programs

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“Graham” or “the Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer, and vacuum technologies for the defense, space, energy, and process industries, today announced that its wholly-owned subsidiary Barber-Nichols, LLC (“Barber-Nichols”) has been awarded a $136.5 million follow-on contract to support the U.S. Navy’s Virginia Class Submarine program.

The period of performance extends from April 2025 through February 2034. The Company recognized approximately $50 million in backlog1 from this contract award during the fourth quarter of its fiscal year ending March 31, 2025 to procure long-lead time materials.

Michael E. Dixon, General Manager of Barber-Nichols, commented, “This substantial contract award reinforces our position as a trusted supplier of critical naval components and builds upon our successful execution of previous contracts for Virginia Class Submarines.”

This contract provides an opportunity to showcase the Company’s advanced engineering and manufacturing capabilities. Graham’s long-standing partnership with HII’s Newport News Shipbuilding division (NNS) has led to significant investments in machinery and facilities, ensuring optimal performance in delivering mission-critical systems for the U.S. Navy.

About Graham Corporation