MALVERN, Pa., Feb. 09, 2026 (GLOBE NEWSWIRE) — Ocugen, Inc. (Ocugen or the Company) (NASDAQ: OCGN), a pioneering biotechnology leader in gene therapies for blindness diseases, today announced the appointment of Rita Johnson-Greene as Chief Financial Officer (CFO).

“Mrs. Johnson-Greene’s diverse background across a variety of strategic roles at organizations representing many facets of the industry make her well-suited to serve as Ocugen’s CFO,” said Dr. Shankar Musunuri, Chairman, CEO, and Co-founder of Ocugen. “We look forward to her leadership as we enter into a transformative time at Ocugen, beginning with the submission of the first of three Biologics License Applications (BLAs) this year.”

Mrs. Johnson-Greene has more than 20 years of healthcare experience. She most recently served as Chief Operating Officer at the Alliance for Regenerative Medicine (ARM) where she led ARM’s operations, finance, and global expansion initiatives to advance the development of engineered cell therapies and genetic medicines and promote access for all patients. Prior to her role at ARM, she was the Vice President of Sales and Qualified Treatment Centers (QTC) at Genetix Biotherapeutics (formerly known as bluebird bio), where she built and scaled pre-commercial U.S. sales and QTC operations teams to support the launch of the ZYNTEGLO™ and SKYSONA™ gene therapy brands. Mrs. Johnson-Greene also held senior leadership positions at Spark Therapeutics and supported the launch of LUXTURNA®. Previously, she held roles in finance, commercial operations, and sales in both North and South America for AstraZeneca. Mrs. Johnson-Greene began her career in strategic consulting with Accenture’s strategy practice.

“I am excited to join Ocugen and believe in the potential of the Company’s novel modifier gene therapy platform to address unmet medical needs that still exist for major blindness diseases,” said Mrs. Johnson-Greene. “Having been in the cell and gene therapy space for many years, I understand the unique business needs required to operate efficiently and drive future success.”

Mrs. Johnson-Greene earned her MBA in Finance and Strategic Management from The Wharton School at the University of Pennsylvania, and her undergraduate degree in Electrical Computer Engineering from Drexel University. She serves on the Drexel University Biomed Dean’s Executive Advisory Council and is a guest lecturer for biomedical graduate students.

About Ocugen, Inc. Ocugen, Inc. is a pioneering biotechnology leader in gene therapies for blindness diseases. Our breakthrough modifier gene therapy platform has the potential to address significant unmet medical need for large patient populations through our gene-agnostic approach. Unlike traditional gene therapies and gene editing, Ocugen’s modifier gene therapies address the entire disease—complex diseases that are potentially caused by imbalances in multiple gene networks. Currently we have programs in development for inherited retinal diseases and blindness diseases affecting millions across the globe, including retinitis pigmentosa, Stargardt disease, and geographic atrophy—late stage dry age-related macular degeneration. Discover more at www.ocugen.com and follow us on X and LinkedIn.

Cautionary Note on Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, which are subject to risks and uncertainties. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations. These and other risks and uncertainties are more fully described in our periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.

Weight-loss drugs have moved from niche medical treatments to mainstream consumer products. Television commercials, celebrity endorsements, and telehealth platforms have helped propel GLP-1–based therapies into the public consciousness — and into millions of medicine cabinets.

But as demand has surged, so have tensions across the healthcare, regulatory, and investment landscape.

That tension came sharply into focus today after Hims & Hers Health, Inc. (HIMS) shares fell more than 20% following news that Novo Nordisk has filed a lawsuit seeking to permanently block Hims from selling compounded versions of drugs that allegedly infringe on Novo’s patents — including versions tied to Wegovy, its blockbuster obesity treatment.

The dispute highlights a broader reckoning underway in the fast-growing — and fast-changing — obesity drug market.

A Market Built on Demand — and a Regulatory Loophole

GLP-1 drugs such as Wegovy (Novo Nordisk) and Zepbound/Mounjaro (Eli Lilly) have reshaped expectations around medical weight loss. Unprecedented demand led analysts to project a global obesity drug market of $150 billion to $200 billion by the early 2030s.

But demand quickly ran into supply constraints, high prices, and limited insurance coverage. That gap created an opening for compounded versions of GLP-1 drugs — products mixed by pharmacies and prescribed on a case-by-case basis under the Federal Food, Drug, and Cosmetic Act.

Under U.S. law, compounding is permitted in limited circumstances, such as:

When a patient cannot tolerate an ingredient in a branded drug

When a specific dosage or formulation is medically necessary

When an FDA-approved drug is in short supply

Novo has estimated that as many as 1.5 million Americans are currently using compounded GLP-1 drugs.

Telehealth companies like Hims moved aggressively into this space, marketing lower-cost alternatives to branded therapies — often directly to cash-pay consumers.

Novo vs. Hims: From Tension to Litigation

Novo Nordisk’s lawsuit represents a major escalation.

The company is asking the court to:

Permanently ban Hims from selling compounded versions of its drugs

Recover damages for alleged patent infringement

Novo argues that Hims’ compounded products contain semaglutide, the active ingredient in Wegovy, which is protected by U.S. patents through 2032. Importantly, Novo has stated that semaglutide is no longer in short supply in the U.S. — undermining one of the key legal justifications for compounding.

Hims, for its part, has argued that its products are legal because they are “personalized” in dosage. The company had planned to offer an oral obesity pill for as little as $49 for the first month, roughly $100 less than Novo’s approved Wegovy pill.

However, the pressure intensified last week when:

Hims said it would stop offering its newly launched obesity pill copycat

The FDA announced it planned to take legal action against Hims

Federal regulators said they would restrict access to GLP-1 ingredients used in non-approved compounded drugs

The FDA indicated it may refer the matter to the Department of Justice over potential violations of federal law

In a public statement, Hims called Novo’s lawsuit “a blatant attack by a Danish company on millions of Americans who rely on compounded medications for access to personalized care,” accusing Big Pharma of weaponizing the U.S. judicial system to limit consumer choice.

FDA Scrutiny Raises the Stakes

The FDA has made clear it is increasingly concerned about the quality, safety, and legality of compounded GLP-1 products.

Unlike branded drugs:

Compounded drugs are not FDA-approved

They have not undergone clinical trials to demonstrate efficacy

Oversight is more fragmented

According to legal experts, potential FDA enforcement actions could include:

Warning letters

Court injunctions (with DOJ involvement)

Administrative seizure of products

Novo and Eli Lilly have both taken aggressive steps over the past two years to crack down on compounding pharmacies and marketers. Novo has reportedly filed around 130 lawsuits related to deceptive marketing practices and consumer fraud, while Lilly has pursued similar actions tied to tirzepatide, its active ingredient.

Investors Reassess the Obesity Drug Opportunity

Beyond the immediate legal headlines, the episode underscores a broader shift in how Wall Street views the obesity drug market.

While demand remains strong, expectations around pricing power and long-term market size are being recalibrated:

Forecasts for the global obesity market have fallen roughly 30%, to around $100 billion by 2030

The once-common $150 billion target has been pushed out to 2035 by some analysts

Jefferies recently cut its peak market estimate by 20%, projecting a peak of $80 billion

As Jefferies analyst Michael Leuchten put it: “That $150 billion pie is gone, even if you’re very bullish on volumes.”

Competition is intensifying as well. Novo and Lilly remain the dominant players, but falling U.S. prices, the expected entry of new drugs, and eventual generic competition are reshaping the outlook — particularly in the cash-pay consumer segment.

What This Means Going Forward

For consumers, the crackdown on compounding could limit access to lower-cost alternatives — at least in the near term.

For telehealth companies, the legal and regulatory risks around drug development and distribution are becoming harder to ignore.

And for investors, the GLP-1 market is entering a new phase: one where growth remains substantial, but margins, market share, and timelines are far less certain than they appeared just a year ago.

The obesity drug boom is real. But as the fight between Novo Nordisk, Hims, the FDA, and regulators shows, the path forward will be shaped as much by courts and policymakers as by science and demand.

MALVERN, Pa., Jan. 23, 2026 (GLOBE NEWSWIRE) — Ocugen, Inc. (Nasdaq: OCGN), a pioneering biotechnology leader in gene therapies for blindness diseases, today announced the closing of its previously announced underwritten registered direct offering of 15,000,000 shares of its common stock at an offering price of $1.50 per share of common stock for net proceeds of $20.85 million, after deducting commissions and other estimated offering expenses payable by Ocugen. The financing was led by RTW Investments, with additional participation from new and existing investors.

Ocugen intends to use the net proceeds from the offering for general corporate purposes, capital expenditures, working capital, and general and administrative expenses and anticipates that the net proceeds will extend the company’s cash runway into the fourth quarter of 2026.

Oppenheimer & Co. acted as the sole book-running manager for the offering.

The offering was made pursuant to a shelf registration statement on Form S-3 (File No. 333-278774) previously filed with the Securities and Exchange Commission (the “SEC”) on April 18, 2024, which became effective on May 1, 2024. The offering was made only by means of a prospectus and prospectus supplement that form a part of the registration statement. A prospectus supplement relating to and describing the terms of the offering has been filed with the SEC. Copies of the prospectus supplement and the accompanying base prospectus relating to the offering, may be obtained by visiting the SEC’s website at www.sec.gov or by contacting Oppenheimer & Co. Inc. Attention: Syndicate Prospectus Department, 85 Broad Street, 26th Floor, New York, NY 10004, or by telephone at (212) 667-8055, or by email at EquityProspectus@opco.com.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of, these securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of such state or jurisdiction.

AboutOcugen,Inc.

Ocugen, Inc. is a pioneering biotechnology leader in gene therapies for blindness diseases. Our breakthrough modifier gene therapy platform has the potential to address significant unmet medical need for large patient populations through our gene-agnostic approach. Unlike traditional gene therapies and gene editing, Ocugen’s modifier gene therapies address the entire disease—complex diseases that are potentially caused by imbalances in multiple gene networks. Currently we have programs in development for inherited retinal diseases and blindness diseases affecting millions across the globe, including retinitis pigmentosa, Stargardt disease, and geographic atrophy—late stage dry age-related macular degeneration.

This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, which are subject to risks and uncertainties. Such forward-looking statements within this press release include, without limitation, statements regarding Ocugen’s expectations regarding the anticipated use of proceeds. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks and uncertainties that may cause actual events or results to differ materially from our current expectations, such as market and other conditions. Further, certain forward-looking statements are based on assumptions as to future events that may not prove to be accurate, including the Company’s expected cash runway and various other factors. These and other risks and uncertainties are more fully described in our periodic filings with the SEC, including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by applicable law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, changed circumstances or otherwise, after the date of this press release.

OcugenContact:

Tiffany Hamilton AVP, Head of Communications Tiffany.Hamilton@Ocugen.com

Ocugen, Inc. is a biotechnology company focused on developing and commercializing novel gene therapies, biologicals, and vaccines. The lead product in its gene therapy program, OCU400, is in Phase 1/2 clinical trials for retinitis pigmentosa.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Positive Preliminary Data From The OCU410 Trial. Ocugen announced first data from its Phase 2 ArMaDa trial testing OCU410 in Geographic Atrophy associated with dry Age-related Macular Degeneration (GA-dAMD). The announcement included the patients who have reached 12 months after treatment, with 23 out of the total 51 patients enrolled. The data shows an overall 46% reduction in lesion growth compared with controls. We see this as a highly meaningful difference.

OCU410 Is A Single-Treatment Gene Therapy. OCU410 is being developed as gene therapy for patients with GA secondary to dry AMD. A single OCU410 intravitreal injection delivers RORA (retinoid-related orphan receptor alpha), a nuclear receptor that regulates key pathways involved in retinal homeostasis with four mechanisms of action.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CERRITOS, Calif., Jan. 05, 2026 (GLOBE NEWSWIRE) — The Oncology Institute, Inc. (“TOI”) (NASDAQ: TOI), one of the largest value-based oncology groups in the United States, today announced that Mark Stolper has joined the Board of Directors, effective January 2, 2026. Mr. Stolper brings significant public markets, financial and operational leadership experience to The Oncology Institute’s board. Mr. Stolper serves as Executive Vice President and Chief Financial Officer of RadNet, Inc. (NASDAQ: RDNT), a position he has held since 2004. Mr. Stolper has also been a member of the Board of Directors of various publicly traded and privately held healthcare companies, including 21st Century Oncology Holdings, Inc., which at the time was one of the nation’s leading radiation and medical oncology companies.

“We are very pleased to have a seasoned public company CFO like Mark join our board,” said Anne McGeorge, Chairman of the Board of The Oncology Institute. “Mark brings tremendous experience in capital markets, fundraising strategies, strategic financial planning and payor strategy that will be invaluable to TOI in our next phase of growth.”

“I am very excited to join The Oncology Institute’s Board of Directors,” commented Mr. Stolper. “The Company’s mission to provide leading-edge, cost-effective cancer care to improve outcomes and streamline the patient journey is critically important at this time in healthcare. I truly believe that TOI is poised for continued growth and profitability in the coming years.”

About The Oncology Institute Founded in 2007, The Oncology Institute (NASDAQ: TOI) is advancing oncology by delivering highly specialized, value-based cancer care in the community setting. TOI offers cutting-edge, evidence-based cancer care to a population of approximately 1.9 million patients, including clinical trials, transfusions, and other care delivery models traditionally associated with the most advanced care delivery organizations. With over 180 employed and affiliate clinicians and over 100 clinics and affiliate locations of care across five states and growing, TOI is changing oncology for the better. For more information, visit www.theoncologyinstitute.com

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Phase 3 Trial Has Treated Its First Patient. MAIA has begun its pivotal Phase 3 trial for THIO in NSCLC (non-small cell Lung Cancer), meeting our expected timeframe. In October, the Phase 2 THIO-101 trial began its Part C and will continue as the Phase 3 is running. These trials are the latest in a series of positive announcements for THIO (ateganosine) clinical development, keeping it on schedule for additional milestones in 2026.

Trial Design Can Lead To First Approval. The Phase 3 THIO-104 is an open-label trial is testing ateganosine in combination with an CPI (immune checkpoint inhibitor) as a third-line treatment in patients who are resistant to CPIs and chemotherapy. Patients who have failed two courses of chemotherapy including CPIs will be randomized into two groups to receive either the ateganosine/CPI combination or standard of care chemotherapy. The primary endpoint is Overall Survival (OS).

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Bridging the Compensation, Culture, and Compliance Gaps for Value Realization in 2025

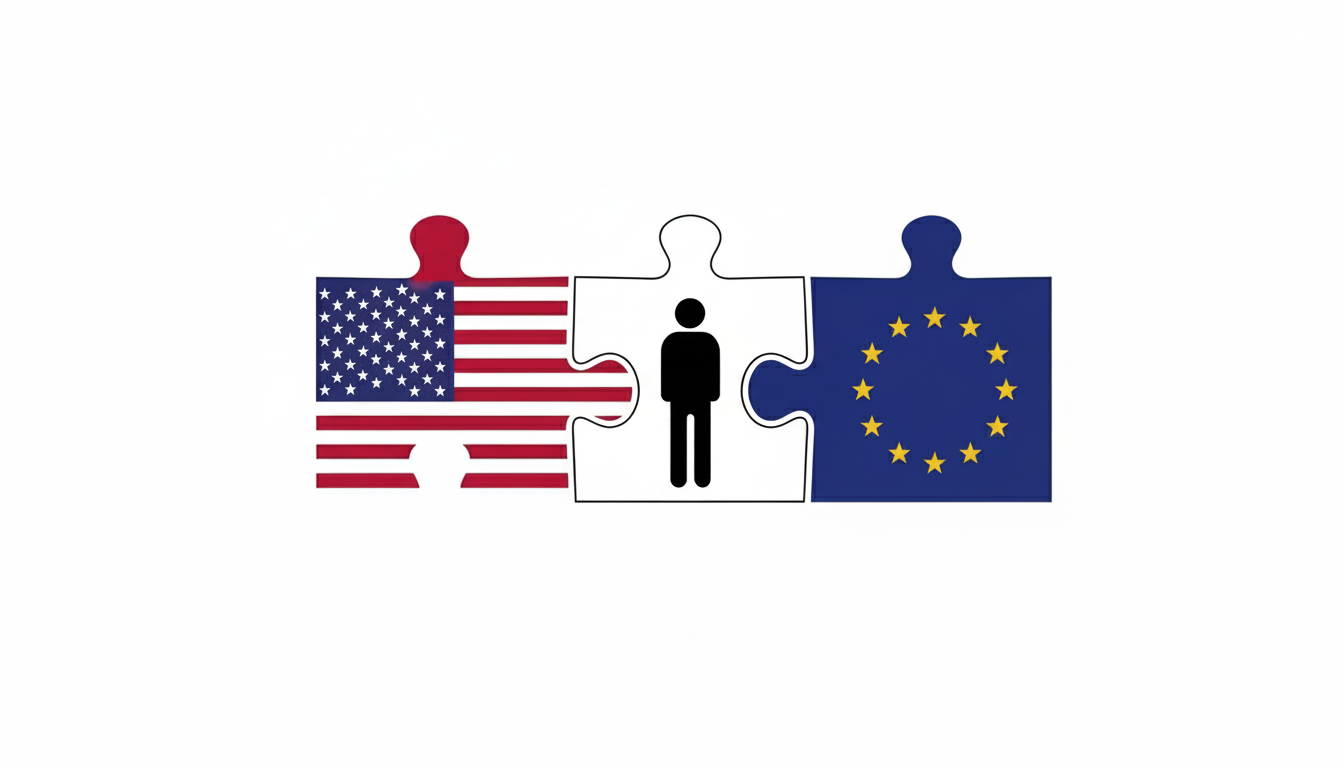

The Healthcare and Life Sciences (HCLS) sector continues to be a powerhouse for global Mergers & Acquisitions (M&A) activity, driven by digitalization, specialized therapeutics, and the imperative for integrated care models. When European entities acquire US counterparts, the primary risk to deal value shifts from financial modeling to human capital integration. In 2025, transatlantic HCLS deals face an unprecedented trifecta of challenges: navigating the US’s competitive, burnout-driven talent market; identifying and realizing true operational synergies; and bridging the fundamental divide between US and EU compensation and benefits philosophies. Successfully integrating talent across these vastly different labor ecosystems is now the defining feature of deal success.

The Fierce Pursuit of Specialized US HCLS Talent

The US HCLS talent market in 2025 is defined by scarcity, rising costs, and high turnover – especially for highly specialized roles in advanced therapeutics, bioinformatics, and AI-driven diagnostics. Would-be European acquirers of US HCLS companies must move beyond reactive hiring to adopt future-ready strategies:

Skills-First & AI Operationalization: The industry is moving toward skills-based hiring, particularly for critical roles that drive transformation and innovation (e.g., Gene Editing, GenAI). While AI is being widely operationalized to streamline administrative burdens (scheduling, screening, drafting job descriptions), it has yet to be proven as a strategic tool for high-level talent strategy or predicting cultural fit. Smart integration plans, therefore, should prioritize leveraging AI to accelerate efficiency while reserving human expertise for assessment and strategic sourcing.

EVP and Retention over Recruitment: High turnover, burnout, and the rise of non-traditional healthcare employers (tech, consulting) have made retention the top priority. The Employer Value Proposition (EVP) must be hyper-personalized and focused on fostering Equity, Inclusion, and Belonging (EIB), shifting the focus from simply who is hired to who stays, grows, and thrives. Post-merger, US employees often prioritize clear career pathways, flexibility, and supportive management when choosing to remain with the combined entity.

Proactive Pipelining: Due to the shrinking talent pool, organizations might rely heavily on talent pipelining and targeted outbound campaigns, establishing relationships with specialized talent before roles are officially posted. Integration teams could leverage the European target’s existing academic partnerships or regional centers of excellence to feed into the US-side pipeline for highly technical roles.

Operational Synergies: A Shift to Scope and Capability

Transatlantic HCLS M&A is increasingly dominated by scope deals—acquisitions focused on new technology, market access, or specific clinical capabilities, rather than simple scale. Synergy capture in these deals is more complex and requires aggressive planning that goes beyond traditional cost-cutting:

Revenue Synergies in R&D and Market Access: The most significant value tends to be found in revenue synergies, such as combining the European acquirer’s innovative R&D capabilities and global footprint with the US target’s vast commercialization strength and specialized talent access. Due diligence must build complex synergy models to validate these revenue forecasts, which are inherently more difficult to predict than cost savings.

Consolidating Back-Office Functions: Classic operational synergies still apply, particularly in consolidating redundant non-patient-facing functions. Examples include streamlining financial administration, IT infrastructure, and back-office services like Revenue Cycle Management (RCM) or billing. This consolidation can lead to immediate cost savings and process standardization but must be executed early in the integration lifecycle to realize value.

Cultural Alignment as a Synergist: Synergy capture is often derailed by poor cultural alignment. Integration planning should prioritize blending cultural elements early on. For a European company acquiring a US firm, navigating different approaches to hierarchy, risk tolerance, and work-life balance will be crucial to retaining the very R&D or specialized operational talent the deal was meant to secure.

Navigating the Transatlantic Compensation & Benefits Chasm

The starkest challenge in harmonizing US and EU operations lies in aligning compensation, benefits, and labor practices, which reflect fundamentally different societal models:

The Salary and Contribution Divide: US salaries are generally higher, often dramatically so for specialized roles (e.g., mid-level tech salaries can show a 30–50% gap). However, the underlying employer cost structure differs significantly. US employers bear steep costs for private, market-driven healthcare ($8,000 to $16,000+ per employee annually), while EU employers bear heavy social charges and payroll contributions that fund state-backed universal healthcare and pensions. Integration teams should employ dual benchmarks, modeling both equal salaries (for equity assessment) and market-specific total compensation (for budget control).

Mandated Benefits and Labor Law: Europe offers generous, often legally mandated benefits, including a minimum of 20+ paid vacation days, comprehensive parental leave, and stricter labor protections regarding notice periods and dismissal costs. In contrast, US benefits are a competitive tool, varying widely by state and company size. Attempting to impose a US-centric “low vacation, high private insurance” model on EU operations could result in catastrophic talent loss and non-compliance with local labor law.

Compliance Complexity: The US operates under a fragmented legal structure of both federal (e.g., ACA and COBRA and state-specific laws (sick leave, minimum wage, worker classification), whereas the EU operates under centralized directives, but implementation varies across 27 Member States (e.g., Spain and Portugal requiring 14-month salaries). HR teams must deploy local expertise to avoid compliance pitfalls, particularly around worker classification and termination processes.

In conclusion, successful transatlantic HCLS M&A requires HR integration teams to treat human capital as a strategic asset, not just a line item. Value is realized when the best of both labor ecosystems is preserved, harmonizing compensation and benefits while leveraging the combined entity’s specialized talent pools through proactive, skills-focused strategies.

In the next installment of our Europe-US Cross-Border HCLS M&A series, we move from people to data, tackling the ultimate transatlantic compliance hurdle: the clash between GDPR and HIPAA. Learn how European acquirers can avoid major fines and deal breaks by meticulously auditing and integrating data governance across two radically different legal frameworks.

About the Authors:

Nathan Caliis a Managing Partner atNoble Capital Marketswith more than 18 years of Capital Markets experience. He has been a lead Managing Director/Head of the Healthcare and Life Sciences Investment Banking and Advisory franchise at NOBLE since 2017 and was previously a sell-side equity analyst for 9 years. Nathan is a Board Member of Precise Bio, a tissue engineering, biomaterials, and cell technologies company, including cardiology, orthopedics, and dermatology. He was previously a board observer of Eledon Pharmaceuticals (ELDN:NASDAQ, f.k.n.a. Anelixis Therapeutics, Inc.), a phase II biotechnology company. Prior to joining NOBLE, Nathan gained investment experience as a portfolio account analyst/manager at Franklin Templeton Investments. Nathan also currently holds series 7, 79, 86, and 87 FINRA designations.

Hinesh Patel, MCMI ChMCis a Partner in CNM LLP’sLos Angeles Office with over 20 years of experience in accounting. He leads and oversees the firm’s Accounting and Transaction Advisory practice. He brings a vast knowledge of US GAAP, technical accounting, and International Financial Reporting Standards (IFRS) reporting requirements to his role at CNM. Hinesh primarily focuses on technical accounting, IPO readiness, SEC reporting, and mergers and acquisitions. Prior to joining CNM, Hinesh worked as a Senior Manager at Deloitte with a primary focus in the technology, manufacturing, consumer business and entertainment industries for both public and private companies. He has assisted various companies through the IPO process and advised on a range of accounting services including technical accounting, financial reporting, and new business processes requirements.

Matthew (Matt) Podowitzis the founder and Principal Consultant ofPathfinder Advisors LLC, bringing experience on 400+ global M&A engagements to his clients. He specializes in the critical operational and technology aspects of M&A transactions, providing due diligence, carve-out, integration, and value creation services. Known for practical, actionable advice derived from extensive hands-on experience with healthcare and life sciences transactions, Matt helps companies, investment banks, and private equity firms navigate complex cross-border HCLS M&A through every step of the transaction lifecycle. Leveraging his perspective as a dual US/EU citizen, he provides seamless support for transactions in both markets. His background includes leadership roles at firms like Ernst & Young, Grant Thornton, and CFGI.

Chris Raphaelyis the Co-Chair ofCozen O’Connor’sHealth Care & Life Sciences Practice where he provides sophisticated transactional and regulatory counsel to an array of health care providers and investors in the health care industry. His practice focuses on mergers, acquisitions, and divestiture transactions for health care clients and the comprehensive regulatory schemes requisite to doing business in the health care space. Chris routinely handles matters involving payer negotiations, payment disputes and contract enforcement, accountable care organizations, management services organization, clinically integrated networks, value based payment arrangements, pharmacy benefit management and third party administrator contracts for self-insured employers, digital health, organizational and governance structures, HIPAA, information privacy and security, tax exemption, Stark Law, fraud and abuse matters, clinical integration, medical staff relations, facility and professional licensing, Pennsylvania’s Medical Marijuana Act, and general compliance. Prior to joining the firm, Chris served as the deputy general counsel to Jefferson Health System and general counsel to the system’s accountable care organization and captive professional liability insurance companies.

CERRITOS, Calif., Nov. 13, 2025 (GLOBE NEWSWIRE) — The Oncology Institute, Inc. (NASDAQ: TOI) (“TOI” or the “Company”), one of the largest value-based community oncology groups in the United States, today reported financial results for its three months ended September 30, 2025 and updated its full year 2025 guidance.

Recent Operational Highlights

Fee-for-service revenue growth of 13% over Q3 2024, driven by continued organic growth performance in Florida and Oregon.

Retail Pharmacy and Dispensary set fill records, contributing $75.9 million in revenue and $12.8 million in gross profit in Q3.

Signed several new in-network MSO providers in the Florida market and opened our new TOI pharmacy location in Florida.

Welcomed Kristin England as our new Chief Administrative Officer overseeing our Enterprise Central Business Operations, Technology Strategy and AI Enablement.

Third Quarter 2025 Financial Highlights

All comparisons are to the quarter ended September 30, 2024 unless otherwise noted

Consolidated revenue of $136.6 million increased 36.7% from $99.9 million

Gross profit of $18.9 million, increased 31.7%

Net loss of $16.5 million compared to net loss of $16.1 million

Basic and diluted (loss) earnings per share of $(0.14) compared to $(0.18)

Adjusted EBITDA of $(3.5) million compared to $(8.2) million

Cash and cash equivalents of $27.7 million as of September 30, 2025

Outlook for Fiscal Year 2025

TOI uses Adjusted EBITDA and Free Cash flow, each a non-GAAP metric, as an additional tool to assess its operational and financial performance. See “Financial Information: Non-GAAP Financial Measures” below. In reliance on the unreasonable efforts exception provided under Regulation S-K, TOI is not reasonably able to provide a quantitative reconciliation for forward-looking information of Adjusted EBITDA and Free Cash Flow to net (loss) income and net cash provided by operations, respectively, the most directly comparable GAAP financial measures, without unreasonable efforts due to uncertainties regarding taxes, capital expenditures, operating activities, share-based compensation, goodwill impairment charges, change in fair value of liabilities, unrealized (gains) losses on investments, practice acquisition-related costs, consulting and legal fees, transaction costs and other non-cash items. The variability of these items could have an unpredictable, and potentially significant, impact on TOI’s future GAAP financial results. The Company, given the revenue and profitability growth in the first three quarters, is updating its full year revenue and Adjusted EBITDA guidance as follows:

2025 Guidance – Previous

2025 Guidance – Updated

Revenue

$460 to $480 million

$495 to $505 million

Gross Profit

$73 to $82 million

$73 to $82 million

Adjusted EBITDA

$(8) to $(17) million

$(11) to $(13) million

Free Cash Flow

$(12) to $(21) million

$(12) to $(21) million

Additionally, the Company expects Adjusted EBITDA of approximately $0 to $2 million in the fourth quarter of 2025. TOI’s achievement of the anticipated results is subject to risks and uncertainties, including those disclosed in its filings with the U.S. Securities and Exchange Commission. The outlook does not take into account the impact of any unanticipated developments in the business or changes in the operating environment, nor does it take into account the impact of TOI’s acquisitions, dispositions or financings. TOI’s outlook assumes a largely stable global market, which would likely be negatively impacted if recent tariff rate increases and exchange rate changes persist and adversely affect world trade.

Management Commentary

Daniel Virnich, CEO of TOI, commented, “We had a solid third quarter across all lines of our business. Our Pharmacy business continues to set records, and our new delegated lives in Florida are ramping nicely with strong MLR performance. During the quarter, we made meaningful progress in leveraging AI to drive efficiencies in our operations and improve the patient experience. These were just some of the factors that allowed us to increase our full-year guidance and reaffirm our positive outlook for Q4 adjusted EBITDA. As a leader in oncology value-based care, it is important for us to not only raise the quality of care but also lower that cost of care. We believe we are well-positioned to achieve this goal, while simultaneously driving durable and sustainable growth.”

Webcast and Conference Call

TOI will host a conference call on Thursday, November 13, 2025 at 5:00 p.m. (Eastern Time) to discuss third quarter results and management’s outlook for future financial and operational performance.

The conference call can be accessed live over the phone by dialing 1-877-407-0789, or for international callers, 1-201-689-8562. A replay will be available two hours after the call and can be accessed by dialing 1-844-512-2921, or for international callers, 1-412-317-6671. The passcode for the live call and the replay is 13756737. The replay will be available until Thursday, November 20, 2025.

Interested investors and other parties may also listen to a simultaneous webcast of the conference call by logging onto the Investor Relations section of TOI’s website at https://investors.theoncologyinstitute.com.

About The Oncology Institute, Inc.

Founded in 2007, The Oncology Institute, Inc. (NASDAQ: TOI) is advancing oncology by delivering highly specialized, value-based cancer care in the community setting. TOI offers cutting-edge, evidence-based cancer care to a population of approximately 1.9 million patients including clinical trials, transfusions, and other care delivery models traditionally associated with the most advanced care delivery organizations. With over 180 employed and affiliate clinicians and over 100 clinics and affiliate locations of care across five states and growing, TOI is changing oncology for the better. For more information visit www.theoncologyinstitute.com.

Forward-Looking Statements

This press release includes certain statements that are not historical facts but are forward-looking statements for purposes of the safe harbor provisions under the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements generally are accompanied by words such as “preliminary,” “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “should,” “would,” “plan,” “project,” “predict,” “potential,” “guidance,” “approximately,” “seem,” “seek,” “future,” “outlook,” and similar expressions that predict or indicate future events or trends or that are not statements of historical matters. These forward-looking statements include, but are not limited to, statements regarding projections, anticipated financial results, estimates and forecasts of revenue and other financial and performance metrics and projections of market opportunity and expectations. These statements are based on various assumptions and on the current expectations of TOI and are not predictions of actual performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on by anyone as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond the control of TOI. These forward-looking statements are subject to a number of risks and uncertainties, including the accuracy of the assumptions underlying the 2025 full fiscal year outlook and the Q4 2025 outlook with respect to Adjusted EBITDA discussed herein, the outcome of judicial and administrative proceedings to which TOI may become a party or investigations to which TOI may become or is subject that could interrupt or limit TOI’s operations, result in adverse judgments, settlements or fines and create negative publicity; changes in TOI’s patient or payors’ preferences, prospects and the competitive conditions prevailing in the healthcare sector; failure to continue to meet stock exchange listing standards; the impact of a cybersecurity incident affecting a software provider on TOI’s business; those factors discussed in the documents of TOI filed, or to be filed, with the SEC, including the Item 1A. “Risk Factors” section of TOI’s Annual Report on Form 10-K for the year ended December 31, 2024 filed with the SEC on March 26, 2025 and any subsequent Quarterly Reports on Form 10-Q or Current Reports on Form 8-K. If the risks materialize or assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that TOI currently is evaluating or does not presently know or that TOI currently believes are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In addition, forward-looking statements reflect TOI’s plans or forecasts of future events and views as of the date of this press release. TOI anticipates that subsequent events and developments will cause TOI’s assessments to change. TOI does not undertake any obligation to update any of these forward-looking statements. These forward-looking statements should not be relied upon as representing TOI’s assessments as of any date subsequent to the date of this press release. Accordingly, undue reliance should not be placed upon the forward-looking statements.

GeoVax Labs, Inc. is a clinical-stage biotechnology company developing novel therapies and vaccines for solid tumor cancers and many of the world’s most threatening infectious diseases. The company’s lead program in oncology is a novel oncolytic solid tumor gene-directed therapy, Gedeptin®, presently in a multicenter Phase 1/2 clinical trial for advanced head and neck cancers. GeoVax’s lead infectious disease candidate is GEO-CM04S1, a next-generation COVID-19 vaccine targeting high-risk immunocompromised patient populations. Currently in three Phase 2 clinical trials, GEO-CM04S1 is being evaluated as a primary vaccine for immunocompromised patients such as those suffering from hematologic cancers and other patient populations for whom the current authorized COVID-19 vaccines are insufficient, and as a booster vaccine in patients with chronic lymphocytic leukemia (CLL). In addition, GEO-CM04S1 is in a Phase 2 clinical trial evaluating the vaccine as a more robust, durable COVID-19 booster among healthy patients who previously received the mRNA vaccines. GeoVax has a leadership team who have driven significant value creation across multiple life science companies over the past several decades.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Plans For MVA Vaccine and Gedeptin Trial Expectations Confirmed. GeoVax reported a 3Q25 loss of $6.3 million or $(0.31) per share, a smaller loss than the $8.0 million loss we had projected. The company reviewed several developments related to the Geo-MVA vaccine for smallpox/Mpox, Gedeptin, and CM04S1. Discussions for possible marketing collaborations continue. The cash balance on September 30, 2025 was $5.0 million.

Moving Forward With Geo-MVA. As discussed in our Research Note on June 17, the Geo-MVA vaccine for smallpox/Mpox is moving forward toward a Phase 3 trial. This follows receipt of Scientific Advice EMA (European Medicines Agency) stating that a marketing approval application can be submitted after a single, Phase 3 immuno-bridging study against the approved MVA vaccine. Phase 1 and Phase 2 would not be required. This saves several years and many millions dollars, allowing the company to sell the vaccine sooner.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CERRITOS, Calif., Oct. 22, 2025 (GLOBE NEWSWIRE) — The Oncology Institute, Inc. (“TOI”) (NASDAQ: TOI), a pioneer in value-based community oncology care, today announced that the company will release its third quarter 2025 financial results after the market close on Thursday, November 13, 2025, to be followed by a conference call the same day at 5:00 p.m. (Eastern Time).

The conference call can be accessed live over the phone by dialing 1-877-407-0789 or for international callers, 1-201-689-8562. A replay will be available two hours after the call and can be accessed by dialing 1-844-512-2921, or for international callers, 1-412-317-6671. The passcode for the live call and the replay is 13756737. The replay will be available until Thursday, November 20, 2025.

Interested investors and other parties may also listen to a simultaneous webcast of the conference call by logging onto the Investor Relations section of the Company’s website at https://investors.theoncologyinstitute.com/.

About The Oncology Institute

Founded in 2007, The Oncology Institute (NASDAQ: TOI) is advancing oncology by delivering highly specialized, value-based cancer care in the community setting. TOI offers cutting-edge, evidence-based cancer care to a population of approximately 1.9 million patients, including clinical trials, transfusions, and other care delivery models traditionally associated with the most advanced care delivery organizations. With over 180 employed and affiliate clinicians and over 100 clinics and affiliate locations of care across five states and growing, TOI is changing oncology for the better.

On October 22, 2025, Alkermes plc (Nasdaq: ALKS) and Avadel Pharmaceuticals plc (Nasdaq: AVDL) announced a definitive merger agreement reflecting a major shift in the sleep medicine sector and the broader biopharmaceutical industry. The all-cash transaction, valued at up to $20 per Avadel share, comprises an $18.50 cash payment plus a contingent value right (CVR) for an additional $1.50 per share linked to final FDA approval of LUMRYZ™ for idiopathic hypersomnia. This structure represents a transaction value of approximately $2.1 billion and a 38% premium to Avadel’s three-month average share price, indicating strong confidence in Avadel’s commercial prospects.

The acquisition marks Alkermes’ strategic expansion into the sleep medicine market—a key area of growth for the company. With this move, Alkermes augments its existing neuroscience and rare disease franchise by adding Avadel’s FDA-approved LUMRYZ™ (sodium oxybate), a once-at-bedtime treatment for cataplexy or excessive daytime sleepiness in narcoleptic patients aged seven and older. LUMRYZ™ distinguishes itself as the market’s only once-nightly oxybate, offering significant convenience and competitive advantage over the twice-nightly alternative. Since its 2023 launch, LUMRYZ™ has experienced rapid adoption, with over 3,100 patients on therapy as of June 2025 and new patient starts outpacing competitors more than two-to-one. Net revenues are projected between $265–275 million for 2025, backed by a U.S. narcolepsy market of over 50,000 eligible patients.

Alkermes’ acquisition is expected to be immediately accretive to earnings and profit margins, providing the scale and financial strength to accelerate both commercial and clinical development programs. For Alkermes, the deal offers a robust foundation to support its late-stage developmental pipeline, specifically its orexin 2 receptor agonist candidates—alixorexton, ALKS 4510 and ALKS 7290—for narcolepsy and idiopathic hypersomnia. The combined company harnesses both organizations’ commercial expertise and operational infrastructure, streamlining R&D and driving cost synergies.

Leadership at both Alkermes and Avadel have expressed optimism about the transaction. Alkermes’ CEO Richard Pops described the acquisition as “a pivotal step” in the company’s evolution—a move that bolsters Alkermes’ entry into sleep medicine as it prepares to advance alixorexton into phase 3 trials. Avadel’s CEO, Greg Divis, characterized the merger as a validation of Avadel’s strategy, highlighting the differentiated value of LUMRYZ™ and the company’s dedication to sleep disorder patients.

Under the transaction’s terms, Alkermes will fund the acquisition with cash on hand and new debt, subject to regulatory and shareholder approvals. Both boards have unanimously approved the deal, targeting a closing date in the first quarter of 2026. Financial and legal advising teams include J.P. Morgan, Morgan Stanley, Goldman Sachs, Paul Weiss, and Cleary Gottlieb.

With this acquisition, Alkermes solidifies its position as a leader in neurological and sleep disorder treatments, accelerating the pace of innovation in a space with significant unmet patient needs. The combined organization is set to pursue further label expansions for LUMRYZ™, bring new therapies to market, and deliver increased value to shareholders and patients alike.

The landmark agreement between Alkermes and Avadel Pharmaceuticals underscores the accelerating consolidation trend within the life sciences sector, where innovative therapies and commercial scale are driving strategic acquisitions. The addition of LUMRYZ™ to Alkermes’ portfolio not only diversifies its product base but strengthens its market position in a segment characterized by high unmet medical need and strong growth potential.

Alkermes’ entry into the sleep medicine market will leverage Avadel’s proven commercial infrastructure and rare disease expertise, enabling more efficient launches and access for future products. The transaction also sets the stage for Alkermes to explore global expansion opportunities for LUMRYZ™ and other pipeline assets, while supporting additional indications such as idiopathic hypersomnia and leveraging Avadel’s salt-free, once-at-bedtime oxybate candidate.

As the two organizations integrate, operational synergies are expected to improve profitability and streamline R&D processes for advancing both existing therapies and new clinical programs. The merger, backed by reputable financial advisors and committed financing, represents a pivotal moment for stakeholders, positioning Alkermes as an emerging leader in neurology and sleep disorder therapeutics with a stronger foundation for future innovation and patient impact.

CERRITOS, Calif., Oct. 01, 2025 (GLOBE NEWSWIRE) — The Oncology Institute (NASDAQ: TOI), a pioneer in value-based community oncology care, today announced that Dr. Daniel Virnich, Chief Executive Officer, and Rob Carter, Chief Financial Officer, will participate in the Noble Capital Markets Emerging Growth Virtual Equity Conference, on October 8, 2025, including a presentation at 11:00am ET.

Interested parties can access a webcast of the presentation by registering at the link listed on the Investor Relations section of the Company’s websites at https://investors.theoncologyinstitute.com/.

Founded in 2007, The Oncology Institute (NASDAQ: TOI) is advancing oncology by delivering highly specialized, value-based cancer care in the community setting. TOI offers cutting-edge, evidence-based cancer care to a population of approximately 1.9 million patients, including clinical trials, transfusions, and other care delivery models traditionally associated with the most advanced care delivery organizations. With over 180 employed and affiliate clinicians and over 100 clinics and affiliate locations of care across five states and growing, TOI is changing oncology for the better.

CERRITOS, Calif., Sept. 29, 2025 (GLOBE NEWSWIRE) — The Oncology Institute (NASDAQ: TOI), a pioneer in value-based community oncology care, is pleased to announce a new partnership with Protocol Behavioral Health, a leading provider of evidence-based mental health care for cancer patients. This collaboration underscores TOI’s commitment to delivering whole-person care by integrating behavioral health services directly into the cancer care journey.

Research shows that approximately 30% of cancer patients experience significant depression or anxiety, and oncologists widely agree that behavioral health support can benefit nearly every patient. Through this partnership, TOI patients will gain timely access to mental health services that are tailored specifically to the emotional and psychological challenges of cancer, with no waitlists and full integration into the patient’s care team, and the added benefit of services offered in multiple languages to support our diverse patient population.

“Anxiety and depression can greatly threaten a patient’s outcome by affecting their ability to complete treatment in the recommended time,” said Yale Podnos, MD, Chief Medical Officer at The Oncology Institute. “By embedding behavioral health services directly into our care model, we’re closing a critical gap in oncology and ensuring our patients have access to the support they need, exactly when they need it.”

Key Benefits of the Partnership:

Integrated Care Delivery: Protocol clinicians collaborate with TOI providers using the Collaborative Care Model (CoCM), an evidence-based framework proven to improve outcomes through team-based care.

Improved Access: Patients receive behavioral health support without delays, removing a major barrier to care in traditional mental health systems.

Specialized Expertise: Protocol’s behavioral health care managers and psychiatric providers are trained specifically to support oncology patients through diagnosis, treatment, survivorship, and beyond.

Improved Patient Outcomes: Studies link integrated behavioral health care to better treatment adherence, quality of life, and patient satisfaction.

“We founded Protocol to meet a clear need in oncology,” said Cara Bohon, PhD, Chief Clinical Officer of Protocol Behavioral Health. “Through this partnership, we’re ensuring that mental health care is not a luxury or an afterthought; it’s a core part of the patient’s treatment plan from day one.”

Founded in 2007, The Oncology Institute (NASDAQ: TOI) is advancing oncology by delivering highly specialized, value-based cancer care in the community setting. TOI offers cutting-edge, evidence-based cancer care to a population of approximately 1.9 million patients, including clinical trials, transfusions, and other care delivery models traditionally associated with the most advanced care delivery organizations. With over 180 employed and affiliate clinicians and over 100 clinics and affiliate locations of care across five states and growing, TOI is changing oncology for the better.

Protocol Behavioral Health provides timely, evidence-based mental health care tailored to the unique needs of cancer patients. Using the Collaborative Care Model, Protocol integrates behavioral health managers and psychiatric providers directly into oncology care teams. This model ensures seamless coordination, personalized support, and better outcomes for patients experiencing depression, anxiety, and other behavioral health challenges.