Alan Smith, Vice President and General Manager of Graham Manufacturing to retire in April 2026 and will serve in an advisory role moving forward

William Zmyndak is expected to assume the role of Vice President and General Manager of Graham Manufacturing upon Mr. Smith’s retirement

Additionally, the Company announces the appointments of Keith Oufnac as Chief Information Officer and Rachel Jaakkola as Chief Human Resources Officer

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer vacuum, and advanced mixing technologies for the Defense, Energy & Process and Space industries, today announced the appointment of William Zmyndak, Deputy General Manager of Graham Manufacturing.

As part of a proactive succession plan, Alan Smith, currently Vice President and General Manager of Graham Manufacturing, will transition to a consulting and advisory role beginning in April 2026. In this capacity, Mr. Smith will continue to support the business and leadership team through a transition period upon his retirement. Effective April 2026, Mr. Zmyndak will assume the role of Vice President and General Manager of Graham Manufacturing upon Alan’s retirement.

Mr. Zmyndak brings more than three decades of manufacturing and operational leadership experience, including senior leadership and P&L responsibility across complex, multi-site aerospace and industrial businesses. Prior to joining Graham, he served as Vice President and General Manager at ITT Control Technologies, where he led operations across multiple U.S. and international locations and drove margin expansion, operational excellence, and growth initiatives. Earlier in his career, Mr. Zmyndak held senior leadership roles at Kaman Aerosystems, Chromalloy, Barnes Aerospace, and Pratt & Whitney. He holds a Master of Business Administration from Purdue University and a Bachelor of Science in Manufacturing Engineering from Boston University.

In addition to this leadership transition, the Company announced two key leadership appointments that further strengthen its executive team.

Keith Oufnac has been appointed Chief Information Officer. Mr. Oufnac has more than 20 years of experience leading digital transformation, IT strategy, and cybersecurity initiatives across defense, aerospace, and highly regulated industries. Most recently, he served as Vice President of Information Technology at Bollinger Shipyards, where he led enterprise-wide infrastructure modernization, cybersecurity enhancements, and large-scale systems integration efforts, including support for significant acquisition activity.

Rachel Jaakkola has been appointed Chief Human Resources Officer. Ms. Jaakkola is a seasoned human resources executive with over a decade of experience building and scaling people organizations within aerospace, defense, and energy companies. She has a proven track record in talent strategy, leadership development, employee engagement, and M&A integration. Prior to joining Graham, Ms. Jaakkola served in senior HR leadership roles at Barber-Nichols, where she established and led the human resources function through periods of significant growth and organizational transformation.

Matthew J. Malone, President and Chief Executive Officer of Graham Corporation, said, “Alan has been instrumental in strengthening Graham Manufacturing for over 30 years of his career, and we are grateful for his continued support during the transition. Will brings extensive operational and P&L leadership experience across complex manufacturing environments, along with a strong commitment to people and execution. I am confident he is the right leader to build on our momentum and continue driving operational excellence and growth. The additions of Keith and Rachel further strengthen our leadership team as we invest in the systems, people and capabilities needed to support our long-term strategy.”

About Graham Corporation

Graham is a global leader in the design and manufacture of mission-critical fluid, power, heat transfer, vacuum, and advanced mixing technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise, proprietary technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “continue,” “expects,” “will,” “plan” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, expected future management personnel changes and the timing of such changes, expected expansion and growth opportunities, and its growth strategy, are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

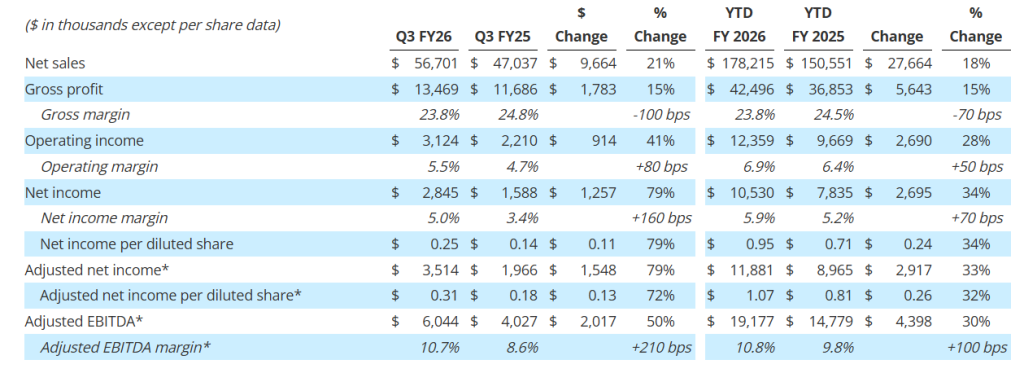

Gross profit increased 15% to $13.5 million; Gross profit margin was 23.8%

Net income per diluted share increased 79% to $0.25; adjusted net income per diluted share1 increased 72% to $0.31

Adjusted EBITDA1 increased 50% to $6.0 million; Adjusted EBITDA margin1 was 10.7%

Orders2 were $71.7 million; Book-to-Bill ratio2 of 1.3x and record backlog2 of $515.6 million

Strong balance sheet with no debt, $22.3 million in cash, and access to $43.0 million under its revolving credit facility at quarter end to support growth initiatives

Updating and increasing full year fiscal 2026 guidance; Remain on track to reach strategic goal of 8% to 10% annual organic revenue growth and low to mid-teen Adjusted EBITDA margins1 by fiscal 2027

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer, vacuum, and advanced mixing technologies for the Defense, Energy & Process, and Space industries, today reported financial results for its third quarter for the fiscal year ending March 31, 2026 (“fiscal 2026”).

Graham’s President and Chief Executive Officer, Matthew J. Malone stated, “Our third quarter results reflect continued strong, disciplined execution across the organization as we progress through the back half of fiscal 2026. Revenue growth and profitability were driven by solid performance across our end markets and supported by a record backlog, which provides meaningful visibility into future demand. Activity in our Defense market remains robust, while the Energy & Process and Space markets continue to perform in line with our expectations.”

Mr. Malone continued, “As we move through the remainder of the fiscal year, we remain focused on disciplined execution, operational efficiency, and advancing strategic initiatives that strengthen our competitive position. We continue to invest in automation, advanced testing, and new technical capabilities that enhance productivity and support margin expansion. In addition, the recent acquisition of FlackTek in January 2026 meaningfully expands our technology portfolio and further positions Graham to deliver differentiated, mission-critical solutions to our core end markets.”

1Adjusted net income per diluted share, Adjusted EBITDA, and Adjusted EBITDA margin are non-GAAP measures. See attached tables and other information for important disclosures regarding Graham’s use of these non-GAAP measures. 2Orders, backlog, and book-to-bill ratio are key performance metrics. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics.

Third Quarter Fiscal 2026 Performance Review

(All comparisons are with the same prior-year period unless noted otherwise.)

*Graham believes that, when used in conjunction with measures prepared in accordance with U.S. generally accepted accounting principles (“GAAP”), adjusted net income, adjusted net income per diluted share, adjusted EBITDA, and adjusted EBITDA margin, which are non-GAAP measures, help in the understanding of its operating performance. See attached tables and other information provided at the end of this press release for important disclosures regarding Graham’s use of these non-GAAP measures.

Quarterly net sales of $56.7 million increased 21%, or $9.7 million over the prior year reflecting our diversified revenue base. Sales to the Defense market contributed $8.3 million to growth primarily due to the timing of project milestones, new programs, and growth in existing programs. Sales to the Energy & Process market increased $2.1 million or 13% over the prior year driven by Aftermarket sales, as well as continued momentum in our New Energy markets and in particular small modular reactors (“SMRs”). Aftermarket sales to the Energy & Process and Defense markets totaled $10.8 million for the quarter, 11% above the prior year. See supplemental data for a further breakdown of sales by market and region.

Gross profit for the quarter increased $1.8 million, or 15%, to $13.5 million compared to the prior-year period of $11.7 million. As a percentage of sales, gross profit margin decreased 100 basis points to 23.8%, compared to the third quarter of fiscal 2025. This decrease in gross profit margin reflects the mix of sales during the third quarter of fiscal 2026, and a higher level of material receipts which carry lower profit margins. Additionally, the third quarter and the first nine months of fiscal 2025 gross profit benefited $0.3 million and $1.5 million, respectively, from a grant received in the prior year from the BlueForge Alliance to reimburse the Company for the cost of its defense welder training programs in Batavia, which did not repeat in fiscal year 2026. For the first nine months of fiscal 2026, we estimate the impact of tariffs on our consolidated financial statements to be approximately $1.0 million compared to the prior year and was immaterial for the third quarter of fiscal 2026. For the full fiscal 2026, we now expect the potential impact of tariffs to be between an incremental $1.0 to $1.5 million compared to the prior year.

Selling, general and administrative expense (“SG&A”), including intangible amortization, totaled $10.6 million, an increase of $0.9 million compared with the prior year due to the investments being made in operations, employees, and technology, higher acquisition and integration costs due to the Xdot and FlackTek acquisitions, as well as higher performance-based compensation due to Graham’s increased profitability, which was partially offset by a reversal of bad debt reserves. As a percentage of sales, SG&A, including amortization of 18.6%, decreased 200 basis points compared to the prior year period, reflecting the higher level of sales during the quarter, as well as our continued financial discipline.

Cash Management and Balance Sheet

Cash provided by operating activities totaled $4.8 million for the quarter ended December 31, 2025. As of December 31, 2025, cash and cash equivalents were $22.3 million.

Capital expenditures, net for the third quarter fiscal 2026 were $2.2 million, focused on capacity expansion, increasing capabilities, and productivity improvements.

The Company had no debt outstanding as of December 31, 2025, with $43.0 million available on its revolving credit facility after taking into account outstanding letters of credit.

Orders, Backlog, and Book-to-Bill Ratio

See supplemental data filed with the Securities and Exchange Commission on Form 8-K and provided on the Company’s website for a further breakdown of orders and backlog by market. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics ($ in millions).

Orders for the third quarter of fiscal 2026 were $71.7 million. This increase was primarily in the Defense and Space markets, which continue to exhibit strong tail-winds. Energy & Process orders were consistent with prior year levels, as strong demand in New Energy offset weaker Aftermarket orders. Total Aftermarket orders for the third quarter of fiscal 2026 decreased $5.2 million to $8.0 million from the record levels of the prior year.

Note that our orders tend to be lumpy given the nature of our business (i.e. large capital projects) and in particular, orders to the Defense industry, which span multiple years and can be significantly larger in size.

Backlog at quarter end was a record $515.6 million, a 34% increase over the prior-year period, driven by strong bookings including contributions from Xdot of $0.5 million, primarily in the Defense and Space markets. For the quarter, the Company achieved a book-to bill ratio of 1.3x. Approximately 35% to 40% of orders currently in backlog are expected to be converted to sales in the next twelve months, another 25% to 30% are expected to convert to sales within one to two years, and the remaining beyond two years. Approximately 85% of our backlog as of December 31, 2025, was to the Defense industry, which provides stability and visibility to our business.

FlackTek Acquisition

On January 23, 2026, subsequent to the end of the third quarter, Graham acquired FlackTek Manufacturing, LLC and FlackTek Sales, LLC (collectively, “FlackTek”). The acquisition establishes advanced mixing and materials processing as a third core technology platform for Graham, complementing its existing vacuum, heat transfer, and turbomachinery capabilities and further aligning with the Company’s Defense, Energy & Process, and Space end markets.

Under the terms of the transaction, Graham acquired 100% of the equity of FlackTek for a purchase price of $35.0 million, comprised of 85% cash and 15% using 75,818 shares of Graham’s common stock, along with the potential to earn an additional $25 million in future performance-based cash earnouts over four years beginning in fiscal year 2027, based upon achieving progressively increasing adjusted EBITDA performance targets. The base purchase price represents approximately 12x FlackTek’s projected adjusted EBITDA for 2026. The transaction was funded through a combination of cash on-hand and borrowings under the Company’s revolving credit facility.

In connection with the acquisition, Graham amended its revolving credit agreement with Wells Fargo Bank, National Association, increasing the borrowing limit from $50 million to $80 million. Following the closing of the transaction, the Company’s pro forma leverage ratio is approximately 1.2x.

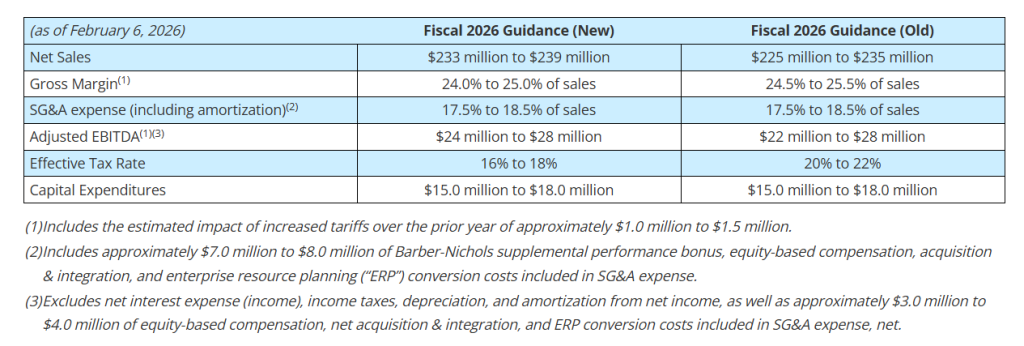

Fiscal 2026 Outlook

Based upon the results for the first nine months of fiscal 2026, our expectations for the remainder of the fiscal year, and inclusive of the acquisition of FlackTek and Xdot, Graham is updating its full year fiscal 2026 guidance as follows:

Graham’s Chief Financial Officer, Christopher J. Thome, said, “We are pleased with our performance through the first nine months of fiscal 2026 and continue to see strong demand across most of the markets we serve. Reflecting this momentum, including the contribution from the FlackTek acquisition, we are increasing our full-year fiscal 2026 guidance.

Mr. Thome continued, “After the acquisition of FlackTek, our balance sheet remains strong with low leverage, a modest amount of debt of $20 million, and increased capacity under our line of credit. We believe this increased capacity, along with our strong operating cash flow, provides us ample liquidity to continue to execute our capital allocation strategy and future growth.”

Webcast and Conference Call

GHM’s management will host a conference call and live webcast on February 6, 2026, at 11:00 a.m. Eastern Time (“ET”) to review its financial results as well as its strategy and outlook. The review will be accompanied by a slide presentation, which will be made available immediately prior to the conference call on GHM’s investor relations website.

A question-and-answer session will follow the formal presentation. GHM’s conference call can be accessed by calling (201)-689-8560. Alternatively, the webcast can be monitored from the events section of GHM’s investor relations website.

A telephonic replay will be available from 3:00 p.m. ET today through Friday, February 13, 2026. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13757532 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer, vacuum, and advanced mixing technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise, proprietary technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Graham Corporation designs, manufactures and sells critical equipment for the energy, defense and chemical/petrochemical industries. The Company designs and manufactures custom-engineered ejectors, vacuum pumping systems, surface condensers and vacuum systems. It is a nuclear code accredited fabrication and specialty machining company. It supplies components used inside reactor vessels and outside containment vessels of nuclear power facilities. Its equipment is found in applications, such as metal refining, pulp and paper processing, water heating, refrigeration, desalination, food processing, pharmaceutical, heating, ventilating and air conditioning. For the defense industry, its equipment is used in nuclear propulsion power systems for the United States Navy. The Company’s products are used in a range of industrial process applications in energy markets, including petroleum refining, defense, chemical and petrochemical processing, power generation/alternative energy and other.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

An Acquisition. Graham has acquired FlackTek, a pioneer in advanced mixing and material processing solutions. The acquisition adds advanced materials processing as a third core platform for Graham, alongside Graham Manufacturing, specializing in vacuum & heat transfer, and Barber-Nichols, specializing in turbomachinery. FlackTek adds a proven and defensible product portfolio with a shared customer base and an installed footprint that extends across the full value chain, from upstream to downstream production and quality control.

Details. The purchase price is $35 million, which was paid 85% in cash and 15% using 75,818 GHM shares. There is a potential $25 million in future performance-based cash earnouts over 4 years based upon achieving progressively increasing adjusted EBITDA performance targets. The base purchase price is approximately 12x FlackTek’s projected 2026 adjusted EBITDA. FlackTek generates approximately $30 million in annualized revenue.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Establishes advanced mixing and material processing as the third pillar to Graham’s mission-critical engineered products portfolio

Adds proprietary mixing products, utilizing bladeless dual asymmetric centrifugal principles, which builds off the strong foundation in vacuum, heat transfer, and high-speed turbomachinery

Strong overlap across Graham’s end markets and customers; Defense, Energy & Process and Space with new sub-markets including battery, medical, nuclear, semiconductor, and personal care

Enhances long-term growth through disruptive technology, recurring consumables, and aftermarket opportunities in established and emerging end-markets

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or “the Company”), a global leader in the design and manufacture of mission-critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space markets, today announced the acquisition of FlackTek Manufacturing, LLC and FlackTek Sales, LLC (“FlackTek”), a pioneer in advanced mixing and material processing solutions.

The acquisition adds advanced materials processing as a third core platform for Graham, alongside Graham Manufacturing, specializing in vacuum & heat transfer, and Barber-Nichols, specializing in turbomachinery. FlackTek will operate as a wholly owned subsidiary of Graham Corporation, maintaining its headquarters in Louisville, Colorado with a satellite location in Greenville, South Carolina, and will be integrated into Graham’s financial, compliance, and operational infrastructure.

Under the terms of the transaction, Graham acquired 100% of the equity of FlackTek for a purchase price of $35 million, which was paid 85% in cash and 15% using 75,818 shares of Graham’s common stock, along with the potential to earn an additional $25 million in future performance-based cash earnouts over four years beginning with the Company’s fiscal year 2027, based upon achieving progressively increasing adjusted EBITDA performance targets each year. The base purchase price represents approximately 12x FlackTek’s projected adjusted EBITDA for 2026.

“FlackTek represents a highly strategic addition to Graham’s mission-critical product portfolio and directly aligns with our long-term vision to build differentiated, technology-led platforms,” said Matthew J. Malone, President and Chief Executive Officer of Graham Corporation. “The fundamental physics behind advanced mixing align closely with Graham’s core competencies in vacuum, heat transfer, and turbomachinery, enabling new opportunities to solve complex materials processing challenges for customers across defense, aerospace, and industrial markets. It’s unique that the FlackTek product portfolio impacts the full value chain from the mine to final assembly with applicability in upstream, midstream, and downstream applications.”

Matt Gross, Chief Executive Officer of FlackTek, said, “Joining Graham marks an exciting new chapter for FlackTek. Graham’s engineering heritage, manufacturing expertise, and strong presence in our core end markets provide an ideal platform to accelerate our growth while preserving the innovation and customer focus that define our culture. I look forward to continuing to lead the FlackTek team as part of Graham and continue to expand the impact of our technology together.”

Overview of FlackTek

Recognized as a leader in high-performance, bladeless centrifugal mixing, FlackTek designs and manufactures advanced mixing systems, accessories, consumables, and material processing solutions built on its proprietary product portfolio. Headquartered in Louisville, Colorado, FlackTek maintains a strong domestic manufacturing footprint complemented by an established international distribution network.

FlackTek’s technology delivers highly repeatable, precision mixing with significantly faster cycle times, minimal entrained air, reduced downtime between batches, consistency in production, and reduced heat transfer compared to traditional bladed methods. These performance advantages are critical in applications where material integrity and consistency are paramount. As a result, FlackTek’s systems are trusted by a global customer base that includes leading OEMs, research and development centers, defense laboratories, and industrial manufacturers serving adhesives, sealants, functional coatings, composites, electronics, and other advanced materials markets.

The company has successfully expanded its portfolio beyond laboratory-scale systems into larger, highly differentiated platforms, most notably the MEGA™ system, enabling customers to scale advanced materials processing from R&D through pilot and into production environments.

With approximately $30 million in annualized revenue, FlackTek has built a growing installed base that generates recurring demand for consumables, accessories, and services, enhancing revenue visibility and durability. FlackTek’s technical excellence, mixing effectiveness and efficiency, service responsiveness, innovation, and reliability, position it well for continued growth through both expanded end-market penetration and broader sales channel development.

FlackTek Strategic Rationale

The acquisition of FlackTek meaningfully expands Graham’s ability to solve complex customer challenges that increasingly demand integrated solutions spanning rotating machinery, vacuum environments, thermal management, and advanced materials processing. FlackTek’s technology sits naturally alongside Barber-Nichols’ turbomachinery and Graham Manufacturing’s vacuum and heat transfer systems, creating a more comprehensive engineered solutions platform.

FlackTek adds a proven and defensible product portfolio with a shared customer base and an installed footprint that extends across the full value chain, from upstream to downstream production and quality control. Its mixing systems are process-critical and market-agnostic, serving defense, energetics, oil & gas, food, battery, aerospace and space, medical, and other industrial applications where precision, repeatability, and consistency drive value.

By adding a differentiated engineered systems business with strong intellectual property and recurring revenue characteristics, the acquisition is expected to enhance margins, deepen customer relationships, and unlock cross-platform innovation opportunities across Graham’s defense, energy & process, and space end markets.

Other Transaction Details

The cash portion of the consideration was funded through a combination of cash on hand and borrowings under the Company’s existing credit facilities.

In connection with the acquisition, Graham amended its credit agreement to enhance financial flexibility and support continued investment in organic growth initiatives and opportunistic acquisitions. The amendment increased the Company’s revolving credit facility from $50 million to $80 million, providing additional capacity to execute its capital allocation strategy and future growth.

Following the closing of the transaction, Graham’s pro forma leverage ratio is approximately 1.2x, consistent with the Company’s disciplined capital allocation framework and targeted leverage profile. The overall transaction structure, including the upfront consideration and a performance-based earnout component, aligns with Graham’s long-term financial objectives while preserving balance sheet strength and liquidity.

FlackTek’s Chief Executive Officer, Matt Gross, will join Graham’s leadership team as Vice President and General Manager and will continue to lead the FlackTek business, ensuring continuity of operations and strategic execution.

The Company has published a supplemental presentation in connection with the announced acquisition. This presentation is available under the “Events & Presentations” section of the Company’s website at ir.grahamcorp.com. The Company will provide additional details on the acquisition and update its fiscal 2026 outlook on its Fiscal 2026 Third Quarter earnings call scheduled for 11:00 am ET on Friday, February 6, 2026.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “expects,” “positions,” “will,” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, profitability of future projects and the business, its ability to deliver to plan, realization of benefits from the acquisition of FlackTek, the integration and operation of FlackTek, and the effect of the FlackTek acquisition on our growth are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries, announced that it will release its third quarter fiscal year 2026 financial results before financial markets open on Friday, February 6, 2026.

The Company will host a conference call and webcast to review its financial and operating results, strategy, and outlook. A question-and-answer session will follow.

Third Quarter Fiscal Year 2026 Financial Results Conference Call

Friday, February 6, 2026 11:00 a.m. Eastern Time Phone: (201) 689-8560 Internet webcast link and accompanying slide presentation: ir.grahamcorp.com

A telephonic replay will be available from 3:00 p.m. ET on the day of the teleconference through Friday, February 13, 2026. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13757532 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

ABOUT GRAHAM CORPORATION Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space, industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Graham Corporation designs, manufactures and sells critical equipment for the energy, defense and chemical/petrochemical industries. The Company designs and manufactures custom-engineered ejectors, vacuum pumping systems, surface condensers and vacuum systems. It is a nuclear code accredited fabrication and specialty machining company. It supplies components used inside reactor vessels and outside containment vessels of nuclear power facilities. Its equipment is found in applications, such as metal refining, pulp and paper processing, water heating, refrigeration, desalination, food processing, pharmaceutical, heating, ventilating and air conditioning. For the defense industry, its equipment is used in nuclear propulsion power systems for the United States Navy. The Company’s products are used in a range of industrial process applications in energy markets, including petroleum refining, defense, chemical and petrochemical processing, power generation/alternative energy and other.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

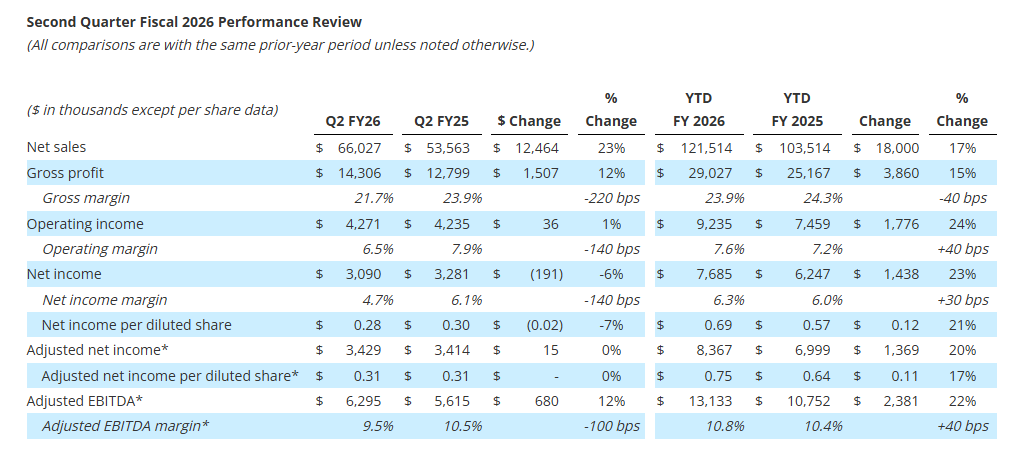

Overview. Graham put up solid results for the second quarter of fiscal 2026. The Company executed well across all the business lines, driving broad based-growth. Demand across the end markets remains healthy, and the Defense and Space markets continue to see robust activity.

2Q26 Results. Revenue grew 23% to $66 million, driven by solid performance across all end markets. We were at $59 million. Adjusted EBITDA was $6.3 million, up 12% from the prior year, and adjusted EBITDA margin was 9.5%. We had forecasted $6.2 million and 10.4%. Net income for the quarter was $0.28 per diluted share, and adjusted net income was $0.31 per diluted share. We were at $0.30 and $0.32, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Gross profit increased 12% to $14.3 million; Gross profit margin was 21.7%

Net income per diluted share was $0.28; adjusted net income per diluted share1 was $0.31

Adjusted EBITDA1 increased 12% to $6.3 million; Adjusted EBITDA margin1 was 9.5%

Orders2 were $83.2 million; Book-to-Bill ratio2 of 1.3x and record backlog2 of $500.1 million

Strong balance sheet with no debt, $20.6 million in cash, and access to $44.7 million under its revolving credit facility at quarter end to support growth initiatives

Reiterating full year fiscal 2026 revenue and adjusted EBITDA guidance; Remain on track to reach strategic goal of 8% to 10% annual organic revenue growth and low to mid-teen Adjusted EBITDA margins1 by fiscal 2027

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries, today reported financial results for its second quarter for the fiscal year ending March 31, 2026 (“fiscal 2026”).

Graham’s President and Chief Executive Officer, Matthew J. Malone stated, “I am pleased with our performance through the first half of the fiscal year. Our team continues to execute well across all business lines, driving broad-based growth supported by a record $500.1 million backlog. Demand across our end markets remains healthy as our Defense and Space markets continue to experience robust activity, and the Energy & Process market remains resilient. These trends are underscored by approximately $14.8 million of new Space orders secured and a $25.5 million follow-on order for the MK48 Torpedo program during the quarter, reinforcing our position as a trusted partner on critical platforms.”

Mr. Malone continued, “As we look to the second half of the year, we remain focused on advancing high-return initiatives that strengthen Graham’s competitive position and drive sustainable value creation. Across our operations, we are investing in automation, advanced testing, and new technical capabilities designed to enhance productivity, efficiency, and profitability. These include automated welding systems, advanced radiographic testing technologies, our NextGenTM steam ejector Nozzle, and our new cryogenic testing facility in Florida. Each of these projects is expected to deliver returns above 20%, improve margins, and create meaningful opportunities for growth in both defense and commercial markets.”

1Adjusted net income per diluted share, Adjusted EBITDA and Adjusted EBITDA margin are non-GAAP measures. See attached tables and other information for important disclosures regarding Graham’s use of these non-GAAP measures. 2Orders, backlog and book-to-bill ratio are key performance metrics. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics.

*Graham believes that, when used in conjunction with measures prepared in accordance with U.S. generally accepted accounting principles (“GAAP”), adjusted net income, adjusted net income per diluted share, adjusted EBITDA and adjusted EBITDA margin, which are non-GAAP measures, help in the understanding of its operating performance. See attached tables and other information provided at the end of this press release for important disclosures regarding Graham’s use of these non-GAAP measures.

Quarterly net sales of $66.0 million increased 23%, or $12.5 million. Sales in the Defense market contributed $9.9 million to growth primarily due to the timing of project milestones (primarily material receipts), new programs and growth in existing programs. Sales for the Energy & Process market increased $2.0 million or 11% driven by increased sales in China and timing of larger capital projects, partially offset by decreased sales in India due to project timing. Aftermarket sales in the Energy & Process and Defense markets of $9.8 million remained strong and were slightly higher than the prior year. See supplemental data for a further breakdown of sales by market and region.

Gross profit for the quarter increased $1.5 million, or 12%, to $14.3 million compared to the prior-year period of $12.8 million. As a percentage of sales, gross profit margin decreased 220 basis points to 21.7%, compared to the second quarter of fiscal 2025. This decrease in gross profit margin reflects the mix of sales during the second quarter of fiscal 2026, and particularly, an extraordinarily high level of material receipts which carry a lower profit margin. Additionally, the second quarter and the first six months of fiscal 2025 gross profit benefited $0.4 million and $0.9 million, respectively, from a grant received in the prior year from the BlueForge Alliance to reimburse the Company for the cost of its defense welder training programs in Batavia which did not repeat in fiscal year 2026. For the first six months of fiscal 2026, we estimate the impact of tariffs on our consolidated financial statements to be approximately $1.0 million compared to the prior year.

Selling, general and administrative expense (“SG&A”), including intangible amortization, totaled $10.2 million, an increase of $1.1 million compared with the prior year due to the investments being made in operations, employees, and technology, as well as higher performance-based compensation due to Graham’s increased profitability. As a percentage of sales, SG&A, including amortization of 15.5%, decreased 160 basis points compared to the prior year period, reflecting the higher level of sales during the quarter as well as our continued financial discipline.

Cash Management and Balance Sheet

Cash provided by operating activities totaled $13.6 million for the quarter-ending September 30, 2025. As of September 30, 2025, cash and cash equivalents were $20.6 million, compared with $32.3 million as of September 30, 2024.

Capital expenditures for the second quarter fiscal 2025 were $4.1 million, focused on capacity expansion, increasing capabilities, and productivity improvements.

The Company had no debt outstanding as of September 30, 2025, with $44.7 million available on its revolving credit facility after taking into account outstanding letters of credit.

Orders, Backlog, and Book-to-Bill Ratio

See supplemental data filed with the Securities and Exchange Commission on Form 8-K and provided on the Company’s website for a further breakdown of orders and backlog by market. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics ($ in millions).

Orders for the second quarter of fiscal 2026 were $83.2 million. The increase in orders was across all our principle markets and included a $25.5 million follow-on order to provide mission-critical hardware for the MK48 Mod 7 Heavyweight Torpedo, as well as orders from leading Space/Aerospace customers. After-market orders for the Energy & Process and Defense markets for the second quarter of fiscal 2026 decreased $3.2 million to $9.6 million from the record levels of the prior year, but still remain strong.

Note that our orders tend to be lumpy given the nature of our business (i.e. large capital projects) and in particular, orders to the Defense industry, which span multiple years and can be significantly larger in size.

Backlog at quarter end was a record $500.1 million, a 23% increase over the prior-year period. Approximately 35% to 40% of orders currently in backlog are expected to be converted to sales in the next twelve months, another 25% to 30% are expected to convert to sales within one to two years, and the remaining beyond two years. Approximately 85% of our backlog as of September 30, 2025, was to the Defense industry, which we believe provides stability and visibility to our business.

Fiscal 2026 Outlook

Based upon the results for the first half of fiscal 2026, as well as our expectations for the remainder of the fiscal year, Graham is reiterating its full year fiscal 2026 guidance for all metrics.

The Company has reduced the high end of its previously announced fiscal 2026 tariff impact by $1.0 million. Graham now expects tariffs to have an estimated impact of approximately $2.0 million to $4.0 million on its consolidated financial results. The Xdot Bearing Technologies (“Xdot”) Acquisition announced in October 2025 does not materially impact this guidance.

Graham’s Chief Financial Officer, Christopher J. Thome, said, “Given the continued strength in demand, we are reaffirming our full-year guidance. As a reminder, our third quarter typically represents our seasonally lowest revenue period, reflecting normal holiday impacts on production schedules.”

Mr. Thome continued, “Additionally, we are narrowing our full-year estimated tariff impact range to $2.0 million to $4.0 million, down from the prior $2.0 million to $5.0 million. With a record backlog and solid order momentum, we remain confident in our full-year outlook and our ability to deliver consistent performance throughout the fiscal year.”

Expectations for sales and profitability assume that the Company will operate its production facilities at planned capacity, maintain access to its global supply chain and subcontractors, avoid significant global disruptions, and not be materially affected by unforeseen events.

Webcast and Conference Call

GHM’s management will host a conference call and live webcast on November 7, 2025 at 11:00 a.m. Eastern Time (“ET”) to review its financial results as well as its strategy and outlook. The review will be accompanied by a slide presentation, which will be made available immediately prior to the conference call on GHM’s investor relations website.

A question-and-answer session will follow the formal presentation. GHM’s conference call can be accessed by calling (201)-689-8560. Alternatively, the webcast can be monitored from the events section of GHM’s investor relations website.

A telephonic replay will be available from 3:00 p.m. ET today through Friday, November 14, 2025. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13756267 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “continue,” “estimate,” “expects,” “future,” “outlook,” “believes,” “could,” “guidance,” “may”, “will,” “plan” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, profitability of future projects and the business, its ability to deliver to plan, its ability to continue to strengthen relationships with customers in the Defense industry, its ability to secure future projects and applications, expected expansion and growth opportunities, anticipated sales, revenues, adjusted EBITDA, adjusted EBITDA margins, capital expenditures and SG&A expenses, the timing of conversion of backlog to sales, orders, market presence, profit margins, tax rates, foreign sales operations, customer preferences, changes in market conditions in the industries in which it operates, changes in general economic conditions and customer behavior, forecasts regarding the timing and scope of the economic recovery in its markets, and its acquisition and growth strategy, are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

Non-GAAP Financial Measures

Adjusted EBITDA is defined as consolidated net income (loss) before net interest expense, income taxes, depreciation, amortization, other acquisition related expenses, equity-based compensation, ERP implementation costs, and other unusual/nonrecurring expenses. Adjusted EBITDA margin is defined as Adjusted EBITDA as a percentage of sales. Adjusted EBITDA and Adjusted EBITDA margin are not measures determined in accordance with generally accepted accounting principles in the United States, commonly known as GAAP. Nevertheless, Graham believes that providing non-GAAP information, such as Adjusted EBITDA and Adjusted EBITDA margin, is important for investors and other readers of Graham’s financial statements, as it is used as an analytical indicator by Graham’s management to better understand operating performance. Moreover, Graham’s credit facility also contains ratios based on Adjusted EBITDA. Because Adjusted EBITDA and Adjusted EBITDA margin are non-GAAP measures and are thus susceptible to varying calculations, Adjusted EBITDA, and Adjusted EBITDA margin, as presented, may not be directly comparable to other similarly titled measures used by other companies.

Adjusted net income and adjusted net income per diluted share are defined as net income and net income per diluted share as reported, adjusted for certain items and at a normalized tax rate. Adjusted net income and adjusted net income per diluted share are not measures determined in accordance with GAAP, and may not be comparable to the measures as used by other companies. Nevertheless, Graham believes that providing non-GAAP information, such as adjusted net income and adjusted net income per diluted share, is important for investors and other readers of the Company’s financial statements and assists in understanding the comparison of the current quarter’s and current fiscal year’s net income and net income per diluted share to the historical periods’ net income and net income per diluted share. Graham also believes that adjusted net income per share, which adds back intangible amortization expense related to acquisitions, provides a better representation of the cash earnings of the Company.

Forward-Looking Non-GAAP Measures

Adjusted EBITDA and adjusted EBITDA margin are non-GAAP measures. The Company is unable to present a quantitative reconciliation of these forward-looking non-GAAP financial measures to their most directly comparable forward-looking GAAP financial measures because such information is not available, and management cannot reliably predict the necessary components of such GAAP measures without unreasonable effort largely because forecasting or predicting our future operating results is subject to many factors out of our control or not readily predictable. In addition, the Company believes that such reconciliations would imply a degree of precision that would be confusing or misleading to investors. The unavailable information could have a significant impact on the Company’s fiscal 2025 financial results. These non-GAAP financial measures are preliminary estimates and are subject to risks and uncertainties, including, among others, changes in connection with purchase accounting, quarter-end, and year-end adjustments. Any variation between the Company’s actual results and preliminary financial estimates set forth above may be material.

Key Performance Indicators

In addition to the foregoing non-GAAP measures, management uses the following key performance metrics to analyze and measure the Company’s financial performance and results of operations: orders, backlog, and book-to-bill ratio. Management uses orders and backlog as measures of current and future business and financial performance, and these may not be comparable with measures provided by other companies. Orders represent definitive agreements with customers to provide products and/or services. Backlog is defined as the total dollar value of net orders received for which revenue has not yet been recognized. Total backlog can include both funded and unfunded orders under government contracts. Management believes tracking orders and backlog are useful as they often times are leading indicators of future performance. In accordance with industry practice, contracts may include provisions for cancellation, termination, or suspension at the discretion of the customer.

The book-to-bill ratio is an operational measure that management uses to track the growth prospects of the Company. The Company calculates the book-to-bill ratio for a given period as net orders divided by net sales.

Given that each of orders, backlog, and book-to-bill ratio are operational measures and that the Company’s methodology for calculating orders, backlog and book-to-bill ratio does not meet the definition of a non-GAAP measure, as that term is defined by the U.S. Securities and Exchange Commission, a quantitative reconciliation for each is not required or provided.

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or “the Company”), a global leader in the design and manufacture of mission-critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space markets, today announced growing momentum in its commercial space business, supported by a series of recent orders from leading Space/Aerospace customers in aggregate value of approximately $22 million.

During its fiscal second and third quarters, Graham’s wholly owned subsidiary, Barber-Nichols LLC (“BN”), booked multiple new orders for advanced turbomachinery and precision-engineered components from six industry leading players in the commercial space launch market. These orders, which are expected to convert into revenue over the next 12 to 24 months, underscores the Company’s expanding role as being a critical supplier for next-generation space systems.

To support this continued demand, Graham is investing in production capacity and capabilities at its Colorado-based Barber-Nichols facility, including the addition of new CNC machining centers, a liquid nitrogen test stand, and supporting infrastructure to increase throughput and meet accelerating customer schedules. These investments are in addition to the previously announced cryogenic test facility the company is constructing near its P3 Technologies subsidiary in Jupiter, Florida expected to be opened later this year.

“We are seeing strong and sustained momentum from both new and existing customers in the space sector,” said Mike Dixon, General Manager of Barber-Nichols. “These orders reflect Barber-Nichols long commitment to the space industry and key development programs that support the commercial launch sector that are now beginning to transition to higher rate production. Our team’s expertise in high-speed rotating equipment and precision manufacturing continues to position us as a trusted supplier for complex, high-performance systems. With additional machining capacity and test capabilities coming online, we are well positioned to deliver on these programs and continue supporting our customers’ missions.”

Graham’s growing presence in the space market complements its established leadership across defense and energy end markets and reinforces the Company’s strategy to diversify its portfolio across high-growth, technology-driven applications.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “continue,” “expected,” “positions,” “will,” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, completion and profitability of future projects and the business, its ability to deliver to plan, potential revenues and timing of such revenues, capacity, demand growth, and delivering timely or otherwise on schedule are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries, announced that it will release its second quarter fiscal year 2026 financial results before financial markets open on Friday, November 7, 2025.

The Company will host a conference call and webcast to review its financial and operating results, strategy, and outlook. A question-and-answer session will follow.

Second Quarter Fiscal Year 2026 Financial Results Conference Call

Friday, November 7, 2025 11:00 a.m. Eastern Time Phone: (201) 689-8560 Internet webcast link and accompanying slide presentation: ir.grahamcorp.com

A telephonic replay will be available from 3:00 p.m. ET on the day of the teleconference through Friday, November 14, 2025. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13756267 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

ABOUT GRAHAM CORPORATION Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space, industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Graham Corporation designs, manufactures and sells critical equipment for the energy, defense and chemical/petrochemical industries. The Company designs and manufactures custom-engineered ejectors, vacuum pumping systems, surface condensers and vacuum systems. It is a nuclear code accredited fabrication and specialty machining company. It supplies components used inside reactor vessels and outside containment vessels of nuclear power facilities. Its equipment is found in applications, such as metal refining, pulp and paper processing, water heating, refrigeration, desalination, food processing, pharmaceutical, heating, ventilating and air conditioning. For the defense industry, its equipment is used in nuclear propulsion power systems for the United States Navy. The Company’s products are used in a range of industrial process applications in energy markets, including petroleum refining, defense, chemical and petrochemical processing, power generation/alternative energy and other.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

An Acquisition. Yesterday, after the market close, Graham announced the acquisition of certain specified assets of Xdot Bearing Technologies (“Xdot”), a specialized consulting, design, and engineering firm focused on foil bearing technology. While the acquisition price was not revealed, Graham noted Xdot has annual sales of approximately $1 million and is expected to be slightly accretive to the Company’s fiscal year 2026 GAAP net income.

Xdot. Xdot has developed and patented a breakthrough foil bearing design that delivers superior performance while lowering development and production costs. Xdot’s products are complementary to the existing product portfolio of Graham’s Barber-Nichols (BN) subsidiary and will expand capabilities within BN. Notably, Dr. Erik Swanson, Founder, President, and Chief Engineer of Xdot is a world renowned expert in foil bearing analysis, application, and fabrication and will join the BN team upon closing.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or “the Company”), a global leader in the design and manufacture of mission-critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space markets, today announced the appointment of Mauro Gregorio to its Board of Directors, effective September 1, 2025.

Mr. Gregorio brings extensive global executive leadership experience and board governance expertise to Graham Corporation. He currently serves as a board member at Eagle Materials, and most recently served as a Board member of Radius Recycling and was President of the Performance Materials & Coatings division at Dow Inc., where he oversaw a $10 billion business segment focused on several industrial sectors related to Energy and other complex manufacturing processes.

“We are delighted to welcome Mauro to Graham’s Board of Directors,” said Matthew J. Malone, President and CEO. “His proven track record of transforming organizations and driving performance improvements on a global scale aligns perfectly with our growth objectives. Mauro’s extensive experience in the Energy & Process markets and operational excellence will be invaluable as we continue to execute our strategic plan.”

During his tenure at Dow Inc., Mr. Gregorio held multiple leadership roles including Business President of Consumer Solutions and Business President for Energy Solutions. His international career spans leadership positions across Europe, Latin America, and the United States. He holds a Bachelor of Science in Chemical Engineering from Escola de Engenharia Maua in São Paulo and an MBA from Northwood University.

“I am honored to join Graham Corporation’s Board of Directors,” said Mr. Gregorio. “Graham’s commitment to innovation and operational excellence resonates strongly with me and my experience. I look forward to contributing to the Company’s continued success and helping drive long-term value creation for shareholders.”

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy, & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Graham Corporation designs, manufactures and sells critical equipment for the energy, defense and chemical/petrochemical industries. The Company designs and manufactures custom-engineered ejectors, vacuum pumping systems, surface condensers and vacuum systems. It is a nuclear code accredited fabrication and specialty machining company. It supplies components used inside reactor vessels and outside containment vessels of nuclear power facilities. Its equipment is found in applications, such as metal refining, pulp and paper processing, water heating, refrigeration, desalination, food processing, pharmaceutical, heating, ventilating and air conditioning. For the defense industry, its equipment is used in nuclear propulsion power systems for the United States Navy. The Company’s products are used in a range of industrial process applications in energy markets, including petroleum refining, defense, chemical and petrochemical processing, power generation/alternative energy and other.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

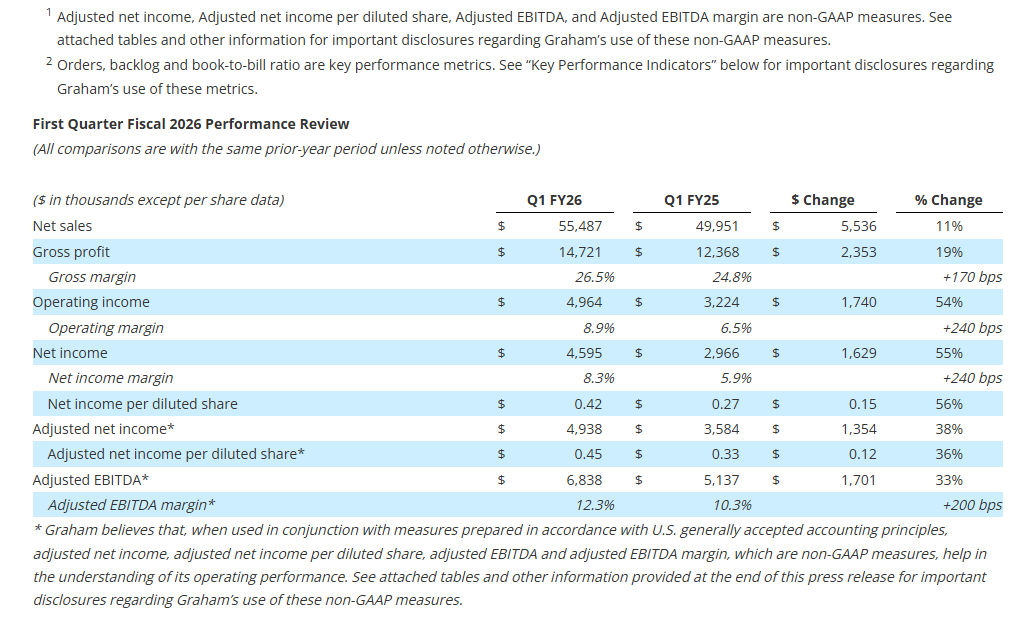

Strong Quarter. Driven by continued strength across the diversified product portfolio, Graham delivered another solid quarter to start fiscal 2026. A highlight was the Energy and Process markets with strong growth driven by execution on major commercial projects and robust aftermarket demand, along with increasing momentum in emerging energy segments.

1Q26 Results. Revenue increased 11% to $55.5 million, slightly above our $54 million estimate. Gross margin improved 170 bp to 26.5%. Adjusted EBITDA rose 33% y-o-y to $6.8 million, with adjusted EBITDA margin up 200 bp to 12.3%. We were at $5.1 million. EPS increased 56% to $0.42 with adjusted EPS up 36% to $0.45. We were at $0.22 and $0.25, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Revenue increased 11% to $55.5 million, reflecting the strength of the Company’s product portfolio and diversified revenue base

Gross profit increased 19% to $14.7 million; Gross margin improved 170 basis points to 26.5%

Net income per diluted share increased 56% to $0.42; adjusted net income per diluted share1 increased 36% to $0.45

Net income increased 55% to $4.6 million; Adjusted EBITDA1 increased 33% to $6.8 million; Adjusted EBITDA margin1 improved 200 basis points to 12.3%

Orders2 were $125.9 million, driven by large defense orders; Book-to-Bill ratio2 of 2.3x and backlog2 of $482.9 million

Strong balance sheet with no debt, $10.8 million in cash, and access to $44.3 million under its revolving credit facility at quarter end to support growth initiatives

Reiterating full year fiscal 2026 guidance for all metrics provided; Remain on track to reach strategic goal of 8% to 10% annual organic revenue growth and low to mid-teen Adjusted EBITDA margins by fiscal 2027

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries, today reported financial results for its first quarter for the fiscal year ending March 31, 2026 (“fiscal 2026”).

Graham’s President and Chief Executive Officer, Matthew J. Malone stated, “The start of fiscal 2026 demonstrates continued strength across our diversified product portfolio. We delivered strong growth in our Energy & Process markets, driven by execution on major commercial projects and robust aftermarket demand, along with increasing momentum in emerging energy segments such as small modular reactors (“SMRs”) and cryogenics. In addition, our Defense business continues to perform well, supported by recent follow-on orders, including $86.5 million to support the Virginia Class submarine program in May and $25.5 million for the MK48 Mod 7 Heavyweight Torpedo program in July, reaffirming our position as a trusted supplier to the U.S. Navy.”

Mr. Malone continued, “We remain focused on high-return initiatives that drive long-term value creation, including numerous in-process capital investments expected to generate returns above 20%. These initiatives include automated welding, enhanced radiographic testing technologies, and our new cryogenic testing facility in Florida, which we expect will improve margins and create new revenue opportunities. I’m also pleased to announce that we’ve completed the expansion of our Batavia defense facility this month. With these investments, we believe Graham is well-positioned to drive sustainable growth, deliver for our customers, and continue expanding margins.”

Quarterly net sales of $55.5 million increased 11%, or $5.5 million. Sales to the Energy & Process market contributed $5.7 million to growth driven by increased sales in the Chemical/Petrochemical and New Energy industries. The increase in Chemical/Petrochemical sales was largely due to a surface condenser order for a North American net-zero carbon emissions ethylene cracker received in June 2024, while the increase in New Energy sales was driven by increased sales to the hydrogen and SMR markets. Aftermarket sales to the Energy & Process and Defense markets of $10.4 million remained strong and were 33% higher than the prior year. See supplemental data for a further breakdown of sales by market and region.

Gross profit for the quarter increased $2.4 million to $14.7 million compared to the prior-year period of $12.4 million. As a percentage of sales, gross profit margin increased 170 basis points to 26.5%, compared to the first quarter of fiscal 2025. Increased leverage on fixed overhead costs due to the higher volume of sales discussed above, as well as an improved mix of sales related to higher margin aftermarket sales, and better execution and pricing on defense contracts were the primary drivers of this increase. For the first quarter of fiscal 2026, the impact of tariffs was not material to our consolidated financial statements in comparison to the prior year. However, we still estimate the range of potential impact of increased tariffs for the full year to be between $2 million to $5 million.

Selling, general and administrative expense (“SG&A”), including amortization, totaled $9.8 million, an increase of $0.6 million compared with the prior year. This increase reflects the investments we are making in our operations, our employees, and our technology. As a percentage of sales, SG&A, including amortization, of 17.7% decreased 90 basis points compared to the prior year period, reflective of our financial discipline.

Cash Management and Balance Sheet As expected, cash used by operating activities totaled $2.3 million for the quarter-ending June 30, 2025, primarily due to the payment of fiscal 2025 bonuses including the supplemental Barber-Nichols earnout bonus of $4.3 million in connection with the acquisition. As of June 30, 2025, cash and cash equivalents were $10.8 million, compared with $21.6 million as of March 31, 2025.

Capital expenditures for the first quarter fiscal 2025 were $7.0 million, focused on capacity expansion, increasing capabilities, and productivity improvements. All major capital projects are on time.

The Company had no debt outstanding as of June 30, 2025, with $44.3 million available on its revolving credit facility after taking into account outstanding letters of credit.

Orders, Backlog, and Book-to-Bill Ratio See supplemental data filed with the Securities and Exchange Commission on Form 8-K and provided on the Company’s website for a further breakdown of orders and backlog by market. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics ($ in millions).

Orders for the first quarter of fiscal 2026 increased to $125.9 million, including the remaining $86.5 million of a $136.5 million follow-on order in support of the U.S. Navy’s Virginia Class Submarine program. Aftermarket orders for the Energy & Process and Defense markets remained strong and totaled $10.5 million for the first quarter of fiscal 2026, increasing 16% over the prior year. Book-to-bill for the first quarter of fiscal 2026 was 2.3x. Note that orders tend to be lumpy given the nature of our business (i.e. large capital projects) and in particular, orders to the Defense industry, which span multiple years and can be significantly larger in size.

Backlog at quarter end was $482.9 million, a 22% increase over the prior-year period. Approximately 35% to 40% of orders currently in backlog are expected to be converted to sales in the next twelve months, another 25% to 30% are expected to convert to sales within one to two years, and the remaining beyond two years. Approximately 87% of our backlog at June 30, 2025, was to the Defense industry, which we believe provides stability and visibility to our business.

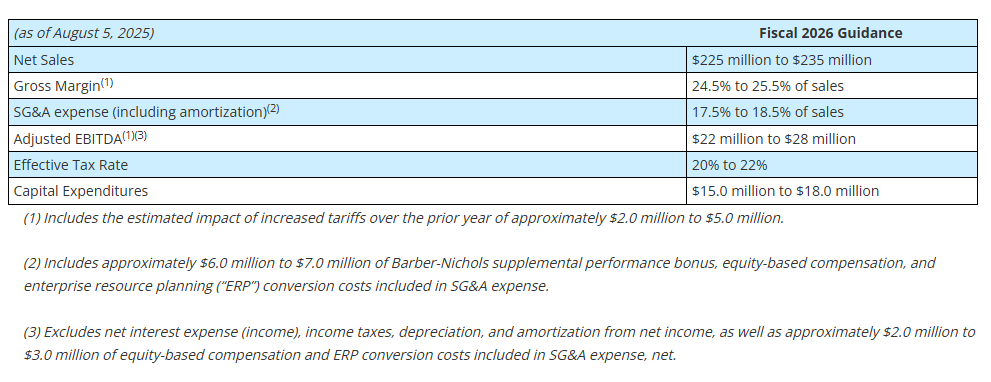

Fiscal 2026 Outlook Based upon the results for the first quarter of fiscal 2026, as well as our expectations for the remainder of the fiscal year, we are reiterating our full year fiscal 2026 guidance provided earlier this year as follows:

Our expectations for sales and profitability assume that we will be able to operate our production facilities at planned capacity, have access to our global supply chain including our subcontractors, do not experience any global disruptions, and experience no impact from any other unforeseen events.

Webcast and Conference Call GHM’s management will host a conference call and live webcast on August 5, 2025 at 11:00 a.m. Eastern Time (“ET”) to review its financial results as well as its strategy and outlook. The review will be accompanied by a slide presentation, which will be made available immediately prior to the conference call on GHM’s investor relations website.

A question-and-answer session will follow the formal presentation. GHM’s conference call can be accessed by calling (412)-317-5195. Alternatively, the webcast can be monitored from the events section of GHM’s investor relations website.

A telephonic replay will be available from 3:00 p.m. ET today through Tuesday, August 12, 2025. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 10201479 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

About Graham Corporation Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the Defense, Energy & Process, and Space industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.