The FOMC Votes to Raise Rates for Sixth Time (2022)

The Federal Open Market Committee (FOMC) voted to raise overnight interest rates from a target of 3.00%-3.25% to the new level of 3.75% – 4.00% at the conclusion of its November 2022 meeting. The monetary policy shift in bank lending rates was as expected by economists and the markets. The recent focus has been more on what the next move in December might look like. There were no clues given in the statement following the meeting. Many, including some members of Congress that recently wrote a letter to Chair Powell, have urged the Fed to be more dovish, while others suggest the central bank is still behind and hasn’t moved aggressively enough. A third contingent believes there may be more work to be done, but there should first be a pause to see what the impact has been of five aggressive moves.

The statement accompanying the policy shift also included a discussion on U.S. economic growth continuing to remain positive. There was little changed. Language from that statement can be found below:

Fed Release November 2, 2022

Recent indicators point to modest growth in spending and production. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher food and energy prices, and broader price pressures.

Russia’s war against Ukraine is causing tremendous human and economic hardship. The war and related events are creating additional upward pressure on inflation and are weighing on global economic activity. The Committee is highly attentive to inflation risks.

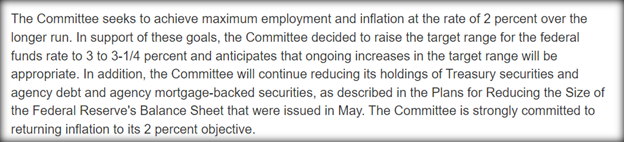

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 3-3/4 to 4 percent. The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in the Plans for Reducing the Size of the Federal Reserve’s Balance Sheet that were issued in May. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on public health, labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Take-Away

Higher interest rates can weigh on stocks as companies that rely on borrowing may find their cost of capital has increased. The risk of inflation also weighs on the markets. Additionally, investors find that alternative investments that pay a known yield may, at some point, be preferred to equities. For these reasons, higher interest rates are of concern to the stock market investor. However, an unhealthy, highly inflationary economy also comes at a cost to the economy, businesses, and households.

The next FOMC meeting is also a two-day meeting that takes place December 14-15. If the updates to GDP, the pace of employment, and overall economic activity is little changed, the Federal Reserve is expected to move again, perhaps not in as big of a step.

The Many Factors that Come Into a Fed Rate Decision are Mind Boggling

What do the FOMC members look at as they’re changing interest rates and whipping up new policy stances?

The Federal Open Market Committee, or FOMC, meets eight times a year. There are 12 members; seven are board members of the Federal Reserve System, and five are Reserve Bank presidents, including the president of the Federal Reserve Bank of New York, who serves as president of the committee. The group, as a whole, is arguably among the most powerful entities in the world. What is it that this group, that impacts all of us, focus on? And what specifically will they weigh into their decision at the current meeting?

Labor markets and prices are top on the Fed’s list and specifically part of their mandate. Also feeding into the mandate are contributing factors like housing, growth trends, and risks to monetary policy.

Prices (Inflation Rates)

Inflation remains elevated. In September, the Consumer Price Index (CPI) picked up to 0.4%. Energy prices declined in each month of the third quarter, dropping a cumulative 11.3% since June. The Fed will have to discern if this is sustainable or a function of oil reserve releases that will need replacing. Food prices continued high, although at a slower 0.8% increase during September.

Core CPI inflation (which strips out energy and food) started the third quarter at a somewhat slow pace—increasing just 0.3% in July. The trend went against the Fed as it rose by 0.6% in both August and September. Price growth for services was the largest contributor to an increase in core CPI in the third quarter.

One of the two mandates of the Federal Reserve is to keep inflation at bay. Chairman Powell has said they are targeting a 2% annual inflation level. While nothing that has been reported in price increases since the last meeting has approached that low of a target, the Fed also has to consider their tightening moves do not work to lower demand (especially in food and energy) rapidly.

The Federal Reserve’s preferred measure of inflation is the PCE price index; this is the measure they use with their 2% target. The PCE price index typically shows lower price growth than CPI because it uses a different methodology in its calculation, but the drivers of both measures remain similar. Over the year ending September, the headline PCE price index rose 6.2 percent, while the core PCE price index was up 5.1 percent.

Jobs (Employment and Wages)

Labor markets are still tight. The economy has added an additional 3.8 million jobs this year through September. This includes 1.1 million during the most recent quarter. During the third quarter, the U.S. economy exceeded pre-pandemic employment levels. The unemployment rate hasn’t budged much, and as of September, the rate held at a comfortable 3.5 percent rate.

The broadest measure of unemployment—the U-6 rate is a measure of labor underutilization that includes underemployment and discouraged workers, in addition to the unemployed. The U-6 rate has also remained behaved all year. It stood at 6.7 percent in September, the lowest rate in the history of the series (starting in January 1994).

When the Fed pushes on a lever for one of its mandates, in this case it is tightening to reign in inflation, it has to watch the impact on its other mandate, in this case, the job market. So far, there is nothing that has occurred on the employment side that should tell the Fed they have gone too far too fast.

.In fact, the labor numbers may suggest they should discuss whether they have moved nearly fast enough. Competition for employees continued as the economy added an additional 3.8 million through September 2022 (1.1 million during the third quarter). Notably, during the third quarter, the economy surpassed pre-pandemic employment levels as of August 2022.

Image: FOMC participants meet in Washington, D.C., for a two-day meeting on September 20-21, 2022, Federal Reserve (Flickr).

Housing Markets

Housing demand decreased in the third quarter as affordability (lending rates + prices), with economic uncertainty weighed on homebuyers. During September, 90% of all home sales were of existing homes. This pace declined 1.5 percent over the month (down 23.8 percent on a twelve-month basis). New single-family home sales dropped a large 10.9% in September; this was the seventh monthly decline.

Homes available for sale have now risen from all-time lows; this includes new and existing.

Over the past few years, home prices have increased dramatically; this was fueled by Fed policy. Prices still remain above longer-term trendlines. The Case-Shiller national house price index measures sales prices of existing homes; this was up 13% over the year ending August 2022. For reference, for the 12 months ended August 2021, prices rose 20%. The prior year they had only increased 5.8%.

Housing plays a huge role in economic health. The Fed is well aware of all the housing-related inputs to the 2008 financial crisis and the part easy money plays in market crashes. Orchestrating an orderly slowdown to the boom in housing is certainly critical to the Fed’s success.

Other Risks to Economy

Eight times a year, information related to each of the 12 Federal Reserve districts is gathered and bound in a publication known as theBeige Book. This summary of economic activity throughout the U.S. is provided approximately two weeks before each FOMC meeting, so members have a chance to evaluate economic activity over the diverse businesses the U.S. engages in.

U.S. Inflation can arise from conditions outside of the control of the U.S. For example Russia’s invasion of Ukraine has added upward pressure to inflation this year. This impact may have to be determined and netted out of calculations and policy as the Fed can’t fight this inflation pressure with monetary policy. An example would be the Fed can’t alter global food shortages brought on by war.

Dollar strength or weakness comes from many things. One of the most impactful is the difference in interest rates net of inflation between countries and their native currency. If the Fed raises rates when a competing currency has not, there is a chance there will be more demand for the alternative currency, which would weaken the dollar. Further complicating this for the Federal Resreve is a lower dollar is inflationary as it causes import prices to rise, a stronger dollar can reduce domestic economic activity as exports fall. The U.S. dollar has been rising and is now at its strongest in 20 years.

Commodity Prices were elevated in the first half of this year, mostly by energy. Although there was some relief from gas prices over the summer, energy is expected to rise into the colder months. They may rise further as the U.S. Strategic Petroleum Reserves are used less to control prices, this may be curtailed. The White House’s two goals of sharply reducing Russian revenue and avoiding further disruptions to global energy supplies while at the same time reducing oil use and production within the U.S. are a tanglement the Fed needs to consider. These can be very impactful to costs and economic activity, yet The Fed has no direct levers to impact these economic inputs.

World economies play a part in our own economic pace. If the Fed were to tighen aggressively while the global business is slowing, the impact of the tightening might be more pronounced than if the world economies are booming. Demand for goods and services impacts prices; the U.S. doesn’t live in a vacuum, and demand for our production and our demand for foreign production all must weigh on the Feds outlook for global economic health.

According to the IMF’s latest World Economic Outlook, global growth is expected to slow to 3.2 percent in 2022 and just 2.7 percent in 2023. At the same time, central banks around the world are tightening monetary policy to fight high global rates of inflation. In addition, there has been financial instability in some major world economies. These rising risks to the global growth outlook may feed back into the U.S. outlook by weakening international demand for U.S. goods and service exports. On the positive economic side, China is considering easing its Zero-COVID policy, which could eventually ease the supply chain impact to inflation.

Take Away

The original question was, “What do the FOMC members look at as they’re changing interest rates and whipping up new policy stances?” The answer is they have to look at everything. The recent mix of “everything” shows growth and employment in the U.S. have sustained at an even keel. Will previous rate hikes to calm inflation eventually take their toll? This is probably the big question the FOMC will be evaluating. Other domestic issues, including housing and the financial markets, are certainly to be weighed as well – a market crash of any magnitude could quickly slow economic activity.

The Fed has little control over what goes on overseas but must be aware of and hedge its policy to allow for.

All told, the Federal Reserve has a very difficult job. The report of the new monetary policy stance should hit the wire at 2 pm ET today (November 2).

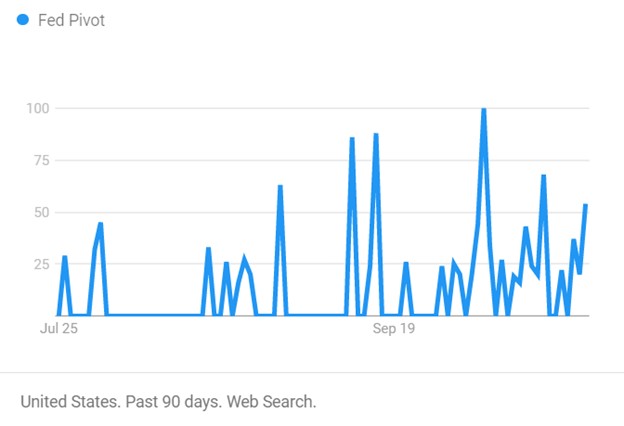

A Lack of Fed Pivot Doesn’t Have to Equate to Lower Stock Prices

The Fed is not likely to have suddenly indicated a pivot.

Despite the stock market rally and fresh news stories suggesting the Fed is indicating a more dovish stance, the notion has one problem. There are limits placed on Federal Open Market Committee (FOMC) participants and whether they can grant interviews or give speeches before policy-setting meetings. They can not interact on the subject of policy. The current blackout period began October 22nd and will carry through the November 2nd final meeting day. So, investors may wish to consider other reasons if the stock market is rallying. Earnings, oversold conditions, year-end rally, perhaps news stories created by bloggers or journalists that don’t possess experience or understanding.

Image: Number of times “Fed Pivot” was searched using Google

Current State of Tightening

This year the Fed has been tightening aggressively after having brought interest rates down aggressively a couple of years back. For many investors, a tightening cycle, ending with interest rates a safe margin above the inflation rate, is not something they can recall. This is because the Fed has been stabilizing employment during tricky times in a way that has lifted the markets out of whatever trouble there may have been. Rates have been well below the average 6% to 8% range. This has been going on since at least 2008 – by some measures, way before.

There have been five times since late Spring that investors and TV’s talking heads were convinced the Fed has gone too far and will now begin bringing rates back. So far, all the hoping has done nothing to help; the track record stands at zero for five. While it remains to be seen and heard what to expect from monetary policy starting mid-next week, the current inflation rate and words that the Fed board members have said indicate another 75 bp hike in funds.

Looking Forward

Can this change? We get a look at third-quarter GDP on Thursday. This measures U.S. domestic production. A bad number could cause the Fed to rethink aggressive tightening. However, the expectations are that it will be higher than it has been all year (2.3% growth rate) which gives the Fed even greater ability to hit the brakes. Also, the PCE Price Index, viewed as the Fed’s preferred inflation indicator, is released Friday (6.3% YoY expected).

The Federal Reserve’s, monetary policy does not cater to the stock market. It does consider it because, of the wealth effect. The wealth effect is where consumers feel poorer because of declines in asset values, and while their disposable income may not have changed, they hunker down and spend less. This secondary impact to spending is the only attention the Fed officially pays to stocks.

Interest Rates

Real interest rates are still negative. Imagine buying a bond knowing that despite being exposed to maturity and credit risk, while tying up money, your spending power will almost certainly be less when it matures. This isn’t why people invest; in fact, if that scenario remains and inflation persists, the best use of savings may be to consider any large purchases you think you may incur in the coming few years and make them now. At the moment, inflation hasn’t shown signs of abating, something has to give; bond investors are going to require higher yields, Japan has already experienced a bond-buyer “strike.”

Where Do We Go from Here

For now, the consensus view is that inflation should drift back down to 3% or even lower by 2025. If energy continues to decline, supply-chain issues are resolved, and a strong U.S. dollar persists, the consensus may be correct. But one should be aware there are very bright economists that deviate from the consensus by plus or minus 300 bp or more.

The markets may have already priced in bad news; rates heading back to normalcy (upward) doesn’t immediately mean a bad stock market. We can easily rally through the end of the year and still experience a sixth time the Fed has refrained from pivoting but instead has made sure its words were cleansed of anything that can be construed as reversing course.

Will the November Fed rate announcement cause a stock market rally?

The next time the Federal Reserve is expected to adjust the target range of the Fed Funds overnight lending rate is Wednesday, November 2nd. Few have doubt at this point that this will again be a 0.75% increase. That level is already baked into equities. Stock market strength and direction shouldn’t veer much from the rate move but could dramatically turn as a result of the Fed’s forward guidance. If Chairman Powell & Co. suggests a slower benchmark lending rate increase, it would be a very welcome sign for investors.

Focus on the Post Meeting Announcement

There are already signs the Fed may slow the pace of Fed Funds increases. There are also indications it may alter its quantitative tightening (QT) in a way that could quicken a yield curve steepening. In other words, the speed of QT may increase. To date, the real rate of return on bonds, of most all maturities, is viewed as unnatural as they are below zero (Yield – Inflation = Real Rate). While an increase in QT may do more to raise rates and reduce the money supply, the effect is stealthier; it doesn’t provide a panicky headline for investors to react to abruptly.

Some Fed governors have already shown signs that they believe the best course from here is to slow the ratcheting up of the funds level and perhaps even stop raising Fed Funds rates early next year. A hiatus would allow them time to see if the moves have had an impact and give members a chance to see if further moves are prudent. The Fed always runs the risk of overreacting and going too far when tightening; this “oversteering” by previous Feds has occurred a high percentage of the time as they contend with a lag between monetary policy shifts and economic reaction.

Where We Are, Where We’re Going

In the most aggressive pace since early 1980, so far in 2022, the Fed raised its benchmark federal-funds rate by 0.75 points at each of its past three meetings. The most recent move was in late September. This left the overnight interest rate at a range between 3% and 3.25%.

The stock market wants the Fed to slow down. It rallied in July and August on expectations that the Fed might slow the pace of increase. Slowing, at least at the time, would have conflicted with the central bank’s inflation target because easy financial conditions stimulate spending, economic growth, and related inflation pressures. This rally in stocks may have prompted Powell to redraft a very public speech to economists in late August. He spoke about nothing else for eight minutes at Jackson Hole except for his resolve to win the fight against higher prices.

But sentiment related to how forceful the FOMC now needs to be may be shifting. Fed Vice Chairwoman Lael Brainard, joined by other officials, have recently hinted they are uneasy with raising rates by 0.75 points beyond next month’s meeting. In a speech on Oct. 10th, Brainard laid out a case for pausing rate rises, noting how they impact the economy over time.

Others that are concerned about the danger of raising rates too high include Chicago Fed President Charles Evans. Evans told reporters on Oct. 10th that he was worried about assumptions that the Fed could just cut rates if it decided they were too high. He felt a need to share his thought that promptly lowering rates is always easier in theory than in practice. The Chicago Fed President said he would prefer to find a rate level that restricted economic growth enough to lower inflation and hold it there even if the Fed faced “a few not-so-great reports” on inflation. “I worry that if the way you judge it is, ‘Oh, another bad inflation report—it must be that we need more [rate hikes],’… that puts us at somewhat greater risk of responding overly aggressive,” Evans said.

Kansas City Fed President Esther George also had something to say on this topic last week. She said she favored moving “steadier and slower” on rate increases. “A series of very super-sized rate increases might cause you to oversteer and not be able to see those turning points,” according to the Kansas City Fed President.

Others like Fed governor Waller don’t view steady 0.75% increases as a done deal but instead something to be reviewed, “We will have a very thoughtful discussion about the pace of tightening at our next meeting,” Waller said in a speech earlier this month.

The caution surrounding oversteering isn’t unanimous; at least one Fed official wants to see proof that inflation is falling before easing up on the economic brake pedal. “Given our frankly disappointing lack of progress on curtailing inflation, I expect we will be well above 4% by the end of the year,” said Philadelphia Fed President Patrick Harker.

The ultimate result is likely to come down to what Mr. Powell decides as he seeks to fashion a consensus. In the past, votes, while not always unanimous, tend to defer to the Chairperson at the time.

Take-Away

If, after the next FOMC meeting, the Fed is entertaining a lower 0.50% rate rise in December (not 0.75%), they will prepare the markets (bond, stock, and foreign exchange) for the decision in the moments and weeks following their Nov. 1-2 meeting. If this occurs, it could cause stocks to perform well just before election day and perhaps make up some lost ground in the year’s final two months.

The Federal Open Market Committee (FOMC) voted to raise overnight interest rates from a target of 2.25%-2.50% to the new level of 3.00% – 3.25% at the conclusion of its September 2022 meeting. The monetary policy shift in bank lending rates was as expected by economists, although many have urged the Fed to be more dovish, others suggest the central bank is behind and should move more quickly. The early reaction from the U.S. Treasury 10-year note ( a benchmark for 30-year mortgage rates) is downward slightly, while the S&P sold off 26 points and the Russell 2000 remained unfazed. Equities later sold off as the Chairman held a press conference.

The statement accompanying the policy shift also included a discussion on U.S. economic growth continuing to remain positive. The FOMC statement said recent indicators point to modest growth in spending and production. Job gains were also seen as strong in recent months, and the unemployment rate remains low.

However, the statement points out that inflation remains elevated. The Fed believes this reflects supply and demand imbalances related to the pandemic, higher food and energy prices, and broader price pressures.

Russia’s war against Ukraine is causing tremendous human and economic hardship, according to the Fed. The statement indicated the inflation risks related to the is an area they are paying attention to.

Source: FOMC Statement (September 21, 2022)

The Federal Reserve made clear it was continually assessing the appropriate actions related to monetary policy and the implications of incoming information on the economic outlook. The Committee says it is prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede reaching the Committee’s goals. This is to include a wide range of information, including readings on public health, labor market conditions, inflation pressures and inflation expectations, and financial and international developments, according to the statement.

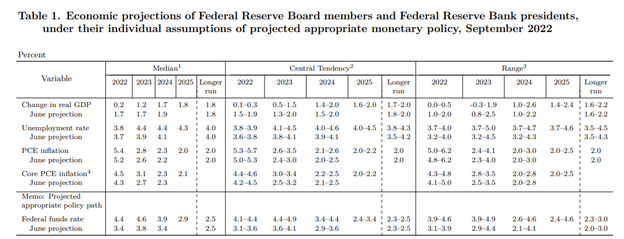

Source: Federal Reserve Board and Federal Open Market Committee release economic projections from the September 20-21 FOMC meeting

Each member of the Federal Open Market Provides forward-looking assumptions on expected growth, employment, inflation, and individual projections of future interest rate policy. The table above indicates the range of expectations.

Take-Away

Higher interest rates can weigh on stocks as companies that rely on borrowing may find their cost of capital has increased. The risk of inflation also weighs on the markets. Additionally, investors find that alternative investments that pay a known yield may, at some point, be preferred to equities. For these reasons, higher interest rates are of concern to the stock market investor. However, an unhealthy, highly inflationary economy also comes at a cost to the economy, businesses, and households.

The next FOMC meeting is also a two-day meeting that takes place July 26-27. If the pace of employment and overall economic activity is little changed, the Federal Reserve is expected to again raise interest rates.

The Federal Reserve (the Fed) will be holding a two-day Federal Open Market Committee (FOMC) meeting next week that ends on September 21. After the FOMC meeting, it is the current practice for the Fed to announce what the target Fed Funds range will be. That is, make the public aware of what overnight bank loan rate the Federal Reserve will work to maintain through open market operations.

Open market operations is the Federal Reserve buying and selling securities on the open market. The purchases are restricted to debt or debt-backed securities so that interest rates are impacted. It’s through controlling interest rates that the Fed works to maintain a sound banking system, keep inflation under control, and help maximize employment. Purchasing securities through its account puts money into the economy, which lowers rates and helps stimulate economic activity. Selling securities takes cash out of circulation. This tightens money’s availability and can also be accomplished by letting the financial instrument mature and then not replacing them with an equal purchase.

Quantitative Easing

If the Federal Reserve hadn’t put money into the economy, they’d have nothing to sell or allow to mature (roll-off). With this in mind, the natural position of the Federal Reserve Bank is stimulative.

Currently, the Fed owns about a third of the U.S.Treasury and mortgage-backed-securities (MBS) that have been issued and are still outstanding. Much of these holdings are a result of its emergency asset-buying to prop up the U.S. economy during the Covid-19 efforts.

Two years of quantitative easing (QE) doubled the central bank’s holdings to $9 trillion. This amount approximates 40% of all the goods and services produced in the U.S. in a year (GDP). By putting so much money in the economy, the cost of the money went down (interest rates), and the excess money, without much of an increase in how many stocks, bonds, or houses there are, made it easier for people to bid prices up for investible assets. For non-investments, the combination of easy money while lockdowns slowed production became a recipe for inflation.

Inflation

Inflation is now a concern for the average household. The Fed, which is supposed to keep inflation slow and steady, needs to act, so they are changing the current mix. It is making these changes by taking out a key inflation ingredient, easy money. This same easy money has been a contributor to the ever-increasing market prices for stocks, bonds, and real estate.

The overnight lending rate the Fed is likely to alter next week is the policy that will create headlines. These headlines may cause kneejerk market reactions that are often short-lived. It is the extra trillions being methodically removed from the economy that will have a longer-term impact on markets. These don’t have much impact on overnight rates, their maturities average much longer, so they impact longer rates, and of course spendable and investible cash in circulation.

Quantitative Tightening

The central bank has only just started to shrink its holdings by letting no more than $30 billion of Treasuries and $17.5 billion of MBS, roll off (cash removed from circulation). They did this in July and again in August. The Fed then has plans to double the amount rolling off this month (most Treasuries mature on the 15th and month-end).

This pace is more aggressive than last time the Fed experimented with shrinking its balance sheet.

Will this lower the value of stocks, crash the economy, and make our homes worth the same as 2019? A lot depends on market expectations, which the Fed also helps control. If the markets, which knows the money that was quickly put in over two years, is now coming back out at a measured pace, and trusts the Fed to not hit the brake pedal too hard, the means exist to succeed without being overly disruptive. If instead the forward-looking stock market believes it sees disaster, an outcome that feels like a disaster increases in likelihood. For bonds, if the Fed does it correctly, rates will rise, which makes bonds cheaper. You’d rather not hold a bond that has gotten cheaper for the same reason that you don’t want to hold a stock that has gotten cheaper. However, buying a cheaper bond means you earn a higher interest rate. This is attractive to conservative investors but also serves as an improved alternative for those deciding to invest in stocks or bonds.

Houses are regional, don’t trade on an exchange and unlike securities, are each unique. They are often purchased with a long-term mortgage. Higher interest rates increase payment costs on the same amount of principal. In order to keep those payments affordable, home purchasers may demand a lower price, thereby causing real estate values to decline.

Take Away

The Fed has told us to expect tightening. They were honest when they promised to ease more than two years ago; there is no reason not to plan for higher rates and tighter money. The overnight rate increases get most of the attention. Further, out on the yield curve, the way quantitative tightening plays out depends on trust in the Fed and a lot of currently unknowns.

Fed Chairman Powell Shows His Steady Hand and Firm Conviction at Monetary Conference

In what is his last scheduled public appearance before the post-FOMC statement expected on Sept. 21, Fed Chairman Powell did not say anything that would change expectations of another 75bp Fed Funds rate hike. He instead emphasized the Fed’s commitment to reduce inflation and believes it can be done and at the same time avoid “very high social costs.”

“It is very much our view, and my view, that we need to act now forthrightly, strongly, as we have been doing, and we need to keep at it until the job is done,” Powell said Thursday (Sept. 8) at the 40th annual Monetary Conference held virtually by the Cato Institute.

The discussion was held after it was known that the Eurozone Central Bank had just raised rates by 75bp. Powell’s talk and the interest rate hike overseas didn’t upset U.S. markets as U.S. Jobless claims had been reported earlier and showed a very strong labor market which helped demonstrate that the Fed’s actions to return inflation to a more acceptable level are not severely hurting business.

The Federal Reserve Chairman continued to reiterate what he has been saying, that the U.S. central bank is focused on bringing down high inflation to prevent it from becoming entrenched as it did in the 1970s. The core theme, most recently heard at the Jackson Hole Economic Symposium, is that he is resolved to return inflation to the Fed’s 2% target.

Mr. Powell said it is critical to prevent households and businesses from ongoing expectations that inflation will rise. He said this is a key lesson taken from the persistent inflation of the 1970s. “The public had really come to think of higher inflation as the norm and to expect it to continue, and that’s what made it so hard to get inflation down in that case,” Powell said. The takeaway for policymakers, he added, is that “the longer inflation remains well above target, the greater the risk the public does begin to see higher inflation as the norm, and that has the capacity to really raise the costs of getting inflation down.”

Speaking the day before at the Economic Outlook and Monetary Policy at The Clearing House and Bank Policy Institute Annual Conference, Fed Vice Chairwoman Lael Brainard, didn’t express a preference on the size of the next increase but underscored the need for rates to rise and stay at levels that would slow economic activity. “We are in this for as long as it takes to get inflation down,” she said.

Fed officials have raised rates this year at the most rapid pace since the early 1980s. The federal funds rate, the percentage banks charge each other for overnight borrowing, rose from near zero in March to a range between 2.25% and 2.5% in July, which is where it sits today.

Take Away

The Fed’s two mandates are to keep inflation at bay and to make sure there are adequate jobs in the U.S. The lessons of the past indicate that expectations of inflation are inflationary themselves. The Fed Chairman and Fed Vice Chairwoman would undermine their goals if they did not talk tough on inflation. With the economy not having sunk into a deep recession, and joblessness at acceptable levels, their actions are likely to match their tough talk.

The stock market typically behaves well when confident that the Fed is fighting inflation and has a steady grasp of what too far is. Overly tight money would dampen business growth.