Anfield Energy Inc. (TSX.V: AEC; NASDAQ: AEC; FRANKFURT: 0AD) announced it has entered into a definitive agreement to acquire BRS Inc., a Wyoming-based engineering and consulting firm specializing in uranium and vanadium projects. The transaction represents a strategic step toward strengthening Anfield’s internal technical capabilities as the company advances its portfolio toward near-term production.

BRS has served as a long-standing technical partner to Anfield since 2014, providing engineering, geology, mine development, and construction management services across multiple assets. The firm has authored numerous technical reports, Preliminary Economic Assessments (PEAs), and resource updates for projects including Slick Rock, the West Slope Projects, and the Velvet-Wood Mine. By integrating BRS directly into its operations, Anfield aims to streamline project execution while reducing reliance on third-party consultants.

The acquisition brings decades of specialized expertise in uranium exploration, in-situ recovery (ISR), conventional mining, and mill reactivation directly under Anfield’s corporate umbrella. Douglas L. Beahm, founder of BRS and Anfield’s Chief Operating Officer, will continue in his executive role while serving as principal engineer. Beahm is a Qualified Person under NI 43-101 with more than 50 years of experience in uranium resource development, mine operations, and regulatory permitting seen as critical to Anfield’s growth strategy.

From an operational standpoint, the transaction is expected to improve cost efficiency and shorten development timelines across Anfield’s asset base. Internalizing engineering and technical functions allows the company to move more quickly on resource updates, economic studies, permitting applications, and mine planning activities. This is particularly relevant as Anfield continues efforts toward restarting the Shootaring Canyon mill, which anchors its hub-and-spoke development strategy in the U.S.

Beyond operational efficiencies, the acquisition also creates new growth avenues. BRS is expected to expand its external consulting services with the support of a publicly traded platform, potentially offering turnkey development solutions to third-party toll-mill partners. The expanded technical team may also help Anfield identify and evaluate acquisition opportunities more rapidly, supporting resource expansion and portfolio optimization.

The deal terms include total cash consideration of US$5 million paid to Beahm over a two-year period. An initial payment of US$1.5 million will be made at closing, followed by US$1.5 million after the first anniversary and a final US$2 million payment after the second anniversary. No securities will be issued as part of the transaction, and no finder’s fees are payable. Completion of the acquisition remains subject to customary closing conditions and regulatory approvals.

As a related-party transaction under Multilateral Instrument 61-101, the acquisition qualifies for exemptions from formal valuation and minority shareholder approval requirements, as the total consideration does not exceed 25% of Anfield’s market capitalization.

Anfield Energy is a uranium and vanadium development company focused on building a vertically integrated domestic energy fuels platform. The acquisition of BRS marks a meaningful step toward that goal, enhancing internal technical depth while positioning the company to advance its projects more efficiently amid rising demand for U.S.-based uranium supply.

Vancouver, British Columbia–(Newsfile Corp. – December 15, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) announces that its Board of Directors has approved grants of incentive restricted share units (“RSU”) and stock options.

Restricted Share Units

Under the Company’s Restricted Share Unit Plan (the “Plan”), RSUs may be granted to directors, employees, and contractors of the Company. At the discretion of the Company’s Board of Directors, the Plan permits the Company to either redeem RSUs for cash or by issuance of Hemisphere’s common shares.

On December 12, 2025, the Company awarded 930,000 incentive RSUs to directors and officers of Hemisphere, all of which will vest one-third annually over a three-year period and will expire on December 15, 2028.

Stock Options

Additionally, in accordance with the Company’s Stock Option Plan, Hemisphere has granted 48,000 incentive stock options to its investor relations service provider on December 15, 2025 at an exercise price of $2.01 per share which will vest quarterly over 12 months and expire on December 15, 2030.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood enhanced oil recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

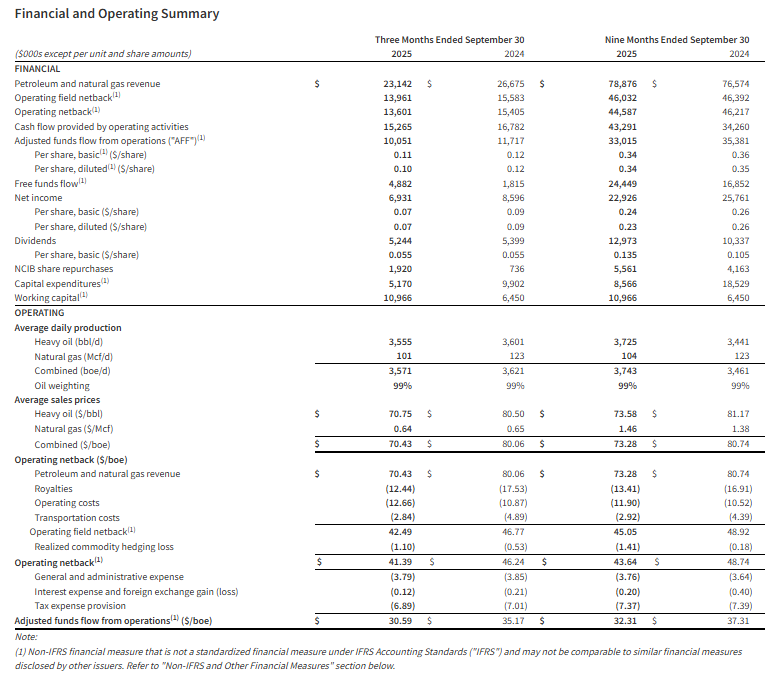

Vancouver, British Columbia–(Newsfile Corp. – November 25, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) provides its financial and operating results for the three and nine months ended September 30, 2025, declares a quarterly dividend payment to shareholders, and provides an operations update.

Q3 2025 Highlights

Attained quarterly production of 3,571 boe/d (99% heavy oil).

Generated quarterly revenue of $23.1 million.

Achieved total operating and transportation costs of $15.50/boe.

Delivered operating netback1 of $13.6 million or $41.39/boe for the quarter.

Realized quarterly adjusted funds flow from operations (“AFF”)1 of $10.1 million or $30.59/boe.

Initiated a 2025 fall drilling program with $5.2 million in capital expenditures1.

Generated quarterly free funds flow1 of $4.9 million.

Exited the third quarter with a positive working capital1 position of $11.0 million.

Paid a special dividend of $2.9 million ($0.03/share) to shareholders on August 15, 2025.

Paid a quarterly base dividend of $2.4 million ($0.025/share) to shareholders on September 12, 2025.

Purchased and cancelled 1.0 million shares for $1.9 million under the Company’s Normal Course Issuer Bid (“NCIB”).

Renewed the Company’s NCIB.

(1) Operating netback, adjusted funds flow from operations (AFF), free funds flow, capital expenditures, and working capital are non-IFRS measures, or when expressed on a per share or boe basis, non-IFRS ratio, that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Non-IFRS financial measures and ratios are not standardized financial measures under IFRS and may not be comparable to similar financial measures disclosed by other issuers. Refer to the section “Non-IFRS and Other Specified Financial Measures”.

Selected financial and operational highlights should be read in conjunction with Hemisphere’s unaudited condensed interim consolidated financial statements and related notes, and the Management’s Discussion and Analysis for the three and nine months ended September 30, 2025 which are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Quarterly Dividend

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on December 30, 2025 to shareholders of record as of the close of business on December 9, 2025. The dividend is designated as an eligible dividend for income tax purposes.

With the payment of the fourth quarter dividend, Hemisphere anticipates returning a minimum of $21.6 million to shareholders in 2025, including $9.6 million in quarterly base dividends, $5.8 million in two special dividends, and $6.2 million through NCIB share repurchases and cancellations. Based on the Company’s current market capitalization of $205 million (94.6 million shares issued and outstanding at a market close price of $2.17 per share on November 24, 2025), this represents an annualized yield of 10.5% to Hemisphere’s shareholders.

Operations Update

During the third quarter of 2025, Hemisphere’s production averaged 3,571 boe/d (99% heavy oil), representing a slight decrease of approximately 1% from the same period in 2024. The Company completed a number of workovers during the summer months, which contributed to production downtime during the quarter. However, September production of approximately 3,800 boe/d (99% heavy oil) was back in line with average levels of 3,830 boe/d (99% heavy oil) during the first six months of the year. This performance highlights the stability and low-decline characteristics of Hemisphere’s polymer flood assets in Atlee Buffalo, particularly given that no new wells had been placed on production since the Company’s third-quarter drilling program in 2024.

Throughout 2025, Hemisphere has taken a cautious approach to capital spending amid volatility in the global economy and oil markets, which resulted in delaying its drilling program until later in the year. In September the Company commenced a fall drilling program, which finished in early November. The new wells have just recently been put on production and will continue to be optimized over the coming months.

In October, Hemisphere successfully completed a scheduled facility turnaround and resolved unexpected issues with its power generation and injection systems. Although this short-term disruption will affect overall fourth-quarter production, all systems are now fully operational. November production has averaged approximately 3,800 boe/d (99% heavy oil, field estimate from November 1-22, 2025). Management anticipates fourth-quarter production will range between 3,400 – 3,500 boe/d (99% heavy oil) following this outage.

At the Company’s Marsden, Saskatchewan property, Hemisphere is continuing to evaluate its polymer pilot project. It has been approximately one year since injection commenced, and while an oil production response has not yet been noted, the data being collected is providing insights into reservoir performance. The Hemisphere team plans to advance its pilot project by evaluating the potential effects of producer/injector well spacing, polymer type and injection water, as well as reservoir heterogeneity and composition.

During its fall drilling program, Hemisphere attempted to test a second oil-bearing zone within its Marsden landbase. Unfortunately, drilling challenges prevented Hemisphere from being able to access the reservoir, and the Company is reviewing alternatives for future evaluation of the prospect.

Management anticipates WTI oil prices will average close to US$65 per barrel in 2025 and expects to exceed Hemisphere’s adjusted funds flow guidance estimate of $40 million for this price scenario, while projecting total capital expenditures to be on budget. This outlook holds despite the Company deferring its drilling program until late in the third quarter and experiencing unscheduled production downtime in the second half of the year. As a result, Hemisphere now estimates average annual 2025 production will be approximately 3,600 – 3,700 boe/d (99% heavy oil), compared to its original guidance of 3,900 boe/d (99% heavy oil).

The Company expects to release details on its 2026 guidance in January as part of its forward development planning. Supported by approximately $11 million in working capital, an undrawn credit facility, and strong cash flow from its low-decline production base, Hemisphere is well positioned with a robust balance sheet to pursue potential acquisition opportunities while continuing to deliver shareholder returns.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood enhanced oil recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Graham Corporation designs, manufactures and sells critical equipment for the energy, defense and chemical/petrochemical industries. The Company designs and manufactures custom-engineered ejectors, vacuum pumping systems, surface condensers and vacuum systems. It is a nuclear code accredited fabrication and specialty machining company. It supplies components used inside reactor vessels and outside containment vessels of nuclear power facilities. Its equipment is found in applications, such as metal refining, pulp and paper processing, water heating, refrigeration, desalination, food processing, pharmaceutical, heating, ventilating and air conditioning. For the defense industry, its equipment is used in nuclear propulsion power systems for the United States Navy. The Company’s products are used in a range of industrial process applications in energy markets, including petroleum refining, defense, chemical and petrochemical processing, power generation/alternative energy and other.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. Graham put up solid results for the second quarter of fiscal 2026. The Company executed well across all the business lines, driving broad based-growth. Demand across the end markets remains healthy, and the Defense and Space markets continue to see robust activity.

2Q26 Results. Revenue grew 23% to $66 million, driven by solid performance across all end markets. We were at $59 million. Adjusted EBITDA was $6.3 million, up 12% from the prior year, and adjusted EBITDA margin was 9.5%. We had forecasted $6.2 million and 10.4%. Net income for the quarter was $0.28 per diluted share, and adjusted net income was $0.31 per diluted share. We were at $0.30 and $0.32, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, Nov. 3, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.09 per common share payable on November 28, 2025, to shareholders of record at the close of business on November 14, 2025. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

SOURCE InPlay Oil Corp.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632, www.inplayoil.com; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

Deal positions Bloom as a preferred power provider for Brookfield’s global AI factories and marks Brookfield’s first investment in its dedicated AI Infrastructure strategy

Shares of Bloom Energy (NYSE: BE) surged more than 20% in early trading Monday after the company announced a $5 billion strategic partnership with Brookfield Asset Management (NYSE: BAM, TSX: BAM) to develop and power next-generation AI infrastructure.

Under the agreement, Brookfield will invest up to $5 billion to deploy Bloom’s advanced fuel cell technology as the companies collaborate on the design and construction of “AI factories” — large-scale data centers purpose-built to meet the surging compute and energy demands of artificial intelligence. Bloom Energy will serve as Brookfield’s preferred onsite power provider for these facilities worldwide.

The partnership marks the first phase of a joint AI infrastructure vision and represents Brookfield’s inaugural investment through its newly established AI Infrastructure strategy, which focuses on power, compute, and capital integration for AI data centers. The two companies plan to announce their first European site before the end of the year.

“AI infrastructure must be built like a factory — with purpose, speed, and scale,” said KR Sridhar, Founder, Chairman and CEO of Bloom Energy. “AI factories demand massive power, rapid deployment and real-time responsiveness that legacy grids cannot support. Together with Brookfield, we’re creating a new blueprint for powering AI at scale.”

“Behind-the-meter power solutions are essential to closing the grid gap for AI factories,” added Sikander Rashid, Global Head of AI Infrastructure at Brookfield. “Bloom’s advanced fuel cell technology gives us the unique capability to design and construct modern AI factories with a holistic and innovative approach to power needs.”

A Blueprint for the AI Era

AI data centers are projected to require over 100 gigawatts of power in the U.S. alone by 2035, according to industry estimates. Bloom Energy’s solid oxide fuel cells generate electricity through chemical reactions rather than combustion, providing clean, resilient, and rapidly deployable onsite power — an attractive alternative to traditional grid dependency.

Bloom has already installed hundreds of megawatts of fuel cell systems supporting data centers for American Electric Power, Equinix, and Oracle. The company’s systems can be scaled modularly, reducing construction timelines and improving energy efficiency for high-demand AI applications.

Brookfield, one of the world’s largest alternative asset managers with over $1 trillion in assets under management, has been expanding aggressively into digital and energy infrastructure. Recent commitments include $9.98 billion to develop an AI data center in Sweden and €20 billion for AI projects in France. The firm also holds major stakes in Compass Datacenters, Duke Energy Florida, Colonial Enterprises, and Hotwire Communications, and recently inked a deal to supply Google with up to 3 GW of hydro power in the U.S.

Strategic Implications

The partnership underscores a growing convergence between energy technology and AI infrastructure. As the global race to build AI data centers accelerates, the need for reliable, low-carbon power sources has become a critical bottleneck. Brookfield’s capital and infrastructure expertise, combined with Bloom’s clean power solutions, could provide a scalable model for sustainable AI expansion.

For Bloom Energy, the partnership offers both near-term revenue visibility and long-term positioning at the center of AI-driven energy demand growth. For Brookfield, it establishes a strategic foothold in the AI ecosystem— one that aligns with its global energy transition and infrastructure investment priorities.

Transaction strengthens IsoEnergy’s top-tier uranium portfolio with Toro’s flagship Wiluna Project and expands presence in key global jurisdictions amid rising nuclear demand

IsoEnergy Ltd. (NYSE American: ISOU) and Toro Energy Ltd. (ASX: TOE) have entered into a scheme implementation deed under which IsoEnergy will acquire all issued and outstanding ordinary shares of Toro. The all-stock transaction will create a globally diversified uranium developer with significant resources and near-term production potential across Canada, the United States, and Australia.

Under the terms of the agreement, Toro shareholders will receive 0.036 IsoEnergy shares for each Toro share held, representing a 79.7% premium to Toro’s last traded price and a 92.2% premium to its 20-day volume-weighted average price (VWAP). Upon completion, IsoEnergy and Toro shareholders will own approximately 92.9% and 7.1%, respectively, of the combined company on a fully diluted basis. The deal values Toro at approximately AUD 75 million (CAD 68 million / USD 49 million) and is expected to close in the first half of 2026, subject to shareholder and regulatory approvals.

A Strengthened Uranium Platform

The merger will add Toro’s Wiluna Uranium Project in Western Australia — comprising the Centipede-Millipede, Lake Way, and Lake Maitland deposits — to IsoEnergy’s existing portfolio, which includes the ultra-high-grade Hurricane deposit in Canada’s Athabasca Basin, several past-producing U.S. uranium mines, and other exploration assets across North America and Australia.

The combined resource base will include:

55.2 million pounds U₃O₈ (M&I) and 4.9 million pounds U₃O₈ (Inferred) compliant under NI 43-101

78.1 million pounds U₃O₈ (M&I) and 34.6 million pounds U₃O₈ (Inferred) compliant under JORC standards

Historical resources totaling 154.3 million pounds U₃O₈ (M&I) and 88.2 million pounds U₃O₈ (Inferred)

This creates one of the largest and most geographically diversified uranium portfolios among mid-tier developers.

Strategic and Market Rationale

The merger comes amid growing confidence in the uranium market’s long-term outlook. The World Nuclear Association’s 2025 Fuel Report projects uranium demand to rise roughly 30% by 2030 and more than double by 2040. IsoEnergy’s expanded scale and jurisdictional diversification position it to capture value from this structural supply-demand imbalance.

Australia, home to the Wiluna Project, ranks #1 globally for uranium resources and is among the Top 5 producers worldwide. Western Australia is emerging as a key uranium jurisdiction alongside Cameco’s Kintyre and Yeelirrie projects and Deep Yellow’s Mulga Rock development.

“The acquisition of Toro Energy marks another important step in advancing IsoEnergy’s strategy to build a globally diversified, development-ready uranium platform,” said Philip Williams, CEO and Director of IsoEnergy. “The Wiluna Uranium Project strengthens our portfolio with a large, previously permitted asset in a top-tier jurisdiction at a time when global nuclear demand is accelerating.”

Richard Homsany, Executive Chairman of Toro, added, “This transaction creates significant value for our shareholders and provides an opportunity to participate in a larger, leading uranium company listed on the TSX and NYSE. Toro shareholders will gain exposure to a diverse uranium portfolio with strong growth potential and enhanced access to capital.”

Positioned for Growth

The merged entity will have enhanced balance sheet strength, improved access to global capital markets, and a broader platform for value-accretive growth opportunities across the uranium cycle. Following completion, Toro will be delisted from the Australian Securities Exchange (ASX), while IsoEnergy will remain publicly traded in Toronto and New York.

The deal follows IsoEnergy’s previously announced — and later terminated — plan to acquire Anfield Energy in early 2024, reflecting the company’s continued pursuit of strategic, scale-building opportunities in the uranium sector. Major Toro shareholders, including Mega Uranium Ltd. (12.7%) and its associate Mega Redport Pty Ltd., have indicated their intention to vote in favor of the scheme, provided no superior proposal emerges.

Shares of Lithium Americas (NYSE: LAC) soared nearly 100% on Wednesday after reports that the Trump administration is considering taking a stake in the company as part of a renegotiated federal loan package tied to the development of the Thacker Pass lithium mine in Nevada.

According to Reuters, the administration is seeking as much as a 10% equity stake in the Vancouver-based miner. The proposed arrangement comes as Lithium Americas works through terms of a $2.26 billion loan from the Department of Energy, originally granted during the first Trump administration.

Under the current negotiations, the company has offered the government no-cost warrants for up to 10% of its common stock. At the same time, the administration is reportedly pressing General Motors (NYSE: GM) — which owns a 38% stake in Thacker Pass and has invested $625 million — for purchase guarantees that would help shore up demand for the lithium produced at the site. GM shares ticked higher by more than 2% on the news.

A Strategic Lithium Project

Thacker Pass is expected to play a central role in U.S. energy security. Once operational, the project is projected to be the largest lithium mining operation in the Western Hemisphere. Its first production phase, slated for 2028, is forecast to produce more than 40,000 metric tons of lithium carbonate annually — enough to power batteries for roughly 800,000 electric vehicles.

For perspective, Albemarle’s (NYSE: ALB) Silver Peak mine in Nevada, currently the only operating lithium mine in the U.S., produces fewer than 5,000 metric tons per year. This makes Thacker Pass a significant leap in domestic production capacity at a time when global demand for electric vehicles, battery storage, and clean energy technologies is surging.

China currently dominates the global lithium industry, producing more than 40,000 metric tons per year and refining more than 65% of the world’s supply. By comparison, the U.S. refines less than 3%. This imbalance has made lithium one of the most strategically sensitive commodities in the energy transition.

“Lithium is the new oil,” said one energy analyst, noting that securing supply has become a cornerstone of U.S. industrial policy. “Without it, you can’t scale EV adoption or battery storage, and that makes projects like Thacker Pass crucial to long-term energy independence.”

The government’s interest in Lithium Americas follows similar moves to shore up domestic supply chains for other critical materials. In July, MP Materials (NYSE: MP) announced a multibillion-dollar deal with the Department of Defense that made the government its largest shareholder, boosting MP’s stock more than 50%. Meanwhile, Intel (NASDAQ: INTC) has climbed over 25% since talks of a potential government stake in the chipmaker became public.

This pattern underscores the administration’s strategy of leveraging federal investment to reduce reliance on foreign sources of essential resources, from rare earth elements to semiconductors.

Lithium Americas stock traded at $6.09 as of 2:08 p.m. EDT, up more than 98% on the day. The sharp rally comes despite ongoing weakness in lithium prices, which have fallen over the past year amid oversupply from China. Futures for lithium carbonate are down more than 12%, while lithium hydroxide has dropped more than 4.5%.

Those price pressures have raised concerns about the financial viability of large-scale U.S. mining projects. The administration’s involvement could provide a stabilizing force, ensuring that key projects like Thacker Pass remain on track. The first loan draw is expected this month, with construction at the Nevada site already underway.

For now, investors appear to be betting that federal backing — and a potential government equity stake — could cement Lithium Americas’ role as a cornerstone of America’s clean energy future.

The U.S. oil industry is facing a sharp slowdown, with layoffs and spending cuts rippling across the sector as lower crude prices and industry consolidation squeeze margins. The wave of belt-tightening could mark the end of the rapid production growth that helped the United States overtake other producers to become the world’s top oil supplier in recent years.

International crude prices have fallen roughly 12% this year, dragged lower in part by rising output from OPEC and its allies, who have been steadily ramping up supply to reclaim market share lost to U.S. shale producers. Prices are now hovering just above $62 a barrel, uncomfortably close to breakeven levels for many U.S. operators. For companies already grappling with higher costs and trade-related tariffs, the weaker pricing environment is forcing tough decisions.

ConocoPhillips, the nation’s third-largest oil producer, recently announced plans to cut up to a quarter of its workforce. The move follows Chevron’s decision earlier this year to trim about 20% of its staff, amounting to roughly 8,000 jobs. Oilfield service providers such as SLB and Halliburton have also been cutting jobs, underscoring how the slowdown is spreading beyond producers to the broader energy ecosystem.

The cuts aren’t limited to people. According to a Reuters review of second-quarter results, 22 publicly traded U.S. producers—including ConocoPhillips, Diamondback Energy, and Occidental Petroleum—have reduced their combined capital spending by about $2 billion. Industry insiders say those pullbacks, along with falling rig counts, are early warning signs that production growth is set to level off. Baker Hughes data shows that the U.S. oil rig count has dropped by nearly 70 so far this year, down to just over 400.

In the Permian Basin, the heart of America’s shale boom, the tone has shifted from aggressive expansion to cautious retrenchment. “We’ve gone from ‘drill, baby, drill’ to ‘wait, baby, wait,’” said one Texas producer, pointing out that prices need to stabilize closer to $70–$75 a barrel before rig activity rebounds. Without that, analysts warn that U.S. output will plateau and could even begin to decline, with OPEC quickly stepping in to fill the gap.

Research firms are already forecasting slower momentum. Energy Aspects expects U.S. onshore production to drop by 300,000 barrels per day in 2025, while Wood Mackenzie projects only modest growth of 200,000 barrels per day—far below the record-setting pace of recent years.

Adding to the pressure are rising costs, much of it tied to tariffs on steel and other inputs. Diamondback Energy expects the price of steel casing for wells to climb by nearly 25% this year, inflating breakeven costs across the industry. For ConocoPhillips, controllable costs have already risen by $2 per barrel since 2021, making profitability harder to sustain.

The impact on employment is significant. Texas labor data shows U.S. oil and gas production jobs fell by nearly 5,000 in the first half of 2025, while energy services jobs have dropped by about 23,000 since January. Even with gains in drilling efficiency, industry analysts caution that technology alone won’t be enough to offset the slowdown.

For now, the U.S. oil industry remains a global leader. But with lower prices, higher costs, and fewer rigs in action, the sector’s once-rapid growth story appears to be entering a more uncertain chapter.

CALGARY, AB, September 2, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.09 per common share payable on September 30, 2025, to shareholders of record at the close of business on September 15, 2025. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

In one of the largest utility deals of the year, Black Hills Corp. (NYSE: BKH) and NorthWestern Energy Group, Inc. (Nasdaq: NWE) announced a definitive agreement to merge in an all-stock, tax-free transaction that gives the combined company an enterprise value of roughly $15.4 billion. The boards of both companies approved the deal unanimously, setting the stage for the creation of a new regulated electric and natural gas utility with operations across eight states.

Together, the companies will serve about 2.1 million customers, including more than 700,000 electric customers and 1.4 million natural gas customers. Their combined footprint will stretch across Arkansas, Colorado, Iowa, Kansas, Montana, Nebraska, South Dakota, and Wyoming, supported by nearly 97,000 miles of transmission and distribution lines and close to 3 gigawatts of generation capacity from a mix of thermal, hydro, and wind resources. The companies expect the deal to nearly double their combined rate base to $11.4 billion, providing the scale needed to meet rising energy demand and expand infrastructure for new industries such as data centers.

Management emphasized that the merger would create long-term value for both shareholders and customers. The new utility is projected to deliver annual earnings-per-share growth in the range of 5 to 7 percent, a pace that exceeds what either company had targeted on a standalone basis. Executives also pointed to stronger access to capital, a more balanced regulatory profile, and improved financial flexibility as key benefits of the transaction. Shareholders of Black Hills will own about 56 percent of the merged company, while NorthWestern shareholders will hold the remaining 44 percent.

The combined company will be headquartered in Rapid City, South Dakota, but leadership responsibilities will be shared. NorthWestern’s chief executive Brian Bird will serve as CEO, while Black Hills’ senior vice president and chief utility officer Marne Jones will become chief operating officer. Crystal Lail, currently CFO of NorthWestern, will take the same role in the new company, and Kimberly Nooney, CFO of Black Hills, will become chief integration officer. The board of directors will include six members from Black Hills and five from NorthWestern.

Both companies said they remain committed to safety, reliability, and sustainability, and they plan to continue investing heavily in grid modernization and renewable energy. With more than $7 billion in planned investments between 2025 and 2029, the new entity expects to play a central role in supporting the energy transition while keeping costs manageable for customers.

The merger, which is subject to shareholder approval, regulatory review in several states, and clearance from the Federal Energy Regulatory Commission, is expected to close within 12 to 15 months. If approved, it would establish a premier mid-cap regulated utility with diversified operations, predictable cash flows, and the capacity to pursue growth opportunities across an expanding energy landscape.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Second quarter financial results. Hemisphere reported oil and gas revenue of C$24.4 million in the second quarter, down 15.7% from the prior year period but ahead of our estimate of C$20.9 million. Net income was C$7.1 million, or C$0.07 per share, compared to C$10.4 million, or C$0.10 per share, last year, and above our forecast of C$5.8 million, or C$0.06 per share. Average daily production rose to 3,826 boe/d, up from 3,628 in Q2 2024 and modestly ahead of our estimate of 3,800 boe/d. The company realized an average sales price of C$70.06/boe, compared to C$87.65/boe in the prior year quarter. Adjusted funds flow totaled C$10.3 million, or C$0.10 per diluted share, versus C$13.6 million, or C$0.14 per diluted share, a year ago. This result exceeded our estimate of C$8.9 million, or C$0.09 per diluted share.

Updating estimates. Given the stronger-than-expected second quarter, we are raising our 2025 revenue forecast to C$97.7 million from C$95.0 million. Our operating expense assumption has been modestly increased to C$38.8 million from C$38.4 million. We now project net income of C$29.6 million, or C$0.30 per share, up from our prior forecast of C$28.7 million, or C$0.28 per share. Adjusted funds flow is expected to reach C$43.3 million, compared to our earlier estimate of C$42.2 million. For 2026, we forecast revenue of C$93.7 million, net income of C$27.5 million, or C$0.28 per share, and AFF of C$39.6 million, reflecting our expectation of a softer commodity price environment relative to 2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, Aug. 13, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) announces its financial and operating results for the three and six months ended June 30, 2025 which is our first quarter following the April 7, 2025 closing date of the strategic acquisition of Cardium focused light oil assets in the Pembina area of Alberta (the “Acquisition“). InPlay’s condensed unaudited interim financial statements and notes, as well as its Management’s Discussion and Analysis (“MD&A”) for the three and six months ended June 30, 2025 will be available at “www.sedarplus.ca” and on our website at “www.inplayoil.com“. An updated corporate presentation is available on our website.

We are excited about InPlay’s future following the highly accretive acquisition completed in the second quarter. This transformative transaction has significantly enhanced the Company’s scale, market capitalization, and long-term sustainability. With a longer reserve life and an expanded inventory of high quality drilling locations, the combined Company is well positioned to generate strong free adjusted funds flow (“FAFF”)(3) for many years to come.

InPlay is off to a very strong start with second quarter production exceeding expectations by approximately 1,000 boe/d. This outperformance was driven by base production performing above expectations and seven (7.0 net) wells brought onstream in March significantly outperforming our type curves by ~135% on average based on the first 120 days of initial production (“IP”). Notably, three wells brought onstream in March ranked among the top ten Cardium producers in April with two of them holding the number one and two spots in April and May, and ranking second and third in June. These wells achieved payout in under 90 days in a US$60 WTI pricing environment. As a result of this outperformance, current production based on field estimates remains at 19,400 boe/d even though no new wells have been brought on since March. We now expect 2025 average production to be at the upper end of our guidance range. In addition, strong capital efficiencies are expected to result in capital spending landing in the lower half of our previously announced capital budget of $53 – $60 million. The Company continues to prioritize free cash flow generation to be used for debt reduction and the continued return of capital to shareholders through our monthly dividend.

Another exciting development is the recent announcement that Delek Group Ltd. (“Delek”) has become a 32.7% strategically aligned shareholder of InPlay. Delek brings a proven track record of value creation in the energy sector. They hold a 45% working interest in the largest natural gas field in the Mediterranean, with an estimated 23 TCF of recoverable natural gas. Additionally, Delek has been instrumental in the growth of Ithaca Energy plc, where they hold a 52% equity stake and have overseen production growth from 30,000 boe/d to over 120,000 boe/d since 2019.

For the remainder of 2025, InPlay plans to drill 5.0 – 5.5 net Cardium wells in Pembina. InPlay’s second half drilling campaign recently commenced in August, with the spudding of a three well pad which are in close proximity to the Company’s top producing Cardium wells and are expected to be on production near the beginning of October. The application of InPlay’s drilling and completion techniques to the acquired assets is expected to drive continued strong performance from new wells with additional capital directed to facility upgrades, optimization and required infrastructure projects.

InPlay will continue to be disciplined and timely in capital spending in the current commodity price environment, maintaining a focus on strong FAFF, debt reduction, per share growth and continuation of our return to shareholder strategy. To further enhance stability and mitigate risk, the Company has secured commodity hedges extending through 2025 and into 2026. InPlay has hedged over 70% of natural gas production and approximately 60% of light crude oil production for the second half of 2025.

Second Quarter 2025 Highlights

Successfully closed the strategic acquisition of Cardium focused light oil assets at highly accretive metrics, enhancing FAFF by 65% on a per share basis, expanding our drilling inventory to over 400 locations, lowering our corporate base decline rate to 24% and strengthening dividend sustainability (2025 forecasted FAFF equal to 2.5 times base dividend).

Achieved average quarterly production of 20,401 boe/d(1) (62% light crude oil and NGLs), a 125% increase from Q1 2025, including a 13% increase to light crude oil and liquids weighting to 62% from 55% and a 35% increase in light oil weighting to 51% from 38% in the first quarter of 2025 with oil being the main driver behind our netbacks.

Generated strong quarterly Adjusted Funds Flow (“AFF”)(2) of $40.1 million ($1.49 per basic share(3)).

Achieved significant FAFF of $35.5 million ($1.32 per basic share(3)) allowing the Company to reduce net debt by approximately $26 million, more than originally forecasted, resulting in a quarterly annualized net debt to earnings before interest, taxes and depreciation (“EBITDA”)(3) ratio of 1.2 times.

Realized operating income of $50.5 million(3), an increase of 140% compared to Q1 2025 leading to a strong operating income profit margin(3) of 55%, up from 54% in Q1 2025.

Improved field operating netbacks(3) to $27.20/boe, a 6% increase compared to Q1 2025 despite an 11% decrease to WTI pricing (13% decrease to realized crude oil pricing) and a 22% decrease in AECO natural gas pricing compared to Q1 2025.

Returned $7.9 million to shareholders via monthly dividends, representing a 10% yield relative to the current share price. Since November 2022, InPlay has distributed $52 million in dividends (including dividends declared to date in the third quarter).

Second Quarter 2025 Financial & Operations Overview:

InPlay’s second quarter results exceeded expectations and marked the first reporting period incorporating the recently acquired assets, with pro forma operations effective April 8, 2025. Due to the outstanding efforts of our team and InPlay’s strong knowledge and focus in the area, the acquired assets were seamlessly integrated with no disruption to the Company’s ongoing operations.

Quarterly production averaged 20,401 boe/d(1) (62% light crude oil and NGLs) which was approximately 1,000 boe/d above internal forecasts. Base production exceeded expectations, and the seven (7.0 net) wells drilled on the combined assets in the first quarter significantly outperformed internal forecasts by approximately 135% (based on IP 120) as highlighted in the table below.

02-25 Pad (per well average)

14-33 Pad (per well average)

08-01 Pad (per well average)

boe/d

Oil and NGLs %

boe/d

Oil and NGLs %

boe/d

Oil and NGLs %

IP 30

887

88 %

680

75 %

265

89 %

IP 60

937

87 %

493

66 %

290

87 %

IP 90

922

85 %

569

63 %

288

86 %

IP 120

892

85 %

430

60 %

285

83 %

IP 150

N/A

N/A

487

58 %

275

82 %

Current

791

82 %

299

44 %

217

77 %

>300% above type curve

>75% above type curve

>25% above type curve

InPlay generated AFF of $40.1 million ($1.49 per basic share) a 138% increase from the first quarter of 2025. Limited capital spending in the second quarter of $4.6 million, resulted in $35.5 million of FAFF ($1.32 per basic share), highlighting the strong FAFF generation of the combined Company. These strong results were achieved despite an 11% decrease to WTI pricing (13% decrease to realized crude oil pricing) and a 22% decrease in AECO natural gas pricing compared to Q1 2025. The Company paid $7.9 million ($12.0 million in the first half of 2025) in dividends during the quarter.

During the quarter InPlay generated a net loss of $3.2 million. After excluding one-time transaction costs and the impact of unrealized mark-to-market hedging gains/losses, InPlay generated adjusted net income(3) of $2.0 million ($0.08 per basic share) in the quarter.

Strong results had net debt levels at the end of the quarter at $223 million, $5 million lower than originally anticipated. The quarterly annualized net debt to EBITDA ratio for the second quarter of 1.2x is evidence that our post-Acquisition accelerated debt reduction goals are well on track.

Operating synergies and stronger production allowed InPlay to maintain operating costs per boe in the second quarter in line with pre-acquisition levels and synergies have started to show a reduction in G&A cost per boe.

On behalf of the entire InPlay team and our Board of Directors, we thank our shareholders for their ongoing support as we execute our strategy of disciplined growth, reliable returns, and long-term value creation. We would like to send a special thanks to our employees for their significant effort in enabling a smooth integration of the new assets. We are very optimistic about building on the momentum from our strategic Acquisition that has transformed the future of the Company.

Notes:

1.

See “Production Breakdown by Product Type” at the end of this press release.

2.

Capital management measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

3.

Non-GAAP financial measure or ratio that does not have a standardized meaning under International Financial Reporting Standards (IFRS) and GAAP and therefore may not be comparable with the calculations of similar measures for other companies. Please refer to “Non-GAAP and Other Financial Measures” contained within this press release and in our most recently filed MD&A.

4.

Supplementary measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

5.

Common share and per common share amounts have been updated to reflect the six for one (6:1) common share consolidation effective April 14, 2025.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

")

")

")