Energy Fuels is a leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. Energy Fuels also produces vanadium from certain of its projects, as market conditions warrant, and is ramping up commercial-scale production of REE carbonate. Its corporate offices are in Lakewood, Colorado, near Denver, and all its assets and employees are in the United States. Energy Fuels holds three of America’s key uranium production centers: the White Mesa Mill in Utah, the Nichols Ranch in-situ recovery (“ISR”) Project in Wyoming, and the Alta Mesa ISR Project in Texas. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, has the ability to produce vanadium when market conditions warrant, as well as REE carbonate from various uranium-bearing ores. The Nichols Ranch ISR Project is on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Alta Mesa ISR Project is also on standby and has a licensed capacity of 1.5 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels also has one of the largest NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

The sales, along with recently signed utility contracts, will generate cash flow as UUUU starts up operations. Congress allocated $75 million to establish a national uranium security reserve in its 2020 budget. The US Energy Secretary indicated earlier that it expects to make four individual awards of 100,000-500,000 pounds of U3O8 for a total of 1 million pounds. Energy Fuels, as the largest licensed producer of uranium, was in a good position to receive one of the rewards. The UUUU announcement did not indicate a volume level. Peninsula Energy announced that it received an award for 300,000 pounds but did not specify a sales amount.

The sales can be done right away before mining operations are restarted. The conditions of the DOE award state that the uranium must be physically located at Honeywell’s conversion facilities in Metropolis, IL. Energy Fuels currently holds about 610,000 pounds of U3O8 at Metropolis worth more than $30 million at current uranium spot prices. A volume awards similar to that for Peninsula seems reasonable implying that the DOE is paying a price near $60/lb. or slightly above current spot prices, and be well within current inventory levels.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

DOE program supports critical domestic clean energy & national security priorities

Pending membership in DOE HALEU Consortium to support fuel for next generation advanced nuclear reactors

LAKEWOOD, Colo., Dec. 16, 2022 /CNW/ – Energy Fuels Inc. (NYSE American: UUUU) (TSX: EFR) (“Energy Fuels” or the “Company”), a leading U.S. producer of uranium and rare earth elements (“REE“), today announced that it has been awarded a contract to sell $18.5 million of natural uranium concentrates (“U3O8“) to the U.S. government for the establishment of a strategic uranium reserve (the “Uranium Reserve“). The U.S. National Nuclear Security Administration (“NNSA“), an office within the U.S. Department of Energy (“DOE“), is the agency tasked with purchasing domestic U3O8 and conversion services for the Uranium Reserve. The Uranium Reserve is intended to be a backup source of supply for domestic nuclear power plants in the event of a significant market disruption. Additionally, the Company announced its application for membership in the DOE’s newly created HALEU Consortium.

Uranium Reserve Award:

Energy Fuels expects to complete the sale of uranium for the Uranium Reserve to NNSA during Q1-2023 and realize total gross proceeds of $18.5 million. The U3O8 the Company expects to sell to the U.S. government is currently held in the Company’s inventory at the Metropolis Works Conversion Facility, located in Metropolis, Illinois. The sale does not involve the physical movement of material, so the sale and transfer can be completed quickly.

Mark S. Chalmers, President and CEO of Energy Fuels stated: “Energy Fuels is pleased to contribute to U.S. energy security by supplying U.S.-origin uranium to the U.S. uranium reserve. Russia’s invasion of Ukraine has highlighted America’s troubling dependence on Russia and its allies for our nuclear fuel and uranium supply, and the need for the U.S. to rebuild its uranium and nuclear fuel capabilities. Today, nuclear energy provides the U.S. with roughly 20% of all electricity, and 50% of our clean, carbon-free electricity. U.S. and European nuclear industries are actively working to shift away from Russian uranium supply, but the process will be difficult and lengthy. The U.S. can rely on supply from allies like Canada, Australia and others for a large proportion of our uranium and nuclear fuel supply, but we must also restore our own capabilities. For the past several years, U.S. uranium production has been near-zero and our only uranium conversion facility has been shut-down. The Uranium Reserve is a small, but important, step toward resolving this untenable situation.”

HALEU Consortium:

On December 12, 2022, Energy Fuels also applied for membership in the DOE’s newly created HALEU Consortium. The HALEU Consortium is a program managed by the DOE’s office of Nuclear Energy (“NE“) intended to help create a secure domestic supply of high-assay, low-enriched uranium (“HALEU“) used by many of the next generation of advanced nuclear reactor technologies. HALEU enables many advanced reactor designs to be smaller and more efficient than traditional reactors. The uranium used in traditional nuclear reactors is enriched to roughly 3% – 5% of the fissionable isotope, uranium-235 (“U-235“). HALEU is enriched to between 5% and 20% U-235. Today, only Russian companies are able to supply HALEU, which is causing delays in the development of advanced reactors. For example, TerraPower recently announced a delay in building its first Natrium reactor in Wyoming. TerraPower is a high-profile next generation advanced reactor developer funded by Bill Gates. TerraPower specifically attributed the delay to the lack of availability of HALEU outside of Russia.

As the leading producer of U3O8 in the U.S., and the owner and operator of the only conventional uranium mill in the U.S., Energy Fuels believes it can play an important role in advising the DOE and teaming with other companies for this critical program. Furthermore, Energy Fuels is pursuing other DOE priorities related to uranium production, including rare earth element and medical isotope production.

Mr. Chalmers continued: “Energy Fuels is increasingly recognized by the U.S. government and other market participants as indispensable to weaning the U.S. off of Russian uranium supply, and as a solid partner in other important priorities. Our White Mesa Mill is critical and unique domestic infrastructure, with licenses, expertise and capabilities found nowhere else in the U.S., that are needed to produce uranium, and many other critical minerals and materials. We stand ready to play a critical role in restoring America’s uranium, rare earths, and other critical material capabilities, while reducing our troubling dependence on Russia and China.”

About Energy Fuels: Energy Fuels is a leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. The Company also produces vanadium from certain of its projects, as market conditions warrant, mixed rare earth element carbonate (“RE Carbonate“) from uranium-bearing monazite ores and is ramping up to full commercial-scale production of separated rare earth oxides. Its corporate offices are in Lakewood, Colorado near Denver, and all its assets and employees are in the United States. Energy Fuels holds two of America’s key uranium production centers: the White Mesa Mill in Utah and the Nichols Ranch ISR Project in Wyoming. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, and has the ability to produce vanadium when market conditions warrant, as well as RE Carbonate from various uranium-bearing ores. The Nichols Ranch ISR Project is currently on standby and has a licensed capacity of 2 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels also has one of the largest S-K 1300 and NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Cautionary Note Regarding Forward-Looking Statements: This news release contains certain “Forward Looking Information” and “Forward Looking Statements” within the meaning of applicable United States and Canadian securities legislation, which may include, but are not limited to, statements with respect to: any expectation that the Company will complete the contemplated sale of uranium to the DOE in Q1-2023 or at all; any expectation that the Company will maintain its position as a leading uranium company in the United States; any expectation that the Company will be admitted as a member of the HALEU Consortium or that the Company can play an important role in this critical program; any expectation that the Mill will be successful in producing RE Carbonate and/or separated rare earth element oxides on a full-scale commercial basis or at all; any expectation that the Company will successfully produce radioisotopes to be used for the production of medical isotopes on a commercial basis or at all; any expectation that the Company is increasingly being recognized by the U.S. government and other market participants as an indispensable party in efforts to wean the U.S. off of Russian uranium supply, and a partner in other important priorities; and any expectation that the Company stands ready to play a critical role in restoring America’s uranium, rare earths and other critical material capabilities, while reducing America’s dependence on Russia and China. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans,” “expects,” “does not expect,” “is expected,” “is likely,” “budgets,” “scheduled,” “estimates,” “forecasts,” “intends,” “anticipates,” “does not anticipate,” or “believes,” or variations of such words and phrases, or state that certain actions, events or results “may,” “could,” “would,” “might” or “will be taken,” “occur,” “be achieved” or “have the potential to.” All statements, other than statements of historical fact, herein are considered to be forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements express or implied by the forward-looking statements. Factors that could cause actual results to differ materially from those anticipated in these forward-looking statements include risks associated with: commodity prices and price fluctuations; processing and mining difficulties, upsets and delays; permitting and licensing requirements and delays; changes to regulatory requirements; legal challenges; the availability of feed sources for the Mill; competition from other producers; public opinion; government and political actions; available supplies of monazite sands; the ability of the Mill to produce RE Carbonate to meet commercial specifications on a commercial scale at acceptable costs; the ability of the Mill to separate rare earth oxides to meet commercial specifications on a commercial scale at acceptable costs; market factors, including future demand for rare earth elements; the ability of the Mill to be able to separate radium or other radioisotopes at reasonable costs or at all; market prices and demand for medical isotopes; and the other factors described under the caption “Risk Factors” in the Company’s most recently filed Annual Report on Form 10-K, which is available for review on EDGAR at www.sec.gov/edgar.shtml, on SEDAR at www.sedar.com, and on the Company’s website at www.energyfuels.com. Forward-looking statements contained herein are made as of the date of this news release, and the Company disclaims, other than as required by law, any obligation to update any forward-looking statements whether as a result of new information, results, future events, circumstances, or if management’s estimates or opinions should change, or otherwise. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, the reader is cautioned not to place undue reliance on forward-looking statements. The Company assumes no obligation to update the information in this communication, except as otherwise required by law.

SOURCE Energy Fuels Inc.

For further information: Investor Inquiries: Energy Fuels Inc., Curtis Moore, VP – Marketing and Corporate Development, (303) 974-2140 or Toll free: (888) 864-2125, investorinfo@energyfuels.com, www.energyfuels.com

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“Alliance” or the “Partnership”) announced today that the Board of Directors of its general partner, Alliance Resource Management GP, LLC, has appointed Cary P. Marshall as Senior Vice President and Chief Financial Officer effective April 1, 2023. The appointment follows the Partnership’s previously announced retirement and succession plan for Brian L. Cantrell, current Chief Financial Officer. Mr. Cantrell will remain with Alliance through March 31, 2023, to facilitate an orderly transition.

“We extend our thanks and appreciation to Brian for his leadership, service, and contributions to Alliance over the past 19 years,” said Joseph W. Craft III, Chairman, President and Chief Executive Officer. “Brian played a critical role in the Partnership’s growth and financial strength during his tenure, and we wish him and his family all the best in his retirement.”

“As we transition Brian’s duties and responsibilities, we are fortunate to have a talented, proven, and capable leader like Cary fully-ready to step-in,” added Mr. Craft. “We are confident that Cary’s extensive knowledge of the business coupled with more than three decades of related experience will allow us to maintain our financial discipline and principles while advancing the performance and practices of the organization.”

Mr. Marshall has served as Alliance’s Vice President, Corporate Finance and Treasurer since May 2003. Mr. Marshall joined Alliance’s predecessor entity, MAPCO Inc., in 1989 and has since held multiple positions across corporate finance and marketing. Mr. Marshall is an alumnus of Southern Methodist University, where he received a Bachelor of Business Administration degree and a Master of Business Administration degree.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the second largest coal producer in the eastern United States. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast-growing energy and infrastructure transition.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7674 or via e-mail at investorrelations@arlp.com.

CALGARY, AB, Dec. 7, 2022 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF) announces November 2022 sales volumes and an operational update.

November 2022 sales volumes

November sales volumes averaged 2,667 boepd, including natural gas sales of 15.2 MMcfpd and associated natural gas liquids sales from condensate of 135 bopd, based on field estimates, a decrease of 2% from the October 2022 average daily volumes and an increase of 1% from our Q3 2022 average.

Operational Update

We have now moved the service rig to our 182-C2 well on our 100% owned and operated Block 182 and expect to commence testing operations shortly. We completed drilling the 182-C2 well in October to a total measured depth (“MD”) of 3,185 metres. Testing of the 182-C2 well will begin with the Sergi Formation, the deepest of two formations with hydrocarbons shows during drilling. As previously announced, the well encountered a 223.7-metre-thick section with 121.3 metres of sand estimated above 6% porosity in the sand-dominated interval between 2,704.1 and 2,927.8 metres total vertical depth in the Sergi Formation. Caliper logs indicate that a significant amount of the wellbore in the Sergi interval contains washouts from drilling and is out of gauge, making open-hole log analysis challenging. As such, hydrocarbon potential in the Sergi will be validated through formation testing. Following testing of the Sergi Formation, testing will proceed up-hole to the Agua Grande Formation where, based on open-hole wireline logs, the well encountered 10.9 metres of potential net hydrocarbon pay, with an average porosity of 8.9% and average water saturation of 25.1%, using a 6% porosity cut-off, 50% Vshale cut-off and 50% water saturation cut-off. This testing will assess the extent, if any, of commercial hydrocarbons associated with the well, the productive capability of the well and will help define the field development plan.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All amounts contained in this new release are in United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Abbreviations:

bbls = barrelsboepd = barrels of oil equivalent (“boe”) per daybopd = barrels of oil and/or natural gas liquids (condensate) per dayMMcf = million cubic feetMMcfpd = million cubic feet per day

BOE Disclosure. The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this news release are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Testing and Well Results. Data obtained from the 182-C2 well identified in this press release, including hydrocarbon shows, open-hole logging, net pay and porosities and initial testing data, should be considered to be preliminary until detailed pressure transient and other analysis and interpretation has been completed. Hydrocarbon shows can be seen during the drilling of a well in numerous circumstances and do not necessarily indicate a commercial discovery or the presence of commercial hydrocarbons in a well. There is no representation by Alvopetro that the data relating to the 182-C2 well contained in this press release is necessarily indicative of long-term performance or ultimate recovery. The reader is cautioned not to unduly rely on such data as such data may not be indicative of future performance of the well or of expected production or operational results for Alvopetro in the future.

Forward-Looking Statements and Cautionary Language. This news release contains “forward-looking information” within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward‐looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning potential hydrocarbon pay in the 182-C2 well, exploration and development prospects of Alvopetro and the expected timing of certain of Alvopetro’s testing and operational activities. The forward‐looking statements are based on certain key expectations and assumptions made by Alvopetro, including but not limited to expectations and assumptions concerning testing results of the 183-B1 well and the 182-C2 well, equipment availability, the timing of regulatory licenses and approvals, the success of future drilling, completion, testing, recompletion and development activities, the outlook for commodity markets and ability to access capital markets, the impact of the COVID-19 pandemic, the performance of producing wells and reservoirs, well development and operating performance, foreign exchange rates, general economic and business conditions, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

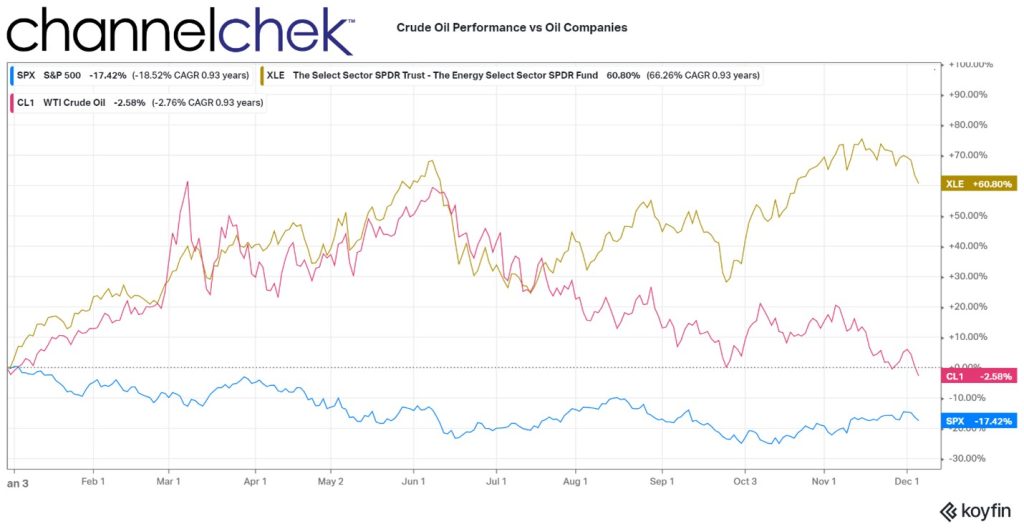

The Argument for Higher Oil Market Prices is Fairly Straightforward

The price of oil is near its 2022 low. This lower per barrel cost is normal when the commodities market perceives the economy as slowing or that it will slow. What is surprising is that the price is near the low for the year when the Chinese are easing Covid restrictions and will soon be requiring more fuel; at the same time, a Russian oil cap, which is sure to bring less supply to the market, was just instituted this week. In the meantime, energy producers, up 60.8% on the year, are not sinking at the pace of oil prices.

Energy shares have been the big winners for 2022. And it is rare that they are flying solo, without the help of price increases of their underlying product. According to Bespoke Investment Group, last month marked the first time since 2006 that the S&P 500 energy sector has traded within 3% of a 12-month high while the price of West Texas Intermediate retreated more than 25% from its one-year peak..

The divergence has caught the attention of investors. Since drillers and miners tend to rise and fall with the prices of the commodities they produce, many expect the gap to narrow to its more historical norm. Most are looking for oil to rise rather than drillers to fall.

Pressures that could cause oil to rise include the EU winter season, the U.S. Strategic Reserves bumping up against depletion, OPEC+ keeping production quotas unchanged, and Western governments’ $60-a-barrel price cap on Russian crude. These, taken together, are expected to put upward pressure on per-barrel prices. The commodities market is not moving in accordance with these factors. Futures contracts for U.S. crude closed Monday 3.8% lower at $76.93 a barrel, its fourth-lowest settle of the year.

Working against the argument for higher crude prices is the expected slowing of world economies. The possibility of a recession in many global economies while central banks raise interest rates, is unknown. Any impact remains to be seen.

CALGARY, AB, Dec. 1, 2022 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.015 per common share payable on December 30, 2022, to shareholders of record at the close of business on December 15, 2022. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

SOURCE InPlay Oil Corp.

For further information: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

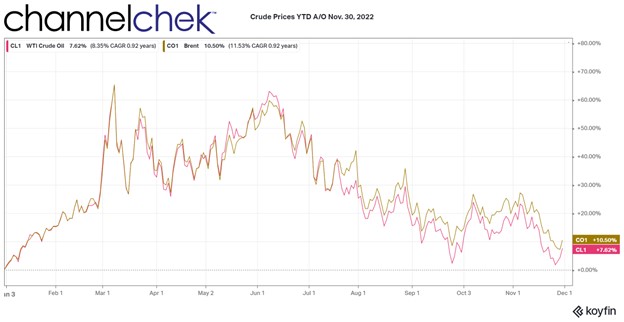

The Odds May Again be Stacked on the Side of a Prolonged Oil Price Rally

Oil markets and the related energy industry have been cheered this year as the one clear winner, yet within the past few days, crude has brushed up against its low recorded at the start of 2022. The commodity has since bounced, and there are at least four reasons to believe that it will continue to rally.

On Wednesday, November 30, news that China will take steps to ease lockdown restrictions, a drop in U.S. oil supplies, a weaker U.S. dollar, and a signal of OPEC+’s intentions helped push crude prices up by more than 3.5%.

China

Major Chinese manufacturing cities are lifting Covid lockdowns, including the financial hub Shanghai and Zhengzhou (the location of the world’s largest iPhone factory). Renewed expectations that China’s economy may strengthen after being held back by restrictions on movement to contain Covid-19 helped lift prices. After lockdown protests last weekend, Chinese authorities reported fewer cases of the virus on Tuesday. Guangzhou, a city in the south of the country, relaxed some rules on Wednesday. Increased economic activity in China could come at a pace that dramatically increases the demand for oil and related products.

US Supply

U.S. petroleum stockpiles declined by 7.9 million barrels last week, according to reports from the American Petroleum Institute. Official figures from the U.S. Energy Information Administration (EIA) shown below indicate a declining trend that is unsustainable and will soon need to be turned around.

Source: EIA

The decline in the days supply is effectively borrowing against future stockpiles as there will need to be a time when this reverses, and more output-increasing stockpiles will add to demand on production.

U.S. Dollar

A weakening dollar has also helped enhance demand globally for crude by making contracts priced in the U.S. currency more affordable for overseas buyers. The dollar index, a measure of strength against a basket of six other major trading currencies, slipped 0.3% on Wednesday. It’s down about 5% in the past month.

While the effect of this FX change may not be felt by U.S. buyers, the added demand by requiring less local currency to translate into dollars effectively creates demand by virtue of its lower cost.

Source: Koyfin

OPEC+

The Saudis had been considering increasing their output to help soften price pressures and increase availability. This would occur when the cartel meets this weekend to decide output levels. It is reported that the meeting will not be in-person. When OPEC+ agrees to meet virtually, it tends to indicate they are not discussing any major changes to output targets.

Expectations of an increase in output had been built into the price; the new expectations are putting upward pressure on crude.

Take Away

A number of factors have caused crude to trade off since late Spring. A number of forces are now stacked up that could push crude levels back upward. These include fewer lockdowns in China, a declining U.S. supply, the added global demand that will be attracted by a weakening dollar, and the new realization that members of OPEC+ are not likely to increase output limits. Additionally, there has been a looming concern as to how much supply will be taken offline with price limits that are to be placed on purchases of Russian oil early next week.

CALGARY, AB, Nov. 29, 2022 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF) announces results from the third interval tested in our 183-B1 well on our 100% owned and operated Block 183.

In July 2022, we completed drilling the 183-B1 exploration well to a total measured depth (“MD”) of 2,917 metres. Based on open-hole wireline logs and fluid samples confirming hydrocarbons, the well discovered hydrocarbons in multiple formations with a total of 34.3 metres of potential net hydrocarbon pay, with an average porosity of 10.6% and average water saturation of 29.0% using a 6% porosity cut-off, 50% Vshale cut-off and 50% water saturation cut-off.

Alvopetro has completed the 183-B1 formation test in the Candeias Formation, the third of three formations with hydrocarbons shows during drilling of the well. We perforated a total of 3 metres in the Candeias Formation between 2,580 to 2,586 metres MD. During the clean up period we swabbed 16 bbls of completion fluid and 12 bbls of 36°API crude oil. Cumulatively, over the duration of the 48-hour production test, we recovered 13 bbls of 35°API crude oil and 21 bbls of formation water.

Following this test, we will turn our focus back to the Sergi Formation in this well where we perforated a total of 26.5 metres in the upper portion of the Sergi Formation at various intervals between 2,811 metres MD and 2,886 metres MD. We initially swabbed 63 bbls of oil and 7 bbls of completions fluid during the clean-up period. After a short shut-in we then initiated the production test. Cumulatively, over the duration of the 72-hour production test, we recovered 59 bbls of 43°API oil, 7 bbls of water identified as completion fluid, and 0.28 MMcf of associated gas. The daily oil rate recovered during swabbing operations averaged 20 bopd. We are engineering a stimulation plan for this upper Sergi section in this well and we have submitted applications to drill two follow up wells from this 183-B1 surface location targeting the full Sergi hydrocarbon column and the potential in the deeper Boipeba Member.

We now plan to move to test multiple zones in our 182-C2 well, commencing with the Sergi Formation where, as previously announced, based on open-hole wireline logs, the well encountered a 223.7-metre-thick section with 121.3 metres of sand estimated above 6% porosity in the sand-dominated interval between 2,704.1 and 2,927.8 metres total vertical depth. Caliper logs indicate that a significant amount of the wellbore in the Sergi interval contains washouts from drilling and is out of gauge, making open-hole log analysis challenging. As such, hydrocarbon potential in the Sergi will be validated through formation testing. Following testing of the Sergi Formation, testing will proceed up-hole to the Agua Grande formation where, based on open-hole wireline logs, the well encountered 10.9 metres of potential net hydrocarbon pay, with an average porosity of 8.9% and average water saturation of 25.1%, using a 6% porosity cut-off, 50% Vshale cut-off and 50% water saturation cut-off. This testing will assess the extent, if any, of commercial hydrocarbons associated with the well, the productive capability of the well and will help define the field development plan.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All amounts contained in this new release are in United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Abbreviations:

API = American Petroleum Institute°API = an indication of the specific gravity of crude oil measured on the API gravity scale.bbls = barrelsboepd = barrels of oil equivalent (“boe”) per daybopd = barrels of oil and/or natural gas liquids (condensate) per dayMMcf = million cubic feetMMcfpd = million cubic feet per day

BOE Disclosure. The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this news release are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Testing and Well Results. Data obtained from the 183-B1 well and the 182-C2 well identified in this press release, including hydrocarbon shows, open-hole logging, net pay and porosities and initial testing data, should be considered to be preliminary until detailed pressure transient and other analysis and interpretation has been completed. Hydrocarbon shows can be seen during the drilling of a well in numerous circumstances and do not necessarily indicate a commercial discovery or the presence of commercial hydrocarbons in a well. There is no representation by Alvopetro that the data relating to the 183-B1 well or the 182-C2 well contained in this press release is necessarily indicative of long-term performance or ultimate recovery. The reader is cautioned not to unduly rely on such data as such data may not be indicative of future performance of the well or of expected production or operational results for Alvopetro in the future.

Forward-Looking Statements and Cautionary Language. This news release contains “forward-looking information” within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward‐looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning potential hydrocarbon pay in the 183-B1 well and the 182-C2 well, exploration and development prospects of Alvopetro and the expected timing of certain of Alvopetro’s testing and operational activities. The forward‐looking statements are based on certain key expectations and assumptions made by Alvopetro, including but not limited to expectations and assumptions concerning testing results of the 183-B1 well and the 182-C2 well, equipment availability, the timing of regulatory licenses and approvals, the success of future drilling, completion, testing, recompletion and development activities, the outlook for commodity markets and ability to access capital markets, the impact of the COVID-19 pandemic, the performance of producing wells and reservoirs, well development and operating performance, foreign exchange rates, general economic and business conditions, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Permex Petroleum decided to postpone its listing on the NYSE American due to market conditions. The company also indicated that a registration statement with the SEC has not yet become effective. The shares of Permex (now trading as OILCD) have fallen approximately 50% following the announcement of a 2 million (later raised to 3.6 million) common share offering. The offering was to be completed in conjunction with the move to the NYSE. Prior to the uplisting and registration announcement, Permex completed a 1-60 reverse stock split.

We are adjusting our estimates and price target to reflect a lower share count associated with the reverse stock split. Our new price target is now $40 per share versus our pre-stock split price target of $4 per share. We have increased our price target by less than a 60-1 multiple due to the following reasons. We have increased the discount rate we are using for the company to reflect what we view as increased financing risk. In addition, we have slowed the assumed pace of new well drilling to one every other quarter instead of one per quarter. We also believe the company will focus primarily on less expensive, but less productive, vertical wells until it starts generating cash flow to fund drilling.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Alvopetro Energy Ltd.’s vision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Alvopetro reported 2022-3Q results significantly higher than last year and above our expectations. Revenues rose 67% due to a 7% increase in production and a 58% increase in gas prices. Higher sales translated into higher cash flow ($13.8 million versus $7.2 million) and earnings ($8.8 million versus $0.0).

Results were due to operations improvements and are likely to continue. The company expanded its gas processing facilities in July raising capacity to 3,000 boe/d. With quarterly results, management indicated that October total production averaged 2,720 boe/d, a nice rise above 2022-3Q levels of 2,642 boe/d.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, Nov. 15, 2022 /CNW/ – Alvopetro Energy Ltd. (TSXV:ALV); (OTCQX: ALVOF) is pleased to announce a 50% increase in our quarterly dividend, to US$0.12 per common share, an intention to launch a share buyback program under a normal course issuer bid (“NCIB”) and operating and financial results for the third quarter of 2022 including another record quarter of funds flow from operations of $13.3 million. We will host a live webcast to discuss Q3 2022 results on Wednesday November 16, 2022, beginning at 9:00 am Mountain time.

President & CEO, Corey C. Ruttan commented:

“With continued strong operating and financial results, and with our debt now fully repaid, we are pleased to announce a 50% increase in our quarterly dividend following on the 33% increase earlier this year. Our dividend program and the proposed NCIB will provide us with maximum flexibility to meet our strategy to maintain a balanced organic growth and stakeholder return model.”

All references herein to $ refer to United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Quarterly Dividend Increased 50% to $0.12 per Share

Alvopetro is pleased to announce that our Board of Directors has approved a 50% increase in our quarterly dividend, to $0.12 per common share, payable in cash on January 13, 2023, to shareholders of record at the close of business on December 30, 2022. This dividend is designated as an “eligible dividend” for Canadian income tax purposes.

Dividend payments to non-residents of Canada will be subject to withholding taxes at the Canadian statutory rate of 25%. Shareholders may be entitled to a reduced withholding tax rate under a tax treaty between their country of residence and Canada. For further information, see Alvopetro’s website at https://alvopetro.com/Dividends-Non-resident-Shareholders.

Normal Course Issuer Bid

In connection with our long-standing balanced and disciplined stakeholder return and organic growth model, our Board has provided approval to submit an application to launch a share buyback program under a NCIB, subject to securities law and customary approvals. Once approved, the NCIB, combined with our quarterly dividends, will provide us with flexibility in managing our returns to stakeholders.

Financial and Operating Highlights – Third Quarter of 2022

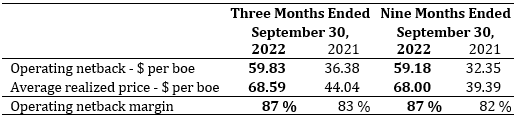

Daily sales averaged 2,642 boepd in Q3 2022, a 7% increase from the Q3 2021 average of 2,459 boepd and a 12% increase from the Q2 2022 average of 2,359 boepd. The expansion of our gas processing facility was completed at the end of July and available processing capacity has now increased to 500,000 m3/d (18 MMcfpd) contributing to higher volumes in the quarter.

As of August 1, 2022, Alvopetro’s natural gas price has been reset to the new ceiling price of $10.22/MMBtu. Due to the appreciation of the BRL in the first half of 2022 compared to second half of 2021, the BRL contracted price remained consistent at BRL1.94/m3. With all natural gas sales in Q3 2022 at the ceiling price, our average realized natural gas price increased to $11.18/Mcf compared to the Q3 2021 average price of $7.07/Mcf. Higher commodity prices and higher daily sales volumes resulted in a 67% increase in our natural gas, condensate and oil revenue compared to Q3 2021.

Our operating netback was $59.83 per boe in Q3 2022, an improvement of $23.45 per boe from Q3 2021 (+64%). Despite consistent BRL denominated natural gas pricing, our operating netback decreased $4.13 per boe from Q2 2022 (-6%) due to the devaluation of the BRL relative to the USD and lower Brent pricing on condensate.

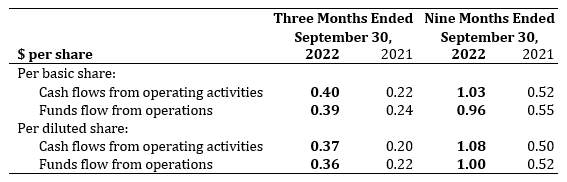

We generated cash flows from operating activities of $13.8 million ($0.40 per basic share and $0.37 per diluted share) and funds flows from operations of $13.3 million ($0.39 per basic share and $0.36 per diluted share), increases of $6.6 million and $5.4 million, respectively compared to Q3 2021.

We reported net income of $8.8 million in Q3 2022 compared to a loss of $0.02 million in Q3 2021.

Capital expenditures totaled $8.7 million, and included drilling costs for our 183-B1, 182-C2 and Unit-C wells, testing costs on our 182-C1 well, long lead purchases and development costs on our Murucututu project.

All outstanding warrants were exercised in the quarter, with 1,342,978 warrants exercised by way of cashless exercise and 1,342,978 warrants exercised at a strike price of $1.80 per share. Alvopetro received cash proceeds of $2.4 million and issued a total of 2,081,616 common shares on the exercise.

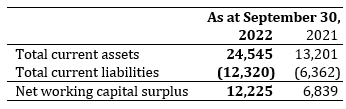

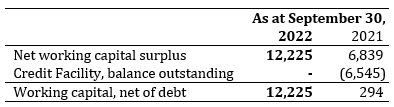

We repaid the final $2.5 million outstanding on the credit facility and the facility has now been cancelled. As at September 30, 2022, we had a net working capital surplus of $12.2 million, including $17.4 million in cash and cash equivalents.

Our October 2022 sales volumes averaged 2,720 boepd based on field estimates, with natural gas sales of 15.6MMcfpd and natural gas liquids from condensate of 124 bopd.

The following table provides a summary of Alvopetro’s financial and operating results for three and nine months ended September 30, 2022 and September 30, 2021. The consolidated financial statements with the Management’s Discussion and Analysis (“MD&A) are available on our website at www.alvopetro.com and will be available on the System for Electronic Document Analysis and Retrieval (SEDAR) website at www.sedar.com.

Notes:

The 2021 comparative periods in the table above have been restated. See “Restatement of the 2021 Comparative Period” section within the MD&A and Note 14 of the unaudited interim condensed consolidated financial statements for the three and nine months ended September 30, 2022 for further details.

Per share amounts are based on weighted average shares outstanding other than dividends per share, which is based on the number of common shares outstanding at each dividend record date. The weighted average number of diluted common shares outstanding in the computation of funds flow from operations and cash flows from operating activities per share is the same as for net income per share.

See “Non-GAAP and Other Financial Measures” section within this news release.

Third Quarter 2022 Results Webcast

Alvopetro will host a live webcast to discuss Q3 2022 financial results at 9:00 am Mountain time on November 16, 2022. Details for joining the event are as follows:

The webcast will include a question-and-answer period. Online participants will be able to ask questions through the Zoom portal. Dial-in participants can email questions directly to socialmedia@alvopetro.com.

Long-term Incentive Compensation Grants

In connection with our long-term incentive compensation program, Alvopetro’s Board of Directors (the “Board”) has approved the annual rolling grants to officers, directors and certain employees under Alvopetro’s Omnibus Incentive Plan. A total of 536,000 stock options, 122,000 restricted share units (“RSUs”) and 40,000 deferred share units (“DSUs”) were approved by the Board and are expected to be granted on November 24, 2022. Of the total grants, 248,000 stock options, 101,000 RSUs and 40,000 DSUs were granted to directors and officers. Each stock option, RSU and DSU entitles the holder to purchase one common share. Each stock option granted will have an exercise price based on the volume weighted average trading price of Alvopetro’s shares on the TSX Venture Exchange for the five (5) consecutive trading days up to and including November 24, 2022. All stock options, RSUs and DSUs granted expire five (5) years from the date of the grant.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Abbreviations:

bbls

=

barrels

boepd

=

barrels of oil equivalent (“boe”) per day

bopd

=

barrels of oil and/or natural gas liquids (condensate) per day

BRL

=

Brazilian Real

m3

=

cubic metre

Mcf

=

thousand cubic feet

Mcfpd

=

thousand cubic feet per day

MMcf

=

million cubic feet

MMcfpd

=

million cubic feet per day

NGLs

=

natural gas liquids

Q2 2022

=

three months ended June 30, 2022

Q3 2021

=

three months ended September 30, 2021

Q3 2022

=

three months ended September 30, 2022

Non-GAAP and Other Financial Measures

This news release contains references to various non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures as such terms are defined in National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure. Such measures are not recognized measures under GAAP and do not have a standardized meaning prescribed by IFRS and might not be comparable to similar financial measures disclosed by other issuers. While these measures may be common in the oil and gas industry, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. The non-GAAP and other financial measures referred to in this report should not be considered an alternative to, or more meaningful than measures prescribed by IFRS and they are not meant to enhance the Company’s reported financial performance or position. These are complementary measures that are used by management in assessing the Company’s financial performance, efficiency and liquidity and they may be used by investors or other users of this document for the same purpose. Below is a description of the non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures used in this news release. For more information with respect to financial measures which have not been defined by GAAP, including reconciliations to the closest comparable GAAP measure, see the “Non-GAAP Measures and Other Financial Measures” section of the Company’s MD&A which may be accessed through the SEDAR website at www.sedar.com.

Non-GAAP Financial Measures

Operating netback

Operating netback is calculated as natural gas, oil and condensate revenues less royalties and production expenses. This calculation is provided in the “Operating Netback” section of the Company’s MD&A using our IFRS measures. The Company’s MD&A may be accessed through the SEDAR website at www.sedar.com. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations.

Non-GAAP Financial Ratios

Operating netback per boe

Operating netback is calculated on a per unit basis, which is per barrel of oil equivalent (“boe”). It is a common non-GAAP measure used in the oil and gas industry and management believes this measurement assists in evaluating the operating performance of the Company. It is a measure of the economic quality of the Company’s producing assets and is useful for evaluating variable costs as it provides a reliable measure regardless of fluctuations in production. Alvopetro calculated operating netback per boe as operating netback divided by total sales volumes (barrels of oil equivalent). This calculation is provided in the “Operating Netback” section of the Company’s MD&A using our IFRS measures. The Company’s MD&A may be accessed through the SEDAR website at www.sedar.com. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations on a per unit basis (boe).

Operating netback margin

Operating netback margin is calculated as operating netback per boe divided by the realized sales price per boe. Operating netback margin is a measure of the profitability per boe relative to natural gas, oil and condensate sales revenues per boe and is calculated as follows:

Funds Flow from Operations Per Share

Funds flow from operations per share is a non-GAAP ratio that includes all cash generated from operating activities and is calculated before changes in non-cash working capital, divided by the weighted the weighted average shares outstanding for the respective period. For the periods reported in this news release the cash flows from operating activities per share and funds flow from operations per share is as follows:

Capital Management Measures

Funds Flow from Operations

Funds flow from operations is a non-GAAP capital management measure that includes all cash generated from operating activities and is calculated before changes in non-cash working capital. The most comparable GAAP measure to funds flow from operations is cash flows from operating activities. Management considers funds flow from operations important as it helps evaluate financial performance and demonstrates the Company’s ability to generate sufficient cash to fund future growth opportunities. Funds flow from operations should not be considered an alternative to, or more meaningful than, cash flows from operating activities however management finds that the impact of working capital items on the cash flows reduces the comparability of the metric from period to period. A reconciliation of funds flow from operations to cash flows from operating activities is as follows:

Net Working Capital

Net working capital is computed as current assets less current liabilities. Net working capital is a measure of liquidity, is used to evaluate financial resources, and is calculated as follows:

Working Capital Net of Debt

Working capital net of debt is computed as net working capital surplus decreased by the carrying amount of the Credit Facility. Working capital net of debt is used by management to assess the Company’s overall financial position.

Supplementary Financial Measures

“Average realized natural gas price – $/Mcf” is comprised of natural gas sales as determined in accordance with IFRS, divided by the Company’s natural gas sales volumes.

“Average realized NGL – condensate price – $/bbl” is comprised of condensate sales as determined in accordance with IFRS, divided by the Company’s NGL sales volumes from condensate.

“Average realized oil price – $/bbl” is comprised of oil sales as determined in accordance with IFRS, divided by the Company’s oil sales volumes.

“Average realized price – $/boe” is comprised of natural gas, condensate and oil sales as determined in accordance with IFRS, divided by the Company’s total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

“Royalties per boe” is comprised of royalties, as determined in accordance with IFRS, divided by the total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

“Production expenses per boe” is comprised of production expenses, as determined in accordance with IFRS, divided by the total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

BOE Disclosure

The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6 Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this MD&A are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Forward-Looking Statements and Cautionary Language

This news release contains forward-looking information within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward‐looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning the Company’s dividend policy, plans for dividends in the future, and the timing and taxation of such dividends, the Company’s intention to proceed with an NCIB, plans relating to the Company’s operational activities, the expected natural gas price, gas sales and gas deliveries under Alvopetro’s long-term gas sales agreement, exploration and development prospects of Alvopetro, the expected timing of certain of Alvopetro’s testing and operational activities, future results from operations, and the Company’s plans for dividends in the future. Forward-looking statements are necessarily based upon assumptions and judgments with respect to the future including, but not limited to, expected approvals and timing thereof with respect to an NCIB, equipment availability, the timing and results of testing the 183-B1 well, the 182-C2 well and the Unit C well, the success of future drilling, completion, recompletion and development activities, foreign exchange rates, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, the outlook for commodity markets and ability to access capital markets, the impact of the COVID-19 pandemic, the performance of producing wells and reservoirs, well development and operating performance, the timing of regulatory licenses and approvals, general economic and business conditions, forecasted demand for oil and natural gas, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. In addition, the declaration, timing, amount and payment of future dividends remain at the discretion of the Board of Directors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our restated annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

SOURCE Alvopetro Energy Ltd.

For further information: Corey C. Ruttan, President, Chief Executive Officer and Director, or Alison Howard, Chief Financial Officer, Phone: 587.794.4224, Email: info@alvopetro.com, www.alvopetro.com, TSX-V: ALV, OTCQX: ALVOF

Energy Fuels is a leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. Energy Fuels also produces vanadium from certain of its projects, as market conditions warrant, and is ramping up commercial-scale production of REE carbonate. Its corporate offices are in Lakewood, Colorado, near Denver, and all its assets and employees are in the United States. Energy Fuels holds three of America’s key uranium production centers: the White Mesa Mill in Utah, the Nichols Ranch in-situ recovery (“ISR”) Project in Wyoming, and the Alta Mesa ISR Project in Texas. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, has the ability to produce vanadium when market conditions warrant, as well as REE carbonate from various uranium-bearing ores. The Nichols Ranch ISR Project is on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Alta Mesa ISR Project is also on standby and has a licensed capacity of 1.5 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels also has one of the largest NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Energy Fuel reached a definitive agreement to sell the Alta Mesa mill to enCore Energy for $120 million. Energy Fuels will receive $60 million in cash upon closing and $60 million in convertible debt bearing an 8% annual interest rate. The mill is one of 11 licensed uranium processing plants and has an operating capacity of 1.5 million pounds per year. UUUU acquired Alta Mesa in 2016 for $13.6 million.

Energy Fuel, which operates Alta Mesa on a standby basis, did not have plans to activate the plant in the near future. Energy Fuel retains three other processing mills including the White Mesa mill which is licensed to produce 8 million pounds of uranium per year. We believe the White Mesa mill is large enough to meet all of UUUU’s uranium production needs in addition to producing vanadium and rare earth elements.The Alta Mesa plant costs approximately $2 million annually to maintain.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Non-dilutive sale of asset expected to materially enhance Energy Fuels’ balance sheet and help to fund the rapid advancement and expansion of near-term U.S. uranium and rare earth production

LAKEWOOD, Colo., Nov. 14, 2022 /CNW/ – Energy Fuels Inc. (NYSE American: UUUU) (TSX: EFR) (“Energy Fuels” or the “Company”), a leading U.S. producer of uranium and rare earth elements (“REE“), is pleased to announce that it has entered into a definitive agreement to sell three wholly-owned subsidiaries that together hold Energy Fuels’ Alta Mesa ISR Project (“Alta Mesa“) to enCore Energy (“enCore“) for total consideration of $120 million (the “Transaction“). The Transaction is expected to close by the end of 2022 or early 2023.

The Transaction is significant for the Company, as the cash received is expected to fully finance much of the Company’s uranium, REE, vanadium and medical isotope business plans for the next two to three years without diluting shareholders. These plans may include:

Ramping-up uranium production at one or more of the White Mesa Mill, the Nichols Ranch ISR Project, the Pinyon Plain mine, the La Sal Complex, and/or the Whirlwind mine which total up to two (2) million pounds of U3O8 per year of near-term, lower cost U.S. production capacity in order to fulfill commitments under existing and future long-term uranium supply agreements and as market conditions may warrant;

Accelerating the licensing and development of the Company’s larger-scale uranium mines, including the Sheep Mountain, Roca Honda, and/or Bullfrog projects, which together will add over five (5) million pounds of production capacity in the next several years;

Establishing an “ore purchasing” program to secure additional feed to the White Mesa Mill, from others in the region as uranium mining picks up in the region, thereby maximizing the facility’s existing eight (8) million pounds per year licensed uranium production capacity and having sole ownership of this production;

Financing the construction of “first to market” in the U.S. “Phase 1” REE separation infrastructure (up to 2,500 – 5,000 MT per year TREO capacity, including 500 – 1,000 MT per year of NdPr oxide or oxalate expected) at the White Mesa Mill;

Advancing the design, engineering and permitting of a planned, large “world significant” “Phase 2” crack-and-leach and “light” and “heavy” REE separation facility (up to 15,000 mT per year TREO capacity).

Developing the Company’s Bahia heavy mineral sand and REE project in Brazil upon successful acquisition of the project; and

Acquiring additional monazite supply to feed the Company’s rapidly growing REE business.

The $120 million of total consideration will be paid by enCore to Energy Fuels as follows:

$60 million cash at closing; and

$60 million in a secured convertible note (the “Note”), payable in two years from the closing, bearing annual interest of eight percent (8%). The Note will be convertible at Energy Fuels’ election into enCore shares at a 20% premium to the 10-day volume-weighted average price of enCore shares ending the day before the closing. enCore is currently traded on the TSXV and has applied for a listing on the NASDAQ. The Note will be guaranteed by enCore Energy Corp., will be fully secured by Alta Mesa, and enCore will not be permitted to further encumber Alta Mesa with any third-party indebtedness, royalty or stream while the Note is outstanding. Unless a block trade or similar distribution is executed by Energy Fuels to sell the enCore common shares underlying the Note, Energy Fuels will be limited to converting the Note into a maximum of $10 million principal amount of the Note per thirty (30) day period.

Furthermore, enCore will assume all reclamation liabilities associated with Alta Mesa (approximately $10.3 million) and pay Energy Fuels the cash collateral on the existing reclamation bonds (approximately $3.6 million). Once the reclamation liabilities are transferred to enCore, Energy Fuels will be nearly 60% collateralized on its remaining reclamation obligations. The Company also estimates that the sale of Alta Mesa will reduce Energy Fuels’ cash burn by approximately $2 million per year.

Energy Fuels acquired Alta Mesa in 2016 for approximately $13.6 million of shares, and currently carries this project on its balance sheet at $8.2 million. The Transaction represents an exceptional return on investment for Energy Fuels, and the value metrics of the Transaction compare favorably against precedent transactions within the uranium sector. Energy Fuels expects to replace the expected uranium production from Alta Mesa through permitting and production from its existing larger mining projects, ore purchases, toll milling arrangements, additional alternate feed and clean-up material, and potentially other transactions as market conditions may warrant.

Mark S. Chalmers, President and CEO of Energy Fuels stated: “This is a unique transaction for Energy Fuels. Not only does it allow us to monetize the Alta Mesa Project for $120 million, it allows our company to focus and accelerate our higher priority uranium and rare earth projects without dilution to our shareholders. This non-dilutive transaction will add cash to Energy Fuels’ significant working capital position, which was $122 million at September 30, 2022. Energy Fuels will also retain some exposure to short-term market upside and optionality at Alta Mesa and enCore through the convertible note.

“With recent uranium market strength and having secured new long-term uranium contracts with major U.S. nuclear utilities earlier this year, the Company is beginning to perform the work needed to recommence production at one or more of our projects, with production expected to start as soon as 2023. We have already hired about 20 people, and the cash we receive from the Alta Mesa transaction will help further fund this ramp-up. On top of this, the Company plans to establish an “ore purchasing” program from future uranium mining from others that maximizes the underutilized uranium production capacity of the White Mesa Mill with the uranium produced going 100% to our account in a way that others cannot. Energy Fuels absolutely intends to retain our position as the leading producer of uranium in the U.S. through our remaining outstanding portfolio of ISR and conventional uranium assets, and this transaction with enCore helps to both finance and focus our plans in this regard without dilution associated with equity financings.

“This cash also helps facilitate our plans to install rare earth separation infrastructure at our White Mesa Mill, including the expected capacity to produce approximately 500 – 1,000 tonnes per annum of separated ‘light’ rare earth oxides (or oxalates) by the end of 2023 or early 2024. We are also working on a number of fronts to secure additional monazite supply to feed our new rare earth infrastructure, and we expect this cash to significantly help finance purchases of monazite, fund our Bahia project in Brazil upon successful completion of that acquisition, and otherwise help in this regard. If we are successful with our rare earth initiatives, we have the potential to be the ‘first-to-market’ in the U.S. for the sale of commercial quantities of separated NdPr oxides (or oxalates), a raw material for rare earth permanent magnets used in electric vehicle drivetrains, wind energy systems, and defense applications. For reference, high-efficiency EVs each require about one to two kilograms of NdPr oxide. Therefore, in the next 12-18 months, if we are successful in constructing our Phase 1 rare earth separation capabilities, Energy Fuels could be domestically producing enough magnet material for 250,000 to 1 million EV drivetrains per year.

“I also believe this Transaction represents an important step forward for enCore Energy. Alta Mesa is a fully permitted and developed U.S. uranium project, and enCore’s President and CEO, Paul Goranson, knows it well, having constructed and operated it himself about ten years ago. To us, this appears to be a value creative transaction for both Energy Fuels and enCore.”

The closing of the Transaction is expected to occur by December 31, 2022. If the Transaction is not completed due to certain circumstances, enCore is required to pay to Energy Fuels a $6 million break fee.

Cantor Fitzgerald Canada Corporation is acting as Energy Fuels’ financial advisor and Dorsey & Whitney LLP and Dentons are acting as Energy Fuels’ legal advisors in connection with the Transaction.

About Energy Fuels: Energy Fuels is a leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. The Company also produces vanadium from certain of its projects, as market conditions warrant, and is ramping up to full commercial-scale production of RE Carbonate. Its corporate offices are in Lakewood, Colorado near Denver, and all its assets and employees are in the United States. Energy Fuels holds three of America’s key uranium production centers: the White Mesa Mill in Utah, the Nichols Ranch ISR Project in Wyoming, and the Alta Mesa ISR Project in Texas. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, and has the ability to produce vanadium when market conditions warrant, as well as RE Carbonate from various uranium-bearing ores. The Nichols Ranch ISR Project is currently on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Alta Mesa ISR Project is also currently on standby and has a licensed capacity of 1.5 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels also has one of the largest S-K 1300 and NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.