CALGARY, AB, Feb. 1, 2024 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.015 per common share payable on February 29, 2024, to shareholders of record at the close of business on February 15, 2024. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

SOURCE InPlay Oil Corp.

For further information: please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632, www.inplayoil.com; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Management updated its 2023 guidance. The adjustment reflects a drop in production expectations. New guidance is significantly below the 9,700 boe/d production flow reported from the field on November 9, 2023. The decline may represent a sharper decline rate from initial production rates than had previously been expected by management. The drop in production lead to a sharp reduction in projected Adjusted Funds Flow and Free Funds Flow.

Management also sharply reduced its 2024 production estimates. New guidance calls for 2024 production that is only slightly higher than newly revised 2023 guidance despite the drilling of 14-15 new wells and an expected reduction in curtailment. While it is possible that management is simply being conservative, it may also reflect well decline rates as discussed above.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, Jan. 29, 2024 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to announce that its Board of Directors have approved a capital program of $64 – $67 million for 2024.

2024 Capital Program Highlights

InPlay’s 2024 exploration and development capital program of $64 – $67 million is forecast to deliver the following(5):

Annual average production of 9,000 – 9,500 boe/d (59% – 61% light crude oil and NGLs);

Drilling program focused on high return oil weighted locations driving annual oil production growth at the midpoint of guidance of 7% over 2023;

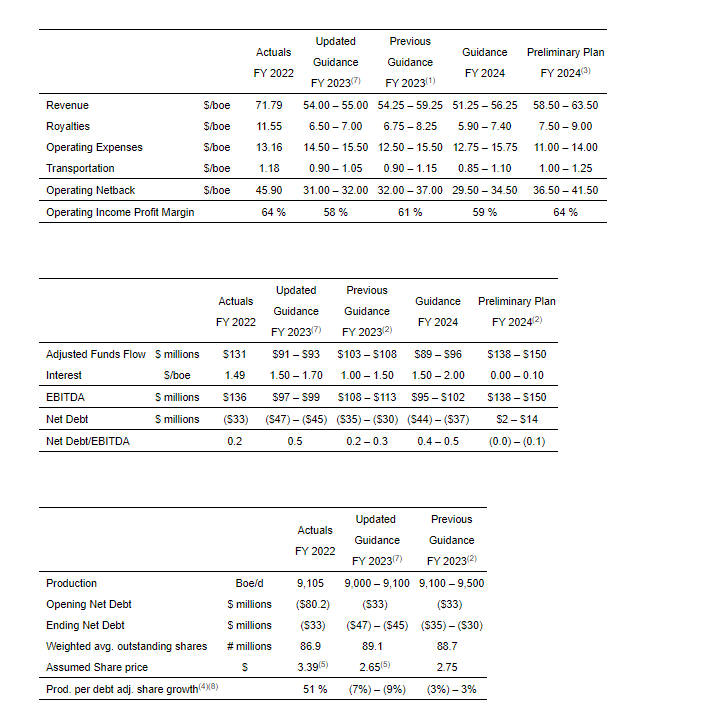

Operating income profit margin(2) of approximately 59%;

Reduction in capital spending of 20% – 25% compared to 2023 including reduced facilities and infrastructure spending by over 50% providing strong capital efficiencies;

Adjusted Funds Flow (“AFF”)(4) of $89 – $96 million;

Free Adjusted Funds Flow (“FAFF”)(2) of $22 – $32 million;

Net debt(4) of $37 – $44 million with a net debt to EBITDA ratio(2) of 0.4 – 0.5 times which is among the lower leverage ratios amongst our peers;

Base dividend of $16 – $17 million at the current monthly dividend rate of $0.015/share ($0.18/share annualized) which represents approximately an 8% yield at the current share price; and

Significant unutilized financial liquidity which can be used to pursue potential tactical capital investments.

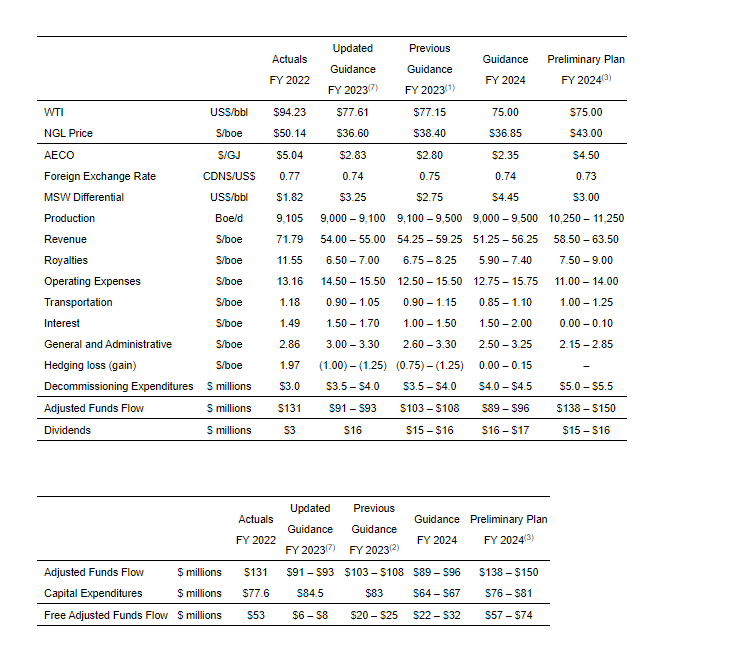

The table below highlights our 2024 guidance:

2024(5)

WTI (US$/bbl)

75.00

Production (boe/d) (1)

9,000 – 9,500

Capital ($ millions)

64 – 67

Net wells

14.0 – 15.0

AFF ($ millions) (4)

89 – 96

FAFF ($ millions) (2)

22 – 32

Net Debt at Year-end ($ millions) (4)

(44) – (37)

Annual Net Debt / EBITDA (2)

0.4 – 0.5

Dividend ($ millions)

16 – 17

The amounts above do not include potential future purchases through the Company’s normal course issuer bid (“NCIB”).

With continued commodity price volatility, specifically weak natural gas fundamentals, and current low investor sentiment, InPlay has taken a measured and disciplined approach to capital allocation for 2024, seeking to maximize capital efficiencies, AFF(2), and FAFF(2) supporting strong returns to shareholders with a priority on maintaining our pristine balance sheet. Despite a 20% to 25% reduction in capital spending year over year, InPlay is forecasting to deliver approximately 7% growth in our oil volumes as we focus on higher oil weighted assets that deliver greater returns. The capital program is designed to responsibly manage the pace of development, maintain flexibility and remain focused on delivering return of capital to shareholders.

Given the higher rate of return of InPlay’s oil weighted properties, the Company plans to direct its 2024 capital budget towards oil weighted drilling in the Cardium and Belly River. Plans are to drill approximately 11 – 12 net Extended Reach Horizontal (“ERH”) Cardium wells in Willesden Green and Pembina. Also, 3.0 net wells are planned in the Belly River taking advantage of the very high oil weighting of approximately 90%. These Belly River wells exhibit increasing oil rates over the first three quarters of production and a low decline rate thereafter. Our two most recent horizontal wells drilled in the Belly River, which came online in November 2022, have delivered operating netbacks of approximately $71.25/boe since being brought on production. Our higher oil weighted locations are characterized by strong light oil rates with lower total boe/d rate relative to wells with higher natural gas weightings. The Company’s 2024 drilling program plans on drilling fewer wells in 2024 compared to 2023, as a result of our cautious, disciplined capital approach for the year and is structured to take advantage of improving differentials starting in the second quarter of 2024 and throughout the balance of the year. Facility capital in 2024 is forecasted to be approximately $6.4 million less than 2023 due to the reduced drilling program and significant capital spent on two major natural gas plant upgrades completed in 2023.

InPlay’s first quarter of 2024 drilling program consists of five (4.9 net) ERH Cardium wells and three (0.7 net) non-operated ERH Cardium wells. Drilling has started on a two well (1.9 net) pad in Willesden Green which is expected to come on production in February. Capital activity will then move to Pembina to drill three (3.0 net) Cardium ERH wells. These wells will offset our five successful wells drilled in 2023 characterized by low decline rates and high light oil and liquids weighting with average initial production (“IP”) rates of 257 boe/d (89% light crude oil and liquids), 265 boe/d (86% light crude oil and liquids) and 239 boe/d (82% light crude oil and liquids) over their first 30, 60 and 180 days respectively.

InPlay made significant investments in 2023 to increase operated natural gas takeaway capacity for future growth in Willesden Green and to mitigate potential production issues arising from third party outage and capacity constraints. These projects have already shown their value by reducing back pressure on wells, lowering declines and providing more consistent runtimes while improving our liquids weighting with a higher natural gas liquids recovery. To further enhance our natural gas takeaway capabilities, InPlay has entered into a long term Gas Handling Agreement with an industry partner guaranteeing access to natural gas takeaway and processing capacity in the Company’s Pembina area where we were initially curtailed by approximately 6 mmcfd and associated oil and liquids starting on February 15, 2023 with the gradual reduction in curtailments and the full resumption of production in September 2023. This contract will allow InPlay to restart with certainty of capacity the development of this prolific and strong rate of return growth area where drilling activity has not occurred since the spring of 2022. InPlay plans on drilling a three (3.0 net) ERH Cardium well pad in this area in the third quarter of 2024. The Company projects fewer operated and non-operated turnarounds and other infrastructure issues during 2024 after an unprecedented high level of disruptions in 2023.

To mitigate risk and add stability during periods of market volatility, commodity hedges have been secured through 2024 and into 2025 as summarized below.

Q1/24

Q2/24

Q3/24

Q4/24

Q1/25

Natural Gas AECO Swap (mcf/d)

–

1,900

1,900

640

–

Hedged price ($AECO/mcf)

–

2.00

2.00

2.00

–

Natural Gas AECO Costless Collar (mcf/d)

4,870

3,790

3,790

5,050

3,790

Hedged price ($AECO/mcf)

2.48 – 3.82

2.08 – 2.77

2.08 – 2.77

2.27 – 3.04

2.48 – 3.46

Crude Oil Costless Collar (bbl/d)

–

1,000

–

–

–

Hedged price ($USD WTI/bbl)

–

72.00 – 80.25

–

–

–

Crude Oil Costless Collar (bbl/d)

330

–

–

–

–

Hedged price ($CAD WTI/bbl)

95.00 – 110.00

–

–

–

–

Crude Oil WTI Three-way Collar (bbl/d) (7)

–

–

1,000

1,000

–

Low sold put price ($USD WTI/bbl)

–

–

64.00

64.00

–

Mid bought put price ($USD WTI/bbl)

–

–

74.00

74.00

–

High sold call price ($USD WTI/bbl)

–

–

82.48

82.48

–

InPlay will continue to prudently allocate capital resources and adjust its capital plans in consideration of commodity prices, inflationary cost pressures and other aspects impacting our business. Should commodity prices improve and stabilize, InPlay will remain disciplined and flexible and can quickly adjust capital activity to respond to changing market conditions.

2023 Update

InPlay’s fourth quarter capital program consisted of drilling two (1.6 net) ERH wells in Willesden Green that were brought on production in November. Also, the company drilled its first (1.0 net) multilateral Belly River horizontal well which was brought on production in December. The well has been on production for approximately one month and is still in its initial stages of cleanup and early production results are meeting our internal expectations with oil cuts increasing, consistent with offsetting wells.

The increase in North American natural gas production coupled with a warm start to winter has natural gas storage inventories at very high levels resulting in weaker than expected natural gas prices during the fourth quarter that continued into 2024. Crude oil differentials began to weaken in November and widened throughout the quarter which impacted realized oil pricing during this period. Higher differentials are extending into the first quarter of 2024 but forward indices show them improving and narrowing starting in the second quarter of 2024 and throughout the remainder of the year.

Annual average production for 2023 is forecast to be approximately 9,050 boe/d(1) (58% light crude oil & NGLs) which was impacted by approximately 650 boe/d over the year due to extraordinary curtailments experienced from third party capacity constraints and turnarounds, Alberta wildfires, and from delays in starting up our natural gas facility in the third quarter as discussed in our prior press releases.

The table below highlights our updated forecasted 2023 guidance:

2023(3)

WTI (US$/bbl)

77.61

Production (boe/d) (1)

9,000 – 9,100

Capital ($ millions)

84.5

Net wells

17.1

AFF ($ millions) (4)

91 – 93

FAFF ($ millions) (2)

6 – 8

Net Debt at Year-end ($ millions) (4)

(45) – (47)

Dividend ($ millions)

16

See Reader Advisories for previous guidance and underlying assumptions.

As commented on above, continued commodity price volatility and current weak industry sentiment has resulted in the Company taking a conservative, disciplined approach to capital allocation in 2024. Preliminary estimates and plans for 2025 and beyond will be dependent on the stability of commodity prices and industry sentiment balancing manageable growth and ensuring the long term sustainability of our return of capital to shareholder strategy. As a result, the Company withdraws its preliminary estimates and plans for 2025.

We look forward to the profitable development of our high rate of return asset base and continuing to provide strong returns to shareholders through 2024 and beyond. On behalf of our employees, management team and Board of Directors, we would like to thank our shareholders for their support.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

See “Reader Advisories – Production Breakdown by Product Type”

2.

Non-GAAP financial measure or ratio that does not have a standardized meaning under International Financial Reporting Standards (IFRS) and GAAP and therefore may not be comparable with the calculations of similar measures for other companies. Please refer to “Non-GAAP and Other Financial Measures” contained within this press release.

3.

Based on estimated, unaudited year-end 2023 results. See “Reader Advisories – Forward Looking Information and Statements” for underlying assumptions related to our estimated, unaudited year-end 2023 results.

4.

Capital management measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

5.

See “Reader Advisories – Forward Looking Information and Statements” for key budget and underlying assumptions related to our 2024 capital program and associated guidance.

6.

Supplementary financial measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

7.

The WTI three-way collars are a combination high priced sold call, low priced sold put and a mid-priced bought put. The high sold call price is the maximum price the Company will receive for the contract volumes. The mid bought put price is the minimum price InPlay will receive, unless the market price falls below the low sold put strike price, in which case InPlay receives market price plus the difference between the mid bought put price minus the low sold put price.

Reader Advisories

Non-GAAP and Other Financial Measures

Throughout this press release and other materials disclosed by the Company, InPlay uses certain measures to analyze financial performance, financial position and cash flow. These non-GAAP and other financial measures do not have any standardized meaning prescribed under GAAP and therefore may not be comparable to similar measures presented by other entities. The non-GAAP and other financial measures should not be considered alternatives to, or more meaningful than, financial measures that are determined in accordance with GAAP as indicators of the Company performance. Management believes that the presentation of these non-GAAP and other financial measures provides useful information to shareholders and investors in understanding and evaluating the Company’s ongoing operating performance, and the measures provide increased transparency and the ability to better analyze InPlay’s business performance against prior periods on a comparable basis.

Non-GAAP Financial Measures and Ratios

Included in this document are references to the terms “free adjusted funds flow”, “operating income”, “operating netback per boe”, “operating income profit margin”, “Net Debt to EBITDA”, “Production per debt adjusted share” and “EV / DAAFF”. Management believes these measures and ratios are helpful supplementary measures of financial and operating performance and provide users with similar, but potentially not comparable, information that is commonly used by other oil and natural gas companies. These terms do not have any standardized meaning prescribed by GAAP and should not be considered an alternative to, or more meaningful than “profit (loss) before taxes”, “profit (loss) and comprehensive income (loss)”, “adjusted funds flow”, “capital expenditures”, “corporate acquisitions, net of cash acquired”, “net debt”, “weighted average number of common shares (basic)” or assets and liabilities as determined in accordance with GAAP as a measure of the Company’s performance and financial position.

Free Adjusted Funds Flow

Management considers FAFF an important measure to identify the Company’s ability to improve its financial condition through debt repayment and its ability to provide returns to shareholders. FAFF should not be considered as an alternative to or more meaningful than AFF as determined in accordance with GAAP as an indicator of the Company’s performance. FAFF is calculated by the Company as AFF less exploration and development capital expenditures and property dispositions (acquisitions) and is a measure of the cashflow remaining after capital expenditures before corporate acquisitions that can be used for additional capital activity, corporate acquisitions, repayment of debt or decommissioning expenditures or potentially return of capital to shareholders. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast FAFF.

Operating Income/Operating Netback per boe/Operating Income Profit Margin

InPlay uses “operating income”, “operating netback per boe” and “operating income profit margin” as key performance indicators. Operating income is calculated by the Company as oil and natural gas sales less royalties, operating expenses and transportation expenses and is a measure of the profitability of operations before administrative, share-based compensation, financing and other non-cash items. Management considers operating income an important measure to evaluate its operational performance as it demonstrates its field level profitability. Operating income should not be considered as an alternative to or more meaningful than net income as determined in accordance with GAAP as an indicator of the Company’s performance. Operating netback per boe is calculated by the Company as operating income divided by average production for the respective period. Management considers operating netback per boe an important measure to evaluate its operational performance as it demonstrates its field level profitability per unit of production. Operating income profit margin is calculated by the Company as operating income as a percentage of oil and natural gas sales. Management considers operating income profit margin an important measure to evaluate its operational performance as it demonstrates how efficiently the Company generates field level profits from its sales revenue. Refer to the “Forward Looking Information and Statements” section for a calculation of operating income, operating netback per boe and operating income profit margin.

Net Debt to EBITDA

Management considers Net Debt to EBITDA an important measure as it is a key metric to identify the Company’s ability to fund financing expenses, net debt reductions and other obligations. EBITDA is calculated by the Company as adjusted funds flow before interest expense. When this measure is presented quarterly, EBITDA is annualized by multiplying by four. When this measure is presented on a trailing twelve month basis, EBITDA for the twelve months preceding the net debt date is used in the calculation. This measure is consistent with the EBITDA formula prescribed under the Company’s Senior Credit Facility. Net Debt to EBITDA is calculated as Net Debt divided by EBITDA. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast Net Debt to EBITDA.

Production per Debt Adjusted Share

InPlay uses “Production per debt adjusted share” as a key performance indicator. Debt adjusted shares should not be considered as an alternative to or more meaningful than common shares as determined in accordance with GAAP as an indicator of the Company’s performance. Debt adjusted shares is a non-GAAP measure used in the calculation of Production per debt adjusted share and is calculated by the Company as common shares outstanding plus the change in net debt divided by the Company’s current trading price on the TSX, converting net debt to equity. Debt adjusted shares should not be considered as an alternative to or more meaningful than weighted average number of common shares (basic) as determined in accordance with GAAP as an indicator of the Company’s performance. Management considers Debt adjusted share to be a key performance indicator as it adjusts for the effects of capital structure in relation to the Company’s peers. Production per debt adjusted share is calculated by the Company as production divided by debt adjusted shares. Management considers Production per debt adjusted share is a key performance indicator as it adjusts for the effects of changes in annual production in relation to the Company’s capital structure. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast Production per debt adjusted share.

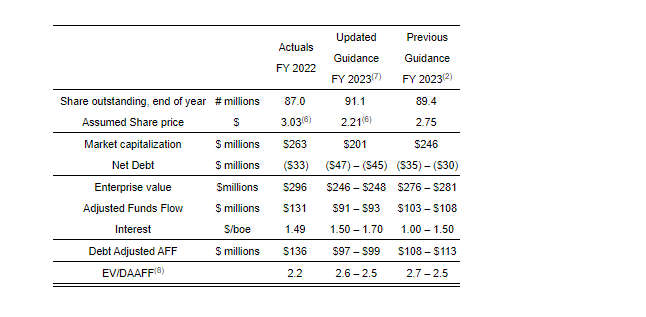

EV / DAAFF

InPlay uses “enterprise value to debt adjusted AFF” or “EV/DAAFF” as a key performance indicator. EV/DAAFF is calculated by the Company as enterprise value divided by debt adjusted AFF for the relevant period. Debt adjusted AFF (“DAAFF”) is calculated by the Company as adjusted funds flow plus financing costs. Enterprise value is a capital management measure that is used in the calculation of EV/DAAFF. Enterprise value is calculated as the Company’s market capitalization plus net debt. Management considers enterprise value a key performance indicator as it identifies the total capital structure of the Company. Management considers EV/DAAFF a key performance indicator as it is a key metric used to evaluate the sustainability of the Company relative to other companies while incorporating the impact of differing capital structures. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast EV/DAAFF.

Capital Management Measures

Adjusted Funds Flow

Management considers adjusted funds flow to be an important measure of InPlay’s ability to generate the funds necessary to finance capital expenditures. Adjusted funds flow is a GAAP measure and is disclosed in the notes to the Company’s financial statements for the year ending December 31, 2022 and the most recently filed quarterly financial statements. All references to adjusted funds flow throughout this document are calculated as funds flow adjusting for decommissioning expenditures and transaction and integration costs. Decommissioning expenditures are adjusted from funds flow as they are incurred on a discretionary and irregular basis and are primarily incurred on previous operating assets. Transaction costs are non-recurring costs for the purposes of an acquisition, making the exclusion of these items relevant in Management’s view to the reader in the evaluation of InPlay’s operating performance. The Company also presents adjusted funds flow per share whereby per share amounts are calculated using weighted average shares outstanding consistent with the calculation of profit per common share.

Net Debt

Net debt is a GAAP measure and is disclosed in the notes to the Company’s financial statements for the year ending December 31, 2022 and the most recently filed quarterly financial statements. The Company closely monitors its capital structure with the goal of maintaining a strong balance sheet to fund the future growth of the Company. The Company monitors net debt as part of its capital structure. The Company uses net debt (bank debt plus accounts payable and accrued liabilities less accounts receivables and accrued receivables, prepaid expenses and deposits and inventory) as an alternative measure of outstanding debt. Management considers net debt an important measure to assist in assessing the liquidity of the Company.

Supplementary Measures

“Average realized crude oil price” is comprised of crude oil commodity sales from production, as determined in accordance with IFRS, divided by the Company’s crude oil production. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“Average realized NGL price” is comprised of NGL commodity sales from production, as determined in accordance with IFRS, divided by the Company’s NGL production. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“Average realized natural gas price” is comprised of natural gas commodity sales from production, as determined in accordance with IFRS, divided by the Company’s natural gas production. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“Average realized commodity price” is comprised of commodity sales from production, as determined in accordance with IFRS, divided by the Company’s production. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“Adjusted funds flow per weighted average basic share” is comprised of adjusted funds flow divided by the basic weighted average common shares.

“Adjusted funds flow per weighted average diluted share” is comprised of adjusted funds flow divided by the diluted weighted average common shares.

“Adjusted funds flow per boe” is comprised of adjusted funds flow divided by total production.

Preliminary Financial Information

The Company’s expectations set forth in the updated forecasted 2023 guidance are based on, among other things, the Company’s anticipated financial results for the three and twelve month periods ended December 31, 2023. The Company’s anticipated financial results are unaudited and preliminary estimates that: (i) represent the most current information available to management as of the date of hereof; (ii) are subject to completion of audit procedures that could result in significant changes to the estimated amounts; and (iii) do not present all information necessary for an understanding of the Company’s financial condition as of, and the Company’s results of operations for, such periods. The anticipated financial results are subject to the same limitations and risks as discussed under “Forward Looking Information and Statements” below. Accordingly, the Company’s anticipated financial results for such periods may change upon the completion and approval of the financial statements for such periods and the changes could be material.

Forward-Looking Information and Statements

This news release contains certain forward–looking information and statements within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”, “may”, “will”, “project”, “should”, “believe”, “plans”, “intends”, “forecast” and similar expressions are intended to identify forward-looking information or statements. In particular, but without limiting the foregoing, this news release contains forward-looking information and statements pertaining to the following: the Company’s business strategy, milestones and objectives; all estimates and guidance related to the year ended 2023 results; the Company’s planned 2024 capital program including wells to be drilled and completed and the timing of the same; 2024 guidance based on the planned capital program and all associated underlying assumptions set forth in this press release including, without limitation, forecasts of 2024 annual average production levels, adjusted funds flow, free adjusted funds flow, Net Debt/EBITDA ratio, operating income profit margin, and Management’s belief that the Company can grow some or all of these attributes and specified measures; light crude oil and NGLs weighting estimates; expectations regarding future commodity prices; future oil and natural gas prices; future liquidity and financial capacity; future results from operations and operating metrics; future costs, expenses and royalty rates; future interest costs; the exchange rate between the $US and $Cdn; future development, exploration, acquisition, development and infrastructure activities and related capital expenditures, including our planned 2024 capital program; the amount and timing of capital projects;; and methods of funding our capital program.

The internal projections, expectations, or beliefs underlying our Board approved 2024 capital budget and associated guidance are subject to change in light of, among other factors, the impact of world events including the Russia/Ukraine conflict and war in the Middle East, ongoing results, prevailing economic circumstances, volatile commodity prices, and changes in industry conditions and regulations. InPlay’s 2024 financial outlook and guidance provides shareholders with relevant information on management’s expectations for results of operations, excluding any potential acquisitions or dispositions, for such time periods based upon the key assumptions outlined herein. Readers are cautioned that events or circumstances could cause capital plans and associated results to differ materially from those predicted and InPlay’s guidance for 2024 may not be appropriate for other purposes. Accordingly, undue reliance should not be placed on same.

Without limitation of the foregoing, readers are cautioned that the Company’s future dividend payments to shareholders of the Company, if any, and the level thereof will be subject to the discretion of the Board of Directors of InPlay. The Company’s dividend policy and funds available for the payment of dividends, if any, from time to time, is dependent upon, among other things, levels of FAFF, leverage ratios, financial requirements for the Company’s operations and execution of its growth strategy, fluctuations in commodity prices and working capital, the timing and amount of capital expenditures, credit facility availability and limitations on distributions existing thereunder, and other factors beyond the Company’s control. Further, the ability of the Company to pay dividends will be subject to applicable laws, including satisfaction of solvency tests under the Business Corporations Act (Alberta), and satisfaction of certain applicable contractual restrictions contained in the agreements governing the Company’s outstanding indebtedness.

Forward-looking statements or information are based on a number of material factors, expectations or assumptions of InPlay which have been used to develop such statements and information but which may prove to be incorrect. Although InPlay believes that the expectations reflected in such forward-looking statements or information are reasonable, undue reliance should not be placed on forward-looking statements because InPlay can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the impact of increasing competition; the general stability of the economic and political environment in which InPlay operates; the timely receipt of any required regulatory approvals; the ability of InPlay to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which InPlay has an interest in to operate the field in a safe, efficient and effective manner; the ability of InPlay to obtain debt financing on acceptable terms; the anticipated tax treatment of the monthly base dividend; the timing and amount of purchases under the Company’s NCIB; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and the ability of InPlay to secure adequate product transportation; future commodity prices; that various conditions to a shareholder return strategy can be satisfied; the ongoing impact of the Russia/Ukraine conflict and war in the Middle East; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which InPlay operates; and the ability of InPlay to successfully market its oil and natural gas products.

The forward-looking information and statements included herein are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward-looking information or statements including, without limitation: the continuing impact of the Russia/Ukraine conflict and war in the Middle East; inflation and the risk of a global recession; changes in our planned 2023 capital program; changes in our approach to shareholder returns; changes in commodity prices and other assumptions outlined herein; the risk that dividend payments may be reduced, suspended or cancelled; the potential for variation in the quality of the reservoirs in which we operate; changes in the demand for or supply of our products; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans or strategies of InPlay or by third party operators of our properties; changes in our credit structure, increased debt levels or debt service requirements; inaccurate estimation of our light crude oil and natural gas reserve and resource volumes; limited, unfavorable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time-to-time in InPlay’s continuous disclosure documents filed on SEDAR including our Annual Information Form and our MD&A.

This press release contains future-oriented financial information and financial outlook information (collectively, “FOFI”) about InPlay’s financial and leverage targets and objectives, potential dividends, share buybacks and beliefs underlying our Board approved 2024 capital budget and associated guidance, all of which are subject to the same assumptions, risk factors, limitations, and qualifications as set forth in the above paragraphs. The actual results of operations of InPlay and the resulting financial results will likely vary from the amounts set forth in this press release and such variation may be material. InPlay and its management believe that the FOFI has been prepared on a reasonable basis, reflecting management’s reasonable estimates and judgments. However, because this information is subjective and subject to numerous risks, it should not be relied on as necessarily indicative of future results. Except as required by applicable securities laws, InPlay undertakes no obligation to update such FOFI. FOFI contained in this press release was made as of the date of this press release and was provided for the purpose of providing further information about InPlay’s anticipated future business operations and strategy. Readers are cautioned that the FOFI contained in this press release should not be used for purposes other than for which it is disclosed herein.

The forward-looking information and statements contained in this news release speak only as of the date hereof and InPlay does not assume any obligation to publicly update or revise any of the included forward-looking statements or information, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Risk Factors to FLI

Risk factors that could materially impact successful execution and actual results of the Company’s 2023 and 2024 capital program and associated guidance and estimates include:

volatility of petroleum and natural gas prices and inherent difficulty in the accuracy of predictions related thereto;

the extent of any unfavourable impacts of wildfires in the province of Alberta.

changes in Federal and Provincial regulations;

the Company’s ability to secure financing for the Board approved 2024 capital program and longer-term capital plans sourced from AFF, bank or other debt instruments, asset sales, equity issuance, infrastructure financing or some combination thereof; and

those additional risk factors set forth in the Company’s MD&A and most recent Annual Information Form filed on SEDAR

Key Budget and Underlying Material Assumptions to FLI

The key budget and underlying material assumptions used by the Company in the development of its current and previous 2023 guidance and 2024 guidance are as follows:

The change in production per debt adjusted share growth between previous and updated guidance is primarily due to 2023 production being impacted by approximately 650 boe/d as a result of curtailments, Alberta wildfires, natural gas facility startup delays as discussed in the body of this press release.

(1)

As previously released August 14, 2023.

(2)

As previously released November 9, 2023.

(3)

As previously released January 18, 2023.

(4)

Production per debt adjusted share is calculated by the Company as production divided by debt adjusted shares. Debt adjusted shares is calculated by the Company as common shares outstanding plus the change in net debt divided by the Company’s current trading price on the TSX, converting net debt to equity. Future share prices are assumed to be consistent with the current share price.

(5)

Weighted average share price throughout 2022 and 2023.

(6)

Ending share price at December 31, 2022 and December 31, 2023.

(7)

The change in the 2023 forecasted results from prior guidance results from an increase in capital expenditures and decrease in adjusted funds flow as a result of a reduction to production, a higher natural gas weighting of total production and lower AECO natural gas prices than previously forecasted.

(8)

The Company has withdrawn its 2024 and 2025 production per debt adjusted share and EV/DAAFF forecast for 2024 and 2025. The Company believes that these metrics can be quite variable and hard to reasonably estimate given the volatility in the Company’s share price, which is a material assumption used in the calculation of these metrics.

(9)

Continued commodity price volatility and current weak industry sentiment has resulted in the Company taking a conservative and disciplined approach to capital allocation in 2024 and future years. Preliminary estimates and plans for 2025 and beyond will be dependent on the stability of commodity prices and industry sentiment balancing manageable growth and ensuring the long term sustainability of our return of capital to shareholder strategy. As a result, the Company withdraws its preliminary estimates and plans for 2025.

See “Production Breakdown by Product Type” below

Quality and pipeline transmission adjustments may impact realized oil prices in addition to the MSW Differential provided above

Changes in working capital are not assumed to have a material impact between the years presented above.

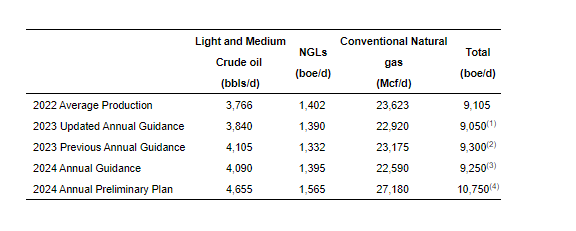

Production Breakdown by Product Type

Disclosure of production on a per boe basis in this press release consists of the constituent product types as defined in NI 51–101 and their respective quantities disclosed in the table below:

Notes:

1.

This reflects the mid-point of the Company’s 2023 updated production guidance range of 9,000 to 9,100 boe/d.

2.

This reflects the mid-point of the Company’s 2023 previous production guidance range of 9,100 to 9,500 boe/d.

3.

This reflects the mid-point of the Company’s 2024 production guidance range of 9,000 to 9,500 boe/d.

4.

This reflects the midpoint of the Company’s annual production previous preliminary estimate range.

5.

With respect to forward–looking production guidance, product type breakdown is based upon management’s expectations based on reasonable assumptions but are subject to variability based on actual well results.

References to crude oil, light oil, NGLs or natural gas production in this press release refer to the light and medium crude oil, natural gas liquids and conventional natural gas product types, respectively, as defined in National Instrument 51-101, Standards of Disclosure for Oil and Gas Activities (“NI 51-101”).

BOE Equivalent

Barrel of oil equivalents or BOEs may be misleading, particularly if used in isolation. A BOE conversion ratio of 6 mcf: 1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different than the energy equivalency of 6:1, utilizing a 6:1 conversion basis may be misleading as an indication of value.

Initial Production Rates

References in this press release to IP rates, other short-term production rates or initial performance measures relating to new wells are useful in confirming the presence of hydrocarbons; however, such rates are not determinative of the rates at which such wells will commence production and decline thereafter and are not indicative of long-term performance or of ultimate recovery. While encouraging, readers are cautioned not to place reliance on such rates in calculating the aggregate production for the Company. Accordingly, the Company cautions that the test results should be considered to be preliminary.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Hemisphere Energy reported 2024-4Q production results. Hemisphere Energy reported production of 3,375 boe/d, a 16% increase over the same period in 2022 and an 11% increase over 2023-3Q results. Production for the most recent quarter surpassed the 3,325 boe/d rate we had been using in our models.

Management gives initial 2024 production, pricing, and cost guidance. Management gave initial 2024 production, cash flow and capital expenditure guidance. Guidance was largely in line with our expectations.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

In the investing world, money often rotates between different sectors over time. After a long period of technology stocks dominating, we may now be entering a new cycle where mining and natural resource stocks start to outperform other industries and sectors. There are several compelling reasons mining could be the next big thing for investors.

First, demand is soaring for the critical minerals and metals used in electric vehicles, batteries, and clean energy. Metals like lithium, nickel, cobalt, and copper are essential for manufacturing electric car batteries, solar panels, wind turbines, and other green technologies. With many countries pushing for faster adoption of EVs and renewable power, demand for these key minerals is skyrocketing. Major automakers have announced ambitious electric vehicle plans, which requires secure access to raw materials. This imbalance between booming demand and limited supply bodes well for mining firms.

Additionally, the pandemic exposed risks of relying on a few countries for critical minerals. It revealed the need for domestic mining capacity to ensure stable access to essential inputs like lithium. For instance, the U.S. aims to boost domestic production of strategic minerals and reduce dependence on China. The EU also has a new plan to secure rare earth supplies within Europe. This focus on mineral independence is a plus for miners in North America and Europe.

Rising inflation and gold prices also bolster the case for mining stocks. With central banks printing huge amounts of money, many investors see gold as an inflation hedge. This has helped push gold prices to an 8-month high around $1900/ounce. Higher inflation tends to lift gold and silver prices as people flock to hard assets. Many miners produce both precious metals alongside base metals. They benefit from rising gold and silver prices.

Additionally, gold often rises when risks are high, like the current Russia-Ukraine and Israel-Gaza crises. Its safe haven appeal attracts buyers during geopolitical tensions. Between high inflation and geopolitical uncertainty, the macroeconomic environment seems favorable for both precious metal and base metal prices. This could kickstart a broad recovery across the mining sector.

The recent wave of mergers and acquisitions in mining also signals a positive shift. . In November 2023, Newmont Corporation completed its acquisition of Newcrest Mining Limited to create a leading global gold mining company with robust copper production. Just this month, Rio Tinto announced an $825 million lithium project purchase to support its battery materials business. These deals indicate big miners are positioning to capitalize on the electric vehicle revolution. Other companies like Century Lithium Corp. aim to produce lithium for the electric vehicle and battery storage market.

Additionally, mining stocks have held up well compared to the broader market’s decline. The global lithium stock index has surged over 110% in the past year. Many mining stocks linked to EVs have shown resilience amidst the tech stock plunge. This relative strength highlights the bullish outlook for miners enabling the energy transition. Noble Capital Markets’ investment banker Francisco Penafiel shared that “In the recent past, battery minerals have been getting the attention from investors, especially critical metals such as lithium and cobalt. However, base metals like copper and nickel should also gain a healthy traction from the investment community, narrowing the existing valuation gap for junior miners, due to the expected increase in their market demand as those are essential in the creation process of more efficient battery technologies”.

After years of underperformance, mining stocks also look attractive relative to potential growth. For instance, the price-to-earnings ratio for diversified mining giant Glencore is under 6x, a bargain compared to high-flying tech stocks. While mining is volatile, long-term investors could be rewarded handsomely for their patience. The time seems ripe for mining stocks to revert upward after years of neglect.

Of course, risks exist like policy changes, permitting issues, cost inflation, and ESG concerns. But the overarching trend toward electrification seems unstoppable. While mining is cyclical, we appear to be entering an upcycle driven by underinvestment in new supply and exploding demand for the minerals needed to power the green transition.

Noble Capital Markets’ Senior Research Analyst, Mark Reichman states, “Our outlook for the mining sector remains favorable, particularly for the precious metals mining sub-sector. We believe growing electrification among developed nations and increased infrastructure spending bodes well for the long-term outlooks for metals such as copper, lithium, rare earths, and nickel. We think M&A activity will continue as large mining, energy, car manufacturers, and battery makers seek to de-risk their long-term strategies by ensuring long-term supplies of raw materials.”

In summary, mining stocks check many important boxes right now – strong demand drivers, favorable macro conditions, M&A activity, and reasonable valuations after a prolonged slump. The long-overlooked mining space seems poised for a renaissance, offering investors exciting opportunities. The winds appear to be shifting in favor of mining stocks as we embark on the new year and beyond. After years stuck in the doldrums, mining finally looks set to retake the spotlight.

The energy sector experienced a major shakeup today as Sunoco LP announced it will acquire NuStar Energy in an all-stock deal valued at approximately $7.3 billion including debt. The blockbuster acquisition aims to create a more diversified and vertically integrated energy company with an expanded footprint across the value chain.

For Sunoco, the deal provides a number of key benefits that will strengthen its operations and financial position. Most notably, it will gain NuStar’s extensive pipeline and storage terminal network which spans over 9,500 miles across the United States. This will provide greater scale and diversification to Sunoco’s current focus on fuel distribution and retail. As pipeline assets generate steady contracted revenues, the acquisition is expected to add stability and predictability to cash flows.

The larger cash flow base will also improve Sunoco’s credit profile and enhance its financial flexibility. This will enable accelerated deleveraging while also supporting steady distribution growth. Management estimates the deal will be immediately accretive to distributable cash flow per unit by 10%+ within three years. Ongoing synergies of $150 million annually will also boost the bottom line.

Vertically integrating NuStar’s transportation and storage activities with Sunoco’s strengths in distribution and retail is another major strategic benefit. This will help optimize operations across the integrated value chain and lead to further efficiency gains over time. Cost savings are forecasted at $50 million per year.

For the energy sector overall, the deal also has important implications. The combined entity will control critical infrastructure delivering refined products across the United States. With its expanded footprint, Sunoco will play an even more pivotal role ensuring energy supplies are reliably transported to end-users nationwide.

The acquisition also arrives at a challenging time for the industry. Many energy companies are facing pressure from the transition towards renewable power. By combining forces, Sunoco and NuStar can cut costs, leverage their size and scale, and invest in new growth opportunities. This will ultimately strengthen their competitiveness and staying power.

However, the deal does raise some regulatory concerns. With its extensive control over pipelines and storage capacity, the merged company could potentially restrict competitors’ access. Watchdogs will want to ensure open access at fair rates. Still, management emphasized the acquisition will have a positive financial outlook and support continued distribution growth. This should benefit both sets of unitholders if the deal is approved as expected.

Looking ahead, the acquisition positions Sunoco and NuStar to play a pivotal role in the future of US energy infrastructure. Their integrated network will be crucial for delivering traditional and renewable fuels as the industry evolves. With enhanced financial strength and flexibility, the combined giants now have greater capacity to adapt and seize new opportunities in the years ahead.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

As indicated in our recent energy industry report, energy prices were weak in the quarter ended December 21, 2023. WTI oil prices averaged $78.41/bbl. below our $80/bbl. estimate. Henry Hub natural gas prices averaged $2.74/mcf. versus our $3.25/mcf estimate due to warm weather. The C$ to US$ exchange rate was 1.35 times versus our 1.33 estimate.

We are adjusted our estimates modestly to reflect updated energy price and exchange rate numbers. We now project December quarter revenues of C$27.1 million, down from C$27.7 million. Our EBITDA estimate for the quarter is now C$16.7 million versus C$17.2 million and our Adjusted Fund Flow estimate is C$13.2 million versus C$13.4 million. Our earnings per share estimate remains $0.11. We have not made any changes to our 2024 estimates.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

As indicated in our last energy industry report, oil and natural gas prices were weak in the December quarter. WTI oil prices averaged $78.40/bbl. in the quarter, below our previous estimate of $80/bbl. Henry Hub natural gas prices average $2.74/mcf., below our previous estimate of $3.25/mcf. due to warm weather. The C$ to US$ exchange rate was 1.35 times, slightly higher than our 1.33 estimate. We have adjusted our InPlay models to reflect updated results.

We are fine tuning our estimates to reflect lower energy prices and a higher exchange rate. Our revenue estimate for the 2023 December quarter has been lowered to C$44.7 million from C$47.2 million. Our EBITDA estimate for the quarter is now C$23.3 million, down from C$25.5 million and our Adjusted Fund Flow estimate is C$18.9 million, down from C$20.6 million. Our EPS estimate for the quarter drops to C$0.08 from C$0.09. We have not made any changes to our 2024 estimates. With this report, we are initiating 2024 quarterly estimates.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Independent oil and gas producer APA Corporation has agreed to purchase rival Callon Petroleum Company in an all-stock transaction valued at approximately $4.5 billion including debt. The deal expands APA’s operations in Texas’ prolific Permian Basin as the company continues building out a diversified oil and gas portfolio.

Under the definitive agreement announced Thursday, each Callon share will be exchanged for 1.0425 shares of APA common stock. This represents a purchase price of $38.31 per Callon share based on APA’s closing stock price on January 3rd.

APA expects to issue around 70 million new shares to fund the acquisition, leaving existing APA shareholders with 81% of the combined company. Callon shareholders will own the remaining 19% once the deal closes.

Strategic Fit

According to APA CEO and President John J. Christmann IV, Callon’s Delaware Basin assets perfectly complement APA’s existing Permian footprint.

He stated the deal “fits all the criteria of our disciplined approach to evaluating external growth opportunities.” It provides additional scale across the Permian while increasing APA’s oil mix.

Notably, Callon holds nearly 120,000 net acres in the Delaware Basin, an oil-rich subsection of the larger Permian. APA’s Delaware acreage will expand by over 50% after absorbing Callon’s properties.

Meanwhile, APA’s Midland Basin presence will continue driving natural gas volumes. The combined Permian portfolio increases APA’s total company oil production mix from 37% to 43%.

Accretive Metrics

APA expects the deal will prove accretive to key financial and value metrics. Management sees over $150 million in annual overhead, operational, and cost of capital synergies resulting from the increased scale.

The company will also benefit from Callon’s inventory of short-cycle drilling opportunities in the Permian. APA believes the deal enhances its portfolio of low-risk, high-return investments.

What’s more, the transaction stands to improve APA’s credit profile. The company will retire all of Callon’s existing debt after closing, replacing it with $2 billion in APA term loan facilities. This is expected to provide flexibility for near-term debt pay-down.

Conditions and Close

The definitive agreement has received unanimous approval from the boards of directors at both companies. The deal now requires customary regulatory clearances along with a thumbs up from Callon shareholders.

APA anticipates the acquisition will close during the second quarter of 2024. Upon closing, a representative from Callon will join APA’s board of directors.

APA’s current executive team led by Christmann will continue managing the expanded company. Headquarters will remain in Houston, Texas.

Diversified Portfolio

According to Christmann, the deal aligns with APA’s strategy of maintaining a globally diversified oil and gas portfolio. The company runs both legacy and exploration assets across the United States, Egypt, the UK, and offshore Suriname.

Post-acquisition, 36% of APA’s total production will come from international plays. The remaining 64% stems from U.S. assets, with the bulk supplied by the newly expanded Permian footprint.

Callon Brings Strong Permian Position

Founded in 1950, Callon Petroleum has grown into a leading independent Permian producer. The Houston-based company focuses on acquiring, exploring, and developing high-quality assets across the prolific West Texas basin.

As of September 2022, Callon reported net production of over 106,000 barrels of oil equivalent per day. Its portfolio includes a mix of productive acreage, infrastructure, and upside opportunities in both the Midland and Delaware Basins.

According to Callon President and CEO Joe Gatto, the combination with APA will enhance value for Callon shareholders. It also provides increased capital flexibility and potential from APA’s robust Permian operations.

The proposed acquisition marks the latest move in APA’s ongoing growth strategy. The company continues positioning itself as a diversified, large-scale independent oil and gas producer able to drive value across business cycles.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Energy stocks declined in the fourth quarter in response to falling energy prices. Energy stocks declined 7.2% during the 2023 fourth quarter. The movement of the XLE is similar to that of near-month oil future prices.

Oil prices declined sharply in the fourth quarter after a runup in the third quarter. West Texas Intermediate oil prices declined 21.1% in the fourth quarter to $71.65 per barrel. Domestic oil production continues to grow (up 7% year over year through October) even as the number of domestic oil rigs has decreased 20% since this time last year. Natural gas prices declined 14.2% during the quarter to $2.51 per thousand cubic feet (mcf) of gas. Weather was 13% warmer than normal in the December quarter. As a result, natural gas storage levels are at five-year seasonally high levels as they have been for the last twelve months.

Merger Activity is heating up. More than $100 billion in acquisitions were announced in the last three months as APA, Exxon Mobil and Chevron all announced transactions. The acquisitions come as major energy companies seek to expand production during a period when production growth from technological improvements seems to be slowing.

Energy Companies continue to generate high cash levels at current energy prices. Despite the drop in energy prices, operating netbacks (revenues less royalties and operating costs) remain high. With debt levels low, energy managements have raised capital budgets, increased dividends, and repurchased shares.

Valuations remain attractive. With the decline in energy company stock values, many companies are trading at enterprise values that are less than five times free cash flow. Given our belief that energy prices are entering a period of relative stability (oil prices trade in a range of $60-$10/bbl) and that stock prices have already reacted to energy price declines to the lower end of this range, we see limited downside to investing in energy stocks and large upside should energy prices rise.

Energy stocks declined in the fourth quarter in response to falling energy prices.

Energy stocks, as measured by the Energy Select Sector SPDR Fund (XLE) declined 7.2% during the 2023 fourth quarter. The decline stands in sharp contrast to an 11.2% increase in the S&P Composite index. The decline in the XLE began early with the index dropping almost 10% in the first week of the quarter before regaining its losses in the next two weeks. After peaking on October 18th, the index fell sharply over the next two months and never recovered from its losses. The movement of the XLE is similar to that of near-month oil future prices.

Oil prices declined sharply in the fourth quarter after a runup in the third quarter.

West Texas Intermediate oil prices declined 21.1% in the fourth quarter to $71.65 per barrel, offsetting a 30.0% increase in the third quarter. For the year, WTI declined 10%. The oil price spikes of 2022 that sent prices above $120 per barrel shortly after Russia invaded Ukraine seem a distant memory. Energy production disruptions and political sanctions have changed the direction of the flow of energy but not the overall global demand and supply of energy. We are keeping an eye on political developments in the Red Sea, but to date there has been little impact on oil prices. Domestic oil production continues to grow (up 7% year over year through October) even as the number of domestic oil rigs has decreased 20% since this time last year. The biggest decline has been in the Permian Basin. Almost all wells being drilled are now horizontal wells.

The decline in natural gas prices was not as sharp and was largely explained by warm weather.

Natural gas prices declined 14.2% during the quarter to $2.51 per thousand cubic feet (mcf) of gas. After sharp spikes in 2022, natural gas prices have settled into a narrow range between $2.00/mcf and $3.00/mcf. Weather was 13% warmer than normal on a population-weighted basis in the December quarter. As a result, natural gas storage levels are at five-year seasonally high levels as they have been for the last twelve months. Gas production continues to increase steadily, mainly to feed an increased demand for natural gas for power generation.

Merger Activity is heating up.

On January 4, 2024, APA Corporation, parent of Apache Corporation, agreed to acquire Callon Petroleum for approximately $4.5 billion in a stock-swap deal. The acquisition follows Exxon Mobil’s $59.5 billion agreement to buy Pioneer Natural Resources and Chevron’s $53 billion deal to buy Hess Corporation in October 2023. The acquisitions come as major energy companies seek to expand production during a period when production growth from technological improvements seems to be slowing. The acquisitions, while all three stock transactions, may also represent improved balance sheets and cash flow. As we have discussed in the past, energy companies have used recent energy price upcycles to pay down debt and repurchase shares as opposed to previous cycles when management expanded drilling efforts that eventually drove down energy prices. The result has been more muted energy price cycles that extend for longer periods of time.

Energy Companies continue to generate high cash levels at current energy prices.

Despite the drop in energy prices, operating netbacks (revenues less royalties and operating costs) remain high. With debt levels low, energy management have raised capital budgets, increased dividends, and repurchased shares. Management is always reluctant to raise dividends to levels that are unsustainable in a down cycle. As a result several energy companies have begun to institute special dividends. We expect manage to continue to invest in growth and reward shareholders even at current energy levels. Should energy prices rise, these activities should accelerate.

Valuations remain attractive.

With the decline in energy company stock values, many companies are trading at enterprise values that are less than five times free cash flow. We view this multiple as unsustainable given an increased use of cash flow to repurchase shares. This is especially true of companies with slow production decline curves such as the companies we follow in western Canada. Given our belief that energy prices are entering a period of relative stability (oil prices trade in a range of $60-$10/bbl) and that stock prices have already reacted to energy price declines to the lower end of this range, we see limited downside to investing in energy stocks and large upside should energy prices rise. We believe this is especially true for smaller cap energy stocks that have ample drilling opportunities and that could be takeover targets for larger energy companies that do not.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

Energy Fuels is a leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. Energy Fuels also produces vanadium from certain of its projects, as market conditions warrant, and is ramping up commercial-scale production of REE carbonate. Its corporate offices are in Lakewood, Colorado, near Denver, and all its assets and employees are in the United States. Energy Fuels holds three of America’s key uranium production centers: the White Mesa Mill in Utah, the Nichols Ranch in-situ recovery (“ISR”) Project in Wyoming, and the Alta Mesa ISR Project in Texas. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, has the ability to produce vanadium when market conditions warrant, as well as REE carbonate from various uranium-bearing ores. The Nichols Ranch ISR Project is on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Alta Mesa ISR Project is also on standby and has a licensed capacity of 1.5 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels also has one of the largest NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

UUUU and Astron Corp. executed a non-binding agreement to develop the Donald Mineral Sands Project. UUUU will contribute US$122 million in cash and $17.5 million in shares for a 49% interest and exclusive offtake for 7,000 (ramping up to 14,000) metric tons of monzanite sand annually. Energy Fuels has struggled to secure monzanite sand supply as it develops Rare Earth Element (REE) separation ability at its White Plains mill operations. The Donald Project is capable of supplying all of UUUU’s projected supply needs beginning in 2026 and supplements a similar size investment project for Energy Fuels in Brazil currently under development. Our models assume monazite supply of 20,000 metric tons in 2027 and beyond. The combined supply projects could mean Energy Fuels could expand REE operations beyond 20,000 tons faster than previously expected.

A MOU is just a MOU but the potential impact on revenues is significant. UUUU has exclusive investment rights through March 1, 2024 but has no assurances that the agreement will become official. Furthermore, the MOU does not indicate any implied supply costs. Management estimates that the monazite will produce 4,000-8,000 tonnes of TREO. The primary element from TREO is Neodymium currently trading around $56/kg or $56 million per 1,000 tonnes. With 850-1,700 tonnes of NdPr expected to be produced, the project could generate $100 million in sales before we start adding in the value of other elements. Margins are tougher to predict. We have assumed margins of 33% based on the operations of other publicly traded REE companies.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.