BRENTWOOD, Tenn., April 01, 2026 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (“CoreCivic”) announced today that it will release its 2026 first quarter financial results after the market closes on Wednesday, May 6, 2026. A live broadcast of CoreCivic’s conference call will begin at 10:00 a.m. central time (11:00 a.m. eastern time) on Thursday, May 7, 2026.

To participate via telephone and join the call live, please register in advance. Upon registration at https://register-conf.media-server.com/register/BI100ac825f20b4333aeddd3f8e1c0fdff, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

Participants may access the audio-only webcast of the conference call from the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page. A replay of the webcast will be available for seven days.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

BRENTWOOD, Tenn., March 11, 2026 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (“CoreCivic”) announced today that it has received approval for a Special Use Permit (SUP) at the Company’s 1,033-bed Midwest Regional Reception Center in Leavenworth, Kansas. The facility has been undergoing reactivation since a new contract was awarded in the third quarter of 2025 but experienced a temporary delay in the intake process as we worked through legal challenges and the SUP approval process.

Now that the SUP has been approved, we expect to begin accepting detainees at the Midwest Regional Reception Center in the coming weeks. In preparation for reactivation last year, we initiated hiring efforts and attracted a strong candidate pool. We subsequently paused hiring in December 2025 while the SUP application was under review, reflecting a disciplined approach to aligning staffing with regulatory timing and operational readiness. Taking into account start-up activities and the phased commencement of intake operations, we currently expect this facility to contribute approximately $0.05 to $0.06 in incremental earnings per share for the remainder of 2026.

Patrick D. Swindle, CoreCivic’s President and Chief Executive Officer, commented, “I would like to thank the Leavenworth City Commission for their collaboration and trust. We value our longstanding relationship with the Leavenworth community and are pleased with the outcome of the SUP application process. This approval allows us to move ahead with reactivation of the Midwest Regional Reception Center as we continue to deliver safe, effective solutions for our government partners.”

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

This press release includes statements as to our beliefs and expectations of the outcome of future events that are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements may include such words as “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “may,” “will,” “should,” “can have,” “likely,” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events. Such forward-looking statements may be affected by risks and uncertainties in CoreCivic’s business and market conditions. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. Important factors that could cause actual results to differ are described in the filings made from time to time by CoreCivic with the Securities and Exchange Commission (“SEC”) and include the risk factors described in CoreCivic’s Annual Report on Form 10-K for the fiscal year ended December 31, 2025, filed with the SEC on February 20, 2026. Except as required by applicable law, CoreCivic undertakes no obligation to update forward-looking statements made by it to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events.

Facility Activations and Higher Occupancy Drive Strong Financial Performance Establishes 2026 Full Year Guidance

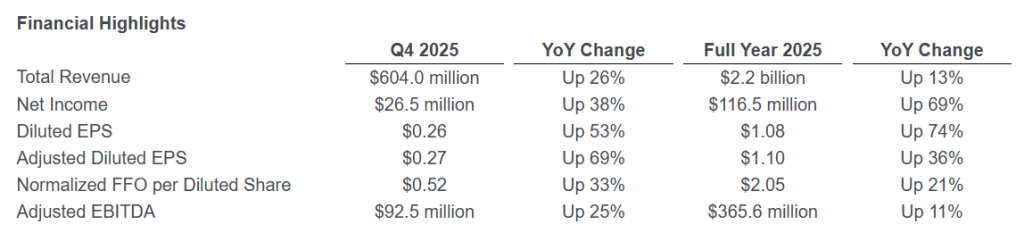

BRENTWOOD, Tenn., Feb. 11, 2026 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (CoreCivic or the Company) announced today its fourth quarter and full year 2025 financial results.

Patrick Swindle, CoreCivic’s President and Chief Executive Officer, commented, “We closed 2025 with strong financial performance, which wouldn’t have been possible without the tremendous efforts of our professional staff and the trust of our government partners. We anticipate 2026 will be a continued period of increased demand from our federal, state, and local government partners. CoreCivic is well-positioned to meet this growing demand given our readily available capacity, experienced management team, and our strong balance sheet.”

“CoreCivic has strategically deployed capital investments over the past year, enabling us to win new contract awards at four of the nine facilities that were idle at the beginning of the year, while positioning our remaining five idle facilities for potential re-activation. As indicated in our financial guidance, we expect 2026 to be another year of strong growth as several of our previously idle facilities continue to receive additional populations during 2026, and as demand for our solutions persists.”

Swindle continued, “CoreCivic’s balance sheet remains strong, and we are pleased with the continued execution of our capital strategy, ending the quarter with leverage, measured as net debt to Adjusted EBITDA, at 2.8x for the trailing twelve months. With the strength of earnings and growth outlook in 2026, and balance sheet flexibility enhanced through our recently expanded revolving credit facility, we expect to remain active with our share repurchase program, as our stock price is trading below historical multiples.”

Fourth Quarter 2025 Financial Results Compared With Fourth Quarter 2024

Net income in the fourth quarter of 2025 was $26.5 million, or $0.26 per diluted share, compared with net income in the fourth quarter of 2024 of $19.3 million, or $0.17 per diluted share (Diluted EPS). When adjusted for special items, Adjusted Net Income for the fourth quarter of 2025 was $28.1 million, or $0.27 per diluted share (Adjusted Diluted EPS), compared with Adjusted Net Income in the fourth quarter of 2024 of $18.2 million, or $0.16 per diluted share. Special items for each period are presented in detail in the calculation of Adjusted Net Income and Adjusted Diluted EPS in the Supplemental Financial Information following the financial statements presented herein.

The increase in Diluted EPS and Adjusted Diluted EPS compared with the prior year quarter resulted from the resumption of operations at the 2,400-bed Dilley Immigration Processing Center (Dilley Facility) in the first quarter of 2025, higher federal and state populations, and the acquisition of the Farmville Detention Center on July 1, 2025. Funding for the Dilley Facility was previously terminated effective August 9, 2024, and the facility remained idle until its reactivation effective March 5, 2025. Occupancy levels in our Safety and Community segments combined increased to 78.1% in the fourth quarter of 2025 compared with 75.5% in the fourth quarter of 2024.

Per share results were also favorably impacted by a decrease in shares of our common stock outstanding as a result of our share repurchase program. These favorable results were partially offset by $3.6 million of facility net operating losses in the fourth quarter of 2025 at our 2,560-bed California City Immigration Processing Center (California City Facility) and our 2,160-bed Diamondback Correctional Facility, two previously idle facilities currently being activated pursuant to new management contracts. We currently expect the California City Facility and the Diamondback Correctional Facility to reach stabilized occupancy in the first and second quarters of 2026, respectively. Results for the fourth quarter of 2025 also reflected strategic investments in staffing to support elevated demand for bed capacity, as well as a mission transition at our 2,552-bed Trousdale Turner Correctional Center that aligns the facility’s reentry-focused services with changing population demographics. That transition resulted in temporarily lower population levels and higher expenses but is expected to strengthen long-term operational performance.

Management revenue from U.S. Immigration & Customs Enforcement (ICE), our largest government partner, more than doubled from the fourth quarter of 2024, reflecting the resumption of operations at the Dilley Facility, the activations of our California City Facility and our 600-bed West Tennessee Detention Facility, and the acquisition of the Farmville Detention Center. During the fourth quarter of 2025, revenue from ICE was $244.7 million compared to $120.3 million during the fourth quarter of 2024. Revenue from state customers increased 5.0% compared with the year-ago quarter, with broad-based improvement, highlighted by growth within the states of Georgia, Montana and Colorado.

Facility operating margins in the Safety segment were negatively impacted during 2025 by start-up expenses incurred during the activation of our previously idled California City, West Tennessee, and Diamondback facilities, none of which has yet reached stabilized occupancy. While the facility operating margin in our Safety and Community segments decreased to 22.2% in the fourth quarter of 2025 from 23.6% in the prior year quarter, we expect margin improvement in 2026 as these facilities reach stabilized occupancy.

Earnings before interest, taxes, depreciation and amortization (EBITDA) was $90.3 million in the fourth quarter of 2025, compared with $75.7 million in the fourth quarter of 2024. Adjusted EBITDA, which excludes special items, was $92.5 million in the fourth quarter of 2025, compared with $74.2 million in the fourth quarter of 2024. The increase in Adjusted EBITDA was primarily driven by the resumption of operations at the Dilley Facility, the acquisition of the Farmville Detention Facility, and a general increase in occupancy throughout our portfolio.

Funds From Operations (FFO) for the fourth quarter of 2025 was $53.5 million, compared with $43.3 million in the fourth quarter of 2024. Normalized FFO, which excludes special items, increased to $54.0 million, or $0.52 per diluted share, in the fourth quarter of 2025, compared with $43.3 million, or $0.39 per diluted share, in the fourth quarter of 2024. Normalized FFO per share was positively impacted by the same factors that affected Adjusted EBITDA, as well as a 6.6% reduction in weighted average shares outstanding compared with the prior year quarter, partially offset by increases in interest and general and administrative expenses.

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share amounts, are measures calculated and presented on the basis of methodologies other than in accordance with generally accepted accounting principles (GAAP). Please refer to the Supplemental Financial Information and the note following the financial statements herein for further discussion and reconciliations of these measures to net income, the most directly comparable GAAP measure.

Capital Strategy

Share Repurchases. Our Board of Directors (BOD) previously approved a share repurchase program authorizing the Company to repurchase up to $225.0 million of our common stock in 2022, which has subsequently been increased to up to an aggregate amount of $700.0 million of our common stock through a series of increases by our BOD, including two increases during 2025. During 2025, we repurchased 11.2 million shares of common stock under the share repurchase program at an aggregate purchase price of $218.4 million, including 5.3 million shares during the fourth quarter of 2025 at an aggregate purchase price of $97.3 million. Since the share repurchase program was authorized in May 2022, through December 31, 2025, we have repurchased a total of 25.7 million shares at an aggregate price of $399.5 million, or $15.52 per share, excluding fees, commissions and other costs related to the repurchases.

As of December 31, 2025, we had $300.5 million remaining under the share repurchase program. Additional repurchases of common stock will be made in accordance with applicable securities laws and may be made at management’s discretion within parameters set by the BOD from time to time in the open market, through privately negotiated transactions, or otherwise, subject to restricted payment limitations in our debt agreements. The share repurchase program has no time limit and does not obligate us to purchase any particular amount of our common stock. The authorization for the share repurchase program may be terminated, suspended, increased or decreased by our BOD in its discretion at any time.

Expanded Revolving Credit Facility. On December 1, 2025, we amended our Bank Credit Facility to increase the size of the accordion feature that provides for uncommitted incremental extensions of credit from the greater of $200.0 million or 50% of Consolidated EBITDA for the period of four fiscal quarters most recently ended to the greater of $300.0 million or 50% of Consolidated EBITDA for the period of four quarters most recently ended, and to exercise the accordion feature by expanding the capacity under our revolving credit facility from $275.0 million to $575.0 million. Expanding the size of our revolving credit facility provides us with enhanced balance sheet flexibility while remaining positioned for strategic investments and long-term value creation, such as through our share repurchase program.

Business Developments

West Tennessee Detention Facility. On August 14, 2025, we announced that we had been awarded a new contract under an Intergovernmental Services Agreement (IGSA) between the City of Mason, Tennessee and ICE to resume operations at our 600-bed West Tennessee Detention Facility. We began receiving detainees at the facility in September 2025, and as of December 31, 2025, we cared for 449 residents. Activation is currently expected to be completed by the end of the first quarter 2026. Total annual revenue once the facility is fully activated is expected to be $30 million.

California City Immigration Processing Center. On September 29, 2025, we transitioned from a short-term Letter Contract and, effective September 1, 2025, entered into a longer-term definitized contract with ICE for a two-year period at our 2,560-bed California City Facility. We began receiving detainees at the facility in August 2025, and as of December 31, 2025, we cared for 1,436 residents. Activation is expected to be completed in the first quarter of 2026. Total annual revenue once the facility is fully activated is expected to be approximately $130 million.

Midwest Regional Reception Center. On September 29, 2025, we transitioned from a short-term Letter Contract and, effective September 7, 2025, entered into a longer-term definitized contract with ICE for a two-year period at our 1,033-bed Midwest Regional Reception Center in Leavenworth, Kansas. The intake process continues to be delayed by the City of Leavenworth alleging that a Special Use Permit (SUP) is required to operate the facility. A lawsuit we filed in state court alleging that an SUP is not applicable under existing statute remains under appeal. However, after unsuccessfully pursuing a lawsuit in federal court alleging violations of certain federal rights, in December 2025 we filed an application for the SUP. We can provide no assurance that the SUP will be approved or that the legal appeal in state court will be successful, and therefore, cannot predict if or when we will be able to accept detainee populations at this facility. Total annual revenue if the facility is fully activated is expected to be approximately $60 million.

Diamondback Correctional Facility. On October 1, 2025, we announced a new contract award under an IGSA between the Oklahoma Department of Corrections and ICE to resume operations at our 2,160-bed Diamondback Correctional Facility. The new contract commenced on September 30, 2025, expires in September 2029, and may be extended through bilateral modification. We began receiving detainees in December 2025, with stabilized occupancy estimated to be reached in the second quarter of 2026. Total annual revenue once the facility reaches stabilized occupancy is expected to be approximately $100 million.

2026 Financial Guidance

Based on current business conditions, we are providing the following financial guidance for the full year 2026:

Full Year 2026

Net income

$147.5 million to $157.5 million

Diluted EPS

$1.49 to $1.59

FFO per diluted share

$2.54 to $2.64

EBITDA

$437.0 million to $445.0 million

Consistent with our past practice, our guidance does not include the impact of any new contract awards not previously announced, or the activation of any of our remaining five idle correctional and detention facilities. Additionally, our guidance does not include activation of the Midwest Regional Reception Center, which could be activated promptly if delays related to a SUP are resolved satisfactorily. Our guidance does not include any acquisitions or dispositions, nor does it contemplate any significant changes in how the federal government, including ICE, elects to use our detention capacity or otherwise procures alternative detention capacity.

The activation of an idle facility generally requires three to six months to hire, train, and prepare the facility to accept residential populations, which, depending on contract structure, can result in additional expenses before we are able to realize additional revenue. To the extent any new contract requires the activation of an idle facility, our guidance will likely be negatively impacted by these start-up expenses until the revenue we generate offsets these expenses.

During 2026, we expect to invest $30.0 million to $35.0 million in maintenance capital expenditures on real estate assets, $30.0 million to $35.0 million for maintenance capital expenditures on other assets and information technology, and $15.0 million for other capital investments. We also expect to invest $35.0 million to $40.0 million for capital expenditures associated with previously idled facilities we are activating and for additional potential facility activations, in order to prepare these facilities to quickly accept residential populations if opportunities arise, which includes approximately $23.5 million of such expenditures included in our 2025 guidance but not spent by year-end.

Supplemental Financial Information and Investor Presentations

We have made available on our website supplemental financial information and other data for the fourth quarter of 2025. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Financial Information” of the Investors section. We do not undertake any obligation and disclaim any duties to update any of the information disclosed in this report.

Management may meet with investors from time to time during the first quarter of 2026. Written materials used in the investor presentations will also be available on our website beginning on or about February 24, 2026. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Events & Presentations” of the Investors section.

Conference Call, Webcast and Replay Information

We will host a webcast conference call at 10:00 a.m. central time (11:00 a.m. eastern time) on Thursday, February 12, 2026, which will be accessible through the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page.

To participate via telephone and join the call live, please register in advance here https://register-conf.media-server.com/register/BId7159f6814fc440f9348e9f8e6ec91f1. Upon registration, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements

This press release contains statements as to our beliefs and expectations of the outcome of future events that are “forward-looking” statements as defined within the meaning of the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. These include, but are not limited to, the risks and uncertainties associated with: (i) changes in government policy, legislation and regulations that affect utilization of the private sector for corrections, detention, and residential reentry services, in general, or our business, in particular, including, but not limited to, the continued utilization of our correctional and detention facilities by the federal government as a consequence of presidential executive orders, changes in how the federal government, including ICE, elects to use our detention capacity or otherwise procures alternative detention capacity, and the impact of any changes to immigration reform and sentencing laws (we do not, under longstanding policy, lobby for or against policies or legislation that would determine the basis for, or duration of, an individual’s incarceration or detention); (ii) our ability to obtain and maintain correctional, detention, and residential reentry facility management contracts because of reasons including, but not limited to, sufficient governmental appropriations, contract compliance, negative publicity and effects of inmate disturbances; (iii) changes in the privatization of the corrections and detention industry, the acceptance of our services, the timing of the opening of new facilities and the commencement of new management contracts (including the extent and pace at which new contracts are utilized), as well as our ability to utilize available beds; (iv) our ability to successfully activate idle facilities in a timely manner in order to meet the growth in demand for our facilities and services from the federal government that has occurred as a result of changes in policies and actions of the current presidential administration, and to realize projected returns resulting therefrom; (v) general economic and market conditions, including, but not limited to, the impact governmental budgets can have on our contract renewals and renegotiations, per diem rates, and occupancy; (vi) fluctuations in our operating results because of, among other things, changes in occupancy levels; competition; contract renegotiations or terminations; inflation and other increases in costs of operations, including a rise in labor costs; fluctuations in interest rates and risks of operations; (vii) government budget uncertainty, the impact of debt ceilings and the potential for government shutdowns and changing budget priorities; (viii) our ability to successfully identify and consummate future development and acquisition opportunities, integrate their operations, and realize projected returns resulting therefrom; and (ix) the availability of debt and equity financing on terms that are favorable to us, or at all. Other factors that could cause operating and financial results to differ are described in the filings we make from time to time with the Securities and Exchange Commission.

We take no responsibility for updating the information contained in this press release following the date hereof to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events or for any changes or modifications made to this press release or the information contained herein by any third-parties, including, but not limited to, any wire or internet services, except as may be required by law.

BRENTWOOD, Tenn., Jan. 06, 2026 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (“CoreCivic”) announced today that it will release its 2025 fourth quarter financial results after the market closes on Wednesday, February 11, 2026. A live broadcast of CoreCivic’s conference call will begin at 10:00 a.m. central time (11:00 a.m. eastern time) on Thursday, February 12, 2026.

To participate via telephone and join the call live, please register in advance. Upon registration at https://register-conf.media-server.com/register/BId7159f6814fc440f9348e9f8e6ec91f1, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

Participants may access the audio-only webcast of the conference call from the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page. A replay of the webcast will be available for seven days.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

BRENTWOOD, Tenn., Dec. 12, 2025 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (“CoreCivic” or the “Company”) announced today that CoreCivic’s Board of Directors (the “Board”) has appointed Daren Swenson, who currently serves as CoreCivic’s Senior Vice President and Chief Corrections Officer, to Executive Vice President and Chief Corrections and Reentry Officer (CCRO), effective January 1, 2026, overseeing the operations for our corrections, detention, and reentry facilities.

Damon T. Hininger, CoreCivic’s Chief Executive Officer, commented, “Daren is an exceptional leader whose decades of service within the organization has allowed him to develop an in-depth knowledge of our business. I am confident that Daren’s demonstrated abilities will serve us well in the midst of a period of rapid growth.”

Patrick D. Swindle, CoreCivic’s President and Chief Operating Officer, added, “I look forward to Daren’s continued contributions to operational excellence, drawing on his extensive experience with the Company, as we tend to the growing needs of our government partners.”

Mr. Swenson said, “I am deeply honored by the trust CoreCivic’s Board and executive leadership have placed in me with this new role. Having spent my career with CoreCivic since 1992, I have witnessed firsthand the dedication and professionalism of our team as we work to serve our government partners and the public good. I am grateful for the opportunity to continue helping individuals on their path to reentry and addressing the complex needs of our government partners. As we move forward during this exciting period of growth, I look forward to working alongside my colleagues to deliver innovative solutions and uphold the high standards that define CoreCivic.”

Mr. Swenson began his career with CoreCivic in 1992 at our Prairie Correctional Facility in Appleton, Minnesota as a Correctional Sergeant. Before becoming Senior Vice President and Chief Corrections Officer of the Company, Mr. Swenson progressed through multiple leadership positions including Warden, Managing Director, and Vice President. Mr. Swenson holds bachelor’s degrees in psychology and sociology from North Dakota State University and a master’s degree in management with a concentration in Organizational Leadership from Middle Tennessee State University.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

This press release includes forward-looking statements concerning executive leadership positions at CoreCivic and prospects of growth in CoreCivic’s business. These forward-looking statements may include such words as “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “may,” “will,” “should,” “can have,” “likely,” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events. Such forward-looking statements may be affected by risks and uncertainties in CoreCivic’s business and market conditions. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. Important factors that could cause actual results to differ are described in the filings made from time to time by CoreCivic with the Securities and Exchange Commission (“SEC”) and include the risk factors described in CoreCivic’s Annual Report on Form 10-K for the fiscal year ended December 31, 2024, filed with the SEC on February 21, 2025. Except as required by applicable law, CoreCivic undertakes no obligation to update forward-looking statements made by it to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events.

BRENTWOOD, Tenn., Nov. 10, 2025 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (“CoreCivic”) announced today that its Board of Directors authorized an increase to its existing share repurchase program pursuant to which CoreCivic may purchase up to an additional $200 million in shares of CoreCivic’s outstanding common stock. As a result of the increase, the aggregate authorization under CoreCivic’s repurchase program increased from up to $500.0 million shares of common stock to up to $700.0 million shares of common stock.

Since the share repurchase program was authorized in May 2022, through November 7, 2025, we have repurchased a total of 21.5 million shares of our common stock at an aggregate cost of $322.1 million, or $14.98 per share, excluding fees, commissions and other costs related to the repurchases. As of November 7, 2025, including the additional authorization, we have $377.9 million of repurchase authorization available under the share repurchase program.

Damon T. Hininger, CoreCivic’s Chief Executive Officer, commented, “We are pleased to announce an increase to our stock repurchase authorization. We remain committed to deploying capital in ways that we believe will enhance long-term shareholder value. While our share price is influenced by many factors outside our control, we believe our current valuation does not fully reflect the progress and opportunities we see in our business.”

Patrick D. Swindle, CoreCivic’s President and Chief Operating Officer, added, “We believe our recently announced contract awards and the overall strength of our business position us well to execute on our capital allocation strategy. Given our earnings trajectory, alternative opportunities to deploy capital, and our current share price, we are prioritizing the allocation of our cash flows to our share repurchase program.”

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

This press release includes statements as to our beliefs and expectations of the outcome of future events that are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements may include such words as “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “may,” “will,” “should,” “can have,” “likely,” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events. Such forward-looking statements may be affected by risks and uncertainties in CoreCivic’s business and market conditions. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. Important factors that could cause actual results to differ are described in the filings made from time to time by CoreCivic with the Securities and Exchange Commission (“SEC”) and include the risk factors described in CoreCivic’s Annual Report on Form 10-K for the fiscal year ended December 31, 2024, filed with the SEC on February 21, 2025. Except as required by applicable law, CoreCivic undertakes no obligation to update forward-looking statements made by it to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events.

BRENTWOOD, Tenn., Oct. 02, 2025 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (“CoreCivic”) announced today that it will release its 2025 third quarter financial results after the market closes on Wednesday, November 5, 2025. A live broadcast of CoreCivic’s conference call will begin at 1:30 p.m. central time (2:30 p.m. eastern time) on Thursday, November 6, 2025.

To participate via telephone and join the call live, please register in advance. Upon registration at https://register-conf.media-server.com/register/BIa303aaae094f4f2fa02657400a84f3c6, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

Participants may access the audio-only webcast of the conference call from the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page. A replay of the webcast will be available for seven days.

About CoreCivic CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Estimated Annual Revenue From Contracts Signed In The Third Quarter of 2025 To Activate Idle Facilities Increases to $325 Million

BRENTWOOD, Tenn., Oct. 01, 2025 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (“CoreCivic”) announced today that it has been awarded a new contract under an Intergovernmental Services Agreement (“IGSA”) between the Oklahoma Department of Corrections (“OKDOC”) and U.S. Immigration and Customs Enforcement (“ICE”) to resume operations at the Company’s 2,160-bed Diamondback Correctional Facility, a facility that has been idle since 2010.

The new contract commences on September 30, 2025, for a term of five years, and may be extended through bilateral modification. The agreement provides for a fixed monthly payment plus an incremental per diem payment based on detainee populations. Total annual revenue once the facility is fully activated is expected to be approximately $100 million. We expect to begin receiving detainees in the first quarter of 2026, with the full ramp estimated to be complete in the second quarter of 2026.

Damon T. Hininger, CoreCivic’s Chief Executive Officer, commented, “We are pleased to expand our relationship with OKDOC while providing ICE with critical infrastructure capacity at our Diamondback Correctional Facility. While this facility has been idle since 2010, we have made investments to help ensure a seamless reactivation in the event of a new contract. Further, we expect to invest an additional $13 million over the next several quarters for renovations requested by ICE.”

Patrick D. Swindle, CoreCivic’s President and Chief Operating Officer, added, “Including the new contract awards at three of our other facilities previously announced during the third quarter of 2025, we have signed new contracts aggregating 6,353 beds across our four facilities, all of which were idle at the beginning of the year, with approximately $325 million of annual revenue once the facilities are fully activated. Reactivating the Diamondback facility is another step towards realizing the growth potential of the Company.”

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

This press release includes statements as to our beliefs and expectations of the outcome of future events that are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements may include such words as “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “may,” “will,” “should,” “can have,” “likely,” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events. Such forward-looking statements may be affected by risks and uncertainties in CoreCivic’s business and market conditions. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. Important factors that could cause actual results to differ are described in the filings made from time to time by CoreCivic with the Securities and Exchange Commission (“SEC”) and include the risk factors described in CoreCivic’s Annual Report on Form 10-K for the fiscal year ended December 31, 2024, filed with the SEC on February 21, 2025. Except as required by applicable law, CoreCivic undertakes no obligation to update forward-looking statements made by it to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events.

BRENTWOOD, Tenn., Sept. 29, 2025 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (“CoreCivic”) announced today that it has been awarded two new contracts with U.S. Immigration and Customs Enforcement (“ICE”) to utilize 3,593 beds at two facilities we own in core enforcement areas of the United States. Once fully activated, we expect to generate total annual revenue at the two facilities combined of nearly $200 million.

California City Immigration Processing Center – 2,560 beds

New contract with ICE to utilize our 2,560-bed California City Immigration Processing Center. We have been preparing to accept detainees at this facility since April 1, 2025, when we entered into a six-month Letter Contract with ICE to resume operations at the facility while we worked to negotiate and execute a longer-term contract.

We began receiving detainees at the facility on August 27, 2025 under terms of the Letter Contract. Transitioning from a Letter Contract to the definitive contract effective September 1, 2025 will result in variability in revenue and cash flow as we continue to successfully hire staff and receive additional detainees during the activation period. We currently expect the activation to be complete in the first quarter of 2026, achieving a normalized run-rate in the second quarter of 2026. Total annual revenue once the activation is complete is expected to be approximately $130 million. The new contract expires in August 2027.

Midwest Regional Reception Center – 1,033 beds

New contract with ICE at our 1,033-bed Midwest Regional Reception Center in Leavenworth, Kansas. We entered into a six-month Letter Contract with ICE on March 7, 2025 to begin activation efforts at the facility while we worked to negotiate and execute a longer-term contract. Although we have been successful in hiring staff and have prepared the facility to accept detainees during this term, the intake process has been delayed by legal challenges.

The new contract commenced on September 7, 2025, and is for a term of 24 months. The agreement provides for a fixed monthly payment plus an incremental per diem payment based on detainee populations, both of which commence once the temporary injunction currently prohibiting the intake of detainees is no longer enforceable. Total annual revenue once the facility is fully activated is expected to be approximately $60 million. However, we cannot predict if or when the legal challenges will be successfully resolved.

Damon T. Hininger, CoreCivic’s Chief Executive Officer, commented, “We are pleased to announce the finalization of contracts for these two facilities, both of which were idle at the beginning of the year. The geographic locations of each of these facilities will enhance our ability to support our government partner in its effort to enforce immigration laws in areas of need across the United States. Looking forward, we anticipate additional contracting activity that will help satisfy ICE’s growing needs.”

Patrick D. Swindle, CoreCivic’s President and Chief Operating Officer, added, “Once fully activated, these two facilities are expected to generate combined annual revenue of nearly $200 million. While the intake process has been delayed at the Midwest Regional Reception Center, we will offer newly hired employees opportunities to be redeployed at our other activations until the legal challenges are resolved. Our team continues to work hard on activating our idle facilities, which helps lay the foundation for continued earnings growth into 2026 and beyond.”

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

This press release includes statements as to our beliefs and expectations of the outcome of future events that are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements may include such words as “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “may,” “will,” “should,” “can have,” “likely,” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events. Such forward-looking statements may be affected by risks and uncertainties in CoreCivic’s business and market conditions. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. Important factors that could cause actual results to differ are described in the filings made from time to time by CoreCivic with the Securities and Exchange Commission (“SEC”) and include the risk factors described in CoreCivic’s Annual Report on Form 10-K for the fiscal year ended December 31, 2024, filed with the SEC on February 21, 2025. Except as required by applicable law, CoreCivic undertakes no obligation to update forward-looking statements made by it to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

West Tennessee. As anticipated, CoreCivic announced another new contract with U.S. Immigration and Customs Enforcement (ICE). Through an intergovernmental services agreement (IGSA) between the City of Mason, Tennessee, and ICE, CoreCivic will resume operations at the Company’s 600-bed West Tennessee Detention Facility, a facility that has been idle since September 2021.

Details. The IGSA expires in August 2030 and may be further extended through bilateral modification. The agreement provides for a fixed monthly payment plus an incremental per diem payment based on detainee populations. Total annual revenue once the facility is fully activated is expected to be approximately $30 million to $35 million, with margins consistent with the CoreCivic Safety segment.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Availability. Increased use of CoreCivic’s remaining beds will help drive operating results going forward. If all of the idle 13,419 beds were activated, this would imply around $500 million in annual revenue, and around $200 million to $225 million in incremental EBITDA.

Activations. During the quarter, CoreCivic made substantial progress in reactivating three previously idled facilities, and the Company’s activation teams are preparing for additional contracting activity. Management noted that CoreCivic is in advanced negotiations to activate a fourth idle facility and has just begun negotiations for a fifth facility.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Increasing Demand. Increasing demand for the solutions provided, particularly from ICE, contributed to a strong second quarter, as nationwide detention populations under ICE custody reached an all-time high. ICE revenue rose 17.2% y-o-y, but we also note revenue from state partners increased 5.2% y-o-y and U.S. Marshals revenue increased 2.7% y-o-y.

2Q25 Results. Revenue was $538.2 million in 2Q25, up from $490.1 million last year. We were at $500.6 million. Safety and Community average occupancy increased to 76.8% from 74.3%, even with an overhang from the recently activated California City facility. Adjusted EBITDA was $103.3 million, up 23.2% y-o-y. NFFO per share was $0.59, up 40.5%. CoreCivic reported adjusted EPS of $0.36, up 80%.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Raises 2025 Full Year Guidance Increasing Demand Drives Strong Financial Performance

BRENTWOOD, Tenn., Aug. 06, 2025 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (CoreCivic or the Company) announced today its second quarter 2025 financial results.

Financial Highlights – Second Quarter 2025

Total revenue of $538.2 million, up 9.8% from the prior year quarter

Net income of $38.5 million, up 103.4% from the prior year quarter

Diluted earnings per share of $0.35, up 105.9% from the prior year quarter

Adjusted diluted earnings per share of $0.36, up 80.0% from the prior year quarter

Normalized FFO per diluted share of $0.59, up 40.5% from the prior year quarter

Adjusted EBITDA of $103.3 million, up 23.2% from the prior year quarter

Repurchased 2.0 million shares of our common stock at an aggregate cost of $43.2 million

Damon T. Hininger, CoreCivic’s Chief Executive Officer, commented, “Increasing demand for the solutions we provide, particularly from U.S. Immigration and Customs Enforcement (ICE), contributed to a strong second quarter, as nationwide detention populations under ICE custody reached an all-time high. We expect the substantial increase in government funding approved during July to result in further increases in the utilization of our existing capacity. Based on the strength of our second quarter financial results and outlook for our business during the second half of 2025, we are increasing our 2025 financial guidance.”

Hininger continued, “We continued to deploy capital in ways that we believe add shareholder value. During the second quarter, we repurchased 2.0 million shares of our common stock at an aggregate cost of $43.2 million. At the beginning of the third quarter, we completed the acquisition of the Farmville Detention Center in Virginia for $67 million at an attractive return.”

Patrick Swindle, CoreCivic’s President and Chief Operating Officer, remarked, “We made substantial progress in re-activating three previously idled facilities during the second quarter, and our activation teams are preparing for additional contracting activity. ICE has been deliberate in increasing detention utilization under existing contracts while also executing new contracts at previously idled facilities. We expect to begin receiving detainees at our California City Immigration Processing Center in the near term, we are in advanced negotiations to activate a fourth idle facility, and we continue discussions to activate additional idle facilities. During the third quarter we also began integrating operations at the Farmville Detention Center, where we provide transportation, care, and civil detention services to adult male noncitizens under ICE custody. Along with the acquisition of the facility, we welcomed approximately 200 employees to our team.”

Second Quarter 2025 Financial Results Compared With Second Quarter 2024

Net income in the second quarter of 2025 was $38.5 million, or $0.35 per diluted share, compared with net income in the second quarter of 2024 of $19.0 million, or $0.17 per diluted share (Diluted EPS). Adjusted for special items, Adjusted Net Income for the second quarter of 2025 was $39.7 million, or $0.36 per diluted share (Adjusted Diluted EPS), compared with Adjusted Net Income of $21.8 million, or $0.20 per diluted share, in the prior year quarter. Special items in the second quarter of 2025 included charges of $1.5 million associated with the acquisition of the Farmville Detention Center, included in general and administrative expenses in our consolidated statement of operations. Special items in the prior year quarter included $4.1 million of expenses associated with debt repayments and refinancing transactions. Special items are presented in detail in the calculation of Adjusted Net Income and Adjusted Diluted EPS in the Supplemental Financial Information following the financial statements presented herein.

The increase in Diluted EPS and Adjusted Diluted EPS compared with the prior year quarter resulted from higher federal and state populations as well as higher average per diem rates across much of our portfolio, combined with the recognition of employee retention credits (ERCs) available under the Coronavirus Aid, Relief and Economic Security Act amounting to $0.08 per share. These increases were net of the financial impact of the termination of our contract with ICE at the Dilley Immigration Processing Center effective August 9, 2024. However, we began re-activating the Dilley facility during March 2025. The agreement governing the reactivation provides for a fixed monthly payment from ICE in accordance with a graduated schedule to correlate with the activation of each neighborhood within the facility. The Dilley facility accounted for a $0.07 per share reduction compared with the second quarter of 2024.

We cared for an average daily residential population of 54,026 during the second quarter of 2025 in our Safety and Community segments compared with 51,541 during the second quarter of 2024. Average occupancy during the second quarter of 2025 was 76.8% in our Safety and Community segments, compared with 74.3% during the second quarter of 2024, even after reflecting the activation and transfer of our 2,560-bed California City Immigration Processing Center from the Properties segment to the Safety segment effective April 1, 2025, when we entered into a Letter Contract with ICE to reactive operations at the facility. The California City facility was previously in our Properties segment because it was leased to the California Department of Corrections and Rehabilitation until the lease expired March 31, 2024. We expect to begin receiving detainees from ICE at the California City facility in the near term under terms of the Letter Contract.

During the second quarter of 2025, revenue from ICE, our largest government partner, was $176.9 million compared to $151.0 million during the second quarter of 2024, an increase of 17.2%, including the termination of our ICE contract at the Dilley facility effective August 9, 2024, partially offset by its reactivation effective April 1, 2025. The termination and reactivation accounted for a net reduction in revenue of $12.8 million. Revenue from state customers increased 5.2% compared with the prior year quarter, with increases across many of our government customers. New contracts with the state of Montana executed in August 2024 and January 2025 accounted for the largest increase in revenue from state customers. Further, revenue from the U.S. Marshals Service, our second largest government customer, increased 2.7% from the prior year quarter.

Earnings before interest, taxes, depreciation and amortization (EBITDA) for the second quarter of 2025 was $101.8 million, compared with $79.8 million in the second quarter of 2024. Adjusted EBITDA, which excludes special items, was $103.3 million in the second quarter of 2025, compared with $83.9 million in the second quarter of 2024. The increases in EBITDA and Adjusted EBITDA from the prior year quarter were primarily attributable to higher residential populations in our portfolio, net of reductions for the contract termination at the Dilley facility and the expiration of the lease with the CDCR at the California City facility. The increases in EBITDA and Adjusted EBITDA also included $8.3 million of ERCs recognized during the second quarter of 2025, and $3.2 million of interest collected on the ERCs.

Funds From Operations (FFO) for the second quarter of 2025 was $63.5 million, or $0.58 per share, compared with $43.8 million, or $0.39 per share, in the second quarter of 2024. Normalized FFO, which excludes special items, was $64.6 million, or $0.59 per diluted share, in the second quarter of 2025, compared with $46.6 million, or $0.42 per share, in the second quarter of 2024. Normalized FFO was impacted by the same factors that affected Adjusted EBITDA, further improved by a reduction in gross interest expense that is not reflected in Adjusted EBITDA. The reduction in gross interest expense resulted from a decrease in our average outstanding debt balance combined with a decrease in the interest rates associated with our variable rate debt. Per share amounts were also favorably impacted by a 2.1% reduction in weighted average shares outstanding compared with the prior year quarter resulting from repurchases we made under our share repurchase program.

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share amounts, are measures calculated and presented on the basis of methodologies other than in accordance with generally accepted accounting principles (GAAP). Please refer to the Supplemental Financial Information and the note following the financial statements herein for further discussion and reconciliations of these measures to net income, the most directly comparable GAAP measure.

Capital Strategy

Share Repurchases. Our Board of Directors (BOD) previously approved a share repurchase program authorizing the Company to repurchase up to $350.0 million of our common stock. On May 15, 2025, the BOD authorized an increase to the share repurchase program by which we may purchase up to an additional $150.0 million in shares of our outstanding common stock, increasing the total aggregate authorization to up to $500.0 million. During the six months ended June 30, 2025, we repurchased 3.9 million shares of common stock under the share repurchase program at an aggregate cost of $81.0 million, or $20.52 per share, excluding costs associated with the share repurchase program, including 2.0 million shares at an aggregate cost of $43.2 million during the second quarter of 2025. Since the share repurchase program was authorized in May 2022, through June 30, 2025, we have repurchased a total of 18.5 million shares of our common stock at an aggregate cost of $262.1 million, or $14.19 per share, excluding fees, commissions and other costs related to the repurchases.

As of June 30, 2025, we had $237.9 million of repurchase authorization available under the share repurchase program. Additional repurchases of common stock will be made in accordance with applicable securities laws and may be made at management’s discretion within parameters set by the BOD from time to time in the open market, through privately negotiated transactions, or otherwise. The share repurchase program has no time limit and does not obligate us to purchase any particular amount of our common stock. The authorization for the share repurchase program may be terminated, suspended, increased or decreased by our BOD in its discretion at any time.

Acquisition of Farmville Detention Center. On July 1, 2025, we completed the acquisition of the Farmville Detention Center, a 736-bed facility constructed in 2010 and located in Farmville, Virginia. The transaction was consummated through the acquisition of 100% of the membership interests in entities that own and operate the facility, as well as the acquisition of certain assets utilized in the operation of the business. Farmville Detention Center provides transportation, care, and civil detention services to adult male noncitizens through an Intergovernmental Service Agreement (IGSA) between Prince Edward County, Virginia and ICE, which expires in March 2029. The total purchase price, amounting to $67.0 million, was funded with cash on hand and borrowing capacity under our revolving bank credit facility. We expect annual incremental revenue of approximately $40.0 million resulting from this acquisition.

Business Development Updates

Activation of the Dilley Immigration Processing Center. On March 5, 2025, we announced that we had agreed under an amendment to an IGSA to resume operations and care for up to 2,400 individuals at the 2,400-bed Dilley Immigration Processing Center in Dilley, Texas. We began receiving residents at this facility during the second quarter of 2025. By the end of the second quarter of 2025, three of the five neighborhoods at the facility were operational. We currently expect all five neighborhoods at the facility to be fully operational on schedule by the end of the third quarter of 2025, when we expect to generate the full fixed monthly payment for the facility.

Intake Process Expected to Begin at the California City Immigration Processing Center. Effective April 1, 2025, we entered into a Letter Contract with ICE to begin activation efforts at our 2,560-bed California City Immigration Processing Center. The Letter Contract authorizes initial funding up to $10.0 million with maximum funding up to $31.2 million for a six-month period to help cover our start-up expenses while we work to negotiate and execute a long-term contract. We expect to begin receiving detainees from ICE at the California City facility in the near term under terms of the Letter Contract.

Midwest Regional Reception Center. Effective March 7, 2025, we entered into a Letter Contract with ICE to begin activation efforts at our 1,033-bed Midwest Regional Reception Center. The Letter Contract authorizes initial funding up to $5.0 million with maximum funding up to $22.6 million for a six-month period to help cover our start-up expenses while we work to negotiate and execute a long-term contract. The intake process has been delayed by a lawsuit filed by the City of Leavenworth alleging that a Special Use Permit (SUP) is required to operate the facility. A state court granted a temporary restraining order barring us from housing detainees at the facility without first obtaining an SUP. We have filed an appeal in the state court on the basis that the SUP is not applicable under existing statute. We believe ICE remains intent on using this facility.

2025 Financial Guidance

Based on current business conditions, we are providing the following updated financial guidance for the full year 2025:

Revised Guidance Full Year 2025

Prior Guidance Full Year 2025

Net income

$116.4 million to $124.4 million

$91.3 million to $101.3 million

Adjusted Net Income

$115.5 million to $123.5 million

$91.3 million to $101.3 million

Diluted EPS

$1.08 to $1.15

$0.83 to $0.92

Adjusted Diluted EPS

$1.07 to $1.14

$0.83 to $0.92

FFO per diluted share

$1.98 to $2.06

$1.72 to $1.82

Normalized FFO per diluted share

$1.99 to $2.07

$1.72 to $1.82

EBITDA

$366.3 million to $372.3 million

$331.0 million to $339.0 million

Adjusted EBITDA

$365.0 million to $371.0 million

$331.0 million to $339.0 million

Compared with our prior 2025 annual guidance provided on May 7, 2025, our revised 2025 guidance reflects the favorable results for the second quarter, updated occupancy projections consistent with current trends, the acquisition of the Farmville Detention Center, as well as our assumptions for the reactivation of the California City Immigration Processing Center based on the expectation of receiving detainee populations during the third quarter of 2025.

Consistent with our past practice, our guidance does not include the impact of any new contract awards not previously announced. However, we may continue to execute new contracts during the balance of 2025, and may revise guidance throughout the year if and when new contracts are signed. Although we can provide no assurance, based on significant funding levels for detention capacity that will be available under the One Big Beautiful Bill Act, modified immigration policies of the current administration, as well as newly enacted legislation pertaining to illegal immigrants requiring the utilization of detention for certain criminal violations, we expect new contracts to require the activation of more of our idle facilities. The activation of an idle facility generally requires four to six months to hire, train, and prepare the facility to accept residential populations, which, depending on contract structure, could result in additional expenses before we are able to realize additional revenue. To the extent any new contract requires the activation of an idle facility before we begin to recognize revenue, our guidance could be negatively impacted by start-up expenses until the revenue we generate offsets these expenses. Due to activation timing, full year benefits from idle facility activations are likely to be more impactful to 2026 results.

During 2025, we expect to invest $29.0 million to $31.0 million in maintenance capital expenditures on real estate assets, $31.0 million to $34.0 million for maintenance capital expenditures on other assets and information technology, and $9.0 million to $10.0 million for other capital investments. Although our guidance does not include any new contract awards beyond those previously announced, we also expect to incur approximately $70.0 million to $75.0 million of capital expenditures associated with previously idled facilities we are activating and for additional potential facility activations, in order to prepare these facilities to quickly accept residential populations if opportunities arise, as well as to provide transportation services.

Supplemental Financial Information and Investor Presentations

We have made available on our website supplemental financial information and other data for the second quarter of 2025. Interested parties may access this information at http://ir.corecivic.com/ under “Financial Information” of the Investors section. We do not undertake any obligation and disclaim any duties to update any information disclosed in this report.

Management may meet with investors from time to time during the third quarter of 2025. Written materials used in the investor presentations will also be available on our website beginning on or about August 29, 2025. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Events & Presentations” of the Investors section.

Conference Call, Webcast and Replay Information

We will host a webcast conference call at 10:00 a.m. central time (11:00 a.m. eastern time) on Thursday, August 7, 2025, which will be accessible through the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page. To participate via telephone and join the call live, please register in advance here https://register-conf.media-server.com/register/BI826b7187965c436ca353a3af4a956fed. Upon registration, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements