Research News and Market Data on CXW

May 3, 2023

Updates 2023 Full Year Guidance

BRENTWOOD, Tenn., May 03, 2023 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (the Company) announced today its financial results for the first quarter of 2023.

Damon T. Hininger, CoreCivic’s President and Chief Executive Officer, said, “We are pleased to report first quarter results that were in line with our expectations, while we continue to operate through a challenging labor market and execute on our long-term capital allocation strategy. During the first quarter, we generated $73.7 million of EBITDA that, along with existing liquidity, enabled us to repay in full the $153.8 million outstanding balance of our 4.625% Senior Notes that were scheduled to mature on May 1, 2023. We also continued to execute on our share repurchase program during the quarter by repurchasing 2.5 million shares, representing an additional 2% of our outstanding shares, at a total cost of $24.9 million.

Hininger continued, “We’re also proud to have recently released our fifth Environmental, Social and Governance (ESG) Report. The ESG report details the ways we delivered reentry and vocational programming designed to prepare those in our care for long-lasting success upon reentry to their communities during 2022, a mission that our organization has been carrying out for more than 40 years. I hope you have an opportunity to review our latest ESG report to learn more about CoreCivic and the important services we provide. We are proud of our history and our accomplishments that truly help individuals in our care change their lives for the better primarily through the strength and volume of our evidence-based programs.”

Financial Highlights – First Quarter 2023

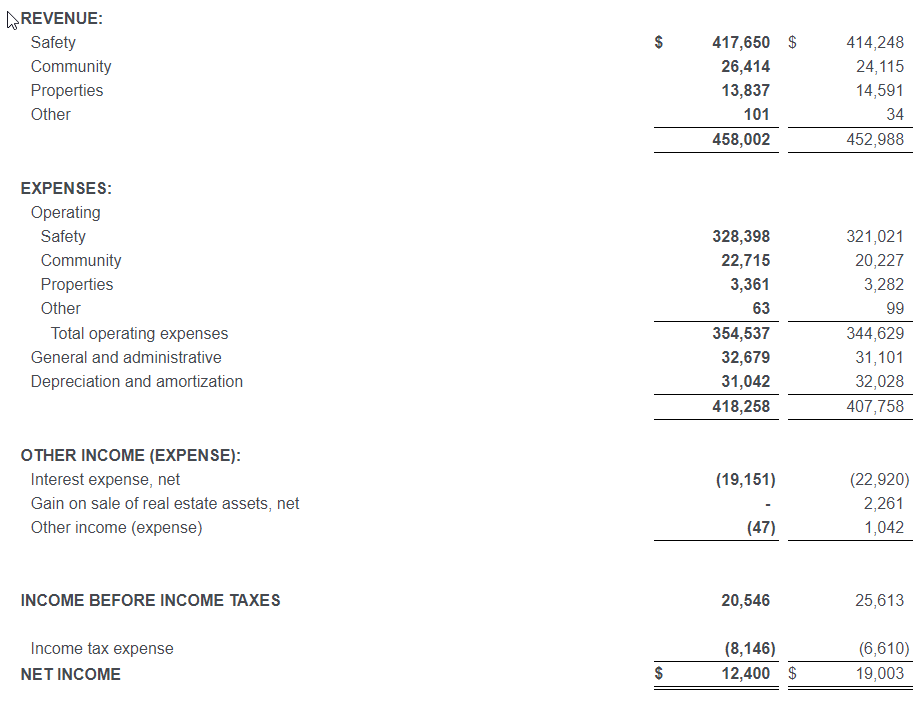

- Total revenue of $458.0 million

- CoreCivic Safety revenue of $417.7 million

- CoreCivic Community revenue of $26.4 million

- CoreCivic Properties revenue of $13.8 million

- Net Income of $12.4 million

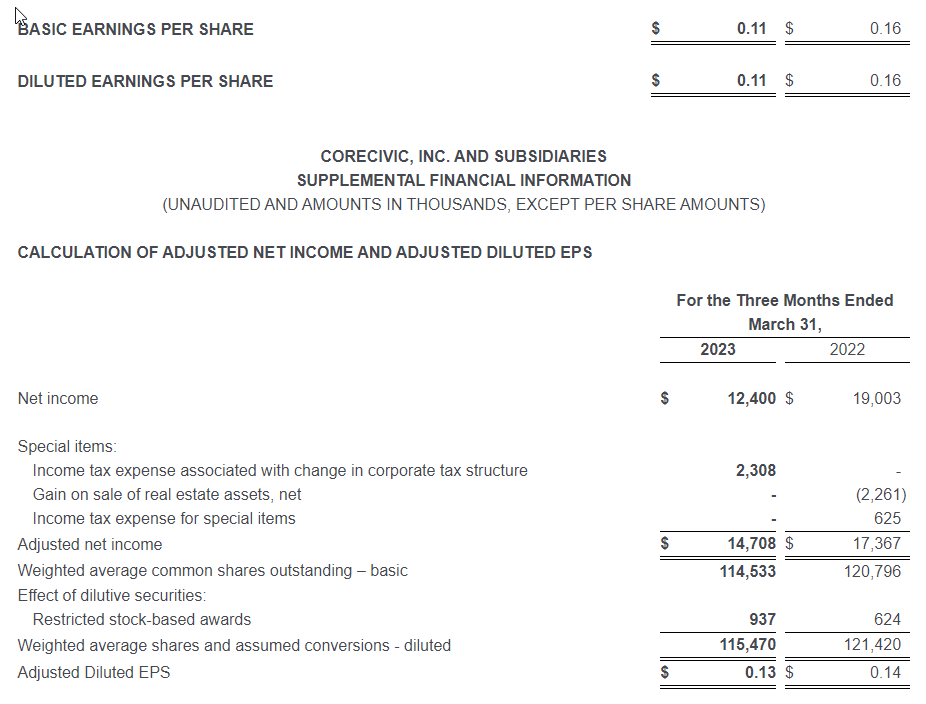

- Diluted earnings per share of $0.11

- Adjusted Diluted EPS of $0.13

- Normalized Funds From Operations per diluted share of $0.34

- EBITDA of $73.7 million

First Quarter 2023 Financial Results Compared With First Quarter 2022

Net income in the first quarter of 2023 totaled $12.4 million, or $0.11 per diluted share, compared with net income in the first quarter of 2022 of $19.0 million, or $0.16 per diluted share. Adjusted for special items, adjusted net income in the first quarter of 2023 was $14.7 million, or $0.13 per diluted share (Adjusted Diluted EPS), compared with adjusted net income in the first quarter of 2022 of $17.4 million, or $0.14 per diluted share. Special items for each period are presented in detail in the calculation of Adjusted Diluted EPS in the Supplemental Financial Information following the financial statements presented herein.

The $0.01 per share decline in Adjusted Diluted EPS occurred despite transitioning to the previously announced contract with the state of Arizona at our 3,060-bed La Palma Correctional Center in Arizona, the expiration of our contract with the Federal Bureau of Prisons (BOP) at the McRae Correctional Facility on November 30, 2022, and ongoing labor market pressures, including above average wage inflation. We substantially completed the transition of inmate populations at the La Palma facility by the end of 2022, but we continued to incur elevated operating expenses during the first quarter of 2023 due to ongoing efforts to attract and retain local staff at the facility. Despite the expiration of the contract with the BOP at the McRae facility, a facility we sold to the state of Georgia in 2022, our renewal rate on owned and controlled facilities remains high at 94% over the previous five years. We believe our renewal rate on existing contracts remains high due to a variety of reasons including the aged and constrained supply of available beds within the U.S. correctional system, our ownership of the majority of the beds we operate, the value our government partners place in the wide range of recidivism-reducing programs we offer to those in our care, and the cost effectiveness of the services we provide.

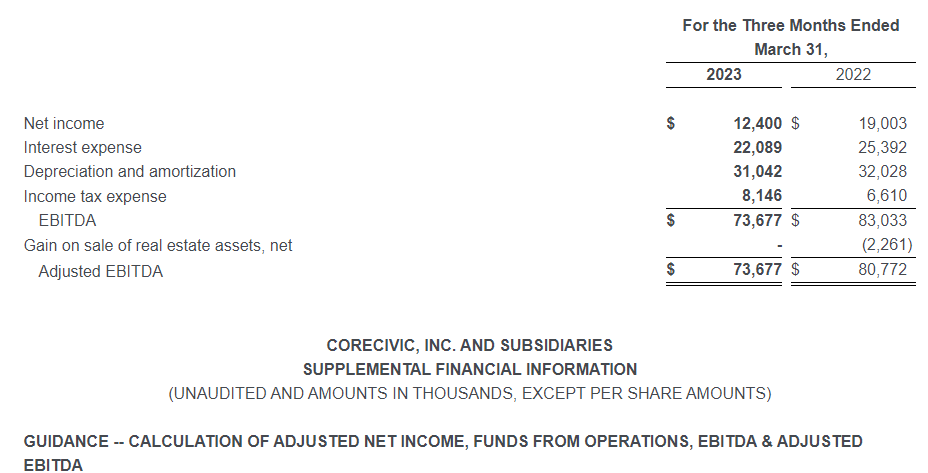

Earnings before interest, taxes, depreciation and amortization (EBITDA) was $73.7 million in the first quarter of 2023, compared with $83.0 million in the first quarter of 2022. Adjusted EBITDA was $73.7 million in the first quarter of 2023, compared with $80.8 million in the first quarter of 2022. Adjusted EBITDA of $80.8 million in the prior year quarter excludes a net gain on sale of real estate assets. Adjusted EBITDA decreased from the prior year quarter primarily due to the previously mentioned transition of offender populations at our La Palma Correctional Center, which resulted in a reduction in EBITDA of $7.4 million, and the expiration of our BOP contract at the McRae Correctional Facility in November 2022, which resulted in a reduction in EBITDA of $2.3 million from the first quarter of 2022 to the first quarter of 2023. Due to an improving labor market, we achieved higher staffing levels in the first quarter of 2023 than in the prior year quarter; however, we incurred higher wage rates than in the prior year quarter in order to attract and retain facility staff in the challenging labor market. We also incurred higher travel expenses in order to augment staffing levels at multiple facilities. We believe these investments in staffing are positioning us to manage the increased number of residents we anticipate at our facilities once the remaining occupancy restrictions attributable to COVID-19 are removed, most notably Title 42, a policy that denies entry at the United States border to asylum-seekers and anyone crossing the border without proper documentation or authority in an effort to contain the spread of COVID-19. Title 42 is currently scheduled to end in May 2023. Despite the difficult labor market, we have been able to reduce certain labor-related expenses, such as registry nursing and temporary incentives, which moderated during the first quarter of 2023 compared with the first quarter of 2022.

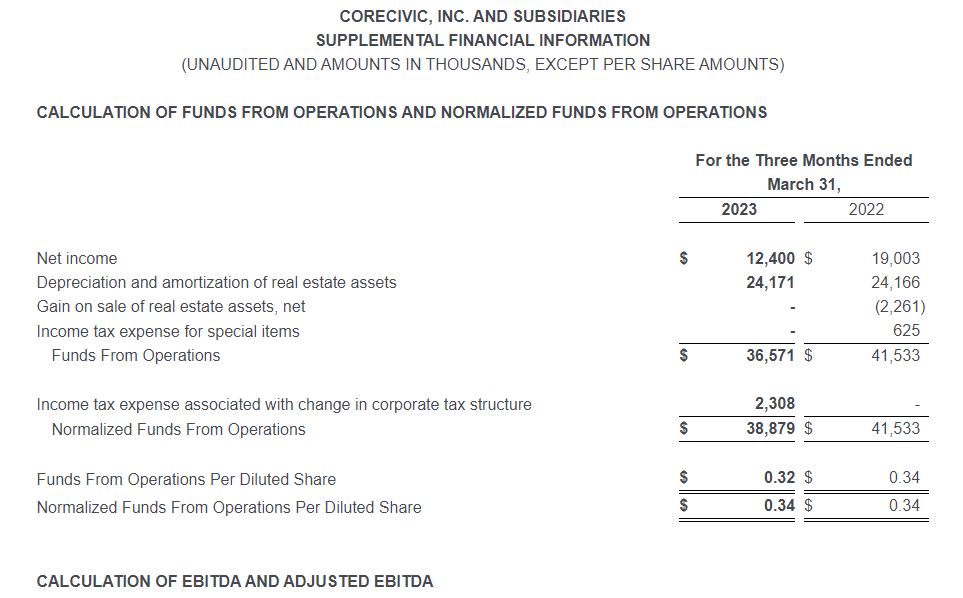

Funds From Operations (FFO) was $36.6 million, or $0.32 per diluted share, in the first quarter of 2023, compared to $41.5 million, or $0.34 per diluted share, in the first quarter of 2022. Normalized FFO, which excludes special items, was $38.9 million, or $0.34 per diluted share, in the first quarter of 2023, compared with $41.5 million, or $0.34 per diluted share, in the first quarter of 2022. Normalized FFO was impacted by the same factors that affected Adjusted EBITDA.

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share amounts, are measures calculated and presented on the basis of methodologies other than in accordance with generally accepted accounting principles (GAAP). Please refer to the Supplemental Financial Information and the note following the financial statements herein for further discussion and reconciliations of these measures to net income, the most directly comparable GAAP measure.

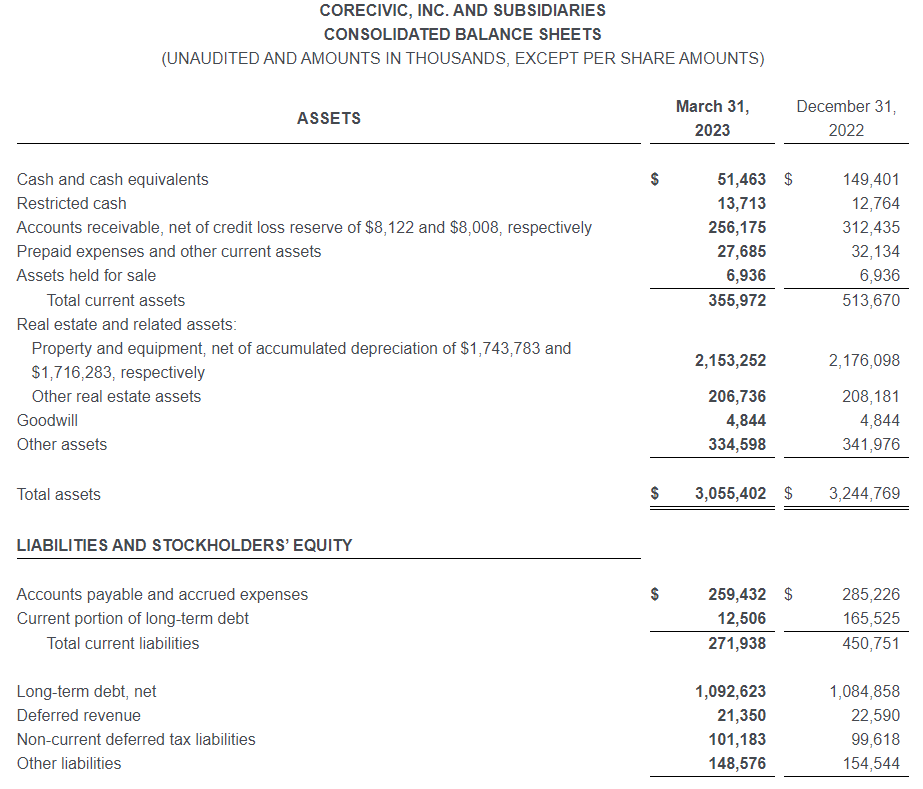

Asset Dispositions and Assets Held for Sale

During the third quarter of 2022, we began marketing for sale our Roth Hall Residential Reentry Center and the Walker Hall Residential Reentry Center, both of which are located in Philadelphia, Pennsylvania and reported in our CoreCivic Properties segment. The properties were classified as held for sale as of March 31, 2023 and December 31, 2022. A purchase and sale agreement for these two Philadelphia properties was executed in March 2023 and the properties were sold on May 2, 2023, generating net sales proceeds of $5.8 million, which approximated the carrying value of the properties. We are also marketing for sale a residential reentry center in Denver, Colorado with a carrying value of $1.2 million and reported in our CoreCivic Community segment, which was also classified as held for sale as of March 31, 2023.

Share Repurchases

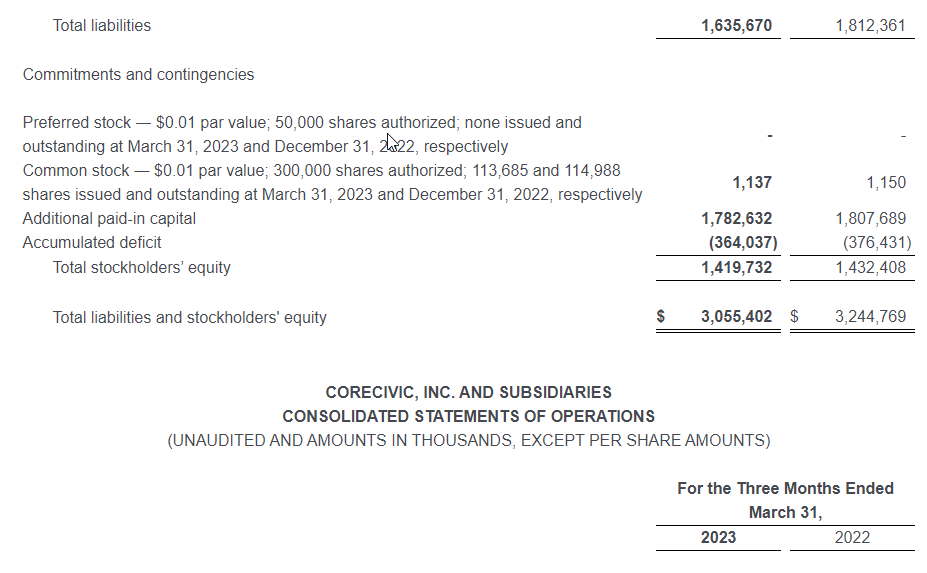

On May 12, 2022, our Board of Directors approved a share repurchase program authorizing the Company to repurchase up to $150.0 million of our common stock. On August 2, 2022, our Board of Directors authorized an increase in our share repurchase program of up to an additional $75.0 million in shares of our common stock, or a total of up to $225.0 million. During the first quarter of 2023, we repurchased 2.5 million shares of our common stock at an aggregate purchase price of $24.9 million, excluding fees, commissions and other costs related to the repurchases. Since the share repurchase program was authorized, through March 31, 2023, we have repurchased a total of 9.1 million shares at an aggregate price of $99.4 million under this share repurchase program.

As of March 31, 2023, we had $125.6 million remaining under the share repurchase program authorized by the Board of Directors. Additional repurchases of common stock will be made in accordance with applicable securities laws and may be made at management’s discretion within parameters set by the Board of Directors from time to time in the open market, through privately negotiated transactions, or otherwise. The share repurchase program has no time limit and does not obligate us to purchase any particular amount of our common stock. The authorization for the share repurchase program may be terminated, suspended, increased or decreased by our Board of Directors in its discretion at any time.

Debt Repayments

On December 22, 2022, we delivered an irrevocable notice to the trustee of the holders of the 4.625% Senior Notes that we elected to redeem in full the 4.625% Senior Notes that remained outstanding on February 1, 2023. The 4.625% Senior Notes were redeemed on February 1, 2023 at a redemption price equal to 100% of the principal amount of the outstanding 4.625% Senior Notes, which amounted to $153.8 million, plus accrued and unpaid interest to, but not including, the redemption date. We used a combination of cash on hand and available capacity under our Revolving Credit Facility to fund the redemption. During the first quarter of 2023, we reduced our total debt balance by $146.2 million, or by $48.2 million net of the change in cash. Following the redemption of the 4.625% Senior Notes, we have no debt maturities until 2026.

2023 Financial Guidance

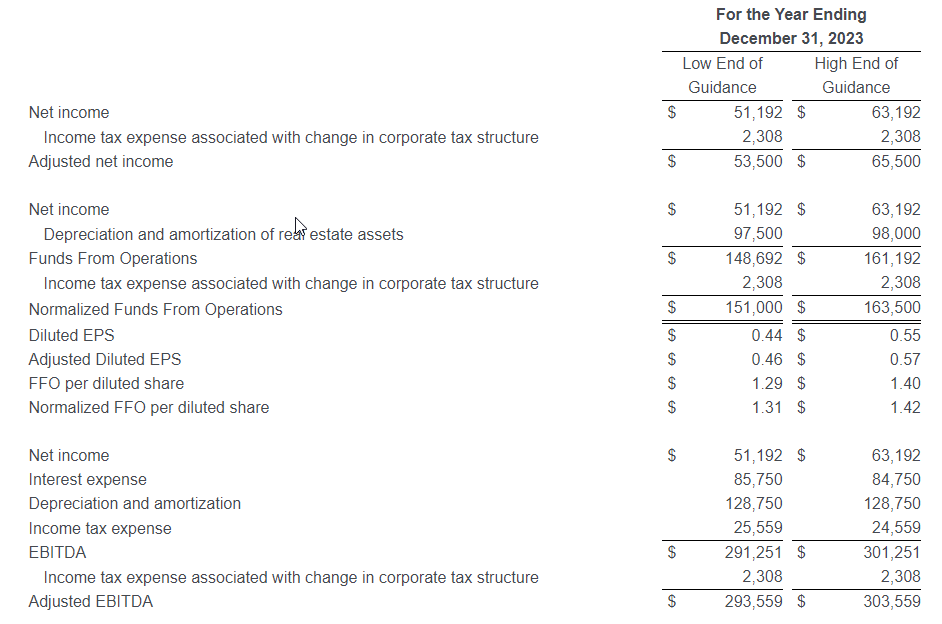

Based on current business conditions, we are providing the following update to our financial guidance for the full year 2023:

| Guidance Full Year 2023 | Prior Guidance Full Year 2023 | |

| Net income | $51.2 million to $63.2 million | $58.0 million to $75.0 million |

| Adjusted net income | $53.5 million to $65.5 million | $58.0 million to $75.0 million |

| Diluted EPS | $0.44 to $0.55 | $0.50 to $0.65 |

| Adjusted Diluted EPS | $0.46 to $0.57 | $0.50 to $0.65 |

| FFO per diluted share | $1.29 to $1.40 | $1.35 to $1.50 |

| Normalized FFO per diluted share | $1.31 to $1.42 | $1.35 to $1.50 |

| EBITDA | $291.3 million to $301.3 million | $298.5 million to $313.5 million |

| Adjusted EBITDA | $293.6 million to $303.6 million | $298.5 million to $313.5 million |

Financial guidance has been updated to reflect a favorable $0.01 per share variance to our internal forecast for the first quarter of 2023, offset by $0.04 per share to reflect the non-renewal of our lease with the state of Oklahoma at our North Fork Correctional Facility expiring June 30, 2023, which we previously disclosed on April 24, 2023. In addition, we continue to negotiate in good faith with the state of Oklahoma for the renewal of our contract to manage our Davis Correctional Facility, which also expires June 30, 2023, and operated at a loss during 2022 and the first quarter of 2023. However, we have not yet been able to reach acceptable terms. Our updated guidance was further reduced by $0.03 per share to reflect the potential transition of inmate populations out of the Davis Correctional Facility during the second quarter of 2023 and idle operations during the second half of the year, which we did not contemplate in our previous forecast. If we are able to reach acceptable terms on a new agreement, the $0.03 per share reduction will be avoided, as we would exceed our forecast by approximately $0.02 per share during the second quarter by avoiding the transition, and we would further exceed our guidance during the second half of 2023, the magnitude of which would depend on the terms of a new agreement.

During 2023, we expect to invest $64.0 million to $67.0 million in capital expenditures, consisting of $36.0 million to $37.0 million in maintenance capital expenditures on real estate assets, $25.0 million to $26.0 million for maintenance capital expenditures on other assets and information technology, and $3.0 million to $4.0 million for other capital investments. These capital expenditure amounts are unchanged from our previous guidance.

Supplemental Financial Information and Investor Presentations

We have made available on our website supplemental financial information and other data for the first quarter of 2023. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Financial Information” of the Investors section. We do not undertake any obligation and disclaim any duties to update any of the information disclosed in this report.

Management may meet with investors from time to time during the second quarter of 2023. Written materials used in the investor presentations will also be available on our website beginning on or about May 19, 2023. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Events & Presentations” of the Investors section.

Conference Call, Webcast and Replay Information

We will host a webcast conference call at 10:00 a.m. central time (11:00 a.m. eastern time) on Thursday, May 4, 2023, which will be accessible through the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page.

To participate via telephone and join the call live, please register in advance here https://register.vevent.com/register/BI6394fffe952b47d497a2735e53d08f32. Upon registration, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest prison operators in the United States. We have been a flexible and dependable partner for government for 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements

This press release contains statements as to our beliefs and expectations of the outcome of future events that are “forward-looking” statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. These include, but are not limited to, the risks and uncertainties associated with: (i) changes in government policy, legislation and regulations that affect utilization of the private sector for corrections, detention, and residential reentry services, in general, or our business, in particular, including, but not limited to, the continued utilization of our correctional and detention facilities by the federal government, including as a consequence of the United States Department of Justice, or DOJ, not renewing contracts as a result of President Biden’s Executive Order on Reforming Our Incarceration System to Eliminate the Use of Privately Operated Criminal Detention Facilities, or the Private Prison EO, impacting utilization primarily by the BOP and the United States Marshals Service, and the impact of any changes to immigration reform and sentencing laws (we do not, under longstanding policy, lobby for or against policies or legislation that would determine the basis for, or duration of, an individual’s incarceration or detention); (ii) our ability to obtain and maintain correctional, detention, and residential reentry facility management contracts because of reasons including, but not limited to, sufficient governmental appropriations, contract compliance, negative publicity and effects of inmate disturbances; (iii) changes in the privatization of the corrections and detention industry, the acceptance of our services, the timing of the opening of new facilities and the commencement of new management contracts (including the extent and pace at which new contracts are utilized), as well as our ability to utilize available beds; (iv) general economic and market conditions, including, but not limited to, the impact governmental budgets can have on our contract renewals and renegotiations, per diem rates, and occupancy; (v) fluctuations in our operating results because of, among other things, changes in occupancy levels; competition; contract renegotiations or terminations; inflation and other increases in costs of operations, including a continuing rise in labor costs; fluctuations in interest rates and risks of operations; (vi) the duration of the federal government’s denial of entry at the United States southern border to asylum-seekers and anyone crossing the southern border without proper documentation or authority in an effort to contain the spread of COVID-19, a policy known as Title 42 (Title 42 is expected to end May 11, 2023, when President Biden has decided to lift the public health emergency for COVID-19, although its termination may be subject to ongoing litigation, the outcome of which is unclear. Most recently, on December 27, 2022, the Supreme Court granted a stay on the cessation of Title 42, while it considers an appeal by a group of states to continue the expulsions.); (vii) our ability to successfully identify and consummate future development and acquisition opportunities and realize projected returns resulting therefrom; (viii) our ability to have met and maintained qualification for taxation as a real estate investment trust, or REIT, for the years we elected REIT status; and (ix) the availability of debt and equity financing on terms that are favorable to us, or at all. Other factors that could cause operating and financial results to differ are described in the filings we make from time to time with the Securities and Exchange Commission.

We take no responsibility for updating the information contained in this press release following the date hereof to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events or for any changes or modifications made to this press release or the information contained herein by any third-parties, including, but not limited to, any wire or internet services.

NOTE TO SUPPLEMENTAL FINANCIAL INFORMATION

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share metrics are non-GAAP financial measures. The Company believes that these measures are important operating measures that supplement discussion and analysis of the Company’s results of operations and are used to review and assess operating performance of the Company and its properties and their management teams. The Company believes that it is useful to provide investors, lenders and security analysts disclosures of its results of operations on the same basis that is used by management.

FFO, in particular, is a widely accepted non-GAAP supplemental measure of performance of real estate companies, grounded in the standards for FFO established by the National Association of Real Estate Investment Trusts (NAREIT). NAREIT defines FFO as net income computed in accordance with GAAP, excluding gains (or losses) from sales of property and extraordinary items, plus depreciation and amortization of real estate and impairment of depreciable real estate and after adjustments for unconsolidated partnerships and joint ventures calculated to reflect funds from operations on the same basis. As a company with extensive real estate holdings, we believe FFO and FFO per share are important supplemental measures of our operating performance and believe they are frequently used by securities analysts, investors and other interested parties in the evaluation of REITs and other real estate operating companies, many of which present FFO and FFO per share when reporting results. EBITDA, Adjusted EBITDA, and FFO are useful as supplemental measures of performance of the Company’s properties because such measures do not take into account depreciation and amortization, or with respect to EBITDA, the impact of the Company’s tax provision and financing strategies. Because the historical cost accounting convention used for real estate assets requires depreciation (except on land), this accounting presentation assumes that the value of real estate assets diminishes at a level rate over time. Because of the unique structure, design and use of the Company’s properties, management believes that assessing performance of the Company’s properties without the impact of depreciation or amortization is useful. The Company may make adjustments to FFO from time to time for certain other income and expenses that it considers non-recurring, infrequent or unusual, even though such items may require cash settlement, because such items do not reflect a necessary or ordinary component of the ongoing operations of the Company. Normalized FFO excludes the effects of such items. The Company calculates Adjusted Net Income by adding to GAAP Net Income expenses associated with the Company’s debt repayments and refinancing transactions, and certain impairments and other charges that the Company believes are unusual or non-recurring to provide an alternative measure of comparing operating performance for the periods presented.

Other companies may calculate Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO differently than the Company does, or adjust for other items, and therefore comparability may be limited. Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO and, where appropriate, their corresponding per share measures are not measures of performance under GAAP, and should not be considered as an alternative to cash flows from operating activities, a measure of liquidity or an alternative to net income as indicators of the Company’s operating performance or any other measure of performance derived in accordance with GAAP. This data should be read in conjunction with the Company’s consolidated financial statements and related notes included in its filings with the Securities and Exchange Commission.

| Contact: | Investors: Cameron Hopewell – Managing Director, Investor Relations – (615) 263-3024 |

| Financial Media: David Gutierrez, Dresner Corporate Services – (312) 780-7204 |