Key Points: – Tesla’s stock price jumps significantly following the U.S. Department of Transportation’s new self-driving car regulations. – The potential entry into the Indian market adds another positive catalyst for the electric vehicle and technology giant. – CEO Elon Musk’s reduced involvement in the Trump administration is seen as a positive for the brand.

Tesla (TSLA) has seen a dramatic resurgence this week, with its stock price soaring on a wave of positive news, positioning it for a near-20% weekly gain. This rally comes after a challenging period for the electric vehicle (EV) and technology leader, which saw its stock plummet 50% from its December highs to its yearly lows.

The latest spark igniting investor enthusiasm came from the U.S. Department of Transportation (DoT), which unveiled a new framework for self-driving car regulations late Thursday. This framework includes measures to “streamline” reporting requirements for vehicles equipped with automated or driver-assist systems. Transportation Secretary Sean Duffy emphasized the administration’s focus on outpacing China in innovation, stating that the new rules aim to cut red tape and establish a unified national standard that encourages both innovation and safety.

Adding to the positive momentum, the National Highway Traffic Safety Administration (NHTSA) announced an expansion of an existing program. This program, which previously exempted certain foreign-made autonomous vehicles from some review processes to accelerate testing, will now include U.S.-made vehicles. This development is seen as a significant tailwind for Tesla, which has been aggressively pursuing advancements in autonomous driving technology.

During the company’s recent earnings call, CEO Elon Musk reiterated Tesla’s expectation to begin “selling fully autonomous rides in June in Austin.” He further emphasized the company’s long-term vision, stating that “the future of the company is fundamentally based on large-scale autonomous cars and large-scale … numbers of autonomous humanoid robots.” Musk believes that Tesla’s ability to produce truly useful autonomous vehicles and robots at scale and low cost positions the company for “staggering” future value.

Beyond self-driving advancements, Tesla’s stock also received a boost from a Bloomberg report suggesting a potential imminent entry into the Indian market. The report indicated that some customers who had previously placed reservation deposits were receiving refunds, often seen as a precursor to a formal market entry. Tesla acknowledged on its earnings call that it had been “very careful trying to figure out when is the right time” to enter India, given the current tariff structure that could significantly inflate the price of its vehicles. This renewed speculation of entering a potentially massive market like India has clearly excited investors.

Earlier in the week, Tesla’s stock experienced its most significant jump following Elon Musk’s announcement during the earnings call that he would be “significantly” reducing his time spent in the Trump administration, specifically his role leading the Department of Government Efficiency (DOGE). Musk’s involvement in the administration had reportedly weighed on the brand’s perception, particularly in Europe, contributing to slower sales growth in the early part of the year.

Noted Tesla bull Dan Ives of Wedbush Securities described Musk’s step back from his government role as “an off ramp” from a period of “global brand damage” and “political firestorm.” Ives believes this move will allow Musk to refocus on Tesla’s core strengths, particularly autonomous driving and robotics, potentially ushering in a “brighter chapter” for the company.

While this week’s rally has been significant, pushing the stock to its highest level in a month, it’s important to note that Tesla’s stock remains down approximately 30% year-to-date. Ives also cautioned that the “brand damage” caused by Musk’s political involvement “will not go away just by this move” and could have some lasting impact.

Nevertheless, the combination of favorable regulatory developments in the self-driving space, renewed hopes for entry into the Indian market, and a perceived positive shift in Elon Musk’s focus has created a powerful upward momentum for Tesla’s stock, offering a glimmer of hope for investors who have endured a challenging start to 2025.

Key Points: – UPS will acquire Canada-based Andlauer Healthcare Group for $1.6B to strengthen cold chain and healthcare logistics capabilities. – The deal gives UPS deeper access to Canadian markets and expands its global healthcare supply chain footprint. – AHG’s founder Michael Andlauer will continue to lead operations post-acquisition, helping to integrate and scale services under UPS Healthcare.

UPS is taking a significant leap forward in healthcare logistics with its agreement to acquire Canada-based Andlauer Healthcare Group (AHG) for approximately $1.6 billion USD (CAD $2.2 billion). The deal, set to close in the second half of 2025, marks a strategic expansion of UPS Healthcare’s cold chain capabilities and its broader push to become the global leader in complex healthcare logistics.

Under the terms of the acquisition, AHG shareholders will receive CAD $55.00 per share in cash, a substantial premium that reflects the value of AHG’s specialized supply chain and third-party logistics offerings tailored to the healthcare sector. The transaction is subject to shareholder approval and regulatory clearance but has already secured support from AHG’s controlling shareholder, Michael Andlauer.

This acquisition arrives at a critical moment for healthcare logistics. Demand for temperature-sensitive and high-precision delivery of pharmaceuticals, biologics, and medical devices has grown rapidly in recent years, driven by the rise of advanced therapies, clinical trials, and global vaccine distribution efforts. UPS is positioning itself to meet those demands with a highly integrated global network, now enhanced by AHG’s robust infrastructure and expertise.

AHG brings to the table a coast-to-coast Canadian distribution network, a suite of customized logistics solutions, and proven cold chain transportation capabilities. These services will become part of UPS Healthcare’s expanding footprint, which already boasts over 19 million square feet of cGMP and GDP-compliant distribution space across the globe.

Michael Andlauer, AHG’s founder and CEO, will continue to lead the company following the acquisition, heading UPS Canada Healthcare and helping to guide the integration. “UPS Healthcare and AHG employees share a similar customer and patient-centric culture,” said Andlauer. “Once the transaction is completed, the businesses will offer an even broader set of specialized logistics services to customers throughout Canada.”

Kate Gutmann, EVP and president of International, Healthcare and Supply Chain Solutions at UPS, said the move is aligned with UPS’s mission to be the premier global healthcare logistics provider. “This acquisition marks another important step in our declaration to be the number one complex healthcare logistics and premium international logistics provider in the world,” she said.

The acquisition is also expected to drive growth for UPS by expanding its cold chain capabilities and enhancing services for healthcare customers who require strict temperature control, visibility, and compliance throughout the logistics chain. As UPS builds out its global logistics infrastructure, this move strategically complements earlier investments in technology, infrastructure, and customer-driven healthcare solutions.

For investors in the healthcare logistics and small-cap space, the AHG acquisition underscores growing M&A interest in niche logistics providers with deep industry specialization. It also signals UPS’s continued focus on high-growth, high-margin sectors, and its commitment to staying ahead in the evolving global healthcare ecosystem.

Key Points: – U.S.-based production shields Tesla from Trump’s auto tariffs, unlike GM and Ford. – Musk says ending tax credits would hurt rivals more than Tesla. – Musk sees self-driving tech as Tesla’s key long-term value.

President Donald Trump’s latest move to impose 25% tariffs on foreign automobiles and certain auto parts has shaken the auto industry, sending shares of major automakers tumbling. General Motors (GM) stock fell nearly 7%, while Ford (F) dropped 3%. But Tesla (TSLA) went in the opposite direction, climbing 5% in early trading, as analysts suggested the EV leader may be a “relative winner” in the tariff battle.

Unlike many of its competitors, Tesla is largely insulated from the impact of Trump’s tariffs thanks to its U.S.-based production. While the company operates gigafactories in China and Germany, none of the EVs built at those sites are sold in the U.S. Instead, Tesla’s American customers receive vehicles manufactured in Fremont, California, or Austin, Texas. This domestic production model allows Tesla to avoid the direct cost increases that automakers relying on foreign imports will now face.

By comparison, 77% of Ford’s vehicles are made in the U.S., followed by Stellantis (57%), Nissan (52%), and GM (52%). Many of these companies now find themselves in a difficult position, forced to absorb higher costs or pass them on to consumers. According to TD Cowen analyst Itay Michaeli, Tesla stands to benefit as its competitors struggle with price hikes. In particular, Tesla’s Model Y, a leading seller in the midsize crossover category, faces competition in a segment where nearly half of vehicles could now be subject to tariffs.

Despite Tesla’s apparent advantage, CEO Elon Musk has downplayed the impact of the tariffs on the company. In a post on X, Musk stated that Tesla is “NOT unscathed here” and that the impact on the company remains “significant.” However, he did not elaborate on how or why Tesla might be affected. While the new policy appears to hit Tesla’s competitors far harder, Musk’s comments suggest the company is still navigating challenges related to supply chains and international trade.

Trump, for his part, confirmed that he did not consult Musk before finalizing the tariffs, suggesting that the billionaire CEO “may have a conflict.” While Trump did not clarify the statement, it raises questions about whether Tesla’s relatively strong position under the new policy influenced the decision to exclude Musk from discussions.

Beyond tariffs, another potential battleground is the federal EV tax credit. Under the Inflation Reduction Act signed by President Biden in 2022, buyers can receive up to $7,500 in tax credits for purchasing an electric vehicle. Tesla has benefited from these incentives for years, particularly in its early days when it relied on federal subsidies to boost demand. However, Musk has previously indicated that Tesla no longer depends on these credits. He even suggested that if Trump and a Republican-controlled Congress were to eliminate them, it would hurt Tesla’s competitors far more than Tesla itself.

“I think it would be devastating for our competitors and for Tesla slightly. But long term, probably actually helps Tesla, would be my guess,” Musk said during Tesla’s Q2 earnings call last year.

The bigger bet for Tesla, however, isn’t just EVs—it’s autonomy. Musk has repeatedly stated that self-driving technology is Tesla’s true long-term value driver, not car sales. If Trump’s administration eases regulations around self-driving and robotaxi deployment, Tesla could benefit significantly.

For now, investors seem to agree with Musk. While traditional automakers scramble to reassess their supply chains and pricing strategies, Tesla’s stock continues to rise, reinforcing its position as one of the few beneficiaries of Trump’s aggressive trade policies.

In a major boost to its defense business, Boeing has been awarded the contract to develop the U.S. Air Force’s next-generation fighter jet under the Next Generation Air Dominance (NGAD) program. The aircraft, now officially named the F-47, will replace the Lockheed Martin F-22 Raptor and is expected to serve alongside autonomous drone aircraft in future combat scenarios.

The announcement, made by President Donald Trump in the Oval Office, marks a critical turning point for Boeing, which has faced severe challenges in both its commercial and defense divisions. The engineering and manufacturing development contract, valued at over $20 billion, could ultimately yield hundreds of billions in future orders spanning multiple decades. Boeing’s victory over Lockheed Martin in securing this contract is a defining moment in the aerospace industry, shifting the balance of power in the defense sector.

The design and capabilities of the F-47 remain closely guarded secrets, but military officials have emphasized its advancements over the F-22 Raptor. Chief of Staff of the Air Force General David Allvin highlighted the F-47’s longer range, superior stealth capabilities, and increased adaptability to future threats. The aircraft is expected to feature cutting-edge avionics, enhanced sensors, and next-generation propulsion systems, making it a formidable asset in countering emerging threats from nations like China and Russia.

The NGAD initiative is envisioned as a “family of systems” incorporating manned and unmanned platforms to dominate future battlefields. The F-47 will play a pivotal role in this strategy, integrating seamlessly with artificial intelligence-driven drone squadrons to enhance operational efficiency and combat effectiveness.

Boeing’s stock surged 4% following the announcement, while Lockheed Martin’s shares dropped nearly 7%, reflecting investor sentiment regarding the shift in defense contracting priorities. For Boeing, this win represents a much-needed resurgence in its defense business, particularly after suffering major setbacks in commercial aviation, including production delays, safety concerns, and financial losses from the 737 MAX crisis.

Industry analysts view this contract as a significant validation of Boeing’s ability to execute high-stakes defense projects despite its recent challenges. Roman Schweizer, an analyst at TD Cowen, described the win as a “major boost” for Boeing, particularly given its struggles with cost overruns and delays on previous Department of Defense programs, including the KC-46 tanker and Air Force One modifications.

Lockheed Martin, meanwhile, faces an uncertain future in high-end fighter production. The company recently lost its bid to develop the Navy’s next-generation carrier-based stealth fighter, and this latest defeat raises questions about its long-term dominance in the military aviation sector. Despite these challenges, Lockheed continues to hold a strong position with its F-35 Lightning II program, which remains a critical component of U.S. and allied air forces.

Beyond domestic implications, the F-47 program may have significant international ramifications. Trump hinted that U.S. allies have already expressed interest in purchasing the aircraft, signaling potential foreign military sales that could further bolster Boeing’s defense revenue. Countries seeking advanced air superiority solutions may turn to the F-47 as a viable alternative to existing platforms, further extending its market potential.

While Lockheed may still have the option to challenge the contract award, the high-profile nature of Trump’s announcement makes such a move less likely. The public endorsement of Boeing’s selection could mitigate political or legal challenges, cementing the company’s role in shaping the future of American airpower.

As Boeing embarks on this ambitious defense project, the F-47 contract underscores the evolving landscape of military aviation, the growing reliance on next-generation technologies, and the shifting power dynamics within the aerospace industry. The coming years will reveal whether Boeing can successfully deliver on its promises and reestablish itself as a dominant force in the global defense market.

– GM and Nvidia are partnering to integrate AI-powered solutions into vehicle design, advanced driver-assistance systems (ADAS), and factory automation. – GM will leverage Nvidia’s Omniverse platform for digital factory planning, optimizing manufacturing processes, and improving robotics. – Nvidia continues its push into the automotive industry, competing with rivals in AI-driven vehicle technology.

General Motors and Nvidia have announced a major collaboration aimed at revolutionizing the automotive industry with AI-driven technology. This strategic partnership will see GM leveraging Nvidia’s advanced artificial intelligence solutions across multiple facets of its business, from vehicle development to factory optimization.

“The era of physical AI is here, and together with GM, we’re transforming transportation, from vehicles to the factories where they’re made,” said Jensen Huang, Nvidia founder and CEO. “We are thrilled to partner with GM to build AI systems tailored to their vision, craft, and know-how.”

A central component of this partnership is GM’s adoption of Nvidia’s Omniverse platform, which enables the creation of “digital twins”—virtual replicas of real-world environments. GM has already been experimenting with Omniverse since 2022 to digitally simulate its design centers and optimize vehicle development. This new collaboration extends those efforts, incorporating Nvidia’s AI-powered solutions into GM’s assembly plants and production facilities.

Beyond manufacturing, GM will integrate Nvidia’s Drive AGX platform into its next-generation vehicles. This hardware will support future advanced driver-assistance systems (ADAS) and enhance in-cabin safety features. The partnership positions GM to further compete in the race toward fully autonomous and AI-enhanced vehicles, an area where competitors like Tesla and Mercedes-Benz have been making significant strides.

While GM has relied on Nvidia’s graphics processing units (GPUs) for AI model training, this expanded agreement takes their collaboration to a new level. The financial terms of the deal were not disclosed, but Nvidia has been known to license Omniverse for $4,500 per GPU, per year. Given the scale of GM’s operations, the automaker is expected to require a substantial number of GPUs to power its AI-driven initiatives.

The announcement coincides with Nvidia’s GTC AI conference, where the company has been showcasing its advancements in AI and simulation technology. The move comes as both Nvidia and GM navigate competitive and regulatory challenges, including increased competition from China and evolving U.S. trade policies. GM’s stock has dropped roughly 8% in 2025, while Nvidia has seen a 12% decline, underscoring the pressure both companies face to innovate and expand their market presence.

GM CEO Mary Barra highlighted the broader implications of the partnership, stating, “AI not only optimizes manufacturing processes and accelerates virtual testing but also helps us build smarter vehicles while empowering our workforce to focus on craftsmanship. By merging technology with human ingenuity, we unlock new levels of innovation in vehicle manufacturing and beyond.”

With over 20 other automakers—including Mercedes-Benz, Volvo, and Volkswagen—already using Nvidia’s automotive AI solutions, this partnership further cements Nvidia’s role in the future of intelligent vehicles. As demand for AI-powered automotive solutions continues to grow, this collaboration between GM and Nvidia represents a significant step forward in reshaping how vehicles are designed, built, and driven.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Full year 2024 financial results. FreightCar America generated 2024 adjusted net income to common stockholders of $4.5 million or $0.15 per share compared to a loss of $11.0 million or $(0.39) per share in 2023 and our estimate of $5.5 million or $0.17 per share. Gross margin as a percentage of revenue increased to 12.0% compared to 11.7% in FY 2023. Revenue and rail car deliveries increased to $559.4 million and 4,362 compared to $358.1 million and 3,022 in 2023. We had forecast revenue of $577.4 million and deliveries of 4,550. Adjusted EBITDA increased to $43.0 million compared to $20.1 million in 2023 and our estimate of $38.3 million. Full year adjusted free cash flow amounted to $21.7 million versus $(17.6) million in 2023.

Full Year 2025 corporate guidance. Management issued full year 2025 guidance. Railcar deliveries are expected to be in the range of 4,500 to 4,900, revenue is expected to be in the range of $530 million to $595 million, and adjusted EBITDA is expected to be in the range of $43 to $49 million. Compared to 2024, railcar deliveries, revenue, and adjusted EBITDA are expected to increase 7.7%, 0.6%, and 7.0%, respectively, at the midpoints of guidance. Our current 2025 estimates include railcar deliveries of 4,675 units, revenue of $580.6 million and EBITDA of $44.9 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – GM announced a $6B share buyback and a 25% dividend increase to $0.15 per share – Investors reacted positively, pushing GM stock up over 5% in morning trading – Company maintains strong R&D spending of $8B+ while navigating potential tariff challenges

General Motors announced a significant boost to shareholder returns on Wednesday, unveiling a new $6 billion share repurchase program and increasing its quarterly dividend. The move comes just weeks after investors expressed disappointment when the automaker’s Q4 earnings call failed to include new capital return initiatives.

GM’s quarterly dividend will rise by $0.03 to $0.15 per share, marking the company’s first dividend increase since 2023. The $6 billion share repurchase authorization includes plans for a $2 billion accelerated share repurchase (ASR) program to be implemented in the near term.

Investors responded positively to the announcement, sending GM shares up more than 5% in morning trading to $49.22.

CEO Mary Barra emphasized the company’s strong execution across all three pillars of its capital allocation strategy. These include reinvesting for profitable growth, maintaining a strong investment-grade balance sheet, and returning capital to shareholders.

This latest buyback program follows GM’s previous $6 billion share repurchase plan and the $10 billion ASR program introduced in late 2023. The earlier initiatives coincided with a 33% dividend increase that took effect in January 2024.

During GM’s most recent earnings call, CFO Paul Jacobson had indicated the company would explore prudent ways to expand shareholder returns. In today’s announcement, he expressed confidence in the business plan and balance sheet strength, noting GM would remain agile in responding to potential policy changes.

Despite the increased focus on shareholder returns, GM confirmed its commitment to continued investment in its core business. The company expects 2025 capital spending to remain between $10-11 billion, including investments in battery manufacturing joint ventures. Research and product development spending is projected to exceed $8 billion for the year.

For fiscal 2025, GM has forecast profits between $13.7 billion and $15.7 billion, with diluted and adjusted earnings per share of $11-12. The company noted these projections don’t account for potential impacts from tariffs that might be implemented by the Trump administration on imported vehicles or parts.

While GM is clearly a large-cap stock, its shareholder-friendly actions could signal a broader trend that might eventually benefit small-cap stocks and the Russell 2000 index. Historically, when large corporations increase dividends and buybacks, it often reflects growing confidence in economic conditions that eventually filters down to smaller companies. The Russell 2000 has underperformed larger indices in recent years, but increased capital returns across the market could indicate improving liquidity conditions that typically benefit smaller firms more dramatically.

Additionally, GM’s ability to maintain robust capital returns while facing potential tariff challenges demonstrates corporate resilience that could reassure investors about smaller domestic manufacturers’ prospects. Many Russell 2000 companies are more domestically focused than their large-cap counterparts, potentially insulating them from international trade disruptions.

The shareholder return increases demonstrate GM’s financial strength despite ongoing challenges in the automotive industry, including electrification costs, competition, and potential trade policy changes. The company’s willingness to boost returns while maintaining substantial investments in future technologies suggests management’s confidence in its long-term business strategy.

As GM navigates the evolving automotive landscape, this balanced approach to capital allocation appears designed to keep both long-term investors and those seeking immediate returns satisfied while the company continues its transition toward an electric future.

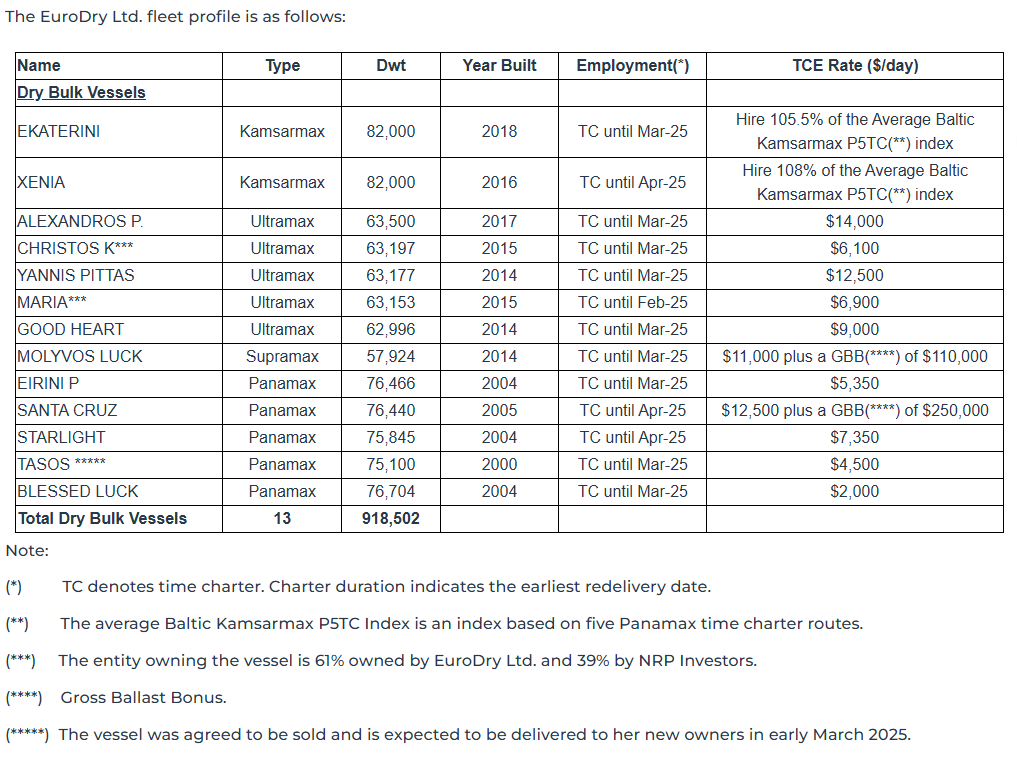

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

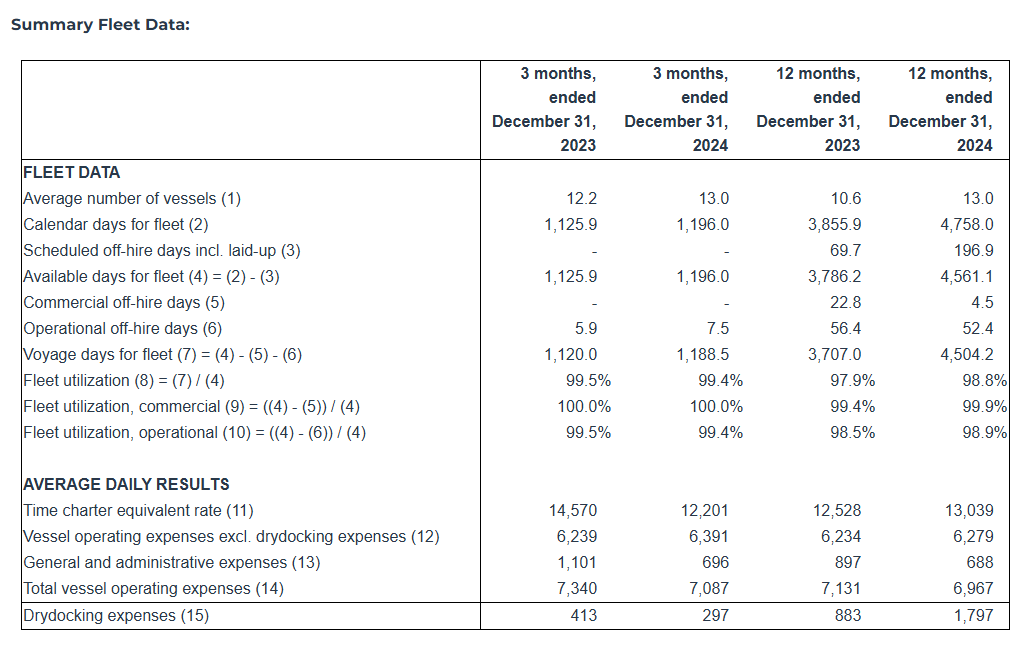

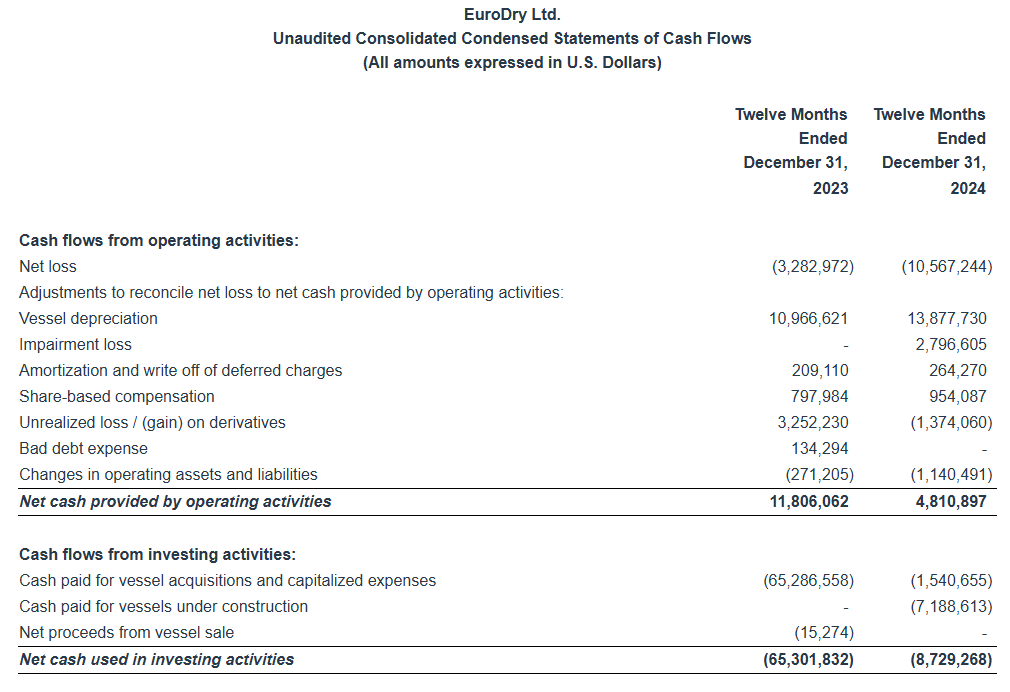

Fourth quarter financial results. EuroDry Ltd. reported an adjusted fourth-quarter net loss to controlling shareholders of $0.7 million, or ($0.25) per share, compared to adjusted net income of $1.9 million, or $0.70 per share, during the prior year period. Adjusted EBITDA declined to $4.8 million compared to $6.6 million during the prior year period. The year-over-year decline is due to low market rates as trade volume has fallen amid a slowdown in the Chinese economy.

Full year 2024 earnings and updated 2025 estimates. For the full year 2024, adjusted EBITDA and earnings per share declined to $12.4 million and ($3.02), respectively, from $14.6 million and $0.12 in 2023. We have lowered our 2025 adjusted EBITDA and EPS estimates to $19.6 million and ($0.43), respectively, from $22.0 million and ($0.34). While we expect spot and one-year time charter equivalent rates to improve throughout the year, our estimates have been lowered compared to our previous expectations due to weak market conditions.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ATHENS, Greece, Feb. 24, 2025 (GLOBE NEWSWIRE) — EuroDry Ltd. (NASDAQ: EDRY, the “Company” or “EuroDry”), an owner and operator of drybulk vessels and provider of seaborne transportation for drybulk cargoes, announced today its results for the three and twelve-month periods ended December 31, 2024.

Fourth Quarter 2024 Highlights:

Total net revenues of $14.5 million.

Net loss attributable to controlling shareholders, of $3.3 million or $1.20 loss per share basic and diluted.

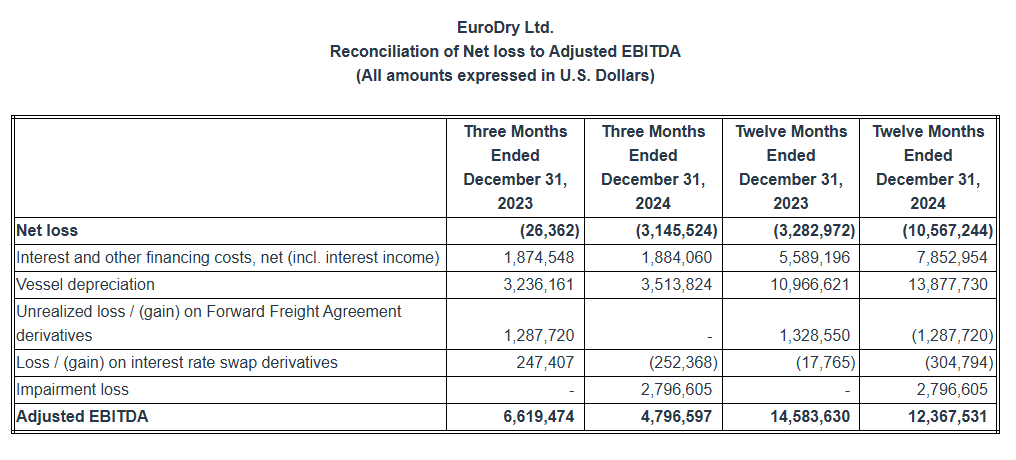

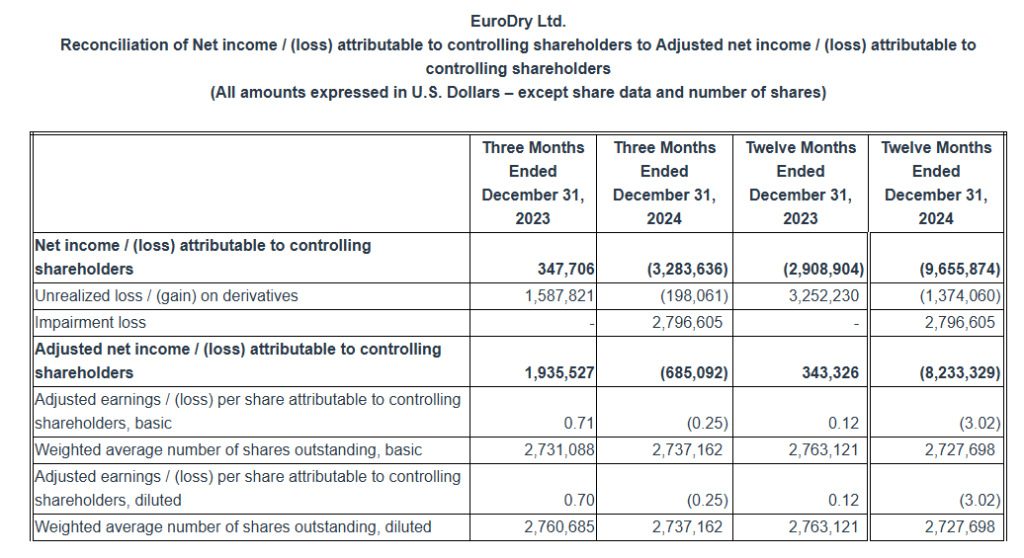

Adjusted net loss1 attributable to controlling shareholders, for the quarter of $0.7 million, or, $0.25 per share basic and diluted which excludes among other items an impairment charge of $2.8 million on one of our vessels.

Adjusted EBITDA1 was $4.8 million.

An average of 13.0 vessels were owned and operated during the fourth quarter of 2024 earning an average time charter equivalent rate of $12,201 per day.

To date, about $5.3 million has been used to repurchase 334,674 shares of the Company, under our share repurchase plan of up to $10 million, announced in August 2022.

Recent developments:

In November 2024, the Company signed two contracts with Nantong Xiangyu Shipbuilding for the construction of two 63,500 DWT ultramax bulk carriers. Both vessels are geared, eco, and are built to EEDI phase 3 design standard. The two newbuildings are scheduled to be delivered during the second and third quarters of 2027. The total consideration for the two newbuilding contracts is approximately $71.8 million and will be financed with a combination of debt and equity.

The Company on January 29, 2025, signed an agreement to sell M/V Tasos, a 75,100 dwt drybulk vessel, built in 2000, for demolition, for approximately $5 million. The vessel is expected to be delivered to its buyers, an unaffiliated third party, until early-March 2025, upon completion of her present charter. As a result of the vessel sale, we expect to record a gain of approximately $2.1million.

Full Year 2024 Highlights:

Total net revenues of $61.1 million.

Net loss attributable to controlling shareholders, of $9.7 million, or $3.54 loss per share basic and diluted.

Adjusted net loss1 attributable to controlling shareholders, for the period was $8.2 million or $3.02 adjusted loss per share basic and diluted.

Adjusted EBITDA1 was $12.4 million.

An average of 13.0 vessels were owned and operated during the twelve months of 2024 earning an average time charter equivalent rate of $13,039 per day.

Aristides Pittas, Chairman and CEO of EuroDry commented: “During the last couple of months of 2024 and during January and February of 2025, the drybulk market dropped to rates not seen since the early days of the COVID pandemic and touched decade-long lows last seen in 2016. It appears that a combination of low trade volumes due to low demand from China combined with a record low percentage of the fleet tied up in ports more than counterbalanced the low fleet growth during the period. There is some expectation, though, that the various stimuli packages released by the Chinese government during the fourth quarter of 2024 would start showing results in the near future; such stimuli combined with the typical seasonal recovery of the drybulk markets during the second quarter could lead to a noticeable recovery of the charter rates as already indicated by the forward (“FFA”) market.

“The low market of the fourth quarter was reflected in our results for the period although our vessels achieved better charters than market averages indicate. And while the low market of January and February 2025 will affect our first quarter results, we expect a recovery of the market in March and during the second quarter of 2025 to return us to profitability as our fleet is positioned to take full advantage of it having passed most drydockings in 2024. At the same time, as prices for vessels have also weakened, we are diligent in searching for potential investment opportunities; and to help finance such opportunities should they arise, we have committed to sell our eldest vessel M/V Tasos, as we recently announced.”

Tasos Aslidis, Chief Financial Officer of EuroDry commented: “In the fourth quarter of 2024 the Company operated an average of 13.0 vessels, versus 12.2 vessels during the same period last year. Our net revenues decreased to $14.5 million in the fourth quarter of 2024 compared to $15.9 million during the same period of last year. Our vessels earned in the fourth quarter of 2024 approximately 16.3% lower time charter equivalent rates compared to the corresponding period of 2023. At the same time, total daily vessel operating expenses, including management fees, general and administrative expenses but excluding drydocking costs, during the fourth quarter of 2024, averaged $7,087 per vessel per day, as compared to $7,340 for the same period of last year and $6,967 per vessel per day for the year 2024 as compared to $7,131 per vessel per day for the same period of 2023. The decreased total vessel operating expenses in the recent periods are attributable to the significantly lower daily general and administrative expenses. General and administrative expenses for the same period of 2023 included additional costs incurred in relation to the formation of a partnership with a number of investors represented by NRP Project Finance AS (“NRP Investors”) regarding the ownership of the entities owning M/V Christos K and M/V Maria (the “Partnership”).

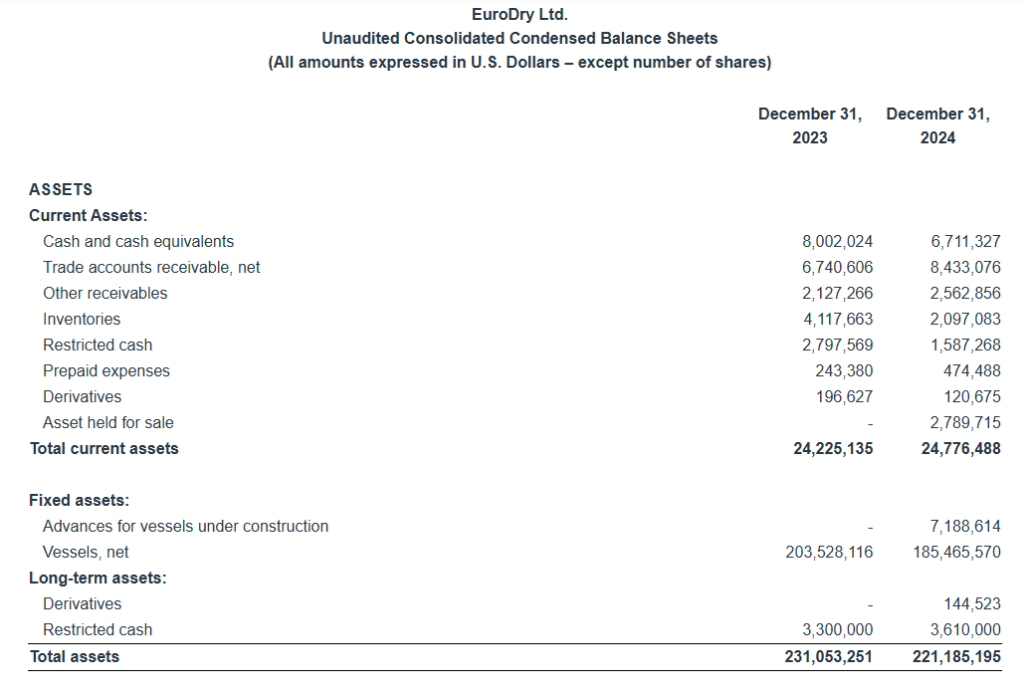

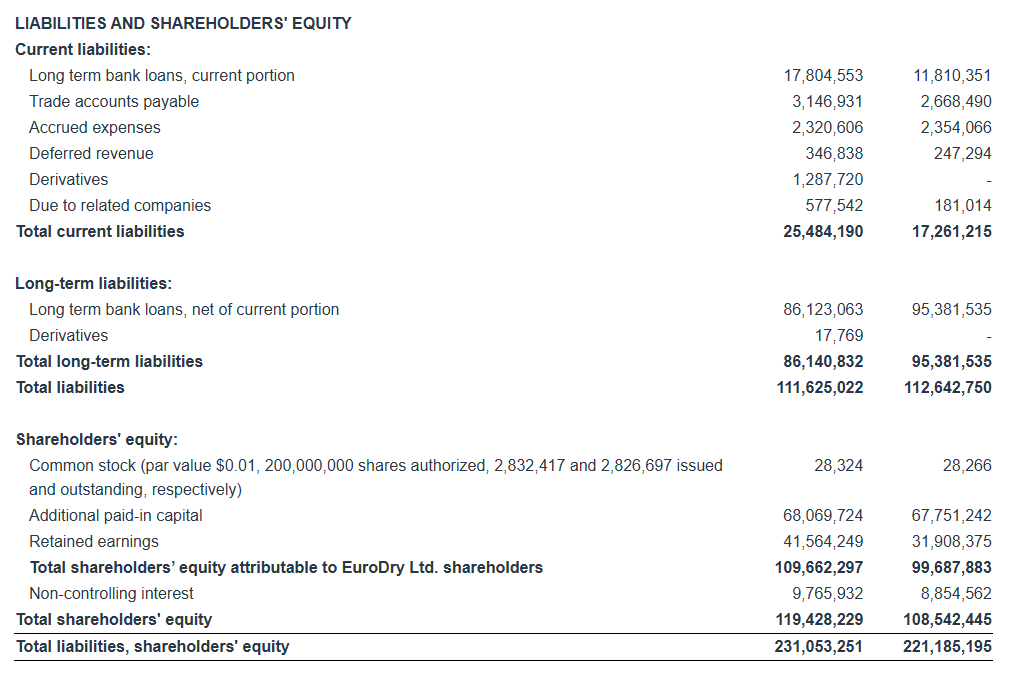

“Adjusted EBITDA during the fourth quarter of 2024 was $4.8 million versus $6.6 million in the fourth quarter of last year, and $12.4 million versus $14.6 million for the respective twelve-month periods of 2024 and 2023, respectively. As of December 31, 2024, our outstanding debt (excluding the unamortized loan fees) was $108.2 million versus unrestricted and restricted cash of $11.9 million. As of the same date, our scheduled debt repayments over the next 12 months amounted to about $12.1 million (excluding the unamortized loan fees).”

Fourth Quarter 2024 Results: For the fourth quarter of 2024, the Company reported total net revenues of $14.5 million representing a 8.8% decrease over total net revenues of $15.9 million during the fourth quarter of 2023. This was the result of the lower time charter rates our vessels earned in the fourth quarter of 2024, partly offset by the higher average number of vessels operated compared to the same period of 2023. On average, 13.0 vessels were owned and operated during the fourth quarter of 2024 earning an average time charter equivalent rate of $12,201 per day compared to 12.2 vessels in the same period of 2023 earning on average $14,570 per day.

For the fourth quarter of 2024, voyage expenses, net amounted to $0.9 million and mainly relate to vessels repositioning between charters and expenses during operational off-hire time. For the same period of 2023 voyage expenses net amounted to $0.6 million.

Vessel operating expenses were $6.6 million for the fourth quarter of 2024 as compared to $6.1 million for the same period of 2023. The increase is mainly attributable to the increased number of vessels operating in the fourth quarter of 2024 compared to the corresponding period in 2023.

Depreciation expense for the fourth quarter of 2024 amounted to $3.5 million, as compared to $3.2 million for the same period of 2023. This increase is again due to the higher number of vessels operating in the fourth quarter of 2024 as compared to the same period of 2023.

General and administrative expenses for the fourth quarter of 2024 were $0.8 million compared to $1.2 million of the fourth quarter of 2023. The decrease is mainly attributable to an additional cost of $0.44 million that was incurred during the last quarter of 2023 in relation to the formation of the Partnership.

Related party management fees for the fourth quarter of 2024 increased to $1.1 million from $1.0 million for the same period of 2023 as a result of an adjustment for inflation in the daily vessel management fee, effective from January 1, 2024, increasing the daily vessel management fee from 775 Euros to 810 Euros, as well as the increased number of vessels operating in the fourth quarter of 2024 compared to the corresponding period in 2023, partly offset by the favorable movement of the euro/dollar exchange rate.

During the fourth quarter of 2024 and 2023, none of our vessels underwent drydocking. The total cost for the fourth quarter of 2024 and 2023 of $0.4 million and $0.5 million, respectively, relates to drydocking expenses incurred in relation to upcoming drydockings.

In the fourth quarter of 2024 the Company recorded an impairment charge of $2.8 million. The impairment was booked to reduce the carrying amount of a drybulk vessel (M/V “Santa Cruz”) to its estimated market value, since based on the Company’s impairment test results it was determined that its carrying amount was not recoverable. No such cost existed in the fourth quarter of 2023.

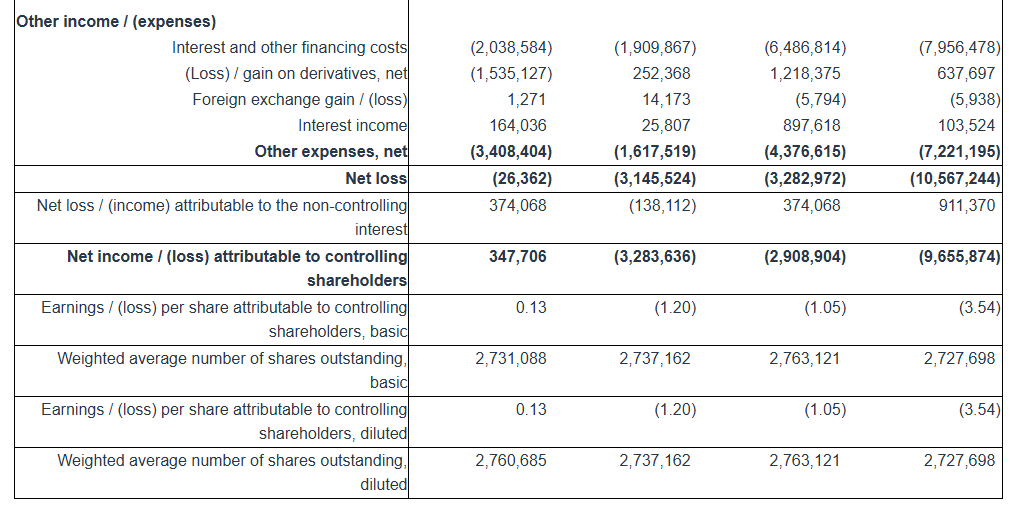

Interest and other financing costs for the fourth quarter of 2024 decreased to $1.9 million as compared to $2.0 million for the same period of 2023. Interest expense during the fourth quarter of 2024 was slightly lower mainly due to the slightly decreased benchmark rates of our loans, partly offset by the increased average debt during the period as compared to the same period of last year.

For the three months ended December 31, 2024, the Company recognized a gain on an interest rate swap of $0.25 million, as compared to a loss on an interest rate swap of $0.25 million and a loss on forward freight agreement (“FFA”) contracts of $1.3 million for the same period of 2023.

Interest income for the fourth quarter of 2024 amounted to $0.03 million compared to $0.16 million for the same period of 2023. The decrease in interest income is attributable to lower cash balances maintained during the fourth quarter of 2024 compared to the corresponding period in 2023.

The Company reported a net loss for the period of $3.1 million and a net loss attributable to controlling shareholders for the period of $3.3 million, as compared to a net loss of $0.03 million and a net income attributable to controlling shareholders of $0.3 million for the same period of 2023. The net income attributable to the non-controlling interest of $0.1 million in the fourth quarter of 2024 represents the income attributable to the 39% ownership of the Partnership.

Adjusted EBITDA for the fourth quarter of 2024 was $4.8 million compared to $6.6 million achieved during the fourth quarter of 2023.

Basic and diluted loss per share attributable to controlling shareholders for the fourth quarter of 2024 was $1.20 calculated on 2,737,162 basic and diluted weighted average number of shares outstanding, compared to earnings per share of $0.13, calculated on 2,731,088 basic and 2,760,685 diluted weighted average number of shares outstanding for the fourth quarter of 2023.

Excluding the effect on the net loss attributable to controlling shareholders for the quarter of the unrealized loss / (gain) on derivatives and the impairment loss on a vessel, the adjusted loss per share attributable to controlling shareholders for the quarter ended December 31, 2024 would have been $0.25 basic and diluted, compared to adjusted earnings of $0.71 and $0.70 per share basic and diluted, respectively, for the quarter ended December 31, 2023. Usually, security analysts do not include the above items in their published estimates of earnings per share.

Full Year 2024 Results: For the full year of 2024, the Company reported total net revenues of $61.1 million representing a 28.3% increase over total net revenues of $47.6 million during the twelve months of 2023, as a result of the increased number of vessels operated during the year and the slightly higher time charter equivalent rates earned by our vessels in the twelve months of 2024 compared to the same period of 2023. On average, 13.0 vessels were owned and operated during the twelve months of 2024 earning an average time charter equivalent rate of $13,039 per day compared to 10.6 vessels in the same period of 2023 earning on average $12,528 per day.

For the twelve months of 2024, voyage expenses, net, were $6.1 million and mainly relate to vessels repositioning between charters and expenses during operational off-hire time. For the same period of 2023, voyage expenses, net, were $4.0 million and mainly relate to expenses incurred by one of our vessels while employed under a voyage charter, vessels repositioning between charters and expenses during the detention of one of our vessels in Corpus Christi.

Vessel operating expenses were $25.7 million for the twelve months of 2024 as compared to $20.8 million for the same period of 2023. The increase is mainly attributable to the increased number of vessels operating in 2024 compared to the corresponding period in 2023.

Depreciation expense for the year 2024 was $13.9 million compared to $11.0 million during the same period of 2023, again, mainly due to the higher number of vessels operating in the same period.

Related party management fees for the year of 2024 were increased to $4.2 million from $3.3 million for the same period of 2023 as a result of an adjustment for inflation in the daily vessel management fee, effective from January 1, 2024, increasing the daily vessel management fee from 775 Euros to 810 Euros and the increased number of vessels operated.

General and administrative expenses during the twelve months of 2024 were $3.3 million compared to $3.5 million during the same period in 2023. The decrease is attributable to an additional cost of $0.44 million that was incurred during the last quarter of 2023 in relation to the formation of the Partnership, partly offset by the increased cost of our stock incentive plan in 2024.

During the twelve months of 2023, we recorded a provision of $0.5 million for anticipated costs related to the detention of one of our vessels in Corpus Christi presented as other operating loss.

In 2023, we wrote-off certain trade receivables by recording a bad debt expense of $0.1 million. In 2024, we had no bad debt expense.

In the twelve months of 2024, seven of our vessels completed their special survey with drydocking for a total cost of $8.5 million. In the twelve months of 2023, three of our vessels completed their special or intermediate survey with drydocking and one vessel passed her intermediate survey in water (in lieu of drydock), for a total cost of $3.4 million.

Interest and other financing costs for the twelve months of 2024 amounted to $8.0 million compared to $6.5 million for the same period of 2023. Interest expense for the twelve months of 2024 was higher due to the increased average debt as compared to the same period of last year.

For the twelve months ended December 31, 2024, the Company recognized a $0.1 million unrealized gain and a $0.2 million realized gain on one interest rate swap, as well as a 1.3 million unrealized gain and a $1.0 million realized loss on FFA contracts as compared to a $1.9 million unrealized loss and a $1.9 million realized gain on interest rate swaps, as well as a 1.3 million unrealized loss and a $2.5 million realized gain on FFA contracts for the same period of 2023.

Interest income for 2024 amounted to $0.1 million compared to $0.9 million interest income for the same period of 2023. The decrease of interest income is attributable to lower cash balances maintained during the twelve months of 2024 compared to the corresponding period in 2023.

The Company reported a net loss for the period of $10.6 million and a net loss attributable to controlling shareholders of $9.7 million, as compared to a net loss of $3.3 million and a net loss attributable to controlling shareholders of $2.9 million, for the same period of 2023. The net loss attributable to the non-controlling interest of $0.9 million in 2024 represents the loss attributable to the 39% ownership of the Partnership.

Adjusted EBITDA for the twelve months of 2024 was $12.4 million compared to $14.6 million achieved during the twelve months of 2023.

Basic and diluted loss per share attributable to controlling shareholders for the twelve months of 2024 was $3.54, calculated on 2,727,698 basic and diluted weighted average number of shares outstanding, compared to basic and diluted loss per share attributable to controlling shareholders for the twelve months of 2023 of $1.05, calculated on 2,763,121 basic and diluted weighted average number of shares outstanding.

Excluding the effect on the net loss attributable to controlling shareholders for the year of the unrealized loss / (gain) on derivatives and the impairment loss on a vessel, the adjusted loss per share attributable to controlling shareholders for the year ended December 31, 2024 would have been $3.02 basic and diluted, compared to adjusted earnings per share of $0.12 basic and diluted for the same period of 2023. As previously mentioned, usually, security analysts do not include the above items in their published estimates of earnings per share.

(1) Average number of vessels is the number of vessels that constituted the Company’s fleet for the relevant period, as measured by the sum of the number of calendar days each vessel was a part of the Company’s fleet during the period divided by the number of calendar days in that period.

(2) Calendar days. We define calendar days as the total number of days in a period during which each vessel in our fleet was owned by us including off-hire days associated with major repairs, drydockings or special or intermediate surveys or days of vessels in lay-up. Calendar days are an indicator of the size of our fleet over a period and affect both the amount of revenues and the amount of expenses that we record during that period.

(3) The scheduled off-hire days including vessels laid-up are days associated with scheduled repairs, drydockings or special or intermediate surveys or days of vessels in lay-up.

(4) Available days. We define available days as the total number of Calendar days in a period net of scheduled off-hire days incl. laid up. We use available days to measure the number of days in a period during which vessels were available to generate revenues.

(5) Commercial off-hire days. We define commercial off-hire days as days a vessel is idle without employment.

(6) Operational off-hire days. We define operational off-hire days as days associated with unscheduled repairs or other off-hire time related to the operation of the vessels.

(7) Voyage days. We define voyage days as the total number of days in a period during which each vessel in our fleet was in our possession net of commercial and operational off-hire days. We use voyage days to measure the number of days in a period during which vessels actually generate revenues or are sailing for repositioning purposes.

(8) Fleet utilization. We calculate fleet utilization by dividing the number of our voyage days during a period by the number of our available days during that period. We use fleet utilization to measure a company’s efficiency in finding suitable employment for its vessels and minimizing the amount of days that its vessels are off-hire for reasons such as unscheduled repairs or days waiting to find employment.

(9) Fleet utilization, commercial. We calculate commercial fleet utilization by dividing our available days net of commercial off-hire days during a period by our available days during that period.

(10) Fleet utilization, operational. We calculate operational fleet utilization by dividing our available days net of operational off-hire days during a period by our available days during that period.

(11) Time charter equivalent rate, or TCE, is a measure of the average daily net revenue performance of our vessels. Our method of calculating TCE is determined by dividing time charter revenue and voyage charter revenue net of voyage expenses by voyage days for the relevant time period. Voyage expenses primarily consist of port, canal and fuel costs that are unique to a particular voyage, which would otherwise be paid by the charterer under a time charter contract, or are related to repositioning the vessel for the next charter. TCE provides additional meaningful information in conjunction with time charter revenue and voyage charter revenue, the most directly comparable GAAP measure, because it assists our management in making decisions regarding the deployment and use of our vessels and because we believe that it provides useful information to investors regarding our financial performance. TCE is a standard shipping industry performance measure used primarily to compare period-to-period changes in a shipping company’s performance despite changes in the mix of charter types (i.e., spot voyage charters, time charters, pool agreements and bareboat charters) under which the vessels may be employed between the periods. Our definition of TCE may not be comparable to that used by other companies in the shipping industry.

(12) We calculate daily vessel operating expenses, which include crew costs, provisions, deck and engine stores, lubricating oil, insurance, maintenance and repairs and related party management fees by dividing vessel operating expenses and related party management fees by fleet calendar days for the relevant time period. Drydocking expenses are reported separately.

(13) Daily general and administrative expenses are calculated by us by dividing general and administrative expenses by fleet calendar days for the relevant time period.

(14) Total vessel operating expenses, or TVOE, is a measure of our total expenses associated with operating our vessels. We compute TVOE as the sum of vessel operating expenses, related party management fees and general and administrative expenses; drydocking expenses are not included. Daily TVOE is calculated by dividing TVOE by fleet calendar days for the relevant time period.

(15) Daily drydocking expenses are calculated by us by dividing drydocking expenses by the fleet calendar days for the relevant period. Drydocking expenses include expenses during drydockings that would have been capitalized and amortized under the deferral method. Drydocking expenses could vary substantially from period to period depending on how many vessels underwent drydocking during the period. The Company expenses drydocking expenses as incurred.

Conference Call and Webcast: Today, February 24, 2025 at 9:00 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

Conference Call details: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “EuroDry” to the operator and/or conference ID 13751962. Click here for additional participant International Toll -Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

Audio webcast – Slides Presentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.eurodry.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the fourth quarter ended December 31, 2024, will also be available in PDF format 10 minutes prior to the conference call and webcast, accessible on the company’s website (www.eurodry.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

Adjusted EBITDA Reconciliation: EuroDry Ltd. considers Adjusted EBITDA to represent net loss before interest and other financing costs, income taxes, depreciation, unrealized loss / (gain) on Forward Freight Agreement derivatives (“FFAs”), loss / (gain) on interest rate swap derivatives and impairment loss. Adjusted EBITDA does not represent and should not be considered as an alternative to net loss, as determined by United States generally accepted accounting principles, or GAAP. Adjusted EBITDA is included herein because it is a basis upon which the Company assesses its financial performance because the Company believes that this non-GAAP financial measure assists our management and investors by increasing the comparability of our performance from period to period by excluding the potentially disparate effects between periods of, financial costs, unrealized loss / (gain) on FFAs, loss / (gain) on interest rate swap derivatives, depreciation and impairment loss. The Company’s definition of Adjusted EBITDA may not be the same as that used by other companies in the shipping or other industries.

Adjusted net income / (loss) attributable to controlling shareholders and Adjusted earnings / (loss) per share attributable to controlling shareholders Reconciliation:

EuroDry Ltd. considers Adjusted net income / (loss) attributable to controlling shareholders, to represent net income / (loss) before unrealized loss / (gain) on derivatives, which includes FFAs and interest rate swaps, and impairment loss. Adjusted net income / (loss) attributable to controlling shareholders and Adjusted earnings / (loss) per share attributable to common shareholders are included herein because we believe they assist our management and investors by increasing the comparability of the Company’s fundamental performance from period to period by excluding the potentially disparate effects between periods of the aforementioned items , which may significantly affect results of operations between periods. Adjusted net income / (loss) attributable to controlling shareholders and Adjusted earnings / (loss) per share attributable to common shareholders do not represent and should not be considered as an alternative to net income / (loss) attributable to controlling shareholders or earnings / (loss) per share attributable to common shareholders, as determined by GAAP. The Company’s definition of Adjusted net income / (loss) attributable to controlling shareholders and Adjusted earnings / (loss) per share attributable to common shareholders may not be the same as that used by other companies in the shipping or other industries. Adjusted net income / (loss) attributable to controlling shareholders and Adjusted earnings / (loss) per share attributable to common shareholders are not adjusted for all non-cash income and expense items that are reflected in our statement of cash flows.

About EuroDry Ltd. EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd into a separate listed public company. EuroDry was spun-off from Euroseas Ltd on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY.

EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day-to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

The Company has a fleet of 13 vessels, including 5 Panamax drybulk carriers, 5 Ultramax drybulk carriers, 2 Kamsarmax drybulk carriers and 1 Supramax drybulk carrier. EuroDry’s 13 drybulk carriers have a total cargo capacity of 918,502 dwt. After the delivery of two Ultramax vessels in 2027 and the completion of the sale of one Panamax vessel, the Company’s fleet will consist of 14 vessels with a total carrying capacity of 970,402 dwt.

Forward Looking Statement This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events and the Company’s growth strategy and measures to implement such strategy; including expected vessel acquisitions and entering into further time charters. Words such as “expects,” “intends,” “plans,” “believes,” “anticipates,” “hopes,” “estimates,” and variations of such words and similar expressions are intended to identify forward-looking statements. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates that are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to changes in the demand for dry bulk vessels, competitive factors in the market in which the Company operates; risks associated with operations outside the United States; and other factors listed from time to time in the Company’s filings with the Securities and Exchange Commission. The Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

Nicolas Bornozis Markella Kara Capital Link, Inc. 230 Park Avenue, Suite 1540 New York, NY10169 Tel. (212) 661-7566 E-mail: [email protected]

__________________ 1Adjusted EBITDA, Adjusted net income / (loss) attributable to controlling shareholders and Adjusted earnings / (loss) per share are not recognized measurements under US GAAP (GAAP) and should not be used in isolation or as a substitute for EuroDry’s financial results presented in accordance with GAAP. Refer to a subsequent section of the Press Release for the definitions and reconciliation of these measurements to the most directly comparable financial measures calculated and presented in accordance with GAAP.

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New time charter contract. Euroseas Ltd. executed a time charter contract for the M/V EM Hydra at a gross daily rate of $19,000 for a minimum period of 24 months to a maximum of 26 months at the charterer’s option. The M/V EM Hydra is a 1,740 twenty-foot equivalent unit (TEU) feeder container ship. The new charter will commence on May 1, 2025, in continuation of its current charter.

Attractive rate and improved charter coverage. The new time charter is an improvement over the previous contract rate of $13,000 per day and is expected to contribute EBITDA of $7.3 million during the minimum contracted period. We had previously assumed the vessel would be re-contracted at a rate of $16,000 per day. The new time charter enhances Euroseas’ charter coverage for the remainder of 2025 and 2026 to ~85% and ~50%, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Tariffs. Pursuant to the International Emergency Economic Powers Act, the Trump Administration is implementing a 25% additional tariff on imports from Canada and Mexico and a 10% additional tariff on imports from China. The tariffs are effective on February 4. Energy resources from Canada will have a lower 10% tariff. The action is intended to hold Mexico, Canada, and Mexico accountable for their promises of halting illegal immigration and preventing fentanyl and other drugs from entering the United States. The ad valorem duties do not appear to consider the origin of raw materials or to be subject to exemption.

Exposure. In 2021, FreightCar moved its manufacturing activities in the United States to a new state-of-the-art facility in Castanos, Mexico. It steadily grew production capacity to 5,000 rail cars per year with the addition of a fourth production line during the fourth quarter of 2023. Importantly, the company’s competitors, Greenbrier Companies (NYSE-GBX) and Trinity Industries (NYSE-TRN), also have significant manufacturing operations in Mexico that serve the U.S. market.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Acquires DealerClub for $25 million to revolutionize dealer-to-dealer digital auctions with reputation-based transparency. – Integrates DealerClub’s innovative platform with AccuTrade, creating a seamless retail and wholesale ecosystem for automotive dealers. – Strengthens Cars Commerce’s role in the $10B wholesale market, empowering dealers to optimize inventory and boost profitability.

Cars Commerce, the parent company of Cars.com, is making a bold move into the wholesale automotive market with its acquisition of DealerClub, a reputation-driven digital auction platform. This purchase, finalized for $25 million in cash with the potential for up to $88 million in performance-based payouts, reflects Cars Commerce’s strategic vision to streamline how dealers trade vehicles and optimize inventory management.

DealerClub’s innovative platform has made waves in the industry since its launch in 2024. Unlike traditional wholesale systems, DealerClub focuses on reputation-based transactions, which foster trust between dealers and reduce common challenges like arbitration disputes and title issues. This groundbreaking approach has attracted over 650 dealers to the platform and provides Cars Commerce with a strong foothold in the $10 billion wholesale used car market.

Revolutionizing Wholesale with Technology

The acquisition builds on Cars Commerce’s mission to use technology to simplify the car-buying and selling process. DealerClub’s platform, designed to facilitate seamless dealer-to-dealer transactions, aligns perfectly with this goal.

“This is a critical step for us,” said Alex Vetter, CEO of Cars Commerce. “Dealers need efficient, transparent solutions to manage inventory and boost profitability. DealerClub’s technology adds a new dimension to our platform, making it easier for dealers to trade within a trusted network while keeping more profit in their pockets.”

Cars Commerce plans to integrate DealerClub with its existing tools, such as the AccuTrade appraisal platform, creating a full-service solution that combines retail and wholesale capabilities. This unified ecosystem will allow dealers to handle every aspect of vehicle trading—from appraisal to resale—on a single platform.

What It Means for Dealers

The acquisition introduces several new opportunities for automotive dealers:

Greater Transparency: DealerClub’s reputation-based model brings a level of trust and clarity to the wholesale market that hasn’t been seen before, mirroring Cars Commerce’s success in consumer and dealer reviews.

Efficiency Gains: Dealers can now manage wholesale transactions with minimal risk and streamlined processes, saving time and money.

New Revenue Potential: Cars Commerce’s transactional model, combined with its established subscription business, promises long-term financial benefits for both the company and its dealer partners.

The integration also strengthens Cars Commerce’s position as a technology leader in the automotive space. As the industry moves toward digitization, platforms like DealerClub are becoming essential tools for dealers looking to stay competitive.

What’s Next for Cars Commerce?

While the acquisition is expected to have minimal financial impact in 2025, Cars Commerce sees it as a long-term investment. The company is committed to scaling DealerClub, even if it means short-term costs. Given the proven track record of DealerClub’s founder, Joe Neiman—who previously built ACV Auctions into an industry leader—expectations are high for the platform’s growth and success.

This move highlights Cars Commerce’s broader ambition to be a one-stop shop for all aspects of the car trade, from consumer-facing marketplaces to behind-the-scenes wholesale operations. As dealers continue to navigate challenges like inventory shortages and shifting market demands, Cars Commerce is positioning itself as the partner they can rely on for innovative solutions.

With DealerClub in its portfolio, Cars Commerce is no longer just a leader in the retail automotive space; it’s reshaping the future of wholesale as well.

Key Points: – Over 3.2 million electrified vehicles sold in 2024 – Tesla maintains EV leadership despite market share drop to 49% – Traditional combustion engine sales fall below 80% for first time

The U.S. automotive industry achieved a significant milestone in 2024, with electric and hybrid vehicles reaching 20% of the total market share for the first time, according to new data from Motor Intelligence. This marks a turning point in the evolution of consumer preferences, signaling a transition toward sustainable transportation options. While the shift to electrified vehicles has been slower than expected by some industry analysts, the data confirms that the momentum behind electrification is undeniable.

A total of more than 3.2 million electrified vehicles were sold last year, with hybrid vehicles—including plug-in models—accounting for 1.9 million units, and pure electric vehicles (EVs) making up 1.3 million sales. This surge has driven traditional internal combustion engine vehicles below the 80% market share threshold for the first time in modern automotive history, further emphasizing the growing importance of electrification in the U.S. automotive sector.

Tesla remains the dominant force in the EV market, despite a slight decline in its market share from 55% in 2023 to around 49% in 2024. While this drop may raise some eyebrows, it highlights the expanding competitiveness in the EV space rather than a downturn in Tesla’s performance. In fact, Tesla’s Model Y and Model 3 retained their positions as the bestselling electric vehicles in the U.S., continuing to set the pace for the industry.

The shift in Tesla’s market share also reflects an influx of new competitors entering the EV market. Hyundai Motor Group, including Kia, secured second place with 9.3% of the market, followed by General Motors at 8.7%, Ford at 7.5%, and BMW at 4.1%. This competition is reshaping the investment landscape, with traditional automakers like Ford and GM making aggressive pushes into the EV market, while luxury brands like BMW tap into the demand for high-end electrified models.

The evolving EV market is creating both opportunities and challenges for investors. The increasing competition, driven by both established automakers and new entrants, is a key factor reshaping the investment dynamics within the electric vehicle sector. Companies that are able to secure significant market share in the EV space, such as Tesla, GM, and Hyundai, are well-positioned to capitalize on the ongoing transition. At the same time, investors must remain vigilant to the competitive pressures that could impact individual companies’ performance, especially as the market continues to mature.

The 2024 data shows that the pace of electrification is accelerating, with over 68 mainstream EV models tracked by Cox’s Kelley Blue Book, and 24 of them showing year-over-year sales growth. The number of new models entering the market (17 in 2024) reflects the increasing commitment of manufacturers to the electric vehicle sector. Yet, it also underscores the need for companies to innovate and differentiate themselves in a crowded marketplace.

Looking ahead, the outlook for 2025 is promising. With projections for EV sales to potentially hit 10% of all new vehicle sales, and electrified vehicles (EVs and hybrids) possibly making up 25% of all new cars sold, the industry is poised for continued growth. However, the investment landscape could be impacted by policy changes, such as the potential reconsideration of the $7,500 federal tax credit for EVs under a new administration. Any changes to such incentives could influence future adoption rates and, in turn, investor sentiment in the electric vehicle market.

In conclusion, the electric vehicle market is undergoing a profound transformation, reshaping the U.S. automotive industry and the broader investment landscape. As more consumers make the switch to electrified vehicles and new players enter the market, investors will need to stay informed and strategically assess the opportunities and risks associated with this rapidly evolving sector.