Airline stocks moved sharply lower Monday as oil prices surged above $100 per barrel, raising concerns about rising jet fuel costs and pressure on industry profitability.

Shares of major U.S. carriers fell after crude oil briefly climbed above $110 per barrel, the highest level since 2022. The move followed escalating geopolitical tensions in the Middle East that disrupted shipping traffic through the Strait of Hormuz, one of the world’s most critical oil transit routes.

Delta Air Lines, American Airlines, and United Airlines all declined in early trading before trimming some losses. Domestic-focused carriers including Southwest Airlines, JetBlue Airways, and Alaska Air Group also traded lower as investors weighed the financial impact of higher fuel prices.

Fuel represents one of the largest operating expenses for airlines, typically accounting for roughly one-fifth to one-quarter of total costs. When oil prices climb quickly, airlines often face immediate margin pressure, particularly if ticket prices cannot be adjusted quickly enough to offset the increase.

Jet fuel prices have climbed significantly in recent weeks, rising by as much as $1.75 per gallon. At those levels, the largest U.S. airlines could see quarterly fuel expenses increase by roughly $1.5 billion each if elevated prices persist. Across the three largest carriers, the additional costs could approach $5 billion.

Higher fuel costs often translate into higher ticket prices as airlines attempt to protect margins. Carriers may adjust fares, reduce promotional pricing, or alter route capacity in response to sustained increases in fuel expenses.

The current price spike also highlights the industry’s increased exposure to energy market volatility. Many airlines previously used fuel hedging strategies to limit the impact of oil price swings. Over the past decade, however, most carriers have moved away from large-scale hedging programs after experiencing losses during periods of falling oil prices. Southwest Airlines, long known for its fuel hedging approach, ended its program in 2025.

In addition to rising energy costs, airlines are facing operational disruptions tied to the conflict. Thousands of flights have been grounded globally as airlines reroute aircraft away from affected airspace, leaving travelers stranded and adding complexity to airline scheduling.

European airline stocks also declined amid the developments. Lufthansa shares dropped roughly 5%, while International Consolidated Airlines Group, the parent company of British Airways and Aer Lingus, fell about 3%. Air France-KLM also moved lower during the session.

The latest selloff adds to a difficult year for airline equities. Shares of Delta, American, and United are down roughly 20% to 30% year to date. Domestic carriers such as JetBlue, Southwest, and Alaska Air have also experienced steep declines in recent weeks.

For investors, the move underscores how closely airline performance remains tied to global energy markets. Even with steady travel demand, sudden spikes in oil prices can quickly reshape the profitability outlook for carriers.

If crude oil remains elevated, airlines may continue adjusting pricing strategies and operating plans as they navigate the industry’s most volatile cost variable.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fourth quarter and FY2025 earnings. FreightCar will release its fourth quarter and FY2025 financial results after the market close on Monday, March 9. Management will host an investor teleconference and webinar on Tuesday, March 10, at 11:00 am ET. We expect management to release corporate guidance for FY2026 railcar deliveries, revenue, and adjusted EBITDA. In addition to a market outlook, we think management will discuss its strategy for growing its aftermarket parts business along with its plans to enter the tank car market.

Noble estimates. Our fourth quarter 2025 revenue, EBITDA, and adjusted EPS estimates are $139.9 million, $12.5 million, and $0.18, respectively. For FY2025, we forecast $515.3 million, $46.8 million, and $0.58, respectively. For 2026, our revenue, EBITDA, and EPS estimates are also unchanged at $636.7 million, $59.4 million, and $0.76, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q4 and FY2025 financial results. Fourth quarter net revenue increased 7.7% to $57.4 million compared to $53.3 million during the prior year period. Adjusted EBITDA and EPS were $40.7 million and $4.48, respectively, compared to $32.8 million and $3.33 during the prior year quarter. During the fourth quarter, the average time charter equivalent rate amounted to $30,268 per day compared to $26,479 during the prior year period. The company reported FY2025 adjusted EBITDA and EPS of $155.9 million and $16.74, respectively, compared to $135.8 million and $14.87 in 2024.

Revenue and earnings visibility. For 2026, Euroseas has secured 86.6% of available voyage days at an average rate of ~$30,700 per day and 71.1% of 2027 available voyage days at an average rate of $31,890 per day. For 2028, 40.8% of available voyage days are covered at ~$32,400 per day. This robust charter coverage not only underpins earnings but also provides a strong buffer against rate volatility, positioning the company to benefit from sustained high utilization in 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fourth quarter and full year results. EuroDry reported fourth-quarter net revenues of $17.4 million, exceeding our estimate of $16.5 million, driven by a stronger average TCE rate of $16,262 per day versus our $15,900 estimate and lighter drydocking of 13.7 days against our 22-day assumption. Adjusted EBITDA of $7.5 million and adjusted EPS of $0.88 came in ahead of our estimates of $6.7 million and $0.78, respectively. For the full year, net revenues of $52.3 million, adjusted EBITDA of $12.5 million, and an adjusted net loss of $2.50 per share all modestly surpassed our estimates of $51.4 million, $11.7 million, and a loss of $2.57.

Market update. Dry-bulk fundamentals strengthened in the fourth quarter, with average TCE rates rising to the highest levels in approximately two years. The global order book remains near historically low levels, at approximately 13.4% of the existing fleet, providing structural support. Near-term demand tailwinds include growing bauxite trade from West Africa, continued grain flows following the U.S.–China trade truce, and longer voyage distances due to Red Sea disruptions, though geopolitical uncertainty and tariff-related volatility remain risks.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Tidewater Inc. (NYSE: TDW) is expanding its global offshore footprint with a $500 million all-cash acquisition of Wilson Sons Ultratug Participações S.A. and its affiliate Atlantic Offshore Services S.A. (collectively, “WSUT”). The transaction, which includes the assumption of approximately $261 million in existing debt, significantly scales Tidewater’s presence in Brazil—one of the world’s most active offshore energy markets.

The deal adds 22 platform supply vessels (PSVs) to Tidewater’s fleet. Pro forma for the acquisition, Tidewater will own 213 offshore support vessels (OSVs) and 231 total vessels globally, including crew boats, tug boats, and maintenance vessels.

The most immediate impact is geographic. Tidewater’s fleet in Brazil will expand from six vessels to 28, creating meaningful operating scale in a market widely viewed as structurally attractive due to sustained offshore development activity.

Notably, 19 of WSUT’s 22 PSVs are Brazilian-built. That distinction carries strategic weight. Brazilian-built vessels receive priority in local tenders and also provide access to Brazilian Special Registry (REB) tonnage rights. Through REB, Tidewater may import certain international-flagged vessels into Brazil while enjoying similar status to locally built ships.

In effect, the transaction provides both domestic positioning and optionality for additional fleet deployment.

WSUT brings approximately $441 million in existing backlog. According to Tidewater, many of those contracts are priced at day rates below current market levels, creating potential earnings leverage as contracts roll over.

Assuming a late second-quarter 2026 close, Tidewater expects the acquired business to generate roughly $220 million in revenue over the first twelve months, with gross margins around 58%. Annual G&A expenses are projected at approximately $14 million.

Management also characterized the deal as immediately accretive to 2026 and 2027 estimated earnings and free cash flow per share, though final outcomes will depend on closing timing, integration, and market conditions.

The acquisition will be funded with cash on hand. Tidewater intends to novate WSUT’s existing long-duration amortizing debt, provided by BNDES and Banco do Brasil, preserving what management describes as low-cost financing already embedded in the capital structure.

Following refinancing transactions in 2025 and this acquisition, Tidewater expects pro forma net leverage below 1.0x at closing, assuming a June 30, 2026 completion. A lower leverage profile could provide flexibility for future capital allocation decisions, subject to market conditions.

Brazil’s offshore sector remains one of the largest globally, with sustained activity in deepwater and pre-salt developments. Vessel supply dynamics, local content requirements, and regulatory structures create a market where scale and local tonnage matter.

For investors tracking the offshore services cycle, this transaction underscores a broader theme: operators are positioning for sustained utilization and disciplined fleet growth rather than speculative expansion. Consolidation also remains a key lever for improving operating leverage in a capital-intensive industry.

The transaction has been unanimously approved by Tidewater’s board and is expected to close late in the second quarter of 2026, pending regulatory approvals, including from Brazil’s antitrust authority (CADE).

As the offshore support vessel market continues to recalibrate following years of volatility, Tidewater’s Brazil-focused expansion signals confidence in long-term regional fundamentals—while also highlighting how capital structure discipline is shaping today’s consolidation playbook.

ATHENS, Greece, Feb. 18, 2026 (GLOBE NEWSWIRE) — EuroDry Ltd. (NASDAQ: EDRY, the “Company” or “EuroDry”), an owner and operator of drybulk vessels and provider of seaborne transportation for drybulk cargoes, announced today that it will release its financial results for the fourth quarter ended December 31, 2025, on Thursday, February 19, 2026 after market closes in New York.

On the next day, Friday, February 20, 2026, at 8:00 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

ConferenceCalldetails: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “EuroDry” to the operator and/or conference ID 13758897. Click here for additional participant International Toll-Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

AudioWebcast-SlidesPresentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.eurodry.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the fourth quarter ended December 31, 2025, will also be available in PDF format 10 minutes prior to the conference call and webcast, accessible on the company’s website (www.eurodry.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

About EuroDryLtd. EuroDry Ltd. was formed on January 8, 2018, under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spunoff from Euroseas Ltd on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY.

EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day-to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

The Company has a fleet of 11 vessels, including 3 Panamax drybulk carriers, 5 Ultramax drybulk carriers, 2 Kamsarmax drybulk carriers and 1 Supramax drybulk carrier. EuroDry’s 11 drybulk carriers have a total cargo capacity of 766,420 dwt. After the delivery of two Ultramax vessels in 2027, the Company’s fleet will consist of 13 vessels with a total carrying capacity of 893,420 dwt.

InvestorRelations/FinancialMedia Nicolas Bornozis Markella Kara Capital Link, Inc. 230 Park Avenue, Suite 1540 New York, NY 10169 Tel. (212) 661-7566 E-mail: eurodry@capitallink.com

Seanergy Maritime Holdings Corp. is a prominent pure-play Capesize shipping company listed in the U.S. capital markets. Seanergy provides marine dry bulk transportation services through a modern fleet of Capesize vessels. The Company’s operating fleet consists of 18 vessels (1 Newcastlemax and 17 Capesize) with an average age of approximately 13.4 years and an aggregate cargo carrying capacity of approximately 3,236,212 dwt. Upon completion of the delivery of the previously announced Capesize vessel acquisition, the Company’s operating fleet will consist of 19 vessels (1 Newcastlemax and 18 Capesize) with an aggregate cargo carrying capacity of approximately 3,417,608 dwt. The Company is incorporated in the Marshall Islands and has executive offices in Glyfada, Greece. The Company’s common shares trade on the Nasdaq Capital Market under the symbol “SHIP”.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

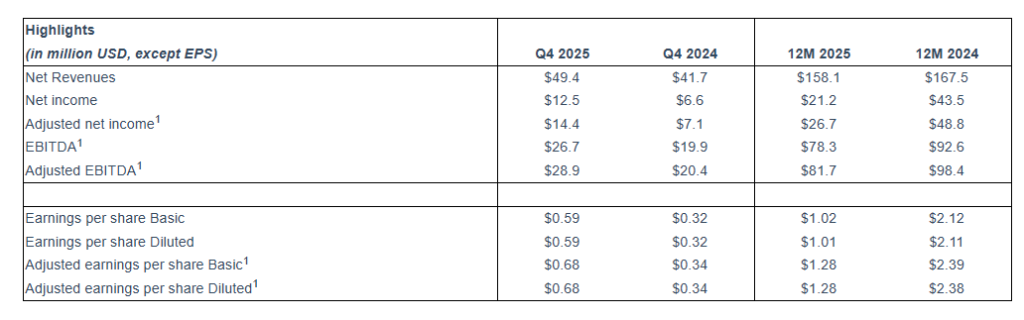

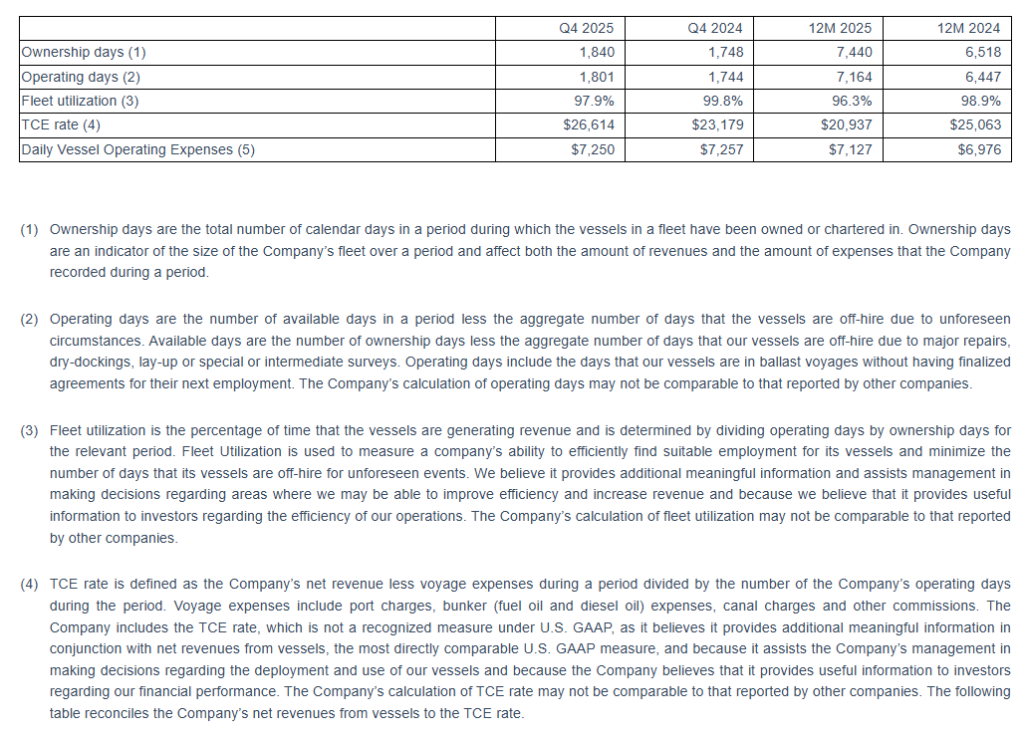

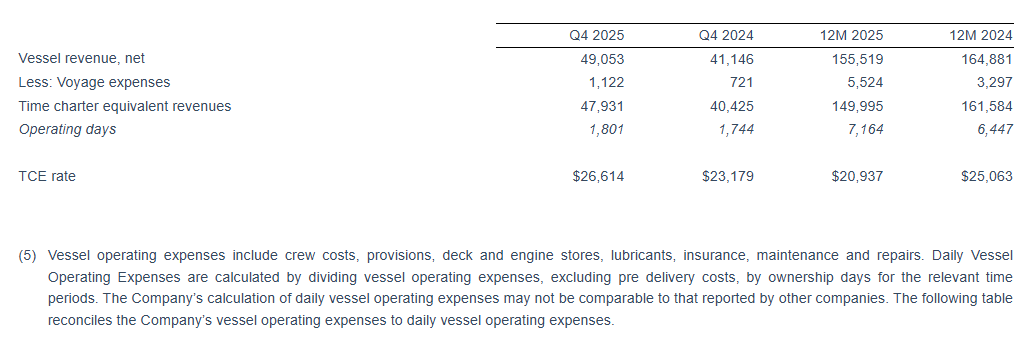

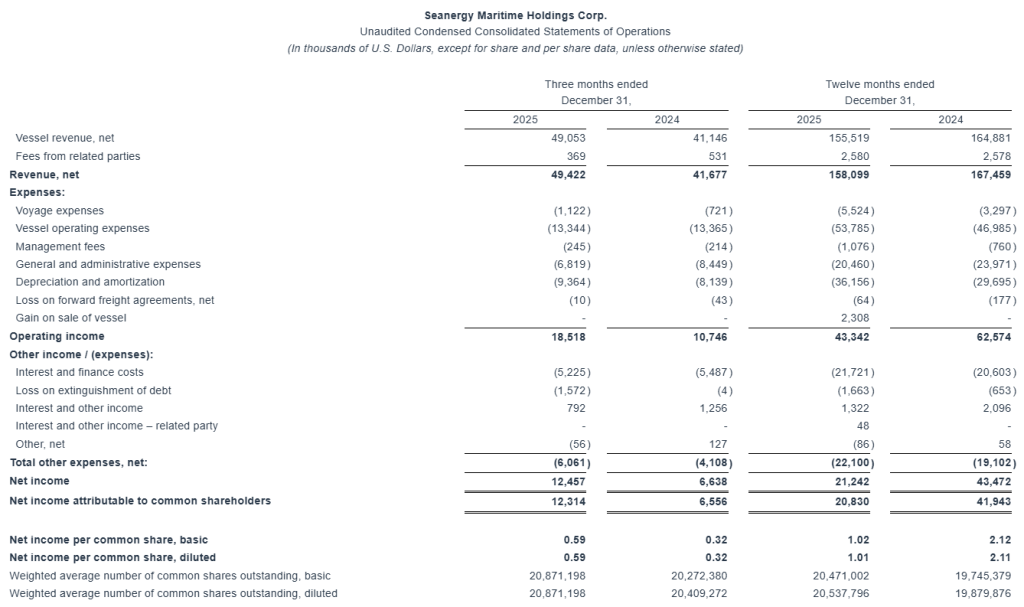

Q4’25 financial results. Seanergy reported Q4 net revenues of $49.4 million and adjusted EBITDA of $28.9 million, exceeding our estimates of $48.3 million and $28.2 million, respectively. Adjusted net income and adjusted EPS were $14.2 million and $0.68, ahead of our $11.7 million and $0.56 estimates. The stronger than expected earnings were due to a higher average time charter equivalent (TCE) rate of $26,614 per day versus our $26,000 estimate.

Favorable Capesize market. The Capesize market is supported by favorable supply and demand fundamentals. The global orderbook stands at roughly 12% of the fleet, while approximately 40% of Capesize, Newcastlemax, and VLOC vessels are over 15 years old, with special surveys expected to reduce effective supply by 1.5% to 2.5% annually. Additionally, Brazilian iron ore exports and West African bauxite shipments continue to expand, with Simandou expected to add incremental long-haul volumes in 2026 and 2027. In our view, this combination of structural supply constraints and steady commodity trade flows supports a constructive rate environment throughout 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Declares $0.20 Per Share Dividend and Expands Prompt Newbuilding Program Totaling $226m

Highlights and Developments:

Fifth consecutive year of profitability, delivering adjusted EPS of $1.28, underscoring the resilience and earnings power of Seanergy’s pure-play Capesize strategy across cycles

Declared a Q4 cash dividend of $0.20 per share and total cash dividends for 2025 of $0.43 per share

The Q4 dividend marks the Company’s 17th consecutive quarterly dividend bringing cumulative distributions to $2.64 per share, or approximately $51.2 million

Expanded the prompt newbuilding program to three eco vessels totaling $226million, securing attractive early delivery positions and enhancing future earnings capacity:

Two scrubber-fitted 181,000 dwt Capesize bulkers with expected deliveries in Q2 and Q3 2027

One scrubber-fitted 211,000 dwt Newcastlemax bulker with expected delivery in Q2 2028

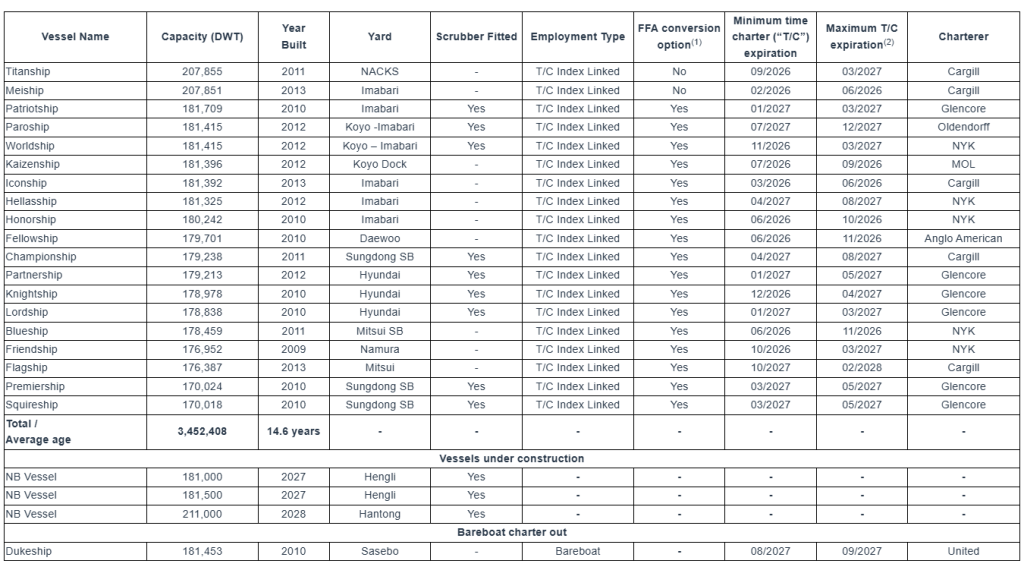

Advanced fleet renewal through the sale of the 2010-built M/V Dukeship at a highly attractive valuation, via an 18-month bareboat charter with purchase obligation, generating positive cash flows and releasing significant liquidity

Completed $123.0 million of refinancings at improved terms, generating $51.9 million of incremental liquidity in Q4 and this year to date

Q1 TCE guidance of $25,2732, representing a 14% premium to the average AV5 Baltic Capesize Index year-to-date

____________________________ 1 Adjusted earnings per share, Adjusted Net Income, EBITDA and Adjusted EBITDA are non-GAAP measures. Please see the reconciliation below of Adjusted earnings per share, Adjusted Net Income, EBITDA and Adjusted EBITDA to net income, the most directly comparable U.S. GAAP measure.

ATHENS, Greece, Feb. 17, 2026 (GLOBE NEWSWIRE) — Seanergy Maritime Holdings Corp. (“Seanergy” or the “Company”) (NASDAQ: SHIP), a leading pure-play Capesize shipping company, today reported its financial results for the fourth quarter and twelve months ended December 31, 2025, and announced a quarterly cash dividend of $0.20 per common share. This represents Seanergy’s 17th consecutive quarterly dividend under its capital return policy, with total cash dividends for 2025 of $0.43 per common share, underscoring the Company’s commitment to disciplined capital allocation and consistent shareholder returns.

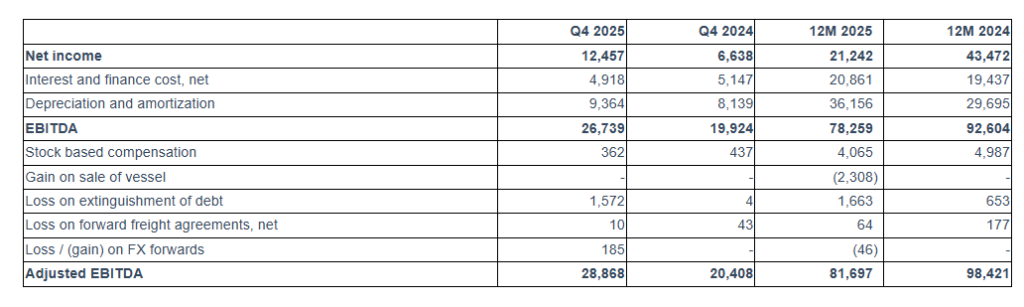

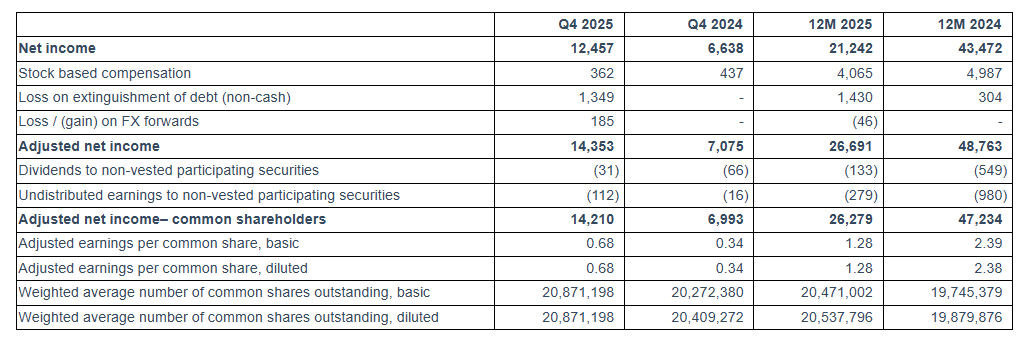

For the quarter ended December 31, 2025, Seanergy generated Net Revenues of $49.4 million, up from $41.7 million in the fourth quarter of 2024. Net Income and Adjusted Net Income for the quarter were $12.5 million and $14.4 million, respectively, compared to Net Income of $6.6 million and Adjusted Net Income of $7.1 million in the fourth quarter of 2024. Adjusted EBITDA for the quarter was $28.9 million, compared to $20.4 million in the same period of 2024. The fleet achieved a daily Time Charter Equivalent (“TCE”) of $26,614 for the fourth quarter of 2025.

For the full year 2025, Seanergy delivered Net Revenues of $158.1 million, compared to $167.5 million in 2024. Net Income and Adjusted Net Income were $21.2 million and $26.7 million, respectively, compared to Net Income of $43.5 million and Adjusted Net Income of $48.8 million in 2024. Adjusted EBITDA for the twelve months was $81.7 million, compared to $98.4 million for 2024. The daily TCE rate of the fleet for 2025 was $20,937, compared to $25,063 in 2024. The average daily OPEX was $7,127 compared to $6,976 in 2024.

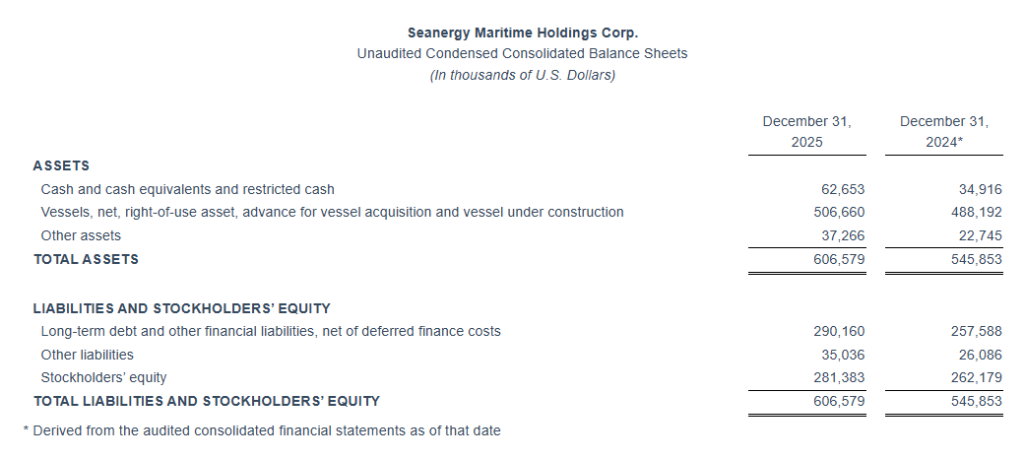

Cash and cash-equivalents and restricted cash, as of December 31, 2025, stood at $62.7 million. Stockholders’ equity at the end of the fourth quarter was $281.4 million. Long-term debt (senior loans and other financial liabilities) net of deferred charges stood at $290.2 million, while the book value of the fleet was $506.7 million, including vessels under construction.

Stamatis Tsantanis, the Company’s Chairman & Chief Executive Officer, stated:

“Driven by a strong Capesize market, Seanergy delivered a very strong fourth quarter, marking our fifth consecutive year of profitability. This performance reflects the durability of our pure-play Capesize strategy, disciplined balance sheet management, and our ability to consistently capture market upside.

“We remain firmly focused on delivering consistent shareholder returns. In 2025, we distributed $0.43 per common share in cash dividends, and with the declaration of the Q4 dividend of $0.20 per common share, we marked our 17th consecutive quarterly dividend. Since launching our dividend program, we have returned $2.64 per common share, or approximately $51.2 million, to our shareholders, underscoring both the strong earnings capacity of our fleet and our disciplined approach to capital allocation.

“Looking ahead, market fundamentals remain constructive as we move into 2026. Robust iron ore and bauxite trade flows, limited Capesize newbuilding supply, and favorable ton-mile dynamics continue to support earnings visibility. With a high-quality fleet, predominantly index-linked employment, and balanced leverage profile, we believe Seanergy is well positioned to capture meaningful upside in this favorable environment.

“Our fleet renewal program is progressing as planned and remains a core strategic priority. In recent months, we added two prompt, eco newbuilding orders at leading Chinese shipyards: a scrubber-fitted Capesize sister vessel to the unit previously announced, scheduled for delivery in Q3 2027, and a scrubber-fitted Newcastlemax scheduled for delivery in Q2 2028. The total current newbuilding investment of approximately $226 million reflects our intention to continue pursuing selective and prompt newbuilding opportunities when market conditions and financing terms are favorably aligned.

“In parallel, and taking advantage of firm secondhand values, we recently agreed to sell the 2010-built Dukeship through an 18-month bareboat arrangement, crystallizing a solid price and generating positive cash flows through the bareboat period. We continue to actively evaluate opportunities to optimize our fleet through selective acquisitions and targeted disposals, while keeping long-term shareholder value and returns as a top priority.

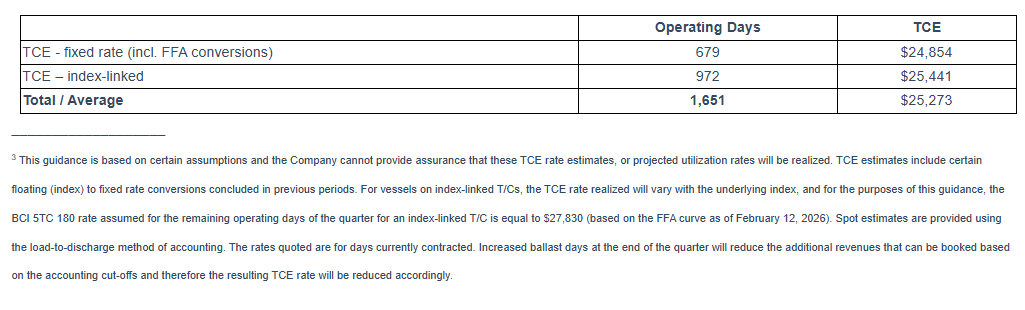

“On the commercial front, we secured index-linked renewals for five vessels, maintaining full participation in a strengthening market while selectively utilizing FFAs to manage volatility. This disciplined approach continues to deliver strong commercial performance. For the first quarter of 2026, we estimate a daily TCE of approximately $25,300, representing a 14% premium to the prevailing AV5 BCI year-to-date, based on the current FFA curve, with approximately 77% of available days fixed at an average rate of $24,739.

“Seanergy enters 2026 from a position of financial strength, operational excellence, and strategic clarity, with a clear path toward continued per-share value creation for our shareholders.”

______________________________ 2 This guidance is based on certain assumptions and the Company cannot provide assurance that these TCE rate estimates, or projected utilization rates will be realized. TCE estimates include certain floating (index) to fixed rate conversions concluded in previous periods. For vessels on index-linked T/Cs, the TCE rate realized will vary with the underlying index, and for the purposes of this guidance, the BCI 5TC 180 rate assumed for the remaining operating days of the quarter for an index-linked T/C is equal to $27,830 (based on the FFA curve as of February 12, 2026). Spot estimates are provided using the load-to-discharge method of accounting. The rates quoted are for days currently contracted. Increased ballast days at the end of the quarter will reduce the additional revenues that can be booked based on the accounting cut-offs and therefore the resulting TCE rate will be reduced accordingly.

Company Fleet:

Fleet Data:

(U.S. Dollars in thousands)

(In thousands of U.S. Dollars, except operating days and TCE rate)

(In thousands of U.S. Dollars, except ownership days and Daily Vessel Operating Expenses)

Net income to EBITDA and Adjusted EBITDA Reconciliation:

(In thousands of U.S. Dollars)

Earnings Before Interest, Taxes, Depreciation and Amortization (“EBITDA”) represents the sum of net income, net interest and finance costs, depreciation and amortization and, if any, income taxes during a period. EBITDA and Adjusted EBITDA are not recognized measurements under U.S. GAAP. Adjusted EBITDA represents EBITDA adjusted to exclude stock-based compensation, gain on sale of vessel, loss on forward freight agreements, net, loss on extinguishment of debt, and loss / (gain) on FX forwards (“Other, net” in statement of operations), which the Company believes are not indicative of the ongoing performance of its core operations.

EBITDA and adjusted EBITDA are presented as we believe that these measures are useful to investors as a widely used means of evaluating operating profitability. Management also uses these non-GAAP financial measures in making financial, operating and planning decisions and in evaluating the Company’s performance. EBITDA and adjusted EBITDA as presented here may not be comparable to similarly titled measures presented by other companies. These non-GAAP measures should not be considered in isolation from, as a substitute for, or superior to, financial measures prepared in accordance with U.S. GAAP.

Adjusted Net Income Reconciliation and calculation of Adjusted Earnings Per Share

(In thousands of U.S. Dollars, except for share and per share data)

To derive Adjusted Earnings Per Share, a non-GAAP financial measure, from Net Income, we adjust for dividends and undistributed earnings to non-vested participating securities and exclude non-cash items, as provided in the table above. We believe that Adjusted Net Income and Adjusted Earnings Per Share assist our management and investors by increasing the comparability of our performance from period to period since each such measure eliminates the effects of such non-cash items as loss on extinguishment of debt, stock based compensation, loss / (gain) on FX forwards and other items which may vary from year to year, for reasons unrelated to overall operating performance. In addition, we believe that the presentation of the respective measure provides investors with supplemental data relating to our results of operations, and therefore, with a more complete understanding of factors affecting our business than with GAAP measures alone. Our method of computing Adjusted Net Income and Adjusted Earnings Per Share may not necessarily be comparable to other similarly titled captions of other companies due to differences in methods of calculation.

First Quarter 2026 TCE Rate Guidance:

As of the date hereof, approximately 77% of the Company fleet’s expected operating days in the first quarter of 2026 have been fixed at an estimated TCE rate of approximately $24,739. Assuming that for the remaining operating days of our index-linked time charters, the BCI 5TC 180 rate will be equal to $27,830 (based on the FFA curve as of February 12, 2026), our estimated TCE rate for the first quarter of 2026 will be approximately $25,2733. The following table provides the breakdown of index-linked charters and fixed-rate charters in the first quarter of 2026:

Fourth Quarter and Recent Developments:

Dividend Distribution for Q3 2025 and Declaration of Q4 2025 Dividend

On January 9, 2026, the Company paid a quarterly cash dividend of $0.13 per common share for the third quarter of 2025 to all shareholders of record as of December 29, 2025.

The Company has declared a quarterly cash dividend of $0.20 per common share for the fourth quarter of 2025 payable on or about April 10, 2026, to all shareholders of record as of March 27, 2026.

Fleet Updates

Newbuilding Contract for a Newcastlemax Vessel at Hantong Shipyard

In November 2025, the Company entered into an agreement for the acquisition of a newbuilding 211,000 dwt scrubber-fitted Newcastlemax vessel from Jiangsu Hantong Ship Heavy Industry Co., Ltd., with delivery expected in the second quarter of 2028. The purchase price is approximately $75.8 million. The first installment, representing 15% of the purchase price, has already been paid. The remaining installments are linked to the vessel’s construction milestones, with 30% of the purchase price payable over the next 2 years and the remaining 55% upon delivery of the vessel.

The new vessel will be built incorporating the latest technological advancements and eco-friendly design features, resulting in enhanced fuel efficiency and reduced emissions in line with the Company’s ongoing fleet renewal and decarbonization strategy.

Newbuilding Contract for a Second Capesize Vessel at Hengli Shipyard

In January 2026, the Company entered into an agreement with Hengli Shipbuilding (Dalian) Co., Ltd. and Hengli Shipbuilding (Singapore) Pte. Ltd. for the construction of a 181,500 dwt scrubber-fitted Capesize vessel. The contract price is approximately $75.2 million, with delivery expected in the third quarter of 2027. The purchase price will be paid in five installments, linked to the vessel’s construction milestones, with 45% of the purchase price payable over the next 14 months and the remaining 55% upon delivery of the vessel.

The new vessel will be built incorporating the latest technological advancements and eco-friendly design features, resulting in enhanced fuel efficiency and reduced emissions in line with the Company’s ongoing fleet renewal and decarbonization strategy.

M/V Dukeship – Disposal of Vessel through Bareboat Charter

In February 2026, the Company entered into an agreement with United Maritime Corporation (“United”), a related party, for the disposal of the M/V Dukeship through an 18-month bareboat charter. The charter period commenced following the delivery of the vessel on February 12, 2026. United has advanced a downpayment of $5.5 million and will pay a daily charter rate of $9,450, with a purchase obligation of $22.1 million at the end of the bareboat charter. A special committee of disinterested members of our Board of Directors negotiated the terms and approved the agreement.

Commercial Updates

M/V Flagship – New T/C agreement

In December 2025, the M/V Flagship commenced a new T/C agreement with Cargill International SA with the agreement set to terminate between November 1, 2027 to February 1, 2028, each date subject to (+/- 15 days). The daily hire is based on the 5 T/C routes of the BCI, with an option for the Company to fix the rate for 3 to 9 months based on the prevailing Capesize FFA curve.

M/V Paroship – New T/C agreement

In December 2025, the M/V Paroship commenced a new T/C agreement with Oldendorff GMBH & CO. KG., Ltd for a period of about 20 to about 24 months. The daily hire is based on the 5 T/C routes of the BCI, with an option for the Company to fix the rate for 3 to 9 months based on the prevailing Capesize FFA curve. The Company will also receive most of the benefit from the scrubber profit-sharing scheme.

M/V Friendship – New T/C agreement

In January 2026, the M/V Friendship commenced a new T/C agreement with Glencore Freight Pte. Ltd (“Glencore”) for a period of about 10 to about 14 months. The daily hire is based on the 5 T/C routes of the BCI, with an option for the Company to fix the rate for 1 to 9 months based on the prevailing Capesize FFA curve.

M/V Partnership – New T/C agreement

In February 2026, the M/V Partnership commenced a new T/C agreement with Glencore for a period of about 12 to about 15 months. The daily hire is based on the 5 T/C routes of the BCI, with an option for the Company to fix the rate for 1 to 9 months based on the prevailing Capesize FFA curve. The Company will also receive most of the benefit from the scrubber profit-sharing scheme.

M/V Lordship – Time charter extension

In January 2026, the charterer of the M/V Lordship agreed to extend the time charter agreement in direct continuation from the previous agreement. The extension period will commence on August 21, 2026, for a duration of minimum January 1st, 2027 until maximum March 31st, 2027. The Company receives most of the benefit from the scrubber profit-sharing scheme while the daily hire will be based on a revised premium over the BCI.

M/V Hellasship – Time charter extension

In February 2026, the charterer of the M/V Hellasship agreed to extend the time charter agreement in direct continuation from the previous agreement. The extension period will commence on April 9, 2026, for a duration of minimum 12 to maximum 16 months. The daily hire is based on a revised premium over the BCI, while all other main terms of the time charter remain materially the same.

In December 2025, the Company entered into a new sustainability linked loan facility with Danish Ship Finance secured by the M/Vs Fellowship, Premiership, Championship and Flagship to refinance the sale and leaseback agreement for the M/V Flagship and to increase the existing indebtedness of the other three vessels.

The facility includes a new tranche of $16.8 million secured by the M/V Flagship, with a five-year term. The principal is repayable in 20 quarterly installments of $0.8 million each and a balloon of $1.8 million payable together with the final installment. The interest rate is 2.10% plus 3-month Term SOFR and can fluctuate by 0.05% based on certain emission reduction thresholds.

The additional top-up tranche of $7.3 million, secured by the M/Vs Fellowship, Premiership & Championship, has a three-and-a-half year term and is repayable in 14 quarterly payments of $0.5 million resulting in zero outstanding balance at maturity. The interest rate is 1.95% plus 3-month Term SOFR and can fluctuate by 0.05% based on certain emission reduction thresholds.

M/Vs Hellasship, Patriotship, Iconship & Newbuilding Capesize vessel – Huarong Sale and Leaseback agreements

In December 2025, the Company entered into three separate sale and leaseback agreements totaling $72.5 million for the M/Vs Hellasship, Patriotship & Iconship with entities affiliated with China Huarong Financial Leasing Co., Ltd. The proceeds were used to refinance the outstanding indebtedness of the respective vessels under three sale and leaseback agreements with AVIC International Leasing Co., Ltd. On January 8, 2026, the vessels were sold and chartered back on a bareboat basis for a period of 81 months. The Company has continuous options to purchase the vessels at predetermined prices, starting one year after the commencement date and a purchase obligation at expiry date of each charter. The charterhire principal for the three agreements amortizes in 27 quarterly installments of $2.0 million along with the aggregate purchase obligations of $18.3 million at the expiry of the bareboat charters. Each financing bears interest at a rate of 3-month Term SOFR plus 2.00% per annum, 55 bps lower than the rate of the refinanced agreements. The sale and leaseback agreements do not include any financial covenants or security value maintenance provisions.

Regarding the upcoming delivery of our newbuilding Capesize vessel previously announced, the Company has agreed to enter into a sale and leaseback agreement of $56.3 million to partially finance its acquisition with an entity affiliated with China Huarong Financial Leasing Co., Ltd., which will also provide pre-delivery financing for certain installments under the shipbuilding contract. Upon delivery, the vessel will be sold and chartered back for a period of 60 months. The Company will have continuous purchase options at predetermined prices, commencing one year after the charter commencement date and a purchase obligation at the expiry date. The charterhire principal amortizes in 20 quarterly installments of $0.6 million along with a purchase obligation of $43.5 million at the expiry of the bareboat charter. The financing will bear interest at a rate of 3-month Term SOFR plus 1.80% per annum, while pre-delivery financing amounts will accrue interest payable quarterly in arrears. The sale and leaseback agreement will not include any financial covenants or security value maintenance provisions.

M/V Partnership and Newbuilding Newcastlemax vessel – BOCL Sale and Leaseback agreement

The Company is in the process of finalizing a $26.5 million sale and leaseback agreement for the M/V Partnership with an affiliate of BOC Financial Leasing Corporation Limited to refinance the outstanding indebtedness of the respective vessel under the sale and leaseback agreement with Chugoku Bank, Ltd. The agreement will become effective upon the delivery of the M/V Partnership to the lessor which is expected in March 2026. The Company will sell and charter back the vessel on a bareboat basis for a period of 78 months and will have continuous options to repurchase the vessel at any time following the second anniversary of the delivery at predetermined prices as set forth in the agreement. The charterhire principal will amortize in 26 quarterly installments of $0.8 million along with a purchase option of $6.3 million at the expiry of the bareboat charter. The financing will bear an interest rate of 3-month Term SOFR plus 1.85% per annum, 105 bps lower than the rate of the refinanced agreement. The sale and leaseback agreement will not include any financial covenants or security value maintenance provisions.

Regarding the upcoming delivery of our newbuilding Newcastlemax vessel described above, the Company has agreed to enter into a sale and leaseback agreement of $57.8 million to partially finance its acquisition. The lessor will be an affiliate of BOC Financial Leasing Corporation Limited, which will also provide pre-delivery financing for certain installments under the shipsales contract. Upon delivery, the vessel will be sold and chartered back for a period of 96 months. The Company will have continuous purchase options at predetermined prices as set forth in the agreement, commencing two years after the charter commencement date. The charterhire principal will amortize in 32 quarterly installments of $0.7 million along with a purchase option of $36.3 million at the expiry of the bareboat charter. The financing will bear interest at a rate of 3-month Term SOFR plus 1.85% per annum, while pre-delivery financing amounts will accrue interest payable quarterly in arrears. The sale and leaseback agreement will not include any financial covenants or security value maintenance provisions.

Conference Call:

The Company’s management will host a conference call to discuss financial results on February 17, 2026, at 10:00 a.m. Eastern Time.

Audio Webcast and Earnings Presentation:

There will be a live, and then archived, webcast of the conference call and accompanying presentation available through the Company’s website. To access the presentation and listen to the archived audio file, visit our website, following the Webcast & Presentations section under our Investor Relations page. Participants to the live webcast should register on Seanergy’s website approximately 10 minutes prior to the start of the webcast, following this link.

Conference Call Details:

Participants have the option to register for the call using the following link. You can use any number from the list or add your phone number and let the system call you right away.

About Seanergy Maritime Holdings Corp.

Seanergy Maritime Holdings Corp. is a prominent pure-play Capesize shipping company publicly listed in the U.S. Seanergy provides marine dry bulk transportation services through a modern fleet of Capesize vessels. The Company’s operating fleet consists of 19 vessels (2 Newcastlemax and 17 Capesize) with an average age of approximately 14.6 years and an aggregate cargo carrying capacity of 3,452,408 dwt. Upon the delivery of the newbuilding vessels, the Company’s operating fleet will consist of 22 vessels (3 Newcastlemax and 19 Capesize), with an aggregate cargo carrying capacity of 4,025,908 dwt. Additionally, the Company owns one Capesize vessel that has been chartered out on a bareboat basis.

The Company is incorporated in the Republic of the Marshall Islands and has executive offices in Glyfada, Greece. The Company’s common shares trade on the Nasdaq Capital Market under the symbol “SHIP”.

This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events, including with respect to declaration of dividends, market trends and shareholder returns. Words such as “may”, “should”, “expects”, “intends”, “plans”, “believes”, “anticipates”, “hopes”, “estimates” and variations of such words and similar expressions are intended to identify forward-looking statements. These statements involve known and unknown risks and are based upon a number of assumptions and estimates, which are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to, the Company’s operating or financial results; the Company’s liquidity, including its ability to service its indebtedness; competitive factors in the market in which the Company operates; shipping industry trends, including charter rates, vessel values and factors affecting vessel supply and demand; future, pending or recent acquisitions and dispositions, business strategy, impacts of litigation, areas of possible expansion or contraction, and expected capital spending or operating expenses; risks associated with operations outside the United States; risks arising from trade disputes between the U.S. and China, including the re-imposition of reciprocal port fees; broader market impacts arising from trade disputes or war (or threatened war) or international hostilities, such as between the U.S. and Venezuela, Israel and Hamas or Iran, China and Taiwan and Russia and Ukraine; risks associated with the length and severity of pandemics; and other factors listed from time to time in the Company’s filings with the SEC, including its most recent annual report on Form 20-F. The Company’s filings can be obtained free of charge on the SEC’s website at www.sec.gov. Except to the extent required by law, the Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

On The Board. Commercial Vehicle Group has added Ari Levy of Lakeview Investment Group as an independent director. Lakeview owns approximately 8.9% of the outstanding shares of the Company. In connection with Mr. Levy’s appointment, the Board was expanded to 7 members. Mr. Levy will serve on the Board’s Nominating, Governance and Sustainability, and Audit Committees.

Ari Levy. Mr. Levy is the founder, President, and Chief Investment Officer of Lakeview, a Chicago based investment manager focused on the public markets. Mr. Levy was the President of Levy Acquisition Corp, a NASDAQ listed acquisition vehicle, and subsequently served on the Board of the resulting public company, Del Taco, until it was acquired by Jack in the Box in early 2022.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Earnings Release: Tuesday, February 17, 2026, Before Market Open in New York Conference Call and Webcast: Tuesday, February 17, 2026, at 10:00 a.m. Eastern Time

GLYFADA, Greece, Feb. 12, 2026 (GLOBE NEWSWIRE) — Seanergy Maritime Holdings Corp. (the “Company” or “Seanergy”) (NASDAQ: SHIP) announced today that it will release its financial results for the fourth quarter and year ended December 31, 2025, prior to the open of the market in New York on Tuesday, February 17, 2026.

Seanergy’s senior management will conduct a conference call and simultaneous Internet webcast to review these results on Tuesday, February 17, 2026, at 10:00 a.m. Eastern Time.

Audio Webcast and Earnings Presentation: There will be a live, and then archived, webcast of the conference call and accompanying slides available through the Company’s website. To access the slides and listen to the archived audio file, visit our website, following the Webcast & Presentations section under our Investor Relations page. Participants to the live webcast should register on Seanergy’s website approximately 10 minutes prior to the start of the webcast, by following this link.

Conference Call Details: Participants have the option to register for the call using the following link. You can use any number from the list or add your phone number and let the system call you right away.

About Seanergy Maritime Holdings Corp. Seanergy Maritime Holdings Corp. is a prominent pure-play Capesize shipping company publicly listed in the U.S. Seanergy provides marine dry bulk transportation services through a modern fleet of Capesize vessels. The Company’s operating fleet consists of 20 vessels (2 Newcastlemax and 18 Capesize) with an average age of approximately 14.6 years and an aggregate cargo carrying capacity of approximately 3,633,861 dwt.

The Company is incorporated in the Republic of the Marshall Islands and has executive offices in Glyfada, Greece. The Company’s common shares trade on the Nasdaq Capital Market under the symbol “SHIP”.

Forward-Looking Statements This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events, including with respect to declaration of dividends, market trends and shareholder returns. Words such as “may”, “should”, “expects”, “intends”, “plans”, “believes”, “anticipates”, “hopes”, “estimates” and variations of such words and similar expressions are intended to identify forward-looking statements. These statements involve known and unknown risks and are based upon a number of assumptions and estimates, which are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to, the Company’s operating or financial results; the Company’s liquidity, including its ability to service its indebtedness; competitive factors in the market in which the Company operates; shipping industry trends, including charter rates, vessel values and factors affecting vessel supply and demand; future, pending or recent acquisitions and dispositions, business strategy, impacts of litigation, areas of possible expansion or contraction, and expected capital spending or operating expenses; risks associated with operations outside the United States; broader market impacts arising from trade disputes or war (or threatened war) or international hostilities, such as between Israel and Hamas or Iran, China and Taiwan and between Russia and Ukraine; risks associated with the length and severity of pandemics, including their effects on demand for dry bulk products and the transportation thereof; and other factors listed from time to time in the Company’s filings with the SEC, including its most recent annual report on Form 20-F. The Company’s filings can be obtained free of charge on the SEC’s website at www.sec.gov. Except to the extent required by law, the Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

For further information please contact: Seanergy Investor Relations Tel: +30 213 0181 522 E-mail: ir@seanergy.gr

Capital Link, Inc. Paul Lampoutis 230 Park Avenue Suite 1540 New York, NY 10169 Tel: (212) 661-7566 Email: seanergy@capitallink.com

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New time charter for the EM Spetses. Euroseas Ltd. announced a new time charter for its 1,740 twenty-foot equivalent feeder containership, EM Spetses, for a minimum period of 22 to a maximum period of 24 months, at the option of the charterer, at a gross daily rate of $21,500. The new charter will commence on April 12, 2026, in direct continuation of its present charter, and represents a daily increase of over $3,000 compared to the vessel’s current rate.

Incremental EBITDA with Expanded Coverage. The charter is expected to generate approximately $8.9 million in EBITDA over the minimum term and increase Euroseas’ charter coverage to approximately 87% in 2026, 71% in 2027, and 41% in 2028. The higher rate on the new time charter reflects a tight container market with limited vessel availability. Demand in the feeder segment remains strong as operators secure vessels to meet their requirements.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Increasing FY 2026 estimates. We have increased our FY 2026 revenue, adjusted EBITDA, and adjusted EPS estimates to $60.8 million, $25.5 million, and $2.82, respectively, from $57.3 million, $22.4 million, and $1.46. The upward revisions are driven by higher expected vessel earnings, with our forecast average TCE rate rising to $14,743 from $13,873 previously.

Eurodry’s sweet spot. Eurodry owns and operates vessels in the middle of the size range of dry bulk carriers, or 50,000 to 85,000 dead weight tons (dwt), which present the most flexible employment opportunities. EDRY’s fleet consists of 11 vessels with a total carrying capacity of 766,420 dwt. With two Ultramax vessels of 63,500 dwt each under construction and scheduled for delivery in the second and third quarters of 2027, the total carrying capacity will increase to 893,000 dwt. Growth will be driven by the charter rate environment, coupled with fleet growth. While EDRY continues to renew and modernize its fleet, it expects to acquire and consolidate smaller owners.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ATHENS, Greece, Feb. 11, 2026 (GLOBE NEWSWIRE) — Euroseas Ltd. (NASDAQ: ESEA, the “Company” or “Euroseas”), an owner and operator of container carrier vessels and provider of seaborne transportation for containerized cargoes, announced today a new time charter contract for its 2007-built 1,740 teu feeder containership, EM Spetses, for a minimum period of 22 to a maximum period of 24 months, at the option of the charterer, at a gross daily rate of $21,500. The new charter period will commence on April 12, 2026, in direct continuation of its present charter, and represents a daily increase of over $3,000 over the vessel’s current rate.

Aristides Pittas, Chairman and CEO of Euroseas, commented: “We are very pleased to that we have extended the time charter contract for our 2007-built EM Spetses with a top-class charterer, in direct continuation of its present charter, for 22-24 months at a profitable rate of $21,500. This fixture highlights that despite the upcoming Lunar New Year holidays, activity across the feeder segment remains firm, as operators move to secure their requirements amid a tight container chartering market with very limited tonnage availability. The charter is expected to generate about $8.9 million of EBITDA over the minimum contracted period and increases our charter coverage for 2026, 2027, and 2028 to about 87%, 71% and 41% respectively.”

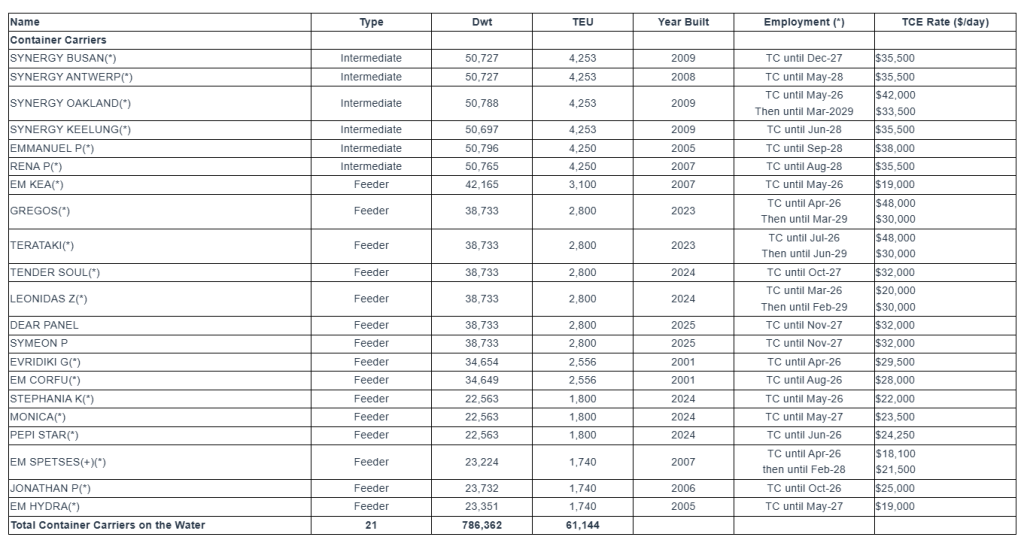

Fleet Profile: The Euroseas Ltd. fleet profile is currently as follows:

Notes: (*)TC denotes time charter. Charter duration indicates the earliest redelivery date; all dates listed are the earliest redelivery dates under each TC unless the contract rate is lower than the current market rate in which cases the latest redelivery date is assumed; vessels with the latest redelivery date shown are marked by (+). (**) The charterer has the option until Nov-2026 to extend the charters by one year with the rate for the five-year period becoming $32,500/day.

About Euroseas Ltd.

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 150 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA.

Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

The Company has a fleet of 21 vessels, including 15 Feeder containerships and 6 Intermediate containerships with a cargo capacity of 61,144 teu. After the delivery of four intermediate containership newbuildings in 2027 and 2028, respectively, Euroseas’ fleet will consist of 25 vessels with a total carrying capacity of 79,080 teu.

Forward Looking Statement

This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events and the Company’s growth strategy and measures to implement such strategy; including expected vessel acquisitions and entering into further time charters. Words such as “expects,” “intends,” “plans,” “believes,” “anticipates,” “hopes,” “estimates,” and variations of such words and similar expressions are intended to identify forward-looking statements. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates that are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to changes in the demand for containerships, competitive factors in the market in which the Company operates; risks associated with operations outside the United States; and other factors listed from time to time in the Company’s filings with the Securities and Exchange Commission. The Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.