Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

George Proost, Research Intern, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating Estimates. We made modest adjustments to our Q2 and full-year 2026 estimates. We now project Q2 revenue of $111.9 million, adjusted EBITDA of $5.9 million, and EPS of $0.01, respectively, compared to our prior estimates of $100.9 million, $7.2 million, and $0.04. While our 2026 delivery estimate remains unchanged at 4,100 units, we pulled forward 100 units from the third quarter into the second quarter. We lowered our margin expectations in the second quarter due to product mix. Our full-year revenue, EBITDA, and EPS estimates are $509.0 million, $46.5 million, and $0.46, respectively, compared to previous estimates of $510.0 million, $41.8 million, and $0.48. We expect a strong second half.

Near-Term Outlook. The value of RAIL’s Q1 2026 backlog increased 13.5% sequentially to approximately $156 million based on 2,058 railcars. We think the company’s order activity has accelerated as customers have started to place orders following a period of deferment. A growing backlog provides revenue visibility for the next several quarters. Corporate 2026 guidance suggests railcar deliveries in the range of 4,000 to 4,500, revenue in the range of $500 to $550 million, and adjusted EBITDA of $41 to $50 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First quarter 2026 Financial Results. For the first quarter of 2026,Seanergy reported net revenues of $42.9 million, up 77% from $24.2 million in the prior-year period, driven by significantly stronger charter rates and improved fleet performance. EBITDA increased to $23.6 million from $6.6 million, while adjusted EBITDA rose to $28.1 million from $8.0 million. The company generated net income of $9.7 million, or $0.45 per diluted share, compared to a net loss of $6.8 million, or $0.34 per diluted share, in the first quarter of 2025. Adjusted net income totaled $13.4 million, or $0.63 per diluted share, versus an adjusted net loss of $5.5 million, or $0.27 per share, in the prior-year quarter.

Updating Estimates. We have increased our 2026 revenue, EBITDA, and EPS estimates to $198.3 million, $130.2 million, and $3.45, respectively, from $182.1 million, $106.7 million, and $2.40. The increase in our estimates reflects higher time charter equivalent rates. The company has 83% of its fleet expected operating days during the second quarter fixed at an estimated TCE rate of $29,725. During the first quarter, Seanergy earned an average fleet time charter equivalent rate of approximately $24,219 per day.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First quarter financial results. Euroseas Ltd. reported solid first-quarter 2026 financial performance supported by elevated charter rates, full fleet utilization, and disciplined cost management. Although net revenues declined slightly to $55.8 million from $56.3 million in the prior year period due to a smaller average fleet size, adjusted EBITDA increased to $40.9 million from $37.1 million, and adjusted earnings per share rose to $4.70 from $3.76. The Company also maintained a strong balance sheet with substantial liquidity, moderate leverage, and approximately $650 million in contracted revenue backlog, providing significant visibility into future cash flow generation.

Outlook remains favorable. In our view, the outlook for the feeder and intermediate containership segments remains favorable through the remainder of 2026 based on constrained vessel supply, high fleet utilization, and ongoing supply chain disruptions. However, growing macro and geopolitical risks, including slowing global growth, evolving trade policies, and Middle East tensions, could temper containerized trade growth in 2027. Euroseas’ strong charter coverage of 92.4% in 2026, 75.9% in 2027, and 43.1% in 2028 is expected to insulate the company from any volatility in the market.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

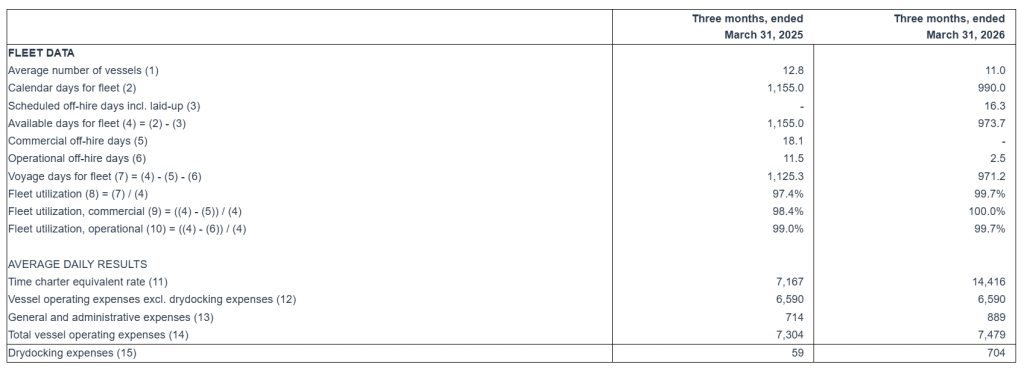

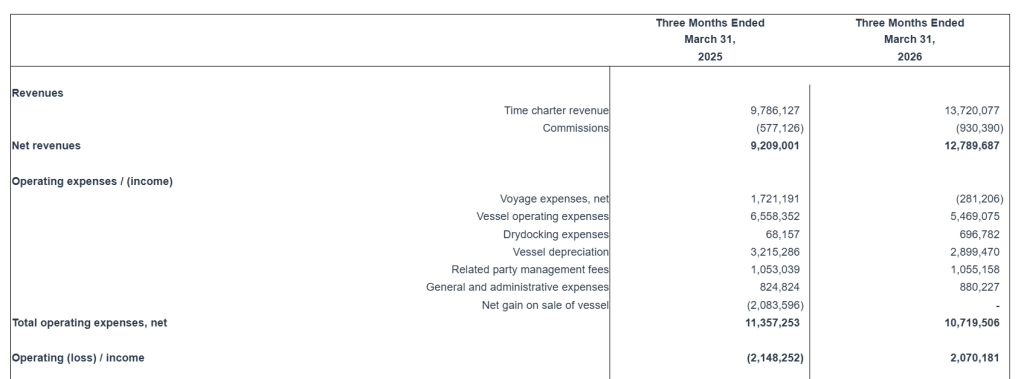

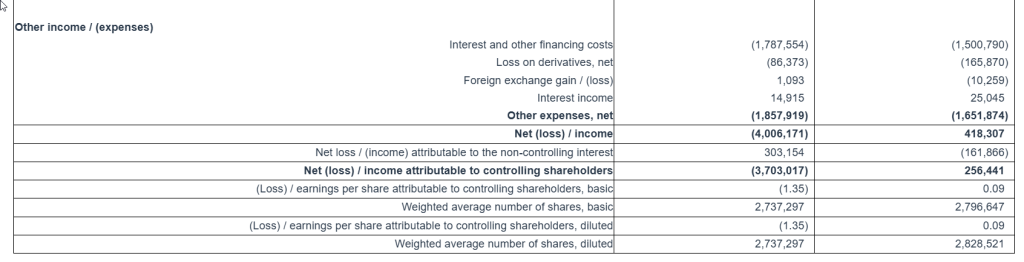

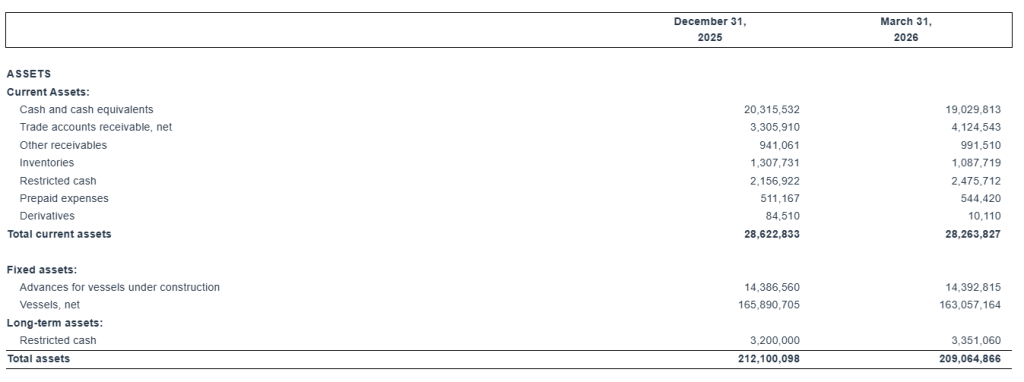

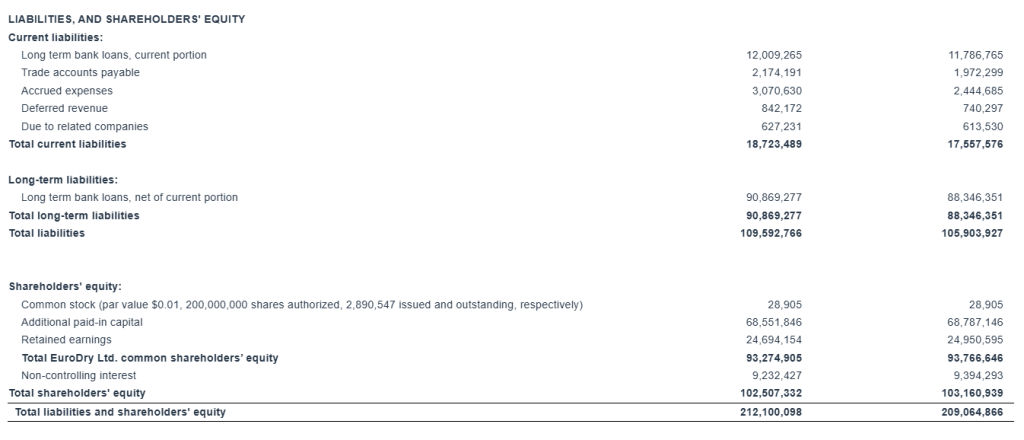

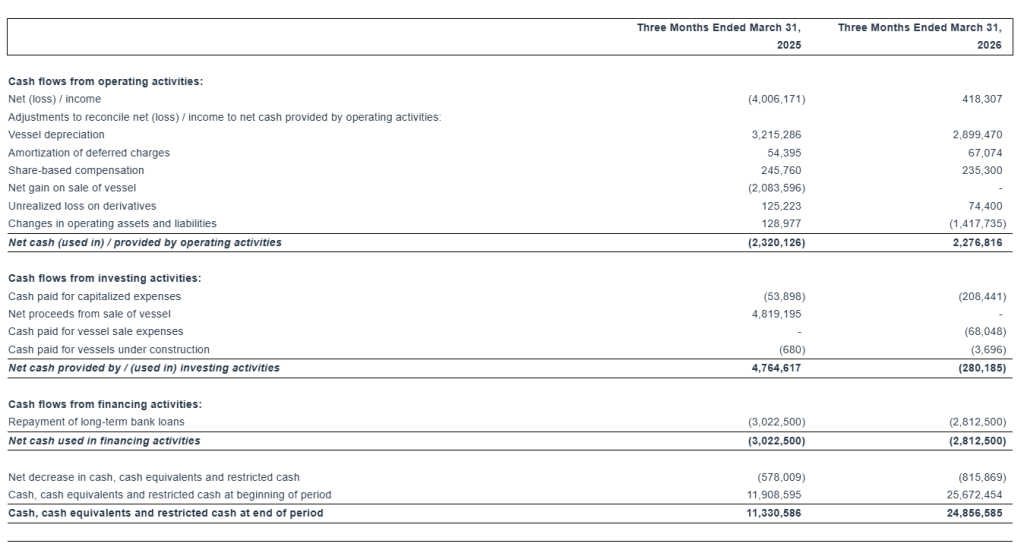

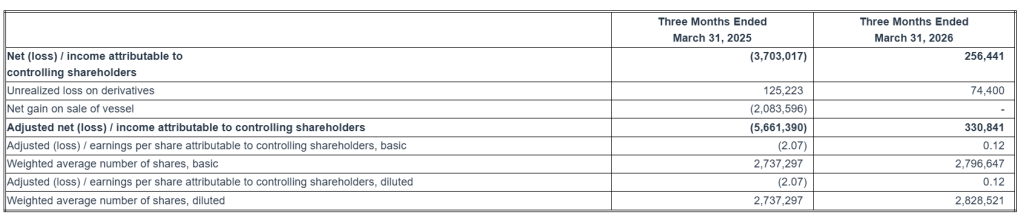

1Q 2026 Financial Results. EuroDry Ltd. reported an improvement in 1Q 2026 financial performance compared to the prior year period, driven primarily by stronger dry bulk charter markets and improved fleet utilization. Total net revenues increased 38.9% year-over-year to $12.8 million, while average time charter equivalent rates more than doubled to $14,416 per day from $7,167 per day during the prior year period. Adjusted net income attributable to controlling shareholders amounted to $330.8 thousand, or $0.12 per share, compared to a net loss of $5.7 million, or $(2.07) per share, in the prior year period. Adjusted EBITDA increased to $4.9 million compared to a loss of $1.0 million during the prior year period, reflecting strong operating leverage as freight rates recovered.

Strong Operational Quarter. Fleet utilization improved to 99.7%, with commercial utilization at 100%, reflecting minimal downtime and effective charter execution. Vessel operating expenses declined year-over-year due to a smaller average fleet size, while daily operating costs remained stable despite inflation. Meanwhile, dry bulk market conditions strengthened in April and May 2026, with one-year Ultramax and Kamsarmax charter rates nearing or surpassing $20,000 per day, supporting improved earnings prospects for the coming quarters.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ATHENS, Greece, May 21, 2026 (GLOBE NEWSWIRE) — Euroseas Ltd. (NASDAQ: ESEA, the “Company” or “Euroseas”), an owner and operator of container carrier vessels and provider of seaborne transportation for containerized cargoes, announced today its results for the three-month period ended March 31, 2026 and declared a common stock dividend.

First Quarter 2026 Financial Highlights:

Total net revenues of $55.8 million. Net income of $32.5 million or $4.67 and $4.65 earnings per share basic and diluted, respectively. Adjusted net income1 for the period was $32.9 million or $4.72 and $4.70 per share basic and diluted, respectively.

Adjusted EBITDA1 was $40.9 million.

An average of 21.0 vessels were owned and operated during the first quarter of 2026 earning an average time charter equivalent rate of $30,354 per day.

Declared a quarterly dividend of $0.80 per share for the first quarter of 2026 payable on or about June 16, 2026 to shareholders of record on June 9, 2026, as part of the Company’s common stock dividend plan.

As of May 21, 2026 we had repurchased 480,460 of our common stock in the open market, representing about 6.8% of the outstanding shares, for a total of about $11.36 million, under the share repurchase plan of up to $20 million announced in May 2022. The Board approved the continuation of the share repurchase plan for a further year in May 2026 and will review it again after a period of twelve months

Recent developments:

On May 4, 2026, Euroseas formed a joint venture with a group of investors represented by NRP Project Finance AS (“NRP Investors”) in relation to the ownership of the third 4,484 TEU vessel in the series of four 4,484 TEU vessels announced on August 25, 2025. The vessel, M/V Thrylos, is expected to be delivered in the first quarter of 2028 Under the terms of the transaction, the NRP Investors will acquire a 49% ownership interest in the vessel for total consideration of approximately $12.2 million, including certain transaction structuring costs, with the assumption that the vessel will be financed with at least 60% of debt.

________________ 1 Adjusted EBITDA, Adjusted net income and Adjusted earnings per share are not recognized measurements under US GAAP (GAAP) and should not be used in isolation or as a substitute for Euroseas financial results presented in accordance with GAAP. Refer to a subsequent section of the Press Release for the definitions and reconciliation of these measurements to the most directly comparable financial measures calculated and presented in accordance with GAAP.

Aristides Pittas, Chairman and CEO of Euroseas commented: “We are pleased to report the financial results for one of the most profitable quarters of the last fifteen years. This was the result of our solid contracts at very profitable rates and low drydocking expenses incurred during the period. Throughout the first quarter of 2026 and in April and May 2026 to date, containership charter rates maintain their high levels. Container freight rates also maintained their level during the first quarter of 2026 and, subsequently, increased notably in April and May. Secondhand prices have remained elevated at near record levels since their recent peak in 2022.

“Our latest charter fixtures have confirmed the continuing strength of the market. With the last charters just announced today, we have [$650m] contracted revenues backlog over the next five years. Our coverage is over 90% for the rest of 2026, 88% for 2027 and 48% for 2028 ensuring that our profitability will remain strong regardless of the levels that expiring charters will be renewed at.

“During the first quarter of 2026, the shipping and macroeconomic environment we operate in has become even more uncertain due to the Iran war and the practical closure of the Strait of Hormuz. Although the near-term effect of these developments on shipping are positive due to the inefficiencies introduced in the transport of goods and the necessary vessel rerouting, the medium-term risks of increased inflation and world economic slowdown are negative factors for our industry. Other trade-related matters like the almost forgotten by now US imposed tariffs can only add to the overall uncertainty. In addition to the above, the containership market has to cope with an increasing orderbook across all segments. Still though, feeders and intermediate containerships are to face a much better supply side situation with their segment fleets likely to shrink over the next 2-3 years rather than grow as the great majority of the new orders are for larger vessels.

“We feel that the very high secondhand prices of containerships make the acquisition of secondhand vessels, less attractive. However, we feel that there is an opportunity to invest in building new vessels, the price of which is less volatile. We decided to expand our newbuilding program by adding four new shipbuilding contracts to our existing orderbook of six vessels bringing our total number of vessels on order to ten. This ten-vessel newbuilding program complements the previous nine-vessel newbuilding program we completed in early 2025. When all the ten vessels are delivered, we will have one of the youngest feeder and intermediate containership fleets amongst our peers.

“Finaly, I am also pleased to announce that our balance sheet strength and contracted revenues backlog provide us with sufficient comfort to increase the rewards to our shareholders by increasing our dividend by 6.7% to $0.80 per share providing an annualized yield of between 4.5-5% on the recent range our share price trades.”

Tasos Aslidis, Chief Financial Officer of Euroseas commented: “Our revenues for the first quarter of 2026 are slightly decreased by approximately 1% compared to the same period of 2025. The Company operated an average of 21.0 vessels, versus 23.68 vessels during the same period last year. At the same time the average time charter rates our vessels earned in the first quarter of 2026 increased by 10.1% compared to the same period of last year. Net revenues amounted to $55.8 million for the first quarter of 2026 compared to $56.3 million for the first quarter of 2025.

“Total daily vessel operating expenses, including management fees, general and administrative expenses, but excluding drydocking costs, increased by approximately 5.0%, during the first quarter of 2026 compared to the same quarter of last year. This increase is mainly attributable to the softening of the USD which increases the dollar costs of our euro denominated costs.

“Adjusted EBITDA1 during the first quarter of 2026 was $40.9 million compared to $37.1 million achieved in the first quarter of last year.

“As of March 31, 2026, our outstanding bank debt (before deducting the unamortized loan fees) was $213.3 million, versus restricted and unrestricted cash of approximately $161.4 million. As of the same date, our scheduled debt repayments over the next 12 months amounted to about $18.7 million (excluding the unamortized loan fees).”

First Quarter 2026 Results: For the first quarter of 2026, the Company reported total net revenues of $55.8 million representing a 1% decrease over total net revenues of $56.3 million during the first quarter of 2025. On average, 21.0 vessels were owned and operated during the first quarter of 2026 earning an average time charter equivalent rate of $30,354 per day compared to 23.68 vessels in the same period of 2025 earning on average $27,563 per day. The Company reported net income for the period of $32.5 million, as compared to net income of $36.9 million for the first quarter of 2025.

Voyage expenses for the first quarter of 2026 amounted to $0.2 million remaining at the same levels compared to the same period of 2025 and related to owners’ expenses incurred in various ports.

Vessel operating expenses for the first quarter of 2026 amounted to $11.2 million as compared to $12.3 million for the same period of 2025. The decreased amount is due to the lower number of vessels owned and operated in the first quarter of 2026 compared to the corresponding period of 2025.

Vessel depreciation expense for the first quarter of 2026 amounted to $6.7 million compared to $8.0 million for the same period of 2025 due to the decreased number of vessels in the Company’s fleet.

Despite the decreased numbers of vessels owned and operated, related party management fees for the first quarter of 2026 were $2.0 million, at the same level compared to the first quarter of 2025. This was the result of the adjustment for inflation in the daily vessel management fee, effective from January 1, 2026, increasing it from 840 Euros to 875 Euros, and the softening of the euro/dollar exchange rate during the period.

In the first quarter of 2025, we recorded a $10.23 million gain on the sale of M/V “Diamantis” that was completed in January 2025. No such case existed in the first quarter of 2026.

In the first quarter of 2026 none of our vessels was drydocked. The total cost of $0.05 million for the quarter relates to supplies performed for upcoming drydocks. In the first quarter of 2025 two of our vessels completed extensive repairs afloat for a total cost of $1.8 million.

General and administrative expenses slightly decreased to $1.7 million in the first quarter of 2026, as compared to $1.8 million in the first quarter of 2025 due to decreased professional fees.

Other operating income of $0.16 million recognized in the first quarter of 2026 refers to a settlement and closure of a claim with a charterer. No such case existed in the respective period of 2025.

Interest and other financing costs for the first quarter of 2026 amounted to $3.0 million. For the same period of 2025 interest and other financing costs amounted $3.9 million and the capitalized interest charged on the cost of our newbuilding program was $0.1 million. This decrease is due to the decreased benchmark rates of our loans and the decreased amount of debt in the current period compared to the same period of 2025.

For the three months ended March 31, 2026, the Company recognized a $0.3 million unrealized loss on its investments in equity securities. This was the result of an investment in equity securities with an initial cost of $20.0 million acquired in the first quarter of 2026 and fair valued at $19.7 million as of the end of the reporting period. This investment was made as part of the Company’s short-term cash and liquidity management strategy, in the context of which the Company also acquired debt securities of initial cost of $20.0 million and fair valued at $19.2 million as of March 31, 2026, classified as available-for-sale under US GAAP, for which an unrealized loss of $0.8 million was recorded in “Other comprehensive loss”.

For the three months ended March 31, 2025, the Company recognized a $0.17 million loss on its interest rate swap contract, comprising a $0.07 million realized gain and a $0.24 million unrealized loss. The specific contract was closed within the year 2025 and no such case existed in the first quarter of 2026.

Adjusted EBITDA1 for the first quarter of 2026 was $40.9 million, compared to $37.1 million achieved for the first quarter of 2025.

Basic and diluted earnings per share for the first quarter of 2026 was $4.67 and $4.65, respectively, calculated on 6,962,481 basic and 6,990,935 diluted weighted average number of shares outstanding compared to basic and diluted earnings per share of $5.31 and $5.29, respectively for the first quarter of 2025, calculated on 6,958,137 basic and 6,974,994 diluted weighted average number of shares outstanding.

The adjusted earnings per share for the quarter ended March 31, 2026, would have been $4.72 and $4.70 per share basic and diluted, respectively, compared to adjusted earnings of $3.76 per share basic and diluted for the first quarter of 2025. Usually, security analysts include Adjusted Net Income in their determination of published estimates of earnings per share.

Fleet Profile: The Euroseas Ltd. fleet profile as of May 21, 2026 is as follows:

Name

Type

Dwt

TEU

Year Built

Employment(*)

TCE Rate ($/day)

Container Carriers

SYNERGY BUSAN (*)

Intermediate

50,727

4,253

2009

TC until Dec-27

$35,500

SYNERGY ANTWERP (*)

Intermediate

50,727

4,253

2008

TC until May-28

$35,500

SYNERGY OAKLAND (*)

Intermediate

50,788

4,253

2009

TC until May-26 then until Mar-29

$42,000 $33,500

SYNERGY KEELUNG (*)

Intermediate

50,697

4,253

2009

TC until Jun-28

$35,500

EMMANUEL P (*)

Intermediate

50,796

4,250

2005

TC until Sep-28

$38,000

RENA P (*)

Intermediate

50,765

4,250

2007

TC until Jul-28

$35,500

EM KEA (*)

Feeder

42,165

3,100

2007

TC until Jul-26 then until Jul-29

$19,000 $30,000

GREGOS (*)

Feeder

38,733

2,800

2024

TC until Mar-29

$30,000

TERATAKI (*)

Feeder

38,733

2,800

2024

TC until Jul-26 Then until Jun-29

$48,000 $30,000

TENDER SOUL (*)

Feeder

38,733

2,800

2024

TC until Oct-27

$32,000

LEONIDAS Z (*)

Feeder

38,733

2,800

2024

TC until May-26 Then until Apr-29

$20,000 $30,000

DEAR PANEL(*)

Feeder

38,733

2,800

2025

TC until Nov-27

$32,000

SYMEON P(*)

Feeder

38,733

2,800

2025

TC until Nov-27

$32,000

PEPI STAR(*)

Feeder

22,563

1,800

2024

TC until Jun-26

$24,250

EVRIDIKI G (+)

Feeder

34,654

2,556

2001

TC until Jun-26

$29,500

EM CORFU (*)

Feeder

34,649

2,556

2001

TC until Aug-26

$28,000

MONICA (*)

Feeder

22,563

1,800

2024

TC until May-27

$23,500

STEPHANIA(*)

Feeder

22,563

1,800

2024

TC until May-26

$22,000

EM SPETSES (*)

Feeder

23,224

1,740

2007

TC until Feb-28

$21,500

JONATHAN P (*)

Feeder

23,732

1,740

2006

TC until Oct-26

$25,000

EM HYDRA (*)

Feeder

23,351

1,740

2005

TC until May-27

$19,000

Total Container Carriers

21

786,362

61,144

Note: (*) TC denotes time charter. All dates listed are the earliest redelivery dates under each TC unless the contract rate is lower than the current market rate in which cases the latest redelivery date is assumed; vessels with the latest redelivery date shown are marked by (+).

Vessels under construction

Type

Dwt

TEU

To be delivered

Employment

TCE Rate ($/day)

ELENA (H1711)(**)

Intermediate

56,266

4,484

Q3 2027

TC until Jun-31

$35,500

NIKITAS G (H1712) (**)

Intermediate

56,266

4,484

Q4 2027

TC until Sep-31

$35,500

THRYLOS(YZJ-1768) (**) (***)

Intermediate

56,266

4,484

Q1 2028

TC until Feb-32

$35,500

SOCRATES CH (YZJ-1769) (**)

Intermediate

56,266

4,484

Q2 2028

TC until Apr-32

$35,500

DANAI (HCY- 438)

Feeder

35,100

2,798

Q2 2028

NENI (HCY- 439)

Feeder

35,100

2,798

Q3 2028

SPYROS CH (S-1170)

Feeder

23,850

1,781

Q2 2028

GAVROS (S-1171)

Feeder

23,850

1,781

Q3 2028

TONIS M (HCY – 440)

Feeder

35,100

2,798

Q4 2028

SWEET EVELINA (HCY-441)

Feeder

35,100

2,798

Q1 2029

Total vessels under construction

10

413,164

32,690

(**) Charterer has the option to convert to a five-year charter at $32,500/day for the entire period. (***) The entity owning the vessel is 51% owned by Euroseas Ltd. and 49% by NRP Investors.

(1) Average number of vessels is the number of vessels that constituted the Company’s fleet for the relevant period, as measured by the sum of the number of calendar days each vessel was a part of the Company’s fleet during the period divided by the number of calendar days in that period.

(2) Calendar days. We define calendar days as the total number of days in a period during which each vessel in our fleet was in our possession including off-hire days associated with major repairs, drydockings or special or intermediate surveys or days of vessels in lay-up. Calendar days are an indicator of the size of our fleet over a period and affect both the amount of revenues and the amount of expenses that we record during that period.

(3) The scheduled off-hire days including vessels laid-up, vessels committed for sale or vessels that suffered unrepaired damages, are days associated with scheduled repairs, drydockings or special or intermediate surveys or days of vessels in lay-up, or vessels that were committed for sale or suffered unrepaired damages.

(4) Available days. We define available days as the Calendar days in a period net of scheduled off-hire days as defined above. We use available days to measure the number of days in a period during which vessels were available to generate revenues.

(5) Commercial off-hire days. We define commercial off-hire days as days a vessel is idle without employment.

(6) Operational off-hire days. We define operational off-hire days as days associated with unscheduled repairs or other off-hire time related to the operation of the vessels.

(7) Voyage days. We define voyage days as the total number of days in a period during which each vessel in our fleet was in our possession net of commercial and operational off-hire days. We use voyage days to measure the number of days in a period during which vessels actually generate revenues or are sailing for repositioning purposes.

(8) Fleet utilization. We calculate fleet utilization by dividing the number of our voyage days during a period by the number of our available days during that period. We use fleet utilization to measure a company’s efficiency in finding suitable employment for its vessels and minimizing the amount of days that its vessels are off-hire for reasons such as unscheduled repairs or days waiting to find employment.

(9) Fleet utilization, commercial. We calculate commercial fleet utilization by dividing our available days net of commercial off-hire days during a period by our available days during that period.

(10) Fleet utilization, operational. We calculate operational fleet utilization by dividing our available days net of operational off-hire days during a period by our available days during that period.

(11) Average time charter equivalent rate, or average TCE, is a measure of the average daily net revenue performance of our vessels. Our method of calculating average TCE is determined by dividing time charter revenue and voyage charter revenue, if any, net of voyage expenses by voyage days for the relevant time period. Voyage expenses primarily consist of port, canal and fuel costs that are unique to a particular voyage, which would otherwise be paid by the charterer under a time charter contract, or are related to repositioning the vessel for the next charter. Average TCE, which is a non-GAAP measure, provides additional meaningful information in conjunction with time charter revenue and voyage charter revenue, if any,, the most directly comparable GAAP measure, because it assists our management in making decisions regarding the deployment and use of our vessels and because we believe that it provides useful information to investors regarding our financial performance. Average TCE is a standard shipping industry performance measure used primarily to compare period-to-period changes in a shipping company’s performance despite changes in the mix of charter types (i.e., spot voyage charters, time charters and bareboat charters) under which the vessels may be employed between the periods. Our definition of average TCE may not be comparable to that used by other companies in the shipping industry.

(12) We calculate daily vessel operating expenses, which includes crew costs, provisions, deck and engine stores, lubricating oil, insurance, maintenance and repairs and related party management fees by dividing vessel operating expenses and related party management fees by fleet calendar days for the relevant time period. Drydocking expenses are reported separately.

(13) Daily general and administrative expenses are calculated by us by dividing general and administrative expenses by fleet calendar days for the relevant time period.

(14) Total vessel operating expenses, or TVOE, is a measure of our total expenses associated with operating our vessels. TVOE is the sum of vessel operating expenses, related party management fees and general and administrative expenses; drydocking expenses are not included. Daily TVOE is calculated by dividing TVOE by fleet calendar days for the relevant time period.

(15) Daily drydocking expenses are calculated by us by dividing drydocking expenses by the fleet calendar days for the relevant period, Drydocking expenses include expenses during drydockings that would have been capitalized and amortized under the deferral method. Drydocking expenses could vary substantially from period to period depending on how many vessels underwent drydocking during the period. The Company expenses drydocking expenses as incurred.

Conference Call and Webcast: Today, Thursday, May 21, 2026 at 08:30 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

Conference Call details: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “Euroseas” to the operator and/or conference ID 13760749. Click here for additional participant International Toll-Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

Audio Webcast – Slides Presentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.euroseas.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the first quarter ended March 31, 2026, will also be available in PDF format minutes prior to the conference call and webcast, accessible on the company’s website (www.euroseas.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

Euroseas Ltd. Unaudited Consolidated Condensed Statements of Comprehensive Income (All amounts expressed in U.S. Dollars except number of shares)

Three Months Ended March 31, 2025

Three Months Ended March 31, 2026

Revenues

Time charter revenue

57,983,415

57,535,733

Commissions

(1,637,320

)

(1,698,949

)

Net revenues

56,346,095

55,836,784

Operating expenses / (income)

Voyage expenses

232,976

166,347

Vessel operating expenses

12,251,094

11,216,018

Drydocking expenses

1,808,342

45,706

Vessel depreciation

8,045,067

6,680,851

Related party management fees

1,975,705

1,993,330

Gain on sale of vessel

(10,230,210

)

–

General and administrative expenses

1,778,918

1,701,518

Other operating income

–

(163,021

)

Total operating expenses, net

15,861,892

21,640,749

Operating income

40,484,203

34,196,035

Other (expenses) / income

Interest and other financing costs

(3,907,453

)

(3,009,526

)

Loss on derivative, net

(173,386

)

–

Loss on investments in equity securities

–

(348,820

)

Foreign exchange gain / (loss)

2,027

(17,241

)

Interest income

509,603

1,699,808

Other expenses, net

(3,569,209

)

(1,675,779

)

Net income

36,914,994

32,520,256

Earnings per share, basic

5.31

4.67

Weighted average number of shares, basic

6,958,137

6,962,481

Earnings per share, diluted

5.29

4.65

Weighted average number of shares, diluted

6,974,994

6,990,935

Other comprehensive loss:

Unrealized loss on investments in debt securities

–

(818,000

)

Other comprehensive loss

–

(818,000

)

Total comprehensive income

36,914,994

31,702,256

Euroseas Ltd. Unaudited Consolidated Condensed Balance Sheets (All amounts expressed in U.S. Dollars – except number of shares)

December 31, 2025

March 31, 2026

ASSETS

Current Assets:

Cash and cash equivalents

176,460,053

154,452,650

Restricted cash

564,027

608,168

Trade accounts receivable

10,159,572

12,257,574

Other receivables

1,365,550

1,026,227

Inventories

2,817,493

3,031,029

Accrued interest income

–

162,405

Investment in debt securities

–

19,182,000

Investment in equity securities

–

19,651,180

Prepaid expenses

984,394

1,295,371

Total current assets

192,351,089

211,666,604

Fixed assets:

Advances for vessels under construction

35,890,936

45,164,359

Vessels, net

465,913,492

459,550,867

Long-term assets:

Restricted cash

6,300,000

6,300,000

Total assets

700,455,517

722,681,830

LIABILITIES AND SHAREHOLDERS’ EQUITY

Current liabilities:

Long-term debt, current portion

19,151,932

18,301,932

Trade accounts payable

3,907,792

4,202,066

Accrued expenses

9,035,452

10,730,328

Accrued dividends

143,510

213,560

Deferred revenue

5,291,870

5,227,669

Due to related company

1,821,723

78,267

Total current liabilities

39,352,279

38,753,822

Long-term liabilities:

Long-term debt, net of current portion

197,659,451

193,239,404

Total long-term liabilities

197,659,451

193,239,404

Total liabilities

237,011,730

231,993,226

Shareholders’ equity:

Common stock (par value $0.03, 200,000,000 shares authorized, 7,055,881 issued and outstanding)

211,676

211,676

Additional paid-in capital

258,724,564

259,559,036

Retained earnings

204,507,547

231,735,892

Accumulated other comprehensive loss

–

(818,000

)

Total shareholders’ equity

463,443,787

490,688,604

Total liabilities and shareholders’ equity

700,455,517

722,681,830

Euroseas Ltd. Unaudited Consolidated Condensed Statements of Cash Flows (All amounts expressed in U.S. Dollars)

Three Months Ended March 31, 2025

Three Months Ended March 31, 2026

Cash flows from operating activities:

Net income

36,914,994

32,520,256

Adjustments to reconcile net income to net cash provided by operating activities:

Vessel depreciation

8,045,067

6,680,851

Amortization and write off of deferred charges

127,945

99,045

Share-based compensation

509,096

834,472

Unrealized loss on investments in equity securities

–

348,820

Gain on sale of vessel

(10,230,210

)

–

Unrealized loss on derivative

238,431

–

Amortization of fair value of below market time charters acquired

(1,218,240

)

–

Changes in operating assets and liabilities

6,838,283

(2,063,336

)

Net cash provided by operating activities

41,225,366

38,420,108

Cash flows from investing activities:

Cash paid for vessels under construction

(56,525,006

)

(9,278,133

)

Cash paid for vessel improvements

(155,303

)

(514,286

)

Net proceeds from sale of a vessel

12,875,660

–

Investment in equity securities

–

(20,000,000

)

Investment in debt securities

–

(20,000,000

)

Net cash used in investing activities

(43,804,649

)

(49,792,419

)

Cash flows from financing activities:

Cash paid for share repurchase

(1,206,021

)

–

Dividends paid

(4,518,889

)

(5,221,861

)

Loan arrangement fees paid

(429,000

)

–

Proceeds from long-term debt

52,000,000

–

Repayment of long-term debt

(15,259,090

)

(5,369,090

)

Cash retained by Euroholdings Ltd. at spin-off

(13,129,541

)

–

Net cash provided by financing activities

17,457,459

(10,590,951

)

Net increase / (decrease) in cash, cash equivalents, and restricted cash

14,878,176

(21,963,262

)

Cash, cash equivalents, and restricted cash at beginning of period

80,666,327

183,324,080

Cash, cash equivalents, and restricted cash at end of period

95,544,503

161,360,818

Cash breakdown

Cash and cash equivalents

88,333,158

154,452,650

Restricted cash, current

911,345

608,168

Restricted cash, long term

6,300,000

6,300,000

Total cash, cash equivalents, and restricted cash shown in the statement of cash flows

95,544,503

161,360,818

Euroseas Ltd. Reconciliation of Adjusted EBITDA to Net income (All amounts expressed in U.S. Dollars)

Three Months Ended March 31, 2025

Three Months Ended March 31, 2026

Net income

36,914,994

32,520,256

Interest and other financing costs, net (incl. interest income)

3,397,850

1,309,718

Vessel depreciation

8,045,067

6,680,851

Gain on sale of vessel

(10,230,210

)

–

Loss on interest rate swap derivative, net

173,386

–

Amortization of below market time charters acquired

(1,218,240

)

–

Unrealized loss on investments in equity securities

–

348,820

Adjusted EBITDA

37,082,847

40,859,645

Adjusted EBITDA Reconciliation: Euroseas Ltd. considers Adjusted EBITDA to represent net income before interest and other financing costs, net, depreciation, loss on interest rate swap derivative, net, gain on sale of vessel, amortization of fair value of below market time charters acquired and unrealized loss on investments in equity securities. Adjusted EBITDA does not represent and should not be considered as an alternative to net income, as determined by United States generally accepted accounting principles, or GAAP. Adjusted EBITDA is included herein because it is a basis upon which the Company assesses its financial performance and liquidity position and because the Company believes that this non-GAAP financial measure assists our management and investors by increasing the comparability of our performance from period to period by excluding the potentially disparate effects between periods of financial costs, loss on interest rate swaps, gain on sale of vessel, depreciation, amortization of below market time charters acquired and unrealized loss on investments in equity securities. The Company’s definition of Adjusted EBITDA may not be the same as that used by other companies in the shipping or other industries.

Euroseas Ltd. Reconciliation of Adjusted Net Income to Net Income (All amounts expressed in U.S. Dollars except share data and per share amounts)

Three Months Ended March 31, 2025

Three Months Ended March 31, 2026

Net income

36,914,994

32,520,256

Unrealized loss on derivative

238,431

–

Gain on sale of vessel

(10,230,210

)

–

Amortization of below market time charters acquired

(1,218,240

)

–

Vessel depreciation on the portion of the consideration of vessels acquired with attached time charters allocated to below market time charters

488,312

–

Unrealized loss on investments in equity securities

–

348,820

Adjusted net income

26,193,287

32,869,076

Adjusted earnings per share, basic

3.76

4.72

Weighted average number of shares, basic

6,958,137

6,962,481

Adjusted earnings per share, diluted

3.76

4.70

Weighted average number of shares, diluted

6,974,994

6,990,935

Adjusted net income and Adjusted earnings per share Reconciliation: Euroseas Ltd. considers Adjusted net income to represent net income before unrealized loss on derivative, gain on sale of vessel, amortization of below market time charters acquired, vessel depreciation on the portion of the consideration of vessels acquired with attached time charters allocated to below market time charters and unrealized loss on investments in equity securities. Adjusted net income and Adjusted earnings per share are included herein because we believe they assist our management and investors by increasing the comparability of the Company’s fundamental performance from period to period by excluding the potentially disparate effects between periods of the aforementioned items, which may significantly affect results of operations between periods.

Adjusted net income and Adjusted earnings per share do not represent and should not be considered as an alternative to net income or earnings per share, as determined by GAAP. The Company’s definition of Adjusted net income and Adjusted earnings per share may not be the same as that used by other companies in the shipping or other industries. Adjusted net income and Adjusted earnings per share are not adjusted for all non-cash income and expense items that are reflected in our statement of cash flows.

About Euroseas Ltd. Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA.

Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

The Company has a fleet of 21 vessels, including 15 Feeder containerships and 6 Intermediate containerships. Euroseas 21 containerships have a cargo capacity of 61,144 teu. After the delivery of ten containership newbuilding containerships gradually from the third quarter of 2027 until the first quarter of 2029, Euroseas’ fleet will consist of 31 vessels with a total carrying capacity of 93,834 teu.

Forward Looking Statement This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events and the Company’s growth strategy and measures to implement such strategy; including expected vessel acquisitions and entering into further time charters. Words such as “expects,” “intends,” “plans,” “believes,” “anticipates,” “hopes,” “estimates,” and variations of such words and similar expressions are intended to identify forward-looking statements. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates that are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to changes in the demand for containerships, competitive factors in the market in which the Company operates; risks associated with operations outside the United States; and other factors listed from time to time in the Company’s filings with the Securities and Exchange Commission. The Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

ATHENS, Greece, May 20, 2026 (GLOBE NEWSWIRE) — EuroDry Ltd. (NASDAQ: EDRY, the “Company” or “EuroDry”), an owner and operator of drybulk vessels and provider of seaborne transportation for drybulk cargoes, announced today its results for the three-month period ended March 31, 2026.

First Quarter 2026 Highlights:

Total net revenues of $12.8 million.

Net income attributable to controlling shareholders, of $0.26 million or $0.09 earnings per share attributable to controlling shareholders basic and diluted.

Adjusted net income1 attributable to controlling shareholders for the quarter of $0.33 million or $0.12 earnings per share attributable to controlling shareholders basic and diluted, which represents the net income attributable to controlling shareholders excluding the unrealized loss on derivatives.

Adjusted EBITDA1 was $4.9 million.

An average of 11.0 vessels were owned and operated during the first quarter of 2026 earning an average time charter equivalent rate of $14,416 per day. Refer to a subsequent section of the Press Release for the definition and method of calculation of the time charter equivalent rate.

To date, about $5.6 million has been used to repurchase 349,330 shares of the Company, under our share repurchase plan of up to $10 million, announced in August 2022. The Board approved the continuation of the share repurchase plan for a further year in August 2025 and will review it again after a period of twelve months.

____________________________ 1Adjusted EBITDA, Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders are not recognized measurements under US GAAP (GAAP) and should not be used in isolation or as a substitute for EuroDry’s financial results presented in accordance with GAAP. Refer to a subsequent section of the Press Release for the definitions and reconciliation of these measurements to the most directly comparable financial measures calculated and presented in accordance with GAAP.

Recent developments

The Company has signed two contracts with Hengli Shipbuilding (Dalian) for the construction of two 82,000 DWT Kamsarmax bulk carriers. Both vessels are eco and are built to EEDI phase 3 design standard; they are scheduled to be delivered during the first and second quarters of 2028. The total consideration for the two newbuilding contracts is approximately $74.0 million and will be financed with a combination of debt and equity. The contracts are conditional upon receiving a refund guarantee from a bank acceptable to the Company.

Aristides Pittas, Chairman and CEO of EuroDry commented: “During the first quarter of 2026, a seasonally slow quarter, the drybulk market gave up very little ground as compared to the last quarter of last year. Additionally in April and May 2026, the market has firmed across the board with one-year time charter rates and trip earnings flirting and reaching $20,000 per day for both Ultramaxes and Kamsarmaxes.

“Our profitability during the first quarter fully reflected the market conditions with our earnings dropping compared to the fourth quarter in consequence of the easing of market rates during the quarter. But as the market has increased during the last month and a half, so has our profitability, a development that we expect to be reflected in next quarter’s results.

“Whilst the global fleet is aging and the need to provide the market with newer and more efficient vessels is becoming apparent, we see that prices of modern secondhand vessels have significantly increased. Under the circumstances we believe that newbuilding orders which can be placed at prices below modern secondhand ship prices present a better opportunity. We have therefore decided to expand our newbuilding program to include two Kamsarmax vessels to complement the two Ultramaxes we had ordered earlier. After the delivery of all four vessels between Q2 2027 and Q2 2028, our fleet will consist almost entirely of modern eco vessels. As, I believe, we have demonstrated over the past eight years as an independent public company, we invest in a disciplined manner with the sole focus on identifying accretive opportunities for our shareholders and we intend to continue with the same philosophy.”

Tasos Aslidis, Chief Financial Officer of EuroDry commented: “Our net revenues for the first quarter of 2026 were higher by 38.9% as compared to the first quarter of 2025. This is primarily driven by the increase of 101.1% in average time charter equivalent rates our vessels earned during the current quarter as compared to the first quarter of 2025, partly offset by the decreased average number of vessels owned and operated in the current period compared to the same period of 2025.”

“Vessel operating expenses were $5.5 million for the first quarter of 2026 as compared to $6.6 million for the same period of 2025. The decrease is mainly attributable to the decreased average number of vessels owned and operated in the first quarter of 2026 compared to the corresponding period in 2025.“

“Adjusted EBITDA during the first quarter of 2026 was $4.9 million compared to $(1.0) million achieved for the first quarter of last year. As of March 31, 2026, our outstanding debt (excluding the unamortized loan fees) was $100.9 million versus restricted and unrestricted cash of approximately $24.9 million.”

First Quarter 2026 Results: For the first quarter of 2026, the Company reported total net revenues of $12.8 million representing a 38.9% increase over total net revenues of $9.2 million during the first quarter of 2025, which was the result of the increased time charter rates our vessels earned during the first quarter of 2026, partly offset by the decreased average number of vessels owned and operated during the first quarter of 2026, compared to the same period of 2025. On average, 11.0 vessels were owned and operated during the first quarter of 2026 earning an average time charter equivalent rate of $14,416 per day compared to 12.8 vessels in the same period of 2025 earning on average $7,167 per day.

For the first quarter of 2026, a gain on bunkers resulted in positive voyage expenses of $0.3 million compared to voyage expenses of $1.7 million in the first quarter of 2025 that mainly related to vessels repositioning between charters and expenses during operational off-hire time.

Vessel operating expenses decreased to $5.5 million for the first quarter of 2026 from $6.6 million in the same period of 2025. The decrease is mainly attributable to the decreased average number of vessels owned and operated in the first quarter of 2026 compared to the corresponding period in 2025.

In the first quarter of 2026, one of our vessels completed its special survey with drydock for a total cost of $0.7 million. In the first quarter of 2025 one of our vessels completed its intermediate survey in water, for a total cost of $0.1 million.

Depreciation expense for the first quarter of 2026 was $2.9 million compared to $3.2 million for the same period of 2025 as a result of the lower number of vessels owned and operated in the first quarter of 2026.

Related party management fees for the period were $1.1 million remaining at the same level compared to the same period of 2025. This was the result of the decreased number of vessels owned and operated in the first quarter of 2026, offset by the adjustment for inflation in the daily vessel management fee, effective from January 1, 2026, increasing it from 850 Euros to 875 Euros, as well as by the unfavorable movement of the euro/dollar exchange rate during the period.

General and administrative expenses were $0.9 million for the first quarter of 2026, slightly increased compared to the same period of last year.

On January 29, 2025, the Company signed an agreement to sell M/V Tasos, a 75,100 dwt drybulk vessel, built in 2000, for demolition, for approximately $5 million. The vessel was delivered to its buyers, an unaffiliated third party, on March 17, 2025, resulting in a gain on sale of $2.1 million. No case of vessel sale exists within the first quarter of 2026.

Interest and other financing costs for the first quarter of 2026 decreased to $1.5 million as compared to $1.8 million for the same period of 2025. Interest expense during the first quarter of 2026 was lower mainly due to the decreased benchmark rates of our loans and the decreased average debt during the first quarter of 2026, as compared to the same period of last year.

For the three months ended March 31, 2026, the Company recognized a $0.07 million unrealized loss and a $0.09 million realized loss on forward freight agreement contracts. For the three months ended March 31, 2025, the Company recognized a $0.13 million unrealized loss and a $0.04 million realized gain on one interest rate swap.

The Company reported a net income for the period of $0.4 million and a net income attributable to controlling shareholders of $0.3 million, as compared to a net loss of $4.0 million and a net loss attributable to controlling shareholders of $3.7 million for the same period of 2025. The net income attributable to the non-controlling interest of $0.2 million in the first quarter of 2026 represents the income attributable to the 39% ownership of the entities owning the M/V Christos K and M/V Maria represented by NRP Project Finance AS (“NRP investors”) (the “Partnership”).

Adjusted EBITDA for the first quarter of 2026 was $4.9 million compared to $(1.0) million achieved during the first quarter of 2025.

Basic and diluted earnings per share attributable to controlling shareholders for the first quarter of 2026 were $0.09, calculated on 2,796,647 and 2,828,521 basic and diluted weighted average number of shares outstanding, respectively, compared to a basic and diluted loss per share attributable to controlling shareholders of $1.35 for the first quarter of 2025, calculated on 2,737,297 basic and diluted weighted average number of shares outstanding.

Excluding the effect on the net (loss) / income attributable to controlling shareholders for the quarter of the unrealized loss on derivatives and the net gain on sale of vessel (if any), the adjusted earnings attributable to controlling shareholders for the quarter ended March 31, 2026 would have been $0.12 per share basic and diluted, compared to an adjusted loss of $2.07 per share, basic and diluted, attributable to controlling shareholders for the quarter ended March 31, 2025. Usually, security analysts do not include the above item in their published estimates of earnings per share.

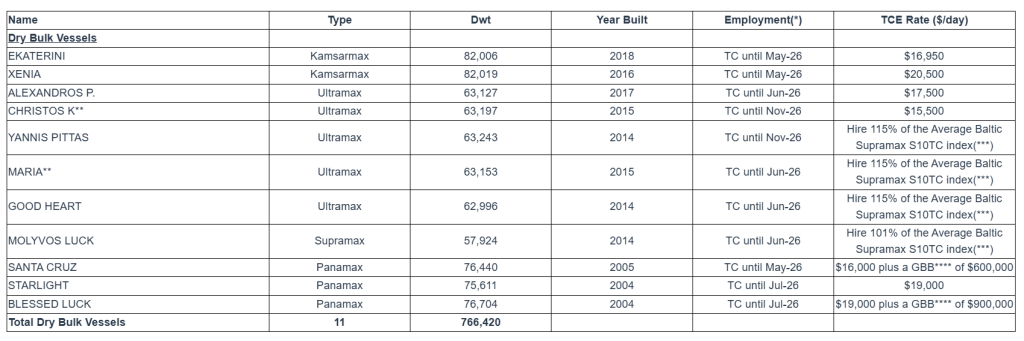

Fleet Profile:

The EuroDry Ltd. fleet profile is as follows:

Note: (*) TC denotes time charter. Charter duration indicates the earliest redelivery date. (**) The entity owning the vessel is 61% owned by EuroDry and 39% by NRP Investors. (***) The average Baltic Supramax S10TC Index is an index based on ten Supramax time charter routes. (****) Gross Ballast Bonus (GBB), refers to the payments made by the charterer which serve as compensation for the ballast trip of the vessel from the last port of discharge to the delivery port.

Summary Fleet Data:

(1) Average number of vessels is the number of vessels that constituted the Company’s fleet for the relevant period, as measured by the sum of the number of calendar days each vessel was a part of the Company’s fleet during the period divided by the number of calendar days in that period.

(2) Calendar days. We define calendar days as the total number of days in a period during which each vessel in our fleet was owned by us including off-hire days associated with major repairs, drydockings or special or intermediate surveys or days of vessels in lay-up. Calendar days are an indicator of the size of our fleet over a period and affect both the amount of revenues and the amount of expenses that we record during that period.

(3) The scheduled off-hire days including vessels laid-up are days associated with scheduled repairs, drydockings or special or intermediate surveys or days of vessels in lay-up.

(4) Available days. We define available days as the total number of Calendar days in a period net of scheduled off-hire days incl. laid up. We use available days to measure the number of days in a period during which vessels were available to generate revenues.

(5) Commercial off-hire days. We define commercial off-hire days as days a vessel is idle without employment.

(6) Operational off-hire days. We define operational off-hire days as days associated with unscheduled repairs or other off-hire time related to the operation of the vessels.

(7) Voyage days. We define voyage days as the total number of days in a period during which each vessel in our fleet was in our possession net of commercial and operational off-hire days but including days our vessels were sailing for repositioning. We use voyage days to measure the number of days in a period during which vessels actually generate revenues or are sailing for repositioning purposes.

(8) Fleet utilization. We calculate fleet utilization by dividing the number of our voyage days during a period by the number of our available days during that period. We use fleet utilization to measure a company’s efficiency in finding suitable employment for its vessels and minimizing the amount of days that its vessels are off-hire for reasons such as unscheduled repairs or days waiting to find employment.

(9) Fleet utilization, commercial. We calculate commercial fleet utilization by dividing our available days net of commercial off-hire days during a period by our available days during that period.

(10) Fleet utilization, operational. We calculate operational fleet utilization by dividing our available days net of operational off-hire days during a period by our available days during that period.

(11) Average time charter equivalent rate, or average TCE, is a measure of the average daily net revenue performance of our vessels. Our method of calculating average TCE is determined by dividing time charter revenue and voyage charter revenue, if any, net of voyage expenses by voyage days for the relevant time period. Voyage expenses primarily consist of port, canal and fuel costs that are unique to a particular voyage, which would otherwise be paid by the charterer under a time charter contract or are related to repositioning the vessel for the next charter. Average TCE provides additional meaningful information in conjunction with time charter revenue and voyage charter revenue, if any, the most directly comparable GAAP measure, because it assists our management in making decisions regarding the deployment and use of our vessels and because we believe that it provides useful information to investors regarding our financial performance. Average TCE is a standard shipping industry performance measure used primarily to compare period-to-period changes in a shipping company’s performance despite changes in the mix of charter types (i.e., spot voyage charters, time charters, pool agreements and bareboat charters) under which the vessels may be employed between the periods. Our definition of average TCE may not be comparable to that used by other companies in the shipping industry.

(12) We calculate daily vessel operating expenses, which include crew costs, provisions, deck and engine stores, lubricating oil, insurance, maintenance and repairs and related party management fees by dividing vessel operating expenses and related party management fees by fleet calendar days for the relevant time period. Drydocking expenses are reported separately.

(13) Daily general and administrative expense is calculated by us by dividing general and administrative expenses by fleet calendar days for the relevant time period.

(14) Total vessel operating expenses, or TVOE, is a measure of our total expenses associated with operating our vessels. We compute TVOE as the sum of vessel operating expenses, related party management fees and general and administrative expenses; drydocking expenses are not included. Daily TVOE is calculated by dividing TVOE by fleet calendar days for the relevant time period.

(15) Daily drydocking expenses is calculated by us by dividing drydocking expenses by the fleet calendar days for the relevant period. Drydocking expenses include expenses during drydockings that would have been capitalized and amortized under the deferral method. Drydocking expenses could vary substantially from period to period depending on how many vessels underwent drydocking during the period. The Company expenses drydocking expenses as incurred.

Conference Call and Webcast: Today, May 20, 2026 at 9:00 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

ConferenceCalldetails: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “EuroDry” to the operator and/or conference ID 13760747. Click here for additional participant International Toll -Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

AudioWebcast-SlidesPresentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.eurodry.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the first quarter ended March 31, 2026, will also be available in PDF format 10 minutes prior to the conference call and webcast, accessible on the company’s website (www.eurodry.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

EuroDry Ltd. Unaudited Consolidated Condensed Statements of Operations (All amounts expressed in U.S. Dollars – except number of shares)

EuroDry Ltd. Unaudited Consolidated Condensed Statements of Operations (All amounts expressed in U.S. Dollars – except number of shares)

EuroDry Ltd. Unaudited Consolidated Condensed Statements of Cash Flows (All amounts expressed in U.S. Dollars)

EuroDry Ltd. Reconciliation of Net (loss) / income to Adjusted EBITDA (All amounts expressed in U.S. Dollars)

Adjusted EBITDA Reconciliation: EuroDry Ltd. considers Adjusted EBITDA to represent net (loss) / income before interest and other financing costs, income taxes, vessel depreciation, unrealized loss on Forward Freight Agreements (“FFAs”), loss on interest rate swap derivative and net gain on sale of vessel. Adjusted EBITDA does not represent and should not be considered as an alternative to net loss, as determined by United States generally accepted accounting principles, or GAAP. Adjusted EBITDA is included herein because it is a basis upon which the Company assesses its financial performance because the Company believes that this non-GAAP financial measure assists our management and investors by increasing the comparability of our performance from period to period by excluding the potentially disparate effects between periods of, financial costs, unrealized loss on FFAs, loss on interest rate swap derivative, vessel depreciation and net gain on sale of vessel. The Company’s definition of Adjusted EBITDA may not be the same as that used by other companies in the shipping or other industries.

EuroDry Ltd. Reconciliation of Net (loss) / income attributable to controlling shareholders to Adjusted net (loss) / income attributable to controlling shareholders (All amounts expressed in U.S. Dollars – except share data and number of shares)

Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders Reconciliation:

EuroDry Ltd. considers Adjusted net (loss) / income attributable to controlling shareholders, to represent net (loss) / income before unrealized loss on derivatives, which includes FFAs and interest rate swaps, and net gain on sale of vessel. Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders is included herein because we believe they assist our management and investors by increasing the comparability of the Company’s fundamental performance from period to period by excluding the potentially disparate effects between periods of the abovementioned items, which may significantly affect results of operations between periods.

Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders do not represent and should not be considered as an alternative to net (loss) / income attributable to controlling shareholders or (loss) / earnings per share attributable to controlling shareholders, as determined by GAAP. The Company’s definition of Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders may not be the same as that used by other companies in the shipping or other industries. Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders are not adjusted for all non-cash income and expense items that are reflected in our statement of cash flows.

About EuroDry Ltd. EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd into a separate listed public company. EuroDry was spun-off from Euroseas Ltd on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY.

EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day-to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters.

The Company has a fleet of 11 vessels, including 3 Panamax drybulk carriers, 5 Ultramax drybulk carriers, 2 Kamsarmax drybulk carriers and 1 Supramax drybulk carrier. EuroDry’s 12 drybulk carriers have a total cargo capacity of 766,420 dwt. After the delivery of two Ultramax vessels in 2027 and the delivery of the two Kamsarmax vessels in 2028, the Company’s fleet will consist of 15 vessels with a total carrying capacity of 1,050,420 dwt.

Forward Looking Statement This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events and the Company’s growth strategy and measures to implement such strategy; including expected vessel acquisitions and entering into further time charters. Words such as “expects,” “intends,” “plans,” “believes,” “anticipates,” “hopes,” “estimates,” and variations of such words and similar expressions are intended to identify forward-looking statements. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates that are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to changes in the demand for dry bulk vessels, competitive factors in the market in which the Company operates; risks associated with operations outside the United States; and other factors listed from time to time in the Company’s filings with the Securities and Exchange Commission. The Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

ATHENS, Greece, May 19, 2026 (GLOBE NEWSWIRE) — Euroseas Ltd. (NASDAQ: ESEA), an owner and operator of container carrier vessels and provider of seaborne transportation for containerized cargoes, announced today that it will release its financial results for the first quarter ended March 31, 2026, on May 21, 2026, before market opens in New York.

On the same day, Thursday, May 21, 2026, at 8:30 am Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

ConferenceCalldetails: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “Euroseas” to the operator and/or conference ID 13760749. Click here for additional participant International Toll -Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

AudioWebcast–SlidesPresentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.euroseas.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the first quarter ended March 31, 2026, will also be available in PDF format minutes prior to the conference call and webcast, accessible on the company’s website (www.euroseas.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

AboutEuroseasLtd. Euroseas Ltd. was formed on May 5, 2005, under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 150 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA.

Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

The Company has a fleet of 21 vessels, including 15 Feeder containerships and 6 Intermediate containerships. Euroseas 21 containerships have a cargo capacity of 61,144 teu. Following the gradual delivery of ten containership newbuildings from the third quarter of 2027 through the first quarter of 2029, Euroseas’ fleet is expected to consist of 31 vessels with an aggregate carrying capacity of 93,834 TEU.

Oil markets whipsawed Tuesday after President Trump announced he had called off a planned military strike on Iran scheduled for that morning, citing active negotiations brokered by Gulf allies. The announcement briefly pulled crude prices lower, but the relief was short-lived. The underlying supply crisis has not been resolved, and the data emerging from global inventory trackers suggests the window for a clean diplomatic outcome is narrowing fast.

Brent crude slipped to around $110 per barrel following Trump’s announcement while West Texas Intermediate pulled back to approximately $103. Both contracts had been climbing sharply the session prior, with Brent settling above $112 and WTT rising more than 3% on Monday alone. The combined 54% rise in both benchmarks since the US-Iran conflict began February 28 represents one of the most sustained energy price shocks in recent memory.

What Trump Said — and What It Means

Trump posted on Truth Social Monday evening that the leaders of Saudi Arabia, Qatar, and the United Arab Emirates personally requested he hold off on the strike while serious negotiations proceed. He confirmed the military had been placed on full alert and instructed to act on short notice if a deal is not reached. A senior US official told reporters that Iran’s latest proposal remains insufficient, and no framework has been announced. The ceasefire is intact — but barely.

The Inventory Problem

The diplomatic pause may have eased prices temporarily, but the physical oil market tells a more urgent story. The International Energy Agency warned Monday at the G7 finance ministers meeting in Paris that global commercial oil inventories are depleting at a record pace. Stockpiles fell 129 million barrels in March and another 117 million barrels in April. At the current rate of depletion, inventories will approach all-time lows of approximately 7.6 billion barrels by end of May — a timeline measured in days, not months.

Complicating matters further, Iran has effectively converted the strait into a toll-collecting operation. Reports indicate the Iranian Revolutionary Guards are charging vessels fees for passage, with nearly two dozen tankers sitting idle around Kharg Island. Traffic through the strait last week totaled just 55 vessels — still well below pre-conflict norms and only a marginal recovery from the wartime low of 19 crossings the prior week.

The Small Cap Exposure

For investors in the sub-$2 billion market cap space, the Iran situation is an active P&L event. Consumer-facing small caps in transportation, logistics, food services, and manufacturing continue absorbing elevated fuel costs that compress margins in real time. Limited pricing power and thin operating margins make smaller companies structurally more vulnerable to a prolonged energy shock than large cap counterparts.

The counterweight remains domestic energy producers. With WTI holding above $100 despite Tuesday’s pullback, the economics for independent US oil and gas operators remain highly favorable. Energy services companies and midstream operators in the small cap space are direct beneficiaries — and a negotiated resolution that reopens the strait would not necessarily collapse prices overnight given how severely inventories have been drawn down.

Trump’s call to stand down bought time. Whether that time produces a deal or simply delays the next escalation remains the most consequential open question in global energy markets right now.

ATHENS, Greece, May 18, 2026 (GLOBE NEWSWIRE) — EuroDry Ltd. (NASDAQ: EDRY, the “Company” or “EuroDry”), an owner and operator of drybulk vessels and provider of seaborne transportation for drybulk cargoes, announced today that it will release its financial results for the first quarter ended March 31, 2026, on May 20, 2026 before market opens in New York.

On the same day, Wednesday, May 20, 2026, at 9:00 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

ConferenceCalldetails: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “EuroDry” to the operator and/or conference ID 13760747. Click here for additional participant International Toll-Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

Audio Webcast-SlidesPresentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.eurodry.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.