The digital media landscape is witnessing a dramatic shakeup as Trump Media & Technology Group, the company behind the conservative social network Truth Social, experiences a sharp decline in its stock value. The Nasdaq-listed company, trading under the ticker DJT, has seen its shares plummet by over 40% since early June, opening at a mere $27 per share on Thursday. This downturn has sent shockwaves through the social media stock market, raising questions about the future of alternative platforms in an increasingly competitive digital ecosystem.

The sell-off intensified Thursday, with shares sinking as much as 15% shortly after the opening bell, continuing a trend that has wiped billions from the company’s market capitalization. This steep decline has had a profound impact on the paper wealth of former President Donald Trump, the majority stakeholder in the company. Trump’s 114,750,000 shares, once valued at over $5.6 billion in early June, have now plummeted to around $3.2 billion – a staggering loss of approximately $2.4 billion in less than a month.

The catalyst for this market turbulence appears to be rooted in recent legal developments. The company’s stock began its downward spiral on May 30, coinciding with a New York jury’s decision to convict the former president on 34 felony counts of falsifying business records. This legal setback has evidently shaken investor confidence, highlighting the potential risks associated with companies closely tied to controversial public figures.

Adding to the tumult, Trump Media recently reached a crucial milestone in its regulatory journey. The Securities and Exchange Commission (SEC) declared the company’s registration statement effective, a development that triggered significant market reaction. The stock fell nearly 10% during Tuesday’s trading session on more than double the average volume, followed by a further 17% plunge in after-hours trading following the announcement.

This SEC approval marks a pivotal moment for Trump Media, authorizing early investors to exercise warrants and allowing stockholders to publicly resell securities covered by the registration statement. While this development provides greater liquidity for existing shareholders, it also introduces the potential for increased selling pressure, which could further impact the stock’s performance.

The volatility surrounding Trump Media serves as a case study in the challenges faced by emerging social media platforms as they navigate the complex interplay of market forces, regulatory requirements, and public perception. As the digital advertising landscape continues to evolve, investors and industry observers are closely watching how alternative social networks like Truth Social can carve out their niche and sustain growth in a highly competitive market.

The unfolding situation at Trump Media also underscores the importance of diversification in investment portfolios, particularly when dealing with stocks tied to high-profile individuals or emerging technologies. As the company strives to weather this storm, its ability to adapt to changing market conditions and demonstrate sustainable user growth will be crucial in regaining investor confidence.

In the broader context of social media innovation and digital marketing trends, the Trump Media saga highlights the ongoing shifts in online engagement and content monetization strategies. As users increasingly seek out niche platforms that align with their values and interests, the success of companies like Trump Media may hinge on their ability to foster engaged communities while navigating the complex regulatory and financial landscapes of the modern digital economy.

As this story continues to develop, it will undoubtedly remain a focal point for those interested in the intersection of technology, politics, and finance, offering valuable insights into the future of social media entrepreneurship and the challenges of building sustainable digital platforms in today’s rapidly changing online environment.

In a move that epitomizes the AI revolution’s inexorable rise and its rippling effects across economic sectors, Sam Altman’s advanced nuclear company Oklo has gone public through a SPAC deal. The transaction netted over $306 million for the fledgling firm to propel its quest to deliver miniaturized, modular nuclear reactors to power everything from military bases to the server farms underpinning large language models like ChatGPT.

Altman, the high-profile CEO of OpenAI, has been vocal about prioritizing sustainable energy solutions like nuclear to meet ballooning computational demands across the AI landscape. Oklo represents a manifestation of that vision, an audacious startup aiming to disrupt antiquated nuclear plant designs with smaller, more nimble fission reactors enclosed in A-frame structures.

As revolutionary AI systems smash through prior technical constraints, their insatiable appetite for energy poses both an opportunity and existential risk. Without abundant, reliable, and climate-friendly power sources, the sector’s terrific growth could stumble or succumb to overreliance on carbon-intensive alternatives. Nascent AI companies embracing pioneers like Oklo could leapfrog that hurdle entirely.

The company’s unconventional public debut via a SPAC merger, while risky, underscores the urgency around securing capital and resources to outpace competing nuclear upstarts and legacy utilities. It also spotlights intensifying investor zeal around potential disruptors servicing the unique infrastructure needs of AI.

At the vanguard are deep-pocketed tech titans like Microsoft, Amazon, and Google parent Alphabet, all operating gargantuan data centers tasked with training and running large language models, computer vision, and myriad other AI workloads. These digital refineries have grown so prodigious they now rank among the world’s top consumers of electricity.

In recent years, the likes of Microsoft and Google have inked deals with nuclear upstarts while voicing public support for next-generation reactors to enhance sustainability and feed AI growth. Amazon cloud chief Andy Jassy has advocated exploring nuclear at scale as a critical lever.

Oklo positions itself as an ideal partner straddling these ambitions. In addition to the company’s modular nuclear plants aimed at localized power generation, the startup’s energy-dense reactors could be co-located at data center campuses requiring immense on-site capacity. Its small-scale model obviates the hazards and complexities of colossal conventional nuclear facilities situated far from demand.

This dystopian vision — fleets of miniature, mobile nuclear generators powering the AI revolution’s factories — may spark backlash from environmental groups wary of distributed radiation risks. But the reality is computing’s ecological footprint has become too ravenous to ignore.

According to one estimate, the energy already consumed by AI could produce the emissions of the entire country of Spain. Left unfettered, ML training workloads alone may comprise a third of the world’s total power demands by 2030. Nuclear proponents cast reactors like Oklo’s as potentially vital circuit-breakers preventing a climate catastrophe.

Altman’s multi-front assault on solving AI’s existential scaling crisis doesn’t stop at Oklo. Through OpenAI and his investment vehicles, the tech mogul is betting big on a range of startups pushing the boundaries in fields like nuclear fusion, data center chips, and ultra-dense computing. Audacious ventures once relegated to science fiction now rank among the most coveted opportunities for VCs and growth investors.

Whether Oklo and its ilk can clear the considerable technical and regulatory hurdles to commercial viability fast enough remains an open question. The challenges of improving nuclear economics, public perception, and building an adept workforce remain immense.

But as AI continues its relentless expansion defying prior predictions, the companies capable of architecting sustainable infrastructure solutions may prove as indispensable to the revolution as the algorithms and models powering the systems themselves. Altman is among the growing chorus sounding that clarion call to action.

Donald Trump’s social media platform Truth Social hit the public markets with a bang, surging over 30% on its first day of trading and ballooning the former president’s stake in the company to over $5 billion. However, the staggering valuation and volatility highlight both the risks and potential rewards for investors looking to capitalize on Truth Social’s polarizing popularity.

Trading under the appropriate ticker DJT, Truth Social’s parent company managed to achieve a peak market capitalization around $9 billion despite the fledgling business having under $5 million in sales over the prior year. The massive $6.8 billion opening valuation put Truth Social on par with well-established companies like U.S. Steel and Skechers.

This eye-popping disconnect from financial fundamentals echoes the frenzied trading in meme stocks like GameStop that has gripped markets in recent years. In Truth Social’s case, the dramatic stock rise seems fueled largely by Trump’s devoted base of supporters, who have banded together to push up the shares.

Trump and the seven-member Truth Social board, stacked with allies like his son Don Jr., certainly have incentive to allow some profits to be taken off the table soon. Any signal of insider selling could severely dent the company’s lofty stock price if shareholders perceive waning confidence.

Therein lies one of the biggest risks surrounding an investment in Truth Social – the potential for exceedingly high volatility driven by speculation rather than business performance. If Trump’s devoted base sours on the company’s prospects, a spiral could ensue.

On the other hand, the frenzied first day demonstrated how Trump’s mere involvement and ability to marshal his base can supercharge an investment thesis, at least in the short term.

Additionally, Trump may receive tens of millions of extra shares if the sky-high valuation holds up in the coming weeks. This would further concentrate his influence over the company’s future.

For risk-tolerant investors, there’s also the potential that Truth Social could eventually disrupt incumbent social media platforms and transform into a financially viable business at scale. Though it has struggled against larger rivals thus far, Trump’s massive following of over 90 million combined on X and Facebook could provide a springboard.

From a trading perspective, Truth Social’s arrival has already juiced options volumes to potentially record levels. Traders loaded up on bullish call options betting on shares surging to $80 or $90 in a sign of the speculative frenzy around the stock.

Ultimately, while Truth Social’s jaw-dropping debut minted a new billionaire out of Trump, it has set the stage for a gladiator battle between bullish and bearish investors. With both immense risks and rewards, Truth Social is shaping up as the ultimate “investor Rorschach test” based on one’s convictions around Trump and his ability to create a viable media business.

Abpro, an emerging biotechnology company developing novel antibody therapies, has entered into a definitive agreement to go public via a merger with Atlantic Coastal Acquisition Corp. II, a special purpose acquisition company (SPAC). The deal values Abpro at $725 million and will provide capital to advance its drug pipeline.

Abpro specializes in leveraging its proprietary technology platform to create next-generation antibody treatments for cancer, eye diseases, and viral infections. The company aims to develop breakthrough immunotherapies to help patients facing life-threatening conditions.

Though Abpro is still in the preclinical phase, it has made significant progress with its pipeline of antibody therapies. Its lead candidates target HER2+ cancers, which include aggressive forms of breast, gastric, and colorectal cancer. Abpro is also pursuing antibodies for COVID-19 treatment and ophthalmic conditions like wet AMD and DME.

Last year, Abpro announced a partnership with South Korea’s Celltrion to further develop ABP 102, an antibody-based treatment for HER2+ cancers. Under the deal, Abpro received a direct equity investment from Celltrion along with eligibility for up to $1.75 billion in milestone payments.

Abpro leverages its DiversImmune platform to design diverse antibody libraries and identify optimal drug candidates. The technology enables more precise targeting compared to conventional antibodies.

The merger with Atlantic Coastal will provide capital for Abpro to advance its most promising therapies into clinical studies. Abpro also plans to use the funds for business development activities and expanding its pipeline.

Atlantic Coastal is a SPAC focused on finding and merging with high-potential healthcare companies. The transaction is expected to close in Q2 2024, at which point the combined company will trade publicly.

Commenting on the merger, Abpro CEO Ian Chan stated: “This milestone will accelerate getting our therapies to patients needing life-changing treatments.”

Abpro represents an attractive investment opportunity within biotech. Analysts project the global antibody technology market to reach $272 billion by 2030, driven by rising demand for targeted immunotherapies. With its next-generation platform and infusion of growth capital, Abpro is well-positioned to compete in this thriving sector.

The transaction comes amidst a wave of biotech SPAC deals, as pre-revenue companies aim to access public growth financing. With its proprietary technology and strategic partnership in place, Abpro seems poised to leverage this deal to evolve from an R&D startup into a fully integrated biopharma company.

Explore other SPAC Mergers via Spactrac reports from Noble Capital Markets

Greenfire Resources, a Calgary-based oil sands company, began public trading on the New York Stock Exchange on Thursday through a merger with a special purpose acquisition company (SPAC). However, shares of Greenfire fell sharply on its debut, dropping around 11% in morning trading.

Greenfire combined with M3-Brigade Acquisition III Corp, a SPAC sponsored by New York-based private investment firm Brigade Capital Management. The deal, first announced in December 2022, valued Greenfire at $950 million.

The new company, Greenfire Resources Ltd, is now listed on the NYSE under the ticker “GFR”. But investors reacted negatively to the stock early on. After opening at $9.80 per share, GFR declined over 37% to around $6.10 by Friday morning.

SPAC deals have faced increased skepticism from investors amid high market volatility this year. Many companies that went public via SPACs have seen their share prices sink below initial trading levels. This broader SPAC downturn could be contributing to the weak debut for Greenfire.

Greenfire operates steam-assisted gravity drainage (SAGD) facilities in Alberta’s prolific oil sands region. It has a 75% stake in the Hangingstone expansion project, which came online in 2017, and 100% ownership of the adjacent Hangingstone demonstration facility. Both produce bitumen using steam injection to mobilize viscous oil sands deposits.

The company raised approximately $42 million through a private placement that closed concurrently with the SPAC merger on September 20. It also put in place $300 million in new senior secured notes and a $50 million senior secured credit facility to boost liquidity.

According to Greenfire’s management, the company will prioritize debt reduction in the near-term to strengthen its financial position. It also plans to increase production at its existing facilities through techniques like infill drilling and debottlenecking.

For example, Greenfire is currently drilling extended reach “refill” wells at the Hangingstone expansion site. These wells are intended to produce incremental volumes from between existing well pairs. No new drilling has occurred at the project since its commissioning in 2017.

In the long-term, Greenfire aims to generate free cash flow thanks to controlled capex spending and its high quality oil sands reservoirs. The company believes it has a structural cost advantage compared to some other SAGD operators in the Athabasca region.

Greenfire says its assets have long-life reserves and relatively low decline rates versus conventional oil and gas resources. For instance, the Hangingstone demonstration project has maintained steady production for nearly 20 years without new wells. This could support continued output for decades.

The company intends to initiate a shareholder returns policy over time once it has made sufficient progress on debt reduction. It also plans to evaluate potential acquisition opportunities to drive further growth down the line.

But in the short-term, investors seem cautious on the newly public company as oil prices waver. Energy stocks have seen significant volatility in 2022. Greenfire traded down double-digits in its NYSE debut as traders reacted hesitantly.

Its success at boosting production from existing assets through relatively low-cost techniques like infill drilling may dictate whether shares can rebound over the coming months. For now, the market is taking a wait-and-see approach with the SPAC-backed oil sands operator.

Explore other SPAC Mergers via SPACtrac reports from Noble Capital markets

DevvStream Holdings, a leading developer of carbon offset projects and associated credit streams, has signed a definitive agreement to go public through a merger with special purpose acquisition company (SPAC) Focus Impact Acquisition Corp.

The combined company will be named DevvStream Corp. and is expected to list on the Nasdaq under ticker “DEVS”. The deal values DevvStream at an implied $212.8 million enterprise value.

Founded in 2021, Vancouver-based DevvStream partners with corporations and governments on sustainability initiatives. It brings projects generating carbon credits to market by co-investing or providing technical services in exchange for a share of long-term credit streams.

This capital-light model requires little upfront investment for participation in the fast-growing carbon markets. DevvStream estimates its current portfolio will generate $13 million in net revenue in 2024 and $55 million in 2025 as projects are expanded.

DevvStream participates in both regulated compliance markets and the rapidly expanding voluntary carbon credit market. The voluntary market hit $2 billion in 2022 but could reach up to $250 billion by 2030 according to estimates.

The merger will provide further expansion capital to DevvStream as it scales its portfolio of emissions-reducing projects. Focus Impact raised $172.5 million in its May 2021 IPO into a trust that will go to the combined company after redemptions.

According to DevvStream CEO Sunny Trinh, “Entering into a definitive agreement to merge with Focus Impact is a significant step towards accelerating the growth of our differentiated technology-based approach to carbon markets.”

He added that enhancing transparency and reliability in voluntary markets in particular can help drive participation and meaningful emissions reductions.

Focus Impact CEO Carl Stanton said the proposed merger “presents a significant opportunity to create substantial value for our shareholders.” He cited DevvStream’s systematic approach to carbon project development and blockchain-enabled tracking.

The transaction is expected to close in the first half of 2023, subject to shareholder approvals and other customary closing conditions. Upon completion, DevvStream will be listed on the Nasdaq under ticker “DEVS”.

With global momentum building around carbon markets and climate action, the merger comes at an opportune time. DevvStream is now poised to capitalize on surging demand as both corporations and governments seek to curb emissions.

Calidi Biotherapeutics has completed its merger with special purpose acquisition company First Light Acquisition Group (FLAG), debuting as a publicly traded cancer immunotherapy company. The combined entity, now named Calidi Biotherapeutics, Inc., will commence trading on the NYSE American under ticker symbols “CLDI” and “CLDI WS” on September 13.

The merger provides Calidi with gross proceeds of approximately $28 million before expenses and debt repayments. This consists of $25 million raised in a concurrent private offering, $1 million in cash from FLAG’s trust, and $2 million in PIPE and non-redemption agreements.

Founded in 2014, Calidi is developing first-in-class immunotherapies using allogeneic stem cells to deliver targeted cancer treatments. The SPAC deal enables the company to continue advancing its pipeline as a publicly listed firm.

Calidi’s lead candidates CLD-101 and CLD-201 leverage proprietary platforms called NeuroNova and SuperNova. Both utilize allogeneic stem cells loaded with oncolytic viruses that directly infect and kill tumor cells.

CLD-101, which employs neural stem cells, is currently in a Phase 1 trial for recurrent high-grade glioma brain tumors. Interim data is expected in 2024. CLD-201 uses mesenchymal stem cells to treat advanced solid tumors, with a Phase 1/2 study slated for 2024.

According to Calidi CEO Allan Camaisa, the IPO “will allow us to push the boundaries of cell-based virotherapies and continue to research novel ways to eradicate cancer.”

SPACs have become an increasingly popular alternative to traditional IPOs in the biotech sector. Also known as “blank check companies”, SPACs raise capital through an IPO and then merge with a private entity to take it public. This allows the operating company to avoid some of the uncertainty associated with a traditional public debut.

First Light Acquisition Group, led by CEO Tom Vecchiolla, raised $172.5 million in its own IPO in May 2021. The team then sought a merger target that could benefit from the injection of public capital. They ultimately settled on clinical-stage Calidi and its novel immunotherapy approach.

In addition to the SPAC proceeds, Calidi has secured a $10 million forward purchase agreement from several institutional investors. It also intends to execute a $50 million purchase agreement with Lincoln Park Capital Fund.

Between its strengthened balance sheet and non-dilutive financing options, Calidi believes it now has the runway to advance its programs into 2025 without need for further equity funding.

According to Vecchiolla, “We are excited to see Calidi continue to grow as they transition into a public company and look forward to their clinical pursuit of new treatment options for patients everywhere in need.”

The merger completes Calidi’s transformation into a publicly traded company. With shares soon to start trading on the NYSE American under ticker “CLDI”, the company is poised to continue developing its promising immunotherapy candidates for cancer patients in need of new treatment options.

Shareholders of Digital World Acquisition (DWAC), the investment partner of former President Donald Trump’s media venture, have granted an extension to the company’s merger deadline. This extension allows the special purpose acquisition company (SPAC) more time to complete its long-pending merger with Truth Social, a social network with pro-Trump leanings.

The extension comes after a concerted effort to secure shareholder approval, arriving just three days before the liquidation deadline of Truth Social on September 8. A failure to secure shareholder approval would have compelled the SPAC to dissolve, resulting in the return of $300 million to shareholders, depriving Trump Media & Technology Group of the funds associated with the deal.

However, the merger still faces challenges, including meeting closing conditions and resolving issues raised by the Securities and Exchange Commission (SEC). In July, the SEC alleged that Digital World had misled investors in its official merger documents. Correcting these inaccuracies and resubmitting the filings is necessary before the merger process can proceed. Additionally, required quarterly financial statements covering operations in the first half of 2023 have not been filed with the SEC.

Digital World Acquisition had initially anticipated a year for the merger process when it went public in September 2021 but has encountered several hurdles necessitating deadline extensions, including a previous one in September 2022.

Following the news of the extension, Digital World’s shares experienced a rise to over $18 before settling at $16.80 per share at 11 a.m. The stock had reached its peak at approximately $175 per share in 2021.

Explore other SPAC Mergers via SPACtrac reports from Noble Capital Markets

Image: Devin Nunes, CEO Trump Media (Flickr, Gage Skidmore)

DWAC, Trump Media Merger Now With Fewer Hurdles

Digital World Acquisition Corp. (DWAC), the Special Purpose Acquisition Corp. (SPAC), which agreed to merge with a Twitter competitor, Trump Media & Technology Group (TMTG), reported news that is driving its stock price higher. The agreement to merge back in October 2021 has encountered a number of unexpected hurdles as it has moved toward a planned merger before September 8, 2023. This week, DWAC, which went public in September 2021, reached an agreement with the enforcement division of the SEC that should again clear the way to complete the planned merger.

DWAC announced on Friday that it had reached a preliminary settlement with the Enforcement Division of the U.S. Securities and Exchange Commission (SEC) involving an investigation started on December 2021 by the regulator, which on March 8, 2022, then issued a subpoena to DWAC seeking information about its merger with TMTG.

According to the proposed settlement, DWAC will make the requested revisions to its previously submitted Form S-4 (acquisition registration statement) to ensure its accuracy and alignment with the SEC’s findings. Along with the revised S-4, Digital World Acquisition Corp has agreed to pay an $18 million civil money penalty to the SEC following the completion of any merger, business combination, or transaction, whether with the Truth Network or another entity.

Shares of DWAC are well off the highs reached after the agreement to merge had been announced. For those in the initial public offering (IPO) they have still experienced performance better than the overall market, despite the roadblocks over almost two years.

In addition to the proposed SEC settlement, DWAC also just disclosed it received a note from TMTG expressing disagreement regarding a section of the Merger Agreement that relates to deadlines. According to the Company’s interpretation, upon obtaining approval from its shareholders to extend the liquidation date by three additional months (totaling 12 additional months from September 8, 2023, to September 8, 2024), DWAC then has the right to extend the Outside Date of the Merger Agreement for the same period.

This runs counter to what the TMTG believes which is that it is only bound by the Merger Agreement until September 8, 2023. Due to previous extensions of the liquidation date and Truth Network’s acknowledgment of being bound until September 8, 2023, the DWAC aims to now address this disagreement in good faith, considering the historical extensions and the delayed submission of required deliverables by TMTG.

DWAC remains interested in the transaction and hopes to resolve this discrepancy with Trump Media.

Less Attention is Being Paid to SPACs, But the Risk Reward Scenario Can’t Be Ignored

Uncertain markets warrant additional attention to risk versus possible reward on investments, especially when the least risky money funds pay 4% or more. This need to minimize risk, yet desire to have the opportunity to, at a minimum, beat inflation and in the best case scenario, hit a grand slam, might cause investors to revisit the hot investment of 2021. Like most investment sectors that do well, back then it became too crowded with issuance and overpromise. But the Special Purpose Acquisition Corp (SPAC), is getting far less attention these days – yet the relatively low risk for investors, and low competition for acquisition corps. to find that “unicorn,” it could increase the percentage of SPAC home runs. All the while limiting potential downside returns.

Special Purpose Acquisition Corps.

Investors that just want to make (or lose) the returns of a major index may not find investing in individual SPACs, at any stage, fits their investment approach. But the SPAC legal structure could suit investors that want to minimize their downside to a more or less known potential, and maximize their possible above average returns – SPACs may match these investment objectives better than alternatives.

Let’s cover risk first. SPAC investors have limited risk as their investment is held in a trust account until the SPAC identifies a target company and completes a merger. If the SPAC fails to identify a target, the investors will return their money, plus today’s higher accrued interest rates, less management, legal, and administrative fees. That is to say, a SPAC purchased as an IPO could be expected to be up or down one or two percent from the initial (usually $10) IPO price.

As ulcer-producing volatility in the major indices over the past year has shown, the feeling of having a floor on losses is comforting. The monetary distance to this floor is reduced if a post SPAC IPO, still looking for a target is trading below the $10 IPO price.

Does low risk mean low returns? SPACs offer the potential for low risk/high returns for investors who get in before an announced target. If the SPAC is successful in identifying and merging with a high-growth company, the share price could increase significantly. The targets often are successful private companies with tremendous potential, more of the potential could be realized with an injection of cash from the SPAC merger/acquisition. that would be able to expand.

What if an investor is opposed to the proposed merger? SPAC investors have the flexibility to decide whether or not to participate in the merger with the target company. If they choose not to participate, they can redeem their shares for the original investment amount plus interest, less administrative costs. This is another way that investors minimize their downside risk.

What are the risks? Investing in SPACs also comes with potential risks, such as the possibility of the SPAC failing to identify a suitable target company, this would essentially have tied up the investment capital used to purchase the SPAC. Another risk is the target company not performing as expected after the merger; as mentioned above, the pre-merger investor gets to decide if they opt in or opt to have pro-rata share of initial investment returned. As with any investment, it’s important to do your due diligence, look at any changes in the regulatory environment, and carefully evaluate the structure and goals.

What Does SPAC Investment Success Look Like?

Not all SPACs find a suitable target. An investor wants the management team exploring possibilities to be diligent and picky. But despite the large number of SPACs that have gone no place during the abundance offered in 2021, it’s easy to find examples of why investors like the market. Below are three very different examples of what success looks like:

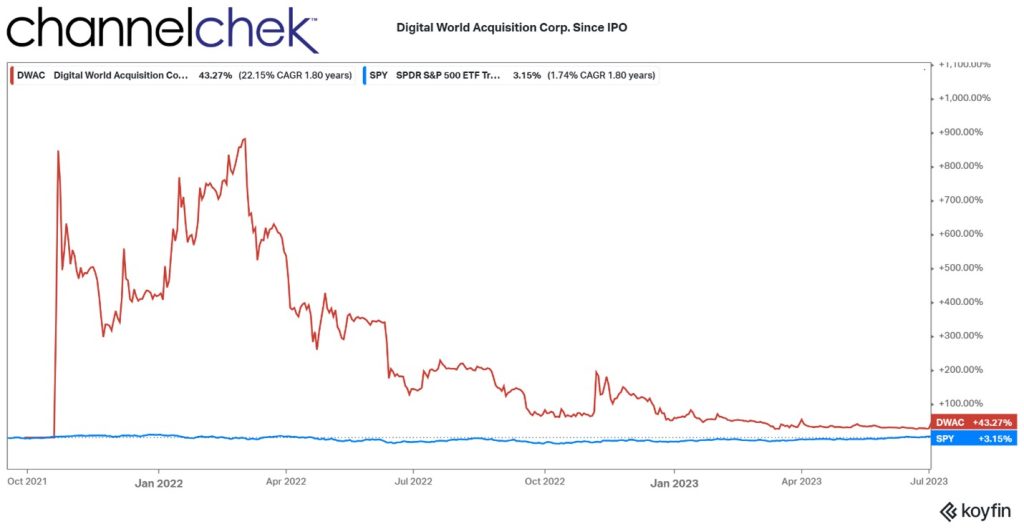

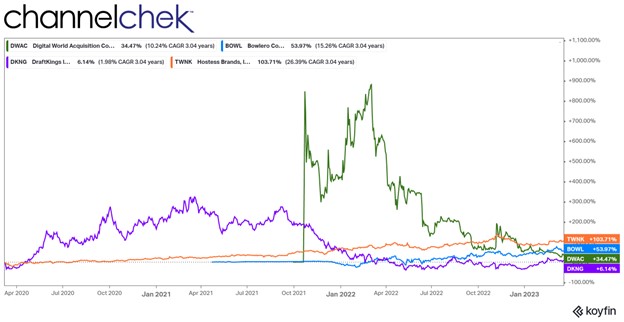

In green is Digital World Acquisition Corp. (DWAC). It’s the only stock represented below that is pre-merger. The initial IPO was for $10 back in April 2021. Recent numbers show that a failure to merge with its current target, Trump Media, would result in approximately a $10 per share liquidation. Initial investors will have lost opportunity should this occur as they took the full ride from beginning to this possible end.

In October after the IPO, Digital World announced it had reached a preliminary agreement to merge with the digital media company founded by the former U.S. president. The shares skyrocketed over 900%. For those that bought the once $10 shares for $96, they may not have called this right, for those that purchased around the offer price, their risk of losing money is low, and they currently sit at a 34% profit.

In orange is Hostess (TWNK). This has been a SPAC success story which dates back to 2016 when there were only 13 SPAC IPOs all year. By comparison, there were 613 in 2021, and to date only 8 in 2023. Fewer SPACs chasing the same potential targets could work in investors’ favor. Many of the SPACs that are still less than two year old are still shopping. However most of those arrangements are expected to be returning shareholder funds. While Hostess is up 103% since March three years ago, it has gained 236% since the merger announcement.

Bowlero (BOWL), shown in blue, announced the merger with Isos Acquisition Corp. on July 1, 2021. The merged company would have at first disappointed investors as it dipped slightly. This is understandable as investing in leisure did not seem that it would offer quick gratification, as the pandemic hit this sector hard. However, the stock is up 54% in less than two years and up 58% YTD.

Shown here in purple, DraftKings (DKNG) merged April 24, 2020. Post merger, for those who held the Diamond Eagle Acquisition SPAC shares, they saw the stock jump 5% on the day of the announcement, eventually rise over 350%, and over time come back down to match the initial jump, 6% YTD.

Above are success stories, of varying degrees. There are many SPACs that don’t find the ideal merger partner, for the initial purchasers at $10, or those buying shares sub-$10 after the offering, their risk can be considered lower than the overall market. The potential for large gains, exists.

What Does a SPAC Investment Failure Look Like?

The most an investor will lose in an index fund investment approximates the decline of the index less management fees. The most an investor in any of the individual stocks in a major market index can lose is all of their investment. When an investor takes part in a SPAC IPO or purchases shares trading below the IPO price later, they have claim to funds held in escrow that would have been used for an acquisition. These funds seldom grow or shrink by more than 2%. SPAC investors could look at the risk of losing $2 per share (2%), versus possibly gaining double or triple-digit returns as better than market risk. But investors have lost some of their initial investment, and once the deal is struck, voted on by shareholders, and moves forward, the investment risk goes from very low, to just as risky as any other company traded. In other words, up to 100%.

Take Away

Low-risk and high-reward investments may not suit all portfolios. But for those that like to reduce the odds of loss, the glut of previously offered SPACs that are retiring this year, coupled with the lack of new offerings, could set the stage for easier target hunting for unmatched SPACs. Also, older SPACs trading at or below the enterprise value may be worth looking at, the cash in the escrow accounts are earning today’s yields, and may even be worth more than the share price.

To look for current opportunities of companies that have announced a merger, but not yet completed one, a source of information is Channelchek. Earlier this month, Better World Acquisition Corp. (BWAC) announced it will be merging with Heritage Distilling Co. The combined company expects to trade under the ticker CASK. A current research report detailing the planned acquisition along with valuation is made available here, from Noble Capital Markets.

Noble Capital Markets SPACtrac Report Thursday, March 02, 2023

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

The Deal. Better World Acquisition Corp. will be merging with Heritage Distilling Company, Inc. in a deal that will bring Heritage Distilling public. The deal, which values Heritage Distilling at an enterprise value of $122.2 million, provides growth capital to achieve Heritage Distilling’s aim to become the leading national craft spirits company.

The Target. Founded in 2012, Heritage Distilling is a leading, fast-growing distiller of innovative premium brands, with a history of award winning, innovative products. The Company is expanding its wholesale footprint nationwide in conjunction with RNDC, the second largest spirits distributor in the U.S., while its proprietary Tribal Beverage Network provides the potential of developing a “local” presence across the nation that will generate high margin, tax advantaged recurring revenue license streams.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Recent Investment Trends Include Small-Cap Artificial Intelligence Stocks

C3 AI, sometimes written C3.ai, is an artificial intelligence platform that provides services for companies to build large-scale AI applications. Its stock had the fifth highest traded shares among Fidelity’s retail investors on Monday (February 6). This included a record-breaking $31.4 million worth of shares traded among the broker’s individual self-directed traders. According to Reuters, “Retail investors are piling up on small-cap firms that employ artificial intelligence amid intensifying competition between tech titans.” The article points to Google and Microsoft as examples of companies that expect AI to be the next meaningful driver of growth.

Investors, for their part, are looking to get ahead of any acquisition spree that deep-pocketed companies may embark on, which could include buying the advanced technology by acquiring small-cap tech firms.

Focus Heightened by ChatGPT

The spotlight ChatGPT finds itself in, three months after its launch, is indicicative of the interest in this technology amongst investors and users. With applications as numerous than one can think up, the technology could outdate many services provided by tech companies like Alphabet (GOOGL), or Microsoft (MSFT) – big tech has catching up to do. This seems to have created a race by cash rich companies to not be disrupted and left behind.

Investor’s recent focus on small companies in this space prefer those that are concentrated in AI technology. One main reason is that small-cap or microcap firms in this space are likely to have AI as a more concentrated part of their business. The bet being that whether the small company continues to grow independently, or is acquired by a larger firm looking to instantly be par with current technology, doesn’t much matter, it is a win for the investor if either occurs.

And it is a win, C3 AI stock rallied 46% last week, and climbed another 6.5% on Monday. It is now up 146% year to date.

Other Companies Involved

SoundHound AI, provides a voice AI platform services, and Thailand-based security firm Guardforce AI have more than doubled so far this year, while analytics firm BigBear.AI has increased ninefold.

US-listed shares of Baidu Inc climbed after the Chinese search engine indicated it would complete an internal test of a ChatGPT-style project called “Ernie Bot” next month.

Shares of Microsoft, which supports ChatGPT parent OpenAI, had been ratcheting up over the past month. The company is expected to make an announcement on their AI gained 1.5% in premarket trading ahead of the AI plans this week.

Google-owner Alphabet Inc said this week it would launch Bard, a chatbot service for developers, alongside its search engine.

Take Away

Change in technology that leads to improvements in daily lives has always been a focus of investors betting on which companies will outlast the others with “the next big thing.” These companies start out as small growth companies as Apple (AAPL) did in 1976. Then, a number of paths lay ahead. They either grow on their own like the Jobs/Wozniak computer maker did, get acquired for an early payday for investors and other stakeholders, or they can be outcompeted leaving investors with a non-performing asset.

Channelchek is a platform that specializes in bringing data and research on small-cap companies, including many varieties of new technology, to the investors that insist on being informed before they place a trade. Discover more on the industries of tomorrow by signing up for notifications in your inbox from Channelchek by registering here.

Image Credit: Trump White House Archive (Public Domain)

The Wild Ride of Digital World Acquisition Corp. Has Mostly Been Positive

You never know what kind of surprise you may eventually end up with when purchasing a Special Purpose Acquisition Corp (SPAC). Digital World Acquisition Corp. (DWAC) is the perfect example of how a SPAC can provide a wild ride for those that were originally involved in the IPO and those that have since been involved in the stock of the “blank check company.” Before plans to merge with Truth Media, a subsidiary of Trump Media Group, it started out as most SPACs do, with a $10 a share price and a description of what an appropriate target would look like, and credentials of managing a financial company.

Most Recent

News impacting social media competitors to Truth Social and information involving the former President’s stature have historically driven prices of the acquiring company in a sporadic fashion. On Monday, DWAC took off by 66.5% to $29.10 during the trading day. On the prior trading day it had already risen 7% to $17.48. The impetus for this was news that Donald J. Trump was making plans to announce his candidacy as a Republican hopeful in the 2024 election.

The strong updraft of the DWAC price came the day before the US Election Day when political power struggles are at the forefront of most investors’ minds. It also occurred on the same day the former President announced plans to make a “Big” announcement next week.

Last week the SPAC shares rose after management delayed a shareholder vote — for the sixth time — on whether to approve a year extension to complete its merger with Trump Media and Technology Group. The shareholders meeting is now set for Nov. 22. DWAC’s deadline to complete its merger with Trump’s company had originally been in early September. However, the SPAC has said an SEC investigation of the merger deal delayed progress.

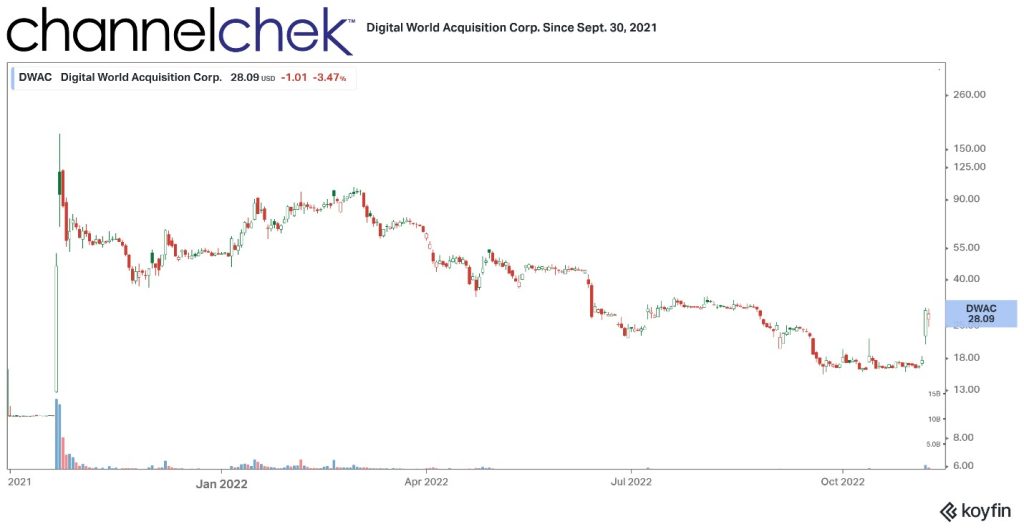

October 2021 – The chart above shows the upward SPAC spike (1,650%) as it became known in late October of its intent to merge with Trump’s fledgling social media venture. A retail trading frenzy had sent prices of the Trump media-linked SPAC, Digital World Acquisition Corp., ripping up an incredible 1,650% in just two days.

The stock reached a peak of $175, within two days and closed the week up 845% from an unusual amount of enthusiasm from retail interest.

News reports at the time highlighted the company had no fundamentals to speak of and te action was purely speculation and momentum.

Digital World Acquisition Corp. ended on the Friday at $94.20 after closing Wednesday at $9.96.

December 2021 –The stock traded off after the initial enthusiasm, especially after the media company fell short of its plan to have a beta version of Truth Social in November. It then caught fire later during the first week of December 2021. The impetus here was an announcement that the former President was raising $1 billion (mostly from family offices and hedge funds) to support the company’s projects.

Federal regulators cast a dark cloud over the deal, beginning the second week of December. The SEC was overall looking at tax and accounting of all SPACs, this had the potential to impact DWAC. Additionally, FINRA requested information to investigate whether than were any improper communications between Trump Media and Digital World.

Image Credit: Trump White House Archive (Public Domain)

Moving forward that December, a new CEO of Truth Social was appointed. This was a former representative to the House, Devin Nunes from California.

January 2022 – On the 7th of January, the stock rose 20%, up 505% from the day the plans to merge was announced. The stock’s market cap was also up by the same percentage at $2.24 billion.

Plans were made to launch the social platform on February 21st. The company had been still sitting at lofty heights on faith, not an actual product.

In late January, the SPAC experienced its largest one-day jump of the year (to date), a 21% increase on no new information. There was, however speculation that the stock’s rally may have been connected to a Trump rally the still politically active Trump held in his home state.

As shown on the chart above, momentum for the stock was again building after a January 6 announcement of the launch date, the stock climbed 71%. Phunware (PHUN), the designer of the platform, was up 25%.

February 2022 – The Trump social media platform becomes available in the app store in late February and the price of DWAC increases 28% pre-market open. Institutional investors gain a new respect for the power of self-directed retail investors and the power they hold. Prices in February are sitting at a 750% increase from the day the SPAC merger was announced.

April 2022 – Two private investors bail on Truth Social, and shares of Digital World drop following a negative (30%) March. The share value has now declined 70% from its all-time high. Adding to the drag on values, new SPAC rules from the SEC cast even more doubt on the ability to bring the deal to a close.

June 2022 – Since the beginning of the year, the stock’s value dropped 47%. The SEC began expanding its inquiry into the proposed merger, having subpoenaed the company for more information on the deal. Investors think the deal will likely be delayed, perhaps even torpedoed.

July 2022 – Elon Musk made good on a Tweet to offer to buy Twitter. His intent was to “free the bird” and allow open discourse, in other words, turn it into what Trump envisioned for Truth Social. Both Trump and Musk have fans and foes, so the drama picked up when Elon suggested openly Trump ought to “hang up his hat and sail into the sunset.”

Prices of DWAC originally declined but then found their footing as expectations of Elon Musk successfully buying the huge competitor of Truth Social waned.

August 2022 –Digital World says it isn’t sure whether they are the right vehicle to take Truth Social public. And it wants to keep financials under wraps until it can decide. The SEC allows an automatic five-day extension.

It’s the regulatory and legal obstacles DWAC’s been faced with since announcing the merger that could have caused them to look for the surrender flag. The two entities were subjected to a federal criminal probe that caused every single one of the SPAC’s board members to receive a subpoena after already warning that any investigations would jeopardize the deal. Shares were down 73% since October.

November 2022 – The momentum that may have been responsible for the original run-up over a year earlier again surfaces as it is rumored that the ex-President with a massive amount of loyal followers will be running to be re-elected. “In a very, very, very short period of time, you’re going to be very happy,” former president Donald Trump told attendees at a rally on November 5.

Trump Media’s merger with DWAC still faces many legal and financial hurdles that have resulted in at least $138m in investment being pulled. Trump will post on Truth Social exclusively for 8 hours before posting elsewhere. He has been widely followed on the social platforms he has been part of, so whether investors support the potential candidacy, they’re almost certain it’ll drive traffic to the app.

Take Away

One never knows what target companies a SPAC may unearth, if any, as a suitor for its acquisition plans. For investors that jump into the unknown early, before a SPAC announces any plans, their downside is somewhat limited as their investments are held in escrow as the target is procured. Should a deal be struck, they get to decide if they wish to stay involved. If, after two years, the SPAC fails to close on a target, investors still holding shares receive the original purchase price (usually $10), fewer expenses, plus interest. Considering how volatile other investments have been, this effectively puts a floor in to protect against the downside for investors near the $10 level.