Toronto, Ontario–(Newsfile Corp. – June 13, 2025) – Aurania Resources Ltd. (TSXV: ARU) (OTCQB: AUIAF) (FSE: 20Q) (“Aurania” or the “Company”) announces that its shareholders approved all resolutions at the Company’s Annual and Special Meeting of Shareholders (the “Meeting”) which was held on Thursday, June 12, 2025. The formal part of the Meeting was followed by an update from Aurania’s President & CEO, Dr. Keith Barron. To access the replay of Dr. Barron’s update on YouTube, click this link: https://youtu.be/m0SIk501QtY

At the Meeting, shareholders approved the financial statements for the year-ended December 31, 2024, and the report of the auditors thereon, the appointment of auditors, election of directors, and the Company’s incentive stock option plan for the upcoming year. Details of these matters are disclosed in the Management Information Circular for the Meeting dated April 30, 2025, and posted under the Company’s profile on www.sedarplus.ca and on the Company’s corporate website http://www.aurania.com/investors/annual-general-meeting/.

Clarification to Press Release Dated June 11, 2025

Further to the Company’s press release dated June 11, 2025, the Company wishes to clarify the terms of the proposed fee that the Company would be required to pay as presented by ARCOM. As currently contemplated, half of this fee is expected to be due by July 31, 2025, and the remaining 50% is expected to be due by January 31, 2026.

About Aurania

Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and copper in South America. Its flagship asset, The Lost Cities – Cutucu Project, is located in the Jurassic Metallogenic Belt in the eastern foothills of the Andes mountain range of southeastern Ecuador.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Demand for rare earth elements expected to grow. Demand for rare earth elements is expected to grow meaningfully through 2030 and beyond, driven by electric vehicles, wind turbines, grid upgrades, and advanced defense technologies. According to the IEA, global rare earth demand could double by 2050 under a net-zero scenario, underscoring the growing strategic relevance in the global energy transition.

China dominates the REE market. According to the 2024 edition of the Energy Institute Statistical Review of World Energy, China accounted for 67.9% of rare earth mineral production in 2023 and 38.1% of rare earth mineral reserves, while accounting for most of the midstream and downstream capacity. While mining activity is gradually diversifying, the refining stage remains concentrated. This level of concentration poses a risk to both the U.S. supply chain and national security.

U.S. policymakers seek to reduce dependence on China. U.S. policymakers are increasingly focused on reducing dependence on China for rare earth elements, viewing it as a national security and industrial resilience issue. Recent actions include invoking the Defense Production Act, funding domestic processing projects, and expanding international partnerships through initiatives like the Minerals Security Partnership. Legislative efforts and strategic investments are aimed at reshoring supply chains and building alternative capacity in allied countries such as Canada and Australia.

Necessity is the mother of invention. While the Trump Administration is taking appropriate action and policy momentum is growing, the path to increasing rare earth supply chain independence is complex and will take time. Policymakers may need to work with allies, such as Canada, to promote a North American supply chain that encompasses all aspects of the REE value chain, including upstream, midstream, and downstream. In addition to supportive public policy, private industry will likely need financial support from governments to kick start the effort.

Metals and Mining Spotlight: Rare Earth Elements

Rare earth elements (REEs) are comprised of 15 elements in the lanthanum series, along with scandium and yttrium. While not lanthanides, scandium and yttrium are classified as rare earth elements because they occur within the same ore deposits and share similar chemical properties. While the actual elements may not be rare, it is often difficult to find them in sufficient concentrations for economic extraction, and they require extensive processing. Cerium, lanthanum, neodymium, praseodymium, and promethium are considered light rare earth elements. Europium, gadolinium, and samarium are often referred to as medium rare earth elements, while dysprosium, erbium, holmium, lutetium, terbium, thulium, and ytterbium are considered heavy rare earth elements. We do not classify scandium (Sc) or yttrium (Y) as light, medium, or heavy. Below is a table summarizing the elements and their symbols.

Figure 1: Rare Earth Elements and Atomic Number and Symbol

Source: Noble Capital Markets, Inc.

One of the many uses of rare earth elements is in the production of permanent magnets which are critical components in electric vehicles, wind turbines, and other communication and defense technologies. Neodymium and praseodymium are critical materials in the manufacturing of neodymium-iron-boron (NdFeB) magnets, which have among the highest magnetic strength among commercially available magnets and promote high energy density and efficiency in energy technologies. They are often referred to as NdPr magnets because they generally contain about one-third neodymium, of which some of that can be replaced by praseodymium. While REEs are used for a variety of applications, the highest value REEs are neodymium and praseodymium, which currently drive the value of mixed rare earth concentrates and precipitates. By economic value, neodymium-praseodymium (NdPr) is the largest segment of the REE market. NdPr is primarily used in neodymium-iron-boron (NdFeB) permanent magnets for electric machines, such as electric vehicle (EV) traction motors, wind power generators, drones, robotics, electronics, and other applications. Given the wide-ranging uses of these component materials in critical infrastructure essential for national security and economic growth, the U.S. government has taken an interest in industry concentration.

Figure 2: Rare Earth Applications

Source: National Energy Technology Laboratory

According to the 2024 edition of the Energy Institute Statistical Review of World Energy, China accounted for 67.9% of rare earth mineral production in 2023 and 38.1% of rare earth mineral reserves. Conversely, the United States accounted for 12.2% of rare earth mineral production in 2023 and 1.6% of rare earth mineral reserves.

Figure 3: Rare Earth Metals Production and Reserves

Source: Energy Institute Statistical Review of World Energy 2024

Supply Chain and Pricing Overview

The supply chain for rare earths includes upstream, midstream, and downstream components.

Figure 4: Rare Earth Element Supply Chain

Source: Critical Materials Rare Earths Supply Chain: A Situational White Paper, U.S. Department of Energy, Office of Energy Efficiency & Renewable Energy, April 2020

As illustrated in Figure 4, concentration or beneficiation is an extractive metallurgy process that upgrades the value of mineral ores that contain raw REEs by removing low value minerals and resulting in a higher-grade product such as rare-earth concentrate.

Separation is the process of separating individual REEs from one another in the rare earth oxide (REO) concentrates. Separation of REEs is chemically intensive because the REEs are chemically similar. Processing refers to the conversion of REOs to rare earth metals, such as neodymium metal which can then be used to form alloys. China controls most of the midstream separating and processing capacity.

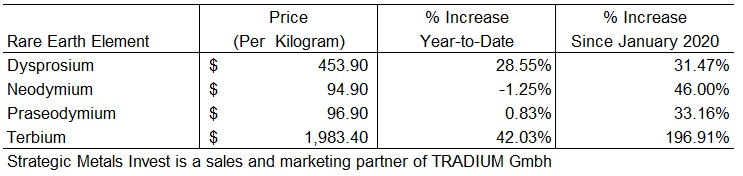

There is no single price for REEs collectively, but numerous prices for REE oxides and compounds individually. Pricing information for rare earths is opaque and generally available by paid subscription. Public information is generally not comprehensive and generally does not provide detailed information as to quality and origin, which makes comparisons difficult. Below we have provided a pricing sample of the most valuable elements as of June 11, 2025.

Figure 5: Pricing Data for Select Rare Earth Elements (REE)

Source: Strategic Metals Invest

U.S. Rare Earth Element Market

According to the U.S. Department of the Interior, the estimated value of rare-earth compounds and metals imported by the United States in 2023 was $190 million, down 7% from $208 million in 2022. Catalysts represented the leading domestic end use for rare earths, followed by applications in ceramics and glass, metallurgical alloys, polishing, and embedded permanent magnets in finished goods. While rare earth recycling is expected to grow in the coming years, current recovery rates from sources such as batteries and permanent magnets remain limited. The table below provides some statistics associated with the rare earths market in the United States.

Figure 6: United States REE Market Statistics

Source: Mineral Commodity Summaries 2024, U.S. Department of the Interior, U.S. Geological Survey

Given the United States’ reliance on imports, we think Canadian producers stand to benefit from a shift away from sources in China. As processing capabilities are developed, the U.S. could be an important destination for Canada sourced materials.

Key REE Market Participants

The global rare earth industry remains defined by a limited number of dominant players, most of which are concentrated in China. China Northern Rare Earth Group (SHH: 600111), and China Minmetals are the largest vertically integrated producers, with strong government alignment and control over both upstream mining and midstream separation capacity. These firms benefit from large-scale infrastructure, domestic demand, and preferential access to processing technology that remains restricted from foreign use.

Outside China, Lynas Rare Earths (ASX: LYC, OTC: LYSDY), in Australia is the largest fully integrated producer, with upstream operations at Mount Weld and a separation plant in Malaysia. Lynas is expanding into heavy rare earth processing in Texas through a strategic partnership with the U.S. Department of Defense.

MP Materials, the most significant rare earth materials producer in the United States, completed a business combination with Fortress Value Acquisition Corp., a special purpose acquisition company and began trading on the New York Stock Exchange on November 18, 2020, under the ticker MP. MP Materials owns and operates the Mountain Pass rare earth mine and processing facility in California which opened in 1952 as a uranium producer, pivoted to one of the largest suppliers of rare earth minerals, but closed in 2002 as environmental restrictions and imports made it difficult to compete. The facility underwent various ownership changes and reopened in 2017 under MP Materials’ ownership. It is North America’s only active and scaled rare earth production site and now has a market capitalization of $4.1 billion as of June 11, 2025.

The Mountain Pass mine in California and is the only active rare-earth mine in the United States. The company has restarted oxide production and is building refining and alloying capacity in Texas. MP has signed multi-year offtake agreements with original equipment manufacturers (OEMs), including General Motors, aimed at creating a vertically integrated domestic supply chain. However, the company still relies on China to assist in the separation process for some of its output, underscoring the current U.S. capabilities gap.

Additional participants working to expand non-Chinese supply chains include Iluka Resources (ASX: ILU, OTC: ILKAF) and Arafura Rare Earths (ASX: ARU, OTC: ARAFF), both based in Australia. Iluka is building a new facility with support from the Australian government, aimed at handling all stages of rare earth production. Arafura is also developing a new project with backing from international lenders, focused on supplying materials used in magnets for electric motors and other technologies. On the downstream side, magnet production is dominated by firms such as Shin-Etsu (TSE: 4063, OTC: SHECY), Hitachi Metals, and JL MAG (SZSC: 300748, OTC: JMREY), with capacity heavily skewed toward Asia. Efforts among U.S. and allied countries to establish domestic magnet manufacturing are progressing but remain in the early stages.

China dominates the production of many critical minerals, including rare earth elements. There appears to be an awakening among U.S. policy makers of the dangers of dependence on foreign sources for critical minerals, especially those that are adversarial to the United States. We believe a shift is underway to source REEs from countries that are friendly to the United States, including Canada. As part of its strategy to ensure secure and reliable supplies of critical minerals, the U.S. Department of the Interior identified 35 critical minerals, including the rare earth elements group. The U.S. Government is planning to fund rare earths projects to reduce reliance on China. In January 2022, bipartisan legislation was introduced, the Restoring Essential Energy and Security Holdings Onshore for Rare Earths Act, to protect the U.S. from the threat of rare-earth element supply disruptions, encourage domestic production, and reduce reliance on China. REEs are found in mineral deposits such as bastnaesite and monazite, the two largest sources of REEs. Bastnaesite, a carbonate-fluoride mineral, typically contains cerium, lanthanum, neodymium, and praseodymium. Monazite, a phosphate mineral, typically contains cerium, lanthanum, neodymium, and samarium. Rare earths are mined domestically in the United States. Bastnaesite is extracted at the mine in Mountain Pass, California.

Since January 2025, the Trump administration has significantly expanded its strategic focus on rare earth supply chain security. In April, an executive order initiated an investigation into whether U.S. dependence on foreign sources of rare earths constitutes a national security threat. An additional order opened up new offshore exploration zones for critical minerals, including seabed areas believed to contain rare earth and battery metals.

Furthermore, the administration has invoked the Defense Production Act to allocate capital and permit support to midstream and downstream segments of the rare earth supply chain. MP Materials began producing rare earth metals at its Texas facility, while Lynas advanced its U.S. processing plant with support from the Department of Defense. These efforts are part of a broader strategy to rebuild U.S. capabilities across the rare earth value chain.

International partnerships have also gained momentum. The U.S. is advancing cooperation with Australia, Canada, and Ukraine to secure alternative sources of supply and coordinate project financing through the Minerals Security Partnership. A bilateral agreement with Ukraine is expected to facilitate exploration and development of new deposits, while Australia remains a primary ally for both upstream mining and technical collaboration.

Outlook

The rare earth industry is entering a period of strong growth and growing strategic relevance. According to the International Energy Agency (IEA), magnet-grade rare earth demand could double by 2050, and mining projects could rise by 52% by 2040, under current policy (IEA, Critical Minerals Report, 2024). These forecasts are driven by growth in electric vehicle drivetrains, offshore wind development, and precision defense systems, all of which rely heavily on rare earth magnets for performance, efficiency, and miniaturization. As a result, rare earths have transitioned from niche industrial inputs to core strategic resources.

Figure 7: REE Demand Outlook and Mining Requirements (kt REE)

Source: Global Critical Minerals Outlook 2024, International Energy Agency (IEA)

We note that the IEA’s forecasts are based on three scenarios. These include: 1) the Stated Policies Scenario (STEPS), 2) the Announced Pledges Scenario (APS), and 3) the Net Zero Emissions by 2050 Scenario (NZE). The Stated Policies Scenario is based on current policy settings. The Announced Pledges Scenario assumes that governments will meet all climate-related commitments they have announced, including net zero emissions targets. The Net Zero Emissions by 2050 Scenario represents a pathway for the global energy sector to achieve net zero carbon dioxide emissions by 2050. These are summarized, of course, and readers may consult the IEA’s report for a more detailed description.

In the short term, challenges will continue to shape how supply chains evolve outside of China. Most new projects in Western countries face long approval timelines due to environmental reviews, local opposition, and infrastructure gaps. While government funding and procurement support are improving, the limited availability of midstream processing remains a key constraint.

In our view, rare earths are evolving from niche industrial inputs to foundational resources for advanced economies. Although the industry currently operates at a scale that lags its growing strategic importance, recent policy momentum and expanded investment across allied nations are setting the stage for meaningful transformation. Looking ahead, we expect a more balanced and resilient global supply chain to emerge—anchored by deepening cooperation between the United States, Canada, Australia, and European partners. While China will remain a major player in the near term, the diversification of supply chains is gaining traction, signaling a shift toward greater self-sufficiency and long-term security among like-minded nations.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest

Key Points: – Oil prices jumped over 4% after reports of a partial U.S. embassy evacuation in Iraq raised geopolitical concerns. – Additional support came from President Trump’s doubts over a nuclear deal with Iran, potentially limiting future oil supply. – A breakthrough in U.S.-China trade talks also boosted sentiment, helping crude extend its recent rally.

Crude oil prices soared on Wednesday, climbing more than 4% amid escalating geopolitical tensions and renewed concerns over global supply disruptions. The sharp move followed reports that the U.S. embassy in Baghdad is preparing for a partial evacuation due to rising security threats.

West Texas Intermediate (WTI) crude futures closed at $68.15 per barrel, up 4.5%, while Brent crude, the global benchmark, settled at $69.77, a gain of 4%. The rally reflects growing unease in energy markets over the stability of the Middle East, a region critical to global oil production and transportation.

The price spike was triggered by a Reuters report indicating that U.S. and Iraqi officials are coordinating plans for an “ordered departure” of embassy personnel in Iraq. The development comes amid mounting threats in the region, raising fears that oil infrastructure or transportation routes could be impacted if tensions escalate further.

In addition to the embassy-related concerns, oil prices were also supported by comments from President Donald Trump, who expressed skepticism over the prospects of reaching a new nuclear agreement with Iran — a major oil-producing nation. Speaking during a podcast, Trump said his confidence in a deal had “diminished,” casting doubt on the potential return of sanctioned Iranian barrels to the market.

Oil prices found further support from signs of easing trade tensions between the U.S. and China. Following high-level discussions in London, both nations reportedly agreed to a framework aimed at reducing tariffs and improving trade flows. President Trump hinted that a formal agreement could be imminent, pending final approval from Chinese President Xi Jinping.

The latest surge adds to a month-long recovery in oil prices, which have rebounded from a sharp sell-off in April driven by global economic concerns and softer demand projections. Despite the rebound, both WTI and Brent remain down year-to-date, reflecting the broader market’s caution around demand durability and geopolitical risk.

Analysts are closely watching developments in the Middle East and diplomatic signals from Washington and Beijing, noting that any further escalation or policy shifts could significantly impact global supply dynamics in the weeks ahead

Toronto, Ontario–(Newsfile Corp. – June 11, 2025) – Aurania Resources Ltd. (TSXV: ARU) (OTCQB: AUIAF) (FSE: 20Q) (“Aurania” or the “Company”) reports on a resolution recently put forth by the Ecuadorian Control and Regulation Agency (“ARCOM” for its Spanish acronym) related to a new administrative fee on the mining sector. This resolution has not yet been published in the Official Registry, and therefore, to our knowledge is not yet in effect.

The intention of this resolution is for all participants in the mining/exploration industry in Ecuador to fund ARCOM’s efforts to stop illegal mining, strengthen oversight, and enhance the operational capacity of ARCOM.

The document provides assessments of the amount each mining/exploration company is expected to pay based on the type of regime, size of concessions and stage of exploration. As presented, this proposed fee would require the Company to pay approximately US$24 million this year by July 31st. This figure is insupportable and represents approximately ten times the amount the Company pays for its annual concession fees in Ecuador.

The Company is collaborating with the Mining Chamber of Ecuador’s legal commission and all other mining/exploration companies in Ecuador, to ensure that relevant authorities understand that this fee is not feasible and will likely place the whole mining/exploration industry in Ecuador at risk. If the resolution is implemented as currently outlined, the regulation would result in an unsustainable cost burden for companies operating within the sector and may undermine confidence in Ecuador’s regulatory consistency and commitment to mining development.

The Company has reached out to the Ecuadorian Government at the highest levels and will continue in discussions with the Mining Chamber of Ecuador and the Company’s respective legal counsels as joint industry efforts are taking place to prevent this regulation from being implemented. The Company will assess options for further courses of action.

About Aurania

Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and copper in South America. Its flagship asset, The Lost Cities – Cutucu Project, is located in the Jurassic Metallogenic Belt in the eastern foothills of the Andes mountain range of southeastern Ecuador.

Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

Forward Looking Statements

This news release contains forward-looking information as such term is defined in applicable securities laws, which relate to future events or future performance and reflect management’s current expectations and assumptions. The forward-looking information includes statements regarding the ARCOM resolution, its impact on the Company and the mining sector in Ecuador, and Aurania’s objectives, goals and future plans in light of the ARCOM resolution. Such forward-looking statements reflect management’s current beliefs and are based on assumptions made by and information currently available to Aurania, including the current status of the ARCOM resolution and the interpretation of the application of the resolution. Investors are cautioned that these forward-looking statements are neither promises nor guarantees and are subject to risks and uncertainties that may cause future results to differ materially from those expected. Risk factors that could cause actual results to differ materially from the results expressed or implied by the forward-looking information include, among other things, the failure of efforts to dissuade the relevant authorities to proceed with the ARMCOM resolution, the publication of the ARCOM resolution in its current form, an application of the ARCOM resolution of more severe consequences than currently understood and a lack of options for further courses of action, including legal action which would not provide appropriate relief and, generally, the additional risks identified in our filings with Canadian securities regulators on SEDAR+ (available at www.sedarplus.ca). Aurania cautions the reader that the above list of risk factors is not exhaustive. Although the Company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause results not to be as anticipated, estimated, described, or intended. Investors are cautioned against undue reliance on forward-looking statements or information. These forward-looking statements are made as of the date hereof and, except as required by applicable securities regulations, the Company does not intend, and does not assume any obligation, to update the forward-looking information.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

LIFE offering. Century Lithium has commenced an offering, under the Listed Issuer Financing Exemption (LIFE), to raise a minimum of C$2,000,000 and a maximum of C$5,000,000 with an offering of up to 16,666,667 units at a price of C$0.30 per unit. Each unit will consist of one common share and one common share purchase warrant. Each warrant entitles the holder to purchase one common share at an exercise price of C$0.45 for a period of 24 months following the issuance of the units. After selling commissions, fees, and estimated offering costs, the company expects to receive net proceeds of C$1,810,000 to C$4,600,000.

Use of net proceeds. Net proceeds from the financing will be used to complete an updated feasibility study for the company’s Angel Island Lithium Project, complete the project’s Plan of Operations, work towards National Environmental Policy Act (NEPA) compliance, and general working capital. The offering is expected to close on or about July 7 and is not expected to close in tranches.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Treasure Mountain. Nicola Mining’s (TSX.V: NIM, OTCQB: HUSIF) Treasure Mountain Project is a 100% owned high-grade silver, lead, and zinc past-producing underground mine located 29 kilometers northeast of Hope, British Columbia. It offers significant exploration potential and has a valid permit (M-239) for mining operations through April 26, 2032, that permits the company to mine up to 60,000 tonnes per year. The company holds 31 contiguous mineral claims over an area of approximately 2,200 hectares and one mining lease covering 335 hectares, including 248 hectares of historic workings.

Receipt of exploration permit. On June 4, Nicola Mining received a multi-year area-based (MYAB) exploration permit to conduct extensive exploration at Treasure Mountain. The MYAB permit allows the company to carry out exploration activities, including 30 drill holes, 1,400 meters of trenching, 4,500 meters of trail building, and 20 kilometers of geophysical surveys over the next five years within certain boundaries of the project.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Amended agreement with Mackay Precious Metals. Comstock Inc. amended the membership interest purchase agreement to sell 100% of its northern most patented and unpatented mining claims, mineral exploration rights and town lots owned by Comstock Northern Exploration, LLC, plus the 25% issued and outstanding membership interest that Comstock owns in Pelen LLC to Mackay Precious Metals Inc. Consideration includes $2.95 million in cash plus a 1.5% NSR production royalty associated with the properties.

More favorable terms. The amendment increases the sale price to $2.95 million in cash from the previous $2.75 million in both cash and stock, thus increasing the cash component of the transaction by $1.2 million. Comstock previously received $1.0 million in cash. The remaining $1.95 million is due in a series of payments in June, July, and ending on or before August 30. Additionally, Mackay will transfer approximately 300 acres of patented and unpatented mining properties in Lyon County, Nevada, that are adjacent to and expand the area of Comstock’s Dayton Consolidated and Spring Valley mineral claims and lands for no consideration.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

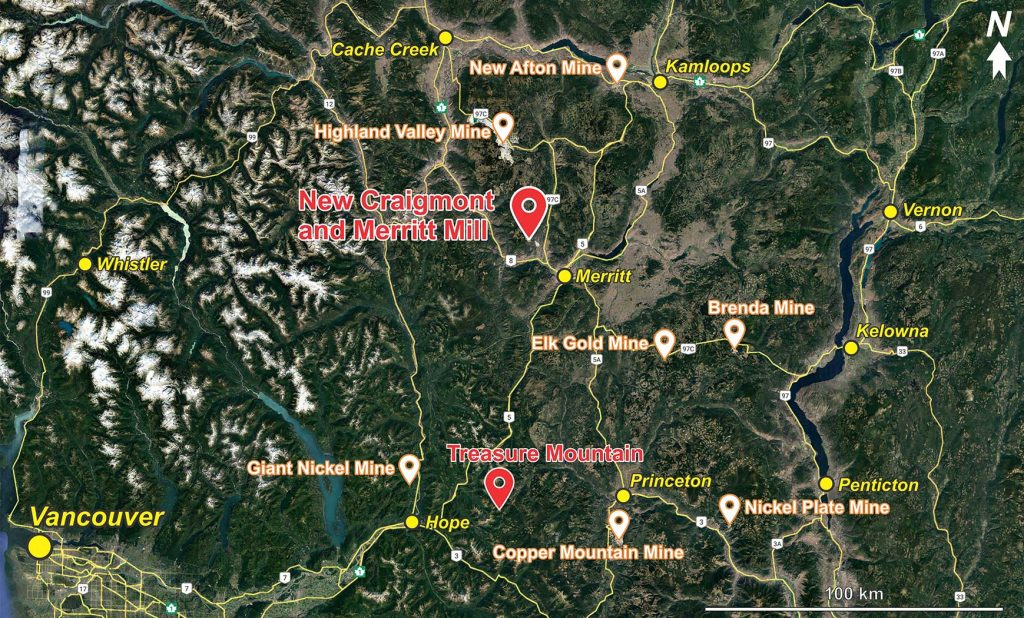

VANCOUVER, BC, June 9, 2025 – Nicola Mining Inc. (the “Company” or “Nicola”) (TSX: NIM) (OTCQB: HUSIF) (FSE: HLIA) is pleased to announce that it has received a multi-year area-based exploration permit, Permit Number MX-15-121 (the “MYAB Permit”) on June 4th, 2025. The MYAB Permit allows Nicola to conduct extensive exploration on its wholly owned Treasure Mountain Silver Project[1] (the “Treasure Mountain”), a fully permitted silver mine (Permit 239) located 30 km northeast of Hope and about a 3-hour drive from Vancouver, British Columbia (Fig. 1).

Figure 1. Treasure Mountain location

Receipt of the MYAB Permit, follows the Company’s August 30th, 2024, announcement that it had received a ten-year mining lease extension (the “Extension”) for Treasure Mountain[2] under its M-239 permit. The Extension is valid through April 26, 2032, and receipt of the MYAB Permit positions the Company to leverage both mining and exploration options.

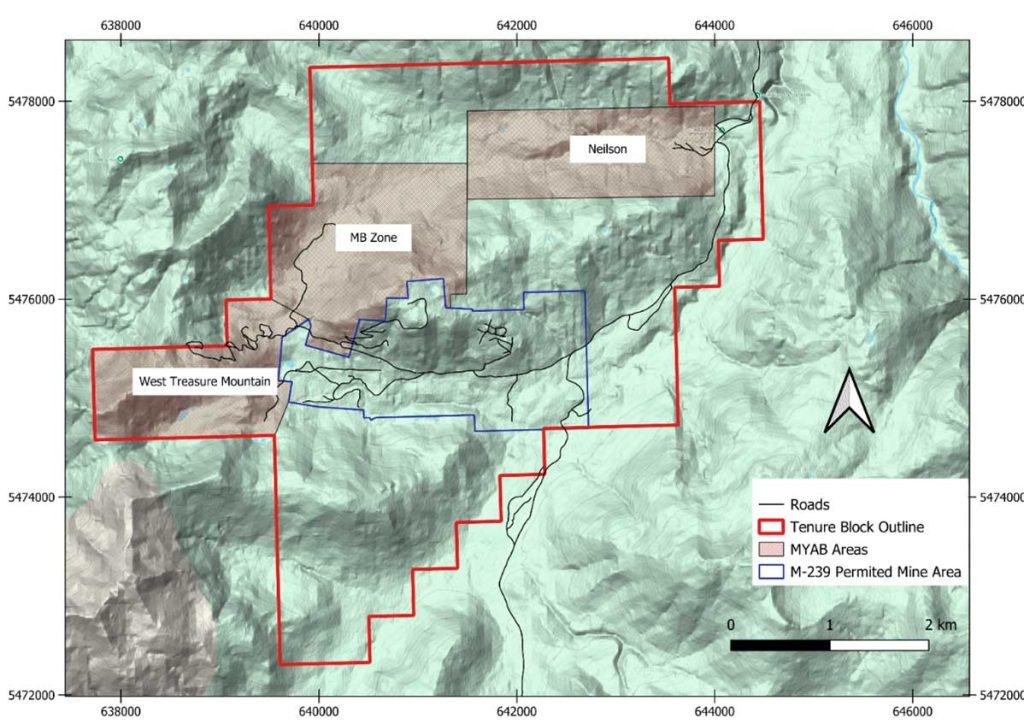

Treasure Mountain consists of an historic underground silver mine with a resource estimate in accordance with CIM definition standards[3] and exploration upside to the north and west of the historic mine. The MB Zone is approximately 800 m northwest of the current mine workings on undrilled northern flank of the mountain. The Cal Vein was discovered at this location in 2010 and return a surface sample grading as high as 9,221g/t Ag, 1.02% Cu, 1.14% Pb and 1.03% Zn[4]. Subsequent soil sampling was conducted in 2011/2012 and 2013 with encouraging results.[5] Small exploration programs conducted between 2019 and 2021 on the northwestern side of the mountain included soil sampling, rock sampling, mapping, and shallow drilling campaigns. These programs successfully identified a 2 km soil anomaly which appears to be related to a vein system of roughly the same strike length. Drill testing of the exposed vein confirmed continuity of mineralization coincidental with the soil anomaly.[6]

The MYAB Permit allows the Company to carry out the following exploration activities over the next five years in the areas shown below (Fig. 2):

30 drill holes

1,400 m of trenching

4,500 m of trail building

20 km of geophysical surveys with exposed electrodes

Figure 2. Site map with MYAB Permit boundaries

Peter Espig, CEO of Nicola Mining Inc., commented, “Receipt of the MYAB under Permit Number MX-15-121 coupled with our recently received ten-year mine life extension under Permit M-239, puts Nicola into an envious position as the confluence of mine and exploration potential brings forth a project that most investors have forgotten. Bolstered by solid silver prices and with permits in hand, we are very excited about its potential and look forward to exploring our Treasure Mountain Project for the first time in over a decade”

Qualified Person

William Whitty, P. Geo., the Company’s VP Exploration, is the Qualified Person as defined by National Instrument 43-101 – Standards of Disclosure for Mineral Projects and supervised the preparation of, and has reviewed and approved the technical information in this release.

About Nicola Mining

Nicola Mining Inc. is a junior mining company listed on the TSX-V Exchange and Frankfurt Exchange that maintains a 100% owned mill and tailings facility, located near Merritt, British Columbia. It has signed Mining and Milling Profit Share Agreements with high-grade BC-based gold projects. Nicola’s fully permitted mill can process both gold and silver mill feed via gravity and flotation processes.

The Company owns 100% of the New Craigmont Project, a property that hosts historic high-grade copper mineralization and covers an area of over 10,800 hectares along the southern end of the Guichon Batholith and is adjacent to Highland Valley Copper, Canada’s largest copper mine. The Company also owns 100% of the Treasure Mountain Property, which includes 30 mineral claims and a mineral lease, spanning an area exceeding 2,200 hectares.

On behalf of the Board of Directors

“Peter Espig”

Peter Espig

CEO & Director

For additional information

Contact: Peter Espig

Phone: (778) 385-1213

Email: info@nicolamining.com

URL: www.nicolamining.com

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

VANCOUVER, BC, June 4, 2025 – Nicola Mining Inc. (the “Company” or “Nicola”) (TSX: NIM) (OTCQB: HUSIF) (FSE: HLIA) is pleased to announce that it has hired Vicente García as Senior Geologist. His experience is expected to deepen the Company’s copper porphyry expertise, as it commences an aggressive 2025 exploration program.

Mr. García has over seven years of exploration experience across porphyry Cu-Mo, IOCG, stratabound-copper, epithermal gold-silver, and lithium-rich brine systems. He holds a B.Sc. in Geology from the University of Concepción in Chile. After graduating, he worked for several years with Kura Minerals, an exploration consulting company, where he was involved in programs targeting a variety of commodities. He later joined Quiborax, where he focused on the exploration of Ulexite in salar environments. In 2020, he founded Mayal Exploration, a consulting company through which he provided geological services including drill core re-logging, surface mapping, and 3D geological modeling for various mining clients in Chile. In 2022, Mr. García relocated to Canada and joined Dahrouge Geological Consulting, contributing to Ni-Cu sulfide and lithium pegmatite exploration projects in the Timmins region of Ontario and the James Bay area of Quebec. Before joining Nicola Mining, he worked at Anglo American, where he supported international exploration programs targeting Cu-Mo porphyry systems in Arizona and orthomagmatic Ni-Cu-PGE systems in Greenland. Mr. García’s experience and technical knowledge is a valuable addition to Nicola’s exploration team.

Peter Espig, CEO of Nicola Mining Inc., commented, “Nicola continues to aggressively execute on both operations and exploration. Recently, the Company has garnered significant media relating to gold and silver production; however, we truly believe in the copper exploration upside of our New Craigmont Project. In addition, Vincente and Will Whitty, our VP of Exploration, will look at conducting exploration on the backside of our fully permitted Treasure Mountain Silver Mine. We look forward to providing a news explanation on our 2025 Exploration Plan at the New Craigmont Project in the near future.”

Qualified Person

William Whitty, P. Geo., the Company’s VP Exploration, is the Qualified Person as defined by National Instrument 43-101 – Standards of Disclosure for Mineral Projects and supervised the preparation, review and has also approved the technical information in this release.

About Nicola Mining

Nicola Mining Inc. is a junior mining company listed on the TSX-V Exchange and Frankfurt Exchange that maintains a 100% owned mill and tailings facility, located near Merritt, British Columbia. It has signed Mining and Milling Profit Share Agreements with high-grade BC-based gold projects. Nicola’s fully permitted mill can process both gold and silver mill feed via gravity and flotation processes.

The Company owns 100% of the New Craigmont Project, a property that hosts historic high-grade copper mineralization and covers an area of over 10,800 hectares along the southern end of the Guichon Batholith and is adjacent to Highland Valley Copper, Canada’s largest copper mine. The Company also owns 100% of the Treasure Mountain Property, which includes 30 mineral claims and a mineral lease, spanning an area exceeding 2,200 hectares.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First quarter 2025 financial results. Nicola Mining (TSX.V: NIM, OTCQB: HUSIF) reported a first quarter 2025 loss of C$475,808 or C$(0.00) per share compared to a loss of C$1,028,129 or $(0.01) per share during the prior year period. We had projected a loss of C$1,044,879 or C$(0.01) per share. The variance to our estimates was largely due to a gain on marketable securities. We increased our 2025 net income and EPS estimates to C$8,803,755 and C$0.05 per share, respectively, from C$7,724,367 and C$0.04. We updated our commodity grade assumptions, along with higher metals price estimates based on actual April and May pricing and CME futures settlements for the remainder of the year.

Mill operations to commence shortly. We expect Nicola Mining to commence milling operations on or around June 15. On May 11, Talisker Resources Ltd. (TSX: TSK, OTCQX: TSKFF) began trucking run of mine material from its Mustang Mine to Nicola’s Craigmont Mill in British Columbia. Approximately 2,000 tonnes of ore had been delivered as of June 1, and we expect a stockpile of 2,500 to 3,000 tonnes prior to the mill commencing operations.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Annual general meeting. Aurania Resources will host its Annual Meeting of Shareholders at 1:30 pm ET on Thursday, June 12. Shareholders will vote to elect directors, appoint McGovern Hurley LLP as auditor for the ensuing year, and approve Aurania’s incentive stock option plan. Dr. Keith Barron, Chairman, President, and CEO, is expected to provide a brief update on activities following the formal part of the meeting. Aurania will provide a link to a video and/or audio replay of Dr. Barron’s update.

First quarter financial results. As an exploration company, Aurania does not generate revenue and incurs costs to advance its projects. During the first quarter, the company reported a net loss of C$5,106,264 or C$(0.05) per share compared to a loss of C$4,736,264 or C$(0.07) per share during the prior year period. Weighted average shares outstanding increased to 104,168,397 compared to 67,471,7737 during the first quarter of 2024. Exploration expenditures increased to C$3,949,010 compared to C$3,536,819 during the prior year period to fund activities in both Ecuador and France.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Aura Minerals to buy Serra Grande gold mine from AngloGold for $76M plus royalties. – The mine has produced 3M+ oz of gold, with Aura aiming to boost output and cut costs. – Deal set to close by late 2025, pending regulatory and operational approvals.

Aura Minerals Inc. has announced a major step in its growth trajectory with the acquisition of the Mineração Serra Grande (MSG) gold mine from AngloGold Ashanti, in a deal that could significantly reshape the company’s position in Brazil’s mining sector. The transaction, valued at an upfront $76 million plus a 3% net smelter return on existing resources, reflects Aura’s confidence in the long-term potential of this historically productive asset.

Located near Crixás in the northwest of Goiás, Brazil, Serra Grande has been a cornerstone of AngloGold’s Brazilian portfolio, producing over 3 million ounces of gold since 1998. With three underground mines, an open-pit operation, and a metallurgical plant boasting a capacity of 1.5 million tonnes per year, the site is well-established. The acquisition marks Aura’s strategic return to a familiar asset – several team members have prior experience with Serra Grande, positioning them to optimize its future operations.

Rodrigo Barbosa, Aura’s President and CEO, emphasized the transformative potential of the deal. “Through our disciplined capital allocation, Aura 360 culture, and a targeted exploration program, we believe we can significantly enhance performance, boost production, reduce costs, and extend the Life of Mine at Serra Grande,” Barbosa said. He also hinted at ambitions to make Serra Grande a new cornerstone in Aura’s diversified portfolio, which already includes operations across Brazil, Mexico, and Central America.

However, the acquisition comes with conditions. It is contingent upon antitrust approval from Brazilian authorities (CADE), the completion of a legacy tailings dam decommissioning, and a corporate restructuring to spin off certain non-core subsidiaries of MSG. Barring unforeseen delays, Aura expects to finalize the deal by the third or fourth quarter of 2025.

From a technical standpoint, AngloGold’s last reported resource statement (Dec. 2024) estimated over 1 million ounces of Measured and Indicated gold resources, with an additional 1.4 million ounces classified as Inferred. While Aura considers these numbers as “historical estimates” and not compliant with Canadian NI 43-101 reporting standards, they highlight the untapped potential of the site. Aura plans to verify and potentially expand these resources through further exploration and technical work.

This acquisition reflects broader trends in the gold mining industry: mid-tier players like Aura are increasingly seizing opportunities to acquire under-optimized assets from global majors. The shift also demonstrates growing investor appetite for junior and mid-cap miners with clear value creation plans.

By reinvigorating a legacy operation with fresh capital, experienced leadership, and its unique Aura 360 philosophy—which balances profitability with environmental and social responsibility—Aura is making a bold statement. If successful, Serra Grande could represent not just an increase in output, but a model for revitalizing aging mining assets across Latin America.

As global gold demand remains resilient and macroeconomic uncertainty supports strong prices, Aura’s calculated risk may well pay off, cementing its role as a nimble and forward-looking player in the mining industry.

Toronto, Ontario–(Newsfile Corp. – May 29, 2025) – Aurania Resources Ltd. (TSXV: ARU) (OTCQB: AUIAF) (FSE: 20Q) (“Aurania” or the “Company”) announces that its Annual and Special Meeting of Shareholders (the “Meeting”) will be held at 1:30pm ET on Thursday, June 12, 2025, at the Company’s offices at 8 King Street East, Suite 1800, Toronto, ON M5C 1B5.

Aurania’s President & CEO, Dr. Keith Barron, is planning to provide a brief update on activities following the formal part of the Meeting. The Company expects to provide a link to a video and/or audio replay of Dr. Barron’s update sometime following the Meeting.

Proxy Voting Deadline To ensure your vote is counted, please cast your vote prior to Tuesday, June 10th, 2025, at 1:30pm ET as per the details in your form of proxy. Meeting materials can be found on Aurania’s website under the Annual General Meeting tab.

Financial Statements and MD&A (Management’s Discussion & Analysis) Aurania’s interim financial statements and MD&A for three months ended March 31, 2025, are available on SEDAR+ and the Company’s website.

About Aurania Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and copper in South America. Its flagship asset, The Lost Cities – Cutucu Project, is located in the Jurassic Metallogenic Belt in the eastern foothills of the Andes mountain range of southeastern Ecuador.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.