Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

GLSI-100 Received Fast Track Designation. Greenwich LifeSciences announced that GLSI-100 has received Fast Track designation from the FDA. In the near term, this designation allows GLSI increased communications and more FDA meetings regarding regulatory requirements for its clinical trial data and use of biomarkers. Once the FLAMINGO-01 trial is completed, GLSI will be eligible to apply for Accelerated Approval and Priority Review, potentially shortening the time to market.

The Designation Mirrors The Trial Entry Criteria. GLSI-100 has received Fast Track Designation from the FDA for the treatment of “patients with HLA-A*02 genotype and HER2-positive breast cancer who have completed treatment with standard of care HER2/neu targeted therapy to improve invasive breast cancer free survival…” This includes the clinical trial entry criteria and endpoints for the current double-blind arms of the trial.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Euroseas Ltd. was formed on May 5, 2005 under the laws of the Republic of the Marshall Islands to consolidate the ship owning interests of the Pittas family of Athens, Greece, which has been in the shipping business over the past 140 years. Euroseas trades on the NASDAQ Capital Market under the ticker ESEA. Euroseas operates in the container shipping market. Euroseas’ operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company, which is responsible for the day-to-day commercial and technical management and operations of the vessels. Euroseas employs its vessels on spot and period charters and through pool arrangements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New time charter contract. Euroseas Ltd. announced a new time charter for the M/V Jonathan P at a gross daily rate of $25,000 for a minimum of 11 months, with an option to extend to a maximum of 12 months at the charterer’s option. The charter will commence on November 17th.

Attractive rate and improved charter coverage. The new contract is in direct continuation of the current charter and represents a $5,000 per day increase. It is expected to contribute approximately $5.7 million in EBITDA over the minimum contract period and raise Euroseas’ charter coverage to 100% for the remainder of 2025 and 70% for 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

$4.7 million upfront with up to an additional approximately $8.3 million of potential aggregate gross proceeds upon the exercise in full of warrants

BOTHELL, Wash., Sept. 12, 2025 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc., (Nasdaq: COCP) (the “Company” or “Cocrystal”), today announced that it has entered into definitive agreements for the purchase and sale of 2,764,710 shares of its common stock (or common stock equivalents in lieu thereof) at a purchase price of $1.70 per share in a registered direct offering priced at-the-market under Nasdaq rules. In a concurrent private placement, the Company will issue unregistered warrants to purchase up to 5,529,420 shares of common stock at an exercise price of $1.50 per share that will be exercisable upon issuance and will expire twenty-four months from the effective date of the registration statement covering the resale of the shares of common stock issuable upon exercise of the unregistered warrants. The closing of the offering is expected to occur on or about September 15, 2025, subject to the satisfaction of customary closing conditions.

H.C. Wainwright & Co. is acting as the exclusive placement agent for the offering.

The gross proceeds to the Company from the offering, before deducting the placement agent’s fees and other offering expenses payable by the Company, are expected to be approximately $4.7 million. The potential additional gross proceeds to the Company from the warrants, if fully-exercised on a cash basis, will be approximately $8.3 million. No assurance can be given that any of such short-term warrants will be exercised. The Company intends to use the net proceeds from this offering for working capital and general corporate purposes.

The common stock (or common stock equivalents in lieu thereof, but not the unregistered warrants and the shares of common stock underlying the unregistered warrants) described above are being offered by the Company pursuant to a “shelf” registration statement on Form S-3 (File No. 333-271883) that was declared effective by the Securities and Exchange Commission (the “SEC”) on May 26, 2023. The offering of the shares of common stock is being made only by means of a prospectus, including a prospectus supplement, forming a part of the effective registration statement. A final prospectus supplement and accompanying prospectus relating to the registered direct offering will be filed with the SEC. Electronic copies of the final prospectus supplement and accompanying prospectus may be obtained, when available, on the SEC’s website at http://www.sec.gov or by contacting H.C. Wainwright & Co., LLC at 430 Park Avenue, 3rd Floor, New York, New York 10022, by phone at (212) 856-5711 or e-mail at placements@hcwco.com.

The unregistered warrants described above are being offered in a private placement under Section 4(a)(2) of the Securities Act of 1933, as amended (the “Securities Act”), and/or Regulation D promulgated thereunder and, along with the shares of common stock underlying such unregistered warrants, have not been registered under the Securities Act, or applicable state securities laws. Accordingly, the unregistered warrants and underlying shares of common stock may not be offered or sold in the United States except pursuant to an effective registration statement or an applicable exemption from the registration requirements of the Securities Act and such applicable state securities laws.

This press release shall not constitute an offer to sell or a solicitation of an offer to buy any of the securities described herein, nor shall there be any sale of these securities in any state or other jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such state or other jurisdiction.

About Cocrystal Pharma, Inc.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company that addresses significant unmet needs by developing innovative antiviral treatments for challenging diseases including influenza, viral gastroenteritis, COVID, and hepatitis. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs.

Forward-Looking Statements

The information in this press release includes “forward-looking statements.” Any statements other than statements of historical fact contained herein, including statements as to the completion of the offering, the satisfaction of customary closing conditions related to the offering and the intended use of net proceeds from the offering, are forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “could”, “might”, “plan”, “possible”, “project”, “strive”, “budget”, “forecast”, “expect”, “intend”, “will”, “estimate”, “anticipate”, “believe”, “predict”, “potential” or “continue”, or the negatives of these terms or variations of them or similar terminology.

The Russell 2000 Index, which tracks smaller and riskier U.S. companies, has staged an impressive rally in recent weeks — and analysts believe the momentum could last well into the next 12 months.

Since the end of July, the Russell 2000 has climbed nearly 10%, more than double the advance of the S&P 500. Wall Street strategists see room for an additional 20% gain in the index over the next year, compared to expectations of an 11% rise in the broader S&P 500, according to Bloomberg data.

The outlook is notable given small caps’ underperformance in recent years. Since 2020, the Russell 2000 has consistently lagged behind large-cap peers. Even after the latest rebound, the index trails the S&P 500 for 2025. However, analysts argue that a shift in monetary policy could change the dynamic.

With the Federal Reserve expected to begin cutting interest rates, borrowing costs for smaller firms are likely to ease, providing a meaningful boost to margins. Because companies in the Russell 2000 are more sensitive to credit conditions, lower rates could spark renewed investor interest and broaden a bull market that has so far been led by large-cap names.

Recent market reactions highlight the trend. After new inflation and jobs data reinforced expectations for Fed rate cuts, the Russell 2000 rose 1.2% in a single session, outpacing the S&P 500’s 0.7% gain. Investors appear to be positioning for an extended period of small-cap outperformance.

Corporate earnings are also helping the case. In the second quarter, more than 60% of Russell 2000 companies beat profit forecasts, with average revenue growth surpassing expectations by 130 basis points. Stronger earnings, combined with rate cuts and attractive valuations, provide what some strategists describe as a compelling setup for small-cap equities.

Valuations remain a central theme. While the Russell 2000’s price-to-earnings ratio has risen to slightly above its long-term average following the recent rally, the index still trades at a wide discount to large-cap stocks. This valuation gap, coupled with improved sentiment, suggests further upside potential.

Options activity reflects the growing bullish stance. Data from Cboe Global Markets indicates stronger demand for upside calls on the Russell 2000 than on the S&P 500, showing investors are positioning for continued gains in areas where they remain underexposed.

Fund flows are also supportive. Passive investments into small-cap funds have turned positive, reversing prior outflows. Some strategists caution that sustained gains will still depend on broader economic momentum, but improving earnings revisions and investor interest point to a constructive backdrop.

Wall Street firms including Barclays, Goldman Sachs, and U.S. Bank have highlighted small caps as an underappreciated segment with significant catch-up potential. If the Fed delivers the expected series of rate cuts, the coming year could see the Russell 2000 play a leading role in U.S. equity markets for the first time in years.

BOTHELL, Wash., Sept. 12, 2025 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) announces that President and co-CEO Sam Lee, PhD discussed the scientific foundation and clinical progress with the Company’s lead pan-viral protease inhibitor CDI-988 during a podium presentation at the 9thInternational Calicivirus Conference, held September 7–11, 2025 in Banff, Alberta. Based on a novel mechanism of action and superior broad-spectrum antiviral activity, CDI-988 represents a potential first oral antiviral for the prevention and treatment of norovirus infection.

“It was an honor to share highlights of our CDI-988 Phase 1 data with global norovirus experts at the leading calicivirus scientific meeting,” said Dr. Lee. “The recent completion of Phase 1 study and U.S. Food and Drug Administration’s (FDA) Investigation New Drug (IND) clearance for the next study mark significant milestones for our clinical development of CDI-988.”

CDI-988 was rationally designed with Cocrystal’s proprietary structure-based drug discovery platform technology. In vitro potency data and high-resolution crystal structures have shown broad-spectrum antiviral activity against multiple norovirus genogroups including GII.4 and GII.17, the strain responsible for the majority of circulating infections.

Dr. Lee also discussed previously reported Phase 1 results demonstrating CDI-988’s favorable safety and tolerability profile, with no serious adverse events. Earlier this week, Cocrystal announced FDA authorization to proceed with a Phase 1b human challenge study to evaluate CDI-988 as a potential norovirus prophylaxis and treatment. The study is expected to begin before year end.

The Calicivirus Conference is held every three years and unites scientists from across the globe who study calicivirus virology, evolution, pathogenesis, structural biology, diagnosis, epidemiology, treatment and prevention. The conference aims to foster open discussions, spark new collaborations and explore groundbreaking research. Delegates at this year’s conference engaged with the latest advances in the field through state-of-the-art lectures, oral presentations and poster sessions.

Protease Inhibitor CDI-988 CDI-988 was designed and developed with Cocrystal’s proprietary structure-based platform technology as a broad-spectrum inhibitor to a highly conserved region in the active site of 3CL viral proteases. It targets a highly conserved region in the active site of noroviruses, coronaviruses and other 3CL viral proteases.

Norovirus Infection Norovirus, the leading cause of viral gastroenteritis worldwide, spreads rapidly in community settings such as hospitals, nursing homes, childcare facilities, schools and cruise ships. It causes nausea, vomiting, diarrhea, abdominal pain and dehydration, and is responsible for an estimated $60 billion worldwide in direct healthcare costs and lost productivity.

Cocrystal Structure-Based Platform Technology CDI-988 leverages Cocrystal’s proprietary structure-based drug discovery platform, which provides three-dimensional visualization of inhibitor complexes at near-atomic resolution. This technology enables rapid identification of novel drug binding sites and accelerates the development of broad-spectrum antivirals for the treatment of acute and chronic viral diseases.

About Cocrystal Pharma, Inc. Cocrystal Pharma, Inc. is a clinical-stage biotechnology company that addresses significant unmet needs by developing innovative antiviral treatments for challenging diseases including influenza, viral gastroenteritis, COVID, and hepatitis. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs.

Cautionary Note Regarding Forward-Looking Statements This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the potential efficacy of CDI-988 as a potential antiviral for the prevention and treatment of norovirus infection, and the Company’s plan to initiate a Phase 1b study in 2025. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, the risks and uncertainties arising from the ability of our clinical research organization to recruit volunteers for, and to otherwise proceed with the challenge study, our contract manufacturing organization’s ability to produce the products needed for the study, risks relating to our ability to obtain regulatory approval for and proceed with clinical trials and our liquidity needs. Further information on our risk factors is contained in our filings with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2024. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

AVERSA Fentanyl Is Moving Forward. Nutriband reported results from 2Q26, ended July 31, 2025, with a loss of $2.12 per share. Revenues for 2Q26 were $0.6 million compared with $0.4 million in 2Q25. The increase was attributed to the expansion of contract manufacturing services in the Pocono Pharma division that produces kinesiology tape. Net loss was $2.0 million before Preferred Dividends of $21.8 million, bringing Net Loss Available To Shareholders to $23.8 million. Cash at the end of the quarter was $6.9 million.

Meeting With The FDA Later In September. The company has scheduled a meeting with the FDA on September 18, 2025, to discuss the upcoming Phase 1 clinical trial for AVERSA Fentanyl. This is a Type C Meeting, requested by the company to discuss product development. The meeting agenda includes the CMC (Chemistry, Manufacturing, and Controls) and other aspects of the Investigational New Drug Application (IND) using the 505(b)(2) route of regulatory approval.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Initiation of coverage with Outperform rating and $20 price target. We are initiating coverage on SEGG Media (NASDAQ: SEGG) with an Outperform rating and $20 target. The company is a development-stage operator of international sports and gaming businesses, anchored by valuable brand assets including Sports.com, Lottery.com, TicketStub.com, and Concerts.com.

Developmental stage. Formed out of Lottery.com’s collapse, SEGG has been reconstituted under new leadership with a defined focus on leveraging globally recognized brands. Management is pursuing an asset-light model combining digital platforms, sports media rights, and consumer venues. We believe this strategy positions SEGG to re-establish credibility and execute a compelling growth plan.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The wave of cryptocurrency-linked companies hitting the public markets this year gained fresh momentum on Friday, as Gemini Space Station made its long-awaited debut on the Nasdaq.

Shares in the exchange, founded by Cameron and Tyler Winklevoss, opened at $37.01 after its initial public offering was priced at $28. Within minutes, the stock soared above $45 before retreating to trade around $35 by mid-afternoon. Even after paring gains, Gemini shares were still up more than 20% from their offering price, valuing the company at roughly $1.5 billion.

The trading session wasn’t without drama. A sharp spike in volatility triggered an automatic 10-minute halt shortly after the open, a common safeguard for new listings experiencing outsized swings.

The offering itself raised approximately $425 million, reflecting robust investor demand. Pricing came in well above early estimates of $17 to $19, which were later raised to $24 to $26. By the time Gemini hit the market, enthusiasm had pushed the IPO into the upper range of expectations.

Gemini enters public trading during an especially fertile period for crypto-related IPOs. In June, stablecoin operator Circle Internet Group priced its shares at $31 before closing its first day at $83. Two months later, fintech exchange Bullish went public at $37 and ended its first session near $68. Just yesterday, Figure Technologies, another blockchain player, surged more than 40% in its debut.

These strong first-day performances reflect a broader investor appetite for digital-asset infrastructure, even amid lingering questions around regulation and long-term adoption. Data shows tech IPOs overall have averaged a 36% first-day return over the past year, but crypto-linked listings have consistently outpaced that benchmark.

For Gemini, the IPO marks both a validation and an expansion opportunity. The firm currently manages more than $21 billion in assets and serves approximately 10,000 institutional clients worldwide. Beyond its core exchange platform, the company has diversified into stablecoins, a U.S. credit card product, and a studio dedicated to nonfungible tokens (NFTs).

The timing is strategic. With digital assets edging closer to mainstream financial adoption and institutional participation rising, public investors are eager to gain direct exposure to companies positioned at the center of this ecosystem. Gemini’s listing provides exactly that.

The company’s trajectory also underscores how far the Winklevoss brothers have come since their early public battles in the tech world. Once known primarily for their legal dispute with Facebook founder Mark Zuckerberg, the twins have steadily built Gemini into a brand synonymous with regulatory compliance, security, and user trust in crypto markets.

As the stock settles in the days ahead, traders and analysts will be watching closely to see whether Gemini can maintain momentum — and whether this latest IPO is another signal that crypto finance is entering a new phase of market maturity.

Barrick Mining Corporation (NYSE:B)(TSX:ABX) has agreed to sell its Hemlo Gold Mine in Ontario, Canada, to Carcetti Capital Corp., which will be renamed Hemlo Mining Corp. (HMC) upon closing. The deal, valued at up to $1.09 billion, underscores Barrick’s ongoing strategy of streamlining its portfolio to focus on Tier One gold and copper assets.

The transaction includes $875 million in cash upon closing, $50 million in HMC shares, and up to $165 million in additional cash payments linked to production and gold prices over a five-year period beginning in 2027. This structured consideration provides Barrick with near-term liquidity while also allowing exposure to Hemlo’s future performance through contingent payments.

HMC, currently listed on the NEX Board of the TSX Venture Exchange, plans to graduate to the main TSXV board in connection with the acquisition. The company is backed by a consortium of well-known investors in the mining sector, including Wheaton Precious Metals and Orion Mine Finance. Its management team brings strong credentials, highlighted by industry veteran Robert Quartermain, who played a role in the original discovery of Hemlo and later built SSR Mining and Pretium Resources into respected gold producers.

For Barrick, the Hemlo divestiture reflects a disciplined capital allocation strategy. Proceeds will be used to strengthen the company’s balance sheet and return capital to shareholders, aligning with its broader plan to prioritize Tier One operations that deliver the largest scale, lowest cost, and longest life. With the sale of Hemlo, alongside earlier transactions involving Donlin and Alturas, Barrick expects to generate more than $2 billion from non-core asset sales in 2025 alone.

Despite the divestment, Canada remains a core part of Barrick’s global footprint. The company continues to advance exploration projects and early-stage opportunities across the country, underscoring its commitment to discovering and developing world-class gold and copper mines within the region.

The sale also positions Hemlo for a new phase of growth under HMC. With dedicated focus, a seasoned leadership team, and the backing of strategic investors, Hemlo may benefit from renewed investment and operational improvements that could unlock further value.

Subject to customary regulatory approvals and closing conditions, the transaction is expected to close in the fourth quarter of 2025. CIBC World Markets acted as Barrick’s financial advisor, while Davies Ward Phillips & Vineberg LLP and Blake, Cassels & Graydon LLP provided legal counsel.

Barrick remains one of the world’s leading gold producers, with a global portfolio spanning 18 countries and six of the industry’s Tier One mines. The Hemlo sale marks the end of a long chapter for Barrick in northern Ontario, while reinforcing its commitment to building shareholder value through operational excellence and portfolio discipline.

U.S. inflation edged higher in August, complicating the Federal Reserve’s decision-making as it prepares for its September policy meeting. The Consumer Price Index (CPI) rose 2.9% year-over-year, up from July’s 2.7% pace, while monthly prices climbed 0.4%—a faster increase than the prior month. The uptick was fueled by persistently high gasoline prices and firmer food costs, underscoring the challenge of controlling inflation while navigating a slowing economy.

Core inflation, which excludes food and energy, held steady at 3.1% year-over-year. On a monthly basis, core prices rose 0.3%, marking the strongest two-month stretch in half a year. Travel and transportation costs stood out as particular pressure points, with airfares jumping nearly 6% in August after a strong gain the previous month. Vehicle prices, both new and used, also reversed earlier declines. Meanwhile, some categories showed moderation, such as medical care and communication services, which provided modest relief.

While the inflation data reflects lingering price pressures, the labor market tells a different story. Weekly jobless claims surged to 263,000—the highest level in nearly four years—suggesting that hiring momentum continues to cool. This comes on the heels of government revisions showing that the economy added 911,000 fewer jobs than previously reported between March 2024 and March 2025. Taken together, the data points to a labor market losing steam even as certain costs remain stubborn.

Markets are betting that the Fed will still cut interest rates next week, with traders pricing in an 88% probability of a quarter-point reduction and an 11% chance of a half-point move. By year-end, expectations remain for a total of 75 basis points in cuts. For policymakers, the dilemma is clear: inflation is not fully under control, but economic softness is becoming too pronounced to ignore.

The inflation numbers also highlight the effect of tariffs imposed by the Trump administration, which are filtering into consumer prices unevenly. Gasoline and travel costs remain elevated, while categories such as lodging and some services show weakness, pointing to households feeling the pinch in essential spending areas. At the same time, producer prices declined 0.1% in August, suggesting that businesses are absorbing some of the additional costs rather than passing them entirely to consumers.

The Federal Reserve now faces a delicate balancing act. Cutting rates too aggressively could risk reigniting inflationary pressures, especially if energy and trade-related costs remain sticky. Moving too cautiously, however, could deepen the strain on employment and consumer confidence, potentially tipping the economy toward recessionary conditions.

Investors are watching closely not only for the rate decision but also for Fed Chair Jerome Powell’s messaging. With both inflation and unemployment data pulling in different directions, the September meeting will serve as a pivotal moment for how the Fed charts its course through a complex and fragile economic backdrop.

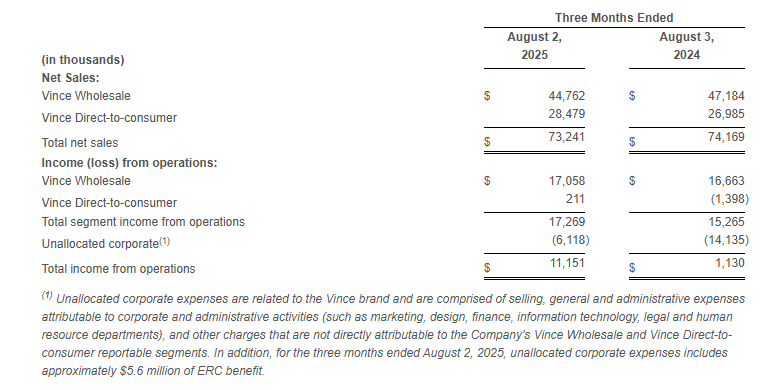

Net Sales of $73.2 Million Net Income of $12.1 Million; Adjusted Net Income of $4.9 Million Adjusted EBITDA of $6.7 Million, an increase of $4.0 Million vs. Q2 FY2024

NEW YORK–(BUSINESS WIRE)– Vince Holding Corp. (NYSE: VNCE) (“VNCE” or the “Company”), a global contemporary retailer, today reported its financial results for the second quarter ended August 2, 2025.

Brendan Hoffman, Chief Executive Officer of VNCE said, “We are very proud of our second quarter performance which reflects disciplined execution and strong customer reception to our product offerings especially as we elongated our full-price selling season. As we remain mindful of the dynamic macro environment, our ability to navigate today’s challenges while preserving product quality and customer loyalty remains our utmost priority. Given the strength of our underlying trends, we are pleased to be in a position to begin to reinvest in the business as we remain focused on the growth opportunities ahead for the Vince brand as well as the Vince Holding Corp. platform.”

In this press release, the Company is presenting its financial results in conformity with U.S. generally accepted accounting principles (“GAAP”) as well as on an “adjusted” basis. Adjusted results presented in this press release are non-GAAP financial measures. See “Non-GAAP Financial Measures” below for more information about the Company’s use of non-GAAP financial measures and Exhibit 3 and Exhibit 4 to this press release for a reconciliation of GAAP measures to such non-GAAP measures.

For the second quarter ended August 2, 2025:

Total Company net sales decreased 1.3% to $73.2 million compared to $74.2 million in the second quarter of fiscal 2024. The year-over-year decrease was driven by a 5.1% decline in the wholesale segment partially offset by a 5.5% increase in direct-to-consumer segment. The decline in the wholesale segment was primarily due to the shift in timing of fall shipments compared to the prior year as a result of the earlier uncertainty with respect to tariff policies and impact.

Gross profit was $36.9 million, or 50.4% of net sales, compared to gross profit of $35.1 million, or 47.4% of net sales, in the second quarter of fiscal 2024. The increase in gross margin rate was primarily driven by approximately 340 basis points due to the favorable impact of lower product costing and higher pricing, and approximately 210 basis points due to the favorable impact of lower discounting, partially offset by approximately 170 basis points due to higher tariffs, and approximately 100 basis points due to increased freight costs.

Selling, general, and administrative expenses were $25.8 million, or 35.2% of sales, compared to $34.0 million, or 45.8% of sales, in the second quarter of fiscal 2024. The decrease in SG&A dollars was primarily driven by the receipt of payroll tax credit payments from the U.S. Department of the Treasury under the Employee Retention Credit program (the “ERC benefit”). The ERC benefit was approximately $7.2 million, of which $5.6 million related to the original payroll tax credit claims and was recorded in SG&A as an offset to compensation expenses, with the remaining $1.6 million of interest payments recorded as Other income.

Income from operations was $11.2 million compared to income from operations of $1.1 million in the same period last year. Excluding the payments from the ERC benefit, Adjusted income from operations* was $5.5 million for the second quarter of fiscal 2025.

Income tax expense was $0.1 million, which represents a discrete tax expense relating to interest received in connection with the ERC benefit. The Company has year-to-date ordinary pre-tax losses and is anticipating annual ordinary pre-tax income for the fiscal year. The Company has determined that it is more likely than not that the tax benefit of the year-to-date ordinary pre-tax loss will not be realized in the current or future years and as such, tax provisions for the interim periods should not be recognized until the Company has year-to-date ordinary pre-tax income. The tax provision in the second quarter of fiscal 2025 compares to an income tax benefit of $0.8 million in the same period last year.

Net income was $12.1 million or $0.93 per diluted share compared to net income of $0.6 million or $0.05 per diluted share in the same period last year. Excluding the payments from the ERC benefit and its discrete tax effect, the Adjusted net income* was $4.9 million or $0.38 per diluted share in the second quarter of fiscal 2025.

Adjusted EBITDA* was $6.7 million compared to $2.7 million in the same period last year.

The Company ended the quarter with 58 company-operated Vince stores, a net decrease of 3 stores since the second quarter of fiscal 2024.

Second Quarter Review

Net sales decreased 1.3% to $73.2 million as compared to the second quarter of fiscal 2024.

Wholesale segment sales decreased 5.1% to $44.8 million compared to the second quarter of fiscal 2024.

Direct-to-consumer segment sales increased 5.5% to $28.5 million compared to the second quarter of fiscal 2024.

Income from operations excluding unallocated corporate expenses was $17.3 million compared to income from operations of $15.3 million in the same period last year.

Net Sales and Operating Results by Segment:

Balance Sheet

At the end of the second quarter of fiscal 2025, total borrowings under the Company’s debt agreements totaled $31.1 million and the Company had $42.6 million of excess availability under its revolving credit facility.

Net inventory at the end of the second quarter of fiscal 2025 was $76.7 million compared to $66.3 million at the end of the second quarter of fiscal 2024. The year-over-year increase in inventory was driven by approximately $5.2 million higher inventory carrying value due to tariffs as well as our strategic decision to ship goods earlier in advance of the expiration of reciprocal tariff extensions.

During the quarter ended August 2, 2025, the Company did not issue shares of common stock under the ATM program. The Company continues to have shares available under the program to exercise with proceeds to be used as sources, along with cash from operations, to fund future growth.

Outlook

For the third quarter of fiscal 2025 the Company expects the following:

• Net sales to be approximately flat to up 3% compared to the prior year period.

• Adjusted operating income as a percentage of net sales to be approximately 1% to 4%.

• Adjusted EBITDA as a percentage of net sales to be approximately 2% to 5%.

The above guidance assumes $4 million to $5 million in expected incremental tariff costs, of which the Company expects to mitigate approximately 50% through changes to country of origin, vendor negotiations as well as select and strategic price increases.

Given the uncertainty related to the potential impact and duration of current tariff policy, the Company is not providing guidance for the full year fiscal 2025.

Strategic Partnership with Authentic Brands Group

On May 25, 2023, the Company announced that it completed the previously announced transaction (the “Authentic Transaction”) with Authentic Brands Group (“Authentic”).

In connection with the Authentic Transaction, VNCE entered into an exclusive, long-term license agreement (the “License Agreement”) with Authentic for usage of the contributed intellectual property for VNCE’s existing business in a manner consistent with the Company’s current wholesale, retail and e-commerce operations. The License Agreement contains an initial ten-year term and eight ten-year renewal options allowing VNCE to renew the agreement.

*Non-GAAP Financial Measures

In addition to reporting financial results in accordance with GAAP, the Company has provided, with respect to the financial results relating to the three and six months ended August 2, 2025 and August 3, 2024, adjusted EBITDA, which is a non-GAAP measure. Adjusted EBITDA is calculated as earnings before interest, taxes, depreciation and amortization, share-based compensation, capitalized cloud computing amortization, ERC benefit, and gain on sale of Rebecca Taylor, Inc. and its wholly owned subsidiary (“Gain on Sale of Subsidiary”). For the three and six months ended August 2, 2025 and August 3, 2024, respectively, the Company has provided adjusted income (loss) from operations, adjusted income (loss) before income taxes and equity in net income (loss) of equity method investment, adjusted income (loss) before equity in net income (loss) of equity method investment, adjusted net income (loss), and adjusted earnings (loss) per share, which are non-GAAP measures, in order to eliminate the effect of the ERC benefit, Discrete Tax Effect Associated with ERC benefit, and Gain on Sale of Subsidiary.

The Company believes that the presentation of these non-GAAP measures facilitates an understanding of the Company’s continuing operations without the impact associated with the aforementioned items. While these types of events can and do recur periodically, they are excluded from the indicated financial information due to their impact on the comparability of earnings across periods. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information prepared in accordance with GAAP. A reconciliation of GAAP to non-GAAP results has been provided in Exhibit 3 and Exhibit 4 to this press release.

Conference Call

A conference call to discuss the first quarter results will be held today, September 10, 2025, at 4:30 p.m. ET, hosted by Vince Holding Corp. Chief Executive Officer, Brendan Hoffman, and Chief Financial Officer, Yuji Okumura. During the conference call, the Company may make comments concerning business and financial developments, trends and other business or financial matters. The Company’s comments, as well as other matters discussed during the conference call, may contain or constitute information that has not been previously disclosed.

Those who wish to participate in the call may do so by dialing (833) 470-1428, conference ID 030527. Any interested party will also have the opportunity to access the call via the Internet at http://investors.vince.com/. To listen to the live call, please go to the website at least 15 minutes early to register and download any necessary audio software. For those who cannot listen to the live broadcast, a recording will be available for 12 months after the date of the event. Recordings may be accessed at http://investors.vince.com.

ABOUT VINCE HOLDING CORP.

Vince Holding Corp. is a global retail company that operates the Vince brand women’s and men’s ready to wear business. Vince, established in 2002, is a leading global luxury apparel and accessories brand best known for creating elevated yet understated pieces for every day effortless style. Vince Holding Corp. operates 45 full-price retail stores, 14 outlet stores, and its e-commerce site, as well as through premium wholesale channels globally. Please visit www.vince.com for more information.

Forward-Looking Statements: This document, and any statements incorporated by reference herein contain forward-looking statements under the Private Securities Litigation Reform Act of 1995. Forward-looking statements include the statements under “Outlook” above as well as statements regarding, among other things, our current expectations about possible or assumed future results of operations of the Company and are indicated by words or phrases such as “may,” “will,” “should,” “believe,” “expect,” “seek,” “anticipate,” “intend,” “estimate,” “plan,” “target,” “project,” “forecast,” “envision” and other similar phrases. Although we believe the assumptions and expectations reflected in these forward-looking statements are reasonable, these assumptions and expectations may not prove to be correct and we may not achieve the results or benefits anticipated. These forward-looking statements are not guarantees of actual results, and our actual results may differ materially from those suggested in the forward-looking statements. These forward-looking statements involve a number of risks and uncertainties, some of which are beyond our control, including, without limitation: changes to and unpredictability in the trade policies and tariffs imposed by the U.S. and the governments of other nations; our ability to maintain adequate cash flow from operations or availability under our revolving credit facility to meet our liquidity needs; general economic conditions; restrictions on our operations under our credit facilities; our ability to improve our profitability; our ability to maintain our larger wholesale partners; our ability to accurately forecast customer demand for our products; our ability to maintain the license agreement with ABG Vince, a subsidiary of Authentic Brands Group; ABG Vince’s expansion of the Vince brand into other categories and territories; ABG Vince’s approval rights and other actions; our ability to realize the benefits of our strategic initiatives; the execution of our customer strategy; our ability to make lease payments when due; our ability to open retail stores under favorable lease terms and operate and maintain new and existing retail stores successfully; our operating experience and brand recognition in international markets; our ability to remediate the identified material weakness in our internal control over financial reporting; our ability to comply with domestic and international laws, regulations and orders; increased scrutiny regarding our approach to sustainability matters and environmental, social and governance practices; competition in the apparel and fashion industry; the transition associated with the appointment of new chief executive officer and new chief financial officer; our ability to attract and retain key personnel; seasonal and quarterly variations in our revenue and income; the protection and enforcement of intellectual property rights relating to the Vince brand; our ability to successfully conclude remaining matters following the wind down of the Rebecca Taylor business; the extent of our foreign sourcing; our reliance on independent manufacturers; our ability to ensure the proper operation of the distribution facilities by third-party logistics providers; fluctuations in the price, availability and quality of raw materials; the ethical business and compliance practices of our independent manufacturers; our ability to mitigate system or data security issues, such as cyber or malware attacks, as well as other major system failures; our ability to adopt, optimize and improve our information technology systems, processes and functions; our ability to comply with privacy-related obligations; our ability to regain compliance with the New York Stock Exchange (the “NYSE”) Listed Company Manual and maintain a listing of our common stock on the NYSE; our status as a “controlled company”; our status as a “smaller reporting company”; and other factors as set forth from time to time in our Securities and Exchange Commission filings, including those described under “Item 1A—Risk Factors” in our Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. We intend these forward-looking statements to speak only as of the time of this release and do not undertake to update or revise them as more information becomes available, except as required by law.

CHICAGO, Sept. 11, 2025 (GLOBE NEWSWIRE) — MAIA Biotechnology, Inc. (NYSE American: MAIA) (“MAIA”, the “Company”), a clinical-stage biopharmaceutical company focused on developing targeted immunotherapies for cancer, today highlighted positive efficacy data from its Phase 2 clinical trial, THIO-101, evaluating ateganosine (THIO) sequenced with the immune checkpoint inhibitor (CPI) cemiplimab (Libtayo®) in patients with advanced non-small cell lung cancer (NSCLC) who had failed two or more standard-of-care therapy regimens.

As of June 30, 2025,

Estimated median progression free survival (PFS) in third-line treatment (180 mg dose) was 5.6 months. The comparable PFS threshold in standard of care treatments is 2.5 months1.

Estimated median overall survival (OS) was 17.8 months, with a 95% confidence interval (CI) lower bound of 12.5 months and a 99% CI lower bound of 10.8 months, consistent with the prior data readout (May 15, 2025).

Across patients of all treatment lines, 2 patients have completed 33 cycles of therapy, highlighting ateganosine’ potential for extended dosing, which usually translates into longer patient survival.

“THIO-101 continues to reveal impressive efficacy with observed progression free survival of 5.6 months, which is more than double the standard of care PFS of just 2.5 months. The data also demonstrates the durability of ateganosine treatment through extended treatment cycles, which is in line with consistent tolerability and low toxicity,” said MAIA Chairman and CEO Vlad Vitoc, M.D. “We are seeking further validation of ateganosine’s strong efficacy in our THIO-101 Phase 2 expansion trial, which began enrolling patients in July 2025.”

Details of THIO-101, including efficacy data and safety findings, are included in MAIA’s poster for the 2025 IASLC World Conference on Lung Cancer (WCLC), available at maiabiotech.com/publications.

About Ateganosine

Ateganosine (THIO, 6-thio-dG or 6-thio-2’-deoxyguanosine) is a first-in-class investigational telomere-targeting agent currently in clinical development to evaluate its activity in non-small cell lung cancer (NSCLC). Telomeres, along with the enzyme telomerase, play a fundamental role in the survival of cancer cells and their resistance to current therapies. The modified nucleotide 6-thio-2’-deoxyguanosine induces telomerase-dependent telomeric DNA modification, DNA damage responses, and selective cancer cell death. Ateganosine-damaged telomeric fragments accumulate in cytosolic micronuclei and activates both innate (cGAS/STING) and adaptive (T-cell) immune responses. The sequential treatment of ateganosine followed by PD-(L)1 inhibitors resulted in profound and persistent tumor regression in advanced, in vivo cancer models by induction of cancer type–specific immune memory. Ateganosine is presently developed as a second or later line of treatment for NSCLC for patients that have progressed beyond the standard-of-care regimen of existing checkpoint inhibitors.

About THIO-101 Phase 2 Clinical Trial

THIO-101 is a multicenter, open-label, dose finding Phase 2 clinical trial. It is the first trial designed to evaluate ateganosine’s anti-tumor activity when followed by PD-(L)1 inhibition. The trial is testing the hypothesis that low doses of ateganosine administered prior to cemiplimab (Libtayo®) will enhance and prolong immune response in patients with advanced NSCLC who previously did not respond or developed resistance and progressed after first-line treatment regimen containing another checkpoint inhibitor. The trial design has two primary objectives: (1) to evaluate the safety and tolerability of ateganosine administered as an anticancer compound and a priming immune activator (2) to assess the clinical efficacy of ateganosine using Overall Response Rate (ORR) as the primary clinical endpoint. The expansion of the study will assess overall response rates (ORR) in advanced NSCLC patients receiving third line (3L) therapy who were resistant to previous checkpoint inhibitor treatments (CPI) and chemotherapy. Treatment with ateganosine followed by cemiplimab (Libtayo®) has shown an acceptable safety profile to date in a heavily pre-treated population. For more information on this Phase II trial, please visit ClinicalTrials.gov using the identifier NCT05208944.

About MAIA Biotechnology, Inc.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is ateganosine (THIO), a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Forward Looking Statements

MAIA cautions that all statements, other than statements of historical facts contained in this press release, are forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels or activity, performance or achievements to be materially different from those anticipated by such statements. The use of words such as “may,” “might,” “will,” “should,” “could,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “project,” “intend,” “future,” “potential,” or “continue,” and other similar expressions are intended to identify forward looking statements. However, the absence of these words does not mean that statements are not forward-looking. For example, all statements we make regarding (i) the initiation, timing, cost, progress and results of our preclinical and clinical studies and our research and development programs, (ii) our ability to advance product candidates into, and successfully complete, clinical studies, (iii) the timing or likelihood of regulatory filings and approvals, (iv) our ability to develop, manufacture and commercialize our product candidates and to improve the manufacturing process, (v) the rate and degree of market acceptance of our product candidates, (vi) the size and growth potential of the markets for our product candidates and our ability to serve those markets, and (vii) our expectations regarding our ability to obtain and maintain intellectual property protection for our product candidates, are forward looking. All forward-looking statements are based on current estimates, assumptions and expectations by our management that, although we believe to be reasonable, are inherently uncertain. Any forward-looking statement expressing an expectation or belief as to future events is expressed in good faith and believed to be reasonable at the time such forward-looking statement is made. However, these statements are not guarantees of future events and are subject to risks and uncertainties and other factors beyond our control that may cause actual results to differ materially from those expressed in any forward-looking statement. Any forward-looking statement speaks only as of the date on which it was made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. In this release, unless the context requires otherwise, “MAIA,” “Company,” “we,” “our,” and “us” refers to MAIA Biotechnology, Inc. and its subsidiaries.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q2 Results. The company reported Q2 revenue of $73.2 million, modestly beating our estimate of $72.0 million, and adj. EBITDA of $6.7 million, which strongly outperformed our estimate of $0.85 million by 685%, as illustrated in Figure #1 Q2 Results. The strong adj. EBITDA was largely driven by management’s ability to execute on its tariff mitigation strategies, resulting in an improved gross profit margin.

Mitigating tariff impacts. Importantly, the company’s gross profit margin increased 300 basis points over the prior year period. The improvement was driven by lower product costing and higher pricing, contributing a 340 basis point improvement, as well as less discounting, which resulted in a 210 basis point improvement. However, the positive margin contributions were softened by tariff and freight impacts of 170 basis points and 100 basis points, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.