Key Points: – Shares of Geo Group and CoreCivic saw significant increases (over 7% and 8%, respectively) after the appointment of Tom Homan as “border czar,” – Homan’s appointment aligns with Trump’s strong stance on deportation and border security, so there is an anticipated increase in federal contracts for private detention companies – Renewed focus on immigration enforcement marks a a significant departure from the current adminstration’s stance

Private prison stocks surged Monday after President-elect Donald Trump appointed Tom Homan as “border czar,” sparking market optimism about a renewed focus on immigration enforcement. Shares of Geo Group and CoreCivic, both major players in the private detention sector, jumped over 7% and 8%, respectively, in response to the announcement. Homan, previously the head of Immigration and Customs Enforcement (ICE) under Trump’s first term, is known for his firm stance on deportation and border security. His appointment signals a potential increase in federal contracting for companies that provide detention services, specifically for ICE operations.

Trump’s announcement on Truth Social stated that Homan will be in charge of all deportation efforts, encompassing both land and maritime borders, with an emphasis on accelerating deportations. During a conservative conference in July, Homan declared he would lead the “biggest deportation force” in U.S. history if Trump was re-elected. This strong stance aligns with Trump’s previous immigration policies, which saw heightened demand for detention facilities, and is expected to bolster the private prison industry, including companies like Geo Group and CoreCivic, which have contracts with ICE and the U.S. Marshals Service.

The renewed focus on immigration enforcement under Trump is a significant shift from the current administration’s approach, which has limited federal use of private detention centers. This shift presents a potential growth opportunity for private prison companies, which struggled as President Biden worked to reduce private prison contracts. With Homan’s appointment, investors anticipate a resurgence of federal reliance on private detention services to meet increased demand for housing immigrant detainees.

Analysts have responded positively to this development, citing that Trump’s administration will likely “embrace” companies like Geo Group and CoreCivic. Isaac Boltansky, an analyst with BTIG, noted that private prison companies are positioned for growth under an immigration-focused administration, specifically due to likely contracting needs with the U.S. Marshals Service and ICE. Analysts expect Homan’s policies to generate consistent demand for private facilities, which could lead to stronger financial performance and increased market value for these companies.

Trump’s firm stance on deportation and his choice of Homan as border czar have energized investors. The expected rise in federal contracts signals a favorable outlook for private prison stocks. With immigration reform likely to be a focal point in Trump’s administration, CoreCivic and Geo Group could see sustained growth, especially as they support the expanded need for detention services. The private prison sector, long entangled with federal enforcement policies, now faces a potential resurgence as market trends align with anticipated shifts in government policy.

MIAMI, Nov. 08, 2024 (GLOBE NEWSWIRE) — SKYX (NASDAQ: SKYX) (d/b/a “SKYX Technologies”), a highly disruptive smart platform technology company with over 97 issued and pending patents in the U.S. and globally, and which owns over 60 lighting and home décor websites with a mission to make homes and buildings become smart, safe, and advanced as the new standard, announced today that it will host a Corporate Update call and present third quarter 2024 financial results. The conference call will be held on Tuesday, November 12, 2024 at 4:30 p.m. Eastern Time.

SKYX Participating Members will Include:

Rani Kohen, Founder and Executive Chairman

Steve Schmidt, SKYX President, (Former CEO of Nielsen Data Corporation and President of Office Depot International)

Lenny Sokolow, Co-CEO

Marc Boisseau, CFO

SKYX Platforms – Q3 2024 Corporate Update Call

Date: Tuesday, November 12, 2024 Time: 4:30 p.m. Eastern Time U.S./Canada Dial-in: 1-866-652-5200 International Dial-in: 1-412-317-6060

Please dial in at least 10 minutes before the start of the call to ensure timely participation.

A playback of the call will be available until November 19, 2024. To listen, call 1-844-512-2921 within the United States and Canada or 1-412-317-6671 when calling internationally. Please use the replay pin number 10194478. A webcast is also available at the following link: https://viavid.webcasts.com/starthere.jsp?ei=1697666&tp_key=fff51f3b32

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 97 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

HOUSTON, Nov. 8, 2024 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”) and Orange 142, LLC (“Orange 142”), today announced that the Company will report financial results for the third quarter of fiscal year 2024 ended September 30, 2024 on Tuesday, November 12, 2024 after the U.S. stock market closes.

Management will host a conference call and webcast on the same day at 5:00 PM ET to discuss the results. The live webcast and replay can be accessed at https://ir.directdigitalholdings.com/.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT) brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within the general market and multicultural media properties. The Company’s buy-side platform, Orange 142, delivers significant ROI for middle-market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Combined, Direct Digital Holdings’ sell- and buy-side solutions generate billions of impressions per month across display, CTV, in-app and other media channels.

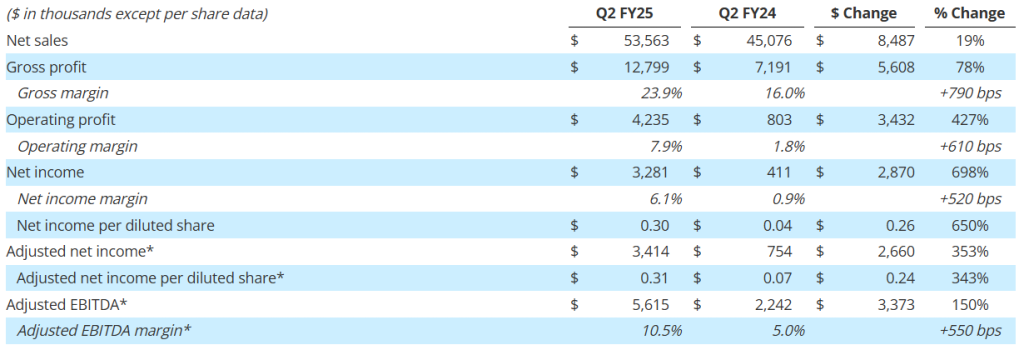

Revenue increased 19% to $53.6 million, driven by strength across its markets

Margin expansion fueled by sales growth and execution: Gross margin improved 790 basis points to 23.9% of sales, net margin increased 520 basis points to 6.1% of sales, and adjusted EBITDA1 margin expanded 550 basis points to 10.5% of sales

Net income per diluted share was $0.30 in the second quarter; adjusted net income per diluted share¹ was $0.31

Strong orders of $63.7 million, driven by demand from defense, space, and refining, resulted in a book-to-bill ratio of 1.2x and a record backlog of $407 million1

Strong balance sheet with no debt, $32.3 million in cash, and access to $43 million under its revolving credit facility at quarter end to support growth initiatives

Raised full year guidance for gross margin and adjusted EBITDA¹ to reflect improved profitability

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy, and process industries, today reported financial results for its second quarter for the fiscal year ending March 31, 2025 (“fiscal 2025”). Results for the quarter include the P3 Technologies, LLC (“P3”) acquisition, which closed on November 9, 2023.

“Our team’s efforts to diversify and strengthen the business over the past few years are clearly yielding results, as shown by our record second-quarter performance,” commented Daniel J. Thoren, President and Chief Executive Officer. “Strong sales growth in our markets, along with exceptional execution throughout the business, have driven meaningful margin expansion. Our strategic emphasis on higher-margin opportunities and operational efficiencies has been a key driver of this success.”

Mr. Thoren added, “We are also focused on recruiting and retaining top talent, and have initiatives to enhance our supply chain, which helps us to improve performance and manage our risk. These initiatives, along with our strengthened balance sheet, robust orders2, and growing backlog2, we believe positions us well to sustain growth and profitability for the next several years. Importantly, we have raised our full-year adjusted EBITDA guidance, keeping us firmly on track to achieve our FY2027 target of low to mid-teen adjusted EBITDA margins.”

Second Quarter Fiscal 2025 Performance Review

(All comparisons are with the same prior-year period unless noted otherwise.)

*Graham believes that, when used in conjunction with measures prepared in accordance with U.S. generally accepted accounting principles, adjusted net income, adjusted net income per diluted share, adjusted EBITDA and adjusted EBITDA margin, which are non-GAAP measures, help in the understanding of its operating performance. See attached tables and other information on pages 10 and 11 for important disclosures regarding Graham’s use of these non-GAAP measures.

Record quarterly net sales of $53.6 million increased 19%, or $8.5 million, and included $0.9 million of incremental sales from P3. Sales to the defense market grew by $5.8 million, or 23%, driven by the expansion of new defense programs, the ramp-up of existing programs, and the timing of key project milestones. Additionally, higher refining and chemical/petrochemical sales contributed $2.2 million to the growth, largely reflecting the timing of capital improvement projects. Aftermarket sales to the refining, chemical/petrochemical, and defense markets of $9.8 million remained strong but were $1.5 million lower than the prior year record levels. See supplemental data for a further breakdown of sales by market and region.

Gross margin expanded 790 basis points to 23.9%, driven by the leverage on higher volume, a favorable mix toward higher margin projects, improved pricing, and better execution. Additionally, gross profit for the quarter benefited $0.4 million, or approximately 80 basis points, due to the $2.1 million grant from the BlueForge Alliance. This grant is reimbursing the Company for the cost of its defense welder training programs in Batavia and related equipment. Graham expects to realize similar gross profit benefits from the grant over the next two quarters, or for the remainder of fiscal 2025.

Selling, general and administrative expense (“SG&A”), including amortization, totaled $9.2 million, or 17.1% of sales, up $2.8 million compared with the prior year. This increase reflects the Company’s continued investments in its operations, employees, and technology. Notable contributors to the increase included $0.4 million of incremental costs related to P3, $0.3 million increase in the supplemental performance bonus for Barber-Nichols employees2, $0.2 million for enterprise resource planning (“ERP”) conversion costs at the Batavia facility, and $0.2 million of incremental research and development expenses. The remainder of the increase in SG&A was primarily related to increased costs associated with the Company’s growth and various other initiatives.

Included in other operating income for the second quarter of fiscal 2025 was a $0.6 million reversal of a previously accrued contingent earnout liability for P3. The reversal was not due to any lost orders, but rather a delayed project that extended beyond the earnout period.

Cash Management and Balance Sheet

Cash provided by operating activities totaled $22.6 million for the six month period ending September 30, 2024, nearly double the amount from the comparable period in fiscal 2024. As of September 30, 2024, cash and cash equivalents were $32.3 million, up from $16.9 million at the end of fiscal 2024.

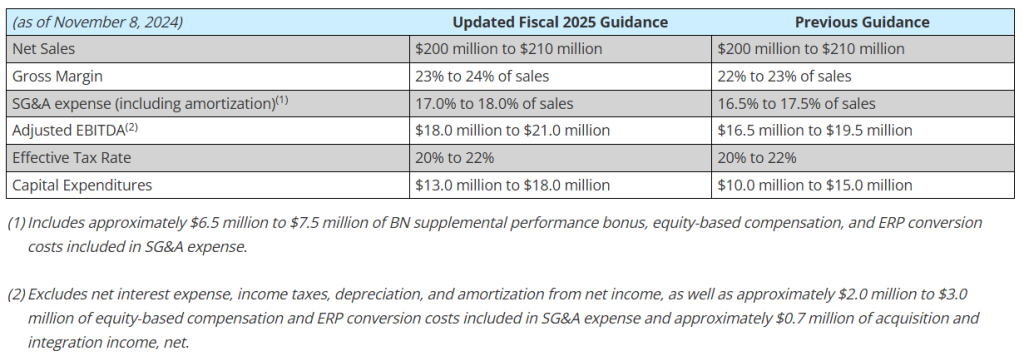

Capital expenditures of $6.5 million for the first six months of fiscal 2025 were focused on capacity expansion and productivity improvements. The Company increased its expected fiscal 2025 capital expenditures to be in the range of $13.0 million to $18.0 million from its previous expectations of $10.0 million to $15.0 million due to a land purchase in Arvada, CO, and plans to build a liquid hydrogen and oxygen testing facility to support future growth and customer needs.

The Company had no debt outstanding at September 30, 2024 with $43 million available on its senior secured revolving credit facility after taking into account outstanding letters of credit.

Orders for the three-month period ended September 30, 2024, were $63.7 million, resulting in a book-to-bill ratio of 1.2x. Defense orders represented 48% of total orders and included a contract to supply the MK19 air turbine pump for the torpedo ejection system on the Columbia-class submarine. Space orders, which can fluctuate due to the timing of projects, saw a meaningful increase to $13.5 million, which included a contract for the cryogenic recirculation pump that provides thermal conditioning for upper stage engines on launch vehicles in space. Refining orders totaled $10.6 million and were driven by continued strength in aftermarket demand and the timing of new capital projects.

Backlog at quarter end reached a record $407.0 million, up 30% over the prior-year period and up 3% sequentially. Approximately 35% to 45% of orders currently in backlog are expected to be converted to sales in the next twelve months and another 30% to 40% is expected to convert to sales over the following year. The majority of orders expected to convert beyond twelve months are for the defense industry, specifically the U.S. Navy.

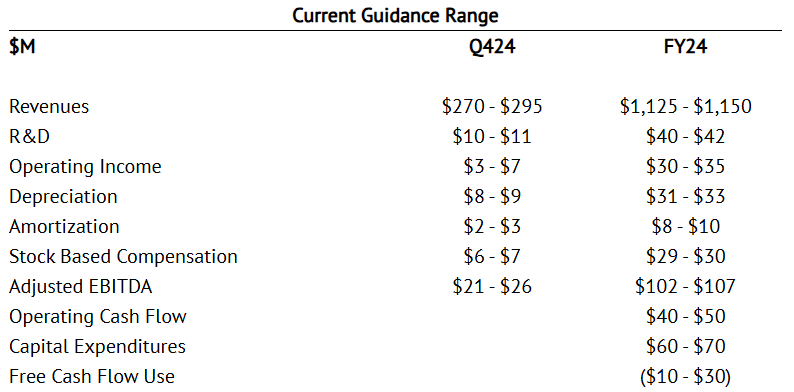

Fiscal 2025 Outlook

The Company’s outlook for 2025 was updated as follows:

Webcast and Conference Call

GHM’s management will host a conference call and live webcast on November 8, 2024 at 11:00 a.m. Eastern Time (“ET”) to review its financial results as well as its strategy and outlook. The review will be accompanied by a slide presentation, which will be made available immediately prior to the conference call on GHM’s investor relations website.

A question-and-answer session will follow the formal presentation. GHM’s conference call can be accessed by calling (201) 689-8560. Alternatively, the webcast can be monitored from the events section of GHM’s investor relations website.

A telephonic replay will be available from 3:00 p.m. ET today through Friday, November 15, 2024. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13749103 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy, and process industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “expects,” “future,” “outlook,” “anticipates,” “believes,” “could,” “guidance,” ”may”, “will,” “plan” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, profitability of future projects and the business, its ability to deliver to plan, its ability to continue to strengthen relationships with customers in the defense industry, its ability to secure future projects and applications, expected expansion and growth opportunities, anticipated sales, revenues, adjusted EBITDA, adjusted EBITDA margins, capital expenditures and SG&A expenses, the timing of conversion of backlog to sales, orders, market presence, profit margins, tax rates, foreign sales operations, customer preferences, changes in market conditions in the industries in which it operates, changes in general economic conditions and customer behavior, forecasts regarding the timing and scope of the economic recovery in its markets, and its acquisition and growth strategy, are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

Non-GAAP Financial Measures

Adjusted EBITDA is defined as consolidated net income (loss) before net interest expense, income taxes, depreciation, amortization, other acquisition related expenses, and other unusual/nonrecurring expenses. Adjusted EBITDA margin is defined as Adjusted EBITDA as a percentage of sales. Adjusted EBITDA and Adjusted EBITDA margin are not measures determined in accordance with generally accepted accounting principles in the United States, commonly known as GAAP. Nevertheless, Graham believes that providing non-GAAP information, such as Adjusted EBITDA and Adjusted EBITDA margin, is important for investors and other readers of Graham’s financial statements, as it is used as an analytical indicator by Graham’s management to better understand operating performance. Moreover, Graham’s credit facility also contains ratios based on Adjusted EBITDA. Because Adjusted EBITDA and Adjusted EBITDA margin are non-GAAP measures and are thus susceptible to varying calculations, Adjusted EBITDA, and Adjusted EBITDA margin, as presented, may not be directly comparable to other similarly titled measures used by other companies.

Adjusted net income and adjusted net income per diluted share are defined as net income and net income per diluted share as reported, adjusted for certain items and at a normalized tax rate. Adjusted net income and adjusted net income per diluted share are not measures determined in accordance with GAAP, and may not be comparable to the measures as used by other companies. Nevertheless, Graham believes that providing non-GAAP information, such as adjusted net income and adjusted net income per diluted share, is important for investors and other readers of the Company’s financial statements and assists in understanding the comparison of the current quarter’s and current fiscal year’s net income and net income per diluted share to the historical periods’ net income and net income per diluted share. Graham also believes that adjusted net income per share, which adds back intangible amortization expense related to acquisitions, provides a better representation of the cash earnings of the Company.

Forward-Looking Non-GAAP Measures

Forward-looking adjusted EBITDA and adjusted EBITDA margin are non-GAAP measures. The Company is unable to present a quantitative reconciliation of these forward-looking non-GAAP financial measures to their most directly comparable forward-looking GAAP financial measures because such information is not available, and management cannot reliably predict the necessary components of such GAAP measures without unreasonable effort largely because forecasting or predicting our future operating results is subject to many factors out of our control or not readily predictable. In addition, the Company believes that such reconciliations would imply a degree of precision that would be confusing or misleading to investors. The unavailable information could have a significant impact on the Company’s fiscal 2025 financial results. These non-GAAP financial measures are preliminary estimates and are subject to risks and uncertainties, including, among others, changes in connection with purchase accounting, quarter-end, and year-end adjustments. Any variation between the Company’s actual results and preliminary financial estimates set forth above may be material.

Key Performance Indicators

In addition to the foregoing non-GAAP measures, management uses the following key performance metrics to analyze and measure the Company’s financial performance and results of operations: orders, backlog, and book-to-bill ratio. Management uses orders and backlog as measures of current and future business and financial performance, and these may not be comparable with measures provided by other companies. Orders represent written communications received from customers requesting the Company to provide products and/or services. Backlog is defined as the total dollar value of net orders received for which revenue has not yet been recognized. Management believes tracking orders and backlog are useful as they often times are leading indicators of future performance. In accordance with industry practice, contracts may include provisions for cancellation, termination, or suspension at the discretion of the customer.

The book-to-bill ratio is an operational measure that management uses to track the growth prospects of the Company. The Company calculates the book-to-bill ratio for a given period as net orders divided by net sales.

Given that each of orders, backlog, and book-to-bill ratio are operational measures and that the Company’s methodology for calculating orders, backlog and book-to-bill ratio does not meet the definition of a non-GAAP measure, as that term is defined by the U.S. Securities and Exchange Commission, a quantitative reconciliation for each is not required or provided.

Subsequent to quarter-end, closed $30 million in debt financing

OCU400 Phase 3 liMeliGhT clinical trial for retinitis pigmentosa (RP) on track to complete enrollment in 1H2025

OCU410 is currently in Phase 2 of the Phase 1/2 ArMaDa clinical trial

Data and Safety Monitoring Board (DSMB) for the OCU410ST GARDian clinical trial approved enrollment for the second phase of the Phase 1/2 clinical trial

New data on Phase 1/2 clinical trials for OCU410, OCU410ST and OCU400 to be presented at upcoming Clinical Showcase

MALVERN, Pa., Nov. 08, 2024 (GLOBE NEWSWIRE) — Ocugen, Inc. (Ocugen or the Company) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines, today reported third quarter 2024 financial results along with a general business update.

“I am very encouraged by the progress of our gene therapy programs and the clinical and regulatory milestones achieved in the third quarter of 2024, including the expansion of the OCU400 Phase 3 liMeliGhT clinical trial into Canada,” said Dr. Shankar Musunuri, Chairman, CEO, and Co-founder of Ocugen. “With the recent equity and debt financings, we have sufficient cash-on-hand to continue supporting our robust ophthalmology pipeline and extend our cash runway into 1Q2026.”

As OCU400 is advancing through Phase 3 clinical development, the expanded access program (EAP) for adult patients with early to advanced RP makes it possible to reach a greater segment of the RP patient population—300,000 in the U.S., Canada, and Europe combined. Additionally, including Canadian patients in the OCU400 Phase 3 liMeliGhT trial may allow for broader commercialization with the U.S. and Europe. These accomplishments and consistent trial enrollment are bringing the Company even closer to providing a potential one-time treatment for life to patients living with RP.

Phase 2 of the OCU410 Phase 1/2 ArMaDa clinical trial is underway and will assess the safety and efficacy of OCU410 in a larger group of patients who are randomized into either of two treatment groups (medium- or high-dose) or a control group. OCU410 is being developed for geographic atrophy (GA), an advanced stage of dry age-related macular degeneration (dAMD). GA affects approximately 2-3 million people in the U.S. & EU. Current FDA-approved treatments address only the complement system and require approximately 6-12 intravitreal injections per year, whereas OCU410 addresses all four pathways linked with dAMD pathophysiology and is delivered through a single subretinal injection. There remains no approved product to treat GA in the EU.

Over a series of conferences during the third quarter 2024, Ocugen had the opportunity to provide an update on its three clinical-stage modifier gene therapies to significant investor audiences as well as industry decision-makers during meetings like the Cell & Gene Meeting on the Mesa hosted by the Alliance for Regenerative Medicine.

“It is imperative to continue educating our key stakeholders about the differentiated mechanism of action of our gene-agnostic modifier gene therapy platform,” said Dr. Musunuri. “Unlike other product candidates in development to treat blindness diseases, our approach leverages master gene regulators that reset the functional network—rather than targeting a single mutation—and restore overall health to the retina. Our data continues to support the potential to treat multiple disease mutations with a one-time therapy for life.”

While gene therapy remains the primary focus for the Company, Ocugen continues to pursue funding opportunities across the portfolio to ensure that its innovative platforms reach the people who need them.

A clinical showcase, providing updates from Ocugen’s ongoing gene therapy trials, will be held on November 12, 2024, and will include preliminary safety and efficacy data from the Phase 1/2 OCU410 ArMaDa clinical trial for geographic atrophy and Phase 1/2 OCU410ST GARDian clinical trial for Stargardt disease, along with RP and LCA data updates from the OCU400 Phase 1/2 clinical trial.

Ophthalmic Gene Therapies—First-in-class

OCU400 – Enrollment continues in the Phase 3 liMeliGhT clinical trial and Health Canada approved enrollment across a maximum of 5 sites in Canada. FDA approved EAP for the treatment of adult patients with RP who may benefit from the mechanism of action of OCU400.

OCU410 – Actively recruiting patients in Phase 2 of the Phase 1/2 ArMaDa clinical trial. Preliminary safety and efficacy update on OCU410 Phase 1/2 ArMaDa clinical trial will be shared at upcoming clinical showcase.

OCU410ST – DSMB approved proceeding to Phase 2 of the Phase 1/2 GARDian clinical trial. Preliminary safety and efficacy update will be shared at upcoming clinical showcase.

Ophthalmic Biologic Product

OCU200 – FDA cleared the investigational new drug application for the Phase 1 clinical trial evaluating OCU200. The Company is planning to initiate the OCU200 Phase I clinical trial this quarter.

Third Quarter 2024 Financial Results

With the recent $30 million debt financing and $35 million equity financing in the third quarter, the cash runway now extends into 1Q2026.

The Company’s cash and restricted cash totaled $39.0 million as of September 30, 2024, compared to $39.5 million as of December 31, 2023.

Total operating expenses for the three months ended September 30, 2024 were $14.4 million and included research and development expenses of $8.1 million and general and administrative expenses of $6.3 million. This compares to total operating expenses for the three months ended September 30, 2023 of $16.1 million that included research and development expenses of $7.0 million and general and administrative expenses of $9.1 million.

Conference Call and Webcast Details

Ocugen has scheduled a conference call and webcast for 8:30 a.m. ET today to discuss the financial results and recent business highlights. Ocugen’s senior management team will host the call, which will be open to all listeners. There will also be a question-and-answer session following the prepared remarks.

Attendees are invited to participate on the call or webcast using the following details:

Dial-in Numbers: (800) 715-9871 for U.S. callers and (646) 307-1963 for international callers Conference ID: 9923172 Webcast: Available on the events section of the Ocugen investor site

A replay of the call and archived webcast will be available for approximately 45 days following the event on the Ocugen investor site.

About Ocugen, Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patient’s lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on X and LinkedIn.

Cautionary Note on Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, including, but not limited to, strategy, business plans and objectives for Ocugen’s clinical programs, plans and timelines for the preclinical and clinical development of Ocugen’s product candidates, including the therapeutic potential, clinical benefits and safety thereof, expectations regarding timing, success and data announcements of current ongoing preclinical and clinical trials, expected cash runway into the first quarter of 2026, the ability to initiate new clinical programs, statements regarding qualitative assessments of available data, potential benefits, expectations for ongoing clinical trials, anticipated regulatory filings and anticipated development timelines, which are subject to risks and uncertainties. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations, including, but not limited to, the risks that preliminary, interim and top-line clinical trial results may not be indicative of, and may differ from, final clinical data; that unfavorable new clinical trial data may emerge in ongoing clinical trials or through further analyses of existing clinical trial data; that earlier non-clinical and clinical data and testing of may not be predictive of the results or success of later clinical trials; and that that clinical trial data are subject to differing interpretations and assessments, including by regulatory authorities. These and other risks and uncertainties are more fully described in our annual and periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.

Reports third-quarter GAAP revenues of $61 million

Reports third-quarter net income of $1.1 million, GAAP EPS of $0.02 and adjusted EPS of $0.05

Reports third-quarter adjusted EBITDA of $7 million

Reports strong cash flow from operations of $8.8 million

Sells its automation unit on October 1, 2024, for $27 million in cash, with $7 million held in escrow

Declares fourth-quarter dividend of $0.045 per share, payable December 20, 2024, to shareholders of record as of December 3, 2024

Sets fourth-quarter guidance: revenues between $57 million and $58 million and adjusted EBITDA between $6.0 and $7.0 million

STAMFORD, Conn.–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III ), a leading global technology research and advisory firm, today announced its financial results for the third quarter ended September 30, 2024.

“ISG closed the third quarter strong, achieving the top of our updated guidance, with strong operating cash flow in the quarter,” said Michael P. Connors, chairman and CEO. “As we look ahead to 2025, we see signs that client demand in the U.S. is on the rise, including $5 billion of contract value now flowing through ISG Tango™, our digital sourcing platform, up 25 percent sequentially from the second quarter.”

Divestiture of Automation Unit

On October 1, ISG sold its robotic process automation unit to UST, a leading digital transformation solutions company, for $27 million in an all-cash transaction. ISG received $20 million in cash at closing with the remaining $7 million held in escrow, $4 million of which is subject to meeting certain contractual conditions with clients within 90 days and the remaining amount subject to the divested automation unit meeting certain revenue objectives by the end of the first quarter of 2025.

Third-Quarter 2024 Results

Reported revenues for the third quarter were $61.3 million, down 15 percent from $71.8 million in the prior year’s third quarter. Reported revenues were $40.1 million in the Americas, down 5 percent; $16.2 million in Europe, down 27 percent; and $4.9 million in Asia Pacific, down 32 percent, all versus the prior year.

ISG reported third-quarter operating income of $4.3 million, compared with operating income of $6.2 million in the prior year. The firm’s reported third-quarter net income was $1.1 million, compared with net income of $3.2 million in the prior year. Income per fully diluted share was $0.02, compared with income per fully diluted share of $0.06 in the prior year.

Adjusted net income (a non-GAAP measure defined below under “Non-GAAP Financial Measures”) for the third quarter was $2.5 million, or $0.05 per share on a fully diluted basis, compared with adjusted net income of $5.7 million, or $0.11 per share on a fully diluted basis, in the prior year’s third quarter.

Third-quarter adjusted EBITDA (a non-GAAP measure defined below under “Non-GAAP Financial Measures”) was $7.1 million, down 34 percent from the prior-year third quarter. Adjusted EBITDA margin (a non-GAAP measure calculated by dividing adjusted EBITDA by reported revenues) was 11.6 percent, compared with 14.8 percent in the prior year.

Other Financial and Operating Highlights

ISG generated $8.8 million of cash from operations in the third quarter, compared with generating $3.2 million of cash in the third quarter last year. The firm’s cash balance totaled $9.7 million at September 30, 2024, down from $11.8 million at June 30, 2024. During the third quarter, ISG paid down $8.0 million of debt, paid dividends of $2.3 million and repurchased $0.8 million of shares. As of September 30, 2024, ISG had $66.2 million in debt outstanding, down from $79.2 million at the end of last year.

2024 Fourth-Quarter Revenue and Adjusted EBITDA Guidance

“For the fourth quarter, ISG is targeting revenues of between $57 million and $58 million and adjusted EBITDA of between $6.0 million and $7.0 million. We will continue to monitor the macroeconomic environment, including the impact of FX, inflation and other factors, and adjust our business plans accordingly,” said Connors.

Quarterly Dividend

The ISG Board of Directors declared a fourth-quarter dividend of $0.045 per share, payable on December 20, 2024, to shareholders of record as of December 3, 2024.

“ISG remains committed to a disciplined capital allocation strategy that includes reinvesting in our business, managing our debt, returning capital to shareholders in the form of dividends and share repurchases, and supplementing our organic growth with strategic acquisitions to drive long-term shareholder value,” Connors said.

Conference Call

ISG has scheduled a call for 9 a.m., U.S. Eastern Time, November 8, 2024, to discuss the firm’s third-quarter results. The call can be accessed by dialing +1 (800) 715-9871 , or, for international callers, by dialing +1 (646) 307-1963 . The access code is 8229408 . A recording of the conference call will be accessible on ISG’s investor relations page for approximately four weeks following the call.

Forward-Looking Statements

This communication contains “forward-looking statements” which represent the current expectations and beliefs of management of ISG concerning future events and their potential effects. Statements contained herein including words such as “anticipate,” “believe,” “contemplate,” “plan,” “estimate,” “target,” “expect,” “intend,” “will,” “continue,” “should,” “may,” and other similar expressions are “forward-looking statements” under the Private Securities Litigation Reform Act of 1995. These forward-looking statements are not guarantees of future results and are subject to certain risks and uncertainties that could cause actual results to differ materially from those anticipated. Those risks relate to inherent business, economic and competitive uncertainties and contingencies relating to the businesses of ISG and its subsidiaries, including without limitation: (1) the failure to secure new engagements or loss of important clients; (2) the ability to hire and retain enough qualified employees to support operations; (3) the ability to maintain or increase billing and utilization rates; (4) management of growth; (5) the success of expansion internationally; (6) competition; (7) the ability to move the product mix into higher margin businesses; (8) the effect of the divestiture of the automation unit on ISG’s relationships with its customers and suppliers and on its retained business generally; (9) general political and social conditions such as war, political unrest and terrorism; (10) healthcare and benefit cost management; (11) the ability to protect ISG and its subsidiaries’ intellectual property or data and the intellectual property or data of others; (12) currency fluctuations and exchange rate adjustments; (13) the ability to successfully consummate or integrate strategic acquisitions; (14) outbreaks of diseases, including coronavirus, or similar public health threats or fear of such an event; and (15) potential terminations of engagements, delays or reductions in scope by clients. Certain of these and other applicable risks, cautionary statements and factors that could cause actual results to differ from ISG’s forward-looking statements are included in ISG’s filings with the U.S. Securities and Exchange Commission. ISG undertakes no obligation to update or revise any forward-looking statements to reflect subsequent events or circumstances.

Non-GAAP Financial Measures

ISG reports all financial information required in accordance with U.S. generally accepted accounting principles (GAAP). In this release, ISG has presented both GAAP financial results as well as non-GAAP information for the three and nine months ended September 30, 2024 and September 30, 2023. ISG believes that evaluating its ongoing operating results will be enhanced if it discloses certain non-GAAP information. These non-GAAP financial measures exclude non-cash and certain other special charges that many investors believe may obscure the user’s overall understanding of ISG’s current financial performance and the Company’s prospects for the future. ISG believes that these non-GAAP measures provide useful information to investors because they improve the comparability of the financial results between periods and provide for greater transparency of key measures used to evaluate the Company’s performance.

ISG provides adjusted EBITDA (defined as net income, plus interest, taxes, depreciation and amortization, foreign currency transaction gains/losses, non-cash stock compensation, interest accretion associated with contingent consideration, change in contingent consideration, acquisition-related costs, and severance, integration and other expense), adjusted net income (defined as net income, plus amortization of intangible assets, non-cash stock compensation, foreign currency transaction gains/losses, interest accretion associated with contingent consideration, change in contingent consideration, acquisition-related costs, write-off of deferred financing cost and severance, integration and other expense on a tax-adjusted basis), adjusted net income per diluted share, adjusted EBITDA margin, and selected financial data on a constant currency basis which are non-GAAP measures that the Company believes provide useful information to both management and investors by excluding certain expenses and financial implications of foreign currency translations, which management believes are not indicative of ISG’s core operations. These non-GAAP measures are used by ISG to evaluate the Company’s business strategies and management’s performance.

We evaluate our results of operations on both an as reported and a constant currency basis. The constant currency presentation, which is a non-GAAP financial measure, excludes the impact of year-over-year fluctuations in foreign currency exchange rates. We believe providing constant currency information provides valuable supplemental information regarding our results of operations, thereby facilitating period-to-period comparisons of our business performance, and is consistent with how management evaluates the Company’s performance. We calculate constant currency percentages by converting our current and prior periods’ local currency financial results using the same point in time exchange rates and then comparing the adjusted current and prior period results. This calculation may differ from similarly titled measures used by others and, accordingly, the constant currency presentation is not meant to be a substitution for recorded amounts presented in conformity with GAAP, nor should such amounts be considered in isolation.

Management believes this information facilitates comparison of underlying results over time. Non-GAAP financial measures, when presented, are reconciled to the most closely applicable GAAP measure. Non-GAAP measures are provided as additional information and should not be considered in isolation or as a substitute for results prepared in accordance with GAAP. A reconciliation of the forward-looking non-GAAP estimates contained herein to the corresponding GAAP measures is not being provided, due to the unreasonable efforts required to prepare it.

About ISG

ISG (Information Services Group) (Nasdaq: III ) is a leading global technology research and advisory firm. A trusted business partner to more than 900 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including AI, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs 1,600 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For more information, visit www.isg-one.com.

New facility will enable testing of liquid hydrogen (LH2), liquid oxygen (LOX) and liquid methane (LCH4)

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“Graham” or “the Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy and process industries, announced today its plans to construct a state-of-the-art cryogenic propellant testing facility in Florida, near its P3 Technologies, LLC subsidiary. Leveraging Graham’s longstanding expertise in the cryogenic and space launch industries, this new facility will help to meet increasing demand for efficient, scalable testing solutions in key markets, including Space, Defense, New Energy, and potential applications in the medical field.

The facility will offer a cost-effective, timely alternative to existing testing centers, which often prioritize flagship programs and leave other critical programs with limited options. This new facility will enable liquid hydrogen (LH2), liquid oxygen (LOX), and liquid methane (LCH4) testing at pressurized, sub-cooled, or saturated conditions, and is ideally suited for testing pumps, components, fluid management systems, and combustion devices. By expanding Graham’s capabilities in cryogenic propellant testing, the Company aims to better support both current and future customer programs, adding agility and depth to its testing services in response to diverse and evolving program requirements.

“We believe this new testing facility will strengthen our position as a trusted partner by directly addressing customer needs for timely and cost-effective cryogenic propellant testing, complementing our existing capabilities and advancing the support we can offer current programs,” said Dan Thoren, Graham Corporation President and Chief Executive Officer. “This investment underscores our commitment to supporting both current and future customer programs through innovative and accessible testing solutions, while enhancing Graham’s role across the Space, Defense, and New Energy sectors.”

The project will be executed over the next year, with initial tests anticipated to begin by mid-2025. The facility is projected to achieve a cash payback period of approximately two to three years and deliver an internal rate of return exceeding 20%, representing a strategic investment in Graham’s future.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy, and process industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “can,” “expects,” “potential,” “will,” “plans,” “aims,” “believe,” “projected,” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, the completion of the testing facility within the projected timeline, the Company’s ability to capitalize on the potential benefits of the new facility and timing to realize expected returns on investment, the estimated total market opportunity and the Company’s ability to capitalize on such market opportunity. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission, including under the heading entitled “Risk Factors,” its quarterly reports on Form 10-Q, and other filings it makes with the Securities and Exchange Commission. Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

New Zeus Motors are in Production and Ready for Use

SAN DIEGO, Nov. 07, 2024 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in Defense, National Security and Global Markets, today announced that its Zeus 1 and Zeus 2 Solid Rocket Motors (SRMs) completed their first successful flight on October 24, 2024, from the NASA Wallops Flight Facility in Virginia. This milestone launch provides the qualifications necessary to transition the Zeus SRMs to test programs supporting the U.S. Department of Defense, Foreign Allies, NASA, and commercial launch sponsors.

Kratos Zeus Solid Rocket Motors Complete Successful First Flight at Wallops

The flight test featured a Kratos two-stage Zeus 1 – Zeus 2 suborbital launch vehicle and provided substantial data to support rocket motor evaluation for use by future customers and sponsors who have baselined the Zeus rocket motors as part of their future test plans. Kratos expects to have production motors ready in the first quarter of 2025.

Kratos developed the Zeus family of SRMs in direct response to the need for affordable commercial launch vehicle stages for hypersonic test, ballistic missile targets, scientific research, sounding rocket and special customer missions. Kratos applied its significant rocket launch experience to establish the Zeus 1 and Zeus 2 motor specifications in close coordination with respective customer and user communities. Kratos internally funded development of the Zeus SRMs which are designed and manufactured to Kratos’ specifications by key merchant supplier and partner, L3Harris Technologies. L3Harris is on contract to begin delivering production motors to Kratos in the first quarter of 2025.

George Rumford, Director of the Department of Defense Test Resource Management Center, said, “Advancements in solid rocket motor development are critical to achieving rapid, affordable hypersonic testing.”

Dave Carter, President of Kratos’ Defense & Rocket Support Services Division, said, “I couldn’t be prouder of our whole team. They met the challenge to deliver these robust motors to market as fast as possible and meet the growing demand for rapid, reliable testing. The motors performed exceptionally well against predictions and are ready for immediate use by the broader test and research community.”

The Zeus 1 and Zeus 2 are high-performance, 32.5-inch diameter SRMs providing substantial performance improvements over similar legacy rockets. They are purposely designed to be fully compatible with existing payloads and launch infrastructure to enable rapid integration of new technologies and advanced payloads, including those currently under development by Kratos. These and other key attributes will provide Kratos and our customers with opportunities to fly more often, faster and farther, using fewer stages, and at a substantially reduced cost.

The Zeus SRM family is designed with versatility and affordability in mind as a complement to Kratos’ other internally funded investments such as the Erinyes hypersonic test “flyer” that debuted in June of this year. Kratos’ investments in the hypersonic and other relevant areas create a versatile family of test and evaluation products that offer complete systems. With the Zeus SRMs, the Erinyes, and other Kratos front end systems, Kratos is one of the only companies boasting both launcher and flyer systems within one organization, providing unmatched innovation, disruptive capabilities, mission responsiveness and affordability to the customer.

Eric DeMarco, President & CEO of Kratos Defense & Security Solutions, Inc., said, “Kratos is laser focused on supporting the Department of Defense, U.S. National Security requirements and working with our government partners to reinvigorate our country’s defense industrial base. Zeus’ successful mission is representative of the value Kratos’ strategy delivers to our stakeholders, with Kratos’ internally funded investments allowing us to rapidly develop and be first to market with affordable relevant systems for our partners and customers.”

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading-edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value-add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 31, 2023, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

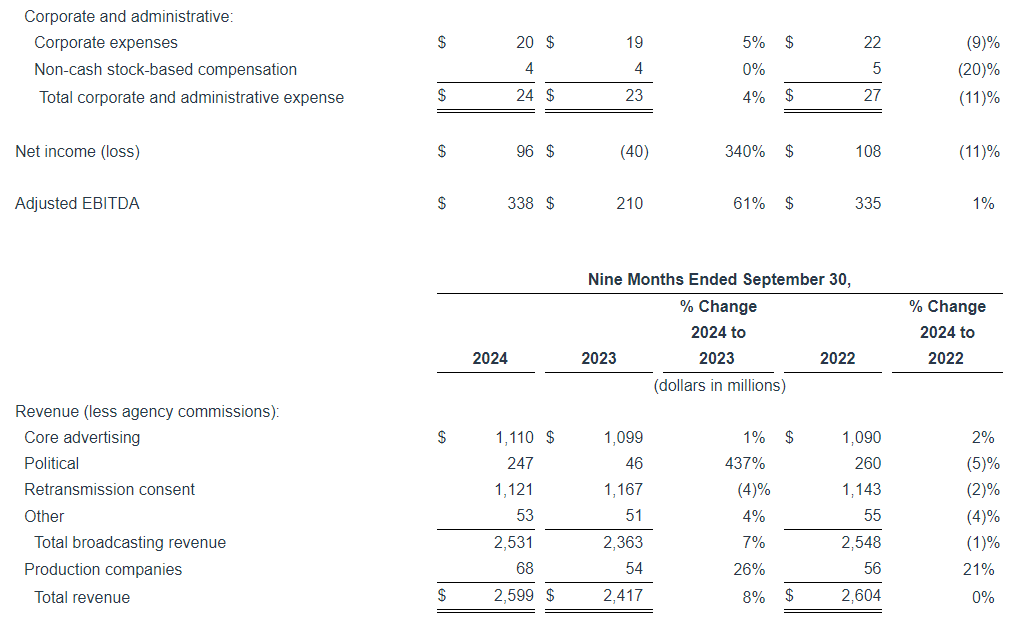

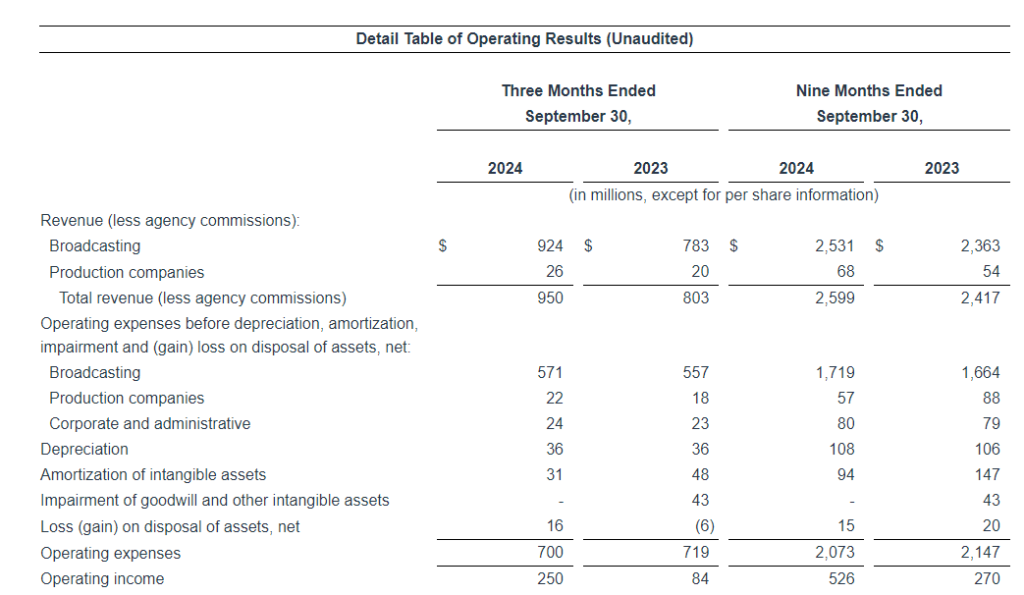

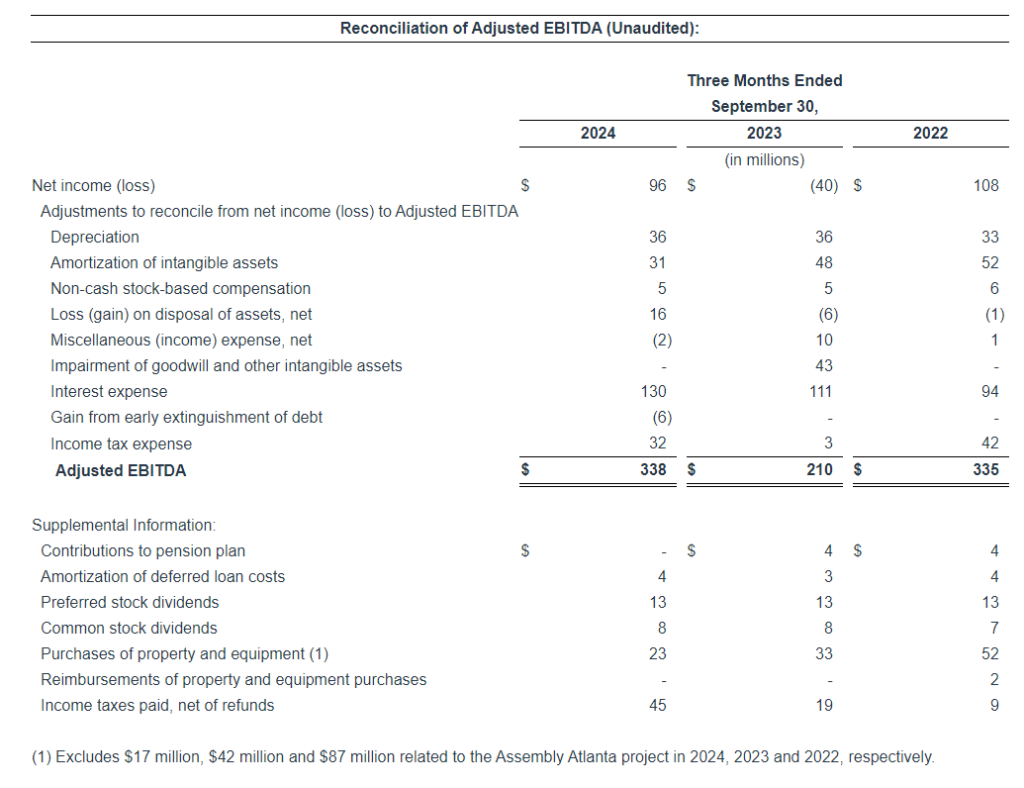

ATLANTA, Nov. 08, 2024 (GLOBE NEWSWIRE) — Gray Television, Inc. (“Gray,” “Gray Media,” “we,” “us” or “our”) (NYSE: GTN) today announced a strong third quarter ended September 30, 2024. Gray also projected full-year 2024 political advertising revenue of $500 million, as well as full-year 2024 Net Debt reduction of $500 million.

SUMMARY OF THIRD QUARTER RESULTS

OPERATING HIGHLIGHTS:

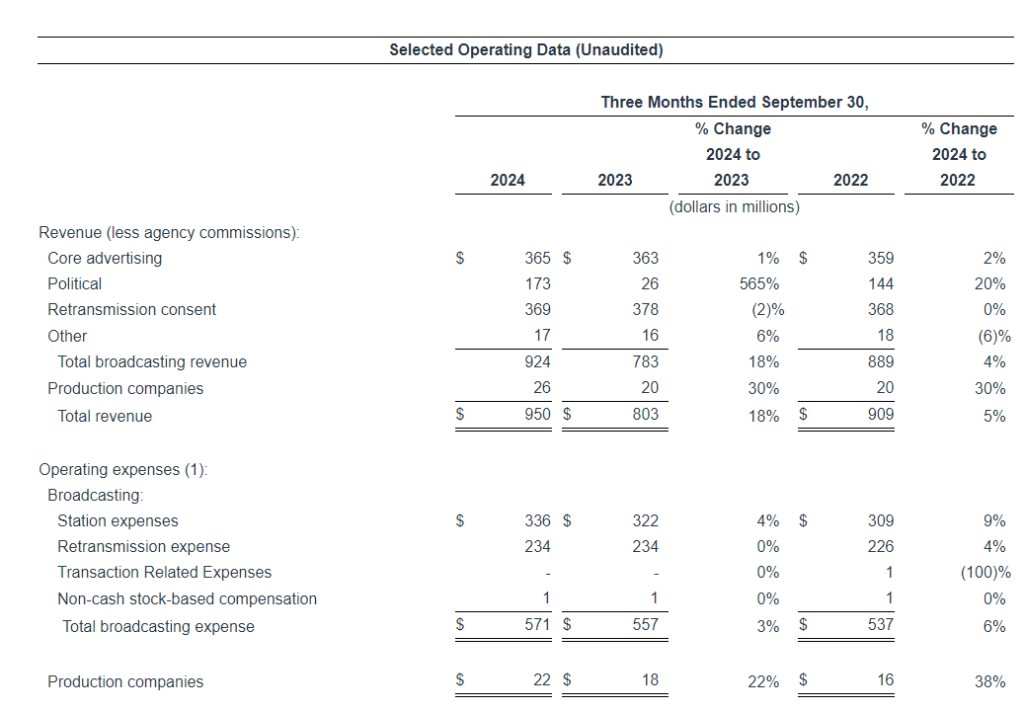

Total revenue in the third quarter of 2024 was $950 million, an increase of 18% from the third quarter of 2023.

Core advertising revenue in the third quarter of 2024 was $365 million, an increase of 1% from the third quarter of 2023.

Retransmission consent revenue in the third quarter of 2024 was $369 million, a decrease of 2% from the third quarter of 2023.

Political advertising revenue in the third quarter of 2024 was $173 million, an increase of 565% from the third quarter of 2023.

Total operating expenses (before depreciation, amortization and loss on disposal of assets) in the third quarter of 2024 was $617 million, which was 2% below the low end of our previously announced guidance for the quarter.

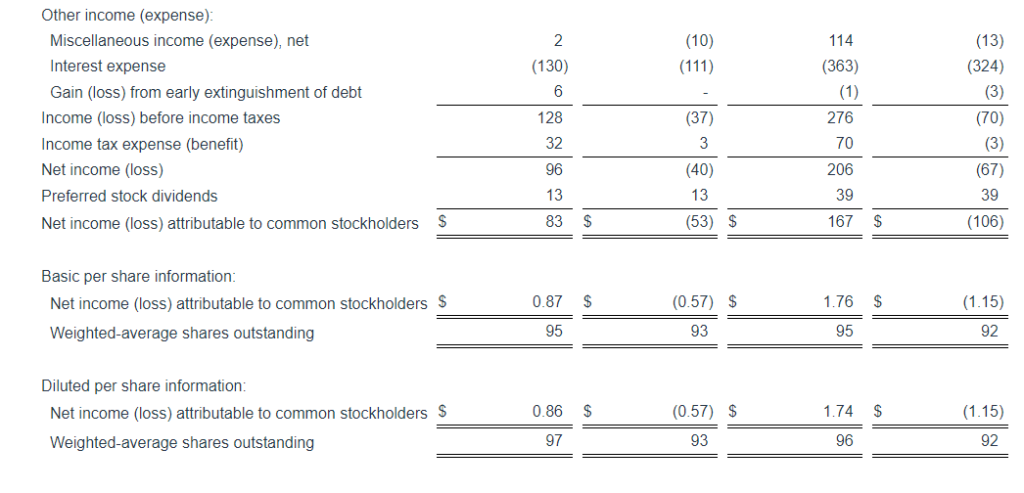

Net income attributable to common stockholders was $83 million in the third quarter of 2024, compared to a net loss attributable to common stockholders of $53 million in the third quarter of 2023.

Adjusted EBITDA was $338 million in the third quarter of 2024, an increase of 61% from the third quarter of 2023, due primarily to the cyclical increase in political advertising revenue.

OTHER KEY METRICS:

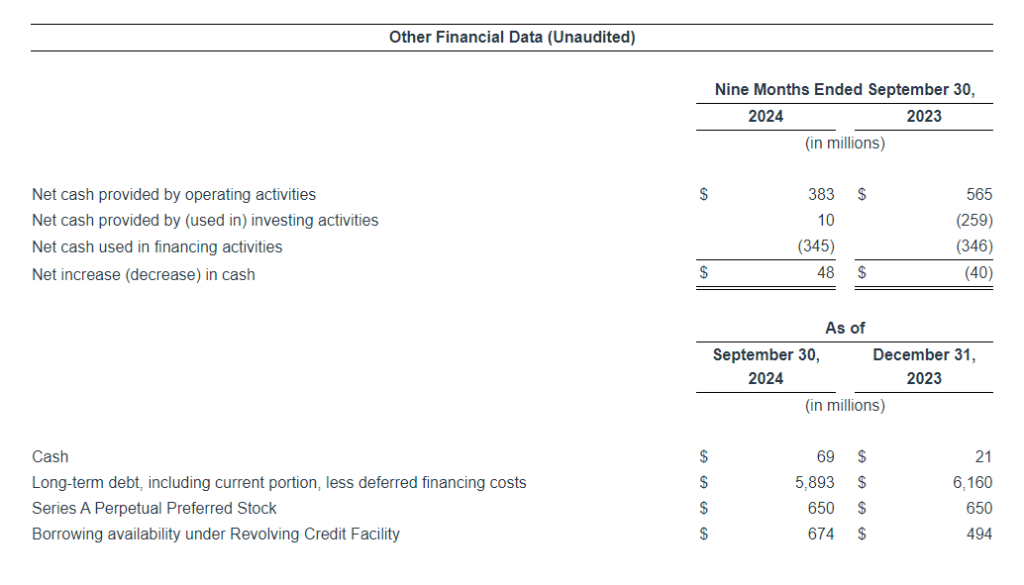

Through September 30, 2024, we reduced the principal amount of our debt by $241 million in 2024 and expect full-year 2024 Net Debt reduction of approximately $500 million.

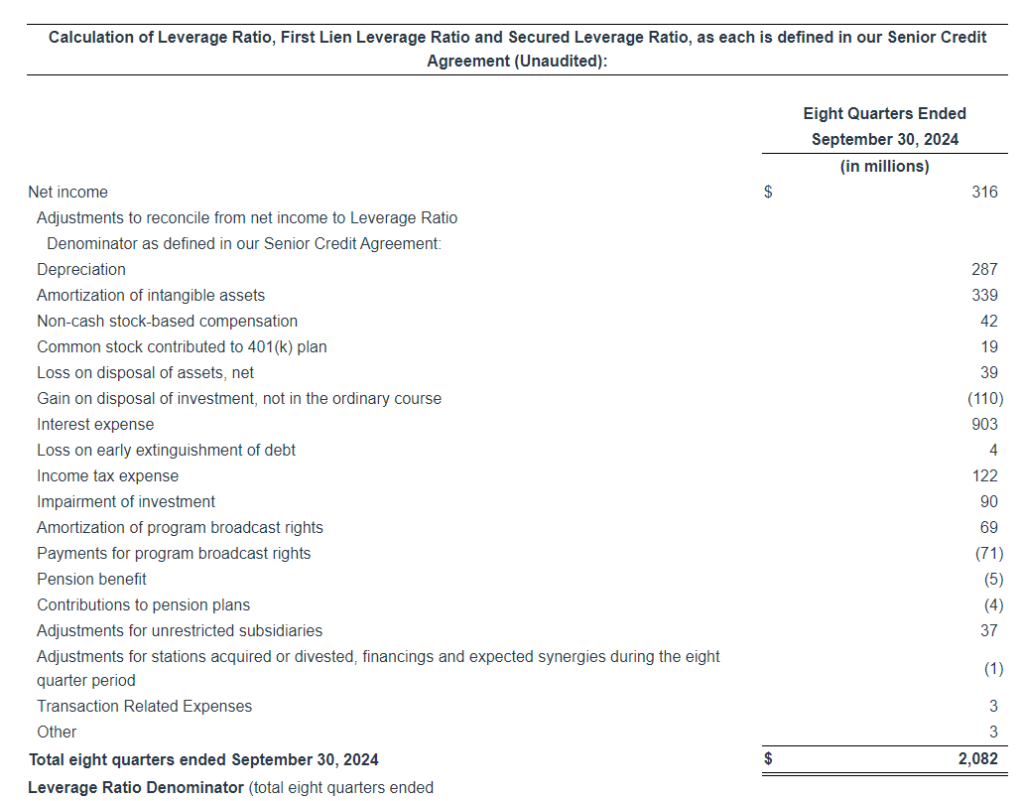

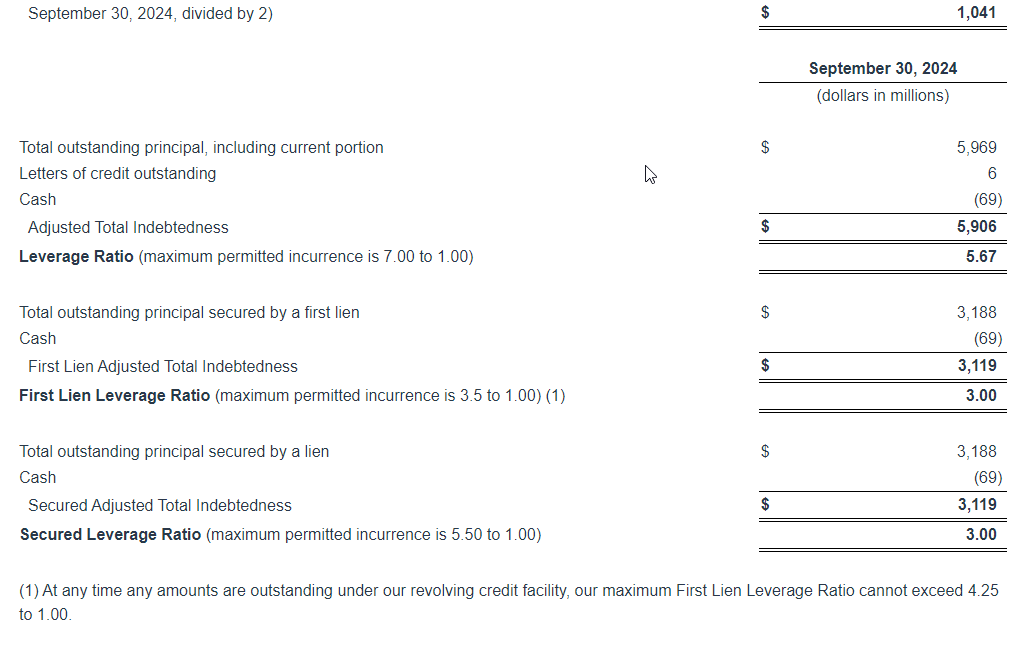

As of September 30, 2024, calculated as set forth in our Senior Credit Agreement, our First Lien Leverage Ratio and Leverage Ratio, which are net of $69 million of cash, were 3.00 to 1.00 and 5.67 to 1.00, respectively.

Currently, we have $674 million of borrowing availability under our undrawn Revolving Credit Facility.

Non-cash stock-based compensation was $5 million during each of the third quarters ended September 30, 2024 and 2023.

FINANCIAL RESULTS AND EXPECTATIONS

Our results in the third quarter were largely in line with our guidance, with the exception of political advertising revenues, which, while strong, were slightly below our expectations. Our broadcast and corporate operating expenses were much lower than expectations.

Our total revenue and our Core advertising revenue were within our guidance range at $950 million and $365 million, respectively, with Core advertising revenue up 1% compared to the third quarter of 2023. Our local television stations in several Southeastern markets experienced reductions in Core and political advertising revenues during late September, due to their extensive, often round-the-clock and commercial-free coverage of Hurricane Helene to support those affected communities in the third quarter.

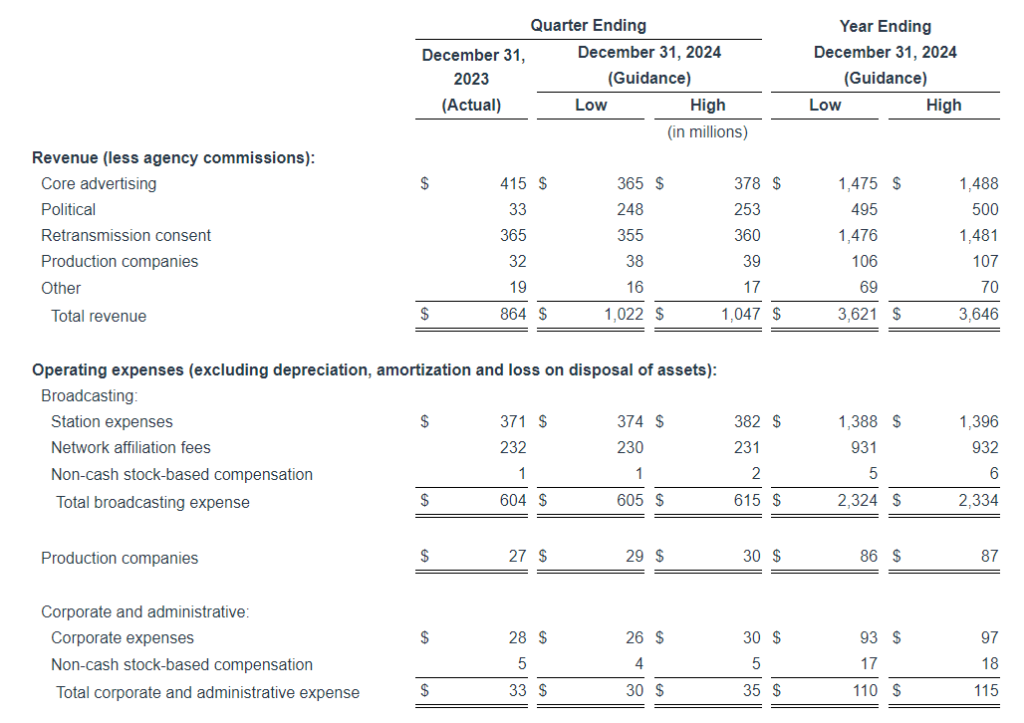

For the fourth quarter of 2024, we currently expect that Core advertising revenue will be down approximately 11% compared to the fourth quarter of 2023, due primarily to political advertising revenue displacement and the movement of SEC college football games in our Southeastern markets from the CBS Network to the ABC Network. In addition, the continuing impact of Hurricane Helene and the added impact of Hurricane Milton in the fourth quarter is expected to adversely impact Core advertising revenue in several of our Southeastern markets. We now anticipate Core advertising revenues within a range of $1.475 billion to $1.488 billion for full-year 2024, which is down approximately 3% from our earlier guidance of $1.525 billion and down approximately 2% compared to full-year 2023.

Our political advertising revenue in the third quarter of 2024 was $173 million, compared to the $190 million of political advertising revenue during the third quarter of 2020 that was recorded by our current television station portfolio. We anticipate that political advertising revenues for the fourth quarter of 2024 will be within a range of $248 million to $253 million, and for full-year 2024 within a range of $495 million to $500 million. Our political advertising revenue was impacted by fewer competitive non-presidential races in some of our markets during the second half of this year as well as the same significant factors affecting core advertising that are identified above.

Our retransmission consent revenue in the third quarter of 2024 was $369 million, which was within our guidance range. We currently expect retransmission consent revenues in the range of $355 million to $360 million for the fourth quarter of 2024 and, in a range of approximately $1.476 billion to $1.481 billion, for full-year 2024.

For the third quarter of 2024, our broadcasting operating expenses and corporate operating expenses were $14 million and $3 million below the low end of the expense guidance ranges, respectively. For full-year 2024, we currently expect broadcasting operating expenses and corporate operating expenses will be within the range of $2.324 billion to $2.334 billion, and $110 million to $115 million, respectively. These updated full-year expense estimates reflect significant decreases from the initial full-year guidance, provided in February of this year, of approximately $2.4 billion and $125 million, respectively. In addition, we currently anticipate capital expenditures for full-year 2024 of $135 million, which includes approximately $35 million, net of reimbursements, related to Assembly Atlanta. We expect additional reimbursements of approximately $18 million in the first quarter of 2025 related to 2024 capital expenditures at Assembly Atlanta.

COST CONTAINMENT INITIATIVES

Starting in August 2024, we began identifying and implementing various measures throughout the company that we expect will further reduce our operating expense run-rate by approximately $60 million on an annualized basis. As part of our routine budgeting process, we are carefully evaluating our capital expenditure needs for 2025.

We have taken several steps to reduce personnel expenses in 2025. These steps include streamlining workflows at our television stations and other business units, closing certain unfilled positions for which we were recruiting, eliminating certain positions that will not be filled following normal attrition throughout the second half of this year, and, for the first time in many years, eliminating certain positions in a handful of television stations and certain business units. Importantly, despite these staffing changes, we will continue to produce local newscasts with local journalists and local meteorologists in all of our existing local news markets, including small markets.

In terms of non-operating expenses, we anticipate a significant amount of interest savings due to lower debt balances resulting from open market debt repurchases and debt paydowns that have already occurred, and we anticipate will continue on an ongoing basis. We also anticipate that our cash income tax payments, net of refunds, for full-year 2024 will be approximately $133 million, approximately $49 million less than estimated in August of this year, due in part to interest expense deductibility in connection with Gray’s real estate assets, driven primarily by our Assembly Atlanta development.

DEBT REPURCHASES AND REPAYMENTS

We continue to focus on improving our balance sheet. From January 1, 2024 through September 30, 2024, we have reduced our principal amount of debt outstanding by $241 million. During the third quarter of 2024, we:

Repurchased and retired $29 million of our outstanding 2027 Notes on the open market at an average price of approximately 92.1% of par value, thereby reducing the remaining par value of our 2027 Notes to $671 million;

Repaid all amounts outstanding under our Revolving Credit Facility; and

Repurchased and retired approximately $16 million of our outstanding 2021 Term Loan on the open market at an average price of approximately 90.8% of par value.

In addition to the amounts above, we have previously entered into agreements to further reduce our 2021 Term Loan by an additional $39 million at an average price of approximately 92.6% of par value, which transactions will close in November 2024. We anticipate that upon completion of all of the above transactions, the remaining 2021 Term Loan principal outstanding at par value will be $1.400 billion.

We project, including actions taken to date, reduction of our Net Debt (also referred to herein as Adjusted Total Indebtedness) during full-year 2024 of $500 million during full-year 2024.

On November 7, 2024, our Board of Directors approved an increase in our debt repurchase authorization to repurchase additional debt in the open market, which replenished the previous authorization, bringing the total current authorization to $250 million. The extent of such repurchases, including the amount and timing of any repurchases, will depend on general market conditions, regulatory requirements, alternative investment opportunities and other considerations. This repurchase program supersedes any previous repurchase authorization, does not require us to repurchase a minimum amount of debt, and it may be modified, suspended or terminated at any time without prior notice.

TAXES

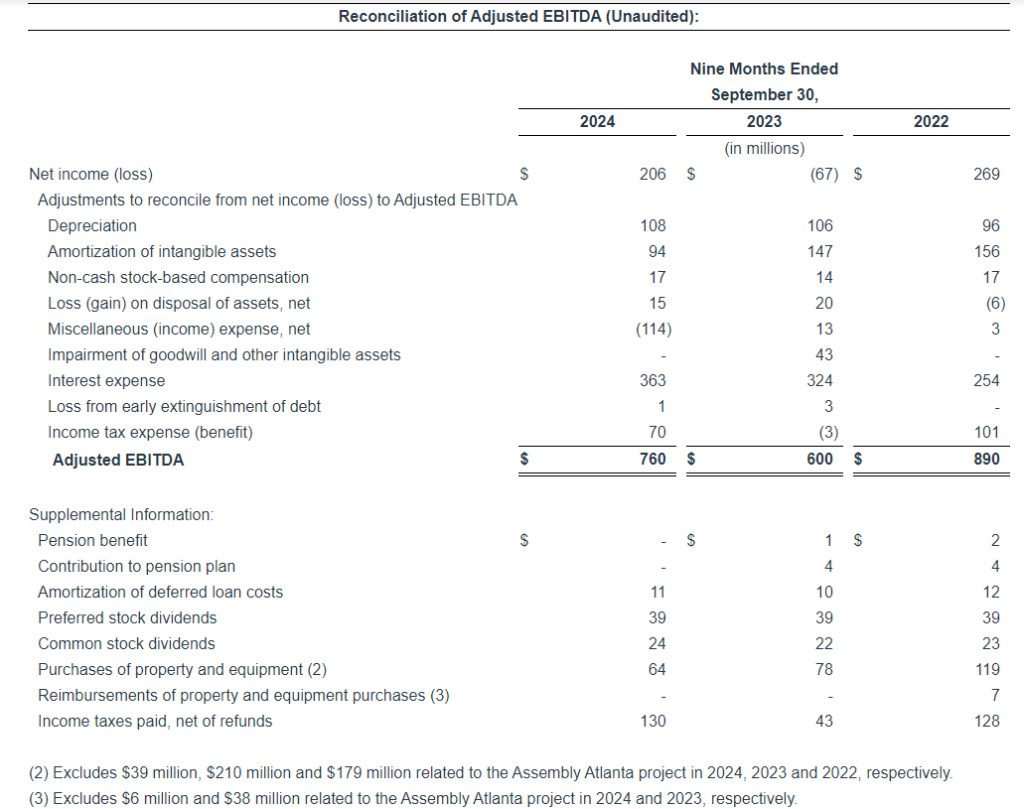

During the nine-months ended September 30, 2024 and 2023, we made income tax payments, net of refunds, of $130 million and $43 million, respectively. During the fourth quarter of 2024, based on our current forecasts, we anticipate making income tax payments, net of refunds, of approximately $3 million.

As of September 30, 2024, we have an aggregate of $282 million of various state operating loss carryforwards, of which we expect that approximately $201 million will not be utilized.

GUIDANCE FOR THE THREE MONTHS AND TWELVE MONTHS ENDING DECEMBER 31, 2024

Based on our current forecasts for the quarter ending December 31, 2024, we anticipate the following key financial results, as outlined below in approximate ranges and as compared to the quarter ended December 31, 2023, as well as certain currently anticipated full-year financial results. As always, guidance may change in the future based on several factors and therefore may not reflect actual results:

The Company

We are a multimedia company headquartered in Atlanta, Georgia. We are the nation’s largest owner of top-rated local television stations and digital assets serving 113 television markets that collectively reach approximately 36 percent of US television households. The portfolio includes 77 markets with the top-rated television station and 100 markets with the first and/or second highest rated television station, as well as the largest Telemundo Affiliate group with 43 markets totaling nearly 1.5 million Hispanic TV households. We also own Gray Digital Media, a full-service digital agency offering national and local clients digital marketing strategies with the most advanced digital products and services. Our additional media properties include video production companies Raycom Sports, Tupelo Media Group, and PowerNation Studios, and studio production facilities Assembly Atlanta and Third Rail Studios. Gray also owns a majority interest in Swirl Films.

Cautionary Statements for Purposes of the “Safe Harbor” Provisions of the Private Securities Litigation Reform Act

This press release contains certain forward-looking statements that are based largely on our current expectations and reflect various estimates and assumptions by us. These statements are statements other than those of historical fact and may be identified by words such as “estimates,” “expect,” “anticipate,” “will,” “implied,” “assume” and similar expressions. Forward-looking statements are subject to certain risks, trends and uncertainties that could cause actual results and achievements to differ materially from those expressed in such forward-looking statements. Such risks, trends and uncertainties, which in some instances are beyond our control, include: estimates of future revenue, future expenses, future capital expenditures, future income tax payments, future workforce reductions and other future events. We are subject to additional risks and uncertainties described in our quarterly and annual reports filed with the Securities and Exchange Commission from time to time, including in the “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections contained therein, which reports are made publicly available via our website, www.graymedia.com. Any forward-looking statements in this press release should be evaluated in light of these important risk factors. This press release reflects management’s views as of the date hereof. Except to the extent required by applicable law, Gray undertakes no obligation to update or revise any information contained in this press release beyond the published date, whether as a result of new information, future events or otherwise. Information about certain potential factors that could affect our business and financial results and cause actual results to differ materially from those expressed or implied in any forward-looking statements are included under the captions “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in our Annual Report on Form 10-K for the year ended December 31, 2023, and may be contained in reports subsequently filed with the U.S. Securities and Exchange Commission and available at www.sec.gov.

Conference Call Information:

We will host a conference call to discuss our third quarter operating results on November 8, 2024. The call will begin at 11:00 AM Eastern Time. The live dial-in number is 1 (800) 285-6670. The call will be webcast live and available for replay at www.graymedia.com. The taped replay of the conference call will be available at 1 (888) 556-3470, Confirmation Code: 898476# until December 8, 2024.

Gray Contacts

Web site: www.graymedia.com

Hilton H. Howell, Jr., Executive Chairman and Chief Executive Officer, (404) 266-5513

Pat LaPlatney, President and Co-Chief Executive Officer, (334) 206-1400

Jeffrey R. Gignac, Executive Vice President and Chief Financial Officer, (404) 504-9828

Kevin P. Latek, Executive Vice President, Chief Legal and Development Officer, (404) 266-8333

Non-GAAP Terms

In addition to results prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”), this earnings release discusses “Adjusted EBITDA” a non-GAAP performance measure that management uses to evaluate the performance of the business. Adjusted EBITDA is calculated as net income (loss), adjusted for income tax expense (benefit), interest expense, loss on extinguishment of debt, non-cash stock-based compensation costs, non-cash 401(k) expense, depreciation, amortization of intangible assets, impairment of goodwill and other intangible assets, impairment of investments, loss (gain) on asset disposals and certain other miscellaneous items. We consider Adjusted EBITDA to be an indicator of our operating performance.