ISG (Information Services Group) (Nasdaq: III) is a leading global technology research and advisory firm. A trusted business partner to more than 700 clients, including more than 75 of the world’s top 100 enterprises, ISG is committed to helping corporations, public sector organizations, and service and technology providers achieve operational excellence and faster growth. The firm specializes in digital transformation services, including automation, cloud and data analytics; sourcing advisory; managed governance and risk services; network carrier services; strategy and operations design; change management; market intelligence and technology research and analysis. Founded in 2006, and based in Stamford, Conn., ISG employs more than 1,300 digital-ready professionals operating in more than 20 countries—a global team known for its innovative thinking, market influence, deep industry and technology expertise, and world-class research and analytical capabilities based on the industry’s most comprehensive marketplace data. For additional information, visit www.ISG-One.com

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q25 Results. Revenue of $61.6 million was up 7% versus last year, excluding results for the divested automation unit. On the same basis, revenues were $39.5 million in the Americas, up 16% versus the prior year, revenues in Europe were $16.6 million, down 7%, and Asia Pacific revenues were $5.4 million, down 1%. Adjusted EBITDA of $8.3 million rose 17% y-o-y. ISG reported adjusted net income of $4.1 million, or $0.08/sh, compared with adjusted net income of $3.8 million, or $0.08/sh last year. We were at $60 million, $7.25 million, and $0.07/sh, respectively.

An Acquisition. ISG has signed a definitive agreement to acquire Martino & Partners, a highly respected strategic advisory firm serving public and private sector clients in Italy. The transaction is expected to close in early September. The acquisition is expected to expand ISG’s client base, geographic footprint, and capabilities in Italy, including AI, in a market with emerging growth potential.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

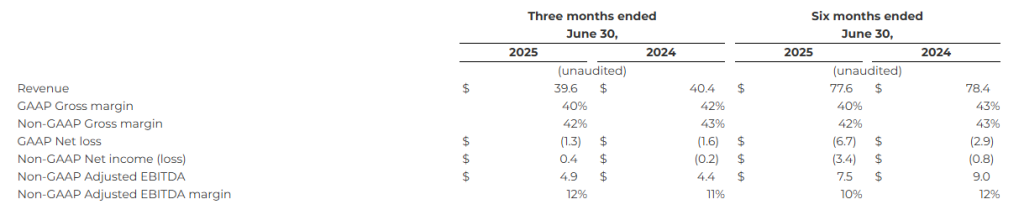

Mixed Q2 results. The company reported Q2 revenue of $10.1 million, below our forecast of $12.5 million, driven by continued underperformance in the Sell-side business, which generated $2.5 million vs. our forecast of $4.5 million. Despite the shortfall, adj. EBITDA loss of $1.5 million was better than expected, aided by cost reductions and lower headcount from increased automation.

Implications for second half performance. The Q2 revenue miss was largely attributable to slower-than-expected progress with the company’s “direct connections” initiative, in which its SSP integrates directly with DSPs to bypass intermediaries. While the strategy remains a critical long-term growth lever, the implementation delays have weighed on near-term Sell-side revenue performance, as well as the outlook for the second half 2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Increasing Demand. Increasing demand for the solutions provided, particularly from ICE, contributed to a strong second quarter, as nationwide detention populations under ICE custody reached an all-time high. ICE revenue rose 17.2% y-o-y, but we also note revenue from state partners increased 5.2% y-o-y and U.S. Marshals revenue increased 2.7% y-o-y.

2Q25 Results. Revenue was $538.2 million in 2Q25, up from $490.1 million last year. We were at $500.6 million. Safety and Community average occupancy increased to 76.8% from 74.3%, even with an overhang from the recently activated California City facility. Adjusted EBITDA was $103.3 million, up 23.2% y-o-y. NFFO per share was $0.59, up 40.5%. CoreCivic reported adjusted EPS of $0.36, up 80%.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q2 results. Conduent reported second-quarter revenue of $754 million, in line with our estimate. Adj. EBITDA of $37 million exceeded our $33 million forecast. Importantly, all three business segments posted sequential growth in new business annual contract value, signaling building commercial momentum and suggesting that execution is improving across the platform.

Portfolio rationalization in the works. The company collected the remaining $50 million from its Curbside Management divestiture, completing phase one of its portfolio rationalization strategy. Management indicated additional transactions are in progress, aimed at boosting profitability. We believe updates are likely by year-end, as the team continues to reshape the business with a focus on higher-margin opportunities.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Western Midstream to acquire Aris Water Solutions for ~$2B in cash and equity. – Deal creates a fully integrated produced-water system in the Delaware Basin. – Acquisition expands WES’s New Mexico footprint and diversifies its customer base.

Western Midstream Partners announced Tuesday that it will acquire Aris Water Solutions in a cash-and-equity deal valued at approximately $2 billion. The transaction aims to strengthen Western Midstream’s position as a leading full-cycle water infrastructure provider in the Permian Basin, particularly in the Delaware sub-basin.

Under the agreement, Aris shareholders will receive either 0.625 Western Midstream common units or $25 per share in cash, subject to proration and totaling no more than $415 million in cash consideration. The deal represents a 23% premium to Aris’s closing share price and a 10% premium to its 30-day volume-weighted average price. Once completed, Aris shareholders are expected to own about 7% of the combined company.

The acquisition is expected to significantly enhance Western Midstream’s ability to serve oil and gas producers with water gathering, recycling, disposal, and transport services. Aris brings a portfolio of assets that includes approximately 790 miles of water pipelines, 1,800 MBbls/d of disposal capacity, and 1,400 MBbls/d of recycling capacity. The company also operates on over 625,000 dedicated acres under long-term contracts with a number of investment-grade exploration and production customers.

In addition to operational expansion, the transaction provides access to the McNeill Ranch in New Mexico. The asset includes surface rights and pore space that can be used to expand disposal capacity in a region that has seen accelerated drilling activity and increased water-handling demand.

Executives from both companies say the integration will create long-term value through infrastructure synergies, increased flow assurance for producers, and more efficient capital allocation. The combination also positions the new entity as a differentiated provider of water infrastructure services at a time when producers are looking for environmentally sustainable and cost-effective water management solutions.

Western Midstream expects the deal to be accretive to its free cash flow per unit in 2026. The company is targeting $40 million in annual cost synergies and plans to maintain a pro forma net leverage ratio of approximately 3.0x. Additionally, the ongoing development of long-haul infrastructure like the Pathfinder pipeline is expected to provide added operational flexibility and growth potential.

The acquisition underscores a growing trend in the energy sector, where midstream companies are investing more heavily in water infrastructure as a strategic asset. With environmental regulations tightening and production efficiency under the spotlight, control over water recycling and disposal has become a core competitive advantage for Permian operators.

Apple Inc. (AAPL) is ramping up its domestic investment strategy with a newly announced $100 billion commitment to U.S. manufacturing and infrastructure, expanding its total U.S. investment to $600 billion over the next four years. The announcement comes just hours ahead of a scheduled White House event where Apple CEO Tim Cook will join President Donald Trump in the Oval Office.

The announcement is viewed as both a response to and a strategic buffer against mounting trade tensions. The Trump administration has signaled its intent to impose a 25% tariff on iPhones imported from India, where Apple now manufactures the majority of U.S.-bound iPhones after shifting production away from China.

These escalating tariff threats are already hitting the bottom line. In its most recent quarterly earnings report, Apple disclosed an $800 million tariff-related impact and forecasted another $1.1 billion in related costs this quarter. The company’s shift toward increased U.S. investment appears aimed at minimizing long-term exposure to geopolitical trade risks while addressing growing political pressure to manufacture more within the United States.

The centerpiece of this new initiative is the American Manufacturing Program, which will involve expanded partnerships with U.S.-based suppliers, additional AI-focused data centers, and a potential new semiconductor facility. These moves reflect a broader trend in tech: companies are reassessing global supply chains not just for efficiency, but for resiliency.

Apple’s share price responded sharply to the news, jumping more than 5% in midday trading. The stock move reflects both investor confidence in Apple’s ability to navigate regulatory challenges and the perceived benefits of deeper integration into the U.S. industrial base.

For Apple, this could be a turning point. The tech giant has long relied on overseas manufacturing for its scale, efficiency, and cost advantages. But the dual pressures of tariffs and supply chain vulnerabilities exposed during the COVID-19 pandemic have reshaped that calculus. Bringing more production stateside not only helps Apple hedge against future tariffs—it may also give the company greater control over component access and intellectual property protections.

Still, scaling U.S.-based iPhone production remains a complex challenge. Industry experts warn that building out sufficient infrastructure, skilled labor pools, and logistical networks could take years. Apple’s long-term strategy may involve a hybrid model, combining strategic U.S. investments with continued production in global hubs like India and Vietnam.

With the 2026 presidential election already on the horizon, companies like Apple are likely to face increased scrutiny over domestic job creation and industrial policy alignment. This latest move positions Apple as both a responsive corporate citizen and a resilient global operator—prepared for whatever comes next in an increasingly fragmented trade landscape.

Improvement in Operating Income, Adjusted EBITDA, and New Business Program

Company Reiterates Full Year 2025 Guidance

CHARLOTTE, N.C., Aug. 06, 2025 (GLOBE NEWSWIRE) — NN, Inc. (NASDAQ: NNBR) (“NN” or the “Company”), a global diversified industrial company that engineers and manufactures high-precision components and assemblies, today reported results for the second quarter ended June 30, 2025.

Second Quarter Highlights: (results from continuing operations compared with prior year, where comparisons are noted)

Net sales of $107.9 million, down 2.4% on a pro forma basis

Gross margin of 16.9%, and adjusted gross margin of 19.5%

Operating loss of $1.5 million and adjusted operating income of $4.9 million, an increase of $2.8 million

Adjusted EBITDA of $13.2 million, with an adjusted EBITDA margin of 12.2%

New business wins were $32.7 million in the first half of 2025, and NN has over 100 programs launching in 2025 that are expected to add greater than $45 million in future sales at full run-rate

Harold Bevis, President and Chief Executive Officer, said, “NN delivered a solid quarter for gross margins, operating income, adjusted operating income, and adjusted EBITDA. We are pleased with our reported results, new business acquisition, and new business launches. We leveraged the soft market environment to upsize our business development activities and investments. Our soft top-line centers around certain automotive customers. Conversely, we have been able to partially offset this weakness through the contribution of new business launches and precious metals pass-through pricing.”

“We have increased the size of our new business program in terms of prospecting, launching, and investing. We now have over 40 people in business development and launch, and we expect to launch over 100 new programs in 2025. We expect those launches will add over $45 million in future sales at run-rate. We plan to invest $18 to $20 million on capital projects in 2025. The twin goals of lowering our costs overall as a company while adding increased focus on growth is working and will be the main drivers of sustained top-line growth and increased profitability.”

Mr. Bevis continued, “Our current expectation is that some of our automotive markets may have similar soft patterns in the second half of 2025. In response, we have activated our own mitigation levers including tight cost controls and working capital actions. We are underway with tariff mitigation efforts with our customers and have positioned ourselves as a tariff problem solver.”

“We are using this opportunity to accelerate our transformation activities. We are actively investing in growth capex, and we have hired additional personnel to accelerate growth in our targeted areas. We recently announced the hiring of Tim Erro as NN’s new Chief Commercial Officer and have also added new account managers in our targeted areas of medical, stampings, and electrical products. We now have a core team of electrical harness experts and are evaluating an organic entry into this new market, just as we have done to enter the medical market.”

Mr. Bevis concluded, “Our transformation plan is working and we have increased our efforts during this slow auto market. Lastly, we have fully kicked off an M&A program and are seeking targets that are consistent with our strategy and can help refinance our preferred stock.”

Second Quarter Results

Net sales were $107.9 million, a decrease of 12.3% compared to the second quarter of 2024 net sales of $123.0 million, primarily due to the rationalization of underperforming business and plants in 2024, the sale of our Lubbock operations in 2024, and lower automotive volumes. These decreases were partially offset by the contribution of 70 new business launches in the first half of 2025 and higher precious metals pass-through pricing. Loss from operations for the second quarter of 2025 was $1.5 million, an improvement of 28.6% compared to the second quarter of 2024 loss from operations of $2.1 million.

Second Quarter Adjusted Results

Pro forma net sales when adjusted for rationalized sales, currency changes, and the sale of Lubbock, were a decrease of 2.4% in the second quarter when compared to the second quarter of 2024.

Adjusted income from operations for the second quarter of 2025 was $4.9 million compared to adjusted income from operations of $2.1 million for the same period in 2024. Adjusted EBITDA was $13.2 million, or 12.2% of sales, compared to $13.4 million, or 10.9% of sales, for the same period in 2024.

Adjusted net income was $0.7 million, or $0.02 per diluted share, compared to adjusted net loss of $0.7 million, or $(0.02) per diluted share, for the same period in 2024. Free cash flow was a use of cash of $3.2 million compared to a use of cash of $1.3 million for the same period in 2024.

Power Solutions

Net sales for the second quarter of 2025 were $44.6 million compared to $50.2 million in the same period in 2024. The decrease is primarily due to the sale of our Lubbock operations, partially offset by higher precious metals pass-through pricing. Income from operations was $5.8 million compared to income from operations of $5.3 million for the same period in 2024.

Adjusted income from operations was $8.4 million compared to $8.1 million in the second quarter of 2024. The increase in adjusted income from operations was primarily due to favorable product mix, and lower operating costs.

Mobile Solutions

Net sales for the second quarter of 2025 were $63.4 million compared to $72.9 million in the second quarter of 2024. The decrease in sales was primarily due to rationalized volume and lower automotive volume. Loss from operations was $1.1 million compared to loss from operations of $1.6 million for the same period in 2024.

Adjusted income from operations was $2.3 million compared to adjusted loss from operations of $0.7 million in the second quarter of 2024. The increase in adjusted income from operations was primarily due to improved margin mix of sales and lower operating costs.

2025 Outlook

NN is maintaining its full-year 2025 outlook.

Net sales to range between $430 to $460 million

Adjusted EBITDA to range between $53 to $63 million

Free cash flow to range between $14 to $16 million; guidance assumes receipt of CARES Act refund in 2025

New business wins to range between $60 to $70 million

Chris Bohnert, Senior Vice President and Chief Financial Officer, commented, “Our second quarter results were largely in line with expectations. We are maintaining our current guidance and given the ongoing tariff-driven uncertainties and the anticipated downstream effects for our customers, we continue to direct expectations towards the lower end of our guided ranges. We note that the uncertainty of the current macroeconomic environment, particularly the potential for shifts in trade policy and interest rates could drive variability in our results, which may fall above or below our current forecasts. Irrespective of the near-term macroeconomic backdrop, we continue to pursue expense mitigation and operational efficiencies to partially offset potential impacts to end market demand. We are investing in commercial enhancements to accelerate future growth, and we remain optimistic about the strong pace of our transformation and growth opportunities.”

Conference Call

NN will discuss its results during its quarterly investor conference call on August 7, 2025, at 9 a.m. ET. The call and supplemental presentation may be accessed via NN’s website, www.nninc.com. The conference call can also be accessed by dialing 1-888-999-3182 or 1-848-280-6330. For those who are unavailable to listen to the live broadcast, a replay will be available shortly after the call until August 7, 2026.

NN discloses in this press release the non-GAAP financial measures of adjusted income (loss) from operations, adjusted EBITDA, adjusted EBITDA margin, adjusted net income (loss), adjusted net income (loss) per diluted common share, and free cash flow. Each of these non-GAAP financial measures provides supplementary information about the impacts of acquisition, divestiture and integration related expenses, foreign-exchange impacts on inter-company loans, reorganizational and impairment charges.

The financial tables found later in this press release include a reconciliation of adjusted income (loss) from operations, adjusted operating margin, adjusted EBITDA, adjusted EBITDA margin, adjusted net income (loss), adjusted net income (loss) per diluted share, free cash flow to the U.S. GAAP financial measures of income (loss) from operations, net income (loss), net income (loss) per diluted common share, and cash provided (used) by operating activities.

About NN, Inc.

NN, Inc., a global diversified industrial company, combines advanced engineering and production capabilities with in-depth materials science expertise to design and manufacture high-precision components and assemblies for a variety of markets on a global basis. Headquartered in Charlotte, North Carolina, NN has facilities in North America, South America, Europe and China. For more information about the company and its products, please visit www.nninc.com.

This press release contains express and implied forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our financial outlook for the full year of fiscal 2025, the impact of, and our ability to execute, our corporate strategies and business initiatives and the potential impact tariffs, high interest rates, high metal costs and additional economic uncertainties may have on our financial statements and results of operations. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “growth,” “guidance,” “intend,” “may,” “will,” “possible,” “potential,” “predict,” “project”, “trajectory” or other similar words, phrases or expressions. Forward-looking statements involve a number of risks and uncertainties that are outside of management’s control and that may cause actual results to be materially different from such statements. Such factors include, among others, general economic conditions and economic conditions in the industrial sector; the potential impacts of tariffs on the U.S. economy, the economy of other countries in which we conduct operations and our industry, as well as the potential implications and ramifications of tariffs on our business and the local and global supply chains supporting the same, and our ability to mitigate any adverse impacts of such; competitive influences; risks that current customers will commence or increase captive production; risks of capacity underutilization; quality issues; material changes in the costs and availability of raw materials; economic, social, political and geopolitical instability, military conflict, currency fluctuation, and other risks of doing business outside of the United States; inflationary pressures and changes in the cost or availability of materials, supply chain shortages and disruptions, the availability of labor and labor disruptions along the supply chain; our dependence on certain major customers, some of whom are not parties to long-term agreements (and/or are terminable on short notice); the impact of acquisitions and divestitures, as well as expansion of end markets and product offerings; our ability to hire or retain key personnel; the level of our indebtedness; the restrictions contained in our debt agreements; our ability to obtain financing at favorable rates, if at all, and to refinance existing debt as it matures; our ability to secure, maintain or enforce patents or other appropriate protections for our intellectual property; uncertainty of government policies and actions after recent U.S. elections in respect to global trade, tariffs and international trade agreements; and cyber liability or potential liability for breaches of our or our service providers’ information technology systems or business operations disruptions. The foregoing factors should not be construed as exhaustive and should be read in conjunction with the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in the Company’s filings made with the U.S. Securities and Exchange Commission. Any forward-looking statement speaks only as of the date of this press release and are based on information available to NN at the time those statements are made and/or management’s good faith belief as of that time with respect to future events. The Company undertakes no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law. New risks and uncertainties may emerge from time to time, and it is not possible for the Company to predict their occurrence or how they will affect the Company. The Company qualifies all forward-looking statements by these cautionary statements.

With respect to any non-GAAP financial measures included in the following document, the accompanying information required by SEC Regulation G can be found in the back of this document or in the “Investors” section of the Company’s web site, www.nninc.com, under the heading “News & Events” and subheading “Presentations.”

Investor & Media Contacts: Joe Caminiti or Stephen Poe NNBR@alpha-ir.com 312-445-2870

NORWOOD, Mass., Aug. 06, 2025 (GLOBE NEWSWIRE) — MariMed Inc. (“MariMed” or the “Company”) (CSE: MRMD) (OTCQX: MRMD), a leading multi-state cannabis operator focused on improving lives every day, today announced its financial results for the second quarter ended June 30, 2025.

Management Commentary

“We delivered growth and expanded operations across our business during the second quarter, continuing our progress of building a leading cannabis consumer packaged goods company,” said Jon Levine, MariMed Chief Executive Officer. “Our ‘Expand the Brand’ strategy is working. Our innovative, high-quality portfolio of brands grew or maintained their market share across our core markets. We remain confident in delivering the shareholder value our investors deserve by leveraging our brands as the primary growth engine of our company. Looking ahead, we anticipate increasing product distribution through the addition of adult-use sales in Delaware, a new licensing agreement in Maine, and our recently announced entry into Pennsylvania. In addition, the strength of our balance sheet affords us optionality with respect to M&A and licensing opportunities.”

“We delivered sequential growth in both wholesale and retail revenues for the second quarter, a substantial increase in adjusted EBITDA, and we were cash flow positive,” said Mario Pinho, MariMed Chief Financial Officer. “Our performance reflects strong execution in Massachusetts, full-quarter contributions from Delaware, and a solid retail strategy. With the METRC system migration in Illinois behind us and Missouri under active review, we remain confident in the revenue catalysts we have built for the second half of the year, including adult use in Delaware, entry into Pennsylvania, and expanded wholesale.”

Financial Highlights1

The following table summarizes the Company’s consolidated financial highlights (in millions, except percentage amounts):

1 See the reconciliations of non-GAAP financial measures to the most directly comparable GAAP measures and additional information about non-GAAP measures in the section entitled “Discussion of Non-GAAP Financial Measures” below and in the financials information included herewith.

CONFERENCE CALL

MariMed management will host a conference call on Thursday, August 7, 2025 at 8:00 a.m. Eastern time, to discuss these results. The conference call may be accessed through MariMed’s Investor Relations website, or by clicking the following link: Q2 2025 MRMD Earnings Call.

SECOND QUARTER 2025 OPERATIONAL HIGHLIGHTS

During the second quarter, the Company announced the following development in the implementation of its strategic growth plan:

April 1: Launched its Nature’s Heritage™-branded cannabis flower, pre-rolls, and vapes in Illinois, marking the first time the brand’s premium products are available in the state.

April 3: Expanded the line-up of its top-selling Betty’s Eddies™-branded cannabis chews with the introduction of a new caramel chew, Betty’s Caramelt Away.

April 8: Promoted Ryan Crandall to Chief Commercial Officer to lead the Company’s commercial strategy and activities, including Sales, Marketing, Product Development, and Retail Operations. He had served as the Company’s Chief Revenue Officer since July 2022, and previously was its Chief Products Officer and SVP, Sales for four years.

May 29: Expended its branded product line-up with the introduction of MycroDose by Nature’s Heritage, a vegan pill that combines full-spectrum cannabis with the added benefits of functional mushrooms.

OTHER DEVELOPMENTS

Subsequent to the end of the second quarter, the Company announced the following further developments:

July 14: Expanded the distribution of Betty’s Eddies to Maine for both adult-use cannabis consumers and medical patients through a new licensing partnership.

July 31: Announced a Managed Services Agreement (“MSA”) to assume day-to-day management of a cultivation and processing facility in Pennsylvania owned by a division of multi-state cannabis operator TILT Holdings. In addition, a licensing agreement will enable the Company to distribute its award-winning, branded products in Pennsylvania, which is anticipated to become the next state to expand its legal cannabis program to include adult-use sales.

DISCUSSION OF NON-GAAP FINANCIAL MEASURES

MariMed’s management uses several different financial measures, both GAAP and non-GAAP, in analyzing and assessing the overall performance of its business, making operating decisions, and planning and forecasting future periods. The Company has provided in this release several non-GAAP financial measures: Non-GAAP Adjusted EBITDA and non-GAAP Adjusted EBITDA margin, Non-GAAP Gross margin, Non-GAAP Operating expenses and Non-GAAP Net income (loss), as supplements to Revenue, Gross margin, Operating expenses, Income (loss) from operations, Net income (loss) and other financial measures prepared in accordance with GAAP.

Management believes these non-GAAP financial measures are useful in reviewing and assessing the performance of the Company, and when planning and forecasting future periods, as they provide meaningful operating results by excluding the effects of expenses that are not reflective of its operating business performance. In addition, the Company’s management uses these non-GAAP financial measures to understand and compare operating results across accounting periods and for financial and operational decision-making. The presentation of these non-GAAP measures is not intended to be considered in isolation or as a substitute for the financial information prepared in accordance with GAAP.

Management believes that investors and analysts benefit from considering non-GAAP financial measures in assessing the Company’s financial results and its ongoing business, as it allows for meaningful comparisons and analysis of trends in the business. In particular, non-GAAP adjusted EBITDA is used by many investors and analysts themselves, along with other metrics, to compare financial results across accounting periods and to those of peer companies.

As there are no standardized methods of calculating non-GAAP financial measures, the Company’s calculations may differ from those used by analysts, investors and other companies, even those within the cannabis industry, and therefore may not be directly comparable to similarly titled measures used by others.

Management defines non-GAAP Adjusted EBITDA as income (loss) from operations, determined in accordance with GAAP, excluding the following items:

depreciation and amortization of property and equipment;

amortization of acquired intangible assets;

impairment or write-downs of acquired intangible assets;

inventory revaluation;

stock-based compensation;

severance;

legal settlements; and

acquisition-related and other expenses.

For further information, please refer to the publicly available financial filings available on MariMed’s Investor Relations website, as filed with the U.S. Securities and Exchange Commission, or as filed with the Canadian securities regulatory authorities on the SEDAR website.

ABOUT MARIMED MariMed Inc. is a leading multi-state cannabis operator, known for developing and managing state-of-the-art cultivation, production, and retail facilities. Our award-winning portfolio of cannabis brands, including Betty’s Eddies™, Bubby’s Baked™, Vibations™, InHouse™, and Nature’s Heritage™, sets us apart as an industry leader. These trusted brands, crafted with quality and innovation, are recognized and loved by consumers across the country. With a commitment to excellence, MariMed continues to drive growth and set new standards in the cannabis industry. For additional information, visit www.marimedinc.com.

IMPORTANT CAUTION REGARDING FORWARD-LOOKING STATEMENTS: The information in this release contains “forward-looking” statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995, which are subject to several risks and uncertainties. All statements other than statements of historical facts contained in this release, including without limitation statements regarding projected financial results for 2025, including anticipated openings of dispensaries and facilities, timing of regulatory approvals, plans and objectives of management for future operations, are forward-looking statements. Without limiting the foregoing, the words “anticipates”, “believes”, “estimates”, “expects”, “expectations”, “intends”, “may”, “plans”, and other similar language, whether in the negative or affirmative, are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words.

Forward-looking statements are based on our current beliefs and assumptions regarding our business, timing of regulatory approvals, the ability to obtain new licenses, business prospects and strategic growth plan, and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. Our actual results may differ materially from those contemplated in these forward-looking statements due to various risks, uncertainties, and other important factors, including, among others, reductions in customer spending, our ability to recruit and retain key personnel, and disruptions from the integration efforts of acquired companies.

These factors are not intended to be an all-encompassing list of risks and uncertainties that may affect our business and results of operations. These statements are not a guarantee of future performance and involve risk and uncertainties that are difficult to predict, including, among other factors, changes in demand for the Company’s services and products, changes in the law and its enforcement, and changes in the economic environment. Additional information regarding these and other factors can be found in our reports filed with the U.S. Securities and Exchange Commission. In providing these forward-looking statements, the Company expressly disclaims any obligation to update these statements publicly or otherwise, whether as a result of new information, future events or otherwise, except as required by law.

All trademarks and service marks are the property of their respective owners.

Neither the CSE nor its Regulation Services accepts responsibility for the adequacy or accuracy of this release.

For More Information Contact:

Howard Schacter, Chief Communications Officer Email: hschacter@marimedinc.com Phone: (781) 277-0007

The following news was originally announced in ISG’s second-quarter 2025 results release today:

Acquisition will add to ISG’s client base, geographic footprint and capabilities to serve Italy’s public and private sectors

STAMFORD, Conn. ― Information Services Group (ISG) (Nasdaq: III), a global AI-centered technology research and advisory firm, today announced it has signed a definitive agreement to acquire Martino & Partners, a highly respected strategic advisory firm serving public and private sectors clients in Italy. The transaction is expected to close in early September.

The addition of Milan-based Martino & Partners will expand ISG’s client base, geographic footprint and capabilities in Italy, including AI, in a market with emerging growth potential fueled by European Union-funded technology modernization programs and a focus on AI and cost optimization.

“This acquisition represents a further investment in our European business and expands our addressable market in Italy, where we see an emerging growth opportunity,” said Michael P. Connors, chairman and CEO of ISG. “Martino & Partners brings more than 20 new clients to ISG Italy; expands our public sector reach beyond the central government to serve municipal entities, and gives us a strong presence in northern Italy, where many leading commercial enterprises are located.”

The combined businesses, which will go to market as ISG Italy, will have nearly 40 professionals working out of multiple locations, including Milan and Rome.

“Martino and Partners is the perfect complement to our ISG Italy business,” Connors said. “We have worked together previously on several client engagements, so we are very familiar with the firm, their leadership and their talented professionals. This is a win-win for both firms.”

The acquisition comes at a time of emerging demand for advisory services in Italy, particularly in the public sector, which is seeking strategic advice and support to leverage programs such as the Next Generation EU and Digital Decade initiatives to modernize technology infrastructure and services. Overall interest in AI and cost optimization continues to be high as companies look to use technology to become more efficient and gain competitive advantage in a challenging macro environment.

“Since our founding 10 years ago, Martino & Partners has earned a reputation as one of the leading strategic advisory firms in Italy,” said Andrea Martino, the firm’s co-founder and CEO, who will serve as CEO of ISG Italy. “Our approach is to think big, speak plainly and challenge conventional wisdom. We are excited to be joining forces with ISG, whose global resources and strong domain expertise will make our combined businesses an even more powerful player with stronger growth potential in the Italian marketplace.”

In addition to Martino, ISG Italy’s senior management team will include Claudia De Roma, Martino & Partners co-founder, who will lead the ISG Italy public administration segment.

ISG (Nasdaq: III) is a global AI-centered technology research and advisory firm. A trusted partner to more than 900 clients, including 75 of the world’s top 100 enterprises, ISG is a long-time leader in technology and business services that is now at the forefront of leveraging AI to help organizations achieve operational excellence and faster growth. The firm, founded in 2006, is known for its proprietary market data, in-depth knowledge of provider ecosystems, and the expertise of its 1,600 professionals worldwide working together to help clients maximize the value of their technology investments.

Reports second-quarter GAAP revenues of $62 million, exceeding guidance and up 7% versus prior year, excluding results from divested automation unit

Reports second-quarter GAAP net income of $2.2 million, GAAP EPS of $0.04 and adjusted EPS of $0.08

Reports second-quarter adjusted EBITDA of $8.3 million, up 17% versus prior year

Generates $12 million in cash from operations, up from $2.2 million in prior year

Agrees to acquire Martino & Partners, a strategic advisory firm serving clients in Italy

Declares third-quarter dividend of $0.045 per share, payable September 26, 2025, to shareholders of record as of September 5, 2025

Sets third-quarter guidance: revenues between $60.5 million and $61.5 million and adjusted EBITDA between $7.5 million and $8.5 million

STAMFORD, Conn.–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III), a global AI-centered technology research and advisory firm, today announced financial results for the second quarter ended June 30, 2025.

“ISG delivered an excellent second quarter, underscoring our momentum as an AI-centered firm with strong, trusted client relationships,” said Michael P. Connors, chairman and CEO. “Excluding our divested automation unit, Q2 revenues were up 7 percent, led by our surging Americas business, up 16 percent. Our adjusted EBITDA was up 17 percent, with our adjusted EBITDA margin up more than 200 basis points. And we achieved strong operating cash flow of $12 million, one of our best quarters ever for cash generation.

“For the first half of 2025, adjusted EBITDA was nearly $16 million, up 36 percent from the prior year, and our adjusted EBITDA margin was up nearly 400 basis points, reflecting our improved global business mix and strong execution of our business strategy.”

Connors said ISG is well positioned to compete in a business environment where uncertainty “has become the norm.”

“Enterprises remain cautious about tech spending in general but continue to leverage technology for cost optimization while moving forward aggressively to modernize their infrastructure as they prepare for broad adoption of AI,” Connors said. “These trends are right in ISG’s sweet spot. Our AI-centered positioning, investment in expanded AI capabilities and long-term focus on operational excellence continue to resonate with our client base. We are well positioned for success.”

ISG Agrees to Acquire Martino & Partners

ISG has signed a definitive agreement to acquire Martino & Partners, a highly respected strategic advisory firm serving public and private sectors clients in Italy. The transaction is expected to close in early September.

The addition of Milan-based Martino & Partners will expand ISG’s client base, geographic footprint and capabilities in Italy, including AI, in a market with emerging growth potential fueled by European Union-funded technology modernization programs and a focus on AI and cost optimization.

“This acquisition represents a further investment in our European business and expands our addressable market in Italy, where we see an emerging growth opportunity,” said Connors. “Martino & Partners brings more than 20 new clients to ISG Italy; expands our public sector reach beyond the central government to serve municipal entities, and gives us a strong presence in northern Italy, where many leading commercial enterprises are located.”

Second-Quarter 2025 Results

Reported revenues for the second quarter were $61.6 million, down 4 percent from $64.3 million in the prior year. Excluding second-quarter 2024 results from ISG’s automation unit, which the firm divested on October 1, 2024, revenues were up 7 percent. Currency translation positively impacted reported revenues by $0.8 million versus the prior year.

Excluding second-quarter 2024 automation results, revenues were $39.5 million in the Americas, up 16 percent versus the prior year, and down 1 percent on a reported basis. Revenues in Europe were $16.6 million, down 7 percent, excluding automation results, and down 12 percent on a reported basis, and Asia Pacific revenues were $5.4 million, down 1 percent on a reported basis, all versus the prior year.

ISG reported second-quarter operating income of $4.7 million, compared with operating income of $3.7 million in the prior year. Reported second-quarter net income was $2.2 million, compared with net income of $2.0 million in the prior year. Fully diluted income per share was $0.04, compared with income per fully diluted share of $0.04 in the prior year.

Adjusted net income (a non-GAAP measure defined below under “Non-GAAP Financial Measures”) for the second quarter was $4.1 million, or $0.08 per share on a fully diluted basis, compared with adjusted net income of $3.8 million, or $0.08 per share on a fully diluted basis, in the prior year’s second quarter.

Second-quarter adjusted EBITDA (a non-GAAP measure defined below under “Non-GAAP Financial Measures”) was $8.3 million, up 17 percent from the prior year. Adjusted EBITDA margin (a non-GAAP measure calculated by dividing adjusted EBITDA by reported revenues) was 13.5 percent, up 241 basis points from 11.1 percent in the prior year.

Other Financial and Operating Highlights

ISG generated $11.9 million of cash from operations in the second quarter, compared with generating $2.2 million of cash in the second quarter last year. The firm’s cash balance totaled $25.2 million at June 30, 2025, up 25 percent from $20.1 million at March 31, 2025.

During the second quarter, ISG paid dividends of $2.4 million and repurchased $4.0 million of shares.

2025 Third-Quarter Revenue and Adjusted EBITDA Guidance

“ISG is well positioned for continuing success, with a mix of cost optimization, research and digital transformation platforms and services focused on AI that meet the needs of the market,” Connors said. “For the third quarter, ISG is targeting revenues of between $60.5 million and $61.5 million and adjusted EBITDA of between $7.5 million and $8.5 million. We will continue to monitor the macro environment, including the impact of tariffs, FX, inflation and other factors, and adjust our business plans accordingly.”

Quarterly Dividend

The ISG Board of Directors declared a third-quarter dividend of $0.045 per share, payable on September 26, 2025, to shareholders of record as of September 5, 2025.

Conference Call

ISG has scheduled a call for 9 a.m., U.S. Eastern Time, August 7, 2025, to discuss the company’s second-quarter results. The call can be accessed by dialing +1 (800) 715-9871; or, for international callers, by dialing +1 (646) 307-1963. The access code is 9414856. A recording of the conference call will be accessible on ISG’s investor relations page for approximately four weeks following the call.

Forward-Looking Statements

This communication contains “forward-looking statements” which represent the current expectations and beliefs of management of ISG concerning future events and their potential effects. Statements contained herein including words such as “anticipate,” “believe,” “contemplate,” “plan,” “estimate,” “target,” “expect,” “intend,” “will,” “continue,” “should,” “may,” and other similar expressions, are “forward-looking statements” under the Private Securities Litigation Reform Act of 1995. These forward-looking statements are not guarantees of future results and are subject to certain risks and uncertainties that could cause actual results to differ materially from those anticipated. Those risks relate to inherent business, economic and competitive uncertainties and contingencies relating to the businesses of ISG and its subsidiaries including without limitation: (1) failure to secure new engagements or loss of important clients; (2) ability to hire and retain enough qualified employees to support operations; (3) ability to maintain or increase billing and utilization rates; (4) management of growth; (5) success of expansion internationally; (6) competition; (7) ability to move the product mix into higher margin businesses; (8) general political and social conditions such as war, political unrest and terrorism; (9) healthcare and benefit cost management; (10) ability to protect ISG and its subsidiaries’ intellectual property or data and the intellectual property or data of others; (11) currency fluctuations and exchange rate adjustments; (12) ability to successfully consummate or integrate strategic acquisitions; (13) outbreaks of diseases, including coronavirus, or similar public health threats or fear of such an event; (14) engagements may be terminated, delayed or reduced in scope by clients; (15) the effect of the divestiture of the automation unit on ISG’s relationships with its customers and suppliers and on its retained business generally; (16) the success of ISG’s focus on AI advisory and AI-powered platforms; (17) changes to trade policy, and (18) potential employment-related claims. Certain of these and other applicable risks, cautionary statements and factors that could cause actual results to differ from ISG’s forward-looking statements are included in ISG’s filings with the U.S. Securities and Exchange Commission. ISG undertakes no obligation to update or revise any forward-looking statements to reflect subsequent events or circumstances.

Non-GAAP Financial Measures

ISG reports all financial information required in accordance with U.S. generally accepted accounting principles (GAAP). In this release, ISG has presented both GAAP financial results as well as non-GAAP information for the three and six months ended June 30, 2025, and June 30, 2024. ISG believes that evaluating its ongoing operating results will be enhanced if it discloses certain non-GAAP information. These non-GAAP financial measures exclude non-cash and certain other special charges that many investors believe may obscure the user’s overall understanding of ISG’s current financial performance and the Company’s prospects for the future. ISG believes that these non-GAAP measures provide useful information to investors because they improve the comparability of the financial results between periods and provide for greater transparency of key measures used to evaluate the Company’s performance.

ISG provides adjusted EBITDA (defined as net income, plus interest, taxes, depreciation and amortization, foreign currency transaction gains/losses, non-cash stock compensation, interest accretion associated with contingent consideration, acquisition- and disposition-related costs, and severance, integration and other expense), adjusted net income (defined as net income, plus amortization of intangible assets, non-cash stock compensation, foreign currency transaction gains/losses, interest accretion associated with contingent consideration, acquisition- and disposition-related costs and severance, integration and other expense on a tax-adjusted basis), adjusted net income per diluted share, adjusted EBITDA margin, and selected financial data on a constant currency basis which are non-GAAP measures that the Company believes provide useful information to both management and investors by excluding certain expenses and financial implications of foreign currency translations, which management believes are not indicative of ISG’s core operations. These non-GAAP measures are used by ISG to evaluate the Company’s business strategies and management’s performance.

We evaluate our results of operations on both an as reported and a constant currency basis. The constant currency presentation, which is a non-GAAP financial measure, excludes the impact of year-over-year fluctuations in foreign currency exchange rates. We believe providing constant currency information provides valuable supplemental information regarding our results of operations, thereby facilitating period-to-period comparisons of our business performance and is consistent with how management evaluates the Company’s performance. We calculate constant currency percentages by converting our current and prior-periods local currency financial results using the same point in time exchange rates and then compare the adjusted current and prior period results. This calculation may differ from similarly titled measures used by others and, accordingly, the constant currency presentation is not meant to be a substitution for recorded amounts presented in conformity with GAAP, nor should such amounts be considered in isolation.

Management believes this information facilitates comparison of underlying results over time. Non-GAAP financial measures, when presented, are reconciled to the most closely applicable GAAP measure. Non-GAAP measures are provided as additional information and should not be considered in isolation or as a substitute for results prepared in accordance with GAAP. A reconciliation of the forward-looking non-GAAP estimates contained herein to the corresponding GAAP measures is not being provided, due to the unreasonable efforts required to prepare it.

About ISG

ISG (Nasdaq: III) is a global AI-centered technology research and advisory firm. A trusted partner to more than 900 clients, including 75 of the world’s top 100 enterprises, ISG is a long-time leader in technology and business services that is now at the forefront of leveraging AI to help organizations achieve operational excellence and faster growth. The firm, founded in 2006, is known for its proprietary market data, in-depth knowledge of provider ecosystems, and the expertise of its 1,600 professionals worldwide working together to help clients maximize the value of their technology investments.

Raises 2025 Full Year Guidance Increasing Demand Drives Strong Financial Performance

BRENTWOOD, Tenn., Aug. 06, 2025 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (CoreCivic or the Company) announced today its second quarter 2025 financial results.

Financial Highlights – Second Quarter 2025

Total revenue of $538.2 million, up 9.8% from the prior year quarter

Net income of $38.5 million, up 103.4% from the prior year quarter

Diluted earnings per share of $0.35, up 105.9% from the prior year quarter

Adjusted diluted earnings per share of $0.36, up 80.0% from the prior year quarter

Normalized FFO per diluted share of $0.59, up 40.5% from the prior year quarter

Adjusted EBITDA of $103.3 million, up 23.2% from the prior year quarter

Repurchased 2.0 million shares of our common stock at an aggregate cost of $43.2 million

Damon T. Hininger, CoreCivic’s Chief Executive Officer, commented, “Increasing demand for the solutions we provide, particularly from U.S. Immigration and Customs Enforcement (ICE), contributed to a strong second quarter, as nationwide detention populations under ICE custody reached an all-time high. We expect the substantial increase in government funding approved during July to result in further increases in the utilization of our existing capacity. Based on the strength of our second quarter financial results and outlook for our business during the second half of 2025, we are increasing our 2025 financial guidance.”

Hininger continued, “We continued to deploy capital in ways that we believe add shareholder value. During the second quarter, we repurchased 2.0 million shares of our common stock at an aggregate cost of $43.2 million. At the beginning of the third quarter, we completed the acquisition of the Farmville Detention Center in Virginia for $67 million at an attractive return.”

Patrick Swindle, CoreCivic’s President and Chief Operating Officer, remarked, “We made substantial progress in re-activating three previously idled facilities during the second quarter, and our activation teams are preparing for additional contracting activity. ICE has been deliberate in increasing detention utilization under existing contracts while also executing new contracts at previously idled facilities. We expect to begin receiving detainees at our California City Immigration Processing Center in the near term, we are in advanced negotiations to activate a fourth idle facility, and we continue discussions to activate additional idle facilities. During the third quarter we also began integrating operations at the Farmville Detention Center, where we provide transportation, care, and civil detention services to adult male noncitizens under ICE custody. Along with the acquisition of the facility, we welcomed approximately 200 employees to our team.”

Second Quarter 2025 Financial Results Compared With Second Quarter 2024

Net income in the second quarter of 2025 was $38.5 million, or $0.35 per diluted share, compared with net income in the second quarter of 2024 of $19.0 million, or $0.17 per diluted share (Diluted EPS). Adjusted for special items, Adjusted Net Income for the second quarter of 2025 was $39.7 million, or $0.36 per diluted share (Adjusted Diluted EPS), compared with Adjusted Net Income of $21.8 million, or $0.20 per diluted share, in the prior year quarter. Special items in the second quarter of 2025 included charges of $1.5 million associated with the acquisition of the Farmville Detention Center, included in general and administrative expenses in our consolidated statement of operations. Special items in the prior year quarter included $4.1 million of expenses associated with debt repayments and refinancing transactions. Special items are presented in detail in the calculation of Adjusted Net Income and Adjusted Diluted EPS in the Supplemental Financial Information following the financial statements presented herein.

The increase in Diluted EPS and Adjusted Diluted EPS compared with the prior year quarter resulted from higher federal and state populations as well as higher average per diem rates across much of our portfolio, combined with the recognition of employee retention credits (ERCs) available under the Coronavirus Aid, Relief and Economic Security Act amounting to $0.08 per share. These increases were net of the financial impact of the termination of our contract with ICE at the Dilley Immigration Processing Center effective August 9, 2024. However, we began re-activating the Dilley facility during March 2025. The agreement governing the reactivation provides for a fixed monthly payment from ICE in accordance with a graduated schedule to correlate with the activation of each neighborhood within the facility. The Dilley facility accounted for a $0.07 per share reduction compared with the second quarter of 2024.

We cared for an average daily residential population of 54,026 during the second quarter of 2025 in our Safety and Community segments compared with 51,541 during the second quarter of 2024. Average occupancy during the second quarter of 2025 was 76.8% in our Safety and Community segments, compared with 74.3% during the second quarter of 2024, even after reflecting the activation and transfer of our 2,560-bed California City Immigration Processing Center from the Properties segment to the Safety segment effective April 1, 2025, when we entered into a Letter Contract with ICE to reactive operations at the facility. The California City facility was previously in our Properties segment because it was leased to the California Department of Corrections and Rehabilitation until the lease expired March 31, 2024. We expect to begin receiving detainees from ICE at the California City facility in the near term under terms of the Letter Contract.

During the second quarter of 2025, revenue from ICE, our largest government partner, was $176.9 million compared to $151.0 million during the second quarter of 2024, an increase of 17.2%, including the termination of our ICE contract at the Dilley facility effective August 9, 2024, partially offset by its reactivation effective April 1, 2025. The termination and reactivation accounted for a net reduction in revenue of $12.8 million. Revenue from state customers increased 5.2% compared with the prior year quarter, with increases across many of our government customers. New contracts with the state of Montana executed in August 2024 and January 2025 accounted for the largest increase in revenue from state customers. Further, revenue from the U.S. Marshals Service, our second largest government customer, increased 2.7% from the prior year quarter.

Earnings before interest, taxes, depreciation and amortization (EBITDA) for the second quarter of 2025 was $101.8 million, compared with $79.8 million in the second quarter of 2024. Adjusted EBITDA, which excludes special items, was $103.3 million in the second quarter of 2025, compared with $83.9 million in the second quarter of 2024. The increases in EBITDA and Adjusted EBITDA from the prior year quarter were primarily attributable to higher residential populations in our portfolio, net of reductions for the contract termination at the Dilley facility and the expiration of the lease with the CDCR at the California City facility. The increases in EBITDA and Adjusted EBITDA also included $8.3 million of ERCs recognized during the second quarter of 2025, and $3.2 million of interest collected on the ERCs.

Funds From Operations (FFO) for the second quarter of 2025 was $63.5 million, or $0.58 per share, compared with $43.8 million, or $0.39 per share, in the second quarter of 2024. Normalized FFO, which excludes special items, was $64.6 million, or $0.59 per diluted share, in the second quarter of 2025, compared with $46.6 million, or $0.42 per share, in the second quarter of 2024. Normalized FFO was impacted by the same factors that affected Adjusted EBITDA, further improved by a reduction in gross interest expense that is not reflected in Adjusted EBITDA. The reduction in gross interest expense resulted from a decrease in our average outstanding debt balance combined with a decrease in the interest rates associated with our variable rate debt. Per share amounts were also favorably impacted by a 2.1% reduction in weighted average shares outstanding compared with the prior year quarter resulting from repurchases we made under our share repurchase program.

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share amounts, are measures calculated and presented on the basis of methodologies other than in accordance with generally accepted accounting principles (GAAP). Please refer to the Supplemental Financial Information and the note following the financial statements herein for further discussion and reconciliations of these measures to net income, the most directly comparable GAAP measure.

Capital Strategy

Share Repurchases. Our Board of Directors (BOD) previously approved a share repurchase program authorizing the Company to repurchase up to $350.0 million of our common stock. On May 15, 2025, the BOD authorized an increase to the share repurchase program by which we may purchase up to an additional $150.0 million in shares of our outstanding common stock, increasing the total aggregate authorization to up to $500.0 million. During the six months ended June 30, 2025, we repurchased 3.9 million shares of common stock under the share repurchase program at an aggregate cost of $81.0 million, or $20.52 per share, excluding costs associated with the share repurchase program, including 2.0 million shares at an aggregate cost of $43.2 million during the second quarter of 2025. Since the share repurchase program was authorized in May 2022, through June 30, 2025, we have repurchased a total of 18.5 million shares of our common stock at an aggregate cost of $262.1 million, or $14.19 per share, excluding fees, commissions and other costs related to the repurchases.

As of June 30, 2025, we had $237.9 million of repurchase authorization available under the share repurchase program. Additional repurchases of common stock will be made in accordance with applicable securities laws and may be made at management’s discretion within parameters set by the BOD from time to time in the open market, through privately negotiated transactions, or otherwise. The share repurchase program has no time limit and does not obligate us to purchase any particular amount of our common stock. The authorization for the share repurchase program may be terminated, suspended, increased or decreased by our BOD in its discretion at any time.

Acquisition of Farmville Detention Center. On July 1, 2025, we completed the acquisition of the Farmville Detention Center, a 736-bed facility constructed in 2010 and located in Farmville, Virginia. The transaction was consummated through the acquisition of 100% of the membership interests in entities that own and operate the facility, as well as the acquisition of certain assets utilized in the operation of the business. Farmville Detention Center provides transportation, care, and civil detention services to adult male noncitizens through an Intergovernmental Service Agreement (IGSA) between Prince Edward County, Virginia and ICE, which expires in March 2029. The total purchase price, amounting to $67.0 million, was funded with cash on hand and borrowing capacity under our revolving bank credit facility. We expect annual incremental revenue of approximately $40.0 million resulting from this acquisition.

Business Development Updates

Activation of the Dilley Immigration Processing Center. On March 5, 2025, we announced that we had agreed under an amendment to an IGSA to resume operations and care for up to 2,400 individuals at the 2,400-bed Dilley Immigration Processing Center in Dilley, Texas. We began receiving residents at this facility during the second quarter of 2025. By the end of the second quarter of 2025, three of the five neighborhoods at the facility were operational. We currently expect all five neighborhoods at the facility to be fully operational on schedule by the end of the third quarter of 2025, when we expect to generate the full fixed monthly payment for the facility.

Intake Process Expected to Begin at the California City Immigration Processing Center. Effective April 1, 2025, we entered into a Letter Contract with ICE to begin activation efforts at our 2,560-bed California City Immigration Processing Center. The Letter Contract authorizes initial funding up to $10.0 million with maximum funding up to $31.2 million for a six-month period to help cover our start-up expenses while we work to negotiate and execute a long-term contract. We expect to begin receiving detainees from ICE at the California City facility in the near term under terms of the Letter Contract.

Midwest Regional Reception Center. Effective March 7, 2025, we entered into a Letter Contract with ICE to begin activation efforts at our 1,033-bed Midwest Regional Reception Center. The Letter Contract authorizes initial funding up to $5.0 million with maximum funding up to $22.6 million for a six-month period to help cover our start-up expenses while we work to negotiate and execute a long-term contract. The intake process has been delayed by a lawsuit filed by the City of Leavenworth alleging that a Special Use Permit (SUP) is required to operate the facility. A state court granted a temporary restraining order barring us from housing detainees at the facility without first obtaining an SUP. We have filed an appeal in the state court on the basis that the SUP is not applicable under existing statute. We believe ICE remains intent on using this facility.

2025 Financial Guidance

Based on current business conditions, we are providing the following updated financial guidance for the full year 2025:

Revised Guidance Full Year 2025

Prior Guidance Full Year 2025

Net income

$116.4 million to $124.4 million

$91.3 million to $101.3 million

Adjusted Net Income

$115.5 million to $123.5 million

$91.3 million to $101.3 million

Diluted EPS

$1.08 to $1.15

$0.83 to $0.92

Adjusted Diluted EPS

$1.07 to $1.14

$0.83 to $0.92

FFO per diluted share

$1.98 to $2.06

$1.72 to $1.82

Normalized FFO per diluted share

$1.99 to $2.07

$1.72 to $1.82

EBITDA

$366.3 million to $372.3 million

$331.0 million to $339.0 million

Adjusted EBITDA

$365.0 million to $371.0 million

$331.0 million to $339.0 million

Compared with our prior 2025 annual guidance provided on May 7, 2025, our revised 2025 guidance reflects the favorable results for the second quarter, updated occupancy projections consistent with current trends, the acquisition of the Farmville Detention Center, as well as our assumptions for the reactivation of the California City Immigration Processing Center based on the expectation of receiving detainee populations during the third quarter of 2025.

Consistent with our past practice, our guidance does not include the impact of any new contract awards not previously announced. However, we may continue to execute new contracts during the balance of 2025, and may revise guidance throughout the year if and when new contracts are signed. Although we can provide no assurance, based on significant funding levels for detention capacity that will be available under the One Big Beautiful Bill Act, modified immigration policies of the current administration, as well as newly enacted legislation pertaining to illegal immigrants requiring the utilization of detention for certain criminal violations, we expect new contracts to require the activation of more of our idle facilities. The activation of an idle facility generally requires four to six months to hire, train, and prepare the facility to accept residential populations, which, depending on contract structure, could result in additional expenses before we are able to realize additional revenue. To the extent any new contract requires the activation of an idle facility before we begin to recognize revenue, our guidance could be negatively impacted by start-up expenses until the revenue we generate offsets these expenses. Due to activation timing, full year benefits from idle facility activations are likely to be more impactful to 2026 results.

During 2025, we expect to invest $29.0 million to $31.0 million in maintenance capital expenditures on real estate assets, $31.0 million to $34.0 million for maintenance capital expenditures on other assets and information technology, and $9.0 million to $10.0 million for other capital investments. Although our guidance does not include any new contract awards beyond those previously announced, we also expect to incur approximately $70.0 million to $75.0 million of capital expenditures associated with previously idled facilities we are activating and for additional potential facility activations, in order to prepare these facilities to quickly accept residential populations if opportunities arise, as well as to provide transportation services.

Supplemental Financial Information and Investor Presentations

We have made available on our website supplemental financial information and other data for the second quarter of 2025. Interested parties may access this information at http://ir.corecivic.com/ under “Financial Information” of the Investors section. We do not undertake any obligation and disclaim any duties to update any information disclosed in this report.

Management may meet with investors from time to time during the third quarter of 2025. Written materials used in the investor presentations will also be available on our website beginning on or about August 29, 2025. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Events & Presentations” of the Investors section.

Conference Call, Webcast and Replay Information

We will host a webcast conference call at 10:00 a.m. central time (11:00 a.m. eastern time) on Thursday, August 7, 2025, which will be accessible through the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page. To participate via telephone and join the call live, please register in advance here https://register-conf.media-server.com/register/BI826b7187965c436ca353a3af4a956fed. Upon registration, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest operators of such facilities in the United States. We have been a flexible and dependable partner for government for more than 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements

This press release contains statements as to our beliefs and expectations of the outcome of future events that are “forward-looking” statements as defined within the meaning of the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. These include, but are not limited to, the risks and uncertainties associated with: (i) changes in government policy, legislation and regulations that affect utilization of the private sector for corrections, detention, and residential reentry services, in general, or our business, in particular, including, but not limited to, the continued utilization of our correctional and detention facilities by the federal government as a consequence of presidential executive orders, and the impact of any changes to immigration reform and sentencing laws (we do not, under longstanding policy, lobby for or against policies or legislation that would determine the basis for, or duration of, an individual’s incarceration or detention); (ii) our ability to obtain and maintain correctional, detention, and residential reentry facility management contracts because of reasons including, but not limited to, sufficient governmental appropriations, contract compliance, negative publicity and effects of inmate disturbances; (iii) changes in the privatization of the corrections and detention industry, the acceptance of our services, the timing of the opening of new facilities and the commencement of new management contracts (including the extent and pace at which new contracts are utilized), as well as our ability to utilize available beds; (iv) our ability to activate idle facilities in a timely manner in order to meet the expected growth in demand for our facilities and services from the federal government that may occur as a result of changes in policies and actions of the current presidential administration, and to realize projected returns resulting therefrom; (v) general economic and market conditions, including, but not limited to, the impact governmental budgets can have on our contract renewals and renegotiations, per diem rates, and occupancy; (vi) fluctuations in our operating results because of, among other things, changes in occupancy levels; competition; contract renegotiations or terminations; inflation and other increases in costs of operations, including a rise in labor costs; fluctuations in interest rates and risks of operations; (vii) government budget uncertainty, the impact of the debt ceiling and the potential for government shutdowns and changing budget priorities; (viii) our ability to successfully identify and consummate future development and acquisition opportunities and realize projected returns resulting therefrom; and (ix) the availability of debt and equity financing on terms that are favorable to us, or at all. Other factors that could cause operating and financial results to differ are described in the filings we make from time to time with the Securities and Exchange Commission.