MALVERN, Pa., July 29, 2024 (GLOBE NEWSWIRE) — Ocugen, Inc. (Ocugen or the Company) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines, today announced that it will host a conference call and live webcast to discuss the Company’s second quarter 2024 financial results and provide a business update at 8:30 a.m. ET on Thursday, August 8, 2024.

Ocugen will issue a pre-market earnings announcement on the same day. Attendees are invited to participate on the call using the following details:

Dial-in Numbers: (800) 715-9871 for U.S. callers and (646) 307-1963 for international callers Conference ID: 7453742 Webcast: Available on the events section of the Ocugen investor site

A replay of the call and archived webcast will be available for approximately 45 days following the event on the Ocugen investor site.

About Ocugen, Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patient’s lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on X and LinkedIn.

Cautionary Note on Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, including, but not limited to, statements regarding qualitative assessments of available data, potential benefits, expectations for ongoing clinical trials, anticipated regulatory filings and anticipated development timelines, which are subject to risks and uncertainties. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations. These and other risks and uncertainties are more fully described in our periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.

Second quarter 2024 total revenue of $593.4 million, net income of $100.2 million, and EBITDA of $177.7 million

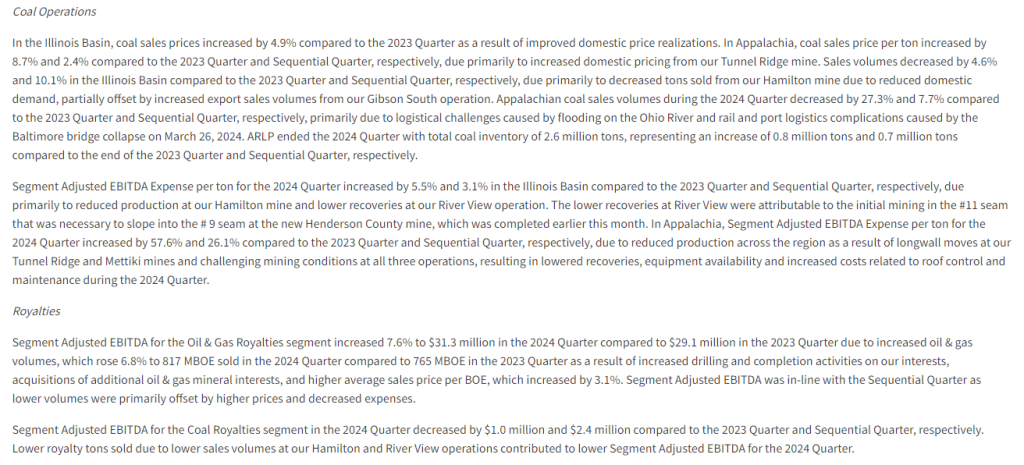

Coal sales price realizations of $65.30 per ton sold, up 3.8% year-over-year

Increased oil & gas royalty volumes to 817 MBOE, up 6.8% year-over-year

In June 2024, issued $400 million in 8.625% Senior Notes due 2029 and redeemed outstanding balance of Senior Notes due 2025

Extended revolving credit facility maturity to March 2028

Enhanced liquidity position to $666.0 million, which included $203.7 million in cash and $462.3 million of borrowings available under credit facilities

In July 2024, declared quarterly cash distribution of $0.70 per unit, or $2.80 per unit annualized

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported financial and operating results for the three and six months ended June 30, 2024 (the “2024 Quarter” and “2024 Period,” respectively). This release includes comparisons of results to the three and six months ended June 30, 2023 (the “2023 Quarter” and “2023 Period,” respectively) and to the quarter ended March 31, 2024 (the “Sequential Quarter”). All references in the text of this release to “net income” refer to “net income attributable to ARLP.” For a definition of EBITDA and related reconciliation to its comparable GAAP financial measure, please see the end of this release.

Total revenues in the 2024 Quarter decreased 7.6% to $593.4 million compared to $641.8 million for the 2023 Quarter primarily as a result of reduced coal sales volumes, which declined 11.8% primarily due to transportation delays, partially offset by increased coal sales price realizations, which rose 3.8% to $65.30 per ton sold in the 2024 Quarter compared to $62.93 per ton sold in the 2023 Quarter. Net income for the 2024 Quarter was $100.2 million, or $0.77 per basic and diluted limited partner unit, compared to $169.8 million, or $1.30 per basic and diluted limited partner unit, for the 2023 Quarter as a result of lower revenues and increased total operating expenses. EBITDA for the 2024 Quarter was $177.7 million compared to $249.2 million in the 2023 Quarter.

Compared to the Sequential Quarter, total revenues in the 2024 Quarter decreased 9.0% primarily as a result of lower tons sold. Lower revenues and a $3.7 million reduction in the fair value of our digital assets, partially offset by reduced operating expenses, reduced net income and EBITDA by 36.6% and 24.4%, respectively, compared to the Sequential Quarter.

Total revenues decreased 4.6% to $1.25 billion for the 2024 Period compared to $1.30 billion for the 2023 Period primarily due to lower coal sales, partially offset by higher oil & gas royalties and other revenues. Net income for the 2024 Period was $258.2 million, or $1.98 per basic and diluted limited partner unit, compared to $361.0 million, or $2.75 per basic and diluted limited partner unit, for the 2023 Period as a result of lower revenues and increased total operating expenses. EBITDA for the 2024 Period was $412.7 million compared to $520.1 million in the 2023 Period.

CEO Commentary

“During the 2024 Quarter we enhanced our liquidity position,” highlighted Joseph W. Craft III, Chairman, President, and Chief Executive Officer. “The successful completion of our Senior Notes offering further strengthened our balance sheet and represents a vote of confidence from the capital markets for our business strategy and plans for execution. As we have said time and again, reliable, affordable, baseload energy is a cornerstone of our nation’s economy, and our strong financial position means we are well-positioned to provide strategic energy supply from our well-capitalized and strategically located coal mines and growing minerals acreage portfolio for many years to come.”

“Coal sales volumes during the 2024 Quarter were impacted by flooding on the Ohio River delaying barge deliveries. Rail and port logistics were disrupted by the Baltimore bridge incident, which as time progressed impacted shipments from our Appalachia rail operations. These delays, combined with lower export sales, lifted our inventories higher by 0.8 million tons compared to the Sequential Quarter,” commented Mr. Craft. “Our well-contracted order book continued to provide stability for our business, delivering improvements in coal sales pricing per ton compared to both the 2023 Quarter and the Sequential Quarter. Additionally, our Oil & Gas Royalties segment reported a 6.8% increase in BOE volumes year-over-year during the 2024 Quarter as our Permian-weighted minerals portfolio continues to realize production growth from recently drilled and completed wells.”

Balance Sheet and Liquidity

As of June 30, 2024, total debt and finance leases outstanding were $503.9 million, including $400 million in newly issued Senior Notes due 2029. The Partnership’s total and net leverage ratios were 0.61 times and 0.36 times debt to trailing twelve months Adjusted EBITDA, respectively, as of June 30, 2024. ARLP ended the 2024 Quarter with total liquidity of $666.0 million, which included $203.7 million of cash and cash equivalents and $462.3 million of borrowings available under its revolving credit and accounts receivable securitization facilities.

During the 2024 Quarter, the Partnership issued $400 million in 8.625% Senior Notes due 2029 and redeemed the outstanding balance of $284.6 million in ARLP’s 7.5% Senior Notes due 2025. The Partnership also amended its revolving credit facility to extend the maturity date to March 9, 2028.

Distributions

On July 26, 2024, we announced that the Board of Directors of ARLP’s general partner (the “Board”) approved a cash distribution to unitholders for the 2024 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on August 14, 2024, to all unitholders of record as of the close of trading on August 7, 2024. The announced distribution is consistent with the cash distributions for the 2023 Quarter and Sequential Quarter.

Outlook

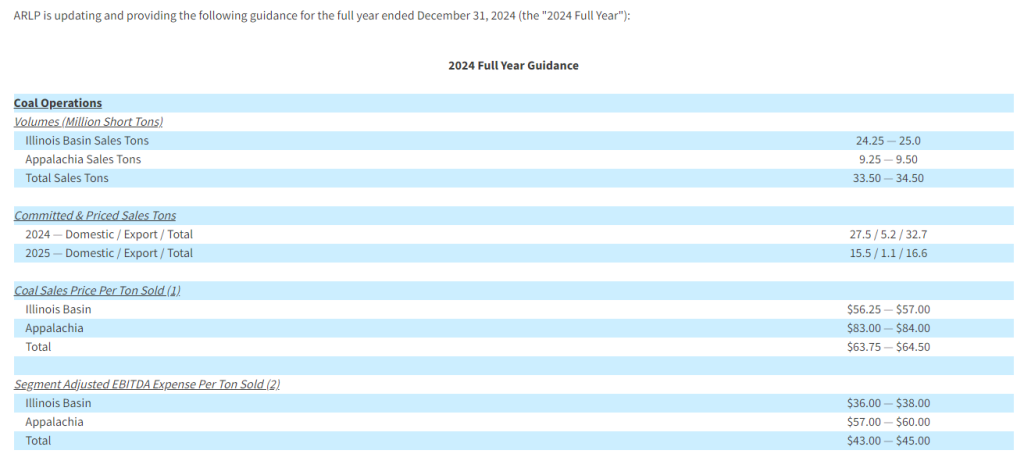

“For the first half of 2024, utility coal burn has been essentially flat with 2023,” commented Mr. Craft. “Since the start of this summer, cooling demand has been strong across many parts of the country driven by recent record-breaking temperatures and accelerating coal-based power generation. This is encouraging considering the very mild 2024 winter and persistently low natural gas prices. At the same time, while demand is holding up, U.S. thermal coal production has slowed significantly (Eastern U.S. production down 11% year-over-year) as utilities are relying on consuming coal from their elevated inventories to meet this demand. Weather forecasts suggest this heat wave will continue through August and an industry publication is projecting demand will exceed supply by close to 20 million tons in the second half of 2024.”

“Turning to the export markets, net back pricing for high sulfur Illinois Basin coal has declined to a level that we have decided it is prudent to slow down production for the back half of the year. Therefore, we are adjusting 2024 full-year guidance for our coal operations. At the midpoint, we now expect to sell approximately 34.0 million tons in 2024, or 2.6% below the mid-point of our original guidance for the year. Due to the increased summer burn, we now expect more than half of our uncontracted tonnage position will be sold in the domestic market.”

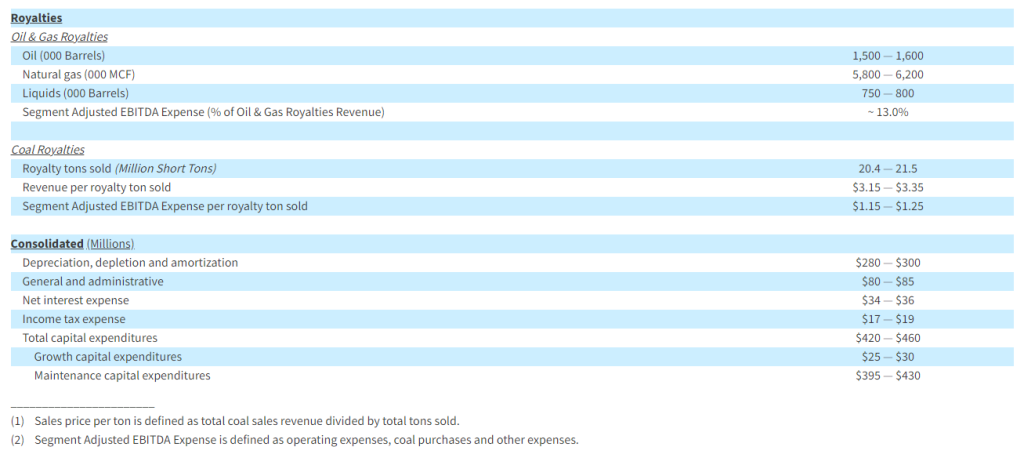

Mr. Craft continued, “Looking at our Oil & Gas Royalties platform, year-to-date performance and continued strong activity across our Permian Basin acreage has set the tone for another robust year. As a result, we are pleased to increase volumetric guidance across all three commodity streams within our Oil & Gas Royalties segment.”

Mr. Craft concluded, “The increase in coal-fired generation and inventory drawdown is constructive for the U.S. thermal coal market and for ARLP as we look forward to next year and beyond. We remain confident in the core fundamentals expected to drive rapid growth in electricity demand for many years to come, including the increasing power requirements stemming from AI, data centers, and the onshoring of U.S. manufacturing.”

Conference Call

A conference call regarding ARLP’s 2024 Quarter financial results is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com .

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13747640.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com . For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com .

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial performance, coal and oil & gas consumption and expected future prices, our ability to increase unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, infrastructure projects at our existing properties, growth in domestic electricity demand, preserving liquidity and maintaining financial flexibility, and our future repurchases of units and senior notes, among others. These risks to our ability to achieve these outcomes include, but are not limited to, the following: decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion, the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels and the planned retirement of coal-fired power plants in the U.S.; our ability to provide fuel for growth in domestic energy demand, should it materialize; changes in macroeconomic and market conditions and market volatility, and the impact of such changes and volatility on our financial position; changes in global economic and geo-political conditions or changes in industries in which our customers operate; changes in commodity prices, demand and availability which could affect our operating results and cash flows; the outcome or escalation of current hostilities in Ukraine and the Israel-Gaza conflict; the severity, magnitude and duration of any future pandemics and impacts of such pandemics and of businesses’ and governments’ responses to such pandemics on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers and operators, available liquidity and capital sources and broader economic disruptions; actions of the major oil-producing countries with respect to oil production volumes and prices could have direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by the operators of the properties in which we hold oil & gas mineral interests due to low commodity prices or the lack of downstream demand or storage capacity; risks associated with the expansion of and investments into the infrastructure of our operations and properties; our ability to identify and complete acquisitions and to successfully integrate such acquisitions into our business and achieve the anticipated benefits therefrom; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, Matrix Design Group, LLC, and our investments in emerging infrastructure and technology companies; dependence on significant customer contracts, including renewing existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws, central bank policy actions including interest rates, bank failures and associated liquidity risks; the effects of and changes in taxes or tariffs and other trade measures adopted by the United States and foreign governments; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, such as the Environmental Protection Agency’s recently promulgated emissions regulations for coal-fired power plants, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ increasing attention to environmental, social, and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor; our ability to maintain satisfactory relations with our employees; increases in labor costs including costs of health insurance and taxes resulting from the Affordable Care Act, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortage of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these, and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2023, filed on February 23, 2024,and ARLP’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2024, filed on May 9, 2024. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

For more than 70 years, Vectrus has provided critical mission support for our customers’ toughest operational challenges. As a high-performing organization with exceptional talent, deep domain knowledge, a history of long-term customer relationships, and groundbreaking technical expertise, we deliver innovative, mission-matched solutions for our military and government customers worldwide. Whether it’s base operations support, supply chain and logistics, IT mission support, engineering and digital integration, security, or maintenance, repair and overhaul, our customers count on us for on-target solutions that increase efficiency, reduce costs, improve readiness, and strengthen national security. Vectrus is headquartered in Colorado Springs, Colo., and includes about 8,100 employees spanning 205 locations in 28 countries. In 2021, Vectrus generated sales of $1.8 billion. For more information, visit the company’s website at www.vectrus.com or connect with Vectrus on Facebook, Twitter, and LinkedIn.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Awards. Returning to a continuing theme, V2X recently has been awarded some significant new and re-compete business. We believe the awards demonstrate the Company’s ability to compete, and win, in the converged environment.

GMR Award. Notably, on July 22nd V2X secured a $48.5 million ID/IQ contract with the U.S. Army for V2X’s Gateway Mission Router. This is a significant award, in our view, as it highlights V2X’s ability to deliver cutting edge solutions to its partners and expands the number of platforms on which GMR can reside. In addition, margins on the GMR product should be additive to the Company’s overall margin profile.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics and diagnostics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of immunology, rare disease, infectious disease, and central nervous system (CNS) product candidates. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-15001 which is a humanized monoclonal antibody targeting CD40-ligand being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the second half of 2022. Tonix’s rare disease portfolio includes TNX-29002 for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan-Drug Designation by the FDA. Tonix’s infectious disease pipeline includes a vaccine in development to prevent smallpox and monkeypox called TNX-8013, next-generation vaccines to prevent COVID-19, and an antiviral to treat COVID-19. Tonix’s lead vaccine candidates for COVID-19 are TNX-1840 and TNX-18504, which are live virus vaccines based on Tonix’s recombinant pox vaccine (RPV) platform. TNX-35005 (sangivamycin, i.v. solution) is a small molecule antiviral drug to treat acute COVID-19 and is in the pre-IND stage of development. TNX-102 SL6, (cyclobenzaprine HCl sublingual tablets), is a small molecule drug being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix expects to initiate a Phase 2 study in Long COVID in the second quarter of 2022. The Company’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL, is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022. Finally, TNX-13007 is a biologic designed to treat cocaine intoxication that is expected to start a Phase 2 trial in the second quarter of 2022. TNX-1300 has been granted Breakthrough Therapy Designation by the FDA.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Tonix Announced Two Significant Developments In Late July. Tonmya (TNX-102 SL) has received Fast Track Review designation from the FDA. This designation is awarded to products that can make significant impact on serious medical conditions. The designation provides important benefits for Tonmya including eligibility for Accelerated Approval and Priority Review Fast Track Review. The NDA application for approval is expected to be filed in 2H24.

Fast Track Review Is A Significant Distinction. The FDA awards Fast Track Review to drugs that treat serious conditions with unmet needs. It is given when the FDA believes the drug is either providing a therapy where none exists and/or has meaningful advantages over existing therapies. We have long believed the Tonmya Phase 3 data meets both requirements.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Eurodry operates a competitive fleet. EuroDry Ltd. owns and operates dry bulk carriers that transport major bulks, including iron ore, coal, grains, and minor bulks such as bauxite, phosphate, and fertilizer. Eurodry’s fleet is comprised of 13 dry bulk carriers, including five Panamax, five Ultramax, two Kamsarmax, and one Supramax dry bulk carriers all of which are in operation. The total cargo carrying capacity of the company’s 13 dry bulk carriers is 918,502 deadweight tonnes (dwt). The average age of the fleet is 13.5 years. The orderbook in the sector is nearing a 20-year low and demand growth for drybulk vessels appears strong through at least the remainder of 2024. Some uncertainty exists beyond 2024, particularly with respect to bulk commodity demand in China.

Updating estimates. We have lowered our 2024 EBITDA and EPS estimates to $23.8 million and $1.54, respectively, from $28.1 million and $2.05. The revisions reflect fewer available days in the second and third quarters due to drydocking, along with modestly lower time charter equivalent rates.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) today announced that the Board of Directors of ARLP’s general partner (“Board of Directors”) approved a cash distribution to its unitholders for the quarter ended June 30, 2024 (the “2024 Quarter”).

ARLP unitholders of record as of the close of trading on August 7, 2024 will receive a cash distribution for the 2024 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on August 14, 2024. The announced distribution is consistent with the cash distributions of $0.70 per unit for the quarters ended June 30, 2023 and March 31, 2024.

As previously announced, ARLP will report financial results for the 2024 Quarter before the market opens on Monday, July 29, 2024 and Alliance management will discuss these results during a conference call beginning at 10:00 a.m. Eastern that same day.

To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13747640.

In addition to the cash distribution for the 2024 Quarter, ARLP is announcing that John H. Robinson will retire from the Board of Directors at the end of the year.

“John has been an invaluable asset of Alliance since 1999,” said Mr. Joseph W. Craft III, Chairman, President and CEO of ARLP’s general partner. “John’s service on the Board of Directors has been instrumental to ARLP’s success since its inception and we are grateful for his thoughtful guidance over the years and wish him the best in retirement.”

Mr. Robinson has stepped down as Chairman of the Compensation Committee, but he will remain a member of the Audit, Compensation and Conflicts Committee until his retirement at the end of the year. Board of Director member Nick Carter, who is a member of the Compensation Committee, has been appointed as Chairman of such committee. In addition, Wilson M. Torrence, who is the Chairman of the Audit Committee, has been appointed as a member of the Conflicts Committee.

ARLP is also announcing that on July 24, 2024, Paul H. Vining has been elected to the Board of Directors and will serve as the board’s lead director. In such capacity, Mr. Vining will assist the Board of Directors and ARLP’s management team on planning and other initiatives as directed from time to time by the Board of Directors or Mr. Craft.

“I am pleased to welcome Paul to the ARLP team,” Mr. Craft said. “Paul’s extensive background and leadership in the natural resources mining industry brings a unique level of knowledge and experience of global energy markets to the Board of Directors. We look forward to working with Paul as lead director to continue positioning ARLP as a reliable energy provider now and into the future.”

Mr. Vining has served as Chairman of the Board of Directors of Westmoreland Mining, LLC, a privately held coal producer, since October 2019, and as Chairman of the Board of Directors of The Frazier Quarry Inc. since July 2023. From May through July 2022, Mr. Vining served as Chairman of the Board of Directors of Allegiance Coal Limited (ASX: AHQ) and from 2016 to 2019 served as a member of the Board of Directors of the general partner of then NYSE-listed Foresight Energy LP. Mr. Vining began his career in 1979 as a mineral engineer and has held a variety of senior executive positions over the years with several companies, including as Chief Executive Officer of Minerals Refining Company throughout 2022, Executive Vice President Global Investment and Development for Xcoal Energy and Resources LLC from 2019 to 2021, and Chief Executive Officer of The Cline Group, LLC from 2015 to 2019. Prior to that, Mr. Vining held senior executive positions in several major companies including as Chief Operating Officer and then President of Alpha Natural Resources, Inc., President and Chief Operating Officer of Patriot Coal Company, Chief Executive Officer of Magnum Coal Company, Chief Commercial Officer of Arch Coal Inc. and Chief Commercial Officer of Peabody Energy, Corporation. Earlier in his career, Mr. Vining held various commercial and marketing positions at Massey Energy Company, Occidental Petroleum Corp., and ENI S.p.A. Mr. Vining holds a Bachelor and a Master of Science degree in Mining and Minerals Engineering from Columbia University and a Bachelor of Science degree in Chemistry from the College of William and Mary.

In addition to news regarding the Board of Directors, ARLP is announcing that Mark A. Watson has been promoted to the role of Senior Vice President – Operations and Technology of the Partnership’s general partner.

“Please join me in congratulating Mark on his promotion to Senior Vice President,” commented Mr. Craft. “Mark has been with Alliance since starting as an intern in 1994, holds a Bachelor of Science degree and a Master of Science degree in Electrical Engineering from the University of Kentucky, and has contributed significantly to the operations side as well as the technology development side of ARLP’s business over many years. Mark’s strong leadership and expertise at our Matrix Design Group (“Matrix”) has seen Matrix expand its products and services beyond the domestic underground mining industry into the international mining and industrial markets positioning Matrix to accelerate innovation and growth at ARLP. In Mark’s expanded role he will continue to lead Matrix as well as advance other technology growth opportunities in different markets for ARLP.”

Concurrent with this announcement we are providing qualified notice to brokers and nominees that hold ARLP units on behalf of non-U.S. investors under Treasury Regulation Section 1.1446-4(b) and (d) and Treasury Regulation Section 1.1446(f)-4(c)(2)(iii). Brokers and nominees should treat one hundred percent (100%) of ARLP’s distributions to non-U.S. investors as being attributable to income that is effectively connected with a United States trade or business. In addition, brokers and nominees should treat one hundred percent (100%) of the distribution as being in excess of cumulative net income for purposes of determining the amount to withhold. Accordingly, ARLP’s distributions to non-U.S. investors are subject to federal income tax withholding at a rate equal to the highest applicable effective tax rate plus ten percent (10%). Nominees, and not ARLP, are treated as the withholding agents responsible for withholding on the distributions received by them on behalf of non-U.S. investors.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

Investor Relations Contact

Cary P. Marshall Senior Vice President and Chief Financial Officer 918-295-7673 investorrelations@arlp.com

Key Points: – Core PCE Index rose 2.6% year-over-year in June, unchanged from May. – Three-month annualized inflation rate fell to 2.3% from 2.9%. – Economists anticipate the Fed may signal a September rate cut at next week’s meeting.

The Federal Reserve’s preferred inflation gauge, the Personal Consumption Expenditures (PCE) Index, showed signs of stabilization in June, potentially paving the way for a rate cut in September. This development has caught the attention of economists and market watchers alike, as it could mark a significant shift in the Fed’s monetary policy.

According to the latest data, the core PCE Index, which excludes volatile food and energy prices, rose 2.6% year-over-year in June. While this figure slightly exceeded economists’ expectations, it remained unchanged from the previous month and represented the slowest annual increase in over three years. More importantly, the three-month annualized rate declined to 2.3% from 2.9%, indicating progress towards the Fed’s 2% inflation target.

Economists are divided on the implications of this data. Wilmer Stith, a bond portfolio manager at Wilmington Trust, believes that this reinforces the likelihood of no rate movement in July and sets the stage for a potential rate cut in September. Gregory Daco, chief economist at EY, anticipates a lively debate among policymakers about signaling a September rate cut.

However, the path forward is not without challenges. Scott Helfstein, head of investment strategy at Global X ETFs, cautioned that while the current outcome is nearly ideal, modestly accelerating inflation could still put the anticipated September rate cut in question.

The Fed’s upcoming policy meeting on July 30-31 is expected to be a crucial event. While traders widely anticipate the central bank to hold steady next week, there’s growing speculation about a potential rate cut in September. Luke Tilley, chief economist at Wilmington Trust, suggests that while the data supports a July cut, the Fed may prefer to avoid surprising the markets.

Fed Chair Jerome Powell’s recent comments have added weight to the possibility of a rate cut. In a testimony to US lawmakers, Powell noted that recent inflation numbers have shown “modest further progress” and that additional positive data would strengthen confidence in inflation moving sustainably toward the 2% target.

Other Fed officials have echoed this sentiment. Fed Governor Chris Waller suggested that disappointing inflation data from the first quarter may have been an “aberration,” and the Fed is getting closer to a point where a policy rate cut could be warranted.

As the Fed enters its blackout period ahead of the policy meeting, market participants are left to speculate on how officials might interpret the latest PCE data. The steady inflation reading provides the Fed with more time to examine July and August data before making a decision on a September rate cut.

The upcoming Fed meeting will be closely watched for any signals about future rate movements. While a July rate cut seems unlikely, the focus will be on any language that might hint at a September adjustment. As Bill Adams, chief economist for Comerica, noted, the June PCE report is consistent with the Fed holding rates steady next week but potentially making a first rate cut in September.

As the economic landscape continues to evolve, the Fed’s decision-making process remains under intense scrutiny. The balance between controlling inflation and supporting economic growth will undoubtedly be at the forefront of discussions as policymakers navigate these uncertain waters. The coming months will be crucial in determining whether the Fed’s cautious approach to rate cuts will be validated by continued progress in taming inflation.

NEW ALBANY, Ohio, July 26, 2024 (GLOBE NEWSWIRE) — CVG (NASDAQ: CVGI) will hold its quarterly conference call on Tuesday, August 6, 2024, at 8:30 a.m. ET, to discuss second quarter 2024 financial results. CVG will issue a press release and presentation prior to the conference call.

Toll-free participants dial (800) 549-8228 using conference code 11335. International participants dial (289) 819-1520 using conference code 11335. This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com where it will be archived for one year.

A telephonic replay of the conference call will be available until August 20, 2024. To access the replay, toll-free callers can dial (877) 674-7070 using access code 11335#.

About CVG

At CVG, we deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries, and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Investor Relations Contact: Ross Collins or Stephen Poe Alpha IR Group CVGI@alpha-ir.com

CHARLOTTE, N.C., July 26, 2024 (GLOBE NEWSWIRE) — NN, Inc. (NASDAQ: NNBR), a global diversified industrial company that engineers and manufactures high-precision components and assemblies, announced today that it will release its second quarter 2024 financial results for the period ended June 30, 2024, after the close of the market on Wednesday, August 7, 2024. The company will hold a related conference call on Thursday, August 8, 2024, at 10 a.m. E.T. Participants on the call are asked to register five to 10 minutes prior to the scheduled start time by dialing 1-877-255-4315 and from outside the U.S. at 1-412-317-6579.

The conference call will be webcast simultaneously and in its entirety through the NN, Inc. Investor Relations website. Shareholders, media representatives and others may participate in the webcast by registering through the Investor Relations section on the company’s website at https://investors.nninc.com/.

For those who are unavailable to listen to the live call, a replay will be available shortly after the call on NN’s website through August 8, 2025.

About NN, Inc.

NN, Inc., a global diversified industrial company, combines advanced engineering and production capabilities with in-depth materials science expertise to design and manufacture high-precision components and assemblies for a variety of markets on a global basis. Headquartered in Charlotte, North Carolina, NN has facilities in North America, Europe, South America, and Asia. For more information about the company and its products, please visit www.nninc.com.

Investor & Media Contacts: Joe Caminiti or Stephen Poe, Investors Tim Peters or Emma Brandeis, Media NNBR@alpha-ir.com 312-445-2870

LAKE ZURICH, Ill.–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) today announced that its board of directors has declared a quarterly cash dividend of $0.075 per share. The dividend will be paid on September 4, 2024, to stockholders of record as of the close of business on August 16, 2024.

“This is the Company’s 27th quarterly cash dividend since it began paying dividends in 2018. The Company’s dividend has become an important part of our capital allocation strategy, and we remain committed to supporting our quarterly dividend with our robust free cash flow. At the current stock price, on an annualized basis, our shareholders are receiving an approximate 6% yield on their investment,” said Tom Tedford, President, and Chief Executive Officer of ACCO Brands.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn and play. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

Chris McGinnis Investor Relations (847) 796-4320

Kori Reed Media Relations (224) 501-0406Source: ACCO Brands Corporation

Resources Connection, Inc. provides agile consulting services in North America, Europe, and the Asia Pacific. The company offers finance and accounting services, including process transformation and optimization, financial reporting and analysis, technical and operational accounting, merger and acquisition due diligence and integration, audit readiness, preparation and response, implementation of new accounting standards, and remediation support. It also provides information management services, such as program and project management, business and technology integration, data strategy, and business performance management. In addition, the company offers corporate advisory, strategic communications, and restructuring services; and corporate governance, risk, and compliance management services, such as contract and regulatory compliance, enterprise risk management, internal controls management, and operation and information technology (IT) audits. Further, it provides supply chain management services comprising strategy development, procurement and supplier management, logistics and materials management, supply chain planning and forecasting, and unique device identification compliance; and human capital services, including change management, organization development and effectiveness, compensation and incentive plan strategies, and optimization of human resources technology and operations. Additionally, the company offers legal and regulatory supporting services for commercial transactions, global compliance initiatives, law department operations, and law department business strategies and analytics. It also provides policyIQ, a proprietary cloud-based governance, risk, and compliance software application. The company was formerly known as RC Transaction Corp. and changed its name to Resources Connection, Inc. in August 2000. Resources Connection, Inc. was founded in 1996 and is headquartered in Irvine, California.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

10-K Filed. We had the opportunity to review the Company’s 10-K filed earlier in the week. Some key takeaways from the 10-K include the Company’s continuation of its pristine balance sheet, solid cash flow generation, and the return of capital to shareholders.

Pristine Balance Sheet. The Company continues to have plenty of liquidity to work with, as RGP’s total liquidity at year end was $283 million, with no outstanding debt. We believe the Company can utilize the liquidity in the balance sheet towards acquisitions should the opportunity present itself to RGP. Outside of acquisitions, management can utilize its liquidity towards organic growth, including its technology transformation initiative, in our view.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Travelzoo® provides its 30 million members with exclusive offers and one-of-a-kind experiences personally reviewed by our deal experts around the globe. We have our finger on the pulse of outstanding travel, entertainment, and lifestyle experiences. We work in partnership with more than 5,000 top travel suppliers—our long-standing relationships give Travelzoo members access to irresistible deals.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

In line quarter. Second quarter results were largely in line with our estimates. Q2 revenue of $21.1 million was a touch below our estimate of $22.4 million, and roughly flat with the prior year period. Adj. EBITDA in the quarter was $4.9 million, above our estimate of $4.4 million by roughly 11.0%, as a result of lower marketing expenses and higher gross margin. Gross margins were 88.1%, better than our 86.2% estimate.

A focus on subscribers. The Company introduced an annual $40 paid subscription for its travel deals at the beginning of the calendar year. All of its 30 million legacy members will be introduced to the paid model beginning in 2025. Management plans to add new benefits for the paid membership, although it did not yet identify what those benefits might be.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Ocugen, Inc. is a biotechnology company focused on developing and commercializing novel gene therapies, biologicals, and vaccines. The lead product in its gene therapy program, OCU400, is in Phase 1/2 clinical trials for retinitis pigmentosa.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Escalating Dose Stage Has Completed Dosing. Ocugen reported completion of the escalating dose stage of its Phase 1/2 ArMaDa trial testing OCU410 in Geographic Atrophy (GA), a late-stage complication of dry age-related macular degeneration (dry AMD). OCU410 uses Ocugen’s “master regulatory gene” approach, with a single injection to deliver the nuclear receptor gene RAR-related orphan receptor A (RORA). This gene regulates pathways that lead to dry age-related macular degeneration.

Next Stage In Phase 1/2 Trial Expected In 3Q24. The Phase 1/2 ArMaDa trial is testing OCU410 in geographic atrophy (GA), a lesion secondary to dry AMD at 14 retina surgical centers in the US. The first stage of the trial administered three escalating doses of OCU410. The second stage will randomize patients into three arms at a ratio of 1:1:1 to compare the medium and high dosage levels to a control group. Endpoints will be efficacy and safety.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.