Endeavour Silver is a mid-tier precious metals mining company that operates two high-grade, underground, silver-gold mines in Mexico. Endeavour is currently advancing the Terronera mine project towards a development decision, pending financing and final permits and exploring its portfolio of exploration and development projects in Mexico, Chile and the United States to facilitate its goal to become a premier senior silver producer. Our philosophy of corporate social integrity creates value for all stakeholders.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third quarter production exceeded our estimates. On a silver equivalent basis, third quarter production exceeded our expectations due to higher silver grades at both mines. Compared to the second quarter of 2022, silver production increased 7.3% to 1,458,448 ounces, while gold production decreased 1.0% to 9,194 ounces. Third quarter silver and gold sales amounted to 1,327,325 ounces and 8,852 ounces, respectively. At quarter end, Endeavour held 1,527,548 ounces of silver and 3,210 ounces of gold in bullion inventory and 2,769 ounces of silver and 144 ounces of gold in concentrate inventory. Relative to the end of the second quarter, bullion inventory increased while concentrate inventory declined.

Updating estimates. While production was ahead of our estimates, we had assumed greater sales from inventory. Due to lower than expected sales in the third quarter, we have lowered our net income and earnings per share estimates to $2.0 million and $0.01, respectively, from $5.6 million and $0.03. We have lowered our full year EBITDA and EPS estimates to $42.9 million and $0.09, respectively, from $49.9 million and $0.11. Due to modestly lower 2023 silver and gold pricing assumptions, we have trimmed our 2023 EBITDA and EPS estimates to $53.3 million and $0.11, respectively, from $58.6 million and $0.13.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power market, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Property located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Recent drill results. Defense Metals released assay results from two additional core drill holes which highlight the Wicheeda REE deposit’s potential for high REE grades over significant widths. The two holes, representing 717 meters of drilling, were collared from the same site within the northern part of the project area.

High grade results in the northern portion of the Wicheeda deposit. Infill drill hole WI22-68, the deepest hole drilled to date at 395 meters, was drilled southwest within the northern area of the deposit and yielded a broad mineralized intercept of high-grade dolomite carbonatite averaging 3.58% total rare earth oxide (TREO) over 124 meters, including a high-grade zone of 6.7% TREO over 18 meters that included a 3-meter sample yielding 8.58% TREO. Hole WI22-63 collared from the same drill site, tested the interpreted eastern contact of the carbonatite body at depth and returned 2.29% TREO over 39 meters, including 5.08% TREO over 9 meters.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Bassett Furniture Industries, Incorporated manufactures, markets, and retails home furnishings in the United States. The company operates in three segments: Wholesale, Retail, and Logistical Services. It is involved in the design, manufacture, sourcing, sale, and distribution of furniture products to a network of company-owned and licensee-owned Bassett Home Furnishings (BHF) retail stores, as well as independent furniture retailers; and wood and upholstery operations. As of September 16, 2017, the company operated a network of 91 company-and licensee-owned stores. It also provides shipping, delivery, and warehousing services to customers in the furniture industry. In addition, the company owns and leases retail store properties. It also distributes its products through other multi-line furniture stores, Bassett galleries or design centers, specialty stores, and mass merchants. Bassett Furniture Industries was founded in 1902 and is based in Bassett, Virginia.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Acquisition Proposal. Yesterday, CSC Generation Holdings, Inc. released correspondence sent to Bassett Furniture Industries, Incorporated offering to purchase the Company for $21 per share in an all-cash acquisition. According to the letter, CSC “submitted bona fide, attractive acquisition proposals to the Board of Directors of the Company on June 30, 2022 and September 26, 2022, the Board has been unwilling to engage with us in any meaningful way.”

Who Is CSC? Founded in 2016, CSC has a successful track record of acquiring store and catalogue-based companies and then transforming them into high-performance, digital-first brands through CSC’s proven omni-channel technology platform, operating expertise and scale. CSC is backed by world-class institutional investors, including Altos Ventures, Khosla Ventures, Panasonic, and the family offices of domain experts in the industry, such as the founders of Wayfair and Build.com. Since its founding, CSC has acquired and successfully integrated a number of well-known brands, such as Sur La Table and One Kings Lane.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Overview: Developing A Shopping List. With the U.S. economy in the midst of a recession, we believe investors should be on the lookout for stocks on the “discount rack.” In our view, companies that possess ample funding and favorable growth characteristics could be well positioned to survive the downturn and be on the forefront of the subsequent economic recovery. This report highlights some of our favorite picks in the Entertainment & Leisure industries.

Entertainment: Bowlero Bowls Over Its Peers. Bowlero’s most recent fiscal quarter illustrated a continuation of the entertainment industry’s COVID rebound. Bowlero’s Group Event revenue grew 140% from the prior year period while total revenue was up 68%. With cash flow margins above 30% and cash on the balance sheet of $132 million, the company is poised to continue making accretive acquisitions in the fragmented bowling industry.

Gaming: Placing A Bet On Codere. The CDRO shares have been punished year-to-date (-58%) despite the company executing on its growth strategy as planned and maintaining pace to meet full-year guidance. Given a combination of robust growth in key Latin American markets and a balance sheet that boasts €84 million in cash and no LT debt, we believe the shares offer a favorable risk/reward relationship.

Esports: Motorsport Games Gets Funding. After a difficult second quarter a transformative restructuring plan has been implemented, which is estimated by the company to reduce overhead costs by 20% and save $4 million by the end of 2023. Additionally, Motorsport has secured $3 million from an existing credit line. These promising changes allow for more dollars to be spent on key revenue drivers.

Leisure. Travelzoo Readies A New Journey. Although Travelzoo (TZOO) is a digital media company, it is one of our favorite ways to play the recovering travel industry.

Investment Overview

Developing A Shopping List

The best time to buy stocks is typically in the midst of an economic recession. Investors begin to look beyond the economic weakness and begin positioning portfolios for an economic rebound. The hard part is determining when the economy is in the middle of the downturn. It appears by all standard definitions of an economic downturn that the U.S. is in an economic recession. But, how long will a downturn last? Should investors try to be cute to predict the midpoint of the downturn?

Many economic pundits paint the current state of the economy against the canvass of the 1970s, a period of high inflation and low economic growth. There are many similarities. The Federal Reserve in the early 70s was willing to provide cheap money to fuel the economy, without much concern about inflation. In the second half of the 70s, the economy was rocked by fuel supply shortages and high inflation. During the Covid pandemic, both fiscal and monetary policy was designed to provide liquidity and to make sure that people were able to pay their bills during the economic lockdowns. This had the affect of increasing personal income, even though GDP declined 31.4% in 2020. As the economy reopened, there was significant demand for goods and services, some of which were in short supply because of the previous and recurring economic lock downs. Simplistically, this fueled inflation, high demand with a consumer that had disposable income and limited supply.

As Figure #1 Early 1970s chart illustrates, the US economy grew 9.8%, as measured by real GDP, from January 1972 to September 1975. Notably, the stock market, as measured by the S&P 500 Index, declined a significant 18.6%. This was a period marked by rising inflation due to government spending. The inflation rate, as measured by the US Bureau of Labor Statistics, was a reasonable 3.3% in 1972, but increased to 11.1% in 1974 and then moderated slightly to 9.1% in 1975. The inflation rate remained above 5% for the following 3 years.

Figure #1 Early 1970s

Source: US Bureau of Economic Analysis and Yahoo Finance.

Given the current state of rising energy prices, many pundits paint the current US economic plight similar to the period of fuel shortages of the late 1970s. As Figure #2 Late 1970s illustrates, the US economy, as measured by real GDP, grew 13.5% from January 1977 to October 1981, an average of slightly more than 3% per year. Notably, inflation increased significantly, from 6.5% in 1977 to 11.3% in 1979, followed by 13.5% in 1980, and 10.3% in 1981. The stock market, as measured by the S&P 500 Index, did not react well, up 9.3% from January 1977 to October 1981, an average of 2.3% growth.

Figure #2 Late 1970s

Source: US Bureau of Economic Analysis and Yahoo Finance.

So, where are we now? In the present, the Covid induced government spending and stimulus related fiscal policy, large spending on the Ukraine war, and a Fed unwilling to reign in early signs of inflation has put the US in a dire economic position. Certainly, supply chain shortages contributed to the current rise in inflation, as well. The Fed now appears to have religion on inflation and is aggressively raising interest rates. The Fed indicated that it is willing to create economic pain to arrest inflationary pressures. Most certainly this will cause additional economic weakness. The stock market in the near to intermediate term will need to digest the likelihood of weakening corporate profits, as well. Furthermore, as it relates to the equity markets, other investment classes, such as bonds, may become more appealing, taking demand from the stock market.

We believe that arresting inflation would set a favorable trajectory for the stock market, as investors position for the prospect of an economic recovery. To some degree, the 24.4% drop in the stock market, as measured by the S&P 500 index, from January 2022 to near current levels, anticipate some of the headwinds for investors described earlier in this report, including weakening corporate profits, the prospect of a further weakened US, and, even global economy, a move toward other investment classes, and stubborn inflation. What is different this time is that the Fed now appears to be aggressively tackling inflation. As such, the 47% drop in the stock market from highs in 1973 to the low in 1974 may not be a prelude to the current environment. It was a different Fed and it took different actions.

We encourage a different approach than trying to time the market. Our advice is for investors to develop a shopping list and begin accumulating. But, be selective. We focus on companies with favorable balance sheets, or are well funded, have compelling growth characteristics, and attractive free cash flow. In other words, we look for companies that appear well positioned to come out on the other side of the recession and will benefit from an economic recovery.

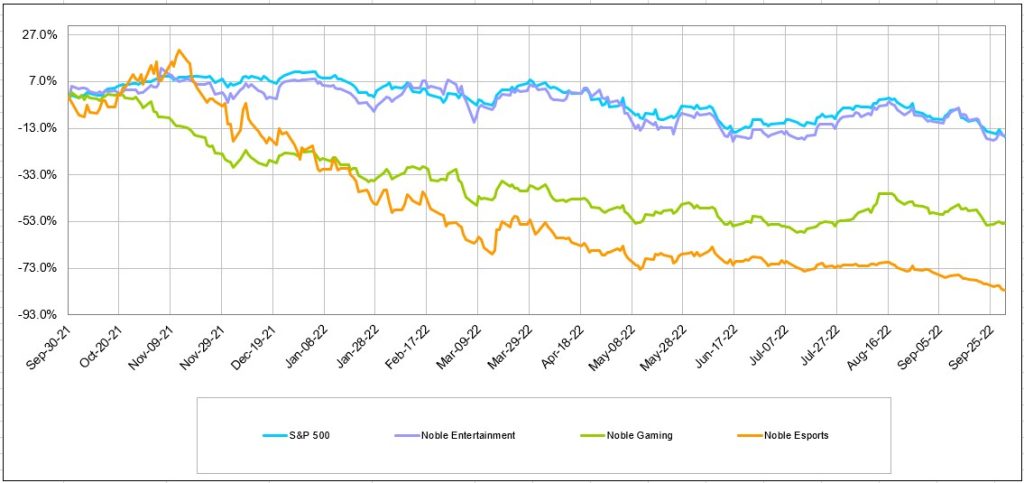

In this, our inaugural issue of the Entertainment and Leisure Industry Quarterly, we look at several companies that have favorable investment attributes for investors to consider. As Figure #3 Entertainment 12 Month Trailing Stock Performance Chart illustrates, the Entertainment Group performed poorly over the past 12 months. The Noble Entertainment index performed the best among our three Entertainment & Leisure sectors, down 16.1%, slightly outperforming the general market as measured by the S&P 500 Index, which decreased 16.8% in the comparable period. The Noble iGaming Index decreased 53.6% and the Noble eSports Index decreased 82.5% as these developmental industries were adversely affected by the closing of the capital markets to fund expansion. Given the weakness in these sectors, we look for the hidden gems. Some of our favorites highlighted in this report include: Bowlero (BOWL), Motorsport Games (MSGM), Travelzoo (TZOO) and Codere Online Luxemburg (CDRO)

Figure #3 Entertainment 12 Month Trailing Stock Performance

Source: Capital IQ

Entertainment Industry

Bowlero Bowls Over Its Peers

While the entertainment industry is broadly defined, we take a look at the Experiential Entertainment industry, in general, and at Bowlero (BOWL), specifically. In the latest quarter, the Noble Entertainment Index outperformed the general market, as measured by the S&P 500 Index, up 0.7% versus the general market decline of 5.3%. One of the contributors to the outperformance of the Entertainment group was Bowlero, up 16.2% in the comparable period.

The Bowlero shares reacted well to the company’s fiscal fourth quarter earnings release on September 15th. Q4 revenue of $267.7 million increased a strong 68% from year earlier levels and an impressive 42% above our estimate of $188.3 million. The strong revenue was attributed to favorable “walk-in” revenue, driven in part by a continuation of the Covid recovery. Adj. EBITDA was well above our estimate at $82.4 million, 45% higher than our forecast of $56.8 million.

How did Bowlero perform relative to its peers? As Figures #4 and #5 Entertainment Q2 Performance illustrates, Bowlero’s revenue growth for the comparable company peer second quarter outperformed its peers, save Live Nation. Live Nation’s revenue growth was 670%, reflecting the year earlier absence of events. Outside of Live Nation, Bowlero’s revenue growth of 68% compared favorably with the rest of its experiential entertainment peers, including Dave & Buster’s Entertainment’s, up 24%, and Vail Resorts, up roughly 31%.

Notably, management indicated that first quarter revenues are pacing 23% higher than year earlier results. As such, we raised our fiscal Q1 revenue forecast from $193.5 million to $222.5 million and raised our Q1 Adj. EBITDA estimate from $61.4 million to $72.0 million. Given strong operating momentum, we raised our fiscal full year 2023 revenue estimate to $983.5 million from $899.3 million and our Adj. EBITDA estimate to $322.2 million from $301.3 million. While we anticipate Bowlero’s revenue growth will slow as it faces more difficult comps due to the post Covid recovery and potential economic weakness, we believe that the company is well positioned. Furthermore, we expect that the company will grow revenues faster than most of its peers post Covid recovery due to the growth potential of its industry.

Figure #4 Entertainment Q2 Performance

Source: Company 10Qs

Figure #5 Entertainment Q2 Performance

Source: Company 10Qs

As of July 3, the company had $132.2 million in cash and $865.1 million in long-term debt. Debt is a comfortable 2.6 times our calendar year 2023 adj. EBITDA estimate, with net debt a conservative 2.1 times. With a large cash balance and strong cash flow generation (32% adj. EBITDA margin), we believe the company is well positioned to repurchase stock, upgrade its facilities, and/or acquire new facilities. The company has a large $200 million share repurchase authorization, of which it repurchased 3.3 million shares at an average share price of $10.07. There is a large repurchase authorization remaining. Furthermore, we believe that the company will seek acquisition fueled growth, possibly in other experiential center based facilities other than bowling.

Notably, the BOWL shares trade at 8.6 times our revised calendar full year 2023 adj. EBITDA forecast, below peers which currently trade near 9.5 times. Figure #6 Entertainment Comparables highlight the stock valuations in the experiential entertainment group. Given its favorable growth profile, (the company has grown faster than its peers), a healthy balance sheet, compelling stock valuation, and prospects for acquisition fueled growth, we view the Bowlero shares as among our favorites in the sector and one to put on a shopping list for a recovery play.

Figure #6 Entertainment Comparables

Source: Capital IQ and Noble estimates.

iGaming Industry

Placing A Bet On Codere

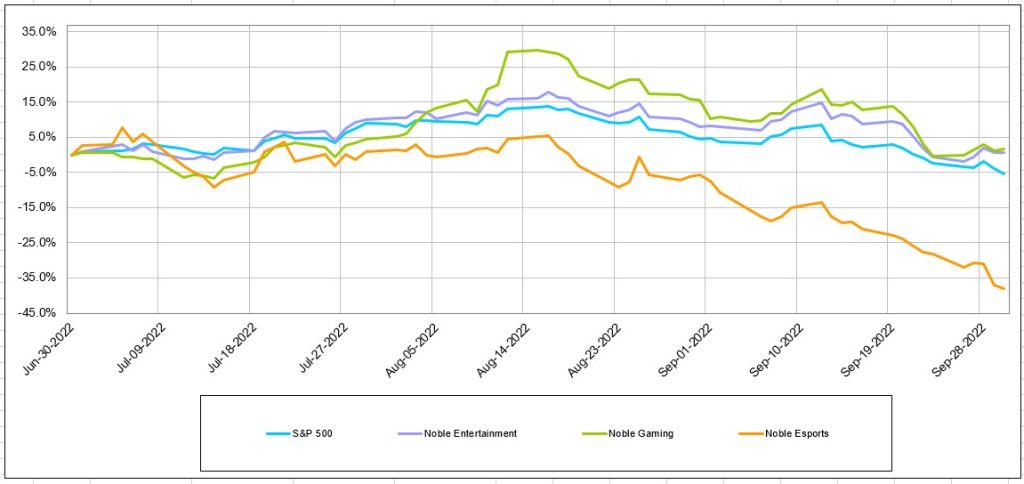

The past year has been tough on the iGaming industry. The Noble iGaming Index is down nearly 54% versus a negative 17% for the general market, as measured by the S&P 500 Index. In the latest quarter, the iGaming stocks seemed to have stabilized, up 1.6% versus a continued general market decline, down 5.3% for the general market. Interestingly, as Figure #7 Third Quarter Stock Performance chart illustrates, the iGaming sector was the best performing sector among the Entertainment and Esports sectors, which were up a modest 0.7% and down 38.1%, respectively.

The shares of Codere Online Luxembourg could not fight the headwinds of the industry wide selling pressure. The CDRO shares dropped 70% from its post de-SPACing in December 2021 to near current levels. The weakness in the shares has been in spite of the company executing on its growth strategy as planned and maintaining its fundamental pace to meet full-year guidance. In the latest quarter, the shares drifted 3.9% versus the industry which increased 1.6%.

Figure #7 Third Quarter Stock Performance

Source: Capital IQ

We believe that the CDRO shares are a victim of throwing the baby out with the bath water. The poor performance of the iGaming industry in many respects is due to the developmental nature of the industry. Many of the companies included in the Noble iGaming index do not generate positive cash flow. As such, balance sheets have been supporting growth investment. Certainly, there will be a shake-out of players in the industry that do not have the financial capability to invest for growth. We believe that Codere Online is one of the survivors.

First, the company has been executing on its development plans to expand its operations in Latin America, as evidenced by favorable quarterly results. The latest second quarter net gaming revenue grew 41% to $29.2 million, accelerating from the 24% year-over-year growth in Q1. At $11.9 million, Mexico accounted for nearly 41% of the revenue, growing 85% over the prior year period. Operations in Columbia contributed $2.2 million, with 56% growth. Even revenue in Spain grew 12%, despite restrictions on marketing in the country.

Given a combination of robust growth in key Latin American markets and a balance sheet that boasts €84 million in cash and no LT debt, we believe the shares offer a favorable risk/reward relationship. We believe the company is off to a good start since the completion of the SPAC merger, with strong execution of its growth strategy in Latin America. Management is continuing expansion with plans to add to the company’s presence in Argentina. In August, the company completed its application for an online gambling license in Cordoba, Argentina’s second-most populous province. If the company is granted a license, which would likely happen before year-end, it would begin operations shortly after the issuance. Notably, Cordoba will issue up to 10 licenses and Codere Online is one of just 10 applicants. Management believes there is an opportunity for the company to be a market leader in Argentina. To that end, the company expanded its partnership with Argentine soccer club River Plate, during the quarter becoming the club’s primary sponsor. The Codere logo is now on the front of the club’s jersey, which will increase the company’s visibility in the country.

Although the company is not yet cash flow positive, its operations in Spain generated its highest quarterly cash flow since Q2 2020. Adj. EBITDA in Spain was $3.6 million, enough to offset 87% of the $4.1 million adj. EBITDA loss from the company’s operations in Mexico. Interestingly, the marketing restrictions in the country came with a silver lining of lower competition. This is because the restrictions make it harder for newer operators to establish their brands in the country. Additionally, the lower marketing costs contributed to the strong cash flow generation. Notably, management expects similar cash flow generation going forward for the Spanish operations. We view the situation in Spain favorably as the consistent cash flow profile will help fund the expansion in Latin America and have a mitigating impact on the company’s cash burn.

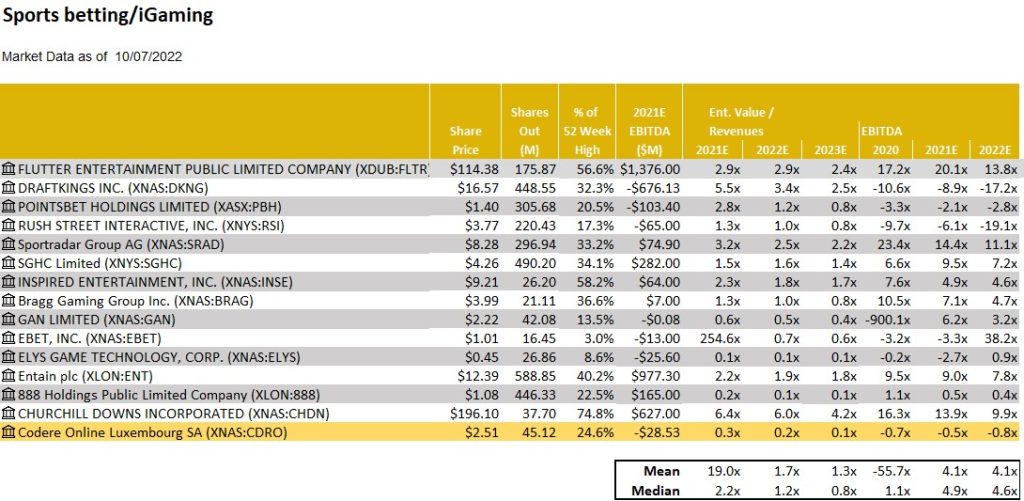

Figure #8 iGaming Comparables highlight the stock valuations in the iGaming industry and the valuation gap between the industry and Codere. Near current levels, the CDRO shares trade at 0.2 times enterprise value to 2023 expected revenue. Like other companies that have negative cash flow, the CDRO shares have suffered in recent months. However, Codere Online does not appear to be in need of funding to execute on its growth strategy. As such, we believe that investors have not differentiated it from its peers. Our price target of $9 reflects a target EV/2023 revenue multiple of 2 times, more in line with peers of 4 times, but with additional headroom for upside. The shares are rated Outperform.

Figure #8 iGaming Comparables

Source: Capital IQ and Noble estimates.

Esports Industry

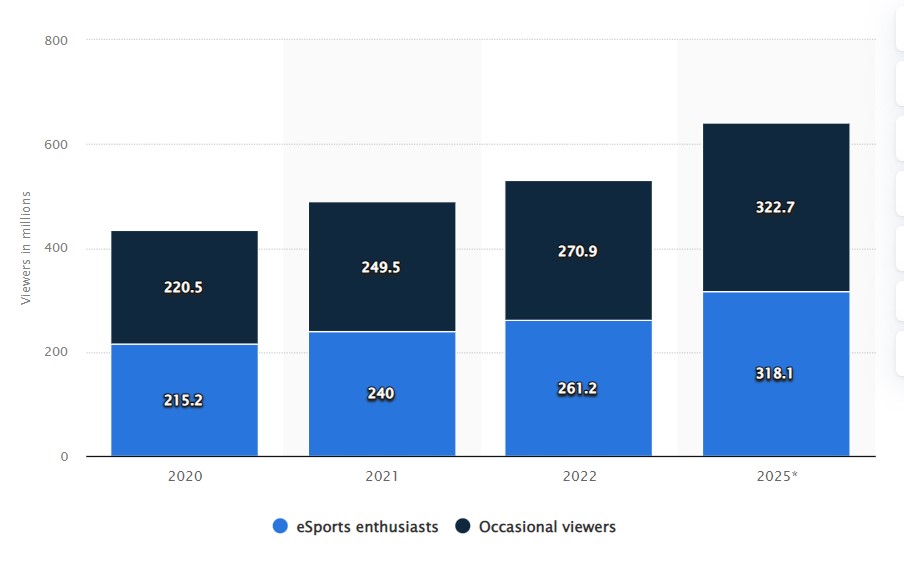

The Esports industry had a difficult year and a difficult quarter in terms of stock performance. The horrible stock performance does not reflect the overall industry trends. Video gaming is still on the rise. It is estimated that there are 2.7 billion gamers worldwide, expected to achieve an estimated 3.0 billion gamers in 2023, based on Newzoo’s numbers. The video game market is expected to reach $159.3 billion this year and grow to $200.0 billion in 2023. So, what about the Esports industry? Esports viewership was elevated during the Covid lockdowns, with viewership significantly higher. As Figure #9 Esports Viewership Outlook illustrates, viewership trends are expected to increase even from the elevated 2020 levels to over 640 million viewers in 2025.

In spite of the compelling industry fundamental trends, the individual esports companies in the space are struggling. Many of the companies were developmental, and, as such, were caught without investment spend as the capital markets closed. We find some gems in the rubble of the esports industry. The stock that we would like to highlight in this report is Motorsport Games (MSGM). Motorsport Games is a publisher of motorsport video games, with the rights to iconic racing games such as NASCAR and 24 Hour of LeMans. After a high of $15.50 in October 2021, the shares are currently trading at $0.78 per share.

Recently, the company announced several moves to shore up its financing until it releases a set of new motorsport games in 2023. At that time, the company is expected to significantly improve its financial capability to invest in future updates to its expanding game portfolio. First, the company announced that it will decrease overhead by an annualized $4 million. Secondly, the company will receive a $3 million cash advance from its majority shareholder, Motorsport Network. This agreement is under the same terms as its previous $12 million line of credit, which had been paid off. Finally, the company plans to have a 1 for 10 reverse stock split. This move is to maintain NASDAQ listing requirements.

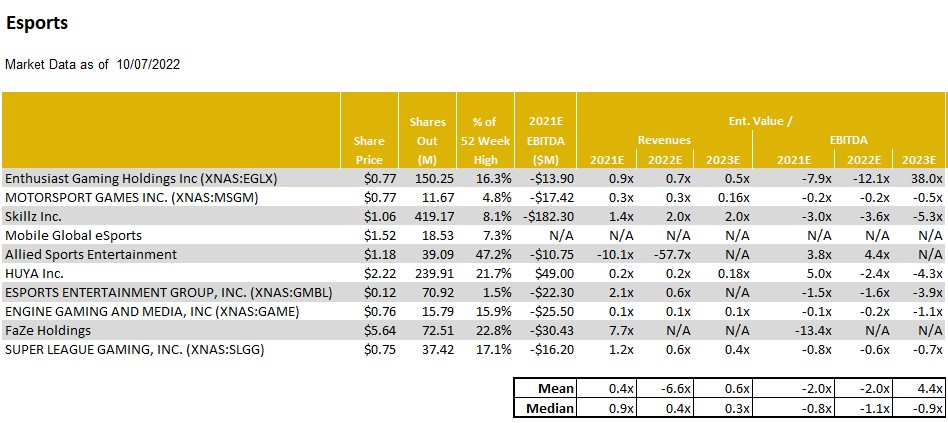

Near current levels, the MSGM shares trade at an enterprise value below cash value, well below peers as Figure #10 Esports Comparables illustrate. We view the shares as an option on the company’s ability to fund its operations long enough to launch its new titles and cash in on its world class licensing agreements. We view the shares as a high risk/high reward opportunity, suitable only for speculative investors. We rate the shares Outperform with a price target of $2.50. Notably, our price target, which represents significant upside, implies a conservative target enterprise value of just 0.7 times 2023 revenue. Please read the attached report for important disclosures.

Figure #9 Esports Viewership Outlook

Source: Newzoo/Statista

Figure #10 Esports Comparables

Source: Capital IQ and Noble estimates.

Leisure Industry

The Leisure industry is a very broad industry. In this report, we highlight a company that is in the Travel Leisure industry, but is really an advertising/media company. But, because its business is closely aligned with the travel industry, we have included it in this Leisure report. The company is Travelzoo. Much like the travel industry, there has been fits and starts with the recovery post Covid. Many countries are now open, travel restrictions are gone, and, even Covid/mask policies have relaxed. But, the industry, in general, and Travelzoo, in particular, are dealing with the weakening global economies.

In the recent second quarter, the favorable revenue momentum from the first quarter fizzled. Total company revenues declined 7.3% year over year and were down roughly 4% from the first quarter. Some seasonality appears to be at play here. The question will be whether the softness in the quarter was related to general macro economic trends and if those trends appear to be evident heading into the third quarter. We believe that the weak quarter is related to choppiness in revenue due to the company’s transition toward advertising rather than “getaway” voucher sales. As such, we do not believe that there is an unraveling of the fundamental underpinning of the company.

The company sold travel “getaway” vouchers during the Covid pandemic. Those voucher sales accounted for as much as 60% of total company revenues. Now that the travel industry is coming back, the company has pivoted toward its traditional advertising focused model. We estimate that “getaway” voucher sales were between 15% to 20% of total revenues in the latest quarter. Given that advertising represents a higher margin business, gross margins were higher than expected in the quarter (87.8% versus our 85.4% estimate). But, advertising was not as strong as what we had hoped. Management believes that travel demand increased beyond the capability of the travel industry. While prices increased for airline tickets, the industry was not able to deal with the demand given staffing shortages. Similarly, hotels faced the same issue. As a result, airlines have cutback on flights. More recently, given a waning consumer demand and softening US economy, airline prices are coming back down. We believe that the company is entering a more favorable environment given softening demand. In other words, the travel industry will need to provide favorable deals to lure consumers to travel. That is the sweet spot for Travelzoo.

Notably, the company has a flexible and improving balance sheet. As of June 30, the company had $26.6 million in cash and restricted cash and no long term debt. The company had $47.9 million in merchant liabilities (which reflects the amount of un-redeemed voucher sales). The amount of cash would be expected to be reduced as vouchers are redeemed. There are roughly $14 million in receivables. Management indicated that credit card receivables collection should significantly enhance its cash position in 2023. Given that the company will be generating positive cash flow, it is possible that the company will begin share repurchases. The company has a 1 million share repurchase authorization. The company did not repurchase shares in the latest quarter.

Near current levels, the shares trade at just 4.6 times enterprise value to our 2023 adj. EBITDA estimate, using a fully-diluted share count of 14.9 million. Our price target of $10, reflects a target multiple of 8.3 times enterprise value to our 2023 adj. EBITDA estimate. We believe over the next quarter or two revenue growth acceleration could serve as a catalyst to drive the share price higher. The shares are rated Outperform. Please see the report for important disclosures and information.

The latest report on the companies mentioned in this report may be downloaded by clicking on the respective company name:

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

Elon Musk’s Hair-Brained Ideas are Very Marketable

If your last name was Musk and one of your companies created a perfume, what would you name it? Perhaps Eau de Elon, or S3XY, an outlandish guess would be Neurastink, or simply Elon’s Musk. Here’s a hint, Musk’s perfume is a product of The Boring Company, the company that builds tunnels to enable rapid point-to-point transportation. Before this fragrance thrower, the company’s only other product was a flame thrower. So naturally, the company decided to call their new perfume, Burnt Hair. And it has already sold $1,000,000 worth.

Image: The Boring Company

A bottle of what his company referred to as ‘the essence of repugnant desire,’ will set you back about Ð1,666 or $100 USD. That’s if you buy it online. There is now an Ebay aftermarket where resellers are looking to fetch up to Ð16,666 for the product that was only released this week – 10,000 bottles of Burnt Hair have already been sold as of Wednesday morning.

“Just like leaning over a candle at the dinner table, but without all the hard work” – Boring Company Website

Image: The Boring Company

When he’s not tunneling, launching rockets, reinventing things on four wheels, neuralinking, or tweeting, Musk does keep busy with other strokes of brilliance. Did you know that in 2020 Tesla (TSLA) launched its own brand of tequila? That year Tesla, the world’s most valuable automaker, also offered limited edition satin short-shorts.

Image Credit: Tesla

It isn’t clear what the inspiration was for this new product entry; developing a perfume that has earned revenue of $1,000,000 within a couple of days of launch is quite a feat, although certainly easier than colonizing Mars, and buying a microblogging social media company. Two things on Musk’s To-Do list that he seems to have fallen behind on.

The Boring Company product page doesn’t say whether the fragrance is a limited edition item – just in time for Halloween or a long-term offering from The Boring Company. Something more exciting than a company that usually just sells holes in the ground.

The Connection Between Producer Price (PPI) and Consumer Price (CPI) Inflation

Does a higher PPI mean a higher CPI? A newly released report shows U.S. suppliers raised prices by 0.4% in September from August, when the Producer Price Index report had shown a 0.2% drop. The inflation measure that has impacted the stock market most severely this year is the Consumer Price Index. The two Bureau of Labor Statistics (BLS) releases are related but not directly correlated and are often used to measure different things by economists and those in industry.

The PPI rose 8.5% in September from a year before, down from its 8.7% annual increase in August and 11.3% in June. – BLS

How CPI and PPI are Different

The PPI for personal consumption includes all marketable production sold by U.S.-domiciled businesses for personal consumption. The majority of the products sold by domestic producers come from non-governmental sectors. However, government produces some marketable output that is under the PPI umbrella. In contrast to the PPI’s components, CPI includes goods and services provided by businesses or governments when direct costs to the consumer are levied.

The most heavily weighted item in CPI is rent. It’s weighted at 24% of the index. What the BLS calls owners’ equivalent rent is the implied rent occupants would have to pay if they were renting their homes. This is how the Bureau of Labor Statistics captures the cost of housing for owner-occupied and rented housing. This heavily weighted component is not in PPI – obviously, owners’ equivalent rent is not a domestically produced output.

The PPI for personal consumption and the CPI also differ in their treatment of imports. The CPI includes, within its basket, goods and services purchased by domestic consumers and therefore includes imports. The PPI, in contrast, does not include imports because imports are, by definition, not produced by domestic firms.

How PPI Impacts CPI

The PPI trends often work their way into consumer price movements, but not at a one-to-one basis or even a standard delayed interval. The demand component of consumer’s impact, what the consumers are willing to consume at certain price levels, is at play with what is charged for goods at the retail level. So even if the cost to manufacture goods has risen, passing the cost on is not always possible without hurting sales. At some level of price increases, demand decreases. This is different for each type of product. For instance, food, medical care, and housing may not be impacted as much as recreation, clothing, and other items which are easier to put off or do without.

Companies are trying to manage higher costs without alienating consumers who are weary of price increases. So far in the 2022 U.S. economy, consumer spending has remained strong despite the rate of CPI, but economists worry that we’re approaching a tipping point.

The Fed has raised the benchmark federal funds rate at its last three meetings by 0.75 percentage points, it now sits in the range of 3% and 3.25%. Officials have indicated they are prepared to raise rates over the course of their final two gatherings this year to around 4.25%.

Today, with consumer inflation running at a four-decade high and savings measurements trending lower, consumers are expected to begin to change buying habits. This overall is bad for business and the economy, which is why the Federal Reserve is expected to continue its fight against price increases, despite their lack of popularity with the financial markets.

“Monetary policy will be restrictive for some time to ensure that inflation moves back” Fed Vice Chair Lael Brainard (October 10).

Prices have begun to fall for some goods and services, including commodities, freight shipping, and housing. Those declines have led some Fed watchers to warn that the central bank risks tightening financial conditions too much.

Take Away

Increases in producer prices are passed to consumers when they can be. However, there is only so much a consumer is willing to pay for a purchase they can put off or substitute for something cheaper. This has ramifications for investors.

Companies where demand will wain when prices rise, may find earnings weaken; these could include producers of discretionary goods. Stocks that are shares of consumer staple companies may not feel the brunt of consumer pushback; those that produce more cost-effective brands, including white label providers, may outshine their brand name competitors if consumers increase their substituting for lower priced alternatives. Health care is one area where demand changes little as prices change at the producer or consumer level.

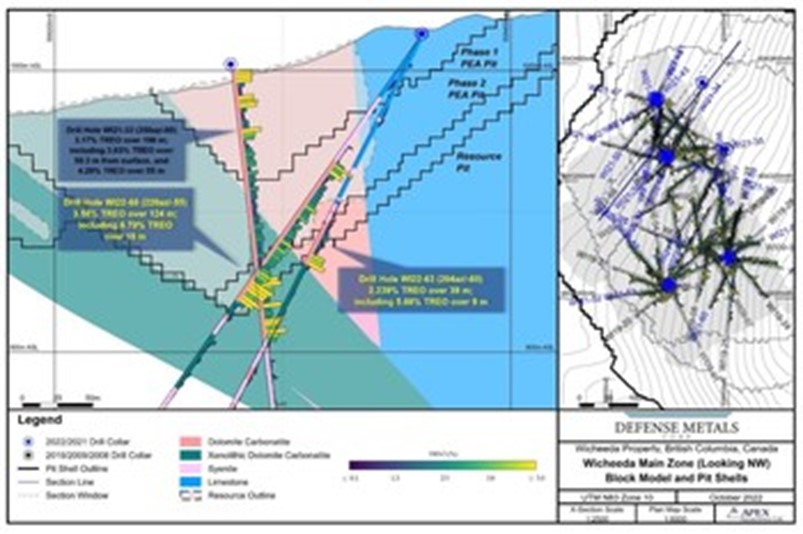

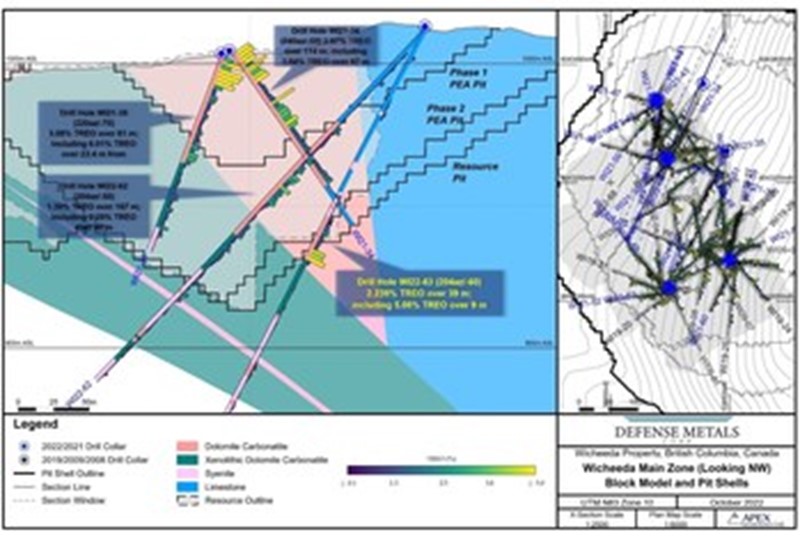

VANCOUVER, BC, Oct. 11, 2022 /PRNewswire/ – Defense Metals Corp. (“Defense Metals” or the “Company“) (TSXV: DEFN) (OTCQB: DFMTF) (FSE: 35D) announces high-grade Rare Earth Element (“REE“) assay results from an additional two core drill holes, totalling 717 metres (m), collared from the same site within the northern area of Defense Metals’ 100% owned Wicheeda REE Deposit.

Infill drill hole WI22-68 (-55o dip / 220o azimuth), the deepest hole to date on the Wicheeda Project at 395 metres, was drilled southwest within the northern area of the deposit and yielded a broad mineralized intercept of high-grade dolomite carbonatite averaging 3.58% total rare earth oxide (“TREO”) over 124 metres; including an exceptionally high-grade zone of 6.70% TREO over 18 m1 that included one 3 m sample yielding 8.58% TREO (Figure 1, and Image 1).

Drill hole WI22-63 (-60o dip / 204o azimuth) collared from the same drill site, tested the interpreted eastern contact of the carbonatite body at depth and returned 2.29% TREO over 39 m; including 5.08% TREO over 9 m1 (Figure 2).

Luisa Moreno, President, and Director of Defense Metals stated: “These two core drill holes, in particular WI22-68, once again demonstrate the potential for high REE grades over significant widths within the northern Wicheeda Deposit. Assays for WI22-68 were prioritized based on readily visible, coarse-grained REE mineralization. We look forward to receiving additional assay results of other resource infill drill holes from the northern and central Wicheeda Deposit that appear similar in terms of visually estimated REE mineralization percentage.”

1The true width of REE mineralization is estimated to be 70-100% of the drilled interval.

2 TREO % sum of CeO2, La2O3, Nd2O3, Pr6O11, Sm2O3, Eu2O3, Gd2O3, Tb4O7, Dy2O3 and Ho2O3.

Figure 1. Drill Section Holes WI22-68

Image 1: WI22-68 Visibly Coarse-grained REE Mineralization Within Interval Grading 6.70% TREO Over 18 Metres (CNW Group/Defense Metals Corp.)

About the Wicheeda REE Property

The 100% owned 4,244-hectare Wicheeda REE Property, located approximately 80 km northeast of the city of Prince George, British Columbia, is readily accessible by all-weather gravel roads and is near infrastructure, including power transmission lines, the CN railway, and major highways.

The Wicheeda REE Project yielded a robust 2021 preliminary economic assessment technical report (PEA) that demonstrated an after-tax net present value (NPV@8%) of $517 million, and 18% IRR3. A unique advantage of the Wicheeda REE Project is the production of a saleable high-grade flotation-concentrate. The PEA contemplates a 1.8 Mtpa (million tonnes per year) mill throughput open pit mining operation with 1.75:1 (waste:mill feed) strip ratio over a 19 year mine (project) life producing and average of 25,423 tonnes REO annually. A Phase 1 initial pit strip ratio of 0.63:1 (waste:mill feed) would yield rapid access to higher grade surface mineralization in year 1 and payback of $440 million initial capital within 5 years.

3 Independent Preliminary Economic Assessment for the Wicheeda Rare Earth Element Project, British Columbia, Canada, dated January 6, 2022, with an effective date of November 7, 2021, and prepared by SRK Consulting (Canada) Inc. is filed under Defense Metals Corp.’s Issuer Profile on SEDAR (www.sedar.com).

Methodology and QA/QC

The analytical work reported on herein was performed by ALS Canada Ltd. (ALS) at Langley (sample preparation) and Vancouver (ICP-MS fusion), B.C. ALS is an ISO-IEC 17025:2017 and ISO 9001:2015 accredited geoanalytical laboratory and is independent of the Defense Metals and the QP. Drill core samples were subject to crushing at a minimum of 70% passing 2 mm, followed by pulverizing of a 250-gram split to 85% passing 75 microns. A 0.1-gram sample pulp was then subject to multi-element ICP-MS analysis via lithium-borate fusion to determine individual REE content (ME-MS81h). Defense Metals follows industry standard procedures for the work carried out on the Wicheeda Project, with a quality assurance/quality control (QA/QC) program. Blank, duplicate, and standard samples were inserted into the sample sequence sent to the laboratory for analysis. Defense Metals detected no significant QA/QC issues during review of the data.

Qualified Person

The scientific and technical information contained in this news release as it relates to the Wicheeda REE Project has been reviewed and approved by Kristopher J. Raffle, P.Geo. (BC) Principal and Consultant of APEX Geoscience Ltd. of Edmonton, AB, a director of Defense Metals and a “Qualified Person” as defined in NI 43-101. Mr. Raffle verified the data disclosed which includes a review of the sampling, analytical and test data underlying the information and opinions contained therein.

About Defense Metals Corp.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power markets, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Deposit located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward‐looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, drill results including anticipated timeline of such results/assays, the Company’s plans for its Wicheeda REE Project, expanded resource and scale of expanded resource, expected results and outcomes, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration results, risks related to the inherent uncertainty of exploration and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed drilling results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward‐looking statements or forward‐looking information, except as required by law.

66% of HPV 16-positive checkpoint inhibitor refractory patients are alive at median follow up of 16 months

FLORHAM PARK, N.J., Oct. 11, 2022 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB), a clinical-stage immunotherapy company developing a growing pipeline of targeted immunotherapies for cancer and infectious disease, today announced expanded interim data in the Phase 2 clinical trial investigating the PDS0101-based triple combination therapy in advanced human papillomavirus (HPV)-positive cancers. This Phase 2 study is being conducted at the Center for Cancer Research (CCR) at the National Cancer Institute (NCI), one of the Institutes of the National Institutes of Health. The interim efficacy data from 37 HPV16-positive evaluable patients, including 29 patients in the checkpoint inhibitor (CPI) refractory arm, are consistent with the results presented at ASCO 2022 and affirm the selection of CPI refractory patients as the initial patient population for ongoing clinical development of the triple combination.

The NCI-led Phase 2 clinical trial (NCT04287868) is investigating PDS0101 in combination with two investigational immune-modulating agents – M9241, a tumor-targeting IL-12 (immunocytokine), and bintrafusp alfa, a bifunctional checkpoint inhibitor (PD-L1/ TGF-β) – in recurrent or metastatic HPV-positive cancers in patients who have failed prior therapy. The triple combination is being studied in CPI-naïve and -refractory patients with advanced HPV-positive anal, cervical, head and neck, vaginal, and vulvar cancers. Both M9241 and bintrafusp alfa are owned by Merck KGaA, Darmstadt, Germany.

Highlights of the expanded interim data are as follows:

Survival data: 66% (19/29) of HPV 16-positive CPI refractory patients in the cohort were alive at a median follow up of 16 months. Historically, this group has a median overall survival of only 3-4 months. i

Safety profile: 48% (24/50) of patients experienced Grade 3 treatment-related adverse events (AEs), and 4% (2/50) patients experienced Grade 4 AEs. There were no grade 5 treatment-related AEs

Results for HPV 16-positive checkpoint inhibitor naïve patients also continue to appear to be encouraging: 75% (6/8) of CPI naïve patients were alive at a median of 25 months of follow up. 38% (3/8) of responders had a complete response.

“The expanded interim data investigating the PDS0101-based triple combination therapy in advanced HPV-positive cancers continue to appear to show clinical signs of efficacy, durability and safety in an extremely challenging patient population with very few available treatment options,” stated Dr. Frank Bedu-Addo, President and Chief Executive Officer of PDS Biotech. “Importantly, these results affirm the decision to explore this novel combination for the treatment of CPI refractory patients, who have no approved standard of care, and support development of a combination therapy to address the significant unmet need.”

About PDS Biotechnology

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune® and Infectimune™ T cell-activating technology platforms. We believe our targeted Versamune® based candidates have the potential to overcome the limitations of current immunotherapy by inducing large quantities of high-quality, potent polyfunctional tumor specific CD4+ helper and CD8+ killer T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the potential to reduce tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV-positive cancers in multiple Phase 2 clinical trials. Our Infectimune™ based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

About PDS0101

PDS Biotech’s lead candidate, PDS0101, combines the utility of the Versamune® platform with targeted antigens in HPV-positive cancers. In partnership with Merck & Co., PDS Biotech is evaluating a combination of PDS0101 and KEYTRUDA® in a Phase 2 study in first-line treatment of recurrent or metastatic head and neck cancer, and also in second line treatment of recurrent or metastatic head and neck cancer in patients who have failed prior checkpoint inhibitor therapy. A Phase 2 clinical study is also being conducted in both second- and third-line treatment of multiple advanced HPV-positive cancers in partnership with the National Cancer Institute (NCI). A third phase 2 clinical trial in first line treatment of locally advanced cervical cancer is being performed with The University of Texas, MD Anderson Cancer Center.

KEYTRUDA® is a registered trademark of Merck Sharp and Dohme LLC, a subsidiary of Merck & Co., Inc., Rahway, NJ, USA.

Forward Looking Statements

This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to our currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control, including unforeseen circumstances or other disruptions to normal business operations arising from or related to COVID-19. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the risk factors included in the Company’s annual and periodic reports filed with the SEC. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

Versamune® is a registered trademark and Infectimune™ is a trademark of PDS Biotechnology.

BOTHELL, Wash., Oct. 11, 2022 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) announces the selection of its novel, broad-spectrum antiviral drug candidate CDI-988 for clinical development as an oral treatment for SARS-CoV-2, the virus that causes COVID-19. CDI-988 targets a highly conserved region in the active site of SARS-CoV-2 main (3CL) protease required for viral replication, and was specifically designed and developed as an oral antiviral candidate for COVID-19 using Cocrystal’s proprietary structure-based drug discovery platform technology.

In January 2022 the Company announced its intention to evaluate two oral protease inhibitors prior to selecting a lead candidate for clinical development. Both CDI-988 and the other candidate exhibited superior in vitro potency and broad-spectrum antiviral activity against SARS-CoV-2 and other coronaviruses. In preclinical studies, both candidates demonstrated favorable safety profiles and pharmacokinetic properties supportive of oral administration for the treatment of COVID-19.

“We reached the decision to move forward with clinical development of CDI-988 based on its distinct mechanism of action including an exceptionally strong affinity to the SARS-CoV-2 3CL (or main) protease compared to the known protease inhibitors and superior broad-spectrum antiviral activity against other RNA viruses,” said Sam Lee, Ph.D., Cocrystal’s President and co-interim CEO. “We are very excited about the selection of the first oral clinical candidate among our proprietary protease inhibitors.

In addition to COVID-19 antivirals, we are committed to developing potential best-in-class antiviral therapeutics to protect people worldwide from the threats of viral diseases,” he added. “Upon completion of IND-enabling toxicology studies of CDI-988, we plan to file for regulatory approval to begin a first-in-human trial in Australia in the first quarter of 2023.”

About SARS-CoV-2 SARS-CoV-2 is part of a family of coronaviruses that historically has been associated with a wide range of responses in infected individuals, ranging from no symptoms to severe disease that includes pneumonia, severe acute respiratory syndrome (SARS), kidney failure and death. By targeting the viral replication enzymes and protease, Cocrystal believes it is possible to develop an effective treatment for all illnesses caused by coronaviruses including COVID-19, SARS and Middle East Respiratory Syndrome.

Cocrystal is executing on a strategy to develop highly potent and safe pan-coronavirus antivirals for SARS-CoV-2 and its variants for hospitalized and non-hospitalized patients, as well as for prophylactic use by uninfected individuals.

About Cocrystal Pharma, Inc. Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

Cocrystal Pharma Cautionary Note Regarding Forward-Looking Statements This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our completing IND-enabling toxicology studies and the timing of our filing the Australian regulatory submission. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, but are not limited to, the uncertainties arising from any future impact of COVID-19 including in Australia, the Russian invasion of Ukraine, and/or inflation and Federal Reserve interest rate increases in response thereto on the global economy and on our Company, including supply chain disruptions and our continued ability to proceed with our program with our research with CDI-988. Further information on our risk factors is contained in our filings with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2021. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

Saskatoon, Saskatchewan–(Newsfile Corp. – October 11, 2022) – MustGrow Biologics Corp. (CSE: MGRO) (OTCQB: MGROF) (FSE: 0C0) (the “Company” or “MustGrow“), is pleased to announce that it has received conditional approval to list its common shares on the TSX Venture Exchange (the “TSXV”). The listing is subject to the Company fulfilling certain requirements of the TSXV in accordance with the terms of its conditional approval letter dated October 6, 2022.

MustGrow is actively working to satisfy the requirements and conditions that were highlighted in the approval letter and management is confident that all conditions for listing will be met in the coming weeks. Upon obtaining final approval, the Company will issue an additional news release to inform shareholders when it anticipates that its common shares will commence trading on the TSXV.

Upon completion of the final listing requirements, the Company’s common shares will be delisted from the Canadian Securities Exchange (the “CSE”) and commence trading on the TSXV under the trading symbol “MGRO”. MustGrow’s common shares will continue to trade on the OTCQB market under the symbol “MGROF” and on the Frankfurt Stock Exchange under the symbol “0C0”.

———

About MustGrow

MustGrow is an agriculture biotech company developing organic biopesticides and bioherbicides by harnessing the natural defense mechanism of the mustard plant to protect the global food supply from diseases, insect pests, and weeds. MustGrow and its leading global partners – Janssen PMP (pharmaceutical division of Johnson & Johnson), Bayer, Sumitomo Corporation, and Univar Solutions’ NexusBioAg – are developing mustard-based organic solutions to potentially replace harmful synthetic chemicals. Over 150 independent tests have been completed, validating MustGrow’s safe and effective approach to crop and food protection. Pending regulatory approval, MustGrow’s patented liquid products could be applied through injection, standard drip, or spray equipment, improving functionality and performance features. Now a platform technology, MustGrow and its global partners are pursuing applications in several different industries from preplant soil treatment and weed control, to postharvest disease control and food preservation. MustGrow has approximately 49.7 million basic common shares issued and outstanding and 55.6 million shares fully diluted. For further details, please visit www.mustgrow.ca.

Certain statements included in this news release constitute “forward-looking statements” which involve known and unknown risks, uncertainties and other factors that may affect the results, performance or achievements of MustGrow.

Generally, forward-looking information can be identified by the use of forward-looking terminology such as “plans”, “expects”, “is expected”, “budget”, “estimates”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, “occur” or “be achieved”. Examples of forward-looking statements in this news release include, among others, statements MustGrow makes regarding: (i) potential product approvals; (ii) anticipated actions by partners to drive field development work including dose rates, application frequency, application methods, and the regulatory work necessary for commercialization; (iii) expected product efficacy of MustGrow’s mustard-based technologies; (iv) expected outcomes from collaborations with commercial partners, (v) the ability of the Company to satisfy the TSXV’s requirements and conditions for final approval to list its common shares on the TSXV; and (vi) the timing and commencement of trading of the Company’s common shares on the TSXV.

Forward-looking statements are subject to a number of risks and uncertainties that may cause the actual results of MustGrow to differ materially from those discussed in such forward-looking statements, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on, MustGrow. Important factors that could cause MustGrow’s actual results and financial condition to differ materially from those indicated in the forward-looking statements include, among others, the following: (i) the preferences and choices of agricultural regulators with respect to product approval timelines; (ii) the ability of MustGrow’s partners to meet obligations under their respective agreements; and (iii) other risks described in more detail in MustGrow’s Annual Information Form for the year ended December 31, 2021 and other continuous disclosure documents filed by MustGrow with the applicable securities regulatory authorities which are available at www.sedar.com. Readers are referred to such documents for more detailed information about MustGrow, which is subject to the qualifications, assumptions and notes set forth therein.

This release does not constitute an offer for sale of, nor a solicitation for offers to buy, any securities in the United States.

Neither the CSE, the TSXV, nor their Regulation Services Provider (as that term is defined in the policies of the CSE and TSXV), nor the OTC Markets has approved the contents of this release or accepts responsibility for the adequacy or accuracy of this release.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Phase III drill program at Eagle. Maple Gold secured a third drill rig to begin a 5,000-meter Phase III drill program at its 100%-controlled Eagle Mine Property to follow up on the first two phases and test additional targets. The rig is expected to be on site by mid-October. In aggregate, Maple Gold expects to complete approximately 30,000 meters of drilling across its district-scale property package in Quebec, Canada by year-end.

Two rigs operating at Joutel. Two rigs are deployed for the deep drilling program beneath and adjacent to historic underground mine workings in the Telbel mine area at the Joutel Project, which is held in the company’s joint venture with Agnico Eagle Mines Limited. The program represents the first drilling at Telbel since the early 1990s.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Comstock (NYSE: LODE) innovates technologies that contribute to global decarbonization and circularity by efficiently converting under-utilized natural resources into renewable fuels and electrification products that contribute to balancing global uses and emissions of carbon. The Company intends to achieve exponential growth and extraordinary financial, natural, and social gains by building, owning, and operating a fleet of advanced carbon neutral extraction and refining facilities, by selling an array of complimentary process solutions and related services, and by licensing selected technologies to qualified strategic partners. To learn more, please visit www.comstock.inc.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Key permit approved for battery storage. LiNiCo Corporation, of which Comstock owns 90%, received a Conditional Use Permit to operate a lithium-ion battery (LIB) pre-recycling storage facility at an ~200-acre industrial property in Mound House, Nevada. The Lyon County Board of Commissioners unanimously approved the permit. The facility will receive, sort, and store waste LIBs, with capacity for expansion. The facility offers the potential for crushing and separating operations to supplement LiNiCo’s 137,000 square foot battery metal recycling facility in the Tahoe Reno Industrial (TRI) Center in Storey County, Nevada.

Battery recycling expected to commence in 2023. Recall that LiNiCo was recently issued an operating permit by the Nevada Division of Environmental Protection to conduct lithium-ion battery recycling and related operations at its 137,000 square foot battery metal recycling facility in the Tahoe Reno Industrial (TRI) Center in Nevada. The company expects to commence recycling operations in 2023 following receipt of an air quality permit for the TRI Facility which we anticipate in the second quarter of 2023.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Why Blockchain Could Mean Fewer Hassles for Students and Workers Proving their Credentials

Microcredentials — attestations of proficiency in a specific skill or knowledge base that are certified by an authority — can provide evidence of a person’s skills to employers.

While microcredentials are becoming more popular, the concept is hardly new: A driver’s license or the St. John Ambulance certificate could be considered as microcredentials, attesting respectively to a person’s driving skill or their competency in administering first aid.

Blockchain technology is appropriate for microcredential implementation. Blockchain can best be described as a digital ledger that records information that can be shared among a community of users. Bitcoin and other crypto-currencies are the best-known examples of blockchain, but blockchain has uses beyond financial transactions.

Student records stored in blockchain for security limit access only to legitimate users, such as institutional administrators and potential employers selected by students or job seekers. Traditionally, institutions own and control certifications like degrees, but that could shift with “digital degrees” and microcredentials that rely on blockchain.

Verifying Accomplishments