Inflation Still Surprisingly Strong and Economy Weak

Two important numbers were released on the last day of September. One was based on old news but significant in its finality; it’s the final revision to GDP for the second quarter. The next is viewed as the Fed’s preferred inflation gauge, the PCE deflator. The final GDP number will make it more difficult for public officials or pundits to suggest we can avoid a recession in 2022, and the second did not give any hope that the Fed will have any reason to change course on tightening.

A Recession By Any Other Name

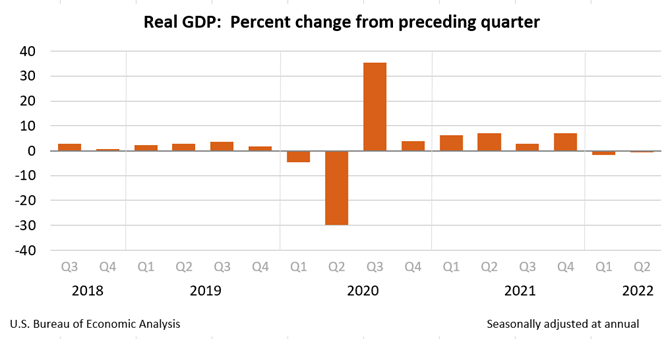

Gross domestic product (GDP) is the indicator that reflects the amount of output produced quarterly in a country. In the U.S., the Bureau of Economic Analysis (BEA) releases two estimates of quarterly GDP, known as the advance and preliminary estimates, in the two months before the release of the final number. So until the final number prints, the number GDP measure is subject to revision.

On September 30, 2022, the Final GDP report for the second quarter was released by the BEA. The report shows that GDP decreased at an annual rate of 0.6 percent in the second quarter of 2022 (table 1). This decline in economic output follows a decline of 1.6% in the first quarter of 2022.

Do two-quarters of a receding economy, based on GDP, indicate the U.S. is in the recessionary part of the business cycle? Most textbooks would agree with that definition. However, there is a Business Cycle Dating Committee within the National Bureau of Economic Research (NBER) that determines and labels where the nation is within the economic cycles; they have not made any declaration.

So far, in 2022, the economy has not experienced any economic growth. If the six months of contraction is eventually deemed an official recession, it will thus far have been a shallow one, characterized by strong employment.

Price Increases Higher than Expected

Inflation is still on many investor’s radar. The Fed is targeting reducing inflation to its 2% target. The inflation measure they use for this target is the PCE Deflator. That measure was released this morning, and it validates the aggressive actions being taken by the Federal Reserve. And suggests the Fed has a lot more work to do.

The personal consumption expenditures price index (PCE), which the Fed targets at 2%, rose 6.2% in August from a year earlier, the Commerce Department reported. Underlying inflation, as measured by a core reading that excludes food and energy prices, rose 4.9% from 4.7% previously.

These numbers are well in excess of the Fed’s target and seemingly trending upward. Expectations are the Fed will provide up to another 150 bp increase (1.50%) over the coming months. This would cause the Fed Funds rate to trade near 5%. There is nothing in today’s release that would likely cause expectations to change.

Stagflation?

High inflation and negative growth have many repeating the word “stagflation”. Stagflation has one more element missing, which is high unemployment. The current economic conditions in the U.S. include high demand for workers, this shortage actually helps feed into the inflation the Fed is trying to tame.

Take Away

The economy contracted slightly in the second quarter of 2022. The decline in production was smaller than measured during the first quarter. Federal Reserve policymakers saw one more reason to keep applying the economic brake pedal by taking money out of the economy, increasing upward rate pressures. The Fed caused rates to rise from 40-year lows faster than any time since the 1980s.

Stock market participants are factored into the Fed’s policy only to the extent that market moves may impact inflation or employment. The markets (stocks, bonds, real estate, gold) are negative on the year. There are some who suggest the Fed will use this as a signal to alter policy, if the Fed bowed to any of the markets listed here, the sign of weakness might actually cause a market collapse in stocks and bonds.

Event will feature a review ofdata from part A of the Phase 2/3 RINGSIDE trial of AL102

KOLs and management to present on Thursday, October 6th @ 8AM ET

REHOVOT, Israel and WILMINGTON, Del., Sept. 29, 2022 (GLOBE NEWSWIRE) — Ayala Pharmaceuticals, Inc. (Nasdaq: AYLA), a clinical-stage oncology company focused on developing and commercializing small molecule therapeutics for patients suffering from rare tumors and aggressive cancers, today announced that it will host a key opinion leader (KOL) webinar on unmet medical needs and evolving treatment landscape of desmoid tumors on Thursday, October 6, 2022, at 8:00 am ET.

The webinar will include presentations by Professors Bernd Kasper, MD, Ph.D., from the Mannheim University Medical Center, and Robin Jones, MD, from The Royal Marsden Hospital and Institute of Cancer Research. Prof. Kasper will discuss the current treatment landscape for desmoid tumors and Prof. Jones will review the positive data from Part A of the ongoing Phase 2/3 RINGSIDE trial of AL102 that were presented at ESMO 2022.

Ayala management will provide a company update. A live Q&A session will follow the formal presentations. To register for the event, please click here.

Professor Robin Jones is Head of the Sarcoma Unit at The Royal Marsden Hospital and Team Leader in Sarcoma Clinical Trials at The Institute of Cancer Research. Professor Jones received his medical training at Guy’s and St Thomas’ Hospital and his oncology training at The Royal Marsden. Between 2010 and 2014 he was Head of the Sarcoma Program at the University of Washington/Fred Hutchinson Cancer Research Center in Seattle. His research focuses on developing novel therapies for soft tissue sarcomas and he is currently working on a number of trials of investigational agents as well as laboratory-based studies.

Professor Bernd Kasper is Chair of the Mannheim Cancer Center (MCC) at the Mannheim University Medical Center. Professor Kasper received his MD from Heidelberg University in 2000 and also studied at the Imperial College School of Medicine, Jules Bordet Institute in Brussels, and in South Kerala, India. He has a lifetime professional dedication to patient care and research in soft tissue sarcomas, desmoid-type fibromatosis, and gastrointestinal stromal tumors and is the Principal Investigator of several national and international trials.

AL102 is being evaluated in the ongoing RINGSIDE pivotal Phase 2/3 clinical trial in desmoid tumors. Positive interim results from Part A, the Phase 2 segment of this study, were presented at ESMO 2022, showing efficacy across all cohorts, with early tumor responses that deepened over time. AL102 was well tolerated, which could allow for long term treatment of patients. The company has initiated Part B of RINGSIDE (Phase 3), as well as enrolling patients in an open label extension study.

About the RINGSIDE study The RINGSIDE pivotal Phase 2/3 study is a randomized global multi-center trial. Part A of the study is evaluating the efficacy, safety, tolerability, and tumor volume by MRI after 16 weeks of AL102 in patients with desmoid tumors. It enrolled 42 patients and is evaluating 3 doses of AL102. Patients who participated in Part A are eligible to enroll into an open-label extension study at the Part B selected dose of 1.2 mg daily, and long-term efficacy and safety will be monitored.

Part B of the study, the Phase 3 segment, has been initiated. This is a double-blind, placebo-controlled segment enrolling up to 156 patients with progressive disease, comparing AL102 at 1.2 mg once daily to placebo. The primary endpoint for Part B is progression-free survival (PFS) with secondary endpoints including objective response rate (ORR), duration of response (DOR), tumor volume reduction, and patient-reported Quality of Life (QOL) measures. For more information on the RINGSIDE Phase 2/3 study with AL102 for the treatment of desmoid tumors, please visit ClinicalTrials.gov and reference Identifier NCT04871282 (RINGSIDE).

About Desmoid Tumors Desmoid tumors, also called aggressive fibromatosis or desmoid-type fibromatosis, are rare connective tissue tumors that typically arise in the upper and lower extremities, abdominal wall, head and neck area, mesenteric root, and chest wall with the potential to arise in additional parts of the body. Desmoid tumors do not metastasize, but often aggressively infiltrate neurovascular structures and vital organs. People living with desmoid tumors are often limited in their daily life due to chronic pain, functional deficits, general decrease in their quality of life and organ dysfunction. Desmoid tumors have an annual incidence of approximately 1,700 patients in the United States and typically occur in patients between the ages of 15 and 60 years. They are most commonly diagnosed in young adults between 30-40 years of age and are more prevalent in females. Today, surgery is no longer regarded as the cornerstone treatment of desmoid tumors due to a high rate of recurrence post-surgery and there are currently no FDA-approved systemic therapies for the treatment of unresectable, recurrent or progressive desmoid tumors.

About Ayala Pharmaceuticals Ayala Pharmaceuticals, Inc. is a clinical-stage oncology company focused on developing and commercializing small molecule therapeutics for patients suffering from rare tumors and aggressive cancers. Ayala’s approach is focused on predicating, identifying and addressing tumorigenic drivers of cancer through a combination of its bioinformatics platform and next-generation sequencing to deliver targeted therapies to underserved patient populations. The company has two product candidates under development, AL101 and AL102, targeting the aberrant activation of the Notch pathway with gamma secretase inhibitors to treat a variety of tumors including Adenoid Cystic Carcinoma (ACC), T-cell Acute Lymphoblastic Leukemia (T-ALL), Desmoid Tumors and Multiple Myeloma (MM). AL101, has received Fast Track Designation and Orphan Drug Designation from the U.S. FDA and is currently in a Phase 2 clinical trial for patients with ACC (ACCURACY) bearing Notch activating mutations. AL102 is currently in a Pivotal Phase 2/3 clinical trials for patients with desmoid tumors (RINGSIDE). For more information, visit www.ayalapharma.com.

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements, including statements relating to our development of AL102, the promise and potential impact of AL102, the timing and results of our clinical trials or readouts, the prevalence of desmoid tumors and the treatment required to manage the disease, and the design of our clinical trials. These forward-looking statements are based on management’s current expectations. The words ”may,” “will,” “should,” “expect,” “plan,” “anticipate,” “could,” “intend,” “target,” “project,” “estimate,” “believe,” “predict,” “potential” or “continue” or the negative of these terms or other similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words.

These statements are neither promises nor guarantees, but involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements, including, but not limited to, the following: we have incurred significant losses since inception and anticipate that we will continue to incur losses for the foreseeable future; we are not currently profitable, and we may never achieve or sustain profitability; we will require additional capital to fund our operations, and if we fail to obtain necessary financing, we may not be able to complete the development and commercialization of AL101 and AL102; we have a limited operating history and no history of commercializing pharmaceutical products, which may make it difficult to evaluate the prospects for our future viability; we are heavily dependent on the success of AL101 and AL102, our most advanced product candidates, which are still under clinical development, and if either AL101 or AL102 does not receive regulatory approval or is not successfully commercialized, our business may be harmed; due to our limited resources and access to capital, we must prioritize development of certain programs and product candidates; these decisions may prove to be wrong and may adversely affect our business; the outbreak of COVID-19, may adversely affect our business, including our clinical trials; our ability to use our net operating loss carry forwards to offset future taxable income may be subject to certain limitations; our product candidates are designed for patients with genetically defined cancers, which is a rapidly evolving area of science, and the approach we are taking to discover and develop product candidates is novel and may never lead to marketable products; we were not involved in the early development of our lead product candidates, therefore, we are dependent on third parties having accurately generated, collected and interpreted data from certain preclinical studies and clinical trials for our product candidates; enrollment and retention of patients in clinical trials is an expensive and time-consuming process and could be made more difficult or rendered impossible by multiple factors outside our control; if we do not achieve our projected development and commercialization goals in the timeframes we announce and expect, the commercialization of our product candidates may be delayed and our business will be harmed; our product candidates may cause serious adverse events or undesirable side effects, which may delay or prevent marketing approval, or, if approved, require them to be taken off the market, require them to include safety warnings or otherwise limit their sales; the market opportunities for AL101 and AL102, if approved, may be smaller than we anticipate; we may not be successful in developing, or collaborating with others to develop, diagnostic tests to identify patients with Notch-activating mutations; we have never obtained marketing approval for a product candidate and we may be unable to obtain, or may be delayed in obtaining, marketing approval for any of our product candidates; even if we obtain FDA approval for our product candidates in the United States, we may never obtain approval for or commercialize them in any other jurisdiction, which would limit our ability to realize their full market potential; we have been granted Orphan Drug Designation for AL101 for the treatment of ACC and may seek Orphan Drug Designation for other indications or product candidates, and we may be unable to maintain the benefits associated with Orphan Drug Designation, including the potential for market exclusivity, and may not receive Orphan Drug Designation for other indications or for our other product candidates; although we have received Fast Track designation for AL101, and may seek Fast Track designation for our other product candidates, such designations may not actually lead to a faster development timeline, regulatory review or approval process; we face significant competition from other biotechnology and pharmaceutical companies and our operating results will suffer if we fail to compete effectively; we are dependent on a small number of suppliers for some of the materials used to manufacture our product candidates, and on one company for the manufacture of the active pharmaceutical ingredient for each of our product candidates; if we are unable to enter into new collaborations, or if these collaborations are not successful, our business could be adversely affected; enacted and future healthcare legislation may increase the difficulty and cost for us to obtain marketing approval of and commercialize our product candidates, if approved, and may affect the prices we may set; if we are unable to obtain, maintain, protect and enforce patent and other intellectual property protection for our technology and products or if the scope of the patent or other intellectual property protection obtained is not sufficiently broad, our competitors could develop and commercialize products and technology similar or identical to ours, and we may not be able to compete effectively in our markets; we may engage in acquisitions or in-licensing transactions that could disrupt our business, cause dilution to our stockholders or reduce our financial resources; and risks related to our operations in Israel could materially adversely impact our business, financial condition and results of operations.

These and other important factors discussed under the caption “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2021 filed with the U.S. Securities and Exchange Commission (SEC) on March 28, 2022 and our other filings with the SEC, could cause actual results to differ materially from those indicated by the forward-looking statements made in this press release. Any such forward-looking statements represent management’s estimates as of the date of this press release. New risk factors and uncertainties may emerge from time to time, and it is not possible to predict all risk factors and uncertainties. While we may elect to update such forward-looking statements at some point in the future, except as required by law, we disclaim any obligation to do so, even if subsequent events cause our views to change. Although we believe the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. These forward-looking statements should not be relied upon as representing our views as of any date subsequent to the date of this press release.

THE CONTEMPORARY ARTIST AND LEADING MOTORSPORTS VIDEO GAME PUBLISHER COLLABORATE WITH LIVE FAST MOTORSPORTS FOR UPCOMING NASCAR CUP SERIES AND CHARITY EVENTS

MIAMI, Sept. 29, 2022 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games”), a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world, announces today its partnership with contemporary artist Frankie Zombie. The partnership, done in collaboration with Live Fast Motorsports, will see a series of charity activations and a custom-made, stock-car paint scheme for the No. 78 Ford Mustang.

The Frankie Zombie-designed custom paint scheme will be showcased and driven by BJ McLeod during the NASCAR Cup Series Dixie Vodka 400 on October 23rd at Homestead-Miami Speedway. Prior to watching McLeod race in the custom wrapping, fans will be able to download the paint scheme as part of the NASCAR 21: Ignition Victory Edition, 2022 Throwback Pack DLC, Season Pass 2 and Season Pass Complete for Xbox, PlayStation and PC through the Steam store. Players that purchase NASCAR 21: Ignition Victory Edition, Season Pass 2 or Season Pass Complete will have access to the custom-designed scheme on October 6, weeks before the car hits the track in real life.

In addition to designing the custom wrap for the NASCAR Cup Series race, Zombie will be appearing at a series of in-person, live painting events during the weekends of the Bank of America ROVAL 400 at Charlotte Motor Speedway (October 8th and 9th) and the aforementioned Dixie Vodka 400 at Homestead-Miami Speedway (October 22nd and 23rd). At the events, two additional car hoods with custom-designed wrappings done by Zombie will be raffled off for charity, with the proceeds going to Speedway Children’s Charity and the NASCAR Foundation, a leading charity that works to improve the lives of children who need it most in the NASCAR communities, through the Speediatrics Children’s Fund and the Betty Jane France Humanitarian Award.

“We’re excited to kick off our partnership with Frankie Zombie, as it will push our philanthropic efforts forward, pay respect to the art community and provide a new way for our community to interact with the sport,” said Jay Pennell, Brand Manager, NASCAR atMotorsport Games. “It is an ongoing priority for Motorsport Games to take new approaches in expanding our audience offerings and events and we feel Frankie is the perfect person to help bridge fans together through crossover appeal. Frankie is a one-of-a-kind artist, and we hope this upcoming initiative will not only welcome a new community into the Motorsport Games ecosystem, but give our pre-existing fans even more unique and creative elements to our in-person activations and game offerings.”

“Converting a NASCAR stock car into a piece of art is not something you would typically see nor expect, and as a lifelong fan of racing, I cannot wait to see the design putting in 400 laps of racing,” said Frankie Zombie. “I’m excited to partner with Motorsport Games and Live Fast Motorsports to bring these paint schemes to life for fans and help them gain a new appreciation for art and vice versa. I encourage everyone to come to the live painting events to be a part of some great initiatives for charity.”

About Motorsport Games: Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. RFactor 2 also serves as the official sim racing platform of Formula E, while also powering Formula 1™ centers through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Forward-Looking Statements: Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. These forward-looking statements include, but are not limited to, statements concerning the timing, participants and expected benefits of the activations, such as expanding the Company’s audience offerings and events, welcoming a new community into the Motorsport Games ecosystem, and giving the Company’s pre-existing fans even more unique and creative elements to its in-person activations and game offerings. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, without limitation: difficulties, delays in or unanticipated events that may impact the timing and expected benefits of the activations, such as due to unexpected changes in the event participants, as well as less than anticipated participation in the activations. Factors other than those referred to above could also cause Motorsport Games’ results to differ materially from expected results. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the Securities and Exchange Commission (the “SEC”), including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date. Additionally, the business and financial materials and any other statement or disclosure on, or made available through, Motorsport Games’ website or other websites referenced or linked to this press release shall not be incorporated by reference into this press release.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

MALVERN, Pa., Sept. 29, 2022 (GLOBE NEWSWIRE) — Ocugen, Inc. (“Ocugen” or the “Company”) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines, today announced that Dr. Shankar Musunuri, Chairman, Chief Executive Officer and Co-Founder of Ocugen, will participate in an in-person fireside chat at the Chardan 6th Annual Genetic Medicines Conference being held October 3-4, 2022 in New York, NY.

Details regarding Dr. Musunuri’s fireside chat are as follows:

Event: Chardan 6th Annual Genetic Medicines Conference Date: October 4, 2022 Time: 8:30 – 8:55 a.m. ET Location: Westin Grand Central Hotel Webcast: Live Fireside Chat

A live video webcast beginning at 8:30 a.m. ET on the day of the presentation will be available on the events page of the Ocugen investor site. The webcast replay will be archived for 90 days following the event.

About Ocugen, Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patient’s lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on Twitter and LinkedIn.

Cautionary Note on Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, which are subject to risks and uncertainties. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations. These and other risks and uncertainties are more fully described in our periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.

Contact: Tiffany Hamilton Head of Communications IR@ocugen.com

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Production surpassing expectations. InPlay announced production levels of 9,600 boe/d, a significant increase over 2022-2Q average of 9,063 BOE/d. Management now believes 2022 production will be at the upper half of a previously stated range of 9,150-9,400 BOE/d. so we are raising our production forecast to 9,400 BOE/d. In addition, two other wells will be brought to production in the next few days leading us to believe production will continue to grow into the fourth quarter.

Drilling success leads to more activity. The company is adding two Extended Reach Horizontal (ERH) wells in 2022. We suspect InPlay may be drilling ERH wells to forego building infrastructure. In addition to drilling longer well spurs, management announced that it is planning to move part of its 2023 drilling program into late 2022. InPlay is adding two horizontal wells in the Belly River where it has not drilled since 2016. Management believes utilizing the success it has found in the Cardium play (Pembina and Willesden Green) will translate into the Belly River.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q22 Results. Lifeway reported mixed results in its delayed filing for the second quarter of 2022. Revenue of $33.5 million was up 14.8% y-o-y, but fell short of our $34.5 million estimate. Strong expense control, however, resulted in net income of $120,000, or $0.01 per share, compared to our forecast of a net loss of $340,000, or a loss of $0.02 per share.

GM Still Pressured. Unfavorable milk pricing continued to negatively impact gross margin in 2Q22. Combined with increased pricing of freight costs and other costs, gross margin in 2Q22 fell to 17.0% from 26.3% in 2Q21. We expect continued pressure in milk pricing in 2H22.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Ocugen, Inc. is a biotechnology company focused on developing and commercializing novel gene therapies, biologicals, and vaccines. The lead product, Covaxin, is a killed-virus vaccine for COVID-19 in-licensed from Bharat Biotech (India). The lead product in its gene therapy program, OCU400, is in Phase 1/2 clinical trials for retinitis pigmentosa.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Vaccine For Protection and Prevention of Transmission. Ocugen has licensed a nasally administered COVID-19 vaccine from Washington University. Preclinical models show the vaccine produces a strong immune response in the tissues of the nasal passages and respiratory tract where the SARS-CoV-2 virus enters the body and first colonizes. This strong local immunity could potentially stop both infection and transmission. Ocugen plans to develop the vaccine as a “universal booster” for protection against current and future strains.

The Vaccine Has Been Licensed For Other Territories. Ocugen’s partner for Covaxin, Bharat Biotech (India), has also licensed the vaccine from Washington University and received Emergency Use authorization for India. We see this as positive sign for regulatory approval in the US and other territories. Ocugen plans to begin discussions with the FDA to determine the clinical requirements for approval.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

When Markets are Stormy, Remind Yourself of these Three Rules

Investing is necessary to help build for a future where inflation hasn’t eaten away at savings. But when the investment markets have been at their most difficult in years, most long-term investors have found their investment portfolios have gone into reverse. Many have then committed more cash to their eroding positions as the “buy the dip” thinking, up until recently, has, overall, worked out.

Whether by managing several billion for a large mutual fund or by keeping my household’s stock portfolio out of trouble, I’ve learned a lot. Most of what has been fruitful seems basic but is often forgotten when battling the markets. The information is easy to convey, the actions take discipline. Here are three key thoughts and actions to help you make decisions.

Know that There are Good and Bad Days

Do you fish? Most people understand fishing. You use past experience and current conditions to estimate (guess) what kind of fish might be biting. You then gather the right equipment and bring yourself to the place where you’re most likely to catch something worthwhile and at a time when the fish are most likely to satisfy your desire to catch them.

You choose the tackle that has been most productive for whatever you’re fishing for, get your lines in the water, and then sit patiently.

More often than not, when fishing, things don’t go as planned. The fish may not be as eager to get caught as you had hoped, or you might quickly catch as much as your freezer can hold, or the law allows. Sometimes a boat comes by and cuts your line. Stuff happens.

If the fish aren’t biting, you evaluate if waiting will yield more than fishing elsewhere. If they instead are biting like crazy, and there seems to be a storm approaching, it might be best to reduce your risk and head back before being caught in a storm. Often the best fishing is right before or after a storm, mid storm is a net negative and could be damaging.

Treat investing like fishing. Learn the best spots for the current conditions. This could be industry sectors, or segments based on market cap., within the categories, ask what companies have the highest probability of a positive outcome. Read up on the companies and see what professional analysts are saying about the financials, business model, management, and outlook. As with fishing, the old guy at the dock that has been fishing the area for years may steer you into (or out of) a boatload of success. Still, use your own judgment, and never act on a hot tip blindly.

Investing, like fishing, can be most successful before or after a storm. Taking positions in the middle is for thrill seekers, not investors.

Have a Plan

Seems simple enough. If you are fishing, you may schedule yourself for what time of day the fish are likely to be feeding, and if they aren’t, how long, you’ll wait before you try a different lure or a different location? You’re likely to have several hooks in the water at different depths and a plan to switch to whichever depth is getting the most action.

Moving to a different fishing spot when the one you’re at is still productive may seem unreasonable, but if other fishermen have moved to fish where you are, taking your current catch and moving to where you think you’ll do better can be smart.

As a portfolio manager, I held dozens of positions simultaneously, they all had a purpose. If I couldn’t say what the expectations were of any position, I got rid of it. Rolling the dice is expensive. My portfolio objective was to beat the benchmark and consistently be a top-five fund in the category. My plan to accomplish the objective was to have pre-assessed the possibilities before entering any position. I also told myself what I’d do when any of them occurred. In this way, I had a plan for most all scenarios.

The plan helped prevent me from ever trying to take more out of a trade than it is willing to give. It also forced me to never enter a position without having done my homework on the company and the environment in which the company operates.

Technology makes it easier than ever to do preliminary reading and research. Channelchek and other outlets for quality research, coupled with information and tools usually provided by your broker, means today’s retail investor has more than most professionals did in 2000.

Part of the plan should be when to do nothing. The top portfolio managers get paid quite well to do very little each day except monitoring positions in case something, based on their plan, happens. Don’t ever transact because you’re bored. Each position should have a purpose, if there is something else that is likely to better provide that purpose, no-cost trading makes it efficient to adjust your holdings. But if it is doing everything it should, doing nothing is often the best action. Sit on your hands.

Plan your trade, trade your plan, and get out when it is not the best commitment of your money.

Know What You Trade

I’m a student of and a participant in the markets, I suppose I’m also a teacher of sorts, but I never stop learning. This makes me a generalist in many categories, with above-average knowledge in a few. It’s important to know your investment realm. If your fishing is to stand waist deep in water with a flyrod catching more than anyone else on the river, it doesn’t mean you’d have the ability to go offshore and have any success. In fact, offshore, you’d probably throw up. Flyfishing and deep sea fishing are related but not the same. If you knowledgeably trade a few small-cap mining stocks and decide to one day buy TSLA or AAPL, your experience may not translate well. If either one dropped $50 a share, it might make you want to throw up.

Knowing different investment types and sectors better so you can focus on those you’re best suited to is, like everything else, education and experience.

Learn to decipher what is good information and what is mostly entertainment. Then immerse yourself. Don’t feel that you have to go where the crowd is. Social media has been powerful in getting us to follow the crowd, but defining the right or best thing for us is critical to any success. No one knows what you want more than you, no one knows what you can stomach better than you, and not everyone enjoys any type of fishing or any type of investing. For those people, there are food stores and wealth managers or funds.

Take Away

No matter the caliber of trader/investor, when markets are turbulent, it’s a good habit to refresh yourself on basics. These investing basics include you don’t always have to be in the market – you can expect to run into problem periods, it’s better to avoid these storms than have to rebuild afterward. Also, pre-thinking actions in an “if this, then that” format before even entering a position will prevent bigger problems and provide greater success. Decision-making while the market is either making you euphoric or the market is punching you in the face is the wrong time. Better decisions are made when thinking clearly. If you don’t think you enjoy investing, leave it to someone else, not everything is for everybody.

For those wishing to hone their expertise, try to learn about everything, but pick a few specialties. I know people that only trade the FAANG stocks and have superior performance. I know others that focus only on biotech and overtime have done well. Then there is the person that only invests in companies with products or services they themselves use, no matter what your focus is, read up on the company and understand how it trades and what its business is impacted by.

It’s a small world, and as we’ve seen, if something happens with one trading partner, it impacts them all.

Rapid moves and turnarounds in the U.S. Treasury market, considered the bedrock of all other markets, have increased the volatility in equity markets, commodities trading, and, more directly to, currency exchange rates across the globe. The uncertainty has caused investment capital to gravitate to U.S. markets; however, prolonged gyrations, especially in “risk-free” U.S. Treasuries, could put many investors on the sidelines and weaken asset prices globally.

The U.S./U.K. Example

At the end of 2021, the ten-year U.S. Treasury note was yielding 1.5%. Earlier this week a ten-year U.S. Treasury (backed by the same entity that backs the U.S. Currency) rose to yield 4%. That’s a 270% rise in the yield – for bondholders, prices of bonds decline as yields rise. So while the stock market frets over what a Federal Reserve increase in rates may do for equities, bond market investors can usually pull out a calculator and get a fairly precise answer as to how bonds will reprice. If the reaction is radically different, an important foundation is lost. The reaction has been unpredictable.

While the ten-year did hit 4% this week, after lingering around 3.50% the prior week, the yield abruptly dropped after news from across the Atlantic that England’s central bank, the Bank of England (BOE), was taking steps to halt rate increases, effectively implementing quantitative easing. The BOE buying bonds puts pound sterling into their economy and adds to inflation pressures. The immediate reaction was for rates to come down, there, in the U.S., and in other economies that have been tightening. This provided a feeling of relief from equity markets, as it was a sign that the central banks may one by one abandon their plans to fight inflation, choosing instead to fuel it.

The BOE’s move to buy bonds “on whatever scale is necessary” to stabilize its bond market, a move that followed large tax cuts last week by the U.K. government, despite double-digit inflation, many believe indicates a possible problem with a major financial institution or pension fund.

The world’s markets don’t trade in a vacuum. The sudden reversal in the U.K. to stop interest rate hikes and perhaps lower rates brought a positive tone to stocks and bonds in U.S. markets, each having historically challenging years. The conversation in the U.S. is that the Fed may have to pause its own aggressive direction. This would be either because increased rates would further strengthen the dollar, or because the U.S. may have its own underlying time bomb(s), institutions that would fail or bubbles that could burst.

The rallies in the U.S. stock and bond markets gained momentum after the BOE move as the Chicago Mercantile Exchange (CME) data showed reduced expectations of a terminal or neutral Fed Funds rate of 5%, with expectations now for the policy rate to top out around 4.25-4.5%.

Take Away

While the Fed taking its foot off the brake pedal would be a remarkable turnaround after Chairman Powell’s efforts to be clear about his intent to tighten, the reasons for the CME data shift are twofold. First, the Fed won’t be able to keep aggressively raising rates ad simultaneously reducing bond holdings (shrink its balance sheet), because the strong U.S. dollar is disrupting global markets. Secondly, as mentioned before, checking the health of major institutions, housing, and pension funds in the U.S. may be prudent before administering more economic medicine.

Uncertainty has the effect of investors pulling assets out of markets and businesses acting with more caution. Hopefully, clarity, one way or the other, soon presents itself so volatility is reduced and investors can better understand the playing field.

VANCOUVER, British Columbia, Sept. 28, 2022 (GLOBE NEWSWIRE) — Permex Petroleum Corporation (CSE: OIL) (OTCQB: OILCF) (FSE: 75P) (“Permex” or the “Company“), a junior oil and gas company, is pleased to announce that the Company has started drilling on its Breedlove Field Prospect located in Martin County, Texas.

The PPC Eoff #3 well, operated by Permex Petroleum, is the first well to be drilled on the 7,780 gross acre Breedlove oil field. Two initial wells have been permitted and are expected to be drilled and completed on the property in the short term.

Permex Petroleum President and CEO Mehran Ehsan stated, “This makes for a transformative step towards the Company’s next phase of growth and scalability. We are excited to not only have started the drilling program, but to aggressively take advantage of the current high price environment and move the Company towards a cash-flow positive position.”

Drilling of the first well commenced on Wednesday, September 14, 2022, with a possible lateral conversion to follow upon successful mud logging and various zone tests. The drilling and completion of the vertical well will take approximately 60 days and for the horizontal well 90 days.

About Permex Petroleum Corporation

Permex Petroleum (CSE: OIL) (OTCQB: OILCF) (FSE: 75P) is a uniquely positioned junior oil & gas company with assets and operations across the Permian Basin of West Texas and the Delaware Sub-Basin of New Mexico. The Company focuses on combining its low-cost development of Held by Production assets for sustainable growth with its current and future Blue-Sky projects for scale growth. The Company, through its wholly owned subsidiary, Permex Petroleum US Corporation, is a licensed operator in both states, and owns and operates on private, state and federal land. For more information, please visit www.permexpetroleum.com.

CAUTIONARY DISCLAIMER STATEMENT:

The Canadian Securities Exchange has neither approved nor disapproved the contents of this press release.

Forward-Looking Statements

This news release includes certain statements and information that may constitute forward-looking information within the meaning of applicable Canadian securities laws. Forward-looking statements relate to future events or future performance and reflect the expectations or beliefs of management of the Company regarding future events. Generally, forward-looking statements and information can be identified by the use of forward-looking terminology such as “intends”, “expects” or “anticipates”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “should”, “would” or will “potentially” or “likely” occur. This information and these statements, referred to herein as “forward‐looking statements”, are not historical facts, are made as of the date of this news release and include without limitation, statements regarding Permex’s expectations of entering into a growth phase in relation to its business and drilling programs; the market opportunity in the oil and gas industry; Permex’s future plans to bring additional shut-in wells online, and the deployment of the Company’s capital.

In addition, forward-looking statements or information are based on a number of material factors, expectations or assumptions of Permex which have been used to develop such statements and information but which may prove to be incorrect. Although Permex believes that the expectations reflected in such forward-looking statements or information are reasonable, undue reliance should not be placed on forward-looking statements because Permex can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: that Permex will continue to conduct its operations in a manner consistent with past operations; continued performance from existing wells; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Permex’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Permex’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Permex operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Permex to obtain qualified staff, equipment and services in a timely and cost efficient manner; the ability of Permex to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Permex operates; and the ability of Permex to successfully market its oil and natural gas products.

Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements and information. Readers are cautioned that reliance on such information may not be appropriate for other purposes. The Company does not undertake to update any forward-looking statement, forward-looking information or financial outlook that are incorporated by reference herein, except in accordance with applicable securities laws. We seek safe harbor.

Grand Opening Event Scheduled for Saturday, October 8th; Major Expansion of R.Greenleaf Retail Banner Begins

DENVER, Sept. 28, 2022 /PRNewswire/ – Schwazze, (OTCQX: SHWZ) (NEO: SHWZ) (“Schwazze” or the “Company”), a premier vertically integrated, multi-state operating cannabis company with assets in Colorado and New Mexico, announces the grand opening of its adult-use dispensary, R.Greenleaf, located in the heart of Ruidoso, New Mexico. The new store, located at 360 Sudderth Drive in Ruidoso, officially opened its doors for business at 12p on Saturday, September 24th. Normal store operating hours are 10a to 9p Monday through Saturday; 10a to 8p on Sunday.

This store opening kicks off Schwazze’s deliberate expansion throughout the state of New Mexico. This new store in Ruidoso brings R.Greenleaf’s number of New Mexico retail dispensaries to 11. All locations serve the needs of medical patients as well as recreational adult-use consumers.

“Schwazze is excited to add to our retail footprint in New Mexico with our latest store opening in Ruidoso. Our team is thrilled to be opening our first new store since adult recreational cannabis was legalized in New Mexico on April 1st,” said Steve Pear, New Mexico Division President for Schwazze. “We feel honored to service the Ruidoso community with top-notch, knowledgeable staff and a wide variety of quality products.”

Grand opening product specials and promotions are already in full swing with multiple flower pack offers, pre-rolls, gummies, chocolates and distillate vaporizer cartridges. Bundled kits or cannabis product starter packs will be offered for sale as well to provide patients and recreational customers a variety of product forms and consumption methods based on individual needs and preferences.

A grand opening celebration will be held on Saturday, October 8th beginning at 10a and running until 3p. Swag bags containing limited edition holographic stickers, t-shirts and beanies will be available while supplies last. Music will accompany a food truck offering free burritos and tacos to the first 75 customers making a purchase.

Ruidoso Store Location

R.Greenleaf 360 Sudderth Dr. Ruidoso, New Mexico 88345

Grand Opening Celebration

Saturday, October 8th 10a to 3p

Since April 2020, Schwazze has acquired, opened or announced the planned acquisition of 36 cannabis retail dispensaries as well as seven cultivation facilities and two manufacturing plants in Colorado and New Mexico. In May 2021, Schwazze announced its Biosciences division and in August 2021 it commenced home delivery services in Colorado.

About Schwazze

Schwazze (OTCQX: SHWZ NEO: SHWZ) is building a premier vertically integrated regional cannabis company with assets in Colorado and New Mexico and will continue to take its operating system to other states where it can develop a differentiated regional leadership position. Schwazze is the parent company of a portfolio of leading cannabis businesses and brands spanning seed to sale. The Company is committed to unlocking the full potential of the cannabis plant to improve the human condition. Schwazze is anchored by a high-performance culture that combines customer-centric thinking and data science to test, measure, and drive decisions and outcomes. The Company’s leadership team has deep expertise in retailing, wholesaling, and building consumer brands at Fortune 500 companies as well as in the cannabis sector. Schwazze is passionate about making a difference in our communities, promoting diversity and inclusion, and doing our part to incorporate climate-conscious best practices.

Medicine Man Technologies, Inc. was Schwazze’s former operating trade name. The corporate entity continues to be named Medicine Man Technologies, Inc. Schwazze derives its name from the pruning technique of a cannabis plant to enhance plant structure and promote healthy growth.

Forward-Looking Statements

This press release contains “forward-looking statements.” Such statements may be preceded by the words “plan,” “will,” “may,” “continue,” “predicts,” or similar words. Forward-looking statements are not guarantees of future events or performance, are based on certain assumptions, and are subject to various known and unknown risks and uncertainties, many of which are beyond the Company’s control and cannot be predicted or quantified. Consequently, actual events and results may differ materially from those expressed or implied by such forward-looking statements. Such risks and uncertainties include, without limitation, risks and uncertainties associated with (i) our inability to manufacture our products and product candidates on a commercial scale on our own or in collaboration with third parties; (ii) difficulties in obtaining financing on commercially reasonable terms; (iii) changes in the size and nature of our competition; (iv) loss of one or more key executives or scientists; (v) difficulties in securing regulatory approval to market our products and product candidates; (vi) our ability to successfully execute our growth strategy in Colorado and outside the state, (vii) our ability to consummate the acquisition described in this press release or to identify and consummate future acquisitions that meet our criteria, (viii) our ability to successfully integrate acquired businesses, including the acquisition described in this press release, and realize synergies therefrom, (ix) the ongoing COVID-19 pandemic, * the timing and extent of governmental stimulus programs, and (xi) the uncertainty in the application of federal, state and local laws to our business, and any changes in such laws. More detailed information about the Company and the risk factors that may affect the realization of forward-looking statements is set forth in the Company’s filings with the Securities and Exchange Commission (SEC), including the Company’s Annual Report on Form 10-K and its Quarterly Reports on Form 10-Q. Investors and security holders are urged to read these documents free of charge on the SEC’s website at http://www.sec.gov. The Company assumes no obligation to publicly update or revise its forward-looking statements as a result of new information, future events or otherwise except as required by law.

CALGARY, Alberta, Sept. 28, 2022 (GLOBE NEWSWIRE) — InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to announce an operations update and a long-term forecast through 2025.

Operations Update

InPlay is currently producing at record production levels of 9,600 boe/d(2) (57% light oil and NGLs) based on field estimates. In Willesden Green, three (2.9 net) Extended Reach Horizontal (“ERH”) wells were brought on production approximately ten days ago and an additional two (1.9 net) ERH wells will be brought on production in the next few days. These wells are currently in the early clean-up stage and should achieve peak production over the next 30 to 60 days. The Company’s current plans from our original capital program is to drill one (0.95 net) additional two-mile well in Willesden Green.

Given the strong operational results in 2022 to date, InPlay expects to be in the upper half of our full year 2022 production guidance which equates to 9,150 to 9,400 boe/d(2). This forecast is estimated to deliver production growth of 28% to 31% on a per share basis (83% to 92% on a debt adjusted per share basis (1)) which is expected to be top-tier amongst light oil peers.

InPlay has elected to drill additional extended reach wells in 2022 (and fewer one-mile wells) than originally planned, including two two-mile ERH wells which achieved exceptional efficient drill times. The Company is also expecting increased industry activity levels in the first quarter of 2023. With our strong balance sheet, InPlay plans to take advantage of utilizing our preferred contractors and is now tactically planning to start 2023 expenditures in late 2022 by initiating preliminary construction work and adding two horizontal (2.0 net) Belly River light oil wells to the 2022 capital program. These wells are expected to be brought on production late in the fourth quarter positioning the Company for significant production increases in 2023. The Belly River is a producing play which we have not drilled in since 2016 and plans are to utilize the technologies and expertise developed in our Cardium play over the years. These wells have a high light oil weighting (approximately 90% – 95% light oil) that receives a premium to our benchmark Mixed Sweet Blend (“MSW”) pricing. The Company also plans to invest in environmental initiatives by constructing a third vapour recovery unit for additional emission conservation. As a result, the Board of Directors have approved an increased 2022 development capital budget of $70 to $72 million.

Outlook and Long-Term Forecast (3)

InPlay is continuously evaluating market conditions including current recession concerns in order to maximize shareholder returns. Even with the current volatility, commodity prices continue to remain historically strong in part due to the weak Canadian dollar, resulting in high rates of return on capital investment and short payout periods. It is InPlay’s belief that long-term commodity pricing will remain strong due to the lack of industry wide capital spending over recent years, restrictive government regulations and mandates and unstable global geopolitics leading to a multi-year bull cycle in crude oil prices. The Company is continuing to rapidly pay down debt and is in the best operational and financial position in our history while remaining focused on our disciplined strategy.

InPlay is pleased to provide a forecast to the end of 2025. The Company’s strategy is to continue to provide top-tier light-oil weighted growth, maintaining a strong financial position while providing significant FAFF and sustainable returns to shareholders. Our strategy is to provide organic production growth in a range of 6% – 10%. At a WTI price of US $80/bbl or better, we target 10% production growth and with WTI pricing of approximately US $60/bbl, production growth of 6% is targeted. This is demonstrated in our forecast to 2025 which would provide a meaningful return to shareholders.

The table below outlines the highlights of the four year forecast based on the following WTI pricing scenarios:

2022

2023

2024

2025

WTI (US$/bbl)

93.25

75.00

70.00

65.00

Production (boe/d)(2)

9,150 – 9,400

9,900 – 10,400

10,650 – 11,200

11,300 – 11,900

Capital ($ millions)

70 – 72

69 – 71

75 – 77

80 – 82

Net wells

17.5

17.5 – 18.5

18.5 – 19.5

21.0 – 22.0

DAPPS Growth (%)(1) *

83 – 92

46 – 59

40 – 45

30 – 35

AFF ($ millions)(4)

139 – 143

134 – 140

136 – 142

133 – 139

FAFF ($ millions)(1)

67 – 73

63 – 71

59 – 67

51 – 59

Working Capital (Net Debt) at Year-end ($ millions)(4)

(12) – (16)

43 – 50

97 – 103

141 – 147

Annual Net Debt / EBITDA(1)

0.1 – 0.2

(0.3) – (0.4)

(0.7) – (0.8)

(1.0) – (1.1)

EV / DAAFF(1)*

1.5 – 1.6

1.2 – 1.3

0.8 – 0.9

0.5 – 0.6

* Assumes a $2.50 share price

This forecast shows the high quality deliverability and return of our assets evidencing the sustainability of the Company with increasing positive working capital and minimal leverage.

Return of Shareholder Capital

InPlay’s trailing 12 month net debt to earnings before interest, taxes and depletion (“EBITDA”) ratio was less than 0.5 times at the end of the second quarter and is forecast to be 0.1 – 0.2 times at the end of 2022. With this threshold achieved, in addition to the continued generation of FAFF, elimination of debt and generation of positive working capital forecasted through to 2025, the Company is committed towards providing a return of capital to shareholders. The Company believes that our share price is currently significantly undervalued and the prudent first step in enhancing returns to shareholders is a share buyback program which the Company’s Board of Director’s has approved for implementation and will be subject to regulatory approval. With this in place the Company will be able to acquire common shares at opportunistic times and share prices.

As outlined above in the long term forecast, the Company is forecasting to generate material FAFF resulting in a growing positive working capital balance through to 2025. Our strategy for the accumulating additional FAFF is to provide returns to shareholders through potential share buybacks, dividends, increased tactical capital investment and accretive strategic acquisitions.

Given the significant volatility in both commodity prices and market conditions experienced in recent weeks, the Company and its Board of Directors will continue to monitor and evaluate the timing and implementation of additional returns to shareholders.

The Company has been disciplined in maintaining operational flexibility by quickly adapting to changing market conditions and commodity price fluctuations in making business decisions. This same prudent approach is currently being followed. Management would like to thank our employees, board members, lenders and shareholders for their support and we look forward to continuing our journey of deleveraging and delivering strong returns to shareholders in a sustainable, prudent and responsible manner.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

Non-GAAP financial measure or ratio that does not have a standardized meaning under International Financial Reporting Standards (IFRS) and GAAP and therefore may not be comparable with the calculations of similar measures for other companies. Please refer to “Non-GAAP and Other Financial Measures” contained within this press release.

See “Production Breakdown by Product Type” at the end of this press release.

See “Reader Advisories – Forward Looking Information and Statements” for full details and key budget and underlying assumptions related to our 2022 capital program and associated guidance and long-term forecast.

Capital management measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

Reader Advisories

Non-GAAP and Other Financial Measures

Throughout this press release and other materials disclosed by the Company, InPlay uses certain measures to analyze financial performance, financial position and cash flow. These non-GAAP and other financial measures do not have any standardized meaning prescribed under GAAP and therefore may not be comparable to similar measures presented by other entities. The non-GAAP and other financial measures should not be considered alternatives to, or more meaningful than, financial measures that are determined in accordance with GAAP as indicators of the Company performance. Management believes that the presentation of these non-GAAP and other financial measures provides useful information to shareholders and investors in understanding and evaluating the Company’s ongoing operating performance, and the measures provide increased transparency and the ability to better analyze InPlay’s business performance against prior periods on a comparable basis.

Non-GAAP Financial Measures and Ratios

Included in this document are references to the terms “free adjusted funds flow (“FAFF”)”, “Net Debt to EBITDA”, “Production per debt adjusted share (“DAPPS”)” and “EV / DAAFF”. Management believes these measures and ratios are helpful supplementary measures of financial and operating performance and provide users with similar, but potentially not comparable, information that is commonly used by other oil and natural gas companies. These terms do not have any standardized meaning prescribed by GAAP and should not be considered an alternative to, or more meaningful than “profit (loss) before taxes”, “profit (loss) and comprehensive income (loss)”, “adjusted funds flow”, “capital expenditures”, “corporate acquisitions, net of cash acquired”, “working capital (net debt)”, “weighted average number of common shares (basic)” or assets and liabilities as determined in accordance with GAAP as a measure of the Company’s performance and financial position.

Free Adjusted Funds Flow (“FAFF”)

Management considers FAFF per share important measures to identify the Company’s ability to improve its financial condition through debt repayment, which has become more important recently with the introduction of second lien lenders, on an absolute and weighted average per share basis. FAFF should not be considered as an alternative to or more meaningful than AFF as determined in accordance with GAAP as an indicator of the Company’s performance. FAFF is calculated by the Company as AFF less exploration and development capital expenditures and property dispositions (acquisitions) and is a measure of the cashflow remaining after capital expenditures before corporate acquisitions that can be used for additional capital activity, corporate acquisitions, and repayment of debt or decommissioning expenditures or potentially return of capital to shareholders. FAFF per share is calculated by the Company as FAFF divided by weighted average outstanding shares. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast FAFF.

Net Debt to EBITDA

Management considers Net Debt to EBITDA an important measure as it is a key metric to identify the Company’s ability to fund financing expenses, net debt reductions and other obligations. EBITDA is calculated by the Company as adjusted funds flow before interest expense. When this measure is presented quarterly, EBITDA is annualized by multiplying by four. When this measure is presented on a trailing twelve month basis, EBITDA for the twelve months preceding the Net Debt date is used in the calculation. This measure is consistent with the EBITDA formula prescribed under the Company’s Senior Credit Facility. Net Debt to EBITDA is calculated as Net Debt divided by EBITDA. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast Net Debt to EBITDA.

Production per Debt Adjusted Share

InPlay uses “Production per debt adjusted share” as a key performance indicator. Debt adjusted shares should not be considered as an alternative to or more meaningful than common shares as determined in accordance with GAAP as an indicator of the Company’s performance. Debt adjusted shares is a non-GAAP measure used in the calculation of Production per debt adjusted share and is calculated by the Company as common shares outstanding plus the change in working capital (net debt) divided by the Company’s current trading price on the TSX, converting working capital (net debt) to equity. Debt adjusted shares should not be considered as an alternative to or more meaningful than weighted average number of common shares (basic) as determined in accordance with GAAP as an indicator of the Company’s performance. Management considers Debt adjusted share is a key performance indicator as it adjusts for the effects of capital structure in relation to the Company’s peers. Production per debt adjusted share is calculated by the Company as production divided by debt adjusted shares. Management considers Production per debt adjusted share is a key performance indicator as it adjusts for the effects of changes in annual production in relation to the Company’s capital structure. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast production per debt adjusted share.

EV / DAAFF

InPlay uses “enterprise value to debt adjusted AFF” or “EV/DAAFF” as a key performance indicator. EV/DAAFF is calculated by the Company as enterprise value divided by debt adjusted AFF for the relevant period. Debt adjusted AFF (“DAAFF”) is calculated by the Company as adjusted funds flow plus financing costs. Enterprise value is a capital management measures that is used in the calculation of EV/DAAFF. Enterprise value is calculated as the Company’s market capitalization plus working capital (net debt). Management considers enterprise value a key performance indicator as it identifies the total capital structure of the Company. Management considers EV/DAAFF a key performance indicator as it is a key metric used to evaluate the sustainability of the Company relative to other companies while incorporating the impact of differing capital structures. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast EV/DAAFF.

Capital Management Measures

Adjusted Funds Flow

Management considers adjusted funds flow to be an important measure of InPlay’s ability to generate the funds necessary to finance capital expenditures. Adjusted funds flow (“AFF”) is a GAAP measure and is disclosed in the notes to the Company’s consolidated financial statements for the year ending December 31, 2021 and the most recently filed quarterly financial statements. All references to AFF throughout this document are calculated as funds flow adjusting for decommissioning expenditures and transaction and integration costs. This item is adjusted from funds flow as decommissioning expenditures are incurred on a discretionary and irregular basis and are primarily incurred on previous operating assets and transaction costs are non-recurring costs for the purposes of an acquisition, making the exclusion of these items relevant in Management’s view to the reader in the evaluation of InPlay’s operating performance. The Company also presents AFF per share whereby per share amounts are calculated using weighted average shares outstanding consistent with the calculation of profit (loss) per common share.

Working Capital (Net Debt)

Working capital (Net Debt) is a GAAP measure and is disclosed in the notes to the Company’s consolidated financial statements for the year ending December 31, 2021 and the most recently filed quarterly financial statements. The Company closely monitors its capital structure with a goal of maintaining a strong balance sheet to fund the future growth of the Company. The Company monitors working capital (net debt) as part of its capital structure. The Company uses working capital (net debt) (bank debt plus accounts payable and accrued liabilities less accounts receivables and accrued receivables, prepaid expenses and deposits and inventory) as an alternative measure of outstanding debt. Management considers working capital (net debt) an important measure to assist in assessing the liquidity of the Company.

Forward-Looking Information and Statements

This news release contains certain forward–looking information and statements within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”, “may”, “will”, “project”, “should”, “believe”, “plans”, “intends”, “forecast”, “targets”, “framework” and similar expressions are intended to identify forward-looking information or statements. In particular, but without limiting the foregoing, this news release contains forward looking information and statements pertaining to the following: the Company’s planned 2022 capital program including wells to be drilled and completed and the timing of the same; 2022 guidance based on the planned capital program including forecasts of 2022 annual average production levels, debt adjusted production levels, adjusted funds flow, free adjusted funds flow, Net Debt/EBITDA ratio, and growth rates; the Company’s long-term forecast including wells to be drilled and completed and the timing of the same; production estimates based on the planned capital program including forecasts of annual average production levels, debt adjusted production levels, adjusted funds flow, free adjusted funds flow, working capital, Net Debt/EBITDA ratio, EV/DAAFF and growth rates; light oil and liquids weighting estimates; the expectation that the Company will be in the upper half of our full year 2022 production guidance; the expectation of high industry activity levels in the first quarter of 2023; the expectation that the Belly River wells will significantly reduce operating expenses in the field; the Company’s business strategy, milestones and objectives including, without limitation, the anticipated continuation of debt reduction throughout the year; the expectation that the Company will generate strong FAFF through 2025; expectations regarding the use of additional FAFF; expectations regarding the Company’s share buyback program, including the timing of the same; expectations regarding future commodity prices including InPlay’s belief that strong commodity pricing will remain leading to a multi-year crude bull cycle in crude oil prices; future oil and natural gas prices; future liquidity and financial capacity; future results from operations and operating metrics; future costs, expenses and royalty rates; future interest costs; the exchange rate between the $US and $Cdn; future development, exploration, acquisition, development and infrastructure activities and related capital expenditures, including our planned 2022 capital program and associated guidance.

Without limitation of the foregoing, readers are cautioned that the Company’s return to shareholders framework including a share buyback program and future dividend payments to shareholders of the Company, if any, and the level thereof remains uncertain and accordingly management’s expectations related thereto should not be unduly relied upon. The Company’s share buyback program, if any, dividend policy and funds available for the repurchase of shares or payment of dividends, if any, from time to time, is dependent upon, among other things, levels of FAFF, leverage ratios, financial requirements for the Company’s operations and execution of its growth strategy, fluctuations in commodity prices and working capital, the timing and amount of capital expenditures, credit facility availability and limitations on distributions existing thereunder, and other factors beyond the Company’s control. Further, the ability of the Company to implement a return to shareholder program will be subject to applicable laws, including, but not limited to, satisfaction of solvency tests under the ABCA, approval of the Toronto Stock Exchange (“TSX”) and satisfaction of certain applicable contractual restrictions contained in the agreements governing the Company’s outstanding indebtedness.