SANTA MONICA, Calif.–(BUSINESS WIRE)– Entravision (NYSE: EVC), a leading global advertising solutions, media and technology company, today announced Chris Young, Chief Financial Officer and Treasurer, will present at the 2022 Southwest IDEAS Investor Conference to be held November 16-17, 2022 in Dallas, Texas. Management is scheduled to present on Wednesday, November 16th at 11:00 am CT.

The presentation will be webcast live over the Internet, and links to the live webcast and replay will be available on Entravision’s Investor Relations website at investor.entravision.com.

About Entravision Communications Corporation

Entravision is a leading global advertising, media and ad-tech solutions company connecting brands to consumers by representing top platforms and publishers. Our dynamic portfolio includes digital, television and audio offerings. Digital, our largest revenue segment, is comprised of four business units: our digital sales representation business; Smadex, our programmatic ad purchasing platform; our branding and mobile performance solutions business; and our digital audio business. Through our digital sales representation business, we connect global media companies such as Meta, Twitter, TikTok and Spotify with advertisers in primarily emerging growth markets worldwide. Smadex is our mobile-first demand side platform, enabling advertisers to execute performance campaigns using machine learning. We also offer a branding and mobile performance solutions business, which provides managed services to advertisers looking to connect with global consumers, primarily on mobile devices, and our digital audio business provides digital audio advertising solutions for advertisers in the Americas. In addition to digital, Entravision has 49 television stations and is the largest affiliate group of the Univision and UniMás television networks. Entravision also manages 45 primarily Spanish-language radio stations that feature nationally recognized, Emmy award-winning talent. Shares of Entravision Class A Common Stock trade on the NYSE under ticker: EVC. Learn more about our offerings at entravision.com or connect with us on LinkedIn and Facebook.

LOS ANGELES, Nov. 10, 2022 (GLOBE NEWSWIRE) — FAT(Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT), a leading global franchising company and parent company of iconic brands including Round Table Pizza, Fatburger, Johnny Rockets, Twin Peaks, Fazoli’s and 12 other restaurant concepts, today announced their participation in Sequire’s Virtual Restaurants & Foodservice Conference, which will take place on Nov. 17, 2022. Andy Wiederhorn, President and CEO, will be presenting at 11:00 a.m. ET.

Summary of SequireRestaurants & Foodservice Conference

The restaurant & foodservice industry has flourished for years, forecasting to reach $898 billion in sales this year. This one-day virtual investor event, highlighting public companies in the restaurant and foodservice sector, will be held via SRAX’s Sequire Virtual Events platform. Thousands of active small-cap investors have been invited to the event, which will feature several restaurant and foodservice focused companies hosting 25-minute presentations, alongside keynotes highlighting prominent names in this space.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

Advice is Plentiful on When to Buy Stocks, But When Should You Sell?

During the fourth quarter of 2022, stocks have climbed dramatically. The Russell 2000 small cap index is up double-digits in percentage, and the S&P 500 is approaching a ten percent increase. This is a welcome run-up over such a short period of time. The sudden move has investors, some of whom still hold paper losses, asking themselves, do I sell now, do I add to my positions, or should I sit tight and wait?

Information on when to buy into a position is abundant. Advice on when to decide your assets are better off elsewhere is much less available. There is just less demand from readers on the topic.

Selling Considerations

First off, one does need to consider their financial plan. Is this money that is needed within the next few months, or can the value of the position or positions change without much impact on future plans? Also, is there a better use for the proceeds? If the position one is holding is still the best use of funds, then the answer, net of any emotions, may be to hold.And emotions can make for bad decisions.

Some investors that were about to pull the trigger on the sale of a position weeks ago when stocks were falling may find their position has regained much of the loss, but now they are back in greedy mode, hoping for more, despite being able to get more.

Let’s take a level-headed look at the factors involved in making the decision regarding selling.

Opportunity Cost

One fundamental question should ask themselves regularly is, do I think the risk-reward of each position and all positions taken together are best for the portfolio? If not, depending on tax consequences, if it’s determined that other opportunities might perform better, then it should be of little concern if the stock is up or down from where it was purchased. In fact, depending on what kind of investor you are, it may make sense to lighten up with the plan to re-evaluate if prices fall again.

One way to get a handle on this is to determine, does the stock underperform in a rising market. Does it fall at a faster pace than the market when the market is falling? The answers to these questions can help identify if the position should be cut loose and may be replaced by a better performer.

Moving Averages

Investors can look to moving averages for a hint as to whether the position might be overbought or oversold. Which moving average you use should be based on the expected holding period and also what works best for the stock you are reviewing. For a seldom traded portfolio with longer-term positions, its common to use a 200-day moving average, but depending on the stock’s past performance, the investor may wish to overlay different averages to guide their thoughts on whether the stock might give back recent gains and fall back in line with past performance.

Time Horizon

Many investors skip the step of determining the expected holding period before a purchase of an investment. This is like leaving for a trip without any directions to get you started. If you didn’t do this before your purchase, do it now. Ask, when do you think this will pay-off, what is the anticipated pay-off, and how do I identify if something has changed and the holding period should change? Investors with a long-term time horizon could find that over the years, they can avoid missing the up periods if they don’t get too intent on missing down periods. If your holdings closely follow the S&P 500 index, it may be down 18% this year, but last year it was up nearly 27%, and that could be a compounded increase from the 16% it was up the prior year.

If instead, your holding period is short, you may know within weeks, days, or minutes if you met your goal or if it is not playing out as expected. At that point, if you would not enter the position (whether you made money or not), getting out may be wise. Smart traders know that if they don’t stick to their plan, even if rewarded, they might be reinforcing a bad behavior that will cost them down the road.

Other Considerations

A large percentage of portfolios managed by self-directed investors are qualified accounts; that is, they are tax-deferred, so any gain does not cost the account holder until funds are taken from the account. This largely takes the tax impact question out of the decision to sell or not. However, if it is a taxable portfolio, it’s important to consider whether the tax consequences and the sale are still worthwhile. In some cases selling at a loss may even help offset gains in some other area of the portfolio owner’s financial condition.

It’s wise to consult a tax professional to review your specific financial and tax situation before selling a stock or investment for tax purposes.

If you have made a mistake and purchased the wrong ticker, it isn’t likely the shares fit your parameters and the best time to sell is usually immediately.

Change in Ownership

Sometimes it may make sense to sell a company if it has been acquired or merges with another company. Often before an event like this, the stock price rises well above the overall market movement. The question once again is, is this the best use of one’s investible assets? The new fundamentals and cost-saving synergies between the two companies may place it in a more competitive or more profitable position, in this case, not taking the sudden profit could pay off long term.

Selling a Portion

Did the stock you are holding just shoot up 5%-10%, and you think it is likely to back-off but don’t want to miss out if the euphoria surrounding it continues? Why not make selling a portion, perhaps with the idea that you will re-enter for that portion if the price does drop? In this way, you stand the chance of capturing some of the original run-up, and while you may miss further upward momentum, you have left yourself the opportunity of buying the shares back at a lower price from which they were sold.

Take Away

The decision on whether or not to sell an investment should be held up against the plan you had when you purchased it. Far too many investors make sensible plans entering a trade, but once in and it is either rising or falling, a less sensible side often takes over. Fear and greed are powerful emotions that can undo a good strategy.

DALLAS, Nov. 10, 2022 (GLOBE NEWSWIRE) — Permex Petroleum Corporation (CSE: OIL) (OTCQB: OILCD) (FSE: 75P) (“Permex” or the “Company”), an independent energy company engaged in the acquisition, exploration, development and production of oil and natural gas properties on private, state and federal land in the United States, today announced that it has received approval to uplist its common shares and list its warrants on the NYSE American in connection with an underwritten public offering of its common shares (or common share equivalents) and warrants to purchase common shares. Trading of the Company’s common shares and warrants is expected to commence on the NYSE at the opening of trading on November 15, 2022 under the ticker symbols “OILS” and “OILSW,” respectively. Permex’s listing is subject to meeting all NYSE American requirements at the time of listing. Trading on the OTCQB will cease concurrent with the NYSE American listing.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy these securities, nor shall there be any sale of these securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction.

About Permex Petroleum Corporation

Permex Petroleum is a uniquely positioned junior oil and gas company with assets and operations across the Permian Basin of West Texas and the Delaware Sub-Basin of New Mexico. The Company focuses on combining its low-cost development of Held by Production assets for sustainable growth with its current and future Blue-Sky projects for scale growth. The Company, through its wholly-owned subsidiary, Permex Petroleum US Corporation, is a licensed operator in both states, and owns and operates on private, state and federal land. For more information, please visit www.permexpetroleum.com.

FORWARD-LOOKING STATEMENTS

Statements in this press release may constitute forward-looking statements for the purposes of the safe harbor provisions under the Private Securities Litigation Reform Act of 1995 and other federal securities laws. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of management, are not guarantees of performance and are subject to significant risks and uncertainty. These forward- looking statements should, therefore, be considered in light of various important factors, including those set forth in Company’s reports that it files from time to time with the U.S. Securities and Exchange Commission and the Canadian securities regulators which you should review. When used in this press release, words such as “will,” “could,” “plan,” “estimate”, “expect”, “intend”, “may”, “potential”, “believe”, “should” and similar expressions, are forward-looking statements. Forward-looking statements may include, without limitation, statements relating to the Company’s listing on NYSE American, financial condition and operating results, legal, economic, business, competitive and/or regulatory factors affecting Permex’s businesses and any other statements regarding events or developments Permex believes or anticipates will or may occur in the future. These forward-looking statements should not be relied upon as predictions of future events, and the Company cannot assure you that the events or circumstances discussed or reflected in these statements will be achieved or will occur. If such forward-looking statements prove to be inaccurate, the inaccuracy may be material. You should not regard these statements as a representation or warranty by the Company or any other person that it will achieve its objectives and plans in any specified timeframe, or at all. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release. The Company disclaims any obligation to publicly update or release any revisions to these forward- looking statements, whether as a result of new information, future events or otherwise, after the date of this news release or to reflect the occurrence of unanticipated events, except as required by law.

PHOENIX, Nov. 10, 2022 (GLOBE NEWSWIRE) — QuoteMedia, Inc. (OTCQB: QMCI), a leading provider of market data and financial applications, announced financial results for the quarter ended September 30, 2022.

QuoteMedia provides banks, brokerage firms, private equity firms, financial planners and sophisticated investors with a more economical, higher quality alternative source of stock market data and related research information. We compete with several larger legacy organizations and a modest community of other smaller companies. QuoteMedia provides comprehensive market data services, including streaming data feeds, on-demand request-based data (XML/JSON), web content solutions (financial content for website integration) and applications such as Quotestream Professional and Quotestream Web Trader.

Highlights for Q3 2022 include the following:

Quarterly revenue increased to $4,390,667 in Q3 2022 from $3,818,713 in Q3 2021, an increase of $571,954 (15%).

Gross Margin percentage improved to 52% in Q3 2022, compared to 47% in Q3 2021.

Net income for Q3 2022 was $309,543 compared to $154,931 in Q3 2021, an increase of $154,612.

Adjusted EBITDA for Q3 2022 was $670,145 compared to $539,534 in Q3 2021, an improvement of $130,611.

“We are very pleased with what we accomplished this quarter, and over the year to date,” said Robert J. Thompson, Chairman of the Board. “We have closed several major agreements with high profile clients including two of Canada’s largest banks, with the second contract commencing in November 2022. We achieved record profits this quarter, and we expect to improve upon this moving forward. We anticipate that the pace of our revenue growth will continue in the coming quarters, with the launch of more enterprise deployments and exciting partnerships.

“We have made extensive time and financial investments into operations and infrastructure improvements this year, to ensure we are able to provide the highest levels of service, support and security for our clients, and we expect that these investments will yield dividends in the months and years to come.

“Due to the significant devaluation of the Canadian dollar, we are revising our revenue growth projection for the 2022 year. A substantial number of our contracts (and new contracts) are denominated in Canadian dollars, and this is re-measured into US Dollars when reporting our financial results. We are now projecting a 16% revenue growth for 2022, down from 19%. This will not have a meaningful impact on our bottom-line profitability, as our Canadian dollar revenue and expenses are almost equal. In fact, we anticipate significantly increased profitability in upcoming quarters.”

QuoteMedia will host a conference call Thursday, November 10, 2022 at 2:00 PM Eastern Time to discuss the Q3 2022 financial results and provide a business update.

Conference Call Details:

Date: November 10, 2022

Time: 2:00 PM Eastern

Dial-in number: 800 445-7795; 203-518-9843

Conference ID: QUOTEMEDIA

An audio rebroadcast of the call will be available later at: www.quotemedia.com

About QuoteMedia

QuoteMedia is a leading software developer and cloud-based syndicator of financial market information and streaming financial data solutions to media, corporations, online brokerages, and financial services companies. The Company licenses interactive stock research tools such as streaming real-time quotes, market research, news, charting, option chains, filings, corporate financials, insider reports, market indices, portfolio management systems, and data feeds. QuoteMedia provides industry leading market data solutions and financial services for companies such as the Nasdaq Stock Exchange, TMX Group (TSX Stock Exchange), Canadian Securities Exchange (CSE), London Stock Exchange Group, FIS, U.S. Bank, Bank of Montreal (BMO), Broadridge Financial Systems, JPMorgan Chase, Scotiabank, CI Financial, Canaccord Genuity Corp., Hilltop Securities, HD Vest, Stockhouse, Zacks Investment Research, General Electric, Boeing, Bombardier, Telus International, Business Wire, PR Newswire, FolioFN, Regal Securities, ChoiceTrade, Cetera Financial Group, Dynamic Trend, Inc., Qtrade Financial, CNW Group, IA Private Wealth, Ally Invest, Inc., Suncor, Leede Jones Gable, Firstrade Securities, Charles Schwab, First Financial, Equisolve, Stock-Trak, Mergent, Cision, Warrior Trading and others. Quotestream®, QMod TM and Quotestream Connect TM are trademarks of QuoteMedia. For more information, please visit www.quotemedia.com .

Statements about QuoteMedia’s future expectations, including future revenue, earnings, and transactions, as well as all other statements in this press release other than historical facts are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. QuoteMedia intends that such forward-looking statements be subject to the safe harbors created thereby. These statements involve risks and uncertainties that are identified from time to time in the Company’s SEC reports and filings and are subject to change at any time. QuoteMedia’s actual results and other corporate developments could differ materially from that which has been anticipated in such statements.

Below are the specific forward-looking statements included in this press release:

We achieved record profits this quarter, and we expect to improve upon this moving forward. We anticipate that the pace of our revenue growth will continue in the coming quarters, with the launch of more enterprise deployments and exciting partnerships.

Due to the significant depreciation of the Canadian dollar, we are revising our revenue growth projection for the 2022 year. A substantial number of our contracts (and new contracts) are denominated in Canadian dollars, and this is re-measured into US Dollars when reporting our financial results. We are now projecting a 16% revenue growth for 2022, down from 19%. This will not have a meaningful impact on our bottom-line profitability, though, as our Canadian dollar revenue and expenses are almost equal. In fact, we anticipate significantly increased profitability in upcoming quarters.

We believe that Adjusted EBITDA, as a non-GAAP pro forma financial measure, provides meaningful information to investors in terms of enhancing their understanding of our operating performance and results, as it allows investors to more easily compare our financial performance on a consistent basis compared to the prior year periods. This non-GAAP financial measure also corresponds with the way we expect investment analysts to evaluate and compare our results. Any non-GAAP pro forma financial measures should be considered only as supplements to, and not as substitutes for or in isolation from, or superior to, our other measures of financial information prepared in accordance with GAAP, such as net income attributable to QuoteMedia, Inc.

We define and calculate Adjusted EBITDA as net income attributable to QuoteMedia, Inc., plus: 1) depreciation and amortization, 2) stock compensation expense, 3) interest expense, 4) foreign exchange loss (or minus a foreign exchange gain), and 5) income tax expense. We disclose Adjusted EBITDA because we believe it is a useful metric by which to compare the performance of our business from period to period. We understand that measures similar to Adjusted EBITDA are broadly used by analysts, rating agencies, investors and financial institutions in assessing our performance. Accordingly, we believe that the presentation of Adjusted EBITDA provides useful information to investors. The table below provides a reconciliation of Adjusted EBITDA to net income attributable to QuoteMedia, Inc., the most directly comparable GAAP financial measure.

QuoteMedia, Inc. Adjusted EBITDA Reconciliation to Net Income

Q3 revenue down 2.3%; up 0.3% in constant currency

Q3 operating loss of $21.4 million and loss per share of $0.43 down from a year ago on a non-cash goodwill impairment charge

Adjusted operating earnings of $9.5 million; up 7% from a year ago or up 21% in constant currency

Kelly’s Board of Directors approves a $50 million share repurchase plan

TROY, Mich., Nov. 10, 2022 /PRNewswire/ — Kelly (Nasdaq: KELYA, KELYB), a leading specialty talent solutions provider, today announced results for the third quarter of 2022.

Peter Quigley, president and chief executive officer, announced revenue for the third quarter of 2022 totaled $1.2 billion, a 2.3% decrease, or 0.3% increase in constant currency, compared to the corresponding quarter of 2021. Year-over-year revenue trends were impacted by foreign currency headwinds and the impact of the sale of our Russian operations in July 2022. Year-over-year results in the quarter also reflect the impact of the recent acquisitions of RocketPower, a recruitment process outsourcing firm, and Pediatric Therapeutic Services, a specialty firm providing in-school therapy services.

Kelly reported a loss from operations in the third quarter of 2022 of $21.4 million, compared to earnings of $9.0 million reported in the third quarter of 2021. The loss in the third quarter of 2022 resulted from a $30.7 million goodwill impairment charge related to RocketPower. The charge reflects the impact of increasing economic uncertainty including the sharp decline in hiring in the high-tech industry in which RocketPower specializes, as well as slowing growth in the near-term demand for recruitment process outsourcing more broadly. Excluding the impairment charge, adjusted earnings from operations were $9.5 million compared to $8.9 million in the third quarter of 2021. Earnings improved primarily as a result of structural improvements in the business mix which resulted in higher gross profit.

Loss per share in the third quarter of 2022 was $0.43 compared to earnings per share of $0.87 in the third quarter of 2021. Included in the loss per share in the third quarter of 2022 is a $0.67 per share goodwill impairment charge, net of tax, related to RocketPower, and a $0.01 loss per share, net of tax, related to the completion of the sale of our Russian operations. Included in the third quarter of 2021 earnings per share is a $0.62 gain, net of tax, related to non-cash gains, net of tax, on Persol Holding common shares. On an adjusted basis, earnings per share were $0.25 in the third quarter of 2022, consistent with $0.25 in the corresponding quarter of 2021.

“Kelly’s third-quarter performance demonstrates that our more profitable solutions are in demand and our specialty growth strategy is delivering a higher-margin, higher-value business mix even in the face of heightened uncertainty, rising interest rates, and inflationary pressures,” said Quigley. “We saw solid revenue growth in our SET and Education specialties, and all five operating segments delivered GP rate growth in the quarter. While challenges precipitated the RocketPower goodwill impairment, we remain confident that with diversification and integration this acquisition will bring strategic long-term value to our business. Finally, our planned buyback of Kelly Class A common shares highlights our flexible and balanced capital allocation strategy to maximize the return on capital and complements our organic and inorganic specialty growth strategy.”

Kelly also reported that on November 9, its board of directors declared a dividend of $0.075 per share. The dividend is payable on December 7, 2022 to stockholders of record as of the close of business on November 23, 2022.

In conjunction with its third-quarter earnings release, Kelly has published a financial presentation on the Investor Relations page of its public website and will host a conference call at 9 a.m. ET on November 10 to review the results and answer questions. The call may be accessed in one of the following ways:

Via the Telephone (877) 692-8955 (toll free) or (234) 720-6979 (caller paid) Enter access code 5728672 After the prompt, please enter ”#”

A recording of the conference call will be available after 2:30 p.m. ET on November 10, 2022, at (866) 207-1041 (toll-free) and (402) 970-0847 (caller-paid). The access code is 8237932#. The recording will also be available at kellyservices.com during this period.

This release contains statements that are forward looking in nature and, accordingly, are subject to risks and uncertainties. These factors include, but are not limited to, changing market and economic conditions, the impact of the novel coronavirus (COVID-19) outbreak, competitive market pressures including pricing and technology introductions and disruptions, disruption in the labor market and weakened demand for human capital resulting from technological advances, competition law risks, the impact of changes in laws and regulations (including federal, state and international tax laws), unexpected changes in claim trends on workers’ compensation, unemployment, disability and medical benefit plans, or the risk of additional tax liabilities in excess of our estimates, our ability to achieve our business strategy, our ability to successfully develop new service offerings, material changes in demand from or loss of large corporate customers as well as changes in their buying practices, risks particular to doing business with government or government contractors, the risk of damage to our brand, our exposure to risks associated with services outside traditional staffing, including business process outsourcing, services of licensed professionals and services connecting talent to independent work, our increasing dependency on third parties for the execution of critical functions, our ability to effectively implement and manage our information technology strategy, the risks associated with past and future acquisitions, including risk of related impairment of goodwill and intangible assets, risks associated with conducting business in foreign countries, including foreign currency fluctuations, risks associated with violations of anti-corruption, trade protection and other laws and regulations, availability of qualified full-time employees, availability of temporary workers with appropriate skills required by customers, liabilities for employment-related claims and losses, including class action lawsuits and collective actions, our ability to sustain critical business applications through our key data centers, risks arising from failure to preserve the privacy of information entrusted to us or to meet our obligations under global privacy laws, the risk of cyberattacks or other breaches of network or information technology security, our ability to realize value from our tax credit and net operating loss carryforwards, our ability to maintain specified financial covenants in our bank facilities to continue to access credit markets, and other risks, uncertainties and factors discussed in this release and in the Company’s filings with the Securities and Exchange Commission. Actual results may differ materially from any forward-looking statements contained herein, and we undertake no duty to update any forward-looking statement to conform the statement to actual results or changes in the Company’s expectations.

About Kelly®

Kelly Services, Inc. (Nasdaq: KELYA, KELYB) connects talented people to companies in need of their skills in areas including Science, Engineering, Education, Office, Contact Center, Light Industrial, and more. We’re always thinking about what’s next in the evolving world of work, and we help people ditch the script on old ways of thinking and embrace the value of all workstyles in the workplace. We directly employ more than 350,000 people around the world, and we connect thousands more with work through our global network of talent suppliers and partners in our outsourcing and consulting practice. Revenue in 2021 was $4.9 billion. Visit kellyservices.com and let us help with what’s next for you.

Third Quarter 2022 Revenue Up 211% Year-Over-Year to $26.0 Million

Third Quarter Net Income Up Year-Over-Year to $0.8 Million, or $0.06 per Share

Company Raises Revenue Guidance to $85 Million-$90 Million for Full-Year 2022

HOUSTON, Nov. 10, 2022 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced financial results for the third quarter ended September 30, 2022.

Mark Walker, Chairman and Chief Executive Officer of Direct Digital Holdings, commented, “We are pleased to report strong revenue and EBITDA for the third quarter of 2022, demonstrating strong growth across both our sell- and buy-side business segments and continued expansion of our portfolio and client reach.”

Keith Smith, President of Direct Digital Holdings, added, “Our team has effectively responded to the recent uncertainty and volatility in the market, capitalizing on brands and businesses moving dollars from less efficient traditional advertising outlets towards digital media. We believe that Direct Digital Holdings is well-positioned to continue its record of strong growth and market expansion or the remainder of the year and, as such, we are thrilled to announce we will be raising revenue guidance for full-year 2022.”

Third Quarter 2022 Financial Highlights:

Revenue increased to $26.0 million in the third quarter of 2022, an increase of $17.6 million, or up 211% over the $8.4 million in the same period of 2021.

Sell-side advertising segment, consisting of the Colossus SSP business, grew to $18.9 million and contributed $16.5 million of the increase, or up 710% over the $2.3 million in the same period of 2021.

Buy-side advertising segment, consisting of the Huddled Masses and Orange142 businesses, grew to $7.1 million and contributed $1.1 million of the increase, or up 18% over the $6.0 million in the same period of 2021.

Operating income increased $1.3 million, up 225%, to $1.8 million for the third quarter of 2022, compared to income of $0.6 million in the same period of 2021. Increased costs resulting from headcount additions, higher commission and bonus expense, public company related costs, as well as a one-time severance charge of approximately $0.5 million impacted operating income in the third quarter of 2022.

Net income was $0.8 million in the third quarter of 2022, up 458%, compared to ($0.2) million loss in the same period of 2021.

Adjusted EBITDA(1) increased 128% to $2.4 million in the third quarter 2022, compared to $1.1 million in the same period of 2021.

Net operating cash provided by operating activities for the nine-months ended September 30, 2022 was $3.4 million, compared to a net operating cash of $3.2 million generated in the same period of 2021.

Business Highlights

For the third quarter ended September 30, 2022, Direct Digital Holdings processed approximately 125 billion monthly impressions through its sell-side advertising segment, an increase of 56% over the same period of 2021, with over 1.3 trillion bid requests for the quarter.

In addition, the Company’s sell-side advertising platforms received over 11 billion bid responses, an increase of over 120% over the same period in 2021, through 129,000 buyers for the quarter.

The Company’s buy-side advertising segment served over 200 customers, an increase of 2% compared to the same period of 2021.

Financial Outlook

Direct Digital Holdings’ guidance assumes that the U.S. economy continues to grow at a moderate pace, and there are no major COVID-19-related setbacks or other shocks that may cause economic conditions to deteriorate or otherwise significantly reduce advertiser demand. Direct Digital Holdings plans to offer annual guidance and update it throughout the year. Accordingly, the Company estimates the following:

For fiscal year 2022, Direct Digital Holdings is raising expectations for guidance by approximately 20% to increase from a range of $70 million-$75 million to $85 million-$90 million, or up 130% year-over-year growth at the mid-point, while targeting an Adjusted EBITDA Margin in the double digits.

Conference Call and Webcast Details

Direct Digital Holdings will host a conference call on Thursday, November 10, 2022 at 5:00 p.m. Eastern Time to discuss the Company’s quarterly results. The live webcast and replay can be accessed at https://ir.directdigitalholdings.com/. Please access the website at least fifteen minutes prior to the call to register, download and install any necessary audio software. For those who cannot access the webcast, a replay will be available at https://ir.directdigitalholdings.com/ for a period of twelve months following the live webcast.

Footnote

(1) “Adjusted EBITDA” is a non-GAAP financial measure and Adjusted EBITDA Margin is an operating ratio derived from a non-GAAP financial measure. The section titled “Non-GAAP Financial Measures” below describes our usage of non-GAAP financial measures and provides reconciliations between historical GAAP and non-GAAP information contained in this press release.

Forward Looking Statements

This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to Direct Digital Holdings. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics, such as the ongoing global COVID-19 pandemic; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, of receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the SEC that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this release to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

About Direct Digital Holdings

Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 90,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app and other media channels. The company has been named a top minority-owned business by The Houston Business Journal.

Baudax Bio is a pharmaceutical company focused on innovative products for acute care settings. ANJESO is the first and only 24-hour, intravenous (IV) COX-2 preferential non-steroidal anti-inflammatory (NSAID) for the management of moderate to severe pain. In addition to ANJESO, Baudax Bio has a pipeline of other innovative pharmaceutical assets including two novel neuromuscular blocking agents (NMBs) and a proprietary chemical reversal agent specific to these NMBs. For more information, please visit www.baudaxbio.com.

Gregory Aurand, Senior Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Baudax reported 3Q 2022 results. 3Q revenues reported of $0.238 million were well below our expectation of $0.965 million. While vials sold increased year-over-year approximately 16%, much of the 3Q volume was discounted into 340B hospitals causing revenues to decline 15% from the prior year.

Feeling the pain. In the Covid environment that doesn’t seem to go away, hospitals face financial pressures as they struggle to curtail costs. For a single product company like Baudax Bio, the hospital issues have inflicted continued pain that is difficult to overcome. Hospitals look for less expensive alternatives in pain management. Recognizing that Covid-related issues facing hospitals now could continue into and through 2023, the Company eliminated the remaining commercial team in September 2022.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Townsquare is a community-focused digital media and digital marketing solutions company with market leading local radio stations, principally focused outside the top 50 markets in the U.S. Our assets include a subscription digital marketing services business, Townsquare Interactive, providing website design, creation and hosting, search engine optimization, social media and online reputation management as well as other digital monthly services for approximately 26,800 SMBs; a robust digital advertising division, Townsquare IGNITE, a powerful combination of a) an owned and operated portfolio of more than 330 local news and entertainment websites and mobile apps along with a network of leading national music and entertainment brands, collecting valuable first party data, and b) a proprietary digital programmatic advertising technology stack with an in-house demand and data management platform; and a portfolio of 321 local terrestrial radio stations in 67 U.S. markets strategically situated outside the Top 50 markets in the United States. Our portfolio includes local media brands such as WYRK.com, WJON.com, and NJ101.5.com and premier national music brands such as XXLmag.com, TasteofCountry.com, UltimateClassicRock.com and Loudwire.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

In line Q3 results. The company reported quarterly revenue of $120.6 million, up 8.4% year over year and in line with our estimate of $121.2 million. The revenue variance was due to softer Political advertising. Adj. EBITDA of $30.9 million was marginally higher than our estimate of $30.7 million. The company’s quarterly results demonstrated continued growth despite a difficult macroeconomic environment.

Strong financials. As of September 30th, the company had $27 million in cash and $524 million in long-term debt, and a net leverage ratio of 4.5 times. Management plans to reduce net leverage to 4 times by the end of year, and sits in a favorable position for opportunistic bond buy backs in a rising interest rate environment.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

For more than 70 years, Vectrus has provided critical mission support for our customers’ toughest operational challenges. As a high-performing organization with exceptional talent, deep domain knowledge, a history of long-term customer relationships, and groundbreaking technical expertise, we deliver innovative, mission-matched solutions for our military and government customers worldwide. Whether it’s base operations support, supply chain and logistics, IT mission support, engineering and digital integration, security, or maintenance, repair and overhaul, our customers count on us for on-target solutions that increase efficiency, reduce costs, improve readiness, and strengthen national security. Vectrus is headquartered in Colorado Springs, Colo., and includes about 8,100 employees spanning 205 locations in 28 countries. In 2021, Vectrus generated sales of $1.8 billion. For more information, visit the company’s website at www.vectrus.com or connect with Vectrus on Facebook, Twitter, and LinkedIn.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q22 Operating Results. In the first quarter as a combined entity, V2X reported strong results. Revenue of $958.2 million was up 10% year-over-year. Both the legacy Vectrus and Vertex businesses grew in the 10% y-o-y range. We had projected revenue of $855 million. The Company reported a GAAP net loss of $17 million, or a loss of $0.56 per share, driven by costs related to the merger. On an adjusted basis, net income totaled $40.2 million, or EPS of $1.33. We had projected adjusted EPS of $0.81. Adjusted EBITDA totaled $79 million for an 8.2% margin.

Drivers. The strong operating resultswere driven by continued expansion on existing business and the phase-in of new awards. Notably, year-over-year organic growth for the legacy Vectrus was approximately 10% in the quarter, driven by performance in INDOPACOM, growth on LOGCAP, contribution from Fort Benning as well as volume associated with rapid response and contingency support.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third-quarter results were below expectations due to lower-than-expected energy pricing. Production levels were in line with expectations and management guidance given on September 29. Realized oil and gas prices were well below U.S. reported oil and gas prices when adjusted to Canadian prices, reflecting a widening basis discount for western Canada production. We will incorporate a widening basis differential going forward.

InPlay is able to offset a weakening pricing environment with ever-improving production results. Management provided production guidance for 2023-25 for the first time. Guidance was well above production levels assumed in our models and reflects an acceleration of capital investments going forward. We believe increased investment is prudent at current payback rates of less than one year. We also believe management’s commitment to higher spending levels is a positive sign that it believes it has ample areas to drill at attractive returns.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

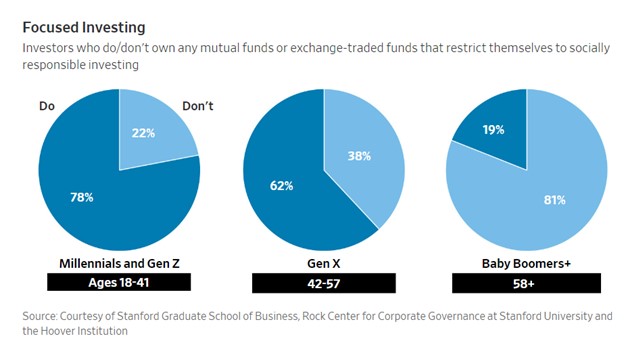

When a person invests in a mutual fund, ETF, or other managed asset pool that owns stocks, they are usually relinquishing a right to the fund manager. This is the right to vote as a shareholder on one’s own behalf. Shares held in the fund or trust are instead voted by the fund manager. Are the managers voting in a way the participants in the pooled assets would prefer? Does the environmental, social, and governance (ESG) vote on by fund managers meet their average client’s own leaning for their investment fund shares?

There is newly reported results of a research survey by Stanford University. The survey’s goal was assessing individual investors’ views about ESG investing. The authors surveyed 2,470 investors in the summer of 2022, with accounts ranging from $10,000 to more than $500,000. The survey found that investors’ tolerance or support for ESG measures, including a willingness to have poorer returns, varied by their age, current wealth, as well as the specific ESG issue.

Looking at Return vs. Alternative Objectives

Investors closest to retirement age, 58 years old and over, were the least likely to support ESG objectives. Those farthest from retirement age, 18 to 41 were the most likely. The data showed more than one-third of the younger investors said they would be willing to lose 11% to 15% of their retirement savings to encourage companies to have gender and racial diversity mirroring the general population. Of the more experienced older grouping, only 3% said they would risk or be willing to lose that amount for an ESG priority. A full 66% of the older investors said they were unwilling to lose any money to support ESG principles.

“Older investors want fund managers to generate financial returns to support their spending needs during retirement and don’t have a lot of time to recoup big losses,” says David Larcker, a professor at Stanford’s Graduate School of Business and one of the researchers.

The survey further confirmed that those where a loss was less troubling were more inclined to support and allow a large firm like Blackrock to decide what to support. The results showed wealthier young investors tended to be the largest group of ESG positive investors. For example, young investors with at least $250,000 under management said on average that they would be willing to lose about 14% of their retirement savings to have companies reduce carbon emissions to net zero by 2050. Alternatively, young investors with savings of less than $50,000 they would be willing to lose 6% on average to accomplish that goal.

Not all ESG initiatives rank the same for investors. Those surveyed held a higher level of support for those involving environmental issues. Social issues came next, and they were concerned the least about governance.

Vote Preferences

The investors surveyed also said they wanted the investment managers’ vote to reflect their own individual personal views related to ESG initiatives. In a related inquiry, 79% of the survey’s respondents with money at BlackRock managed assets said they approved of the firm’s use of its voting power to promote diversity on corporate boards.

Fully reflecting their clients’ views on ESG initiatives would be a high hurdle for investment managers, given the range of investors’ positions on so many issues. One potentiality is Investment managers could split their votes to weight individual investors’ views, Prof. Larcker says. For instance, that could mean voting 70% of their shares in a company in favor of a specific ESG proposal and 30% of their shares against the proposal.

Return Expectations

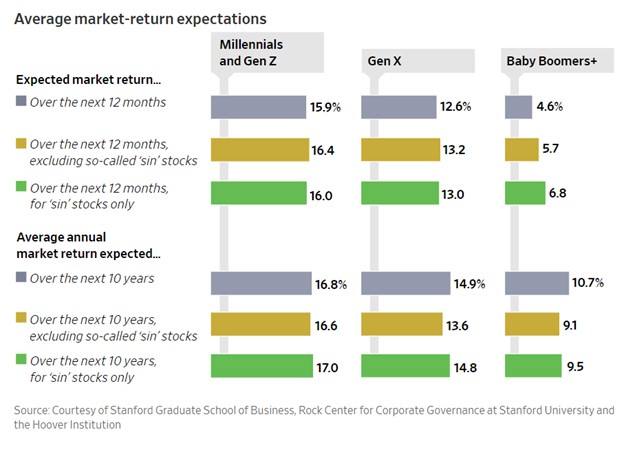

The older, more experienced respondents also had a significantly different view of expectations of return on investments.

Investment managers may want to provide data to try to improve fund participants’ understanding of the extent to which they have increased their risk to support the plans of an ESG-managed fund. Prof. Larcker suggests this could entail making it clear how returns of voting choices differed financially and from an ESG perspective, he says: “Did a vote improve or hurt the company’s financial performance in the short or long term? Was there a tangible effect on the environment or on employee diversity?”

“Fund managers need to acknowledge that there is likely to be some trade-off between ESG and financial returns,” he says, “and that trade-off may matter to individual investors.”

Take Away

Investing for the social good is not a new concept. The latest incarnation, ESG, has gained much more traction than the socially responsible investing initiatives of the past. The performance data, both financial and goal satisfaction, are difficult to measure. The survey done this past summer demonstrates the differences between demographic groups, a difference of expectations, and the weight of importance of, say, environmental issues over others.

As ESG-based investments evolve, Channelchek will keep you up to date on how others are looking at this category, what is new within the category, and other news that can keep you aware of the changing face of ESG. Sign up for Channelchek emails and information here.

MIAMI, Nov. 09, 2022 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games”), a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world, today announced that it is postponing its earnings release and conference call for the third quarter ended September 30, 2022, previously scheduled for November 10, 2022. The Company will issue a press release announcing the new date and time for the postponed earnings call.

About Motorsport Games: Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.