Entrepreneurial Courage and Perseverance Define the Pilgrims

Originally Published November 27, 2019 (Channelchek)

This week, across the U.S., families and friends, young and old, will gather to celebrate the “most American” of holidays, Thanksgiving. The gatherings will most surely include traditional foods of the holiday while families enjoy their own tradition of sharing and gratitude. Thoughts may also drift to almost 400 years ago when in 1621 a determined group of 102 Pilgrims persevered to achieve a mission they believed in – an accomplishment that has had a positive impact for centuries. They met challenges from the very beginning during their two-month-long voyage on the Mayflower, and they struggled as the first Winter took the lives of half the population of settlers. These resolute individuals share many of the same characteristics as today’s newer business owners who are making sacrifices in their own lives, for a better tomorrow for themselves and their descendants.

Dictionary.com has four definitions for the word “entrepreneur,” the first reads: “a person who organizes and manages any enterprise, especially a business, usually with considerable initiative and risk.” It’s not a stretch to call the original settlers of Plymouth Massachusetts entrepreneurs. Their grit, ingenuity, initiative, and even willingness to learn and rely on others more experienced in their environment, was certainly entrepreneurial.

The Mayflower colonists did not go by the moniker “Pilgrims,” that tag came 200 years after their landing at Plymouth Rock. Instead they referred to themselves as the “Saints” to indicate their purity and feelings of being special or chosen. This feeling must have been a strong driver as they risked so much in a way that is extreme by any standard in modern America.

Today’s Pilgrims

The risk-takers today, at least those looking to sacrifice more than others for the dream of a better tomorrow, whether for themselves and their families or for the world at large, are the business entrepreneurs. Especially in fields that are “uncharted territory.” Some examples are companies relying on developing technology, scientific breakthroughs, or mineral exploration. As with most “firsts”, there are always unknowns, long lead times before any profit, and a shortage of capital. These are among the reasons building a business today, particularly in a groundbreaking field with unproven outcome, is a path taken by very few. Those that do, and then survive and thrive, have embraced being nimble, building alliances, persistence, belief in themselves, and asking for help when needed.

“All great and honorable actions are accompanied by great difficulties, and both must be enterprised and overcome with answerable courage.” – William Bradford, Second Governor, Plymouth Colony

Flexibility

The Pilgrims initially went to Holland, where they expected to be welcomed by people of different religions. Their main reason for having left England was to worship without constraints. The Pilgrims made their home at first in Holland, but the more secular life they found there was not going to lead to a future that matched their vision. They wanted to build their own colony where they would attract others who believed as they did – even if it meant starting with close to nothing. As entrepreneurs, they didn’t accept an undesirable outcome; they pivoted, changed their plans and redirected their effort, deciding to establish themselves and their future near Virginia’s Hudson River. While traveling, storms pushed them into Massachusetts, where they decided to rethink their plan once again. They then revised their plan and decided to find an area close to where they landed that would be suitable for farming.

To begin the two-month trip across the Atlantic, the Pilgrims borrowed money that, at the time, was an astronomical amount. The loan from, English capitalists looking to profit off the venture was for 1700 pounds. At the time, the average Englishman earned a tenth of a pound per day. As colonists, they first worked collectively to pay back this loan. They later divided acreage to work individually at farming their own land.

Alliances

After the first brutal Winter, the Pilgrims, who raised money in a business arrangement to finance their journey, again opened themselves up to being helped. This time by native Americans. They learned how to best plant corn, where to fish, and how to trap beaver and other furs. This helped lead the pilgrims to an abundance just one year later and a profit in their second year. Their debt was fully paid off in 23 years.

There are now over 10 million living Americans who are descendants of the Mayflower passengers. The undeniable traits of the entrepreneurs we now call Pilgrims have impacted the world. Entrepreneurs of today share the same traits and skills of those that came before; intention toward a dream, plan, persevere, adjust, negotiate, orchestrate help, and implement. The impact of entrepreneurs continues to shape the world and continue to have a positive impact on the future with their efforts.

Giving Thanks

Ideas have the ability to change the world. Those ideas that improve lives and positively impact the world are on the list of things we can be thankful for.

CAMH to use Filament’s natural psilocybin drug candidate for a clinical trial studying treatment-resistant depression

Vancouver, British Columbia, November 17, 2022 – Filament Health Corp. (OTCQB:FLHLF) (NEO:FH) (FSE:7QS) (“Filament”or the “Company”), a clinical‐stage natural psychedelic drug development company, today announced an agreement with the Centre forAddiction and Mental Health (CAMH), Canada’s largest mental health teaching hospital and one of the world’s leading research centres in the field. Filament will supply CAMH with its natural psilocybin drug candidate for a proposed clinical trial studying the effects of psilocybin for treatment-resistant depression (TRD). The trial will be funded by the first ever Canadian federal grant to study psilocybin.

“Treatment-resistant depression affects millions of people and is a leading cause of disability worldwide, and current treatments are limited by either poor efficacy or tolerability,” said Dr. Ishrat Husain, the CAMH trial’s lead investigator. “Existing clinical data suggests that psilocybin shows promise for treating treatment-resistant depression; our intention is to expand on this research by examining whether psychedelic effects are necessary to achieve an antidepressant response. The trial design relies upon a supply of safe, high quality psilocybin so Filament Health’s support is crucial to our success.”

Treatment-resistant depression (TRD)affects up to a third of all depressed individuals, and results in substantial functional decline and high mortality rates.Current treatment options for TRD, can have either inadequate efficacy, adverse effects, or are difficult to access. With this trial, CAMH intends to determine whether psychedelic-assisted psychotherapy with psilocybin is a viable alternative treatment, and whether psychedelic effects are necessary for efficacy.

“CAMH is one of the world’s most well-regarded mental health research institutions,” said Benjamin Lightburn, Chief Executive Officer and Co-Founder of Filament Health. “We’re proud to donate our natural psilocybin drug candidate to support this vital research.It’s another important step in our mission of getting safe, natural psychedelics into the hands of everyone who needs them, as soon as possible.

The clinical trial application is under review by Health Canada with approval anticipated by January 2023.

ABOUT FILAMENT HEALTH (OTCQB:FLHLF)(NEO:FH) (FSE:7QS)

Filament Health is a clinical-stage natural psychedelic drug development company. We believe that safe, standardized, naturally-derived psychedelic medicines can improve the lives of many, and our mission is to see them in the hands of everyone who needs them as soon as possible. Filament’s platform of proprietary intellectual property enables the discovery, development, and delivery of natural psychedelic medicines for clinical development. We are paving the way with the first-ever natural psychedelic drug candidates.

Certain statements and information contained herein may constitute “forward‐looking statements” and “forward‐looking information,” respectively, under Canadian securities legislation. Generally, forward‐looking information can be identified by the use of forward‐looking terminology such as, “expect”,“anticipate”, “continue”, “estimate”, “may”, “will”, “should”, “believe”,“intends”, “forecast”, “plans”, “guidance” and similar expressions are intended to identify forward‐looking statements or information. The forward‐looking statements are not historical facts, but reflect the current expectations of management of Filament regarding future results or events and are based on information currently available to them. Certain material factors and assumptions were applied in providing these forward‐looking statements.Forward‐looking statements regarding the Company are based on the Company’s estimates and are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, levels of activity, performance or achievements of Filament to be materially different from those expressed or implied by such forward‐looking statements or forward‐looking information, including status of patent applications and the ability to secure patents.There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward‐ looking statements and forward‐looking information. Filament will not update any forward‐ looking statements or forward‐looking information that are incorporated by reference herein, except as required by applicable securities laws.

LOS ANGELES, Nov. 23, 2022 (GLOBE NEWSWIRE) — FAT(Fresh. Authentic. Tasty.) Brands Inc. (NASDAQ: FAT), a leading global franchising company and parent company of iconic brands including Round Table Pizza, Fatburger, Johnny Rockets, Twin Peaks, Fazoli’s and 12 other restaurant concepts, today announced their participation in the Benchmark Company’s 11th Annual Discovery One-on-One Investor Conference on Thursday, December 1, 2022 at the New York Athletic Club in New York City.

FAT Brands is scheduled to participate in one-on-one meetings with institutional analysts and investors throughout the day. The conference offers emerging growth and dynamic publicly traded companies access to institutional and individual investors in a unique one-on-one format.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

About The Benchmark Company

The Benchmark Company is an institutionally focused, research driven, sales trading and investment banking firm. We were founded in 1988 and are headquartered in New York City. Our focus is on fostering the long-term success of our corporate clients through raising capital, providing strategic advisory services, generating insightful research and developing institutional sponsorship by leveraging the firm’s sales, trading and equity research capabilities. https://www.benchmarkcompany.com.

CHATHAM, N.J., Nov. 23, 2022 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP), a clinical-stage biopharmaceutical company, announced today that management will participate virtually in the A.G.P. Biotech Conference and host investor meetings. The conference is being held Wednesday, November 30, 2022 – Thursday, December 1, 2022.

Investors interested in arranging a meeting with the Company’s management during the conference should contact the conference coordinator or Ian Frost at ian.frost@westwicke.com.

Tonix Pharmaceuticals Holding Corp.*

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022 and interim data expected in the second quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix initiated a Phase 2 study in Long COVID in the third quarter of 2022 and expects interim data in the second quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the first quarter of 2023. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is expected to enter the clinic with a Phase 2 study in the fourth quarter of 2022. TNX-601 ER (tianeptine hemioxalate extended-release tablets) is a once-daily formulation of tianeptine being developed as a potential treatment for major depressive disorder (MDD) with a Phase 2 study expected to be initiated in the first quarter of 2023. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the first half of 2023. Tonix’s infectious disease pipeline consists of a vaccine in development to prevent smallpox and monkeypox, next-generation vaccines to prevent COVID-19, and a platform to make fully human monoclonal antibodies to treat COVID-19. TNX-801, Tonix’s vaccine in development to prevent smallpox and monkeypox, also serves as the live virus vaccine platform or recombinant pox vaccine (RPV) platform for other infectious diseases. A Phase 1 study of TNX-801 is expected to be initiated in Kenya in the first half of 2023. Tonix’s lead vaccine candidate for COVID-19 is TNX-1850, a live virus vaccines based on Tonix’s recombinant pox live virus vector vaccine platform.

*All of Tonix’s product candidates are investigational new drugs or biologics and have not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2021, as filed with the Securities and Exchange Commission (the “SEC”) on March 14, 2022, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Grand Opening Event Scheduled for Wednesday, November 23rd

DENVER, Colo., Nov. 23, 2022 /CNW/ – Schwazze, (OTCQX: SHWZ) (NEO: SHWZ) (“Schwazze” or the “Company”), a premier vertically integrated, multi-state operating cannabis company with assets in Colorado and New Mexico, announces the grand opening of its adult-use dispensary, R.Greenleaf, located in Sunland Park, New Mexico. The new store, located at 1541 Appaloosa Drive in Sunland Park, officially opened its doors for business on November 22nd. Thanksgiving Day the store will be open from 10a to 4p. Regular store operating hours are 8a to 10p Monday through Saturday; 8a to 8p on Sunday.

The Sunland Park store opening continues the intentional expansion throughout the state of New Mexico and comes on the heels of the store openings in Ruidoso and Clovis within the last 60 days. This brings R.Greenleaf’s number of New Mexico retail dispensaries to a total of 13. All locations serve the needs of medical patients as well as recreational adult-use consumers.

“This week in particular, Schwazze gives tremendous thanks to be contributing to the Sunland Park community and to serve its residents. We are very grateful to add our third R.Greenleaf retail dispensary in New Mexico within the last two months and since adult recreational cannabis was legalized in New Mexico on April 1st,” said Steve Pear, New Mexico Division President for Schwazze. “R.Greenleaf offers a wide variety of quality products serviced by top-notch, knowledgeable staff.”

Grand opening product specials and promotions are already in full swing with multiple flower pack offers, pre-rolls, gummies, chocolates, and distillate vaporizer cartridges. Introductory pricing will be offered through November 30th to provide patients and recreational customers special savings on a variety of product forms based on individual needs and preferences.

A grand opening celebration will be held today, Wednesday, November 23rd beginning at 12 noon and running until 6p. Swag bags will be available to the first 50 shoppers featuring a water bottle, rolling papers and other R.Greenleaf gear, with one lucky customer receiving a 50% discount coupon. DJ Sonya G will be on site during the event to provide tunes for all in attendance, and the Sunland Park BBQ Company will provide free food for the first 50 customers making a purchase.

Sunland Park Store Location R.Greenleaf 1541 Appaloosa Drive Sunland Park, New Mexico 88063

Grand Opening Celebration Wednesday, November 23rd 12 noon to 6p

Since April 2020, Schwazze has acquired, opened or announced the planned acquisition of 38 cannabis retail dispensaries as well as seven cultivation facilities and two manufacturing plants in Colorado and New Mexico. In May 2021, Schwazze announced its Biosciences division and in August 2021 it commenced home delivery services in Colorado.

About Schwazze

Schwazze (OTCQX: SHWZ) (NEO: SHWZ) is building a premier vertically integrated regional cannabis company with assets in Colorado and New Mexico and will continue to take its operating system to other states where it can develop a differentiated regional leadership position. Schwazze is the parent company of a portfolio of leading cannabis businesses and brands spanning seed to sale. The Company is committed to unlocking the full potential of the cannabis plant to improve the human condition. Schwazze is anchored by a high-performance culture that combines customer-centric thinking and data science to test, measure, and drive decisions and outcomes. The Company’s leadership team has deep expertise in retailing, wholesaling, and building consumer brands at Fortune 500 companies as well as in the cannabis sector. Schwazze is passionate about making a difference in our communities, promoting diversity and inclusion, and doing our part to incorporate climate-conscious best practices.

Medicine Man Technologies, Inc. was Schwazze’s former operating trade name. The corporate entity continues to be named Medicine Man Technologies, Inc. Schwazze derives its name from the pruning technique of a cannabis plant to enhance plant structure and promote healthy growth.

Forward-Looking Statements

This press release contains “forward-looking statements.” Such statements may be preceded by the words “plan,” “will,” “may,” “continue,” “predicts,” or similar words. Forward-looking statements are not guarantees of future events or performance, are based on certain assumptions, and are subject to various known and unknown risks and uncertainties, many of which are beyond the Company’s control and cannot be predicted or quantified. Consequently, actual events and results may differ materially from those expressed or implied by such forward-looking statements. Such risks and uncertainties include, without limitation, risks and uncertainties associated with (i) our inability to manufacture our products and product candidates on a commercial scale on our own or in collaboration with third parties; (ii) difficulties in obtaining financing on commercially reasonable terms; (iii) changes in the size and nature of our competition; (iv) loss of one or more key executives or scientists; (v) difficulties in securing regulatory approval to market our products and product candidates; (vi) our ability to successfully execute our growth strategy in Colorado and outside the state, (vii) our ability to consummate the acquisition described in this press release or to identify and consummate future acquisitions that meet our criteria, (viii) our ability to successfully integrate acquired businesses, including the acquisition described in this press release, and realize synergies therefrom, (ix) the ongoing COVID-19 pandemic, * the timing and extent of governmental stimulus programs, and (xi) the uncertainty in the application of federal, state and local laws to our business, and any changes in such laws. More detailed information about the Company and the risk factors that may affect the realization of forward-looking statements is set forth in the Company’s filings with the Securities and Exchange Commission (SEC), including the Company’s Annual Report on Form 10-K and its Quarterly Reports on Form 10-Q. Investors and security holders are urged to read these documents free of charge on the SEC’s website at http://www.sec.gov. The Company assumes no obligation to publicly update or revise its forward-looking statements as a result of new information, future events or otherwise except as required by law.

CALGARY, AB, Nov. 22, 2022 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF) announces initial results from the second interval tested in our 183-B1 well on our 100% owned and operated Block 183.

In July 2022, we completed drilling the 183-B1 exploration well to a total measured depth (“MD”) of 2,917 metres. Based on open-hole wireline logs and fluid samples confirming hydrocarbons, the well discovered hydrocarbons in multiple formations with a total of 34.3 metres of potential net hydrocarbon pay, with an average porosity of 10.6% and average water saturation of 29.0% using a 6% porosity cut-off, 50% Vshale cut-off and 50% water saturation cut-off.

Alvopetro has completed the 183-B1 formation test in the Agua Grande formation, the second deepest of three formations with hydrocarbons shows during drilling of the well. We perforated a total of 8.5 metres in the Agua Grande formation at various intervals between 2,680 metres and 2,699 metres MD. During the clean up flow period we recovered 16 bbls of completion fluid and 1 bbl of 52°API natural gas liquids (condensate). After a short shut-in we initiated the production test on a 32/64″ choke. Cumulatively, over the duration of the 72-hour production test, we recovered 2.4 bbls of 48°API natural gas liquids (condensate), 9.4 bbls of formation water and 2.4 MMcf of gas. During the test, the flowing rate decreased from 5.7 MMcfpd to 0.3 MMcfpd, the average gas rate during testing operations was 0.8 MMcfpd. At the beginning of the testing operations the shut-in wellhead pressure (“SIWHP”) was 2,555 psi, and the final flowing wellhead pressure was 40 psi. After 32 hours of buildup the SIWHP was 610 psi.

These results indicate a high permeability zone that delivered strong initial production flow rates but, based on pressure and production declines over the flow period, and slow pressure build up following the test, the Agua Grande reservoir appears to be areally constrained in the high permeability zone and likely sub-commercial in the remaining Agua Grande zones. We will now proceed up-hole to test the Candeias Formation. Based on open-hole logs, using a 6% porosity cut-off, 50% Vshale cut-off and 50% water saturation cut-off the Gomo member of the Candeias Formation was encountered at 2,578 to 2,583 metres total vertical depth, with 5.3 metres of potential net light oil pay, at an average 35.0% water saturation and average porosity of 15.7%. A fluid sample in this Candeias interval was also collected with a dual packer wireline tool recovering 37.1°API oil with no water to surface from 2,580 metres depth at a formation pressure of 4,317 psi.

We previously announced the results of the 183-B1 formation test in the Sergi Formation, the deepest of three formations with hydrocarbons shows during drilling of the well. We perforated a total of 26.5 metres in the upper portion of the Sergi formation at various intervals between 2,811 metres MD and 2,886 metres MD. We initially swabbed 63 bbls of oil and 7 bbls of completions fluid during the clean-up period. After a short shut-in we then initiated the production test. Cumulatively, over the duration of the 72-hour production test, we recovered 59 bbls of 43°API oil, 7 bbls of water identified as completion fluid, and 0.28 MMcf of associated gas. The daily oil rate recovered during swabbing operations averaged 20 bopd. We are engineering a stimulation plan for this upper Sergi section in this well and we have submitted applications to drill two follow up wells from this 183-B1 surface location targeting the full Sergi hydrocarbon column and the potential in the deeper Boipeba Formation.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All amounts contained in this new release are in United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Abbreviations:

API

=

American Petroleum Institute

°API

=

an indication of the specific gravity of crude oil measured on the API gravity scale.

bbls

=

barrels

boepd

=

barrels of oil equivalent (“boe”) per day

bopd

=

barrels of oil and/or natural gas liquids (condensate) per day

MMcf

=

million cubic feet

MMcfpd

=

million cubic feet per day

BOE Disclosure. The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this news release are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Testing and Well Results. Data obtained from the 183-B1 well identified in this press release, including hydrocarbon shows, open-hole logging, net pay and porosities and initial testing data, should be considered to be preliminary until detailed pressure transient and other analysis and interpretation has been completed. Hydrocarbon shows can be seen during the drilling of a well in numerous circumstances and do not necessarily indicate a commercial discovery or the presence of commercial hydrocarbons in a well. There is no representation by Alvopetro that the data relating to the 183-B1 well contained in this press release is necessarily indicative of long-term performance or ultimate recovery. The reader is cautioned not to unduly rely on such data as such data may not be indicative of future performance of the well or of expected production or operational results for Alvopetro in the future.

Forward-Looking Statements and Cautionary Language. This news release contains “forward-looking information” within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward‐looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning potential hydrocarbon pay in the 183-B1 well, exploration and development prospects of Alvopetro and the expected timing of certain of Alvopetro’s testing and operational activities. The forward‐looking statements are based on certain key expectations and assumptions made by Alvopetro, including but not limited to expectations and assumptions concerning testing results of the 183-B1 well and the 182-C2 well, equipment availability, the timing of regulatory licenses and approvals, the success of future drilling, completion, testing, recompletion and development activities, the outlook for commodity markets and ability to access capital markets, the impact of the COVID-19 pandemic, the performance of producing wells and reservoirs, well development and operating performance, foreign exchange rates, general economic and business conditions, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power market, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Property located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Going deep. Defense Metals released assay results from Hole WI22-72, totaling 374 meters and the deepest hole drilled to date to test below the mineral resource pit shell, terminating 360 meters below surface and 150 meters below the pit shell at the company’s Wicheeda REE Deposit. The hole was drilled within the central area of the deposit and intersected high-grade mineralized dolomite carbonate from surface grading 3.02% total rare earth oxides (TREO) over 55 meters within a broader zone averaging 2.56% TREO over 122 meters, and a well mineralized mixed lithology lower zone grading 0.9% TREO over 97 meters.

Results for ten drill holes remain outstanding. With over 5,500 meters of drilling in 18 holes completed as part of the 2022 resource delineation and pit geotechnical program, Defense Metals has released assays for eight holes representing 2,867 meters of drilling. Assays for the remaining 10 holes are expected to be released in the coming weeks and months.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The idea that correlation does not imply causation is a fundamental caveat in epidemiological research. A classic example involves a hypothetical link between ice cream sales and drownings – instead of increased ice cream consumption causing more people to drown, it’s plausible that a third variable, summer weather, is driving up an appetite for ice cream and swimming, and hence opportunities to drown.

But what about correlations involving genes? How can researchers be sure that a particular trait or disease is truly genetically linked, and not caused by something else?

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Richard Border, Postdoctoral Researcher in Statistical Genetics, University of California, Los Angeles and Noah Zaitlen, Professor of Neurology and Human Genetics, University of California, Los Angeles.

We are statistical geneticists who study the genetic and nongenetic factors that influence human variation. In our recently published research, we found that the genetic links between traits found in many studies might not be connected by genes at all. Instead, many are a result of how humans mate.

Genome-wide association studies try to link genes to traits

Because the genes you inherit from your parents remain unchanged throughout your life, with rare exception, it makes sense to assume that there is a causal relationship between certain traits you have and your genetics.

This logic is the basis for genome-wide association studies, or GWAS. These studies collect DNA from many people to identify positions in the genome that might be correlated with a trait of interest. For example, if you have certain forms of the BRCA1 and BRCA2 genes, you may have an increased risk for certain types of cancer.

Similarly, there may be gene variants that play a role in whether or not someone has schizophrenia. The hope is to learn something about the complex mechanisms that link variation at the molecular level to individual differences. With a clearer understanding of the genetic basis of different traits, scientists would be better able to determine risk factors for related diseases.

GWAS studies seek to find genetic associations between individual traits.

Researchers have run thousands of GWAS to date, identifying genetic variants associated with myriad diseases and disease-related traits. In many instances, researchers have identified genetic variants that affect more than one trait. This form of biological overlap, in which the same genes are thought to influence several apparently unrelated traits, is known as pleiotropy. For example, certain variants of the PAH gene can have several distinct effects, including altering skin pigmentation and causing seizures.

One way scientists assess pleiotropy is through genetic correlation analysis. Here, geneticists investigate whether the genes associated with a given trait are associated with other traits or diseases by statistically analyzing large samples of genetic data. Over the past decade, genetic correlation analysis has become the primary method for assessing potential pleiotropy across fields as diverse as internal medicine, social science and psychiatry.

Scientists use the findings from genetic correlation analyses to figure out the potential shared causes of these traits. For instance, if genes associated with bipolar disorders also predict anxiety disorders, perhaps the two conditions may partially involve some of the same neural circuits or respond to similar treatments.

Assortative Mating and Genetic Correlation

However, just because a gene is correlated with two or more traits doesn’t necessarily mean it causes them.

Virtually all the statistical methods researchers commonly use to assess genetic correlations assume that mating is random. That is, they assume that potential mating partners decide who they will have children with based on a roll of the dice. In reality, many factors likely influence who mates with whom. The simplest example of this is geography – people living in different parts of the world are less likely to end up together than people living nearby.

We wanted to find out how much the assumption of random mating affects the accuracy of genetic correlation analyses. In particular, we focused on the potential confounding effects of assortative mating, or how people tend to mate with those who share similar characteristics with them. Assortative mating is a widely documented phenomenon seen across a broad array of traits, interests, measures and social factors, including height, education and psychiatric conditions.

In our study we examined cross-trait assortative mating, whereby people with one trait (for example, being tall) tend to mate with people with a completely different trait (for example, being wealthy). From our database of 413,980 mate pairs in the U.K. and Denmark, we found evidence of cross-trait assortative mating for many traits – for instance, an individual’s time spent in formal schooling was correlated not only with their mate’s educational attainment, but also with many other characteristics, including height, smoking behaviors and risk for different diseases.

We found that taking into consideration the similarities across mates could strongly predict which traits would be considered genetically linked. In other words, just based on how many characteristics a pair of mates shared, we could identify around 75% of the presumed genetic links between these traits – all without sampling any DNA.

Genetic Correlation Does Not Imply Causation

Cross-trait assortative mating shapes the genome. If people with one heritable trait tend to mate with people with another heritable trait, then these two distinct characteristics will become genetically correlated to each other in subsequent generations. This will happen regardless of whether or not these traits are truly genetically linked to each other.

Cross-trait assortative mating means that the genes you inherit from one parent will be correlated with those you inherit from the other. How people mate is not random, violating the key assumption behind genetic correlation analyses. This inflates the genetic association between traits that aren’t truly linked together by genes.

If dinosaurs with long horns preferentially mate with dinosaurs with spiked backs, genes for both of these traits can become associated with each other in subsequent generations even though the same gene doesn’t code for them.

Recent studies corroborate our findings. Earlier this year, researchers computed genetic correlations using a method that examines the association between the traits and genes of siblings. The genetic links between traits influenced by cross-trait assortative mating were substantially weakened.

But without accounting for cross-trait assortative mating, using genetic correlation estimates to study the biological pathways causing disease can be misleading. Genes that affect only one trait will appear to influence multiple different conditions. For example, a genetic test designed to assess the risk for one disease may incorrectly detect vulnerability for a broad number of unrelated conditions.

The ability to measure variation across individuals at the genetic and molecular level is truly a feat of modern science. However, genetic epidemiology is still an observational enterprise, subject to the same caveats and challenges facing other forms of nonexperimental research. Though our findings don’t discount all genetic epidemiology research, understanding what genetic studies are truly measuring will be essential to translate research findings into new ways to treat and assess disease.

Why the Fed Needs to Gain Trust, Gain Momentum, and Gain More Yards

Monetary policy and its implementation is as much sport as science. Economics is actually a social science, so it relies on human behavior to mimic past behaviors as its prediction guide. But as in sports, victory is difficult if there is distrust in the coach that’s calling the shots (in this case Powell), or if there are people on your side that have reason to work against you, (an example would be Yellen). Consistency in blocking and tackling (doing the right thing) and not giving up, over time, wins games. Knowing what to expect from the opposing team (consumers) wins a healthy economy.

One repeated trait in monetary policy is that there is a lag between implementation (easing or tightening) and a change in economic conditions. It isn’t a short lag, and the impact varies. Since it could take more than a year for a policy change to begin to impact the economy, the Fed usually moves at a slow and measured pace in order to not overdo it.

The slow pace allows policymakers to observe the impact of their moves and change tactics (positions on the playing field) mid-game.

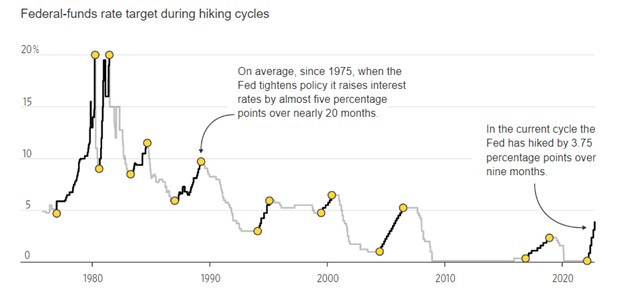

Federal-Funds Rate During Tightening Cycles

Note: From December 2008, midpoint of target range. December 2015 hike excluded from 2016-18 cycle

Source: Federal Reserve

Over the past nine months, we have been in a tightening cycle. During this period, the Fed has raised rates by 3.75%. On average (since 1975), when the Fed has tightened rates, they are notched up by 5.00% over 20 months.

The Fed’s current pace is faster than average. This is because inflation took them by surprise, and rose rapidly. Putting up a strong defense against inflation that has been rampant is necessary to not be shut out and allow the Fed to gain control over the outcome.

Because one has to be able to reflect back more than 40 years to have experienced the Fed raising rates this fast. Many have lost confidence in its ability, and are in their own way working against a winning outcome.

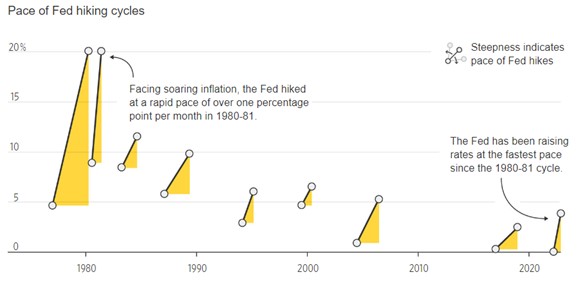

Pace of Fed Hiking Cycles

Note: From December 2008, the midpoint of target range

Source: Federal Reserve

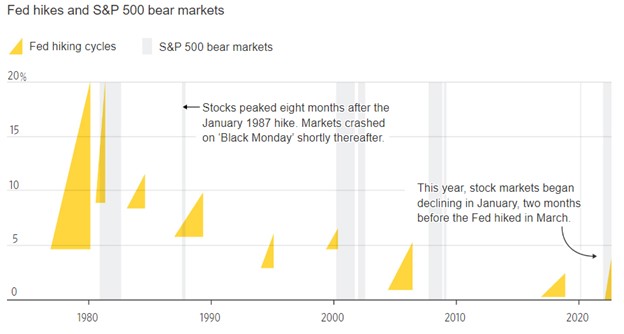

The stock and bond markets move in group anticipation of expected policy moves by the Fed. This has been more pronounced in recent years as the Fed has basically shared its expectations after each meeting, setting up for the next. Higher rates make bonds and bank deposits more attractive. Higher rates also weaken the economy and corporate profits, and that induces investors to move away from stocks and even real estate.

Bonds now offer the highest yields since 2007. The stock market may have anticipated what was to come as it peaked in early January of this year, more than two months before the Fed began hiking in March.

Fed Hikes and S&P 500 Bear Markets

Sources: Federal Reserve; Dow Jones Market Data

Sources: Federal Reserve; Dow Jones Market Data

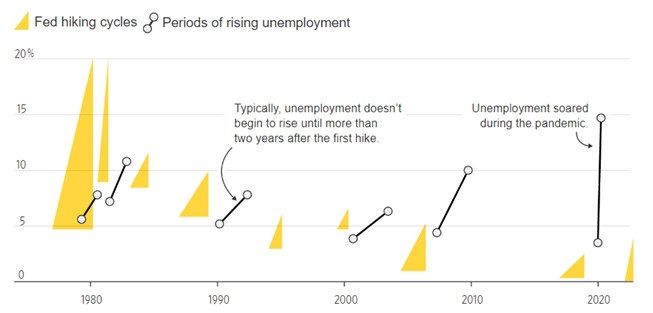

Employment

The Fed is concerned with a wage-price spiral feeding on itself. It likely won’t be satisfied that its tightening has been sufficient until it can be confident that it has avoided a wage-price storm on the economy.

Ideally, this would happen without unemployment rising. Soft landings took place in 1983-84 and 1994-95. But when inflation starts out too high, as it is now, unemployment usually rises notably, and a recession occurs.

Historically, this doesn’t happen until several years after the first increase. This time it is hoped it will be different, since the Fed is playing more aggressively.

Periods of Fed Hiking and Rising Unemployment

Note: The unemployment rate rose to 3.7% in October, up from the pandemic low of 3.5% a month earlier. Sources: Federal Reserve; Labor Department

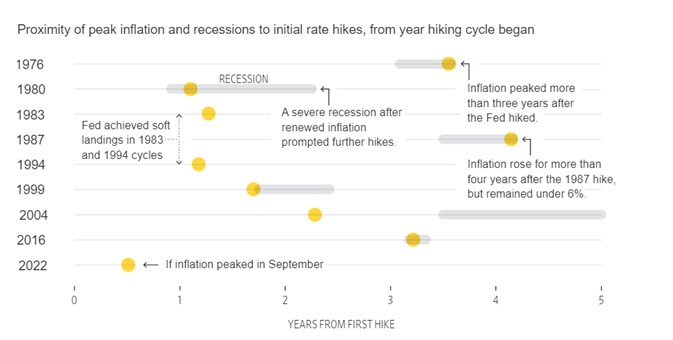

Inflation

Historically, inflation has only fallen to acceptable levels after unemployment has increased, and long after the first rate increase – the exact timing has varied. If the fall in core inflation (which excludes the volatile food and energy components) between September and October continues, and September proves to be the peak, the time between the first Fed increase and the high point of inflation will be one of the shortest of any Fed hiking cycle.

Often, the break in inflation has been accompanied by a recession. The economy receded in each of the first two quarters and then grew in the third. The changes in the inflation component in Gross Domestic Product may have borrowed from one quarter and have been additive to the next. The fourth quarter reading should help level the growth averages out to see if we were indeed in a shallow recession.

Proximity of Peak Inflation and Recessions to Initial Rate Hikes, from Year Hiking Cycle Began

Note: Inflation refers to core CPI.

Sources: Federal Reserve; Labor Department

Take Away

As in many team sports, once one side gets momentum, they are difficult to stop . The Fed needs to gain the trust of the individual players in the economy in order to be successful. Saying one thing, then doing another, would undermine this trust. So far, despite the Fed originally being wrong about inflation, the Fed has done what it has said it would do. Stock and bond markets, which are a considerable part of the economy, have been slow to understand the Fed’s resolve.

It has been implementing the balance sheet run-off plan and raising rates toward a level it believes would equate to a future 2% inflation rate. Like so many other things in the social sciences, widely held expectations of the future become self-fulfilling.

CHATHAM, N.J., Nov. 22, 2022 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP), a clinical-stage biopharmaceutical company, today announced that Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals, will deliver an oral presentation at the World Vaccine and Immunotherapy Congress 2022, which will be held in San Diego, Calif., November 28 – December 1, 2022. A copy of the Company’s presentation will be available under the Scientific Presentations tab of the Tonix website at www.tonixpharma.com following the conference. Additional meeting information can be found on the World Vaccine and Immunotherapy Congress website here.

Oral Presentation Details

Title:

Showcase 1: Early Development of Smallpox & Monkey Pox Vaccines

Location:

Loews Coronado Bay Resort, San Diego, Calif.

Date:

December 1, 2022

Time:

10:40 a.m. PT (1:40 p.m. ET)

Tonix Pharmaceuticals Holding Corp.*

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022 and interim data expected in the second quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix initiated a Phase 2 study in Long COVID in the third quarter of 2022 and expects interim data in the second quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the first quarter of 2023. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is expected to enter the clinic with a Phase 2 study in the fourth quarter of 2022. TNX-601 ER (tianeptine hemioxalate extended-release tablets) is a once-daily formulation of tianeptine being developed as a potential treatment for major depressive disorder (MDD) with a Phase 2 study expected to be initiated in the first quarter of 2023. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the first half of 2023. Tonix’s infectious disease pipeline consists of a vaccine in development to prevent smallpox and monkeypox, next-generation vaccines to prevent COVID-19, and a platform to make fully human monoclonal antibodies to treat COVID-19. TNX-801, Tonix’s vaccine in development to prevent smallpox and monkeypox, also serves as the live virus vaccine platform or recombinant pox vaccine (RPV) platform for other infectious diseases. A Phase 1 study of TNX-801 is expected to be initiated in Kenya in the first half of 2023. Tonix’s lead vaccine candidate for COVID-19 is TNX-1850, a live virus vaccines based on Tonix’s recombinant pox live virus vector vaccine platform.

*All of Tonix’s product candidates are investigational new drugs or biologics and have not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2021, as filed with the Securities and Exchange Commission (the “SEC”) on March 14, 2022, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Railroad Unions and Their Employers at an Impasse: Freight-Halting Strikes are Rare, and this Would be the First in 3 Decades

The prospect of a potentially devastating rail workers strike is looming again.

Fears of a strike in September 2022 prompted the Biden administration to pull out all the stops to get a deal between railroads and the largest unions representing their employees.

That deal hinged on ratification by a majority of members at all 12 of those unions. So far, eight have voted in favor, but four have rejected the terms. If even one continues to reject the deal after further negotiations, it could mean a full-scale freight strike will start as soon as midnight on Dec. 5, 2022. Any work stoppage by conductors and engineers would surely interfere with the delivery of gifts and other items Americans will want to receive in time for the holiday season, along with coal, lumber and other key commodities.

Strikes that obstruct transportation rarely occur in the United States, and the last one involving rail workers happened three decades ago. But when these workers do walk off the job, it can thrash the economy, inconveniencing millions of people and creating a large-scale crisis.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of Erik Loomis, Professor of History, University of Rhode Island.

I’m a labor historian who has studied the history of American strikes. I believe that with the U.S. teetering toward at least a mild recession and some of the supply chain disruptions that arose at the outset of the COVID-19 pandemic still wreaking havoc, I don’t think the administration would accept a rail strike for long.

19th Century Rail Strikes

Few, if any, workers have more power over the economy than transportation workers. Their ability to shut down the entire economy has often led to heavy retaliation from the government when they have tried to exercise that power.

In 1877, a small strike against a West Virginia railroad that had cut wages spread. It grew into what became known as the Great Railroad Strike, a general rebellion against railroads that brought thousands of unemployed workers into the streets.

Seventeen years later, in 1894, the American Railway Union went on strike in solidarity with the Pullman Sleeping Car company workers who had gone on strike due to their boss lowering wages while maintaining rents on their company housing.

In both cases, the threat of a railroad strike led the federal government to call out the military to crush the labor actions. Dozens of workers died.

Once those dramatic clashes ended, for more than a century rail unions have played a generally quiet role, preferring to focus on the needs of their members and avoiding most broader social and political questions. Fearful of more rail strikes, the government passed the Railway Labor Act of 1926, which gives Congress the power to intervene before a rail strike starts.

Breaking the Air Traffic Controllers Union

With travel by road and air growing in importance in the 20th century, other transportation workers also engaged in actions that could shut down the economy.

The Professional Air Traffic Controllers Association walked off the job in 1981 after a decade of increased militancy over the stress and conditions of their job. The union had engaged in a series of slowdowns through the 1970s, delaying airplanes and frustrating passengers.

When it went on strike in 1981, the union broke the law, as federal workers do not have the right to strike. That’s when President Ronald Reagan became the first modern U.S. leader to retaliate against striking transportation workers. Two days after warning the striking workers that they would lose their jobs unless they returned to work, Reagan fired more than 11,000 of them. He also banned them from ever being rehired.

In the aftermath of Reagan’s actions, the number of strikes by U.S. workers plummeted. Rail unions engaged in brief strikes in both 1991 and 1992, but Congress used the Railway Labor Act to halt them, ordering workers back on the job and imposing a contract upon the workers.

In 1992, Congress passed another measure that forced a system of arbitration upon railroad workers before a strike – that took power away from workers to strike.

New Era of Labor Militancy

Following decades of decline in the late 20th century, U.S. labor organizing has surged in recent years.

Most notably, unionization attempts at Starbucks and Amazon have led to surprising successes against some of the biggest corporations in the country. Teachers’ unions around the nation have also held a series of successful strikes everywhere from Los Angeles to West Virginia.

United Parcel Service workers, who held the nation’s last major transportation strike, in 1997, may head back to the picket lines after their contract expires in June 2023. UPS workers, members of the Teamsters union, are angry over a two-tiered system that pays newer workers lower wages, and they are also demanding greater overtime protections.

But rail workers, angered by their employers’ refusal to offer sick leave and other concerns, may go on strike first.

Rail companies have greatly reduced the number of people they employ on freight trains as part of their efforts to maximize profits and take advantage of technological progress. They generally keep the size of crews limited to only two per train.

Many companies want to pare back their workforce further, saying that it can be safe to have crews consisting of a single crew member on freight trains. The unions reject this arrangement, saying that lacking a second set of eyes would be a recipe for mistakes, accidents and disasters.

The deal the Biden administration brokered in September would raise annual pay by 24% over several years, raising the average pay for rail workers to $110,000 by 2024. But strikes are often about much more than wages. The companies have also long refused to provide paid sick leave or to stop demanding that their workers have inflexible and unpredictable schedules.

The Biden administration had to cajole the rail companies into offering a single personal day, while workers demanded 15 days of sick leave. Companies had offered zero. The agreement did remove penalties from workers who took unpaid sick or family leave, but this would still leave a group of well-paid workers whose daily lives are filled with stress and fear.

What Lies Ahead

Seeing highly paid workers threaten to take action that would surely compound strains on supply chains at a time when inflation is at a four-decade high may not win rail unions much public support.

A coalition representing hundreds of business groups has called for government intervention to make sure freight trains keep moving, and it’s highly likely that Congress will again impose a decision on workers under the Railway Labor Act. The Biden administration, which has shown significant sympathy to unions, has resisted supporting such a step so far.

No one should expect the military to intervene like it did in the 19th century. But labor law remains tilted toward companies, and I believe that if the government were to compel striking rail workers back on the job, the move might find a receptive audience.

A team of scientists at the Whitehead Institute for Biomedical Research and the Broad Institute of MIT and Harvard has systematically evaluated the functions of over 5,000 essential human genes using a novel, pooled, imaged-based screening method. Their analysis harnesses CRISPR-Cas9 to knock out gene activity and forms a first-of-its-kind resource for understanding and visualizing gene function in a wide range of cellular processes with both spatial and temporal resolution. The team’s findings span over 31 million individual cells and include quantitative data on hundreds of different parameters that enable predictions about how genes work and operate together. The new study appears in the Nov. 7 online issue of the journal Cell.

“For my entire career, I’ve wanted to see what happens in cells when the function of an essential gene is eliminated,” says MIT Professor Iain Cheeseman, who is a senior author of the study and a member of Whitehead Institute. “Now, we can do that, not just for one gene but for every single gene that matters for a human cell dividing in a dish, and it’s enormously powerful. The resource we’ve created will benefit not just our own lab, but labs around the world.”

Systematically disrupting the function of essential genes is not a new concept, but conventional methods have been limited by various factors, including cost, feasibility, and the ability to fully eliminate the activity of essential genes. Cheeseman, who is the Herman and Margaret Sokol Professor of Biology at MIT, and his colleagues collaborated with MIT Associate Professor Paul Blainey and his team at the Broad Institute to define and realize this ambitious joint goal. The Broad Institute researchers have pioneered a new genetic screening technology that marries two approaches — large-scale, pooled, genetic screens using CRISPR-Cas9 and imaging of cells to reveal both quantitative and qualitative differences. Moreover, the method is inexpensive compared to other methods and is practiced using commercially available equipment.

“We are proud to show the incredible resolution of cellular processes that are accessible with low-cost imaging assays in partnership with Iain’s lab at the Whitehead Institute,” says Blainey, a senior author of the study, an associate professor in the Department of Biological Engineering at MIT, a member of the Koch Institute for Integrative Cancer Research at MIT, and a core institute member at the Broad Institute. “And it’s clear that this is just the tip of the iceberg for our approach. The ability to relate genetic perturbations based on even more detailed phenotypic readouts is imperative, and now accessible, for many areas of research going forward.”

Cheeseman adds, “The ability to do pooled cell biological screening just fundamentally changes the game. You have two cells sitting next to each other and so your ability to make statistically significant calculations about whether they are the same or not is just so much higher, and you can discern very small differences.”

Cheeseman, Blainey, lead authors Luke Funk and Kuan-Chung Su, and their colleagues evaluated the functions of 5,072 essential genes in a human cell line. They analyzed four markers across the cells in their screen — DNA; the DNA damage response, a key cellular pathway that detects and responds to damaged DNA; and two important structural proteins, actin and tubulin. In addition to their primary screen, the scientists also conducted a smaller, follow-up screen focused on some 200 genes involved in cell division (also called “mitosis”). The genes were identified in their initial screen as playing a clear role in mitosis but had not been previously associated with the process. These data, which are made available via a companion website, provide a resource for other scientists to investigate the functions of genes they are interested in.

“There’s a huge amount of information that we collected on these cells. For example, for the cells’ nucleus, it is not just how brightly stained it is, but how large is it, how round is it, are the edges smooth or bumpy?” says Cheeseman. “A computer really can extract a wealth of spatial information.”

Flowing from this rich, multi-dimensional data, the scientists’ work provides a kind of cell biological “fingerprint” for each gene analyzed in the screen. Using sophisticated computational clustering strategies, the researchers can compare these fingerprints to each other and construct potential regulatory relationships among genes. Because the team’s data confirms multiple relationships that are already known, it can be used to confidently make predictions about genes whose functions and/or interactions with other genes are unknown.

There are a multitude of notable discoveries to emerge from the researchers’ screening data, including a surprising one related to ion channels. Two genes, AQP7 and ATP1A1, were identified for their roles in mitosis, specifically the proper segregation of chromosomes. These genes encode membrane-bound proteins that transport ions into and out of the cell. “In all the years I’ve been working on mitosis, I never imagined ion channels were involved,” says Cheeseman.

He adds, “We’re really just scratching the surface of what can be unearthed from our data. We hope many others will not only benefit from — but also build upon — this resource.”

This work was supported by grants from the U.S. National Institutes of Health as well as support from the Gordon and Betty Moore Foundation, a National Defense Science and Engineering Graduate Fellowship, and a Natural Sciences and Engineering Research Council Fellowship.

A team of scientists at the Whitehead Institute for Biomedical Research and the Broad Institute of MIT and Harvard has systematically evaluated the functions of over 5,000 essential human genes using a novel, pooled, imaged-based screening method. Their analysis harnesses CRISPR-Cas9 to knock out gene activity and forms a first-of-its-kind resource for understanding and visualizing gene function in a wide range of cellular processes with both spatial and temporal resolution. The team’s findings span over 31 million individual cells and include quantitative data on hundreds of different parameters that enable predictions about how genes work and operate together. The new study appears in the Nov. 7 online issue of the journal Cell.

“For my entire career, I’ve wanted to see what happens in cells when the function of an essential gene is eliminated,” says MIT Professor Iain Cheeseman, who is a senior author of the study and a member of Whitehead Institute. “Now, we can do that, not just for one gene but for every single gene that matters for a human cell dividing in a dish, and it’s enormously powerful. The resource we’ve created will benefit not just our own lab, but labs around the world.”

Systematically disrupting the function of essential genes is not a new concept, but conventional methods have been limited by various factors, including cost, feasibility, and the ability to fully eliminate the activity of essential genes. Cheeseman, who is the Herman and Margaret Sokol Professor of Biology at MIT, and his colleagues collaborated with MIT Associate Professor Paul Blainey and his team at the Broad Institute to define and realize this ambitious joint goal. The Broad Institute researchers have pioneered a new genetic screening technology that marries two approaches — large-scale, pooled, genetic screens using CRISPR-Cas9 and imaging of cells to reveal both quantitative and qualitative differences. Moreover, the method is inexpensive compared to other methods and is practiced using commercially available equipment.

“We are proud to show the incredible resolution of cellular processes that are accessible with low-cost imaging assays in partnership with Iain’s lab at the Whitehead Institute,” says Blainey, a senior author of the study, an associate professor in the Department of Biological Engineering at MIT, a member of the Koch Institute for Integrative Cancer Research at MIT, and a core institute member at the Broad Institute. “And it’s clear that this is just the tip of the iceberg for our approach. The ability to relate genetic perturbations based on even more detailed phenotypic readouts is imperative, and now accessible, for many areas of research going forward.”

Cheeseman adds, “The ability to do pooled cell biological screening just fundamentally changes the game. You have two cells sitting next to each other and so your ability to make statistically significant calculations about whether they are the same or not is just so much higher, and you can discern very small differences.”

Cheeseman, Blainey, lead authors Luke Funk and Kuan-Chung Su, and their colleagues evaluated the functions of 5,072 essential genes in a human cell line. They analyzed four markers across the cells in their screen — DNA; the DNA damage response, a key cellular pathway that detects and responds to damaged DNA; and two important structural proteins, actin and tubulin. In addition to their primary screen, the scientists also conducted a smaller, follow-up screen focused on some 200 genes involved in cell division (also called “mitosis”). The genes were identified in their initial screen as playing a clear role in mitosis but had not been previously associated with the process. These data, which are made available via a companion website, provide a resource for other scientists to investigate the functions of genes they are interested in.

“There’s a huge amount of information that we collected on these cells. For example, for the cells’ nucleus, it is not just how brightly stained it is, but how large is it, how round is it, are the edges smooth or bumpy?” says Cheeseman. “A computer really can extract a wealth of spatial information.”

Flowing from this rich, multi-dimensional data, the scientists’ work provides a kind of cell biological “fingerprint” for each gene analyzed in the screen. Using sophisticated computational clustering strategies, the researchers can compare these fingerprints to each other and construct potential regulatory relationships among genes. Because the team’s data confirms multiple relationships that are already known, it can be used to confidently make predictions about genes whose functions and/or interactions with other genes are unknown.

There are a multitude of notable discoveries to emerge from the researchers’ screening data, including a surprising one related to ion channels. Two genes, AQP7 and ATP1A1, were identified for their roles in mitosis, specifically the proper segregation of chromosomes. These genes encode membrane-bound proteins that transport ions into and out of the cell. “In all the years I’ve been working on mitosis, I never imagined ion channels were involved,” says Cheeseman.

He adds, “We’re really just scratching the surface of what can be unearthed from our data. We hope many others will not only benefit from — but also build upon — this resource.”

This work was supported by grants from the U.S. National Institutes of Health as well as support from the Gordon and Betty Moore Foundation, a National Defense Science and Engineering Graduate Fellowship, and a Natural Sciences and Engineering Research Council Fellowship.

Will Global Rate Hikes Set Off a Global Debt Bomb?

The higher levels of risky corporate debt issuance over the past few year will need to be refinanced between 2023 and 2025, In numbers terms, there will be over $10 trillion of the riskiest debt at much higher interest rates and with less liquidity. In addition to domestic high yield issuance, the majority of the major European economies have issued negative-yielding debt over the past three years and must now refinance at significantly higher rates. In 2020–21. the annual increase in the US money supply (M2) was 27 percent, more than 2.5 times higher than the quantitative easing peak of 2009 and the highest level since 1960. Negative yielding bonds, an economic anomaly that should have set off alarm bells as an example of a bubble worse than the “subprime” bubble, amounted to over $12 trillion. Even if refinancing occurs smoothly but at higher costs, the impact on new credit and innovation will be enormous, and the crowding out effect of government debt absorbing the majority of liquidity and the zombification of the already indebted will result in weaker growth and decreased productivity in the future.

Raising interest rates is a necessary but insufficient measure to combat inflation. To reduce inflation to 2 percent, central banks must significantly reduce their balance sheets, which has not yet occurred in local currency, and governments must reduce spending, which is highly unlikely.

The most challenging obstacle is also the accumulation of debt.

The so-called expansionary policies have not been an instrument for reducing debt, but rather for increasing it. In the second quarter of 2022, according to the Institute of International Finance (IIF), the global debt-to-GDP ratio will approach 350 percent of GDP. IIF anticipates that the global debt-to-GDP ratio will reach 352 percent by the end of 2022.

Global issuances of high-yield debt have slowed but remain elevated. According to the IMF, the total issuance of European and American high-yield bonds reached a record high of $1,6 trillion in 2021, as businesses and investors capitalized on still low interest rates and high liquidity. According to the IMF, high-yield bond issuances in the United States and Europe will reach $700 billion in 2022, similar to 2008 levels. All of the risky debt accumulated over the past few years will need to be refinanced between 2023 and 2025, requiring the refinancing of over $10 trillion of the riskiest debt at much higher interest rates and with less liquidity.

Moody’s estimates that United States corporate debt maturities will total $785 billion in 2023 and $800 billion in 2024. This increases the maturities of the Federal government. The United States has $31 trillion in outstanding debt with a five-year average maturity, resulting in $5 trillion in refinancing needs during fiscal 2023 and a $2 trillion budget deficit. Knowing that the federal debt of the United States will be refinanced increases the risk of crowding out and liquidity stress on the debt market.

According to The Economist, the cumulative interest bill for the United States between 2023 and 2027 should be less than 3 percent of GDP, which appears manageable. However, as a result of the current path of rate hikes, this number has increased, which exacerbates an already unsustainable fiscal problem.

If you think the problem in the United States is significant, the situation in the eurozone is even worse. Governments in the euro area are accustomed to negative nominal and real interest rates. The majority of the major European economies have issued negative-yielding debt over the past three years and must now refinance at significantly higher rates. France and Italy have longer average debt maturities than the United States, but their debt and growing structural deficits are also greater. Morgan Stanley estimates that, over the next two years, the major economies of the eurozone will require a total of $3 trillion in refinancing.

Although at higher rates, governments will refinance their debt. What will become of businesses and families? If quantitative tightening is added to the liquidity gap, a credit crunch is likely to ensue. However, the issue is not rate hikes but excessive debt accumulation complacency.

Explaining to citizens that negative real interest rates are an anomaly that should never have been implemented is challenging. Families may be concerned about the possibility of a higher mortgage payment, but they are oblivious to the fact that house prices have skyrocketed due to risk accumulation caused by excessively low interest rates.