Anticipate topline results from the Phase 1 monotherapy and Phase 1/2 combination study with letrozole in Q4 2023

Plans are underway for a registrational trial with rigosertib in patients with RDEB-associated squamous cell carcinoma based on a constructive Type B FDA meeting held in June

Company to host conference call and webcast at 4:30 p.m. ET on Thursday, August 10, 2023

NEWTOWN, Pa., Aug. 10, 2023 (GLOBE NEWSWIRE) — Onconova Therapeutics, Inc. (NASDAQ: ONTX), (“Onconova” or “the Company”), a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer, today reported second quarter 2023 financial results and provided an update on recent pipeline progress. Management plans to host a conference call and live webcast at 4:30 p.m. ET today to discuss these results.

“We are very encouraged about the recent progress that the Onconova team has made for our two lead programs, narazaciclib, a differentiated multikinase CDK4/6 inhibitor targeting proteins involved in resistance pathways, and rigosertib, a cell signaling inhibitor, over the last few months, while effectively managing our financial resources. In addition, we are pleased that Victor Moyo, M.D., a highly experienced and successful clinical researcher and drug developer, has agreed to join the Company as Consulting Chief Medical Officer. We look forward to sharing several important updates in the coming months,” said Steve Fruchtman, M.D., President and Chief Executive Officer.

Dr. Fruchtman continued, “For narazaciclib, our efforts have been dedicated to completing a Phase 1 program and defining a recommended Phase 2 dose to support evaluation of narazaciclib in a randomized trial. Onconova believes this CDK4/6 compound has the potential to provide differentiated efficacy based on targeting proteins that have been implicated in resistance mechanisms and the potential for an improved safety profile. We are pleased to see target engagement based on an assay measuring proliferation. We expect to report the results from our Phase 1 monotherapy and Phase 1/2 combination study with letrozole in Q4 2023. The readout will include safety, pharmacokinetics and the definition of a recommended Phase 2 dose.”

Dr. Fruchtman concluded, “For rigosertib, we continue to believe this rigosertib’s unique action on cell signaling pathways, including K-RAS and PLK-1, combined with an acceptable safety profile, could position it as an attractive anti-cancer agent. In June, we had a constructive Type B meeting with the FDA for the use of rigosertib monotherapy in the lead, ultra-rare indication of RDEB-associated squamous cell carcinoma. Based on that meeting and the impressive clinical responses in previously refractory patients we have seen and presented at major medical meetings, we plan to design a registrational trial and will look to provide an update on next steps in H1 2024. In the meantime, we continue to support two investigator sponsored studies for rigosertib, underway in melanoma and KRAS mutated non-small cell lung cancer which includes any KRAS mutation that may be present.”

Second Quarter Financial Results Cash and cash equivalents as of June 30, 2023, were $29.7 million, compared to $38.8 million as of December 31, 2022. The Company believes that its cash and cash equivalents will be sufficient to fund ongoing clinical trials and business into the second quarter of 2024.

Research and development expenses were $2.5 million for the second quarter of 2023, compared with $2.0 million for the second quarter of 2022.

General and administrative expenses were $2.2 million for the second quarter of 2023, compared with $2.1 million for the second quarter of 2022.

Net loss for the second quarter of 2023 was $4.3 million, or $0.20 per share on 21.0 million weighted shares outstanding, compared with a net loss of $4.0 million, or $0.19 per share for the second quarter of 2022 on 20.9 million weighted shares outstanding.

Conference Call and Webcast Information Interested parties who wish to participate in the conference call may do so by dialing:

(800) 715-9871 for domestic and

(646) 307-1963 for international callers and

Using conference ID 9506701

Those interested in listening to the conference call via the internet may do so by visiting the investors and media page on the Company’s website at www.onconova.com and clicking on the webcast link. In addition to the live webcast, a replay will be available on the Onconova website for 90 days following the call.

About Onconova Therapeutics, Inc. Onconova Therapeutics is a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer. The Company’s product candidates include proprietary targeted anti-cancer agents designed to disrupt specific cellular pathways that are important for cancer cell proliferation.

Onconova’s novel, proprietary multi-kinase inhibitor narazaciclib (formerly ON 123300) is being evaluated in a Phase 1/2 combination trial with the estrogen blocker, letrozole, in advanced low grade endometrial cancer (NCT05705505). Based on preclinical and clinical studies of CDK 4/6 inhibitors, Onconova is also evaluating opportunities for combination studies with narazaciclib and letrozole in additional indications.

Onconova’s product candidate rigosertib is being studied in multiple investigator-sponsored studies. These studies include a dose-escalation and expansion Phase 1/2a study of oral rigosertib in combination with nivolumab in patients with KRAS+ non-small cell lung cancer (NCT04263090), a Phase 2 program evaluating oral or IV rigosertib monotherapy in advanced squamous cell carcinoma complicating recessive dystrophic epidermolysis bullosa (RDEB-associated SCC (NCT03786237, NCT04177498), and a Phase 2 trial evaluating rigosertib in combination with pembrolizumab in patients with metastatic melanoma (NCT05764395).

Forward Looking Statements Some of the statements in this release are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, and involve risks and uncertainties. These statements relate to Onconova’s expectations regarding its clinical development and trials, its product candidates and its business and financial position. Onconova has attempted to identify forward-looking statements by terminology including “believes,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” “preliminary,” “encouraging,” “approximately” or other words that convey uncertainty of future events or outcomes. Although Onconova believes that the expectations reflected in such forward-looking statements are reasonable as of the date made, expectations may prove to have been materially different from the results expressed or implied by such forward-looking statements. These statements are only predictions and involve known and unknown risks, uncertainties, and other factors, including the success and timing of Onconova’s clinical trials, investigator-sponsored trials, regulatory agency and institutional review board approvals of protocols, Onconova’s collaborations, market conditions and those discussed under the heading “Risk Factors” in Onconova’s most recent Annual Report on Form 10-K and quarterly reports on Form 10-Q. Any forward-looking statements contained in this release speak only as of its date. Onconova undertakes no obligation to update any forward-looking statements contained in this release to reflect events or circumstances occurring after its date or to reflect the occurrence of unanticipated events.

CHELMSFORD, MA / ACCESSWIRE / August 10, 2023 / Harte Hanks, Inc. (NASDAQ:HHS), a leading global customer experience company focused on bringing companies closer to customers for 100 years, today announced financial results for the second quarter and six-month period ended June 30, 2023.

Kirk Davis, Chief Executive Officer, commented: “My favorable impressions of Harte Hanks were confirmed in my first month as CEO; Harte Hanks has great people and significant capabilities that are desired by global brands. The pandemic had a positive, multi-year impact on our business, which we’re now beyond. In addition, many of our customers have curtailed budgets for 2023 due to concerns about the economy. This necessitates our near-term focus on further aligning our cost structure, and in addition, shifting some of our current spend to bolster sales productivity.”

“The second quarter results represent a baseline for our expectations in the near term and present a solid foundation on which to build,” added Mr. Davis. “We’re focused on bolstering our sales pipeline, retooling our marketing programs, improving sales effectiveness, and leveraging a new partnership we’ve struck with a highly reputable business development company. Our acquisition of InsideOut in December of 2022 expands our end-to-end offering and specifically our lead generation capabilities. We expect to build on the consistent profitability that has been achieved and position Harte Hanks to generate more sustainable, profitable growth. We’re excited to deliver on these objectives. Additionally, the company executed on its stock repurchase plan by repurchasing almost 315,000 shares.”

Second Quarter Financial Highlights

Total revenues for Q2 2023 were $47.8 million, up 1.4% sequentially and down 1.6% year over year compared to $48.6 million in Q2 2022. Included in 2023 was $2.3 million from InsideOut acquired in fourth quarter of 2022.

Operating income was $1.7 million compared to $4.0 million in the prior-year quarter.

Net income of $0.6 million compared to net income of $4.5 million in the prior year.

Diluted EPS was $0.08 compared to $0.52 for the prior year’s second quarter.

EBITDA was $2.7 million compared to $4.6 million in the same period in the prior year.[1] Adjusted EBITDA, which excludes stock-based compensation and severance, was $4.4 million compared to $5.2 million.

Segment Highlights

Customer Care, $17.2 million in revenue, 36% of total – Segment revenue increased $1.8 million or 11.9% versus prior year and EBITDA totaled $3.0 million for the quarter, up 18.3% year-over-year. New business wins that are expected to positively impact results during the second quarter include:

A multi-national pharmaceutical company has engaged Harte Hanks to develop the strategy for their long-term Customer Service Experience. The scope includes the analysis and validation of their Customer Service vision, benchmarking, gap analysis and a blueprint with an implementation roadmap to inform their 2024 plans to optimize their Customer Care strategy and delivery.

One of the largest consultancy firms in the world has selected Harte Hanks to support a state government’s rollout of Medicaid renewal support for its constituents. This program helps Medicaid users renew for services, as well as provides education on how to engage and leverage the online systems to improve use of these benefits.

Fulfillment & Logistics Services, $19.6 million in revenue, 41% of total – Segment revenue decreased slightly versus the prior year quarter and EBITDA for Q2 2023 totaled $1.9 million, down $1.2 million or 39%. Revenue mix drove the reduced EBITDA margins as growth in lower-margin logistics revenue was offset by reduced volumes in our financial services vertical that yielded higher margins. New business wins during the second quarter include:

Harte Hanks Fulfillment won New Logo business with a major international manufacturer, providing fulfillment support for a new program of Direct-to-Customer hearing aid sales. As a major player in the industry, the manufacturer is well-positioned for growth as the hearing aid market pivots from prescription-only into “Over the Counter” space.

A leading branding company selected Harte Hanks Fulfillment to manage the production, kitting, and distribution of 150k+ curated Food & Beverage product gift boxes for a Fortune 50 retail partner. After producing several million kits on this partner’s behalf over the past year, this represents the first instance where the relationship has fully leveraged our FDA approved, climate-controlled facility for food grade items.

Marketing Services, $10.9 million in revenue, 23% of total – Segment revenue declined $2.5 million (19%) compared to the prior year quarterand EBITDA for the quarter totaled $1.3 million vs. $1.8 million. Pressure on both revenue and EBITDA was driven by a reduction in legacy direct mail campaigns and lighter project volumes. New business wins during second quarter include:

A major insurance carrier supporting government employees has selected Harte Hanks to help facilitate their email transition to a new CRM. While this organization is an existing customer for our Customer Care and Fulfillment segments, this is the first engagement for this client with our Marketing Services team.

One of the largest online travel agencies has expanded its services with Harte Hanks to support an ‘Always On’ nurture program for their global business customers.

Consolidated Second Quarter 2023 Results

Second quarter revenues were $47.8 million, down 1.6% from $48.6 million in the second quarter of 2022. The Company’s Customer Care segment grew, largely offsetting declines in Fulfillment & Logistics Services and Marketing Services.

Second quarter operating income was $1.7 million, compared to operating income of $4.0 million in the second quarter of 2022. The decrease resulted from a less favorable revenue mix and lower consolidated revenue.

Net income for the quarter was $0.6 million, or $0.08 per diluted share, compared to net income of $4.5 million, or $0.52 per diluted share, in the second quarter last year. Results this quarter included $1.2 million of pension expense, as well as $503,000 in stock-based compensation and $1.2 million in severance, largely related to the CEO transition. The severance and other costs related to the CEO transition created a non-recurring, $0.12 per share impact, without tax impact, in the second quarter of 2023.

Consolidated Year-to-Date 2023 Results

Year-to-date revenues were $94.9 million, down 2.8% from $97.6 million in the same period of 2022. Year-to-date operating income was $2.7 million, compared to operating income of $7.9 million. Net loss for the first six months was $(0.2) million, or $(0.03) per diluted share, compared to net income of $7.8 million, or $0.91 per diluted share, in the first six months of last year.

Balance Sheet and Liquidity

Harte Hanks ended the quarter with $13.4 million in cash and cash equivalents and $24 million of capacity on its credit line. The Company has no outstanding debt as of June 30, 2023. The Company’s financial position continues to be strong, and it is well-positioned to execute on its long-term growth strategies in 2023 and beyond.

During the quarter, Harte Hanks repurchased approximately 315,000 shares at an average price of $5.97 per share for a total of $1.9 million.

Conference Call Information

The Company will host a conference call and live webcast to discuss these results on Thursday, August 10, 2023 at 4:30 p.m. EST. Interested parties may access the webcast at https://investors.hartehanks.com/events or may access the conference call by dialing (877) 545-0320 in the United States or (973) 528-0002 from outside the U.S. and using access code 183563.

A replay of the call can also be accessed via phone through August 24, 2023 by dialing (877) 481-4010 from the U.S., or (919) 882-2331 from outside the U.S. The conference call replay passcode is 48804.

About Harte Hanks:

Harte Hanks (NASDAQ:HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract and engage their customers.

Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands, including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony and IBM among others. Headquartered in Chelmsford, Massachusetts, Harte Hanks has over 2,500 employees in offices across the Americas, Europe, and Asia Pacific.

As used herein, “Harte Hanks” or “the Company” refers to Harte Hanks, Inc. and/or its applicable operating subsidiaries, as the context may require. Harte Hanks’ logo and name are trademarks of Harte Hanks.

Our press release and related earnings conference call contain “forward-looking statements” within the meaning of U.S. federal securities laws. All such statements are qualified by this cautionary note, provided pursuant to the safe harbor provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Statements other than historical facts are forward-looking and may be identified by words such as “may,” “will,” “expects,” “believes,” “anticipates,” “plans,” “estimates,” “seeks,” “could,” “intends,” or words of similar meaning. These forward-looking statements are based on current information, expectations and estimates and involve risks, uncertainties, assumptions and other factors that are difficult to predict and that could cause actual results to vary materially from what is expressed in or indicated by the forward-looking statements. In that event, our business, financial condition, results of operations or liquidity could be materially adversely affected and investors in our securities could lose part or all of their investments. These risks, uncertainties, assumptions and other factors include: (a) local, national and international economic and business conditions, including (i) the outbreak of diseases, such as the COVID-19 coronavirus, which has curtailed travel to and from certain countries and geographic regions, created supply chain disruption and shortages, disrupted business operations and reduced consumer spending, (ii) market conditions that may adversely impact marketing expenditures, (iii) the impact of the Russia/Ukraine conflict on the global economy and our business, including impacts from related sanctions and export controls and (iv) the impact of economic environments and competitive pressures on the financial condition, marketing expenditures and activities of our clients and prospects; (b) the demand for our products and services by clients and prospective clients, including (i) the willingness of existing clients to maintain or increase their spending on products and services that are or remain profitable for us, and (ii) our ability to predict changes in client needs and preferences; (c) economic and other business factors that impact the industry verticals we serve, including competition and consolidation of current and prospective clients, vendors and partners in these verticals; (d) our ability to manage and timely adjust our facilities, capacity, workforce and cost structure to effectively serve our clients; (e) our ability to improve our processes and to provide new products and services in a timely and cost-effective manner though development, license, partnership or acquisition; (f) our ability to protect our facilities against security breaches and other interruptions and to protect sensitive personal information of our clients and their customers; (g) our ability to respond to increasing concern, regulation and legal action over consumer privacy issues, including changing requirements for collection, processing and use of information; (h) the impact of privacy and other regulations, including restrictions on unsolicited marketing communications and other consumer protection laws; (i) fluctuations in fuel prices, paper prices, postal rates and postal delivery schedules; (j) the number of shares, if any, that we may repurchase in connection with our repurchase program; (k) unanticipated developments regarding litigation or other contingent liabilities; (l) our ability to complete anticipated divestitures and reorganizations, including cost-saving initiatives; (m) our ability to realize the expected tax refunds; and (n) other factors discussed from time to time in our filings with the Securities and Exchange Commission, including under “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2022 which was filed on March 31, 2023. The forward-looking statements in this press release and our related earnings conference call are made only as of the date hereof, and we undertake no obligation to update publicly any forward-looking statement, even if new information becomes available or other events occur in the future.

Supplemental Non-GAAP Financial Measures:

The Company reports its financial results in accordance with generally accepted accounting principles (“GAAP”). However, the Company may use certain non-GAAP measures of financial performance in order to provide investors with a better understanding of operating results and underlying trends to assess the Company’s performance and liquidity in this press release and our related earnings conference call. We have presented herein a reconciliation of these measures to the most directly comparable GAAP financial measure.

The Company presents the non-GAAP financial measure “Adjusted Operating Income (Loss)” as a measure useful to both management and investors in their analysis of the Company’s financial results because it facilitates a period-to-period comparison of Operating Revenue and Operating Income (Loss) by excluding restructuring expense, impairment expense and stock-based compensation. The most directly comparable measure for this non-GAAP financial measure is Operating Income (Loss).

The Company presents the non-GAAP financial measure “EBITDA” and “Adjusted EBITDA” as a supplemental measure of operating performance in order to provide an improved understanding of underlying performance trends. The Company defines “Adjusted EBITDA” as earnings before interest expense net, income tax expense (benefit), depreciation expense, stock compensation expense and severance expenses. The most directly comparable measure for each of EBITDA and Adjusted EBITDA is Net Income (Loss). We believe each of EBITDA and Adjusted EBITDA are important performance metrics because they facilitates the analysis of our results, exclusive of certain non-cash items, non-recurring or special charges and items we believe do not directly correlate to our business operations; however, we urge investors to review the reconciliation of each of EBITDA and Adjusted EBITDA to the comparable GAAP Net Income (Loss), which is included in this press release, and not to rely on any single financial measure to evaluate the Company’s financial performance.

The use of non-GAAP measures do not serve as a substitute and should not be construed as a substitute for GAAP performance but should provide supplemental information concerning our performance that our investors and we find useful. The Company evaluates its operating performance based on several measures, including this non-GAAP financial measures. The Company believes that the presentation of this non-GAAP financial measures in this press release and earnings conference call presentations are useful supplemental financial measures of operating performance for investors because they facilitate investors’ ability to evaluate the operational strength of the Company’s business. However, there are limitations to the use of this non-GAAP measures, including that they may not be calculated the same by other companies in our industry limiting their use as a tool to compare results. Any supplemental non-GAAP financial measures referred to herein are not calculated in accordance with GAAP and they should not be considered in isolation or as substitutes for the most comparable GAAP financial measures.

EBITDA is the Company’s measure of segment profitability.

1 EBITDA is a non-GAAP financial measure. See “Supplemental Non-GAAP Financial Measures” below. EBITDA is also the Company’s measure of segment profitability.

Investor Relations Contact:

Rob Fink or Tom Baumann 646.809.4048 / 646.349.6641 FNK IR HHS@fnkir.com

Harte Hanks, Inc.

Consolidated Statements of Operations (Unaudited)

Three Months Ended June 30,

Six Months Ended June 30,

In thousands, except per share data

2023

2022

2023

2022

Revenues………………………………………………………………………………..

$

47,762

$

48,553

$

94,882

$

97,615

Operating expenses

Labor…………………………………………………………………………………..

26,666

25,109

51,131

51,027

Production and distribution……………………………………………………….

13,328

13,507

27,780

26,225

Advertising, selling, general and administrative………………………………

5,065

5,340

11,149

11,273

Depreciation and amortization expense………………………………………..

Second Quarter 2023 Revenue Up 67% Year-Over-Year to $35.4 Million

Company Raises Full-Year 2023 Revenue Guidance

HOUSTON, Aug. 10, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced financial results for the second quarter ended June 30, 2023.

Mark D. Walker, Chairman and Chief Executive Officer, commented, “We are thrilled to report substantial growth this quarter in both our buy- and sell-side businesses. We continue to see a shift in media spend from traditional to digital as well as an increase in media spend targeted at the middle market. The results of our second quarter begin to demonstrate the fruits of our previous strategic investments across our platform and we will continue executing on our growth strategies in the back half of the year.”

Keith Smith, President, added, “We find the current market dynamics to be greatly favorable for Direct Digital Holdings as we continue to see strong demand for our advertising solutions within the numerous industries in which we operate. Our unique, differentiated approach to both the buy- and sell-side verticals within our business continue to separate Direct Digital Holdings from the rest and we greatly look forward to growing all aspects of our business through the rest of 2023 and beyond.”

Second Quarter 2023 Business Highlights

For the second quarter ended June 30, 2023, Direct Digital Holdings processed approximately 300 billion monthly impressions through its sell-side advertising segment, an increase of 205% over the same period of 2022.

In addition, the Company’s sell-side advertising platforms received over 11.2 billion bid responses in the second quarter of 2023, an increase of over 70% over the same period in 2022, through 119,000 advertisers for the quarter, which equates to a 34% increase over the same period in 2022.

The Company’s buy-side advertising segment served approximately 227 customers in the second quarter of 2023, a decrease of 7% compared to the same period of 2022. However, revenue per customer of $52,000 in the second quarter of 2023 increased 36% compared to the same period of 2022.

Second quarter 2023 Financial Highlights:

Revenue was $35.4 million in the second quarter of 2023, an increase of $14.1 million, or 67% over the $21.3 million in the same period of 2022.

Sell-side advertising segment revenue grew to $23.6 million and contributed $11.7 million of the increase, or 98% growth over the $11.9 million of sell-side revenue in the same period of 2022.

Buy-side advertising segment revenue grew to $11.8 million and contributed $2.5 million of the increase, or 27% growth over the $9.3 million of buy-side revenue in the same period of 2022.

Consolidated operating income was $2.3 million for the second quarter of 2023 compared to consolidated operating income of $3.1 million in the same period of 2022.

The operating income of our business segments for the second quarter of 2023 was $6.1 million compared to the operating income of our business segments of $4.8 million in the same period of 2022, an increase of 28% year-over-year.

Net income was $1.2 million in the second quarter of 2023, compared to net income of $2.6 million in the same period of 2022. Net income was negatively impacted by higher operating expenses associated with investments in growth as well as operating as a public company and higher interest expense.

Adjusted EBITDA(1) was $3.1 million in the second quarter 2023, compared to $3.6 million in the same period of 2022.

Financial Outlook

Assuming the U.S. economy does not experience any major economic conditions that deteriorate or otherwise significantly reduce advertiser demand, we are increasing our previously issued estimate as disclosed in our Q1 2023 update:

For fiscal year 2023, we expect revenue to be in the range of $125 million to $130 million, or 43% year-over-year growth at the mid-point.

“Our financial results illustrate the momentum we continue to see in our overall business and specifically a strong acceleration within our sell-side segment. We have also further solidified our balance sheet and provided the company additional financial flexibility via our previously announced $5 million revolving credit facility, positioning us well to continue growing in 2023 and maximizing value for our shareholders,” commented Diana Diaz, Chief Financial Officer.

Conference Call and Webcast Details

Direct Digital Holdings will host a conference call on Thursday, August 10, 2023 at 5:00 p.m. Eastern Time to discuss the Company’s second quarter 2023 financial results. The live webcast and replay can be accessed at https://ir.directdigitalholdings.com/. Please access the website at least fifteen minutes prior to the call to register, download and install any necessary audio software. For those who cannot access the webcast, a replay will be available at https://ir.directdigitalholdings.com/ for a period of twelve months.

Footnotes

(1) “Adjusted EBITDA” is a non-GAAP financial measure. The section titled “Non-GAAP Financial Measures” below describes our usage of non-GAAP financial measures and provides reconciliations between historical GAAP and non-GAAP information contained in this press release.

Forward Looking Statements

This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to the Company. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this press release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; our limited operating history, which could result in our past results not being indicative of future operating performance; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, on receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the Securities and Exchange Commission that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this press release to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

About Direct Digital Holdings

Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 136,000 clients monthly, generating over 250 billion impressions per month across display, CTV, in-app and other media channels.

CONSOLIDATED BALANCE SHEETS

June 30, 2023

December 31, 2022

ASSETS

CURRENT ASSETS

Cash and cash equivalents

$

5,668,479

$

4,047,453

Accounts receivable, net

29,628,797

26,354,114

Prepaid expenses and other current assets

1,051,982

883,322

Total current assets

36,349,258

31,284,889

Property, equipment and software, net of accumulated depreciation and amortization of $155,698 and $34,218, respectively

688,716

673,218

Goodwill

6,519,636

6,519,636

Intangible assets, net

12,660,850

13,637,759

Deferred tax asset, net

5,170,870

5,164,776

Operating lease right-of-use assets

714,129

798,774

Other long-term assets

46,987

46,987

Total assets

$

62,150,446

$

58,126,039

LIABILITIES AND STOCKHOLDERS’ EQUITY

CURRENT LIABILITIES

Accounts payable

$

23,357,665

$

17,695,404

Accrued liabilities

3,879,420

4,777,764

Liability related to tax receivable agreement, current portion

40,112

182,571

Notes payable, current portion

982,500

655,000

Deferred revenues

950,831

546,710

Operating lease liabilities, current portion

47,668

91,989

Income taxes payable

22,280

174,438

Related party payables

1,197,175

1,448,333

Total current liabilities

30,477,651

25,572,209

Notes payable, net of short-term portion and deferred financing cost of $1,858,720 and $2,115,161, respectively

22,515,030

22,913,589

Economic Injury Disaster Loan

150,000

150,000

Liability related to tax receivable agreement, net of current portion

4,246,263

4,149,619

Operating lease liabilities, net of current portion

741,771

745,340

Total liabilities

58,130,715

53,530,757

COMMITMENTS AND CONTINGENCIES (Note 9)

STOCKHOLDERS’ EQUITY

Class A common stock, $0.001 par value per share, 160,000,000 shares authorized, 3,519,780 and 3,252,764 shares issued and outstanding, respectively

3,520

3,253

Class B common stock, $0.001 par value per share, 20,000,000 shares authorized, 11,278,000 shares issued and outstanding

11,278

11,278

Additional paid-in capital

8,539,858

8,224,012

Accumulated deficit

(4,534,925)

(3,643,261)

Total stockholders’ equity

4,019,731

4,595,282

Total liabilities and stockholders’ equity

$

62,150,446

$

58,126,039

CONSOLIDATED STATEMENTS OF OPERATIONS

For the Three Months Ended

For the Six Months Ended

June 30,

June 30,

2023

2022

2023

2022

Revenues

Buy-side advertising

$

11,803,092

$

9,321,267

$

19,242,758

$

15,152,308

Sell-side advertising

23,600,708

11,940,041

37,383,952

17,479,337

Total revenues

35,403,800

21,261,308

56,626,710

32,631,645

Cost of revenues

Buy-side advertising

4,587,897

3,154,471

7,537,050

5,223,817

Sell-side advertising

20,743,266

9,771,017

32,583,972

14,291,209

Total cost of revenues

25,331,163

12,925,488

40,121,022

19,515,026

Gross profit

10,072,637

8,335,820

16,505,688

13,116,619

Operating expenses

Compensation, taxes and benefits

4,553,029

3,494,692

8,187,325

6,049,728

General and administrative

3,265,160

1,776,981

6,205,254

3,417,873

Total operating expenses

7,818,189

5,271,673

14,392,579

9,467,601

Income from operations

2,254,448

3,064,147

2,113,109

3,649,018

Other income (expense)

Other income

42,313

—

92,141

47,982

Forgiveness of Paycheck Protection Program loan

—

287,143

—

287,143

Loss on redemption of non-participating preferred units

—

—

—

(590,689)

Contingent loss on early termination of line of credit

—

—

(299,770)

—

Interest expense

(1,027,493)

(650,251)

(2,044,794)

(1,364,038)

Total other expense

(985,180)

(363,108)

(2,252,423)

(1,619,602)

Income (loss) before taxes

1,269,268

2,701,039

(139,314)

2,029,416

Tax expense (benefit)

74,312

86,676

(336)

86,676

Net income (loss)

$

1,194,956

$

2,614,363

$

(138,978)

$

1,942,740

Net income (loss) per common share:

Basic

$

0.08

$

0.18

$

(0.01)

$

0.18

Diluted

$

0.08

$

0.18

$

(0.01)

$

0.18

Weighted-average number of shares of common stock outstanding:

Basic

14,772,624

14,257,827

14,676,096

10,701,715

Diluted

14,834,051

14,257,827

14,676,096

10,701,715

CONSOLIDATED STATEMENTS OF CASH FLOWS

For the Six Months Ended June 30,

2023

2022

Cash Flows Provided By Operating Activities:

Net income (loss)

$

(138,978)

$

1,942,740

Adjustments to reconcile net income (loss) to net cash provided by operating activities:

Amortization of deferred financing costs

272,008

301,105

Amortization of intangible assets

976,909

976,909

Amortization of right-of-use assets

84,645

50,021

Amortization of capitalized software

104,005

—

Depreciation of property and equipment

17,475

—

Stock-based compensation

304,013

15,407

Forgiveness of Paycheck Protection Program loan

—

(287,143)

Deferred income taxes

(6,094)

38,966

Payment on tax receivable agreement

(45,815)

—

Loss on redemption of non-participating preferred units

—

590,689

Contingent loss on early termination of line of credit

299,770

—

Bad debt expense

51,532

24,799

Changes in operating assets and liabilities:

Accounts receivable

(3,326,215)

(6,996,667)

Prepaid expenses and other assets

(256,496)

386,258

Accounts payable

5,662,261

3,406,355

Accrued liabilities

(769,344)

601,699

Income taxes payable

(152,158)

47,710

Deferred revenues

404,121

(905,111)

Operating lease liability

(47,890)

(49,422)

Related party payable

(251,158)

(70,801)

Net cash provided by operating activities

3,182,591

73,514

Cash Flows Used In Investing Activities:

Cash paid for capitalized software and property and equipment

(136,978)

—

Net cash used in investing activities

(136,978)

—

Cash Flows Provided by (Used In) Financing Activities:

Payments on term loan

(327,500)

(275,000)

Payments of litigation settlement

(129,000)

—

Payment of deferred financing costs

(227,501)

(185,093)

Proceeds from Issuance of Class A common stock, net of transaction costs

—

11,212,043

Redemption of common units

—

(3,237,838)

Redemption of non-participating preferred units

—

(7,046,251)

Proceeds from warrants exercised

12,100

—

Distributions to members

(752,686)

(309,991)

Net cash provided by (used in) financing activities

(1,424,587)

157,870

Net increase in cash and cash equivalents

1,621,026

231,384

Cash and cash equivalents, beginning of the period

4,047,453

4,684,431

Cash and cash equivalents, end of the period

$

5,668,479

$

4,915,815

Supplemental Disclosure of Cash Flow Information:

Cash paid for taxes

$

348,862

$

—

Cash paid for interest

$

1,769,452

$

1,058,548

Non-cash Financing Activities:

Transaction costs related to issuances of Class A shares included in accrued liabilities

$

—

$

1,045,000

Common unit redemption balance included in accrued liabilities

$

—

$

3,962,162

Outside basis difference in partnership

$

—

$

3,234,000

Tax receivable agreement payable to Direct Digital Management, LLC

$

—

$

2,748,900

Tax benefit on tax receivable agreement

$

—

$

485,100

NON-GAAP FINANCIAL MEASURES

In addition to our results determined in accordance with U.S. generally accepted accounting principles (“GAAP”), including, in particular operating income, net cash provided by operating activities, and net income, we believe that earnings before interest, taxes, depreciation and amortization (“EBITDA”), as adjusted for stock compensation expense, loss on early termination of line of credit, and loss on early extinguishment of debt, and loss on early redemption of non-participating preferred units (“Adjusted EBITDA”), a non-GAAP financial measure, is useful in evaluating our operating performance. The most directly comparable GAAP measure to Adjusted EBITDA is net income (loss).

In addition to operating income and net income, we use Adjusted EBITDA as a measure of operational efficiency. We believe that this non-GAAP financial measure is useful to investors for period-to-period comparisons of our business and in understanding and evaluating our operating results for the following reasons:

Adjusted EBITDA is widely used by investors and securities analysts to measure a company’s operating performance without regard to items such as depreciation and amortization, interest expense, provision for income taxes, and certain one-time items such as acquisition transaction costs and gains from settlements or loan forgiveness that can vary substantially from company to company depending upon their financing, capital structures and the method by which assets were acquired;

Our management uses Adjusted EBITDA in conjunction with GAAP financial measures for planning purposes, including the preparation of our annual operating budget, as a measure of operating performance and the effectiveness of our business strategies and in communications with our board of directors concerning our financial performance; and

Adjusted EBITDA provides consistency and comparability with our past financial performance, facilitates period-to-period comparisons of operations, and also facilitates comparisons with other peer companies, many of which use similar non-GAAP financial measures to supplement their GAAP results.

Our use of this non-GAAP financial measure has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our financial results as reported under GAAP. The following table presents a reconciliation of Adjusted EBITDA to net income (loss) for each of the periods presented:

NON-GAAP FINANCIAL METRICS(unaudited)

For the Three Months Ended June 30,

For the Six Months Ended June 30,

2023

2022

2023

2022

Net income (loss)

$

1,194,956

$

2,614,363

$

(138,978)

$

1,942,740

Add back (deduct):

Interest expense

1,027,493

650,251

2,044,794

1,364,038

Stock-based compensation

209,475

15,407

304,014

15,407

Amortization of intangible assets

488,455

488,455

976,909

976,909

Depreciation and amortization of property and equipment

64,988

—

121,480

—

Contingent loss on early termination of line of credit

—

—

299,770

—

Tax expense (benefit)

74,312

86,676

(336)

86,676

Forgiveness of PPP loan

—

(287,143)

—

(287,143)

Loss on early redemption of non-participating preferred units

Largo has a long and successful history as one of the world’s preferred vanadium companies through the supply of its VPURE™ and VPURE+™ products, which are sourced from one of the world’s highest-grade vanadium deposits at the Company’s Maracás Menchen Mine in Brazil. Aiming to enhance value creation at Largo, the Company is in the process of implementing a titanium dioxide pigment plant using feedstock sourced from its existing operations in addition to advancing its U.S.-based clean energy division with its VCHARGE vanadium batteries. Largo’s VCHARGE vanadium batteries contain a variety of innovations, enabling an efficient, safe and ESG-aligned long duration solution that is fully recyclable at the end of its 25+ year lifespan. Producing some of the world’s highest quality vanadium, Largo’s strategic business plan is based on two pillars: 1.) leading vanadium supplier with an outlined growth plan and 2.) U.S.-based energy storage business support a low carbon future.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Quarterly results were below expectations as a decline in vanadium prices and lower sales led to decreased revenues. The company is working hard to return mining activity to normal levels while at the same time reducing costs. Largo had been making strides toward achieving both goals, even if the financial numbers do not demonstrate the improvement due to the decline in vanadium prices. Largo sold less than it produced reversing a trend in the first quarter, as expected.

Vanadium prices declined 19% to $8.46/lb. Largo received a premium to benchmark prices during the quarter that it did not receive in the first quarter. We believe improving premiums reflect additional drilling in the first half of the year that allowed the company to blend vanadium concentrations and achieve a higher-premium product. Vanadium prices continued to sink during the quarter and were $7.98/lb. on June 30, 2023. Management indicates that vanadium prices have stabilized since the end of June and showed some signs of improving.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Harte Hanks (NASDAQ: HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract, and engage their customers. Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony, and IBM among others. Headquartered in Chelmsford, Massachusetts , Harte Hanks has over 2,500 employees in offices across the Americas, Europe and Asia Pacific .

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q2 results. The company reported Q2 revenue of $47.8 million, 3% lower than our estimate of $49.3 million. The slight miss was attributed to softer than expected revenues from Marketing Services and Fulfillment & Logistics. Adj. EBITDA in the quarter was $4.4 million, which beat our estimate of $3.9 million by 12.6%. The favorable adj. EBITDA surprise was due to stronger than expected Customer Care revenue, which boasts higher margins than its other revenue streams.

Second-half outlook. Management indicated that Q3 and Q4 likely will be similar to the revenue baseline of Q2 results. Notably, management highlighted that each quarter is expected to be profitable due to costs and expected improvements in the Customer Care pipeline.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Alvopetro Energy Ltd.’s vision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Alvopetro reported financial results for the quarter ended June 30, 2023 that were above our expectations. Results reflect a decline in production volume which had been preannounced through monthly production releases and thus expected. Realized gas prices were above expectations. Favorable results also reflect a decline in royalty rates. Royalty rates for natural gas production are based on Henry Hub natural gas prices, not realized gas sales prices. Henry Hub prices have been weak relative to realized gas prices resulting in a lower rate per boe produced.

Alvopetro is taking steps to replace production. The decline in production began in April and reflect higher nominations claimed by Alvopetro’s partner in the Cabure Field. Higher partner nominations will mean Alvopetro will own more of future production when prices are expected to be higher. Meanwhile, Alvopetro has accelerated drilling in fields in which it has a 100% ownership. We believe production from these wells will replace the production decline and even has the potential to double production levels in the next four years using internally generated cash.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

One Stop Systems, Inc. (OSS) designs and manufactures innovative AI Transportable edge computing modules and systems, including ruggedized servers, compute accelerators, expansion systems, flash storage arrays, and Ion Accelerator™ SAN, NAS, and data recording software for AI workflows. These products are used for AI data set capture, training, and large-scale inference in the defense, oil and gas, mining, autonomous vehicles, and rugged entertainment applications. OSS utilizes the power of PCI Express, the latest GPU accelerators and NVMe storage to build award-winning systems, including many industry firsts, for industrial OEMs and government customers. The company enables AI on the Fly® by bringing AI datacenter performance to ‘the edge,’ especially on mobile platforms, and by addressing the entire AI workflow, from high-speed data acquisition to deep learning, training, and inference. OSS products are available directly or through global distributors. For more information, go to www.onestopsystems.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q23 Results. Revenue of $17.2 million, slightly below guidance and down 6% y-o-y, reflecting the continued runoff of the Disguise business. Higher operating expenses, including some one-time items, drove a net loss of $2.4 million, or a loss of $0.12/sh in the quarter, compared to net income of $322,822, or EPS of $0.02/sh per share last year. We had forecast a net loss of $415,700, or a loss of $0.02/sh. Adjusted EPS was $0.01 compared to $0.04 last year.

Delays and Departures. The decline in Disguise (substantially complete), delays in defense and commercial program orders, and the exit of an autonomous trucking client, a top 10 client in 2022, have combined to stall the momentum of OSS’ business. Revenue guidance for 3Q23 is $13.5 million, a level last seen in the first quarter of 2021.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Onconova Therapeutics is a clinical-stage biopharmaceutical company focused on discovering and developing novel products for patients with cancer. The Company has proprietary targeted anti-cancer agents designed to disrupt specific cellular pathways that are important for cancer cell proliferation. Onconova’s novel, proprietary multi-kinase inhibitor narazaciclib (formerly ON 123300) is being evaluated in a combination trial with estrogen blockade in advanced endometrial cancer. Based on preclinical and clinical studies of CDK 4/6 inhibitors, Onconova is also evaluating opportunities for combination studies with narazaciclib in additional indications. Onconova’s product candidate rigosertib is being studied in multiple investigator-sponsored studies. These studies include a dose-escalation and expansion Phase 1/2a study of oral rigosertib in combination with nivolumab in patients with KRAS+ non-small cell lung cancer, a Phase 2 program evaluating rigosertib monotherapy in advanced squamous cell carcinoma complicating recessive dystrophic epidermolysis bullosa (RDEB-associated SCC), and a Phase 2 trial evaluating rigosertib in combination with pembrolizumab in patients with metastatic melanoma.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Incremental Progress Reported During 2Q23. Onconova reported a 2Q23 loss of $4.3 million or $(0.20) per share. R&D expense of $2.5 million was lower than our estimate of $4.5 million, attributed to previous completion of clinical trial start-up costs. We expect clinical costs to rise in coming quarters as patients are accrued and have adjusted our quarterly estimates. We now expect the $29.7 million cash balance to last through 2Q24.

Narazaciclib Makes Progress In Endometrial Cancer. A Phase 1/2 clinical trial testing the combination of narazaciclib with letrozole (Femara, from Novartis) in LGEEC (low grade endometrioid endometrial cancer) began treating patients in 1Q23. Onconova plans to announce results in 4Q23 including safety, pharmacokinetics, and a recommended Phase 2 dose. The Phase 2 trial is planned for 1H24 as a randomized trial against standard therapy.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q2 in line. The company reported Q2 revenue of $35.4 million, above our previously lowered forecast of $29.7 million. Adj. EBITDA of $3.1 million was largely in line with our forecast of $3.2 million. Total company revenue grew a strong 66.5% over the prior year period, despite economic headwinds.

Sell-side revenue bucks trends. The robust revenue growth in the quarter was lead by the company’s Sell-side programmatic platform. Sell-side revenue nearly doubled (+97.7%) over the prior year period to $23.6 million. We believe the strong results reflect well on the technology investments management has made to position the platform for favorable growth.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

How the Popularity of Parlay Betting is Helping the Major Players

The business of gambling keeps growing as more types of wagers become popular and a friendlier legal environment encourages major players like DraftKings (DKNG) and FanDuel (PDYPF), as well as smaller online sites. A new online betting trend has been particularly profitable for companies who include it in their product line-up. Although specific financials remain undisclosed, parlay betting has dramatically added to the bottom line of some sportsbooks.

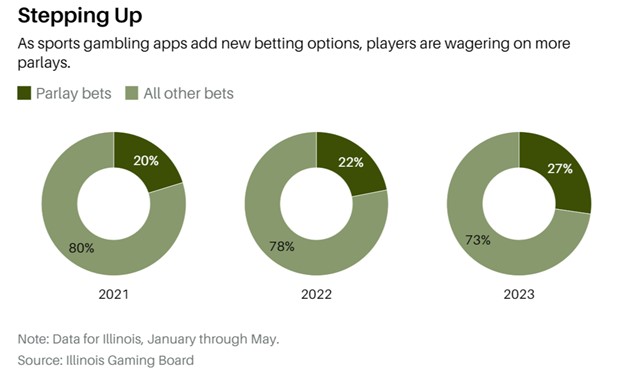

While not public, an analysis published in Barron’s of state gambling regulatory data shows the average amount the house keeps from the wagers is around 20% for parlay bets. This compares quite favorably to the 5% kept by conventional individual outcome wagers.

What is a Parlay Bet?

A parlay bet is a type of sports bet where you combine two or more individual bets into one single all-or-nothing bet. The payout for a parlay bet is much higher than for a single bet, but the probability of winning is much lower.

For example, let’s say you want to bet on the following three NFL games:

The Dallas Cowboys to beat the New York Giants

The Tampa Bay Buccaneers to beat the Philadelphia Eagles

The Miami Dolphins to beat the New York Jets

You could place three separate bets on these games, but you would only win a small amount of money if all three bets won. Instead, you could place a parlay bet on all three games. If you win the parlay bet, you will win a much larger amount.

The payout for a parlay bet is calculated by multiplying the odds of each individual bet together. So, if the odds of the Cowboys winning are 1.50, the odds of the Buccaneers winning are 2.00, and the odds of the Dolphins winning are 1.75, the odds of the parlay bet winning would be 1.50 x 2.00 x 1.75 = 5.25.

This means that if you bet $100 on the parlay bet, you would win $525 if all three bets won.

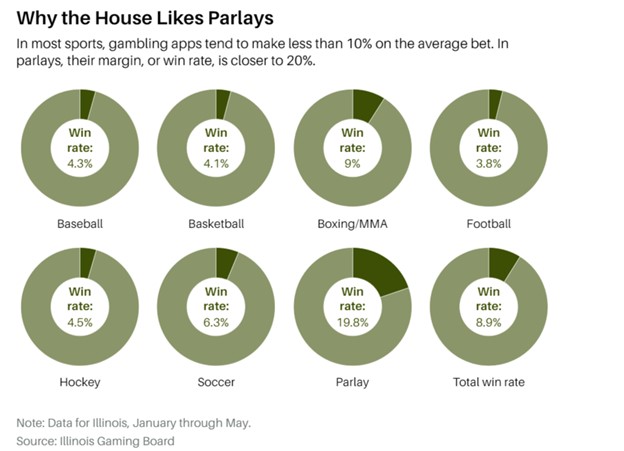

Gambling companies emphasize that parlays are no gimmick. The odds aren’t skewed in the company’s favor or anything shifty; rather, parlays introduce higher odds against bettors due to the cumulative impact of various outcomes. Betting on multiple events, even up to 10, compounds the odds of each event’s success. This is how the casinos’ 4% to 5% edge evolves into a substantial 20%.

Margins are Better for Companies

The increase in earnings from these bets has helped lift stock values much higher than the overall market.

The growing popularity of parlay bets has also served to increase the appetite in the U.S. for sports betting. In 2018 a Supreme Court’s ruling opened the doors for sports gambling, leaving the decision to legalize it to individual states. Since then, 38 states and Washington, D.C. have legalized sports betting, with online betting approved in 24 of them. The operators amassed a gross revenue of $7.5 billion in 2022, as per the American Gaming Association, and numerous analysts speculate that further state legalization and innovative trends such as parlays could propel the market up to $30 billion or more.

The big two, DraftKings and Flutter/FanDuel dominate the market after spending heavily for years on advertising. Their state-of-the-art technology and popular parlays have helped increase market share. The companies are now veering away from over-the-top marketing, as evidenced by the 49% dip in TV ad spending by online sports betting firms in Q2, and DraftKings’ 10% reduction in marketing expenditures in established markets during the latest quarter.

Regardless of market dominance, parlays are poised to proliferate due to their popularity and profitability. While Las Vegas has long capitalized on the attractiveness of quick riches, the advent of online companies’ represents a distinct shift in the dynamics. Unlike casinos that can’t dramatically boost their own profitability in games like blackjack, the digital platforms can reach the masses electronically and digitally.

As mentioned, this surge in parlays resonates with the penchant for sudden riches, and can be witnessed far beyond Las Vegas. The recent Mega-Millions $1.55 billion prize had players lined up in the summer heat to pay for an almost impossible chance of winning. Platforms like Robinhood appealed to the high-risk high-return nature of many and amassed more brokerage customers in a year than any other company in history.

Parlays effectively tap into and profit handsomely off the mentality of all-or-nothing large gains. A mere $10 parlay could translate into thousands in winnings, mirroring the “got to be in it to win it” feeling of the lottery. But here, the bettor can feel more in control.

Take Away

The overall stock market performance is reported each trading day in popular indexes, but there are individual sectors that rise, or fall separately and at a different pace than each index. Index funds and ETF buyers are beginning to realize that a portion of their portfolio invested in industries and companies that are showing more strength than the S&P, Dow, or Nasdaq indexes may allow for enhanced performance. Many keep the largest allocation in an indexed fund or ETF to still maintain the diversification that prompted the indexed fund investment to begin with.

This December hundreds of investors will be attending NobleCon19 in order to discover actionable ideas they can invest in. The investment conference is the place where both professional and self-directed market participants go to become familiar with less mainstream companies and management. You’re invited – go here for all the information you will need to join us in Florida later this year.

X, the Company Formerly Known as Twitter – Here’s Why It Rebranded

If you’re like me, when Elon Musk announced a rebranding of Twitter to the new name X, you waited for the punchline – or thought of it as a stunt. Although weeks later I’m still typing “Twitter” into my search bar, and still refer to posts as tweets.” I have become sure that this is no stunt, it is a business decision. A decision that begs the question, Why?

This week, X’s CEO, Linda Yaccarino shared her insights in a CNBC interview. She explained the company’s decision to rebrand from Twitter, citing alignment with owner Elon Musk’s overall strategic vision for the platform and how Musk, who has owned the URL X.com since his PayPal days, has championed the social media company as the future, all-encompassing app.

“Elon has been talking about X, the everything app, for a very long time,” Yaccarino said during the interview with CNBC’s Sara Eisen. “Even when we announced that I was joining the company, I was joining the company to partner with Elon to transform Twitter into X, the everything app,” Yaccarino said.

Yaccarino, who took the helm in June, indicated the transformation and growth include extended video content, articles, and even subscriptions to content providers.

“Think about what’s happened since the acquisition,” X’s CEO elaborated, “Experiences and evolution into long-form video and articles, subscribe to your favorite creators, who are now earning a real living on the platform. You look at video, and soon you’ll be able to make video chat calls without having to give your phone number to anyone on the platform.”

Attention was brought to the once microblogging platform’s intentions to facilitate transactions between users, friends, and content creators. The past Twitter was confining, she explained, the new brand will allow evolution without a legacy mindset.

“The rebrand represented really a liberation from Twitter,” she said. “A liberation that allowed us to evolve past a legacy mindset and thinking. And to reimagine how everyone, how everyone on Spaces who’s listening, everybody who’s watching around the world. It’s going to change how we congregate, how we entertain, and how we transact all in one platform.”

The CNBC host asked about the risk in light of name recognition, Yaccarino responded likening the change Johnson & Johnson made by spinning off Band-Aids and Tylenol brands under the new name Kenvue. Her reply suggested the tech giant is almost entrepreneurial now, and can begin with a start-up mentality.

“If you stay Twitter, or you stay whatever your previous brand is, change tends to be only incremental. And you get graded by a legacy report card,” Yaccarino said. “And at X we think about what’s possible. Not the incremental change of what can’t be done.” She pointed to the new product changes and infrastructure improvements, saying it “answers the question of ‘why rebrand?’”

About Yaccarino’s Duties

She is operating independently under Musk’s leadership, Yaccarino assured.

“The roles of Elon and myself are well-defined.” She continued, “Elon is working on accelerating the rebrand and working on the future,” adding, “and I’m responsible for the rest. Running the company, from partnerships to legal to sales to finance.”

Questions regarding Yaccarino’s autonomy within Musk’s framework had arisen due to his comprehensive control over the company and his ventures like Tesla and SpaceX.

Yaccarino, formerly a senior advertising executive at NBC Universal, underscored X’s dedication to enhancing the advertiser experience. This commitment arose from brands withdrawing from the platform following Musk’s acquisition of Twitter.

A large part of the Twitter brand has in the past been questioned by advertisers related to trust and safety. Yaccarino disclosed that X’s trust and safety team is now more capable compared to its pre-acquisition state. While acknowledging that not all content may align with everyone’s views, she highlighted efforts to improve the platform’s content environment.

In November, Twitter disbanded its ethical artificial intelligence team and downsized its trust and safety department. This move halted the team’s work on “algorithmic amplification monitoring,” which mainly aimed to scrutinize content amplification during elections and political events. This stands in sharp contrast to the trust which the new brand has been building.

Rebuilding advertiser confidence stands as a large challenge for Yaccarino. Musk has claimed continuous spikes in user engagement, but concrete data supporting these claims are slim. Yaccarino pointed out the return of prominent brands like Coca-Cola and Visa to advertising under her leadership, facilitated by her direct engagement with marketing and communication executives.

Yaccarino asserted that brands are now insulated from the risk of adjacency to problematic content. She acknowledged that content that is “lawful but awful” can be challenging to manage but emphasized the company’s new content controls in reducing such risks for advertisers.

Yaccarino also addressed the threat posed by Meta’s Threads, indicating that while it hasn’t fully taken off since its high-profile launch, it’s essential to stay vigilant about competitors. Despite already commanding substantial advertiser spending through Instagram and Facebook, Meta’s Threads has yet to introduce advertising.

As for a potential octagon face-off between Musk and Meta CEO Mark Zuckerberg, Yaccarino took a playful stance saying that if the event occurred, Musk “is training” and noted the potential for a great brand sponsorship opportunity.

Full Patient Enrollment Expected Within Six Months

ATLANTA, GA, August 10, 2023 — GeoVax Labs, Inc. (Nasdaq: GOVX), a biotechnology company developing immunotherapies and vaccines against cancers and infectious diseases, today announced that vaccinations have begun in an investigator-initiated clinical trial (ClinicalTrials.gov Identifier: NCT05672355) of GEO-CM04S1 in patients with chronic lymphocytic leukemia (CLL), being conducted at City of Hope National Medical Center.

Despite a high vaccination rate, CLL patients may be at high risk for lethal COVID-19 infection due to poor immune response to currently available vaccines. The GEO-CM04S1 vaccine uses a modified vaccinia virus (MVA) backbone to carry SARS-CoV-2 virus antigens that may be more effective at inducing COVID-19 immunity in patients with poor humoral immune responses since MVA strongly induces T cell expansion even in the background of immunosuppression. By targeting both the spike (S) and nucleocapsid (N) protein antigens, GEO-CM04S1 broadens the specificity of the immune responses and protects against the loss of efficacy associated with current vaccines due to the significant sequence variation observed with the spike antigen.

The study is examining the use of two injections of GEO-CM04S1, three months apart, to assess immune responses in these vulnerable patients, with an mRNA vaccine (currently, the Pfizer-BioNTech Bivalent vaccine) as the control arm. Participants will be randomized 1:1 to receive two boosters with either the GEO-CM04S1 or the control vaccine. The primary immune response outcome will be assessed at 56 days following the first booster injection. Up to 40 participants in each arm will be vaccinated, with immune responses evaluated and compared at the interim and final analyses.

David Dodd, GeoVax President and CEO, stated, “We are very pleased with the rapid start for this third important study for GEO-CM04S1, which we expect will achieve full patient enrollment within six months. We believe the GEO-CM04S1 vaccine, containing the two antigens, S and N, along with the recognized antibody and cellular immune responses resulting from the MVA approach, has the potential to offer greater booster protection than that from the current vaccines in use, as well as provide a greater degree of protection within immunocompromised patients. We expect the CLL trial will add to the data coming from our other ongoing trials, confirming the potential benefit of GEO-CM04S1 in another population of immunocompromised individuals. We look forward to sharing progress reports as we advance.”

About GEO-CM04S1

GEO-CM04S1 is a next-generation COVID-19 vaccine based on GeoVax’s MVA viral vector platform, which supports the presentation of multiple vaccine antigens to the immune system in a single dose. GEO-CM04S1 presents both the spike and nucleocapsid antigens of SARS-CoV-2 and is specifically designed to induce both antibody and T cell responses to non-variable parts of the virus. The more broadly specific and functional engagement of the immune system is designed to protect against the new and continually emerging variants of COVID-19. Based on data from animal models and a completed Phase 1 clinical study, vaccine-induced immune responses were shown to recognize both early and later variants of SARS-CoV-2, including the Omicron variant. Vaccines of this format should not require repeated modification and updating.

A recent presentation of unpublished data from the open-label portion of the Phase 2 trial of GEO-CM04S1 (ClinicalTrials.gov Identifier: NCT04977024) in patients undergoing hematological cancer treatment (i.e., patients who have reduced immune system function as a result of treatment) indicates that GEO-CM04S1 is highly immunogenic in these patients, inducing both antibody responses, including neutralizing antibodies, and T cell responses. These data support the planned progression of the Phase 2 clinical study, which will include a direct comparison to currently approved mRNA vaccines. GEO-CM04S1 also continues to advance in another Phase 2 clinical trial as a booster for healthy patients who have previously received the Pfizer or Moderna mRNA vaccine (ClinicalTrials.gov Identifier: NCT04639466). Data from these studies will form the basis for comparing vaccine potential in unique patient groups as well as the general population.

About GeoVax