MIAMI, Jan. 30, 2023 (GLOBE NEWSWIRE) — Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games” or the “Company”) today announced that the Company has entered into a debt-for-equity exchange agreement (the “Agreement”) with its majority stockholder, Motorsport Network, LLC (“Motorsport Network”), to repay $1,000,000 in debt (including principal and accrued and not yet paid interest) of the Company under its $12 million line of credit with Motorsport Network.

Under the Agreement, for a period of 60 days from the closing of the transactions contemplated under the Agreement, the Company agreed to file a registration statement with the Securities and Exchange Commission (“SEC”) upon Motorsport Network’s demand in order to register the resale of the shares acquired by Motorsport Network under the Agreement, subject to the terms and conditions of the Agreement. The Agreement also granted certain piggyback registration rights to Motorsport Network.

“This debt exchange benefits our balance sheet, allows us to pay less interest expense and will help Motorsport Games to pursue product development and growth opportunities,” said Dmitry Kozko, CEO and Executive Chairman of Motorsport Games. “This debt exchange also signals the ongoing confidence that our majority shareholder, Motorsport Network, has in Motorsport Games.”

The foregoing summary of the Agreement is incomplete, and further details relating to the Agreement, including additional terms and conditions, and this transaction will be contained in the Current Report on Form 8-K the Company intends to file with the SEC later today.

About Motorsport Games:

Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Forward Looking Statements:

Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, without limitation, issuance of shares of Class A common stock under the Agreement impacting the value of the Company’s Class A common stock and less than expected benefits, such as the ability to develop product and achieve growth, from any transaction under the Agreement. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the SEC, including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

MIAMI, Jan. 30, 2023 (GLOBE NEWSWIRE) — Adam Breeden, the pioneer of competitive socialising in the UK and entrepreneurial force behind some of the sector’s most successful concepts, has officially opened his most ambitious and exciting project. F1® Arcade, the world’s first official premium F1 experiential venue, opened on December 12, 2022 in London at One New Change, St Pauls.

The immersive state of the art F1 racing simulation experience comes with 60 motion F1 simulators, powered by the rFactor 2 racing simulation software provided by Motorsport Games, combined with exclusive F1® content, enabling guests to live the thrill of racing, complemented by a best-in-class food and beverage offering created by an executive chef and expert mixologists.

“With a mission of making the thrill of motorsports available to everyone, we graciously appreciate the selection of rFactor 2 to provide the virtual racing experience and real world handling and competition to F1® Arcade and their customers!” said Dmitry Kozko, CEO, at Motorsport Games Inc. (NASDAQ: MSGM) (“Motorsport Games”), a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world.

Dom Duhan, Executive Producer at Studio 397 added, “It was a pleasure for our expert simulation development team at Studio 397 to collaborate on developing the racing elements, and we expect that customers will be blown away by the experience.”

“Since opening F1® Arcade in December, the take up has been absolutely phenomenal. Our ambition was to introduce a truly innovative experience that makes sim racing accessible for all in a fun and premium competitive socialising environment. To deliver on this, we needed a partner that could fully tailor the game experience, which is why we selected rFactor 2 and Motorsport Games to work with us on this project. The reaction from customers in our first month has been fantastic and we look forward to welcoming many more at our first London venue and future venues as we expand,” said Adam Breeden, Founder and Chief Executive of Kindred Concepts.

Future plans for F1® Arcade include a Birmingham, UK site in 2023 with further locations powered by rFactor 2 set to be announced. For all F1® Arcade news, be sure to follow @F1Arcade on social media platforms.

About Motorsport Games: Motorsport Games, a Motorsport Network company, is a leading racing game developer, publisher and esports ecosystem provider of official motorsport racing series throughout the world. Combining innovative and engaging video games with exciting esports competitions and content for racing fans and gamers, Motorsport Games strives to make the joy of racing accessible to everyone. The Company is the officially licensed video game developer and publisher for iconic motorsport racing series across PC, PlayStation, Xbox, Nintendo Switch and mobile, including NASCAR, INDYCAR, 24 Hours of Le Mans and the British Touring Car Championship (“BTCC”), as well as the industry leading rFactor 2 and KartKraft simulations. rFactor 2 also serves as the official sim racing platform of Formula E, while also powering F1 Arcade through a partnership with Kindred Concepts. Motorsport Games is an award-winning esports partner of choice for 24 Hours of Le Mans, Formula E, BTCC, the FIA World Rallycross Championship and the eNASCAR Heat Pro League, among others. Motorsport Games is building a virtual racing ecosystem where each product drives excitement, every esports event is an adventure and every story inspires.

Forward-Looking Statements: Certain statements in this press release which are not historical facts are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Any statements in this press release that are not statements of historical fact may be deemed forward-looking statements. Words such as “continue,” “will,” “may,” “could,” “should,” “expect,” “expected,” “plans,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” and similar expressions are intended to identify such forward-looking statements. These forward-looking statements include, but are not limited to, statements concerning expectations and benefits of the rFactor 2 simulation platform in powering F1® Arcade, as well as expectations that future F1® Arcade locations will be powered by the rFactor 2 simulation platform. All forward-looking statements involve significant risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements, many of which are generally outside the control of Motorsport Games and are difficult to predict. Examples of such risks and uncertainties include, but are not limited to: difficulties, delays in or unanticipated events that may impact the timing and expected benefits of the rFactor 2 simulation platform, such as rFactor 2 updates and/or related products and features. Factors other than those referred to above could also cause Motorsport Games’ results to differ materially from expected results. Additional examples of such risks and uncertainties include, but are not limited to: (i) delays and higher than anticipated expenses related to the ongoing and prolonged COVID-19 pandemic, any resurgence of COVID-19 and the Russia invasion of Ukraine; (ii) Motorsport Games’ ability (or inability) to maintain existing, and to secure additional, licenses and other agreements with various racing series; (iii) Motorsport Games’ ability to successfully manage and integrate any joint ventures, acquisitions of businesses, solutions or technologies; (iv) unanticipated operating costs, transaction costs and actual or contingent liabilities; (v) the ability to attract and retain qualified employees and key personnel; (vi) adverse effects of increased competition; (vii) changes in consumer behavior, including as a result of general economic factors, such as increased inflation, higher energy prices and higher interest rates; (viii) Motorsport Games’ inability to protect its intellectual property; and/or (ix) local, industry and general business and economic conditions. Additional factors that could cause actual results to differ materially from those expressed or implied in the forward-looking statements can be found in Motorsport Games’ filings with the Securities and Exchange Commission (the “SEC”), including its Annual Report on Form 10-K for the fiscal year ended December 31, 2021, its Quarterly Reports on Form 10-Q filed with the SEC during 2022, as well as in its subsequent filings with the SEC. Motorsport Games anticipates that subsequent events and developments may cause its plans, intentions and expectations to change. Motorsport Games assumes no obligation, and it specifically disclaims any intention or obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as expressly required by law. Forward-looking statements speak only as of the date they are made and should not be relied upon as representing Motorsport Games’ plans and expectations as of any subsequent date. Additionally, the business and financial materials and any other statement or disclosure on, or made available through, Motorsport Games’ website or other websites referenced or linked to this press release shall not be incorporated by reference into this press release.

Website and Social Media Disclosure:

Investors and others should note that we announce material financial information to our investors using our investor relations website (ir.motorsportgames.com), SEC filings, press releases, public conference calls and webcasts. We use these channels, as well as social media and blogs, to communicate with our investors and the public about our company and our products. It is possible that the information we post on our websites, social media and blogs could be deemed to be material information. Therefore, we encourage investors, the media and others interested in our company to review the information we post on the websites, social media channels and blogs, including the following (which list we will update from time to time on our investor relations website):

CHATHAM, N.J., Jan. 30, 2023 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a clinical-stage biopharmaceutical company, announced today that it has regained compliance with the minimum bid price requirement for continued listing on The Nasdaq Capital Market. On January 27, 2023, Tonix received a letter from The Nasdaq Stock Market LLC stating that because Tonix’s shares had a closing bid price at or above $1.00 per share for a minimum of 10 consecutive business days, Tonix’s stock had regained compliance with the minimum bid price requirement of $1.00 per share for continued listing on The Nasdaq Capital Market, as set forth in Nasdaq Listing Rule 5550(a)(2), and the matter is now closed.

Tonix Pharmaceuticals Holding Corp.*

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022 and interim data expected in the second quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix initiated a Phase 2 study in Long COVID in the third quarter of 2022 and expects interim data in the third quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the first quarter of 2023. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is expected to enter the clinic with a Phase 2 study in the first quarter of 2023. TNX-601 ER (tianeptine hemioxalate extended-release tablets) is a once-daily formulation of tianeptine being developed as a potential treatment for major depressive disorder (MDD) with a Phase 2 study expected to be initiated in the first quarter of 2023. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the first half of 2023. Tonix’s infectious disease pipeline includes a vaccine in development to prevent smallpox and monkeypox, TNX-801, a next-generation vaccine to prevent COVID-19, TNX-1850, a platform to make fully human monoclonal antibodies to treat COVID-19, TNX-3600, and humanized anti-SARS-CoV-2 monoclonal antibodies, TNX-3800, recently licensed from Curia. TNX-801, Tonix’s vaccine in development to prevent smallpox and monkeypox, also serves as the live virus vaccine platform or recombinant pox vaccine (RPV) platform for other infectious diseases. A Phase 1 study of TNX-801 is expected to be initiated in Kenya in the second half of 2023.

*All of Tonix’s product candidates are investigational new drugs or biologics and have not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2021, as filed with the Securities and Exchange Commission (the “SEC”) on March 14, 2022, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

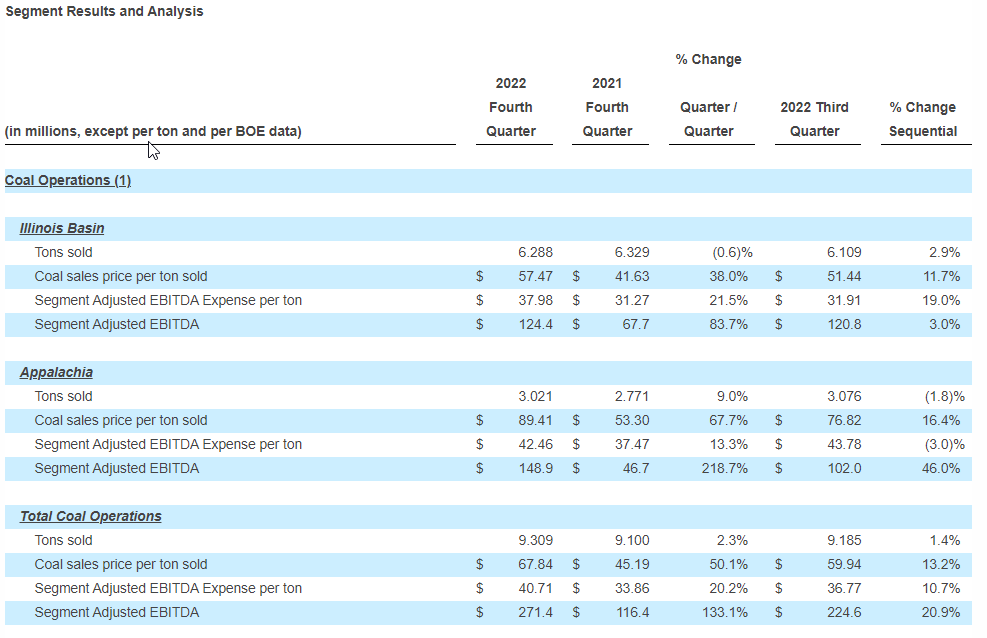

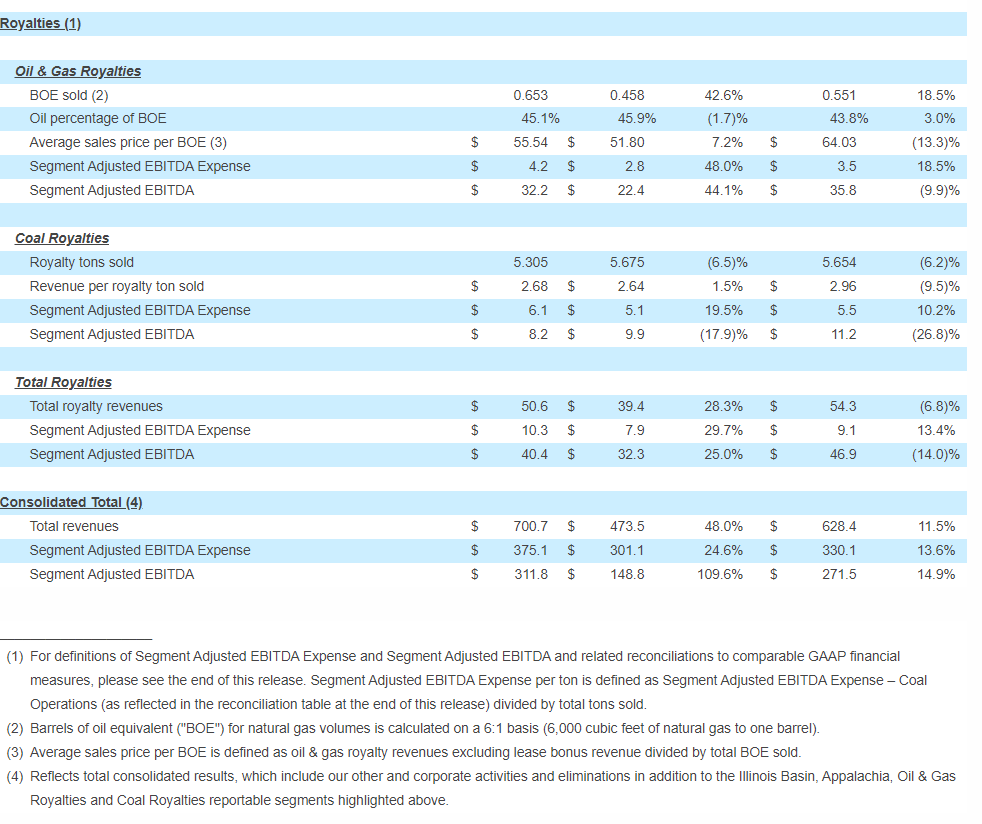

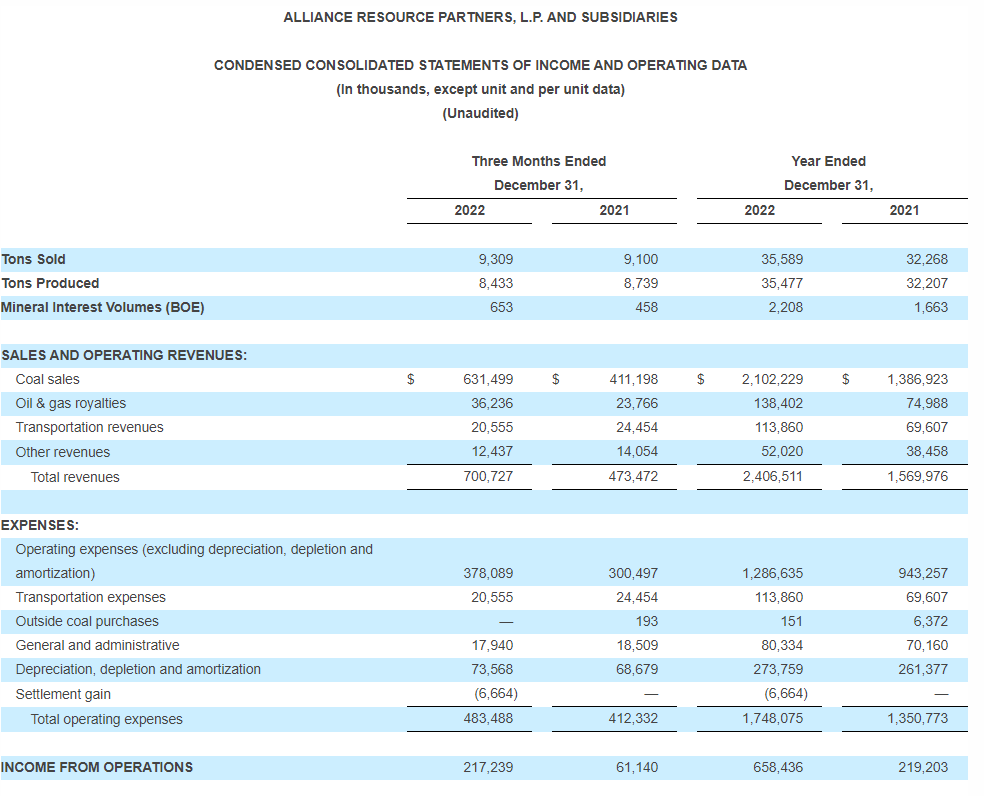

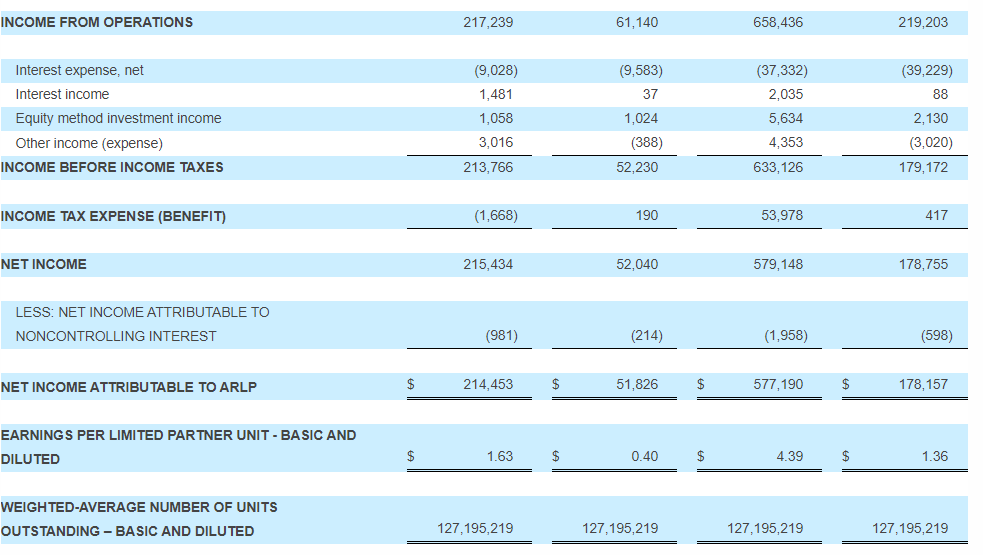

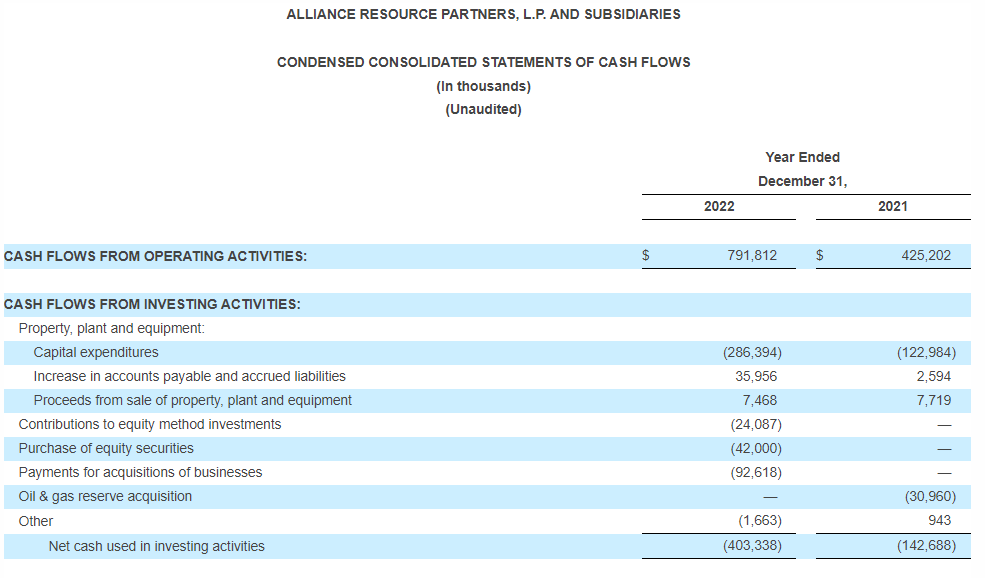

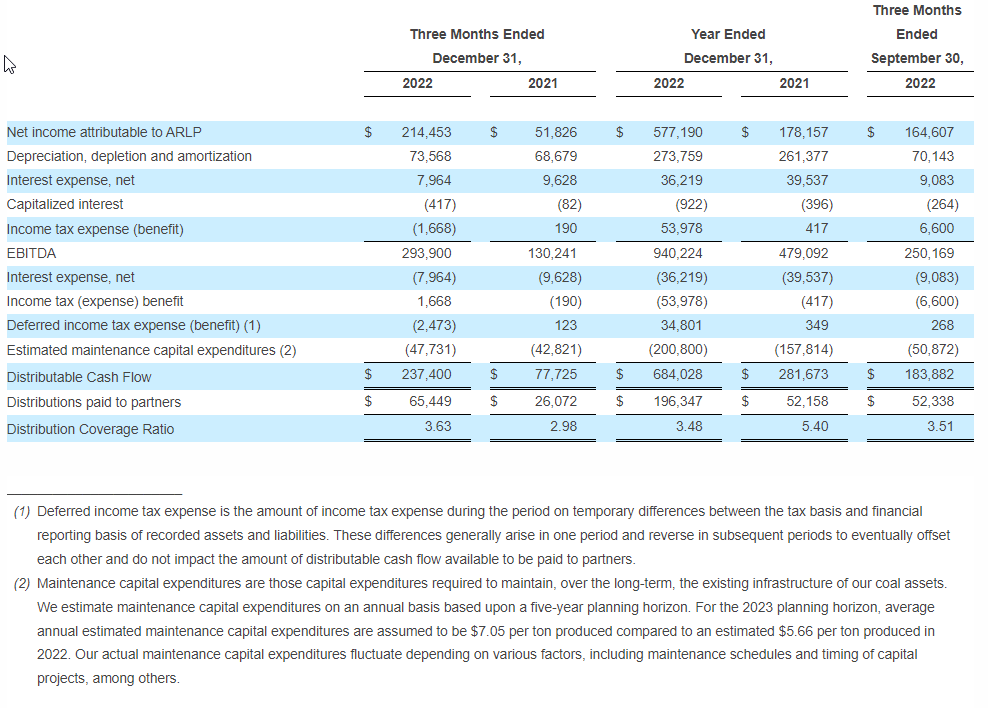

Fourth quarter 2022 revenue of $700.7 million, net income of $214.5 million, and EBITDA of $293.9 million, up 48.0%, 313.8%, and 125.7%, respectively, year-over-year

Record full year 2022 revenue of $2.4 billion, net income of $577.2 million, and EBITDA of $940.2 million, up 53.3%, 224.0%, and 96.3%, respectively, year-over-year

In January 2023, increased quarterly cash distribution rate to $0.70 per unit, or $2.80 per unit annualized, up 40.0% from the last quarter and 180.0% year-over-year

In January 2023, increased unit repurchase program to $100.0 million

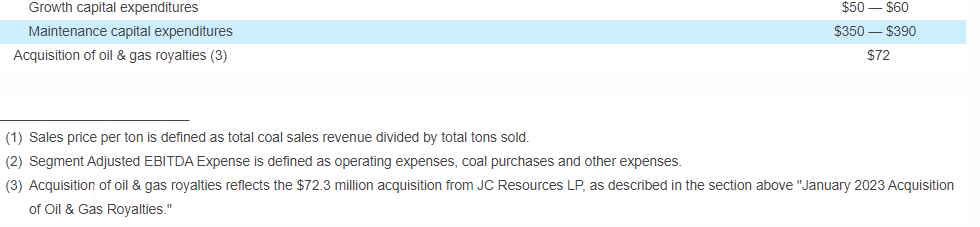

Completed $81.2 million acquisition of previously announced oil & gas mineral interests in October 2022, and today, separately announced a $72.3 million acquisition of oil & gas mineral interests

In January 2023, successfully refinanced existing revolving credit facility, extending liquidity and financial flexibility through March 2027

2023 expected coal sales volumes approximately 94% committed and priced above 2022 per ton levels

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported substantial increases to financial and operating results for the quarter and year ended December 31, 2022 (the “2022 Quarter” and “2022 Full Year”, respectively) compared to the quarter and year ended December 31, 2021 (the “2021 Quarter” and “2021 Full Year”, respectively).

Total revenues in the 2022 Quarter increased 48.0% to a record $700.7 million compared to $473.5 million for the 2021 Quarter as a result of significantly higher coal sales and oil & gas royalties revenues. Increased revenues, partially offset by higher total operating expenses, led net income for the 2022 Quarter to a record $214.5 million, or $1.63 per basic and diluted limited partner unit, compared to $51.8 million, or $0.40 per basic and diluted limited partner unit, for the 2021 Quarter. EBITDA also increased 125.7% in the 2022 Quarter to $293.9 million compared to $130.2 million in the 2021 Quarter. (Unless otherwise noted, all references in the text of this release to “net income” refer to “net income attributable to ARLP.” For a definition of EBITDA and related reconciliation to its comparable GAAP financial measure, please see the end of this release.)

2022 Full Year performance saw total revenues increase 53.3% to a record $2.4 billion compared to $1.6 billion for the 2021 Full Year, primarily due to substantial increases in prices and volumes from both ARLP’s coal operations and royalty segments. Higher revenues, partially offset by increased total operating and income tax expenses, led to significantly higher net income, which rose 224.0% to a record $577.2 million, or $4.39 per basic and diluted limited partner unit, compared to $178.2 million, or $1.36 per basic and diluted limited partner unit, for the 2021 Full Year. EBITDA increased 96.3% to $940.2 million compared to $479.1 million for the 2021 Full Year.

CEO Commentary

“ARLP’s record performance during the 2022 quarter and full year, in a supply and transportation constrained operating environment, is a testament to our team’s ability to execute and deliver reliable energy supply under challenging circumstances,” commented Joseph W. Craft III, Chairman, President, and Chief Executive Officer. “In 2022, ARLP achieved its highest reported EBITDA and operating cash flow in the Partnership’s 23-year history, driven by continued growth in sales volumes coupled with higher price realizations across our coal operations and royalty segments.”

Mr. Craft added, “With our strong balance sheet and relentless focus on cash flow generation, we are well positioned to capitalize on growth opportunities in the market and return capital to our unitholders. Based on our highly committed coal sales book and visibility into our end markets, last week we were pleased to announce a 40% increase in ARLP’s quarterly cash distribution rate to $0.70 per unit, or $2.80 per unit on an annualized basis. This increase is consistent with our long-term strategic capital allocation plans and is well-supported by strong visibility into future cash flows with approximately 94% of our expected 2023 coal sales volumes committed and priced as we enter the year. I am proud of the team’s record of success, and, as reflected in our initial guidance, look forward to achieving even stronger results in 2023.”

Coal Operations

ARLP’s coal sales prices per ton increased significantly compared to the 2021 Quarter as improved price realizations in both the domestic and export markets drove coal sales prices higher by 38.0% and 67.7% in the Illinois Basin and Appalachia, respectively. Compared to the quarter ended September 30, 2022 (the “Sequential Quarter”), higher export prices led to an 11.7% increase in coal sales price realizations in the Illinois Basin while higher domestic prices primarily from our Tunnel Ridge mine resulted in an increase of 16.4% in Appalachian coal sales prices. Tons sold remained relatively consistent in the Illinois Basin compared to the 2021 Quarter while increasing by 9.0% in Appalachia due primarily to increased sales volumes from Tunnel Ridge as a result of higher recoveries. Compared to the Sequential Quarter, increased sales volumes from our Gibson South and River View mines resulted in 2.9% higher tons sold in the Illinois Basin. Coal sales volumes in Appalachia decreased by 1.8% compared to the Sequential Quarter due to higher sales from inventory at Tunnel Ridge in the Sequential Quarter. ARLP ended the 2022 Quarter with total coal inventory of 0.5 million tons, which included 0.2 million tons staged at ports for vessel export in early 2023.

Segment Adjusted EBITDA Expense per ton increased by 21.5% and 13.3% in the Illinois Basin and Appalachia, respectively, compared to the 2021 Quarter primarily as a result of ongoing inflationary pressures on certain expense items, most notably labor-related expenses, supply and maintenance costs, increased sales-related expenses due to higher price realizations, and $6.5 million of non-cash accruals for certain long-term liabilities. Also specific to the 2022 Quarter, a thermal event at our Hamilton mine resulted in an unexpected outage that lasted approximately four weeks. There were no injuries to personnel, no damage to the equipment, and mining operations returned to normal production levels in December 2022; however, third-party expenses related to the event were approximately $5.8 million and approximately 0.5 million tons of production was lost in the 2022 Quarter. Excluding certain non-cash liability accruals and the Hamilton event related expenses, Illinois Basin Segment Adjusted EBITDA Expense per ton for the 2022 Quarter would have been more in-line with the percentage increases realized in Appalachia for the 2022 Quarter.

Royalties

Segment Adjusted EBITDA for our Oil & Gas Royalties segment increased 44.1% to $32.2 million in the 2022 Quarter compared to $22.4 million in the 2021 Quarter primarily due to significantly higher oil & gas royalty volumes, which rose by 42.6% to a record 653,000 BOE sold as a result of increased drilling and completion activities and additional volumes from oil & gas mineral interest acquisitions completed during 2022. Compared to the Sequential Quarter, Segment Adjusted EBITDA decreased by 9.9% in the 2022 Quarter primarily due to lower price realizations, which decreased by 13.3%, partially offset by higher oil & gas volumes, which increased by 18.5%.

Segment Adjusted EBITDA for our Coal Royalties segment decreased 17.9% to $8.2 million for the 2022 Quarter compared to $9.9 million for the 2021 Quarter primarily related to the Hamilton thermal event which reduced royalty tons sold by 8.5%. Compared to the Sequential Quarter, Segment Adjusted EBITDA decreased 26.8% due to lower royalty tons sold and average royalty rates per ton due to the Hamilton thermal event.

Balance Sheet and Liquidity

In January 2023, the Partnership entered into a new $425.0 million senior secured revolving credit facility and $75.0 million term loan (the “Credit Facilities”), which will mature in March 2027, and renewed its $60.0 million accounts receivable securitization facility. The Credit Facilities will replace the previous revolving credit facility, which was set to mature in March 2024. More information regarding the Credit Facilities is provided in our Form 8-K filing made on January 20, 2023.

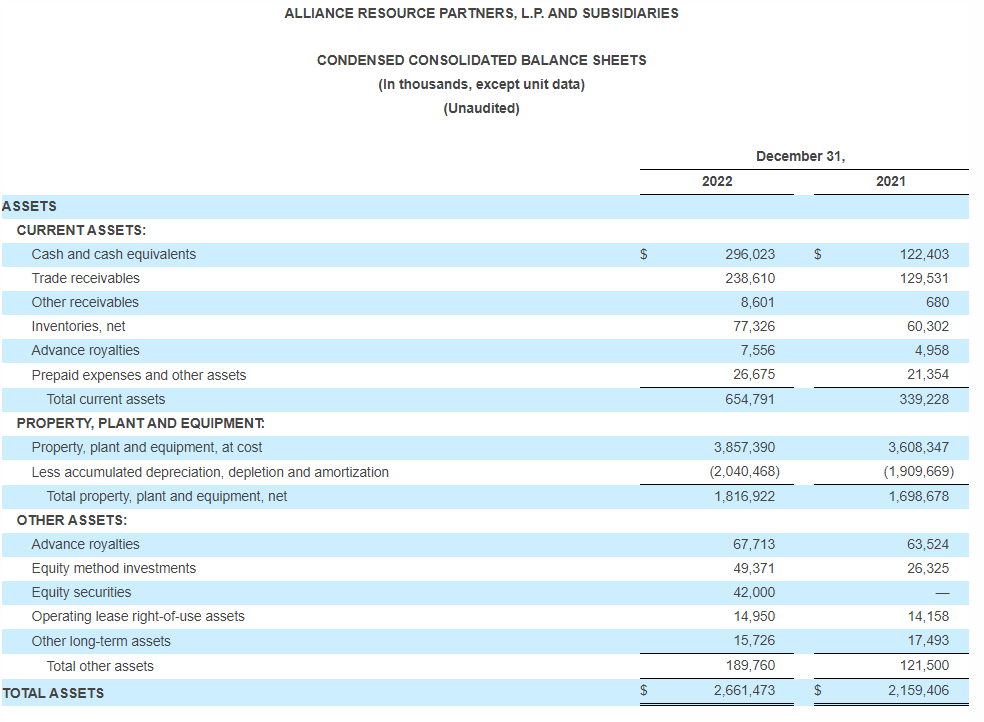

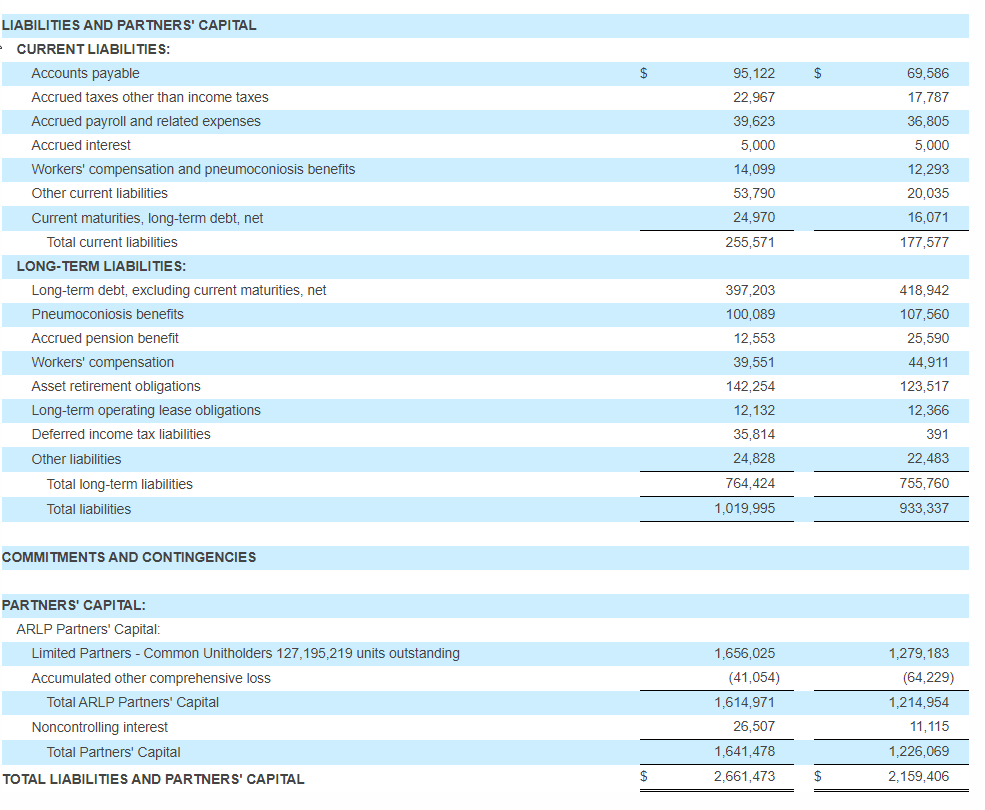

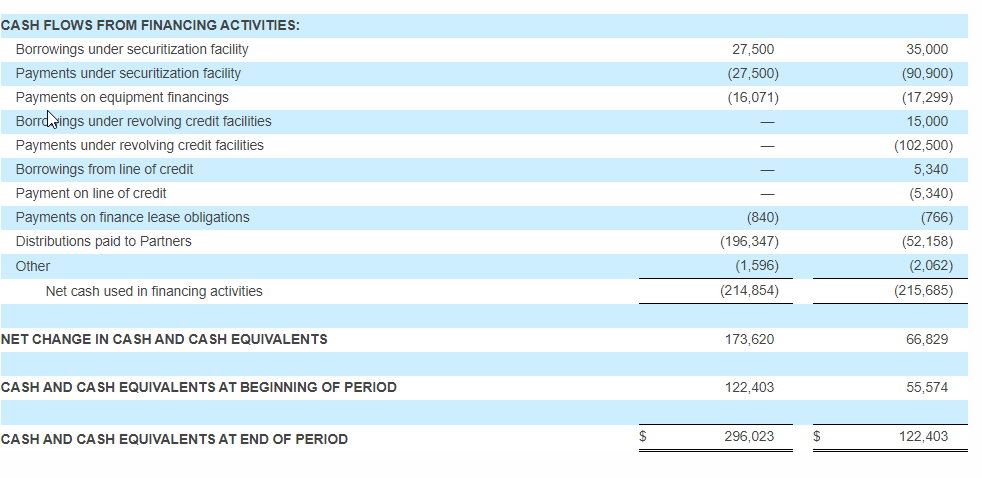

As of December 31, 2022, total debt and finance leases outstanding were $427.6 million, including $400.0 million in ARLP’s 2025 senior notes. The Partnership’s total and net leverage ratio improved to 0.45 times and 0.14 times, respectively, during the 2022 Quarter. ARLP ended the year with total liquidity of $762.8 million, which included $296.0 million of cash and cash equivalents and $466.7 million of borrowings available under our previous revolving credit and accounts receivable securitization facilities.

Distributions

As previously announced on January 27, 2023, the Board of Directors of ARLP’s general partner (the “Board”) approved a cash distribution to unitholders for the 2022 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on February 14, 2023, to all unitholders of record as of the close of trading on February 7, 2023. The announced distribution represents a 180.0% increase over the cash distribution of $0.25 per unit for the 2021 Quarter and is a 40.0% increase over the cash distribution of $0.50 per unit for the Sequential Quarter.

Unit Repurchase Program

ARLP also announced today that the Board has authorized an increase to the previously established unit repurchase program, which had $6.5 million of available capacity as of December 31, 2022. The expanded unit repurchase program authorizes ARLP to repurchase up to $100.0 million of its outstanding limited partner common units. The unit repurchase program announced today is intended to enhance ARLP’s ability to achieve its goal of creating long-term value for unitholders and, along with management’s objective of increasing quarterly cash distributions, increases flexibility in returning cash to unitholders. Future unit repurchases and distributions will be subject to ongoing Board review and authorization and will be based on a number of factors, including ARLP’s financial and operating performance and other capital requirements as well as future economic, business and market conditions.

The unit repurchase program has no time limit and ARLP may repurchase units from time to time in the open market or in other privately negotiated transactions. The unit repurchase program authorization does not obligate ARLP to repurchase any dollar amount or number of its units and repurchases may be commenced or suspended from time to time without prior notice.

January 2023 Acquisition of Oil & Gas Royalties

On January 27, 2023, the Board approved an acquisition of 2,682 net oil and gas royalty acres in the Permian Basin from JC Resources LP, an entity owned by Mr. Craft, for a cash purchase price of $72.3 million, subject to customary closing adjustments. Upon closing, the acquisition is expected to be immediately accretive to cash flow. The purchase price will be funded with available cash and is expected to close within the next 30 days based on an effective date of January 1, 2023. Since the acquisition involves a related party, terms of the transaction were approved by the Board’s conflicts committee, which is comprised entirely of independent directors.

Outlook

“The supply driven energy crisis, Russia’s invasion of Ukraine and the steep build of inflation disrupted energy prices and placed a new emphasis on energy security in 2022,” commented Mr. Craft. “Europe’s shift from Russian energy and U.S. and its allies’ economic sanctions are lowering Russian supply to the world, changing global energy trade routes and energy markets for several years to come, if not permanently. U.S. natural gas and coal exports should benefit in 2023 and beyond.”

“Due in part to this ongoing disruption, ARLP is well positioned to achieve another record year in 2023 by increasing production and sales by one to two million tons and relying on our highly committed coal contract book and a favorable market outlook to deliver 13.0 to 17.0% higher realized pricing compared to 2022,” commented Mr. Craft. “Even though natural gas prices have fallen recently due to the warm winter experienced so far, coal prices remain elevated in anticipation of international demand firming throughout the year as China’s economy reopens and as European markets look to replace 40 million tons of Russian coal imports received last year but unavailable this year. While the recent decline in natural gas prices are expected to impact our oil & gas royalties segment in the front half of the year, our coal segment should not be meaningfully affected due to our contracted position. In the back of this year and into 2024, we expect global economic activity will result in rising oil, gas and coal prices, and support our guidance.”

Mr. Craft concluded, “We are beginning to see the significant inflation experienced last year start to level off, however labor pressures and higher sales related expenses as a result of higher price realizations and coal sales volumes will continue to add to our costs in 2023. However, we expect favorable market forces and our current coal sales commitments will drive top line growth that should more than offset these inflationary pressures as margins are expected to improve across our business in 2023 versus the prior year.”

ARLP is providing the following initial guidance for the 2023 full year:

Conference Call

A conference call regarding ARLP’s 2022 Quarter and Year financial results and 2023 outlook is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “investor relations” section of ARLP’s website at http://www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13735338.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is one of the largest coal producers in the eastern United States. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast-growing energy and infrastructure transition.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at http://www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7674 or via e-mail at investorrelations@arlp.com.

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial performance, coal and oil & gas consumption and expected future prices, our ability to increase unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, preserving liquidity and maintaining financial flexibility, among others. These risks to our ability to achieve these outcomes include, but are not limited to, the following: the outcome or escalation of current hostilities in Ukraine, the severity, magnitude, and duration of the COVID-19 pandemic and the emergence of new virus variants, and impacts of the pandemic and of businesses’ and governments’ responses to the pandemic, including actions to mitigate its impact and the development of treatments and vaccines, on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers, available liquidity and capital sources and broader economic disruptions; changes in macroeconomic and market conditions and market volatility, and the impact of such changes and volatility on our financial position; decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion and the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels; changes in global economic and geo-political conditions or in industries in which we or our customers operate; changes in commodity prices, demand and availability which could affect our operating results and cash flows; actions of the major oil-producing countries with respect to oil production volumes and prices could have direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by operators of the properties in which we hold oil & gas mineral interests due to low commodity prices or the lack of downstream demand or storage capacity; risks associated with the expansion of our operations and properties; our ability to identify and complete acquisitions and to successfully integrate acquisitions into our business and achieve the anticipated benefits therefrom; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, MatrixDesign Group, LLC, and our investments in emerging infrastructure and technology companies; dependence on significant customer contracts, including renewing existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws, including the interest rate policies of the Federal Reserve Board; the effects of and changes in taxes or tariffs and other trade measures adopted by the United States and foreign governments; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ increasing attention to environmental, social and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor, including as a result of the potential impact of government-imposed vaccine mandates; our ability to maintain satisfactory relations with our employees; increases in labor costs including costs of health insurance and taxes resulting from the Affordable Care Act, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortages of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing-attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2021, filed on February 25, 2022 and amended on August 26, 2022, and ARLP’s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2022, June 30, 2022 and September 30, 2022, filed on May 9, 2022, August 8, 2022 and November 7, 2022, respectively. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

Reconciliation of Non-GAAP Financial Measures

Reconciliation of GAAP “net income attributable to ARLP” to non-GAAP “EBITDA” and “Distributable Cash Flow” (in thousands).

EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes and depreciation, depletion and amortization. Distributable cash flow (“DCF”) is defined as EBITDA excluding interest expense (before capitalized interest), interest income, income taxes and estimated maintenance capital expenditures. Distribution coverage ratio (“DCR”) is defined as DCF divided by distributions paid to partners.

Management believes that the presentation of such additional financial measures provides useful information to investors regarding our performance and results of operations because these measures, when used in conjunction with related GAAP financial measures, (i) provide additional information about our core operating performance and ability to generate and distribute cash flow, (ii) provide investors with the financial analytical framework upon which management bases financial, operational, compensation and planning decisions and (iii) present measurements that investors, rating agencies and debt holders have indicated are useful in assessing us and our results of operations.

EBITDA, DCF and DCR should not be considered as alternatives to net income attributable to ARLP, net income, income from operations, cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. EBITDA and DCF are not intended to represent cash flow and do not represent the measure of cash available for distribution. Our method of computing EBITDA, DCF and DCR may not be the same method used to compute similar measures reported by other companies, or EBITDA, DCF and DCR may be computed differently by us in different contexts (i.e. public reporting versus computation under financing agreements).

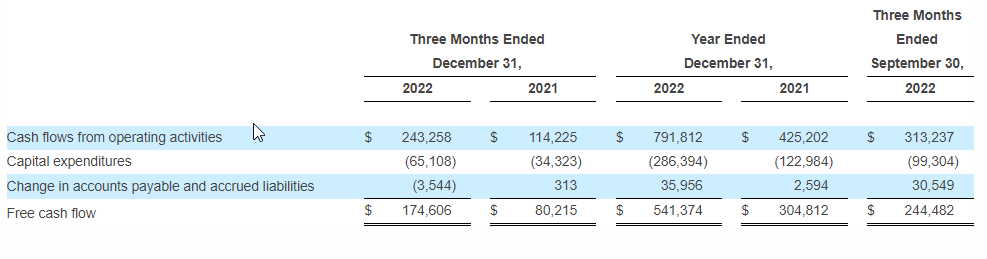

Reconciliation of GAAP “Cash flows from operating activities” to non-GAAP “Free cash flow” (in thousands).

Free cash flow is defined as cash flows from operating activities less capital expenditures and the change in accounts payable and accrued liabilities from purchases of property plant and equipment. Free cash flow should not be considered as an alternative to cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. Our method of computing free cash flow may not be the same method used by other companies. Free cash flow is a supplemental liquidity measure used by our management to assess our ability to generate excess cash flow from our operations.

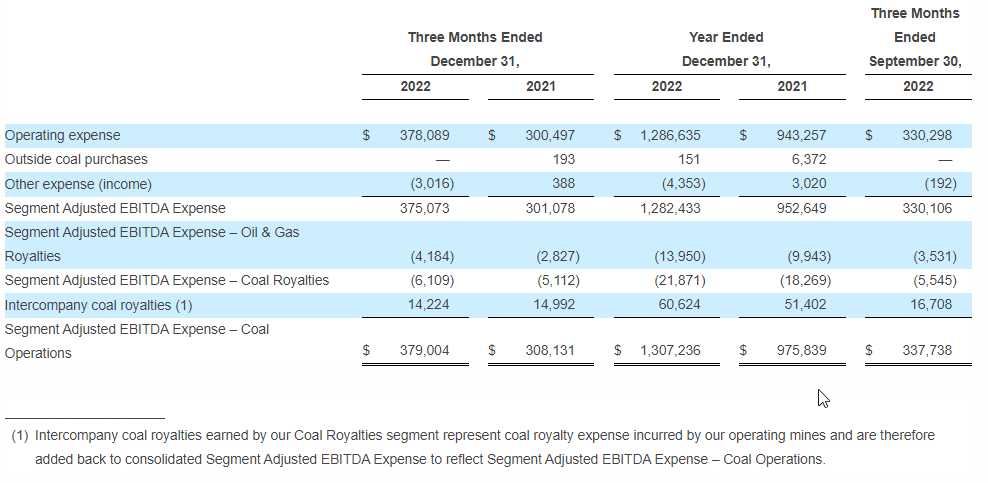

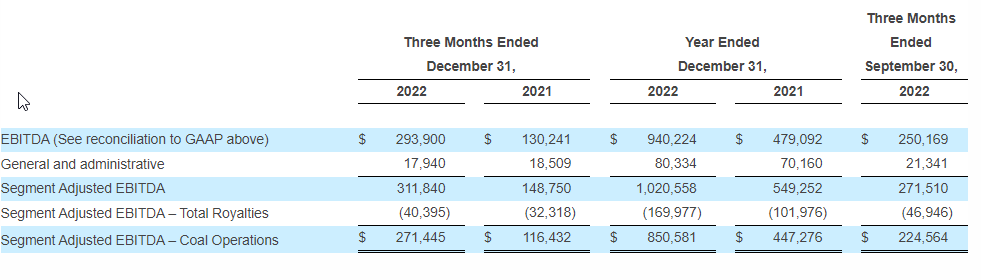

Reconciliation of GAAP “Operating Expenses” to non-GAAP “Segment Adjusted EBITDA Expense” and Reconciliation of non-GAAP ” EBITDA” to “Segment Adjusted EBITDA” (in thousands).

Segment Adjusted EBITDA Expense includes operating expenses, coal purchases and other income or expense. Transportation expenses are excluded as these expenses are passed through to our customers and, consequently, we do not realize any margin on transportation revenues. Segment Adjusted EBITDA Expense is used as a supplemental financial measure by our management to assess the operating performance of our segments. Segment Adjusted EBITDA Expense is a key component of EBITDA in addition to coal sales, royalty revenues and other revenues. The exclusion of corporate general and administrative expenses from Segment Adjusted EBITDA Expense allows management to focus solely on the evaluation of segment operating performance as it primarily relates to our operating expenses. Segment Adjusted EBITDA Expense – Coal Operations excludes expenses of our Oil & Gas Royalties segment and is adjusted for intercompany interactions with our Coal Royalties segment.

Segment Adjusted EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes, depreciation, depletion and amortization, general and administrative expenses and settlement gains. Segment Adjusted EBITDA – Coal Operations excludes the contribution of our Oil & Gas and Coal Royalties segments to allow management to focus solely on the operating performance of our Illinois Basin and Appalachia segments.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

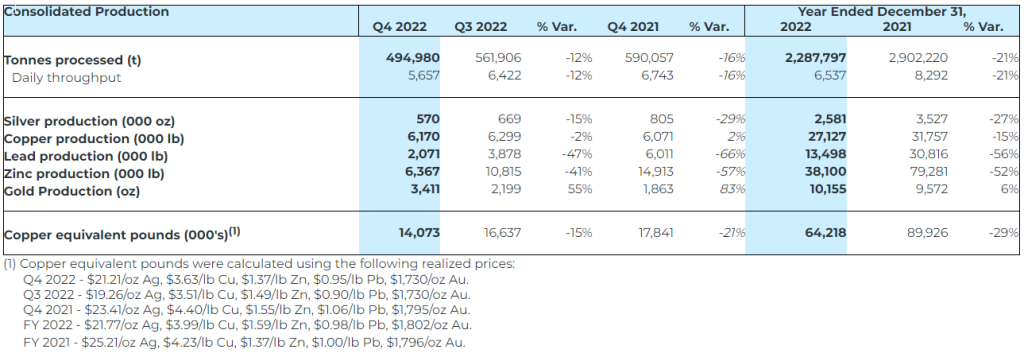

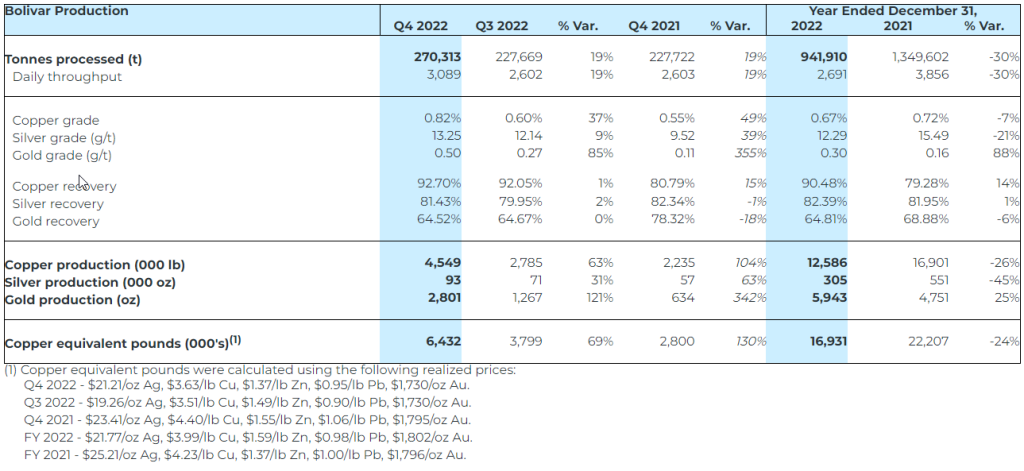

Fourth quarter and full year 2022 production. During the fourth quarter, Sierra Metals produced 6.2 million pounds of copper, 2.1 million pounds of lead, 6.4 million pounds of zinc, 3.4 thousand ounces of gold, and 570 thousand ounces of silver. Compared with the prior year period, production of copper and gold increased 2% and 83%, respectively, while lead, zinc, and silver declined 66%, 57%, and 29%. On a sequential basis, gold production increased 55%, while lead, zinc, silver, and copper declined 47%, 41%, 15%, and 2%, respectively. Compared to 2021, gold production in 2022 increased 6%, while lead, zinc, silver, and copper production declined 56%, 52%, 27%, and 15%, respectively. Copper equivalent production decreased 15% versus the prior quarter, 21% versus the prior year period, and 29% on a full year basis.

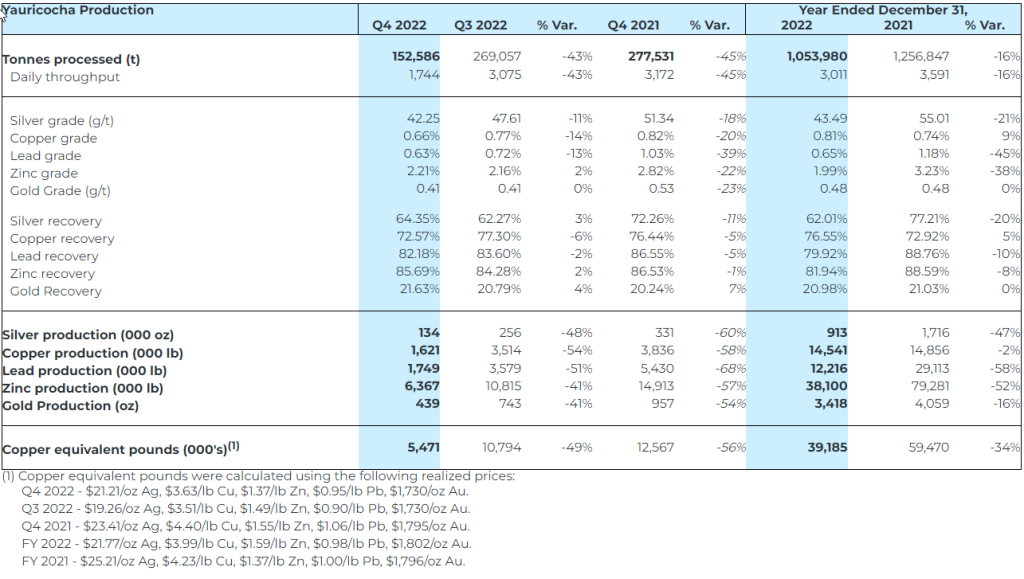

Operational performance. During the fourth quarter, Sierra achieved meaningful improvement at the Bolivar mine due to infrastructure upgrades and advances in the mine’s development work. Compared to the prior quarter, copper equivalent production increased 69% due to a 19% increase in throughput and improved head grades. While Cusi silver equivalent production was relatively flat relative to the prior quarter, an 11% increase in throughput helped offset the impact of lower grades and recoveries. Yauricocha performance was negatively impacted by a progressive restart of operations following a mudslide that led to the suspension of operations late in the third quarter.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ARLP is a diversified natural resource company that generates operating and royalty income from coal produced by its mining complexes and royalty income from mineral interests it owns in strategic oil & gas producing regions in the United States, primarily the Permian, Anadarko and Williston basins. ARLP currently produces coal from seven mining complexes its subsidiaries operate in Illinois, Indiana, Kentucky, Maryland and West Virginia. ARLP also operates a coal loading terminal on the Ohio River at Mount Vernon, Indiana. ARLP markets its coal production to major domestic and international utilities and industrial users and is currently the second largest coal producer in the eastern United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast growing energy and infrastructure transition.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Quarterly cash distribution increased 40%. For the December 2022 quarter, ARLP unit holders will receive a cash distribution of $0.70 per unit, or $2.80 on an annualized basis, payable on February 14, 2023 to unit holders of record as of the February 7, 2023 close. The announced distribution represents a 180% increase over the cash distribution of $0.25 per unit for the quarter ended December 31, 2021 and a 40% increase over the cash distribution of $0.50 per unit for the quarter ended September 30, 2022. We had assumed the quarterly cash distribution would be increased to $0.55.

Fourth quarter and full year 2022 financial results. ARLP will report financial results for the fourth quarter and full year 2022 before the market opens on Monday, January 30, 2023. Management will host a conference call for investors at 10:00 am ET on the same day.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

According to popular thinking, the government’s definition of money is of a flexible nature. Sometimes it could be M1, and at other times it could be M2 or some other M money supply. M1 includes currency and demand deposits. M2 includes all of M1, plus savings deposits, time deposits, and money market funds. By popular thinking what determines whether M1, M2, or some other M is considered money is whether it has high correlation with key economic data such as the gross domestic product (GDP).

However, since the early 1980s, correlations between various definitions of money and the GDP have broken down. The reason for this breakdown, many economists believe, is that financial deregulation has made the demand for money unstable. Consequently, the usefulness of money as a predictor of economic activity has significantly diminished.

Some economists believe that the relationship between money supply and the GDP could be strengthened by assigning weights to money supply components. The Divisia indicator, named after the French economist François Divisia, adjusts for differences in the degree to which various components of the monetary aggregate serve as money. This, in turn, supposedly offers a more accurate picture of what is happening to money supply.

The primary Divisia monetary indicator for the US is M4. It is a broad aggregate that includes negotiable money market securities, such as commercial paper, negotiable CDs, and T-bills. By assigning suitable weights, which are estimated by means of quantitative methods, it is held that one is likely to improve the correlation between the weighted monetary gauge and economic indicators.

Consequently, one could employ this monetary measure to ascertain the future course of key economic indicators. However, does it make sense?

Defining Money

No definition of money can be established by means of a correlation. A definition is supposed to present the essence of the subject being identified.

To establish the definition of money, we must determine how a money-using economy came about. Money emerged because barter could not support the market economy. A butcher who wanted to exchange his meat for fruit would have difficulty finding a fruit farmer who wanted his meat, while the fruit farmer who wanted to exchange his fruit for shoes might not have been able to find a shoemaker who wanted his fruit.

The distinguishing characteristic of money is that it is the general medium of exchange. It has evolved from the most marketable commodity. According to Murray Rothbard:

Just as in nature there is a great variety of skills and resources, so there is a variety in the marketability of goods. Some goods are more widely demanded than others, some are more divisible into smaller units without loss of value, some more durable over long periods of time, some more transportable over large distances. All of these advantages make for greater marketability. Eventually, one or two commodities are used as general media—in almost all exchanges—and these are called money.

With money, the butcher can exchange his meat for money and then exchange money for fruits. Likewise, the fruit farmer could exchange his fruit for money. With the obtained money, the fruit farmer can now exchange it for shoes. The reason why all these transactions become possible is because money is the most marketable commodity (i.e., the most accepted commodity).

According to Rothbard:

Money is not an abstract unit of account, divorceable from a concrete good; it is not a useless token only good for exchanging; it is not a “claim on society”; it is not a guarantee of a fixed price level. It is simply a commodity.

It follows then that all other goods and services are traded for money. This fundamental characteristic of money is contrasted with other goods. For instance, food supplies the necessary energy to human beings. Capital goods permit the expansion of the infrastructure that, in turn, permits the production of a larger quantity of goods and services. Contrary to the mainstream thinking, the essence of money has nothing to do with financial deregulation as this essence will remain intact in the most deregulated of markets.

Some commentators maintain that money’s main function is to fulfill the role of a means of savings. Others argue that its main role is to be a unit of account and a store of value. While all these roles are important, they are not fundamental. The basic role of money is to be a medium of exchange, with other functions such as unit of account, a store of value, and a means of savings arising from that role.

Through an ongoing selection process over thousands of years, individuals have settled on gold as money. In today’s monetary system, the money supply is no longer gold, but metal coins and paper notes issued by the government and the central bank. Consequently, coins and notes constitute money, known as cash, that is employed in transactions.

Distinction between Claim and Credit Transactions

At any point in time, an individual can keep money in a wallet or somewhere at home or deposit the money with a bank. In depositing money, an individual never relinquishes ownership over the money having an absolute claim over it.

This contrasts with a credit transaction, in which the lender of money relinquishes a claim over one’s money for the duration of the loan. As a result, in a credit transaction, money is transferred from a lender to a borrower. Credit transactions do not alter the amount of money. If Bob lends $1,000 to Joe, the money is transferred from Bob’s demand deposit or from Bob’s wallet to Joe’s possession.

Why Are Various Popular Definitions of Money Misleading?

Consider the money M2 definition, which includes money market securities, mutual funds, and other time deposits. However, investing in a mutual fund is, in fact, an investment in various money market instruments. The quantity of money is not altered because of this investment; only the ownership of money has temporarily changed. Hence, including mutual funds as part of money results in double counting.

The Divisia monetary gauge is of little help in establishing what money is. Because this indicator was designed to strengthen the correlation between monetary aggregates such as M4 and other Ms with an economic activity indicator, the Divisia gauge can better be seen as an exercise in curve fitting.

The Divisia of various Ms, such as the Divisia M4, does not address the double counting of money. The M4 is a broad aggregate and includes a mixture of claim and credit transactions (i.e., a double counting of money). This generates a misleading picture of what money is.

Applying various weights to the components of money cannot make the definition of money valid if it is created from erroneous components. Furthermore, even if the components were valid, one does not improve the money definition by assigning weights to components.

The introduction of electronic money has supposedly introduced another confusion regarding the definition of money. It is believed that electronic money is likely to make the cash redundant. We hold that electronic money is not new money, but rather a new way of employing existing monetary transactions. Regardless of these new ways of employing money, definitions and the role of money do not change.

Conclusion

The attempt to strengthen the correlation between various monetary aggregates and economic activity by using variable weighting of money supply components defeats the definition of money. The essence of money cannot be established by means of a statistical correlation, but rather by understanding what money is about.

About the Author

Frank Shostak is an Associated Scholar of the Mises Institute. His consulting firm, Applied Austrian School Economics, provides in-depth assessments and reports of financial markets and global economies. He received his bachelor’s degree from Hebrew University, his master’s degree from Witwatersrand University, and his PhD from Rands Afrikaanse University.

Image: President Biden reads newspaper before a phone call with Kevin McCarthy, Aug. 23, 2021 (The White House)

Could the Debt Ceiling Challenges be Ironed Out Before the Eleventh Hour?

The market-moving potential of key meetings in Washington on Wednesday, February 1st, includes more than the FOMC decision on monetary policy. Up the road from the Federal Reserve building, also scheduled for the first of the month, will be another important meeting for the markets. House of Representatives Speaker Kevin McCarthy will be headed to the Oval Office for a discussion to resolve other risks to the US economy, risks that could quickly spin out of control. High on the list is the national debt limit. Without a plan, the inability for the government to borrow above the current debt ceiling, could impact trust in the credit rating of US debt. This would move bond prices lower as rates would naturally rise at even the smallest prospect of a US default.

Why It’s Critical to Markets

A debt limit increase would allow the government to finance existing obligations. These obligations have, as in the past, expanded beyond the borrowing cap imposed on the US Treasury. An inability to roll existing maturing debt or afford additional interest rate costs would cause a default. The reverberations of this can not be understated as US Treasuries, like US currency, is the backbone of the worlds financial system.

An actual default could precipitate a mega financial crisis, threatening jobs, asset values, and trust.

The US reached its technical borrowing limit of $31.4 trillion in January. US Treasury Secretary Yellen enacted planned accounting moves that will allow the federal government to pay its bills until sometime in June by postponing some obligations. Before then, a solution must be devised by lawmakers that would then be signed by the President in order for the government to take on new debt and fund its responsibilities.

The Meeting Agenda

President Biden and House of Representatives Speaker Kevin McCarthy will meet at the White House to find common negotiating ground to avert a default. They currently seem far apart on a potential solution as the President’s party wishes to raise the debt ceiling quickly and resume business as usual in DC, while many in the House Speaker’s party are looking for concessions and spending cuts before they agree to raise the borrowing limit.

Republican lawmakers don’t currently support a measure that would let the country pay its debts unless there is agreement on various spending cuts going forward. The White House, which must sign or veto anything passed in Congress, has said raising the debt limit is critical and non-negotiable, citing the risk to the US economy from a default.

Both Biden and McCarthy will want to come away from this meeting with something their constituents and the onlooking financial markets can be comfortable with, and at the same time provides assurance to the world that is also looking on.

Congress has always passed an increase in the debt limit. Since 1960, Congress has acted 78 separate times to permanently raise, temporarily extend, or change the definition of the debt limit. Congressional leaders in both parties have believed in the end that it is best. However, the negotiations tend to go to the eleventh hour with escalating showmanship on all sides.

The eleventh hour comes sometime in June. Skeptics of any success of this face-to-face talk have a long history on which to hang their skepticism. However, McCarthy being new to his role and Biden having an aggressive spending agenda may help to shape a quicker outcome than in the past.

On Sunday, January 9th, McCarthy said that Republicans would not allow a US default that cuts into Social Security and Medicare, this would be “off the table” in any debt ceiling negotiations.

“The President will ask Speaker McCarthy if he intends to meet his Constitutional obligation to prevent a national default, as every other House and Senate leader in US history has done,” a White House spokesperson said.

The statements following, both by the White House and the Speakers camp, may cause a sigh of relief or elevate the level of panic.

Politics Involved

House Speaker McCarthy, in order to be elected speaker, agreed to rules that made it easier for his party to oust him over policy disagreements. He said he’d focus on discretionary spending, which has increased dramatically in the past two years with infrastructure and semiconductor legislation and a green-energy bill supported by Democrats.

“I think everything, when you look at discretionary, is sitting there,” McCarthy said. “We shouldn’t just print more money, we should balance our budget. So I want to look at every single department. Where can we become more efficient, more effective and more accountable?”

Biden, who is contemplating seeking re-election in 2024, has been sharply critical of McCarthy’s Republican caucus. He characterized them as “fiscally demented” earlier this month, threatened to veto their legislation and accused them of trying to balloon the deficit, favoring billionaires, raising middle-class taxes and threatening benefit programs.

Take Away

In the past, debt ceiling news typically made the top headline when the negotiations are truly in the eleventh hour. The meeting on Wednesday between two politicians that have a lot to gain from a successful outcome may avert a late Spring crisis and provide calm in what is already a cloudy economic environment. An agreement would be positive for the markets – lack of agreement will likely be taken as business as usual.

The Fed May Try to Talk Rates Up While Increasing Overnight Levels by a Lower Amount

There will be plenty for the market to digest this week. While all ears will be on what Fed Chairman Powell says following Wednesday’s FOMC policy announcement, investors will get to also digest a barage of earnings reports. The quarterly reports, from various sectors, may set the tone for their industries. These include reporting on Monday by Advanced Micro (AMD), Amgen (AMGN), Caterpillar (CAT), Exxon Mobil (XOM), McDonald’s (MCD), Pfizer (PFE), and United Parcel (UPS). On Tuesday Meta Platforms (META) will be one of the most talked about, then on Wednesday the market gets a barrage from tech and pharmaceutical companies as Alphabet (GOOGL), Amazon.com (AMZN), Apple (AAPL), Bristol-Myers (BMY), Eli Lilly (LLY), Honeywell (HON), Merck (MRK), and Qualcomm (QCOM) are all scheduled to report operating performance.

Monday 1/30

With no consequential economic releases, market direction may take its tone from earnings reports from a wide swath of industries (see tickers above).

Tuesday 1/31

The first of 2023’s eight scheduled two-day FOMC meetings begins.

8:30 AM ET, Employment Cost Index is expected to have risen 1.1% for the fourth quarter. For the last five quarters, large gains of 1 percent and more have been keeping wage inflation a concern.

8:30 AM ET, After jumping 7 points in December, the consumer confidence index is expected to firm only 0.7 of a point to 109.0 in January. The pattern in consumer attitudes and spending is often the largest influence on stock and bond markets. For stocks, strong economic growth translates to healthy corporate profits and possibly higher stock prices as a result.

Wednesday 2/1

7:00 AM ET, the Mortgage Bankers’ Association (MBA) compiles various mortgage loan indexes. The purchase applications index measures applications at mortgage lenders. This is a leading indicator for single-family home sales and housing construction. The composite index is expected to come in at 27.9%, while the Purchase applications are expected to show a reading of 24.7%. The data provides a gauge of not only the demand for housing, but economic momentum.

9:45 AM ET, Construction Spending, for December is expected to slip 0.1 percent after moving 0.2 percent higher in November. Spending has been flat in recent months as gains in non-residential construction have been offset by declines on the residential side.

10:00 AM ET, Job Openings and Labor Turnover Survey (JOLTS), which have been steady to lower, are expected to fall to 10.2 million in December versus 10.458 million in November.

2:00 PM ET, FOMC meeting concludes with statement of policy shift. The Fed is expected to reduce its rate hike magnitude to 25 basis points. A 0.25% increase would raise the overnight Fed Funds rate range up to 4.50% – 4.75%.

2:30 PM ET, Fed Chair Powell’s press briefing. The purpose of the briefing is to provide additional context to the FOMC’s policy decisions and to allow for questions-and-answers with the press. There has been concern that the market has been pushing rates down out in terms beyond two years to maturity. This could be a undermining the Fed’s stated objective by tightening. If this is true, the briefing may be filled with language that tries to convince the bond markets, that the Fed is determined to slow the economy by pushing rates up.

Thursday 2/2

7:30 AM ET, the Challenger Job Cut report counts and categorizes announcements of corporate layoffs based on mass layoff data from state departments of labor. The job-cut report doesn’t distinguish between layoffs scheduled for the short-term or the long term, or whether job cuts are handled through attrition or actual dismissals. Also, the job-cut report does not include jobs eliminated in small batches over a longer time period. Unlike most economic data, this series is not adjusted for seasonal variation.

8:30 AM ET, Nonfarm Productivity is expected to rise to a 2.4 percent annualized rate in the fourth quarter versus growth of 0.8 percent in the third quarter. Unit labor costs, which rose 2.4 percent in the third quarter, are expected to rise to a 1.5 percent rate in the fourth quarter.

10:00 AM ET, Factory Orders are expected to rise 2.2 percent in December following November’s steep 1.8 percent drop. The expected increase comes in the wake of a surge in aircraft orders.

Friday 2/3

• 8:30 AM ET, Nonfarm Payroll is expected to have grown 185,000 in January versus 223,000 in December which was the eighth straight month and tenth of the last eleven that payroll growth exceeded the average economists expectation. Average hourly earnings in January are expected to rise 0.3 percent on the month for a year-over-year rate of 4.4 percent.

What Else

The tone of the chatter that is expected to come from Fed officials is one of continued hawkishness. The Fed’s preferred inflation measure (PCE) was at 4.4% for all of 2022, and has been trending downward. This is more than double the stated target of 2%. The question they are now facing is, whether they should soon pause tightening and observe the impact of previous moves. Or if the solid employment numbers and strong bank reserve positions leave room for continuing the war on inflation through aggressive overnight rate hikes. Powell’s press conference after the 2 pm announcement on Wednesday should reveal quite a bit.

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) today announced that the Board of Directors of ARLP’s general partner approved an increased cash distribution to its unitholders for the quarter ended December 31, 2022 (the “2022 Quarter”).

ARLP unitholders will receive a cash distribution for the 2022 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on February 14, 2023 to all unitholders of record as of the close of trading on February 7, 2023. The announced distribution represents a 180% increase over the cash distribution of $0.25 per unit for the quarter ended December 31, 2021 and a 40% increase over the cash distribution of $0.50 per unit for the quarter ended September 30, 2022.

As previously announced, ARLP will report financial results for the 2022 Quarter before the market opens on Monday, January 30, 2023 and Alliance management will discuss these results during a conference call beginning at 10:00 a.m. Eastern that same day.

To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “investor relations” section of ARLP’s website at http://www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13735338.

Concurrent with this announcement we are providing qualified notice to brokers and nominees that hold ARLP units on behalf of non-U.S. investors under Treasury Regulation Section 1.1446-4(b) and (d) and Treasury Regulation Section 1.1446(f)-4(c)(2)(iii). Brokers and nominees should treat one hundred percent (100%) of ARLP’s distributions to non-U.S. investors as being attributable to income that is effectively connected with a United States trade or business. In addition, brokers and nominees should treat one hundred percent (100%) of the distribution as being in excess of cumulative net income for purposes of determining the amount to withhold. Accordingly, ARLP’s distributions to non-U.S. investors are subject to federal income tax withholding at a rate equal to the highest applicable effective tax rate plus ten percent (10%). Nominees, and not ARLP, are treated as the withholding agents responsible for withholding on the distributions received by them on behalf of non-U.S. investors.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is the second largest coal producer in the eastern United States. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast-growing energy and infrastructure transition.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at http://www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7674 or via e-mail at investorrelations@arlp.com.

Brian L. Cantrell Alliance Resource Partners, L.P. (918) 295-7674

Bolivar’s improved operating performance resulted in a 69% and 130% increase in copper equivalent production over Q3 2022 and Q4 2021, respectively.

A measured and progressive approach to reach full operating capacity at Yauricocha continues, following the mudslide in Q3 2022.

Consolidated 2022 copper equivalent production decreased 29% compared to 2021 due to lower production at Yauricocha resulting from the suspension of mining operations and lower grades across all metals, except for gold.

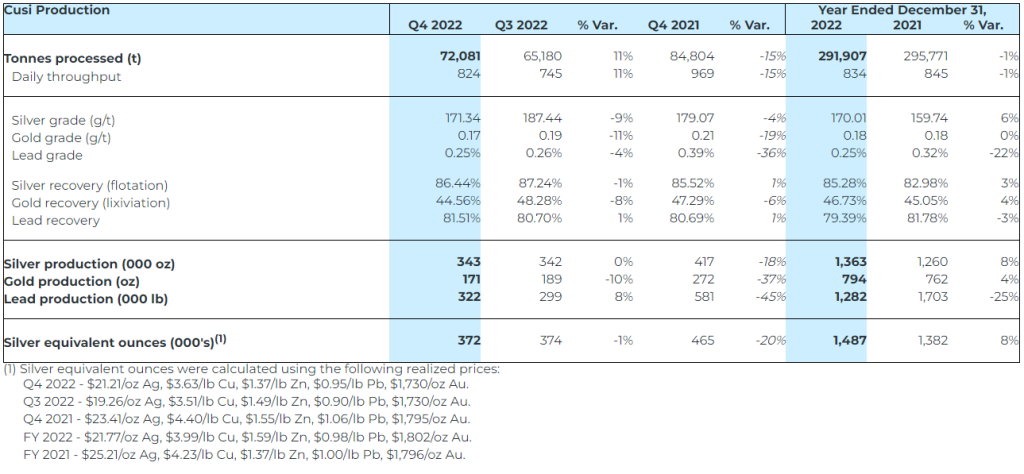

TORONTO–(BUSINESS WIRE)– Sierra Metals Inc. (TSX: SMT) (“Sierra Metals” or the “Company”) reports fourth quarter and full year 2022 production results. Results are from Sierra Metals’ three underground mines in Latin America: The Yauricocha polymetallic mine in Peru, the copper-producing Bolivar mine and the silver-producing Cusi mine in Mexico.

Truck being loaded at Bolivar Rom Pad headed to Concentrate Plant (Photo: Business Wire)

Ernesto Balarezo, Interim CEO of Sierra Metals, commented on a challenging 2022 for the Company, “Early in the year, Yauricocha’s throughput and grades were hindered by a shortage of mine and service personnel due to the COVID-19 pandemic, as well as permitting restrictions. In the third quarter, production was halted due to the tragic mudslide event followed by a road blockade. The mine’s throughput in Q4 declined by 43% when compared to Q3 and 45% when compared to the same quarter last year. While recovery toward Yauricocha’s full production potential continues, safety remains our highest priority. To lead this initiative, Sierra Metals has hired a Vice President, Health & Safety.

At Bolivar, progress in reducing the significant backlog in drilling and mine development that arose during the pandemic was delayed throughout the first half of the year, due to setbacks encountered during the installation of critical infrastructure. These delays were compounded in Q3 by unexpected flooding, negatively affecting production during most of the quarter. However, the Company achieved meaningfully improved performance during Q4 due to infrastructure upgrades in pumping and ventilation, which created improved conditions required to support the advancement of the mine’s preparation and development. A 19% increase in throughput along with improved head grades in all metals resulted in a 69% increase in copper equivalent pounds produced when compared to Q3 2022. When compared to Q4 2021, throughput increased by 19% and copper equivalent production increased by 130%.

Mr. Balarezo concluded,“I am encouraged by the production improvements during the fourth quarter. Our primary goal in the new year is to ramp up production at Yauricocha, stabilize production at Bolivar and optimize Cusi’s production. We are committed to ensuring operations run safely, efficiently and effectively with efforts to streamline processes and reduce inefficiencies where possible. Consistent with the Company’s efforts, the Special Committee of the Board of Directors is continuing to diligently pursue its strategic review process.”

Consolidated Production Results

Consolidated quarterly throughput during Q4 2022 was 494,980 tonnes, a decrease of 12% when compared to Q3 2022, mainly due to the 43% decline in throughput at Yauricocha compared to Q3 2022. As a result, consolidated copper equivalent production also declined by 15% when compared to Q3 2022.

While a 19% increase in throughput during Q4 2022 at the Bolivar Mine, combined with higher grades in all metals, provided a 69% increase in copper equivalent production over the prior quarter, it was not enough to offset the decline in production at Yauricocha. When compared to Q4 2021, a 16% decrease in consolidated throughput resulted in a 21% decrease in consolidated copper equivalent production.