The AVERSA™ transdermal abuse deterrent technology is protected by a broad international intellectual property portfolio with patents already issued in 46 countries including the United States, Europe, Japan, Korea, Russia, China, Canada, Mexico, and Australia

February 07, 2025 08:45 ET

ORLANDO, Fla., Feb. 07, 2025 (GLOBE NEWSWIRE) — Nutriband Inc. (NASDAQ:NTRB)(NASDAQ:NTRBW), a company engaged in the development of prescription transdermal pharmaceutical products, today announced that it received a Notice of Allowance from the United States Patent and Trademark Office (USPTO) on February 3, 2025 for patent application 18/369,241, “Abuse and Misuse Deterrent Transdermal Systems” which covers its Aversa™ abuse deterrent technology. The receipt of a Notice of Allowance means that the USPTO is expected to issue a U.S. patent for this application after administrative processes have been completed.

The expected issuance of this patent further expands Nutriband’s intellectual property protection in the United States for its portfolio of abuse deterrent transdermal products based on its proprietary Aversa™ abuse deterrent technology. This technology can be incorporated into transdermal patches to prevent the abuse, diversion, misuse, and accidental exposure of drugs with abuse potential. Nutriband’s lead product under development is Aversa™ Fentanyl, an abuse deterrent fentanyl transdermal system, with the potential to become the first and only abuse deterrent pain patch on the market.

Nutriband’s AVERSA™ abuse-deterrent technology can be utilized to incorporate aversive agents into transdermal patches to prevent the abuse, diversion, misuse, and accidental exposure of drugs with abuse potential including opioids and stimulants. The technology consists of a proprietary aversive agent coating that employs taste aversion to deter the oral abuse of and accidental exposure to transdermal opioid and stimulant patch products.

The AVERSA™ abuse deterrent technology is protected by a broad international intellectual property portfolio with patents issued in 46 countries including the United States, Europe, Japan, Korea, Russia, China, Canada, Mexico, and Australia.

AVERSA Fentanyl has the potential to be the world’s first abuse-deterrent opioid patch designed to deter the abuse and misuse and reduce the risk of accidental exposure of transdermal fentanyl patches. AVERSA Fentanyl has the potential to reach peak annual US sales of $80 million to $200 million.1

____________________________________________

1 Health Advances Aversa Fentanyl market analysis report 2022

About AVERSA™ Abuse-Deterrent Transdermal Technology

Nutriband’s AVERSA™ abuse-deterrent transdermal technology incorporates aversive agents into transdermal patches to prevent the abuse, diversion, misuse, and accidental exposure of drugs with abuse potential. The AVERSA™ abuse-deterrent technology has the potential to improve the safety profile of transdermal drugs susceptible to abuse, such as fentanyl, while making sure that these drugs remain accessible to those patients who really need them. The technology is covered by a broad intellectual property portfolio with patents granted in the United States, Europe, Japan, Korea, Russia, China, Canada, Mexico, and Australia.

About Nutriband Inc.

We are primarily engaged in the development of a portfolio of transdermal pharmaceutical products. Our lead product under development is an abuse-deterrent fentanyl patch incorporating our AVERSA™ abuse-deterrent technology. AVERSA™ technology can be incorporated into any transdermal patch to prevent the abuse, misuse, diversion, and accidental exposure of drugs with abuse potential.

The Company’s website is www.nutriband.com. Any material contained in or derived from the Company’s websites or any other website is not part of this press release.

Forward-Looking Statements

Certain statements contained in this press release, including, without limitation, statements containing the words “believes,” “anticipates,” “expects” and words of similar import, constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve both known and unknown risks and uncertainties. The Company’s actual results may differ materially from those anticipated in its forward-looking statements as a result of a number of factors, including those including the Company’s ability to develop its proposed abuse-deterrent fentanyl transdermal system and other proposed products, its ability to obtain patent protection for its abuse technology, its ability to obtain the necessary financing to develop products and conduct the necessary clinical testing, its ability to obtain Federal Food and Drug Administration approval to market any product it may develop in the United States and to obtain any other regulatory approval necessary to market any product in other countries, including countries in Europe, its ability to market any product it may develop, its ability to create, sustain, manage or forecast its growth; its ability to attract and retain key personnel; changes in the Company’s business strategy or development plans; competition; business disruptions; adverse publicity and international, national and local general economic and market conditions and risks generally associated with an undercapitalized developing company, as well as the risks contained under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in the Company’s Form S-1, Form 10-K for the year ended January 31, 2024, filed May 1, 2024, the Forms 10-Q’s filed subsequent to the Form 10-K in 2024, and the Company’s other filings with the Securities and Exchange Commission. Except as required by applicable law, we undertake no obligation to revise or update any forward-looking statements to reflect any event or circumstance that may arise after the date hereof.

Patient treated in procedure, conducted at Mass General Transplant Center and in collaboration with partner eGenesis, was recently released from hospital

Investigational therapy tegoprubart targets CD40 ligand (CD40L) with potential to improve both safety and efficacy compared to standard of care immunosuppression regimens

IRVINE, Calif., Feb. 07, 2025 (GLOBE NEWSWIRE) — Eledon Pharmaceuticals, Inc. (“Eledon”) (Nasdaq: ELDN) today announced that tegoprubart, the company’s investigational anti-CD40L antibody, was used as a key component of the immunosuppression therapy regimen in a patient who recently received a transplanted kidney from a genetically modified pig. The procedure was performed on January 25, 2025, by surgeons at Massachusetts General Hospital (MGH) in collaboration with our partner eGenesis. In December 2024, MGH received Food and Drug Administration (FDA) approval to proceed with this transplant and plans to perform two additional xenotransplants this year, further advancing the field of xenotransplantation. Following the successful transplant, the patient was discharged from the hospital and is now off dialysis for the first time in over two years.

“This second kidney xenotransplant conducted at MGH represents another important milestone in the effort to consider new strategies in transplantation and immunosuppression to address the global organ shortage crisis. We are grateful to the patient, the team at MGH, and our partner eGenesis for supporting tegoprubart’s central role in these landmark procedures,” said David-Alexandre C. Gros, M.D., Eledon Chief Executive Officer. “Blocking the CD40 Ligand is a critical component of the immunosuppression regimen for effective translation of organ transplant from nonhuman primates into humans. Our anti-CD40L antibody tegoprubart represents a novel approach to immunosuppression therapy with the potential to improve safety and efficacy and enable patients to live longer with their transplanted organs.”

Similar to the first-ever kidney xenotransplant, also conducted at MGH in March 2024, tegoprubart is being administered to the current patient investigationally as part of a regimen designed to prevent the body from rejecting the transplanted pig organ. Tegoprubart is designed to block CD40L and has been shown to inhibit multiple costimulatory receptors including CD40 and CD11, key components of how immune cells communicate with one another. Based on extensive prior research, tegoprubart has been observed to be generally safe and well-tolerated in multiple potential indications, including for the prevention of rejection following kidney allotransplantation.

“I would like to thank Eledon for their work supporting this historic xenotransplant. Immunosuppression presents one of the greatest challenges for transplantation in both human and non-human organs. The need for advancements in immunosuppressive medications is critical for advancing our field and improving the quality of life for transplant patients everywhere,” said Dr. Leonardo Riella, MD, PhD, Medical Director for Kidney Transplantation at Massachusetts General Hospital.

Tegoprubart was also used as a cornerstone component of the chronic immunosuppression regimen administered following the second-ever transplant of a genetically modified heart from a pig to a human, performed at the University of Maryland Medical Center in September 2023. Currently, tegoprubart is being evaluated in three global clinical studies for the prevention of organ rejection in patients receiving kidney transplants and in a separate investigator sponsored trial for the prevention of islet transplant rejection in patients with type 1 diabetes (T1D). Eledon recently announced initial data from this investigator-initiated islet transplant trial, conducted by the research team at the University of Chicago Medicine Transplant Institute, that demonstrated potentially the first human cases of insulin independence achieved using an anti-CD40L monoclonal antibody therapy without the use of tacrolimus, the current standard of care for prevention of transplant rejection.

The Company plans to report updated interim clinical trial from its ongoing Phase 1b and long-term safety and efficacy extension studies in kidney transplant this summer, topline results from its Phase 2 BESTOW kidney transplant trial in the fourth quarter of 2025, and longer-term follow up results from the investigator-led islet transplant clinical trial at UChicago Medicine Transplant Institute later this year.

About Eledon Pharmaceuticals and tegoprubart

Eledon Pharmaceuticals, Inc. is a clinical stage biotechnology company that is developing immune-modulating therapies for the management and treatment of life-threatening conditions. The Company’s lead investigational product is tegoprubart, an anti-CD40L antibody with high affinity for the CD40 Ligand, a well-validated biological target that has broad therapeutic potential. The central role of CD40L signaling in both adaptive and innate immune cell activation and function positions it as an attractive target for non-lymphocyte depleting, immunomodulatory therapeutic intervention. The Company is building upon a deep historical knowledge of anti-CD40 Ligand biology to conduct preclinical and clinical studies in kidney allograft transplantation, xenotransplantation, and amyotrophic lateral sclerosis (ALS). Eledon is headquartered in Irvine, California. For more information, please visit the Company’s website at www.eledon.com.

Follow Eledon Pharmaceuticals on social media: LinkedIn; Twitter

Forward-Looking Statements

This press release contains forward-looking statements that involve substantial risks and uncertainties. Any statements about the company’s future expectations, plans and prospects, including statements about planned clinical trials, the development of product candidates, expected timing for initiation of future clinical trials, expected timing for receipt of data from clinical trials, as well as other statements containing the words “believes,” “anticipates,” “plans,” “expects,” “estimates,” “intends,” “predicts,” “projects,” “targets,” “looks forward,” “could,” “may,” and similar expressions, constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are inherently uncertain and are subject to numerous risks and uncertainties, including: risks relating to the safety and efficacy of our drug candidates; risks relating to clinical development timelines, including interactions with regulators and clinical sites, as well as patient enrollment; risks relating to costs of clinical trials and the sufficiency of the company’s capital resources to fund planned clinical trials; and risks associated with the impact of the ongoing coronavirus pandemic. Actual results may differ materially from those indicated by such forward-looking statements as a result of various factors. These risks and uncertainties, as well as other risks and uncertainties that could cause the company’s actual results to differ significantly from the forward-looking statements contained herein, are discussed in our quarterly 10-Q, annual 10-K, and other filings with the U.S. Securities and Exchange Commission, which can be found at www.sec.gov. Any forward-looking statements contained in this press release speak only as of the date hereof and not of any future date, and the company expressly disclaims any intent to update any forward-looking statements, whether as a result of new information, future events or otherwise.

Company had $98.8 million in cash as of December 31, 2024; existing cash expected to fund planned operations into the first quarter of 2026

Company is debt-free after repaying mortgage on facilities

TNX-102 SL fibromyalgia FDA PDUFA goal date is August 15, 2025

$10.1 million in net sales from migraine products in 2024

CHATHAM, N.J., Feb. 07, 2025 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a fully-integrated biopharmaceutical company with marketed products and a pipeline of development candidates, recently announced selected preliminary operating results for the year ended December 31, 2024, and certain preliminary financial condition information as of December 31, 2024.

Preliminary Full Year 2024 Financial Results1

The Company had approximately $98.8 million in cash and cash equivalents as of December 31, 2024.

Net cash used in operating activities was approximately $60.9 million, compared to $102.0 million for the prior year.

Capital expenditures was approximately $0.1 million, compared to $29.1 million for the prior year.

Net operating loss was approximately $126.6 million, which includes non-cash impairment charges of approximately $59.0 million, compared to net operating loss of $116.7 million for the prior year.

The Company announced that net revenue from the sale of its marketed products was approximately $10.1 million, compared to $7.8 million for the prior year.

On February 3, 2025, the Company repaid a mortgage (Loan and Guaranty Agreement) with JGB Capital and related parties that was secured by two facilities and the Company is now debt-free.

The Company expects that its cash resources at December 31, 2024, and the gross proceeds of approximately $30.4 million raised from sales under its at-the-market facility in the first quarter of 2025, will be sufficient to fund its planned operations into the first quarter of 2026.

The cash runway is expected to fund the company beyond the August 15, 2025 Prescription Drug User Fee Act (PDUFA) goal date assigned by the U.S. Food and Drug Administration (FDA) for a decision on marketing authorization for TNX-102 SL (cyclobenzaprine HCl sublingual tablets) 5.6 mg for the management of fibromyalgia.

1The above information is preliminary financial information for the year ended December 31, 2024 and subject to completion. The unaudited, estimated results for the year ended December 31, 2024 are preliminary and were prepared by the Company’s management, based upon its estimates, a number of assumptions and currently available information, and are subject to revision based upon, among other things, quarter and year-end closing procedures and/or adjustments, the completion of the Company’s consolidated financial statements and other operational procedures. This preliminary financial information is the responsibility of management and has been prepared in good faith on a consistent basis with prior periods. However, the Company has not completed its financial closing procedures for the year ended December 31, 2024, and its actual results could be materially different from this preliminary financial information, which preliminary information should not be regarded as a representation by the Company or its management as to its actual results for the year ended December 31, 2024. In addition, EisnerAmper LLP, the Company’s independent registered public accounting firm, has not audited, reviewed, compiled, or performed any procedures with respect to this preliminary financial information and does not express an opinion or any other form of assurance with respect to this preliminary financial information. During the course of the preparation of the Company’s financial statements and related notes as of and for the year ended December 31, 2024, the Company may identify items that would require it to make material adjustments to this preliminary financial information. As a result, prospective investors should exercise caution in relying on this information and should not draw any inferences from this information. This preliminary financial information should not be viewed as a substitute for full financial statements prepared in accordance with United States generally accepted accounting principles and reviewed by the Company’s auditors.

Tonix Pharmaceuticals Holding Corp.*

Tonix is a fully-integrated biopharmaceutical company focused on transforming therapies for pain management and vaccines for public health challenges. Tonix’s development portfolio is focused on central nervous system (CNS) disorders. Tonix’s priority is to advance TNX-102 SL, a product candidate for the management of fibromyalgia, for which an NDA was submitted based on two statistically significant Phase 3 studies for the management of fibromyalgia and for which a PDUFA (Prescription Drug User Fee act) goal date of August 15, 2025 has been assigned for a decision on marketing authorization. The FDA has also granted Fast Track designation to TNX-102 SL for the management of fibromyalgia. TNX-102 SL is also being developed to treat acute stress reaction and acute stress disorder under a Physician-Initiated IND at the University of North Carolina in the OASIS study funded by the U.S. Department of Defense (DoD). Tonix’s CNS portfolio includes TNX-1300 (cocaine esterase), a biologic in Phase 2 development designed to treat cocaine intoxication that has FDA Breakthrough Therapy designation, and its development is supported by a grant from the National Institute on Drug Abuse. Tonix’s immunology development portfolio consists of biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is an Fc-modified humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft rejection and for the treatment of autoimmune diseases. Tonix also has product candidates in development in infectious disease, including a vaccine for mpox, TNX-801. Tonix recently announced a contract with the U.S. DoD’s Defense Threat Reduction Agency (DTRA) for up to $34 million over five years to develop TNX-4200, small molecule broad-spectrum antiviral agents targeting CD45 for the prevention or treatment of infections to improve the medical readiness of military personnel in biological threat environments. Tonix owns and operates a state-of-the art infectious disease research facility in Frederick, Md. Tonix Medicines, our commercial subsidiary, markets Zembrace® SymTouch® (sumatriptan injection) 3 mg and Tosymra® (sumatriptan nasal spray) 10 mg for the treatment of acute migraine with or without aura in adults.

* Tonix’s product development candidates are investigational new drugs or biologics; their efficacy and safety have not been established and have not been approved for any indication.

Zembrace SymTouch and Tosymra are registered trademarks of Tonix Medicines. All other marks are property of their respective owners.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the failure to successfully market any of our products; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2023, as filed with the Securities and Exchange Commission (the “SEC”) on April 1, 2024, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

Zembrace® SymTouch® (sumatriptan succinate) injection (Zembrace) and Tosymra® (sumatriptan) nasal spray are prescription medicines used to treat acute migraine headaches with or without aura in adults who have been diagnosed with migraine.

Zembrace and Tosymra are not used to prevent migraines. It is not known if Zembrace or Tosymra are safe and effective in children under 18 years of age.

Important Safety Information

Zembrace and Tosymra can cause serious side effects, including heart attack and other heart problems, which may lead to death. Stop use and get emergency help if you have any signs of a heart attack:

discomfort in the center of your chest that lasts for more than a few minutes or goes away and comes back

severe tightness, pain, pressure, or heaviness in your chest, throat, neck, or jaw

pain or discomfort in your arms, back, neck, jaw or stomach

shortness of breath with or without chest discomfort

breaking out in a cold sweat

nausea or vomiting

feeling lightheaded

Zembrace and Tosymra are not for people with risk factors for heart disease (high blood pressure or cholesterol, smoking, overweight, diabetes, family history of heart disease) unless a heart exam shows no problem.

Do not use Zembrace or Tosymra if you have:

history of heart problems

narrowing of blood vessels to your legs, arms, stomach, or kidney (peripheral vascular disease)

uncontrolled high blood pressure

hemiplegic or basilar migraines. If you are not sure if you have these, ask your provider.

had a stroke, transient ischemic attacks (TIAs), or problems with blood circulation

severe liver problems

taken any of the following medicines in the last 24 hours: almotriptan, eletriptan, frovatriptan, naratriptan, rizatriptan, ergotamines, or dihydroergotamine. Ask your provider for a list of these medicines if you are not sure.

are taking certain antidepressants, known as monoamine oxidase (MAO)-A inhibitors or it has been 2 weeks or less since you stopped taking a MAO-A inhibitor. Ask your provider for a list of these medicines if you are not sure.

an allergy to sumatriptan or any of the components of Zembrace or Tosymra

Tell your provider about all of your medical conditions and medicines you take, including vitamins and supplements.

Zembrace and Tosymra can cause dizziness, weakness, or drowsiness. If so, do not drive a car, use machinery, or do anything where you need to be alert.

Zembrace and Tosymra may cause serious side effects including:

changes in color or sensation in your fingers and toes

sudden or severe stomach pain, stomach pain after meals, weight loss, nausea or vomiting, constipation or diarrhea, bloody diarrhea, fever

cramping and pain in your legs or hips; feeling of heaviness or tightness in your leg muscles; burning or aching pain in your feet or toes while resting; numbness, tingling, or weakness in your legs; cold feeling or color changes in one or both legs or feet

increased blood pressure including a sudden severe increase even if you have no history of high blood pressure

medication overuse headaches from using migraine medicine for 10 or more days each month. If your headaches get worse, call your provider.

serotonin syndrome, a rare but serious problem that can happen in people using Zembrace or Tosymra, especially when used with anti-depressant medicines called SSRIs or SNRIs. Call your provider right away if you have: mental changes such as seeing things that are not there (hallucinations), agitation, or coma; fast heartbeat; changes in blood pressure; high body temperature; tight muscles; or trouble walking.

hives (itchy bumps); swelling of your tongue, mouth, or throat

seizures even in people who have never had seizures before

The most common side effects of Zembrace and Tosymra include: pain and redness at injection site (Zembrace only); tingling or numbness in your fingers or toes; dizziness; warm, hot, burning feeling to your face (flushing); discomfort or stiffness in your neck; feeling weak, drowsy, or tired; application site (nasal) reactions (Tosymra only) and throat irritation (Tosymra only).

Tell your provider if you have any side effect that bothers you or does not go away. These are not all the possible side effects of Zembrace and Tosymra. For more information, ask your provider.

This is the most important information to know about Zembrace and Tosymra but is not comprehensive. For more information, talk to your provider and read the Patient Information and Instructions for Use. You can also visit https://www.tonixpharma.com or call 1-888-869-7633.

You are encouraged to report adverse effects of prescription drugs to the FDA. Visit www.fda.gov/medwatch, or call 1-800-FDA-1088.

LAKE ZURICH, Ill.–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) today announced that it will release its fourth quarter and full year 2024 earnings after the market close on February 20, 2025. The Company will host a conference call and webcast to discuss the results on February 21 at 8:30 a.m. EST. The webcast can be accessed through the Investor Relations section of www.accobrands.com and will be available for replay.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn and play. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

Christopher McGinnis Investor Relations (847) 796-4320

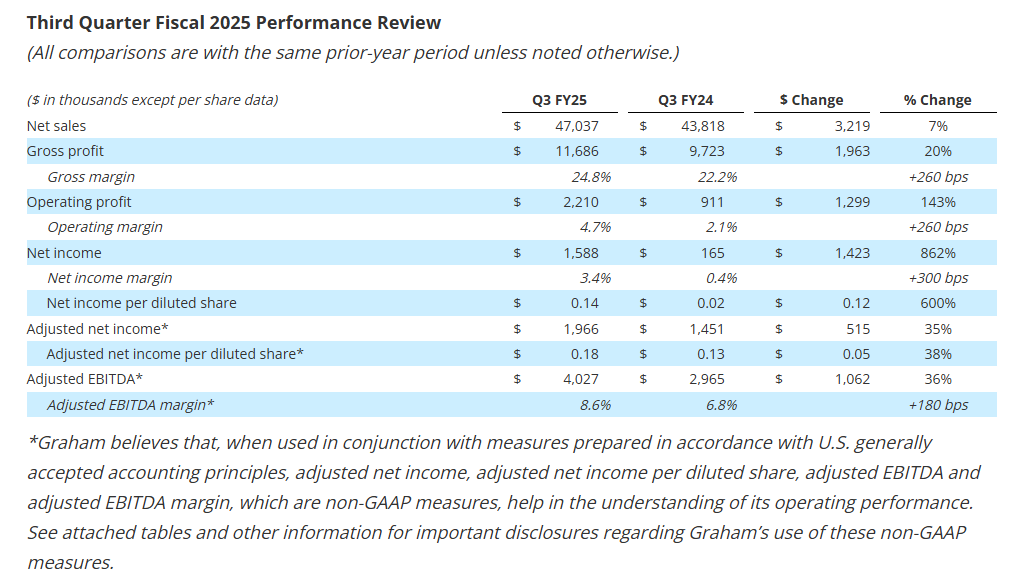

Revenue increased 7.3% to $47.0 million driven by continued strength in key end-markets

Gross profit margin improved 260 basis points to 24.8% of sales, net margin increased 300 basis points to 3.4% of sales, and adjusted EBITDA margin1 expanded 180 basis points to 8.6% of sales

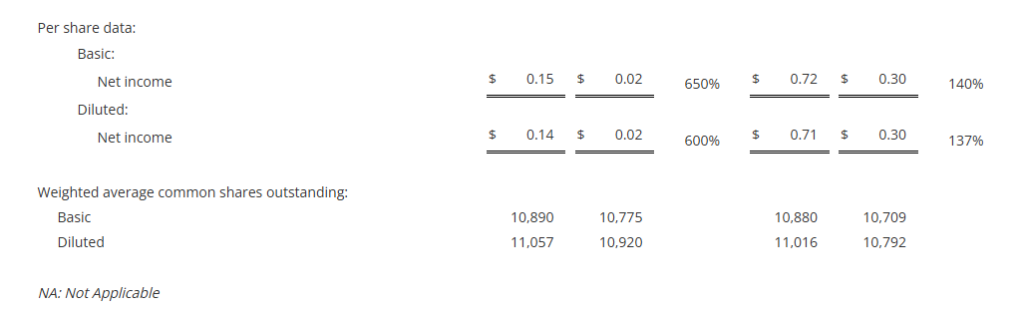

Net income per diluted share increased 600% to $0.14 in the third quarter; adjusted net income per diluted share1 increased 38% to $0.18

Orders of $24.8 million, driven by demand from defense, space, and aftermarket; YTD Book-to-Bill ratio of 1.0x and a backlog of $385 million2

Strong balance sheet with no debt, $30.0 million in cash, and access to $43 million under its revolving credit facility at quarter end to support growth initiatives

Reiterated full year guidance for Sales and adjusted EBITDA1

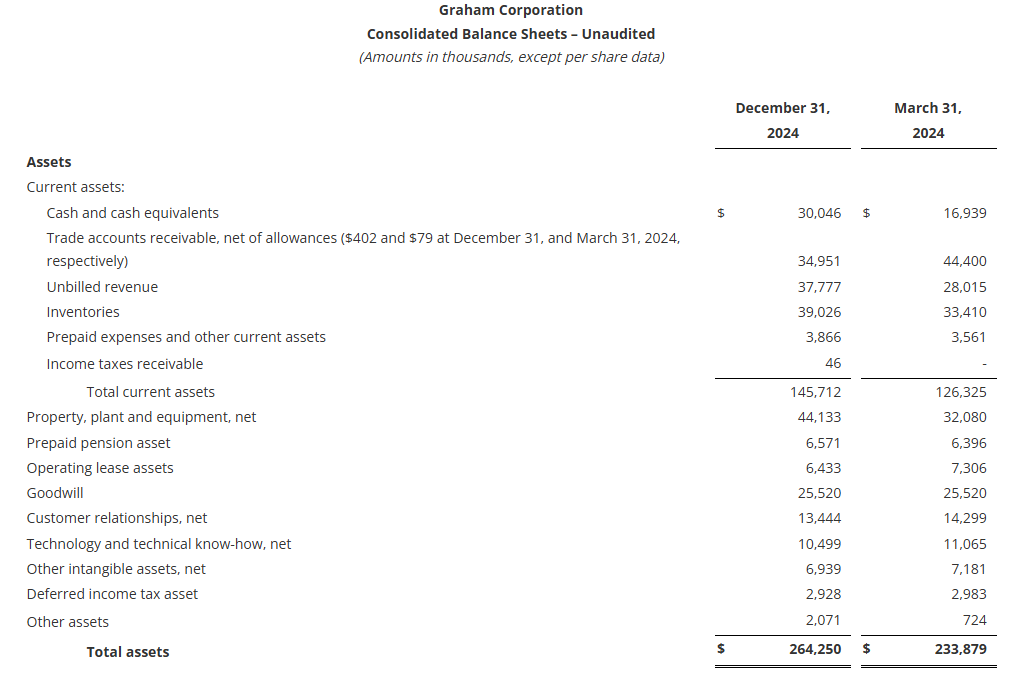

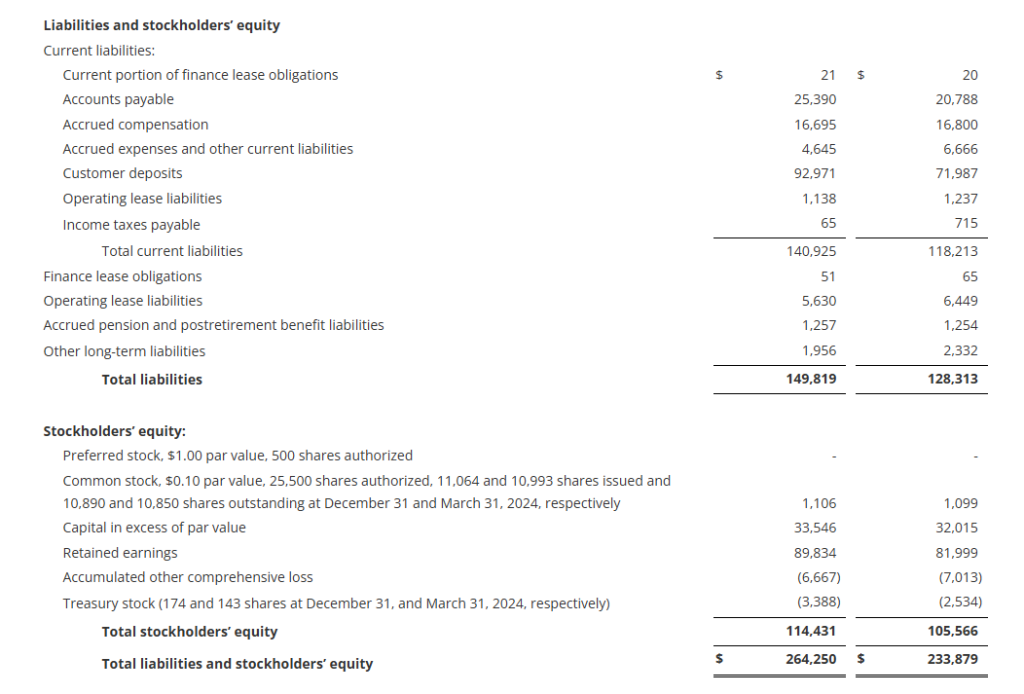

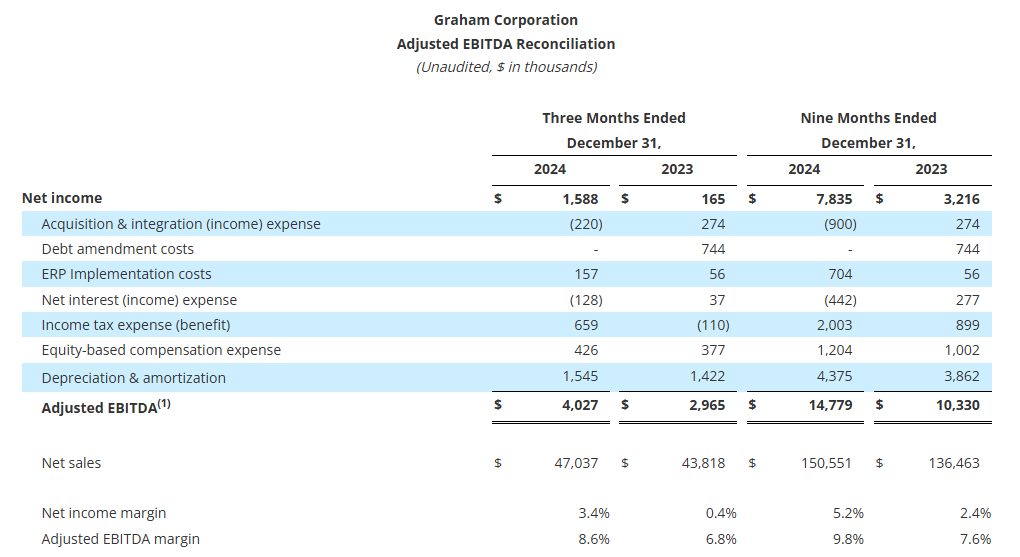

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy, and process industries, today reported financial results for its third quarter for the fiscal year ending March 31, 2025 (“fiscal 2025”).

“Our strong performance through the first three quarters of our fiscal year reflects continually improving execution across our business. Customer demand for our diversified product portfolio is robust, driving margin expansion through improved product mix and operational efficiency. The progress we have shown to date, coupled with advancing discussions on both new programs and expansions with existing customers, reinforces our confidence in achieving our long-term growth targets,” said Daniel J. Thoren, Chief Executive Officer.

____________________ 1Adjusted EBITDA margin, Adjusted Net Income per Diluted Share and Adjusted EBITDA are non-GAAP measures. See attached tables and other information for important disclosures regarding Graham’s use of these non-GAAP measures. 2Orders, backlog and book-to-bill ratio are key performance metrics. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics.

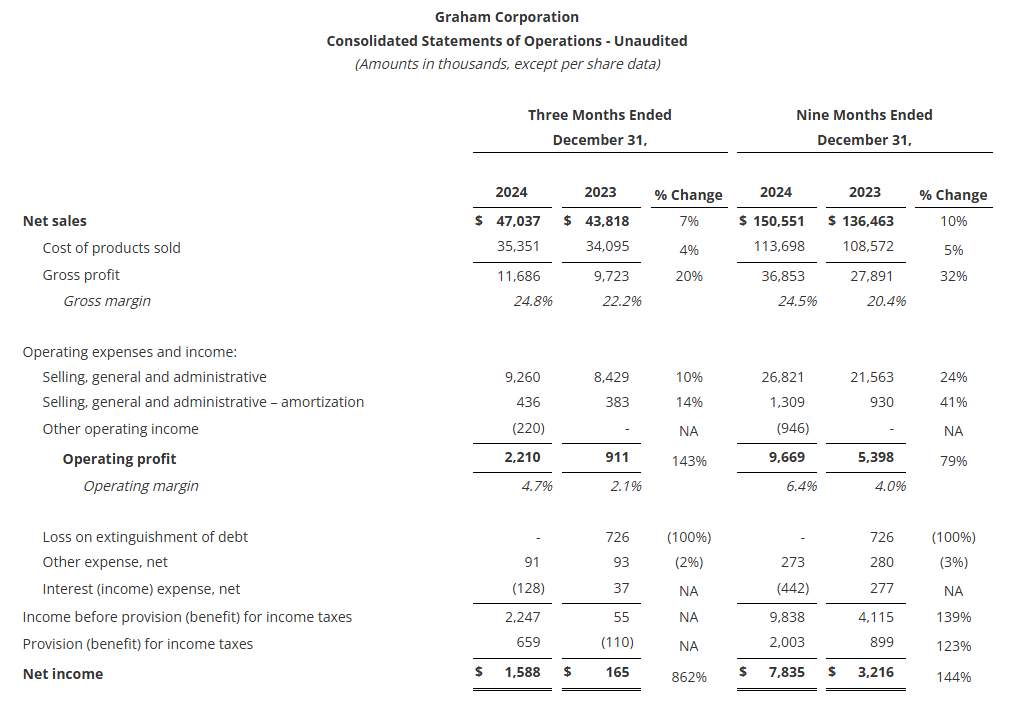

Quarterly net sales of $47.0 million increased 7.3%, or $3.2 million. Sales to the defense market grew by $2.7 million, or 11.1% from the prior year period, driven by the addition of new defense programs, the ramp-up of existing programs, better execution, and the timing of key project milestones. Additionally, higher chemical/petrochemical sales contributed $2.7 million to growth, driven by increased sales of capital equipment. Aftermarket sales to the refining, chemical/petrochemical, and defense markets of $9.7 million remained strong and were 2.4% higher than the prior year. See supplemental data for a further breakdown of sales by market and region.

Gross profit for the quarter increased $2.0 million to $11.7 million compared to the prior-year period of $9.7 million. As a percentage of sales, gross profit margin increased 260 basis points to 24.8%, compared to the fiscal third quarter of 2024. This increase was driven by leverage on higher volume, better execution, and improved pricing, partially offset by higher incentive compensation compared to the prior year period.

Additionally, the third quarter of fiscal 2025 gross profit benefited $0.3 million from a $2.1 million grant received from the BlueForge Alliance earlier this fiscal year to reimburse Graham for the cost of the Company’s defense welder training programs in Batavia and related equipment. To date, the Company has received $1.5 million of funding under this grant.

Selling, general and administrative expense (“SG&A”), including amortization, totaled $9.7 million, or 20.6% of sales, up $0.9 million compared with the prior year. This increase reflects the Company’s continued investments in its people, processes, and technology to drive long-term sustainable growth.

Included in other operating income for the third quarter of fiscal 2025 was a $0.2 million reversal of a previously accrued contingent earnout liability for P3. The reversal was due to delayed orders/projects that extended beyond the earnout period.

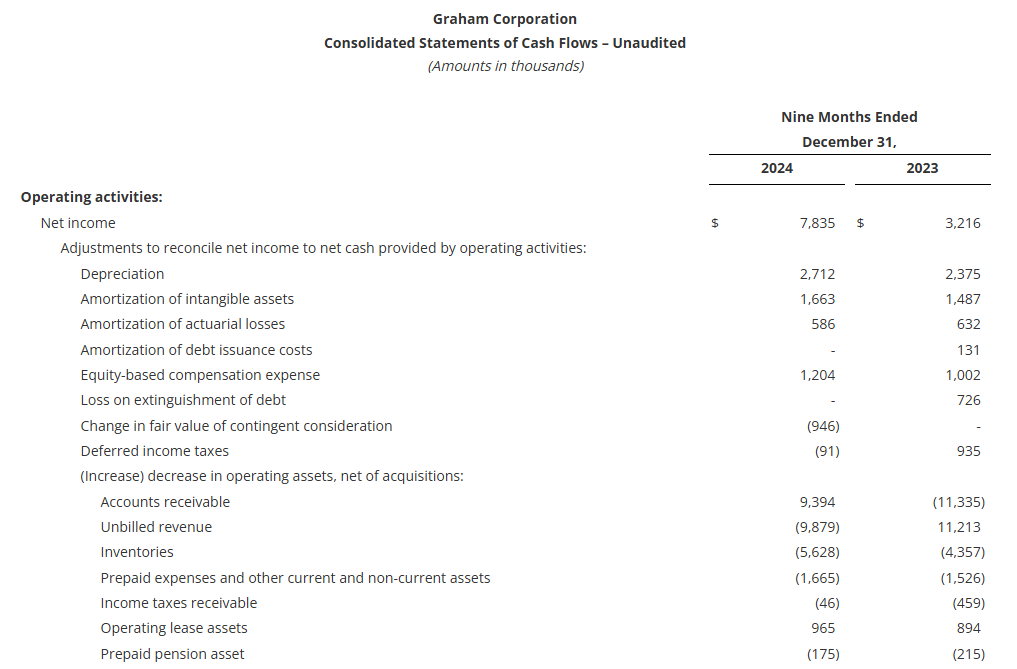

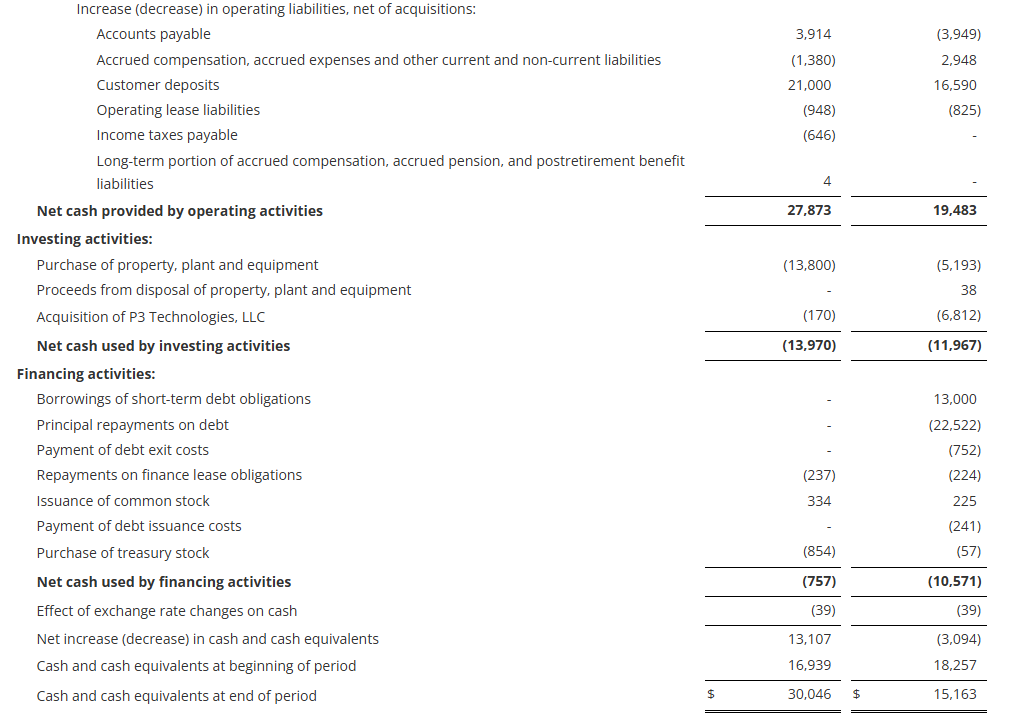

Cash Management and Balance Sheet Cash provided by operating activities totaled $27.9 million for the nine-month period ending December 31, 2024, an increase of $8.4 million from the comparable period in fiscal 2024. As of December 31, 2024, cash and cash equivalents were $30.0 million, up from $16.9 million at the end of fiscal 2024.

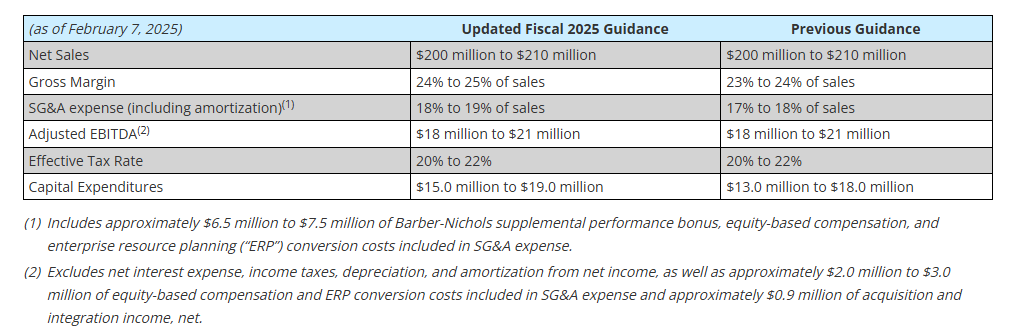

Capital expenditures of $13.8 million for the first nine months of fiscal 2025 were focused on capacity expansion, increasing capabilities, and productivity improvements. The Company increased its expected fiscal 2025 capital expenditures to be in the range of $15.0 million to $19.0 million from its previous expectations of $13.0 million to $18.0 million due to a faster pace of execution on the capital projects in process. All major capital projects are on time and on budget.

The Company had no debt outstanding at December 31, 2024 with $43 million available on its revolving credit facility after taking into account outstanding letters of credit.

Orders, Backlog, and Book-to-Bill Ratio See supplemental data filed with the Securities and Exchange Commission on Form 8-K and provided on the Company’s website for a further breakdown of orders and backlog by market. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics.

As expected, orders for the third quarter of fiscal 2025 declined to $24.8 million given the higher level of orders earlier in the fiscal year. Orders tend to be lumpy given the nature of our business (i.e. large capital projects) and in particular, orders to the defense industry, which span multiple years and are larger in size. Orders for the nine-month period ended December 31, 2024, were $144.2 million, resulting in a year-to-date book-to-bill ratio of 1.0x. After-market orders for the refining, petrochemical, and defense markets remained strong and totaled $13.0 million for the third quarter of fiscal 2025, an increase of 51% over the prior year.

Backlog at quarter end was $384.7 million, down 3.6% over the prior-year period and down 5.5% sequentially. Approximately 45% to 50% of orders currently in backlog are expected to be converted to sales in the next twelve months and another 35% to 40% are expected to convert to sales within one to two years. The majority of orders expected to convert beyond twelve months are for the defense industry, specifically the U.S. Navy.

Fiscal 2025 Outlook The Company’s outlook for 2025 was updated as follows:

Webcast and Conference Call GHM’s management will host a conference call and live webcast on February 7, 2025 at 11:00 a.m. Eastern Time (“ET”) to review its financial results as well as its strategy and outlook. The review will be accompanied by a slide presentation, which will be made available immediately prior to the conference call on GHM’s investor relations website.

A question-and-answer session will follow the formal presentation. GHM’s conference call can be accessed by calling (201) 689-8560. Alternatively, the webcast can be monitored from the events section of GHM’s investor relations website.

A telephonic replay will be available from 3:00 p.m. ET today through Friday, February 14, 2025. To listen to the archived call, dial (412) 317-6671 and enter conference ID number 13750971 or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

About Graham Corporation Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer and vacuum technologies for the defense, space, energy, and process industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise in vacuum and heat transfer, cryogenic pumps, and turbomachinery technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “expects,” “future,” “outlook,” “anticipates,” “believes,” “could,” “guidance,” ”may”, “will,” “plan” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, profitability of future projects and the business, its ability to deliver to plan, its ability to continue to strengthen relationships with customers in the defense industry, its ability to secure future projects and applications, expected expansion and growth opportunities, anticipated sales, revenues, adjusted EBITDA, adjusted EBITDA margins, capital expenditures and SG&A expenses, the timing of conversion of backlog to sales, orders, market presence, profit margins, tax rates, foreign sales operations, customer preferences, changes in market conditions in the industries in which it operates, changes in general economic conditions and customer behavior, forecasts regarding the timing and scope of the economic recovery in its markets, and its acquisition and growth strategy, are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

Non-GAAP Financial Measures Adjusted EBITDA is defined as consolidated net income (loss) before net interest expense, income taxes, depreciation, amortization, other acquisition related expenses, and other unusual/nonrecurring expenses. Adjusted EBITDA margin is defined as Adjusted EBITDA as a percentage of sales. Adjusted EBITDA and Adjusted EBITDA margin are not measures determined in accordance with generally accepted accounting principles in the United States, commonly known as GAAP. Nevertheless, Graham believes that providing non-GAAP information, such as Adjusted EBITDA and Adjusted EBITDA margin, is important for investors and other readers of Graham’s financial statements, as it is used as an analytical indicator by Graham’s management to better understand operating performance. Moreover, Graham’s credit facility also contains ratios based on Adjusted EBITDA. Because Adjusted EBITDA and Adjusted EBITDA margin are non-GAAP measures and are thus susceptible to varying calculations, Adjusted EBITDA, and Adjusted EBITDA margin, as presented, may not be directly comparable to other similarly titled measures used by other companies.

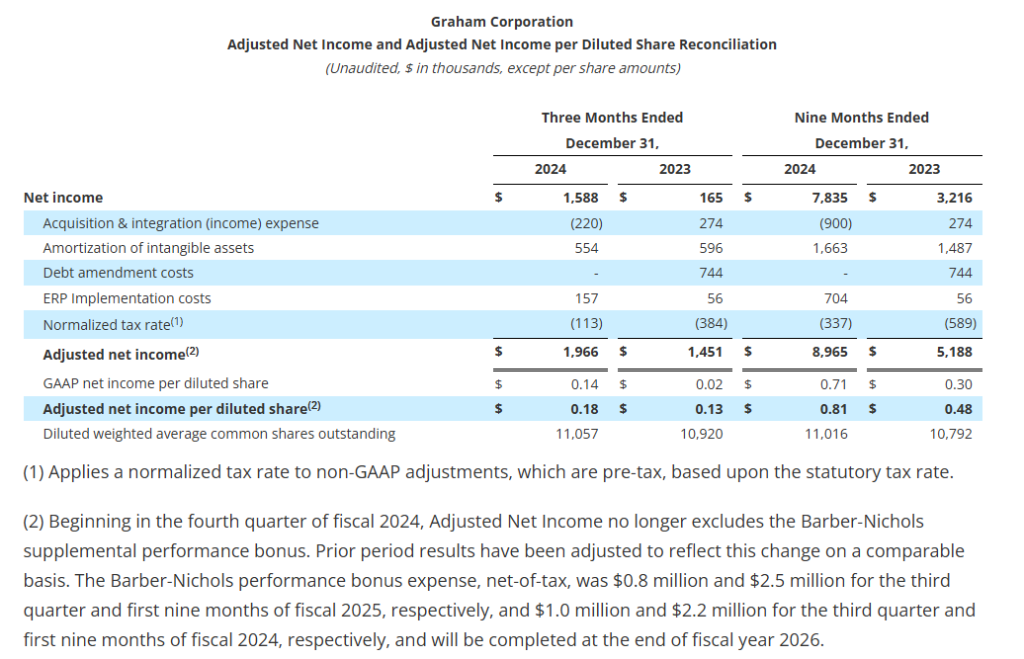

Adjusted net income and adjusted net income per diluted share are defined as net income and net income per diluted share as reported, adjusted for certain items and at a normalized tax rate. Adjusted net income and adjusted net income per diluted share are not measures determined in accordance with GAAP, and may not be comparable to the measures as used by other companies. Nevertheless, Graham believes that providing non-GAAP information, such as adjusted net income and adjusted net income per diluted share, is important for investors and other readers of the Company’s financial statements and assists in understanding the comparison of the current quarter’s and current fiscal year’s net income and net income per diluted share to the historical periods’ net income and net income per diluted share. Graham also believes that adjusted net income per share, which adds back intangible amortization expense related to acquisitions, provides a better representation of the cash earnings of the Company.

Forward-Looking Non-GAAP Measures Forward-looking adjusted EBITDA and adjusted EBITDA margin are non-GAAP measures. The Company is unable to present a quantitative reconciliation of these forward-looking non-GAAP financial measures to their most directly comparable forward-looking GAAP financial measures because such information is not available, and management cannot reliably predict the necessary components of such GAAP measures without unreasonable effort largely because forecasting or predicting our future operating results is subject to many factors out of our control or not readily predictable. In addition, the Company believes that such reconciliations would imply a degree of precision that would be confusing or misleading to investors. The unavailable information could have a significant impact on the Company’s fiscal 2025 financial results. These non-GAAP financial measures are preliminary estimates and are subject to risks and uncertainties, including, among others, changes in connection with purchase accounting, quarter-end, and year-end adjustments. Any variation between the Company’s actual results and preliminary financial estimates set forth above may be material.

Key Performance Indicators In addition to the foregoing non-GAAP measures, management uses the following key performance metrics to analyze and measure the Company’s financial performance and results of operations: orders, backlog, and book-to-bill ratio. Management uses orders and backlog as measures of current and future business and financial performance, and these may not be comparable with measures provided by other companies. Orders represent written communications received from customers requesting the Company to provide products and/or services. Backlog is defined as the total dollar value of net orders received for which revenue has not yet been recognized. Management believes tracking orders and backlog are useful as they often times are leading indicators of future performance. In accordance with industry practice, contracts may include provisions for cancellation, termination, or suspension at the discretion of the customer.

The book-to-bill ratio is an operational measure that management uses to track the growth prospects of the Company. The Company calculates the book-to-bill ratio for a given period as net orders divided by net sales.

Given that each of orders, backlog, and book-to-bill ratio are operational measures and that the Company’s methodology for calculating orders, backlog and book-to-bill ratio does not meet the definition of a non-GAAP measure, as that term is defined by the U.S. Securities and Exchange Commission, a quantitative reconciliation for each is not required or provided.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Zomedica Launches New ACTH Assay For Equine PPID. Zomedica has launched an updated TRUFORMA assay for diagnosis of Equine PPID, Pituitary Pars Intermedia Dysfunction, an endocrine disorder in horses also known as Equine Cushing’s Disease. The new assay measures ACTH and one of its breakdown products, CLIP, then calculates a value that can be compared with established standard levels. The measures in this assay allow for better, faster diagnosis at the point-of-care.

PPID Is A Common Condition In Older Horses. An estimated 20% of the horses over 15 years of age are affected by PPID. Benign tumors or enlargement of the pituitary gland leads to overproduction of endocrine hormones and dysregulation of metabolism. ACTH is one of the hormones affected, causing a variety of symptoms that may lead to muscle wasting, thirst, urination, behavior, immune suppression, and metabolic changes. This affects the horse’s overall health, quality of life, and value to the owner.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Graham Corporation designs, manufactures and sells critical equipment for the energy, defense and chemical/petrochemical industries. The Company designs and manufactures custom-engineered ejectors, vacuum pumping systems, surface condensers and vacuum systems. It is a nuclear code accredited fabrication and specialty machining company. It supplies components used inside reactor vessels and outside containment vessels of nuclear power facilities. Its equipment is found in applications, such as metal refining, pulp and paper processing, water heating, refrigeration, desalination, food processing, pharmaceutical, heating, ventilating and air conditioning. For the defense industry, its equipment is used in nuclear propulsion power systems for the United States Navy. The Company’s products are used in a range of industrial process applications in energy markets, including petroleum refining, defense, chemical and petrochemical processing, power generation/alternative energy and other.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A Transition. Yesterday, Graham Corporation announced its current President and CEO, Daniel Thoren, will transition to the role of Executive Chairman, effective June 10, 2025. Matthew J. Malone, current Vice President and General Manager for Graham subsidiary Barber-Nichols, will be appointed to President & COO effective February 2025 and is expected to assume the CEO role of Graham Corporation in June 2025. The transition is part of an established succession plan.

Malone Background. Mr. Malone brings over 15 years of engineering and executive experience to his new role as President and Chief Operating Officer. Mr. Malone joined Barber-Nichols in 2015 as a Project Engineer focused on rocket engine turbopump design and development. He was promoted to Navy Program Manager in 2018, overseeing key U.S. Navy programs, and was appointed Vice President of Operations at Barber-Nichols in 2020 and then General Manager in 2021.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Sale of M/V Tasos. EuroDry Ltd. recently agreed to sell the M/V Tasos, a vessel built in 2000, for ~$5 million. The vessel is expected to be scrapped and recycled and will be delivered to its buyer between mid-February and mid-March 2025. Eurodry expects to book a gain of approximately $2.1 million. Following the sale of the M/V Tasos, Eurodry will have a fleet of 12 vessels with total cargo capacity of 843,402 dwt. Upon delivery of two Ultramax vessels in 2027, the fleet will consist of 14 vessels with total cargo capacity of 970,402 dwt.

Market environment. Charter rates have continued to decline due, in part, to a weak outlook for the economy in China, which accounts for a large portion of dry bulk trade, and previous route disruptions that have largely abated. The Panama Canal has returned to full capacity, further undermining dry bulk rates. Recent U.S. tariffs imposed on imports from China could also weigh on its economy. While higher scrapping rates and more stringent environmental regulations could constrain the available bulker fleet, we are not optimistic that rates will make a significant recovery in 2025 despite a historically low industry order book.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

DLH delivers improved health and readiness solutions for federal programs through research, development, and innovative care processes. The Company’s experts in public health, performance evaluation, and health operations solve the complex problems faced by civilian and military customers alike, leveraging digital transformation, artificial intelligence, advanced analytics, cloud-based applications, telehealth systems, and more. With over 2,300 employees dedicated to the idea that “Your Mission is Our Passion,” DLH brings a unique combination of government sector experience, proven methodology, and unwavering commitment to public health to improve the lives of millions. For more information, visit www.DLHcorp.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Revenue Decline. 1Q25 y-o-y lower revenue was driven by the unbundling of contracts to small business set-asides, which negatively impacted revenue by $3.5 million, $1.5 million from the winding down of acquired small business contracts, another $1.5 million from winding down of international business, and roughly $2 million of HHS revenue that was pushed out into the second quarter of 2025.

Strong Pipeline. DLH’s pipeline remains strong with over $4.0 billion of new business opportunities. For fiscal year 2025, management identified 13 opportunities worth a total of $700 million. The Company is focused on opportunities that leverage DLH’s digital transformation, cyber security, research and development, and systems engineering capabilities.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Alumis and ACELYRIN have agreed to an all-stock merger, creating a well-capitalized biopharmaceutical company focused on advancing immunology treatments. – The combined company will have approximately $737 million in cash and securities, supporting multiple clinical trial readouts and operations into 2027. – Alumis will retain its name and leadership team, with an expanded board including two ACELYRIN members, and the merger is expected to close in Q2 2025.

Alumis Inc. (NASDAQ: ALMS) and ACELYRIN (NASDAQ: SLRN) have announced a definitive merger agreement, combining the two clinical-stage biopharmaceutical companies in an all-stock transaction aimed at advancing immunology treatments and optimizing clinical outcomes.

Strategic Rationale and Financial Position

The merger will create a strongly capitalized company with a combined cash, cash equivalents, and marketable securities position of approximately $737 million as of year-end 2024. This financial strength is expected to support the advancement of the companies’ combined pipeline through multiple key clinical data readouts and fund operating expenses and capital expenditures into 2027.

The combined company will leverage its track record in research and development and a proprietary data and analytics platform to drive innovation in immune-mediated diseases.

Martin Babler, President, CEO, and Chairman of Alumis, stated: “Through this combination with ACELYRIN, Alumis will have the financial flexibility and runway to advance an expanded late-stage pipeline, now including lonigutamab, and build commercial capabilities. Since completing our IPO, Alumis has operated with speed and rigor, and the multiple development milestones expected in 2025 and 2026, coupled with potential additional indications for ESK-001, represent exciting breakthroughs for our patients and value-driving opportunities for the combined company’s stockholders. As we move forward together, we will maintain financial discipline and a flexible capital allocation strategy with the goal of maximizing the value of our highly differentiated portfolio.”

Pipeline Highlights

Alumis’ ESK-001: A next-generation, allosteric TYK2 inhibitor, currently in Phase 3 ONWARD trials for moderate-to-severe plaque psoriasis (PsO) and Phase 2b LUMUS trials for systemic lupus erythematosus (SLE). Key Phase 2 52-week updates expected in 2025, with Phase 3 topline data in H1 2026.

Alumis’ A-005: A CNS-penetrant allosteric TYK2 inhibitor, targeting neuroinflammatory and neurodegenerative diseases like multiple sclerosis (MS) and Parkinson’s Disease. A Phase 2 trial is set to begin in H2 2025.

ACELYRIN’s Lonigutamab: A subcutaneous anti-IGF-1R therapy with best-in-class potential for thyroid eye disease (TED), currently under Phase 2 evaluation.

Transaction Terms & Leadership Structure

Exchange Ratio: ACELYRIN stockholders will receive 0.4274 shares of Alumis common stock for each ACELYRIN share owned.

Leadership: The combined company will operate under the Alumis name and be led by Alumis’ executive team, strengthened by key ACELYRIN professionals and medical experts.

Board Expansion: The board will grow to nine members, including two from ACELYRIN.

Closing Timeline: The transaction is expected to close in Q2 2025, subject to regulatory and shareholder approvals.

This merger brings together two companies dedicated to transforming immunology treatments, strengthening their pipeline, and delivering long-term value to patients and investors alike.

Key Points: – January job growth slowed to 143,000, falling below expectations and marking a sharp decline from December’s revised 307,000 gain. – Wage growth increased by 4.1% over the past year, outpacing inflation but continuing to pose affordability challenges for consumers. – The Federal Reserve and markets are closely monitoring labor trends, while rising trade policy uncertainty and potential economic shifts under President Trump add to financial volatility.

The U.S. labor market saw weaker-than-expected job growth in January, with nonfarm payrolls increasing by 143,000, below the Dow Jones forecast of 169,000 and down from a revised 307,000 in December. Meanwhile, the unemployment rate declined to 4.0%, showing continued resilience in the job market despite the slowdown in hiring.

Key Takeaways from the January Jobs Report

Weaker Job Growth: January’s 143,000 job gain marks a sharp decline from December and falls below expectations.

Downward Revisions: Total payroll numbers for 2024 were revised downward by 589,000 over the trailing 12-month period ending in March 2024.

Sector Performance:

Healthcare: +44,000 jobs

Retail: +34,000 jobs

Government: +32,000 jobs

Labor Force Participation: Increased 0.1% from December to 62.6%.

2024 Job Growth Trend: The monthly average for job growth in 2024 stood at 166,000 per month.

Wage Growth: Average hourly earnings rose 4.1% over the past year, partly due to minimum wage hikes in parts of the country.

Affordability Challenges: Wage growth continues to outpace recent inflation rates, but many consumers still face affordability challenges.

Market and Federal Reserve Reactions

Markets showed little reaction to the report in early trading, as investors had largely anticipated a slowdown in job creation. Federal Reserve officials are closely monitoring labor market data as they consider future monetary policy moves. The Fed cut its benchmark interest rate by a full percentage point in late 2024, and today’s report may influence their next steps regarding interest rate adjustments. President Trump recently stated that the Fed’s decision last week to hold rates steady was well-advised, despite previously criticizing the move.

Broader Economic and Political Context

Some indicators, such as hiring rates, suggest slower movement in the job market. Meanwhile, business executives remain optimistic that Trump’s policies—such as tax cuts and deregulation—will boost economic growth. However, Trump’s recent tariff decisions have rattled markets, adding to economic uncertainty. Rising trade policy uncertainty could further heighten financial market volatility in the coming months.

The Historical Importance of Jobs Reports

The monthly jobs report is one of the most closely watched economic indicators, providing insights into labor market health, consumer spending power, and broader economic momentum. Historically, strong job growth has been associated with economic expansion, while sluggish reports can indicate slowdowns or even recessions. Policymakers, investors, and businesses use these reports to make critical decisions on interest rates, hiring strategies, and economic forecasts. In the current environment, sustained job growth and wage pressures suggest a resilient labor market, even as broader economic uncertainties loom.

With job growth slowing but unemployment remaining stable, policymakers will weigh the need for further economic stimulus against concerns of overheating the labor market. The upcoming months will be crucial in determining whether this slowdown is temporary or indicative of a broader labor market trend.

James J. Ferguson, MD, FACC, FAHA, joins as Chief Medical Officer

Extensive experience provides strong support for advancing specialized cardiovascular assets, including leading the late-stage clinical development of tecarfarin and other business development opportunities

PONTE VEDRA, Fla. – Cadrenal Therapeutics, Inc. (Nasdaq: CVKD), a late-stage biopharmaceutical company focused on the development of specialized cardiovascular therapies, with the late-stage asset tecarfarin, a new Vitamin K antagonist, today announced a leadership transition appointing James J. Ferguson, MD, FACC, FAHA, as its new Chief Medical Officer, effective immediately. Dr. Ferguson is a distinguished medical expert with over 25 years of leadership in the cardiovascular field and deep expertise in clinical development. Dr. Ferguson will lead the late-stage clinical development of tecarfarin to include the pivotal trial in LVAD patients and other indications in rare cardiovascular conditions requiring life-long anticoagulation therapy as well as other business development opportunities to build the Company’s pipeline.

Dr. Ferguson replaces Douglas W. Losordo, MD. Cadrenal thanks Dr. Douglas Losordo for his contributions to advancing the development of our tecarfarin program.

“We welcome Dr. Ferguson to our team and are confident that he will play a critical role in driving the late-stage clinical development of tecarfarin and the prioritization of indications. Dr. Ferguson brings expertise and strong relationships with cardiovascular clinical and scientific thought leadership, which will be instrumental as we prepare for late-stage clinical development of our tecarfarin program,” said Quang X. Pham, Chief Executive Officer, Cadrenal Therapeutics, Inc.

Dr. Ferguson joins Cadrenal after serving as Chief Medical Officer at Matinas BioPharma. Previously, Dr. Ferguson was Head of U.S. Cardiovascular Medical Affairs at Amgen and held several senior positions at AstraZeneca, including Vice President of US Cardiovascular Medical and Scientific External Relations, Therapeutic Area Vice President of Cardiovascular Global Medical Affairs, and US Development brand leader for BRILINTA.

“I’m truly honored to be joining Cadrenal at this exciting and transformative time. I look forward to advancing the late-stage clinical development of tecarfarin and bringing forward the first innovation in vitamin K-targeted anticoagulation in 70 years. This product could have a truly meaningful impact for patients in whom there continues to be major unmet medical needs with standard warfarin therapy,” said Dr. Ferguson.

About Cadrenal Therapeutics, Inc.

Cadrenal Therapeutics, Inc. is a late-stage biopharmaceutical company focused on developing specialized therapeutics for rare cardiovascular conditions. The Company is developing tecarfarin, a vitamin K antagonist (VKA) designed to be a better and safer anticoagulant than warfarin for individuals with implanted cardiac devices. Cadrenal strives to improve outcomes and reduce major adverse events for these patients. Although warfarin is widely used off-label for several rare cardiovascular diseases, extensive clinical and real-world data have shown it to have significant serious side effects. With its innovation, Cadrenal aims to meet the unmet needs of this patient population by relieving them and their healthcare providers of some of warfarin’s greatest clinical challenges.

Cadrenal is pursuing a product in a pipeline approach with tecarfarin. Tecarfarin received Orphan Drug designation (ODD) for advanced heart failure patients with implanted left ventricular assist devices (LVADs). In 2025, the Company plans to initiate a pivotal Phase 3 trial evaluating tecarfarin versus warfarin for LVAD patients. The Company also received ODD and fast-track status for tecarfarin in end-stage kidney disease and atrial fibrillation (ESKD+AFib).

Cadrenal is opportunistically pursuing business development initiatives with a longer-term focus to build a pipeline of specialized cardiovascular therapies. For more information, visit www.cadrenal.com and connect with us on LinkedIn.

Safe Harbor

Any statements contained in this press release about future expectations, plans, and prospects, as well as any other statements regarding matters that are not historical facts, may constitute “forward-looking statements.” The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potentially,” “predict,” “project,” “should,” “target,” “will,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. These statements include statements regarding the contributions to be made by Dr. Ferguson including leading the late-stage clinical development of tecarfarin to include the pivotal trial in LVAD patients and other indications in rare cardiovascular conditions requiring life-long anticoagulation therapy as well as other business development opportunities to build the Company’s pipeline, as well as advancing other indications in rare cardiovascular conditions requiring chronic anticoagulation; playing a critical role in driving the late-stage clinical development of tecarfarin and the prioritization of indications; Dr. Ferguson’s expertise and strong relationships with cardiovascular clinical and scientific thought leadership being instrumental as the Company prepares for the for late-stage clinical development of our tecarfarin programs; advancing the late-stage clinical development of tecarfarin and bringing forward the first innovation in vitamin K-targeted anticoagulation in 70 years; the product having a truly meaningful impact for patients in whom there continues to be major unmet medical needs with standard warfarin therapy; the Company striving to improve outcomes and reduce major adverse events for patients; the Company aiming to meet the unmet needs of the patient population by relieving them and their healthcare providers of some of warfarin’s greatest clinical challenges; and the Company initiating in 2025 a pivotal Phase 3 trial evaluating tecarfarin versus warfarin for LVAD patients. Actual results may differ materially from those indicated by such forward-looking statements as a result of various important factors, including the ability to derive benefits from the contributions expected to be made by Dr. Ferguson; the ability to initiate the pivotal Phase 3 clinical trial for tecarfarin in LVAD patients in 2025 and provide improved outcomes; the ability to enter into collaborations with development partners; the ability of tecarfarin to provide a safer alternative to LVAD patients and the other risk factors described in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023, and the Company’s subsequent filings with the Securities and Exchange Commission, including subsequent periodic reports on Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Any forward-looking statements contained in this press release speak only as of the date hereof and, except as required by federal securities laws, the Company specifically disclaims any obligation to update any forward-looking statement, whether as a result of new information, future events, or otherwise.

The new initiative aims to ensure SMBs and mid-market brands aren’t left behind in the digital marketplace

HOUSTON, Feb. 6, 2025 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”) and Orange 142, LLC (“Orange 142”), today announced the formation of its Artificial Intelligence (AI) Council, a new initiative aimed at demystifying and operationalizing artificial intelligence for small and mid-sized business (SMB) advertisers. The cutting-edge council will tackle the widening disparity in AI utilization between large corporations and smaller enterprises by equipping these businesses with actionable AI strategies to enhance their competitiveness in the digital arena.

As digital landscapes evolve, the adoption of AI in advertising has become a critical factor for success. Yet, many SMBs and mid-market brands are disadvantaged due to resource limitations and a lack of specialized knowledge. The AI Council at Direct Digital Holdings is designed to change this narrative by providing small and mid-sized businesses with the tools and insights necessary to leverage AI effectively, leveling the playing field with larger competitors.

“Artificial intelligence is transforming digital advertising, but too often, small and mid-sized businesses are left behind,” said Anu Pillai, Chief Technology Officer at Direct Digital Holdings and Member of the AI Council. “The AI Council’s mission is to bridge this gap. By democratizing access to AI tools and strategies, we empower small and medium-sized businesses to participate and lead in their markets.”

The AI Council will focus on supporting small and mid-sized businesses in several key areas:

Education and Workshops: Offering seminars and resources that explain AI concepts in straightforward terms, making the technology accessible and understandable.

Strategy Development: Assisting small and mid-sized businesses in developing AI-driven advertising strategies that are tailored to their unique business needs and market conditions.

Technology Implementation: Providing support in the implementation of AI tools, from automated bidding systems to customer data analysis, ensuring small and mid-sized businesses can harness AI’s full potential without the need for in-house experts.

Performance Monitoring: Guiding businesses in setting up systems to monitor the effectiveness of AI applications, enabling continuous improvement and optimization

Free Ebooks: We have produced a series of eBooks to help guide SMBs through the process of navigating the complex landscape.

In addition to internal experts, the AI Council will collaborate with technologists, academic leaders, and industry innovators to stay on the cutting edge of AI developments. This collaborative approach ensures that the Council’s initiatives are based on the latest research and best practices, making state-of-the-art AI solutions accessible to small and mid-sized business advertisers. “By leveraging both advertising and AI partners, our company will develop innovative products tailored to the unique needs of small businesses. This includes AI-driven marketing tools that help small and mid-sized businesses optimize their dollars as well as strategic initiatives such as AI training programs and workshops to empower small businesses with the knowledge and skills needed to thrive in a competitive market,” said Christy Nolan, VP of Delivery Solutions at Direct Digital Holdings and Member of the AI Council.

The AI Council will be an ongoing effort to ensure that all Direct Digital Holdings customers, regardless of size, have the tools and knowledge to succeed in an increasingly AI-driven world.

Direct Digital Holdings (Nasdaq: DRCT) brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within the general market and multicultural media properties. The Company’s buy-side platform, Orange 142, delivers significant ROI for middle-market advertisers by providing data-optimized programmatic solutions for businesses in sectors ranging from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions generate billions of impressions per month across display, CTV, in-app, and other media channels.