Will the CPI Number or Fed Minutes Change the Market Direction this Week?

Market-moving economic reports are likely this week. Those with the highest chance to move markets are March CPI data on Wednesday, then FOMC minutes from the meeting just after last month’s bank failures, and the Producer Price Index on Thursday.

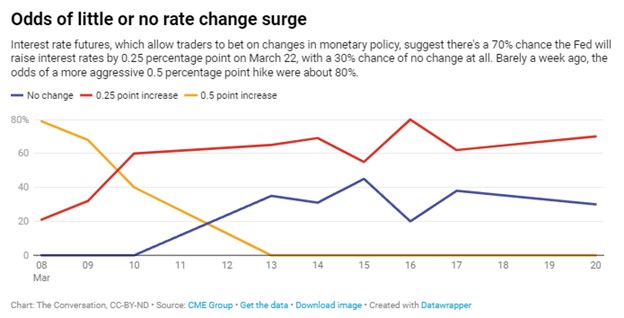

The minutes of the March 21-22 FOMC meeting will be released at 2:00 PM Wednesday, this highly watched information coincides with the half-fiscal year Budget Report from the U.S. Treasury. The FOMC minutes will get a lot of attention, but the U.S. Budget Deficit is likely to receive renewed focus as we approach summer and begin to bump up against the Treasury’s borrowing ceiling.

Monday 4/10

- 10:00 AM ET, Wholesale Inventories’ second estimate for February is expected to show a 0.2 percent build up; this would be unchanged from the first estimate.

Tuesday 4/11

- 6:00 AM ET, Small Business Optimism Index has been below the historical average of 98 for 14 months in a row. March’s consensus is 89.0 versus 90.9 in February. The direction of the health of small businesses can foreshadow changes in the stock market.

- 1:30 PM ET, Austan Goolsbee, President of the Federal Reserve Bank of Chicago will be speaking at a luncheon at the Economic Club of Chicago.

Wednesday 4/12

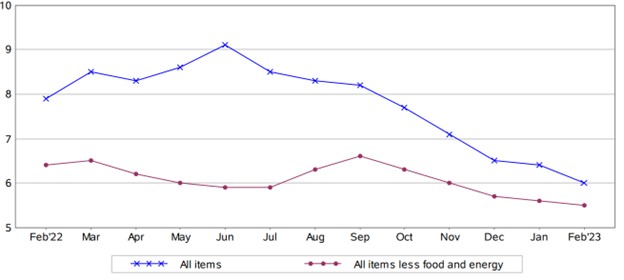

- 8:30 AM ET, The Consumer Price Index (CPI) core prices for March are expected to have risen by 0.4 percent versus February’s sharp and higher-than-expected increase of 0.5 percent. Overall, headline inflation prices are expected to have increased 0.3 percent after February’s 0.4 percent rise. Annual rates, which in February were 6.0 percent overall and 5.5 percent for the core, are expected to show 5.2 and 5.6 percent.

- 9:10 AM ET, Thomas Barkin, President of the Federal Reserve Bank of Richmond will be speaking. He spoke on April 3, indicating his expectations are that low unemployment rates will continue to support the belief that the economy is not at risk of a recession. Inflation, however, is not going away anytime soon, according to Barkin.

- 10:30 AM ET, The Energy Information Administration (EIA) will provide its weekly information on petroleum inventories in the U.S., whether produced here or abroad. The level of inventories helps determine prices for petroleum products. Markets will be paying close attention after OPEC+ cut production one week ago.

- 2:00 PM ET, FOMC minutes from the March 21-22 meeting will be released. This report will have two areas that investors will focus on. These are conversations surrounding U.S. bank health, and those discussions related to inflation and interest rates.

- 2:00 PM ET, the Treasury Statement related to the budget deficit are expected to report a $253.0 billion deficit in March. This would compare with a $192.7 billion deficit in March a year-ago and a deficit in February this year of $262.4 billion. March is the halfway point into the U.S government’s fiscal year.

Thursday 4/13

- 8:30 AM ET, Producer Price Index (PPI), After dropping 0.1 percent lower on the month in February, this inflation index on the producer level in March is expected to be unchanged. March’s ex-food ex-energy rate is seen up 0.3 percent versus February’s no change.

- 4:30 PM ET, the Federal Reserve’s Balance Sheet has been receiving heightened attention. After the Silicon Valley Bank collapse the Fed institutes a new method for banks to get assistance, markets will watch to see if this has grown. Also, as interest rates have risen, the fixed income securities held by the Fed have repriced billions lower, Fed watchers are beginning to comment on how dramatic this drop in value has been. The last line investors will focus on is quantitative easing. Specifically, investors will look to see if the Fed is on track with its letting securities mature off its books without reinvestment – this reduces U.S. dollars in circulation.

Friday 4/14

- 8:30 PM ET, March Retail Sales are expected to have fallen 0.4 percent for a second month in a row. Excluding autos, a 0.4 percent decline is also expected.

- 9:15 AM ET, Industrial Production is expected to rise 0.3 percent in March after being unchanged in February.

- 10:00 AM ET, Business Inventories for February are expected to have risen 0.3 percent following a 0.1 percent draw in January.

- 10:00 AM ET, Consumer Sentiment, which sank five full points in March to 62.0, is expected to improve to 62.7 in the first reading for April.

What Else

Taxes are due April 18 this year. This typically creates a wave of new IRA deposits. On April 13, in NYC there will be a luncheon roadshow with PDS Biotechnology. Noble Capital Markets organize the event, more details are available on Channelchek by clicking here.

Managing Editor, Channelchek

Sources

https://www.guilford.edu/news/2023/04/fed-leader-inflation-remain-persistent