US markets returned Monday from the Juneteenth holiday weekend and walked straight into one of the most consequential data weeks of the year. After Federal Reserve Chair Kevin Warsh’s hawkish debut last Wednesday — which saw the central bank hold rates while signaling that nine of 18 officials now project at least one rate hike before year-end — the coming days will deliver the economic readings that determine whether that hike moves from projection to reality. For small and microcap investors, this is the week the second half of 2026 takes shape.

The May PCE Reading Is the Number That Matters

The single most important data point this week arrives Friday with the release of the May Personal Consumption Expenditures price index — the Fed’s preferred inflation gauge. While the Consumer Price Index gets more headlines, PCE is the measure the FOMC actually uses to assess progress toward its 2% target, which makes Friday’s print the most direct evidence yet of whether inflation is cooling or entrenching.

The context heightens the stakes. May CPI came in at 4.2% year over year, the highest in three years, driven heavily by energy costs tied to the now-easing US-Iran conflict. If PCE confirms that inflation pressure, it strengthens the case for the rate hike the dot plot is signaling. If it shows the energy spike was the dominant and possibly peaking driver — with core inflation more contained — it gives the Fed room to hold without tightening further. Either outcome moves Treasury yields, and Treasury yields move small caps.

GDP Revisions Add Another Layer

Before Friday’s inflation data, markets will digest revised first-quarter GDP figures. The revision matters because it recalibrates the growth side of the Fed’s dual mandate. A stronger-than-expected economy gives the committee more justification to tighten without fear of triggering a downturn. A softer reading complicates the hawkish case and raises the specter of stagflation — weak growth paired with stubborn inflation — which is the single most difficult environment for the Fed to navigate and historically the hardest for smaller, rate-sensitive companies to weather.

Earnings Worth Watching

On the corporate side, two bellwether reports land this week. Micron reports quarterly results that will serve as a direct read on AI-driven memory demand, building on the supercycle narrative that has lifted the entire semiconductor space this year. After Broadcom’s recent guidance-driven selloff reset expectations across chip names, Micron’s numbers will test whether the underlying demand story remains intact for the smaller semiconductor and component companies operating downstream of the same AI buildout.

FedEx also reports, and its results function as a broad economic barometer. As a global logistics operator, FedEx’s volume data and forward guidance offer a real-time read on shipping activity, consumer demand, and industrial output — all directly relevant to the domestically focused small caps that make up the Russell 2000.

Why This Week Matters for Small Caps

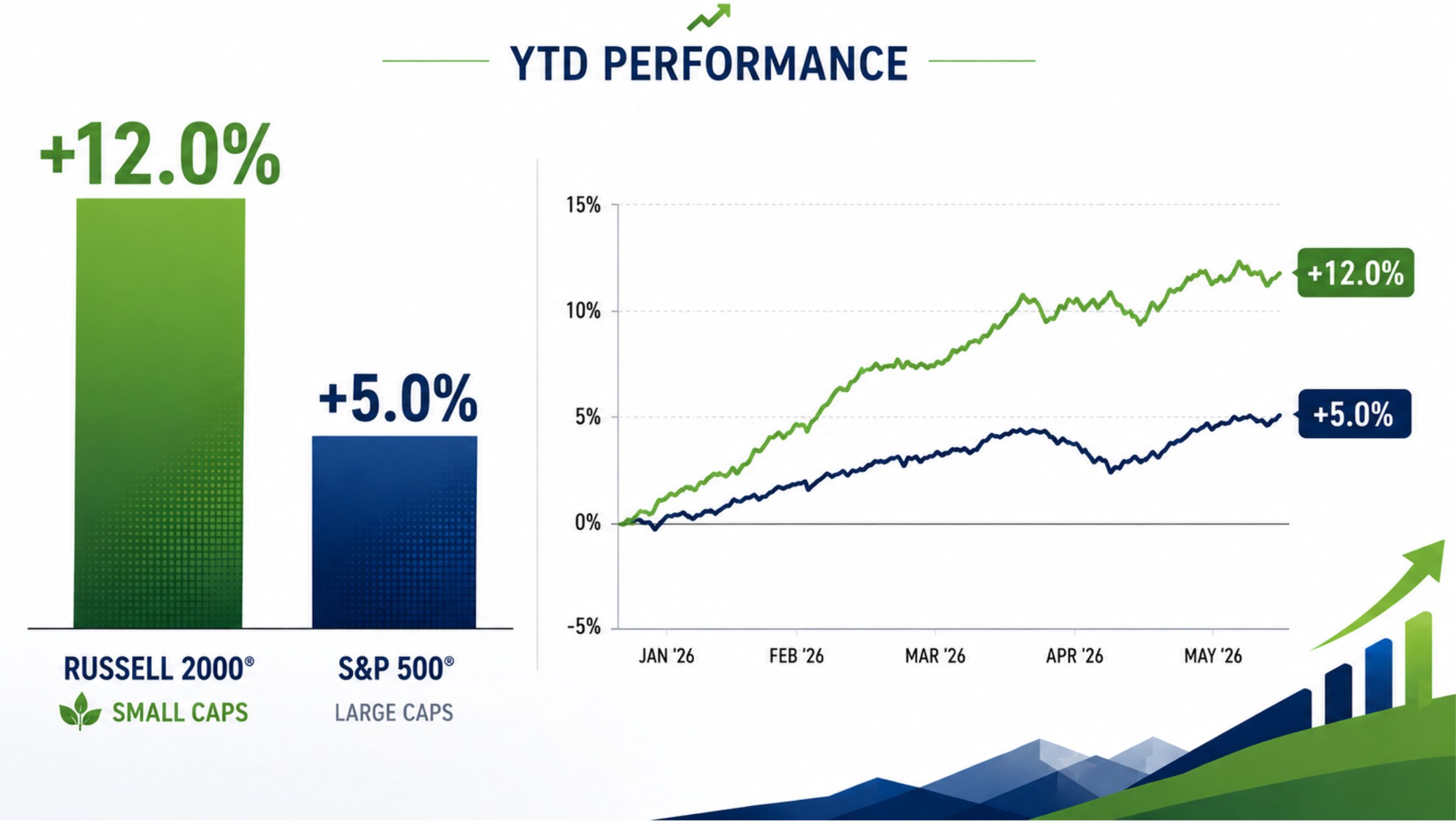

Small and microcap companies carry disproportionately more variable-rate debt than their large cap counterparts, which means the rate path being shaped this week translates directly into their cost of capital and earnings trajectory. The Russell 2000 has spent 2026 caught between strong underlying fundamentals — historic valuation discounts, improving earnings growth, and domestic revenue exposure — and a punishing rate environment that has capped its performance relative to large caps.

This week’s data will tilt that balance. A benign PCE print and solid GDP would support the case that the Fed can hold rather than hike, removing an overhang that has weighed on smaller companies all year. A hot inflation reading paired with strong growth would validate the hawkish dot plot and extend the higher-for-longer environment further into the future. Either way, by Friday afte