Alvopetro Energy Ltd.’s vision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

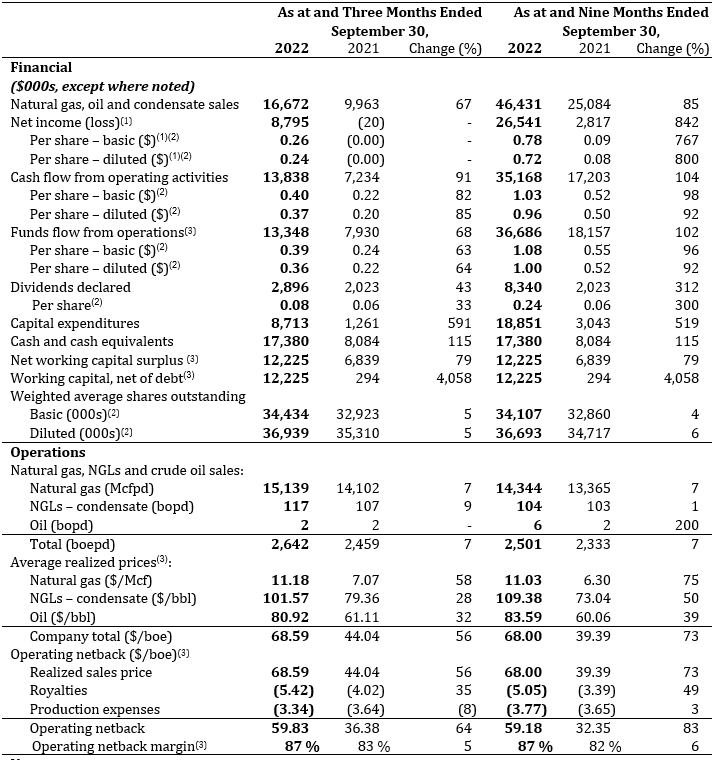

Alvopetro reported 2022-3Q results significantly higher than last year and above our expectations. Revenues rose 67% due to a 7% increase in production and a 58% increase in gas prices. Higher sales translated into higher cash flow ($13.8 million versus $7.2 million) and earnings ($8.8 million versus $0.0).

Results were due to operations improvements and are likely to continue. The company expanded its gas processing facilities in July raising capacity to 3,000 boe/d. With quarterly results, management indicated that October total production averaged 2,720 boe/d, a nice rise above 2022-3Q levels of 2,642 boe/d.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, Nov. 15, 2022 /CNW/ – Alvopetro Energy Ltd. (TSXV:ALV); (OTCQX: ALVOF) is pleased to announce a 50% increase in our quarterly dividend, to US$0.12 per common share, an intention to launch a share buyback program under a normal course issuer bid (“NCIB”) and operating and financial results for the third quarter of 2022 including another record quarter of funds flow from operations of $13.3 million. We will host a live webcast to discuss Q3 2022 results on Wednesday November 16, 2022, beginning at 9:00 am Mountain time.

President & CEO, Corey C. Ruttan commented:

“With continued strong operating and financial results, and with our debt now fully repaid, we are pleased to announce a 50% increase in our quarterly dividend following on the 33% increase earlier this year. Our dividend program and the proposed NCIB will provide us with maximum flexibility to meet our strategy to maintain a balanced organic growth and stakeholder return model.”

All references herein to $ refer to United States dollars, unless otherwise stated and all tabular amounts are in thousands of United States dollars, except as otherwise noted.

Quarterly Dividend Increased 50% to $0.12 per Share

Alvopetro is pleased to announce that our Board of Directors has approved a 50% increase in our quarterly dividend, to $0.12 per common share, payable in cash on January 13, 2023, to shareholders of record at the close of business on December 30, 2022. This dividend is designated as an “eligible dividend” for Canadian income tax purposes.

Dividend payments to non-residents of Canada will be subject to withholding taxes at the Canadian statutory rate of 25%. Shareholders may be entitled to a reduced withholding tax rate under a tax treaty between their country of residence and Canada. For further information, see Alvopetro’s website at https://alvopetro.com/Dividends-Non-resident-Shareholders.

Normal Course Issuer Bid

In connection with our long-standing balanced and disciplined stakeholder return and organic growth model, our Board has provided approval to submit an application to launch a share buyback program under a NCIB, subject to securities law and customary approvals. Once approved, the NCIB, combined with our quarterly dividends, will provide us with flexibility in managing our returns to stakeholders.

Financial and Operating Highlights – Third Quarter of 2022

Daily sales averaged 2,642 boepd in Q3 2022, a 7% increase from the Q3 2021 average of 2,459 boepd and a 12% increase from the Q2 2022 average of 2,359 boepd. The expansion of our gas processing facility was completed at the end of July and available processing capacity has now increased to 500,000 m3/d (18 MMcfpd) contributing to higher volumes in the quarter.

As of August 1, 2022, Alvopetro’s natural gas price has been reset to the new ceiling price of $10.22/MMBtu. Due to the appreciation of the BRL in the first half of 2022 compared to second half of 2021, the BRL contracted price remained consistent at BRL1.94/m3. With all natural gas sales in Q3 2022 at the ceiling price, our average realized natural gas price increased to $11.18/Mcf compared to the Q3 2021 average price of $7.07/Mcf. Higher commodity prices and higher daily sales volumes resulted in a 67% increase in our natural gas, condensate and oil revenue compared to Q3 2021.

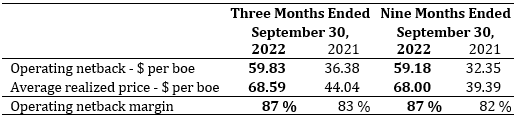

Our operating netback was $59.83 per boe in Q3 2022, an improvement of $23.45 per boe from Q3 2021 (+64%). Despite consistent BRL denominated natural gas pricing, our operating netback decreased $4.13 per boe from Q2 2022 (-6%) due to the devaluation of the BRL relative to the USD and lower Brent pricing on condensate.

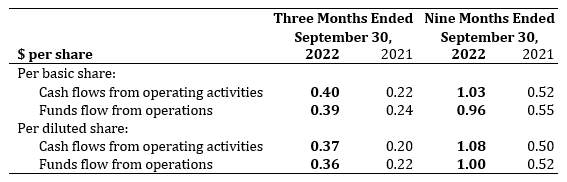

We generated cash flows from operating activities of $13.8 million ($0.40 per basic share and $0.37 per diluted share) and funds flows from operations of $13.3 million ($0.39 per basic share and $0.36 per diluted share), increases of $6.6 million and $5.4 million, respectively compared to Q3 2021.

We reported net income of $8.8 million in Q3 2022 compared to a loss of $0.02 million in Q3 2021.

Capital expenditures totaled $8.7 million, and included drilling costs for our 183-B1, 182-C2 and Unit-C wells, testing costs on our 182-C1 well, long lead purchases and development costs on our Murucututu project.

All outstanding warrants were exercised in the quarter, with 1,342,978 warrants exercised by way of cashless exercise and 1,342,978 warrants exercised at a strike price of $1.80 per share. Alvopetro received cash proceeds of $2.4 million and issued a total of 2,081,616 common shares on the exercise.

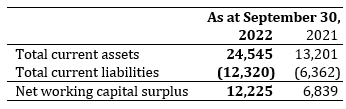

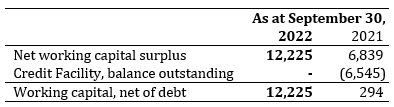

We repaid the final $2.5 million outstanding on the credit facility and the facility has now been cancelled. As at September 30, 2022, we had a net working capital surplus of $12.2 million, including $17.4 million in cash and cash equivalents.

Our October 2022 sales volumes averaged 2,720 boepd based on field estimates, with natural gas sales of 15.6MMcfpd and natural gas liquids from condensate of 124 bopd.

The following table provides a summary of Alvopetro’s financial and operating results for three and nine months ended September 30, 2022 and September 30, 2021. The consolidated financial statements with the Management’s Discussion and Analysis (“MD&A) are available on our website at www.alvopetro.com and will be available on the System for Electronic Document Analysis and Retrieval (SEDAR) website at www.sedar.com.

Notes:

The 2021 comparative periods in the table above have been restated. See “Restatement of the 2021 Comparative Period” section within the MD&A and Note 14 of the unaudited interim condensed consolidated financial statements for the three and nine months ended September 30, 2022 for further details.

Per share amounts are based on weighted average shares outstanding other than dividends per share, which is based on the number of common shares outstanding at each dividend record date. The weighted average number of diluted common shares outstanding in the computation of funds flow from operations and cash flows from operating activities per share is the same as for net income per share.

See “Non-GAAP and Other Financial Measures” section within this news release.

Third Quarter 2022 Results Webcast

Alvopetro will host a live webcast to discuss Q3 2022 financial results at 9:00 am Mountain time on November 16, 2022. Details for joining the event are as follows:

The webcast will include a question-and-answer period. Online participants will be able to ask questions through the Zoom portal. Dial-in participants can email questions directly to socialmedia@alvopetro.com.

Long-term Incentive Compensation Grants

In connection with our long-term incentive compensation program, Alvopetro’s Board of Directors (the “Board”) has approved the annual rolling grants to officers, directors and certain employees under Alvopetro’s Omnibus Incentive Plan. A total of 536,000 stock options, 122,000 restricted share units (“RSUs”) and 40,000 deferred share units (“DSUs”) were approved by the Board and are expected to be granted on November 24, 2022. Of the total grants, 248,000 stock options, 101,000 RSUs and 40,000 DSUs were granted to directors and officers. Each stock option, RSU and DSU entitles the holder to purchase one common share. Each stock option granted will have an exercise price based on the volume weighted average trading price of Alvopetro’s shares on the TSX Venture Exchange for the five (5) consecutive trading days up to and including November 24, 2022. All stock options, RSUs and DSUs granted expire five (5) years from the date of the grant.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Abbreviations:

bbls

=

barrels

boepd

=

barrels of oil equivalent (“boe”) per day

bopd

=

barrels of oil and/or natural gas liquids (condensate) per day

BRL

=

Brazilian Real

m3

=

cubic metre

Mcf

=

thousand cubic feet

Mcfpd

=

thousand cubic feet per day

MMcf

=

million cubic feet

MMcfpd

=

million cubic feet per day

NGLs

=

natural gas liquids

Q2 2022

=

three months ended June 30, 2022

Q3 2021

=

three months ended September 30, 2021

Q3 2022

=

three months ended September 30, 2022

Non-GAAP and Other Financial Measures

This news release contains references to various non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures as such terms are defined in National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure. Such measures are not recognized measures under GAAP and do not have a standardized meaning prescribed by IFRS and might not be comparable to similar financial measures disclosed by other issuers. While these measures may be common in the oil and gas industry, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. The non-GAAP and other financial measures referred to in this report should not be considered an alternative to, or more meaningful than measures prescribed by IFRS and they are not meant to enhance the Company’s reported financial performance or position. These are complementary measures that are used by management in assessing the Company’s financial performance, efficiency and liquidity and they may be used by investors or other users of this document for the same purpose. Below is a description of the non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures used in this news release. For more information with respect to financial measures which have not been defined by GAAP, including reconciliations to the closest comparable GAAP measure, see the “Non-GAAP Measures and Other Financial Measures” section of the Company’s MD&A which may be accessed through the SEDAR website at www.sedar.com.

Non-GAAP Financial Measures

Operating netback

Operating netback is calculated as natural gas, oil and condensate revenues less royalties and production expenses. This calculation is provided in the “Operating Netback” section of the Company’s MD&A using our IFRS measures. The Company’s MD&A may be accessed through the SEDAR website at www.sedar.com. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations.

Non-GAAP Financial Ratios

Operating netback per boe

Operating netback is calculated on a per unit basis, which is per barrel of oil equivalent (“boe”). It is a common non-GAAP measure used in the oil and gas industry and management believes this measurement assists in evaluating the operating performance of the Company. It is a measure of the economic quality of the Company’s producing assets and is useful for evaluating variable costs as it provides a reliable measure regardless of fluctuations in production. Alvopetro calculated operating netback per boe as operating netback divided by total sales volumes (barrels of oil equivalent). This calculation is provided in the “Operating Netback” section of the Company’s MD&A using our IFRS measures. The Company’s MD&A may be accessed through the SEDAR website at www.sedar.com. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations on a per unit basis (boe).

Operating netback margin

Operating netback margin is calculated as operating netback per boe divided by the realized sales price per boe. Operating netback margin is a measure of the profitability per boe relative to natural gas, oil and condensate sales revenues per boe and is calculated as follows:

Funds Flow from Operations Per Share

Funds flow from operations per share is a non-GAAP ratio that includes all cash generated from operating activities and is calculated before changes in non-cash working capital, divided by the weighted the weighted average shares outstanding for the respective period. For the periods reported in this news release the cash flows from operating activities per share and funds flow from operations per share is as follows:

Capital Management Measures

Funds Flow from Operations

Funds flow from operations is a non-GAAP capital management measure that includes all cash generated from operating activities and is calculated before changes in non-cash working capital. The most comparable GAAP measure to funds flow from operations is cash flows from operating activities. Management considers funds flow from operations important as it helps evaluate financial performance and demonstrates the Company’s ability to generate sufficient cash to fund future growth opportunities. Funds flow from operations should not be considered an alternative to, or more meaningful than, cash flows from operating activities however management finds that the impact of working capital items on the cash flows reduces the comparability of the metric from period to period. A reconciliation of funds flow from operations to cash flows from operating activities is as follows:

Net Working Capital

Net working capital is computed as current assets less current liabilities. Net working capital is a measure of liquidity, is used to evaluate financial resources, and is calculated as follows:

Working Capital Net of Debt

Working capital net of debt is computed as net working capital surplus decreased by the carrying amount of the Credit Facility. Working capital net of debt is used by management to assess the Company’s overall financial position.

Supplementary Financial Measures

“Average realized natural gas price – $/Mcf” is comprised of natural gas sales as determined in accordance with IFRS, divided by the Company’s natural gas sales volumes.

“Average realized NGL – condensate price – $/bbl” is comprised of condensate sales as determined in accordance with IFRS, divided by the Company’s NGL sales volumes from condensate.

“Average realized oil price – $/bbl” is comprised of oil sales as determined in accordance with IFRS, divided by the Company’s oil sales volumes.

“Average realized price – $/boe” is comprised of natural gas, condensate and oil sales as determined in accordance with IFRS, divided by the Company’s total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

“Royalties per boe” is comprised of royalties, as determined in accordance with IFRS, divided by the total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

“Production expenses per boe” is comprised of production expenses, as determined in accordance with IFRS, divided by the total natural gas, condensate and oil sales volumes (barrels of oil equivalent).

BOE Disclosure

The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6 Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this MD&A are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Forward-Looking Statements and Cautionary Language

This news release contains forward-looking information within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward‐looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning the Company’s dividend policy, plans for dividends in the future, and the timing and taxation of such dividends, the Company’s intention to proceed with an NCIB, plans relating to the Company’s operational activities, the expected natural gas price, gas sales and gas deliveries under Alvopetro’s long-term gas sales agreement, exploration and development prospects of Alvopetro, the expected timing of certain of Alvopetro’s testing and operational activities, future results from operations, and the Company’s plans for dividends in the future. Forward-looking statements are necessarily based upon assumptions and judgments with respect to the future including, but not limited to, expected approvals and timing thereof with respect to an NCIB, equipment availability, the timing and results of testing the 183-B1 well, the 182-C2 well and the Unit C well, the success of future drilling, completion, recompletion and development activities, foreign exchange rates, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, the outlook for commodity markets and ability to access capital markets, the impact of the COVID-19 pandemic, the performance of producing wells and reservoirs, well development and operating performance, the timing of regulatory licenses and approvals, general economic and business conditions, forecasted demand for oil and natural gas, weather and access to drilling locations, the availability and cost of labour and services, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. In addition, the declaration, timing, amount and payment of future dividends remain at the discretion of the Board of Directors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our restated annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

SOURCE Alvopetro Energy Ltd.

For further information: Corey C. Ruttan, President, Chief Executive Officer and Director, or Alison Howard, Chief Financial Officer, Phone: 587.794.4224, Email: info@alvopetro.com, www.alvopetro.com, TSX-V: ALV, OTCQX: ALVOF

Energy Fuels is a leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. Energy Fuels also produces vanadium from certain of its projects, as market conditions warrant, and is ramping up commercial-scale production of REE carbonate. Its corporate offices are in Lakewood, Colorado, near Denver, and all its assets and employees are in the United States. Energy Fuels holds three of America’s key uranium production centers: the White Mesa Mill in Utah, the Nichols Ranch in-situ recovery (“ISR”) Project in Wyoming, and the Alta Mesa ISR Project in Texas. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, has the ability to produce vanadium when market conditions warrant, as well as REE carbonate from various uranium-bearing ores. The Nichols Ranch ISR Project is on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Alta Mesa ISR Project is also on standby and has a licensed capacity of 1.5 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels also has one of the largest NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Energy Fuel reached a definitive agreement to sell the Alta Mesa mill to enCore Energy for $120 million. Energy Fuels will receive $60 million in cash upon closing and $60 million in convertible debt bearing an 8% annual interest rate. The mill is one of 11 licensed uranium processing plants and has an operating capacity of 1.5 million pounds per year. UUUU acquired Alta Mesa in 2016 for $13.6 million.

Energy Fuel, which operates Alta Mesa on a standby basis, did not have plans to activate the plant in the near future. Energy Fuel retains three other processing mills including the White Mesa mill which is licensed to produce 8 million pounds of uranium per year. We believe the White Mesa mill is large enough to meet all of UUUU’s uranium production needs in addition to producing vanadium and rare earth elements.The Alta Mesa plant costs approximately $2 million annually to maintain.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Non-dilutive sale of asset expected to materially enhance Energy Fuels’ balance sheet and help to fund the rapid advancement and expansion of near-term U.S. uranium and rare earth production

LAKEWOOD, Colo., Nov. 14, 2022 /CNW/ – Energy Fuels Inc. (NYSE American: UUUU) (TSX: EFR) (“Energy Fuels” or the “Company”), a leading U.S. producer of uranium and rare earth elements (“REE“), is pleased to announce that it has entered into a definitive agreement to sell three wholly-owned subsidiaries that together hold Energy Fuels’ Alta Mesa ISR Project (“Alta Mesa“) to enCore Energy (“enCore“) for total consideration of $120 million (the “Transaction“). The Transaction is expected to close by the end of 2022 or early 2023.

The Transaction is significant for the Company, as the cash received is expected to fully finance much of the Company’s uranium, REE, vanadium and medical isotope business plans for the next two to three years without diluting shareholders. These plans may include:

Ramping-up uranium production at one or more of the White Mesa Mill, the Nichols Ranch ISR Project, the Pinyon Plain mine, the La Sal Complex, and/or the Whirlwind mine which total up to two (2) million pounds of U3O8 per year of near-term, lower cost U.S. production capacity in order to fulfill commitments under existing and future long-term uranium supply agreements and as market conditions may warrant;

Accelerating the licensing and development of the Company’s larger-scale uranium mines, including the Sheep Mountain, Roca Honda, and/or Bullfrog projects, which together will add over five (5) million pounds of production capacity in the next several years;

Establishing an “ore purchasing” program to secure additional feed to the White Mesa Mill, from others in the region as uranium mining picks up in the region, thereby maximizing the facility’s existing eight (8) million pounds per year licensed uranium production capacity and having sole ownership of this production;

Financing the construction of “first to market” in the U.S. “Phase 1” REE separation infrastructure (up to 2,500 – 5,000 MT per year TREO capacity, including 500 – 1,000 MT per year of NdPr oxide or oxalate expected) at the White Mesa Mill;

Advancing the design, engineering and permitting of a planned, large “world significant” “Phase 2” crack-and-leach and “light” and “heavy” REE separation facility (up to 15,000 mT per year TREO capacity).

Developing the Company’s Bahia heavy mineral sand and REE project in Brazil upon successful acquisition of the project; and

Acquiring additional monazite supply to feed the Company’s rapidly growing REE business.

The $120 million of total consideration will be paid by enCore to Energy Fuels as follows:

$60 million cash at closing; and

$60 million in a secured convertible note (the “Note”), payable in two years from the closing, bearing annual interest of eight percent (8%). The Note will be convertible at Energy Fuels’ election into enCore shares at a 20% premium to the 10-day volume-weighted average price of enCore shares ending the day before the closing. enCore is currently traded on the TSXV and has applied for a listing on the NASDAQ. The Note will be guaranteed by enCore Energy Corp., will be fully secured by Alta Mesa, and enCore will not be permitted to further encumber Alta Mesa with any third-party indebtedness, royalty or stream while the Note is outstanding. Unless a block trade or similar distribution is executed by Energy Fuels to sell the enCore common shares underlying the Note, Energy Fuels will be limited to converting the Note into a maximum of $10 million principal amount of the Note per thirty (30) day period.

Furthermore, enCore will assume all reclamation liabilities associated with Alta Mesa (approximately $10.3 million) and pay Energy Fuels the cash collateral on the existing reclamation bonds (approximately $3.6 million). Once the reclamation liabilities are transferred to enCore, Energy Fuels will be nearly 60% collateralized on its remaining reclamation obligations. The Company also estimates that the sale of Alta Mesa will reduce Energy Fuels’ cash burn by approximately $2 million per year.

Energy Fuels acquired Alta Mesa in 2016 for approximately $13.6 million of shares, and currently carries this project on its balance sheet at $8.2 million. The Transaction represents an exceptional return on investment for Energy Fuels, and the value metrics of the Transaction compare favorably against precedent transactions within the uranium sector. Energy Fuels expects to replace the expected uranium production from Alta Mesa through permitting and production from its existing larger mining projects, ore purchases, toll milling arrangements, additional alternate feed and clean-up material, and potentially other transactions as market conditions may warrant.

Mark S. Chalmers, President and CEO of Energy Fuels stated: “This is a unique transaction for Energy Fuels. Not only does it allow us to monetize the Alta Mesa Project for $120 million, it allows our company to focus and accelerate our higher priority uranium and rare earth projects without dilution to our shareholders. This non-dilutive transaction will add cash to Energy Fuels’ significant working capital position, which was $122 million at September 30, 2022. Energy Fuels will also retain some exposure to short-term market upside and optionality at Alta Mesa and enCore through the convertible note.

“With recent uranium market strength and having secured new long-term uranium contracts with major U.S. nuclear utilities earlier this year, the Company is beginning to perform the work needed to recommence production at one or more of our projects, with production expected to start as soon as 2023. We have already hired about 20 people, and the cash we receive from the Alta Mesa transaction will help further fund this ramp-up. On top of this, the Company plans to establish an “ore purchasing” program from future uranium mining from others that maximizes the underutilized uranium production capacity of the White Mesa Mill with the uranium produced going 100% to our account in a way that others cannot. Energy Fuels absolutely intends to retain our position as the leading producer of uranium in the U.S. through our remaining outstanding portfolio of ISR and conventional uranium assets, and this transaction with enCore helps to both finance and focus our plans in this regard without dilution associated with equity financings.

“This cash also helps facilitate our plans to install rare earth separation infrastructure at our White Mesa Mill, including the expected capacity to produce approximately 500 – 1,000 tonnes per annum of separated ‘light’ rare earth oxides (or oxalates) by the end of 2023 or early 2024. We are also working on a number of fronts to secure additional monazite supply to feed our new rare earth infrastructure, and we expect this cash to significantly help finance purchases of monazite, fund our Bahia project in Brazil upon successful completion of that acquisition, and otherwise help in this regard. If we are successful with our rare earth initiatives, we have the potential to be the ‘first-to-market’ in the U.S. for the sale of commercial quantities of separated NdPr oxides (or oxalates), a raw material for rare earth permanent magnets used in electric vehicle drivetrains, wind energy systems, and defense applications. For reference, high-efficiency EVs each require about one to two kilograms of NdPr oxide. Therefore, in the next 12-18 months, if we are successful in constructing our Phase 1 rare earth separation capabilities, Energy Fuels could be domestically producing enough magnet material for 250,000 to 1 million EV drivetrains per year.

“I also believe this Transaction represents an important step forward for enCore Energy. Alta Mesa is a fully permitted and developed U.S. uranium project, and enCore’s President and CEO, Paul Goranson, knows it well, having constructed and operated it himself about ten years ago. To us, this appears to be a value creative transaction for both Energy Fuels and enCore.”

The closing of the Transaction is expected to occur by December 31, 2022. If the Transaction is not completed due to certain circumstances, enCore is required to pay to Energy Fuels a $6 million break fee.

Cantor Fitzgerald Canada Corporation is acting as Energy Fuels’ financial advisor and Dorsey & Whitney LLP and Dentons are acting as Energy Fuels’ legal advisors in connection with the Transaction.

About Energy Fuels: Energy Fuels is a leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. The Company also produces vanadium from certain of its projects, as market conditions warrant, and is ramping up to full commercial-scale production of RE Carbonate. Its corporate offices are in Lakewood, Colorado near Denver, and all its assets and employees are in the United States. Energy Fuels holds three of America’s key uranium production centers: the White Mesa Mill in Utah, the Nichols Ranch ISR Project in Wyoming, and the Alta Mesa ISR Project in Texas. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, and has the ability to produce vanadium when market conditions warrant, as well as RE Carbonate from various uranium-bearing ores. The Nichols Ranch ISR Project is currently on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Alta Mesa ISR Project is also currently on standby and has a licensed capacity of 1.5 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels also has one of the largest S-K 1300 and NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Cautionary Note Regarding Forward-Looking Statements: This news release contains certain “Forward Looking Information” and “Forward Looking Statements” within the meaning of applicable United States and Canadian securities legislation, which may include, but are not limited to, statements with respect to: production and sales forecasts; the ability of the Company to accelerate uranium and rare earth production; scalability, and the Company’s ability and readiness to re-start, expand or deploy any of its existing projects or capacity to respond to any improvements in uranium market conditions;; any expectation as to the timing of the closing of the Transaction or whether the closing will in fact occur; any expectation that the Transaction may fully finance much of the Company’s uranium, rare earth, vanadium, and medical isotope business plans for the next two to three years; any expectation that the Company may license and eventually produce uranium from its Sheep Mountain, Roca Honda and/or Bullfrog projects; any expectation as to recommencement of production at any of the Company’s uranium mines or the timing thereof; any expectation as to the ability of the Company to secure any new sources of ore or other processing opportunities at the Mill through an ore purchasing program; any expectation as to timelines for the permitting and development of projects; any expectation that the Company will maintain its position as a leading uranium company in the United States; any expectation with respect to timelines to production; any expectation that the Mill will be successful in producing RE Carbonate and/or separated REE oxides or oxalates on a full-scale commercial basis; any expectation that Energy Fuels will be successful in developing U.S. separation, or other value-added U.S. REE production capabilities at the Mill, or otherwise, including the timing of any such initiatives and the expected production capacity or capital and operating costs associated with any such production capabilities; any expectation with respect to the quantities of monazite sands to be acquired by Energy Fuels, the quantities of RE Carbonate to be produced by the Mill or the quantities of contained TREO in the Mill’s RE Carbonate; any expectation that the Company may sell its separated NdPr oxide (or oxalate) to major electric vehicle manufacturers in the U.S. and Europe; any expectation that the Bahia Project has the potential to feed the Mill with REE and uranium-bearing monazite sand for decades; any expectation as to the quantities to be delivered under existing uranium sales contracts, or that such contracts may help underpin the Company’s uranium business for many years to come; and any expectation that the Company will generate net income in future periods. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans,” “expects,” “does not expect,” “is expected,” “is likely,” “budgets,” “scheduled,” “estimates,” “forecasts,” “intends,” “anticipates,” “does not anticipate,” or “believes,” or variations of such words and phrases, or state that certain actions, events or results “may,” “could,” “would,” “might” or “will be taken,” “occur,” “be achieved” or “have the potential to.” All statements, other than statements of historical fact, herein are considered to be forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements express or implied by the forward-looking statements. Factors that could cause actual results to differ materially from those anticipated in these forward-looking statements include risks associated with: commodity prices and price fluctuations; processing and mining difficulties, upsets and delays; permitting and licensing requirements and delays; changes to regulatory requirements; legal challenges; the availability of sources of Alternate Feed Materials and other feed sources for the Mill; competition from other producers; public opinion; government and political actions; available supplies of monazite sands; the ability of the Mill to produce RE Carbonate to meet commercial specifications on a commercial scale at acceptable costs; the ability of Neo to separate the RE Carbonate produced by the Mill to meet commercial specifications on a commercial scale at acceptable costs; market factors, including future demand for REEs; the ability of the Mill to be able to separate radium or other radioisotopes at reasonable costs or at all; market prices and demand for medical isotopes; and the other factors described under the caption “Risk Factors” in the Company’s most recently filed Annual Report on Form 10-K, which is available for review on EDGAR at www.sec.gov/edgar.shtml, on SEDAR at www.sedar.com, and on the Company’s website at www.energyfuels.com. Forward-looking statements contained herein are made as of the date of this news release, and the Company disclaims, other than as required by law, any obligation to update any forward-looking statements whether as a result of new information, results, future events, circumstances, or if management’s estimates or opinions should change, or otherwise. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, the reader is cautioned not to place undue reliance on forward-looking statements. The Company assumes no obligation to update the information in this communication, except as otherwise required by law.

SOURCE Energy Fuels Inc.

For further information: Investor Inquiries: Energy Fuels Inc., Curtis Moore, VP – Marketing and Corporate Development, (303) 974-2140 or Toll free: (888) 864-2125, investorinfo@energyfuels.com, www.energyfuels.com

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Permex announced it has received approval to uplist to the NYSE. Shares are expected to begin trading on November 15 under the symbol OILS (warrants will trade under OILSW). The uplisting follows a October 31st announcement that Permex would consolidate outstanding shares on the basis of a one for every sixty pre-consolidation shares. We indicated at the time that we believed management was doing a reverse stock split as a prerequisite to uplisting on the NYSE. We believe listing on the NYSE will greatly enhance the company’s ability to attract investor attention and unlock Permex’s hidden value.

Permex has filed an offering registration. On November 4th, Permex file a S-1 Registration Statement with the SEC to offer 2 million common shares (post reverse stock split currently trading under the symbol OIL on the Toronto exchange and on the OTC under the symbol OILCD.) On November 9th, the company filed an addendum increasing the share offering to 3.6 million shares which now include a warrant to purchase shares at a 125% premium to the offering price. The offering is being done in conjunction with the uplisting implying it will be completed by November 15th.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

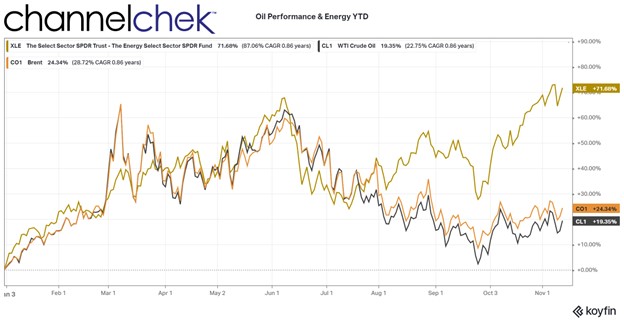

Factors Still Point to Higher Oil Prices and Sizeable Bets on Crude

There are many factors impacting why traditional energy prices and producers may have a hurricane-force tailwind heading into the holidays and next year.

A boost in demand for oil is expected as China just announced that it is lowering its quarantine requirements for visitors from outside the country. But Chinese Covid policies aren’t the only impetus pushing up oil demand – around the globe, there are supply challenges that are playing out. Oil hasn’t risen above $100 a barrel since early Summer, some traders are speculating it will rise above $200 in the coming months. Here’s why.

China

In addition to the announcement that the CPR was cutting the required quarantine period for the country (to five days from seven, with three days of home isolation), the required PCR test hurdle is being lowered as well. And airlines no longer run the risk of being suspended if the travelers they bring in that test positive is five or more.

Europe

The European Union has agreed to stop all oil imports from Russia on Dec. 5. The plan is to cap the prices at which EU nations would buy oil from Russia, that price is expected to be near $60 per barrel. Russia has reacted by increasing exports to Asia, but the price cap is expected to reduce its exports and lower total supply by up to one million barrels per day.

United States

Back in May, the U.S. took the drastic step of increasing available supply by selling oil from the U.S. Strategic Petroleum Reserve at a rate of nearly one million barrels per day starting in May. The increased supply has kept oil prices down. But the sales are unsustainable and expected to be reduced. Congress has allowed another sale of 26 million barrels that are expected to carry through to October 2023. This is a much slower pace of oil releases from the reserves. Plus, the reserves will need to be replenished.

After the Congressionally approved release, the reserve will be down to 348 million barrels, this is half the quantity compared to January of this year —the lowest since 1983. Congress has said that the reserve must stay above 252.4 million barrels, and the incoming Congress is expected to be more conservative when it comes to using these strategic assets to control prices.

Production growth overall in the U.S. has stalled after having increased through most of the year. Government data show that U.S. production dropped to 11.9 million barrels per day last week, this is tied for the lowest level in several months. Supplies of products such as diesel and heating oil in the U.S. are at multiyear lows. So there is not abundant supply should a weather-related or some other fuel-demanding crisis surface.

Oil is now trading between $92 and $93 a barrel. It had reached a high above $130 in March, shortly after the war began, and hasn’t seen the $100 a barrel level since late June.

Trading this week showed significant flows into an options contract that speculates that $200 per barrel may be in store. The most actively traded Brent crude options contract on Thursday was an option to buy Brent at $200 in March 2023. This was the most active oil contract of the day.

How significant is this bullish activity surrounding oil prices? The ratio of bullish to bearish bets in the options market is wider than at any time in recorded history, according to Bloomberg. Oil options traders are positioned more aggressively than ever before.

Take Away

Oil demand could rise soon in China as travel restrictions are lessened. Elsewhere in the world, oil demand is expected to increase as supplies remain the same or decrease. Demand remained elevated globally despite slower economies.

With supply likely to drop and demand ramping up, $200 by the third week in March is one price expectation for a record number of trades transacted at recently. More than doubling in a few months sounds unthinkable, but the massive trades were transacted by experienced institutional traders.

DALLAS, Nov. 10, 2022 (GLOBE NEWSWIRE) — Permex Petroleum Corporation (CSE: OIL) (OTCQB: OILCD) (FSE: 75P) (“Permex” or the “Company”), an independent energy company engaged in the acquisition, exploration, development and production of oil and natural gas properties on private, state and federal land in the United States, today announced that it has received approval to uplist its common shares and list its warrants on the NYSE American in connection with an underwritten public offering of its common shares (or common share equivalents) and warrants to purchase common shares. Trading of the Company’s common shares and warrants is expected to commence on the NYSE at the opening of trading on November 15, 2022 under the ticker symbols “OILS” and “OILSW,” respectively. Permex’s listing is subject to meeting all NYSE American requirements at the time of listing. Trading on the OTCQB will cease concurrent with the NYSE American listing.

This press release shall not constitute an offer to sell or the solicitation of an offer to buy these securities, nor shall there be any sale of these securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction.

About Permex Petroleum Corporation

Permex Petroleum is a uniquely positioned junior oil and gas company with assets and operations across the Permian Basin of West Texas and the Delaware Sub-Basin of New Mexico. The Company focuses on combining its low-cost development of Held by Production assets for sustainable growth with its current and future Blue-Sky projects for scale growth. The Company, through its wholly-owned subsidiary, Permex Petroleum US Corporation, is a licensed operator in both states, and owns and operates on private, state and federal land. For more information, please visit www.permexpetroleum.com.

FORWARD-LOOKING STATEMENTS

Statements in this press release may constitute forward-looking statements for the purposes of the safe harbor provisions under the Private Securities Litigation Reform Act of 1995 and other federal securities laws. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of management, are not guarantees of performance and are subject to significant risks and uncertainty. These forward- looking statements should, therefore, be considered in light of various important factors, including those set forth in Company’s reports that it files from time to time with the U.S. Securities and Exchange Commission and the Canadian securities regulators which you should review. When used in this press release, words such as “will,” “could,” “plan,” “estimate”, “expect”, “intend”, “may”, “potential”, “believe”, “should” and similar expressions, are forward-looking statements. Forward-looking statements may include, without limitation, statements relating to the Company’s listing on NYSE American, financial condition and operating results, legal, economic, business, competitive and/or regulatory factors affecting Permex’s businesses and any other statements regarding events or developments Permex believes or anticipates will or may occur in the future. These forward-looking statements should not be relied upon as predictions of future events, and the Company cannot assure you that the events or circumstances discussed or reflected in these statements will be achieved or will occur. If such forward-looking statements prove to be inaccurate, the inaccuracy may be material. You should not regard these statements as a representation or warranty by the Company or any other person that it will achieve its objectives and plans in any specified timeframe, or at all. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release. The Company disclaims any obligation to publicly update or release any revisions to these forward- looking statements, whether as a result of new information, future events or otherwise, after the date of this news release or to reflect the occurrence of unanticipated events, except as required by law.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third-quarter results were below expectations due to lower-than-expected energy pricing. Production levels were in line with expectations and management guidance given on September 29. Realized oil and gas prices were well below U.S. reported oil and gas prices when adjusted to Canadian prices, reflecting a widening basis discount for western Canada production. We will incorporate a widening basis differential going forward.

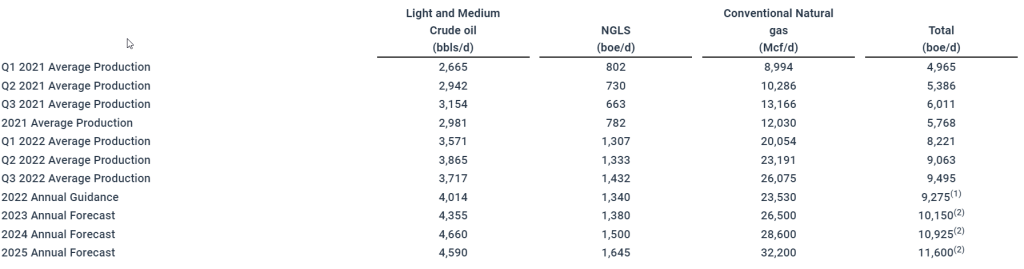

InPlay is able to offset a weakening pricing environment with ever-improving production results. Management provided production guidance for 2023-25 for the first time. Guidance was well above production levels assumed in our models and reflects an acceleration of capital investments going forward. We believe increased investment is prudent at current payback rates of less than one year. We also believe management’s commitment to higher spending levels is a positive sign that it believes it has ample areas to drill at attractive returns.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

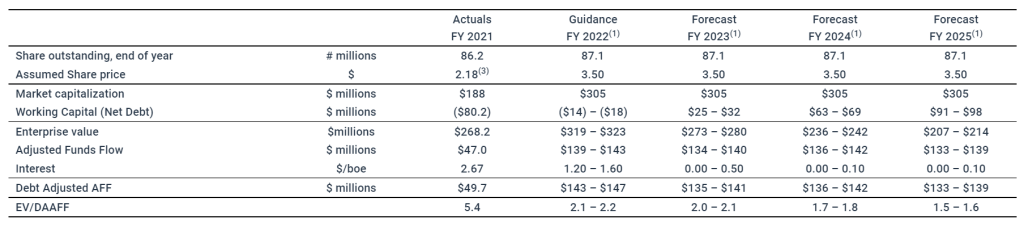

CALGARY, Alberta, Nov. 09, 2022 (GLOBE NEWSWIRE) — InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) announces its record setting financial and operating results for the three and nine months ended September 30, 2022 and the implementation of an inaugural base dividend. The implementation of the inaugural base dividend is a significant milestone in the Company’s strategy of providing additional strong returns to shareholders through the return of capital along with the generation of free adjusted funds flow (“FAFF”)(4) and top-tier light oil weighted production per share growth which has been made possible by the Company’s strong financial and operational position.

InPlay’s condensed unaudited interim financial statements and notes, as well as Management’s Discussion and Analysis (“MD&A”) for the three and nine months ended September 30, 2022 will be available at “www.sedar.com” and our website at “www.inplayoil.com”. An updated presentation will be posted to our website in due course.

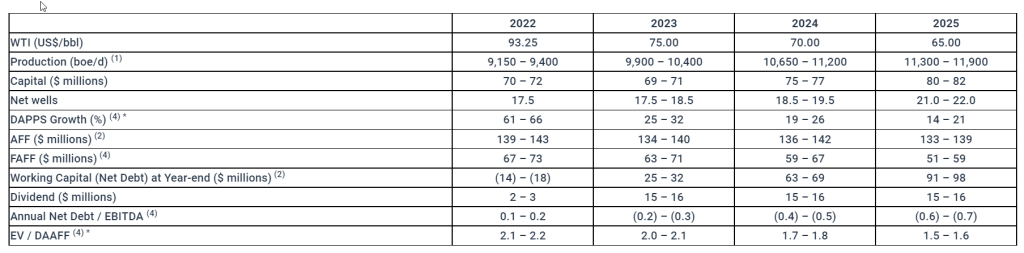

Inaugural Base Dividend

InPlay is pleased to announce that its Board of Directors has approved the implementation of a base cash dividend of $0.015/share per month. The initial dividend is payable on November 30, 2022 to holders of the Company’s common shares of record at the close of business on November 18, 2022. The Company continues to make strong progress with respect to its debt reduction targets with a trailing 12 month net debt(2) to earnings before interest, taxes and depletion (“EBITDA”) ratio(4) of less than 0.4x at the end of the third quarter, which is forecast to be approximately 0.1x to 0.2x at year end (inclusive of the monthly base dividend). Any dividend payment after the initial one will be subject to the approval of InPlay’s Board of Directors at the time of declaration.

In determining the initial base dividend rate, InPlay’s Board of Directors took into account the Company’s strong balance sheet and the sustainability of the dividend in the event of a significant drop in commodity prices. In accordance with the recently released long term forecast, the Company projects that the base dividend is sustainable in a flat US$55/bbl WTI price environment in 2023 through 2025 with net debt to EBITDA levels remaining below 0.3x. Using forward strip pricing, as disclosed in our long term forecast announced on Sept 28, 2022 (which is approximately USD $5 – $7 per barrel lower than current WTI forward strip pricing), the Company is forecasting strong FAFF resulting in a build in our positive working capital balance (inclusive of capital expenditures and the monthly base dividend) to $91 – $98 million through the end of 2025 as outlined in greater detail in the “Outlook” section below. Over time, the Company anticipates that excess FAFF will be used for special dividends, share buybacks, tactical capital investment and strategic acquisitions.

The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

Third Quarter 2022 Financial & Operating Highlights

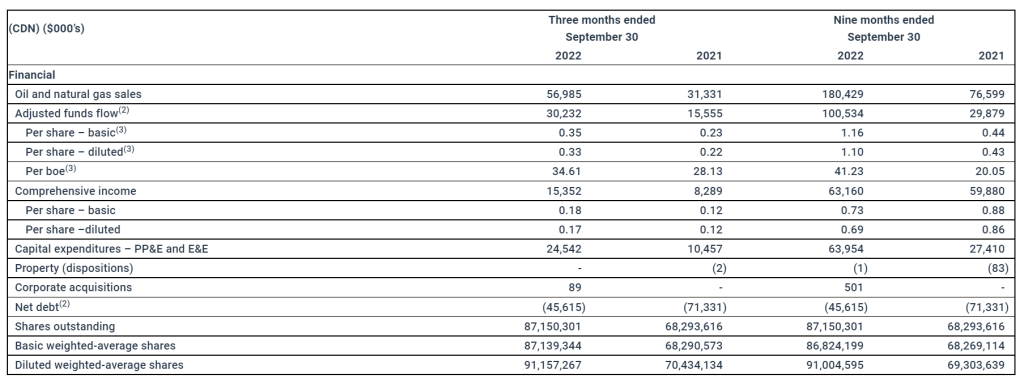

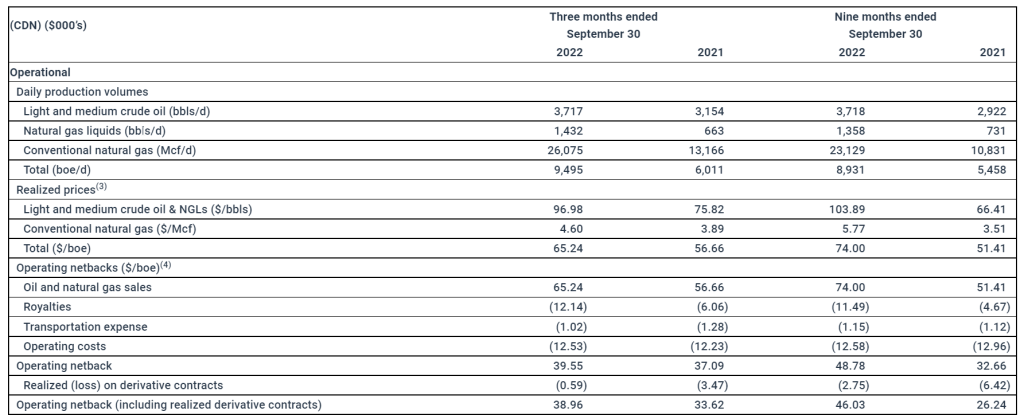

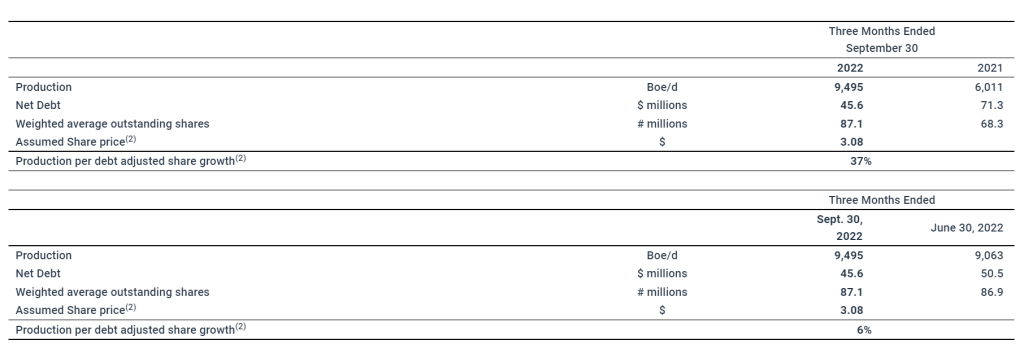

Achieved record average quarterly production of 9,495 boe/d(1) (54% light crude oil and NGLs), an increase of 58% from third quarter production in 2021 of 6,011 boe/d(1) (64% light crude oil and NGLs) and an increase of 5% compared to our previous record of 9,063 boe/d(1) (57% light crude oil and NGLs) in the second quarter of 2022. Average production per weighted average basic share increased 24% compared to the third quarter of 2021 (37% on a debt adjusted(4) basis) and 4% compared to the second quarter of 2022 (6% on a debt adjusted basis).

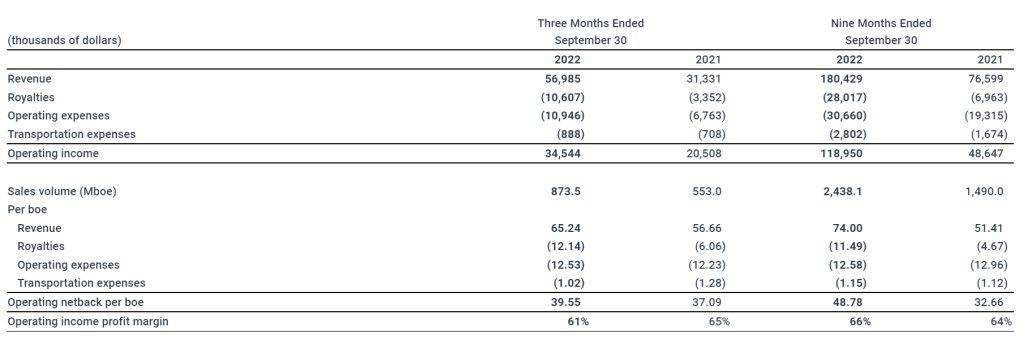

Generated quarterly adjusted funds flow (“AFF”)(2) of $30.2 million ($0.35 per weighted average basic share(3)), an increase of 94% compared to $15.6 million ($0.23 per weighted average basic share) in the third quarter of 2021. On a year-to-date basis, generated AFF of $100.5 million ($1.16 per weighted average basic share(3)), an increase of 236% compared to $29.9 million ($0.44 per weighted average basic share) in 2021.

Increased operating netbacks(4) on a year to date basis by 49% to $48.78/boe from $32.66/boe in 2021.

Realized quarterly operating income(4) of $34.5 million, an increase of 68% compared to $20.5 million in the third quarter of 2021. On a year-to-date basis, realized quarterly operating income $119.0 million, an increase of 145% compared to $48.6 million in 2021.

Maintained operating expenses at $12.53/boe compared to $12.23/boe in the third quarter of 2021 and $12.28/boe in the second quarter of 2022, despite rising costs of industry services as well as fuel and energy costs.

Generated FAFF of $5.7 million resulting in a 10% reduction to net debt from June 30, 2022 with the majority of 2022 annual capital expenditures already incurred. Strong FAFF and resulting debt reductions are expected to accumulate throughout the fourth quarter (inclusive of the monthly base dividend).

Achieved a trailing twelve month net debt to EBITDA ratio of less than 0.4x to September 30, 2022 with a ratio of between 0.1x to 0.2x forecasted by year end (inclusive of the monthly base dividend).

Realized net income of $15.4 million ($0.18 per basic share; $0.17 per diluted share). On a year-to-date basis, realized net income of $63.2 million ($0.73 per basic share; $0.69 per diluted share).

Financial and Operating Results

Third Quarter 2022 Financial & Operations Overview

Production averaged 9,495 boe/d(1) (54% light crude oil & NGLs) of sales in the third quarter of 2022, the sixth consecutive quarter that the Company has increased its quarterly production record. Quarterly production increased by 58% compared to 6,011 boe/d(1) (64% light crude oil & NGLs) in the third quarter of 2021 and 5% compared to 9,063 boe/d(1) (57% light crude oil & NGLs) in the second quarter of 2022, our previous quarterly record. This resulted in $30.2 million of AFF generated during the third quarter of 2022 and $5.7 million of FAFF which has reduced net debt levels by 10% to $45.6 million at September 30, 2022. On a year-to-date basis, the Company has generated AFF of $100.5 million and FAFF of $36.6 million resulting in a 43% reduction to net debt from December 31, 2021. Liquidity ratios to the end of the quarter continued to improve resulting in a trailing twelve month net debt to EBITDA ratio of less than 0.4x to September 30, 2022.

InPlay’s capital program for the third quarter of 2022 consisted of $24.5 million of capital expenditures. During the quarter, the Company completed and brought on production two (1.9 net) Extended Reach Horizontal (“ERH”) wells in Willesden Green that were drilled in the second quarter. Also in Willesden Green, the Company drilled, completed and brought on production three (2.9 net) ERH wells. Drilling operations were completed on an additional two (1.9 net) ERH wells in Willesden Green during the third quarter and these wells were brought on production in October. The Company also allocated capital to the construction of two Vapor Recovery Units which will increase gas conservation and reduce greenhouse gas emissions.

Efficient field operations and increased production levels allowed the Company to limit operating cost increases, achieving operating costs of $12.53/boe compared to $12.23/boe in the third quarter of 2021 and $12.28/boe in the second quarter of 2022. The Company continues to focus on operational efficiency and is proactive in reducing the impact of the inflationary pressures and supply chain disruptions that are impacting the oil and gas industry. This resulted in strong operating income and operating netbacks during the quarter of $34.5 million and $39.55/boe respectively.

Outlook

InPlay began its fourth quarter capital program drilling one (0.95 net) ERH well in Willesden Green which was brought on production in late October and is flowing without artificial lift and the start of drilling operations with our first two (2.0 net) Belly River wells. InPlay utilized the technologies and expertise developed in our Cardium play over the years to complete these Belly River drills in 5.4 and 5.6 days respectively. This was a dramatic improvement compared to our most recent two one-mile drilling operations in the area in 2016 averaging approximately 10 days per well and approximately 2.5 days quicker than recent one-mile wells drilled in the area by other operators.

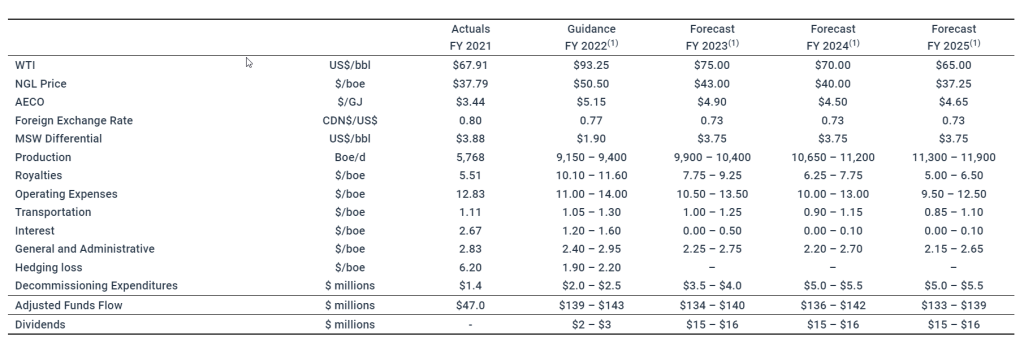

Given the continued strong operational results and positive future commodity prices, the Company reiterates its 2022 guidance and long-term forecast as released September 27, 2022 with the incorporation of the base dividend. The Company remains committed to providing top-tier production per share growth and a return of capital to shareholders. This base dividend and the recently implemented share buyback program in addition to our forecasted measured production per share growth places InPlay in a solid position to continue realizing on meaningful returns to shareholders over the long term.

The table below reiterates the highlights of our 2022 guidance and long-term forecast at our current share price, including the impact of our inaugural base dividend:

* Assumes a $3.50 share price

The amounts above do not include potential future purchases through the Company’s normal course issuer bid (“NCIB”).

As outlined above in the long term forecast, the Company is forecasting to generate material FAFF resulting in a growing positive working capital balance through to 2025. Our strategy for the accumulating additional FAFF is to provide additional means for returns to shareholders through dividends, share buybacks, increased tactical capital investment and accretive strategic acquisitions.

InPlay is pleased to achieve this significant milestone of implementing our inaugural base dividend and would like to thank our employees, board members, lenders and shareholders for their support. The Company looks forward to releasing our 2023 budget outlining our capital program for the year in early January.

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

See “Production Breakdown by Product Type” at the end of this press release.

Capital management measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

Supplementary financial measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

Non-GAAP financial measure or ratio that does not have a standardized meaning under International Financial Reporting Standards (IFRS) and GAAP and therefore may not be comparable with the calculations of similar measures for other companies. Please refer to “Non-GAAP and Other Financial Measures” contained within this press release.

Reader Advisories

Non-GAAP and Other Financial Measures

Throughout this press release and other materials disclosed by the Company, InPlay uses certain measures to analyze financial performance, financial position and cash flow. These non-GAAP and other financial measures do not have any standardized meaning prescribed under GAAP and therefore may not be comparable to similar measures presented by other entities. The non-GAAP and other financial measures should not be considered alternatives to, or more meaningful than, financial measures that are determined in accordance with GAAP as indicators of the Company performance. Management believes that the presentation of these non-GAAP and other financial measures provides useful information to shareholders and investors in understanding and evaluating the Company’s ongoing operating performance, and the measures provide increased transparency and the ability to better analyze InPlay’s business performance against prior periods on a comparable basis.

Non-GAAP Financial Measures and Ratios

Included in this document are references to the terms “free adjusted funds flow”, “operating income”, “operating netback per boe”, “operating income profit margin”, “Net Debt to EBITDA” and “Debt adjusted production per share”. Management believes these measures and ratios are helpful supplementary measures of financial and operating performance and provide users with similar, but potentially not comparable, information that is commonly used by other oil and natural gas companies. These terms do not have any standardized meaning prescribed by GAAP and should not be considered an alternative to, or more meaningful than “profit (loss) before taxes”, “profit (loss) and comprehensive income (loss)”, “adjusted funds flow”, “capital expenditures”, “corporate acquisitions, net of cash acquired”, “net debt”, “weighted average number of common shares (basic)” or assets and liabilities as determined in accordance with GAAP as a measure of the Company’s performance and financial position.

Free Adjusted Funds Flow

Management considers FAFF an important measure to identify the Company’s ability to improve its financial condition through debt repayment and its ability to provide returns to shareholders. FAFF should not be considered as an alternative to or more meaningful than AFF as determined in accordance with GAAP as an indicator of the Company’s performance. FAFF is calculated by the Company as AFF less exploration and development capital expenditures and property dispositions (acquisitions) and is a measure of the cashflow remaining after capital expenditures before corporate acquisitions that can be used for additional capital activity, corporate acquisitions, repayment of debt or decommissioning expenditures or potentially return of capital to shareholders. Refer below for a calculation of historical FAFF and to the “Forward Looking Information and Statements” section for a calculation of forecast FAFF.

Operating Income/Operating Netback per boe/Operating Income Profit Margin

InPlay uses “operating income”, “operating netback per boe” and “operating income profit margin” as key performance indicators. Operating income is calculated by the Company as oil and natural gas sales less royalties, operating expenses and transportation expenses and is a measure of the profitability of operations before administrative, share-based compensation, financing and other non-cash items. Management considers operating income an important measure to evaluate its operational performance as it demonstrates its field level profitability. Operating income should not be considered as an alternative to or more meaningful than net income as determined in accordance with GAAP as an indicator of the Company’s performance. Operating netback per boe is calculated by the Company as operating income divided by average production for the respective period. Management considers operating netback per boe an important measure to evaluate its operational performance as it demonstrates its field level profitability per unit of production. Operating income profit margin is calculated by the Company as operating income as a percentage of oil and natural gas sales. Management considers operating income profit margin an important measure to evaluate its operational performance as it demonstrates how efficiently the Company generates field level profits from its sales revenue. Refer below for a calculation of operating income, operating netback per boe and operating income profit margin.

Net Debt to EBITDA

Management considers Net Debt to EBITDA an important measure as it is a key metric to identify the Company’s ability to fund financing expenses, net debt reductions and other obligations. EBITDA is calculated by the Company as adjusted funds flow before interest expense. When this measure is presented quarterly, EBITDA is annualized by multiplying by four. When this measure is presented on a trailing twelve month basis, EBITDA for the twelve months preceding the net debt date is used in the calculation. This measure is consistent with the EBITDA formula prescribed under the Company’s Senior Credit Facility. Net Debt to EBITDA is calculated as Net Debt divided by EBITDA. Refer below for a calculation of Net Debt to EBITDA and to the “Forward Looking Information and Statements” section for a calculation of forecast Net Debt to EBITDA.

Production per Debt Adjusted Share

InPlay uses “Production per debt adjusted share” as a key performance indicator. Debt adjusted shares should not be considered as an alternative to or more meaningful than common shares as determined in accordance with GAAP as an indicator of the Company’s performance. Debt adjusted shares is a non-GAAP measure used in the calculation of Production per debt adjusted share and is calculated by the Company as common shares outstanding plus the change in net debt divided by the Company’s current trading price on the TSX, converting net debt to equity. Debt adjusted shares should not be considered as an alternative to or more meaningful than weighted average number of common shares (basic) as determined in accordance with GAAP as an indicator of the Company’s performance. Management considers Debt adjusted share is a key performance indicator as it adjusts for the effects of capital structure in relation to the Company’s peers. Production per debt adjusted share is calculated by the Company as production divided by debt adjusted shares. Management considers Production per debt adjusted share is a key performance indicator as it adjusts for the effects of changes in annual production in relation to the Company’s capital structure. Refer below for a calculation of Production per debt adjusted share and to to the “Forward Looking Information and Statements” section for a calculation of forecast Production per debt adjusted share.

EV / DAAFF

InPlay uses “enterprise value to debt adjusted AFF” or “EV/DAAFF” as a key performance indicator. EV/DAAFF is calculated by the Company as enterprise value divided by debt adjusted AFF for the relevant period. Debt adjusted AFF (“DAAFF”) is calculated by the Company as adjusted funds flow plus financing costs. Enterprise value is a capital management measures that is used in the calculation of EV/DAAFF. Enterprise value is calculated as the Company’s market capitalization plus working capital (net debt). Management considers enterprise value a key performance indicator as it identifies the total capital structure of the Company. Management considers EV/DAAFF a key performance indicator as it is a key metric used to evaluate the sustainability of the Company relative to other companies while incorporating the impact of differing capital structures. Refer to the “Forward Looking Information and Statements” section for a calculation of forecast EV/DAAFF.

Capital Management Measures

Adjusted Funds Flow

Management considers adjusted funds flow to be an important measure of InPlay’s ability to generate the funds necessary to finance capital expenditures. AFF is a GAAP measure and is disclosed in the notes to the Company’s consolidated financial statements for the year ending December 31, 2021 and the most recently filed quarterly financial statements. All references to AFF throughout this document are calculated as funds flow adjusting for decommissioning expenditures and transaction and integration costs. This item is adjusted from funds flow as decommissioning expenditures are incurred on a discretionary and irregular basis and are primarily incurred on previous operating assets and transaction costs are non-recurring costs for the purposes of an acquisition, making the exclusion of these items relevant in Management’s view to the reader in the evaluation of InPlay’s operating performance. The Company also presents AFF per share whereby per share amounts are calculated using weighted average shares outstanding consistent with the calculation of profit (loss) per common share.

Net Debt / Working Capital

Net debt / working capital is a GAAP measure and is disclosed in the notes to the Company’s consolidated financial statements for the year ending December 31, 2021 and the most recently filed quarterly financial statements. The Company closely monitors its capital structure with a goal of maintaining a strong balance sheet to fund the future growth of the Company. The Company monitors net debt / working capital as part of its capital structure. The Company uses net debt / working capital (bank debt plus accounts payable and accrued liabilities less accounts receivables and accrued receivables, prepaid expenses and deposits and inventory) as an alternative measure of outstanding debt. Management considers net debt / working capital an important measure to assist in assessing the liquidity of the Company.

Supplementary Measures

“Average realized crude oil price” is comprised of crude oil commodity sales from production, as determined in accordance with IFRS, divided by the Company’s crude oil production. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“Average realized NGL price” is comprised of NGL commodity sales from production, as determined in accordance with IFRS, divided by the Company’s NGL production. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“Average realized natural gas price” is comprised of natural gas commodity sales from production, as determined in accordance with IFRS, divided by the Company’s natural gas production. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“Average realized commodity price” is comprised of commodity sales from production, as determined in accordance with IFRS, divided by the Company’s production. Average prices are before deduction of transportation costs and do not include gains and losses on financial instruments.

“AFF per weighted average basic share” is comprised of AFF divided by the basic weighted average common shares.

“AFF per weighted average diluted share” is comprised of AFF divided by the diluted weighted average common shares.

“AFF per boe” is comprised of AFF divided by total production.

Forward-Looking Information and Statements

This news release contains certain forward–looking information and statements within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”, “may”, “will”, “project”, “should”, “believe”, “plans”, “intends”, “forecast”, “targets”, “framework” and similar expressions are intended to identify forward-looking information or statements. In particular, but without limiting the foregoing, this news release contains forward looking information and statements pertaining to the following: the Company’s business strategy, milestones and objectives including, without limitation, the Company’s forecast net debt to EBITDA ratio at year ended 2022; InPlay’s expectations regarding the sustainability of the base monthly dividend, including in the event of a drop in commodity prices; the projection that the dividend is sustainable in a flat $US 55/bbl WTI price environment; the expectation that the net debt to EBITDA ratio will continue to drop; the anticipated generation of strong FAFF through 2025 and our expected working capital balance; the expectation that additional FAFF will be used for special dividends, share buybacks, tactical capital investment and strategic acquisitions; the expectation of strong debt reductions in the fourth quarter of 2022; the expected results from the construction of the two Vapor Recovery Units; the anticipated timing of the release of the Company’s 2023 budget; expectations regarding future commodity prices; future oil and natural gas prices; future liquidity and financial capacity; future results from operations and operating metrics; future costs, expenses and royalty rates; future interest costs; the exchange rate between the $US and $Cdn; the anticipated tax treatment of the monthly base dividend; future development, exploration, acquisition, development and infrastructure activities and related capital expenditures, including our planned 2022 capital program and associated guidance and long-term forecast to 2025.

Without limitation of the foregoing, readers are cautioned that the Company’s future dividend payments to shareholders of the Company, if any, and the level thereof will be subject to the discretion of the Board of Directors of InPlay. The Company’s dividend policy and funds available for the payment of dividends, if any, from time to time, is dependent upon, among other things, levels of FAFF, leverage ratios, financial requirements for the Company’s operations and execution of its growth strategy, fluctuations in commodity prices and working capital, the timing and amount of capital expenditures, credit facility availability and limitations on distributions existing thereunder, and other factors beyond the Company’s control. Further, the ability of the Company to pay dividends will be subject to applicable laws, including satisfaction of solvency tests under the Business Corporations Act (Alberta), and satisfaction of certain applicable contractual restrictions contained in the agreements governing the Company’s outstanding indebtedness.