This Full Trading Week May Decide the Direction of the Markets for the Rest of 2023

Inflation will be a big focus this week as the CPI, PPI, and import and export prices for June will be released in this order at 8:30 on the last three days of the week. These economic reports are the final inflation readings the Federal Reserve will get before its July 25-26 meeting. The Beige Book also has the ability to alter market sentiment as this is a large part of the data and discussions used at the FOMC meeting. The Beige Book, which is information from each Fed reporting district, is released on Wednesday afternoon.

Monday 7/10

• 10:00 AM ET, The second estimate of Wholesale Inventories is a 0.1 percent draw, unchanged from the first estimate.

• 10:00 AM ET, Mary Daley the President of the San Francisco Fed, will be speaking.

• 3:00 PM ET, Consumer Credit is expected to show that consumers borrowed $20 billion more in May. This compares to a $23 billion increase in April.

Tuesday 7/11

• 6:00 AM ET, The National Federation of Independent Business (NFIB) optimism index has been below, and often far below, the historical average of 98 for the past 17 months. June’s consensus is 89.8 versus 89.4 in May.

Wednesday 7/12

• 8:30 AM ET, The Consumer Price Index, or CPI, is expected to show that core prices in June are slowed to a modest 0.3 percent on the month versus May’s 0.4 percent. Overall prices are also expected to rise 0.3 percent. Annual rates are expected to slow sharply at the headline level, to 3.1 from 4.0 percent, and also for the core, to 5.0 from 5.3 percent.

• 10:00 AM ET, The Atlanta Fed Business Inflation Expectations is not one of the more widely watched inflation reports. But in these times of the markets grasping on anything that may foretell where inflation is headed, this number has the potential to be impactful.

• 10:30 AM ET, The Energy Information Administration (EIA) provides weekly information on petroleum inventories in the US, whether produced here or abroad. The inventory level impacts prices for petroleum products.

• 2:00 PM ET, The Beige Book is a report on economic conditions used at FOMC meetings. This publication is produced roughly two weeks before the monetary policy meetings of the FOMC.

Thursday 7/13

• 8:30 AM ET, Employment numbers seemed to be the new razor-sharp focus among Fed watchers. Initial claims for the prior week are expected to be at the 248,000 level.

• 8:30 AM ET, Producer prices in June are expected to rise 0.2 percent on the month versus a 0.3 percent fall in May. The annual rate in June is seen at plus 0.4 percent versus May’s plus 1.1 percent. June’s ex-food ex-energy rate is seen at 0.2 percent on the month and 2.8 percent on the year which would exactly match May’s results.

• 4:00 PM ET, Fed’s Balance Sheet data is expected to show that the Fed holds $8.98 trillion in US debt. The total assets are forecast to drop by $42,602 billion.

Friday 7/14

• 10:00 AM ET, the Consumer SentIment first indication for July, is expected to rise to 65.0 from June’s surprisingly high 64.4.

What Else

Last week the BLS reported the US economy added 209,000 jobs in June. This helped cause the unemployment rate to fall to 3.6%, near its 50-year low. This spurred inflation worries and spooked the bond market, which in turn impacted the broader stock market. Looking at the make-up of the numbers may be less worrisome. It seems the US government has been the last to begin hiring after the pandemic. Excluding government hiring, private sector payrolls grew by only 149,000 in June. This is the slowest since December 2019 and below the 166,000 monthly average in 2017-19.

So the reaction may have been more of a reason for the market to take a breather after a strong June, than increased concern over a hot job market.

Maximum employment is one of the top mandates of the Federal Reserve, so why is it trying to reduce the number of jobs available? On the surface this would seem backwards. But in economics, everything is related, intentionally slowing growth to the point where resources aren’t stressed, can provide a better balance across the Feds other mandates. These Congressional mandates are stable prices, and moderate long-term interest rates.

Current Employment Situation

The most recent U.S. Employment Report was released on July 7th. It showed that payroll employment was still climbing during June, and 209,000 new employees were added to company payrolls. The same report showed that the unemployment rate dropped to a historically low 3.6%, and workers earned 4.4% more than a year earlier (In May, it was 4.3% more).

The markets immediately viewed these strong job gains, coupled with an acceleration of wage increases and the drop in unemployment, as foreshadowing a Fed hike in late July. And also viewed is as increasing the probability of additional tightening before year-end. Employment is high, and the labor market is so tight that employers are increasing what they have paid workers in order to attract suitable personnel.

A day earlier, the payroll company ADP released its National Employment Report, which is produced in collaboration with the Stanford Digital Economy Lab. This report also showed a strong labor market. The private sector (non-government) jobs increased by 497,000 in June. This was approximately double the strong number of new hires from the previous month.

The U.S. Unemployment Rate continues to remain very low despite the Fed’s aggressive efforts to slow the economy and only a modest 2% GDP growth rate. In fact, in April unemployment hit a 50 year low at 3.4% which is just below the June level.

Employment levels in the U.S. are now a key focus of the Federal Reserve (the Fed) in its effort to slow U.S. economic growth to combat persistent inflation well above the Fed’s target. Fed officials have repeated what most market participants know, that achieving lower inflation would be difficult without addressing the increasing prices that employees are receiving for their labor. A strong jobs market pushes wages higher, which filters into higher consumer inflation.

The job market’s continued strength has been somewhat surprising in what appears to be a slowing economy, with consistently low unemployment and solid job growth. This likely reflects unusual dynamics that stem from the novel economy during the pandemic. The economy hasn’t yet balanced out after massive government stimulus, low production, and a changed sense of work among many that are still of working age.

The employment numbers this year show there are still 1.6 job openings for each person that is looking for work. Considering those looking for work and the positions open are largely mismatched, this leaves employers either bidding up what they are willing to pay to attract the right person or producing less than is demanded by the market for their goods or services. Both situations are inflationary.

There are two sides to every problem; while potential employees willing to work represent far fewer workers than there are jobs, there are fewer, of age, adults willing to participate in the labor force. The labor force participation rate now stands at 62.6%, unchanged from the previous four months. Improving labor participation would be a preferred way to address the tightness in the labor market that’s leading to wage inflation, but the Fed doesn’t have the tools to incentivize this. So it is back to raising rates, draining money from the system, and otherwise taking the punchbowl away to end the party.

Good News is Bad News

This is why the Fed is not excited about job growth and low unemployment. And if the Fed isn’t happy, the markets aren’t happy. The bond market selling off in expectation that the Fed is going to raise interest rates lowers bond prices, and the stock market is concerned on many fronts, as high rates increase costs for companies, slow purchases that are typically financed, and with each tick up in rates, bonds and C.D.s become more attractive as an alternative to stocks.

So the good news which is that almost anyone who wants a job can have one, as it turns out, leads to a chain of events that causes concern among those invested in stocks.

But while unfortunate, the Fed actions are long-term good. Inflation quietly erodes the purchasing power of financial assets. So the Fed is focused on what is driving inflation, wage inflation being chief among them.

Take Away

The job market’s continued strength and the wage growth that comes with it creates a perplexing situation for all involved. The Fed has to work to reduce employment pressures, and stock and bond market participants are cheering on bad economic news – this is perplexing for investors of all levels.

Interest Rate Increases are Less Frightening When the Impact is Understood

The fixed income market, and the interest rates market in general have a pronounced role in shaping stock market dynamics and equity investor sentiment. At a minimum, higher rates, the cost of money, when increasing, will most directly impact businesses that borrow as part of their normal activity. Other industries find that growing profits is more difficult in a less direct way. And then there are actually sectors that can benefit from an upward-sloping yield curve. Below we cover five different ways that higher interest rates impact stocks, and mention sectors that may be especially hurt, and some that could even thrive if the rates continue to climb higher.

Background

The U.S. central bank, The Federal Reserve has raised overnight interest rates from nearly 0.00% to near 5.25%. Longer-term rates have not followed in lock-step as other dynamics such as future economic expectations, flight to quality, and Fed yield-curve-control have caused longer rates to continue to lag below short-term interest rates.

In recent days there has been some selling in bonds which has driven longer interest rates up. The overall reason is the rekindled belief that the Fed is not finished tightening after the FOMC minutes from June indicated such. But other factors such as investors doing break-even analysis on longer term bonds and then raealizing they may not be getting paid enough interest to offset inflation, or to benefit them more than rolling shorter maturities that may be paying 200bp higher.

The sudden increase in rates, especially the ten-year US Treasury Note which is a benchmark for many lending rates, including mortgages, has caused stock market participants to feel unsettled. Some of their fears may be justified, some may not be.

Five Ways Higher Interest Rates Impact Equities

#1 Higher Rates Impact on Equity Valuations

One of the primary concerns for stock market investors, when interest rates rise, is the potential impact on equity valuations. As interest rates increase, the discount rate used to value future cash flows is then higher. This can put downward pressure on equity valuations, particularly for stocks with high price-to-earnings ratios. Investors become concerned about the potential decline in stock prices and the overall effect on the market’s valuation levels.

#2 Profitability of Interest Rate-Sensitive Sectors

Some sectors are particularly interest rate sensitive. Utilities for example, might have a couple of things working against them. First off, they are notorious for carrying a high level of debt. As this debt needs to be refinanced (as bonds mature), the new bonds need to be issued at higher rates, increasing the utility’s cost of doing business.

Utilities also are popular investments among dividend investors. As yields on bonds increase, there is more competition for income investors to choose from, at times with lower risk, which makes utility stocks less attractive.

As one might imagine REITs, by definition, all have real estate as underlying assets. Rising interest rates can increase borrowing costs for REITs involved in property acquisitions and development. This can potentially affect their profitability and underlying property valuations.

As with utilities, the REIT sector attracts income investors; if bonds become a more attractive alternative, this creates lower demand for REIT investing.

Financial institutions are certainly impacted, however, depending on the segment within financials, some may benefit from increased profit margins, while others are weighed down by increased costs. Basic banking is borrowing short and lending out longer, then managing the risk of maturity mismatch. As longer-term rates rise relative to shorter rates, these institutions find their earnings spread increases.

In recent years the trend has been, especially for larger banks, to create loans and then sell them. They profit on the servicing side, or administrative fees to create the loan. In this way they are shielded from interest rate mismatch risk, and they can make more loans on the same deposit base (selling the loans replenished the funds they can loan from). So the benefit of rising rates on benchmark securities relative to the banks deposit rates could have much less positive impact than it might have if they held the loans. What may actually happen within these institutions is that they experience fewer loans as consumers and business borrow take fewer loans, thus earning less fee income.

#3 Investors Lean Toward Bond Investments

The return on anything is the present value, versus future value, over time held. Higher interest rates can make fixed-income investments more attractive than low rates compared to stocks. When interest rates rise, more investors prefer a known return in terms of interest payments than an unknown move in stocks valuations. This shift in investor preferences can lead to reduced demand for equities and potentially impact stock market performance.

Investors buying bonds as rates are rising will experience a decrease in the value of their fixed income securities. So, they may be surprised to learn that they avoided stocks because stocks may go down in value, and instead invested in fixed income which mathematically will go down in value when rates rise.

#4 Borrowing Costs for Companies

As mentioned earlier, rising interest rates increase the borrowing costs for companies. This can impact corporate profitability and investment decisions, which in turn can affect stock prices. Companies that rely heavily on debt financing may experience higher interest expenses, potentially squeezing profit margins. Investors become concerned about the potential impact on corporate earnings and the overall financial health of companies in a higher interest rate environment.

Analyzing a company’s capital structure, and looking for signs of low debt levels, or long-term debt that is locked in at the low interest rates of the early 2020’s, may be a good way to filter companies that have a profit advantage over their competitors

#5 Consumer Spending and Business Investment

Consumer spending levels are a direct driver in consumer stocks. When borrowing becomes more expensive, consumers may reduce their discretionary spending. This can impact businesses that rely on consumer demand, potentially leading to lower revenues and profitability. The stocks that tend to hold up more when spending levels decrease are those that produce necessities.

Business investment during periods of rising interest rates can influence investment decisions for businesses. As borrowing costs increase, companies may reduce or delay capital investments, expansions, or acquisitions. This cautious approach can impact economic growth and overall industry development, which can in turn affect its performance, for much longer than a quarter or two.

Take Away

Stock market investors have legitimate concerns about the impact of higher interest rates on their investments. The potential effects on equity valuations, profitability of interest rate-sensitive sectors, investor preferences for fixed-income investments, borrowing costs for companies, and consumer spending/business investment are key factors that contribute to investor apprehension. It is as important for investors to monitor interest rate trends and understand the impacts as it is for them to monitor.

The Federal Reserve released the minutes of its last Federal Open Market Committee (FOMC) meeting. The minutes show the Fed was largely unified behind the pause (no change in monetary policy) decided at the last meeting. The new release also indicates that most members do not believe the Fed has yet tightened enough to reach a 2% inflation target over time, and that the monetary policy committee would eventually have to move rates higher.

The FOMC holds eight regularly scheduled meetings during the year and may call other meetings as needed. The minutes of regularly scheduled meetings are released three weeks after the date of the policy decision. Committee membership changes at the first regularly scheduled meeting of each year.

Synopsis of FOMC Decision

Buying time to assess the impact of the historically aggressive tightening since March 2022 was an overall message one can derive from the most recent Fed report, and inaction. While “some participants” would have agreed to a rate hike in mid-June, in order to assure the inflation fight headway doesn’t reverse, “almost all participants judged it appropriate or acceptable to maintain” the fed funds rate at the 5% to 5.25% level, to ascertain if more is actually needed.

The minutes provided economic projections not available before its release along with other details not provided in the policy statement or press conference after the meeting. Notable among these disclosures is the level of agreement among voting members to pause. “Most of those participants observed that leaving the target range unchanged at this meeting would allow them more time to assess the economy’s progress,” toward returning inflation to 2% from its current level more which is double the target.

The Fed staff forecasts still foresaw a “mild recession” beginning later in 2023, but those at the Federal Reserve actually responsible for policy were concerned with data that showed a continued tight job market and only modest improvements in inflation. Officials were challenged trying to reconcile economic numbers showing a strong economic trend with evidence of possible weakness, for example, household employment figures pointed to a weaker labor market than the payroll numbers indicated, or national income data that seemed weaker than the more stronger readings of gross domestic product.

It is perhaps easier to understand now after the minutes have been released why Federal Reserve Chair Jerome Powell said just following the June meeting that the decision marked a switch in strategy. The U.S. central bank would now be focused more on just how much additional policy tightening might be needed, and less on maintaining a steady pace of increases.”Stretching out into a more moderate pace is appropriate to allow you to make that judgment” over time, Powell said.

While Powell also emphasized a united front among the 18 Federal Open Market Committee members, noting that all of them foresee rates staying at least where they are through the end of the year, and all but two see rates rising. That is confirmed again by the minutes, which show some misgivings among the more dovish policymakers. Atlanta Fed President Raphael Bostic, for instance, has said he thinks rates are sufficiently restrictive and officials can now back off as they wait for the lagged impact from the 10 hikes making their way through economy.

There are four more FOMC members scheduled in 2023, the next meeting on monetary policy will be held on July 25 and July 26.

The Markets During the First Half of 2023 Were Reflective of the People that Trade Them

Financial markets reflect the collective actions and expectations of market participants. This includes rational analysis, irrational emotions, and at times less than rational analysis. The emotions and number crunching get their cue from a daily barrage of information including: profits, policy, panic, prices, politics, purchasing power, the president …and that’s just the Ps. So each day, as Channelchek prepares to deliver research, articles, and pertinent video content to subscriber’s inboxes, we plow through an abundance of information and hope to share what is either not being addressed or covered, or present front page news from the point of view of seasoned investors, not less experienced news writers.

Below are six articles, one from each month this year. Although I have favorites not included here, and these may not have been the most read or shared, they told a slightly expanded story than found on the mainstream take on the subject and are still relevant to some investors.

As a content provider to this popular investment research platform, my job is not to call the market; it is to present thoughts and knowledge to help investors make decisions on small and microcap stocks along with the overall universe of investment opportunities. The insights below from earlier this year are still quite current, and worth digesting.

On the very first business day of 2023, three regulators announced concerns over businesses involved in cryptocurrency citing the lack of oversight, lack of standards, and unknown risk. As the year progressed, the three federal agencies, which do not include work on oversight being done by the SEC or CFTC, are now working hard to regulate what banks can do involving crypto. The SEC for its part has been creating headaches for some of the larger crypto exchanges. Banks are having a particularly difficult time incorporating the asset in their business.

Investment content providers love Michael Burry. The reason is that readership goes through the roof whenever his name is mentioned. Still, if there is nothing to write about the subject, or if it is old news, the writer, blogger, or vlogger is doing investors a disservice.

We’re choosy about when to take one of Burry’s rare tweets and decipher them for readers. But, we always try to be among the first when his fund’s public holdings are reported each quarter on SEC form 13-F. But there are only few times during the year when there is actually worthwhile news. This is because Burry is usually tightlipped. Unless required by a regulator, the successful hedge fund manager is out of the public spotlight, presumably crunching numbers and rebuilding old guitars.

This article is good advice that can be used any time the Fed is trying to reel in inflation.

It was 1963 the last time the CFA Institute (Chartered Financial Analyst) made any changes to their prestigious designation. However, the investment world is changing, and the CFA Institute is responding in order to better serve those that benefit from the services of skilled analysts. In 2023 CFA candidates will have more choices, more study material available, and the ability to take credit for their rigorous studies beginning after passing Level I.

Some thoughts on why, eligibility, and the new focus are presented here along with how it should help keep the credential fresh and more useful.

It wasn’t too long ago that the Federal Reserve did not announce its intentions. If a Fed-watcher or market participant wanted to know for certain if the FOMC adjusted monetary policy, the best they could do is see if measures of money supply increased or decreased. Weeks later the FOMC Minutes would be released, and the markets would know for sure what the Fed did at the previous meeting.

When the Fed became more transparent, the market focus on money-supply disappeared. This has now reversed as the stimulative money that had been injected into the economy to prevent undue weakness during the pandemic is now being methodically removed via quantitative tightening (Q.T.). The renewed focus on M2 is to make sure the Fed sticks with its plan. Signs that it may not be impact the amount of money available to chase goods and services, this impacts inflation.

The Fed’s battle to drain the cash put into the system, and do it in a way that doesn’t crash banks, or the overall economy is perilous, is continuing and well worth understanding.

Economists and news writers have been negative about the economic outlook, scaring people with the word recession since before the year even began. And while there are some weaknesses, the stimulative money supply is still exceedingly high, jobs are more abundant than workers, and home sales have not reacted as expected when mortgage rates rise from 3% to 7%.

The often-repeated line that the downward slope of the yield curve is a time-tested indicator of an impending recession was the echo chamber talking point that probably didn’t apply to this economy because of a novel Fed policy.

From a textbook position, those saying a negative yield curve indicates a recession got the answer right if they were taking a college quiz. However, those that were saying this inverted yield curve indicates a recession may have flunked. And if you copied off the economist next to you, and they somehow missed that the Fed owned 33% of all U.S. Treasuries outstanding, and because of their policy of yield-curve-control, the yield curve was not market-driven, and therefore not a reliable indicator of anything. What we know is that when the Fed buys one out of every three bonds, it leaves a mark on the area of the curve that they are active.

With higher than expected GDP released last week, most have stopped talking about a recession in 2023. We put out several articles beginning in 2022 explaining why others may have this yield curve indicator wrong, this is addition is most recent.

I highly recommend reviewing this article if your summer backyard barbecues include conversations about economic strength (or weakness).

Small Cap stocks had been lagging behind larger companies. Historically they are more volatile, but investors expect to be compensated over time for the additional risk they take. Yet, over a longer than normal period, they still lagged. This seemed to have changed; during the first week in June there were some days that small company returns had a little more giddy-up than they had in recent months or years. On June 6th we published the above article.

Small cap stocks finished the month well ahead of the large caps and even mega-cap companies. This momentum has carried into the second half.

Let’s Start the Second Half of 2023 Together

If you are one of our free subscribers, thank you for trusting us as one of your news and research resources.

If you have not yet signed up, now is a great time to make sure you don’t miss any research, videos, special events, and market insights. Sign up here.

I hope you found these six articles compelling, and if you have not registered for no-cost insights to your inbox each day, here’s your chance to start the second half with a slightly different investment angle.

Looking Back at the Markets in June and Forward to July

Enthusiasm in the overall stock market was strong in June, the major indices were all up, and every S&P sector closed in positive territory. In fact, there was spectacular performance across market caps as Apple (AAPL) became the first company to reach a $3 trillion market cap, and noteworthy among small caps, Bitcoin mining company Bit Digital (BTBT) was up another 20% and a staggering 685% on the year during the last week in June. The across-the-board positive sentiment came during a month when the market was disappointed by the Federal Reserve’s continued hawkish bias.

Two dark clouds that the markets had hanging over them as they entered June were a possible U.S. default on debt and talk of a recession later this year. A higher debt ceiling law was signed on June 5, and a strong jobs report and higher-than-expected first-quarter GDP have for most, pushed most recession forecasts into 2024 or later. June’s performance may reflect a celebration and feelings of relief from both concerns.

Consumer confidence improved in June to its highest level since January 2022, reflecting a big jump in outlook and expectations. This surprise positive mood is reflected in stock market rotations experienced during June in both market-cap and market sectors.

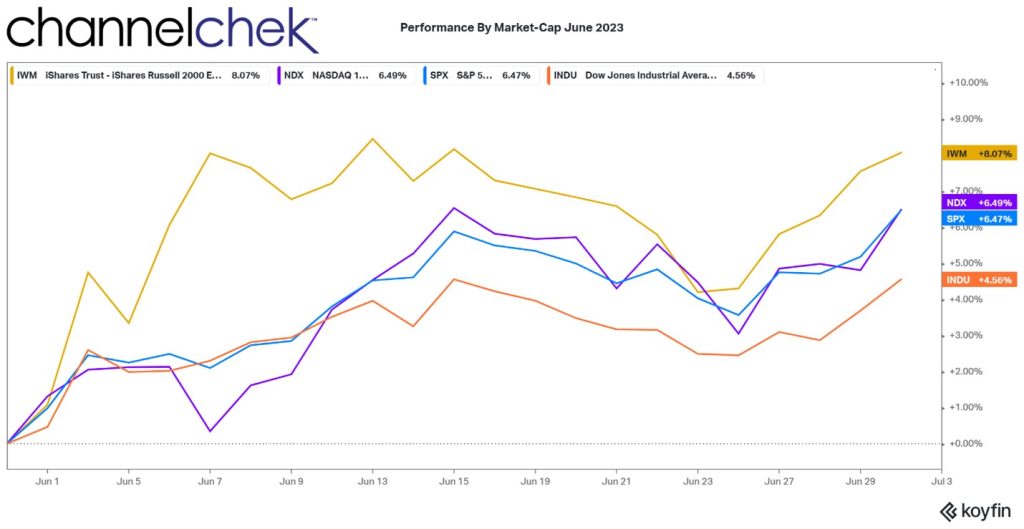

Four broad stock market indices were positive in June. In order, the Russell 2000 Small Caps, Nasdaq 100 Large Caps, the S&P 500 Large Caps, and the Dow Jones Industrials. Small cap stocks are the big winner in June as investors went looking for value. The Russell 2000 rose 8.07%. The smaller stocks may now have more positive impetus that could carry over into July as a report released last week by Goldman Sachs estimates that based on their models, small cap stocks could rise 14% over the next 12 months.

While small cap stocks had their stars, the Nasdaq maintained a startling pace as big tech retained its appeal despite individual company market caps that have exceeded those of developed countries. The Nasdaq 100 was up 6.49% in June. The S&P 500 nearly matched Nasdaq with a 6.47% return. The Dow 30 Industrials, which have had a difficult few months, returned 4.56% to investors.

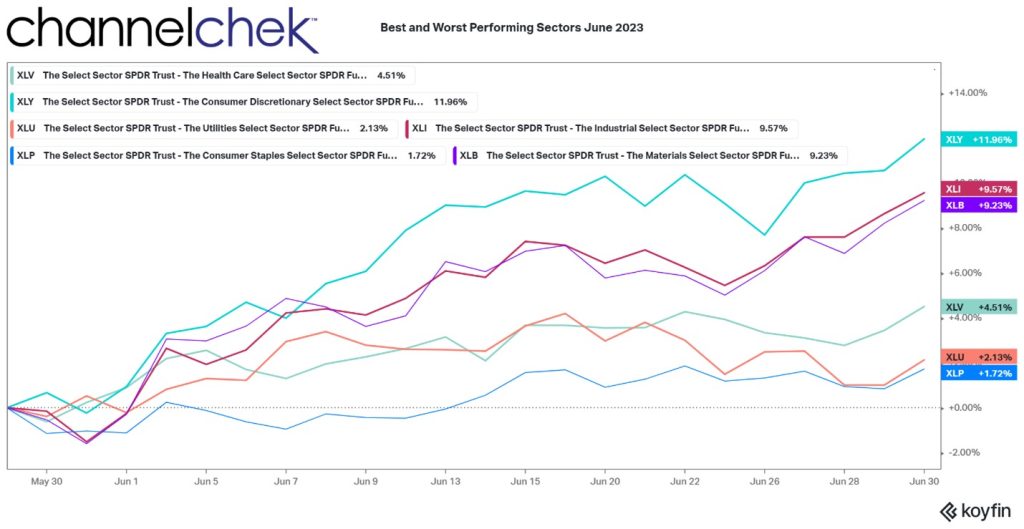

Of the 11 S&P market sectors (SPDRs), even the lowest performer had an impressive one-month return. The chart above reflects the three best-performing sectors and the three worst. The performance indicates that there was a sector rotation away from defensive stocks during June.

Consumer Discretionary had the best return at 11.96%. By definition, these are companies selling products that consumers can cut back on or more easily avoid. The top ten holdings include Starbucks (SBUX), Bookings Holdings (BKNG), and Tesla (TSLA).

What S&P calls the Industrial Select sector finally came to life in June. Its 9.57% return represents almost all of this sector’s performance for the first six months of 2023 (9.73% YTD). Examples of top stocks contained in this index are John Deere (D.E.), General Electric (G.E.), and Union Pacific (UNP).

The third was Materials Select which was negative on the year heading into June. The 9.23% return on the month more than erased the negative 7.67% performance heading into the month.

Each of the top three performers is typically sectors that investors delve into when their economic outlook is more positive.

The three worst-performing sectors also indicate the month was very positive. The Health Care sector was the best of the bottom three at 4.51%. While this did not bring the sector positive on the year, companies like Johnson & Johnson (JNJ), Abbott Labs (ABT), and United Health (UNH), had experienced strong years this decade with growth drivers that have since weakened some.

The second to weakest performer is Utilities Select. Utilities are still negative on the year despite a 2.13% increase in June. Companies like American Electric Power (AEP), Dominion Energy (D), and Consolidated Edison (E.D.) are surrounded by a lot of uncertainty as their costs are driven more than other industries by fuel prices. Additionally, investors in utilities tend to be dividend stock investors. Dividend stocks tend to underperform in a rising interest rate environment as they compete less favorably with bonds.

The worst-performing sector provides further evidence of a rotation during June. Consumer Staples was the second-worst-performing sector at the close of May. While it returned 1.72% in June, the sector, which includes Colgate Palmolive (CL), Walmart (WMT), and Philip Morris (PM), usually gains in popularity when consumer confidence is low, it loses popularity as consumer confidence is high, that’s when, as we saw in June, consumer discretionary stocks get attention.

Looking Forward

The job market is strong, inflation is tapering, and consumers are more confident. There are even signs that companies that have been waiting for an improved market to go public are considering now a good time for an IPO.

Bitcoin mining stocks and artificial intelligence are still be on fire. The crypto-mining stocks interest is tied to the price of Bitcoin – many of the stocks have actually outperformed the cryptocurrency. Artificial intelligence, as its potential becomes better understood, has inspired many to place bets that this will grow into a technology that is indispensable to many industries. Is the next Apple in this tech segment?

The rotation to small caps and sectors that perform better when the economy improves has a lot of momentum heading into July.

The next FOMC meeting is July 25-26; while market participants already expect further tightening, it has not deterred their positive view on the “risk-on” trade.

Take-Away

The market was jubilant in June. The signing into law of an increased debt ceiling helped kick off a change from the uncertain mood in May. It unleashed buyers that continued even after it was clear the Federal Reserve was not finished hiking interest rates.

The year 2023 now sits at the halfway point. And within a few months, we will be in a presidential election year. Stocks tend to do well in election years. While the Russia/Ukraine situation is still uncertain, especially in the energy sector, the markets seem to have already priced in negative scenarios and are marching upward confidently.

On the One Hand, the Russell 2000 Should Outperform, on the Other Hand…

A Goldman Sachs report released Wednesday, June 28 projects that the Russell 2000 should gain 14% over the next 12 months and could outperform the S&P 500 in the coming year. The economic headwinds that companies represented in the index would have to overcome were discussed in the report. Each should come as no surprise. The forecast is based on Goldman’s research using expected economic growth and current valuations.

Based on US economic growth and a model built on initial valuations, the small-cap index should gain 14% over the next 12 months, according to Goldman. This looks even more favorable compared to the reports projection that the S&P 500 is expected to climb 9% over the same period.

The research note said this would mark a position change as the S&P 500 has been outperforming the Russell 2000 Small Cap index.

Goldman outlined three near-term macro headwinds facing the Russell 2000 Index:

Rising Interest Rates

The index is more sensitive to monetary tightening because listed companies tend to have a higher debt burden than the S&P 500. As interest rates continue to rise, the cost of servicing debt could gradually put pressure on small caps, as about one-third of Russell 2000’s debt is floating rate.

This could become a complication through the remainder of the year, as the Federal Reserve has signaled the possibility of two more hikes. For its part, Goldman expects another hike in July, and predicts a cut for 2024.

Economic Development

Compared to the S&P 500, the Russell 2000 is more sensitive to US economic performance, wrote Goldman. Even if a recession has been avoided, small-cap stocks struggle to outperform in the later stages of the business cycle as investors turn to companies with larger balance sheets.

The note recognized another possible bump in the road suggesting it appears that the market has already priced in the GDP forecasts, and growth looks unlikely to pick up any further as long as the Fed continues to tighten to tame inflation.

Sector Composition

Goldman said the Russell 2000’s high exposure to cyclical stocks, regional banks, real estate and biotech makes it more vulnerable to slowing growth, rising rates and the re-emergence of financial stability fears.

This means there could be further cuts in earnings forecasts. The note recognized that while earnings revisions among S&P 500 companies have mostly been flat, Russell 2000 revisions are continuing.

Take Away

Goldman’s basic analysis shows the propensity for the small cap sector to begin to outperform in a big way. As is the case with market forecasters, the story starts out “on the one hand this could happen,” and then transitions with, “but on the other hand…”. It is standard to look out into the future and see where a sector could be headed, but also recognize where there may be trouble along the way.

The report did not lay out a scenario where the report may have underestimated where the Russell Small Cap index may be in 12 months, but with all the less-than-knowns surrounding this year, and an election year, it is safe to presume that the analyst could also have undershot where actual performance will be 12 months into the future.

This Week’s Economic Focus Will be on PCE Inflation

It’s the last trading week of the month, quarter, and first half of 2023. The Fed Chair is scheduled to speak on Wednesday at the ECB Forum on Central Bank Policy, and the Fed’s favored inflation gauge will be released on Friday. As we approach the 2023 halfway point, the S&P 500 is up 13.25% YTD. Historically, whenever the S&P 500 is up at least 10% YTD at the end of June, the index ends the year up on the year 82% of the time. However, it gained 7.7% on average for those years, which suggests some gains were given back in the average year.

Monday 6/26

• The ECB Forum on Central Banking 2023 is a three day event beginning Monday. The US Federal Reserve Chairman will take part in a panel discussion Wednesday.

Tuesday 6/27

• 8:30 PM ET, Durable Goods orders are forecasted to have fallen 1.0 percent in May after April’s 1.1 percent rise. Ex-transportation orders are seen unchanged with core capital goods orders, after jumping 1.3 percent in April, rising a further 0.6 percent.

• 10:00 AM ET, Consumer Confidence is expected to rebound slightly in June to 103.7 versus May’s 102.3 which was better than expected but still down 1.4 points from April. The index has sat at depressed levels for the past year.

• 1:00 PM ET, Money Supply, including the closely watched M2 will be released. M2 had stood at $20,673.1 Billion as of the last reporting. The act of the Fed tightening credit conditions, is typically orchestrated by reducing money in the system which can be expected to reduce money supply by its two most watched measures, M1 and M2.

Wednesday 6/28

• 9:30 AM ET, at 2:30 PM in Portugal a panel discussion on policy will be modersated by CNBCs Sara Eisen. The four member panel will include J. Powell, US Federal Reserve, A. Bailey, Bank of England, C. Lagarde, ECB, and K. Ueda, Bank of Japan.

• 10:30 AM ET, The Energy Information Administration (EIA) provides weekly information on petroleum inventories in the U.S., whether produced here or abroad. The level of inventories helps determine prices for petroleum products.

Thursday 6/29

• 8:30 AM ET, First quarter GDP third estimate is expected to show 1.4% growth. While this is not e a strong pace, it indicates the US is not currently in a recession.

• 8:30 AM ET, Jobless Claims for the week ending June 24 are expected to be 270,000 versus a second straight and elevated 264,000 in the two prior weeks and 262,000 the week before.

• 4:30 PM ET, Factors Affecting Reserve Balances, otherwise known as The Fed’s Balance Sheet or the H.4.1 report is a weekly report of a consolidated balance sheet for all 12 Reserve Banks that lists factors supplying reserves into the banking system and factors absorbing reserves from the system. The report is officially named Factors Affecting Reserve Balances, otherwise known as the “H.4.1” report.

Friday 6/30

• 8:30 AM ET, Personal Income and Outlays, including PCE Inflation, will be released as part of a data set. Income is expected to rise 0.4 percent in May, with consumption expenditures expected to increase by 0.2 percent. These would compare with April’s 0.4 percent gain for income and 0.8 percent jump for consumption. PCE Inflation readings for May are expected at monthly increases of 0.1 percent overall and 0.4 percent for the core (versus April’s respective increases of 0.4 percent for both) for annual rates of 3.8 and 4.7 percent (versus April’s 4.4 and 4.7 percent).

• 10:00 AM ET, Consumer Sentiment is expected to end the first half of 2023 at 63.9 for June, this would be up nearly 4 points from May.

What Else

The summer doldrums is a Wall Street term for reduced trading activity between Memorial Day and Labor Day. Many professional investors take time off from work during the summer; this means portfolios are in the hands of the second-string portfolio managers that are there to monitor and maintain but not take big positions or make big decisions. Volume is often reduced, which could cause exaggerated swings in prices.

Lifeway Foods, Inc. (LWAY), which has been recognized as one of Forbes’ Best Small Companies, is America’s leading supplier of the probiotic fermented beverages. Wherever you are on Monday, you can attend the virtual roadshow and better understand directly from management the many intricacies of the probiotic food business as it relates to Lifeway. Should you have a question for management, there will be an ample Q&A period for participants to get their questions answered.

Are Higher Interest Rates Going to Be Devastatingly Expensive to the US Treasury?

The Federal Open Market Committee (FOMC) has raised the overnight Fed Funds target rate from near zero to around 5% in less than a year and a half. That multiple from its starting point is huge and, as designed, driven up other rates, both savings and lending. Given the pace that rates have gone up, the cost of refinancing or rolling existing debt for the federal and municipal governments, businesses, and households, has obviously experienced a large cost increase. When treasury debt matures, the US government decides whether to “roll over” their debt by issuing new securities at the current rate—or find other resources to repay borrowers. When rolling, far more is required to be borrowed just to stay even and cover interest rate costs. Below we use numbers from Federal Reserve branch to determine how much more it will cost.

The Federal Reserve Bank of St Louis (FRED), compiled data on the increased cost of US borrowing as a direct result of the Federal Reserve’s tighter monetary policy. The sheer magnitude of the amount borrowed, and the impact of interest rates make clear the US either will be increasing its borrowings, just to stay even with rollovers, or will need to cut back by spending. Cutting back spending removes economic stumulus. Below are the FRED numbers on how interest costs are expected to change.

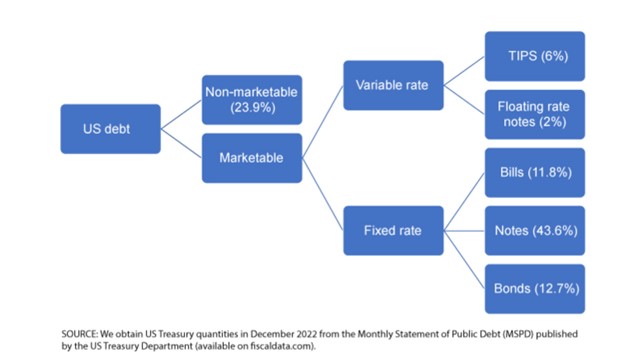

US Government Debt Breakdown

The total public debt, according to the US Treasury Department, is just over $31.4 trillion

Of the $31.4 trillion, about $7.5 trillion or 23.9% is nonmarketable debt—mainly consisting of the social security trust fund, military retirement funds, and the civil service retirement fund.

That leaves $23.9 trillion in marketable debt. $2.5 trillion is in variable-rate debt and increases when rates rise. The variable category is made up of Treasury inflation-indexed notes (TIPS) and floating-rate notes (FRNs). TIPS make up 6% of the overall US debt, have original maturities of 5, 10, or 30 years. FRNs make up only 2% of US debt, have maturity of 2 years, and interest payments are based on a fixed spread and a variable index rate calculated weekly.

Then there are $21.4 trillion in fixed-rate marketable securities. This final category contains bills, notes, and bonds, which make up 11.8%, 43.6%, and 12.7% of the US debt, respectively. The only differences in these instruments is that bills are discounted to yield the rate, while notes and bonds have semiannual interest rate payments. “notes” is the term used from 2-10 year maturities, bonds are from 10-20 years

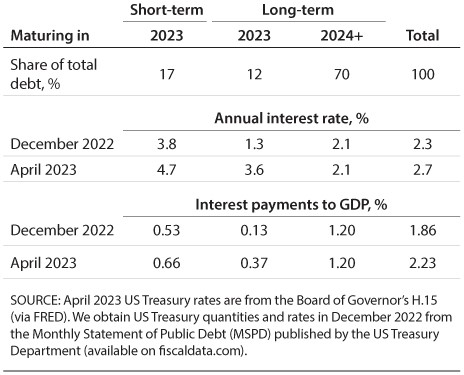

Focusing only on the 68.1% fixed-rate of marketable U.S. debt, consisting of bills, notes, and bonds and for ease, using end of the year December 2022 to use specific securities and their roll dates, this is what the St. Louis Federal Reserve laid out.

The debt maturing each year has been broken down into different colors below by maturity. For example, the orange portion of the 2023 column represents two-year US Treasury debt maturing in the year 2023.

Notice about 30% of existing debt is maturing in 2023. And nearly 62% of existing US debt is coming due in the nine years after 2023. Finally, 18% of existing Treasury debt is very long dated and will not come due for at least 10 years. So 82% will reset at current rates within the next nine years.

Maturity Dispersion

Aside from quantity and maturity, the calculations aren’t complete without factoring in the yield of the current debt. Remember, the current interest rate levels are not the first time visiting 4% or higher.

FRED used data on quantities and prices from December 2022 and compared it with the interest expense the US government would pay on the same quantity of debt using the new, higher interest rates in April 2023. Here, FRED assumed that the US government will keep the same debt schedule as in 2022. In other words, for any debt maturing during 2023, the government will issue another security with the same quantity and maturity—but at the new interest rate. They define short-term debt as any security with maturity less than or equal to one year and long-term debt as any security with maturity greater than one year.

Maturing Interest Rate, New Interest Rate

Short-term debt maturing in 2023 makes up about 17% of the outstanding. However, because this debt is short term, most of it had already been rolled over at higher interest rates in 2022. The December 2022 average rate on the short-term debt was already 3.8% and therefore increased only 0.9%—to 4.7%—in April. The long-term debt maturing in 2023 is almost 12% of debt, and the average rate increases from 1.3% to 3.6%, which is fairly large. Long-term debt maturing after 2024 will have the same interest rate, since the federal government is not rolling it over in 2023. Long-term debt makes up just over 70% of the existing debt.

To get some idea of the magnitude of $98 billion, the St. Louis Fed provided two examples: First, the Federal Reserve pays the Treasury Department revenue or remittances, which basically contain all remaining Fed revenue after operating expense. Fed remittances were $105 billion in 2021 and were negative $54 billion in 2022, in part due to the increases in interest rates. In 2021, this was an example of an inflow, or payment, to the government. Second, an example of an outflow, or expense incurred by the government, the US Department of Transportation spent $114 billion in 2022.

Bringing in the variable rate debt that we excluded earlier, the Congressional Budget Office (CBO) has forecasted for interest expense payments over GDP in the next 10 years. The CBO’s projections include variable-rate marketable securities—TIPS and FRNs—so they of course will of course be added to the fixed rate securities.

Take Away

What the US government spends, is generally stimulative. Money spent on interest would also seem to work its way into the system and be stimulative, but in the face of inflation, more goods or services is not necessarily attainable with the larger payments.

The US government had $21.4 trillion in outstanding US Treasury debt as of December 2022. Given large increases to interest rates over the past year, FRED estimated that it will cost the US government an additional $98 billion to pay interest on their debt in 2023.

The estimate is close to that made by the CBO as well. While the number seems large, relative to flows in and out of the US Treasury it is in line and not by comparison large.

The report from the Federal Reserve Branch concluded if long-term rates remain high, servicing the debt will become a larger and larger portion of the overall government expense.

This Week We’ll See if the Small-Cap Rally Continues, and Which Individual Stocks Move from the Russell Reconstitution

The FOMC interest rate pause at 5.00-5.25% last week created investor uncertainty as there was little forward guidance as the policymakers insist they remain data dependent. Chair Jerome Powell was emphatic in his comments to the press on Wednesday that getting inflation down to the 2 percent average inflation target is the FOMC’s unanimous goal – although there may be differences on the speed or level at which rates need to be adjusted.

Powell will have the spotlight again this week as he gives two testimony’s, the first on Wednesday before the House Financial Services Panel, and then on Thursday before the Senate Banking Committee.

While the mood of markets is still apprehensive, this did not stop the S&P 500 from rallying and reaching the highest weekly close since April 2022.

Monday 6/19

• US Markets closed in celebration of the Juneteenth holiday.

Tuesday 6/20

• 8:30 PM ET, May Housing starts are expected to hold steady after experiencing a bounce in April. Exonomists expect May’s starts to have been 1.433 million, they were 1.416 million in April.

Wednesday 6/21

• 10:00 AM ET, Federal Reserve Chairman Powell will appear before House Financial Services Panel.

• 10:00 AM – 4:00 PM ET, While Fed Chair Powell will be getting the attention as he reads prepared remarks and answers question, the day will be filled with other FOMC members speaking and sharing their view and outlook for the first time since the June FOMC meeting concluded. This includes Lisa Cook at 10:00 AM ET, Philip Jefferson also at 10:00 AM ET, Austan Goolsbee at 12:25 PM ET, and Loretta Mester at 4:00 PM ET.

Thursday 6/22

• 8:30 AM ET, Jobless Claims for the June 17 week, is expected to remain near the previous weeks level. The consensus is 261,000 versus 262,000 last week.

• 10:00 AM ET, Existing Home sales for May are expected to slip slightly to a 4.25 million rate. The National Association of Realtors described sales as “bouncing back and forth” but remaining “above recent cyclical lows.”

• 10:00 AM ET, Federal Reserve Chairman Powell will again be the focus as he appears before the Senate Banking Panel.

• 10:00 AM ET, The Index of Leading Indicators was down by 0.6 percent in April, for May it is expected to post a 14th straight decline, the consensus is down 0.7 percent. This index has been in sharp decline and has long been a trendline toward slow or no economic growth. signaling a pending recession.

• 4:30 PM ET, Factors Affecting Reserve Balances, otherwise known as The Fed’s Balance Sheet or the H.4.1 report is a weekly report of a consolidated balance sheet for all 12 Reserve Banks that lists factors supplying reserves into the banking system and factors absorbing reserves from the system. The report is officially named Factors Affecting Reserve Balances, otherwise known as the “H.4.1” report.

Friday 6/23

• 9:45 AM ET, The Purchasing Managers Index (PMI) is not expected to show significant change in June compared to May; manufacturing underperformed at 48.5 and services even though services were strong at 53.5.

What Else

On Friday the Russell Indexes will have new components beginning the moment the market closes. The following Monday morning the indexes will reflect these changes, and index funds that are designed to match the performance of the funds will hopefully have gotten their trades off in time. Expect some interesting moves of a few stocks on Friday as a result.

Small-cap stocks have joined the stock market rally in June and, according to an article in Morningstar, “trouncing the larger indexes.”

Noble Capital Markets has been hosting road shows of interesting small-cap companies in various cities and towns throughout the US. This week features a very busy week with company’s speaking to potential investors in St. Louis and Florida. Also there will be two virtual events, so that no one is excluded by geography. Become informed here.

The FOMC Member’s Change in Sentiment is a Big Focus

Whether the Fed moves rates up after the June FOMC or not could mean little to whether there is additional drag on the economy. The short end of the yield curve, where savers benefit, has risen each time the Fed has raised rates. Out further, the 10-year T-Note, which is the benchmark for 30-year mortgages and from which corporate 10-year notes are spread, has been remarkably steady. Nine months ago, when Fed Funds were 3.00%- 3.25%, the 10-Year Treasury yielded 3.76%. Today the Fed Funds target rate is 5.00-5.25%, the 10-Year is still at 3.76%. This may be why the Fed has had a difficult time reeling in inflation, longer interest rates, where they impact the economy most, had reached 4.25% last October, the Fed has since tightened 200bp, and 10-year rates have traded around 50 bp lower since the October high, despite the tightening. And for the same reason, mortgage rates are lower now than they were last October.

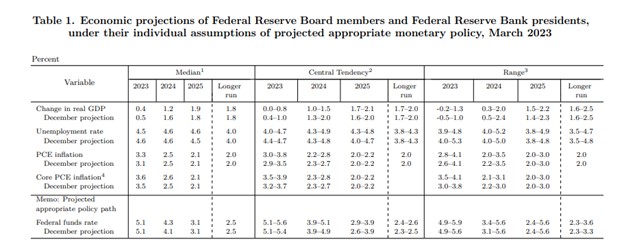

Summary Of Economic Projections

More meaningful for market participants might be the Summary of Economiuc Projections (SEP). Outside of a normal knee-jerk reaction after Wednesday’s policy announcement, or a quick trade that can be had off Powell’s press conference remarks, what the Fed members now expect by year-end is a better indication of any new mindset on monetary policy.

The Summary of Economic Projections includes estimates from the FOMC members showing where they see rates at the end of 2023 (and beyond). At the March meeting (see below), most of the Fed policymakers saw rates staying at current levels, with a few signaling additional hikes may be coming. While Powell will answer questions at the press conference that may be indicative of what they are thinking, the change in the SEP numbers (released in the statement after the meeting) is a better indicator of whether the Fed is now more hawkish or dovish.

A big shift toward expectations of higher rates would indicate a more hawkish stance. It will be useful to note how projections have evolved compared to March – Chair Powell will, of course, provide further color through his press conference.

Pause, Pivot, or Push Higher

Has the view changed with recent economic data? Was the view in March skewed by what could have turned into a banking crisis? We’ll see in hard numbers, without reading between any lines. We can see in black and white what the aggregate thinking is of the members when behind closed doors, where the important discussions happen – inside the FOMC meeting room.

After the announcement, Channelchek subscribers will receive a summary in their email of the announcement, changes in language from previous meetings, and the new SEP to compare any change in sentiment (subscribe at no cost).

While the actual impact on the overall economy of a 25bp move compared to a Fed pause may have little impact on the economy, company earnings, or even Treasury Bonds, each time the Fed raises overnight rates, there are investors that are more comfortable with a larger allocation of cash. Depending on where “uninvested” assets are held, they may be earning near 5%. This is a risk to stock prices as some investors may find be comfortable with money market returns for a larger portion of their portfolios. Fewer assets in the stock market have a depressing effect on prices.

Take Away

While pre and post-Fed meeting investor conversations tend to swirl around words like, “pause”, “pivot”, and “tighten”, the Fed’s overall change in rate expectations, which they have the most control over, is more telling than any polished statement or press briefing. These numbers are on the SEP report.

This Week’s Events are Sure to Keep Investors on Their Toes

I wouldn’t want to be Fed Chair Jerome Powell this week. The June 13-14 FOMC meeting may be the first meeting of the Committee that sets monetary policy, since January 2022, when a tightening of monetary targets doesn’t occur. The decision will come down to the wire as very important inflation data won’t be released until the first day of the meeting on Tuesday. While most on the Committee have expressed seeing current inflation data as problematic, there usually is a delay between when the Fed first alters policy, and the impact it creates.

Whether the Fed again acts to slow the economy, or takes a breather, announced at 2:00 on Wednesday, Powell will face reporters having to explain the Fed’s action or inaction. With likely less personal conviction than at previous press briefings, his responses may be more general than usual.

Monday 6/12

• 2:00 PM ET, The Treasury Statement is the U.S. Treasury’s release of a monthly accounting of the surplus or deficit of the government. Changes in the budget balance reflect Federal policy on spending and taxation. Forecasters see a $205.0 billion deficit in May that would compare with a $66.2 billion deficit in May one year ago, and a surplus of $176.2 billion in April this year.

Tuesday 6/13

• The June FOMC Meeting begins day one of two.

• 6:00 AM ET, NFIB Small Business Optimism Index has been below the historical average of 98 for the past 16 months in a row. May’s consensus is for a decline to 88.4 versus 89.0 in April.

• 8:30 AM ET, The Consumer Price Index this month could move markets significantly if there is a significant change in the data from the previous month. Core price increases in May are not expected to have slowed. They are expected to keep their pace of April’s 0.4 percent monthly increase. The core’s year-over-year rate is seen easing to 5.3 from 5.5 percent. Overall price increases are expected to halve to 0.2 percent on the month from 0.4 percent and 4.1 percent on the year from 4.9 percent.

Wednesday 6/14

• 8:30 PM ET, The Producer Price Index – Final Demand number is another important inflation index that the FOMC members may want to peak at before voting Wednesday on any policy shift. After rising 0.2 percent in April, producer prices in May are expected to fall 0.1 percent. The annual rate in May is seen at 1.6 percent versus April’s plus 2.3 percent. May’s ex-food ex-energy rate is seen up 0.2 percent on the month and up 2.9 percent on the year, matching April’s 0.2 percent monthly rise and just below the month’s 3.2 percent yearly rate.

• 10:30 AM ET, The Energy Information Administration (EIA) will be providing its scheduled weekly information on petroleum inventories, whether produced in the US or abroad. The level of inventories helps determine prices for petroleum products.

• 2:00 PM ET, The FOMC Announcement is when the world gets to learn what the Fed decision is on interest rates, and why.

• 2:30 PM ET, The FOMC Chair press briefing provides additional context to the just announced direction of the FOMC’s policy decision. The questions and answers with the media can shed far more light of the intentions of the Committee than the carefully worded statement released at 2PM.

Thursday 6/15

• 8:30 AM ET, Jobless Claims for the June 10 week are expected to ease back to 250,000 versus the prior week’s large 28,000 jobs jump to 261,000. This has been a very closely watched report. If as expected, it would indicate the Fed has room to tighten further if other data remain strong.

• 8:30 AM ET, May Retail Sales are expected to be unchanged, matching April’s 0.4 percent rise.

• 8:30 PM ET, The Philadelphia Fed (Philly Fed) manufacturing index has been in contraction for the last ten reports. At minus 10.4 in May, with June’s consensus is at minus 13.2.

• 9:15 PM ET, Industrial Production is expected to push 0.1 percent higher in May after April’s 0.5 percent increase that was boosted by manufacturing output which jumped a surprising 1.0 percent. Manufacturing in May is seen up 0.2 percent.

• 4:30 PM ET, The Fed’s Balance Sheet is a weekly report presenting a consolidated balance sheet for all 12 Reserve Banks that lists factors supplying reserves into the banking system and factors absorbing reserves from the system. This has ben getting more attention as it indicates if the fed is on track with its announced quantitative tightening and if any bank borrowing has dramatically increased.

Friday 6/16

• 10:00 AM ET, Consumer Sentiment will be the first indication for June. It fell by 4.3 points to 59.2 last month, it is expected to inch up and report 60.5.

• Quadruple Witching is a phrase used to refer to the expiration of four different derivative contracts: Stock index futures, Stock index options, Single-stock options, Single-stock futures. Quadruple witching happens four times a year, on the third Friday of March, June, September, and December. It is a time of heightened volatility in the markets, as traders adjust their positions in anticipation of the expiration of these contracts.

What Else

The key factors that the Fed will consider when making its decision are the pace and trend of economic growth, the level of inflation, the strength of the labor market, and the risk of recession. Additionally, the FOMC will have to determine if the moves to date will have a more substantial impact if allowed to have more time to have an impact.

While OPEC is cutting output and it seems like we are on a path of oil and natural gas prices again inching up, Alvopetro Energy (ALVOF), an enviable gas company, headquartered in Canada, operating in Brazil, will be conducting roadshows in New York and St. Louis. Learn more about attending here. Paul Hoffman Managing Editor, Channelchek

This Week Will Feature Few Economic Releases and a Focus on Next Weeks FOMC

The week ahead is quiet on the economic release front. And there won’t be any market moving Fed president addresses to keep the market on its toes; the Fed members are in a blackout period leading up to next week’s June 13-14 FOMC meeting.

The markets can also stop talking about whether the US will default on debt as the short end of the fixed-income market will have to adjust to a sudden but short-lived increase in US Treasury bills.

Monday 6/5

10:00 AM ET, Factory Orders are expected to have risen 0.8 percent in April versus March’s 0.9 percent rise. Durable Goods Orders for April, which have already been released and are one of two major components of this report, rose 1.1 percent on the month. Factory Orders are a leading indicator, it represents the dollar level of new orders for both durable and nondurable goods.

10:00 AM ET, The Institute for Supply Management Services (ISM Services) is expected to be relatively steady at 52 for May after a 51.9 print in April.

Tuesday 6/6

Nothing Scheduled

Wednesday 6/7

8:30 PM ET, International Trade in Goods and Services is expected to show a deficit of $75.4 billion for April for total goods and services trade which would compare with a $64.2 billion deficit in March. Advance data on the goods side of April’s report showed a very large $12.1 billion deepening in the deficit.

10:30 AM ET, The Energy Information Administration (EIA) will be providing its scheduled weekly information on petroleum inventories, whether produced in the US or abroad. The level of inventories helps determine prices for petroleum products.

3:00 PM ET, Consumer Credit is expected to have increased by $21.0 billion in April versus an increase of $26.5 billion in March. This report has surprised on the high side the last three months.

Thursday 6/8

8:30 AM ET, Jobless claims for the week ending June 3 are expected to have increased to 240,000 versus 232,000 in the prior week. This has been a very closely watched report as it is expected it has indicated the Fed has room to tighten further if other data remain too strong.

10:00 AM ET, Wholesale Inventories will be released as a second estimate before the final. The second estimate for April is expected to be a 0.2 percent decline, unchanged from the first estimate. Wholesale trade measures the dollar value of sales made and inventories held by merchant wholesalers. It is a component of business sales and inventories Corporate Profits are pulled from the national income and product accounts (NIPA) and are presented in different forms.

4:30 PM ET, The Federal Reserve’s Balance Sheet has attracted additional attention as it is a good indicator of whether it is following its quantitative tightening plan, and whether there has been a significant change in banks looking to the Fed, which may mean trouble in the sector. For the week ending June 7, the Federal Reserve is expected to hold assets worth $8.386 trillion. This would be a week-on-week decline of $50.4 billion. All non-cash assets can be viewed as money that at one time was injected into the economy as stimulation.

Friday 6/9

10:00 AM ET, The Quarterly Services Survey focuses on information and technology-related service industries. These include information; professional, scientific and technical services; administrative & support services; and waste management and remediation services. Services revenue is expected to have increased by 2.9%.

What Else

The key factors that the Fed will consider when making their decision next week at the FOMC meeting are the pace and trend of economic growth, the level of inflation, the strength of the labor market, and the risk of recession.

Additionally, the FOMC will have to determine if the moves to date will have a more substantial impact over time. Currently, inflation is not coming down, jobs are abundant relative to job seekers, and the risk of a recession over the next two quarters seems low. For these reasons, some believe the Fed will remain hawkish yet pause for this meeting. However, next week during the first day of the two-day meeting CPI (consumer inflation) will be released. It would be premature to forecast a Fed decision until the contents of that report are known.