Vacations, Viruses, and Vantage Points

My ex-wife would not get on a plane. She was certain, if we flew, she would die. Together we found other ways to make the planet our playground — workarounds that might scare someone with alternative fears. We’d drive 1200 miles with no sleep, keeping pace with speeding 18-wheelers. Some weekends we’d bicycle the steep inclines in the Pennsylvania mountains. Summers we’d cruise for weeks at a time from as far north as Boston, to as far south as Cape May. On these vacations, she was completely at-ease, paying no mind to the statistical risk, road conditions, sea conditions, or impossibility of stopping a speeding bike while descending down a mountain. She didn’t perceive any of these workarounds as potentially deadly. She would not, however, get on a commercial aircraft, “too dangerous” for her.

Distortion of risk in one’s mode of travel is not unusual. As a person who models investment probabilities, I find this distortion of probabilities and others worth exploring. We are now halfway through 2020, a year marked by fear and panic surrounding the dangers of Covid-19. Measuring then categorizing the risk to health has been tricky; our increased understanding of the disease helps.

Covid-19 Concerns

The novel coronavirus that is the cause of this pandemic has been, for 130,000 Americans, deadly. So, awareness and precautions for individual safety and the well-being of others are prudent. But, the risk of the average person dying compared with the perceived danger may not match. After all, we deal with much deadlier diseases every day without immersing ourselves in concern. We live with the idea that cancer, diabetes, and heart disease each kill far more people a day than coronavirus. Even snakes kill 137 people a day. We are not up in arms clamoring to stay inside until we eradicate snakes. So why is the Covid-19 reaction so extreme? One answer is similar to fear of your plane crashing. When a plane does go down, the story is intensely reported by the media, traditional and social. This exposure causes the risks inherent in flight to feel very high and scary. We know by measuring actual cases that the danger of flight isn’t greater than being killed by, let’s say, the next mosquito we encounter. And yet, we don’t lock ourselves in our homes based on the death risk from mosquitos. Concern surrounding Covid-19 for some is that they will catch it and die. Others don’t want to be infected as they may spread it to someone else who may have a bad outcome. For others, the concern is that the danger or fear will dramatically alter their life, business, family, recreation, travel, etc. There are also people who fear that people they know are at great loss resulting from the reaction to perceived danger.

For now, the historically unprecedented lockdowns and economic sedation continue with very little argument. From discussions I have had, it seems that a significant portion of the population has come to believe that this coronavirus is one of the scariest things the human race has ever dealt with. It is definitely a little scary; it is, after all, it’s invisible, but is it dangerous? Could it be that a large portion of the population may be confusing “scary” with “dangerous.” They are not the same thing.

Covid-19 Dangers

There are four ways to categorize different realities. A situation can be:

- Scary, but not dangerous

- Scary and dangerous

- Dangerous, but not scary

- Not dangerous, not scary

COVID-19 continues to rank high in the scary category. I’m sure that the radio station I listen to is like many others throughout the country; it alerts me every 20 minutes of new cases. TV news, Facebook, and Twitter bombard us with relentless new case tallies without context. This magnified information, as with a single plane crash, impacts the population’s psyche. A Google search of the word “COVID-19” retrieves over 5.8 billion results. We’re surrounded by scary stories from those that are far too closer to home. To date, the virus has cut short the lives of a growing number of citizens. But is it very dangerous? On a scale of harmless to extremely dangerous, it would still fall into the category of slightly dangerous for by most definitions, (excluding the elderly and those with ill-health).

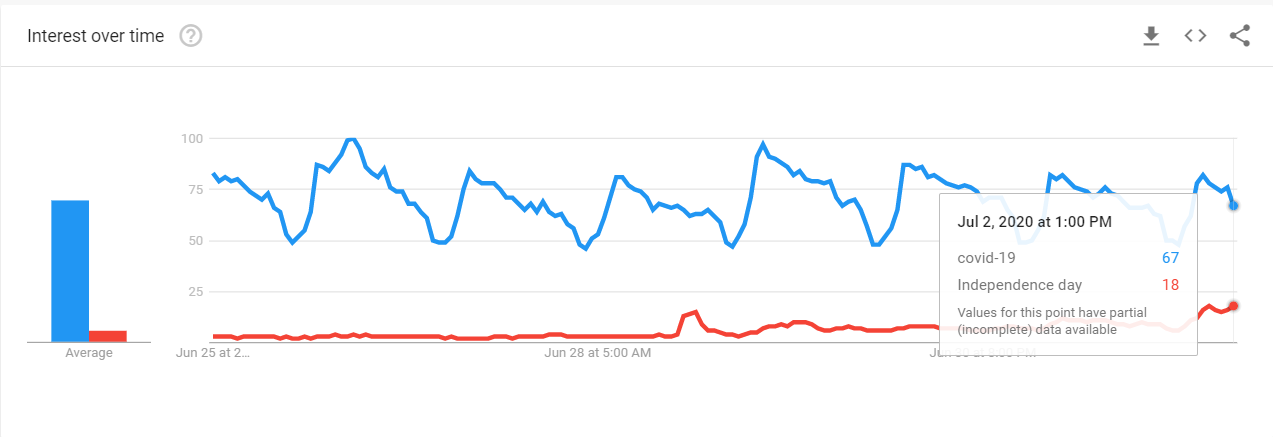

Google Trends

Approaching July 4th

weekend, Google Trends shows the term “Covid-19” being used 375% more than the

term “Independence Day.”

By comparison, there are more dangerous risks. Many give little thought to heart disease, which is the leading cause of death in the United States, killing around 650,000 people every year, 54,000 per month, and 324,000 people at the 2020 mid-year mark. This qualifies as extremely dangerous. Yet, most people are not very frightened at all.

Lives are improved for those that can distinguish between fear and danger. It doesn’t matter if it is fear of getting on a plane or boat or unwillingness to leave one’s house during this health situation. Fear is an emotion; it’s a perception of risk. As an emotion, the most important facts often don’t enter an individual’s calculation. Media hype blurs reality even more.

What if the top analysts at FICO adopted much stricter standards because they felt (emotionally) lending suddenly became much scarier, even if trends and other metrics they follow didn’t support the fear? This would impact the ability of borrowers to get loans, rates on loans, and the overall freedom of innocent people would change because a few people are scared, without supporting data. Imagine if an insurance actuary with a personal fear then grading the risk of something 1,000 times riskier than the measured data indicates. This would unnecessarily have a negative impact on the business and those seeking insurance. This is exactly what people have done regarding COVID-19: decisions based on fear and perception of danger even though data is now available.

Covid-19 Data

According to CDC data, 81% of deaths from COVID-19 in the United States are people over 65 years old, most with preexisting conditions. If 55-64-year-olds are added in, that number jumps to 93%. For those below age 55, preexisting conditions play a significant role, but the death rate is currently around 0.0022% or one death per 45,000 people in this age range. Below 25 years old, the COVID-19 fatality rate is 0.00008%, or roughly one in 1.25 million. Fear, not data, is impacting all industries and every aspect of life. For instance, the perceived danger is keeping schools and daycare centers closed. This makes it harder for mothers and fathers to remain employed and daycare centers to not close forever.

All human death is tragic. But are we allowing feeling scared to dictate decisions when it leads to taking resources away from areas that are more dangerous, but not as scary, and allocate them to areas that are scary, but less dangerous? At times, this is what is being done. Hospitals and medical practices have had to be very selective in the patients they treat; this is done to allow for beds, if needed, for Covid-19 patients, this has severely reduced surgical procedures. In the weeks following the first stat-at-home guidance, cervical cancer screenings were down 68%, cholesterol panels were down 67%, and diabetes blood sugar tests were off 65% nationally.

The U.N. estimates that infant mortality rates could rise by hundreds of thousands in 2020 because of the global recession and diverted health care resources. Add in opioid addiction, alcoholism, domestic violence, and other detrimental reactions from job loss and despair and the price of attributing excessive danger to the Covid-19 response can be viewed as unfortunate and even tragic.

Any benefits gained through this fear-based shutdown have massively increased dangers in both the short term and the long term. Every day that businesses are shuttered while people remain unemployed or underemployed, the economic wounds grow more deadly, and the scars more permanent. The loss of wealth is immense, and this will undermine the ability of nations around the world to deal with true dangers for decades to come.

Shutting down the private sector (which is where all wealth is maintained and created) is truly dangerous even though many of our leaders suggest we shouldn’t be scared to do it. Even stimulus plans are like a Band-Aid on a massive laceration, it may stop a tiny bit of the bleeding, but the wound continues to worsen, as it worsens, another inadequate Band-Aid is applied until you one day run out. Moreover, we are putting huge financial burdens on future generations because we are scared about something that the data reveal as far less dangerous than many other things in life. Putting this monstrous bill on the yet-to-be-born is an ethical decision that a country that stands against taxing the unrepresented should not take lightly.

Take-Away

Although there may be workarounds to the overblown fear that does not correlate to the risks in a given situation, unnecessary decisions compared to rational decisions are at best inefficient. A shutdown may change the pace of the spread of a virus, but it won’t stop it. A vaccine may immune us, an effective one may never be created. What then? In the meantime, we have entered a odd era, one in which fear overrides danger, and near-term risk creates long-term problems. More people are starting to come to this realization as the data builds. Hopefully, lessons are learned, and in the future, reality becomes the chief guide in steering decisions of this magnitude.

Paul Hoffman

Managing Editor

SuggestedReading:

Reconciling CoVID-19 with Statistics-101

Michael Burry Says Covid-19 Cure Worse than disease

Virtual Road Show Series – Channelchek

Enjoy Premium

Channelchek Content at No Cost

Sources:

Plane

Crash Fatalities

USCG

Boat Safety Statistics

How Safe is Commercial Flight

Cyclist Fatality Rate

Cancer Statistics

Coronavirus Death

Toll

How Many People Has Covid-19 Killed?

AHA Hospital Statistics