ELY Consolidates Railroad-Pinion Royalties in Nevada’s Carlin Trend

As of April 24, 2020, Noble Capital Markets research on Ely Gold Royalties is published under ticker symbols (ELYGF and ELY:CA). The price target is in USD and based on ticker symbol ELYGF. Research reports dated prior to April 24, 2020 may not follow these guidelines and could account for a variance in the price target. Ely Gold Royalties Inc is an emerging royalty company with producing and development assets focused in Nevada and the Western US. It offers shareholders a low-risk leverage to the current price of gold and low-cost access to long-term gold royalties.

Mark Reichman, Senior Research Analyst of Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

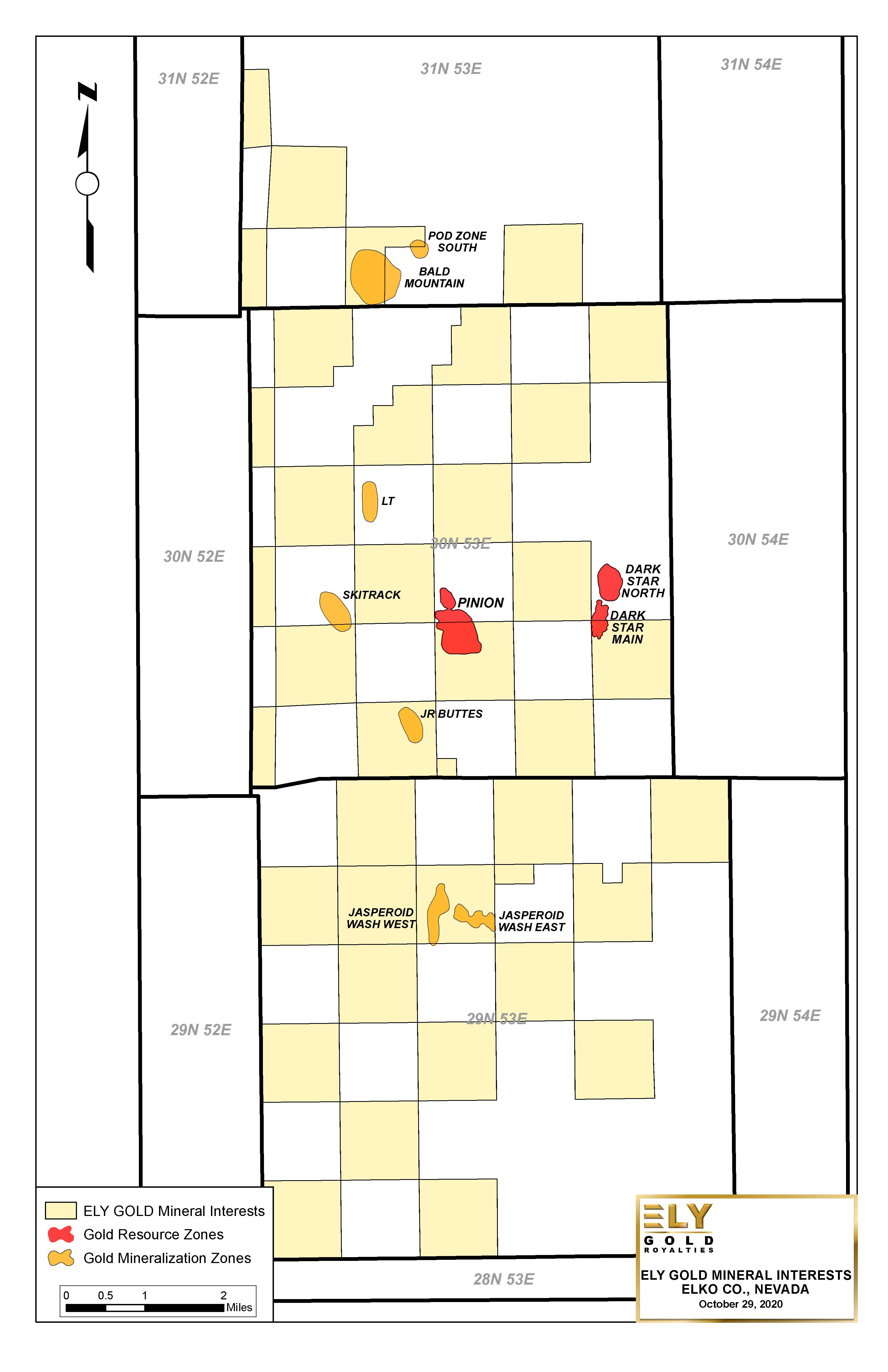

Near-term producing royalty acquisition. Ely Gold Royalties executed binding agreements with 12 private parties to acquire royalty interests covering a portion of the Railroad-Pinion project that is being developed by Gold Standard Ventures Corp. (NYSE American, GSV, Not Rated) as a heap-leach mining operation. The leases provide for an aggregate 1.15% net smelter returns royalty and annual lease payments of over $150 thousand. The mineral interests and leases cover large portions of the Dark Star, Pinion, and Jasperoid Wash deposits and portions of the POD and Bald Mountain zones.

Terms of the transaction. Ely will close the transaction in two tranches. Eleven of the transactions are expected to close on December 1, 2020, while one is subject to approval by the Toronto Venture Exchange. Ely Gold will pay total consideration of US$2,509,543 cash at closing and will separately pay US$1,300,000 cash consideration and issue 300,000 common stock warrants for the transaction …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

IPO finalize lending facility, announces small tuck-in acquisition, details 4Q cap spend

As of April 24, 2020, Noble Capital Markets research on InPlay Oil is published under ticker symbols (IPOOF and IPO:CA). The price target is in USD and based on ticker symbol IPOOF. Research reports dated prior to April 24, 2020 may not follow these guidelines and could account for a variance in the price target. InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQZ Exchange under the symbol IPOOF.

Michael Heim, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

InPlay entered into definitive agreements for a $25 million non-revolving four-year loan. IPO previously announced that it had come to terms on the low-interest loan. We believe the loan was a significant development for the company and will provide the liquidity needed to withstand low oil prices.

IPO makes a $1.9 million acquisition in the Pembina basin. The acquisition is small but a good positive indication of management’s interest in the area. The acquisition adds production (up 5%) and drilling acreage. Cost is reasonable and should add to cash flow at current energy prices …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Energy Fuels Produces First Rare Earth Element Concentrate on a Pilot Scale at its White Mesa Mill (Video Link Included)

LAKEWOOD, Colo., Nov. 3, 2020 /CNW/ – Energy Fuels Inc. (NYSE American: UUUU) (TSX: EFR) (“Energy Fuels” or the “Company”) is pleased to announce that the Company has produced a rare earth element (“REE”) carbonate concentrate (“REE Concentrate”) on a pilot scale at its 100% owned White Mesa Mill (the “Mill”), located near Blanding, Utah. This REE Concentrate was produced using existing infrastructure and technologies at the Mill from a sample of monazite sands from a North American source. Monazite sands are a valuable natural uranium ore, which also contain high concentrations of REEs. The Mill recovered the high concentrations of REEs in the monazite sands, in addition to the contained uranium which will be sold into the nuclear fuel industry. The REE Concentrate produced this weekend is of high purity and is ready to be sent to a separation plant and further downstream REE processing facility for final acceptance test work.

To the Company’s knowledge, this is the first REE Concentrate produced from monazite sands at any significant quantity in North America in over twenty (20) years.

Highlights:

The Company announced its plan to enter the REE Sector on April 13, 2020.

In just over six (6) months, the Company has graduated from laboratory scale testing to producing pilot scale REE Concentrate from a one (1) tonne sample of monazite sands mined in North America.

The Company possesses three (3) tonnes of additional samples of these monazite sands, which it intends to process in the next two months to further refine the process for recovering REEs and uranium from these types of ores.

This pilot scale testing demonstrates the substantial steps the Company has taken in recent months to re-establish the ability of the U.S. to recover REEs from monazite sands using existing facilities and technologies.

The Company continues negotiations with various parties to procure sources of monazite sands that can potentially be processed on a commercial scale at the Mill for the recovery of REE Concentrate and uranium.

The Company is also in ongoing discussions on the possible sale of REE Concentrate produced at the Mill to an REE separation facility.

Mark S. Chalmers, Energy Fuels’ President and CEO, stated:

“This past weekend, Energy Fuels achieved a major milestone in U.S. rare earth element production, when we successfully produced a REE Concentrate from a sample of monazite sands at our White Mesa Mill. Our Company literally accomplished REE production in months, because we utilized existing resources, infrastructure and technologies.

“While it is still early days, and we still have a lot of work to do, this is a proud moment, not just for me, but for the entire Energy Fuels team who has diligently worked on making REE Concentrate production a reality.

“The White Mesa Mill has a long history of recovering other metals along with uranium from uranium ores. Many of our ores from the Colorado Plateau contain vanadium, and the Mill has recovered over 54,000,000 pounds of vanadium as a co-product with uranium from these ores over the life of the Mill, making Energy Fuels the largest conventional vanadium producer in the U.S in recent years. Similarly, the Mill has recovered tantalum and niobium from uranium ores in the past. The recovery of REE Concentrate from monazite sands is no different in concept than the recovery of these other metals. As a result, the Mill is able to recover REEs along with uranium from these monazite sands using existing infrastructure and technologies at the Mill, with only minor routine process adjustments.

“This is the reason we believe we have the potential to enter commercial REE production more quickly and inexpensively than others. By using existing infrastructure and technologies at the Mill to recover the uranium and the REEs from monazite sands, we are able to avoid the years of permitting and development, along with the tens, or even hundreds, of millions of dollars of capital that others would be faced with. Assuming the Company is able to secure adequate quantities of monazite sands, we expect to be in a position to produce commercial quantities of REE Concentrate by early 2021.

“Successful testing at scale also demonstrates the importance of the White Mesa Mill in helping the U.S. re-establish its domestic REE supply chain. While the recovery and management of uranium and other radionuclides is a critical hurdle in REE production for most other facilities, it is a function the White Mesa Mill has performed successfully and responsibly for over 40 years.

We are particularly excited about the potential of our REE project in light of the President’s October 1, 2020 Executive Order on Critical Minerals, which declared a state of emergency to address America’s overreliance on critical minerals from foreign adversaries, including the REE’s, uranium and vanadium that we have the ability to produce at the White Mesa Mill. Furthermore, our work with the U.S. Department of Energy and Penn State on recovering REE’s from coal-based resources is complementary to the commercial REE initiatives discussed in this release.

“Energy Fuels will always, first and foremost, be a uranium producer. We have been the number one uranium miner in the U.S. since 2017, a position we intend to keep for many years to come. However, when other complementary business opportunities arise with the potential to create significant cash flow utilizing our existing facilities and workforce, we will always take a hard look at them with an eye toward building shareholder value.

“We look forward to providing further updates on our REE initiatives in the coming weeks and months as more milestones are reached.”

About Energy Fuels: Energy Fuels is the leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. The Company also produces vanadium from certain of its projects, as market conditions warrant, and is evaluating the potential to recover rare earth elements at its White Mesa Mill. Its corporate offices are near Denver, Colorado, and all of its assets and employees are in the United States. Energy Fuels holds three of America’s key uranium production centers – the White Mesa Mill in Utah, the Nichols Ranch in-situ recovery (“ISR”) Project in Wyoming, and the Alta Mesa ISR Project in Texas. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, and has the ability to produce vanadium when market conditions warrant. The Nichols Ranch ISR Project is on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Alta Mesa ISR Project is also on standby and has a licensed capacity of 1.5 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels has one of the largest NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Cautionary Note Regarding Forward-Looking Statements: This news release contains certain “Forward-Looking Information” and “Forward-Looking Statements” within the meaning of applicable United States and Canadian securities legislation, which may include, but are not limited to, statements with respect to: any expectation that the Company will maintain its position as the leading uranium producer in the United States; any expectation that being debt free will allow the Company to better weather market volatility, or allow the Company to increase uranium production when warranted or launch its rare earth element initiative; any expectation that the Company has a number of opportunities or catalysts in front of it which could result in significant cash flows for the Company; any expectation that the Administration and Congress may create a strategic U.S. uranium reserve, or that the Company may be one of the prime beneficiaries of any U.S. government support; any expectation that the recent actions of the U.S. Department of Commerce may reduce uranium and nuclear fuel imports into the U.S. from Russia over the long-term and eliminate the specter of more state-owned uranium imports entering the U.S.; any expectation that President Trump’s recent Executive Orders on critical minerals may be an important step toward the U.S. government providing tangible support and/or funding to producers and processors of critical minerals; any expectation that current spot and term uranium pricing cannot sustain new or existing primary supply; and any expectation that global uranium markets may continue their bounce-back. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans,” “expects,” “does not expect,” “is expected,” “is likely,” “budgets,” “scheduled,” “estimates,” “forecasts,” “intends,” “anticipates,” “does not anticipate,” or “believes,” or variations of such words and phrases, or state that certain actions, events or results “may,” “could,” “would,” “might” or “will be taken,” “occur,” “be achieved” or “have the potential to.” All statements herein, other than statements of historical fact, are considered to be forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance of or achievements of the Company to be materially different from any future results, performance, or achievements, express or implied, by the forward-looking statements. Factors that could cause actual results to differ materially from those anticipated in these forward-looking statements include risks associated with: any expectation that the Company will maintain its position as the leading uranium producer in the United States; any expectation that being debt free will allow the Company to better weather market volatility, or allow the Company to increase uranium production when warranted or launch its rare earth element initiative; any expectation that the Company has a number of opportunities or catalysts in front of it which could result in significant cash flows for the Company; any expectation that the Administration and Congress may create a strategic U.S. uranium reserve, or that the Company may be one of the prime beneficiaries of any U.S. government support; any expectation that the recent actions of the U.S. Department of Commerce may reduce uranium and nuclear fuel imports into the U.S. from Russia over the long-term and eliminate the specter of more state-owned uranium imports entering the U.S.; any expectation that President Trump’s recent Executive Orders on critical minerals may be an important step toward the U.S. government providing tangible support and/or funding to producers and processors of critical minerals; any expectation that current spot and term uranium pricing cannot sustain new or existing primary supply; any expectation that global uranium markets may continue their bounce-back; and the other factors described under the caption “Risk Factors” in the Company’s most recently filed Annual Report on Form 10-K, which is available for review on EDGAR at www.sec.gov/edgar.shtml, on SEDAR at www.sedar.com, and on the Company’s website at www.energyfuels.com. Forward-looking statements contained herein are made as of the date of this news release, and the Company disclaims, other than as required by law, any obligation to update any forward-looking statements whether as a result of new information, results, future events, circumstances, or as a result of changes in management’s estimates or opinions, or otherwise. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, the reader is cautioned not to place undue reliance on forward-looking statements. The Company assumes no obligation to update the information in this communication, except as otherwise required by law.

SOURCE: Energy Fuels Inc.

For further information: Energy Fuels Inc., Curtis Moore – VP – Marketing & Corporate Development, (303) 974-2140 or Toll free: (888) 864-2125, [email protected], www.energyfuels.com

Outlook Therapeutics Completes Patient Enrollment of Open-Label Safety Study for ONS-5010/LYTENAVA™ (bevacizumab-vikg)

Full enrollment of 195 subjects in NORSE THREE achieved in less than one month, significantly ahead of schedule

All planned clinical trials for ONS-5010/LYTENAVA™ BLA for wet AMD now fully enrolled or completed

Pivotal data expected in mid-2021 from ongoing, fully enrolled Phase 3 registration trial for ONS-5010 (NORSE TWO) with new BLA filing expected in second half of 2021

MONMOUTH JUNCTION, N.J., Nov. 03, 2020 (GLOBE NEWSWIRE) — Outlook Therapeutics, Inc. (Nasdaq: OTLK), a late clinical-stage biopharmaceutical company working to develop the first FDA-approved ophthalmic formulation of bevacizumab-vikg for use in retinal indications, today announced the completion of patient enrollment for its planned open-label safety study evaluating ONS-5010/LYTENAVA™ (NORSE THREE). Patient enrollment for the study was completed in less than one month, significantly ahead of the planned four-month enrollment schedule.

The open-label safety study enrolled 195 subjects with a range of retinal diseases for which an anti-VEGF drug is a therapeutic option, including wet age-related macular degeneration (AMD), diabetic macular edema (DME) and branch retinal vein occlusion (BRVO). Subjects enrolled in the study are receiving three monthly intravitreal (IVT) doses of ONS-5010/LYTENAVA™. The data from this study will be included in the complete data package to support the planned Biologics License Application (BLA) for wet AMD, on schedule for submission to the United States Food and Drug Administration (FDA) in the second half of 2021.

“I am delighted to see the enthusiasm for ONS-5010 that our clinical trial investigators have shown and their ability to rapidly enroll patients. The expedited manner in which enrollment was completed strengthens our confidence that an FDA-approved ophthalmic formulation of bevacizumab represents a significant unmet need in the ophthalmic community,” said Mark Humayun, MD, PhD, Medical Advisor to Outlook Therapeutics.

While unapproved repackaged IV bevacizumab from compounding pharmacies is already widely used in treating retinal diseases, ONS-5010, if approved, will be the first and only on-label ophthalmic formulation of bevacizumab-vikg for the treatment of wet AMD. It will offer a new, approved treatment option for wet-AMD, in the estimated $13 billion global market for anti-VEGF retina therapies.

“On behalf of the entire Outlook Therapeutics team, I would like to express our deep appreciation to the dedicated clinicians conducting this safety study as part of our ONS-5010 registration program,” added Lawrence Kenyon, President, CEO and CFO, Outlook Therapeutics. “The speed with which we completed enrollment in this safety study tells us a lot about the confidence of physicians and patients in ONS-5010. We believe that we remain well-positioned to file a new BLA for wet AMD as planned in 2021, now that all three of the planned clinical trials have either been completed or are fully enrolled.”

In addition to the planned BLA filing in the United States, Outlook Therapeutics is also engaged with regulatory authorities in Europe and other major markets for anticipated approvals in those markets. Outlook Therapeutics also intends to initiate registration clinical trials for ONS-5010 for DME and BRVO.

Commercial launch planning for ONS-5010, including distribution, physician and patient outreach, key opinion leader support and payor community engagement, remains ongoing. With an enhanced safety and cost-effectiveness profile, Outlook Therapeutics expects ONS-5010, if approved, to be widely adopted by payors and clinicians worldwide and to become the first-line drug of choice for payor-mandated “step edit” in the United States for retina indications. Outlook Therapeutics is also engaged with several life sciences companies that could result in a strategic partnership and definitive agreement for ONS-5010 as soon as the end of 2020.

About ONS-5010 / LYTENAVA™ (bevacizumab-vikg)

ONS-5010 / LYTENAVA™ (bevacizumab-vikg) is an investigational ophthalmic formulation of bevacizumab under development to be administered as an intravitreal injection for the treatment of wet AMD and other retinal diseases. Because no currently approved ophthalmic formulations of bevacizumab are available, clinicians wishing to treat retinal patients with bevacizumab have had to use unapproved repackaged IV bevacizumab provided by compounding pharmacists, products that have known risks of contamination and inconsistent potency and availability. If approved, ONS-5010 will reduce the need for use of unapproved repackaged IV bevacizumab from compounding pharmacists for retinal disease.

ONS-5010 is a full-length, humanized anti-VEGF (Vascular Endothelial Growth Factor) recombinant monoclonal antibody (or mAb) that inhibits VEGF and associated angiogenic activity. VEGF is a protein that promotes the growth of new abnormal blood vessels. With wet AMD, abnormally high levels of VEGF are secreted in the eye and lead to loss of vision. Anti-VEGF injection therapy blocks this growth. Since the advent of anti-VEGF therapy, it has become the standard-of-care treatment option within the retina community globally.

About Outlook Therapeutics, Inc.

Outlook Therapeutics is a late clinical-stage biopharmaceutical company working to develop ONS-5010/LYTENAVA™ (bevacizumab-vikg) as the first FDA-approved ophthalmic formulation of bevacizumab-vikg for use in retinal indications, including wet AMD, DME and BRVO. If ONS-5010 is approved, Outlook Therapeutics expects to commercialize it as the first and only FDA-approved ophthalmic formulation of bevacizumab-vikg for use in treating a range of retinal diseases in the United States, United Kingdom, Europe, Japan and other markets. Outlook Therapeutics expects to file ONS-5010 with the U.S. FDA as a new BLA under the PHSA 351(a) regulatory pathway, initially for wet AMD. For more information, please visit www.outlooktherapeutics.com.

Forward-Looking Statements

This press release contains forward-looking statements. All statements other than statements of historical facts are “forward-looking statements,” including those relating to future events. In some cases, you can identify forward-looking statements by terminology such as “expect,” “will,” “could,” “may,” “might,” “should,” “plan,” “anticipate,” “project,” “believe,” “estimate,” “predict,” “potential,” “intend” or “continue,” the negative of terms like these or other comparable terminology, and other words or terms of similar meaning. These include statements about the timing of completion of, and pivotal safety and efficacy data from, the pivotal Phase 3 trial, the timing of BLA submission, sufficiency of exposures and clinical trials conducted to support such submission, ONS-5010’s potential as the first FDA-approved ophthalmic formulation of bevacizumab-vikg, including benefits therefrom to patients, payors and physicians, statements about commercial launch of ONS-5010, the timing of entry into a strategic partnership and definitive agreement with a global ophthalmic company, including its ability to do so, and plans for regulatory approvals in other markets. Although Outlook Therapeutics believes that it has a reasonable basis for the forward-looking statements contained herein, they are based on current expectations about future events affecting Outlook Therapeutics and are subject to risks, uncertainties and factors relating to its operations and business environment, all of which are difficult to predict and many of which are beyond its control. These risk factors include those risks associated with developing pharmaceutical product candidates, risks of conducting clinical trials, risks in obtaining necessary regulatory approvals, and risks of negotiating strategic partnership agreements, as well as those risks detailed in Outlook Therapeutics’ filings with the Securities and Exchange Commission, which include the uncertainty of future impacts related to the ongoing COVID-19 pandemic. These risks may cause actual results to differ materially from those expressed or implied by forward-looking statements in this press release. All forward-looking statements included in this press release are expressly qualified in their entirety by the foregoing cautionary statements. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Outlook Therapeutics does not undertake any obligation to update, amend or clarify these forward-looking statements whether as a result of new information, future events or otherwise, except as may be required under applicable securities law.

CONTACTS:

Media Inquiries: Harriet Ullman Assistant Vice President LaVoieHealthScience

Modestly Wider Loss Than Expected; Webcast on November 3

As of April 24, 2020, Noble Capital Markets research on Energy Fuels is published under ticker symbols (UUUU and EFR:CA). The price target is in USD and based on ticker symbol UUUU. Research reports dated prior to April 24, 2020 may not follow these guidelines and could account for a variance in the price target.

Energy Fuels is the largest uranium producer in the U.S. and holds more production capacity and uranium resources than any other U.S. producer. The Company also produces vanadium. Headquartered in Colorado, Energy Fuels holds three of America’s key uranium production centers: the White Mesa Mill in Utah, the Nichols Ranch ISR Facility in Wyoming, and the Alta Mesa ISR Facility in Texas. The producing White Mesa Mill is the only conventional uranium mill in the U.S. and has a licensed capacity of 8 million pounds of U3O8 per year. Nichols Ranch is in production and has a licensed capacity of 2 million pounds of U3O8 per year. Alta Mesa is currently on standby. Energy Fuels also owns several licensed and developed uranium and vanadium mines on standby and other projects in development.

Mark Reichman, Senior Research Analyst of Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third quarter 2020 results. UUUU reported a 3Q loss of $8.9 million, or $(0.08) per share, compared to a loss of $6.9 million, or $(0.07) during the prior year period and our estimate of a loss of $6.9 million, or $(0.06) per share. The variance to our estimate was largely due to lower revenue and higher standby costs. The company had no sales of uranium or vanadium and all revenue was generated from processing ore received from a third-party uranium mine. Energy Fuels will host a webcast on Tuesday, November 3 at 4:00 pm ET to discuss quarterly results and give an update on the company’s plans and outlook.

Updating estimates. We have revised our 2020 estimate to a loss of $(0.28) per share from $(0.25) to reflect 3Q results and lower revenue. It is difficult to forecast forward earnings given a range of outcomes based on potential actions arising from the U.S. Nuclear Fuel Working Group (NFWG) recommendations, including potential government purchases of uranium for a reserve, which could have a …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Introducing 2021 EBITDA Estimate and Raising Price Target

Orion Group Holdings, based in Houston, Texas, is a specialty construction company within the Marine and Industrial Construction sectors, with operations focused in the continental United States and Caribbean. Revenue is split roughly 50/50 between a Marine Construction segment that provides marine facility, pipeline and structural construction services and a Commercial Concrete segment that provides turnkey concrete services in the light commercial and structural construction markets.

Poe Fratt, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

We were looking for color on the 3Q2020 call in several key areas and there were some noteworthy items discussed. Please see page two for details.

4Q2020 EBITDA guidance of $10-$12 million in line with expectations. Fine-tuning 2020 EBITDA estimate of $52.3 million and introducing 2021 EBITDA estimate of $52.3 million. Flat outlook, but profitability remains strong. Looking for free operating cash flow of $30.5 million ($1.01/share) in 2020 and $15.3 million ($0.50/share) in 2021. Positive free cash flow is driving leverage down, and …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

District Scale Property Currently Being Developed by Gold Standard Ventures

Vancouver, British Columbia, Canada, November 2, 2020. Ely Gold Royalties Inc. (TSXV:ELY, OTCQX:ELYGF) (“Ely Gold” or the “Company”) has reached binding agreements with twelve separate individuals to purchase private mineral interests on over 8,000 acres of private fee ground in Elko County, Nevada (the “Mineral Interests”). All of the fee ground and the Mineral Interests are currently leased to Gold Standard Ventures Corp (NYSE AMERICAN: GSV, TSX: GSV) (“GSV”) and cover certain portions of GSV’s Railroad-Pinion Project that is currently being developed as a heap-leach mining operation (the “Leases”). The Leases provide for a combined 1.15% net smelter returns royalty (“NSR”) and annual lease payments of over $150,000. The Mineral Interests and Leases cover large portions of the Dark Star, Pinion and Jasperoid Wash deposits in the South Railroad Complex as well as portions of the POD and Bald Mountain zones in the North Railroad. (see Figure 1). Eleven of the transactions (the “ORTT Transactions”) are expected to close on December 1, 2020 (the “Closing”). One of Transactions (the “OR Transaction”) is subject to the approval of the Toronto Venture Exchange (“TSXV”).

The Transactions

Ely Gold will pay total consideration of US$2,509,543 cash at Closing (the “Cash Consideration”) for the ORTT Transactions. In addition, Ely Gold will pay US$1,300,000 Cash Consideration and issue 300,000 common stock warrants (the “Ely Warrants”) for the OR Transaction. The Ely Warrants have a five-year term and will have an exercise price of CDN$1.15. Securities issued under the Ely Warrants will be subject to a four-month hold period. In connection with its assistance with both transactions, Ely Gold has agreed to pay a cash finder’s fee to R&R Land, Mineral & Oil LLC totaling US$207,273. Closing of both transactions is subject to final due diligence by the Company.

Trey Wasser, President & CEO of Ely Gold commented, “Ely Gold has successfully consolidated another complex transaction resulting in a meaningful royalty position on one of Nevada’s next mine developments. Not only do these Leases cover approximately 35% of the total resources at South Railroad, they also cover most of GSV’s 2020 expansion drilling at Dark Star, Pinion and Jasperoid Wash.”

Railroad-Pinion

The Railroad-Pinion Project is an intermediate to advanced stage gold project with a favorable structural, geological and stratigraphic setting situated at the southeast end of the Carlin Trend of north-central Nevada, adjacent to and south of Nevada Gold Mines’ Rain Mining District. The Carlin Trend is a northwest alignment of sedimentary rock-hosted gold deposits with past production exceeding 80,000,000 ounces of gold. Each dome or “window” is cored by igneous intrusions that uplift and expose Paleozoic rocks and certain stratigraphic contacts that are favorable for formation of Carlin-style gold deposits. The Railroad-Pinion Project is centered on the fourth and southernmost dome-shaped window on the Carlin Trend.

On February 18, 2020, Gold Standard announced an updated Pre-Feasibility Study for The South Railroad portion of the Railroad-Pinion project consisting of the Dark Star deposit and the Pinion Deposit. Key Highlights of the Updated Base Case South Railroad PFS include: (all currencies are shown in US dollars):

Pre-tax net present value (“NPV”) of $331.4M at a 5% discount rate and an after tax NPV of $265.0M at a $1,400 gold price and a $17.11 silver price, with a mineral reserve pit designs based on a gold price $1,250 per ounce and a silver price of $15.30 per ounce.

Proven and probable mineral reserves of 1.246 million ounces of gold and 2.705 million ounces of silver.

Average annual gold placement of 156,000 ounces of gold per year over an initial 8-year mine life.

Average life of mine cash cost of $582 per ounce after by-product credit, and all in sustaining costs (“AISC”) of $707 per ounce.

In a press release dated July 16, 2020 GSV announced that they had entered into a binding letter of intent with Orion Mine Finance relating to a series of transactions, totaling approximately US$22.5 million. Orion also agreed to provide GSV with a term sheet to provide up to US$200 million of financing support to GSV, following the satisfaction of mutually agreed milestones, to help finance the construction of the South Railroad Project.

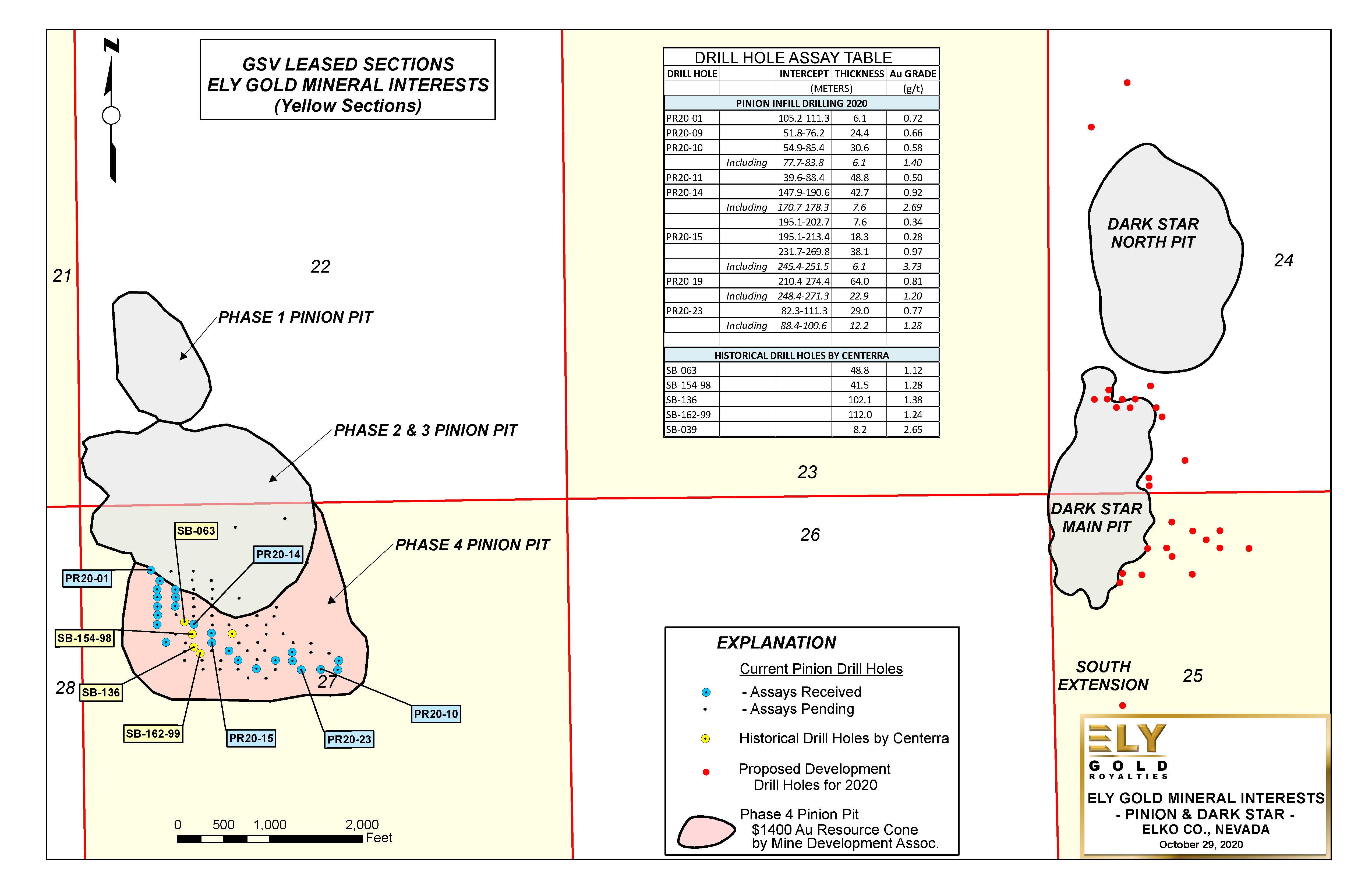

GSV recently announced encouraging drill results from 24 of 75 holes in the 2020 Pinion deposit development program. Oxide results include 42.7m of 0.92 g Au/t, including 7.6m of 2.69 g Au/t in hole PR20-14; 38.1m of 0.97 g Au/t in PR20-15; 64.0m of 0.81 g Au/t, including 22.9m of 1.20 g Au/t in hole PR20-19; and 29.0m of 0.77 g Au/t, including 12.2m of 1.28 g Au/t in PR20-23.Objectives of the 2020 Pinion development program include: 1) decreasing drill spacing on the Pinion Phase 4 ($1400 pit) inferred oxide resource for potential conversion to Measured and Indicated; 2) provide material for metallurgical testing; and 3) tighten the drill spacings near historic Cameco holes SB-136, a RC hole that intersected 102.1m of 1.38 g Au/t, and SB-162-99, a core hole that twinned and verified the SB-136 results with an intercept of 112.0m of 1.24 g Au/t. (see GSV press release dated October 20, 2020)

All 75 of the drill holes in the 2020 Pinion development program are on the Mineral Interests being purchased by Ely Gold. (see Figure 2)

Mineral Interests & Leased Claims

Figure 1

GSV Expansion Drilling

Figure 2

Qualified Person

Stephen Kenwood, P. Geo, is director of the Company and a Qualified Person as defined by NI 43-101. Mr. Kenwood has reviewed and approved the technical information in this press release.

About Ely Gold Royalties Inc.

Ely Gold Royalties Inc. is a Nevada focused gold royalty company. Its current portfolio includes royalties at Jerritt Canyon, Goldstrike and Marigold, three of Nevada’s largest gold mines, as well as the Fenelon mine in Quebec, operated by Wallbridge Mining. The Company continues to actively seek opportunities to purchase producing or near-term producing royalties. Ely Gold also generates development royalties through property sales on projects that are located at or near producing mines. Management believes that due to the Company’s ability to locate and purchase third-party royalties, its strategy of organically creating royalties and its gold focus, Ely Gold offers shareholders a favourable leverage to gold prices and low-cost access to long-term gold royalties in safe mining jurisdictions.

On Behalf of the Board of Directors Signed “Trey Wasser” Trey Wasser, President & CEO

FORWARD-LOOKING CAUTIONS: This press release contains certain “forward-looking statements” within the meaning of Canadian securities legislation, including, but not limited to, statements regarding completion of the Transaction. Forwardlooking statements are statements that are not historical facts; they are generally, but not always, identified by the words “expects,” “plans,” “anticipates,” “believes,” “intends,” “estimates,” “projects,” “aims,” “potential,” “goal,” “objective,” “prospective,” and similar expressions, or that events or conditions “will,” “would,” “may,” “can,” “could” or “should” occur, or are those statements, which, by their nature, refer to future events. The Company cautions that forward-looking statements are based on the beliefs, estimates and opinions of the Company’s management on the date the statements are made and they involve a number of risks and uncertainties. Consequently, there can be no assurances that such statements will prove to be accurate and actual results and future events could differ materially from those anticipated in such statements. Except to the extent required by applicable securities laws and the policies of the TSX Venture Exchange, the Company undertakes no obligation to update these forward-looking statements if management’s beliefs, estimates or opinions, or other factors, should change. Factors that could cause future results to differ materially from those anticipated in these forward-looking statements include the Company’s inability to control whether the buy-down right will ever be exercised, and whether the right of first refusal will ever be triggered, uncertainty as to whether any mining will occur on the property covered by the Probe Royalty such that the Company will receive any payment therefrom, and the general risks and uncertainties relating to the mineral exploration, development and production business. The reader is urged to refer to the Company’s reports, publicly available through the Canadian Securities Administrators’ System for Electronic Document Analysis and Retrieval (SEDAR) at www.sedar.com for a more complete discussion of such risk factors and their potential effect.

Neither the TSX Venture Exchange nor its Regulation Services Provider accepts responsibility for the adequacy or accuracy of this release.

What Investors Should Consider Before Investing in the Esports Industry

Stocks of esports companies are benefitting from rising investor attention. The dramatic growth of esports as a spectator sport, entertainment, and even a gaming outlet makes the attention they’re getting justified.

Recent statistics on electronic sports (sometimes written e-sports or esports) show the events attract more than 500 million viewers worldwide. For those less familiar, esports is defined as organized video gaming. The games may consist of individual or multiplayer teams. Participants train and compete against other players or teams in an organized contest under standard agreed upon rules. The competitions attract large audiences both at the venue and across social media sites such as Twitch.tv. A reported 1.8 billion hours of esports, were watched in 2019, this is a 125% increase from hours reported the previous year. The trend has been positively impacted by the closure of traditional gambling outlets and sports in 2020.

Like any fledgling market with fast-growing revenue, there’s a rush of companies vying for a slice. Coverage of other people playing video games has demonstrated that it has tremendous and growing pull and is able to find an increasing number of followers —the audience is expanding rapidly and appears to have far more potential to the upside.

How Do Esports Profit?

Esports companies are primarily licensing companies, they sell access to branded events similar to other sports business models. This could include broadcast licensing deals, merchandise, live-event tickets, sponsorships, advertising, and clothing. Companies have also sold rights to operate esports teams and officiate organized leagues.

As with many young industries gaining popularity, there is only so much room at the top. So, although this segment within sports entertainment is growing, investor evaluation of the individual companies and their prospects is highly recommended.

What to Look For

When evaluating if esports is a fit for your portfolio and what stock or stocks provide the best risk/return opportunity, start with the basics you look for in other industries and companies.

Measure trends – Data for a number of esports companies including GMBL, GAME:CA, MLLLF, and others can be found under the COMPANY Data section in Channelchek. This could serve as a good place to find key ratios, charts, insider activity, and other statistical trends.

Company strength relative to peers – Every company has advantages and disadvantages relative to the others. Brand recognition, contractual agreements, unsettled legal disputes, and sheer size, to name a few. Learn about the competing companies. This is especially important when a market segment is new and the future looks positive for the segment — there is always a swarm of companies elbowing their way in. There are usually fewer over time as survivors benefit from outcompeting other entrants. Familiarize yourself with the companies you may be interested in by catching up with the news on the tickers. The COMPANY Data section of Channelchek is also a source for news feeds on many of the stocks.

Management Effectiveness – Most investors don’t have the luxury of sitting down with management and understanding the merits of their strategy and ability to implement. Detailed information can still be garnered from the explosion of online conferences and roadshows, many of these can be accessed on “replay” on YouTube and other video sites. Professional research should not be overlooked when evaluating management. Up-to-date research and analysis by FINRA licensed analysts can be invaluable for understanding management and the well-being of a particular company. If research isn’t available on all the companies you’re comparing, it helps to read reports that are available to best understand what a Wall Street professional looks for in this segment. A current example is Esports Entertainment Group (GMBL) covered by Noble Capital Markets.

Take-Away

The popularity of watching online and in-person (most venue events are on hiatus due to COVID-19) professionals play video games is on the rise. This segment of the sports licensing, gaming, and broadcasting industry is in its infancy and yet to be fully defined. Infancy is when the potential for reward is usually greatest, but at the same time risk of loss can also be high. Know as much as you can before deciding to be involved and in which companies. Read what true research analysts think, predictions on where the segment is headed vary greatly. However, most expectations point to increased popularity and acceptance. Esports and gaming video content already have a large audience, the opportunity to further expand into more mainstream acceptance and becoming even more lucrative while other sports entertainment is struggling, make it an interesting business to evaluate, and perhaps weave into a diverse portfolio.

Each event in our popular Virtual Road Shows Series has a maximum capacity of 100 investors online. To take part, listen to and perhaps get your questions answered, see which virtual investor meeting intrigues you here.

Another Solid Quarter in the Face of Covid Challenges

With over 94,000 beds owned, leased or managed across its business lines and serving over 260,000 people daily, GEO is a leading provider of mission critical real estate to its governmental partners. The Company is the first fully integrated equity REIT specializing in the design, financing, development, and operation of secure facilities, processing centers, and community reentry centers in the U.S., Australia, South Africa, and the U.K.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q20 Results. GEO reported third quarter revenue of $579.1 million, EPS of $0.33, and AFFO of $0.67 per share. In the same period last year, the Company reported revenue of $631.6 million, EPS of $0.39, and AFFO of $0.72. While above management expectations, results continue to be negatively impacted by the COVID crisis, which reduced populations and increased costs. We had estimated revenue of $580 million, EPS of $0.27, and AFFO of $0.60.

New Awards. In spite of COVID and political rhetoric, GEO continues to receive new awards. Interestingly, the BoP reversed its stance to close the D. Ray James facility by the end of September and instead entered into a four month extension with GEO. The USMS is taking over the Eagle Pass facility. An ICE annex was activated in the third quarter, another will be activated in the fourth and …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Momentum Continues to Build; Exceeds 3Q Consensus Estimates

Kratos Defense & Security Solutions is a National Security technology provider with proprietary expertise in the area of unmanned aerial vehicles, electronics for missile defense systems, electronic warfare systems, satellite control and management systems and support services for emerging naval weapon systems. Commercial and state and local government revenues are about 25% of the total and comprise primarily of critical infrastructure monitoring and protection systems.

Joe Gomes, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q20 Results. Revenue of $202 million and adjusted EPS of $0.14 topped consensus estimates of $199.7 million and $0.09, respectively. We had projected $205 million and $0.07, respectively. In the third quarter last year, KTOS reported revenue of $184.1 million and adjusted EPS of $0.13. Adjusted EBITDA came in at $24.6 million, up 20.6% y-o-y. Revenues were in the middle of management’s guidance range while adjusted EBITDA exceeded the $17-$20 million guide.

Program Momentum. As we have outlined in previous reports, Kratos continues to pick up momentum among a number of programs. Key highlights in the quarter include going to full rate production on the BQM-177A Subsonic Aerial Target for the U.S. Navy, securing a contract to support the U.S. Air Force’s Ground Based Strategic Deterrent (GBSD) program as part of the team led by Northrop Grumman, and …

This research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Another Quarter Of Enhanced Growth; Raising Target

1-800-FLOWERS.COM, Inc. is the leading provider of gourmet and floral gifts for all occasions. For nearly 40 years, 1-800-FLOWERS® has been helping deliver smiles for customers with gifts for every occasion, including fresh flowers, premium, gift-quality fruits, and other gourmet items from Harry & David®, popcorn and specialty treats from The Popcorn Factory®; cookies and baked gifts from Cheryl’s®; premium chocolates and confections from Fannie May®; gift baskets and towers from 1-800-Baskets.com®; premium English muffins and other breakfast treats from Wolferman’s; carved fresh fruit arrangements from FruitBouquets.com; and top quality steaks and chops from Stock Yards®. The Company’s BloomNet® international floral wire service provides a broad range of quality products and value-added services designed to help professional florists grow their businesses profitably.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Exceeds Q1 expectations. Fiscal Q1 end September 30 revenues increased a strong 51.6% to $283.9 million, above our $263.4 million expectation. The largest upside revenue variance was in its consumer floral division. The company continues to enjoy enhanced revenue growth due to strong ecommerce sales. Adjusted EBITDA from continuing operations was better than expected, $3.2 million versus our estimate of $0.2 million.

Strong consumer floral and ecommerce. Ecommerce revenues increased a strong 85.1% in the quarter, with 1800Flowers’ consumer floral brand increasing revenues 55%. We believe that the company expanded its market leading position in the space. Certainly revenue growth is sequentially decelerating from the extraordinary impact that the Covid pandemic has had on its ecommerce business …

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Zoomtowns: Your Vacation Getaway May Become Your New Home

Are home offices moving to even more remote locations? Everyone is aware that the pandemic has changed the way people work and live. Workers spend less time commuting to a central work place, and video meetings, often Zoom meetings, have replaced conference room meetings. People who didn’t know what Zoom was in 2019 have now become proficient in its operations. It would be easy to think that the shift is temporary, and things will go back to normal once the pandemic passes. This may not be the case. Management of companies has learned that employees can be just as effective (in many cases more effective) working from home. While Zoom type meetings will never replace face-to-face meetings entirely, it’s very probable that many businesses will permanently become a combination of an in-office and work-from-home operation.

Adjusting

Employees have already begun adjusting to the change. If they are going to work from home, they want a high functioning home office setting. Working from the kitchen table may have been fine to finish up a late-night report, but it won’t work for an important teleconference meeting. People want offices with doors they can close to assure some level of privacy. The result has been a run on home office furniture and equipment. Forget paper towels. The new work-at-home employee wants a printer!

The new household are adding more entertainment options since restaurants, movies, theaters, and concerts are limited. It is easier to justify that extra cable or internet channel when less is being spent on other restorative activities. Games and puzzles have become popular again. The same can be said about exercise equipment. There are currently long wait times for trying to buy a treadmill to be delivered to their house. Bikes, roller skates and skateboards are in high demand. People are cooking more, shopping for specific pots and pans is uncovering shortages.

The pandemic is not only changing how people live within their home, it’s changing their home. People are adding additions, putting in swimming pools and spending money on landscaping. Existing and new home sales are soaring as people move to bigger, nicer homes. New homes are being built farther and farther away from urban centers as they commute less. Vacation homes are becoming more popular. People want to live in areas with nicer views. “Zoomtowns” near lakes and rivers or golf courses or mountains are exploding.

Zoomtowns

If you are not familiar with the term Zoomtown, be prepared to see it more often. NPR’s Planet Money defines Zoomtowns as housing markets that are booming as remote work takes off. Zoomtowns are spreading not only because of a decrease in commuting but also a decrease in entertainment venues associated with urban living. To quote Forbes, “your vacation getaway may be your next home.” People want more space because of the virus and that means getting away from crowded cities.

A paper published in the Journal of the American Planning Association shows that Zoomtown populations were already growing before COVID-19 hit. The study identified 1,522 small towns that were withing 10 miles of a national park, monument, forest, lake, or river, and at least 15 miles from a census-designated area. It then compared the growth rate of these towns versus the national average. The popularity of Zoomtowns most likely reflects an increase in disposable income for the wealthy following the rise in the market, a tax decrease and sustained low interest rates.

The sudden boom in zoomtowns comes with the usual growing pains. Healthcare options are ill equipped to handle a larger, older population. Restaurants become overrun and stores providing necessities are rare. Staff is limited and often migratory. There is a lack of inexpensive housing for workers. Jonathan Thompson, a contributor to Writers on the Range, refers to the wave of urban workers moving to Zoomtowns as COVID migrants. Costs are rising quickly. As the exodus to Zoomtowns spreads, the towns are becoming denser, threatening the very reason people moved to these locations in the first place. That will only raise the value of undeveloped areas near natural beauty that could become the next Zoomtown.

Investment Play?

Investors can play the growing popularity of Zoomtowns in many ways. There will be increased need for cellular and internet services. Recreational equipment associated with water or golf courses will become more popular. General stores focused on rural areas should do well. Rural construction companies will see increased business. And of course, the Zoomtown could not exist without media companies like Zoom, Cisco Webex, GoToMeeting, Google Hangouts, etc.

Each event in our popular Virtual Road Shows Series has a maximum capacity of 100 investors online. To take part, listen to and perhaps get your questions answered, see which virtual investor meeting intrigues you here.

Each event in our popular Virtual Road Shows Series has a maximum capacity of 100 investors online. To take part, listen to and perhaps get your questions answered, see which virtual investor meeting intrigues you

Each event in our popular Virtual Road Shows Series has a maximum capacity of 100 investors online. To take part, listen to and perhaps get your questions answered, see which virtual investor meeting intrigues you