Sierra Metals Reports Record Adjusted Ebitda Of $37.2 Million, A 73% Increase Over Q3 2019, As Part Of Its Strong Q3 2020 Consolidated Financial Results

Conference Call November 9, 2020 at 11:00 AM (EST)

- Revenue from metals payable of $73.2 million in Q3 2020 increased 13% from $64.6 million in Q3 2019 due to higher throughput and metal production from all three mines

- Adjusted EBITDA of $37.2 million in Q3 2020 increased 73% from $21.6 million in Q3 2019, primarily due to increased revenues realized and a decrease in operating costs at all three mines

- Operating cash flows before movements in working capital of $37.9 million in Q3 2020 increased from $21.8 million in Q3 2019

- Q3 2020 consolidated copper production of 12.2 million pounds, consolidated silver production of 1.0 million ounces, consolidated gold production of 3,989 ounces, consolidated zinc production of 24.9 million pounds, and consolidated lead production of 9.9 million pounds; a 9% increase, 5% increase, 14% increase, 11% increase, and a 6% decrease respectively, compared to Q3 2019. Management expects to meet the revised annual production guidance issued on August 13, 2020, precluding any further COVID-19 interruptions to operations

- Q3 2020 revenues as a percentage of metals sold represent 37% from copper, 25% from silver, 20% from zinc, 9% from lead and 8% from gold

- Record quarterly ore throughput and copper and gold production at the Bolivar Mine in Mexico; Record quarterly silver production at the Cusi Mine in Mexico, despite being in care and maintenance for part of the quarter

- $63.8 million of cash and cash equivalents as at September 30, 2020

- $62.9 million of working capital as at September 30, 2020

- Revised 2020 Financial Guidance Issued

- A shareholder conference call to be held Monday, November 9, 2020, at 11:00 AM (EST)

TORONTO–(BUSINESS WIRE)– Sierra Metals Inc. (TSX: SMT) (BVL: SMT) (NYSE AMERICAN: SMTS) (“Sierra Metals” or “the Company”) today reported revenue of $73.2 million and adjusted EBITDA of $37.2 million on the throughput of 798,458 tonnes and metal production of 35.2 million copper equivalent pounds, or 4.2 million silver equivalent ounces, for the three month period ended September 30, 2020.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20201109005310/en/

The Company achieved record quarterly consolidated equivalent copper production and ore throughput, driven by a strong operational performance at its three mines despite the difficulties arising from the COVID-19 pandemic. Consolidated production of copper equivalent pounds increased 9% to 35.2 million pounds.

The Company earned revenues of $73.2 million, Adjusted EBITDA of $37.2 million, and operating cash flows before movements in working capital of $37.9 million. Higher revenues are primarily attributable to the 24% increase in throughput, in addition to higher gold head grades and higher recoveries at Bolivar, as well as increased head grades and recoveries, except silver recoveries at Cusi. Quarterly revenues were also boosted by the higher realized prices for all metals.

Quarterly revenues at Yauricocha were in line with the third quarter of 2019, as lower metal sales and increased treatment and refining charges offset the impact of higher metal prices. The Yauricocha Mine processed 318,155 tonnes during Q3 2020, representing a 4% increase compared to Q3 2019. Daily ore throughput averaged 3,636 tpd during the quarter, as the mine continued its efforts to recover some of its annual production lost due to the COVID-19 related shutdown in Peru. Grades for all metals except zinc were lower for the quarter due to a lower proportion of ore coming from the high-grade small ore bodies compared to the third quarter of 2019. Zinc grades were higher during the third quarter of 2020 due to mining in the Cachi Cachi area. However, recoveries were negatively affected by lower head grades and slightly reduced residence capacity in the flotation process, as a result of higher throughput.

The Bolivar Mine processed a quarterly record of 410,468 tonnes in Q3 2020, representing a 24% increase over Q3 2019. The average daily ore throughput realized during the quarter was approximately 4,691 tpd, and the Company remains on track to reach the targeted 5,000 tpd during Q4 2020. The 24% increase in throughput, higher gold head grades and higher recoveries partially offset by lower silver grades resulted in a 37% increase in copper equivalent pounds produced during Q3 2020 compared to Q3 2019.

The Cusi mine produced a record of 304,000 ounces of silver during the quarter, despite being in care and maintenance for part of the quarter. The mine resumed operations on July 28, 2020 and operated for 65 days during the quarter. Ore throughput reached approximately 1,074 tpd during Q3 2020, which was 33% higher than the throughput rate achieved in Q3 2019. The mine continues to work towards reaching full capacity during Q4 2020. Total quarterly throughput was 69,835 tonnes, which was 1% below the Q3 2019 throughput due to a lower number of operating days in Q3 2020. Higher silver and gold grades and higher gold recoveries were partially offset by 5% lower silver recoveries during Q3 2020, resulting in a 12% increase in silver equivalent ounces produced, despite slightly lower throughput.

Luis Marchese, CEO of Sierra Metals, commented,

“I am very pleased with the solid financial and production results achieved in the third quarter. We have continued to improve production rates at Bolivar and Cusi and continued to recover annual production tonnage lost at Yauricocha due to the COVID-19 pandemic. The robust production in the third quarter, along with improved operational efficiencies and improved metal prices, has resulted in record adjusted EBITDA for the Company. We also reported strong cash flow and net income. The Company continues to realize the benefits of our optimized operations and expansions ramp up, which provides for stronger financial and operational performances, which we expect to continue through the upcoming year. These improvements have enhanced the competitive position of both the Bolivar and Yauricocha mines within the cost curve for the global copper mining industry, with both mines now positioned in the lowest half of the cash cost curve.”

He continued,

“The COVID-19 situation in Peru and Mexico remains very serious and is an important factor in our daily operations. Protecting our employees, the communities in which we operate, and our operations are extremely important to us; as such, we continue adhering to strict health protocols. Testing and quarantining have helped identify and keep active cases from occurring in the mines, but as a result, we are operating with a lower than optimal headcount. We appreciate all our employee’s hard work in helping the mines to run safely, efficiently, and in helping us achieve the strong third quarter results.”

He concluded,

“We have reinitiated exploration and infrastructure projects at all mines that had been paused during the COVID-19 shutdowns. These programs and improvements are expected to help improve mine operations, production efficiencies as well as enable us to continue discovering and developing new and existing mineral resource opportunities. Barring any further COVID-19 work interruptions, the fourth quarter should help us to realize a strong finish for the year.”

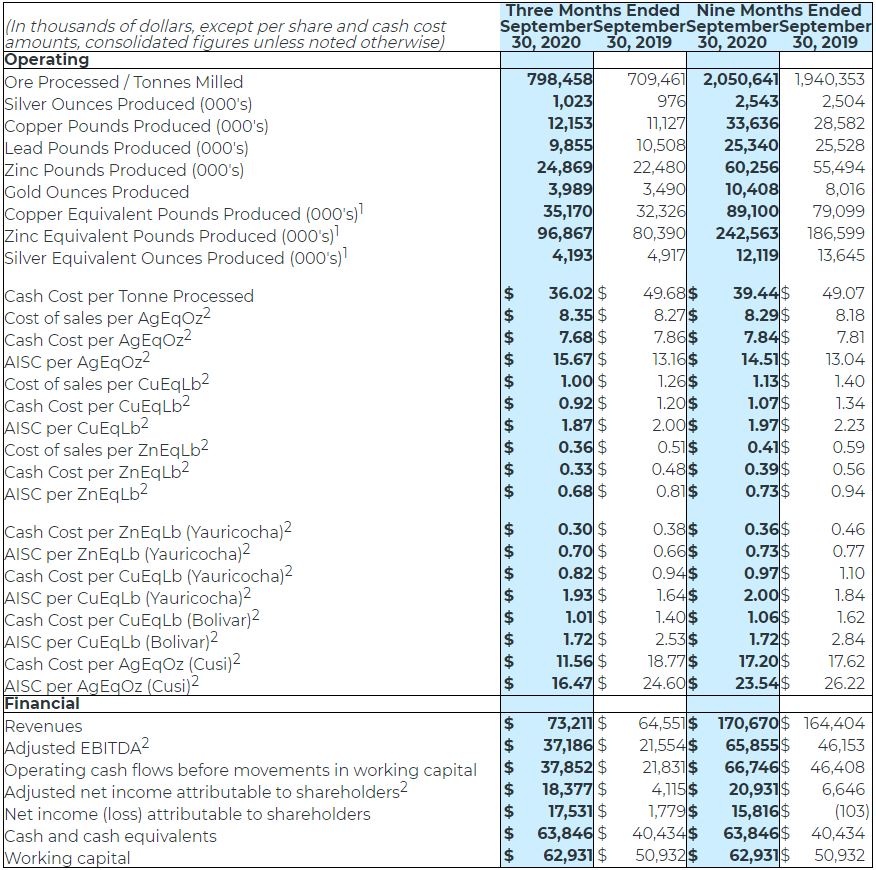

The following table displays selected unaudited financial information for the three months and nine months (“9M 2020”) ended September 30, 2020:

(1) Silver equivalent ounces and copper and zinc equivalent pounds for Q3 2020 were calculated using the following realized prices: $24.89/oz Ag, $2.97/lb Cu, $1.08/lb Zn, $0.85/lb Pb, $1,916/oz Au. Silver equivalent ounces and copper and zinc equivalent pounds for Q3 2019 were calculated using the following realized prices: $17.28/oz Ag, $2.63/lb Cu, $1.06/lb Zn, $0.94/lb Pb, $1,481/oz Au. Silver equivalent ounces and copper and zinc equivalent pounds for 9M 2020 were calculated using the following realized prices: $19.35/oz Ag, $2.63/lb Cu, $0.97/lb Zn, $0.80/lb Pb, $1,742/oz Au. Silver equivalent ounces and copper and zinc equivalent pounds for 9M 2019 were calculated using the following realized prices: $15.91/oz Ag, $2.74/lb Cu, $/1.16lb Zn, $0.91/lb Pb, $1,370/oz Au.

(2) This is a non-IFRS performance measure, see Non-IFRS Performance Measures section of the MD&A.

Q3 2020 Financial Highlights

Revenue from metals payable of $73.2 million in Q3 2020 increased by 13% from $64.6 million in Q3 2019. Revenues in Q3 2020 from metals payable from the Yauricocha Mine in Peru were $44.6 million, in line with $44.4 million in Q3 2019, as the increase in average realized sale prices were offset by lower payable metals and higher treatment and refining costs as compared to Q3 2019. Revenues generated at the Bolivar Mine for Q3 2020 were $23.3 million, compared to $14.7 million for the same period in 2019. The increase in revenues was a result of the 24% increase in throughput, higher recoveries for all metals, and higher realized metal prices for copper (13%), silver (44%) and gold (29%). This was partially offset by an 11% decrease in silver head grades during the quarter. Q3 2020 revenues of $5.3 million generated at the Cusi Mine were in line with revenues of Q3 2019, despite being operational for only 65 days in Q3 2020, as the impact of the 19% higher silver head grades, 20% higher gold head grades and higher realized sale price for both precious metals, were offset by lower silver equivalent ounces sold.

Yauricocha’s cost of sales per copper equivalent payable pound was $0.92 (Q3 2019 – $1.04), cash cost per copper equivalent payable pound was $0.82 (Q3 2019 – $0.94), and AISC per copper equivalent payable pound of $1.93 (Q3 2019 – $1.64). Cash costs per pound were driven lower mainly by the 26% lower operating costs per tonne during Q3 2020. The increase in the AISC per copper equivalent payable pound for Q3 2020 compared to Q3 2019 was due to the higher treatment and refining costs, higher sustaining capital and 5% lower copper equivalent payable pounds attributable to lower head grades and recoveries for all metals, except zinc.

Bolivar’s cost of sales per copper equivalent payable pound was $1.02 (Q3 2019 – $1.86), cash cost per copper equivalent payable pound was $1.01 (Q3 2019 – $1.40), and AISC per copper equivalent payable pound was $1.72 (Q3 2019 – $2.53) for Q3 2020. The decrease in the AISC per copper equivalent payable pound was due to lower operating costs per tonne and lower sustaining capital as compared to Q3 2019. Additionally, copper equivalent payable pounds were driven 36% higher by the 24% higher throughput and the increase in metal recoveries during Q3 2020 as compared to the same quarter of 2019.

Cusi’s cost of sales per silver equivalent payable ounce was $13.53 (Q3 2019 – $10.10), cash cost per silver equivalent payable ounce was $11.56 (Q3 2019 – $18.77), and AISC per silver equivalent payable ounce was $16.47 (Q3 2019 – $24.60) for Q3 2020. AISC per silver equivalent payable ounce decreased despite 31% lower silver equivalent ounces payable, resulting from unsold concentrate inventory at quarter end. Cash costs and AISC per silver equivalent payable ounce was lower due to 13% lower operating costs and 65% lower sustaining costs capital during the Q3 2020 as compared to Q3 2019.

Adjusted EBITDA(1) of $37.2 million for Q3 2020 increased by 73% compared to $21.6 million in Q3 2019. The increase in adjusted EBITDA in Q3 2020 was due to the increase in revenues realized and a decrease in operating costs at all three mines.

Cash flow generated from operations before movements in working capital of $37.9 million for Q3 2020 increased compared to $21.8 million in Q3 2019. The increase in operating cash flow is mainly the result of higher revenues generated and higher gross margins realized.

Net income attributable to Shareholders of the Company for Q3 2020 was $17.5 million (Q3 2019: $1.8 million) or $0.11 per share (basic and diluted) (Q3 2019: $0.01).

Cash and cash equivalents of $63.8 million and working capital of $62.9 million as at September 30, 2020, compared to $43.0 million and $49.9 million, respectively, at the end of 2019. Higher working capital at the end of Q3 2020 was a result of the increase in cash and cash equivalents, and trade receivables, which more than compensated for the increase in current liabilities, attributable to movement between current and long term portion of the credit facility. Cash and cash equivalents have increased during 9M 2020 due to $47.2 million of operating cash flows being partially offset by capital expenditures incurred in Mexico and Peru of $23.0 million and interest payment of $3.2 million.

(1)This is a non-IFRS performance measure, see Non-IFRS Performance Measures section of the MD&A.

Project Development

Mine development at Bolívar during Q3 2020 totaled 1,745 meters. A portion of the meters (928m) were developed to prepare stopes for mine production. The remainder of the meters (817m) were related to the deepening of ramps in the Lower El Gallo Inferior orebody and Bolivar West orebody. During Q3 2020, at the Cusi property, mine development totaled 1,168 meters, which included 998 meters of ramp development at the Promontorio; the rest of the development related to stope preparation in various zones within the mines.

Exploration Update

Peru:

Suspension of surface exploration activities, which started in the second quarter of 2020, continued in Q3 2020 as a result of the COVID-19 emergency declaration and restrictions on manpower at site. During the first half of September 2020, evaluations of the exploration zones were completed to begin drilling operations in the copper and molybdenum porphyry, as well as in the southern end of the Central mine, such as Doña Leona, El Paso, Kilkasca and Fortuna. Exploration is expected to return to normal in Q4 2020.

Mexico:

- Bolivar

At Bolívar during Q3 2020, 8,878 meters were drilled from surface as well as diamond drilling within the mine area towards La Montura which intersected a mineralized skarn orebody of semi-massive magnetite and disseminated chalcopyrite. Exploration also continued in the northwest extension of the Bolivar West.

- Cusi

During Q3 2020, the Company drilled 3,220 meters in the new discovery called NE-SW system from Santa Rosa de Lima.

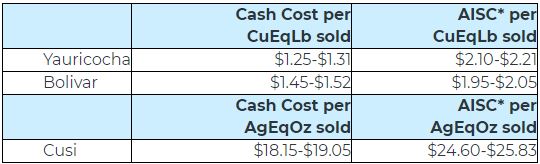

Revised 2020 Financial Guidance Issued

- Revised consolidated EBITDA guidance including corporate expenses is expected to be between $100 and $105 million

- Revised consolidated CAPEX guidance is expected to be between $40 and $45 million

- Revised full year Cash Costs and All-In Sustaining Costs by Mine are as follows:

*AISC includes treatment and refining charges, selling costs, G&A and sustaining capex

Conference Call Webcast

Sierra Metals’ senior management will host a conference call on Monday, November 9, 2020, at 11:00 AM (EST) to discuss the Company’s financial and operating results for the three and nine months ended September 30, 2020.

Via Webcast:

A live audio webcast of the meeting will be available on the Company’s website: https://event.on24.com/wcc/r/2625379/4399524BDDAF896736F6AE5F19B5AB48

The webcast, along with presentation slides, will be archived for 180 days on www.sierrametals.com.

Via phone:

To register for this conference call, please use the link provided below. After registering, a confirmation will be sent through email, including dial-in details and unique conference call codes for entry. As well, reminders will be sent to registered participants in advance of the call. If you have trouble registering, please dial: (888) 869-1189 or (706) 643-5902 for extra assistance.

Registration is open throughout the live call; however, to ensure you are connected for the full call, we suggest registering a day in advance or at minimum 10 minutes before the start of the call.

Conference Call Registration Link: http://www.directeventreg.com/registration/event/5555479

Quality Control

All technical data contained in this news release has been reviewed and approved by:

Americo Zuzunaga, FAusIMM CP (Mining Engineer) and Vice President of Corporate Planning is a Qualified Person under National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

Augusto Chung, FAusIMM CP (Metallurgist) and Vice President of Metallurgy and Projects to Sierra Metals is a Qualified Person under National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

About Sierra Metals

Sierra Metals Inc. is a diversified Canadian mining company focused on the production and development of precious and base metals from its polymetallic Yauricocha Mine in Peru, and Bolivar and Cusi Mines in Mexico. The Company is focused on increasing production volume and growing mineral resources. Sierra Metals has recently had several new key discoveries and still has many more exciting brownfield exploration opportunities at all three Mines in Peru and Mexico that are within close proximity to the existing mines. Additionally, the Company also has large land packages at all three mines with several prospective regional targets providing longer-term exploration upside and mineral resource growth potential.

The Company’s Common Shares trade on the Bolsa de Valores de Lima and on the Toronto Stock Exchange under the symbol “SMT” and on the NYSE American Exchange under the symbol “SMTS”.

For further information regarding Sierra Metals, please visit www.sierrametals.com

Continue to Follow, Like and Watch our progress:

Web: www.sierrametals.com | Twitter: sierrametals | Facebook: SierraMetalsInc | LinkedIn: Sierra Metals Inc

Forward-Looking Statements

This press release contains “forward-looking information” and “forward-looking statements” within the meaning of Canadian and U.S. securities laws (collectively, “forward-looking information“). Forward-looking information includes, but is not limited to, statements with respect to the date of the 2020 Shareholders’ Meeting and the anticipated filing of the Compensation Disclosure. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects”, “anticipates”, “plans”, “projects”, “estimates”, “assumes”, “intends”, “strategy”, “goals”, “objectives”, “potential” or variations thereof, or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking information.

Forward-looking information is subject to a variety of risks and uncertainties, which could cause actual events or results to differ from those reflected in the forward-looking information, including, without limitation, the risks described under the heading “Risk Factors” in the Company’s annual information form dated March 30, 2020 for its fiscal year ended December 31, 2019 and other risks identified in the Company’s filings with Canadian securities regulators and the United States Securities and Exchange Commission, which filings are available at www.sedar.com and www.sec.gov, respectively.

The risk factors referred to above are not an exhaustive list of the factors that may affect any of the Company’s forward-looking information. Forward-looking information includes statements about the future and is inherently uncertain, and the Company’s actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking information due to a variety of risks, uncertainties and other factors. The Company’s statements containing forward-looking information are based on the beliefs, expectations and opinions of management on the date the statements are made, and the Company does not assume any obligation to update such forward-looking information if circumstances or management’s beliefs, expectations or opinions should change, other than as required by applicable law. For the reasons set forth above, one should not place undue reliance on forward-looking information.

Mike McAllister

Vice President, Investor Relations

Sierra Metals Inc.

Tel: +1 (416) 366-7777

Email: [email protected]

Americo Zuzunaga

Vice President of Corporate Planning

Sierra Metals Inc.

Tel: +1 (416) 366-7777

Luis Marchese

CEO

Sierra Metals Inc.

Tel: +1 (416) 366-7777

Source: Sierra Metals Inc.